UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of: August 2024

Commission File Number: 001-36898

COLLIERS INTERNATIONAL GROUP INC.

(Translation of registrant's name into English)

1140 Bay Street, Suite 4000

Toronto, Ontario, Canada

M5S 2B4

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F [ ] Form 40-F [ X ]

Exhibit 99.1 of this Form 6-K shall be incorporated by reference as an exhibit to the registrant’s registration statement on Form F-10 (File No. 333-277184). Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

SIGNATURE

| COLLIERS INTERNATIONAL GROUP INC. | ||

| Date: August 1, 2024 | /s/ Christian Mayer | |

| Name: Christian Mayer | ||

| Title: Chief Financial Officer | ||

EXHIBIT INDEX

EXHIBIT 99.1

Colliers Reports Solid Second Quarter Results

Growth across all service lines and segments

Second quarter and year to date operating highlights:

| Three months ended | Six months ended | ||||||||||||

| June 30 | June 30 | ||||||||||||

| (in millions of US$, except EPS) | 2024 | 2023 | 2024 | 2023 | |||||||||

| Revenues | $ | 1,139.4 | $ | 1,078.0 | $ | 2,141.3 | $ | 2,043.9 | |||||

| Adjusted EBITDA (note 1) | 155.6 | 147.1 | 264.3 | 251.7 | |||||||||

| Adjusted EPS (note 2) | 1.36 | 1.31 | 2.13 | 2.16 | |||||||||

| GAAP operating earnings | 114.7 | 75.3 | 158.1 | 97.4 | |||||||||

| GAAP diluted net earnings (loss) per share | 0.73 | (0.16 | ) | 0.99 | (0.61 | ) | |||||||

TORONTO, Aug. 01, 2024 (GLOBE NEWSWIRE) -- Colliers International Group Inc. (NASDAQ and TSX: CIGI) (“Colliers” or the “Company”) today announced operating and financial results for the second quarter ended June 30, 2024. All amounts are in US dollars.

For the second quarter ended June 30, 2024, revenues were $1.14 billion, up 6% (6% in local currency) and Adjusted EBITDA (note 1) was $155.6 million, up 6% (6% in local currency) versus the prior year quarter. Adjusted EPS (note 2) was $1.36, relative to $1.31 in the prior year quarter. Second quarter adjusted EPS would have been approximately $0.01 higher excluding foreign exchange impacts. The GAAP operating earnings were $114.7 million as compared to $75.3 million in the prior year quarter. The GAAP diluted net earnings per share were $0.73 relative to a diluted net loss per share of $0.16 in the prior year quarter. The second quarter GAAP diluted net earnings per share EPS would have been approximately $0.01 higher excluding foreign exchange impacts.

For the six months ended June 30, 2024, revenues were $2.14 billion, up 5% (5% in local currency) and adjusted EBITDA (note 1) was $264.3 million, up 5% (6% in local currency) versus the prior year period. Adjusted EPS (note 2) was $2.13, relative to $2.16 in the prior year period. Adjusted EPS for the year would have been approximately $0.02 higher excluding foreign exchange impacts. The GAAP operating earnings were $158.1 million as compared to $97.4 million in the prior year period. The GAAP diluted net earnings per share were $0.99 compared to a diluted net loss per share of $0.61 in the prior year period. The GAAP diluted net earnings per share would have been approximately $0.02 higher excluding changes in foreign exchange rates.

“Colliers delivered solid second quarter results with growth across all service lines and segments. Leasing revenues exceeded expectations while Capital Markets saw modest growth for the first time since the second quarter of 2022. As expected, our high-value, recurring service lines – Outsourcing & Advisory and Investment Management – continued to deliver solid and predictable growth during the quarter. As our business continues to meet expectations, we are maintaining our financial outlook for the year,” said Jay S. Hennick, Chairman & CEO of Colliers.

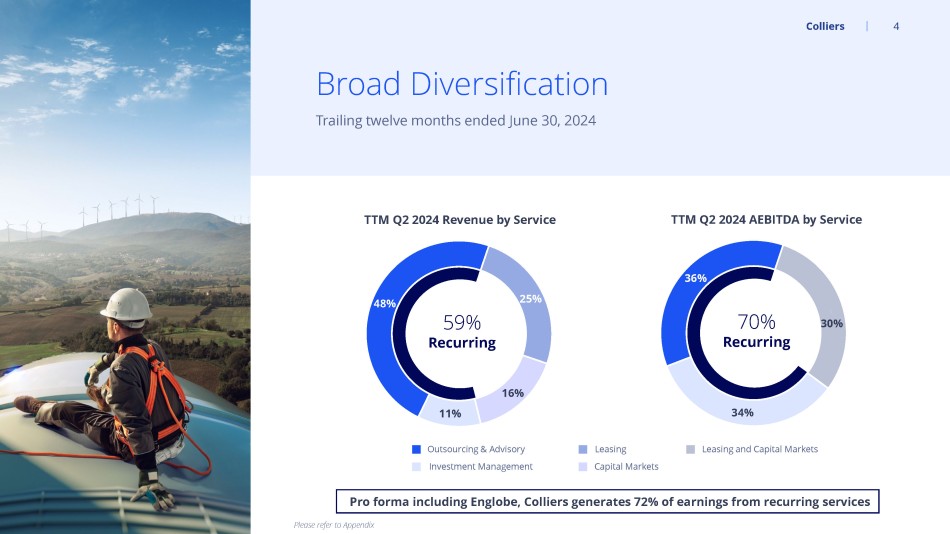

“Earlier this week, we completed the previously announced acquisition of Englobe, a leading multi-discipline engineering, environmental, and inspection services platform. This acquisition establishes Colliers as one of the top players in Canada, complements our rapidly growing engineering operations in the United States and Australia and aligns with our strategy of expanding our high-value recurring revenue streams, which now represents 72% of our earnings.”

“Since 2015, our committed leadership team, with substantial ownership, has continued to reposition our company to create growth and value for our shareholders. One step at a time, we have grown Colliers into a global leader in commercial real estate and expanded our business to include three complementary growth engines – Real Estate Services, Engineering, and Investment Management,” he concluded.

About Colliers

Colliers (NASDAQ, TSX: CIGI) is a leading diversified professional services and investment management company. With operations in 68 countries, our 22,000 enterprising professionals work collaboratively to provide expert real estate and investment advice to clients. For more than 29 years, our experienced leadership with significant inside ownership has delivered compound annual investment returns of approximately 20% for shareholders. With annual revenues of more than $4.4 billion and $96 billion of assets under management, Colliers maximizes the potential of property and real assets to accelerate the success of our clients, our investors and our people. Learn more at corporate.colliers.com, X @Colliers or LinkedIn.

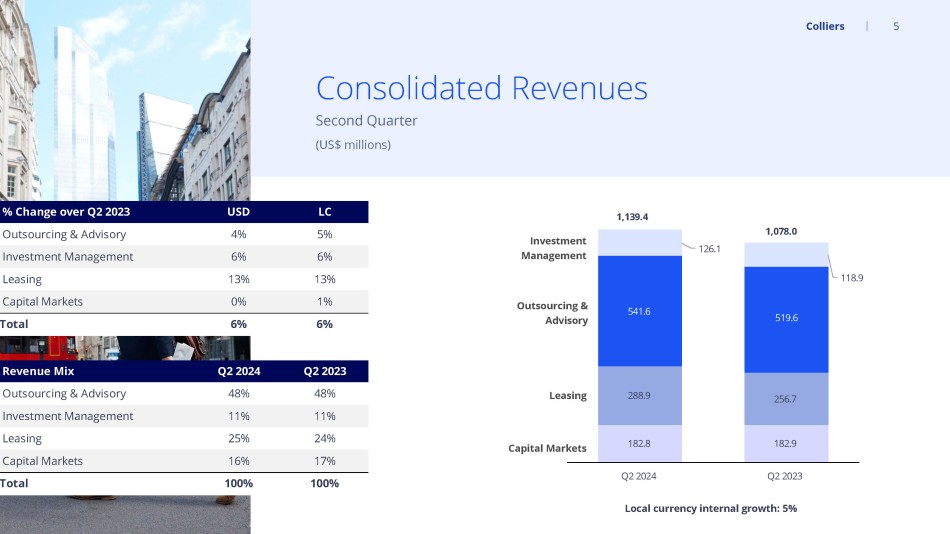

Consolidated Revenues by Line of Service

| Three months ended | Change | Change | Six months ended | Change | Change | ||||||||||||||||

| (in thousands of US$) | June 30 | in US$ % |

in LC % |

June 30 | in US$ % |

in LC % |

|||||||||||||||

| (LC = local currency) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||

| Outsourcing & Advisory | $ | 541,603 | $ | 519,578 | 4 | % | 5 | % | $ | 1,039,092 | $ | 974,508 | 7 | % | 7 | % | |||||

| Investment Management (1) | 126,051 | 118,860 | 6 | % | 6 | % | 248,572 | 239,606 | 4 | % | 4 | % | |||||||||

| Leasing | 288,918 | 256,684 | 13 | % | 13 | % | 532,155 | 495,071 | 7 | % | 8 | % | |||||||||

| Capital Markets | 182,796 | 182,916 | 0 | % | 1 | % | 321,529 | 334,756 | -4 | % | -3 | % | |||||||||

| Total revenues | $ | 1,139,368 | $ | 1,078,038 | 6 | % | 6 | % | $ | 2,141,348 | $ | 2,043,941 | 5 | % | 5 | % | |||||

| (1) Investment Management local currency revenues, excluding pass-through carried interest, were up 6% and 3% for the three and six-month periods ended June 30, 2024, respectively. | |||||||||||||||||||||

Second quarter consolidated revenues were up 6% on a local currency basis driven by growth across all service lines, led by Leasing. Consolidated internal revenue growth measured in local currencies was 5% (note 4) versus the prior year quarter.

For the six months ended June 30, 2024, consolidated revenues increased 5% on a local currency basis on robust growth in Leasing and Outsourcing & Advisory, partly offset by a market-driven slowdown in Capital Markets activity. Consolidated internal revenues measured in local currencies were up 4% (note 4).

Segmented Second Quarter Results

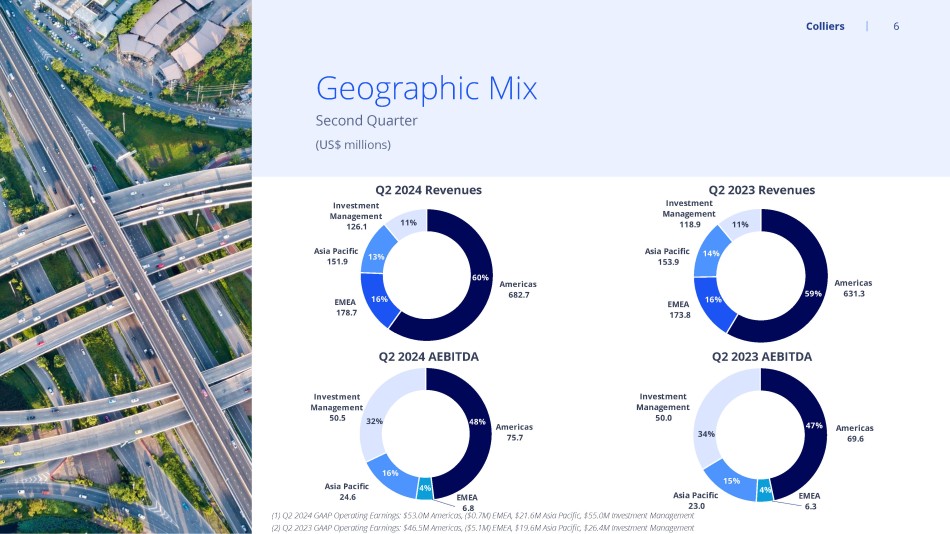

Revenues in the Americas region totalled $682.7 million, up 8% (8% in local currency) versus $631.3 million in the prior year quarter, primarily attributable to higher Leasing activity as well as robust broad-based growth in Outsourcing & Advisory. Capital Markets revenues were up 2%. Adjusted EBITDA was $75.7 million, up 9% (9% in local currency) relative to the prior year quarter on higher revenues. GAAP operating earnings were $53.0 million, relative to $46.5 million in the prior year quarter.

Revenues in the EMEA region totalled $178.7 million, up 3% (3% in local currency) compared to $173.8 million in the prior year quarter, attributable to higher Leasing activity and modest growth in Outsourcing & Advisory revenues, while Capital Markets revenues were essentially flat. Adjusted EBITDA was $6.8 million, up 7% (6% in local currency) compared to $6.3 million in the prior year quarter on a lower cost base. The GAAP operating loss was $0.7 million compared to a loss of $5.1 million in the prior year quarter.

Revenues in the Asia Pacific region totalled $151.9 million, down 1% (up 1% in local currency), compared to $153.9 million in the prior year quarter. Adjusted EBITDA was $24.6 million, up 7% (9% in local currency) primarily on lower operating costs. The GAAP operating earnings were $21.6 million, versus $19.6 million in the prior year quarter.

Investment Management revenues were $126.1 million relative to $118.9 million in the prior year quarter, up 6% (6% in local currency) on incremental revenues from new investor capital commitments. No passthrough revenues from historical carried interest were recognized in the current and prior year quarters. Adjusted EBITDA was $50.5 million, up 1% (1% in local currency) compared to the prior year quarter on higher revenues, partly offset by increased investments in new products, strategies and fundraising capabilities. The GAAP operating earnings were $55.0 million in the quarter versus $26.4 million in the prior year quarter. AUM was $96.4 billion as of June 30, 2024 compared to $96.3 billion as of March 31, 2024.

Unallocated global corporate costs as reported in Adjusted EBITDA were $1.9 million in the second quarter, flat relative to the prior year quarter. The corporate GAAP operating loss for the quarter was $14.2 million, versus $12.1 million in the second quarter of 2023.

Outlook for 2024

The Company’s outlook for 2024 is unchanged, except to reflect the partial year impact of the acquisition of Englobe:

| 2024 Outlook | ||||||

| Measure | Actual 2023 | Prior | Englobe | Revised (with Englobe) | ||

| Revenue growth | -3% |

|

+5% to +10% | +3% |

|

+8% to +13% |

| Adjusted EBITDA growth | -6% |

|

+5% to +15% | +3% |

|

+8% to +18% |

| Adjusted EPS growth | -23% |

|

+10% to +20% | +1% |

|

+11% to +21% |

The financial outlook is based on the Company’s best available information as of the date of this press release, and remains subject to change based on numerous macroeconomic, geopolitical, health, social and related factors. Continued interest rate volatility and/or lack of credit availability for commercial real estate transactions could materially impact the outlook.

Revised Operating Segments

With the acquisition of Englobe, the Company’s engineering and project management capabilities have reached scale, with over 8,000 employees generating approximately $1.3 billion in annual revenues across 15 countries.

Starting in the third quarter of 2024, the Company will re-align its operating segment reporting to better reflect the overall business and its three complementary growth engines – Real Estate Services, Engineering, and Investment Management. The Real Estate Services segment will be comprised of the former Americas, EMEA and Asia Pacific regions, but excluding engineering and project management.

Conference Call

Colliers will be holding a conference call on Thursday, August 1, 2024 at 11:00 a.m. Eastern Time to discuss the quarter’s results. The call, as well as a supplemental slide presentation, will be simultaneously web cast and can be accessed live or after the call at corporate.colliers.com in the Events section.

Forward-looking Statements

This press release includes or may include forward-looking statements. Forward-looking statements include the Company’s financial performance outlook and statements regarding goals, beliefs, strategies, objectives, plans or current expectations. These statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to be materially different from any future results, performance or achievements contemplated in the forward-looking statements. Such factors include: economic conditions, especially as they relate to commercial and consumer credit conditions and consumer spending, particularly in regions where the business may be concentrated; commercial real estate and real asset values, vacancy rates and general conditions of financial liquidity for real estate transactions; trends in pricing and risk assumption for commercial real estate services; the effect of significant movements in capitalization rates across different asset types; a reduction by companies in their reliance on outsourcing for their commercial real estate needs, which would affect revenues and operating performance; competition in the markets served by the Company; the ability to attract new clients and to retain clients and renew related contracts; the ability to attract new capital commitments to Investment Management funds and retain existing capital under management; the ability to retain and incentivize employees; increases in wage and benefit costs; the effects of changes in interest rates on the cost of borrowing; unexpected increases in operating costs, such as insurance, workers’ compensation and health care; changes in the frequency or severity of insurance incidents relative to historical experience; the effects of changes in foreign exchange rates in relation to the US dollar on the Company’s Canadian dollar, Euro, Australian dollar and UK pound sterling denominated revenues and expenses; the impact of pandemics on client demand for the Company’s services, the ability of the Company to deliver its services and the health and productivity of its employees; the impact of global climate change; the impact of political events including elections, referenda, trade policy changes, immigration policy changes, hostilities, war and terrorism on the Company’s operations; the ability to identify and make acquisitions at reasonable prices and successfully integrate acquired operations; the ability to execute on, and adapt to, information technology strategies and trends; the ability to comply with laws and regulations, including real estate investment management and mortgage banking licensure, labour and employment laws and regulations, as well as the anti-corruption laws and trade sanctions; and changes in government laws and policies at the federal, state/provincial or local level that may adversely impact the business.

Additional information and risk factors are identified in the Company’s other periodic filings with Canadian and US securities regulators (which factors are adopted herein and a copy of which can be obtained at www.sedarplus.ca. Forward looking statements contained in this press release are made as of the date hereof and are subject to change. All forward-looking statements in this press release are qualified by these cautionary statements. Except as required by applicable law, Colliers undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

Summary financial information is provided in this press release. This press release should be read in conjunction with the Company's consolidated financial statements and MD&A to be made available on SEDAR+ at www.sedarplus.ca.

This press release does not constitute an offer to sell or a solicitation of an offer to purchase an interest in any fund.

Notes

Non-GAAP Measures

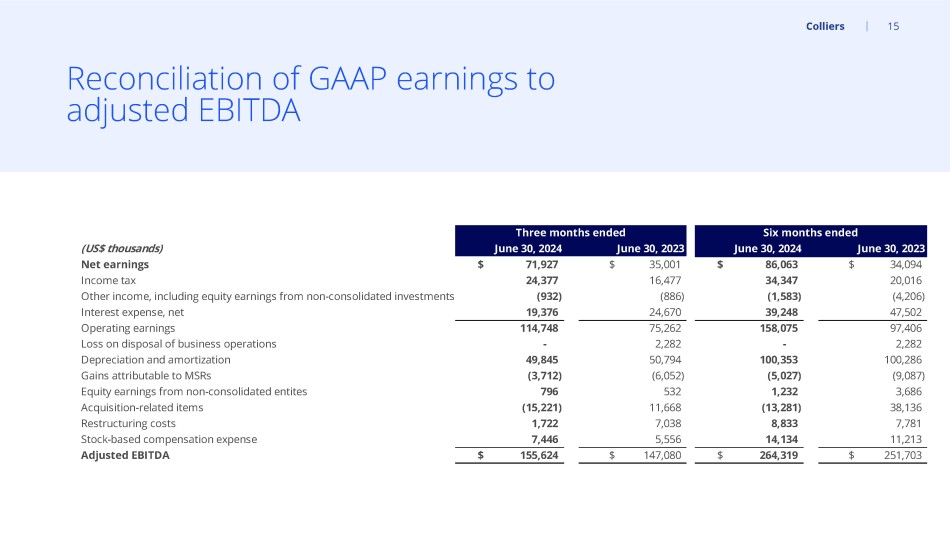

1. Reconciliation of net earnings to Adjusted EBITDA

Adjusted EBITDA is defined as net earnings, adjusted to exclude: (i) income tax; (ii) other income; (iii) interest expense; (iv) loss on disposal of operations; (v) depreciation and amortization, including amortization of mortgage servicing rights (“MSRs”); (vi) gains attributable to MSRs; (vii) acquisition-related items (including contingent acquisition consideration fair value adjustments, contingent acquisition consideration-related compensation expense and transaction costs); (viii) restructuring costs and (ix) stock-based compensation expense. We use Adjusted EBITDA to evaluate our own operating performance and our ability to service debt, as well as an integral part of our planning and reporting systems. Additionally, we use this measure in conjunction with discounted cash flow models to determine the Company’s overall enterprise valuation and to evaluate acquisition targets. We present Adjusted EBITDA as a supplemental measure because we believe such measure is useful to investors as a reasonable indicator of operating performance because of the low capital intensity of the Company’s service operations. We believe this measure is a financial metric used by many investors to compare companies, especially in the services industry. This measure is not a recognized measure of financial performance under GAAP in the United States, and should not be considered as a substitute for operating earnings, net earnings or cash flow from operating activities, as determined in accordance with GAAP. Our method of calculating Adjusted EBITDA may differ from other issuers and accordingly, this measure may not be comparable to measures used by other issuers. A reconciliation of net earnings to Adjusted EBITDA appears below.

| Three months ended | Six months ended | |||||||||||||||

| June 30 | June 30 | |||||||||||||||

| (in thousands of US$) | 2024 | 2023 | 2024 | 2023 | ||||||||||||

| Net earnings | $ | 71,927 | $ | 35,001 | $ | 86,063 | $ | 34,094 | ||||||||

| Income tax | 24,377 | 16,477 | 34,347 | 20,016 | ||||||||||||

| Other income, including equity earnings from non-consolidated investments | (932 | ) | (886 | ) | (1,583 | ) | (4,206 | ) | ||||||||

| Interest expense, net | 19,376 | 24,670 | 39,248 | 47,502 | ||||||||||||

| Operating earnings | 114,748 | 75,262 | 158,075 | 97,406 | ||||||||||||

| Loss on disposal of operations | - | 2,282 | - | 2,282 | ||||||||||||

| Depreciation and amortization | 49,845 | 50,794 | 100,353 | 100,286 | ||||||||||||

| Gains attributable to MSRs | (3,712 | ) | (6,052 | ) | (5,027 | ) | (9,087 | ) | ||||||||

| Equity earnings from non-consolidated investments | 796 | 532 | 1,232 | 3,686 | ||||||||||||

| Acquisition-related items | (15,221 | ) | 11,668 | (13,281 | ) | 38,136 | ||||||||||

| Restructuring costs | 1,722 | 7,038 | 8,833 | 7,781 | ||||||||||||

| Stock-based compensation expense | 7,446 | 5,556 | 14,134 | 11,213 | ||||||||||||

| Adjusted EBITDA | $ | 155,624 | $ | 147,080 | $ | 264,319 | $ | 251,703 | ||||||||

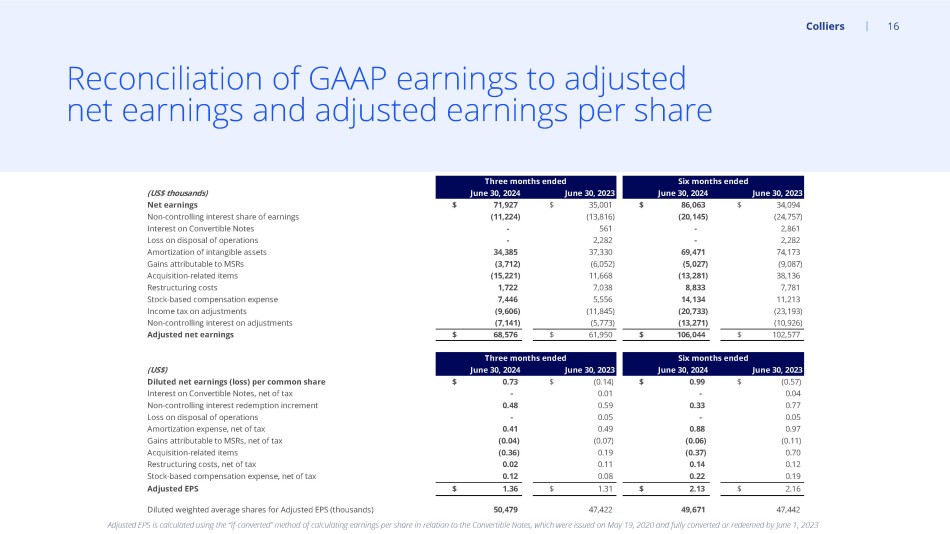

2. Reconciliation of net earnings and diluted net earnings per common share to adjusted net earnings and Adjusted EPS

Adjusted EPS is defined as diluted net earnings per share adjusted for the effect, after income tax, of: (i) the non-controlling interest redemption increment; (ii) loss on disposal of operations; (iii) amortization expense related to intangible assets recognized in connection with acquisitions and MSRs; (iv) gains attributable to MSRs; (v) acquisition-related items; (vi) restructuring costs and (vii) stock-based compensation expense. We believe this measure is useful to investors because it provides a supplemental way to understand the underlying operating performance of the Company and enhances the comparability of operating results from period to period. Adjusted EPS is not a recognized measure of financial performance under GAAP, and should not be considered as a substitute for diluted net earnings per share from continuing operations, as determined in accordance with GAAP. Our method of calculating this non-GAAP measure may differ from other issuers and, accordingly, this measure may not be comparable to measures used by other issuers. A reconciliation of net earnings to adjusted net earnings and of diluted net earnings per share to adjusted EPS appears below.

Similar to GAAP diluted EPS, Adjusted EPS is calculated using the “if-converted” method of calculating earnings per share in relation to the Convertible Notes, which were fully converted or redeemed by June 1, 2023. As such, the interest (net of tax) on the Convertible Notes is added to the numerator and the additional shares issuable on conversion of the Convertible Notes are added to the denominator of the earnings per share calculation to determine if an assumed conversion is more dilutive than no assumption of conversion. The “if-converted” method is used if the impact of the assumed conversion is dilutive. The “if-converted” method is dilutive for the Adjusted EPS calculation for all periods where the Convertible Notes were outstanding.

| Three months ended | Six months ended | |||||||||||||||

| June 30 | June 30 | |||||||||||||||

| (in thousands of US$) | 2024 | 2023 | 2024 | 2023 | ||||||||||||

| Net earnings | $ | 71,927 | $ | 35,001 | $ | 86,063 | $ | 34,094 | ||||||||

| Non-controlling interest share of earnings | (11,224 | ) | (13,816 | ) | (20,145 | ) | (24,757 | ) | ||||||||

| Interest on Convertible Notes | - | 561 | - | 2,861 | ||||||||||||

| Loss on disposal of operations | - | 2,282 | - | 2,282 | ||||||||||||

| Amortization of intangible assets | 34,385 | 37,330 | 69,471 | 74,173 | ||||||||||||

| Gains attributable to MSRs | (3,712 | ) | (6,052 | ) | (5,027 | ) | (9,087 | ) | ||||||||

| Acquisition-related items | (15,221 | ) | 11,668 | (13,281 | ) | 38,136 | ||||||||||

| Restructuring costs | 1,722 | 7,038 | 8,833 | 7,781 | ||||||||||||

| Stock-based compensation expense | 7,446 | 5,556 | 14,134 | 11,213 | ||||||||||||

| Income tax on adjustments | (9,606 | ) | (11,845 | ) | (20,733 | ) | (23,193 | ) | ||||||||

| Non-controlling interest on adjustments | (7,141 | ) | (5,773 | ) | (13,271 | ) | (10,926 | ) | ||||||||

| Adjusted net earnings | $ | 68,576 | $ | 61,950 | $ | 106,044 | $ | 102,577 | ||||||||

| Three months ended | Six months ended | |||||||||||||||

| June 30 | June 30 | |||||||||||||||

| (in US$) | 2024 | 2023 | 2024 | 2023 | ||||||||||||

| Diluted net earnings (loss) per common share(1) | $ | 0.73 | $ | (0.14 | ) | $ | 0.99 | $ | (0.57 | ) | ||||||

| Interest on Convertible Notes, net of tax | - | 0.01 | - | 0.04 | ||||||||||||

| Non-controlling interest redemption increment | 0.48 | 0.59 | 0.33 | 0.77 | ||||||||||||

| Loss on disposal of operations | - | 0.05 | - | 0.05 | ||||||||||||

| Amortization expense, net of tax | 0.41 | 0.49 | 0.88 | 0.97 | ||||||||||||

| Gains attributable to MSRs, net of tax | (0.04 | ) | (0.07 | ) | (0.06 | ) | (0.11 | ) | ||||||||

| Acquisition-related items | (0.36 | ) | 0.19 | (0.37 | ) | 0.70 | ||||||||||

| Restructuring costs, net of tax | 0.02 | 0.11 | 0.14 | 0.12 | ||||||||||||

| Stock-based compensation expense, net of tax | 0.12 | 0.08 | 0.22 | 0.19 | ||||||||||||

| Adjusted EPS | $ | 1.36 | $ | 1.31 | $ | 2.13 | $ | 2.16 | ||||||||

| Diluted weighted average shares for Adjusted EPS (thousands) | 50,479 | 47,422 | 49,671 | 47,442 | ||||||||||||

| (1) Amounts shown reflect the "if-converted" method's dilutive impact on the adjusted EPS calculation. | ||||||||||||||||

3. Reconciliation of net cash flow from operations to free cash flow

Free cash flow is defined as net cash flow from operating activities plus contingent acquisition consideration paid, less purchases of fixed assets, plus cash collections on AR Facility deferred purchase price less distributions to non-controlling interests. We use free cash flow as a measure to evaluate and monitor operating performance as well as our ability to service debt, fund acquisitions and pay dividends to shareholders. We present free cash flow as a supplemental measure because we believe this measure is a financial metric used by many investors to compare valuation and liquidity measures across companies, especially in the services industry. This measure is not a recognized measure of financial performance under GAAP in the United States, and should not be considered as a substitute for operating earnings, net earnings or cash flow from operating activities, as determined in accordance with GAAP. Our method of calculating free cash flow may differ from other issuers and accordingly, this measure may not be comparable to measures used by other issuers. A reconciliation of net cash flow from operating activities to free cash flow appears below.

| Three months ended | Six months ended | |||||||||||||||

| June 30 | June 30 | |||||||||||||||

| (in thousands of US$) | 2024 | 2023 | 2024 | 2023 | ||||||||||||

| Net cash provided by (used in) operating activities | $ | 141,189 | $ | 98,973 | $ | 3,574 | $ | (33,595 | ) | |||||||

| Contingent acquisition consideration paid | 300 | 2,719 | 3,038 | 2,991 | ||||||||||||

| Purchase of fixed assets | (12,480 | ) | (22,179 | ) | (29,353 | ) | (41,062 | ) | ||||||||

| Cash collections on AR Facility deferred purchase price | 34,930 | 28,539 | 68,848 | 59,311 | ||||||||||||

| Distributions paid to non-controlling interests | (38,521 | ) | (40,059 | ) | (48,827 | ) | (51,120 | ) | ||||||||

| Free cash flow | $ | 125,418 | $ | 67,993 | $ | (2,720 | ) | $ | (63,475 | ) | ||||||

4. Local currency revenue and Adjusted EBITDA growth rate and internal revenue growth rate measures

Percentage revenue and Adjusted EBITDA variances presented on a local currency basis are calculated by translating the current period results of our non-US dollar denominated operations to US dollars using the foreign currency exchange rates from the periods against which the current period results are being compared. Percentage revenue variances presented on an internal growth basis are calculated assuming no impact from acquired entities in the current and prior periods. Revenue from acquired entities, including any foreign exchange impacts, are treated as acquisition growth until the respective anniversaries of the acquisitions. We believe that these revenue growth rate methodologies provide a framework for assessing the Company’s performance and operations excluding the effects of foreign currency exchange rate fluctuations and acquisitions. Since these revenue growth rate measures are not calculated under GAAP, they may not be comparable to similar measures used by other issuers.

5. Assets under management

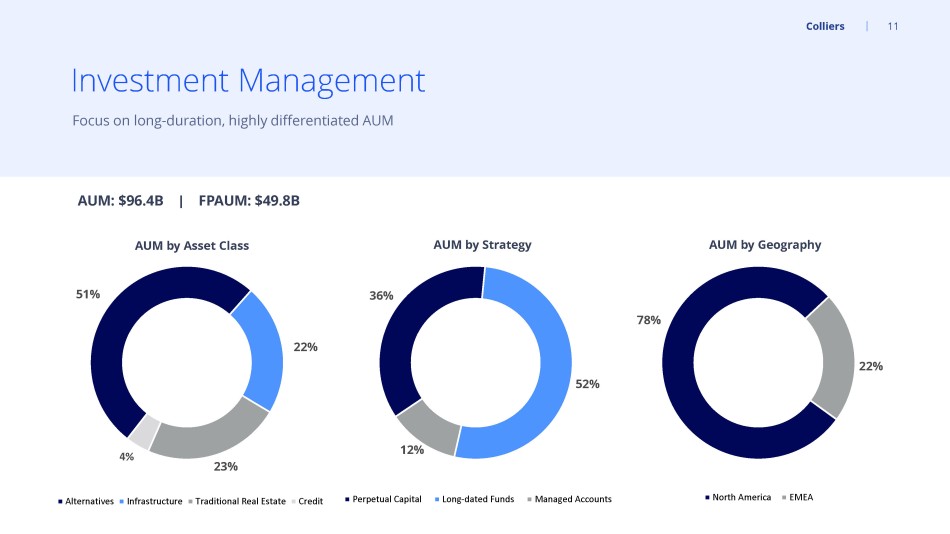

We use the term assets under management (“AUM”) as a measure of the scale of our Investment Management operations. AUM is defined as the gross market value of operating assets and the projected gross cost of development assets of the funds, partnerships and accounts to which we provide management and advisory services, including capital that such funds, partnerships and accounts have the right to call from investors pursuant to capital commitments. Our definition of AUM may differ from those used by other issuers and as such may not be directly comparable to similar measures used by other issuers.

6. Adjusted EBITDA from recurring revenue percentage

Adjusted EBITDA from recurring revenue percentage is computed on a trailing twelve-month basis and represents the proportion of Adjusted EBITDA (note 1) that is derived from Outsourcing & Advisory and Investment Management service lines. Both these service lines represent medium to long-term duration revenue streams that are either contractual or repeatable in nature. Adjusted EBITDA for this purpose is calculated in the same manner as for our debt agreement covenant calculation purposes, incorporating the expected full year impact of business acquisitions and dispositions.

| Colliers International Group Inc. | ||||||||||||||||||

| Condensed Consolidated Statements of Earnings (Loss) | ||||||||||||||||||

| (in thousands of US$, except per share amounts) | ||||||||||||||||||

| Three months | Six months | |||||||||||||||||

| ended June 30 | ended June 30 | |||||||||||||||||

| (unaudited) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||

| Revenues | $ | 1,139,368 | $ | 1,078,038 | $ | 2,141,348 | $ | 2,043,941 | ||||||||||

| Cost of revenues | 687,062 | 640,650 | 1,293,307 | 1,226,910 | ||||||||||||||

| Selling, general and administrative expenses | 302,934 | 297,382 | 602,894 | 578,921 | ||||||||||||||

| Depreciation | 15,460 | 13,464 | 30,882 | 26,113 | ||||||||||||||

| Amortization of intangible assets | 34,385 | 37,330 | 69,471 | 74,173 | ||||||||||||||

| Acquisition-related items (1) | (15,221 | ) | 11,668 | (13,281 | ) | 38,136 | ||||||||||||

| Loss on disposal of operations | - | 2,282 | - | 2,282 | ||||||||||||||

| Operating earnings | 114,748 | 75,262 | 158,075 | 97,406 | ||||||||||||||

| Interest expense, net | 19,376 | 24,670 | 39,248 | 47,502 | ||||||||||||||

| Equity earnings from non-consolidated investments | (796 | ) | (532 | ) | (1,232 | ) | (3,686 | ) | ||||||||||

| Other income | (136 | ) | (354 | ) | (351 | ) | (520 | ) | ||||||||||

| Earnings before income tax | 96,304 | 51,478 | 120,410 | 54,110 | ||||||||||||||

| Income tax | 24,377 | 16,477 | 34,347 | 20,016 | ||||||||||||||

| Net earnings | 71,927 | 35,001 | 86,063 | 34,094 | ||||||||||||||

| Non-controlling interest share of earnings | 11,224 | 13,816 | 20,145 | 24,757 | ||||||||||||||

| Non-controlling interest redemption increment | 23,979 | 28,036 | 16,537 | 36,340 | ||||||||||||||

| Net earnings (loss) attributable to Company | $ | 36,724 | $ | (6,851 | ) | $ | 49,381 | $ | (27,003 | ) | ||||||||

| Net earnings (loss) per common share | ||||||||||||||||||

| Basic | $ | 0.73 | $ | (0.15 | ) | $ | 1.00 | $ | (0.61 | ) | ||||||||

|

|

Diluted (2) |

|

$ | 0.73 |

|

$ | (0.16 | ) |

|

$ | 0.99 |

|

$ | (0.61 | ) | |||

| Adjusted EPS (3) | $ | 1.36 | $ | 1.31 | $ | 2.13 | $ | 2.16 | ||||||||||

| Weighted average common shares (thousands) | ||||||||||||||||||

| Basic | 50,239 |

45,069 |

49,374 | 44,064 |

||||||||||||||

| Diluted | 50,479 |

45,362 |

49,671 |

44,064 |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

| Notes to Condensed Consolidated Statements of Earnings | |

| (1) | Acquisition-related items include contingent acquisition consideration fair value adjustments, contingent acquisition consideration-related compensation expense and transaction costs. |

| (2) | Diluted EPS is calculated using the “if-converted” method of calculating earnings per share in relation to the Convertible Notes, which were fully converted or redeemed by June 1, 2023. As such, the interest (net of tax) on the Convertible Notes is added to the numerator and the additional shares issuable on conversion of the Convertible Notes are added to the denominator of the earnings per share calculation to determine if an assumed conversion is more dilutive than no assumption of conversion. The “if-converted” method is used if the impact of the assumed conversion is dilutive. The “if-converted” method was dilutive for the three months ended June 30, 2023 and anti-dilutive for the six months ended June 30, 2023. |

| (3) | See definition and reconciliation above. |

| Colliers International Group Inc. | |||||||||

| Condensed Consolidated Balance Sheets | |||||||||

| (in thousands of US$) | |||||||||

| June 30, | December 31, | June 30, | |||||||

| (unaudited) | 2024 | 2023 | 2023 | ||||||

| Assets | |||||||||

| Cash and cash equivalents | $ | 162,625 | $ | 181,134 | $ | 172,371 | |||

| Restricted cash (1) | 78,060 | 37,941 | 85,207 | ||||||

| Accounts receivable and contract assets | 723,531 | 726,764 | 669,311 | ||||||

| Mortgage warehouse receivables (2) | 140,974 | 177,104 | 77,443 | ||||||

| Prepaids and other assets | 329,716 | 306,829 | 287,490 | ||||||

| Warehouse fund assets | 49,285 | 44,492 | 41,084 | ||||||

| Current assets | 1,484,191 | 1,474,264 | 1,332,906 | ||||||

| Other non-current assets | 212,301 | 188,745 | 182,305 | ||||||

| Warehouse fund assets | 286,171 | 47,536 | - | ||||||

| Fixed assets | 201,315 | 202,837 | 182,944 | ||||||

| Operating lease right-of-use assets | 380,699 | 390,565 | 365,198 | ||||||

| Deferred tax assets, net | 58,902 | 59,468 | 67,959 | ||||||

| Goodwill and intangible assets | 3,048,187 | 3,118,711 | 3,167,063 | ||||||

| Total assets | $ | 5,671,766 | $ | 5,482,126 | $ | 5,298,375 | |||

| Liabilities and shareholders' equity | |||||||||

| Accounts payable and accrued liabilities | $ | 966,978 | $ | 1,104,935 | $ | 1,008,318 | |||

| Other current liabilities | 97,862 | 75,764 | 101,528 | ||||||

| Long-term debt - current | 9,618 | 1,796 | 8,960 | ||||||

| Mortgage warehouse credit facilities (2) | 132,869 | 168,780 | 70,009 | ||||||

| Operating lease liabilities - current | 87,350 | 89,938 | 88,659 | ||||||

| Liabilities related to warehouse fund assets | 146,636 | - | - | ||||||

| Current liabilities | 1,441,313 | 1,441,213 | 1,277,474 | ||||||

| Long-term debt - non-current | 1,354,241 | 1,500,843 | 1,659,461 | ||||||

| Operating lease liabilities - non-current | 371,618 | 375,454 | 348,707 | ||||||

| Other liabilities | 123,691 | 151,333 | 157,379 | ||||||

| Deferred tax liabilities, net | 37,635 | 43,191 | 44,722 | ||||||

| Liabilities related to warehouse fund assets | 43,000 | 47,536 | - | ||||||

| Redeemable non-controlling interests | 1,105,008 | 1,072,066 | 1,093,696 | ||||||

| Shareholders' equity | 1,195,260 | 850,490 | 716,936 | ||||||

| Total liabilities and equity | $ | 5,671,766 | $ | 5,482,126 | $ | 5,298,375 | |||

| Supplemental balance sheet information | |||||||||

| Total debt (3) | $ | 1,363,859 | $ | 1,502,639 | $ | 1,668,421 | |||

| Total debt, net of cash and cash equivalents (3) | 1,201,234 | 1,321,505 | 1,496,050 | ||||||

| Net debt / pro forma adjusted EBITDA ratio (4) | 2.0 | 2.2 | 2.4 | ||||||

| Notes to Condensed Consolidated Balance Sheets | |

| (1) | Restricted cash consists primarily of cash amounts set aside to satisfy legal or contractual requirements arising in the normal course of business. |

| (2) | Mortgage warehouse receivables represent mortgage loans receivable, the majority of which are offset by borrowings under mortgage warehouse credit facilities which fund loans that financial institutions have committed to purchase. |

| (3) | Excluding mortgage warehouse credit facilities. |

| (4) | Net debt for financial leverage ratio excludes restricted cash and mortgage warehouse credit facilities, in accordance with debt agreements. |

| Colliers International Group Inc. | |||||||||||||||||

| Condensed Consolidated Statements of Cash Flows | |||||||||||||||||

| (in thousands of US$) | |||||||||||||||||

| Three months ended | Six months ended | ||||||||||||||||

| June 30 | June 30 | ||||||||||||||||

| (unaudited) | 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Cash provided by (used in) | |||||||||||||||||

| Operating activities | |||||||||||||||||

| Net earnings | $ | 71,927 | $ | 35,001 | $ | 86,063 | $ | 34,094 | |||||||||

| Items not affecting cash: | |||||||||||||||||

| Depreciation and amortization | 49,845 | 50,794 | 100,353 | 100,286 | |||||||||||||

| Loss on disposal of operations | - | 2,282 | - | 2,282 | |||||||||||||

| Gains attributable to mortgage servicing rights | (3,712 | ) | (6,052 | ) | (5,027 | ) | (9,087 | ) | |||||||||

| Gains attributable to the fair value of loan | |||||||||||||||||

| premiums and origination fees | (3,424 | ) | (4,009 | ) | (5,623 | ) | (8,026 | ) | |||||||||

| Deferred income tax | (3,406 | ) | (10,915 | ) | (7,395 | ) | (21,904 | ) | |||||||||

| Other | 1,686 | 31,212 | 15,148 | 66,521 | |||||||||||||

| 112,916 | 98,313 | 183,519 | 164,166 | ||||||||||||||

| Increase in accounts receivable, prepaid | |||||||||||||||||

| expenses and other assets | (98,930 | ) | (26,970 | ) | (94,289 | ) | (56,725 | ) | |||||||||

| Increase (decrease) in accounts payable, accrued | |||||||||||||||||

| expenses and other liabilities | 43,740 | (2,654 | ) | (2,902 | ) | 457 | |||||||||||

| Decrease (increase) in accrued compensation | 59,914 | 26,678 | (87,018 | ) | (153,630 | ) | |||||||||||

| Contingent acquisition consideration paid | (300 | ) | (2,719 | ) | (3,038 | ) | (2,991 | ) | |||||||||

| Mortgage origination activities, net | 3,694 | 6,285 | 7,192 | 9,070 | |||||||||||||

| Sales to AR Facility, net | 20,155 | 40 | 110 | 6,058 | |||||||||||||

| Net cash provided by (used in) operating activities | 141,189 | 98,973 | 3,574 | (33,595 | ) | ||||||||||||

| Investing activities | |||||||||||||||||

| Acquisition of businesses, net of cash acquired | (17,772 | ) | (59,698 | ) | (17,772 | ) | (59,698 | ) | |||||||||

| Purchases of fixed assets | (12,480 | ) | (22,179 | ) | (29,353 | ) | (41,062 | ) | |||||||||

| Purchases of warehouse fund assets | (220,917 | ) | (2,580 | ) | (257,343 | ) | (40,576 | ) | |||||||||

| Proceeds from disposal of warehouse fund assets | 71,494 | - | 76,438 | 44,000 | |||||||||||||

| Cash collections on AR Facility deferred purchase price | 34,930 | 28,539 | 68,848 | 59,311 | |||||||||||||

| Other investing activities | (22,718 | ) | (8,476 | ) | (58,133 | ) | (29,543 | ) | |||||||||

| Net cash used in investing activities | (167,463 | ) | (64,394 | ) | (217,315 | ) | (67,568 | ) | |||||||||

| Financing activities | |||||||||||||||||

| Increase in long-term debt, net | 106,528 | 47,248 | 1,476 | 219,668 | |||||||||||||

| Purchases of non-controlling interests, net | (7,083 | ) | (3,789 | ) | (9,737 | ) | (16,333 | ) | |||||||||

| Dividends paid to common shareholders | - | - | (7,132 | ) | (6,440 | ) | |||||||||||

| Distributions paid to non-controlling interests | (38,521 | ) | (40,059 | ) | (48,827 | ) | (51,120 | ) | |||||||||

| Issuance of subordinate voting shares | - | - | 286,924 | - | |||||||||||||

| Other financing activities | 2,964 | (1,350 | ) | 17,093 | 13,637 | ||||||||||||

| Net cash provided by financing activities | 63,888 | 2,050 | 239,797 | 159,412 | |||||||||||||

| Effect of exchange rate changes on cash, | |||||||||||||||||

| cash equivalents and restricted cash | (2,386 | ) | (1,704 | ) | (4,446 | ) | 287 | ||||||||||

| Net change in cash and cash | |||||||||||||||||

| equivalents and restricted cash | 35,228 | 34,925 | 21,610 | 58,536 | |||||||||||||

| Cash and cash equivalents and | |||||||||||||||||

| restricted cash, beginning of period | 205,457 | 222,653 | 219,075 | 199,042 | |||||||||||||

| Cash and cash equivalents and | |||||||||||||||||

| restricted cash, end of period | $ | 240,685 | $ | 257,578 | $ | 240,685 | $ | 257,578 | |||||||||

| Colliers International Group Inc. | ||||||||||||||||||||

| Segmented Results | ||||||||||||||||||||

| (in thousands of US dollars) | ||||||||||||||||||||

| Asia | Investment | |||||||||||||||||||

| (unaudited) | Americas | EMEA | Pacific | Management | Corporate | Consolidated | ||||||||||||||

| Three months ended June 30 | ||||||||||||||||||||

| 2024 | ||||||||||||||||||||

| Revenues | $ | 682,679 | $ | 178,650 | $ | 151,884 | $ | 126,051 | $ | 104 | $ | 1,139,368 | ||||||||

| Adjusted EBITDA | 75,667 | 6,777 | 24,553 | 50,489 | (1,862 | ) | 155,624 | |||||||||||||

| Operating earnings (loss) | 53,001 | (661 | ) | 21,567 | 55,032 | (14,191 | ) | 114,748 | ||||||||||||

| 2023 | ||||||||||||||||||||

| Revenues | $ | 631,332 | $ | 173,818 | $ | 153,915 | $ | 118,860 | $ | 113 | $ | 1,078,038 | ||||||||

| Adjusted EBITDA | 69,588 | 6,315 | 23,032 | 50,042 | (1,897 | ) | 147,080 | |||||||||||||

| Operating earnings (loss) | 46,450 | (5,053 | ) | 19,554 | 26,407 | (12,096 | ) | 75,262 | ||||||||||||

| Asia | Investment | |||||||||||||||||||

| Americas | EMEA | Pacific | Management | Corporate | Consolidated | |||||||||||||||

| Six months ended June 30 | ||||||||||||||||||||

| 2024 | ||||||||||||||||||||

| Revenues | $ | 1,289,090 | $ | 325,218 | $ | 278,241 | $ | 248,572 | $ | 227 | $ | 2,141,348 | ||||||||

| Adjusted EBITDA | 130,551 | (5,209 | ) | 39,144 | 103,339 | (3,506 | ) | 264,319 | ||||||||||||

| Operating earnings (loss) | 82,038 | (21,122 | ) | 33,107 | 93,912 | (29,860 | ) | 158,075 | ||||||||||||

| 2023 | ||||||||||||||||||||

| Revenues | $ | 1,212,883 | $ | 317,189 | $ | 274,008 | $ | 239,606 | $ | 255 | $ | 2,043,941 | ||||||||

| Adjusted EBITDA | 123,451 | (4,946 | ) | 31,081 | 104,936 | (2,819 | ) | 251,703 | ||||||||||||

| Operating earnings (loss) | 79,321 | (30,087 | ) | 24,593 | 41,211 | (17,632 | ) | 97,406 | ||||||||||||

COMPANY CONTACTS:

Jay S. Hennick

Chairman & Chief Executive Officer

Chris McLernon

Chief Executive Officer, Real Estate Services

Christian Mayer

Chief Financial Officer

(416) 960-9500

Exhibit 99.2

Second Quarter 2024 Financial Results August 1, 2024

This presentation includes or may include forward - looking statements. Forward - looking statements include the Company’s financial performance outlook and statements regarding goals, beliefs, strategies, objectives, plans or current expectations. These statements involve known and unknown risks, unce rta inties and other factors which may cause the actual results to be materially different from any future results, performance or achievements contemplated in the forward - looking stat ements. Such factors include: economic conditions, especially as they relate to commercial and consumer credit conditions and business spending; commercial real estate property va lues, vacancy rates and general conditions of financial liquidity for real estate transactions; the ability to attract new capital commitments to our Investment Management funds and re tain existing capital under management; the effects of changes in foreign exchange rates in relation to the US dollar on Canadian dollar, Australian dollar, UK pound sterling and E uro denominated revenues and expenses; competition in markets served by the Company; labor shortages or increases in commission, wage and benefit costs; the impact of higher than exp ected inflation could impact profitability of certain contracts; impact of pandemics on client demand, ability to deliver services and ensure the health and productivity of employ ees ; disruptions or security failures in information technology systems; cybersecurity risks; a change in/loss of our relationship with US government agencies could significantly im pact our ability to originate mortgage loans; default on loans originated under the Fannie Mae Delegated Underwriting and Servicing program could materially affect our profitability; th e effect of increases in interest rates on our cost of borrowing and political conditions or events, including elections, referenda, changes to international trade and immigration pol icies and any outbreak or escalation of terrorism or hostilities. Additional factors and explanatory information are identified in the Company’s Annual Information Form for the year ended Dec emb er 31, 2023 under the heading “Risk Factors” (which factors are adopted herein, and which can be accessed at www.sedarplus.ca) and other periodic filings with Canadian and US se cur ities regulators. Forward looking statements contained in this presentation are made as of the date hereof and are subject to change. All forward - looking statements in this press release are qualified by these cautionary statements. Except as required by applicable law, Colliers undertakes no obligation to publicly update or revise any forward - loo king statement, whether as a result of new information, future events or otherwise. This presentation does not constitute an offer to sell or a solicitation of an offer to purchase an interest in any fund. Colliers 2 Forward - Looking Statements Non - GAAP measures This presentation makes reference to certain non - GAAP measures, including local currency (“LC”) revenue growth rate, internal re venue growth rate, Adjusted EBITDA (“AEBITDA”), Adjusted EPS (“AEPS”), free cash flow, assets under management (“AUM”), fee paying assets under management (“FPAUM”). Please re fer to Appendix for reconciliations to GAAP measures.

Colliers 3 (US $ millions, except per share amounts) Highlights • Growth across all service lines and segments, led by Leasing • Strong and predictable growth in recurring service lines – Outsourcing & Advisory and Investment Management • First period of Capital Markets revenue growth since Q2 2022 • Completed the acquisition of Englobe on July 29, 2024 • Outlook for 2024 unchanged, except Englobe impact USD LC (1) Revenue 1,139.4 1,078.0 6% 6% Adjusted EBITDA 155.6 147.1 6% 6% Adjusted EBITDA Margin 13.7% 13.6% Adjusted EPS 1.36 1.31 4% GAAP Operating Earnings 114.7 75.3 52% GAAP Operating Earnings Margin 10.1% 7.0% GAAP diluted EPS 0.73 (0.16) NM USD LC (1) Revenue 2,141.3 2,043.9 5% 5% Adjusted EBITDA 264.3 251.7 5% 6% Adjusted EBITDA Margin 12.3% 12.3% Adjusted EPS 2.13 2.16 -1% GAAP Operating Earnings 158.1 97.4 62% GAAP Operating Earnings Margin 7.4% 4.8% GAAP diluted EPS 0.99 (0.61) NM Three months ended June 30 2024 2023 %Change Six months ended June 30 2024 2023 % Change (1) Local Currency 36% 30% 34% 48% 25% 16% 11% Please refer to Appendix Colliers 4 Trailing twelve months ended June 30, 2024 Broad Diversification Outsourcing & Advisory Investment Management Leasing Capital Markets Leasing and Capital Markets 59% Recurring 70% Recurring TTM Q2 2024 Revenue by Service TTM Q2 2024 AEBITDA by Service Pro forma including Englobe, Colliers generates 72% of earnings from recurring services

Colliers 5 Second Quarter (US$ millions) Consolidated Revenues % Change over Q2 2023 USD LC Outsourcing & Advisory 4% 5% Investment Management 6% 6% Leasing 13% 13% Capital Markets 0% 1% Total 6% 6% Revenue Mix Q2 2024 Q2 2023 Outsourcing & Advisory 48% 48% Investment Management 11% 11% Leasing 25% 24% Capital Markets 16% 17% Total 100% 100% 4 4 Outsourcing & Advisory Investment Management Capital Markets Leasing Local currency internal growth: 5% Colliers 6 Second Quarter (US$ millions) Geographic Mix Q2 2024 Revenues Q2 2023 Revenues $PHULFDV (0($ $VLD3DFLȴF ΖQYHVWPHQW 0DQDJHPHQW Q2 2024 AEBITDA Q2 2023 AEBITDA (1) Q2 2024 GAAP Operating Earnings: $53.0M Americas, ($0.7M) EMEA, $21.6M Asia Pacific, $55.0M Investment Management (2) Q2 2023 GAAP Operating Earnings: $46.5M Americas, ($5.1M) EMEA, $19.6M Asia Pacific, $26.4M Investment Management $PHULFDV (0($ $VLD3DFLȴF ΖQYHVWPHQW 0DQDJHPHQW

Colliers 7 Second Quarter (US$ millions) Americas GAAP Operating Earnings: Q2 2024 $53.0M at 7.8% margin; Q2 2023 $46.5M at 7.4% margin Higher Leasing activity as well as robust broad - based growth in Outsourcing & Advisory Capital Markets revenues up 2% 4 4 USD LC Revenue Growth 8% 8% Revenues AEBITDA Outsourcing & Advisory Leasing Capital Markets Colliers 8 Second Quarter (US$ millions) EMEA GAAP Operating Earnings: Q2 2024 ($0.7M) at (0.4%) margin; Q2 2023 ($5.1M) at (2.9%) margin Higher Leasing activity and modest growth in Outsourcing & Advisory Adjusted EBITDA margin improved on a lower cost base 4 4 USD LC Revenue Growth 3% 3% Revenues AEBITDA Outsourcing & Advisory Leasing Capital Markets

Colliers 9 Second Quarter (US$ millions) APAC GAAP Operating Earnings: Q2 2024 $21.6M at 14.2% margin; Q2 2023 $19.6M at 12.7% margin Revenues up modestly in local currency terms Adjusted EBITDA margin improved on lower operating costs 4 4 USD LC Revenue Growth -1% 1% Revenues AEBITDA Outsourcing & Advisory Leasing Capital Markets Colliers 10 Second Quarter (US$ millions) Investment Management GAAP Operating Earnings: Q2 2024 $55.0M at 43.7% margin; Q2 2023 $26.4M at 22.2% margin Incremental revenues from new investor capital commitments Adjusted EBITDA improved on higher revenues, partly offset by increased investments in new products, strategies and fundraising capabilities AUM of $96.4 billion as of June 30, 2024 relative to $96.3 billion as of March 31, 2024 Revenues AEBITDA 4 4 Investment Management USD LC Revenue Growth 6% 6%

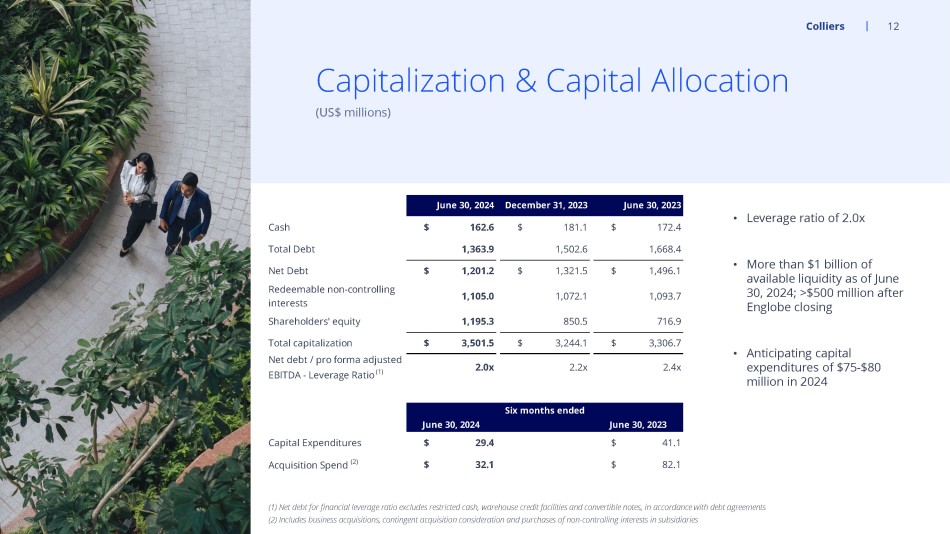

36% 52% 12% Perpetual Capital Long-dated Funds Managed Accounts AUM by Strategy Colliers 11 Investment Management 51% 22% 23% 4% Alternatives Infrastructure Traditional Real Estate Credit AUM by Asset Class 78% 22% North America EMEA AUM by Geography AUM: $96.4B | FPAUM: $49.8B Focus on long - duration, highly differentiated AUM • Leverage ratio of 2.0x • More than $1 billion of available liquidity as of June 30, 2024; >$500 million after Englobe closing • Anticipating capital expenditures of $75 - $80 million in 2024 Colliers 12 (US$ millions) Capitalization & Capital Allocation Cash $ 162.6 $ 181.1 $ 172.4 Total Debt 1,363.9 1,502.6 1,668.4 Net Debt $ 1,201.2 $ 1,321.5 $ 1,496.1 Redeemable non-controlling interests 1,105.0 1,072.1 1,093.7 Shareholders' equity 1,195.3 850.5 716.9 Total capitalization $ 3,501.5 $ 3,244.1 $ 3,306.7 Net debt / pro forma adjusted EBITDA - Leverage Ratio (1) 2.0x 2.2x 2.4x Capital Expenditures $ 29.4 $ 41.1 Acquisition Spend (2) $ 32.1 $ 82.1 Six months ended June 30, 2024 June 30, 2023 June 30, 2024 December 31, 2023 June 30, 2023 (1) Net debt for financial leverage ratio excludes restricted cash, warehouse credit facilities and convertible notes, in acc ord ance with debt agreements (2) Includes business acquisitions, contingent acquisition consideration and purchases of non - controlling interests in subsidiar ies Outlook for 2024 unchanged, except to reflect the partial year impact of the acquisition of Englobe Colliers 13 The financial outlook is based on the Company’s best available information as of the date of this presentation, and remains s ubj ect to change based on numerous macroeconomic, geopolitical, health, social and related factors.

Continued interest rate volatility and/or lack of credit ava ila bility for commercial real estate transactions could materially impact the outlook. 2024 Outlook Revised (with Englobe) Englobe Prior Actual 2023 Measure +8% to +13% +3% +5% to +10% - 3% Revenue growth +8% to +18% +3% +5% to +15% - 6% Adjusted EBITDA growth +11% to +21% +1% +10% to +20% - 23% Adjusted EPS growth (US$ millions) Outlook for 2024 Appendix Reconciliation of non - GAAP measures

Colliers 15 Reconciliation of GAAP earnings to adjusted EBITDA (US$ thousands) Net earnings $ 71,927 $ 35,001 $ 86,063 $ 34,094 Income tax 24,377 16,477 34,347 20,016 Other income, including equity earnings from non-consolidated investments (932) (886) (1,583) (4,206) Interest expense, net 19,376 24,670 39,248 47,502 Operating earnings 114,748 75,262 158,075 97,406 Loss on disposal of business operations - 2,282 - 2,282 Depreciation and amortization 49,845 50,794 100,353 100,286 Gains attributable to MSRs (3,712) (6,052) (5,027) (9,087) Equity earnings from non-consolidated entites 796 532 1,232 3,686 Acquisition-related items (15,221) 11,668 (13,281) 38,136 Restructuring costs 1,722 7,038 8,833 7,781 Stock-based compensation expense 7,446 5,556 14,134 11,213 Adjusted EBITDA $ 155,624 $ 147,080 $ 264,319 $ 251,703 Three months ended Six months ended June 30, 2024 June 30, 2023 June 30, 2024 June 30, 2023 Colliers 16 Reconciliation of GAAP earnings to adjusted net earnings and adjusted earnings per share Adjusted EPS is calculated using the “if - converted” method of calculating earnings per share in relation to the Convertible Note s, which were issued on May 19, 2020 and fully converted or redeemed by June 1, 2023 (US$ thousands) Net earnings $ 71,927 $ 35,001 $ 86,063 $ 34,094 Non-controlling interest share of earnings (11,224) (13,816) (20,145) (24,757) Interest on Convertible Notes - 561 - 2,861 Loss on disposal of operations - 2,282 - 2,282 Amortization of intangible assets 34,385 37,330 69,471 74,173 Gains attributable to MSRs (3,712) (6,052) (5,027) (9,087) Acquisition-related items (15,221) 11,668 (13,281) 38,136 Restructuring costs 1,722 7,038 8,833 7,781 Stock-based compensation expense 7,446 5,556 14,134 11,213 Income tax on adjustments (9,606) (11,845) (20,733) (23,193) Non-controlling interest on adjustments (7,141) (5,773) (13,271) (10,926) Adjusted net earnings $ 68,576 $ 61,950 $ 106,044 $ 102,577 (US$) Diluted net earnings (loss) per common share $ 0.73 $ (0.14) $ 0.99 $ (0.57) Interest on Convertible Notes, net of tax - 0.01 - 0.04 Non-controlling interest redemption increment 0.48 0.59 0.33 0.77 Loss on disposal of operations - 0.05 - 0.05 Amortization expense, net of tax 0.41 0.49 0.88 0.97 Gains attributable to MSRs, net of tax (0.04) (0.07) (0.06) (0.11) Acquisition-related items (0.36) 0.19 (0.37) 0.70 Restructuring costs, net of tax 0.02 0.11 0.14 0.12 Stock-based compensation expense, net of tax 0.12 0.08 0.22 0.19 Adjusted EPS $ 1.36 $ 1.31 $ 2.13 $ 2.16 Diluted weighted average shares for Adjusted EPS (thousands) 50,479 47,422 49,671 47,442 Three months ended Six months ended June 30, 2024 June 30, 2023 June 30, 2024 June 30, 2023 Three months ended Six months ended June 30, 2024 June 30, 2023 June 30, 2024 June 30, 2023 Colliers 17 Reconciliation of net cash flow from operations to free cash flow (US$ thousands) Net cash provided by (used in) operating activities $ 141,189 $ 98,973 $ 3,574 $ (33,595) Contingent acquisition consideration paid 300 2,719 3,038 2,991 Purchase of fixed assets (12,480) (22,179) (29,353) (41,062) Cash collections on AR Facility deferred purchase price 34,930 28,539 68,848 59,311 Distributions paid to non-controlling interests (38,521) (40,059) (48,827) (51,120) Free cash flow $ 125,418 $ 67,993 $ (2,720) $ (63,475) Three months ended Six months ended June 30, 2024 June 30, 2023 June 30, 2024 June 30, 2023

Local currency revenue and adjusted EBITDA growth rate and internal revenue growth rate measures Percentage revenue and adjusted EBITDA variances presented on a local currency basis are calculated by translating the current period results of our non - US dollar denominated operations to US dollars using the foreign currency exchange rates from the periods against which the current period results are being compared. Percentage revenue variances presented on an internal growth basis are calculated assuming no impact from acquired entities in the current and prior periods. Revenue from acquired entities, including any foreign exchange impacts, are treated as acquisition growth until the respective anniversaries of the acquisitions. We believe that these revenue growth rate methodologies provide a framework for assessing the Company’s performance and operations excluding the effects of foreign currency exchange rate fluctuations and acquisitions. Since these revenue growth rate measures are not calculated under GAAP, they may not be comparable to similar measures used by other issuers. Assets under management We use the term assets under management (“AUM”) as a measure of the scale of our Investment Management operations. AUM is defined as the gross market value of operating assets and the projected gross cost of development assets of the funds, partnerships and accounts to which we provide management and advisory services, including capital that such funds, partnerships and accounts have the right to call from investors pursuant to capital commitments. Our definition of AUM may differ from those used by other issuers and as such may not be directly comparable to similar measures used by other issuers. Fee paying assets under management We use the term fee paying assets under management (“FPAUM”) to represent only the AUM on which the Company is entitled to receive management fees. We believe this measure is useful in providing additional insight into the capital base upon which the Company earns management fees. Our definition of FPAUM may differ from those used by other issuers and as such may not be directly comparable to similar measures used by other issuers. Recurring revenue percentage Recurring revenue percentage is computed on a trailing twelve - month basis and represents the proportion that is derived from Outsourcing & Advisory and Investment Management service lines. Both these service lines represent medium to long - term duration revenue streams that are either contractual or repeatable in nature. Revenue for this purpose incorporates the expected full year impact of acquisitions and dispositions. Adjusted EBITDA from recurring revenue percentage Adjusted EBITDA from recurring revenue percentage is computed on a trailing twelve - month basis and represents the proportion of adjusted EBITDA that is derived from Outsourcing & Advisory and Investment Management service lines. Both these service lines represent medium to long - term duration revenue streams that are either contractual or repeatable in nature. Adjusted EBITDA for this purpose is calculated in the same manner as calculated for our debt agreement covenant calculation purposes, incorporating the expected full year impact of business acquisitions and dispositions. Colliers 18 Other Non - GAAP Measures