|

Oklahoma

|

001-38656

|

20-0764349

|

|

(State or other jurisdiction of incorporation)

|

(Commission File Number)

|

(IRS Employer Identification No.)

|

| ☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

|

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

|

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

|

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

|

|

Title of each class

|

Trading

Symbol(s)

|

Name of each exchange on which

registered

|

|

Common Stock, $0.01 par value

|

BSVN

|

The NASDAQ Global Select Market

|

| Item 2.02. |

Results of Operations and Financial Condition

|

| Item 7.01 |

Regulation FD Disclosure

|

|

Item 9.01

|

Financial Statements and Exhibits

|

|

(d)

|

Exhibits.

|

|

Item

|

Description

|

|

|

Press Release dated January 26, 2023

|

||

|

Fourth Quarter and Full Year 2022 Investor Presentation

|

||

|

BANK7 CORP.

|

||

|

Date: January 26, 2023

|

By:

|

/s/ Kelly J. Harris

|

|

Kelly J. Harris

|

||

|

Executive Vice President and Chief Financial Officer

|

||

|

|

- |

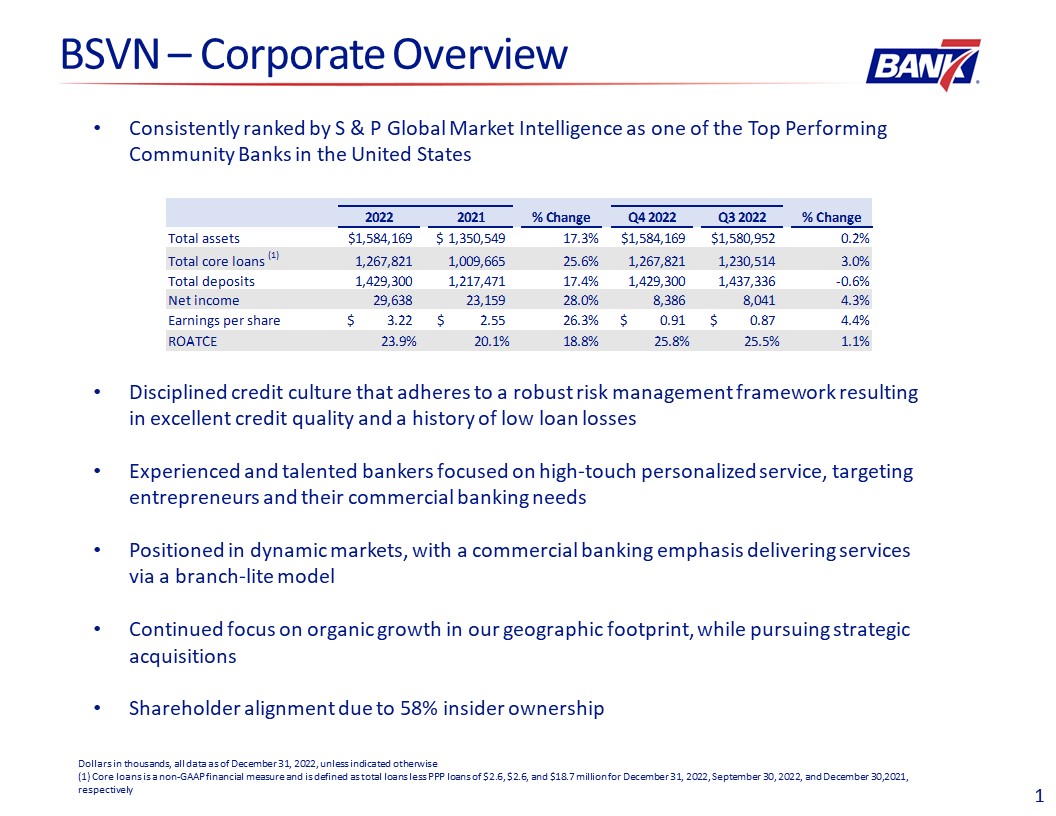

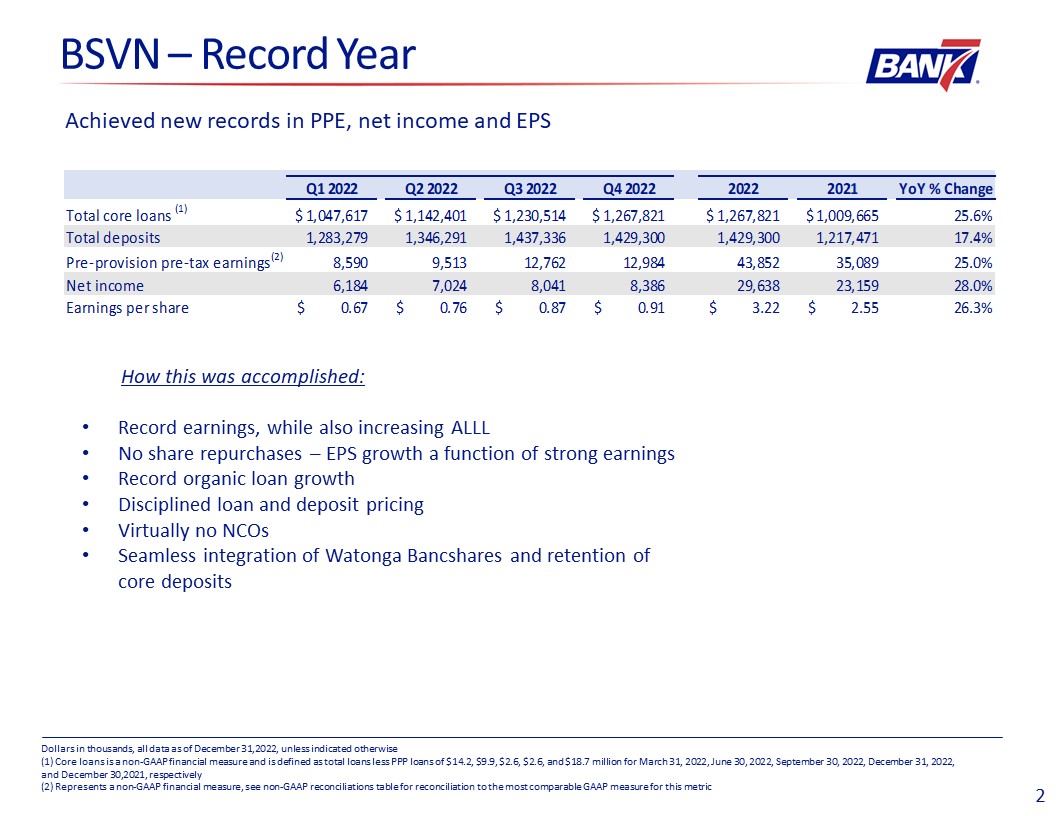

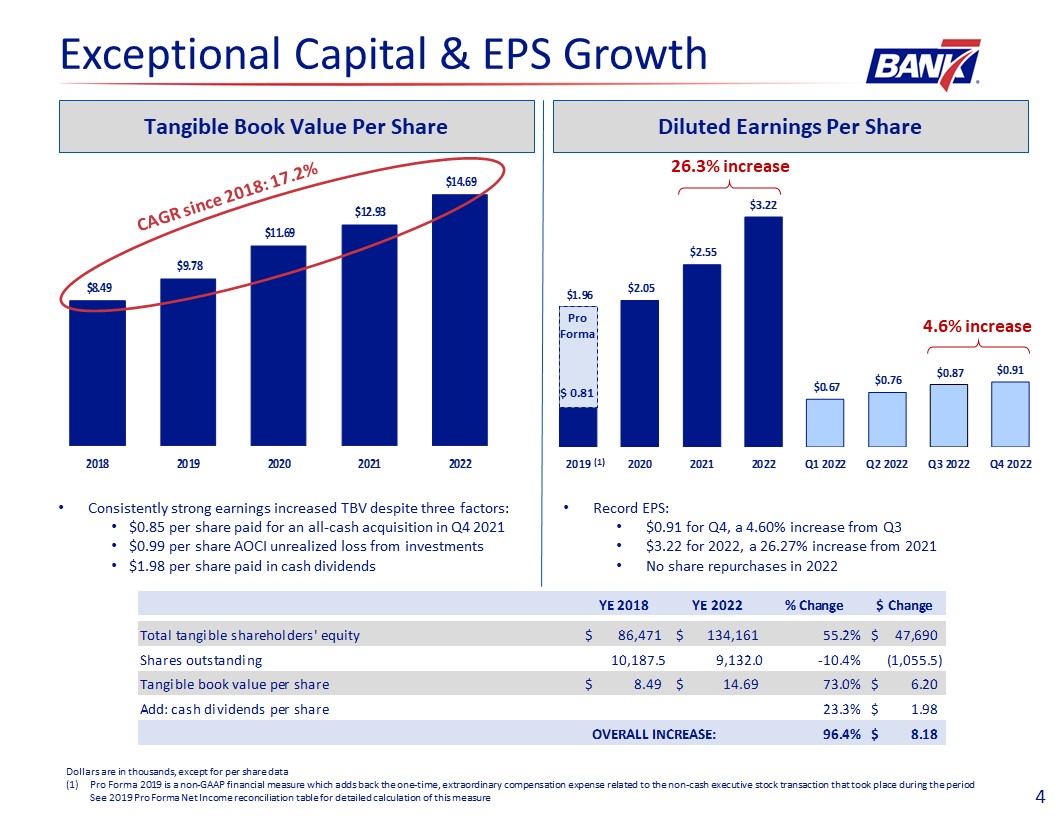

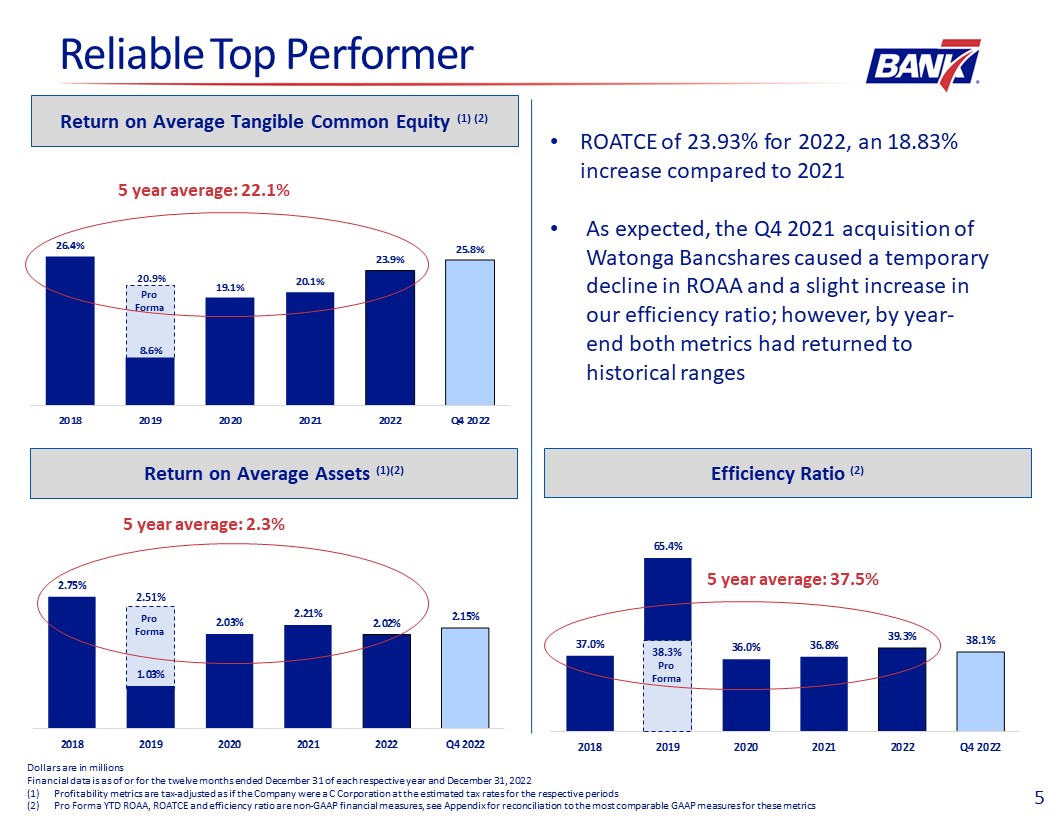

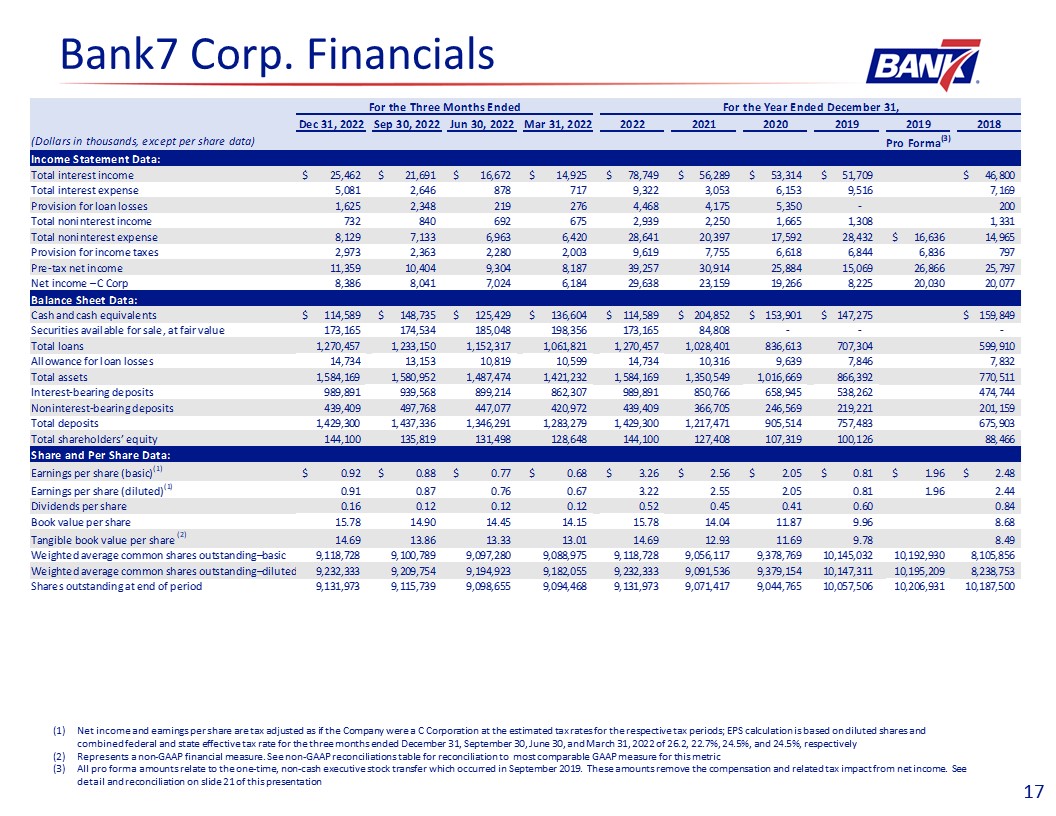

Net income of $29.6 million compared to $23.2 million, an increase of 27.98%

|

|

|

- |

Earnings per share of $3.22 compared to $2.55, an increase of 26.27%

|

|

|

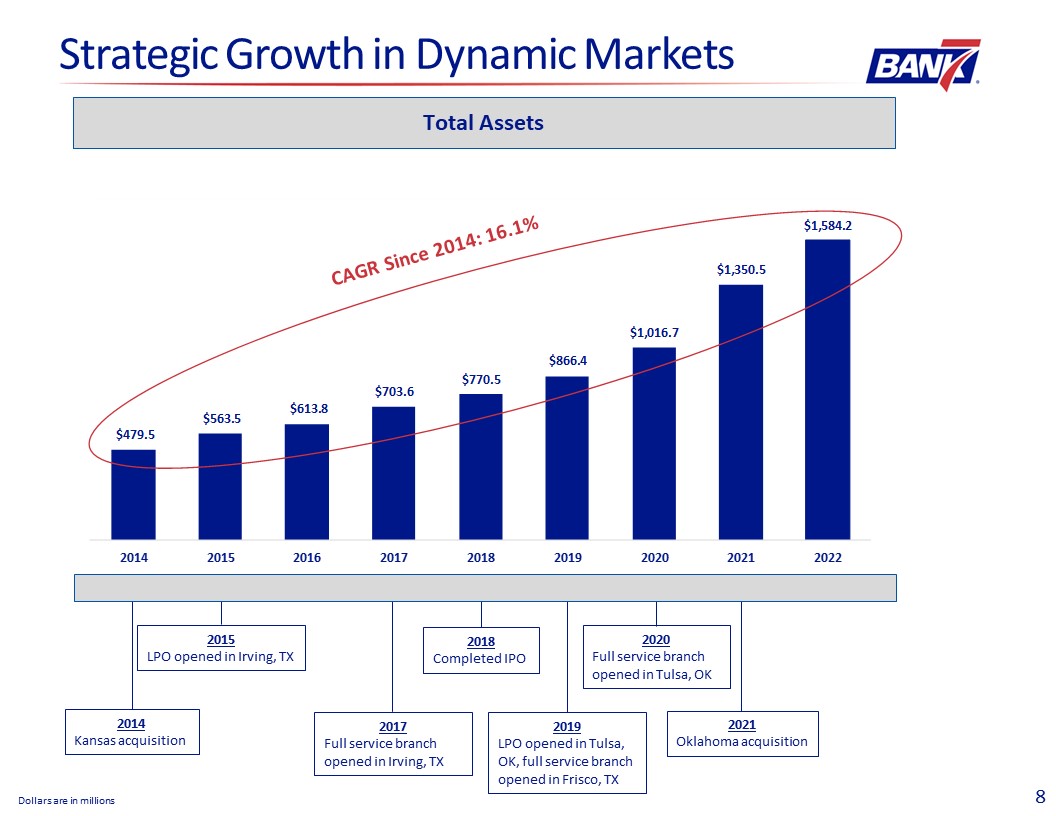

- |

Total assets of $1.6 billion compared to $1.4 billion, an increase of 17.30%

|

|

|

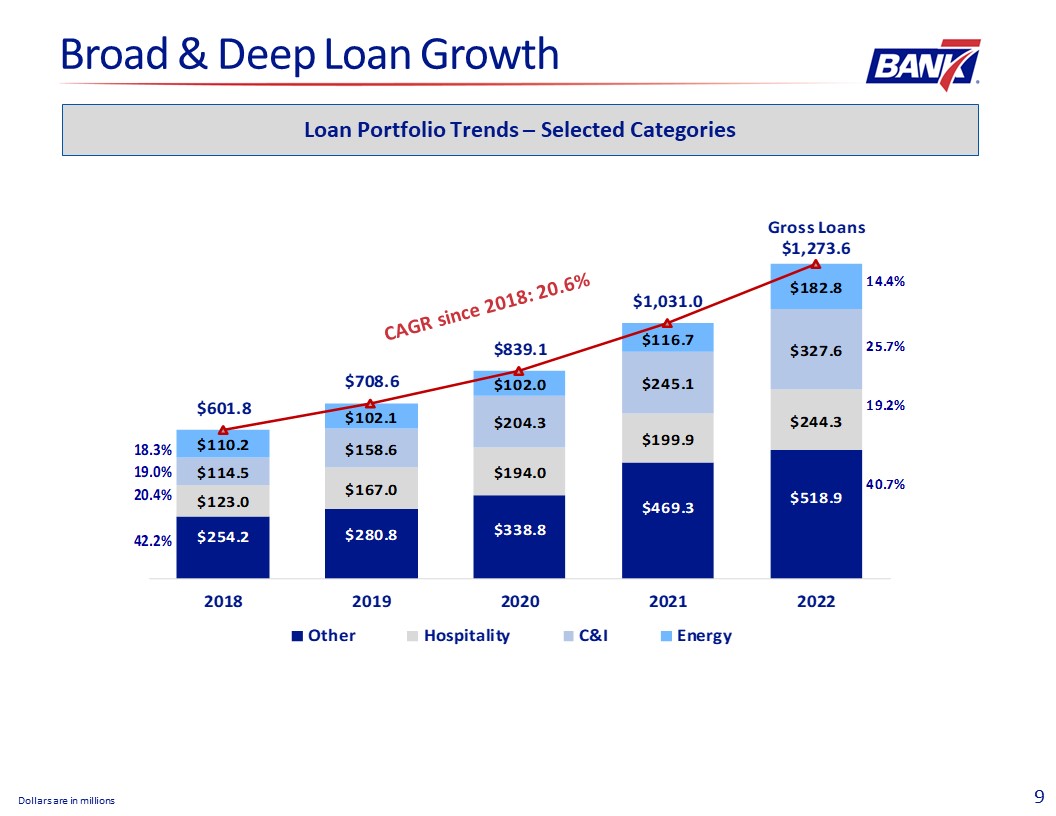

- |

Total loans of $1.3 billion compared to $1.0 billion, an increase of 23.54%

|

|

|

- |

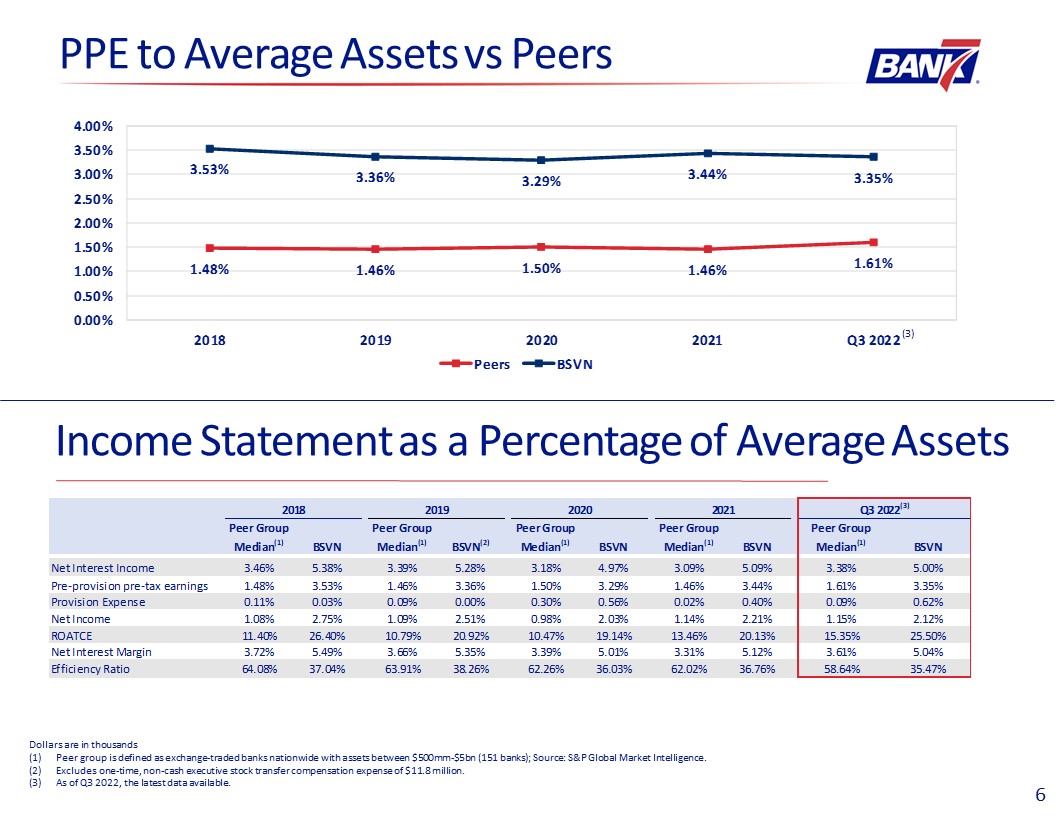

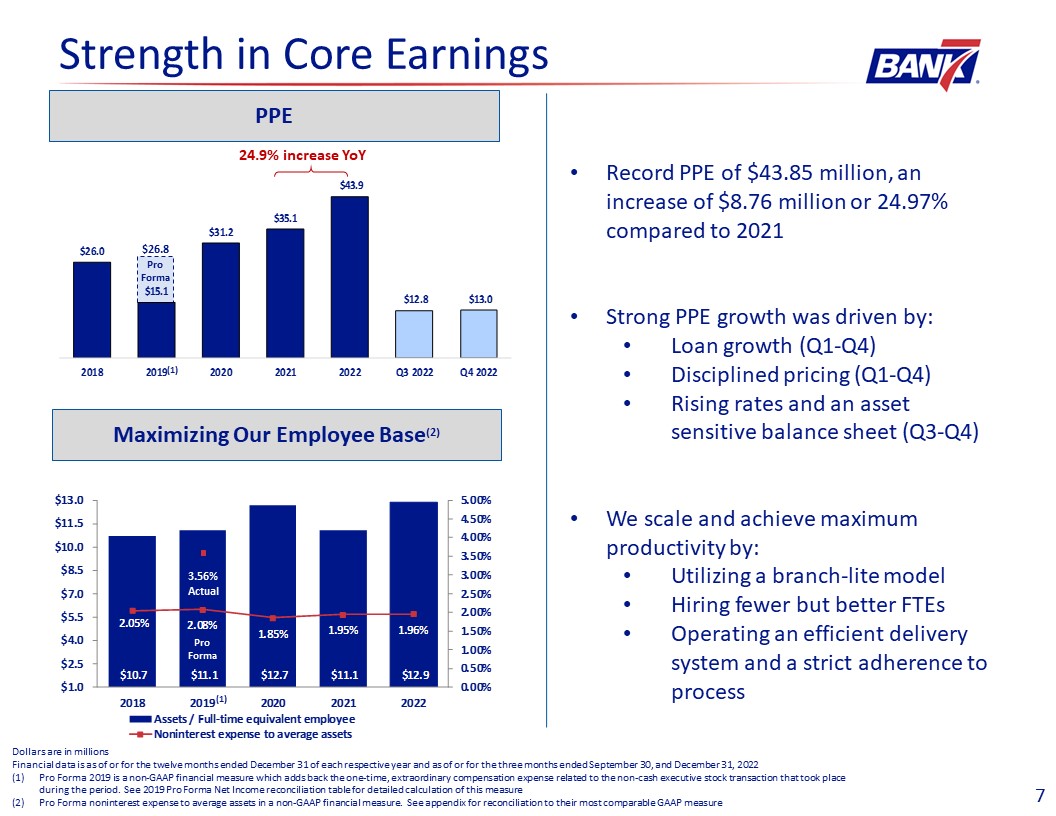

PPE of $43.9 million compared to $35.1 million, an increase of 24.97%

|

|

|

- |

Total interest income of $78.7 million compared to $56.3 million, an increase of 39.90%

|

|

|

- |

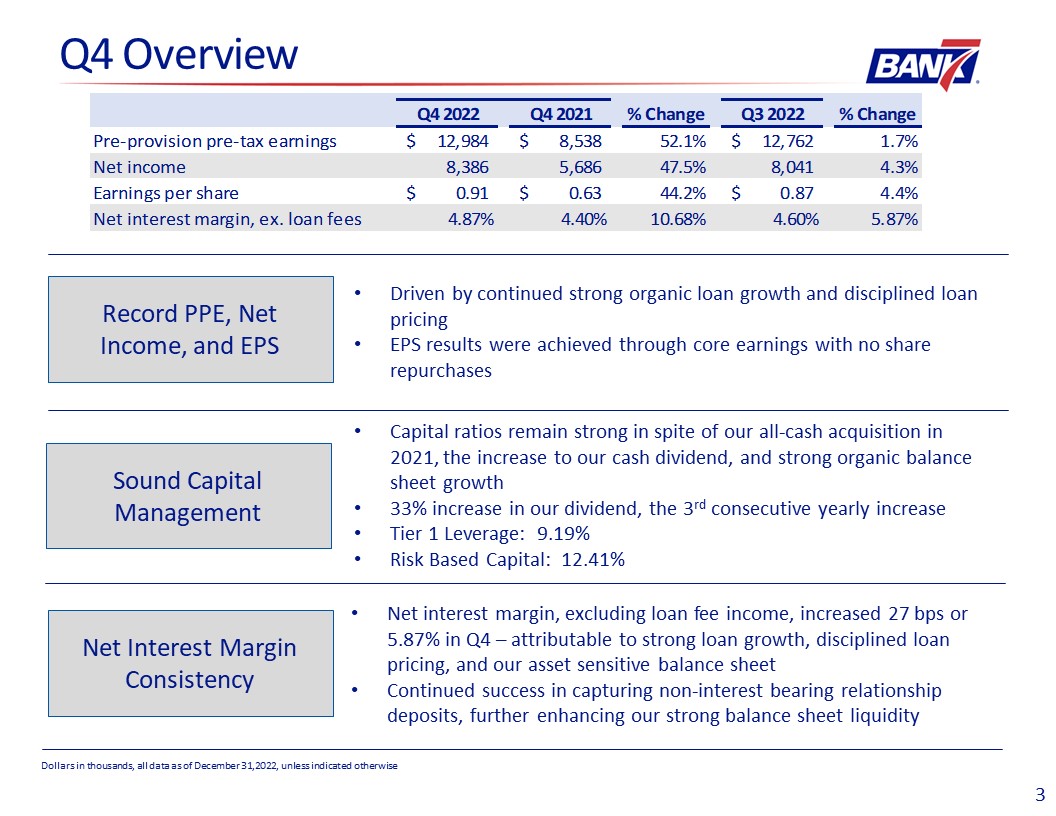

Net income of $8.4 million compared to $8.0 million, an increase of 4.29%

|

|

|

- |

Earnings per share of $0.91 compared to $0.87, an increase of 4.60%

|

|

|

- |

PPE of $13.0 million compared to $12.8 million, an increase of 1.74%

|

|

|

- |

Total interest income of $25.5 million compared to $21.7 million, an increase of 17.39%

|

|

Assets

|

December 31,

2022

(unaudited)

|

December 31,

2021

|

||||||

|

|

||||||||

|

Cash and due from banks

|

$

|

109,115

|

$

|

195,359

|

||||

|

Federal funds sold

|

-

|

9,493

|

||||||

|

Cash and cash equivalents

|

109,115

|

204,852

|

||||||

|

Interest-bearing time deposits in other banks

|

5,474

|

3,237

|

||||||

|

Available-for-sale debt securities

|

173,165

|

84,808

|

||||||

|

Loans, net of allowance for loan losses of $14,734 and $10,316 at December 31, 2022

and December 31, 2021, respectively

|

1,255,722

|

1,018,085

|

||||||

|

Loans held for sale, at fair value

|

-

|

464

|

||||||

|

Premises and equipment, net

|

13,106

|

17,257

|

||||||

|

Nonmarketable equity securities

|

1,209

|

1,202

|

||||||

|

Core deposit intangibles

|

1,336

|

1,643

|

||||||

|

Goodwill

|

8,603

|

8,479

|

||||||

|

Interest receivable and other assets

|

16,439

|

10,522

|

||||||

|

|

||||||||

|

Total assets

|

$

|

1,584,169

|

$

|

1,350,549

|

||||

|

Liabilities and Shareholders’ Equity

|

||||||||

|

Deposits

|

||||||||

|

Noninterest-bearing

|

$

|

439,409

|

$

|

366,705

|

||||

|

Interest-bearing

|

989,891

|

850,766

|

||||||

|

Total deposits

|

1,429,300

|

1,217,471

|

||||||

|

|

||||||||

|

Income taxes payable

|

1,054

|

-

|

||||||

|

Interest payable and other liabilities

|

9,715

|

5,670

|

||||||

|

Total liabilities

|

1,440,069

|

1,223,141

|

||||||

|

Shareholders’ equity

|

||||||||

|

|

||||||||

|

Common stock, $0.01 par value; 50,000,000 shares authorized; shares issued and outstanding:

9,131,973 and 9,071,417 at December 31, 2022 and December 31, 2021 respectively |

91

|

91

|

||||||

|

|

||||||||

|

Additional paid-in capital

|

95,263

|

94,024

|

||||||

|

Retained earnings

|

58,049

|

33,149

|

||||||

|

Accumulated other comprehensive income (loss)

|

(9,303

|

)

|

144

|

|||||

|

Total shareholders’ equity

|

144,100

|

127,408

|

||||||

|

|

||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,584,169

|

$

|

1,350,549

|

||||

|

Three months ended

December 31,

|

Twelve months ended

December 31,

|

|||||||||||||||

|

2022

(unaudited)

|

2021

|

2022

(unaudited)

|

2021

|

|||||||||||||

|

Interest Income

|

||||||||||||||||

|

Loans, including fees

|

$

|

23,806

|

$

|

14,391

|

$

|

74,403

|

$

|

55,768

|

||||||||

|

Interest-bearing time deposits in other banks

|

7

|

28

|

46

|

169

|

||||||||||||

|

Debt securities, taxable

|

688

|

143

|

2,313

|

143

|

||||||||||||

|

Debt securities, tax-exempt

|

87

|

31

|

360

|

31

|

||||||||||||

|

Other interest and dividend income

|

874

|

63

|

1,627

|

178

|

||||||||||||

|

Total interest income

|

25,462

|

14,656

|

78,749

|

56,289

|

||||||||||||

|

Interest Expense

|

||||||||||||||||

|

Deposits

|

5,081

|

677

|

9,322

|

3,053

|

||||||||||||

|

Total interest expense

|

5,081

|

677

|

9,322

|

3,053

|

||||||||||||

|

Net Interest Income

|

20,381

|

13,979

|

69,427

|

53,236

|

||||||||||||

|

Provision for Loan Losses

|

1,625

|

850

|

4,468

|

4,175

|

||||||||||||

|

Net Interest Income After Provision for Loan Losses

|

18,756

|

13,129

|

64,959

|

49,061

|

||||||||||||

|

Noninterest Income

|

||||||||||||||||

|

Secondary market income

|

91

|

182

|

486

|

435

|

||||||||||||

|

Loss on sales and calls of available-for-sale debt securities

|

-

|

-

|

(127

|

)

|

-

|

|||||||||||

|

Service charges on deposit accounts

|

222

|

170

|

900

|

550

|

||||||||||||

|

Other

|

419

|

405

|

1,680

|

1,265

|

||||||||||||

|

Total noninterest income

|

732

|

757

|

2,939

|

2,250

|

||||||||||||

|

Noninterest Expense

|

||||||||||||||||

|

Salaries and employee benefits

|

4,892

|

3,298

|

17,040

|

11,983

|

||||||||||||

|

Furniture and equipment

|

334

|

232

|

1,468

|

883

|

||||||||||||

|

Occupancy

|

593

|

508

|

2,329

|

1,899

|

||||||||||||

|

Data and item processing

|

600

|

380

|

2,068

|

1,237

|

||||||||||||

|

Accounting, marketing and legal fees

|

203

|

353

|

984

|

800

|

||||||||||||

|

Regulatory assessments

|

371

|

140

|

1,344

|

604

|

||||||||||||

|

Advertsing and public relations

|

164

|

101

|

477

|

282

|

||||||||||||

|

Travel, lodging and entertainment

|

147

|

100

|

363

|

409

|

||||||||||||

|

Other

|

825

|

1,086

|

2,568

|

2,300

|

||||||||||||

|

Total noninterest expense

|

8,129

|

6,198

|

28,641

|

20,397

|

||||||||||||

|

Income Before Taxes

|

11,359

|

7,688

|

39,257

|

30,914

|

||||||||||||

|

Income tax expense

|

2,973

|

2,002

|

9,619

|

7,755

|

||||||||||||

|

Net Income

|

$

|

8,386

|

$

|

5,686

|

$

|

29,638

|

$

|

23,159

|

||||||||

|

Earnings per common share - basic

|

$

|

0.92

|

$

|

0.64

|

$

|

3.26

|

$

|

2.56

|

||||||||

|

Earnings per common share - diluted

|

0.91

|

0.63

|

3.22

|

2.55

|

||||||||||||

|

Weighted average common shares outstanding - basic

|

9,118,728

|

9,070,967

|

9,101,523

|

9,056,117

|

||||||||||||

|

Weighted average common shares outstanding - diluted

|

9,232,333

|

9,162,124

|

9,204,716

|

9,091,536

|

||||||||||||

|

Other Comprehensive Income (Loss)

|

||||||||||||||||

|

|

||||||||||||||||

|

Unrealized losses on securities, net of tax benefit of $0 and $0 for the three months ended

December 31, 2022 and 2021, respectively; $2.8 million and $0 for the twelve months ended

December 31, 2022 and 2021, respectively

|

$

|

1,146

|

$

|

144

|

$

|

(9,543

|

)

|

$

|

144

|

|||||||

|

|

||||||||||||||||

|

Reclassification adjustment for realized (gain)loss included in net income, net of tax of $0 and

$0 for the three months ended December 31, 2022 and 2021, respectively; $31 and $0 for the

twelve months ended December 30, 2022 and 2021, respectively

|

-

|

-

|

96

|

-

|

||||||||||||

|

Other comprehensive loss

|

$

|

1,146

|

$

|

144

|

$

|

(9,447

|

)

|

$

|

144

|

|||||||

|

Comprehensive Income (Loss)

|

$

|

9,532

|

$

|

5,830

|

$

|

20,191

|

$

|

23,303

|

||||||||

|

Net Interest Margin

|

||||||||||||||||||||||||

|

For the Twelve Months Ended December 31,

|

||||||||||||||||||||||||

|

2022

(unaudited)

|

2021

|

|||||||||||||||||||||||

|

Average

Balance

|

Interest

Income/

Expense

|

Average

Yield/

Rate

|

Average

Balance

|

Interest

Income/

Expense

|

Average

Yield/

Rate

|

|||||||||||||||||||

|

(Dollars in thousands)

|

||||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

129,624

|

$

|

1,673

|

1.29

|

%

|

$

|

126,136

|

$

|

347

|

0.28

|

%

|

||||||||||||

|

Investment securities, taxable

|

145,915

|

2,313

|

1.59

|

4,663

|

143

|

3.07

|

||||||||||||||||||

|

Debt securities, tax exempt

|

21,635

|

360

|

1.66

|

1,852

|

31

|

1.67

|

||||||||||||||||||

|

Loans held for sale

|

586

|

-

|

-

|

318

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,143,380

|

74,403

|

6.51

|

905,804

|

55,768

|

6.16

|

||||||||||||||||||

|

Total interest-earning assets

|

1,441,140

|

78,749

|

5.46

|

1,038,773

|

56,289

|

5.42

|

||||||||||||||||||

|

Noninterest-earning assets

|

23,532

|

7,361

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,464,672

|

$

|

1,046,134

|

||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

724,617

|

7,842

|

1.08

|

%

|

$

|

430,268

|

1,396

|

0.32

|

%

|

||||||||||||||

|

Time deposits

|

165,735

|

1,480

|

0.89

|

205,437

|

1,657

|

0.81

|

||||||||||||||||||

|

Total interest-bearing deposits

|

890,352

|

9,322

|

1.05

|

635,705

|

3,053

|

0.48

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

890,352

|

9,322

|

1.05

|

635,705

|

3,053

|

0.48

|

||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

432,901

|

288,446

|

||||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

7,520

|

4,930

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

440,421

|

293,376

|

||||||||||||||||||||||

|

Shareholders' equity

|

133,899

|

117,053

|

||||||||||||||||||||||

|

Total liabilities and shareholders' equity

|

$

|

1,464,672

|

$

|

1,046,134

|

||||||||||||||||||||

|

Net interest income

|

$

|

69,427

|

$

|

53,236

|

||||||||||||||||||||

|

Net interest spread

|

4.42

|

%

|

4.94

|

%

|

||||||||||||||||||||

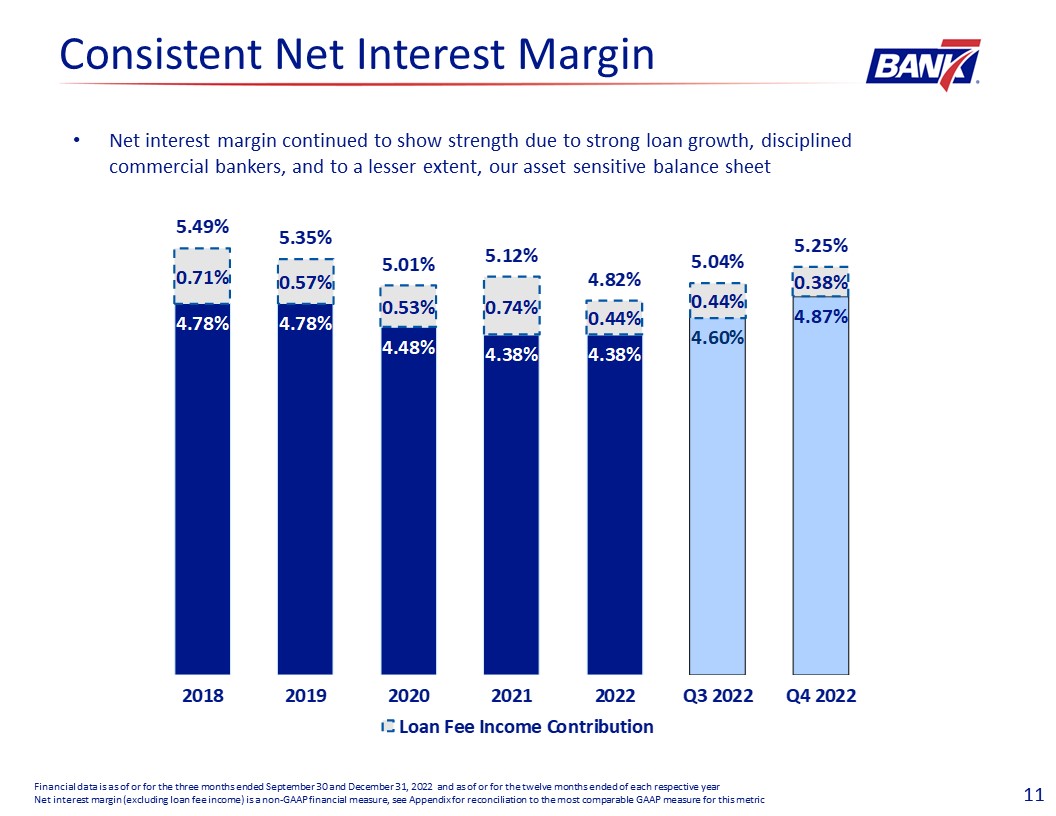

|

Net interest margin

|

4.82

|

%

|

5.12

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|

|

|

For the Three Months Ended December 31,

|

|

||||||||||||||||||||||

|

|

2022

(unaudited)

|

|

|

2021

|

|

|||||||||||||||||||

|

|

Average

Balance

|

Interest

Income/

Expense

|

Average

Yield/

Rate

|

|

|

Average

Balance

|

Interest

Income/

Expense

|

Average

Yield/

Rate

|

|

|||||||||||||||

|

(Dollars in thousands)

|

||||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

101,427

|

$

|

881

|

3.45

|

%

|

$

|

130,106

|

$

|

91

|

0.23

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

154,869

|

688

|

1.76

|

14,992

|

143

|

3.78

|

||||||||||||||||||

|

Debt securities, tax exempt

|

20,247

|

87

|

1.70

|

7,349

|

31

|

16.67

|

||||||||||||||||||

|

Loans held for sale

|

291

|

-

|

-

|

1,090

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,262,864

|

23,806

|

7.48

|

959,243

|

14,391

|

5.95

|

||||||||||||||||||

|

Total interest-earning assets

|

1,539,698

|

25,462

|

6.56

|

1,112,780

|

14,656

|

5.23

|

||||||||||||||||||

|

Noninterest-earning assets

|

21,937

|

11,613

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,561,635

|

$

|

1,124,393

|

||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

798,073

|

4,491

|

2.23

|

%

|

$

|

490,739

|

373

|

0.30

|

%

|

||||||||||||||

|

Time deposits

|

157,211

|

590

|

1.49

|

183,867

|

304

|

0.66

|

||||||||||||||||||

|

Total interest-bearing deposits

|

955,284

|

5,081

|

2.11

|

674,606

|

677

|

0.40

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

$

|

955,284

|

5,081

|

2.11

|

$

|

674,606

|

677

|

0.40

|

||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

$

|

457,753

|

$

|

320,290

|

||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

8,683

|

5,181

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

466,436

|

325,471

|

||||||||||||||||||||||

|

Shareholders' equity

|

139,915

|

124,316

|

||||||||||||||||||||||

|

Total liabilities and shareholders' equity

|

$

|

1,561,635

|

$

|

1,124,393

|

||||||||||||||||||||

|

Net interest income

|

$

|

20,381

|

$

|

13,979

|

||||||||||||||||||||

|

Net interest spread

|

4.46

|

%

|

4.83

|

%

|

||||||||||||||||||||

|

Net interest margin

|

5.25

|

%

|

4.98

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|