Document

MANAGEMENT'S DISCUSSION & ANALYSIS

March 31, 2025

May 14, 2025

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This discussion and analysis should be read in conjunction with our unaudited condensed interim consolidated financial statements and notes thereto as at and for the three months ended March 31, 2025, and should also be read in conjunction with the audited consolidated financial statements and Management's Discussion and Analysis of Financial Condition and Results of Operations ("MD&A") contained in our annual report for the year ended December 31, 2024. The financial statements have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB"). Unless otherwise indicated, all references to "$" and "dollars" in this discussion and analysis mean thousands of Canadian dollars.

All references in this MD&A to "the Company," "Oncolytics," "we," "us," or "our" and similar expressions refer to Oncolytics Biotech Inc. and the subsidiaries through which it conducts its business unless otherwise indicated.

Forward-Looking Statements

The following discussion contains forward-looking statements, within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended and forward-looking information under applicable Canadian securities laws (such forward-looking statements and forward-looking information are collectively referred to herein as "forward-looking statements"). Forward-looking statements, including:

•our belief as to the potential and mechanism of action of pelareorep, an intravenously delivered immunotherapeutic agent, as a cancer therapeutic;

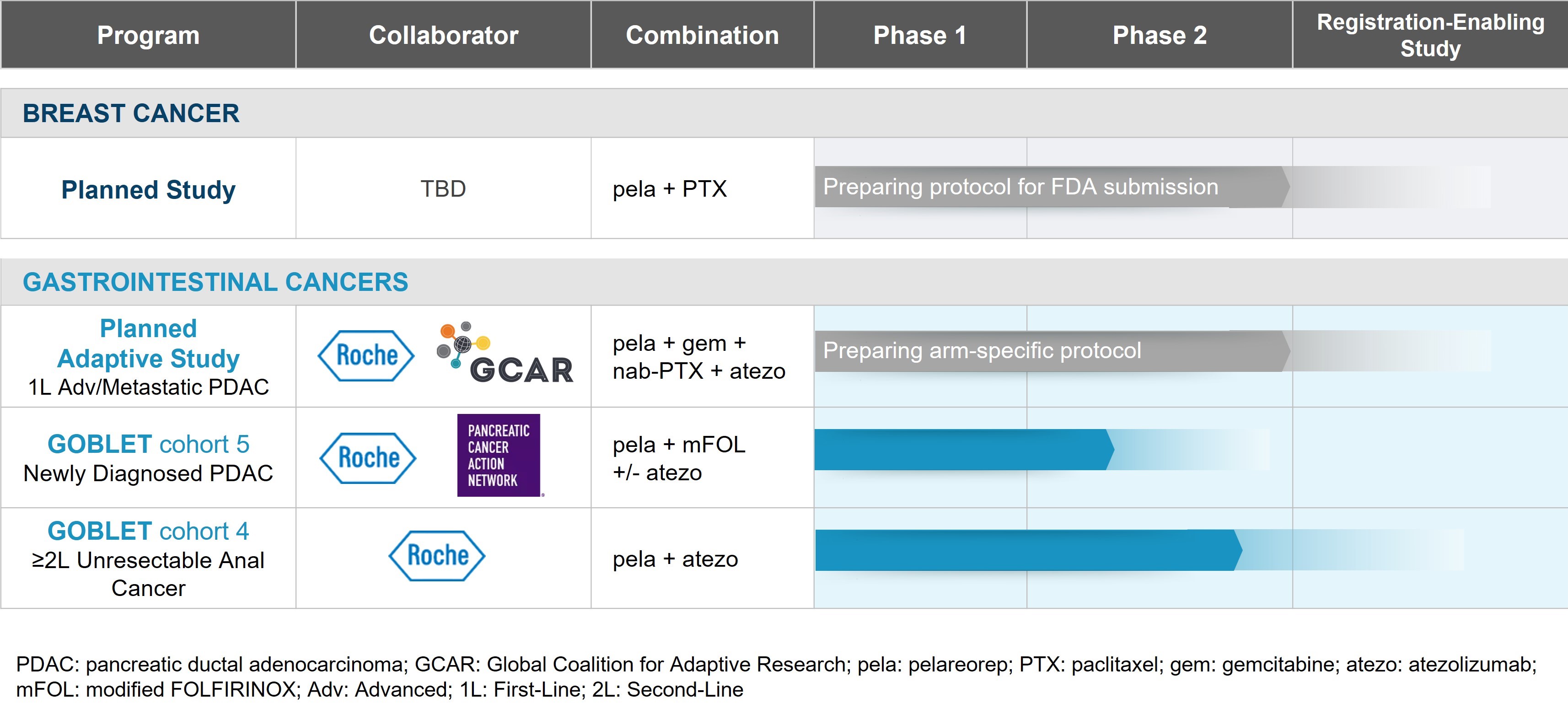

•our business strategy, goals, focus, and objectives for the development of pelareorep, including our immediate primary focus on advancing our programs in hormone receptor-positive / human epidermal growth factor 2-negative advanced and metastatic breast cancer and metastatic pancreatic ductal adenocarcinoma to registration-enabling clinical studies and our exploration of opportunities for registrational programs in other gastrointestinal cancers, including anal cancer, through our GOBLET platform study;

•our expectation that pelareorep’s ability to enhance innate and adaptive immune responses within the TME will play an increasingly important role as our clinical development program advances, and our belief that this approach increases opportunities for expanding our clinical program and business development and partnering opportunities, has the most promise for generating clinically impactful data and offers the most expeditious path to regulatory approval;

•our belief that by priming the immune system with pelareorep, we can increase the proportion of patients who respond to various cancer treatments, including immunotherapies, especially in cancers where existing treatment regimens have failed or provided limited benefit;

•our expectation that we will incur substantial losses and will not generate significant revenues until and unless pelareorep becomes commercially viable;

•our estimations that we can fund operations through the third quarter of 2025;

•our plans to fund ongoing operations by raising additional funds through the sale of our common shares or other capital resources, such as strategic collaborations and debt; the availability of additional liquidity and the terms thereof;

•our ability to reduce or eliminate planned expenditures to extend our operating runway if additional financing cannot be obtained when required;

•our plans to complete our CEO search and secure adequate funding, and actively evaluate multiple strategic options to advance the development of pelareorep;

•our plans to monitor the impact antibody-drug conjugate therapies on our breast cancer program and development strategy;

•our plans to continue working with various collaborators, academics, and stakeholders on the most effective path forward for the pancreatic cancer program;

•the focus of and plans for our manufacturing program and our belief that we have sufficient drug supply to support our clinical development program;

•our plans for our intellectual property program;

•our ongoing evaluation of all types of financing arrangements;

•the sale of securities under the Base Shelf (as defined herein) and our expectations regarding the ability of the Base Shelf to shorten the time required to close a financing and increase the number of potential investors that may be prepared to invest in the Company;

•our plans to use our ATM equity distribution and share purchase agreements to assist us in achieving our capital objective; our expectation that we will continue to access equity arrangements to help support our operations;

•our assessment of marketable securities;

•our objective to maintain adequate cash reserves to support our planned activities, including our clinical trial program, product manufacturing, administrative costs and intellectual property protection and the methods used to achieve such objective;

•our continued management of our research and development plan; our expectation to fund our expenditure requirements and commitments with existing working capital;

•the judgment applied in assessing our ability to continue as a going concern and the material uncertainties that raise substantial doubt on our ability to continue as a going concern;

•our belief that we are not able to fund our operations for at least the next twelve months from the balance sheet date with the cash and cash equivalents on hand;

•the factors that affect our cash usage;

•our expectation that we will increase our spending in connection with the research and development of pelareorep over the next several years as we look to advance our breast and gastrointestinal cancer programs into later stages of clinical development and the increased costs associated with later stages of clinical development;

•our expectation that we will continue to incur additional costs associated with operating as a public company;

•the factors that may affect the probability of successful commercialization of our drug candidates;

•our approach to credit rate, interest rate, foreign exchange, and liquidity risk mitigation;

•our anticipated use of the remaining proceeds raised as part of our 2023 public offering of common shares and warrants;

•the effectiveness of our internal control systems; and

•and other statements that are not historical facts or which are related to anticipated developments in our business and technologies.

In any forward-looking statement in which we express an expectation or belief as to future results, such expectations or beliefs are expressed in good faith and are believed to have a reasonable basis, but there can be no assurance that the statement or expectation, or belief will be achieved. Forward-looking statements involve known and unknown risks and uncertainties, which could cause our actual results to differ materially from those in the forward-looking statements.

Such risks and uncertainties include, among others, the need for and availability of funds and resources to pursue research and development projects, the efficacy of pelareorep as a cancer treatment, the success and timely completion of clinical studies and trials, our ability to successfully commercialize pelareorep, uncertainties related to the research, development, and manufacturing of pelareorep, uncertainties related to competition, changes in technology, the regulatory process, and general changes to the economic environment.

With respect to the forward-looking statements made within this MD&A, we have made numerous assumptions regarding, among other things: our ability to recruit and retain employees, our continued ability to obtain financing to fund our clinical development plan, our ability to receive regulatory approval to commence enrollment in the clinical studies which are part of our clinical development plan, our ability to maintain our supply of pelareorep, and future expense levels being within our current expectations.

Investors should consult our quarterly and annual filings with the Canadian and U.S. securities commissions for additional information on risks and uncertainties relating to the forward-looking statements. Forward-looking statements are based on assumptions, projections, estimates, and expectations of management at the time such forward-looking statements are made, and such assumptions, projections, estimates and/or expectations could change or prove to be incorrect or inaccurate. Investors are cautioned against placing undue reliance on forward-looking statements. We do not undertake any obligation to update these forward-looking statements except as required by applicable law.

Company Overview

We are a clinical-stage biopharmaceutical company developing pelareorep, a well-tolerated intravenously delivered immunotherapeutic agent that activates the innate and adaptive immune systems and weakens tumor defense mechanisms. This improves the ability of the immune system to fight cancer, making tumors more susceptible to a broad range of oncology treatments.

Pelareorep is a proprietary isolate of reovirus, a naturally occurring, non-pathogenic double-stranded RNA (dsRNA) reovirus commonly found in environmental waters. Pelareorep has shown promising results in changing the tumor microenvironment (TME). This creates a more immunologically favorable TME, which in turn makes the tumor more susceptible to various treatment combinations. These treatments include chemotherapies, checkpoint inhibitors, and other immuno-oncology approaches such as CAR T therapies, bispecific antibodies, and CDK4/6 inhibitors.

Pelareorep induces a new army of tumor-reactive T cells, helps these cells to infiltrate the tumor through an inflammatory process, and upregulates the expression of PD-1/PD-L1. By priming the immune system with pelareorep, we believe we can increase the proportion of patients who respond to various cancer treatments, including immunotherapies, especially in cancers where existing treatment regimens have failed or provided limited benefit.

As our clinical development program advances, we anticipate pelareorep's ability to enhance innate and adaptive immune responses within the TME will play an increasingly important role. This greatly increases opportunities for expanding our clinical program, business development, and partnering opportunities to address a broad range of cancers in combination with various other therapies. We believe this approach has the most promise for generating clinically impactful data and offers the most expeditious path to regulatory approval.

Our primary focus is to advance our programs in hormone receptor-positive / human epidermal growth factor 2-negative (HR+/HER2-) advanced and metastatic breast cancer (mBC) and metastatic pancreatic ductal adenocarcinoma (PDAC) to registration-enabling clinical studies. In addition, we are exploring opportunities for registrational programs in other gastrointestinal cancers, including anal cancer, through our GOBLET platform study.

Going Concern

We have not been profitable since our inception and expect to continue to incur substantial losses as we continue research and development efforts. We do not expect to generate significant revenues until and unless pelareorep becomes commercially viable. As at March 31, 2025, we had cash and cash equivalents of $15,303. Subsequent to March 31, 2025, we entered into a share purchase agreement with Alumni Capital LP (Alumni), where we have the right to sell, and Alumni has the obligation to purchase common shares over a 15-month period (see Financing Activity). We estimate we can currently fund our operations through the third quarter of 2025. We plan on raising additional funds through the sale of our common shares or other capital resources, such as collaborations and debt, to fund our ongoing operations. However, given the difficulty for micro-cap market capitalization companies to raise significant capital and the Nasdaq delinquency notification matter discussed below, there can be no assurance that additional liquidity will be available under acceptable terms or at all. Furthermore, if we are unable to obtain additional financing when required, there can be no assurance that we will be able to sufficiently reduce or eliminate our planned expenditures to extend our operating runway. These material uncertainties raise substantial doubt on our ability to continue as a going concern. See further discussion in "Liquidity and Capital Resources".

Program Development Updates and Outlook

The following are the development updates and outlook for each of our programs for the three months ended March 31, 2025, through to the date hereof:

Clinical Trial Program

In the first quarter of 2025, we presented updated results from GOBLET's anal cancer cohort at the 2025 American Society of Clinical Oncology (ASCO) Gastrointestinal Cancers Symposium. The updated results showed that four of twelve evaluable patients achieved a partial response for an objective response rate of 33%. This included one patient with a prolonged complete response that persisted for over 15 months. This was notable because historical response rates to checkpoint inhibitor monotherapy were low, generally 10-24%1-3. There continued to be no safety concerns with the treatment regimen. At treatment cycle four, tumor-infiltrating lymphocyte (TIL) clonal expansion was in the three responding patients for which data is available. Throughout the first quarter, we continued enrolling patients in this cohort.

Reference:

1.Rao S, et al. Phase II study of retifanlimab in patients (pts) with squamous carcinoma of the anal canal (SCAC) who progressed following platinum-based chemotherapy. Annals of Oncology. 2020 September. doi: https://doi.org/10.1016/j.annonc.2020.08.2272.

2.Marabelle A, et al. Pembrolizumab for previously treated advanced anal squamous cell carcinoma: results from the non-randomised, multicohort, multicentre, phase 2 KEYNOTE-158 study. Lancet Gastroenterol Hepatol. 2022 May;7(5):446-454. doi: 10.1016/S2468-1253(21)00382-4.

3.Lonardi S, et al. Randomized phase II trial of avelumab alone or in combination with cetuximab for patients with previously treated, locally advanced, or metastatic squamous cell anal carcinoma: the CARACAS study. J Immunother Cancer. 2021 November;9(11):e002996. doi: 10.1136/jitc-2021-002996. PMID: 34815354; PMCID: PMC8611452.

In the first quarter of 2025, we also received regulatory approval to allow GOBLET's new PDAC mFOLFIRINOX cohort (GOBLET Cohort 5) to progress to full enrollment and presented the safety run-in results at the 2025 ASCO Gastrointestinal Cancers Symposium. GOBLET Cohort 5 is supported by the Pancreatic Cancer Action Network (PanCAN) Therapeutic Accelerator Award for up to US$5 million.

As we work to complete our CEO search and secure adequate funding, we are actively evaluating multiple strategic options to advance the development of pelareorep. We are closely monitoring the impact of recently approved antibody-drug conjugate therapies on our breast cancer program and assessing how they may impact our development strategy. In parallel, we continue to engage with collaborators, academic partners, and other stakeholders to determine the most effective path forward for our pancreatic cancer program.

Manufacturing and Process Development

While we currently have sufficient drug product supply to support our clinical development program, we continued our activities to expand our production capabilities as we focus on advancing our active drug substance and finished drug product toward registration and commercial readiness. During the first quarter of 2025, we began a formal assessment of the drug substance production process in preparation for performance qualification. We also incurred storage and distribution costs to maintain our product supply. Ongoing bulk manufacturing and expanded filling capabilities are both part of the planned process validation. Continued process validation is required to ensure that the resulting product meets the specifications and quality standards and will form part of our submission to regulators, including the FDA, for product approval.

In 2025, our manufacturing program will focus on filling product with a secondary fill/finish supplier, completing a formal assessment of the drug substance production process in preparation for performance qualification, executing a cGMP production run, completing the potency assay validation, and supply distribution for our ongoing and planned studies.

Intellectual Property

At the end of the first quarter of 2025, we had 146 patents, including 11 U.S. and 7 Canadian patents, and issuances in other jurisdictions. We have an extensive patent portfolio covering pelareorep and formulations that we use in our clinical trial program. We also have patents covering methods for manufacturing pelareorep and screening for susceptibility to pelareorep. These patent rights extend to at least the end of 2031. In addition, we have ongoing patent applications that may extend the patent rights beyond 2031.

Financing Activity

U.S. "at-the-market" (ATM) equity distribution agreement

During the three months ended March 31, 2025, we sold 5,302,950 common shares for gross proceeds of $6,228 (US$4,327) at an average price of $1.17 (US$0.82). We received proceeds of $6,041 (US$4,197) after commissions of $187 (US$130). In total, we incurred share issue costs (including commissions) of $235.

Share purchase agreement with Alumni Capital LP

On April 10, 2025, we entered into a share purchase agreement with Alumni Capital LP (Alumni), an institutional investor. Under the terms of the agreement, we have the right to sell, and Alumni has the obligation to purchase up to US$20 million worth of common shares over a 15-month period based on the market price at the time of each sale to Alumni. At the execution of the agreement, we issued an initial commitment fee of 816,326 common shares valued at US$400. An additional 816,326 common shares will be issued on a pro rata basis upon the delivery of purchase notices as an additional commitment fee. We have sole discretion over the timing and amount of all common share sales. This partnership will provide us with a flexible funding source to progress toward key clinical milestones while minimizing dilution to create and sustain shareholder value.

Cash Resources

We ended the first quarter of 2025 with cash and cash equivalents of $15,303 (see "Liquidity and Capital Resources").

Other Corporate Matters

Our other corporate matters included the following:

•In the first quarter of 2025, we announced that Dr. Matt Coffey, President and Chief Executive Officer (CEO), will not be returning following a medical leave of absence announced in the second quarter of 2024 due to ongoing health concerns. Wayne Pisano, Chair of Oncolytics' Board of Directors, will remain Interim CEO until a new CEO is hired. We have commenced a search for a CEO.

•In the first quarter of 2025, we received a delinquency notification letter (the "Notice") from the Listing Qualifications Department of The Nasdaq Stock Market LLC ("Nasdaq") indicating that, for the prior 30 consecutive business days, the closing bid price for our ordinary shares listed on the Nasdaq Capital Market was below the minimum $1.00 per share required for continued listing on the Nasdaq Capital Market pursuant to Nasdaq Listing Rule 5550(a)(2). The Notice provides that we have a period of 180 calendar days from the date of the Notice, or until August 12, 2025, to regain compliance with the minimum bid price requirement. The receipt of the Notice has no immediate effect on our business operations or the listing of our ordinary shares, which will continue to trade uninterrupted on the Nasdaq under the ticker "ONCY." If at any time before August 12, 2025, the bid price of our ordinary shares closes at or above $1.00 per share for a minimum of 10 consecutive business days, Nasdaq will provide written confirmation of compliance to us. In the event that we do not regain compliance by August 12, 2025, we may be eligible for additional time to regain compliance. To qualify, we would be required to meet the continued listing requirement for the market value of publicly held shares and all other initial listing standards for the Nasdaq Capital Market, except for the minimum bid price requirement. In addition, we would be required to notify Nasdaq of its intent to cure the deficiency during the second compliance period.

•In early 2025, the President of the United States issued executive orders directing the United States to impose new tariffs on most imports into the United States. The impacts of these tariffs on our operations remain uncertain. New or increased tariffs, export controls, or other measures discouraging contracts with Chinese companies could materially impact our supply chain and manufacturing costs and our licensing agreement with Adlai Nortye Biopharma Co., Ltd. We are assessing the direct and indirect impacts of such trade protectionist measures to our operations as this situation develops.

Results of Operations

Comparison of the three months ended March 31, 2025, and 2024:

Unless otherwise indicated, all amounts below are presented in thousands of Canadian dollars, except for share amounts.

Net loss for the three months ended March 31, 2025, was $6,687 compared to $6,894 for the three months ended March 31, 2024.

Research and development expenses (“R&D”)

Our R&D expenses decreased by $1,660 from $5,743 for the three months ended March 31, 2024, to $4,083 for the three months ended March 31, 2025. The following table summarizes our R&D expenses for the three months ended March 31, 2025, and 2024:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months Ended March 31, |

|

|

|

2025 |

|

2024 |

|

Change |

| Clinical trial expenses |

$ |

516 |

|

|

$ |

802 |

|

|

$ |

(286) |

|

| Manufacturing and related process development expenses |

578 |

|

|

3,178 |

|

|

(2,600) |

|

| Intellectual property expenses |

149 |

|

|

126 |

|

|

23 |

|

|

|

|

|

|

|

| Personnel-related expenses |

1,900 |

|

|

1,271 |

|

|

629 |

|

| Share-based compensation expense |

892 |

|

|

340 |

|

|

552 |

|

| Other expenses |

48 |

|

|

26 |

|

|

22 |

|

| Research and development expenses |

$ |

4,083 |

|

|

$ |

5,743 |

|

|

$ |

(1,660) |

|

The decrease in our R&D expenses for the three months ended March 31, 2025, was primarily due to the following:

•Decreased manufacturing and related process development expenses as we completed a cGMP production run and the related batch testing during the same period in the previous year; and

•Decreased clinical trial expenses mainly due to lower GOBLET and BRACELET-1 study costs. We incurred lower expenses associated with enrolling and treating patients in GOBLET's expanded anal cancer cohort compared to the legacy cohorts' patient monitoring and sample analysis expenses during the same period in the previous year. During the first three months of 2025, we also focused on enrolling GOBLET Cohort 5, which is supported by the PanCAN Therapeutic Accelerator Award ($836 of the funds received were applied). We completed the BRACELET-1 study in 2024.

The above decreases were partly offset by increased personnel-related expenses and share-based compensation expense mainly due to CEO transition activities.

General and administrative expenses ("G&A")

Our G&A expenses of $2,916 for the three months ended March 31, 2025, were consistent with expenses of $2,983 for the three months ended March 31, 2024. The following table summarizes our G&A expenses for the three months ended March 31, 2025, and 2024:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months Ended March 31, |

|

|

|

2025 |

|

2024 |

|

Change |

| Public company-related expenses |

$ |

1,673 |

|

|

$ |

1,844 |

|

|

$ |

(171) |

|

| Personnel-related expenses |

712 |

|

|

653 |

|

|

59 |

|

| Office expenses |

118 |

|

|

127 |

|

|

(9) |

|

| Share-based compensation expense |

316 |

|

|

236 |

|

|

80 |

|

| Depreciation - property and equipment |

26 |

|

|

28 |

|

|

(2) |

|

| Depreciation - right-of-use assets |

71 |

|

|

95 |

|

|

(24) |

|

| General and administrative expenses |

$ |

2,916 |

|

|

$ |

2,983 |

|

|

$ |

(67) |

|

Change in fair value of warrant derivative

For the three months ended March 31, 2025, we recognized gains of $240 on the change in fair value of our warrant derivative compared to $869 for the three months ended March 31, 2024. For the three months ended March 31, 2025, the underlying market price of these warrants changed from US$0.92 at December 31, 2024, to US$0.55 at March 31, 2025. For the three months ended March 31, 2024, the underlying market price of these warrants changed from US$1.35 at December 31, 2023, to US$1.07 at March 31, 2024. The number of outstanding warrants was 7,667,050 at March 31, 2025, and December 31, 2024.

Foreign exchange

Our foreign exchange losses for the three months ended March 31, 2025, were $51 compared to gains of $517 for the three months ended March 31, 2024. The foreign exchange impact mainly reflected the fluctuation of the U.S. dollar versus the Canadian dollar throughout the respective periods, primarily on our U.S. dollar-denominated cash and cash equivalents.

Summary of Quarterly Results

Historical patterns of expenditures cannot be taken as an indication of future expenditures. Our current and future expenditures are subject to numerous uncertainties, including the duration, timing, and costs of R&D activities ongoing during each period and the availability of funding from investors and prospective partners. As a result, the amount and timing of expenditures and, therefore, liquidity and capital resources may vary substantially from period to period.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2025 |

2024 |

2023 |

|

Mar.(4) |

Dec.(4) |

Sept.(4) |

Jun.(4) |

Mar.(4) |

Dec.(4) |

Sept. |

Jun. |

| Revenue |

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

Net loss(1)(2)(3) |

(6,687) |

|

(8,017) |

|

(9,543) |

|

(7,256) |

|

(6,894) |

|

(3,949) |

|

(9,925) |

|

(7,441) |

|

Basic and diluted loss per common share(1)(2)(3) |

$ |

(0.08) |

|

$ |

(0.10) |

|

$ |

(0.12) |

|

$ |

(0.10) |

|

$ |

(0.09) |

|

$ |

(0.05) |

|

$ |

(0.14) |

|

$ |

(0.12) |

|

Total assets(5) |

19,702 |

20,187 |

24,262 |

32,069 |

|

34,750 |

|

38,820 |

|

46,089 |

|

31,966 |

|

Total cash, cash equivalents, and marketable securities(5) |

15,303 |

|

15,942 |

19,598 |

24,850 |

|

29,603 |

|

34,912 |

|

39,981 |

|

24,351 |

|

| Total long-term debt |

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

Cash dividends declared(6) |

Nil |

Nil |

Nil |

Nil |

Nil |

Nil |

Nil |

Nil |

(1)Included in consolidated net loss and loss per common share were share-based compensation expenses of $1,208, $ $1,196, $445, $506, $576, $759, $599, and $242, respectively.

(2)Included in consolidated net loss and loss per common share were foreign exchange (losses) gains of $(51), $382, $(122), $184, $517, $(392), $310, and $(394), respectively.

(3)Included in consolidated net loss and loss per common share were interest income of $162, $193, $303, $382, $461, $508, $324, and $286, respectively.

(4)Included in consolidated net loss and loss per common share were gains (losses) resulting from a change in fair value of warrant derivative of $240, $(91), $229, $235, $869, and $4,846, respectively.

(5)We raised net cash proceeds of $5,993, $3,439, nil, $2,040, $1,598, $1,846, $20,802, and $3,792, respectively, from issuing common shares.

(6)We have not declared or paid any dividends since incorporation.

During the quarter ended September 30, 2023, we completed an engineering production run, resulting in higher manufacturing and related process development expenses. We also incurred higher public company-related expenses associated with higher investor relations activities and the portion of the 2023 public offering transaction costs allocated to warrants. During the quarter ended September 30, 2024, we completed a cGMP production run, resulting in higher manufacturing and related process development expenses. During the quarters ended December 31, 2024, and 2023, we incurred expenses related to annual short-term incentive awards.

Liquidity and Capital Resources

As a clinical-stage biopharmaceutical company, we have not been profitable since our inception. We expect to continue to incur substantial losses as we continue our research and development efforts. We do not expect to generate significant revenues until and unless pelareorep becomes commercially viable. See "Operating Capital Requirements" below for the discussion on our ability to continue as a going concern. To date, we have funded our operations mainly through issuing additional capital via public offerings, equity distribution arrangements, and the exercise of warrants and stock options. For the three months ended March 31, 2025, we raised funds through our U.S. ATM.

We have no assurances that we will be able to raise additional funds through the sale of our common shares. Consequently, we will continue to evaluate all types of financing arrangements.

On July 19, 2024, we renewed our short form base shelf prospectus (the "Base Shelf") that qualifies for distribution of up to $150 million of common shares, subscription receipts, warrants, or units (the "Securities") in either Canada, the U.S. or both. The Base Shelf will be effective until August 19, 2026. Under the Base Shelf, we may sell Securities to or through underwriters, dealers, placement agents, or other intermediaries. We may also sell Securities directly to purchasers or through agents, subject to obtaining any applicable exemption from registration requirements. The distribution of Securities may be performed from time to time in one or more transactions at a fixed price or prices, which may be subject to change, at market prices prevailing at the time of sale or at prices related to such prevailing market prices to be negotiated with purchasers and as set forth in an accompanying Prospectus Supplement.

Renewing our Base Shelf provides additional flexibility when managing our cash resources as, under certain circumstances, it shortens the time required to close a financing and is expected to increase the number of potential investors that may be prepared to invest in the Company. Funds received from using our Base Shelf would be used in line with our Board-approved budget and multi-year plan.

Our Base Shelf allowed us to enter into our ATM equity distribution agreement and share purchase agreement (see notes 7 and 16 in our condensed interim consolidated financial statements, respectively). We plan to use these equity arrangements to assist us in achieving our capital objective. These arrangements provide us with the opportunity to raise capital and better manage our cash resources. We expect to continue to access equity arrangements to help support our operations.

As at March 31, 2025, and December 31, 2024, we had cash and cash equivalents as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

March 31,

2025 |

|

December 31,

2024 |

| Cash and cash equivalents |

$ |

15,303 |

|

|

$ |

15,942 |

|

We have no debt other than accounts payable and accrued liabilities and lease liabilities. We have commitments relating to completing our research and development of pelareorep.

The following table summarizes our cash flows for the periods indicated:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months Ended March 31, |

|

|

|

2025 |

|

2024 |

|

Change |

| Cash used in operating activities |

$ |

(6,498) |

|

|

$ |

(7,469) |

|

|

$ |

971 |

|

| Cash used in investing activities |

— |

|

|

(46) |

|

|

46 |

|

| Cash provided by financing activities |

5,890 |

|

|

1,495 |

|

|

4,395 |

|

| Impact of foreign exchange on cash and cash equivalents |

(31) |

|

|

711 |

|

|

(742) |

|

| Decrease in cash and cash equivalents |

$ |

(639) |

|

|

$ |

(5,309) |

|

|

$ |

4,670 |

|

Cash used in operating activities

The decrease reflected lower net operating activities in 2025, partly offset by higher non-cash working capital changes.

Cash used in operating activities for the three months ended March 31, 2025, consisted of a net loss of $6,687 offset by non-cash adjustments of $1,043 less non-cash working capital changes of $854. Non-cash items primarily included share-based compensation expense. Non-cash working capital changes mainly reflected decreased other liabilities reflecting utilization of funding received from PanCAN and increased accounts payable and accrued liabilities (see note 13 of our condensed interim consolidated financial statements).

Cash used in operating activities for the three months ended March 31, 2024, consisted of a net loss of $6,894 less non-cash adjustments of $542 and non-cash working capital changes of $33. Non-cash items primarily included change in fair value of

warrant derivative, share-based compensation expense, and unrealized foreign exchange gains. Non-cash working capital

changes mainly reflected decreased prepaid expenses and increased accounts payable and accrued liabilities (see note 13 of our condensed interim consolidated financial statements).

Cash provided by financing activities

The increase was mainly due to our U.S. ATM activities. During the three months ended March 31, 2025, we sold 5,302,950 common shares for gross proceeds of $6,228 (US$4,327) at an average price of $1.17 (US$0.82). During the three months ended March 31, 2024, we sold 994,668 common shares for gross proceeds of $1,669 (US$1,244) at an average price of $1.68 (US$1.25).

Operating Capital Requirements

Our objective is to maintain adequate cash reserves to support our planned activities, including our clinical trial program, product manufacturing, administrative costs, and intellectual property protection. To do so, we estimate our future cash requirements by preparing a budget and a multi-year plan annually for review and approval by our Board. The budget establishes the approved activities for the upcoming year and estimates the associated costs. The multi-year plan estimates future activity along with the potential cash requirements and is based on our assessment of our current clinical trial progress along with the expected results from the coming year’s activity. Budget to actual variances are prepared and reviewed by management and are presented quarterly to the Board. We continue to manage our research and development plan to ensure optimal use of our existing resources as we expect to fund our expenditure requirements and commitments with existing working capital.

Management assesses our ability to continue as a going concern. In our going concern assessment, management takes into account all available information about the future, which is at least, but not limited to, twelve months from the end of the reporting period. We have concluded that our cash and cash equivalents are not sufficient to fund our planned operations and meet our obligations for the twelve months following the balance sheet date without raising additional funding or reducing or eliminating our planned expenditures. Factors that will affect our anticipated cash usage for which additional funding might be required include, but are not limited to, expansion of our clinical trial program, the timing of patient enrollment in our clinical trials, the actual costs incurred to support each clinical trial, the number of treatments each patient will receive, the timing of R&D activity with our clinical trial research collaborations, the number, timing and costs of manufacturing runs required to conclude the validation process and supply product to our clinical trial program, and the level of collaborative activity undertaken, and other factors described in the "Risk Factors" section of our most recent annual report on Form 20-F. The judgment and assumptions applied by management may prove to be wrong, and actual results could vary materially from our expectations as significant risks and uncertainties are involved.

We expect to increase our spending in connection with the research and development of pelareorep over the next several years as we look to advance our breast and gastrointestinal cancer programs into later stages of clinical development. A product candidate in later stages of clinical development generally has higher costs than those in earlier stages, primarily due to the increased size and duration of later-stage clinical trials. Additionally, we expect to continue to incur additional costs associated with operating as a public company.

We plan on raising additional funds through the sale of our common shares or other capital resources, such as strategic collaborations and debt, to fund our ongoing operations. However, given the difficulty for micro-cap market capitalization companies to raise significant capital, there can be no assurance that additional liquidity will be available under acceptable terms or at all. Furthermore, if we are unable to obtain additional financing when required, there can be no assurance that we will be able to sufficiently reduce or eliminate our planned expenditures to extend our operating runway until we obtain sufficient financing. These material uncertainties raise substantial doubt on our ability to continue as a going concern. Our condensed interim consolidated financial statements do not reflect the adjustments that may result from the outcome of these uncertainties. Such adjustments could be material.

To the extent that we can raise additional funds by issuing equity, our shareholders may experience significant dilution. Any debt financing, if available, may involve restrictive covenants that may impact our ability to conduct our business. If we are unable to secure adequate additional funding, we may be forced to make reductions in spending, including potentially delaying, scaling back or eliminating certain of our development programs, extending payment terms with suppliers, or liquidating assets where possible. Any of these actions could materially harm our business, results of operations and future prospects.

Conducting clinical trials necessary to obtain regulatory approval is costly and time-consuming. We may never succeed in achieving marketing approval. The probability of successful commercialization of our drug candidates may be affected by numerous factors, including clinical data obtained in future trials, competition, manufacturing capability and commercial viability. As a result, we are unable to determine the duration and completion costs of our research and development projects or when and to what extent we will generate revenue from the commercialization and sale of any of our product candidates.

We are not subject to externally imposed capital requirements, and there have been no changes in how we define or manage our capital in 2025.

Contractual Obligations and Commitments

The following table summarizes our significant contractual obligations as at March 31, 2025:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

Less than 1 year |

1 -3 years

|

4 - 5 years

|

More than

5 years |

| Accounts payable and accrued liabilities |

$ |

4,948 |

|

$ |

4,948 |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

| Lease obligations |

1,309 |

|

421 |

|

821 |

|

67 |

|

— |

|

| Total contractual obligations |

$ |

6,257 |

|

$ |

5,369 |

|

$ |

821 |

|

$ |

67 |

|

$ |

— |

|

In addition, we are committed to payments totaling approximately $6,800 for activities mainly related to our clinical trial and manufacturing programs, which are expected to occur over the next two years. Approximately one-third of the committed payments relate to a production service agreement with our primary toll manufacturer, which cannot be canceled without a significant penalty. We are able to cancel most of the remaining agreements with notice. The ultimate amount and timing of these payments are subject to changes in our research and development plan.

Off-Balance Sheet Arrangements

As at March 31, 2025, we had not entered into any off-balance sheet arrangements.

Transactions with Related Parties

During the three months ended March 31, 2025, and 2024, we did not enter into any related party transactions other than compensation paid to key management personnel. Key management personnel are those persons having authority and responsibility for planning, directing, and controlling our activities as a whole. We have determined that key management personnel comprise the Board of Directors, Executive Officers, President, and Vice Presidents.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months Ended March 31, |

|

|

|

|

|

2025 |

|

2024 |

| Compensation and short-term benefits |

|

|

|

|

$ |

905 |

|

|

$ |

928 |

|

| Termination benefits |

|

|

|

|

1,190 |

|

|

— |

|

| Share-based compensation expense |

|

|

|

|

363 |

|

|

498 |

|

|

|

|

|

|

$ |

2,458 |

|

|

$ |

1,426 |

|

Termination benefits were provided to our former CEO and included both cash and share-based compensation.

Critical Accounting Policies and Estimates

In preparing our condensed interim consolidated financial statements, we use IFRS as issued by the IASB. IFRS requires us to make certain estimates, judgments, and assumptions that we believe are reasonable based on the information available in applying our accounting policies. These estimates and assumptions affect the reported amounts and disclosures in our condensed interim consolidated financial statements and accompanying notes.

Actual results could differ from those estimates, and such differences could be material.

Our critical accounting policies and estimates are described in our audited consolidated financial statements for the year ended December 31, 2024, and available on SEDAR+ at www.sedarplus.ca and contained in our annual report on Form 20-F filed on EDGAR at www.sec.gov/edgar.

There were no material changes to our critical accounting policies in the three months ended March 31, 2025.

Accounting standards and interpretations issued but not yet effective

IFRS 18 Presentation and Disclosure in Financial Statements

In April 2024, the IASB issued IFRS 18 Presentation and Disclosure in Financial Statements which replaces IAS 1 Presentation of Financial Statements. IFRS 18 introduces new requirements on presentation within the statement of profit or loss, including specified totals and subtotals. It also requires disclosure of management-defined performance measures and includes new requirements for aggregation and disaggregation of financial information based on the identified roles of the primary financial statements and the notes. Narrow scope amendments have been made to IAS 7 Statement of Cash Flows and some requirements previously included within IAS 1 have been moved to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors, which has also been renamed IAS 8 Basis of Preparation of Financial Statements. IAS 34 Interim Financial Reporting has also been amended to require disclosure of management-defined performance measures. IFRS 18 and the amendments to the other standards are effective for annual periods beginning on or after January 1, 2027, with early application permitted. IFRS 18 applies retrospectively to both annual and interim financial statements. We are assessing the impact of adopting this standard on our consolidated financial statements.

Financial Instruments and Other Instruments

Fair value of financial instruments

As at March 31, 2025, and December 31, 2024, the carrying amount of our cash and cash equivalents, other receivables, accounts payable and accrued liabilities, and other liabilities approximated their fair value due to their short-term maturity. The warrant derivative is a recurring Level 2 fair value measurement as these warrants have not been listed on an exchange and, therefore, do not trade on an active market. As at March 31, 2025, the fair value of our warrant derivative was presented as an asset of $1,220 (December 31, 2024 - $980). The change was mainly due to the revaluation of our warrants issued as part of our 2023 public offering. As the unamortized discount balance was greater than the fair value of the warrant derivative liability at March 31, 2025, the net balance was presented as an asset on our condensed interim consolidated statement of financial position. An initial discount was recognized as the difference between the fair value of the warrants and their allocated proceeds, which is amortized on a straight-line basis over the expected life of the warrants (see note 6 of our condensed interim consolidated financial statements). We use the Black-Scholes valuation model to estimate fair value.

Financial risk management

Credit risk

Credit risk is the risk of a financial loss if a counterparty to a financial instrument fails to meet its contractual obligations. As at March 31, 2025, we were exposed to credit risk on our cash and cash equivalents in the event of non-performance by counterparties, but we do not anticipate such non-performance. Our maximum exposure to credit risk at the end of the period is the carrying value of our cash and cash equivalents.

We mitigate our exposure to credit risk connected to our cash and cash equivalents by maintaining our primary operating and investment bank accounts with Schedule I banks in Canada. For our foreign-domiciled bank accounts, we use referrals or recommendations from our Canadian banks to open foreign bank accounts. Our foreign-domiciled bank accounts are used solely for the purpose of settling accounts payable and accrued liabilities or payroll.

Interest rate risk

Interest rate risk is the risk that a financial instrument's fair value or future cash flows will fluctuate because of changes in market interest rates. We hold our cash and cash equivalents in bank accounts or high-interest investment accounts with variable interest rates. We mitigate interest rate risk through our investment policy that only allows the investment of excess cash resources in investment-grade vehicles while matching maturities with our operational requirements.

Fluctuations in market interest rates do not significantly impact our results of operations due to the short-term maturity of the investments held.

Foreign exchange risk

Foreign exchange risk arises from changes in foreign exchange rates that may affect the fair value or future cash flows of our financial assets or liabilities. For the three months ended March 31, 2025, we were primarily exposed to the risk of changes in the Canadian dollar relative to the U.S. dollar and Euro, as a portion of our financial assets and liabilities were denominated in such currencies. The impact of a $0.01 increase in the value of the U.S. dollar against the Canadian dollar would have decreased our comprehensive loss in 2025 by approximately $88 (March 31, 2024 - $216). The impact of a $0.01 increase in the value of the Euro against the Canadian dollar would have increased our comprehensive loss in 2025 by approximately $22 (March 31, 2024 - $14).

We mitigate our foreign exchange risk by maintaining sufficient foreign currencies by purchasing foreign currencies or receiving foreign currencies from financing activities to settle our foreign accounts payable.

Significant balances denominated in U.S. dollars were as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

March 31,

2025 |

|

December 31,

2024 |

| Cash and cash equivalents |

$ |

9,019 |

|

|

$ |

9,534 |

|

|

|

|

|

|

|

|

|

| Accounts payable and accrued liabilities |

(1,921) |

|

|

(1,722) |

|

|

|

|

|

|

$ |

7,098 |

|

|

$ |

7,812 |

|

Significant balances denominated in Euros were as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

March 31,

2025 |

|

December 31,

2024 |

| Accounts payable and accrued liabilities |

€ |

(1,131) |

|

|

€ |

(1,114) |

|

Liquidity risk

Liquidity risk is the risk that we will encounter difficulty in meeting obligations associated with financial liabilities. We manage liquidity risk through the management of our capital structure as outlined in note 11 to our condensed interim consolidated financial statements. Accounts payable and accrued liabilities are all due within the current operating period. Other liabilities associated with funding received from PanCAN (see note 4 in our condensed interim consolidated financial statements) are expected to be applied within the current operating period. See note 5 in our condensed interim consolidated financial statements for a maturity analysis of our lease liabilities.

Use of Proceeds

2023 public offering and use of proceeds

The following table provides an update on the anticipated use of proceeds raised as part of the 2023 public offering of common shares and warrants along with amounts actually expended. Following the announcement of our final BRACELET-1 results in the third quarter of 2024, we redirected proceeds to the breast cancer program. As at March 31, 2025, the following expenditures have been incurred (in thousands of U.S. dollars):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Item |

Amount to Spend |

|

Spent to Date |

|

Adjustments |

|

Remaining to Spend |

| Pancreatic Cancer Program |

$ |

10,500 |

|

|

$ |

(2,931) |

|

|

$ |

(3,846) |

|

|

$ |

3,723 |

|

| Breast Cancer Program |

500 |

|

|

(1,028) |

|

|

3,846 |

|

|

3,318 |

|

| General and Administrative Expenses |

2,650 |

|

|

(740) |

|

|

— |

|

|

1,910 |

|

| Total |

$ |

13,650 |

|

|

$ |

(4,699) |

|

|

$ |

— |

|

|

$ |

8,951 |

|

ATM facility

On August 2, 2024, we entered into an ATM equity distribution agreement with Cantor Fitzgerald & Co. The ATM allows us to issue common shares, at prevailing market prices, with an aggregate offering value of up to US$50.0 million through the facilities of the Nasdaq Capital Market in the United States until August 19, 2026. During the three months ended March 31, 2025, we sold 5,302,950 common shares for gross proceeds of $6,228 (US$4,327). As at March 31, 2025, approximately $62.0 million (US$43.1 million) remains unused under the ATM equity distribution agreement.

Other MD&A Requirements

We have 88,822,240 common shares outstanding at May 14, 2025. If all of our options and restricted share awards (7,362,463) and common share purchase warrants (8,203,743) were exercised, we would have 104,388,446 common shares outstanding.

Our 2024 annual report on Form 20-F is available on SEDAR+ at www.sedarplus.ca and EDGAR at www.sec.gov/edgar.

Disclosure Controls and Procedures

Disclosure controls and procedures (“DC&P”) are designed to provide reasonable assurance that information required to be disclosed by the Company in its reports filed or submitted by it under securities legislation is recorded, processed, summarized and reported within the time periods specified in the securities legislation and include controls and procedures designed to ensure that information required to be disclosed by the Company in its reports filed or submitted under securities legislation is accumulated and communicated to the Company’s management, including its certifying officers, as appropriate to allow timely decisions regarding required disclosure. There were no changes in our DC&P during the three months ended March 31, 2025, that materially affected or are reasonably likely to materially affect, our DC&P.

Internal Controls over Financial Reporting

The Chief Executive Officer ("CEO") and Chief Financial Officer ("CFO") are responsible for designing internal controls over financial reporting (“ICFR”) or causing them to be designed under their supervision in order to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS. The CEO and CFO have designed, or caused to be designed under their supervision, ICFR to provide reasonable assurance that: (i) material information relating to the Company is made known to the Company's CEO and CFO by others; and (ii) information required to be disclosed by the Company in its reports filed or submitted by it under securities legislation is recorded, processed, summarized and reported within the time period specified in securities legislation. The Committee of Sponsoring Organizations of the Treadway Commission (“COSO”) 2013 framework provides the basis for management’s design of internal controls over financial reporting. There were no changes in our ICFR during the three months ended March 31, 2025, that materially affected or are reasonably likely to materially affect, our ICFR.

Management, including the CEO and CFO, does not expect that our internal controls and procedures over financial reporting will prevent all errors and all fraud. A control system can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by management override of the control. The design of any system of controls also is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving our stated goals under all potential future conditions. Because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Risks and Uncertainties

We are a clinical-stage biopharmaceutical company. Prospects for biotechnology companies in the research and development stage should generally be regarded as speculative. It is not possible to predict, based on studies in animals, or early studies in humans, whether a new therapeutic will ultimately prove to be safe and effective in humans or whether necessary and sufficient data can be developed through the clinical trial process to support a successful product application and approval. If a product is approved for sale, product manufacturing at a commercial scale and significant sales to end users at a commercially reasonable price may not be successful. There can be no assurance that we will generate adequate funds to continue development or will ever achieve significant revenues or profitable operations. Many factors (e.g., competition, patent protection, appropriate regulatory approvals) can influence the revenue and product profitability potential. In developing a pharmaceutical product, we rely on our employees, contractors, consultants and collaborators, and other third-party relationships, including the ability to obtain appropriate product liability insurance. There can be no assurance that this reliance and these relationships will continue as required. In addition to developmental and operational considerations, market prices for securities of biotechnology companies generally are volatile, and may or may not move in a manner consistent with the progress we have made or are making.

Investment in our common shares involves a high degree of risk. An investor should carefully consider, among other matters, the risk factors in addition to the other information in our annual report on Form 20-F filed with the U.S. Securities and Exchange Commission (the "SEC"), as well as our other public filings with the Canadian securities regulatory authorities and the SEC, when evaluating our business because these risk factors may have a significant impact on our business, financial condition, operating results or cash flow. If any of the described material risks in our annual report or in subsequent reports we file with the regulatory authorities actually occur, they may materially harm our business, financial condition, operating results or cash flow. Additional risks and uncertainties that we have not yet identified or that we presently consider to be immaterial may also materially harm our business, financial condition, operating results, or cash flow. For information on risks and uncertainties, please refer to the "Risk Factors" section of our most recent annual report on Form 20-F and our other public filings available on www.sedarplus.ca and www.sec.gov/edgar.