UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): April 22, 2026

COLONY BANKCORP, INC.

(Exact name of registrant as specified in its charter)

115 South Grant Street, Fitzgerald, Georgia 31750

(Address of principal executive offices) (Zip Code)

(229) 426-6000

(Registrant's telephone number, including area code)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

Securities registered pursuant to Section 12(b) of the Act:

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02. Results of Operation and Financial Condition

On April 22, 2026, Colony Bankcorp, Inc. issued a press release announcing its consolidated financial results for the first quarter ended March 31, 2026, as well as the announcement of a regular quarterly cash dividend. A copy of the press release is attached hereto as Exhibit 99.1 and is incorporated herein by reference.

Item 7.01. Regulation FD Disclosure

The Company is furnishing a copy of its most recent investor presentation, which it intends to use in connection with certain community group presentations. A copy of the presentation materials to be used by the Company is furnished as Exhibit 99.2 to this Current Report and is incorporated herein by reference. The Company will also host an investor earnings call at 9:00 a.m. ET on Thursday, April 23, 2026.

In accordance with General Instruction B.2 of Form 8-K, the information in this Current Report on Form 8-K, including Exhibits 99.1 and 99.2 attached hereto, is being furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference in such filing.

Item 9.01 Financial Statements and Exhibits

(d) |

Exhibits. |

Exhibit Number |

|

Description |

|

|

|

99.1 |

|

|

99.2 |

|

|

104 |

|

Cover Page Interactive Data File - the cover page XBRL tags are embedded within the Inline XBRL document. |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

COLONY BANKCORP, INC. |

|

|

|

|

|

|

|

Date: April 22, 2026 |

By: |

/s/ Derek Shelnutt |

|

|

Derek Shelnutt |

|

|

Executive Vice President and Chief Financial Officer |

Exhibit 99.1

For additional information, contact:

Derek Shelnutt

EVP & Chief Financial Officer

229-426-6000, extension 6119

COLONY BANKCORP, INC. REPORTS FIRST QUARTER 2026 RESULTS

DECLARES QUARTERLY CASH DIVIDEND OF $0.12 PER SHARE

FITZGERALD, GA. (April 22, 2026) – Colony Bankcorp, Inc. (NYSE: CBAN) (“Colony” or the “Company”) today reported financial results for the first quarter of 2026. Financial highlights are shown below.

Financial Highlights:

| ● | Net income was $8.2 million, or $0.39 per diluted share, for the first quarter of 2026, compared to $7.8 million, or $0.42 per diluted share, for the fourth quarter of 2025, and $6.6 million, or $0.38 per diluted share, for the first quarter of 2025. |

| ● | Operating net income was $9.5 million, or $0.45 of operating earnings per diluted share, for the first quarter of 2026, compared to $8.9 million, or $0.48 of operating earnings per diluted share, for the fourth quarter of 2025, and $6.6 million, or $0.38 of operating earnings per diluted share, for the first quarter of 2025. (See Reconciliation of Non-GAAP Measures). |

| ● | Provision for credit losses of $1.75 million was recorded in the first quarter of 2026 compared to $1.65 million in the fourth quarter of 2025, and $1.50 million in the first quarter of 2025. |

| ● | Total loans, excluding loans held for sale, were $2.41 billion at March 31, 2026, an increase of $32.2 million, or 1.35%, from the prior quarter. |

| ● | Total deposits were $3.05 billion and $3.07 billion at March 31, 2026 and December 31, 2025, respectively, a decrease of $19.1 million. |

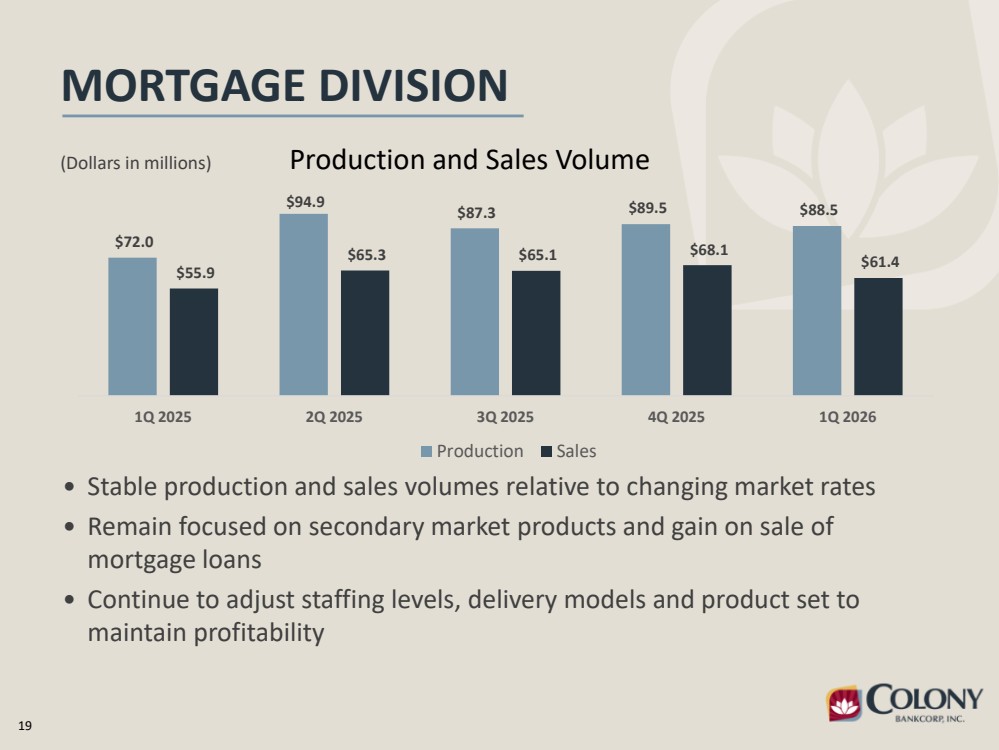

| ● | Mortgage production was $88.5 million, and mortgage sales totaled $61.4 million in the first quarter of 2026 compared to $89.5 million and $68.1 million, respectively, for the fourth quarter of 2025. |

| ● | Small Business Specialty Lending (“SBSL”) closed $13.1 million in Small Business Administration (“SBA”) loans and sold $10.4 million in SBA loans in the first quarter of 2026 compared to $29.1 million and $16.8 million, respectively, for the fourth quarter of 2025. |

The Company also announced that on April 22, 2026, the Board of Directors declared a quarterly cash dividend of $0.12 per share, to be paid on its common stock on May 20, 2026, to shareholders of record as of the close of business on May 6, 2026. The Company had 21,162,104 shares of its common stock outstanding as of April 20, 2026.

"Our first quarter performance represents a strong start to the year, characterized by meaningful improvement compared to the first quarter in the prior year and continued disciplined execution of our strategic initiatives. In addition to our solid financial performance during the quarter, our team successfully completed the TC Federal customer integration and core systems conversion which represents a significant operational achievement that allows us to fully realize the efficiencies of our combined organization and provides a scalable platform for future growth,” said Heath Fountain, Chief Executive Officer.

"Beyond core banking operations, our complementary lines of business continue to demonstrate significant momentum, contributing to a notable increase in noninterest income compared to the first quarter of the prior year. This growth highlights the success of our diversification strategy and our ability to deepen client relationships across our platform.”

1

“Colony Insurance and Colony Financial Advisors both achieved their strongest quarters to date on a pre-tax basis. The performance of these lines of business illustrates the value of our integrated financial services model and provides a resilient, diversified revenue stream that complements our core banking operations."

“We are also encouraged by the continued expansion of our net interest margin, marking another consecutive quarter of improvement. This trend, supported by our diligent management of deposit costs and asset yields, reinforces the underlying strength of our balance sheet. As we move forward, we remain committed to leveraging our enhanced scale and operational stability to deliver consistent results for our shareholders."

Balance Sheet

| ● | Total assets were $3.72 billion at March 31, 2026, a slight decrease of $14.8 million from December 31, 2025. |

| ● | Total loans, excluding loans held for sale, were $2.41 billion at March 31, 2026, an increase of $32.2 million from December 31, 2025. |

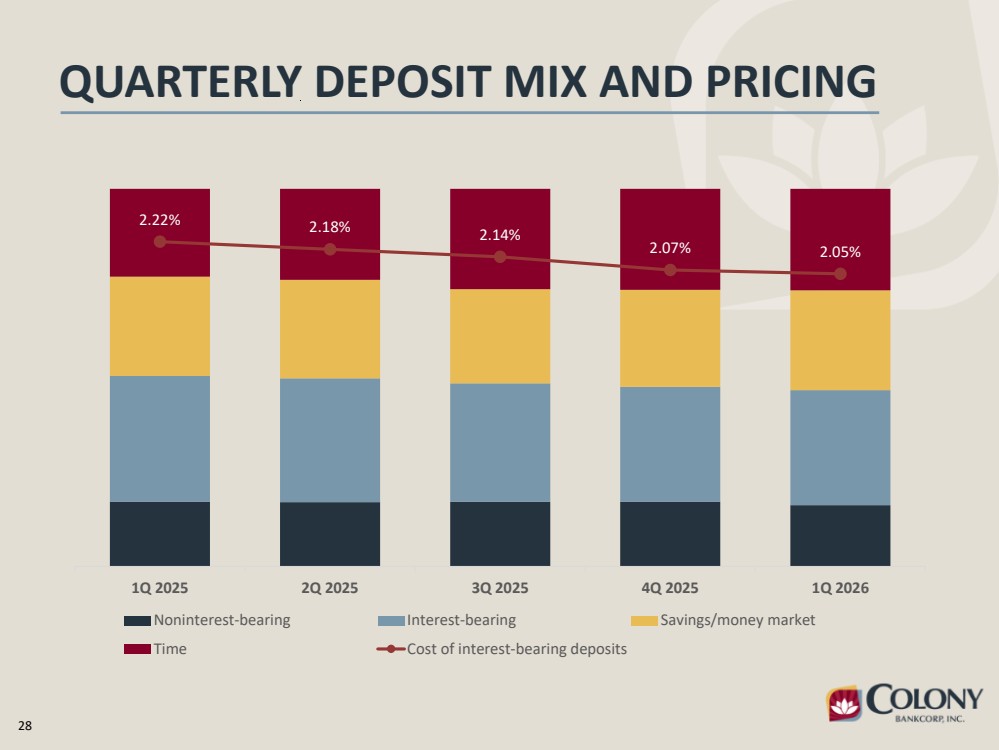

| ● | Total deposits were $3.05 billion and $3.07 billion at March 31, 2026 and December 31, 2025, respectively, a decrease of $19.1 million. Decreases were seen in noninterest-bearing demand deposits of $31.5 million, interest-bearing demand deposits of $4.5 million and time deposits of $1.7 million while savings and money market deposits increased $18.6 million, from December 31, 2025 to March 31, 2026. The decline in organic customer deposits was driven by the seasonal municipal deposit outflow early in the quarter, however customer deposits increased in the month of March. |

| ● | Total borrowings at March 31, 2026 totaled $258.1 million, an increase of $32,000 compared to December 31, 2025. |

Capital

| ● | Colony continues to maintain a strong capital position, with ratios that exceed regulatory minimums required to be considered as “well-capitalized.” |

| ● | Under the Company’s approved stock repurchase program, a total of 89,109 shares of the Company common stock were repurchased during the first quarter of 2026 at an average price of $19.78 per share and a total value of $1,762,839. |

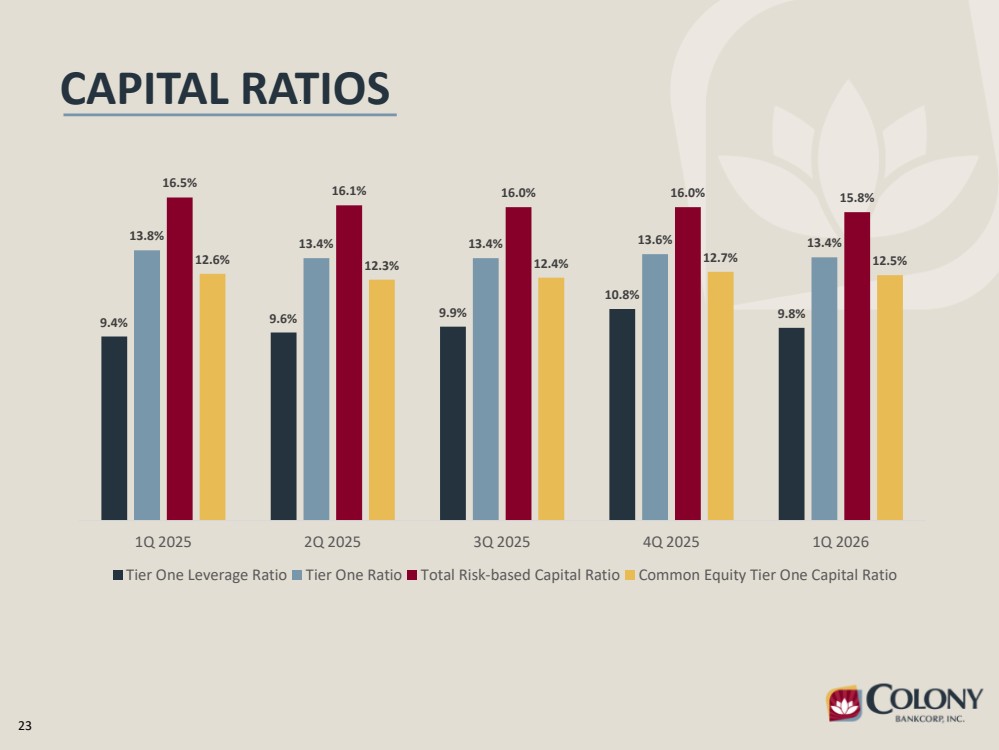

| ● | Preliminary tier one leverage ratio, tier one capital ratio, total risk-based capital ratio and common equity tier one capital ratio were 9.84%, 13.44%, 15.75%, and 12.53%, respectively, at March 31, 2026. |

First Quarter 2026 Results of Operations

| ● | Net interest income, on a tax-equivalent basis, totaled $29.4 million for the first quarter ended March 31, 2026 compared to $21.1 million for the same period in 2025. Increases occurred in income on interest earning assets which was more than offset by a slight increase in interest bearing liabilities. Income on interest earning assets increased $9.3 million to $45.0 million for the first quarter of 2026 compared to the same period in 2025. Expense on interest bearing liabilities increased $1.1 million to $15.7 million for the first quarter of 2026 compared to the same period in 2025. |

| ● | Net interest margin for the first quarter of 2026 was 3.48% compared to 2.93% for the first quarter of 2025. This increase was impacted by the Company’s acquisition of TC Bancshares, Inc. in the fourth quarter of 2025, and in addition related to increases in interest earning asset yields period over period, as well as the decreased cost of funds. |

| ● | Noninterest income totaled $10.7 million for the first quarter of 2026, an increase of $1.6 million, or 18.2%, compared to the same period in 2025. Increases occurred in service charges on deposits, mortgage fee income, interchange fees, insurance commissions and an increase in wealth advisor income included in other noninterest income, partially offset by decreases in gains on sales of SBA loans. |

| ● | Noninterest expense totaled $27.7 million for the first quarter of 2026, compared to $20.2 million for the same period in 2025. This increase was a result of increases in salaries and employee benefits, occupancy and equipment, information technology expenses, professional fees, advertising and public relations, and acquisition expenses related to the acquisition of TC Bancshares, Inc. which occurred in the fourth quarter of 2025. |

Asset Quality

| ● | Nonperforming assets totaled $19.9 million and $24.7 million at March 31, 2026 and December 31, 2025, respectively, a decrease of $4.8 million. |

| ● | Other real estate owned and repossessed assets totaled $2.1 million at March 31, 2026 and $1.2 million at December 31, 2025. |

| ● | Net loans charged-off were $1.7 million, or 0.29% of average loans for the first quarter of 2026, compared to $1.6 million, or 0.30% for the fourth quarter of 2025. |

| ● | The credit loss reserve was $21.7 million, or 0.90% of total loans, at March 31, 2026, compared to $23.0 million, or 0.97% of total loans at December 31, 2025. |

2

Earnings call information

The Company will host an earnings conference call at 9:00 a.m. ET on Thursday, April 23, 2026, to discuss the recent results and answer relevant questions. The conference call can be accessed by dialing 1-800-715-9871 and using the Conference ID: 2679228. A replay of the call will be available until Thursday, April 30, 2026. To listen to the replay, dial 1-800-770-2030 and entering the passcode 2679228#.

About Colony Bankcorp

Colony Bankcorp, Inc. is the bank holding company for Colony Bank. Founded in Fitzgerald, Georgia in 1975, Colony operates locations throughout Georgia as well as in Birmingham, Alabama, and across North Florida, including Tallahassee, Jacksonville, and the Florida Panhandle. Colony Bank provides a consultative approach in offering a range of banking solutions for personal and business customers. In addition to traditional banking services, Colony Bank provides specialized solutions including mortgage lending, government-guaranteed lending, consumer insurance, wealth management, credit cards and merchant services. Colony Bankcorp’s common stock is traded on the New York Stock Exchange (“NYSE”) under the symbol “CBAN.” For more information, please visit www.colony.bank. You can also follow the Company on social media.

Forward-Looking Statements

Certain statements contained in this press release that are not statements of historical fact constitute “forward-looking statements” within the meaning of, and subject to the protections of, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In addition, certain statements may be contained in the Company’s future filings with the Securities and Exchange Commission (the “SEC”), in press releases, and in oral and written statements made by or with the approval of the Company that are not statements of historical fact and constitute “forward-looking statements” within the meaning of, and subject to the protections of, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Examples of forward-looking statements include, but are not limited to: (i) projections and/or expectations of revenues, income or loss, earnings or loss per share, the payment or nonpayment of dividends, capital structure and other financial items; (ii) statement of plans and objectives of Colony Bankcorp, Inc. or its management or Board of Directors, including those relating to products or services; (iii) statements of future economic performance; (iv) statements regarding growth strategy, capital management, liquidity and funding, and future profitability; (v) statements relating to the timing, benefits, costs, and synergies of the recently completed acquisition of TC Bancshares, Inc. (“TC Bancshares”) (the “Merger”), and (vi) statements of assumptions underlying such statements. Words such as “may”, “will”, “anticipate”, “assume”, “should”, “support”, “indicate”, “would”, “believe”, “contemplate”, “expect”, “estimate”, “continue”, “further”, “plan”, “point to”, “project”, “could”, “intend”, “target” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements.

Prospective investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve known and unknown risks and uncertainties. Factors that might cause such differences include, but are not limited to: the impact of current and future economic conditions, particularly those affecting the financial services industry, including the effects of declines in the real estate market, tariffs or trade wars (including the resulting reduced consumer spending, lower economic growth or recession, reduced demand for U.S.

3

exports, disruptions to supply chains, and decreased demand for other banking products and services), high unemployment rates, inflationary pressures, changes in interest rates (including the impact of volatile interest rates on our financial projections and models) and slowdowns in economic growth, as well as the financial stress on borrowers as a result of the foregoing; the risk of reductions in benchmark interest rates and the resulting impacts on net interest income; potential impacts of adverse developments in the banking industry highlighted by high-profile bank failures, including impacts on customer confidence, deposit outflows, liquidity and the regulatory response thereto; risks arising from negative media coverage and perceived instability in the banking industry and the banking sector; the risks of changes in interest rates and their effects on the level, cost, and composition of, and competition for, deposits, loan demand and timing of payments, the values of loan collateral, securities, and interest sensitive assets and liabilities; the ability to attract new or retain existing deposits, to retain or grow loans or additional interest and fee income, or to control noninterest expense; the effect of pricing pressures on the Company’s net interest margin; the failure of assumptions underlying the establishment of reserves for possible credit losses, fair value for loans and other real estate owned; changes in real estate values; the Company’s ability to implement its various strategic and growth initiatives; increased competition in the financial services industry, particularly from regional and national institutions, as well as fintech companies and other non-bank financial service providers offering digital, automated or alternative financial products and services; economic conditions, either nationally or locally, in areas in which the Company conducts operations being less favorable than expected; changes in the prices, values and sales volumes of residential and commercial real estate; developments in our mortgage banking business, including loan modifications, general demand, and the effects of judicial or regulatory requirements or guidance; legislation or regulatory changes which adversely affect the ability of the consolidated Company to conduct business combinations or new operations; adverse results from current or future litigation, regulatory examinations or other legal and/or regulatory actions, including as a result of the Company’s participation in and execution of government programs, those related to credit card interest rates, and legislative, regulatory or supervisory actions related to so-called “de-banking,” including any new prohibitions, requirements or enforcement priorities that could affect customer relationships, compliance obligations, or operational practices; significant turbulence or a disruption in the capital or financial markets and the effect of a fall in the stock market prices on our investment securities; significant volatility in the markets for equity, fixed income and other asset classes globally or within specific markets; the effects of war or other conflicts, including the ongoing conflicts in the Middle East; major political shifts domestically or internationally (including the potential for retaliatory actions by governments, market participants or clients based on diverging perspectives or otherwise and, separately, the recent shutdown of the U.S. federal government); general risks related to the Company’s merger and acquisition activity, including risks associated with integrating and realizing the expected financial benefits of previous or pending acquisitions, and the Company’s pursuit of future acquisitions; risks associated with the recent Merger, including the risk that the cost savings and any revenue synergies may not be realized or take longer than anticipated to be realized as well as disruption with customers, suppliers, employee or other business partners relationships; the risk of successful integration of TC Bancshares’ business into the Company; the reaction of each of the Company’s and TC Bancshares’ customers, suppliers, employees or other business partners to the Merger; the risk that the integration of TC Bancshares’ operations into the operations of the Company will be materially delayed or will be more costly or difficult than expected; the timing and achievement of expected cost reductions following the Merger; the timing and achievement of the recovery of the reduction of tangible book value resulting from the Merger; general competitive, economic, political, and market conditions; the impact of emerging technologies, such as generative artificial intelligence; fraud or misconduct by internal or external actors, and system failures, cybersecurity threats or security breaches and the cost of defending against them; a deterioration of the credit rating for U.S. long-term sovereign debt, actions that the U.S. government may take to avoid exceeding the debt ceiling, and uncertainties surrounding debt ceiling and the federal budget; and general competitive, economic, political and market conditions or other unexpected factors or events. These and other factors, risks and uncertainties could cause the actual results, performance or achievements of the Company to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. Many of these factors are beyond the Company’s ability to control or predict.

Forward-looking statements speak only as of the date on which such statements are made. These forward-looking statements are based upon information presently known to the Company’s management and are inherently subjective, uncertain and subject to change due to any number of risks and uncertainties, including, without limitation, the risks and other factors set forth in the Company’s filings with the Securities and Exchange Commission, the Company’s Annual Report on Form 10-K for the year ended December 31, 2024, under the captions “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors,” and in the Company’s quarterly reports on Form 10-Q and current reports on Form 8-K. The Company undertakes no obligation to update any forward-looking statement to reflect events or circumstances after the date on which such statement is made, or to reflect the occurrence of unanticipated events, except as required by applicable law. Readers are cautioned not to place undue reliance on these forward-looking statements.

4

Explanation of Certain Unaudited Non-GAAP Financial Measures

The measures entitled operating noninterest income, operating noninterest expense, operating net income, operating earnings per diluted share, operating return on average assets, operating return on average equity, operating return on average tangible equity, tangible book value per common share, tangible equity to tangible assets, operating efficiency ratio, operating net noninterest expense to average assets and pre-provision net revenue are not measures recognized under U.S. generally accepted accounting principles (“GAAP”) and therefore are considered non-GAAP financial measures. The most comparable GAAP measures are noninterest income, noninterest expense, net income, diluted earnings per share, return on average assets, return on average equity, book value per common share, total equity to total assets, efficiency ratio, net noninterest expense to average assets and net interest income before provision for credit losses, respectively. Operating noninterest income excludes loss on sales of securities. Operating noninterest expense excludes acquisition-related expenses, severance costs and loss related to wire fraud incident. Operating net income, operating return on average assets, operating return on average equity, operating return on average tangible equity and operating efficiency ratio all exclude acquisition-related expenses, severance costs, loss on sales of securities and loss related to wire fraud incident from net income, return on average assets, return on average equity and efficiency ratio, respectively. Operating net noninterest expense to average assets ratio excludes from net noninterest expense, severance costs, acquisition-related expenses, loss on sales of securities and loss related to wire fraud incident. Acquisition-related expenses includes fees associated with acquisitions and vendor contract buyouts. Severance costs includes costs associated with termination and retirement of employees. Operating earnings per diluted share includes the adjustments to operating net income. Tangible book value per common share, tangible equity to tangible assets and operating return on average tangible equity exclude goodwill and other intangibles from book value per common share, total equity to total assets and return on average equity, respectively. Pre-provision net revenue is calculated by adding noninterest income to net interest income before provision for credit losses, and subtracting noninterest expense.

Management uses these non-GAAP financial measures in its analysis of the Company’s performance and believes these presentations provide useful supplemental information, and a clearer understanding of the Company’s performance, and if not provided would be requested by the investor community. The Company believes the non-GAAP measures enhance investors’ understanding of the Company’s business and performance. These measures are also useful in understanding performance trends and facilitate comparisons with the performance of other financial institutions. The limitations associated with operating measures are the risk that persons might disagree as to the appropriateness of items comprising these measures and that different companies might calculate these measures differently.

These disclosures should not be considered an alternative to GAAP. The computations of operating noninterest income, operating noninterest expense, operating net income, operating earnings per diluted share, operating return on average assets, operating return on average equity, operating return on average tangible equity, tangible book value per common share, tangible equity to tangible assets, operating efficiency ratio, operating net noninterest expense to average assets and pre-provision net revenue and the reconciliation of these measures to noninterest income, noninterest expense, net income, diluted earnings per share, return on average assets, return on average equity, book value per common share, total equity to total assets, efficiency ratio, net noninterest expense to average assets and net interest income before provision for credit losses are set forth in the table below.

5

Colony Bankcorp, Inc.

Reconciliation of Non-GAAP Measures

|

|

2026 |

|

2025 |

|||||||||||

|

|

First |

|

Fourth |

|

Third |

|

Second |

|

First |

|||||

(dollars in thousands, except per share data) |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|||||

Operating noninterest income reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest income (GAAP) |

|

$ |

10,692 |

|

$ |

11,047 |

|

$ |

10,091 |

|

$ |

10,098 |

|

$ |

9,044 |

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

1,039 |

|

|

— |

|

|

— |

Operating noninterest income |

|

$ |

10,692 |

|

$ |

11,047 |

|

$ |

11,130 |

|

$ |

10,098 |

|

$ |

9,044 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating noninterest expense reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest expense (GAAP) |

|

$ |

27,674 |

|

$ |

25,709 |

|

$ |

24,612 |

|

$ |

22,004 |

|

$ |

20,221 |

Acquisition-related expenses |

|

|

(1,637) |

|

|

(1,331) |

|

|

(732) |

|

|

— |

|

|

— |

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

(1,252) |

|

|

— |

|

|

— |

Operating noninterest expense |

|

$ |

26,037 |

|

$ |

24,378 |

|

$ |

22,628 |

|

$ |

22,004 |

|

$ |

20,221 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating net income reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (GAAP) |

|

$ |

8,204 |

|

$ |

7,843 |

|

$ |

5,819 |

|

$ |

7,978 |

|

$ |

6,613 |

Acquisition-related expenses |

|

|

1,637 |

|

|

1,331 |

|

|

732 |

|

|

— |

|

|

— |

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

1,252 |

|

|

— |

|

|

— |

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

1,039 |

|

|

— |

|

|

— |

Income tax benefit |

|

|

(356) |

|

|

(269) |

|

|

(612) |

|

|

— |

|

|

— |

Operating net income |

|

$ |

9,485 |

|

$ |

8,905 |

|

$ |

8,230 |

|

$ |

7,978 |

|

$ |

6,613 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average diluted shares |

|

|

21,222,237 |

|

|

18,729,511 |

|

|

17,461,434 |

|

|

17,448,945 |

|

|

17,509,059 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating earnings per diluted share |

|

$ |

0.45 |

|

$ |

0.48 |

|

$ |

0.47 |

|

$ |

0.46 |

|

$ |

0.38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating return on average assets reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets (GAAP) |

|

|

0.90 |

% |

|

0.93 |

% |

|

0.75 |

% |

|

1.02 |

% |

|

0.85 |

Acquisition-related expenses |

|

|

0.18 |

|

|

0.15 |

|

|

0.10 |

|

|

— |

|

|

— |

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

0.16 |

|

|

— |

|

|

— |

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

0.13 |

|

|

— |

|

|

— |

Tax effect of adjustment items |

|

|

(0.04) |

|

|

(0.03) |

|

|

(0.08) |

|

|

— |

|

|

— |

Operating return on average assets |

|

|

1.04 |

% |

|

1.05 |

% |

|

1.06 |

% |

|

1.02 |

% |

|

0.85 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating return on average equity reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average equity (GAAP) |

|

|

8.77 |

% |

|

9.49 |

% |

|

7.80 |

% |

|

11.14 |

% |

|

9.63 |

Acquisition-related expenses |

|

|

1.74 |

|

|

1.62 |

|

|

0.98 |

|

|

— |

|

|

— |

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

1.68 |

|

|

— |

|

|

— |

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

1.39 |

|

|

— |

|

|

— |

Tax effect of adjustment items |

|

|

(0.38) |

|

|

(0.33) |

|

|

(0.82) |

|

|

— |

|

|

— |

Operating return on average equity |

|

|

10.13 |

% |

|

10.78 |

% |

|

11.03 |

% |

|

11.14 |

% |

|

9.63 |

6

Colony Bankcorp, Inc.

Reconciliation of Non-GAAP Measures

|

|

2026 |

|

2025 |

|

|||||||||||

|

|

First |

|

Fourth |

|

Third |

|

Second |

|

First |

|

|||||

(dollars in thousands, except per share data) |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

|||||

Operating return on average tangible equity reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average tangible equity |

|

|

10.80 |

% |

|

11.63 |

% |

|

9.56 |

% |

|

13.70 |

% |

|

11.83 |

% |

Acquisition-related expenses |

|

|

2.16 |

|

|

1.97 |

|

|

1.20 |

|

|

— |

|

|

— |

|

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

2.06 |

|

|

— |

|

|

— |

|

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

1.71 |

|

|

— |

|

|

— |

|

Tax effect of adjustment items |

|

|

(0.47) |

|

|

(0.40) |

|

|

(1.01) |

|

|

— |

|

|

— |

|

Operating return on average tangible equity |

|

|

12.49 |

% |

|

13.20 |

% |

|

13.52 |

% |

|

13.70 |

% |

|

11.83 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tangible book value per common share reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Book value per common share (GAAP) |

|

$ |

17.98 |

|

$ |

17.69 |

|

$ |

17.31 |

|

$ |

16.87 |

|

$ |

16.41 |

|

Effect of goodwill and other intangibles |

|

|

(3.33) |

|

|

(3.38) |

|

|

(3.11) |

|

|

(3.14) |

|

|

(2.95) |

|

Tangible book value per common share |

|

$ |

14.65 |

|

$ |

14.31 |

|

$ |

14.20 |

|

$ |

13.73 |

|

$ |

13.46 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tangible equity to tangible assets reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity to assets (GAAP) |

|

|

10.22 |

% |

|

10.06 |

% |

|

9.59 |

% |

|

9.43 |

% |

|

9.05 |

% |

Effect of goodwill and other intangibles |

|

|

(1.73) |

|

|

(1.76) |

|

|

(1.59) |

|

|

(1.62) |

|

|

(1.51) |

|

Tangible equity to tangible assets |

|

|

8.49 |

% |

|

8.30 |

% |

|

8.00 |

% |

|

7.81 |

% |

|

7.54 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating efficiency ratio calculation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Efficiency ratio (GAAP) |

|

|

69.37 |

% |

|

69.65 |

% |

|

75.06 |

% |

|

67.74 |

% |

|

67.41 |

% |

Acquisition-related expenses |

|

|

(4.10) |

|

|

(3.61) |

|

|

(1.98) |

|

|

— |

|

|

— |

|

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

(3.38) |

|

|

— |

|

|

— |

|

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

(2.81) |

|

|

— |

|

|

— |

|

Operating efficiency ratio |

|

|

65.27 |

% |

|

66.04 |

% |

|

66.89 |

% |

|

67.74 |

% |

|

67.41 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating net noninterest expense(1) to average assets calculation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net noninterest expense to average assets |

|

|

1.86 |

% |

|

1.73 |

% |

|

1.86 |

% |

|

1.52 |

% |

|

1.44 |

% |

Acquisition-related expenses |

|

|

(0.18) |

|

|

(0.15) |

|

|

(0.09) |

|

|

— |

|

|

— |

|

Loss related to wire fraud incident |

|

|

— |

|

|

— |

|

|

(0.16) |

|

|

— |

|

|

— |

|

Loss on sales of securities |

|

|

— |

|

|

— |

|

|

(0.13) |

|

|

— |

|

|

— |

|

Operating net noninterest expense to average assets |

|

|

1.68 |

% |

|

1.58 |

% |

|

1.48 |

% |

|

1.52 |

% |

|

1.44 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pre-provision net revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income before provision for credit losses |

|

$ |

29,203 |

|

$ |

25,865 |

|

$ |

22,699 |

|

$ |

22,385 |

|

$ |

20,952 |

|

Noninterest income |

|

|

10,692 |

|

|

11,047 |

|

|

10,091 |

|

|

10,098 |

|

|

9,044 |

|

Total income |

|

|

39,895 |

|

|

36,912 |

|

|

32,790 |

|

|

32,483 |

|

|

29,996 |

|

Noninterest expense |

|

|

27,674 |

|

|

25,709 |

|

|

24,612 |

|

|

22,004 |

|

|

20,221 |

|

Pre-provision net revenue |

|

$ |

12,221 |

|

$ |

11,203 |

|

$ |

8,178 |

|

$ |

10,479 |

|

$ |

9,775 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating pre-provision net revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income before provision for credit losses |

|

$ |

29,203 |

|

$ |

25,865 |

|

$ |

22,699 |

|

$ |

22,385 |

|

$ |

20,952 |

|

Operating noninterest income |

|

|

10,692 |

|

|

11,047 |

|

|

11,130 |

|

|

10,098 |

|

|

9,044 |

|

Total operating income |

|

|

39,895 |

|

|

36,912 |

|

|

33,829 |

|

|

32,483 |

|

|

29,996 |

|

Operating noninterest expense |

|

|

26,037 |

|

|

24,378 |

|

|

22,628 |

|

|

22,004 |

|

|

20,221 |

|

Operating pre-provision net revenue |

|

$ |

13,858 |

|

$ |

12,534 |

|

$ |

11,201 |

|

$ |

10,479 |

|

$ |

9,775 |

|

| (1) | Net noninterest expense is defined as noninterest expense less noninterest income. |

7

Colony Bankcorp, Inc.

Selected Financial Information

|

|

2026 |

|

2025 |

|

|||||||||||

|

|

First |

|

Fourth |

|

Third |

|

Second |

|

First |

|

|||||

(dollars in thousands, except per share data) |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

|||||

EARNINGS SUMMARY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

$ |

29,203 |

|

$ |

25,865 |

|

$ |

22,699 |

|

$ |

22,385 |

|

$ |

20,952 |

|

Provision for credit losses |

|

|

1,750 |

|

|

1,650 |

|

|

900 |

|

|

450 |

|

|

1,500 |

|

Noninterest income |

|

|

10,692 |

|

|

11,047 |

|

|

10,091 |

|

|

10,098 |

|

|

9,044 |

|

Noninterest expense |

|

|

27,674 |

|

|

25,709 |

|

|

24,612 |

|

|

22,004 |

|

|

20,221 |

|

Income taxes |

|

|

2,267 |

|

|

1,710 |

|

|

1,459 |

|

|

2,051 |

|

|

1,662 |

|

Net income |

|

$ |

8,204 |

|

$ |

7,843 |

|

$ |

5,819 |

|

$ |

7,978 |

|

$ |

6,613 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PER COMMON SHARE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common shares outstanding |

|

|

21,162,104 |

|

|

21,251,695 |

|

|

17,461,284 |

|

|

17,416,702 |

|

|

17,481,709 |

|

Weighted average basic shares |

|

|

21,222,237 |

|

|

18,729,511 |

|

|

17,461,434 |

|

|

17,448,945 |

|

|

17,509,059 |

|

Weighted average diluted shares |

|

|

21,222,237 |

|

|

18,729,511 |

|

|

17,461,434 |

|

|

17,448,945 |

|

|

17,509,059 |

|

Earnings per basic share |

|

$ |

0.39 |

|

$ |

0.42 |

|

$ |

0.33 |

|

$ |

0.46 |

|

$ |

0.38 |

|

Earnings per diluted share |

|

|

0.39 |

|

|

0.42 |

|

|

0.33 |

|

|

0.46 |

|

|

0.38 |

|

Operating earnings per diluted share(b) |

|

|

0.45 |

|

|

0.48 |

|

|

0.47 |

|

|

0.46 |

|

|

0.38 |

|

Cash dividends declared per share |

|

|

0.1200 |

|

|

0.1150 |

|

|

0.1150 |

|

|

0.1150 |

|

|

0.1150 |

|

Common book value per share |

|

|

17.98 |

|

|

17.69 |

|

|

17.31 |

|

|

16.87 |

|

|

16.41 |

|

Tangible book value per common share(b) |

|

|

14.65 |

|

|

14.31 |

|

|

14.20 |

|

|

13.73 |

|

|

13.46 |

|

Pre-provision net revenue(b) |

|

|

12,221 |

|

|

11,203 |

|

|

8,178 |

|

|

10,479 |

|

|

9,775 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SELECTED PERFORMANCE RATIOS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets |

|

|

0.90 |

% |

|

0.93 |

% |

|

0.75 |

% |

|

1.02 |

% |

|

0.85 |

% |

Return on average total equity |

|

|

8.77 |

|

|

9.49 |

|

|

7.80 |

|

|

11.14 |

|

|

9.63 |

|

Return on average tangible equity |

|

|

10.80 |

|

|

11.63 |

|

|

9.56 |

|

|

13.70 |

|

|

11.83 |

|

Efficiency ratio |

|

|

69.37 |

|

|

69.65 |

|

|

75.06 |

|

|

67.74 |

|

|

67.41 |

|

Net noninterest expense to average assets |

|

|

1.86 |

|

|

1.73 |

|

|

1.86 |

|

|

1.52 |

|

|

1.44 |

|

Total equity to total assets |

|

|

10.22 |

|

|

10.06 |

|

|

9.59 |

|

|

9.43 |

|

|

9.05 |

|

Tangible equity to tangible assets (b) |

|

|

8.49 |

|

|

8.30 |

|

|

8.00 |

|

|

7.81 |

|

|

7.54 |

|

Net interest margin (a) |

|

|

3.48 |

|

|

3.32 |

|

|

3.17 |

|

|

3.12 |

|

|

2.93 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

OPERATING SELECTED PERFORMANCE RATIOS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating return on average assets (b) |

|

|

1.04 |

% |

|

1.05 |

% |

|

1.06 |

% |

|

1.02 |

% |

|

0.85 |

% |

Operating return on average total equity (b) |

|

|

10.13 |

|

|

10.78 |

|

|

11.03 |

|

|

11.14 |

|

|

9.63 |

|

Operating return on average tangible equity (b) |

|

|

12.49 |

|

|

13.20 |

|

|

13.52 |

|

|

13.70 |

|

|

11.83 |

|

Operating efficiency ratio (b) |

|

|

65.27 |

|

|

66.04 |

|

|

66.89 |

|

|

67.74 |

|

|

67.41 |

|

Operating net noninterest expense to average assets(b) |

|

|

1.68 |

|

|

1.58 |

|

|

1.48 |

|

|

1.52 |

|

|

1.44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8

Colony Bankcorp, Inc.

Selected Financial Information

|

|

2026 |

|

2025 |

|

|||||||||||

|

|

First |

|

Fourth |

|

Third |

|

Second |

|

First |

|

|||||

(dollars in thousands, except per share data) |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

|||||

ASSET QUALITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonperforming portfolio loans |

|

$ |

12,619 |

|

$ |

17,190 |

|

$ |

9,082 |

|

$ |

4,760 |

|

$ |

7,538 |

|

Nonperforming SBA government loans-guaranteed portion |

|

|

2,012 |

|

|

4,772 |

|

|

4,076 |

|

|

4,583 |

|

|

3,647 |

|

Nonperforming SBA government loans-unguaranteed portion |

|

|

2,968 |

|

|

1,418 |

|

|

1,110 |

|

|

1,241 |

|

|

1,271 |

|

Loans 90 days past due and still accruing |

|

|

178 |

|

|

95 |

|

|

98 |

|

|

107 |

|

|

22 |

|

Total nonperforming loans (NPLs) |

|

|

17,777 |

|

|

23,475 |

|

|

14,366 |

|

|

10,691 |

|

|

12,478 |

|

Other real estate owned |

|

|

1,873 |

|

|

1,048 |

|

|

710 |

|

|

710 |

|

|

522 |

|

Repossessed assets |

|

|

205 |

|

|

190 |

|

|

160 |

|

|

21 |

|

|

6 |

|

Total nonperforming assets (NPAs) |

|

|

19,855 |

|

|

24,713 |

|

|

15,236 |

|

|

11,422 |

|

|

13,006 |

|

Classified loans |

|

|

39,225 |

|

|

40,481 |

|

|

24,183 |

|

|

25,112 |

|

|

26,453 |

|

Criticized loans |

|

|

86,740 |

|

|

84,721 |

|

|

60,505 |

|

|

54,814 |

|

|

55,823 |

|

Net loan charge-offs (recoveries) |

|

|

1,709 |

|

|

1,600 |

|

|

1,827 |

|

|

1,049 |

|

|

606 |

|

Allowance for credit losses to total loans |

|

|

0.90 |

% |

|

0.97 |

% |

|

0.89 |

% |

|

0.96 |

% |

|

1.04 |

% |

Allowance for credit losses to total NPLs |

|

|

122.10 |

|

|

98.04 |

|

|

125.89 |

|

|

179.15 |

|

|

160.26 |

|

Allowance for credit losses to total NPAs |

|

|

109.32 |

|

|

93.13 |

|

|

118.71 |

|

|

167.69 |

|

|

153.75 |

|

Net charge-offs (recoveries) to average loans, net |

|

|

0.29 |

|

|

0.30 |

|

|

0.36 |

|

|

0.21 |

|

|

0.13 |

|

NPLs to total loans |

|

|

0.74 |

|

|

0.99 |

|

|

0.71 |

|

|

0.54 |

|

|

0.65 |

|

NPAs to total assets |

|

|

0.53 |

|

|

0.66 |

|

|

0.48 |

|

|

0.37 |

|

|

0.41 |

|

NPAs to total loans and foreclosed assets |

|

|

0.82 |

|

|

1.04 |

|

|

0.75 |

|

|

0.57 |

|

|

0.68 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ACTUAL BALANCES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ |

3,720,613 |

|

$ |

3,735,401 |

|

$ |

3,152,746 |

|

$ |

3,115,617 |

|

$ |

3,171,825 |

|

Loans held for sale |

|

|

16,536 |

|

|

78,990 |

|

|

19,286 |

|

|

22,163 |

|

|

24,844 |

|

Loans, net of unearned income |

|

|

2,413,465 |

|

|

2,381,224 |

|

|

2,037,056 |

|

|

1,993,580 |

|

|

1,921,263 |

|

Deposits |

|

|

3,048,419 |

|

|

3,067,521 |

|

|

2,584,329 |

|

|

2,556,230 |

|

|

2,622,531 |

|

Total stockholders’ equity |

|

|

380,403 |

|

|

375,920 |

|

|

302,332 |

|

|

293,857 |

|

|

286,925 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AVERAGE BALANCES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ |

3,698,663 |

|

$ |

3,357,785 |

|

$ |

3,092,411 |

|

$ |

3,138,125 |

|

$ |

3,149,321 |

|

Loans held for sale |

|

|

21,863 |

|

|

59,868 |

|

|

17,062 |

|

|

22,495 |

|

|

23,253 |

|

Loans, net of unearned income |

|

|

2,399,971 |

|

|

2,148,729 |

|

|

2,024,153 |

|

|

1,960,025 |

|

|

1,869,476 |

|

Deposits |

|

|

3,025,462 |

|

|

2,752,576 |

|

|

2,526,739 |

|

|

2,586,620 |

|

|

2,606,706 |

|

Total stockholders’ equity |

|

|

379,582 |

|

|

327,830 |

|

|

296,027 |

|

|

287,325 |

|

|

278,551 |

|

| (a) | Computed using fully taxable-equivalent net income. |

| (b) | Non-GAAP measure - see “Explanation of Certain Unaudited Non-GAAP Financial Measures” for more information and reconciliation to GAAP. |

9

Colony Bankcorp, Inc.

Average Balance Sheet and Net Interest Analysis

|

|

Three Months Ended March 31, |

|

||||||||||||||

|

|

2026 |

|

2025 |

|

||||||||||||

|

|

Average |

|

Income/ |

|

Yields/ |

|

Average |

|

Income/ |

|

Yields/ |

|

||||

(dollars in thousands) |

|

Balances |

|

Expense |

|

Rates |

|

Balances |

|

Expense |

|

Rates |

|

||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-earning assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans held for sale |

|

$ |

21,863 |

|

$ |

454 |

|

8.42 |

% |

$ |

23,253 |

|

$ |

328 |

|

5.73 |

% |

Loans, net of unearned income 1 |

|

|

2,399,971 |

|

|

37,568 |

|

6.35 |

% |

|

1,869,476 |

|

|

27,716 |

|

6.01 |

% |

Investment securities, taxable |

|

|

668,824 |

|

|

4,537 |

|

2.75 |

% |

|

710,293 |

|

|

4,837 |

|

2.76 |

% |

Investment securities, tax-exempt 2 |

|

|

94,588 |

|

|

489 |

|

2.10 |

% |

|

94,379 |

|

|

494 |

|

2.12 |

% |

Deposits in banks and short term investments |

|

|

240,446 |

|

|

1,993 |

|

3.36 |

% |

|

229,016 |

|

|

2,322 |

|

4.11 |

% |

Total interest-earning assets |

|

|

3,425,692 |

|

|

45,041 |

|

5.33 |

% |

|

2,926,417 |

|

|

35,697 |

|

4.95 |

% |

Noninterest-earning assets |

|

|

272,972 |

|

|

|

|

|

|

|

222,904 |

|

|

|

|

|

|

Total assets |

|

$ |

3,698,663 |

|

|

|

|

|

|

$ |

3,149,321 |

|

|

|

|

|

|

Liabilities and stockholders’ equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand and savings |

|

$ |

1,725,632 |

|

$ |

5,951 |

|

1.40 |

% |

$ |

1,549,509 |

|

$ |

6,468 |

|

1.69 |

% |

Other time |

|

|

812,531 |

|

|

6,863 |

|

3.43 |

% |

|

601,920 |

|

|

5,305 |

|

3.57 |

% |

Total interest-bearing deposits |

|

|

2,538,163 |

|

|

12,814 |

|

2.05 |

% |

|

2,151,429 |

|

|

11,773 |

|

2.22 |

% |

Federal funds purchased |

|

|

0 |

|

|

— |

|

— |

% |

|

— |

|

|

— |

|

— |

% |

Federal Home Loan Bank advances |

|

|

195,000 |

|

|

1,985 |

|

4.13 |

% |

|

185,000 |

|

|

1,873 |

|

4.10 |

% |

Other borrowings |

|

|

63,141 |

|

|

888 |

|

5.71 |

% |

|

63,048 |

|

|

927 |

|

5.97 |

% |

Total other interest-bearing liabilities |

|

|

258,141 |

|

|

2,873 |

|

4.51 |

% |

|

248,048 |

|

|

2,800 |

|

4.58 |

% |

Total interest-bearing liabilities |

|

|

2,796,304 |

|

|

15,687 |

|

2.28 |

% |

|

2,399,477 |

|

|

14,573 |

|

2.46 |

% |

Noninterest-bearing liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand deposits |

|

|

487,299 |

|

|

|

|

|

|

$ |

455,277 |

|

|

|

|

|

|

Other liabilities |

|

|

35,479 |

|

|

|

|

|

|

|

16,016 |

|

|

|

|

|

|

Stockholders’ equity |

|

|

379,582 |

|

|

|

|

|

|

|

278,551 |

|

|

|

|

|

|

Total noninterest-bearing liabilities and stockholders’ equity |

|

|

902,360 |

|

|

|

|

|

|

|

749,844 |

|

|

|

|

|

|

Total liabilities and stockholders’ equity |

|

$ |

3,698,663 |

|

|

|

|

|

|

$ |

3,149,321 |

|

|

|

|

|

|

Interest rate spread |

|

|

|

|

|

|

|

3.05 |

% |

|

|

|

|

|

|

2.49 |

% |

Net interest income |

|

|

|

|

$ |

29,354 |

|

|

|

|

|

|

$ |

21,124 |

|

|

|

Net interest margin |

|

|

|

|

|

|

|

3.48 |

% |

|

|

|

|

|

|

2.93 |

% |

1 The average balance of loans includes the average balance of nonaccrual loans. Income on such loans is recognized and recorded on the cash basis. Taxable-equivalent adjustments totaling $48,000 and $68,000 for the quarters ended March 31, 2026 and 2025, respectively, are calculated using the statutory federal tax rate and are included in income and fees on loans. Accretion income of $1.3 million and $20,000 for the quarters ended March 31, 2026 and 2025, respectively, are also included in income and fees on loans.

2 Taxable-equivalent adjustments totaling $103,000 and $104,000 for the quarters ended March 31, 2026 and 2025, respectively, are calculated using the statutory federal tax rate and are included in tax-exempt interest on investment securities.

10

Colony Bankcorp, Inc.

Segment Reporting

|

|

2026 |

|

2025 |

|||||||||||

|

|

First |

|

Fourth |

|

Third |

|

Second |

|

First |

|||||

(dollars in thousands) |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|

Quarter |

|||||

Banking Division |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

$ |

28,223 |

|

$ |

24,781 |

|

$ |

21,629 |

|

$ |

21,319 |

|

$ |

19,989 |

Provision for credit losses |

|

|

780 |

|

|

776 |

|

|

(371) |

|

|

(330) |

|

|

1,221 |

Noninterest income |

|

|

7,131 |

|

|

6,996 |

|

|

6,144 |

|

|

5,969 |

|

|

5,774 |

Noninterest expenses |

|

|

24,420 |

|

|

22,502 |

|

|

21,075 |

|

|

18,269 |

|

|

16,790 |

Income taxes |

|

|

2,194 |

|

|

1,493 |

|

|

1,413 |

|

|

1,908 |

|

|

1,551 |

Segment income |

|

$ |

7,960 |

|

$ |

7,006 |

|

$ |

5,656 |

|

$ |

7,441 |

|

$ |

6,201 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total segment assets |

|

$ |

3,619,249 |

|

$ |

3,625,785 |

|

$ |

3,046,699 |

|

$ |

3,010,416 |

|

$ |

3,065,385 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full time employees |

|

|

426 |

|

|

447 |

|

|

383 |

|

|

390 |

|

|

366 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mortgage Banking Division |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

$ |

38 |

|

$ |

65 |

|

$ |

62 |

|

$ |

44 |

|

$ |

53 |

Provision for credit losses |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

Noninterest income |

|

|

1,886 |

|

|

2,012 |

|

|

1,851 |

|

|

1,984 |

|

|

1,579 |

Noninterest expenses |

|

|

1,702 |

|

|

1,695 |

|

|

2,066 |

|

|

1,710 |

|

|

1,601 |

Income taxes |

|

|

52 |

|

|

81 |

|

|

(27) |

|

|

69 |

|

|

10 |

Segment income |

|

$ |

170 |

|

$ |

301 |

|

$ |

(126) |

|

$ |

249 |

|

$ |

21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total segment assets |

|

$ |

12,036 |

|

$ |

13,648 |

|

$ |

12,959 |

|

$ |

14,296 |

|

$ |

16,041 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Variable noninterest expense(1) |

|

$ |

597 |

|

$ |

984 |

|

$ |

1,229 |

|

$ |

1,157 |

|

$ |

880 |

Fixed noninterest expense |

|

|

1,105 |

|

|

711 |

|

|

837 |

|

|

553 |

|

|

721 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full time employees |

|

|

48 |

|

|

48 |

|

|

46 |

|

|

43 |

|

|

42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Small Business Specialty Lending Division |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

$ |

942 |

|

$ |

1,019 |

|

$ |

1,008 |

|

$ |

1,022 |

|

$ |

910 |

Provision for credit losses |

|

|

970 |

|

|

874 |

|

|

1,271 |

|

|

780 |

|

|

279 |

Noninterest income |

|

|

1,675 |

|

|

2,039 |

|

|

2,096 |

|

|

2,145 |

|

|

1,691 |

Noninterest expenses |

|

|

1,552 |

|

|

1,512 |

|

|

1,471 |

|

|

2,025 |

|

|

1,830 |

Income taxes |

|

|

21 |

|

|

136 |

|

|

73 |

|

|

74 |

|

|

101 |

Segment income |

|

$ |

74 |

|

$ |

536 |

|

$ |

289 |

|

$ |

288 |

|

$ |

391 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total segment assets |

|

$ |

89,328 |

|

$ |

95,968 |

|

$ |

93,088 |

|

$ |

90,905 |

|

$ |

90,399 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full time employees |

|

|

32 |

|

|

31 |

|

|

31 |

|

|

34 |

|

|

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Consolidated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

$ |

29,203 |

|

$ |

25,865 |

|

$ |

22,699 |

|

$ |

22,385 |

|

$ |

20,952 |

Provision for credit losses |

|

|

1,750 |

|

|

1,650 |

|

|

900 |

|

|

450 |

|

|

1,500 |

Noninterest income |

|

|

10,692 |

|

|

11,047 |

|

|

10,091 |

|

|

10,098 |

|

|

9,044 |

Noninterest expenses |

|

|

27,674 |

|

|

25,709 |

|

|

24,612 |

|

|

22,004 |

|

|

20,221 |

Income taxes |

|

|

2,267 |

|

|

1,710 |

|

|

1,459 |

|

|

2,051 |

|

|

1,662 |

Segment income |

|

$ |

8,204 |

|

$ |

7,843 |

|

$ |

5,819 |

|

$ |

7,978 |

|

$ |

6,613 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total segment assets |

|

$ |

3,720,613 |

|

$ |

3,735,401 |

|

$ |

3,152,746 |

|

$ |

3,115,617 |

|

$ |

3,171,825 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full time employees |

|

|

506 |

|

|

526 |

|

|

460 |

|

|

467 |

|

|

443 |

| (1) | Variable noninterest expense includes commission based salary expenses and volume based loan related fees. |

11

Colony Bankcorp, Inc.

Consolidated Balance Sheets

|

|

March 31, 2026 |

|

December 31, 2025 |

||

(dollars in thousands) |

|

(unaudited) |

|

(audited) |

||

ASSETS |

|

|

|

|

|

|

Cash and due from banks |

|

$ |

24,349 |

|

$ |

27,307 |

Interest-bearing deposits in banks and federal funds sold |

|

|

271,457 |

|

|

230,333 |

Cash and cash equivalents |

|

|

295,806 |

|

|

257,640 |

Investment securities available for sale, at fair value |

|

|

375,340 |

|

|

383,817 |

Investment securities held to maturity, at amortized cost |

|

|

371,918 |

|

|

386,618 |

Other investments |

|

|

19,286 |

|

|

19,176 |

Loans held for sale |

|

|

16,536 |

|

|

78,990 |

Loans, net of unearned income |

|

|

2,413,465 |

|

|

2,381,224 |

Allowance for credit losses |

|

|

(21,705) |

|

|

(23,014) |

Loans, net |

|

|

2,391,760 |

|

|

2,358,210 |

Premises and equipment |

|

|

36,842 |

|

|

37,045 |

Other real estate owned |

|

|

1,873 |

|

|

1,048 |

Goodwill |

|

|

63,047 |

|

|

63,873 |

Other intangible assets |

|

|

7,396 |

|

|

7,851 |

Bank owned life insurance |

|

|

68,936 |

|

|

68,457 |

Deferred income taxes, net |

|

|

18,804 |

|

|

19,582 |

Other assets |

|

|

53,069 |

|

|

53,094 |

Total assets |

|

$ |

3,720,613 |

|

$ |

3,735,401 |

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

Liabilities: |

|

|

|

|

|

|

Deposits: |

|

|

|

|

|

|

Noninterest-bearing |

|

$ |

495,234 |

|

$ |

526,803 |

Interest-bearing |

|

|

2,553,185 |

|

|

2,540,718 |

Total deposits |

|

|

3,048,419 |

|

|

3,067,521 |

Federal Home Loan Bank advances |

|

|

194,981 |

|

|

194,972 |

Other borrowed money |

|

|

63,156 |

|

|

63,132 |

Accrued expenses and other liabilities |

|

|

33,654 |

|

|

33,856 |

Total liabilities |

|

|

3,340,210 |