UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 40-F

(Check One)

☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 |

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13(A) OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2025 |

|

Commission file number: 001-33414 |

DENISON MINES CORP.

(Exact name of registrant as specified in its charter)

Ontario, Canada

(Province or other jurisdiction of incorporation or organization)

1090

(Primary standard industrial classification code number)

98-0622284

(I.R.S. employer identification number)

1100 – 40 University Avenue

Toronto, Ontario M5J 1T1 Canada

416-979-1991

(Address and telephone number of registrant’s principal executive offices)

C T Corporation System

28 Liberty Street

New York, NY 10005

Phone number: 212-894-8940

(Name, address and telephone number of agent for service in the United States)

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934 (“Exchange Act”):

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common Shares |

DNN |

NYSE American LLC |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Exchange Act: Not applicable.

For annual reports, indicate by check mark the information filed with this form:

☒ Annual Information Form |

☒ Audited Annual Financial Statements |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 901,610,950 Common Shares as of December 31, 2025.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13(d) or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant has been required to file such reports); and (2) has been subject to such filing requirements in the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Exchange Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

EXPLANATORY NOTE

Denison Mines Corp. (the “Company” or the “Registrant”) is an Ontario corporation eligible to file its Annual Report pursuant to Section 13(a) of the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), on Form 40-F. The Registrant is a “foreign private issuer” as defined in Rule 3b-4 under the Exchange Act. Equity securities of the Registrant are accordingly exempt from Sections 14(a), 14(b), 14(c), 14(f) and 16(b) and 16(c) of the Exchange Act pursuant to Rule 3a12-3 thereunder.

DOCUMENTS FILED PURSUANT TO GENERAL INSTRUCTIONS

In accordance with General Instruction B.(3) of Form 40-F, the Registrant hereby incorporates by reference Exhibits 99.1 through 99.3 as set forth in the Exhibit Index attached hereto, which are deemed filed herewith.

In accordance with General Instruction D.(9) of Form 40-F, the Registrant has filed written consents of certain experts named in the foregoing Exhibits as Exhibits 99.4 and 99.9 through 99.28, as set forth in the Exhibit Index attached hereto.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain of the information contained in this Annual Report on Form 40-F, including the documents incorporated herein by reference, may contain “forward-looking information” and “forward-looking statements” within the meaning of applicable Canadian and U.S. securities laws. Forward-looking information and statements may include, among others, statements regarding the future plans, costs, objectives or performance of the Company, or the assumptions underlying any of the foregoing. In this Annual Report on Form 40-F, words such as “may”, “would”, “could”, “will”, “likely”, “believe”, “expect”, “anticipate”, “intend”, “plan”, “estimate” and similar words and the negative form thereof are used to identify forward-looking statements. Forward-looking statements should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether, or the times at or by which, such future performance will be achieved. Forward-looking statements and information are based on information available at the time and/or management’s good-faith belief with respect to future events and are subject to known or unknown risks, uncertainties and other unpredictable factors, many of which are beyond the Company’s control. These risks, uncertainties and assumptions include, but are not limited to, those described under the section “Risk Factors” in the Company’s Annual Information Form for the fiscal year ended December 31, 2025 (the “AIF”), which is filed as Exhibit 99.1 to this Annual Report on Form 40-F, and could cause actual events or results to differ materially from those projected in any forward-looking statements.

The Company’s forward-looking statements contained in the exhibits incorporated by reference into this Annual Report on Form 40-F are made as of the respective dates set forth in such exhibits. In preparing this Annual Report on Form 40-F, the Company has not updated such forward-looking statements to reflect any subsequent information, events or circumstances or otherwise, or any change in management’s beliefs, expectations or opinions that may have occurred prior to the date hereof, nor does the Company assume any obligation to update such forward-looking statements in the future, except as required by applicable laws.

NOTE TO UNITED STATES READERS – DIFFERENCES IN UNITED STATES AND CANADIAN REPORTING PRACTICES

The Registrant is permitted, under a multijurisdictional disclosure system adopted by the United States, to prepare this Annual Report on Form 40-F in accordance with Canadian disclosure requirements, which are different from those of the United States.

The Registrant prepares its consolidated financial statements, which are filed with this Annual Report on Form 40-F, in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board (“IFRS”). IFRS differs in some significant respects from United States generally accepted accounting principles (“U.S. GAAP”), and thus the Registrant’s financial statements may not be comparable to the financial statements of United States companies. These differences between IFRS and U.S. GAAP might be material to the financial information presented in this Annual Report on Form 40-F. In addition, differences may arise in subsequent periods related to changes in IFRS or U.S. GAAP or due to new transactions that the Registrant enters into. The Registrant is not required to prepare a reconciliation of its consolidated financial statements and related footnote disclosures between IFRS and U.S. GAAP and has not quantified such differences.

CURRENCY

Unless otherwise indicated, all dollar amounts in this Annual Report on Form 40-F are in Canadian dollars. The daily exchange rate published by the Bank of Canada for the exchange of Canadian dollars into United States dollars on December 31, 2025 was CDN$1.00 = U.S.$0.7296. The daily exchange rate published by the Bank of Canada for the exchange of Canadian dollars into United States dollars on December 31, 2024 was CDN$1.00 = U.S.$0.6950.

DISCLOSURE CONTROLS AND PROCEDURES AND

INTERNAL CONTROL OVER FINANCIAL REPORTING

A.Disclosure Controls and Procedures

The Company maintains disclosure controls and procedures to ensure that information required to be disclosed in the Company’s filings under the Exchange Act, is recorded, processed, summarized and reported in accordance with the requirements specified in the rules and forms of the SEC. The Company carried out an evaluation, under the supervision and with the participation of its management, including the Chief Executive Officer and Chief Financial Officer, of the effectiveness of the design and operation of the Company’s “disclosure controls and procedures” (as defined in Rule 13a-15(e) or Rule 15d-15(e) under the Exchange Act) as of the end of the period covered by this Annual Report on Form 40-F. Based upon that evaluation, the Chief Executive Officer and Chief Financial Officer concluded that the Company’s disclosure controls and procedures as of December 31, 2025 were effective to ensure that information required to be disclosed by the Registrant in reports it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms and is accumulated and communicated to the Registrant’s management, including its Chief Executive Officer and Chief Financial Officer, as appropriate to allow timely decisions regarding required disclosure.

The Company’s disclosure controls and procedures are designed to provide reasonable assurance of achieving their objectives and, as indicated in the preceding paragraph, the Chief Executive Officer and Chief Financial Officer believe that the Company’s disclosure controls and procedures are effective at that reasonable assurance level, although the Chief Executive Officer and Chief Financial Officer do not expect that the disclosure controls and procedures will prevent or detect all errors and all fraud.

It should be noted that a control system, no matter how well conceived or operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. The Company will continue to periodically review its disclosure controls and procedures and may make such modifications from time to time as it considers necessary.

B.Management’s Annual Report on Internal Control Over Financial Reporting

The Company’s management, including the Chief Executive Officer and Chief Financial Officer, is responsible for establishing and maintaining adequate internal control over the Company’s financial reporting (as defined in Rules 13a-15(f) or 15d-15(f) under the Exchange Act). Internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of the Company’s financial reporting and the preparation of financial statements for external purposes in accordance with IFRS.

A company’s internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Management, including the Chief Executive Officer and Chief Financial Officer, conducted an assessment of the Company’s internal control over financial reporting based on the framework established by the Committee of Sponsoring Organizations of the Treadway Commission on Internal Control — Integrated Framework (2013). Based on this assessment, management concluded that, as of December 31, 2025, the Company’s internal control over financial reporting is effective.

It should be noted that a control system, no matter how well conceived or operated, can only provide reasonable, not absolute, assurance that the objectives of the control system are met. The Company will continue to periodically review its internal control over financial reporting and may make such modifications from time to time as it considers necessary.

C.Attestation Report of the Independent Registered Public Accounting Firm

The effectiveness of the Registrant’s internal control over financial reporting as of December 31, 2025 has been audited by KPMG LLP, an Independent Registered Public Accounting Firm, as stated in their report included with the Registrant’s Audited Financial Statements, which are incorporated by reference as Exhibit 99.3 to this Annual Report on Form 40-F.

D.Changes in Internal Control Over Financial Reporting

There were no changes in the Company’s internal control over financial reporting during the twelve months ended December 31, 2025 that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

NOTICES PURSUANT TO REGULATION BTR

There were no notices required by Rule 104 of Regulation BTR during the fiscal year ended December 31, 2025, concerning any equity security subject to a blackout period under Rule 101 of Regulation BTR.

AUDIT COMMITTEE FINANCIAL EXPERT AND AUDIT COMMITTEE QUALIFICATIONS

The Company’s Board of Directors has determined that each of Ms. Patricia Volker, Chair of the Audit Committee, and Mr. Ken Hartwick are audit committee financial experts within the meaning of paragraph 8(b) of General Instruction B of Form 40-F, and that all three members of the Audit Committee (Ms. Patricia Volker, Mr. Ken Hartwick and Mr. David Neuburger) are independent within the meaning of United States and Canadian securities regulations and applicable stock exchange requirements.

The SEC has provided that the designation of an audit committee financial expert does not make him or her an “expert” for any purpose, impose on him or her any duties, obligations or liability that are greater than the duties, obligations or liability imposed on him or her as a member of the Audit Committee and the Board in the absence of such designation, or affect the duties, obligations or liability of any other member of the Audit Committee or Board.

CODE OF ETHICS

The Company has adopted a code of ethics that applies to the Company’s directors, officers and employees, including the Chief Executive Officer, the Chief Financial Officer, the principal accounting officer or controller, persons performing similar functions and other officers, directors and employees of the Company. A current copy of the code of ethics is on the Company’s website at www.denisonmines.com. In the fiscal year ended December 31, 2025, the Company has not made any amendment to a provision of its code of ethics that applies to any of its Chief Executive Officer, Chief Financial Officer, principal accounting officer or controller or persons performing similar functions that relates to one or more of the items set forth in paragraph (9)(b) of General Instruction B to Form 40-F. In the fiscal year ended December 31, 2025, the Company has not granted a waiver (including an implicit waiver) from a provision of its code of ethics to any of its Chief Executive Officer, Chief Financial Officer, principal accounting officer or controller or persons performing similar functions that relates to one or more of the items set forth in paragraph (9)(b) of General Instruction B to Form 40-F.

Unless and to the extent specifically referred to herein, the information on the Company’s website shall not be deemed to be incorporated by reference in this Annual Report. Except for the code of ethics, and notwithstanding references to the Company’s website or other websites in the AIF or in the documents incorporated by reference herein or attached as exhibits hereto, no information contained on the Company’s website or any other website shall be incorporated by reference in this Annual Report or in the documents incorporated by reference herein or attached as Exhibits hereto.

PRINCIPAL ACCOUNTANT FEES AND SERVICES

KPMG LLP, Toronto, ON, Canada (Auditor Firm ID: 85), acted as the Company’s independent registered public accounting firm for the fiscal year ended December 31, 2025.

See the section “Denison’s Governance – Standing Committees of the Board – Audit Committee” in the AIF, which section is incorporated by reference herein, for the total fees billed to the Company by KPMG LLP during last two fiscal years by category of service (for audit fees, audit-related fees, tax fees and all other fees).

AUDIT COMMITTEE PRE-APPROVAL POLICIES AND PROCEDURES

The Company’s Audit Committee mandate and charter provides that the Audit Committee shall (i) approve, prior to the auditor’s audit, the auditor’s audit plan (including, without limitation, staffing), the scope of the auditor’s review and all related fees, and (ii) pre-approve any non-audit services (including, without limitation, fees therefor) provided to the Company or its subsidiaries by the auditor or any auditor of any such subsidiary and shall consider whether these services are compatible with the auditor’s independence, including, without limitation, the nature and scope of the specific non-audit services to be performed and whether the audit process would require the auditor to review any advice rendered by the auditor in connection with the provision of non-audit services.

The following sets forth the percentage of services described above that were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X:

|

|

2025 |

|

2024 |

|

Audit Related Fees: |

|

100 |

% |

100 |

% |

Tax Fees: |

|

100 |

% |

100 |

% |

All Other Fees: |

|

100 |

% |

100 |

% |

OFF-BALANCE SHEET ARRANGEMENTS

The Company has no off-balance sheet arrangements that have, or are reasonably likely to have, a material effect on the Company’s financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, cash requirements or capital resources.

IDENTIFICATION OF THE AUDIT COMMITTEE

The Company has a separately-designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Exchange Act. The committee members now, and for the financial year ended December 31, 2025, are Ms. Patricia Volker (Chair), Mr. Ken Hartwick and Mr. David Neuburger. For further information on these members, see “Audit Committee Financial Expert” above.

CORPORATE GOVERNANCE PRACTICES

The Company’s common shares are listed on the NYSE American. Section 110 of the NYSE American Company Guide permits the NYSE American to consider the laws, customs and practices of foreign issuers in relaxing certain NYSE American listing criteria, and to grant exemptions from the NYSE American listing criteria based on these considerations. An issuer seeking relief under these provisions is required to provide written certification from independent local counsel that the non-complying practice is not prohibited by home country law. A description of the significant ways in which the Company’s governance practices differ from those followed by domestic companies pursuant to the NYSE American standards is as follows:

Shareholder Meeting Quorum Requirement: The NYSE American minimum quorum requirement for a shareholder meeting is one-third of the shares issued and outstanding and entitled to vote for a meeting of a listed company’s shareholders. The TSX does not specify a quorum requirement for a meeting of a listed company’s shareholders. The Company’s current required quorum at any meeting of shareholders as set forth in the Company’s by-laws is two persons present, each being a shareholder entitled to vote at the meeting or a duly appointed proxyholder for an absent shareholder so entitled, holding or representing in aggregate not less than 10% of the shares of the Company entitled to be voted at the meeting. The Company’s current quorum requirement is not prohibited by, and does not constitute a breach of, the Business Corporations Act (Ontario) (the “OBCA”), applicable Canadian securities laws or the rules and policies of the TSX.

Proxy Solicitation Requirement: The NYSE American requires the solicitation of proxies and delivery of proxy statements for all shareholder meetings of a listed company, and requires that these proxies be solicited pursuant to a proxy statement that conforms to the proxy rules of the U.S. Securities and Exchange Commission. The Company is a foreign private issuer as defined in Rule 3b-4 under the Exchange Act, and the equity securities of the Company are accordingly exempt from the proxy rules set forth in Sections 14(a), 14(b), 14(c) and 14(f) of the Exchange Act. The Company solicits proxies in accordance with the OBCA, applicable Canadian securities laws and the rules and policies of the TSX.

Shareholder Approval Requirements: The NYSE American requires a listed company to obtain the approval of its shareholders for certain types of securities issuances. One is the sale of common shares (or securities convertible into common shares) at a discount to officers or directors. The TSX rules require shareholder approval for the issuance of shares to insiders in private placements where insiders are being issued more than 10% of the presently issued and outstanding shares. The NYSE American also requires shareholder approval of private placements that may result in the issuance of common shares (or securities convertible into common shares) equal to 20% or more of presently outstanding shares for less than a prescribed minimum price based on recent closing prices. There is no such requirement under Ontario law. The TSX rules require shareholder approval for private placements that materially affect control, or where more than 25% of presently issued and outstanding shares will be issued at a discount to market. The Company will seek a waiver from the NYSE American shareholder approval requirement should a dilutive securities issuance trigger such NYSE American shareholder approval requirement in circumstances where such securities issuance does not trigger a shareholder approval requirement under the rules of the TSX.

The foregoing are consistent with the laws, customs and practices in Canada.

In addition, the Company may from time-to-time seek relief from the NYSE American corporate governance requirements on specific transactions under Section 110 of the NYSE American Company Guide by providing written certification from independent local counsel that the non-complying practice is not prohibited by its home country law, in which case, the Company shall make the disclosure of such transactions available on its website at www.denisonmines.com. Information contained on, or accessible through, our website is not part of this Annual Report on Form 40-F.

MINE SAFETY DISCLOSURE

Not applicable.

UNDERTAKING AND CONSENT TO SERVICE OF PROCESS

A.Undertaking

The Company undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an Annual Report on Form 40-F arises; or transactions in said securities.

B.Consent to Service of Process

The Company has previously filed with the SEC a Form F-X in connection with its common shares. Any change to the name or address of the Company’s agent for service shall be communicated promptly to the SEC by amendment to the Form F-X referencing the file number of the Company.

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Company certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this Annual Report on Form 40-F to be signed on its behalf by the undersigned, thereto duly authorized.

Registrant: DENISON MINES CORP. | ||

| ||

By: |

/s/ David D. Cates |

|

|

|

|

Title: |

President and Chief Executive Officer |

|

|

|

|

Date: |

March 30, 2026 |

|

|

|

|

EXHIBIT INDEX

97.1 |

|

|

|

|

|

99.1 |

|

Annual Information Form for the Year Ended December 31, 2025 |

|

|

|

99.2 |

|

|

|

|

|

99.3 |

|

|

|

|

|

99.4 |

|

|

|

|

|

99.5 |

|

|

|

|

|

99.6 |

|

|

|

|

|

99.7 |

|

|

|

||

99.8 |

|

|

|

|

|

99.9 |

|

|

|

|

|

99.10 |

|

|

|

|

|

99.11 |

|

|

|

|

|

99.12 |

|

|

|

|

|

99.13 |

|

|

|

|

|

99.14 |

|

|

|

|

|

99.15 |

|

|

|

|

|

99.16 |

|

|

|

|

|

99.17 |

|

|

|

|

|

99.18 |

|

|

|

|

|

99.19 |

|

|

|

|

|

99.20 |

|

|

|

|

|

99.21 |

|

|

|

|

|

99.22 |

|

|

|

|

|

99.23 |

|

|

|

|

|

99.24 |

|

|

|

|

|

99.25 |

|

|

|

|

|

99.26 |

|

|

|

|

|

99.27 |

||

|

|

|

99.28 |

|

|

|

|

|

101 |

|

Interactive Data File (formatted as Inline XBRL) |

|

|

|

104 |

|

Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101) |

Exhibit 99.1

Denison Mines Corp.

2025 Annual Information Form

March 30, 2026

About this Annual Information Form

This annual information form (“AIF”) is dated March 30, 2026. Information in this AIF is stated as at December 31, 2025 unless specified otherwise.

In this AIF, references to the “Company” or “Denison” refer to Denison Mines Corp., its subsidiaries and affiliates, or any one of them, as applicable.

This AIF has been prepared in accordance with Canadian securities laws and contains information regarding Denison’s history, business, mineral reserves and resources, the regulatory environment in which Denison does business, the risks that Denison faces and other important information for Denison’s shareholders.

Financial Information

Unless otherwise specified, all dollar amounts referred to in this AIF are stated in Canadian dollars (“CAD”). References to “US$” or “USD” mean United States dollars.

Financial information is generally derived from consolidated financial statements that have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board.

1 |

|

7 |

|

10 |

|

16 |

|

20 |

|

25 |

|

27 |

|

54 |

|

Athabasca Exploration: Sampling, Analysis and Data Verification |

58 |

63 |

|

65 |

|

70 |

|

75 |

|

95 |

|

97 |

|

103 |

|

104 |

|

106 |

|

107 |

|

A-1 |

|

B-1 |

|

2025 ANNUAL INFORMATION FORM 1 |

Caution about Forward-Looking Information

Certain information contained in this AIF and the documents incorporated by reference concerning the business, operations and financial performance and condition of Denison constitutes forward-looking statements and forward-looking information within the meaning of the United States Private Securities Litigation Reform Act of 1995 and similar Canadian legislation (collectively, “forward-looking information”).

Generally, the use of words and phrases like “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes”, or the negatives and/or variations of such words and phrases, or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will” “be taken”, “occur”, “be achieved” or “has the potential to” and similar expressions are intended to identify forward-looking information.

Forward-looking information involves known and unknown risks, uncertainties, material assumptions and other factors that may cause actual results or events to differ materially from those expressed or implied by such forward-looking information. Denison believes that the expectations and assumptions reflected in this forward-looking information are reasonable, but no assurance can be given that these expectations will prove to be correct. Forward-looking information should not be unduly relied upon. This information speaks only as of the date of this AIF, and Denison will not necessarily update this information, unless required by securities laws.

Third Party Information

Certain of the forward-looking information and other information contained herein concerning the uranium industry and mining industry generally and the general expectations of the Company concerning the uranium industry and mining industry generally are based on estimates prepared by third-parties or by the Company using data from publicly available governmental sources, market research, industry analysis, and on assumptions based on data and knowledge of the uranium industry and mining industry generally, which the Company believes to be reasonable. However, such data is inherently imprecise, is subject to interpretation and cannot be verified with complete certainty. Denison has not independently verified any third-party information. While Denison is not aware of any misstatement regarding any industry or government data presented herein, the mining industry overall involves risks and uncertainties that are subject to change based on various factors.

|

2025 ANNUAL INFORMATION FORM 2 |

Examples of Forward-Looking Information

This AIF contains forward-looking information in a number of places, including but not limited to statements pertaining to Denison’s:

|

●

operational and business outlook, including administrative, production, construction, development, evaluation, and exploration plans and objectives

|

|

●

expectations regarding additions to its mineral reserves and mineral resources through acquisitions and exploration

|

|

●

expectations regarding capital and uses of capital, including plans for capital and other expenditures

|

|

●

results of its exploration programs

|

|

●

expectations for Phoenix construction, including readiness for construction, timing plans and budgets

|

|

●

expectations regarding the process for and receipt and maintenance of regulatory approvals, permits and licences

|

|

●

expectations for Phoenix production

|

|

●

expectations regarding future uranium prices and/or applicable foreign exchange rates

|

|

●

results of the Phoenix FS (including the 2026 Capex Update) and Environmental Assessment for the Phoenix mine

|

|

●

expectations about 2026 and future market prices, production costs, nuclear energy and global uranium supply and demand – including potential new sources of uranium production

|

|

●

results of the Gryphon PFS Update

|

|

●

expectations regarding ongoing joint arrangements, Denison’s share of same, and the operational and business outlook for projects Denison does not operate

|

|

●

outlook for the potential and competitiveness of Denison’s deposits relative to global uranium deposits and/or mines

|

|

●

expectations regarding toll milling revenues generated by McClean Lake mill, and the relationships with its contractual partners with respect thereto

|

|

●

estimates of the Company’s mineral reserves and mineral resources

|

|

●

future royalty and tax payments and rates

|

|

●

other technical and economic assessments, and related plans and objectives, for its properties

|

|

●

expectations regarding possible impacts of litigation and regulatory actions

|

Statements relating to “mineral resources” are deemed to be forward-looking information, as they involve the implied assessment, based on certain estimates and assumptions that the mineral resources described can be profitably produced in the future. Capitalized terms bear the meanings as defined elsewhere in this AIF.

|

2025 ANNUAL INFORMATION FORM 3 |

Material Risks

Denison’s actual results could differ materially from those anticipated or indicated by the forward-looking information contained in this AIF. Management has identified the following risk factors which could have a material impact on the Company or the trading price of its common shares (“Shares”):

|

●

the risk of inadequate funding for operations, given capital-intensive nature of the industry

|

|

●

devaluation of any physical uranium held by the Company, and risk of losses, due to fluctuations in the price of uranium and/or foreign exchange rates

|

|

●

history of, and expectations for continued, negative cash flow

|

|

●

the risk of failure to realize benefits from transactions

|

|

●

global financial conditions, including market volatility and global inflation, and related operational risks

|

|

●

the risk of inability to exploit, expand or replace mineral reserves and resources

|

|

●

the speculative nature of exploration and development projects, including risks related to technical or economic feasibility of projects and regulatory approvals

|

|

●

competition for properties

|

|

●

the risks of, and market impacts on, developing mineral properties

|

|

●

risk of challenges to property title and/or contractual interests in Denison’s properties

|

|

●

risks associated with the selection of novel mining methods

|

|

●

the risk of failure by Denison to meet its obligations to its creditors

|

|

●

the impact of uranium price volatility on the valuation of Denison’s assets, including mineral reserves and resources, and operational outlook

|

|

●

change of control restrictions

|

|

●

dependence on licenses and permits

|

|

●

uncertainty as to reclamation and decommissioning liabilities and timing

|

|

●

extensive regulatory and policy oversight and related risks

|

|

●

potential for technological innovation rendering products and services obsolete

|

|

●

uncertainty regarding engagement with Indigenous Nations of Canada (First Nations and Métis)

|

|

●

liabilities inherent in mining operations and the adequacy of insurance coverage

|

|

●

reliance on third parties

|

|

●

containment management of waste materials

|

|

●

challenges in maintaining qualified and experienced employees upon which the Company’s operations will depend

|

|

●

the ability of Denison to ensure compliance with anti-bribery and anti-corruption laws

|

|

●

risk of disagreements or disputes with Denison’s joint venture counterparties that could disrupt operations

|

|

●

the uncertainty regarding risks posed by climate change

|

|

●

risk that public health emergencies could impact business and operations plans

|

|

●

the reliance of the Company on its information systems, including the Company’s use of AI, and the risk of cyber-attacks on those systems

|

|

●

compliance costs and risks of non-compliance with environment, health, safety and other regulatory regimes

|

|

●

maintenance of infrastructure and equipment

|

|

2025 ANNUAL INFORMATION FORM 4 |

|

●

health and safety hazards

|

|

●

potential conflicts of interest for the Company’s directors who are engaged in similar businesses

|

|

●

the imprecision of mineral reserve and resource estimates

|

|

●

limitations of disclosure and internal controls

|

|

●

global demand fluctuations and international trade policies and restrictions

|

|

●

volatility in the market price of the Shares

|

|

●

uncertainty regarding public acceptance of nuclear energy and competition from other energy sources

|

|

●

the risk of dilution from future equity financings

|

|

●

reliance on other operators of certain Company properties

|

|

●

the potential influence of Denison’s largest shareholder, Korea Electric Power Corporation (“KEPCO”) and its subsidiary, Korea Hydro & Nuclear Power (“KHNP”)

|

|

●

reliance on uranium storage facilities

|

|

●

Risks for United States investors

|

The risk factors listed above are discussed in more detail later in this AIF (see “Risk Factors”). The risk factors discussed in this AIF are not, and should not be construed as being, exhaustive or the only risks that affect the Company. Other risks and uncertainties that the Company does not presently consider to be material, or of which the Company is not presently aware, may become important factors that affect the Company’s future financial condition and results of operations.

Material Assumptions

The forward-looking information in this AIF and the documents incorporated by reference are based on material assumptions made by management of the Company, including the following, which may prove to be incorrect:

| ● | the budgets for 2026 and beyond, including plans and estimated costs for exploration, evaluation, development, construction, production and other factors |

| ● | Denison’s ability to execute its business plans for 2026 and beyond and realize on the expected results from mining, development, and exploration activities |

| ● | Denison’s expectations regarding the plans and budgets, and ability to execute, with respect to its joint venture interests, particularly for which it is not the operator |

| ● | the ability of the Company to, and the means by which it can, raise additional capital to advance exploration, evaluation, development, and mining objectives |

| ● | Denison’s ability to obtain all necessary regulatory approvals, permits and licences for its planned activities under governmental and other applicable regulatory regimes |

| ● | expectations regarding the demand for, and supply of, uranium, the outlook for long-term contracting, changes in regulations, public perception of nuclear power, and the construction of new and relicensing of existing nuclear power plants |

| ● | expectations regarding spot and long-term prices and realized prices for uranium |

| ● | expectations regarding Denison’s holdings of physical uranium and future sales of uranium production, including commercial strategies |

| ● | expectations regarding tax rates, currency exchange rates and interest rates |

|

2025 ANNUAL INFORMATION FORM 5 |

| ● | Denison’s decommissioning and reclamation obligations and the status and ongoing maintenance of agreements with third parties with respect thereto |

| ● | mineral reserve and resource estimates, and the assumptions upon which they are based |

| ● | Denison’s, and its contractors’, ability to comply with current and future environmental, safety and other regulatory requirements and to obtain and maintain required regulatory approvals |

| ● | Denison’s operations are not significantly disrupted as a result of social or political activism, natural disasters, public health emergencies, governmental or political actions, litigation or arbitration proceedings, equipment or infrastructure failure, labour shortages, transportation disruptions or accidents, or other development or exploration risks |

Cautionary Notes to U.S. Investors Concerning Resource and Reserve Estimates

As a foreign private issuer reporting under the multijurisdictional disclosure system adopted by the United States, the Company has prepared this AIF in accordance with Canadian securities laws and standards for reporting of mineral resource estimates, which differ in some respects from United States standards. In particular, and without limiting the generality of the foregoing, the terms “measured mineral resources,” “indicated mineral resources,” “inferred mineral resources,” and “mineral resources” used or referenced in this AIF are Canadian mineral disclosure terms as defined in accordance with National Instrument 43-101 — Standards of Disclosure for Mineral Projects (“NI 43-101”) under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum Standards for Mineral Resources and Mineral Reserves, Definitions and Guidelines, May 2014 (the “CIM Standards”). These standards differ significantly from the mineral property disclosure requirements of the U.S. Securities and Exchange Commission (the “SEC”) in Regulation S-K Subpart 1300 (the “SEC Modernization Rules”) under the U.S. Securities Exchange Act of 1934, as amended (the “U.S. Exchange Act”).

Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as “proven mineral reserves”, “probable mineral reserves”, “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would be the same had the Company prepared the mineral reserve or mineral resource estimates under the standards adopted under the SEC Modernization Rules. For the above reasons, information contained in the AIF and other documents incorporated by reference herein containing descriptions of mineral deposits may not be comparable to similar information made public by U.S. companies subject to the SEC Modernization Rules. Additionally, investors are cautioned that “inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic feasibility. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or other economic studies, except in limited circumstances. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. The term “resource” does not equate to the term “reserves”. Investors should not assume that all or any part of measured or indicated mineral resources will ever be converted into mineral reserves. Investors are also cautioned not to assume that all or any part of an inferred mineral resource exists or is economically mineable.

|

2025 ANNUAL INFORMATION FORM 6 |

Denison Mines Corp. is engaged in uranium exploration, development and mining. The registered and head office of Denison is located at 1100 – 40 University Avenue, Toronto, Ontario, M5J 1T1, Canada. Denison’s website address is www.denisonmines.com.

The Shares are listed on the Toronto Stock Exchange (“TSX”) under the symbol “DML” and on the NYSE American under the symbol “DNN.”

Computershare Investor Services Inc. acts as the registrar and transfer agent for the Shares. The address for Computershare Investor Services Inc. is 100 University Avenue, 8th Floor, Toronto, ON, M5J 2Y1, Canada, and the telephone number is 1-800-564-6253.

Denison is a reporting issuer in each of the Canadian provinces and territories. The Shares are also registered under the U.S. Exchange Act, and Denison files periodic reports with the SEC.

Acknowledgement

Denison respectfully acknowledges that its business operates in Canada on lands that are in the traditional territory of Indigenous peoples. Denison’s activities encompass the entire mining life cycle, from early-stage exploration to advanced project evaluation, construction, operation, closure and restoration – with the potential for activities to span many decades. As such, Denison is committed to collaborating with Indigenous peoples and communities to build long-term, respectful, trusting, and mutually beneficial relationships and aspires to avoid any adverse impacts of Denison’s activities and operations.

Denison has adopted an Indigenous Peoples Policy (“IPP”), which reflects the Company’s recognition of the important role of Canadian business in the process of reconciliation with Indigenous peoples in Canada and outlines the Company’s commitment to take action towards advancing reconciliation. See “Environmental, Health, Safety and Sustainability Matters – Indigenous Peoples Policy and Reconciliation Action Plan” in this AIF. A copy of the Indigenous Peoples Policy is available on Denison’s website, in Déne, Cree, English and French languages.

Denison’s head office is located in the traditional territory of many nations, including the Mississaugas of the Credit, the Anishnabeg, the Chippewa, the Haudenosaunee and the Wendat peoples, and is now home to many diverse First Nations, Inuit and Métis peoples. Denison also acknowledges that Toronto is covered by Treaty 13 with the Mississaugas of the Credit.

Denison’s mining and mineral exploration operations in Saskatchewan, including its office in Saskatoon and various project interests in northern Saskatchewan, are located in regions covered by Treaty 6, Treaty 8 and Treaty 10, which encompass the traditional lands of the Cree, Dakota, Déne, Lakota, Nakota, Saulteaux, within the homeland of the Métis and within Nuhenéné.

Denison’s flagship Wheeler River uranium project, in particular, is located in northern Saskatchewan within the boundaries of Treaty 10, in the traditional territory of English River First Nation, in the homeland of the Métis and within Nuhenéné.

Denison’s legacy mines operations in the Elliot Lake region of northern Ontario are located within the boundaries of the Robinson Huron Treaty of 1850, signatories to which include the Serpent River First Nation.

|

2025 ANNUAL INFORMATION FORM 7 |

Denison’s Team

At the end of 2025, Denison had a total of 95 active employees, all of whom were employed in Canada. None of the Company’s employees are unionized.

Denison’s Structure

Denison conducts its business through a number of subsidiaries and joint arrangements. The following is a diagram depicting the corporate structure of Denison, its active subsidiaries and corporate and partnership joint arrangements, including the name, jurisdiction of incorporation and proportion of ownership interest in each, as at December 31, 2025.

The Waterbury Lake Uranium Limited Partnership (“WLULP”) is held by Denison (70.55%) and Korea Waterbury Uranium Limited Partnership (“KWULP”) (29.43%) as limited partners and Waterbury Lake Uranium Corporation (“WLUC”) (0.02%), as general partner.

JCU (Canada) Exploration Company, Ltd. (“JCU”) is owned by Denison (50%) and UEX Corporation (“UEX”, 50%). UEX, a wholly-owned subsidiary of Uranium Energy Corp., is manager of JCU, and JCU’s operations are managed in accordance with a shareholders agreement between Denison, UEX and JCU.

The Formation of Denison Mines Corp.

The Denison name has a long history in the Canadian uranium mining industry. Based on company archives, Denison’s involvement in the uranium mining industry dates back to 1954, when a predecessor to modern Denison acquired uranium claims in the Elliot Lake region.

Modern Denison was established by articles of amalgamation as International Uranium Corporation (“IUC”) on May 9, 1997 pursuant to the Business Corporations Act (Ontario). On December 1, 2006, IUC completed a plan of arrangement (the “IUC Arrangement”) with Denison Mines Inc. (“DMI”). Pursuant to the IUC Arrangement, all of the issued and outstanding shares of DMI were acquired in exchange for IUC’s shares. Effective December 1, 2006, IUC’s articles were amended to change its name to “Denison Mines Corp.” Denison completed a plan of arrangement with Energy Fuels Inc. in 2012 and

|

2025 ANNUAL INFORMATION FORM 8 |

filed articles of amalgamation on January 1, 2014, July 1, 2014 and July 3, 2014 in connection with Denison’s acquisitions of JNR Resources Inc. and Fission Energy Corp.

Denison Overview

Uranium Mining, Development, and Exploration

Denison’s uranium property interests are held directly by the Company and/or indirectly through DMI, Denison Waterbury Corp. and Denison AB Holdings Corp.

|

Focused in the Athabasca Basin Region of Saskatchewan Denison’s Flagship Assets: ●

An effective 95% interest in, and operator of, the Wheeler River Uranium project (“Wheeler” or “Wheeler River”), which is host to the high-grade Phoenix and Gryphon uranium deposits – together representing the largest undeveloped uranium project in the infrastructure rich eastern Athabasca Basin.

Denison’s Extensive Portfolio of Other Uranium Properties: ●

A 70.55% interest in, and operator of, the Waterbury Lake project, which includes the Tthe Heldeth Túé (“THT”, formerly J Zone) and Huskie deposits.

●

A 22.50% interest in the McClean Lake uranium processing facility, the McClean North uranium mine, and unmined uranium deposits, through its interest in the McClean Lake Joint Venture (“MLJV”) operated by Orano Canada Inc. (“Orano Canada”).

●

A 25.17% interest in the Midwest uranium project (“Midwest”), which is host to the Midwest Main and Midwest A deposits, through its interest in the Midwest Joint Venture (“MWJV”) operated by Orano Canada.

●

Through its 50% ownership of JCU, interests in various uranium project joint ventures in Canada, including the Millennium project (JCU 30.099%), the Kiggavik project (JCU 33.8118%) and Christie Lake (JCU 34.4508%).

●

An extensive portfolio of exploration properties located in the Athabasca Basin.

|

Toll Milling

Denison is a party to a toll-milling arrangement through its 22.50% interest in the MLJV, whereby ore is processed for the Cigar Lake Joint Venture (“CLJV”) at the McClean Lake processing facility (the “Cigar Toll Milling”). In February 2017, Denison completed a transaction (the “Ecora Transaction”) with Ecora Resources PLC (“Ecora”) and its wholly owned subsidiary Centaurus Royalties Ltd. to raise gross proceeds to Denison of $43,500,000. The Ecora Transaction monetized Denison’s future share of the Cigar Toll Milling, providing Denison with the financial flexibility to advance its interests in the Athabasca Basin, including the Wheeler River project. See “Denison’s Operations – Cigar Lake Toll Milling – Ecora Transaction”.

|

2025 ANNUAL INFORMATION FORM 9 |

Developments Over the Last Three Years

Developments in Q1 2026

In January, based on the substantial completion of project engineering and execution of significant procurement activities since the effective date of the 2023 feasibility study (the “Phoenix FS”) for the Phoenix In-Situ Recovery (“ISR”) uranium mine (“Phoenix” or the “Project”) at Wheeler, an updated initial capital cost estimate for the Project was released. Accounting for adjustments due to inflation, cost increases, and project refinements, Denison now estimates total initial capital for the Project to be $700 million at a Class 2 equivalent level of precision (the “2026 Capex Update”), including pre-final investment decision (“FID”) spend of approximately $100 million and post-FID spend of approximately $600 million.

Also in January, the Company announced that grid power from Saskatchewan Power Corporation (“SaskPower”) had become available at Phoenix following the installation of a new 138kV transmission line, representing a significant step in de-risking the execution of the Project.

In February, the Company announced the decision of the administrative tribunal (the “Commission”) of the Canadian Nuclear Safety Commission (“CNSC”) to approve the Environmental Assessment (“EA”) and issue the Licence to Prepare a Site & Construct (the “Construction Licence”) for Phoenix, which is the first uranium mine in Canada to receive federal approval for construction in over 20 years. With the EA having previously been approved by the Province of Saskatchewan, and other provincial approvals necessary to commence construction already received, federal approval of the EA and the issuance of the Construction Licence represented the final regulatory approvals required to commence construction of Phoenix.

And in February, Denison announced approval by its Board of Directors (the “Board”) to proceed with the construction of Phoenix. With construction anticipated to take approximately two years, Phoenix remains on track for first production by mid-2028, and Denison is positioned as one of the few uranium suppliers globally that is expected to be able to provide a sizeable new source of uranium production before the end of the decade.

Also in February, Denison announced that, following a competitive tender process, it awarded Wood Canada Limited (“Wood”), a global leader in consulting and engineering, with the construction management contract (the “CM Contract”) to oversee the building of the Phoenix mine. The CM Contract currently contemplates procurement and construction management scopes, whereby Wood is responsible for (i) construction management of the full processing plant scope, (ii) installation of certain site infrastructure, and (iii) integrated project controls, ongoing procurement support, on-site safety oversight, as well as maintaining reporting and performance management standards. Such services will be provided by Wood in close consultation with Denison, with members of Wood’s and Denison’s teams holding complementary roles in an integrated project management team (“IPT”).

In March, the IPT was formed and initial crews mobilized to Phoenix to commence site preparation and construction activities.

Wheeler River

2023…

In August, Denison filed the Wheeler Report (defined below), summarizing the results of (i) the Phoenix FS completed for ISR mining of Phoenix; and (ii) a cost update to the Pre-Feasibility Study (“PFS”) completed in 2018 for conventional underground mining of the basement-hosted Gryphon uranium deposit (“Gryphon PFS Update”). The results of the respective studies illustrated that both deposits have the potential to be competitive with the lowest cost uranium mining operations in the world. See “Wheeler River” for more details.

|

2025 ANNUAL INFORMATION FORM 10 |

In September, Denison announced the signing of a Shared Prosperity Agreement (“SPA”) with English River First Nation (“ERFN”) supporting the development and operation of the Wheeler River project. The SPA received support from a substantial majority of ERFN members who participated in a ratification vote on its key terms. The signing of the SPA follows years of active engagement, including a four-month-long ERFN-led community consultation process ahead of the ratification vote, and represents a significant milestone in the history of both Denison’s relationship with ERFN and the Wheeler River project.

In November, the Company announced the successful completion of the recovered solution management phase of the ISR Feasibility Field Test (“FFT”). The solution recovered during the FFT was stored on site and this final phase of the FFT involved the treatment of the recovered solution via an on-site purpose-built treatment plant. Following treatment, a uranium precipitate product and a treated effluent were produced. The mineralized precipitates were recovered from the process with over 99.99% efficiency. The treated effluent was tested to ensure compliance with permit conditions before being injected into a designated subsurface area.

2024…

In January, Denison awarded Wood a contract for approximately $16 million for the completion of detailed design engineering for Phoenix. The work commenced in the first quarter of 2024, with substantial completion achieved in 2025. Throughout 2024, the Company continued to focus its efforts on the advancement of Phoenix towards FID, in support of its objective to achieve first production by 2028, including the advancement of Phoenix detailed design engineering activities. Total engineering completion at end of 2024 was approximately 65%, supported by finalization of process design, piping and instrumentation diagrams, hazard and operability studies, as well as the selection of major process equipment and electrical distribution infrastructure.

In February, the Company announced its acquisition of fixed and mobile MaxPERF Tool Systems from Penetrators Canada Inc. (“Penetrators”). The MaxPERF Tool Systems have been successfully deployed several times as a method of permeability enhancement in ISR field studies conducted on the Company’s potential ISR mining projects, including at the Phoenix deposit. Penetrators has also agreed to work exclusively with Denison for a 10-year period with respect to the use of the MaxPERF Tool Systems for uranium mining applications, and related services, in Saskatchewan. In March, Denison signed a Sustainable Communities Investment Agreement (the “SCIA”) with the municipalities of the Northern Village of Beauval, the Northern Village of Île-à-la Crosse, the Northern Hamlet of Jans Bay, and the Northern Hamlet of Cole Bay (the “SCIA Communities”). The SCIA reflects a common goal of facilitating qualified businesses and workers in benefitting from opportunities associated with the development of the Wheeler River project. The SCIA establishes commitments for funding to support community development initiatives, focused on contributing to the current and future economic prosperity and sustainability of the Communities by promoting economic development and investments in capital projects, job creation and training, housing, education, and other initiatives. In consideration for such contributions to the Communities’ initiatives, the Communities have provided their consent and support for the Wheeler River project and have committed, amongst other things, to support all regulatory approvals issued for the Wheeler River project related to exploration, evaluation, development, operation, reclamation, and closure activities.

In July, Denison announced the signing of a Mutual Benefits Agreement (“MBA”) with Kineepik Métis Local #9 (“KML”) and a Community Benefit Agreement (“CBA”) with the northern Village of Pinehouse Lake (“Pinehouse”), in support of the development and operation of Wheeler River. The MBA acknowledges that Wheeler River is located within KML’s Land and Occupancy Area in northern Saskatchewan and provides KML’s consent and support to advance the project. Additionally, the MBA recognizes that the development and operation of Wheeler River can support KML in advancing its social and economic development aspirations, while mitigating the impacts on the local environment and KML members. The MBA provides KML and its Métis members an important role in environmental monitoring and commits to the sharing of benefits from the successful operation of Wheeler River – including benefits from community investment, business opportunities, employment and training opportunities, and financial compensation. The CBA acknowledges that Pinehouse is the closest residential community to Wheeler River by road, which relies on much of the same regional infrastructure that Denison will rely on as it advances the project. Pinehouse has provided its consent and support for Wheeler River, while Denison, on behalf of the Wheeler River Joint Venture (“WRJV”), is committed to help Pinehouse develop its own capacity to take advantage of economic and other development opportunities in connection with the advancement and operation of the project.

|

2025 ANNUAL INFORMATION FORM 11 |

Multiple key regulatory milestones were achieved in late 2024, including (i) filing of the final Environmental Impact Statement (“EIS”) with the Saskatchewan Ministry of Environment (“SKMOE”) in October; (ii) completion of a provincial public and Indigenous review period on the EIS in November and December 2024; (iii) completion of the technical review phase of the federal EA approval process and filing of the final EIS with CNSC in November, (iv) the CNSC’s determination of the sufficiency of Denison’s application for a Construction Licence in November, and (v) acceptance by the CNSC of the EIS in December. The next steps for approval of the EA and Phoenix permitting were: (1) ministerial approval of the EA from the Government of Saskatchewan and issuance of applicable provincial permits; and (2) following a two-part public hearing process, CNSC approval of the EA and issuance of the Construction Licence. Such steps were achieved in 2025 and early 2026. For further details, see “Wheeler River” and “Environmental, Health, Safety and Sustainability Matters” below.

In October, the WRJV Management Committee approved the findings and recommendations of the Phoenix FS, which became an Approved Development Program (“ADP”) under the WRJV Agreement, providing the WRJV’s approval for development and construction of the project in accordance with the Phoenix FS.

At the October meeting of the WRJV Management Committee, JCU abstained from voting on the ADP. In accordance with the terms of the WRJV Agreement, non-support of the ADP by a participant means that such participant is no longer liable for its cost share of WRJV expenditures. As a result of JCU’s non-support through abstention, Denison has funded, and expects to continue to fund, 100% of the project expenditures from October 2024. The WRJV Agreement further requires that a participant who does not support an ADP must sell or transfer their interest. UEX, as operator of JCU, has notified Denison that it does not agree that JCU’s abstention from the ADP vote should be taken as non-support for the ADP and the sale or transfer of JCU’s participating interest in the WRJV has not yet occurred. See “Legal and Regulatory Proceedings” for further information.

2025…

In July, Denison received SKMOE Ministerial approval of the EA under The Environmental Assessment Act of Saskatchewan to proceed with the development of Phoenix. With that, Denison submitted the Provincial application to Construct a Pollutant Control Facility. A Pollutant Control Facility Permit is required for the construction of the mining and processing components of the facility and is anticipated to be the primary provincial permit required for construction.

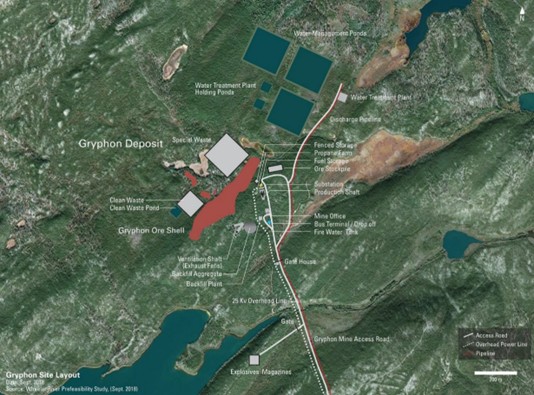

And in July, the Company announced the discovery of additional high-grade mineralization approximately 40 metres outside of the previously estimated mineralized domain associated with the D1 lens of the Gryphon deposit at Wheeler River. A total of ~12,500 metres of diamond drilling was completed in seventeen drill holes and multiple off cuts during the 2025 delineation program at Gryphon. Overall, the delineation program confirmed the current geological interpretation of the deposit and supported the grade-thickness assumptions in the resource block model. The delineation results demonstrate that Gryphon is an excellent high-grade basement-hosted uranium deposit that justifies further project development evaluation and de-risking. Gryphon is situated approximately 3 km northwest of the Phoenix ISR site

In August, the Company acknowledged an application for judicial review filed in the Court of King’s Bench for Saskatchewan by the Peter Ballantyne Cree Nation against the Government of Saskatchewan and the Company, asserting that the Province of Saskatchewan did not adequately exercise its duty to consult prior to its approval of the EA. See “Legal and Regulatory Proceedings” for further information.

In October and December, Denison participated in a two-part public hearing (“Hearing”) of the Commission, considering Denison’s application for the approval of the EA and the Construction Licence. Following the multi-year federal review of the EA and related processes, CNSC staff recommended in their submissions that the Commission grant the EA approval and the Construction Licence. The Hearing was the final step in the federal review process.

In December, the Company announced execution of an Impact Benefit Agreement (“IBA”) with the Métis Nation–Saskatchewan (“MN–S”), 13 individual MN–S Locals, MN-S Northern Region 1 (“MN–S NR-1”), and MN–S Northern Region 3 (“MN–S NR-3”) (collectively, the “Métis Parties”). The IBA confirms the Métis Parties’ consent to and support for the development and operation of Wheeler River. In addition, the parties have also entered into an Exploration Agreement covering Denison’s exploration and evaluation activities.

|

2025 ANNUAL INFORMATION FORM 12 |

And in December, the Company and the Ya’thi Néné Land and Resource Office (“YNLR”) announced the signing of the Nuhenéné Benefit Agreement, which is a regional mutual benefits agreement between Denison, YNLR, and each of the Hatchet Lake Denesułiné First Nation, Black Lake Denesułiné First Nation, Fond du Lac Denesułiné First Nation, the Northern Hamlet of Stony Rapids, the Northern Settlement of Uranium City, the Northern Settlement of Wollaston Lake, the Northern Settlement of Camsell Portage (collectively, the “Athabasca Communities”). The Agreement provides the Athabasca Communities’ consent to and support for the development and operation of Wheeler River, as well as Denison’s Waterbury Lake, Midwest, and McClean Lake projects.

Significant regulatory, engineering, and construction planning progress was made throughout 2025, positioning Phoenix in a construction-ready state and confirming an expected 2-year construction timeline. Approximately 87% of total engineering was completed at the end of 2025 and 92% of primary engineering deliverables were issued for construction.

Other Properties

2023…

In April, Denison announced the completion of an internal conceptual mining study examining the potential application of the ISR mining method at the Midwest project. The concept study was prepared by Denison in 2022 and formally issued to the MWJV in early 2023. Based on the positive results of the concept study, the MWJV approved the completion of additional ISR-related work for Midwest in 2023 and 2024.

In November, the Company announced the completion of an inaugural ISR field test program at THT on the Waterbury Lake property. The program included (i) the installation of an eight well ISR test pattern designed to collect an initial database of hydrogeological data, (ii) testing of a permeability enhancement technique, (iii) the completion of hydrogeologic test work, and (iv) the execution of an ion tracer test which established a 10 hour breakthrough time between the injection and extraction wells, while also demonstrating hydraulic control of the injected solution. Overall, the program successfully achieved each of its planned objectives.

2024…

In January, Denison and Orano Canada announced that the MLJV approved a restart of uranium mining operations using the joint venture’s patented Surface Access Borehole Resource Extraction (“SABRE”) mining method. Activities in 2024 focused on preparations necessary to ready the existing SABRE mining site and equipment for continuous commercial operations, as well as the installation of pilot holes for the first mining cavities planned for excavation. See “Denison Operations-SABRE Mining Program” for further details.

And in January, Denison entered into an agreement (the “KLP Agreement”) with Grounded Lithium Corp. (“Grounded Lithium”) with respect to the Kindersley Lithium Project (“KLP”) in Saskatchewan. The KLP Agreement includes a series of earn-in options, with each earn-in option comprised of a cash payment to Grounded Lithium as well as project expenditures to advance KLP. The investment in KLP was seen as an opportunity for Denison to leverage its technical expertise to potentially unlock greater value for the project. Should Denison complete all three earn-in options, it will have made cumulative cash payments to Grounded Lithium of $3.2 million and have funded $12 million in project expenditures to earn a 75% working interest in the KLP. Upon funding the total amounts of each earn-in option phase, Denison has the right to either exercise the earn-in option and acquire the working interest associated with that phase or move on to the ensuing option phase. The KLP Agreement terminates on the earliest of: (i) Denison electing to acquire its working interest and convert to a formal joint venture or to terminate, (ii) June 30, 2028, or (iii) a date as otherwise agreed between the parties.

In June, Denison and Orano Canada announced the completion of an ISR field test program at Midwest. The program involved drilling ten small diameter boreholes within the Midwest Main deposit, primarily undertaken to evaluate site-specific conditions for ISR mining. A series of tests were successfully performed on each borehole, creating an extensive database of geological, hydrogeological, geotechnical, and metallurgical data and validating certain key assumptions in the previously completed concept study evaluating the potential use of ISR mining at Midwest.

|

2025 ANNUAL INFORMATION FORM 13 |

In September, Denison executed an option agreement with Foremost Clean Energy Ltd. (“Foremost”), which grants Foremost a multi-phase option to acquire up to 70% of Denison’s interest in 10 non-core uranium exploration properties (the “Foremost Transaction”). Pursuant to the Foremost Transaction, Foremost would acquire such total interests upon completion of a combination of direct payments to Denison and funding of exploration expenditures with an aggregate value of up to approximately $30 million. In October 2024, Foremost completed the conditions for the first tranche of the option, pursuant to which Denison received an upfront payment in Foremost common shares. If Foremost completes the remaining two phases of the Foremost Transaction, Denison will receive further cash and/or common share milestone payments of $4.5 million and Foremost will fund $20 million in project exploration expenditures.

2025…

In January, pursuant to an acquisition agreement with Cosa Resources Corp. (“Cosa”), Cosa acquired a 70% interest in three of Denison’s properties in the eastern portion of the Athabasca Basin region in northern Saskatchewan and formed three uranium exploration joint ventures, in exchange for approximately 14.2 million Cosa common shares, $2.25 million in deferred equity consideration, and a commitment to spend $6.5 million in exploration expenditures on the properties (the “Cosa Transaction”).

In July, the MLJV announced the successful start of SABRE uranium mining operations at the McClean North deposit. In 2025, on a 100% basis, 4,392 tonnes of high-grade ore was extracted (Denison’s share: 988 tonnes) with 648,558 pounds of U3O8 in finished product produced at the McClean Lake mill (Denison’s share: 145,926 pounds of U3O8) with an average operating cash cost of approximately $36 per pound U3O8 (approximately US$26 per pound U3O8).

And in July, Denison and Orano Canada announced that several significant new intercepts of shallow high-grade uranium mineralization were encountered at the McClean South zone during a 6,400-metre exploration drilling program completed during the first half of 2025.

In August, the Company reported the results of the Preliminary Economic Assessment (“PEA”) Denison completed for the MWJV assessing ISR mining of the Midwest Main deposit. The PEA highlights that ISR has the potential to be a technically sound and economically robust means to extract significant uranium production from the high-grade Midwest Main deposit with low initial capital costs, a high rate of return, and rapid payback.

In December, the Company completed a transaction with Skyharbour Resources Ltd. (“Skyharbour”) resulting in the formation of four joint ventures proximal to the Company’s Wheeler River property: Russell Lake (“Russell Lake – Skyharbour”), Getty East, Wheeler North, and Wheeler River Inliers. In addition, Denison and Skyharbour entered into option agreements, which will allow Denison to increase its ownership interest in each of the new Wheeler North and Getty East joint ventures to up to 70%.

Commercial Activities

2023…

In 2023, the Company sold 200,000 pounds U3O8 of its physical uranium holdings at a weighted average selling price of $99.50 per pound U3O8 (US$73.38 per pound U3O8), representing a realized gain on sale of $12.6 million (US$8.8 million), based on Denison’s average acquisition cost of $36.67 per pound U3O8 (US$29.66 per pound U3O8). As at December 31, 2023, the Company’s remaining uranium portfolio had increased in value by 228% since acquisition, to $120.35 per pound U3O8 (US$91.00 per pound U3O8), for an aggregate value of approximately $276.8 million (US$209.3 million).

2024…

In 2024, the Company sold 100,000 pounds U3O8 of its physical uranium holdings at a weighted average selling price of $135.98 (US$100.00) per pound, representing a realized gain on sale of $9.9 million (US$7.0 million), based on Denison’s average acquisition cost of $36.67 per pound U3O8 (US$29.66 per pound U3O8). As at December 31, 2024, the Company held 2,200,000 pounds U3O8.

|

2025 ANNUAL INFORMATION FORM 14 |

2025…

In 2025, Denison entered a uranium sales contract with a third party which included upfront cash prepayments. Under this arrangement, Denison received $8.2 million (US$6.0 million) in December 2025, with an additional US$4.0 million due by the end of 2026. As consideration for the prepayments, the counterparty will receive a discount from the then prevailing market price on the purchase of 4.5 million pounds of U3O8, with scheduled deliveries from 2028-2033.

And in 2025, the Company entered into sales commitments with market-related pricing terms for 550,000 pounds of U3O8 with deliveries in 2026 and 250,000 pounds of U3O8 with deliveries in 2027.

Finally in 2025, the Company sold 500,000 pounds U3O8 of its physical uranium holdings at a weighted average selling price of $108.50 (US$78.63) per pound, representing a realized gain on sale of $36.0 million (US$24.6 million), based on Denison’s average acquisition cost of $36.67 per pound U3O8 (US$29.66 per pound U3O8). As at December 31, 2025, the Company held 1.7 million pounds U3O8 of purchased physical uranium holdings, excluding Denison’s share of finished goods produced from McClean North.

Financing Activities

2023…

In October, Denison completed a bought deal equity financing resulting in the issuance of 37,000,000 shares at a price of $2.03 (US$1.49) per share for total gross proceeds of $75.1 million (US$55.1 million). The Company intends to use the net proceeds from the offering to fund (1) the advancement of the proposed Phoenix ISR uranium mining operation through the procurement of long lead items (including associated engineering, testing and design) identified during the ongoing Front End Engineering Design process and the Phoenix FS; (2) exploration and evaluation expenditures; and (3) general corporate and administrative expenses, including those in support of corporate development activities, and working capital requirements.

And in October, the Company completed a $15 million strategic investment in F3 Uranium Corp. (“F3”) with the acquisition of unsecured convertible debentures, which carry a 9% coupon payable quarterly, have a maturity dated of October 18, 2028, and are convertible at Denison’s option into common shares of F3 at a conversion price of $0.56 per share. F3 has the right to pay up to one third of the quarterly interest payable by issuing common shares. F3 will also have certain redemption rights on or after the third anniversary of issuance of the debentures and/or in the event of an F3 change of control.