UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR | |

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2025 |

OR | |

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR | |

☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report___________________

For the transition period from ___________________ to _______________________

Commission file number: 001-41524

RENTOKIL INITIAL PLC |

(Exact name of Registrant as specified in its charter) |

|

England and Wales |

(Jurisdiction of incorporation or organization) |

|

|

Compass House Manor Royal Crawley West Sussex RH10 9PY United Kingdom |

(Address of principal executive offices) |

|

|

Rachel Canham Rentokil Initial plc Compass House Manor Royal Crawley West Sussex RH10 9PY United Kingdom Telephone: +44 (0)1293 858000 E-mail: secretariat@rentokil-initial.com |

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

American Depositary Shares, each representing five ordinary shares of £0.01 each |

|

RTO |

|

New York Stock Exchange |

Ordinary shares of £0.01 each |

|

|

|

New York Stock Exchange* |

*Not for trading, but only in connection with the registration of American Depositary Shares representing such ordinary shares pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None |

(Title of Class) |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None |

(Title of Class) |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

The number of outstanding shares of each class of stock of Rentokil Initial plc as of December 31, 2025 was:

Title of Class |

|

Number of Shares Outstanding |

|

Ordinary shares of £0.01 each: |

|

2,526,039,885 |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ⌧ No ◻

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ◻ No ⌧

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ⌧ No ◻

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ⌧ No ◻

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ⌧ |

|

Accelerated filer ◻ |

|

Non-accelerated filer ◻ |

Emerging growth company ◻ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.◻

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).◻

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP |

◻ |

International Financial Reporting Standards as issued by the International Accounting Standards Board |

⌧ |

Other |

◻ |

|

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

◻ Item 17 ◻ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ◻ No ⌧

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes ◻ No ◻

Pursuant to Rule 12b-23(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), the information for the 2025 Form 20-F of Rentokil Initial plc (the “Company”) set out below is being incorporated by reference from the Company’s Annual Report 2025 included as exhibit 15.1 to this Form 20-F (the “Annual Report 2025”).

Presentation of Financial and Other Information

References below to major headings include all information under such major headings, including subheadings, unless such reference is a reference to a subheading, in which case such reference includes only the information contained under such subheading. To the extent that any information incorporated by reference into this Form 20-F itself incorporates information by reference (including by way of internal cross reference), such information shall not form part of this Form 20-F. All references in this Form 20-F to “us”, “we” or “the Company” are to Rentokil Initial plc. Unless the context otherwise requires, “Rentokil Initial” or “Group” refers to the Company and its consolidated entities. Other information contained within the Annual Report 2025 included as exhibit 15.1 to this Form 20-F, including graphs and tabular data, is not included in this Form 20-F unless specifically identified below. Photographs are also not included. None of the websites referred to in the Annual Report 2025, including where a link or QR code is provided, nor any information contained on such websites is incorporated by reference in this Form 20-F.

In addition to the information set out below, the information set forth under the headings “Glossary” on page 227 and “Cautionary Statement” on page 228, in each case of the Annual Report 2025 included as exhibit 15.1 to this Form 20-F is incorporated by reference.

References herein to Rentokil Initial websites, including where a link is provided, are textual references only and information on or accessible through such websites does not form part of and is not incorporated into this Form 20-F. References to “audited” information (including graphs and tabular data) set forth under the heading “Corporate Governance—Directors’ Annual Remuneration Report-2025—Directors’ remuneration in the year to 31 December 2025” on pages 120 to 130 refer to procedures performed by the Company’s external auditor in accordance with International Standards on Auditing (UK) (‘ISAs (UK)’) and applicable law and does not form part of the “Report of Independent Registered Public Accounting Firm” on pages F-2 to F-4 of this Form 20-F.

Cautionary Note Regarding Forward-Looking Statements

In order, among other things, to utilise the ‘safe harbour’ provisions of the U.S. Private Securities Litigation Reform Act of 1995, we are providing the following cautionary statement:

This Form 20-F and the Annual Report 2025 contain statements that are, or may be, forward-looking regarding the Group’s results of operations, business strategy, plans and objectives, including, among other things, statements about the Group’s financial condition, liquidity, prospects, growth and the economic and business circumstances occurring from time to time in the countries and markets in which the Group operates. These statements are often, but not always, made through the use of words or phrases such as “believe”, “anticipate”, “could”, “shall”, “continues”, “may”, “would”, “is likely to”, “should”, “intend”, “seek”, “aim”, “plan”, “potential”, “predict”, “will”, “expect”, “estimate”, “project”, “positioned”, “strategy”, “outlook”, “target” and similar expressions or negatives of these expressions.

Although we believe that the forward-looking statements in this Form 20-F and the Annual Report 2025 are based on reasonable assumptions, such statements involve risk and uncertainty because they relate to future events and circumstances. There are accordingly a number of factors which might cause actual results and performance to differ materially from those expressed or implied by such statements, including, but not limited to, uncertainties related to the following:

| ● | our ability to integrate acquisitions successfully, or any unexpected costs or liabilities from our disposals; |

| ● | difficulties in integrating, streamlining and optimising our IT systems, processes and technologies, including artificial intelligence technologies; |

| ● | our ability to attract, retain and develop key personnel to lead our business; |

| ● | the availability of a suitably skilled and qualified labour force to maintain our business; |

| ● | cyber security breaches, attacks and other similar incidents, as well as disruptions or failures in our IT systems or data security procedures and those of our third-party service providers; |

| ● | inflationary pressures, such as increases in wages, fuel prices and other operating costs; |

1

| ● | weakening general economic conditions, including changes in the global job market or decreased consumer confidence or spending levels, especially as they may affect demand from our customers; |

| ● | our ability to implement our business strategies successfully, including achieving our growth objectives; |

| ● | our ability to retain existing customers and attract new customers; |

| ● | the highly competitive nature of our industries; |

| ● | extraordinary events that impact our ability to service customers without interruption due to a material incident, including a loss of our third-party distributors; |

| ● | the impact of environmental, social and governance (“ESG”) matters, including those related to climate change and sustainability, on our business, reputation, results of operations, financial condition and/or prospects; |

| ● | supply chain issues, which may result in product shortages, cost increases or other disruptions to our business; |

| ● | our ability to protect our intellectual property and other proprietary rights that are material to our business; |

| ● | our reliance on third parties, including third-party vendors for business process outsourcing initiatives, investment counterparties, and franchisees, and the risk of any termination or disruption of such relationships or counterparty default, fraudulent activity or litigation; |

| ● | any future impairment charges, asset revaluations or downgrades; |

| ● | failure to comply with the many laws and governmental regulations to which we are subject or the implementation of any new or revised laws or regulations that alter the environment in which we do business, as well as the costs to us of complying with any such changes and the risk of related litigation; |

| ● | termite damage claims and lawsuits related thereto and associated impacts on the termite provision; |

| ● | our ability to comply with safety, health and environmental policies, laws and regulations, including laws pertaining to the use of pesticides; |

| ● | any actual or perceived failure to comply with stringent, complex and evolving laws, rules, regulations and standards in many jurisdictions, as well as contractual obligations, including data privacy and security, and any litigation (including class action claims and lawsuits) related to such actual or perceived failures; |

| ● | the identification of a material weakness in our internal control over financial reporting within the meaning of Section 404 of the Sarbanes-Oxley Act; |

| ● | changes in tax laws and any unanticipated tax liabilities; |

| ● | adverse credit and financial market events and conditions, which could, among other things, impede access to, or increase, the cost of financing; |

| ● | the restrictions and limitations within the agreements and instruments governing our indebtedness; |

| ● | a lowering or withdrawal of the ratings, outlook or watch assigned to our debt securities by rating agencies; |

| ● | an increase in interest rates and the resulting increase in the cost of servicing our debt; and |

| ● | exchange rate fluctuations and the impact on our results or the foreign currency value of our American Depositary Shares (“ADSs”) and any dividends. |

Further details on the principal risks that may affect the Group can be found in the “Risks and Uncertainties” section detailed on pages 68 to 70 and the left column on page 71 and under the heading “Strategic Report—Responsible Business—Climate-related risk management” on page 62 (in relation to climate-related risks), in each case of the Company’s Annual Report 2025 included as exhibit 15.1 to this Form 20-F, as well as on pages F-51 to F-54 (in relation to financial risks) and under the heading Item 3.D “Risk Factors”, in each case of this Form 20-F.

Forward-looking statements speak only as of the date they are made and no representation or warranty, whether express or implied, is given in relation to them, including as to their completeness or accuracy or the basis on which they were prepared. Other than in accordance with the Company’s legal or regulatory obligations (including under the UK Listing Rules and the Disclosure Guidance and Transparency Rules), the Company does not undertake any obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events or otherwise. Information contained in this Form 20-F and the Annual Report 2025 relating to the Company or its share price, or the yield on its shares, should not be relied upon as an indicator of future performance. Nothing in this Form 20-F and the Annual Report 2025 should be construed as a profit forecast.

2

TABLE OF CONTENTS

3

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. |

Reserved |

Reserved.

B. |

Capitalization and Indebtedness |

Not applicable.

C. |

Reason for the Offer and Use of Proceeds |

Not applicable.

D. |

Risk Factors |

You should carefully consider the factors described below, in addition to the other information set forth in this Form 20‑F. Providing route-based services carries various inherent risks and uncertainties that may affect our business. In this section, we describe the risks and uncertainties that we consider material to our business in that they may have a significant effect on our business, reputation, results of operations, financial condition and/or prospects.

These disclosures reflect our beliefs and opinions as to factors that could materially and adversely affect us and our securities in the future. References to past events are provided by way of example only and are not intended to be a complete listing or a representation as to whether or not such factors have occurred in the past or their likelihood of occurring in the future.

This Annual Report includes statements that may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act. We believe that the forward-looking statements about Rentokil Initial in this Form 20-F, identified by words such as “believes”, “anticipates”, “could”, “shall”, “continues”, “may”, “would”, “is likely to”, “should”, “intends”, “seeks”, “aims”, “plans”, “potential”, “predicts”, “will”, “expects”, “estimates”, “projects”, “positioned”, “strategy”, “outlook”, “target” and similar expressions or negatives of these expressions, are based on reasonable assumptions. However, forward-looking statements involve inherent risks and uncertainties such as those summarised below. They relate to events that may occur in the future, that may be influenced by factors beyond our control and that may have actual outcomes materially different from our expectations. Therefore, other risks, unknown or not currently considered material, could have a material adverse effect on our financial condition or results of operations.

4

Risks Relating to Business Strategies and Operations

If we are unsuccessful in integrating acquisitions or if our disposals result in unexpected costs or liabilities, our business could be materially and adversely affected.

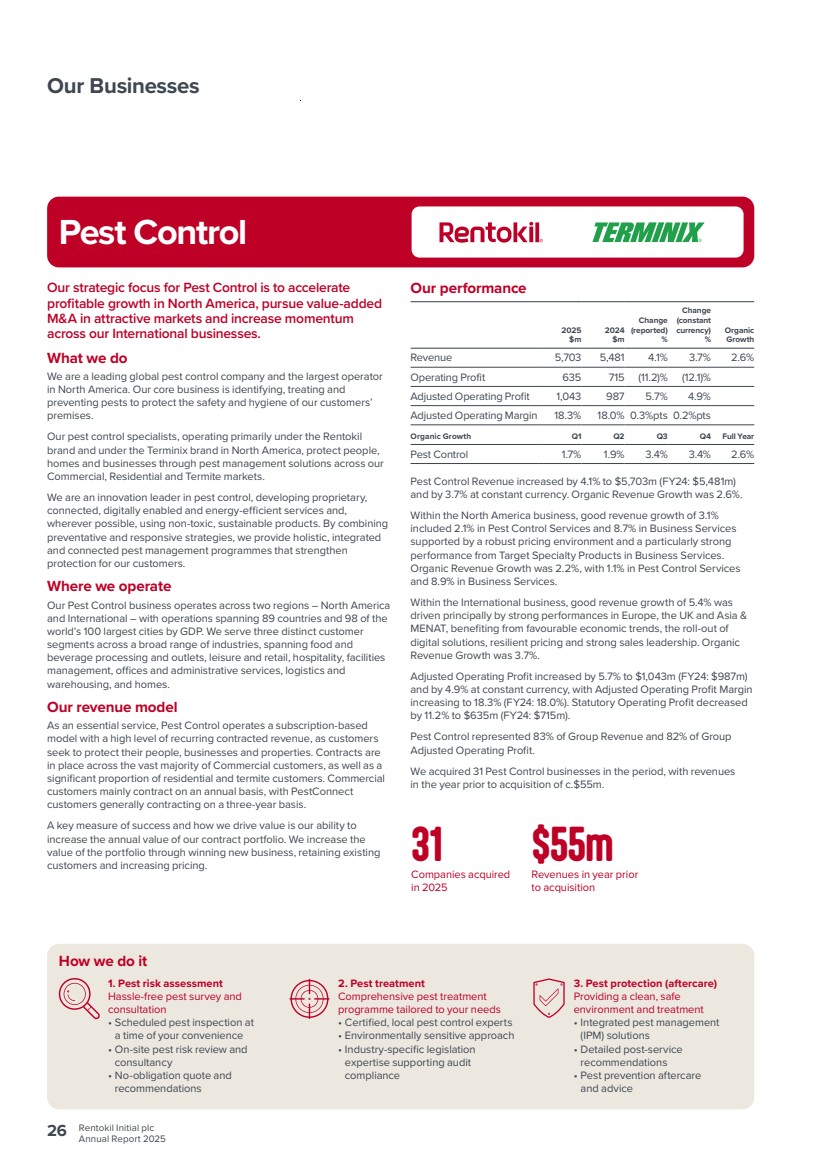

We have a strategy that includes growth by acquisition to extend our geographic footprint and to improve our market share in existing locations. For example, we acquired 36 new businesses in 2025, and we may continue to pursue strategic transactions in the future, which could involve acquisitions or disposals of businesses or assets. These acquisitions need to be integrated quickly and efficiently to minimise potential impact on the operations of the acquired business and the existing business. There are a number of risks to the successful integration of acquired businesses. These risks include, but are not limited to, the possibility that management may be distracted from regular business concerns by the need to integrate operations and that unforeseen difficulties can arise in integrating operations, systems, processes, pay plans, brands and customer offerings as well as difficulties in retaining and assimilating employees and customers. In addition, even where a diligent review of the businesses and/or properties acquired in connection with such acquisitions is performed in accordance with industry norms, such reviews may be incomplete and not necessarily reveal all existing, potential or reasonably foreseeable problems, including actual or contingent liabilities, or permit a full assessment of the deficiencies associated with the businesses or properties. Any acquisition that we make may not provide us with the benefits that were anticipated when entering into such acquisition, or the benefits may not occur within the time periods we anticipated. The realisation of such benefits may be affected by a number of factors, many of which are beyond our control. If we fail to (i) successfully integrate acquisitions into our existing organisational structures and IT systems, (ii) deliver the revenue and profit targets, or (iii) deliver any expected synergy benefits, such as cost savings, the acquired business may not achieve the expected financial and/or operational benefits which could lead to potential adverse short-term or long-term effects on our business, reputation, results of operations, financial condition and/or prospects. Our business may be required to recognise impairment charges or be subject to asset revaluations or downgrades by applying a value in use based test annually. We may also experience difficulties, costs or delays in migrating acquired businesses to our systems, processes and technologies.

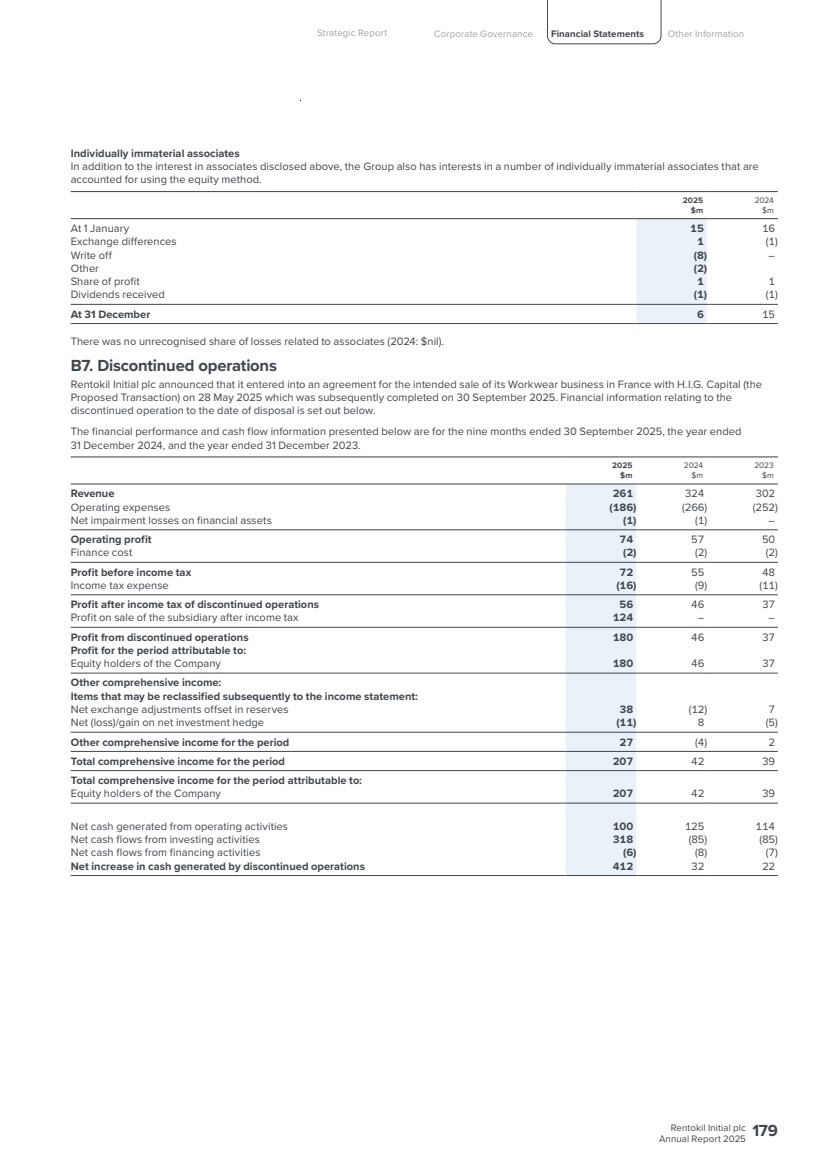

In addition, we have sold a number of our businesses in the past and expect to continue to dispose of businesses from time to time if consistent with our strategy. For example, the Group completed the disposal of its Workwear business in France to H.I.G. Capital on 30 September 2025. Under business sale contracts, we may provide warranties and indemnities to purchasers. Accordingly, we may make provisions in our consolidated financial statements for potential liabilities and costs relating to a disposed business. We may also make provisions in our consolidated financial statements for amounts to cover legal or regulatory claims which are known to be outstanding at the time of sale or which may subsequently become apparent. There can be no assurance that such provisions will be sufficient to cover potential liabilities and consequently disposals of our businesses may have a material adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

We may experience difficulties integrating, streamlining and optimising our IT systems, processes and technologies, including artificial intelligence technologies.

We have invested in, and expect to continue to invest in, a wide range of new systems, processes and technologies intended to improve many aspects of our business, including those incorporating artificial intelligence (“AI”). These systems, processes and technologies impact customers, suppliers, employees and others, including new systems that integrate, streamline and enhance legacy operating IT systems. These activities have required, and may continue to require, significant investment of human and financial resources. We may experience significant delays, increased costs and other difficulties as a consequence of significant disruption or deficiency in implementing such systems, processes and technologies, which could adversely affect our ability to process work orders, send invoices, track and collect payments, fulfil contractual obligations or otherwise operate our business. In addition, our efforts to centralise various business processes within our organisation in connection with this implementation may disrupt operations and negatively impact our business, reputation, results of operations, financial condition and/or prospects.

In addition, a failure to integrate well-designed and properly functioning AI technologies could result in competitive disadvantages, increased costs associated with suboptimal utilisation of AI technology or additional resources to address issues and inefficiencies or non-compliance with applicable AI laws and regulations. Inability to adopt AI technology in an effective and compliant manner could result in reputational damage if we are perceived as being unable to effectively leverage emerging technologies and using data in a manner inconsistent with consumers’ ethical expectations and company values.

5

We depend on key personnel to lead our business.

Our continued success will depend largely on our ability to attract, retain, and develop a high calibre of talent and on the efforts and abilities of our executive officers and certain other key colleagues. As we continue to grow our business, make acquisitions, expand our geographic scope, and offer new products and services, we need the organisational talent necessary to ensure effective succession for executive officer and key colleague roles in order to meet the growth, development and profitability goals of our business. Our operations could be materially and adversely affected if, for any reason, we were unable to attract, retain or develop such officers or key colleagues and successfully execute organisational change and management transitions at leadership levels, or if we have to incur significant costs to retain such individuals or to identify, hire and retain replacements for departing employees. No assurance can be given that we will be able to attract or retain employees to the same extent that we have been able to attract or retain employees in the past.

Mike Duffy was appointed as CEO and Executive Director effective on 16 March 2026, succeeding Andy Ransom, our CEO for the last 12 years. Whilst Andy will continue to work with us to ensure a smooth transition ahead of the Company’s annual general meeting on 7 May 2026, leadership transitions can be difficult to manage and may result in disruptions to our business and increase the likelihood of organisational changes and turnover of other key personnel. In addition, the change in leadership could impact our relationships with existing and potential customers, vendors and other third parties, which could result in a loss of business or otherwise hurt our prospects. Any of these events could have a material adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

We depend on a suitably skilled and qualified labour force to maintain the business.

Our ability to maintain our customer service and execute our business strategy depends on our ability to attract and retain a suitably skilled and qualified labour force. There can be no assurance that we will be able to recruit, train and retain such a labour force in sufficient numbers or of sufficient quality, or that pressure to recruit will not lead to a significant increase in employee costs. In markets where overall employment rates are high, and/or our business is growing quickly, either organically or through acquisitions, we may have difficulties attracting, training and retaining operational personnel of suitable capability. In addition, changes in the global job market may cause, or continue to cause, difficulty in recruiting, training and retaining a suitably skilled and qualified labour force. As a result, we could experience difficulty in responding to customer calls in a timely fashion or delivering our services in a high-quality or timely manner, and could be forced to increase wages to attract, train and retain colleagues, which would result in higher operating costs and reduced profitability. Any of these factors may have a material adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

Moreover, some of our colleagues are members of local trade unions and similar organisations. Industrial action in key operations could result in diminished customer service levels or higher costs and, if prolonged, could damage our reputation and ability to retain existing customers or acquire new customers. Although we believe that all of our operations have good relations with their colleagues and the trade unions that represent those colleagues (where applicable), there can be no assurance that work stoppages or other labour-related developments (including the introduction of new labour regulations in countries where we operate) will not adversely affect our business, reputation, results of operations, financial condition and/or prospects. In addition, potential competition from key colleagues who leave Rentokil Initial could impact our ability to maintain our market share in certain geographic areas.

6

Cyber security breaches, attacks and other similar incidents, as well as disruptions or failures in our IT systems or data security procedures and those of our third-party service providers, could expose us to liability, limit our ability to effectively monitor, operate and control operations and adversely impact our business, reputation, results of operations, financial condition and/or prospects.

Our business is dependent on effective IT systems and data security procedures. We and our third-party service providers may be subject to significant system or network disruptions from numerous causes, including cyber security breaches, attacks or other similar incidents, facility access issues, new system implementations, human error, fraud, theft, fire, power loss, telecommunications failure or a similar catastrophic event. Moreover, computer viruses, worms, malware, ransomware, phishing, spoofing, malicious or destructive code, social engineering, denial-of-service attacks, and other cyber attacks have become more prevalent and sophisticated in recent years. Because the techniques used by computer hackers and others to access or sabotage networks and computer systems constantly evolve and generally are not recognised until launched against a target, we and our third-party service providers may be unable to anticipate, detect, react to, counter or mitigate against all of these techniques or remediate any resulting incident. Cyber security risk has increased due to increased online and remote activity and we have in the past experienced, and may continue to experience, increases in the number and seriousness of cyber attacks, including distributed denial-of-service attacks and ransomware incidents. In 2025, our organisation encountered ten cyber security incidents, each effectively addressed through our established incident response protocol and none of which had a material impact on our business. All of these incidents were reported to the Board or Audit Committee, who have oversight of the risks from cyber security threats, by management, who are responsible for managing prevention, detection, mitigation and remediation of cyber security incidents. While similar attacks have previously been detected and mitigated before causing a material impact on the business, there remains a risk that more sophisticated cyber attacks in the future could evade detection or prevention and result in a material impact on our business, reputation, results of operations, financial condition and/or prospects.

Any IT system disruptions or breaches may lead to unauthorised release of data (including colleague, customer and supplier personal data that we hold) and inefficient business operations, including poor supply chain management, and have a negative impact on customer service, resulting in a loss of customers, which could have a material adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

We may be required to expend significant additional resources to continue to modify or enhance our protective measures or to investigate or remediate any cyber security vulnerabilities, breaches, attacks or other similar incidents. Any cyber security incident, attack or other similar incident, or our failure to make adequate or timely disclosures to the public, regulators, or law enforcement agencies following any such event, could harm our competitive position, result in violations of applicable data privacy or cyber security laws or regulations, result in a loss of customer confidence in the adequacy of threat mitigation and detection processes and procedures, cause disruption to business activities, divert management attention and other resources or otherwise adversely affect our internal operations and reputation, degrade financial results, cause us to incur significant costs to remedy the damages caused by the incident or defend legal claims, subject us to additional regulatory scrutiny and expose us to civil litigation, fines, damages or injunctions. With respect to cyber security-related legal claims and regulatory scrutiny, we also may incur additional costs related to the diverse set of laws, rules and regulations to which we are subject across multiple jurisdictions.

Inflationary pressures, such as increases in wages, fuel prices and other operating costs, could adversely impact our business, results of operations, financial condition and/or prospects.

In the year ended 31 December 2025, global inflation rates have steadily declined from previous years, though rates vary significantly by country and region causing some increases in our operating costs and expenses. Whilst we have, to date, been able to pass on such cost increases to customers in the form of increased prices, we may not in the future be able to pass these cost increases on fully, or in a timely manner, to customers. Our financial performance may therefore be adversely affected by sudden or material increases in the level of our operating costs and expenses, which can be triggered by inflationary pressures. For example, fuel prices are subject to market volatility, and our fleet has been negatively impacted by significant increases in fuel prices in the past and could be negatively impacted in the future. In addition, we continue to monitor the adverse impacts of the ongoing conflict in the Middle East, the situation in Venezuela and the war in Ukraine and the associated sanctions against various Russian organisations, companies and individuals on the global economy in general and on our business operations, although we have no direct operations in Russia or Ukraine. Such events have increased fuel prices, and further prolonged conflicts may have further negative consequences such as increased inflation and transportation costs. Fuel price increases have also caused increases in the cost of chemicals and other materials used in our business. To the extent such costs increase further, we may be prevented, in whole or in part, from passing these cost increases on to our existing and prospective customers, which could have a material adverse impact on our results of operations, financial condition and/or prospects.

7

Weakening general economic conditions, including changes in the global job market or decreased consumer confidence or spending levels, especially as they may affect demand from our customers, may adversely impact our business, results of operations, financial condition and/or prospects.

Ongoing volatility in the global economic environment has led to, and may continue to lead to, economic challenges such as low gross domestic product growth in regional and national economies, high volatility in commodity prices and exchange rates and efforts made by governments to increase the minimum wage across markets, as well as wide variations in local market prices and cost inflation across the globe. This may be exacerbated by economic uncertainty caused by geopolitical events, political instability and civil unrest in some local markets, and catastrophic business events, including the continuation and/or broadening of the conflicts in Ukraine and the Middle East and/or the situation in Venezuela. Further economic slowdown or recessions in the markets in which we operate may lead to a reduction in the level of demand from our customers for existing and new services. Low-growth economies with inherent cost inflation may make it difficult for us to maintain profitability if we have weak pricing power in those markets, in particular, in areas of hyperinflation. Furthermore, adverse economic conditions may lead to an increased number of customers not renewing contracts or seeking to reduce prices leading to a reduction in profit margins and cash flows or being unable to pay for existing or additional services leading to an increase in bad debts. Our pricing may be impacted negatively by an increased presence of multinational competitors in the markets in which we operate or an increased reliance on key customer accounts in markets impacted by adverse economic conditions. The entry of multinational competitors may also make it difficult for us to maintain profitability by increasing the cost of acquisitions. Any of these events could have a material adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

We may not successfully implement our business strategies, including achieving our growth objectives.

We may not be able to fully implement our business strategies or realise, in whole or in part within the expected time frames, the anticipated benefits of various growth plans or other initiatives. Our ability to implement our business strategy may be adversely affected by factors that we cannot foresee currently, such as unanticipated costs and expenses, pandemics and other global health crises, technological change, recession and economic slowdown, the level of interest rates, foreign exchange risks, failure to integrate acquisitions, a decline in the effectiveness of our marketing (including digital marketing) activities or disruptions in the supply chain. All of these factors may necessitate changes to our business strategy or adversely affect our business, reputation, results of operations, financial condition and/or prospects.

In addition, we will incur certain costs to achieve efficiency improvements, systems implementations and growth in our business, and we may not meet anticipated implementation timetables or stay within budgeted costs. As these efficiency improvements, system implementations and growth initiatives are implemented, we may not fully achieve expected cost savings and efficiency improvements, system implementations or growth rates, or these initiatives could adversely impact customer retention or our operations. Also, our business strategies may change in light of our ability to implement new business initiatives, competitive pressures, economic uncertainties or developments or other factors.

Our continued growth depends on our ability to retain existing customers and attract new customers.

Our ability to grow is dependent on our ability to retain existing customers and attract new customers. There can be no assurance that our strategy of using new technology and improved sales techniques to attract profitable new clients, up-selling and cross-selling to existing clients and focusing on retaining profitable business when renewing existing customer contracts will be successful. Moreover, failure to maintain consistently high levels of customer service, client management and sales capability, failure to adapt to local business and consumer needs and/or failure to win and retain profitable customers in the face of competition from competitors (including those with lower costs or which are willing to accept lower margins) may have a material adverse effect on our business, results of operations, financial condition and/or prospects. We must be sufficiently agile to develop and deliver products and services that meet local market needs. If we are not able to adapt to local business and consumer needs, our existing customers may choose not to renew contracts, reduce the use of our services across their operations or seek reductions in prices.

We must continue to develop products and services that meet the needs and expectations of our customer base, including to ensure the continued efficacy of our products in the target pest population. Furthermore, as technological developments disrupt the markets in which we operate and change service offerings across our industries, we may need to develop new products and services. In the future, products and services may interact with each other in new ways and enable new capabilities to be offered to consumers, such as systems that are networked and able to be monitored in real time. Our competitors may be earlier to embrace these new technological developments that are disruptive to the market or to develop more effective products, and a delay in our response may lead to adverse effects to our business, reputation, results of operations, financial condition and/or prospects.

8

Our industries are highly competitive.

We compete with a wide variety of competitors of varying sizes and face competition in many of the markets in which we operate. The growing presence of multinational competitors may increase the cost of acquisitions and/or drive down prices, impacting our profitability. Furthermore, the increased presence of facilities management companies in the markets in which we operate may also drive down prices and adversely impact the quality of our relationships with end customers. The principal methods of competition in our business include quality and speed of customer service, brand awareness and reputation, effective use of technology and systems, customer satisfaction, fairness of contract terms (including price and promotions), professional sales forces and referrals. We may be unable to compete successfully against current or future competitors, and the competitive pressures that we face may result in reduced market share, reduced pricing or an adverse impact on our reputation, business, results of operations, financial condition and/or prospects.

Extraordinary events may significantly impact our business if we are unable to ensure business continuity due to a material incident.

The ability to service customers without interruption is essential to our operations. Contingency plans are required to continue or recover operations following a disruption or incident but may not be adequate to enable us to continue or recommence trading without a loss of business. Such incidents may include (a) a significant cyber attack or IT failure which impacts our ability to plan efficient routing, or ability to invoice, and is not recovered quickly, (b) fire, flood or climate event impacting our premises or transportation/supply chain network preventing goods from being available to enable our technicians to service our customers, (c) industrial action by colleagues, or (d) where third parties are engaged for services, the termination of their engagement or business disruption could materially impact the business. Inability to restore or replace critical capacity to an agreed level within an agreed timeframe would prolong the impact of such disruption or incident and could lead to, among other things, negative publicity and reputational damage and could severely affect our business, reputation, results of operations, financial condition and/or prospects.

We have independent, third-party distributors, the loss of which could have an adverse effect on our business, reputation, results of operations, financial condition and/or prospects. Government shutdowns can have a material adverse effect on operations or cash flows by disrupting or delaying new product launches, renewals of registrations for existing products and receipt of import or export licences for raw materials or products.

War (including acts of terrorism or hostilities), natural or man-made disasters (including earthquakes or pandemics), water shortages or severe weather conditions, in particular enhanced by climate change, affecting the food service, hospitality, travel and other industries can cause a downturn in the business of our customers or impact our supply chain, which in turn can have a material adverse effect on our business, results of operations, financial condition or prospects. Hurricanes or other severe weather events impacting the local markets could materially and adversely affect our ability to obtain raw materials at reasonable cost, or at all, and could adversely affect our business. The health and safety of our colleagues in local markets could be harmed by the detrimental effects of natural and man-made disasters, which could have a material adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

ESG matters, including those related to climate change and sustainability, may have an adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

Ongoing activism related to ESG matters may hinder our access to capital, as investors may reconsider their capital investment as a result of their assessment or perception of our ESG practices. Customers, consumers, investors and other stakeholders are focusing on ESG issues, including climate change, water use, deforestation, plastic waste, human and animal health and welfare, chemical usage and other concerns. Changing customer preferences are resulting in, and may continue to result in, increased demands regarding reducing use of virgin plastics and packaging materials, including single-use and non-recyclable plastic packaging, and other components of our products and their impact on human and animal health, biodiversity, and environmental sustainability, a growing demand for natural, organic or non-toxic products and ingredients; or customer concerns or perceptions (whether accurate or inaccurate) regarding the effects of ingredients or substances present in certain products. Certain animal welfare advocacy groups may raise concerns regarding products such as glue boards, snap traps or other products perceived to have animal cruelty issues, and secondary poisoning of predators. These demands, perceptions and preferences could cause us to incur additional costs or to make changes to our operations to comply with such demands and customer preferences, and a delay in our response (or the failure to respond effectively) may lead to adverse effects to our business, results of operations and financial condition, and recruitment and retention of the labour force that we need.

9

Concern over climate change may result in new or increased legal and regulatory requirements to reduce or mitigate impacts to the environment. Increased regulatory requirements, including in relation to various aspects of ESG, such as disclosure requirements, may result in higher compliance costs or input costs of energy and raw materials, which may cause disruptions in the manufacture of our products, and these costs could have a material adverse effect on our results of operations and cash flows. Any failure to achieve our ESG goals or a perception (whether or not valid) of our failure to act responsibly with respect to ESG issues or to effectively respond to new, or changes in, legal or regulatory requirements concerning environmental or other ESG matters, or increased operating or manufacturing costs due to increased regulation, could adversely affect our business, reputation, results of operation, financial condition and/or prospects. In addition, we may also be adversely impacted as a result of conduct by contractors, customers or suppliers that fail to meet our or our stakeholders’ ESG standards.

Supply chain issues may result in product shortages, cost increases or disruptions to our business.

We have a complex global network of suppliers that continues to expand to meet increased customer demand and may, in the future, further evolve in response to market conditions. Although the majority of the products we use are generally available from multiple sources, and alternatives have been generally available in the event of disruption in the past, we could experience material disruptions in production and other supply chain issues on specific bespoke products (including as a result of recent global events impacting shipping or tariffs), which could result in out-of-stock conditions, and our results of operations and relationships with customers could be adversely affected (a) if new or existing suppliers are unable to meet any standards that we set or that are set by government or industry regulations or customers, (b) if we are unable to contract with suppliers at the quantity, quality and price levels needed for our business, or (c) if any of our key suppliers becomes insolvent, ceases or significantly reduces its operations or experiences financial distress.

Our inability to fully or substantially meet customer demand due to supply chain issues could result in, among other things, unmet consumer demand leading to reduced preference for our products or services in the future, customers purchasing products and services from competitors as a result of such shortage of products, strained customer relationships, termination of customer contracts, additional competition and new entrants into the market, and loss of potential sales and revenue, which could adversely affect our business, reputation, results of operations, financial condition and/or prospects.

We may not be able to adequately protect our intellectual property and other proprietary rights that are material to our business.

Our ability to compete effectively depends in part on our ability to obtain, maintain, protect, defend and enforce our intellectual property and other proprietary rights, including the service marks, trademarks, trade names and other intellectual property rights we own or licence, particularly our brand names, including Rentokil, Initial, Ambius, Terminix, Copesan, Assured, McCloud, Gregory, Ehrlich, Presto-X, Western Exterminator, Florida Pest Control, Bug Out, Steritech, PestConnect, Lumnia, Signature, Eradico, Cannon, Ultraprotect, Calmic, Pestfree365, Entotherm, Medentex, Boecker, Radar and Rapid Pro. We have not sought to register or protect all of our intellectual property, including our trademarks, either in the UK, the U.S. or in every jurisdiction in which they are or may be used. Furthermore, because of the differences in foreign trademark, patent and other intellectual property laws, we may not receive the same protection in other countries as we would in the UK or the U.S.

If we are unable to protect our intellectual property and other proprietary rights, including brand names, it could cause a material adverse impact on our business, reputation, results of operations, financial condition and/or prospects. Litigation may be necessary to enforce our intellectual property rights and protect our proprietary information, or to defend against claims by third parties that our products, services or activities infringe on their intellectual property rights.

We rely on third parties, including third-party vendors for business process outsourcing initiatives, investment counterparties, and franchisees. Any termination or disruption of such relationships or counterparty default, fraudulent activity or litigation could have a material adverse effect on our business.

Our strategy to increase profitability, in part, by reducing our costs of operations, and to mitigate and manage our exposure to financial risk, includes the implementation of certain business process outsourcing initiatives and entry into arrangements with investment counterparties, including lenders, insurers and derivative counterparties. As such, we are exposed to counterparty risk. Any disruption, termination or substandard performance of these outsourced services, including possible breaches by third-party vendors of their agreements with us, fraudulent activity by the counterparty or the failure of counterparties to discharge all or part of their obligations (including, for example, due to the deterioration of a counterparty’s actual or perceived creditworthiness) could adversely affect our reputation, customer and colleague relationships, results of operations and financial condition. Also, to the extent a third-party outsourcing provider or counterparty relationship is terminated, there is a risk of disputes or litigation and that we may not be able to enter into a similar agreement with an alternate provider in a timely manner or on terms that we consider favourable, and even if we find an alternate provider, or choose to insource such services or activities, there are significant risks associated with such transition.

10

In addition, to the extent we decide to terminate outsourcing services and insource such services, there is a risk that we may not have the capabilities to perform these services internally, resulting in a disruption to our business, which could adversely impact our business, reputation, results of operations, financial condition and/or prospects. We could incur costs, including personnel and equipment costs, to insource previously outsourced services like these, and these costs could adversely affect our results of operations and cash flows.

Third-party distributors, subcontractors, vendors and franchisees are independent third parties that we do not control, and who own, operate and oversee the daily operations of their businesses. If third party distributors, subcontractors, vendors and franchisees do not successfully operate their businesses in a manner consistent with required laws, standards and regulations, we could be subject to claims from regulators or legal claims for the actions or omissions of such third-party distributors, subcontractors, vendors and franchisees. In addition, our relationship with third-party distributors, subcontractors, vendors and franchisees could become strained (including resulting in litigation) and these strains in relationships or claims could have a material adverse impact on our business, reputation, results of operations, financial condition and/or prospects.

We may be required to recognise impairment charges or be subject to asset revaluations or downgrades.

We have significant amounts of goodwill and intangible assets, such as customer lists. In accordance with applicable accounting standards, goodwill and indefinite-lived intangible assets are not amortised and are subject to assessment for impairment by applying a value in use or fair value less cost to sell test annually, or more frequently if there are indicators of impairment, including:

| ● | observable indications that the asset’s value has declined significantly more than would be expected as a result of the passage of time or normal use; |

| ● | significant changes with an adverse effect on the entity that have taken place, or will take place in the near future, in the technological, market, economic or legal environment in which the entity operates, or in the market to which an asset is dedicated; |

| ● | market interest rates or other market rates of return on investments have increased, and those increases are likely to affect the discount rate used in calculating an asset’s value in use and decrease the asset’s recoverable amount materially; |

| ● | the carrying amount of the net assets of the entity is more than its market capitalisation; |

| ● | evidence that there is obsolescence or physical damage of the asset; |

| ● | significant changes with an adverse effect on the entity that have taken, or are expected to take place in the near future, in the extent to which, or manner in which, an asset is used or is expected to be used. These changes include the asset becoming idle, plans to discontinue or restructure the operation to which an asset belongs, plans to dispose of an asset before the previously expected date, and reassessing the useful life of an asset as finite rather than indefinite; and |

| ● | indication that the economic performance of an asset is, or will be, worse than expected. |

Based upon future economic and financial market conditions, our operating performance and other factors, including those listed above, we may incur impairment charges in the future, in respect of goodwill created and the value at which assets were recognised at completion. It is possible that such impairment, if required, could be material. Any future impairment charges that we are required to record could have a material adverse impact on our business, results of operations, financial condition and/or prospects.

Risks Relating to Legal and Compliance Matters

Government regulations and enforcement, and potential litigation, could have an adverse effect on our financial results.

As a global company, we are subject to many laws and governmental regulations across all of the countries in which we conduct business, including laws and regulations involving marketing, antitrust, anti-bribery, anti-fraud, anti-corruption, consumer protection, product liability, environmental, health and safety, employment laws, intellectual property, data privacy, compliance and other matters, as well as potential litigation, regulatory and administrative actions. If we are unable to comply with all applicable laws and regulations, it could negatively impact our business, results of operations, financial condition, reputation and/or prospects.

11

In addition, new or revised laws or regulations, or changes to the ways existing laws or regulations apply to our business, may alter the environment in which we do business, which could adversely impact our financial results. For example, the Economic Crime and Corporate Transparency Act introduced a new offence in the United Kingdom, effective from 1 September 2025, whereby an organisation can be held criminally liable for the failure to prevent fraud if reasonable internal procedures are not implemented to prevent the fraud. In addition, Provision 29 of the UK Corporate Governance Code 2024 requires boards to annually monitor, review, and declare the effectiveness of their material internal controls in their annual report, starting with annual reports in respect of the year beginning January 1, 2026.

In addition, we face litigation from time to time. Currently we are defending against multiple purported class action lawsuits, including one filed in November 2024 and one filed in April 2025, further details of which can be found under the heading “Financial Statements—Notes to the Consolidated Financial Statements—D3. Contingent liabilities” on page F-67 of this Form 20-F. We may also face exposure to potential future claims or litigation, including exposure to injunctive relief or damages granted by courts in respect of such claims. Regardless of the outcome of any litigation or claims, we may incur additional costs in defending against such claims. An unfavourable outcome or settlement in any litigation may have an adverse effect on our business, reputation, results of operations, financial condition and/or prospects. Additionally, any loss of Rentokil Initial plc’s status as a “foreign private issuer” would require us to comply with the reporting, disclosure, compliance and governance requirements that are applicable to U.S. domestic issuers and could result in significant additional legal, accounting and other expenses, as well as increased demands on management’s time.

While it is our policy and practice to comply with all legal and regulatory requirements applicable to our business, we cannot provide assurance that our internal control policies and procedures and ethics and compliance program will always protect us from acts committed by our colleagues or agents. A finding that we are in violation of, or out of compliance with, applicable laws or regulations could subject us to civil remedies, including fines, damages, injunctions, product recalls or withdrawal of licenses to operate, or criminal or civil sanctions, any of which could adversely affect our business, reputation, results of operations, financial condition and/or prospects. Even if a claim is unsuccessful, is without merit or is not fully pursued, the negative publicity surrounding such assertions regarding our products, processes or business practices could adversely affect our reputation and brand image.

Further, new legislation or regulations may result in increased costs to us indirectly to the extent suppliers increase prices of goods and services because of increased compliance costs, excise taxes or the reduced availability of raw materials. The enactment of unduly onerous and restrictive regulation could have a material adverse effect on our business, results of operations, financial condition and/or prospects.

Termite damage claims and lawsuits related thereto could increase our legal expenses and may adversely impact our business, reputation, results of operations, financial condition and/or prospects.

Our business may become subject to a significant number of damage claims related to termite activity in homes/commercial premises, often accompanied by a termite damage warranty/guarantee. Currently, the legacy Terminix business is subject to a significant number of damage claims related to its termite control services and termite damage warranties/guarantees. Damage claims may include circumstances when a customer notifies us that they have experienced damage, and we reach an agreement to remediate that damage (a “Non-litigated Claim”), and circumstances when a customer directly initiates litigation or arbitration proceedings or when we do not reach an agreement with a customer to remediate the damage and that customer initiates litigation or arbitration proceedings (a “Litigated Claim”). Some plaintiffs bringing Litigated Claims may seek to demonstrate a pattern and practice of fraud in connection with Litigated Claims and may seek awards, in addition to repair costs, which include punitive damages and damages for mental anguish. In 2025, we assessed the probable future cash outflows arising from termite damage claims. Due to factors such as inflation, the costs for settling claims and the accelerated settlement time to settle a claim, we have recognised additional provisions of $201 million. The closing provision was $384 million at 31 December 2025.

We intend to defend these Litigated Claims vigorously, and we have taken decisive actions to mitigate any increasing claims costs; however, we cannot give assurance that these mitigating actions will be effective in reducing claims or costs related thereto, and this could result in the costs of termite claims or litigation exceeding our accounting provision for termite claims, nor can we give assurance that lawsuits or other proceedings related to termite damage claims will not materially affect our business, reputation, results of operations, financial condition and/or prospects, even if any such lawsuits are found to be without merit.

12

Our business may also become subject to state regulator claims related to trade practices, including termite renewal pricing, inspection and treatment practices (a “Regulator Claim”). Terminix had entered into settlements in relation to such claims in the past and we intend to defend any future Regulator Claims. We also intend to take action to mitigate claims costs; however, we cannot give assurance that these mitigating actions will be effective in reducing claims or costs related thereto, nor can we give assurance that lawsuits or other proceedings related to trade practices will not materially affect our business, reputation, results of operations, financial condition and/or prospects.

Compliance with, or violation of, health and safety and environmental policies, laws and regulations, including laws pertaining to the use of pesticides, could result in significant costs that adversely impact our business, reputation, results of operations, financial condition and/or prospects.

We have an obligation to ensure that colleagues, customers and other stakeholders remain safe, that the working environment is not detrimental to health and that we are aware of and minimise any adverse impact on the environment. In addition, the pest control, hygiene and textile industries are subject to various laws and regulations regarding safety, health and environmental (“SHE”) matters. Among other things, these laws regarding SHE regulate the emission or discharge of materials into the environment, the use, storage, treatment, disposal, transportation and management of hazardous substances and wastes, the impact of chemicals (including fumigant gases), as well as pesticide and biocide products, on people and the environment, and the protection of the health and safety of our colleagues and the public.

These laws also impose liability for the costs of investigating and remediating, and damages resulting from, present and past releases of hazardous substances, including releases from former activities at sites or by prior owners or operators of sites we have acquired or that we currently own or operate. These laws and regulations can result in costs associated with transporting and managing hazardous materials and waste disposal and plant site clean-up, fines, penalties, orders requiring corrective action or suspending or otherwise impacting our operations or other sanctions if we are found to be in violation of law, as well as modifications, disruptions or discontinuation of certain operations or types of operations including product recalls and reformulations. Changes in such laws and regulations, including among others, air, water, chemical and product regulations, could impact the sales of some of our products or services. In addition to an increase in costs of manufacturing and delivering products, a change in production regulations or product regulations could result in interruptions to our business and potentially cause economic or consequential losses should we be unable to meet the demands of our customers for products.

Products that we use containing pesticides generally must be registered with the relevant governmental agencies or authorities before they can be sold or applied. The failure to obtain, or the cancellation of, any such registration, or the withdrawal from the marketplace of such pesticides, could have an adverse effect on our business, the severity of which would depend on the products involved, whether other products could be substituted and whether competitors were similarly affected. Most of the pesticides we use are manufactured by independent third parties and are evaluated by the relevant governmental authorities or agencies as part of our ongoing exposure risk assessment. Any of these authorities or agencies may decide that a pesticide we use will be limited or will not be re-registered for use in the relevant jurisdiction. We cannot predict the outcome or the severity of the effect of any particular authority’s or agency’s continuing evaluations. In addition, the use of certain pesticide products is regulated by various international, national, federal, state, provincial and local environmental and public health agencies and bodies. Some of our products or service models may also become subject to bans or restrictions due to animal cruelty concerns, such as permanent rodent baiting. Given our dispersed locations, distributed operations and numerous colleagues and franchise associates, we may be unable to prevent violations of these or other laws and regulations or misuse of products by colleagues or others from occurring. Even if we are able to comply with all such laws and regulations and obtain all necessary registrations and licences, the pesticides or other products we apply or use, or the manner in which we apply or use them, could be alleged to cause injury to the environment, to people or to animals, or such products could be banned in certain circumstances. The laws and regulations may also apply to third-party vendors who are hired to repair or remediate property and who may fail to comply with SHE laws and regulations and subject us to risk of legal exposure. The costs of compliance or the investigation and remediation of non-compliance, including combating reputational harm or defending civil or criminal proceedings, products liability, personal injury or other lawsuits, could have a material adverse impact on our business, reputation, results of operations, financial condition and/or prospects.

International, national, federal, state, provincial and local agencies and bodies regulate the disposal, handling and storage of waste, discharges from our facilities and the investigation and clean-up of impacted sites. We could incur significant costs, including investigation and remediation costs, fines, penalties and civil or criminal sanctions and claims by third parties for property damage and personal injury, as a result of violations of, or liabilities under, such laws and regulations enforced by these agencies and bodies. Liability under laws and regulations can be imposed on a joint and several basis and without regard to fault or the legality of the underlying conduct. In addition, potentially significant expenditures could be required to comply with SHE laws and regulations, including requirements or changes in expectations that may be adopted or imposed in the future.

13

A violation of SHE laws or regulations relating to our operations or a failure to comply with the instructions of relevant health and safety authorities, environmental agencies or internal policies could lead to, among other things, personal injury, substantial fines or penalties, including withdrawal of licences to operate, and reputational damage. Such violations could, therefore, have an adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

We are required to comply with stringent, complex and evolving laws, rules, regulations and standards in many jurisdictions, as well as contractual obligations, relating to data privacy and security. Any actual or perceived failure to comply, or litigation related to such actual or perceived failure to comply, with these requirements could have a material adverse effect on our business.

We are required to comply with stringent, complex and evolving laws, rules, regulations and standards in many jurisdictions, as well as contractual obligations, relating to data privacy and security. Ensuring that our collection, use, transfer, storage and other processing of personal information complies with such requirements can increase operating costs, impact the development of new products or services, and reduce operational efficiency.

Internationally, virtually every jurisdiction in which we operate has established its own data privacy and security legal framework with which we must comply. The cost of compliance, and the potential for fines and penalties for non-compliance, with applicable data privacy and security laws and regulations may have a significant adverse effect on our business, reputation, results of operations, financial condition and/or prospects.

If we are otherwise unable to transfer personal data between and among countries and regions in which we operate, it could affect the manner in which we provide our services, the geographical location or segregation of our relevant systems and operations and could adversely affect our financial results. In addition, such procedures and controls, which we operate to comply with relevant data privacy and security requirements in the relevant jurisdictions, may not be effective in ensuring compliance or preventing unauthorised transfers of personal data.

While we strive to publish and prominently display privacy policies that are accurate, comprehensive and compliant with applicable laws, rules, regulations and industry standards, we cannot ensure that our privacy policies and other statements regarding our practices will be sufficient to protect us from claims, proceedings, liability or adverse publicity relating to data privacy and security. Although we endeavour to comply with our privacy policies, we may at times fail to do so or be alleged to have failed to do so. If our public statements about our use, collection, disclosure and other processing of personal information, whether made through our privacy policies, information provided on our website, press statements or otherwise, are alleged to be deceptive, unfair or misrepresentative of our actual practices, we may be subject to potential government or legal investigation or action.

Our compliance efforts are further complicated by the fact that data privacy and security laws, rules, regulations and standards around the world are evolving rapidly, may be subject to uncertain or inconsistent interpretations and enforcement, and may conflict among various jurisdictions. Any failure or perceived failure by us to comply with our privacy policies, or applicable data privacy and security laws, rules, regulations, standards or contractual obligations, or a security breach or deliberate action by colleagues or third parties that leads to theft or other unauthorised access to, or loss or unlawful destruction, use, modification, acquisition, disclosure, release or transfer of, personal information, including customer, colleague, supplier or our proprietary, sensitive or confidential data, may result in requirements to modify or cease certain operations or practices, the expenditure of substantial costs, time and other resources, proceedings or actions against us, legal liability, governmental investigations, enforcement actions, claims, fines, judgements, awards, penalties, sanctions and costly litigation (including class actions). Any of the foregoing could lead to significant reputational damage, distract management and technical personnel, increase our costs of doing business, adversely affect the demand for our products and services, and ultimately result in the imposition of liability, any of which could have a material adverse effect on our business, results of operations, financial condition and/or prospects.

14

Material weaknesses in our internal controls over financial reporting within the meaning of Section 404 of the Sarbanes-Oxley Act could adversely affect our ability to report our financial results accurately or in a timely manner, which may adversely affect our business and reputation.

We are required to comply with certain requirements under the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”), including the maintenance of adequate internal control over financial reporting. We are required to evaluate the effectiveness of our internal control over financial reporting and our independent registered public accounting firm is required to audit the effectiveness of our internal control over financial reporting in compliance with Section 404 of the Sarbanes-Oxley Act. While we have designed an internal control over financial reporting framework for the purposes of the effectiveness evaluation described above, if such controls fail, we may be subject to sanctions or investigations by regulatory authorities, including the U.S. Securities and Exchange Commission (the “SEC”) and the NYSE.

As of 31 December 2025, management has concluded that our internal control over financial reporting was effective. However, we may identify material weaknesses or control deficiencies in the future, and we cannot provide assurance that remediation efforts will be successful or that our internal control over financial reporting will be effective in accomplishing all control objectives. If a material weakness in our internal control over financial reporting is identified and not remediated in a timely manner, we could suffer material misstatements in our consolidated financial statements, fail to meet our reporting obligations or fail to prevent fraud, which may cause investors to lose confidence in our reported financial information, which in turn could have a material and adverse effect on the trading price of ordinary shares in the capital of Rentokil Initial plc, and subject us to potential delisting from the NYSE, regulatory investigations and civil or criminal sanctions. Failure to implement or maintain effective internal control systems required of public companies could also restrict our future access to the capital markets. Furthermore, we may need to incur additional costs and use additional management and other resources as our business and operations further expand or in an effort to remediate any significant control deficiencies that may be identified in the future.

Changes in tax laws and unanticipated tax liabilities could materially and adversely affect the taxes we pay and our profitability.

We operate across many different tax jurisdictions and are subject to changing tax laws, regulations and treaties in and between the jurisdictions in which we operate, as well as periodic tax audits which sometimes challenge the basis on which local tax has been calculated and/or withheld. Changes in tax regimes, or in the interpretation thereof, could result in a material impact on our cash tax liabilities and tax charges. For instance, we have a greater presence in the U.S. following the acquisition of Terminix, which means that changes to tax rules in the U.S. could have a more significant impact on our business. Such an impact could also arise from changes in the application of the existing tax rules that apply to us, including UK tax rules. In either case, this could result in a reduction in financial results depending upon the nature of the change. Further, we are subject to periodic tax audits across many different tax jurisdictions and successful challenges by local tax authorities may have an adverse impact on profitability and cash flow. Unanticipated non-compliance with relevant tax legislation and/or reporting requirements may result in material unprovided tax charges relating to prior years which could have a material adverse effect on our financial condition and/or prospects.

Risks Relating to Financial Markets

Adverse credit and financial market events and conditions could, among other things, impede access to, or increase, the cost of financing, which could have a material adverse impact on our business, results of operations, financial condition and/or prospects.