UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2025 | |

☐ |

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission file number 001-33190

McEWEN INC.

(Name of registrant as specified in its charter)

|

|

Colorado |

84-0796160 |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

150 King Street West, Suite 2800, Toronto, Ontario Canada |

M5H 1J9 |

(Address of principal executive offices) |

(Zip Code) |

(866) 441-0690

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Common Stock, no par value |

MUX |

New York Stock Exchange (“NYSE”) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

Large accelerated filer ☐ |

Accelerated filer ☒ |

Non-accelerated filer ☐ |

Smaller reporting company ☐ |

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262 (b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2025 (the last business day of the registrant’s second fiscal quarter), the aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates of the registrant was $519,882,572 based on the closing price of $9.61 per share as reported on the NYSE. There were 59,452,799 shares of common stock outstanding on March 16, 2026.

DOCUMENTS INCORPORATED BY REFERENCE: Portions of the registrant’s Proxy Statement for the 2026 Annual Meeting of Shareholders are incorporated into Part III, Items 10 through 14 of this report.

TABLE OF CONTENTS

ADDITIONAL INFORMATION

Descriptions of agreements or other documents in this report are intended as summaries and are not necessarily complete. Please refer to the agreements or other documents filed or incorporated herein by reference as exhibits. Please see Item 15, Exhibits and Financial Statement Schedules in this report for a complete list of those exhibits.

1

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Please see the note under “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,” for a description of special factors potentially affecting forward-looking statements included in this report.

CAUTIONARY NOTE REGARDING DISCLOSURE OF MINERAL PROPERTIES

Mineral Reserves and Resources

We are subject to the reporting requirements of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”) and applicable Canadian securities laws, and as a result, we have reported our mineral reserves and mineral resources according to two different standards. U.S. reporting requirements are governed by Item 1300 of Regulation S-K (“S-K 1300”), as issued by the U.S. Securities and Exchange Commission (“SEC”). Canadian reporting requirements for disclosure of mineral properties are governed by National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”), as adopted from the definitions provided by the Canadian Institute of Mining, Metallurgy and Petroleum. Both sets of reporting standards have similar goals in terms of conveying an appropriate level of confidence in the disclosures being reported, but the standards embody slightly different approaches and definitions. All disclosures of mineral resources and mineral reserves in this report are reported in accordance with S-K 1300.

Investors should be aware that the estimation of measured and indicated resources involve greater uncertainty as to their existence and economic feasibility than the estimation of proven and probable reserves, and therefore investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves that conform to S-K 1300 guidelines. The estimation of inferred resources involves far greater uncertainty as to their existence and economic viability than the estimation of other categories of resources. It is reasonably expected that the majority of the inferred mineral resource could be upgraded to an indicated mineral resource with continued exploration. Investors are cautioned not to assume that all or any part of inferred resources exist, or that they can be mined legally or economically.

Technical Report Summaries and Qualified Persons

The technical information concerning our mineral projects in this Form 10-K have been reviewed and approved by William Shaver, P.Eng., Chief Operating Officer, Luke Willis, P.Geo, Director, Resource Modeling, and Channa Kumarage, P.Eng., Director, Technical Services, each a “qualified person” under S-K 1300. For a description of the key assumptions, parameters and methods used to estimate mineral reserves and mineral resources included in this Form 10-K, as well as data verification procedures and a general discussion of the extent to which the estimates may be affected by any known environmental, permitting, legal, title, taxation, sociopolitical, marketing or other relevant factors, please review the Technical Report Summaries for our material properties which are included as exhibits to the 2021 Form 10-K, except for Fox Complex, which was updated and filed as an exhibit to the 10-K dated March 14, 2025 and the Los Azules copper project which was updated and filed as an exhibit to this 10-K.

RELIABILITY OF INFORMATION

Minera Santa Cruz S.A. (“MSC”), the owner of the San José mine, is responsible for and has supplied to us all reported results from the San José mine. The technical information contained herein regarding the San José mine is based entirely on information provided to us by MSC. Our joint venture partner, a subsidiary of Hochschild Mining plc (“Hochschild”), and its affiliates other than MSC do not accept responsibility for the use of project data or the adequacy or accuracy of this information.

2

PART I

ITEM 1. BUSINESS

History and Organization

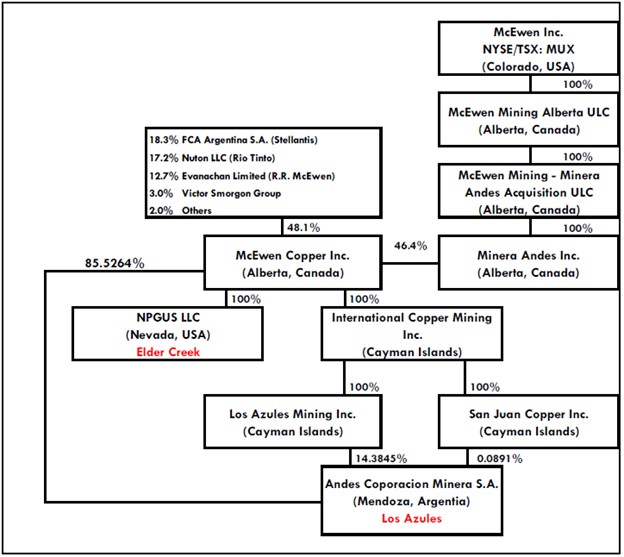

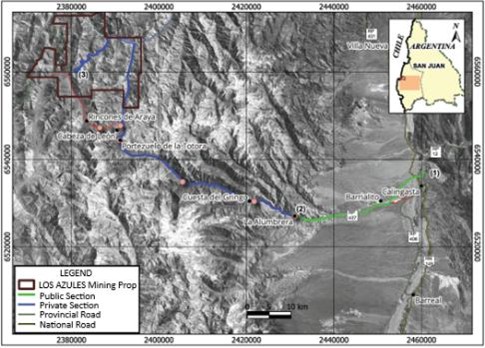

McEwen Inc. (the “Company”) is a gold and silver mining production and exploration company with an advanced copper development project, focused on the Americas. We were incorporated under the laws of the state of Colorado in 1979 as US Gold Corp. In September 2011, US Gold Corp. acquired Minera Andes Inc., and was renamed McEwen Mining Inc. Effective July 7, 2025, the Company changed its name from McEwen Mining Inc. to McEwen Inc. We own 100% of the Froome mine and Stock mill in Ontario, Canada; 100% of the Gold Bar Mine Complex in Nevada; 100% of El Gallo (previously known as the Fenix Project) in Sinaloa, Mexico; a 46.3% interest in McEwen Copper Inc., the owner of the Los Azules copper project (“Los Azules”) in San Juan, Argentina; and a 49% interest in MSC, the owner and operator of the San José mine in Santa Cruz, Argentina. In addition to the above, we hold interests in advanced-stage and exploration-stage projects in the United States, Canada, Mexico, and Argentina.

Our commencement of Canadian operations in 2017 was facilitated by the acquisition of Lexam VG Gold Inc. (“Lexam”) in April 2017, followed by the acquisition of the Black Fox and Stock Properties from Primero Mining Corp. in October 2017. These two acquisitions provided us with an operating mine, mill, and significant land interests in the historic Timmins mining district of Ontario (collectively, the “Fox Complex”). On September 19, 2021, our currently operating Froome mine, located within the Black Fox Property, reached commercial production. The Company is currently developing its Stock Property as an underground mine, with production expected to begin by mid-2026. In January 2026, we closed the acquisition of Canadian Gold Corp. which holds a number of exploration-stage assets, including the Tartan Lake project in Manitoba.

In the United States, construction began on our 100% owned Gold Bar mine in Nevada in 2017. The Gold Bar mine poured its first gold ingot on February 16, 2019, and achieved commercial production on May 23, 2019. Current production is from our Pick, Ridge and Gold Bar South deposits. In August 2024, we expanded our portfolio of exploration-stage properties in Nevada through the acquisition of Timberline Resources Corporation (“Timberline”). Together with our Tonkin Project, acquired in 2005, these properties comprise the Gold Bar Mine Complex.

At El Gallo in Sinaloa, Mexico, mining and crushing activities ceased during the second quarter of 2018. The Company now plans to begin mill construction in H1 2026 as part of its heap leach material (“HLM”) reprocessing project contemplated in its 2021 feasibility study. Production is projected to begin by mid-2027 and is expected to run for 10 years, reaching an average annual output of approximately 20,000 GEOs once commercial production is achieved. A second operational phase focusing on silver dominant material has also been planned (“El Gallo Silver”).

Our objective is to increase shareholder value through the exploration for and economic extraction of gold, silver, and other valuable minerals. Other than the San José mine and the Los Azules copper project, both located in Argentina, we generally conduct our activities as the sole owner, but we may enter into strategic arrangements with other companies through joint venture or similar agreements. We hold our mineral property interests and operate our business through various subsidiary companies.

Our principal executive office is located at 150 King Street West, Suite 2800, Toronto, Ontario, Canada M5H 1J9 and our telephone number is (866) 441-0690. Our website is www.mcewenmining.com. We make available at no cost our periodic reports, including Forms 10-K, 10-Q and 8-K, and news releases and certain of our corporate governance documents, including our Code of Business Conduct and Ethics, on our website. Our common stock is listed on the New York Stock Exchange (“NYSE”) and on the Toronto Stock Exchange (“TSX”) under the symbol “MUX.”

In this report, unless otherwise noted, “Au” represents gold; “Ag” represents silver; “Cu” represents copper; “oz” represents troy ounce; “lb” represents pound; “g/t” represents grams per metric tonne; “o/t” represents troy ounces per short ton; “ft” represents feet; “m” represents meter; “sq” represents square; and C$ refers to Canadian dollars. All our financial information is reported in United States (U.S.) dollars, unless otherwise noted. References to our company include, where the context requires, all our subsidiaries.

3

Segment Information

Our operating segments include Canada, United States, Mexico, MSC and McEwen Copper. Financial information for each of our reportable segments can be found under Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8. Financial Statements and Supplementary Data, Note 3, Operating Segment Reporting.

Products

The end product at our gold and silver operations is generally doré bars or ore concentrate. Doré is an alloy consisting primarily of gold and silver but may also contain other trace elements, cast into unrefined bars. These bars are sent to third party refiners to produce saleable bullion. Ore concentrate, or simply concentrate, is raw mineralized material that has been finely ground into a powdery product from which gangue (waste) is removed, thus concentrating the metal component. Concentrate, as well as slag and fine carbons (which are by-products of the gold production process), are sent to third party smelters for further recovery of gold and silver.

During 2025, production consisted of 100% doré from the Gold Bar Mine Complex, 98% doré and 2% slag and fine carbon from the Fox Complex, and 91% doré and 9% slag and fine carbon from El Gallo. Production from the San José mine consisted of 13% doré and 87% concentrate.

During 2025, we reported the following gold equivalent ounce production attributable to us:

|

|

Gold |

|

Silver |

|

Gold equivalent |

Production |

|

ounces |

|

ounces |

|

ounces(1) |

Gold Bar Mine Complex |

|

33,221 |

|

540 |

|

33,227 |

Fox Complex |

|

23,144 |

|

3,605 |

|

23,187 |

El Gallo |

|

396 |

|

53,047 |

|

1,152 |

San José mine (on 49% basis) |

|

37,715 |

|

1,776,034 |

|

58,120 |

Total production |

|

94,476 |

|

1,833,226 |

|

115,687 |

| (1) | Calculated using an average silver to gold spot price ratio of 86:1. |

Gold and silver contained in our end products are generally sold at the prevailing spot market price per ounce at the time of sale. Concentrates produced by the San José mine are provisionally priced, whereby the selling price is subject to final adjustments at the end of a period ranging from 30 to 90 days after delivery to the customer. The final price is based on the market price of the contained metals at the relevant quotation period stipulated in the contract. Due to the time elapsed between shipment and the final settlement with the buyer, MSC estimates the prices at which sales of metals will be settled. At the end of each financial reporting period, previously recorded provisional sales are adjusted to estimated settlement metals prices based on relevant forward market prices until final settlement with the buyer.

During 2025, revenues from gold and silver sales were $116.7 million from the Gold Bar Mine Complex, $76.0 million from the Fox Complex, $4.8 million from the El Gallo mine, and $225.2 million from the San José mine on a 49% basis. Revenue from the San José mine is not included in our Consolidated Statements of Operations and Comprehensive (Loss) as we use the equity method of accounting for MSC. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional information regarding production and operating results for our properties, and Item 8. Financial Statements and Supplementary Data, Note 2, Summary of Significant Accounting Policies—Investments and Note 9, Equity Investments for additional information regarding the equity method of accounting.

4

Like all metal producers, our operations are affected by fluctuations in metal prices. The following table presents the annual high, low, and average daily London P.M. Fix prices per ounce for gold and London Fix prices per ounce for silver over the past three years and 2026 to the most recent practical date on the London Bullion Market:

|

|

Gold |

|

Silver |

||||||||||||||

Year |

|

High |

|

Low |

|

Average |

|

High |

|

Low |

|

Average |

||||||

|

|

(in dollars per ounce) |

||||||||||||||||

2023 |

|

$ |

2,078 |

|

|

1,811 |

|

|

1,940 |

|

|

26.03 |

|

|

20.09 |

|

|

23.35 |

2024 |

|

|

2,778 |

|

|

1,985 |

|

|

2,386 |

|

|

34.51 |

|

|

22.08 |

|

|

28.27 |

2025 |

|

|

4,449 |

|

|

2,633 |

|

|

3,431 |

|

|

74.84 |

|

|

29.41 |

|

|

39.99 |

2026 (through March 13, 2026) |

|

|

5,405 |

|

|

4,353 |

|

|

4,930 |

|

|

118.45 |

|

|

71.99 |

|

|

86.87 |

On March 13, 2026, the London P.M. Fix for gold was $5,045 per ounce and the London Fix for silver was $83.70 per ounce.

Processing Methods

At our operations, gold and silver are extracted from mineralized material by either milling or heap leaching depending on, among other things, the amount of gold and silver contained in the material, whether the material is naturally oxidized or not, and the amenability of the material to treatment.

At our Froome mine in Canada, mineralized material from the underground mine is fed to a crushing plant at the mine site and the crushed material is transported to our Stock mill. The final sized product is then leached with cyanide, and gold-cyanide in solution is recovered to activated carbon. The gold is stripped from the carbon and recovered with electrowinning cells, after which the gold is poured into doré bars.

At the Gold Bar mine and the previously operating El Gallo mine, both open pit operations, mineralized material is processed using heap leaching methods. Heap leaching consists of stacking crushed, oxidized material on impermeable pads, where a diluted cyanide solution is applied to the surface of the heap to extract the contained gold and silver content. The gold and silver-bearing solution is then recovered through adsorption onto activated carbon, followed by desorption, electrowinning, retorting and finally smelting into doré bars.

At the San José mine, mineralized material from the underground mine is processed initially using a conventional crushing-grinding-flotation mill. A portion of the flotation concentrate is cyanide leached followed by an electrowinning, which produces a precipitate. This precipitate is then smelted and poured into silver and gold doré bars. The remainder of the concentrate is shipped to third-party smelters for toll processing.

Proven and Probable Mineral Reserves

We had attributable estimated proven and probable gold reserves of 0.3 million ounces of gold at our Gold Bar mine and the San José mine, and 5.2 million ounces of proven and probable silver reserves at the San José mine and 4.7 billion pounds (Blbs) of proven and probable copper reserves at Los Azules at December 31, 2025.

A “mineral reserve” is an estimate of tonnage and grade or quality of measured and indicated mineral resources that, in the opinion of the qualified person, can be the basis of an economically viable project. More specifically, it is the economically mineable part of a measured or indicated mineral resource, which includes diluting materials and allowances for losses that may occur when the material is mined or extracted. The term “economically viable,” as used in the definition of reserve, means that the qualified person has analytically determined that extraction of the mineral reserve is economically viable under reasonable investment and market assumptions.

5

The term “proven reserves” means the economically mineable part of a measured mineral resource and can only result from conversion of a measured mineral resource. The term “probable reserves” means reserves for which quantity and grade are computed from information similar to that used for proven reserves, but the sites for sampling are farther apart or are otherwise less closely spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation. Proven and probable reserves include gold and silver attributable to our ownership or economic interest.

The proven and probable reserve figures presented herein are estimates based on information available at the time of calculation. No assurance can be given that the indicated levels of recovery of gold or silver will be realized. Reserve estimates may require revision based on actual production. Market fluctuations in the price of gold or silver, as well as increased production costs or reduced metallurgical recovery rates, could render certain proven and probable reserves containing higher cost reserves uneconomic to exploit and might result in a reduction of reserves.

Proven and probable reserves are based on extensive drilling, sampling, mine modeling, and metallurgical testing from which we determined economic feasibility. The price sensitivity of reserves depends upon several factors including grade, metallurgical recovery, operating cost, waste-to-ore ratio, and ore type. Metallurgical recovery rates vary depending on the metallurgical properties of each deposit and the production process used.

Proven and probable reserves disclosed at December 31, 2025, and 2024 have been prepared in accordance with Regulation S-K 1300.

The following tables summarize the estimated proven and probable gold, silver and copper reserves attributable to our ownership or economic interest as of December 31, 2025:

|

Gold Reserves at December 31, 2025 |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Tonnes |

Gold |

Gold |

|

Tonnes |

Gold |

Gold |

|

Tonnes |

Gold |

Gold |

|

(kt) |

(g/t) |

(koz) |

|

(kt) |

(g/t) |

(koz) |

|

(kt) |

(g/t) |

(koz) |

Gold Bar mine (1) |

— |

— |

— |

|

8,624 |

0.61 |

168.0 |

|

8,624 |

0.61 |

168.0 |

San José mine (2) |

494 |

3.72 |

59.1 |

|

358 |

3.69 |

42.5 |

|

852 |

3.71 |

101.6 |

|

Silver Reserves at December 31, 2025 |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Tonnes |

Silver |

Silver |

|

Tonnes |

Silver |

Silver |

|

Tonnes |

Silver |

Silver |

|

(kt) |

(g/t) |

(Moz) |

|

(kt) |

(g/t) |

(Moz) |

|

(kt) |

(g/t) |

(Moz) |

San José mine (2) |

494 |

199.00 |

3.2 |

|

358 |

175.00 |

2.0 |

|

852 |

189.00 |

5.2 |

|

Copper Reserves at December 31, 2025 |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Tonnes |

Cu |

Cu |

|

Tonnes |

Cu |

Cu |

|

Tonnes |

Cu |

Cu |

|

(kt) |

(%) |

(Mlbs) |

|

(kt) |

(%) |

(Mlbs) |

|

(kt) |

(%) |

(Mlbs) |

Los Azules (3) |

106,434 |

0.683 |

1,603 |

|

367,239 |

0.386 |

3,127 |

|

473,673 |

0.453 |

4,730 |

| (1) | The reserve estimate for the Gold Bar mine as at December 31, 2025 was prepared by Independent Mining Consultants. |

| (2) | The reserve estimate for the San José mine as at December 31, 2025, presented on a 49% basis, was prepared by Hochschild and audited by P&E Mining Consultants Inc. (“P&E”). |

| (3) | The reserve estimate for Los Azules as at December 31, 2025, presented on a 46.3%, was prepared by AGP Mining Consultants. |

6

The following tables summarize the estimated proven and probable gold and silver reserves attributable to our ownership or economic interest as of December 31, 2024:

|

Gold Reserves at December 31, 2024 |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Tonnes |

Gold |

Gold |

|

Tonnes |

Gold |

Gold |

|

Tonnes |

Gold |

Gold |

|

(kt) |

(g/t) |

(koz) |

|

(kt) |

(g/t) |

(koz) |

|

(kt) |

(g/t) |

(koz) |

Gold Bar mine (1) |

— |

— |

— |

|

10,852 |

0.64 |

222.0 |

|

10,852 |

0.64 |

222.0 |

San José mine (2) |

343 |

4.72 |

52.1 |

|

215 |

5.50 |

38.0 |

|

558 |

5.02 |

90.1 |

|

Silver Reserves at December 31, 2024 |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Tonnes |

Silver |

Silver |

|

Tonnes |

Silver |

Silver |

|

Tonnes |

Silver |

Silver |

|

(kt) |

(g/t) |

(Moz) |

|

(kt) |

(g/t) |

(Moz) |

|

(kt) |

(g/t) |

(Moz) |

San José mine (2) |

343 |

295.00 |

3.3 |

|

215 |

272.00 |

1.9 |

|

558 |

286.00 |

5.1 |

|

Copper Reserves at December 31, 2024 |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Tonnes |

Cu |

Cu |

|

Tonnes |

Cu |

Cu |

|

Tonnes |

Cu |

Cu |

|

(kt) |

(%) |

(Mlbs) |

|

(kt) |

(%) |

(Mlbs) |

|

(kt) |

(%) |

(Mlbs) |

Los Azules |

— |

— |

— |

|

— |

— |

— |

|

— |

— |

— |

| (1) | The reserve estimate for the Gold Bar mine Complex as at December 31, 2024, was prepared by Independent Mining Consultants. |

| (2) | The reserve estimate for the San José mine as at December 31, 2024, presented on a 49% basis, was prepared by Hochschild and audited by P&E. |

The following table is a variance of the mineral reserves from December 31, 2024 to December 31, 2025:

|

Gold Reserves |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Mass % |

Au Grade % |

Metal % |

|

Mass % |

Au Grade % |

Metal % |

|

Mass % |

Au Grade % |

Metal % |

Gold Bar mine |

— |

— |

— |

|

(21) |

(5) |

(24) |

|

(21) |

(5) |

(24) |

San José mine |

44 |

(21) |

14 |

|

67 |

(33) |

12 |

|

53 |

(26) |

13 |

|

Silver Reserves |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Mass % |

Ag Grade % |

Metal % |

|

Mass % |

Ag Grade % |

Metal % |

|

Mass % |

Ag Grade % |

Metal % |

San José mine |

44 |

(33) |

(3) |

|

67 |

(36) |

5 |

|

53 |

(34) |

2.0 |

|

Copper Reserves |

||||||||||

|

Proven |

|

Probable |

|

Proven and Probable |

||||||

|

Mass % |

Ag Grade % |

Metal % |

|

Mass % |

Ag Grade % |

Metal % |

|

Mass % |

Ag Grade % |

Metal % |

|

(kt) |

(%) |

(Mlbs) |

|

(kt) |

(%) |

(Mlbs) |

|

(kt) |

(%) |

(Mlbs) |

Los Azules (1) |

— |

— |

— |

|

— |

— |

— |

|

— |

— |

— |

| (1) | A mineral reserve estimate for Los Azules was not reported as at December 31, 2024. |

7

Notes to the 2025 Mineral Reserve tables

Gold Bar mine

Mineral reserves equal the total ore planned for processing from the mine plan based on a $2,750/oz gold price. Mineral reserves are based on the following economic input parameters: $6.17 per average ore tonne mining cost, $4.67 per average waste tonne mining cost, $5.41 per ore tonne crushed process cost, $2.57 per average ore tonne run-of-mine (“ROM”) process cost, $4.24 per average ore tonne general and administrative (“G&A”) cost, $0.475/oz gold refining charge, $1.538/oz transport & sales cost, 99.95% payable gold, a 1% royalty at Gold Bar South and Hunter and a 2% royalty at Cabin. Hunter and Cabin are not included within the stated Reserve Estimate.

The stated mineral reserves are based on a variable cut-off grade (“COG”) based on rock type, mining area, carbon content, clay content and process response. The grades reported from Pick, Ridge and Gold Bar South block models includes adequate mining dilution allowance within the block estimate; therefore, no additional mining dilution was applied. Mineral reserves are contained within an engineered pit design based on the end of December 2025 topography.

The metal price used $2,750/oz for mineral reserves reflects a conservative combination of a recent trailing average sourced from Kitco’s Historic Price data and a consensus forecast via Bloomberg. Recoveries are variable and as follows: 86% crushed oxide recovery at Pick, 90% at Cabin and 78% at Ridge, 50% mid-carbon recovery at Pick, Ridge and Cabin, 79% ROM oxide recovery at Pick, 72% at Ridge, 75% at GBS, 0% ROM mid-carbon recovery. COGs are variable and based on the presence or not of clay content, carbon content and recoveries and range from 0.09 g/t (0.0027 o/t) to 0.71 g/t 0.0206 o/t. The reference point for the mineral reserves is at the primary crusher.

The following changes have impacted mineral reserves during 2025: mining depletion at Pick and Gold Bar South; operating costs increased largely driven by an increase in mining costs; revised interpretation of the mineralization and geological model, an increase to the reserve metal price, project costs were re-estimated based on current mining activity, current contractor quotes and updated engineered pit designs.

San José mine

Mineral reserves are reported at McEwen’s 49% attributable interest. Hochschild hold a 51% interest in San José.

COG is reported in silver equivalent grams per tonne, calculated using a ratio of 83:1 Ag:Au. For mineral reserves, the silver equivalent COG is: cut & fill 192 g/t silver equivalent, long hole 176 g/t silver equivalent.

Mineral reserves as presented are in place and include average internal dilution of 31%, average mining and geotechnical dilution of 50%, and mine extraction of 45%, but do not include allowances for mill or smelter recoveries. For the 2025 mineral reserves estimate, inaccessible mineral resources that contained insufficient tonnages to permit the development of local infrastructure, mineral resources in mined out/isolated areas, mineral resources located in sill and rib pillars and operationally lost mineral resources were not included in the mineral reserves estimate.

The December 31, 2025 mineral reserves estimate was based on a gold price of $2,750/oz and a silver price of $31/oz. P&E determined that these metal prices are suitable to be utilized for mineral reserve estimation since they are based on recognized consensus forecast metal prices.

Ongoing definition, delineation and mine exploration drilling will lead to better definition of existing resources or extensions of known veins that will be reflected on the year-on-year comparison of both mineral reserves. Mine depletion, commodity price changes and equivalents leading to cut-off grade changes will also have an effect on the comparative data.

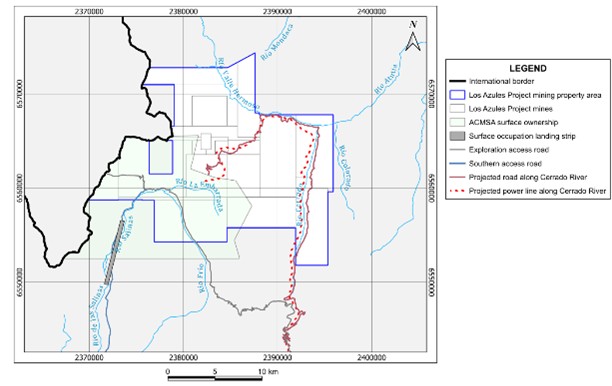

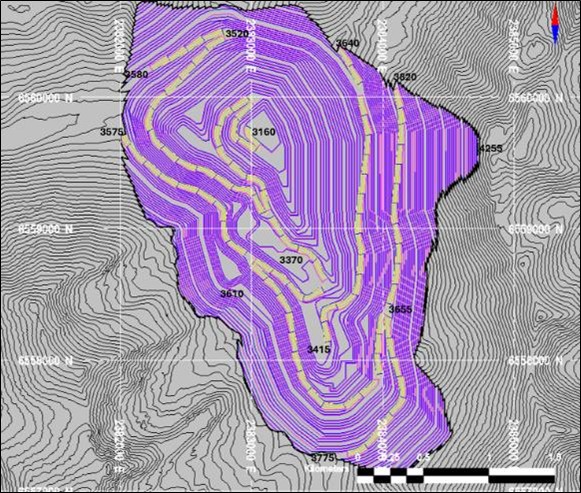

Los Azules

Mineral reserves are reported at McEwen’s 46.3% attributable interest. Only Mineral Resources that were classified as Measured and Indicated were given economic attributes in the mine design and when demonstrating economic viability.

8

Cut-off is variable and ranges from $4.79/t NSR to $7.23/t NSR. Mineral Reserves incorporate appropriate mining dilution and mining recovery estimations for the open pit mining method. The reference point at which the Mineral Reserves are defined is the point where the ore is delivered to the processing plant and include diluting materials and allowances for mine losses, which occur when the material is mined.

The December 31, 2025 mineral reserves estimate was based on a copper price of $4.25/lb of copper. McEwen Copper determined that the metal price is suitable to be utilized for mineral reserve estimation since it is based on recognized consensus forecast metal prices. Copper recovery varies by lithology. Mining costs vary by bench with a minimum of $2.142/t and a maximum of $4.113/t. Processing costs are variable and range from $3.183/t to $5.620/t leached. The processing costs include: $1.607/t G&A, $0.433/t leached sustaining capital, and $0.15/t leached closure cost. Copper cathode sales cost is $0.02/lb Cu. Copper cathode was assumed to be sold FOB the mine site.

Measured, Indicated, and Inferred Mineral Resources

We had attributable estimated measured and indicated mineral resources of 3.93 million ounces of gold, 35.1 million ounces of silver, and 1.1 million tonnes (or 2.52 billion pounds) of copper at December 31, 2025. We had attributable estimated inferred mineral resources of 3.86 million ounces of gold, 79.1 million ounces of silver, and 4.2 million tonnes (or 9.3 billion pounds) of copper at December 31, 2025.

The measured, indicated, and inferred resource figures presented herein are estimates based on information available at the time of calculation and are exclusive of reserves. A “mineral resource” is a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade, or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. The reference point for mineral resources is in situ. Mineral resources are sub-divided, in order of increasing geological confidence, into inferred, indicated and measured categories. Ounces of gold and silver or pounds of copper included in the measured, indicated and inferred resources are those contained prior to losses during metallurgical treatment. The terms "measured resource," "indicated resource," and "inferred resource" mean that part of a mineral resource for which quantity and grade or quality are estimated on the basis of geological evidence and sampling that is considered to be comprehensive, adequate, or limited, respectively. We publish measured, indicated and inferred resources annually, considering metal prices, changes, if any, to future production and capital costs, divestments and depletion as well as any acquisitions and additions. Measured, indicated, and inferred resources disclosed at December 31, 2025, have been prepared in accordance with Regulation S-K 1300 requirements of the SEC.

The following tables summarize measured, indicated and inferred resources, exclusive of reserves attributable to our ownership or economic interest, by operating segment, as of December 31, 2025, and December 31, 2024:

Canada

Mineral resources, exclusive of reserves, as at December 31, 2025:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG Au (g/t) |

Met Rec (%) |

Froome mine |

212 |

2.45 |

17 |

440 |

2.94 |

42 |

651 |

2.78 |

58 |

302 |

2.93 |

28 |

1.35 |

89.5 |

Grey Fox (1) |

— |

— |

— |

19,474 |

3.02 |

1,892 |

19,474 |

3.02 |

1,892 |

5,101 |

2.66 |

436 |

0.4 / 1.35 (1) |

90 |

Stock West & Main |

— |

— |

— |

3,179 |

2.63 |

268 |

3,179 |

2.63 |

268 |

2,468 |

2.31 |

184 |

1.30 |

93 |

Fuller |

— |

— |

— |

1,552 |

3.86 |

193 |

1,552 |

3.86 |

193 |

970 |

2.93 |

91 |

1.95 |

88 |

Stock East |

— |

— |

— |

1,790 |

2.12 |

122 |

1,790 |

2.12 |

122 |

1,350 |

2.02 |

87 |

1.30 |

93 |

Black Fox |

244 |

3.59 |

28 |

141 |

3.54 |

16 |

385 |

3.57 |

44 |

385 |

2.90 |

36 |

1.35 |

95 |

Davidson Tisdale |

223 |

6.87 |

49 |

69 |

6.70 |

15 |

292 |

6.83 |

64 |

133 |

4.01 |

17 |

1.85 |

92 |

Total |

679 |

4.31 |

94 |

26,645 |

2.97 |

2,548 |

27,323 |

3.01 |

2,641 |

10,709 |

2.55 |

879 |

|

|

| (1) | The cut-off grade for the open pit portion of the resource was 0.4 g/t and for the underground portion was 1.35 g/t. |

9

Mineral resources, exclusive of reserves, as at December 31, 2024:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG Au (g/t) |

Met Rec (%) |

Froome mine |

241 |

3.44 |

27 |

259 |

3.62 |

30 |

500 |

3.53 |

57 |

168 |

3.51 |

19 |

2.05 |

90 |

Grey Fox |

— |

— |

— |

13,135 |

3.64 |

1,538 |

13,135 |

3.64 |

1,538 |

4,319 |

3.30 |

458 |

1.60 |

90 |

Stock West & Main |

— |

— |

— |

1,938 |

3.31 |

206 |

1,938 |

3.31 |

206 |

1,386 |

2.96 |

132 |

1.95 |

93 |

Fuller |

— |

— |

— |

1,552 |

3.86 |

193 |

1,552 |

3.86 |

193 |

970 |

2.93 |

91 |

1.95 |

88 |

Stock East |

— |

— |

— |

866 |

2.70 |

75 |

866 |

2.70 |

75 |

579 |

2.66 |

50 |

1.95 |

93 |

Black Fox |

189 |

4.61 |

28 |

100 |

4.38 |

14 |

288 |

4.53 |

42 |

225 |

3.93 |

28 |

2.00 |

95 |

Davidson Tisdale |

223 |

6.87 |

49 |

69 |

6.70 |

15 |

292 |

6.83 |

64 |

133 |

4.01 |

17 |

1.85 |

92 |

Total |

653 |

4.95 |

104 |

17,919 |

3.59 |

2,071 |

18,571 |

3.64 |

2,175 |

7,780 |

3.18 |

795 |

|

|

United States

Mineral resources, exclusive of reserves, as at December 31, 2025:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG Au (g/t) |

Met Rec (%) |

Gold Bar mine |

— |

— |

— |

9,630 |

0.52 |

162.2 |

9,630 |

0.52 |

162.2 |

1,368 |

0.43 |

19.0 |

0.09 - 0.71 |

var (1) |

Lookout Mountain |

— |

— |

— |

19,570 |

0.64 |

402.3 |

19,570 |

0.64 |

402.3 |

7,292 |

0.57 |

134.2 |

0.17 - 1.71 |

75-78 |

Total |

— |

— |

— |

29,200 |

0.60 |

565 |

29,200 |

0.60 |

565 |

8,660 |

0.55 |

153 |

|

|

| (1) | 86% crushed oxide recovery at Pick & Cabin and 78% at Ridge, 50% mid-carbon recovery at Pick, Ridge, and Cabin, 79% ROM oxide recovery at Pick & Cabin and 72% at Ridge, 75% at GBS Hunter, 0% ROM mid-carbon recovery. |

Mineral resources, exclusive of reserves, as at December 31, 2024:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG Au (g/t) |

Met Rec (%) |

Gold Bar mine |

— |

— |

— |

4,368 |

0.68 |

95.9 |

4,368 |

0.68 |

95.9 |

420 |

0.59 |

7.9 |

0.15 - 0.91 |

var (1) |

Lookout Mountain |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

Total |

— |

— |

— |

4,368 |

0.68 |

95.9 |

4,368 |

0.68 |

95.9 |

420 |

0.59 |

7.9 |

|

|

| (1) | 86% crushed oxide recovery at Pick & Cabin and 78% at Ridge, 0% mid-carbon recovery at Pick, Ridge, and Cabin, 79% ROM oxide recovery at Pick & Cabin and 72% at Ridge, 61% ROM oxide recovery at Gold Bar South & Hunter, and 0% ROM mid-carbon recovery. |

10

Mexico

Mineral resources, exclusive of reserves, as at December 31, 2025:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG |

Met Rec (%) |

El Gallo |

9,000 |

0.51 |

148.0 |

5,700 |

0.27 |

50.0 |

14,700 |

0.42 |

199.0 |

300 |

0.41 |

4.0 |

var (1) |

var (2) |

Total |

9,000 |

0.51 |

148.0 |

5,700 |

0.27 |

50.0 |

14,700 |

0.42 |

199.0 |

300 |

0.41 |

4.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Silver |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

COG |

Met Rec (%) |

El Gallo |

9,000 |

19.00 |

5.6 |

5,700 |

79.00 |

14.5 |

14,700 |

42.00 |

20.0 |

300 |

33.00 |

0.3 |

var (1) |

var (2) |

Total |

9,000 |

19.00 |

5.6 |

5,700 |

79.00 |

14.5 |

14,700 |

42.00 |

20.0 |

300 |

33.00 |

0.3 |

|

|

| (1) | The El Gallo mine’s HLM has no COG as the entire heap is processed with zero selectivity. El Gallo Silver’s COG is 58 g/t Ag. |

| (2) | The El Gallo mine’s HLM recoveries are 85% Au and 60% Ag. El Gallo Silver’s recoveries are 86% Au and 75% Ag. |

Mineral resources, exclusive of reserves, as at December 31, 2024:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG |

Met Rec (%) |

El Gallo |

9,000 |

0.51 |

148.0 |

5,700 |

0.27 |

50.0 |

14,700 |

0.42 |

199.0 |

300 |

0.41 |

4.0 |

var (1) |

var (2) |

Total |

9,000 |

0.51 |

148.0 |

5,700 |

0.27 |

50.0 |

14,700 |

0.42 |

199.0 |

300 |

0.41 |

4.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Silver |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

COG |

Met Rec (%) |

El Gallo |

9,000 |

19.00 |

5.6 |

5,700 |

79.00 |

14.5 |

14,700 |

42.00 |

20.0 |

300 |

33.00 |

0.3 |

var (1) |

var (2) |

Total |

9,000 |

19.00 |

5.6 |

5,700 |

79.00 |

15.0 |

14,700 |

42.00 |

20.0 |

300 |

33.00 |

0.3 |

|

|

| (1) | The El Gallo mine’s HLM has no COG as the entire heap is processed with zero selectivity. El Gallo Silver’s COG is 58 g/t Ag. |

| (2) | The El Gallo mine’s HLM recoveries are 85% Au and 60% Ag. El Gallo Silver’s recoveries are 86% Au and 75% Ag. |

MSC

Mineral resources, exclusive of reserves, as at December 31, 2025:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG AgEq (g/t) |

Met Rec (%) |

San José (49% attrib.) |

270 |

2.93 |

25.5 |

203 |

1.93 |

12.6 |

473 |

2.50 |

38.0 |

1,306 |

3.81 |

160.0 |

186.00 |

90 |

Total |

270 |

2.93 |

25.5 |

203 |

1.93 |

12.6 |

473 |

2.50 |

38.0 |

1,306 |

3.81 |

160.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Silver |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

COG AgEq (g/t) |

Met Rec (%) |

San José (49% attrib.) |

270 |

202.00 |

1.8 |

203 |

126.00 |

0.8 |

473 |

169.00 |

2.6 |

1,306 |

222.00 |

9.3 |

186.00 |

90 |

Total |

270 |

202.00 |

1.8 |

203 |

126.00 |

0.8 |

473 |

169.00 |

2.6 |

1,306 |

222.00 |

9.3 |

|

|

11

Mineral resources, exclusive of reserves, as at December 31, 2024:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG AgEq (g/t) |

Met Rec (%) |

San José (49% attrib.) |

283 |

3.65 |

33.2 |

296 |

3.43 |

32.7 |

580 |

3.54 |

66.0 |

1,119 |

4.59 |

165.2 |

217.00 |

90 |

Total |

283 |

3.65 |

33.2 |

296 |

3.44 |

32.7 |

580 |

3.54 |

66.0 |

1,119 |

4.59 |

165.2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Silver |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

COG AgEq (g/t) |

Met Rec (%) |

San José (49% attrib.) |

283 |

181.00 |

1.6 |

296 |

120.00 |

1.1 |

580 |

150.00 |

2.8 |

1,119 |

252.00 |

9.1 |

217.00 |

90 |

Total |

283 |

181.00 |

1.6 |

296 |

120.00 |

1.1 |

580 |

150.00 |

2.8 |

1,119 |

252.00 |

9.1 |

|

|

McEwen Copper

Mineral resources, exclusive of reserves, as at December 31, 2025:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG Cu (%) |

Met Rec (%) |

Los Azules (46.3% attrib.) |

4,739 |

0.06 |

8.6 |

325,629 |

0.05 |

473.9 |

330,369 |

0.05 |

482.5 |

1,962,800 |

0.04 |

2,659.4 |

var NSR |

var. |

Total |

4,739 |

0.06 |

8.6 |

325,629 |

0.05 |

473.9 |

330,369 |

0.05 |

482.5 |

1,962,800 |

0.04 |

2,659.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Silver |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

COG Cu (%) |

Met Rec (%) |

Los Azules (46.3% attrib.) |

4,739 |

1.81 |

0.3 |

325,629 |

1.15 |

12.0 |

330,369 |

0.86 |

12.3 |

1,962,800 |

1.10 |

69.4 |

var NSR |

var. |

Total |

4,739 |

1.81 |

0.3 |

325,629 |

1.15 |

12.0 |

330,369 |

0.86 |

12.3 |

1,962,800 |

1.10 |

69.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Copper |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

COG Cu (%) |

Met Rec (%) |

Los Azules (46.3% attrib.) |

6,389 |

0.16 |

0.02 |

440,619 |

0.26 |

2.5 |

447,007 |

0.26 |

2.5 |

1,962,800 |

0.21 |

9.2 |

var NSR |

var. |

Total |

6,389 |

0.16 |

0.02 |

440,619 |

0.26 |

2.5 |

447,007 |

0.26 |

2.5 |

1,962,800 |

0.21 |

9.2 |

|

|

Mineral resources, exclusive of reserves, as at December 31, 2024:

Gold |

Measured |

Indicated |

Measured & Indicated |

Inferred |

|

|

||||||||

|

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

Tonnes (000s) |

Au Grade (g/t) |

Contained Au (000s oz) |

COG Cu (%) |

Met Rec (%) |

Los Azules (46.4% attrib.) |

— |

— |

— |

135,070 |

0.05 |

208.8 |

135,070 |

0.05 |

208.8 |

1,769,500 |

0.03 |

1,967.4 |

var NSR |

var. |

Total |

— |

— |

— |

135,070 |

0.05 |

208.8 |

135,070 |

0.05 |

208.8 |

1,769,500 |

0.03 |

1,967.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Silver |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

Tonnes (000s) |

Ag Grade (g/t) |

Contained Ag (Moz) |

COG Cu (%) |

Met Rec (%) |

Los Azules (46.4% attrib.) |

— |

— |

— |

135,070 |

1.07 |

4.6 |

135,070 |

1.07 |

4.6 |

1,769,500 |

1.22 |

69.2 |

var NSR |

var. |

Total |

— |

— |

— |

135,070 |

1.07 |

4.6 |

135,070 |

1.07 |

4.6 |

1,769,500 |

1.22 |

69.2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Copper |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

Tonnes (000s) |

Cu Grade (%) |

Contained Cu (Blbs) |

COG Cu (%) |

Met Rec (%) |

Los Azules (46.4% attrib.) |

— |

— |

— |

573,179 |

0.40 |

5.1 |

573,179 |

0.40 |

5.1 |

2,092,315 |

0.27 |

12.4 |

var NSR |

var. |

Total |

— |

— |

— |

573,179 |

0.40 |

5.1 |

573,179 |

0.40 |

5.1 |

2,092,315 |

0.27 |

12.4 |

|

|

12

The following table is a variance of the mineral resources from December 31, 2024 to December 31, 2025:

Property |

Measured |

Indicated |

Measured & Indicated |

Inferred |

||||||||

|

Mass % |

Grade % |

Metal % |

Mass % |

Grade % |

Metal % |

Mass % |

Grade % |

Metal % |

Mass % |

Grade % |

Metal % |

Froome mine |

(12.03) |

(28.78) |

(37.04) |

69.88 |

(18.78) |

40.00 |

30.20 |

(21.25) |

1.75 |

79.76 |

(16.52) |

47.37 |

Grey Fox |

— |

— |

— |

48.26 |

(17.03) |

23.02 |

48.26 |

(17.03) |

23.02 |

18.11 |

(19.39) |

(4.80) |

Stock West & Main |

— |

— |

— |

64.04 |

(20.54) |

30.10 |

64.04 |

(20.54) |

30.10 |

78.07 |

(21.96) |

39.39 |

Fuller |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

Stock East |

— |

— |

— |

106.70 |

(21.48) |

62.67 |

106.70 |

(21.48) |

62.67 |

133.16 |

(24.06) |

74.00 |

Gold Bar mine |

— |

— |

— |

120.47 |

(23.53) |

69.13 |

120.47 |

(23.53) |

69.13 |

225.71 |

(27.12) |

140.51 |

Lookout Mountain |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

El Gallo (Gold) |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

El Gallo (Silver) |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

San José mine (Gold) |

(4.59) |

(19.73) |

(23.28) |

(31.42) |

(43.73) |

(61.46) |

(18.45) |

(29.38) |

(42.40) |

16.71 |

(16.99) |

(3.12) |

San José mine (Silver) |

(4.59) |

11.60 |

12.50 |

(31.42) |

5.00 |

(27.27) |

(18.45) |

12.67 |

(7.14) |

16.71 |

(11.90) |

2.20 |

Los Azules (Gold) |

— |

— |

— |

141.08 |

(5.86) |

126.96 |

144.59 |

(5.53) |

131.06 |

10.92 |

21.87 |

35.18 |

Los Azules (Silver) |

— |

— |

— |

141.08 |

7.54 |

159.25 |

144.59 |

(19.59) |

165.20 |

10.92 |

(9.53) |

0.35 |

Los Azules (Copper) |

— |

— |

— |

(23.13) |

(36.36) |

(50.87) |

(22.01) |

(36.70) |

(50.43) |

(6.19) |

(20.47) |

(25.39) |

Others |

13.35 |

(11.80) |

— |

24.26 |

(14.00) |

6.90 |

16.72 |

(12.70) |

1.89 |

44.69 |

(18.60) |

17.78 |

Notes to the 2025 Mineral Resource tables

Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no certainty that any part of the mineral resources estimated will be converted into a mineral reserve estimate. The numbers in the tables have been rounded to reflect the accuracy of the estimates and may not sum due to rounding. The inferred mineral resource in these estimates has a lower level of confidence than that applied to an indicated mineral resource and must not be converted to a mineral reserve. It is reasonably expected that the majority of the inferred mineral resource could be upgraded to an indicated mineral resource with continued exploration.

Underground mineral resources include the ‘must take’ minor material below cut-off grade within the potentially mineable shape optimizer stopes that are generated by above-cut-off grade blocks.

Canada

Mineral resources for the Froome mine are reported above an economic cut-off grade of 1.35 g/t gold assuming underground extraction methods and based on a mining cost of C$84.59/t, milling cost of C$43.48/t, G&A cost of C$21.70/t, metallurgical recovery of 89.5%, royalty of C$9.72/t, dilution of 15%, and gold price of $3,000/oz.

Mineral resources for Grey Fox are reported for underground extraction methods above an economic cut-off grade of 1.35 g/t gold based on a mining cost of C$91.42/t, milling cost of C$41.54/t, G&A cost of C$22.41/t, metallurgical recovery of 90%, variable NSR royalties of c.2.45%, dilution of 15%, and gold price of $3,000/oz. Open pit mineral resources for Grey Fox are reported above an economic cut-off grade of 0.4g/t gold based on a mining cost of U$3.38/t, milling cost of U$31.16/t, metallurgical recovery of 90%, variable NSR royalties of c.2.45%, dilution of 8%, and gold price of $3,000/oz.

Mineral resources for the Stock project (West and Main zones) are reported above an economic cut-off grade of 1.30 g/t gold assuming underground extraction methods and based on a mining cost of C$84.59/t, milling cost of C$43.48/t, G&A cost of C$27.67/t, metallurgical recovery of 93%, dilution of 15%, and gold price of $3,000/oz.

Mineral resources for Fuller are reported above an economic cut-off grade of 1.95 g/t gold assuming underground extraction methods and based on a mining cost of C$99.9/t, milling cost of C$34.62/t, G&A cost of C$11.65/t, metallurgical recovery of 88%, 10% Net Profits Interest royalty, dilution of 15% and gold price of $2,000/oz.

Mineral resources for Davidson Tisdale are reported above an economic cut-off grade of 1.85 g/t gold assuming underground extraction methods and based on a mining cost of C$99.9/t, milling cost of C$33.60/t, G&A cost of C$11.65/t, metallurgical recovery of 92%, dilution of 15% and gold price of $2,000/oz.

Mineral resources for Black Fox are reported above an economic cut-off grade of 1.35 g/t gold assuming underground extraction methods and based on a mining cost of C$84.59/t, milling cost of C$43.48/t, G&A cost of C$27.67/t, metallurgical recovery of 95%, dilution of 15% and gold price of $3,000/oz.

13

Mineral resources for the Stock project (East zone) are reported above an economic cut-off grade of 1.30 g/t gold assuming underground extraction methods and based on a mining cost of C$84.59/t, milling cost of C$43.48/t, G&A cost of C$27.67/t, metallurgical recovery of 93%, and gold price of $3,000/oz.

The gold price used in estimating mineral resources of $3,000 was based on a combination of the trailing average from 2022 to 2025 and long-term consensus pricing forecasts for 2026 and 2027. Resources are stated as in-situ. In addition, underground constraining shapes were used to better define reasonable prospects for eventual economic extraction. The Froome and Black Fox mines, the Stock project, and Grey Fox mineral resources used improvements to modeling and estimation methodology and updates based on drilling and chip sampling results. The Froome and Black Fox mines also included changes due to mining depletion. Davidson Tisdale and Fuller estimates remained as last year with no updates.

United States

Mineral resources for the Gold Bar mine are based on the following economic input parameters: $6.17 per average ore tonne mining cost, $4.67 per average waste tonne mining cost, $5.41 per ore tonne crushed process cost, $2.57 per average ore tonne run-of-mine (“ROM”) process cost, $4.24 per average ore tonne general and administrative (“G&A”) cost, $0.475/oz gold refining charge, $1.538/oz transport & sales cost, 99.95% payable gold, a 1% royalty (Gold Bar South and Hunter) and a 2% royalty at Cabin. Mineral resources stated are contained within a $3,000/oz gold sales price Lerchs-Grossmann pits based on end of December 2025 topography.

The gold price used in estimating mineral resources of $3,000 was based on the trailing average from 2022 to 2025 and long-term consensus pricing forecasts for 2026 and 2027. Resources are reported as in-situ. Recoveries are variable and as follows: 86% crushed oxide recovery at Pick, 90% at Cabin and 78% at Ridge, 50% mid-carbon recovery at Pick, Ridge and Cabin, 79% ROM oxide recovery at Pick, 90% at Cabin, 72% at Ridge, 75% at GBS & Hunter, 0% ROM mid-carbon recovery. Cut-off grades are variable and based on the presence or not of clay content, carbon content and recoveries.

Changes in mineral resources are due to mining depletion during 2025 at Pick and Gold Bar South, updated metal price, and updated block models at Pick based on new drilling results. The following changes have impacted the project mineral resources: operating costs increase largely driven by an increase in mining costs; project costs were re-estimated based on current mining activity and new contractor quotes; an update to the mining schedule based on the costs.

Mineral resources for Lookout Mountain are reported above economic cut-off grades of 0.17 g/t (0.005 o/t) for oxide and 1.71 g/t (0.050 o/t) for unoxidized material assuming open pit extraction methods and based on an ore mining cost of $4.29/tonne, waste mining cost of $3.10/tonne, processing costs of $5.43/tonne (oxide), toll milling costs $22.05/tonne (unoxidized), G&A cost of $4.41/tonne, refining cost of $0.48/oz, NSR royalty of 4%, metallurgical recovery of 78% (leached oxide) 75% (unoxidized toll milling) and gold price of $3,000/oz.

Mexico

Gold and silver mineral resources were calculated using metal prices of $1,300/oz and $16/oz, respectively. These prices were based off the 3-year trailing average of the London Closing Fix for 2017 to 2019 ($1,306/oz and $16.32/oz) sourced from Kitco’s Historical Data charts.

Mineral resources are stated as in situ for El Gallo Silver, and as crushed and stacked, ready for hauling and processing for the El Gallo HLM.

El Gallo Silver: Milling recovery assumptions of 86% (sulfide) and 75% (oxide) for silver and 86% gold. Mining costs of $1.95/t, processing and G&A costs of $26.15/t milled were used. Mineral resources are stated using a cut-off grade of 58 g/t Ag within an optimized pit shell indicating reasonable prospects for eventual economic extraction.

HLM: Because of the unconsolidated nature of the heap leach material, the mine schedule plans to mine the entire heap without the benefit of selectivity. Sub-cut-off leach pad material will inherently have potential acid generating sulfide liabilities if placed in our waste dumps and so it will be prudent to process the entire leach pad and place tailings in a previously mined pit at an overall environmental and economic benefit. Metallurgical recovery assumptions for the HLM are 85% gold and 60% silver.

14

Mineral resources have remained the same as last year as no drilling, mining or irrigation activity has taken place during 2025. There was a minor amount of metal recovered of 1,152 ounces of gold at the operation in 2025.

MSC

Mineral resources are reported at McEwen’s 49% attributable interest. Hochschild has a 51% interest in San José. Mineral resources are in situ.

Cut-off grades are reported in silver equivalent grams per tonne, calculated using a ratio of 83:1 Ag:Au. For mineral resources, the silver equivalent cut-off grades are: 186 g/t silver equivalent.

The December 31, 2025 mineral resource estimate was based on a gold price of $2,900/oz and a silver price of $32/oz. P&E determined that these metal prices are suitable to be utilized for mineral resource estimation since they are based on recognized consensus forecast prices.

Ongoing definition, delineation and mine exploration drilling will lead to better definition of existing resources or extensions of known veins that will be reflected on the year-on-year comparison of both mineral resources. Mine depletion, commodity price changes and equivalents leading to cut-off grade changes will also have an effect on the comparative data.

McEwen Copper

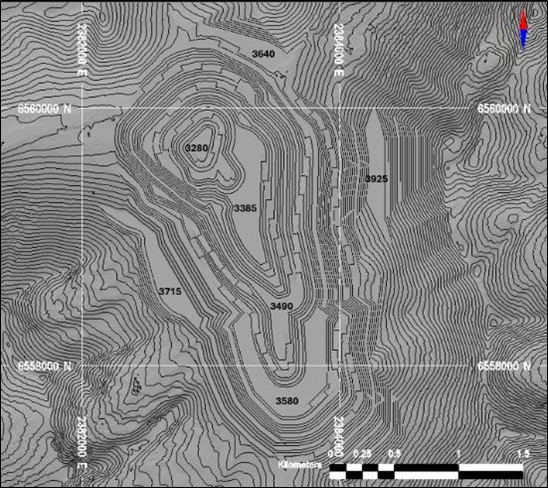

The mineral resources estimate for Los Azules is reported inside of an optimized pit shell demonstrating its reasonable prospects for eventual economic extraction (“RPEEE”). The economic value of each block was calculated based on the metal content, the price of each metal, processing costs, and other downstream costs associated with having a final saleable product. This value is stored for each block of the model as Net Smelter Return (“NSR”) and used to generate an open pit with variable cutoff values to cover the material types and recovery methodology (ranging from $4.79/tonne NSR to $7.23/tonne NSR for the Leach material, $5.13/tonne NSR for Enriched in the mill and $5.11/tonne NSR for Primary in the mill). A copper price of $4.80/lb was used with variable recoveries depending on lithology types for the leach method. With the potential for froth flotation as a recovery method the NSR values were calculated for both high-grade enriched and primary material in a mill. Mineral resources are in-situ and are reported exclusive of reserves at McEwen’s 46.3% attributable interest.

Competitive Business Conditions

We compete with many companies in the mining and mineral exploration and production industry, including large, established mining companies with substantial capabilities, personnel, and financial resources. There is a limited supply of desirable mineral lands available for claim-staking, lease, or acquisition in the United States, Canada, Mexico, Argentina, and other areas where we may conduct our mining or exploration activities. We may be at a competitive disadvantage in acquiring mineral properties, since we compete with these individuals and companies, many of which have significantly greater financial resources and larger technical staffs than we do. From time to time, specific properties or areas that would otherwise be attractive to us for exploration or acquisition may be unavailable due to their previous acquisition by other companies or our lack of financial resources.

Competition in the industry is not limited to the acquisition of mineral properties, but also extends to the technical expertise to find, advance, and operate such properties; the labor to operate the properties; and the capital for the purpose of funding such exploration and development. Many competitors not only explore for and mine precious and base metals but conduct refining and marketing operations on a world-wide basis. Such competition may result in our company not only being unable to acquire desired properties, but to recruit or retain qualified employees or to acquire the capital necessary to fund our operation and advance our properties. Our inability to compete with other companies for these resources would have a material adverse effect on our results of operation, financial condition and cash flows.

15

General Government Regulations

In the United States, Canada, Mexico, and Argentina, we are subject to various governmental laws and regulations, including environmental regulations. Other than operating licenses for our mining and processing facilities and concessions granted under contracts with the host government, there are no third-party patents, licenses or franchises material to our business. The applicable laws and regulations applicable to us include but are not limited to:

| ● | mineral concession rights. |

| ● | surface rights. |

| ● | water rights. |

| ● | mining royalties. |

| ● | environmental laws. |

| ● | mining permits. |

| ● | mining and income taxes. |

| ● | health and safety laws and regulations. |

| ● | labor laws and regulations. |

| ● | export regulations. |

We believe that all of our properties are operated in compliance with all applicable governmental laws and regulations.

Reclamation Obligations

Under applicable laws in the jurisdictions where our properties are located, we are required to reclaim disturbances caused by our mining activities. Accordingly, we have recorded estimates in our financial statements for our reclamation obligations, in accordance with United States Generally Accepted Accounting Principles (“US GAAP” or “GAAP”) the most significant of which are related to our properties in the U.S., Canada, and Mexico.

Estimated future reclamation costs are based primarily on legal and regulatory requirements. As at December 31, 2025, we accrued $45.9 million for reclamation costs relating to currently developed and producing properties. These amounts are included in reclamation and remediation liabilities on Item 8. Financial Statements and Supplementary Data, Consolidated Balance Sheets.

U.S. Environmental Laws

We are subject to extensive environmental regulation under the laws of the U.S. and the state of Nevada, where our U.S. operations are conducted. For example, certain mining wastes resulting from the extraction and processing of ores would be considered hazardous waste under the Resource Conservation and Recovery Act (“RCRA”) and state law equivalents, but such mining wastes are currently excluded from regulation as hazardous waste under Subtitle C of RCRA. If our mine wastes were regulated as hazardous waste under RCRA or if any of our properties were placed on the National Priorities List under the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) or state law equivalents for cleanup, significant expenditures could be required for the construction of additional waste disposal facilities, remediation activities, or natural resource damages. Under CERCLA, any present or past owners or operators of a site may be held jointly and severally liable for investigation and remediation costs and may be required to undertake remedial actions or reimburse the government for its cleanup efforts. Such owners or operators may also be liable to governmental entities for damages to natural resources, which may be substantial. Additional regulations or requirements may also be imposed upon our operations, tailings, and waste disposal areas, as well as upon mine closure, under federal and state environmental laws and regulations, including, without limitation, CERCLA, the Clean Water Act, Clean Air Act, the Safe Drinking Water Act, the Endangered Species Act, and state law equivalents. See Item 8. Financial Statements and Supplementary Data, Note 12, Asset Retirement Obligations, for information on reclamation obligations under governmental environmental laws.

16

We have reviewed and considered current federal legislation relating to climate change and do not believe it to have a material effect on our operations. Future changes in U.S. federal or state laws or regulations could have a material adverse effect upon us and our results of operations.

Foreign Government Regulations

Canada, where the Fox Complex is located, and Mexico, where El Gallo is located, have both adopted laws and guidelines for environmental permitting that are similar to those in effect in the U.S. The permitting process requires a thorough study to determine the baseline condition of the mining site and surrounding area, an environmental impact analysis, and proposed mitigation measures to minimize and offset the environmental impact of exploration and mining operation activities. We have received all permits required to operate our current activities in Canada and Mexico and have received all permits necessary for the exploration activities being conducted at our non-U.S. properties.

Customers

Production from the Gold Bar Mine Complex and the Fox Complex is sold as refined metal on the spot market or doré under the terms set out in doré purchase agreements.