UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): November 11, 2025

HANOVER BANCORP, INC.

(Exact name of registrant as specified in its charter)

Maryland |

001-41384 |

81-3324480 |

(State or other jurisdiction of incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) |

|

|

|

80 East Jericho Turnpike, Mineola, New York |

11501 |

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (516) 548-8500

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading symbol |

Name of each exchange on which registered |

Common stock |

HNVR |

NASDAQ |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 7.01 – Regulation FD Disclosure

On November 11, 2025, representatives of the Registrant will present to various investors the information about the Registrant described in the slides attached to this report as Exhibit 99.1, which are incorporated by reference herein.

The information in Item 7.01 of this report is being furnished, not filed, pursuant to Regulation FD. Accordingly, the information in Item 7.01 of this report will not be incorporated by reference into any registration statement filed by the Registrant under the Securities Act of 1933, as amended, unless specifically identified therein as being incorporated therein by reference. The furnishing of the information in this report is not intended to, and does not, constitute a determination or admission by the Registrant that the information in this report is material or complete, or that investors should consider this information before making an investment decision with respect to any security of the Registrant.

Item 9.01 – Financial Statements and Exhibits

(d) Exhibits

The following Exhibits are furnished as part of this report:

Exhibit |

|

Description |

|

|

|

Exhibit 99.1 |

|

|

Exhibit 104 |

|

Cover Page Interactive Data File (formatted as inline XBRL and contained in Exhibit 101) |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

HANOVER BANCORP, INC. |

|

|

|

|

|

Date: November 11, 2025 |

|

By: |

/s/ Lance P. Burke |

|

|

|

Lance P. Burke |

|

|

|

Executive Vice President & Chief Financial Officer |

|

|

|

(Principal Financial Officer) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Confidential Investor Presentation 1 |

|

2 148, 201, 61 20, 49, 89 Disclaimer (1) The acquisition is subject to applicable regulatory approvals, approval of the Minden shareholders and other customary closing conditions. The private placement is not conditional on the closing of the acquisition. This presentation has been prepared by us solely for informational purposes based on our own information, as well as information from public and industry sources. This presentation does not constitute an offer to sell, nor a solicitation of an offer to buy, any securities by any person in any jurisdiction in which it is unlawful for such person to make such an offering or solicitation. Neither the SEC nor any other regulatory agency has approved or disapproved of our securities or passed upon the accuracy or adequacy of this presentation. Any representation to the contrary is a criminal offense. Our Common Stock is not a deposit account of our bank subsidiary and is not insured by the FDIC or any other governmental agency. Forward-Looking Statements This presentation includes statements that are, or may be deemed, “forward-looking statements.” In some cases, these forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “approximately,” “potential,” “projected,” “pro forma” or, in each case, their negatives or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. Any or all of the forward-looking statements herein made by us may turn out to be incorrect. By their nature, forward-looking statements involve risks and uncertainties because they relate to future events, competitive dynamics, and banking, regulatory, and other developments, and depend on anticipated circumstances that may or may not occur (or may occur on longer or shorter timelines than anticipated). They can be affected by inaccurate assumptions that we might make, or by known or unknown risks and uncertainties, including those discussed in our Annual Report on Form 10-K under Item 1A - Risk Factors, as updated by our subsequent filings with the Securities and Exchange Commission. Forward-looking statements speak only as of the date they are made. Although we believe that we have a reasonable basis for each forward-looking statement contained in this presentation, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition, and liquidity, and the development of the industry in which we operate may differ materially from the forward-looking statements contained in this presentation. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate are consistent with the forward-looking statements contained in this presentation, they may not be predictive of results or developments in future periods. Any forward-looking statements that we make in this presentation speak only as of the respective dates of such statements, and we undertake no obligation to update such statements to reflect events or circumstances after the date of this presentation, except as required by law. Non-GAAP Financial Measures This presentation contains supplemental financial information, which includes the Company’s adjusted net income, adjusted diluted earnings per share, adjusted return on average assets (“Adj. ROAA”), adjusted return on average equity, tangible common equity (“TCE”) ratio, TCE, tangible assets, tangible book value per share, return on average tangible equity (“ROATCE”) and pre-provision net revenue (“PPNR”), determined by methods other than in accordance with accounting principles generally accepted in the United States of America (“GAAP”). Our management uses these non-GAAP measures in its analysis of our performance. These measures should not be considered a substitute for GAAP basis measures nor should they be viewed as a substitute for operating results determined in accordance with GAAP. Management believes that the presentation of non-GAAP financial measures provides both management and investors useful supplemental information that is essential to a proper understanding of our financial condition and results. Non-GAAP measures are not formally defined under GAAP, and other entities may use calculation methods that differ from those used by us. As a complement to GAAP financial measures, our management believes these non-GAAP financial measures assist investors in comparing the financial condition and results of operations of financial institutions due to the industry prevalence of such non-GAAP measures. A reconciliation of our non-GAAP financial measures to the most directly comparable GAAP measures has been provided herein. |

|

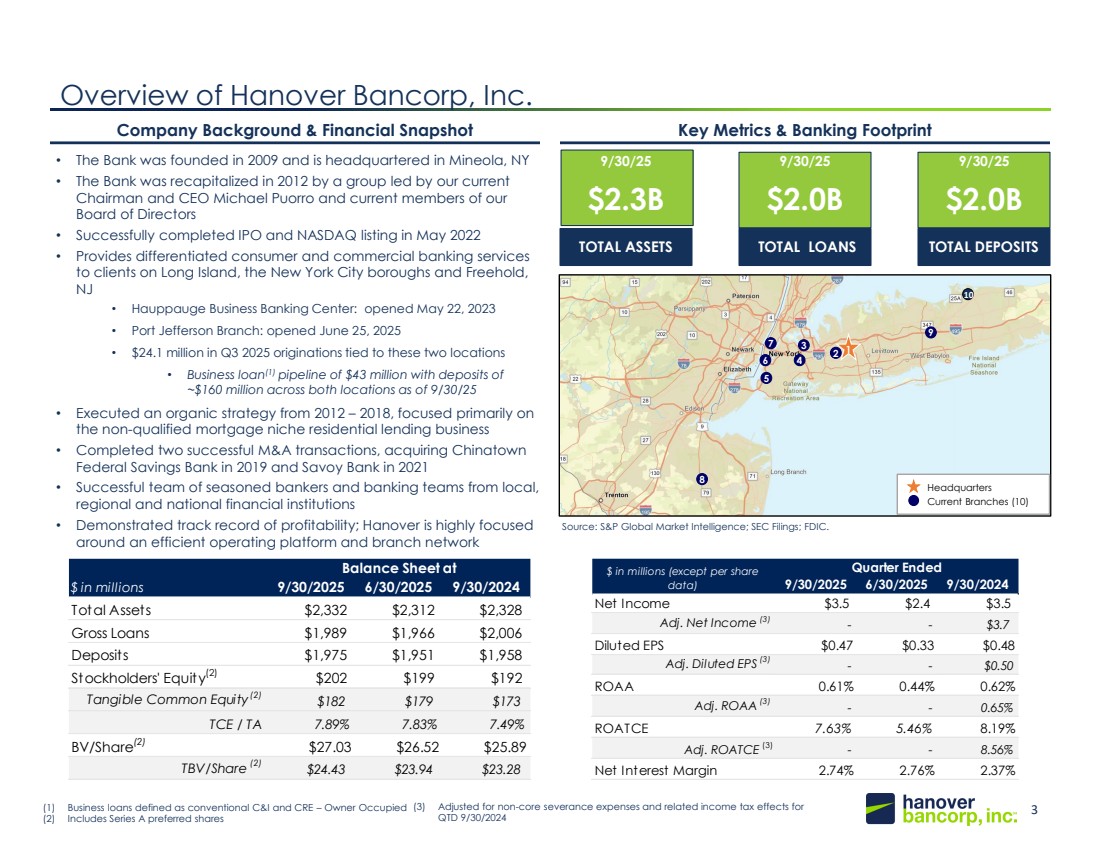

3 148, 201, 61 20, 49, 89 Overview of Hanover Bancorp, Inc. • The Bank was founded in 2009 and is headquartered in Mineola, NY • The Bank was recapitalized in 2012 by a group led by our current Chairman and CEO Michael Puorro and current members of our Board of Directors • Successfully completed IPO and NASDAQ listing in May 2022 • Provides differentiated consumer and commercial banking services to clients on Long Island, the New York City boroughs and Freehold, NJ • Hauppauge Business Banking Center: opened May 22, 2023 • Port Jefferson Branch: opened June 25, 2025 • $24.1 million in Q3 2025 originations tied to these two locations • Business loan(1) pipeline of $43 million with deposits of ~$160 million across both locations as of 9/30/25 • Executed an organic strategy from 2012 – 2018, focused primarily on the non-qualified mortgage niche residential lending business • Completed two successful M&A transactions, acquiring Chinatown Federal Savings Bank in 2019 and Savoy Bank in 2021 • Successful team of seasoned bankers and banking teams from local, regional and national financial institutions • Demonstrated track record of profitability; Hanover is highly focused around an efficient operating platform and branch network Company Background & Financial Snapshot Key Metrics & Banking Footprint 9/30/25 $2.3B TOTAL ASSETS 9/30/25 $2.0B TOTAL LOANS 9/30/25 $2.0B TOTAL DEPOSITS Headquarters Current Branches (10) 9 8 2 3 4 5 6 7 1 10 (1) Business loans defined as conventional C&I and CRE – Owner Occupied (2) Includes Series A preferred shares (3) Adjusted for non-core severance expenses and related income tax effects for QTD 9/30/2024 Source: S&P Global Market Intelligence; SEC Filings; FDIC. $ in millions 9/30/2025 6/30/2025 9/30/2024 Total Assets $2,332 $2,312 $2,328 Gross Loans $1,989 $1,966 $2,006 Deposits $1,975 $1,951 $1,958 Stockholders' Equity(2) $202 $199 $192 Tangible Common Equity(2) $182 $179 $173 TCE / TA 7.89% 7.83% 7.49% BV/Share(2) $27.03 $26.52 $25.89 TBV/Share (2) $24.43 $23.94 $23.28 Balance Sheet at 9/30/2025 6/30/2025 9/30/2024 Net Income $3.5 $2.4 $3.5 Adj. Net Income (3) - - $3.7 Diluted EPS $0.47 $0.33 $0.48 Adj. Diluted EPS (3) - - $0.50 ROAA 0.61% 0.44% 0.62% Adj. ROAA (3) - - 0.65% ROATCE 7.63% 5.46% 8.19% Adj. ROATCE (3) - - 8.56% Net Interest Margin 2.74% 2.76% 2.37% $ in millions (except per share data) Quarter Ended |

|

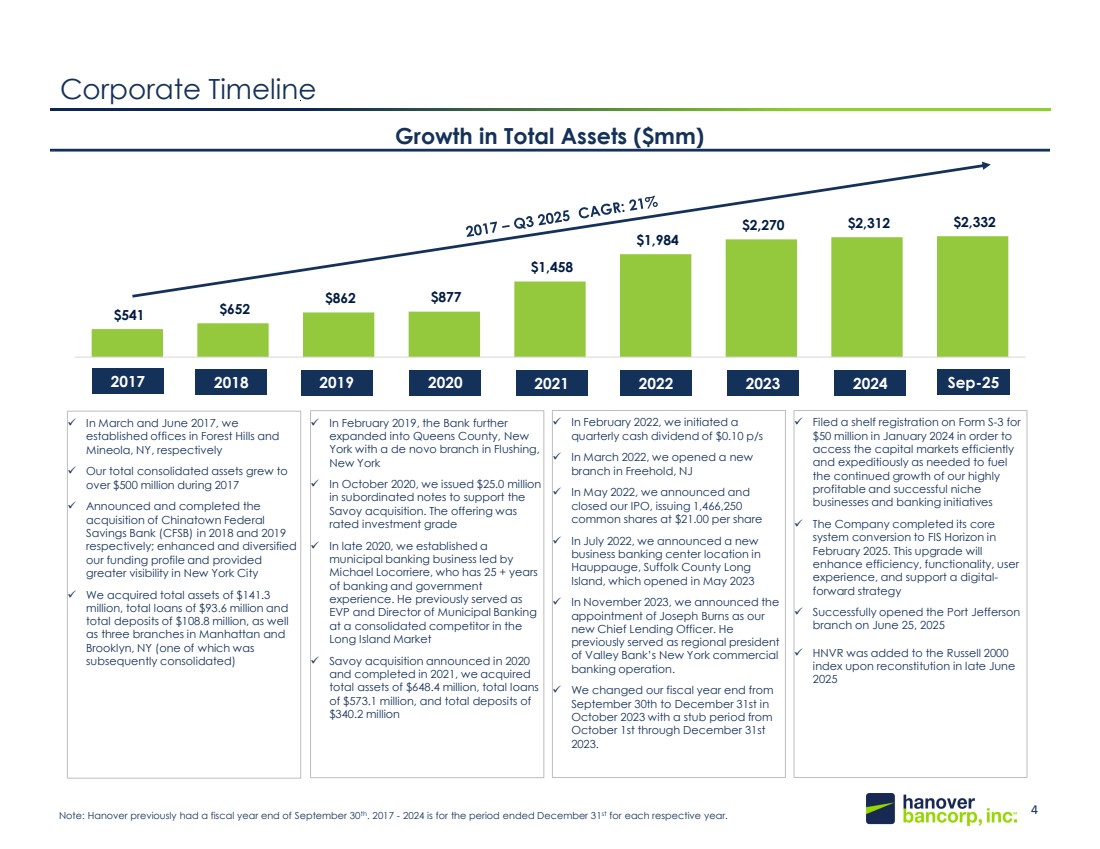

4 148, 201, 61 20, 49, 89 $541 $652 $862 $877 $1,458 $1,984 $2,270 $2,312 $2,332 Corporate Timeline Growth in Total Assets ($mm) Note: Hanover previously had a fiscal year end of September 30th. 2017 - 2024 is for the period ended December 31st for each respective year. ✓ In February 2022, we initiated a quarterly cash dividend of $0.10 p/s ✓ In March 2022, we opened a new branch in Freehold, NJ ✓ In May 2022, we announced and closed our IPO, issuing 1,466,250 common shares at $21.00 per share ✓ In July 2022, we announced a new business banking center location in Hauppauge, Suffolk County Long Island, which opened in May 2023 ✓ In November 2023, we announced the appointment of Joseph Burns as our new Chief Lending Officer. He previously served as regional president of Valley Bank’s New York commercial banking operation. ✓ We changed our fiscal year end from September 30th to December 31st in October 2023 with a stub period from October 1st through December 31st 2023. ✓ In March and June 2017, we established offices in Forest Hills and Mineola, NY, respectively ✓ Our total consolidated assets grew to over $500 million during 2017 ✓ Announced and completed the acquisition of Chinatown Federal Savings Bank (CFSB) in 2018 and 2019 respectively; enhanced and diversified our funding profile and provided greater visibility in New York City ✓ We acquired total assets of $141.3 million, total loans of $93.6 million and total deposits of $108.8 million, as well as three branches in Manhattan and Brooklyn, NY (one of which was subsequently consolidated) ✓ In February 2019, the Bank further expanded into Queens County, New York with a de novo branch in Flushing, New York ✓ In October 2020, we issued $25.0 million in subordinated notes to support the Savoy acquisition. The offering was rated investment grade ✓ In late 2020, we established a municipal banking business led by Michael Locorriere, who has 25 + years of banking and government experience. He previously served as EVP and Director of Municipal Banking at a consolidated competitor in the Long Island Market ✓ Savoy acquisition announced in 2020 and completed in 2021, we acquired total assets of $648.4 million, total loans of $573.1 million, and total deposits of $340.2 million ✓ Filed a shelf registration on Form S-3 for $50 million in January 2024 in order to access the capital markets efficiently and expeditiously as needed to fuel the continued growth of our highly profitable and successful niche businesses and banking initiatives ✓ The Company completed its core system conversion to FIS Horizon in February 2025. This upgrade will enhance efficiency, functionality, user experience, and support a digital-forward strategy ✓ Successfully opened the Port Jefferson branch on June 25, 2025 ✓ HNVR was added to the Russell 2000 index upon reconstitution in late June 2025 2017 2018 2019 2020 2021 2022 2023 2024 Sep-25 |

|

Confidential Investor Presentation 5 Hanover Executive Management Team Note: Throughout the presentation, unless otherwise specified, references to “Hanover” may be to either the holding company or the bank. Name Position with Hanover Age Years of Banking Experience Year Started at Hanover Michael P. Puorro CEO & Chairman 66 35+ 2012 McClelland Wilcox President 53 20+ 2021 Lance P. Burke Exec. VP & Chief Financial Officer 46 25+ 2021 Kevin Corbett Exec. VP & Chief Credit Officer 66 40+ 2020 Joseph F. Burns Exec. VP & Chief Lending Officer 59 35+ 2023 Michael Locorriere Exec. VP & Chief Municipal Officer 57 25+ 2020 Lisa A. Diiorio First Senior VP & Chief Accounting Officer 62 30+ 2016 John P. Vivona First Senior VP & Chief Risk Officer 55 35+ 2023 Raymond Sanchez First Senior VP & Chief Information Officer 59 25+ 2022 |

|

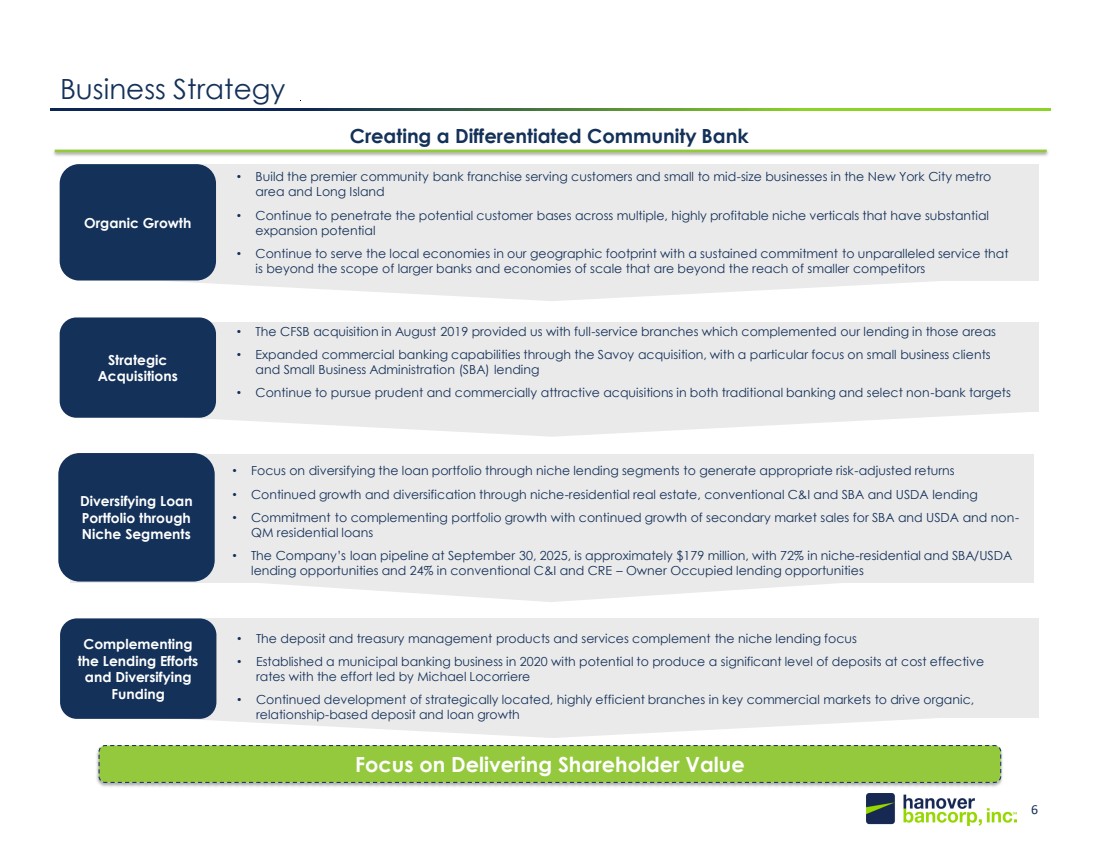

6 148, 201, 61 20, 49, 89 Business Strategy Creating a Differentiated Community Bank Focus on Delivering Shareholder Value Organic Growth • Build the premier community bank franchise serving customers and small to mid-size businesses in the New York City metro area and Long Island • Continue to penetrate the potential customer bases across multiple, highly profitable niche verticals that have substantial expansion potential • Continue to serve the local economies in our geographic footprint with a sustained commitment to unparalleled service that is beyond the scope of larger banks and economies of scale that are beyond the reach of smaller competitors • Focus on diversifying the loan portfolio through niche lending segments to generate appropriate risk-adjusted returns • Continued growth and diversification through niche-residential real estate, conventional C&I and SBA and USDA lending • Commitment to complementing portfolio growth with continued growth of secondary market sales for SBA and USDA and non-QM residential loans • The Company’s loan pipeline at September 30, 2025, is approximately $179 million, with 72% in niche-residential and SBA/USDA lending opportunities and 24% in conventional C&I and CRE – Owner Occupied lending opportunities Diversifying Loan Portfolio through Niche Segments • The deposit and treasury management products and services complement the niche lending focus • Established a municipal banking business in 2020 with potential to produce a significant level of deposits at cost effective rates with the effort led by Michael Locorriere • Continued development of strategically located, highly efficient branches in key commercial markets to drive organic, relationship-based deposit and loan growth Complementing the Lending Efforts and Diversifying Funding Strategic Acquisitions • The CFSB acquisition in August 2019 provided us with full-service branches which complemented our lending in those areas • Expanded commercial banking capabilities through the Savoy acquisition, with a particular focus on small business clients and Small Business Administration (SBA) lending • Continue to pursue prudent and commercially attractive acquisitions in both traditional banking and select non-bank targets |

|

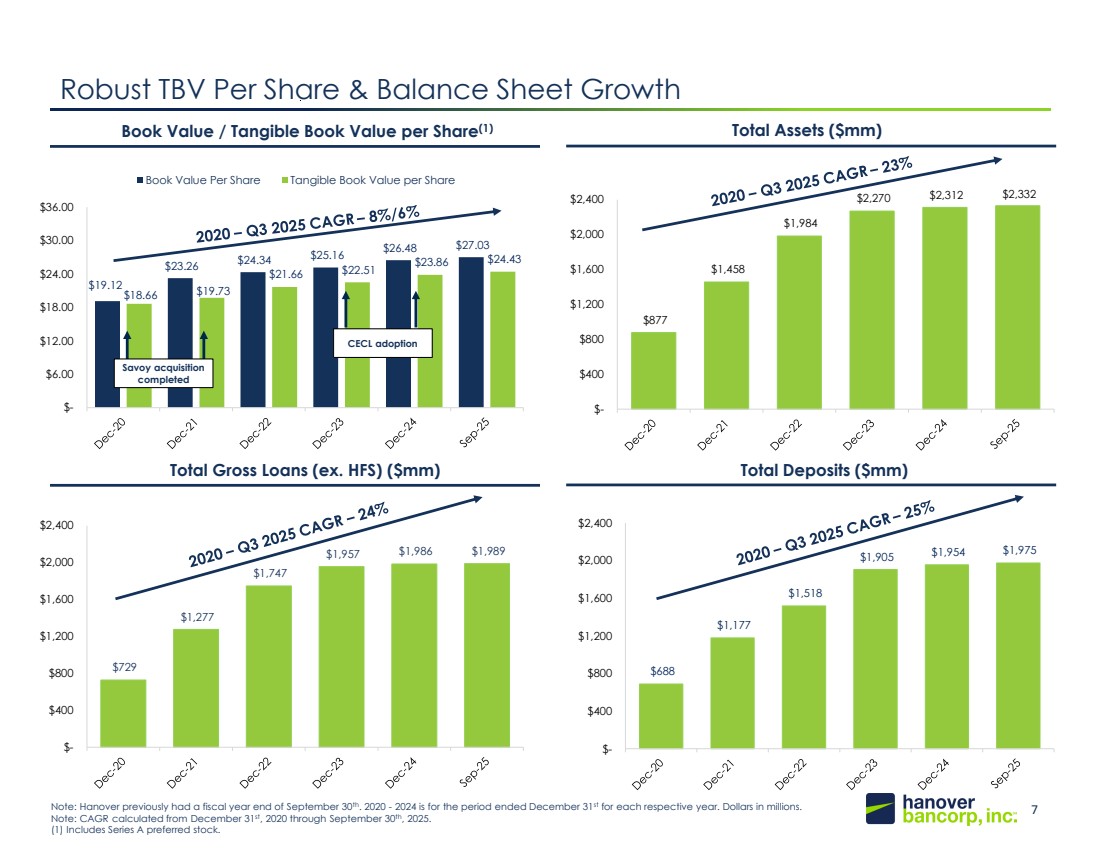

7 148, 201, 61 20, 49, 89 $19.12 $23.26 $24.34 $25.16 $26.48 $27.03 $18.66 $19.73 $21.66 $22.51 $23.86 $24.43 $- $6.00 $12.00 $18.00 $24.00 $30.00 $36.00 Book Value Per Share Tangible Book Value per Share $877 $1,458 $1,984 $2,270 $2,312 $2,332 $- $400 $800 $1,200 $1,600 $2,000 $2,400 Robust TBV Per Share & Balance Sheet Growth Note: Hanover previously had a fiscal year end of September 30th. 2020 - 2024 is for the period ended December 31st for each respective year. Dollars in millions. Note: CAGR calculated from December 31st, 2020 through September 30th, 2025. (1) Includes Series A preferred stock. Book Value / Tangible Book Value per Share(1) $729 $1,277 $1,747 $1,957 $1,986 $1,989 $- $400 $800 $1,200 $1,600 $2,000 $2,400 Total Gross Loans (ex. HFS) ($mm) $688 $1,177 $1,518 $1,905 $1,954 $1,975 $- $400 $800 $1,200 $1,600 $2,000 $2,400 Total Deposits ($mm) Total Assets ($mm) Savoy acquisition completed CECL adoption |

|

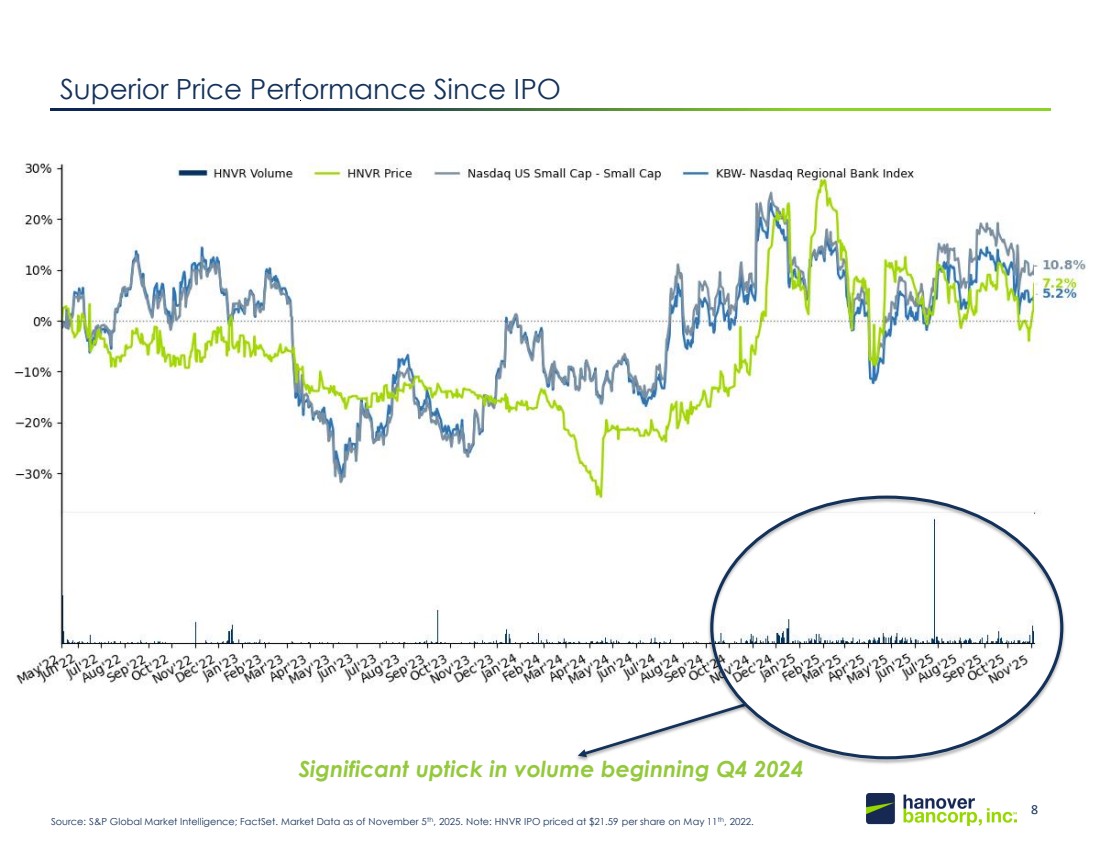

8 148, 201, 61 20, 49, 89 Superior Price Performance Since IPO Source: S&P Global Market Intelligence; FactSet. Market Data as of November 5th, 2025. Note: HNVR IPO priced at $21.59 per share on May 11th, 2022. Significant uptick in volume beginning Q4 2024 |

|

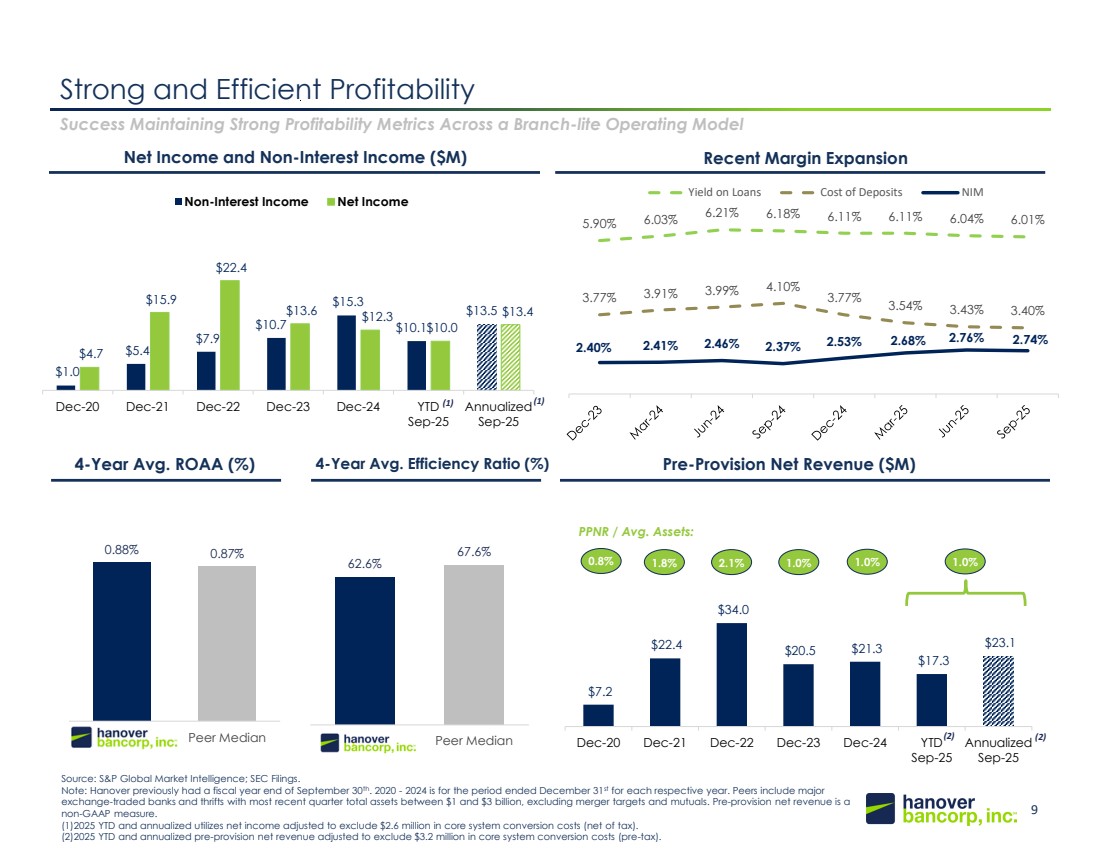

9 148, 201, 61 20, 49, 89 62.6% 67.6% Hanover Bank Peer Median 0.88% 0.87% Hanover Bank Peer Median 5.90% 6.03% 6.21% 6.18% 6.11% 6.11% 6.04% 6.01% 3.77% 3.91% 3.99% 4.10% 3.77% 3.54% 3.43% 3.40% 2.40% 2.41% 2.46% 2.37% 2.53% 2.68% 2.76% 2.74% Yield on Loans Cost of Deposits NIM Strong and Efficient Profitability Success Maintaining Strong Profitability Metrics Across a Branch-lite Operating Model Source: S&P Global Market Intelligence; SEC Filings. Note: Hanover previously had a fiscal year end of September 30th. 2020 - 2024 is for the period ended December 31st for each respective year. Peers include major exchange-traded banks and thrifts with most recent quarter total assets between $1 and $3 billion, excluding merger targets and mutuals. Pre-provision net revenue is a non-GAAP measure. (1)2025 YTD and annualized utilizes net income adjusted to exclude $2.6 million in core system conversion costs (net of tax). (2)2025 YTD and annualized pre-provision net revenue adjusted to exclude $3.2 million in core system conversion costs (pre-tax). Net Income and Non-Interest Income ($M) Recent Margin Expansion 4-Year Avg. ROAA (%) 4-Year Avg. Efficiency Ratio (%) Pre-Provision Net Revenue ($M) $1.0 $5.4 $7.9 $10.7 $15.3 $10.1 $13.5 $4.7 $15.9 $22.4 $13.6 $12.3 $10.0 $13.4 Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 YTD Sep-25 Annualized Sep-25 Non-Interest Income Net Income (1) (1) $7.2 $22.4 $34.0 $20.5 $21.3 $17.3 $23.1 Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 YTD Sep-25 Annualized Sep-25 0.8% 1.8% 1.0% 1.0% PPNR / Avg. Assets: 2.1% 1.0% (2) (2) |

|

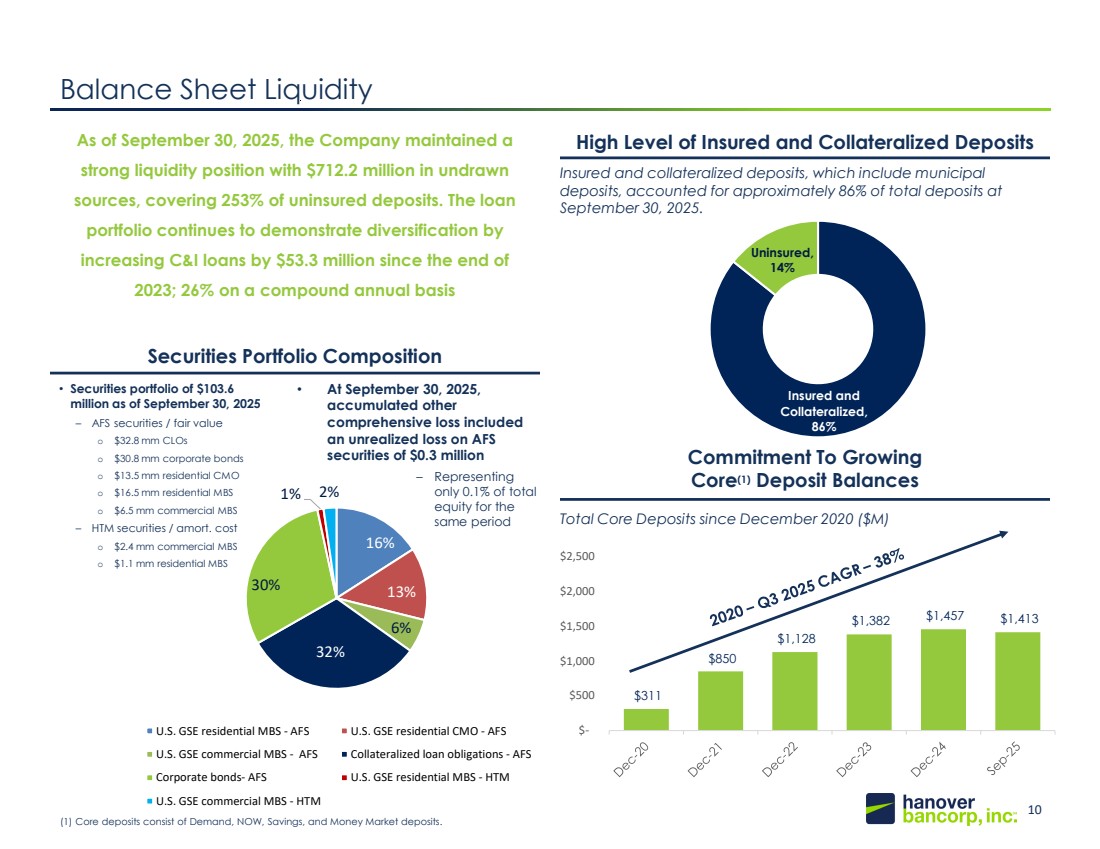

10 148, 201, 61 20, 49, 89 $311 $850 $1,128 $1,382 $1,457 $1,413 $- $500 $1,000 $1,500 $2,000 $2,500 Insured and Collateralized, 86% Uninsured, 14% 16% 13% 6% 32% 30% 1% 2% U.S. GSE residential MBS - AFS U.S. GSE residential CMO - AFS U.S. GSE commercial MBS - AFS Collateralized loan obligations - AFS Corporate bonds- AFS U.S. GSE residential MBS - HTM U.S. GSE commercial MBS - HTM High Level of Insured and Collateralized Deposits Insured and collateralized deposits, which include municipal deposits, accounted for approximately 86% of total deposits at September 30, 2025. Commitment To Growing Core(1) Deposit Balances Balance Sheet Liquidity Securities Portfolio Composition As of September 30, 2025, the Company maintained a strong liquidity position with $712.2 million in undrawn sources, covering 253% of uninsured deposits. The loan portfolio continues to demonstrate diversification by increasing C&I loans by $53.3 million since the end of 2023; 26% on a compound annual basis • At September 30, 2025, accumulated other comprehensive loss included an unrealized loss on AFS securities of $0.3 million – Representing only 0.1% of total equity for the same period Total Core Deposits since December 2020 ($M) (1) Core deposits consist of Demand, NOW, Savings, and Money Market deposits. 151 185 224 • Securities portfolio of $103.6 million as of September 30, 2025 – AFS securities / fair value o $32.8 mm CLOs o $30.8 mm corporate bonds o $13.5 mm residential CMO o $16.5 mm residential MBS o $6.5 mm commercial MBS – HTM securities / amort. cost o $2.4 mm commercial MBS o $1.1 mm residential MBS |

|

11 148, 201, 61 20, 49, 89 Investment Highlights • Recent market consolidation has resulted in a lack of sub-$5 billion asset sized banks in the Long Island and Greater New York City Metro Area. • Since June 2020, there have been 24 bank transactions in the tri-state area, 17 of which involved targets with total assets less than $5 billion. High Degree of Franchise Scarcity Value • Since 2014, the residential mortgage operation has been highly focused on non-conforming lending in New York City. With the addition of Savoy, the Company acquired a niche in SBA and small business commercial banking platform. • Hanover’s municipal deposit banking business is differentiated in that it is focused on long-term relationships that typically have less pricing volatility, particularly in rising rate environments. Niche Lending & Funding Expertise Drives Pricing Power • Significantly enhanced the Bank’s commercial lending activity with the opening of the Hauppauge Business Banking Center in May 2023 and the hiring of our EVP & Chief Lending Officer, Joseph Burns (previously First Senior VP and New York State Market President of Valley Bank). • Demonstrated track record of profitability and investing in the business. Hanover is highly focused around profitability and a highly efficient operating platform and branch network. • The Company’s level of assets, loans, deposits and revenue relative to the number of branch offices is well above peers. Management believes a continued focus on operating efficiently will result in above average levels of profitability over the long-term. Efficient, Profitable and Scalable Business Model • Since 2016, Hanover has incurred $8.1 million in cumulative net charge-offs, representing 75 basis points of average loans over that time period. • Total non-accrual loans at September 30, 2025 were $17.2 million, or 0.86% of total loans. • Hanover’s reserves of $22.4 million represent 1.12% of total loans at September 30, 2025. Disciplined Underwriting and High Quality Balance Sheet • Hanover’s executive team, which is led by Chairman and CEO Michael Puorro, has significant experience with M&A transactions and post-closing integration efforts. • In August 2019, the Company closed the CFSB acquisition and has successfully grown the former CFSB deposit franchise. • In May 2021, the Company closed the Savoy merger, acquiring an approximately $650 million total asset single branch commercial bank located in NYC. The transaction significantly diversified the revenue and lending mix while boosting profitability and leveraging Savoy’s expertise in commercial and SBA lending. Demonstrated Ability to Integrate M&A Transactions |

|

12 148, 201, 61 20, 49, 89 Russell 2000 June 2025 HNVR Included in Russell 2000 Index HNVR was added to the Russell 2000 index in late June 2025. The Russell 2000® Index encompasses the 2,000 largest U.S.-traded stocks by objective, market-capitalization rankings, and style attributes. The Russell Indexes are widely used by investment managers and institutional investors for index funds and as benchmarks for active investment strategies. |

|

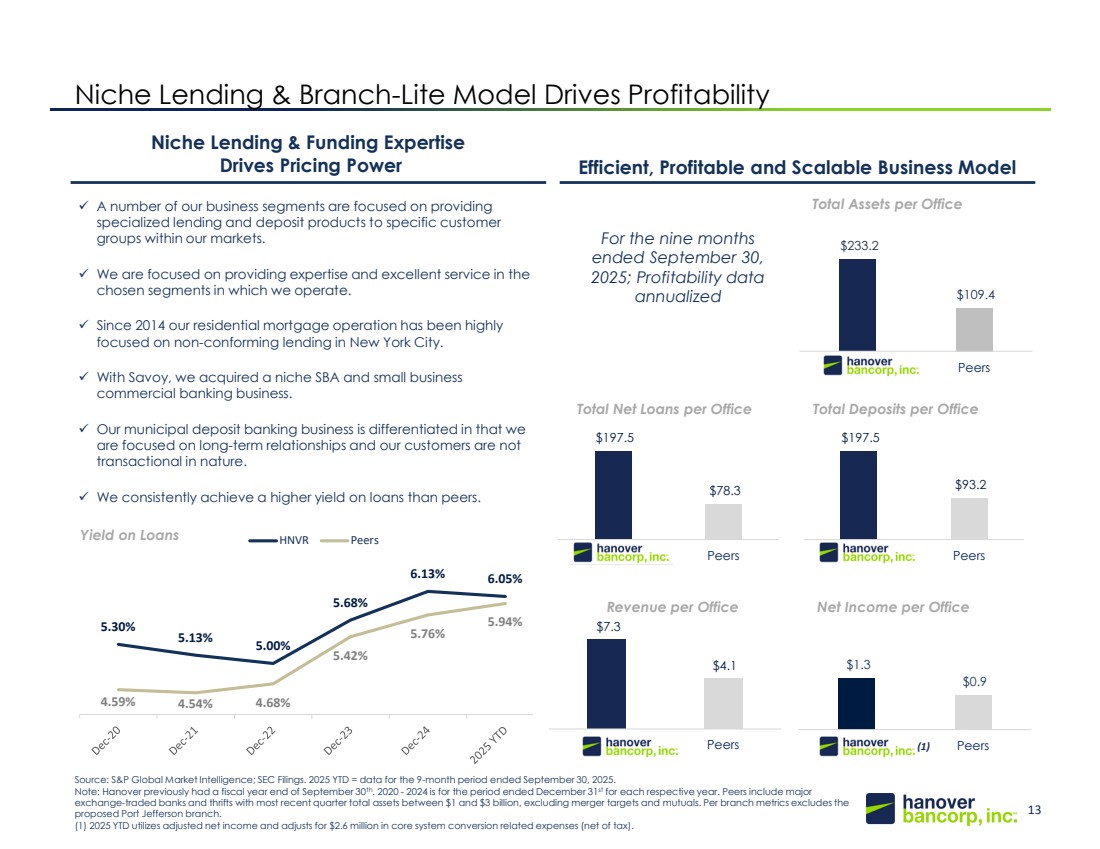

13 148, 201, 61 20, 49, 89 5.30% 5.13% 5.00% 5.68% 6.13% 6.05% 4.59% 4.54% 4.68% 5.42% 5.76% 5.94% HNVR Peers $1.3 $0.9 HNVR Peers $7.3 $4.1 HNVR Peers $197.5 $93.2 HNVR Peers $197.5 $78.3 HNVR Peers $233.2 $109.4 HNVR Peers Niche Lending & Branch-Lite Model Drives Profitability Niche Lending & Funding Expertise Drives Pricing Power Efficient, Profitable and Scalable Business Model Yield on Loans ✓ A number of our business segments are focused on providing specialized lending and deposit products to specific customer groups within our markets. ✓ We are focused on providing expertise and excellent service in the chosen segments in which we operate. ✓ Since 2014 our residential mortgage operation has been highly focused on non-conforming lending in New York City. ✓ With Savoy, we acquired a niche SBA and small business commercial banking business. ✓ Our municipal deposit banking business is differentiated in that we are focused on long-term relationships and our customers are not transactional in nature. ✓ We consistently achieve a higher yield on loans than peers. Revenue per Office Total Net Loans per Office Total Deposits per Office Total Assets per Office Net Income per Office For the nine months ended September 30, 2025; Profitability data annualized Source: S&P Global Market Intelligence; SEC Filings. 2025 YTD = data for the 9-month period ended September 30, 2025. Note: Hanover previously had a fiscal year end of September 30th. 2020 - 2024 is for the period ended December 31st for each respective year. Peers include major exchange-traded banks and thrifts with most recent quarter total assets between $1 and $3 billion, excluding merger targets and mutuals. Per branch metrics excludes the proposed Port Jefferson branch. (1) 2025 YTD utilizes adjusted net income and adjusts for $2.6 million in core system conversion related expenses (net of tax). (1) |

|

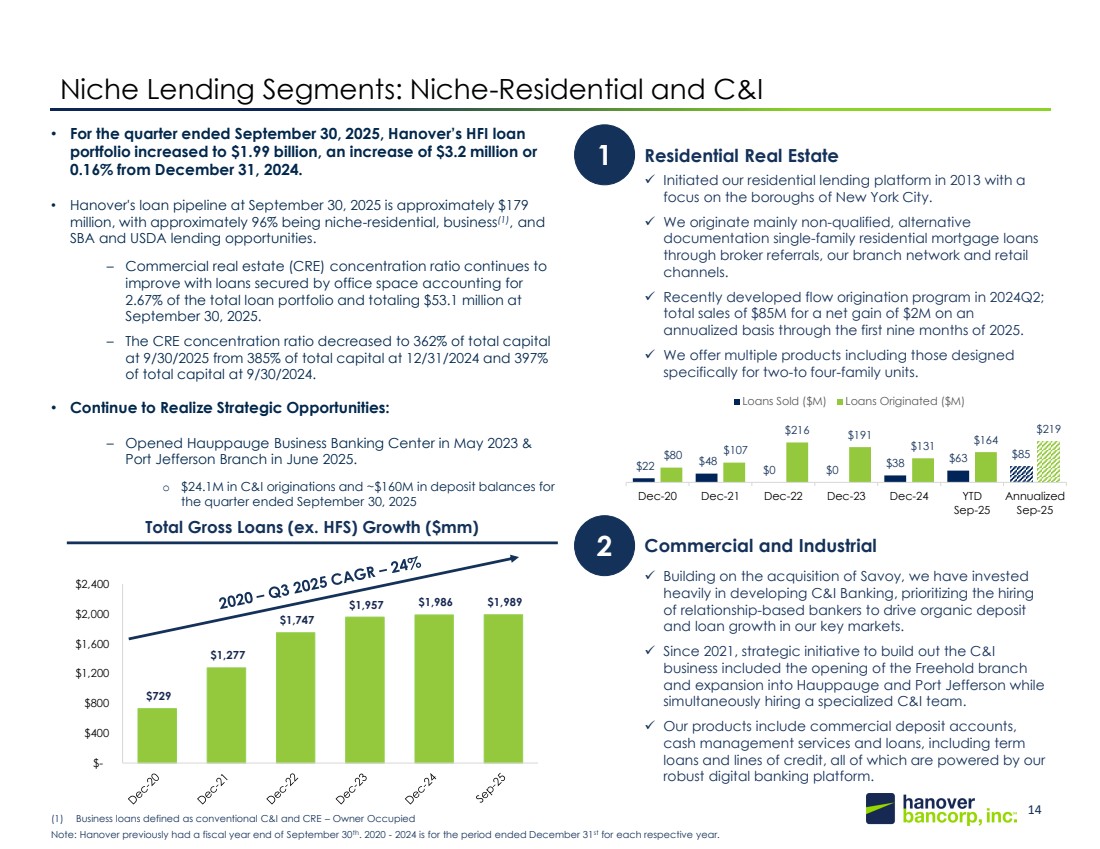

14 148, 201, 61 20, 49, 89 • For the quarter ended September 30, 2025, Hanover’s HFI loan portfolio increased to $1.99 billion, an increase of $3.2 million or 0.16% from December 31, 2024. • Hanover's loan pipeline at September 30, 2025 is approximately $179 million, with approximately 96% being niche-residential, business(1), and SBA and USDA lending opportunities. – Commercial real estate (CRE) concentration ratio continues to improve with loans secured by office space accounting for 2.67% of the total loan portfolio and totaling $53.1 million at September 30, 2025. – The CRE concentration ratio decreased to 362% of total capital at 9/30/2025 from 385% of total capital at 12/31/2024 and 397% of total capital at 9/30/2024. • Continue to Realize Strategic Opportunities: – Opened Hauppauge Business Banking Center in May 2023 & Port Jefferson Branch in June 2025. o $24.1M in C&I originations and ~$160M in deposit balances for the quarter ended September 30, 2025 Niche Lending Segments: Niche-Residential and C&I Note: Hanover previously had a fiscal year end of September 30th. 2020 - 2024 is for the period ended December 31st for each respective year. Total Gross Loans (ex. HFS) Growth ($mm) 1 Residential Real Estate ✓ Initiated our residential lending platform in 2013 with a focus on the boroughs of New York City. ✓ We originate mainly non-qualified, alternative documentation single-family residential mortgage loans through broker referrals, our branch network and retail channels. ✓ Recently developed flow origination program in 2024Q2; total sales of $85M for a net gain of $2M on an annualized basis through the first nine months of 2025. ✓ We offer multiple products including those designed specifically for two-to four-family units. ✓ Building on the acquisition of Savoy, we have invested heavily in developing C&I Banking, prioritizing the hiring of relationship-based bankers to drive organic deposit and loan growth in our key markets. ✓ Since 2021, strategic initiative to build out the C&I business included the opening of the Freehold branch and expansion into Hauppauge and Port Jefferson while simultaneously hiring a specialized C&I team. ✓ Our products include commercial deposit accounts, cash management services and loans, including term loans and lines of credit, all of which are powered by our robust digital banking platform. 2 Commercial and Industrial $729 $1,277 $1,747 $1,957 $1,986 $1,989 $- $400 $800 $1,200 $1,600 $2,000 $2,400 $22 $48 $0 $0 $38 $63 $80 $85 $107 $216 $191 $131 $164 $219 Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 YTD Sep-25 Annualized Sep-25 Loans Sold ($M) Loans Originated ($M) (1) Business loans defined as conventional C&I and CRE – Owner Occupied |

|

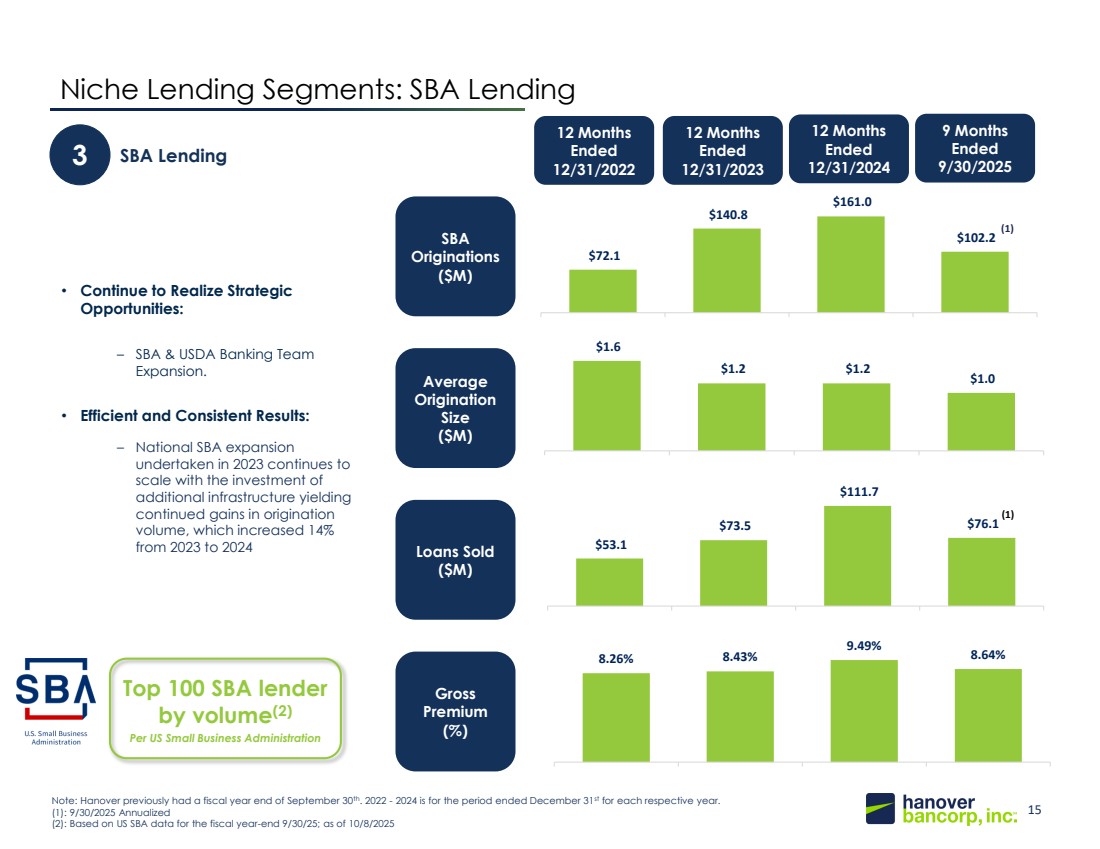

15 148, 201, 61 20, 49, 89 8.26% 8.43% 9.49% 8.64% $53.1 $73.5 $111.7 $76.1 $1.6 $1.2 $1.2 $1.0 $72.1 $140.8 $161.0 $102.2 Niche Lending Segments: SBA Lending 12 Months Ended 12/31/2022 12 Months Ended 3 12/31/2024 SBA Lending • Continue to Realize Strategic Opportunities: – SBA & USDA Banking Team Expansion. • Efficient and Consistent Results: – National SBA expansion undertaken in 2023 continues to scale with the investment of additional infrastructure yielding continued gains in origination volume, which increased 14% from 2023 to 2024 SBA Originations ($M) Average Origination Size ($M) Loans Sold ($M) Gross Premium (%) Note: Hanover previously had a fiscal year end of September 30th. 2022 - 2024 is for the period ended December 31st for each respective year. (1): 9/30/2025 Annualized (2): Based on US SBA data for the fiscal year-end 9/30/25; as of 10/8/2025 Top 100 SBA lender by volume(2) Per US Small Business Administration 9 Months Ended 9/30/2025 12 Months Ended 12/31/2023 (1) (1) |

|

16 148, 201, 61 20, 49, 89 225% 408% 470% 432% 385% 362% Niche Lending Segments: Commercial Real Estate 4 Commercial Real Estate (including Multi-family) ✓ The Bank’s exposure to Land/Construction loans is not significant at $5.9 million at September 30, 2025, all at floating interest rates. As shown at right and on the next slide, 28% of the loan balances in these combined portfolios will either mature or have a rate reset in the remainder of 2025 and 2026, with another 56% with rate resets or maturing in 2027. ✓ At September 30, 2025, 64% of the multi-family loan portfolio is secured by properties subject to free market rental terms, which is the dominant tenant type. Both the Market Rent and Stabilized Rent segments of our portfolio present very similar average borrower profiles. The portfolio is primarily located in the New York City boroughs of Brooklyn, the Bronx and Queens. ✓ The Bank’s exposure to the Office market is not significant at $53 million as of September 30, 2025. The pool has a 2.31x weighted average DSCR, a 52% weighted average LTV and less than $350,000 of exposure in Manhattan. ✓ The Company’s commercial real estate concentration ratio continues to improve, decreasing to 362% of capital at September 30, 2025 from 385% of capital at December 31, 2024 and 397% of capital at September 30, 2024. Fixed Rate Reset / Maturity Schedule ($000s) CRE / TRBC Ratio (%) Calendar Period (Loan Data as of 9/30/2025) # Loans 2025 19 $ 25,621 $ 1,348 7.00 % 2026 32 38,468 1,202 5.17 % 2027 88 148,355 1,686 4.86 % 2028 28 30,613 1,093 6.65 % 2029 5 5,970 1,194 6.70 % 2030+ 20 16,914 846 6.59 % Fixed Rate 192 $ 265,941 $ 1,385 5.47 % Floating Rate 8 10,493 1,312 9.11 % Total CRE-Inv. 200 $ 276,434 $ 1,382 5.60 % CRE Investor Portfolio Total O/S Avg O/S Avg Interest Rate |

|

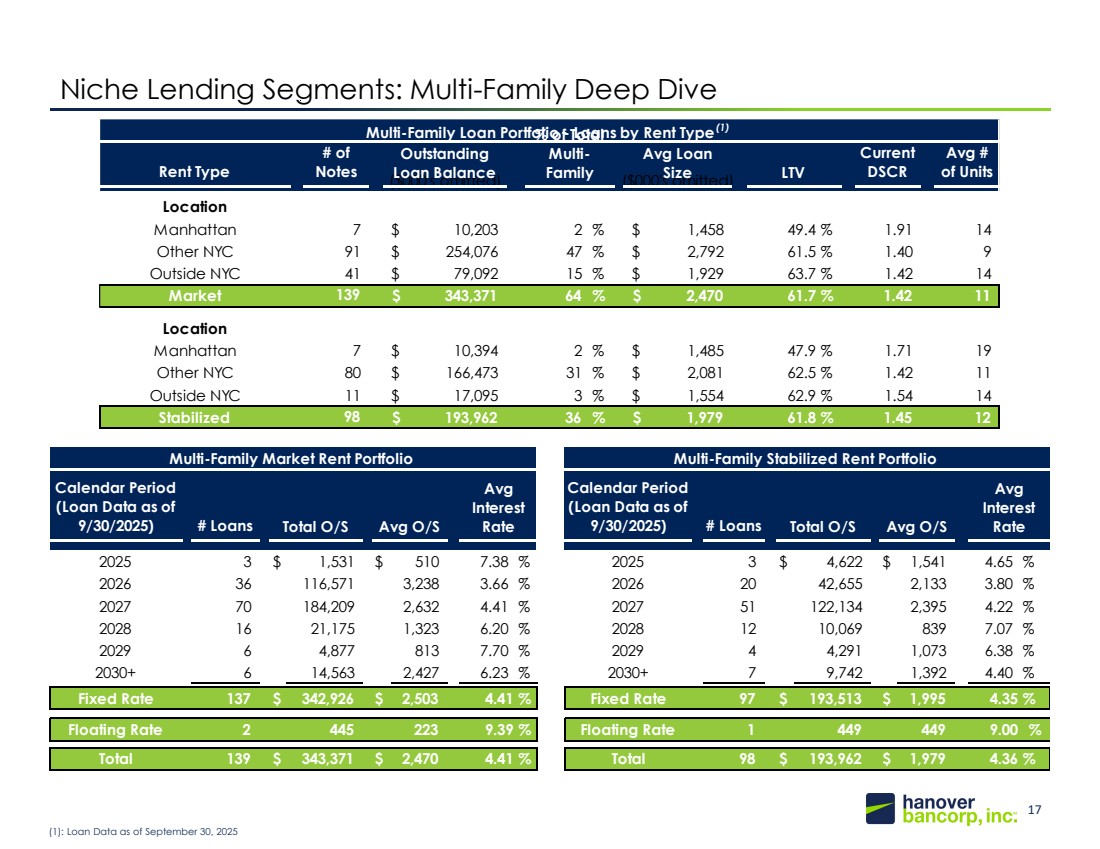

17 148, 201, 61 20, 49, 89 Niche Lending Segments: Multi-Family Deep Dive Calendar Period (Loan Data as of 9/30/2025) # Loans Calendar Period (Loan Data as of 9/30/2025) # Loans 2025 3 $ 1,531 $ 510 7.38 % 2025 3 $ 4,622 $ 1,541 4.65 % 2026 36 116,571 3,238 3.66 % 2026 20 42,655 2,133 3.80 % 2027 70 184,209 2,632 4.41 % 2027 51 122,134 2,395 4.22 % 2028 16 21,175 1,323 6.20 % 2028 12 10,069 839 7.07 % 2029 6 4,877 813 7.70 % 2029 4 4,291 1,073 6.38 % 2030+ 6 14,563 2,427 6.23 % 2030+ 7 9,742 1,392 4.40 % Fixed Rate 137 $ 342,926 $ 2,503 4.41 % Fixed Rate 97 $ 193,513 $ 1,995 4.35 % Floating Rate 2 445 223 9.39 % Floating Rate 1 449 449 9.00 % Total 139 $ 343,371 $ 2,470 4.41 % Total 98 $ 193,962 $ 1,979 4.36 % Multi-Family Market Rent Portfolio Multi-Family Stabilized Rent Portfolio Total O/S Avg O/S Avg Interest Rate Total O/S Avg O/S Avg Interest Rate Rent Type # of Notes Current DSCR Avg # of Units Location Manhattan 7 $ 10,203 2 % $ 1,458 49.4 % 1.91 14 Other NYC 91 $ 254,076 47 % $ 2,792 61.5 % 1.40 9 Outside NYC 41 $ 79,092 15 % $ 1,929 63.7 % 1.42 14 Market 139 $ 343,371 64 % $ 2,470 61.7 % 1.42 11 Location Manhattan 7 $ 10,394 2 % $ 1,485 47.9 % 1.71 19 Other NYC 80 $ 166,473 31 % $ 2,081 62.5 % 1.42 11 Outside NYC 11 $ 17,095 3 % $ 1,554 62.9 % 1.54 14 Stabilized 98 $ 193,962 36 % $ 1,979 61.8 % 1.45 12 ($000's omitted) ($000's omitted) Multi-Family Loan Portfolio - Loans by Rent Type(1) Outstanding Loan Balance % of Total Multi-Family Avg Loan Size LTV (1): Loan Data as of September 30, 2025 |

|

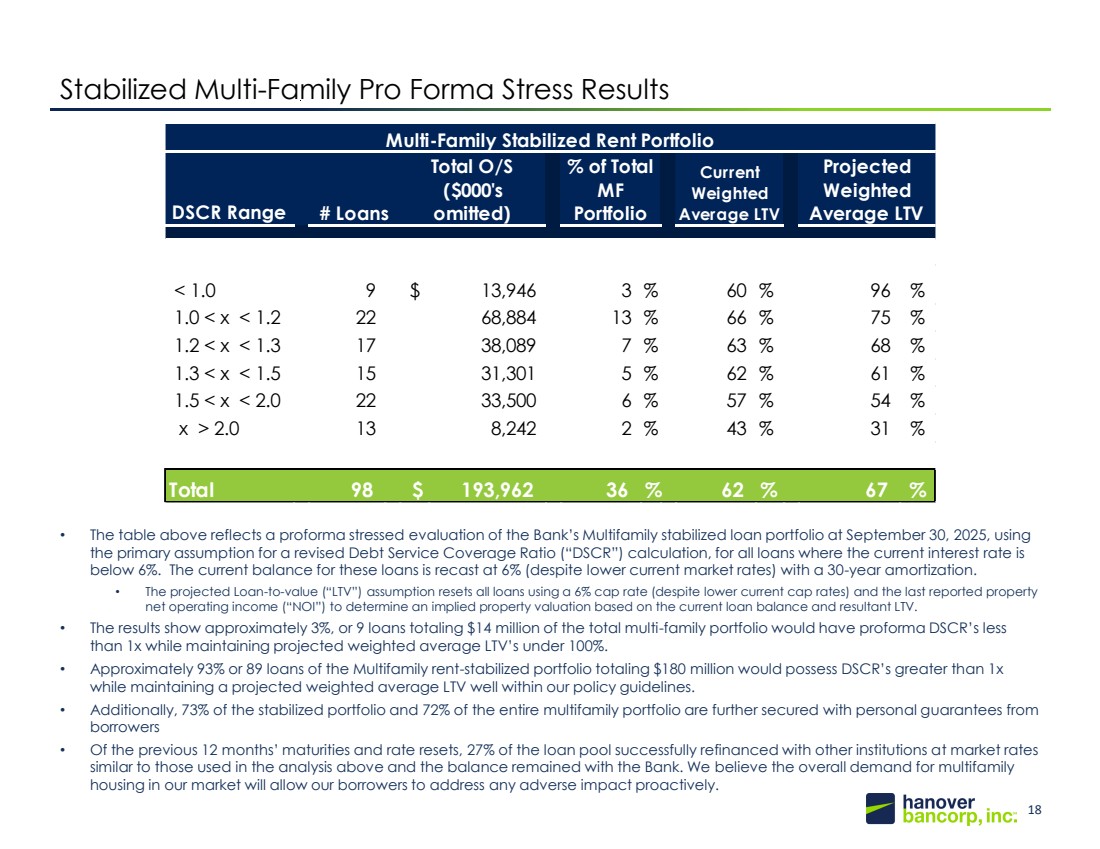

18 148, 201, 61 20, 49, 89 Stabilized Multi-Family Pro Forma Stress Results • The table above reflects a proforma stressed evaluation of the Bank’s Multifamily stabilized loan portfolio at September 30, 2025, using the primary assumption for a revised Debt Service Coverage Ratio (“DSCR”) calculation, for all loans where the current interest rate is below 6%. The current balance for these loans is recast at 6% (despite lower current market rates) with a 30-year amortization. • The projected Loan-to-value (“LTV”) assumption resets all loans using a 6% cap rate (despite lower current cap rates) and the last reported property net operating income (“NOI”) to determine an implied property valuation based on the current loan balance and resultant LTV. • The results show approximately 3%, or 9 loans totaling $14 million of the total multi-family portfolio would have proforma DSCR’s less than 1x while maintaining projected weighted average LTV’s under 100%. • Approximately 93% or 89 loans of the Multifamily rent-stabilized portfolio totaling $180 million would possess DSCR’s greater than 1x while maintaining a projected weighted average LTV well within our policy guidelines. • Additionally, 73% of the stabilized portfolio and 72% of the entire multifamily portfolio are further secured with personal guarantees from borrowers • Of the previous 12 months’ maturities and rate resets, 27% of the loan pool successfully refinanced with other institutions at market rates similar to those used in the analysis above and the balance remained with the Bank. We believe the overall demand for multifamily housing in our market will allow our borrowers to address any adverse impact proactively. DSCR Range < 1.0 9 $ 13,946 3 % 60 % 96 % 1.0 < x < 1.2 22 68,884 13 % 66 % 75 % 1.2 < x < 1.3 17 38,089 7 % 63 % 68 % 1.3 < x < 1.5 15 31,301 5 % 62 % 61 % 1.5 < x < 2.0 22 33,500 6 % 57 % 54 % x > 2.0 13 8,242 2 % 43 % 31 % Total 98 $ 193,962 36 % 62 % 67 % # Loans Multi-Family Stabilized Rent Portfolio Total O/S ($000's omitted) % of Total MF Portfolio Current Weighted Average LTV Projected Weighted Average LTV |

|

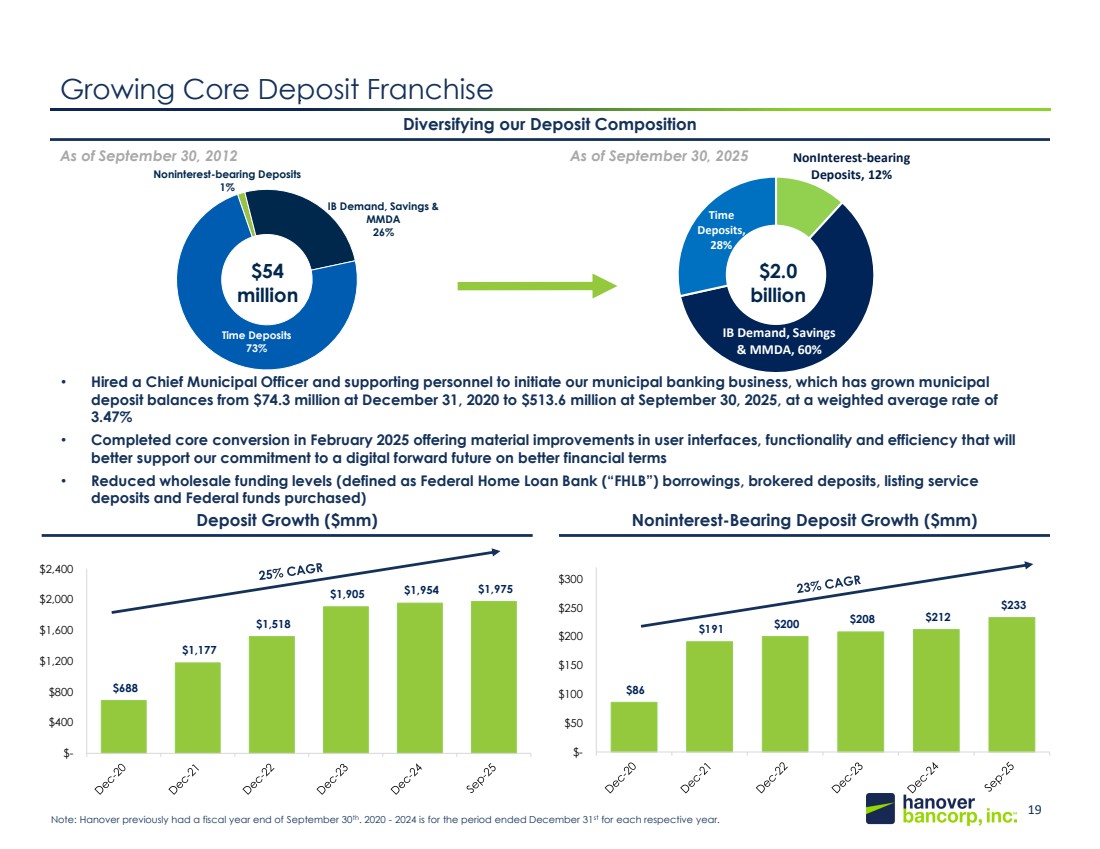

19 148, 201, 61 20, 49, 89 $688 $1,177 $1,518 $1,905 $1,954 $1,975 $- $400 $800 $1,200 $1,600 $2,000 $2,400 $86 $191 $200 $208 $212 $233 $- $50 $100 $150 $200 $250 $300 NonInterest-bearing Deposits, 12% IB Demand, Savings & MMDA, 60% Time Deposits, 28% Deposit Growth ($mm) Noninterest-Bearing Deposit Growth ($mm) Noninterest-bearing Deposits 1% IB Demand, Savings & MMDA 26% Time Deposits 73% Growing Core Deposit Franchise • Hired a Chief Municipal Officer and supporting personnel to initiate our municipal banking business, which has grown municipal deposit balances from $74.3 million at December 31, 2020 to $513.6 million at September 30, 2025, at a weighted average rate of 3.47% • Completed core conversion in February 2025 offering material improvements in user interfaces, functionality and efficiency that will better support our commitment to a digital forward future on better financial terms • Reduced wholesale funding levels (defined as Federal Home Loan Bank (“FHLB”) borrowings, brokered deposits, listing service deposits and Federal funds purchased) Diversifying our Deposit Composition As of September 30, 2012 As of September 30, 2025 $54 million 0 92 176 Note: Hanover previously had a fiscal year end of September 30th. 2020 - 2024 is for the period ended December 31st for each respective year. $2.0 billion |

|

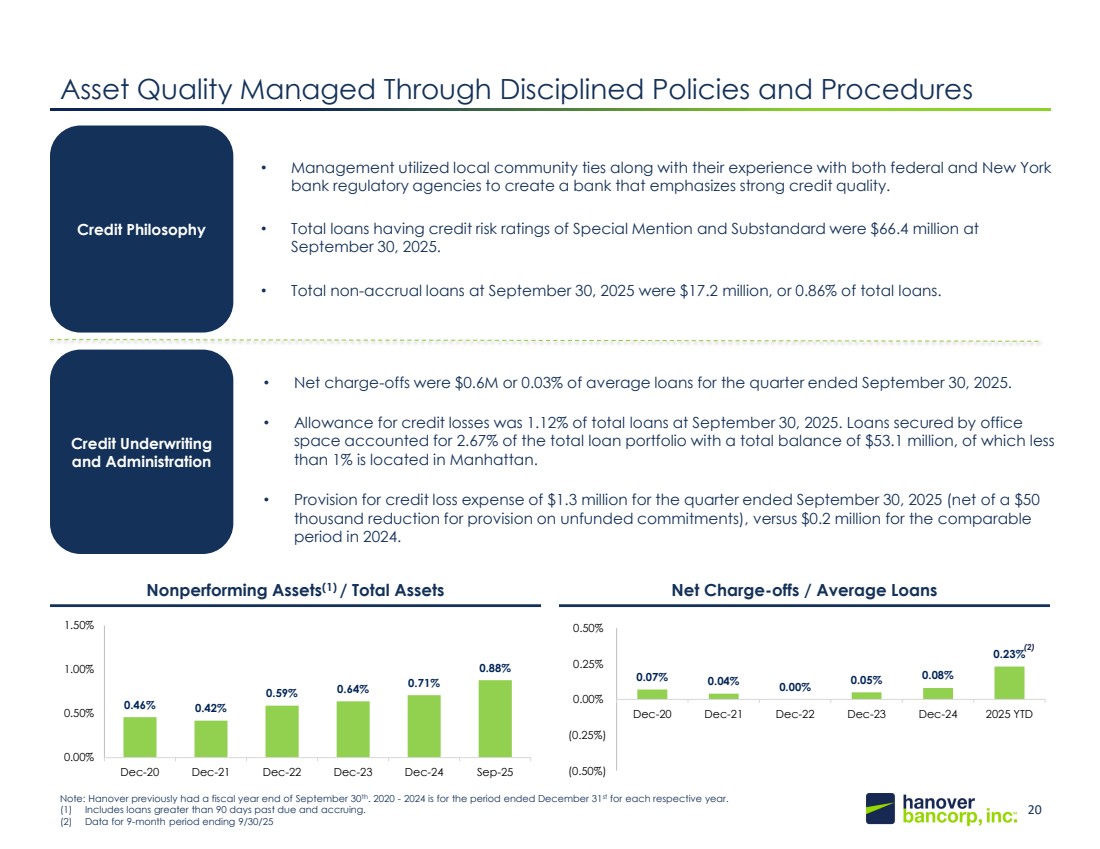

20 148, 201, 61 20, 49, 89 0.07% 0.04% 0.00% 0.05% 0.08% 0.23% (0.50%) (0.25%) 0.00% 0.25% 0.50% Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 2025 YTD 0.46% 0.42% 0.59% 0.64% 0.71% 0.88% 0.00% 0.50% 1.00% 1.50% Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 Sep-25 Note: Hanover previously had a fiscal year end of September 30th. 2020 - 2024 is for the period ended December 31st for each respective year. (1) Includes loans greater than 90 days past due and accruing. (2) Data for 9-month period ending 9/30/25 Asset Quality Managed Through Disciplined Policies and Procedures Credit Philosophy Credit Underwriting and Administration • Management utilized local community ties along with their experience with both federal and New York bank regulatory agencies to create a bank that emphasizes strong credit quality. • Total loans having credit risk ratings of Special Mention and Substandard were $66.4 million at September 30, 2025. • Total non-accrual loans at September 30, 2025 were $17.2 million, or 0.86% of total loans. • Net charge-offs were $0.6M or 0.03% of average loans for the quarter ended September 30, 2025. • Allowance for credit losses was 1.12% of total loans at September 30, 2025. Loans secured by office space accounted for 2.67% of the total loan portfolio with a total balance of $53.1 million, of which less than 1% is located in Manhattan. • Provision for credit loss expense of $1.3 million for the quarter ended September 30, 2025 (net of a $50 thousand reduction for provision on unfunded commitments), versus $0.2 million for the comparable period in 2024. Nonperforming Assets(1) / Total Assets Net Charge-offs / Average Loans (2) |

|

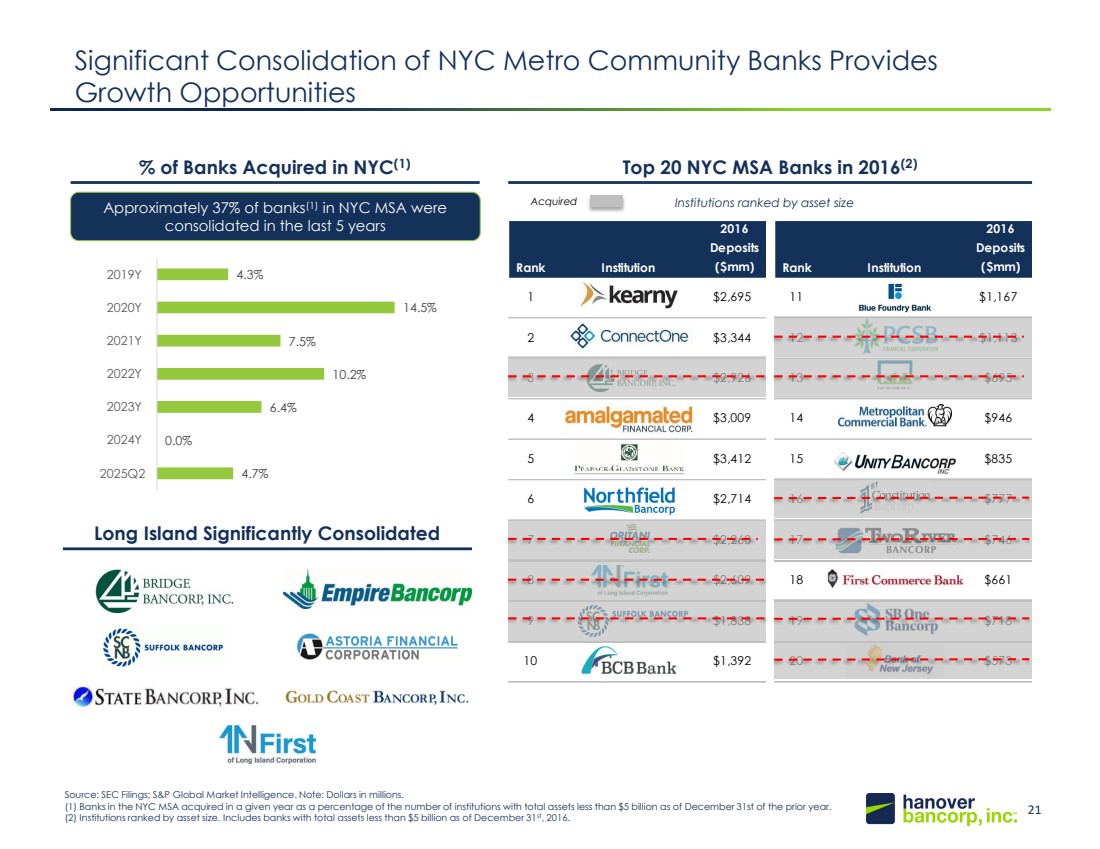

21 148, 201, 61 20, 49, 89 2016 Rank Institution Deposits ($mm) 1 $2,695 2 $3,344 3 $2,926 4 $3,009 5 $3,412 6 $2,714 7 $2,260 8 $2,609 9 $1,838 10 $1,392 Significant Consolidation of NYC Metro Community Banks Provides Growth Opportunities Source: SEC Filings; S&P Global Market Intelligence. Note: Dollars in millions. (1) Banks in the NYC MSA acquired in a given year as a percentage of the number of institutions with total assets less than $5 billion as of December 31st of the prior year. (2) Institutions ranked by asset size. Includes banks with total assets less than $5 billion as of December 31st, 2016. % of Banks Acquired in NYC(1) Top 20 NYC MSA Banks in 2016(2) Approximately 37% of banks(1) in NYC MSA were consolidated in the last 5 years 2016 Rank Institution Deposits ($mm) 11 $1,167 12 $1,113 13 $695 14 $946 15 $835 16 $777 17 $746 18 $661 19 $718 20 $573 Acquired Institutions ranked by asset size Long Island Significantly Consolidated 4.3% 14.5% 7.5% 10.2% 6.4% 0.0% 4.7% 2019Y 2020Y 2021Y 2022Y 2023Y 2024Y 2025Q2 |

|

Confidential Investor Presentation 22 |

|

23 148, 201, 61 20, 49, 89 19.4 12.8 9.2 8.4 7.7 6.4 6.4 6.3 6.3 5.2 New York City Los Angeles Chicago Dallas Houston Atlanta Washington D.C. Miami Philadelphia Phoenix New York MSA – A Leading U.S. Banking Market Source: S&P Global Market Intelligence; SEC Filings; US Census; U.S. Small Business Administration. Note: Small Business data as of 2024. Note – Deposits as of 6/30/2025 and includes all Commercial Banks, Savings Banks, Savings & Loan Associations, and Credit Unions Note – Population data as of 2025 Population (mm) Deposits per Branch ($mm) Deposits ($bn) Most Populated MSA 3 rd Largest Deposits per Branch (min $100bn in MSA) Largest Deposit Market (MSA) Small Businesses (mm) 4 th Most Small Businesses by State $410 $426 $443 $453 $526 $599 $798 $829 $4,098 $4,875 Philadelphia, PA Jacksonville, FL San Antonio, TX Raleigh, NC San Francisco, CA San Jose, CA Charlotte, NC New York City Salt Lake City, UT Sioux Falls, SD $497 $553 $585 $687 $690 $712 $783 $897 $1,049 $4,032 San Francisco, CA Washington, DC Boston, MA Chicago, IL Philadelphia, PA Dallas, TX Los Angeles, CA Sioux Falls, SD Salt Lake City, UT New York City 1.0 1.0 1.0 1.1 1.2 1.3 2.2 3.1 3.2 4.1 New Jersey Ohio North Carolina Pennsylvania Georgia Illinois New York Florida Texas California |

|

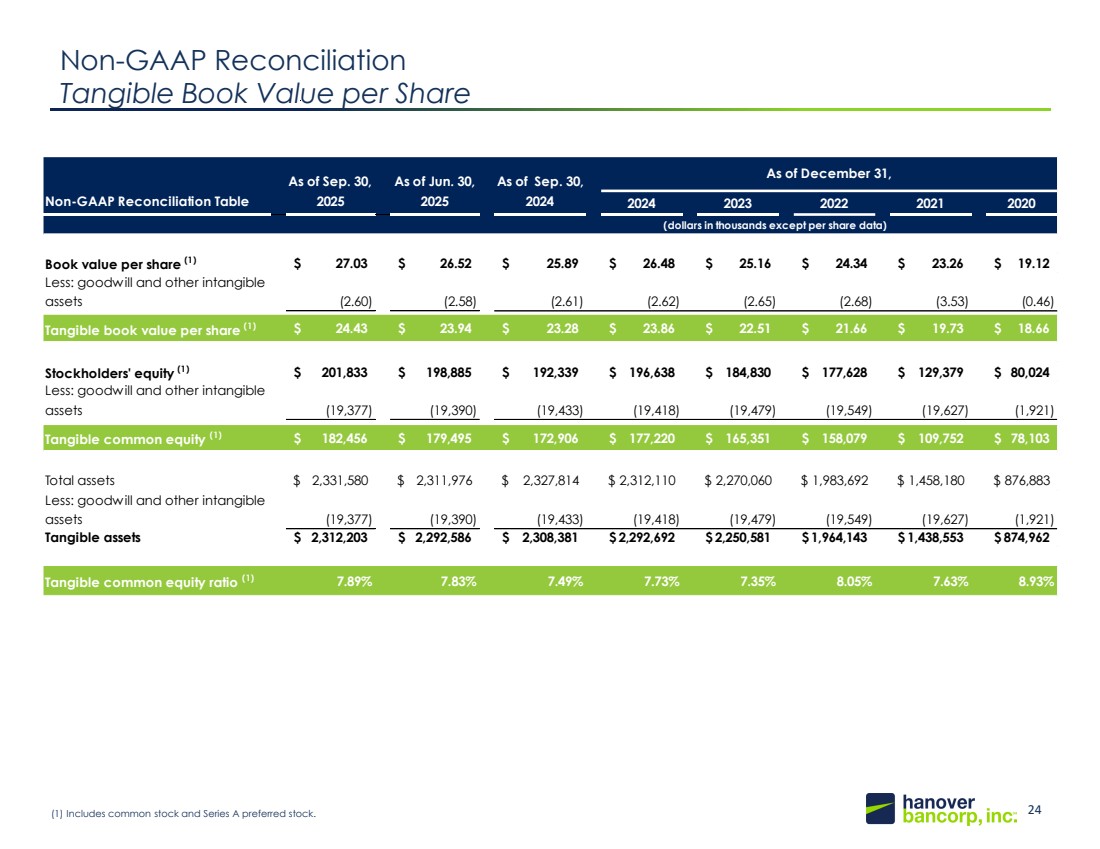

24 148, 201, 61 20, 49, 89 Non-GAAP Reconciliation Tangible Book Value per Share (1) Includes common stock and Series A preferred stock. As of Sep. 30, As of Jun. 30, As of Sep. 30, Non-GAAP Reconciliation Table 2025 2025 2024 2024 2023 2022 2021 2020 Book value per share (1) $ 27.03 $ 26.52 $ 25.89 $ 26.48 $ 25.16 $ 24.34 $ 23.26 $ 19.12 Less: goodwill and other intangible assets (2.60) (2.58) (2.61) (2.62) (2.65) (2.68) (3.53) (0.46) Tangible book value per share (1) $ 24.43 $ 23.94 $ 23.28 $ 23.86 $ 22.51 $ 21.66 $ 19.73 $ 18.66 Stockholders' equity (1) $ 201,833 $ 198,885 $ 192,339 $ 196,638 $ 184,830 $ 177,628 $ 129,379 $ 80,024 Less: goodwill and other intangible assets (19,377) (19,390) (19,433) (19,418) (19,479) (19,549) (19,627) (1,921) Tangible common equity (1) $ 182,456 $ 179,495 $ 172,906 $ 177,220 $ 165,351 $ 158,079 $ 109,752 $ 78,103 Total assets $ 2,331,580 $ 2,311,976 $ 2,327,814 $ 2,312,110 $ 2,270,060 $ 1,983,692 $ 1,458,180 $ 876,883 Less: goodwill and other intangible assets (19,377) (19,390) (19,433) (19,418) (19,479) (19,549) (19,627) (1,921) Tangible assets $ 2,312,203 $ 2,292,586 $ 2,308,381 $ 2,292,692 $ 2,250,581 $ 1,964,143 $ 1,438,553 $ 874,962 Tangible common equity ratio (1) 7.89% 7.83% 7.49% 7.73% 7.35% 8.05% 7.63% 8.93% As of December 31, (dollars in thousands except per share data) |

|

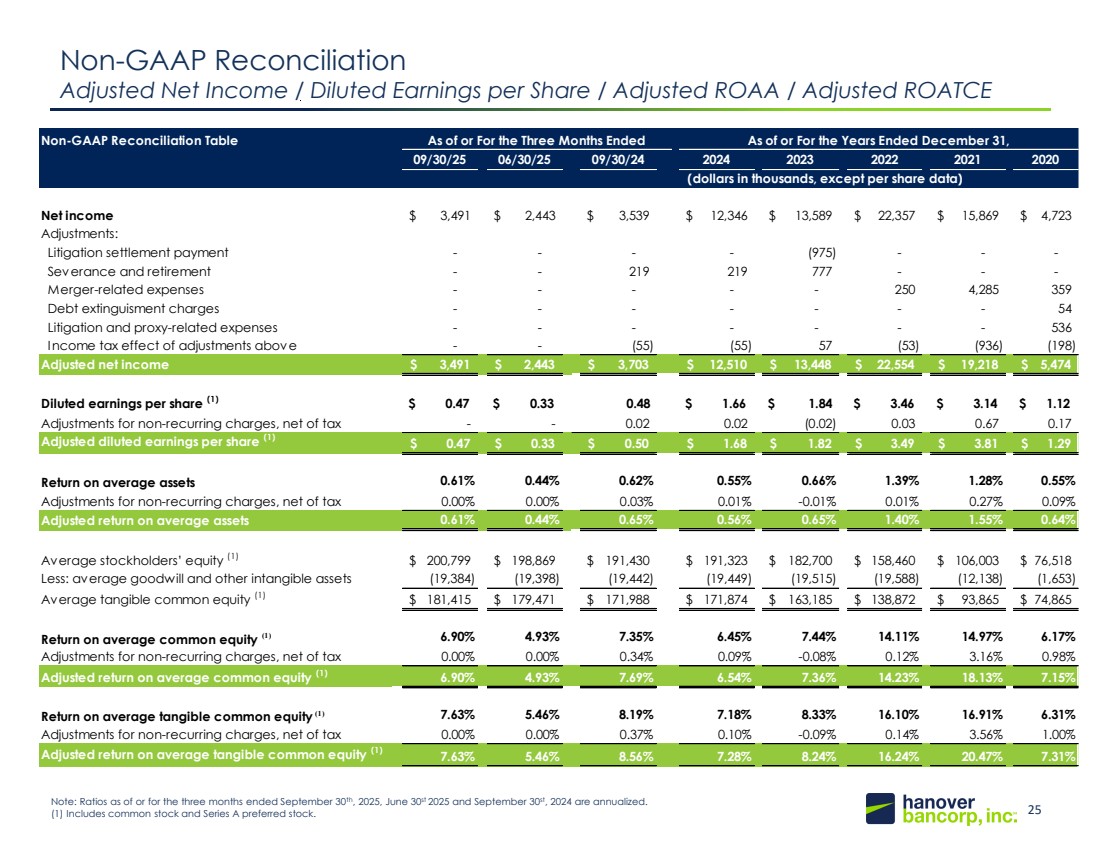

25 148, 201, 61 20, 49, 89 Non-GAAP Reconciliation Adjusted Net Income / Diluted Earnings per Share / Adjusted ROAA / Adjusted ROATCE Note: Ratios as of or for the three months ended September 30th, 2025, June 30st 2025 and September 30st, 2024 are annualized. (1) Includes common stock and Series A preferred stock. Non-GAAP Reconciliation Table 09/30/25 06/30/25 09/30/24 2024 2023 2022 2021 2020 Net income $ 3,491 $ 2,443 $ 3,539 $ 12,346 $ 13,589 $ 22,357 $ 15,869 $ 4,723 Adjustments: Litigation settlement payment - - - - (975) - - - Severance and retirement - - 219 219 777 - - - Merger-related expenses - - - - - 250 4,285 359 Debt extinguisment charges - - - - - - - 54 Litigation and proxy-related expenses - - - - - - - 536 Income tax effect of adjustments above - - (55) (55) 57 (53) (936) (198) Adjusted net income $ 3,491 $ 2,443 $ 3,703 $ 12,510 $ 13,448 $ 22,554 $ 19,218 $ 5,474 Diluted earnings per share (1) $ 0.47 $ 0.33 0.48 $ 1.66 $ 1.84 $ 3.46 $ 3.14 $ 1.12 Adjustments for non-recurring charges, net of tax - - 0.02 0.02 (0.02) 0.03 0.67 0.17 Adjusted diluted earnings per share (1) $ 0.47 $ 0.33 $ 0.50 $ 1.68 $ 1.82 $ 3.49 $ 3.81 $ 1.29 Return on average assets 0.61% 0.44% 0.62% 0.55% 0.66% 1.39% 1.28% 0.55% Adjustments for non-recurring charges, net of tax 0.00% 0.00% 0.03% 0.01% -0.01% 0.01% 0.27% 0.09% Adjusted return on average assets 0.61% 0.44% 0.65% 0.56% 0.65% 1.40% 1.55% 0.64% Average stockholders’ equity (1) $ 200,799 $ 198,869 $ 191,430 $ 191,323 $ 182,700 $ 158,460 $ 106,003 $ 76,518 Less: average goodwill and other intangible assets (19,384) (19,398) (19,442) (19,449) (19,515) (19,588) (12,138) (1,653) Average tangible common equity (1) $ 181,415 $ 179,471 $ 171,988 $ 171,874 $ 163,185 $ 138,872 $ 93,865 $ 74,865 Return on average common equity (1) 6.90% 4.93% 7.35% 6.45% 7.44% 14.11% 14.97% 6.17% Adjustments for non-recurring charges, net of tax 0.00% 0.00% 0.34% 0.09% -0.08% 0.12% 3.16% 0.98% Adjusted return on average common equity (1) 6.90% 4.93% 7.69% 6.54% 7.36% 14.23% 18.13% 7.15% Return on average tangible common equity (1) 7.63% 5.46% 8.19% 7.18% 8.33% 16.10% 16.91% 6.31% Adjustments for non-recurring charges, net of tax 0.00% 0.00% 0.37% 0.10% -0.09% 0.14% 3.56% 1.00% Adjusted return on average tangible common equity (1) 7.63% 5.46% 8.56% 7.28% 8.24% 16.24% 20.47% 7.31% As of or For the Years Ended December 31, (dollars in thousands, except per share data) As of or For the Three Months Ended |

|

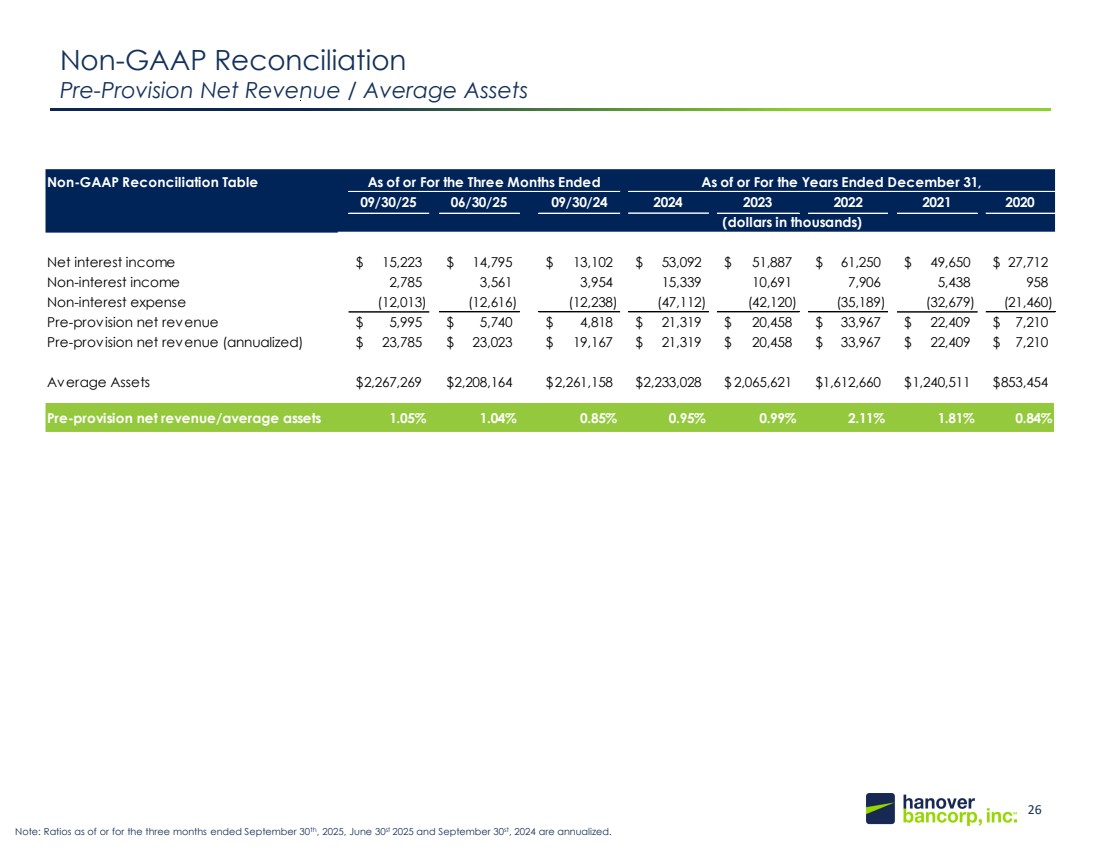

26 148, 201, 61 20, 49, 89 Non-GAAP Reconciliation Pre-Provision Net Revenue / Average Assets Note: Ratios as of or for the three months ended September 30th, 2025, June 30st 2025 and September 30st, 2024 are annualized. Non-GAAP Reconciliation Table 09/30/25 06/30/25 09/30/24 2024 2023 2022 2021 2020 Net interest income $ 15,223 $ 14,795 $ 13,102 $ 53,092 $ 51,887 $ 61,250 $ 49,650 $ 27,712 Non-interest income 2,785 3,561 3,954 15,339 10,691 7,906 5,438 958 Non-interest expense (12,013) (12,616) (12,238) (47,112) (42,120) (35,189) (32,679) (21,460) Pre-provision net revenue $ 5,995 $ 5,740 $ 4,818 $ 21,319 $ 20,458 $ 33,967 $ 22,409 $ 7,210 Pre-provision net revenue (annualized) $ 23,785 $ 23,023 $ 19,167 $ 21,319 $ 20,458 $ 33,967 $ 22,409 $ 7,210 Average Assets $2,267,269 $2,208,164 $2,261,158 $2,233,028 $ 2,065,621 $1,612,660 $1,240,511 $853,454 Pre-provision net revenue/average assets 1.05% 1.04% 0.85% 0.95% 0.99% 2.11% 1.81% 0.84% As of or For the Years Ended December 31, (dollars in thousands) As of or For the Three Months Ended |