UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2025

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to ______

Commission File Number: 001-34857

Gold Resource Corporation

(Exact Name of Registrant as Specified in its charter)

Colorado |

84-1473173 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

7900 E. Union Ave, Suite 320, Denver, Colorado 80237

(Address of Principal Executive Offices) (Zip Code)

(303) 320-7708

(Registrant’s telephone number including area code)

Securities registered pursuant to Section 12(b) of the Act:

a |

||

Title of each class |

Trading Symbol |

Name of each exchange where registered |

Common Stock, $0.001 par value |

GORO |

NYSE American |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.Yes⌧No◻

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes⌧No◻

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

◻ |

Accelerated filer |

◻ |

|

|

|

|

Non-accelerated filer |

☒ |

Smaller reporting company |

☒ |

|

|

|

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act◻

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes☐No⌧

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 161,765,685 shares of common stock outstanding as of October 31, 2025.

GOLD RESOURCE CORPORATION

FORM 10-Q

Table of Contents

|

|

|

Page |

|

|

3 |

|

|

|

|

|

|

|

5 |

|

Condensed Consolidated Interim Financial Statements and Notes |

5 |

||

|

|

5 |

|

|

|

6 |

|

|

|

7 |

|

|

|

9 |

|

|

|

10 |

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

35 |

|

|

58 |

||

|

60 |

||

|

|

|

|

|

|

61 |

|

|

61 |

||

|

61 |

||

|

61 |

||

|

61 |

||

|

61 |

||

|

61 |

||

|

62 |

||

63 |

|||

|

DDGM Processing Plant |

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 2 A summary for the three months ended September 30, 2025 is presented below and discussed further under Item 2—Management’s Discussion and Analysis of Financial Condition and Results of Operations:

THIRD QUARTER 2025 SUMMARY

Don David Gold Mine (“DDGM”)

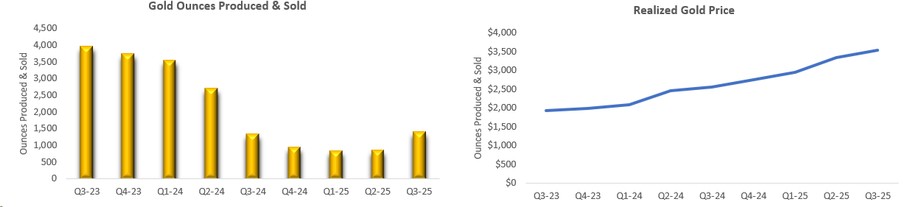

| ● | In the third quarter of 2025, DDGM, located in Mexico, produced and sold a total of 6,298 gold equivalent (“AuEq”) ounces, comprised of 1,422 gold ounces and 417,710 silver ounces, at an average sales price per ounce of $3,546 and $41.39, respectively. |

| ● | By the end of the third quarter, the Company began receiving newly acquired equipment and, when combined with the strategic use of third-party contractors, this enabled an increase in available headings and a subsequent improvement in production. |

| ● | Underground grade control and infill drilling advanced as planned at the Three Sisters vein system, focused on the Sandy and Sadie vein sets. Results from this work continue to refine and validate the geologic model, supporting near-term production planning. Additional drilling targeted the Splay 31, Marena North, Candelaria, and Viridiana veins in the Arista system, and the Soledad South vein in the Switchback system. These programs aim to optimize economic returns from near-term production across multiple vein systems. Underground exploration drilling remains on hold, with step-out targets at Three Sisters and Arista planned for future drill testing following completion of necessary development and improvements in the Company’s working capital position. |

Corporate and Financial

| ● | The Company has $12.8 million in working capital and $9.8 million in cash and cash equivalents as of September 30, 2025. |

| ● | On September 8, 2025, the Company closed on a $11.4 million registered direct offering for the sale of 25,315,954 shares of the Company’s common stock at a price of $0.45 per share. The Company issued 14,204,846 of these shares, for the fair value of approximately $6.4 million, to fully pay off the term loan received in June 2025 as a non-cash equity settlement. |

| ● | The Company had a net loss of $4.7 million, or $0.03 per share, for the quarter, which was primarily the result of lower tonnes produced and less ounces sold. Early in the quarter, output was constrained by limited access to critical mining equipment, stemming from an aging fleet, and by a shortage of alternative ore production headings, but by the end of the third quarter, as mentioned above, the Company made improvements to overcome some of these challenges, and thus increased production. |

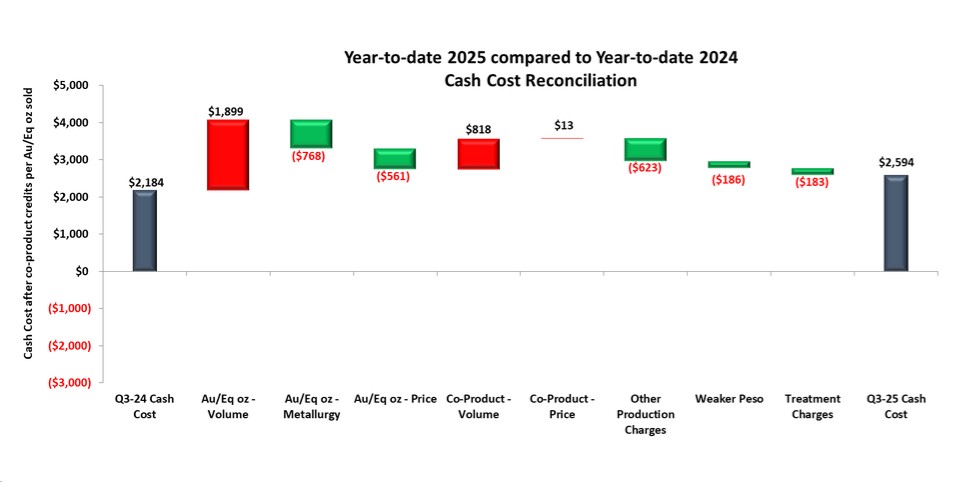

| ● | Total cash cost after co-product credits for the quarter was $2,116 per AuEq ounce, and total all-in sustaining cost (“AISC”) after co-product credits for the quarter was $2,983 per AuEq ounce. (See Item 2—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Measures for a reconciliation of non-GAAP measures to applicable U.S. GAAP measures). |

Liquidity Update

Tonnes produced from the mining operations at DDGM year-to-date 2025 remain lower than in the previous year and, except for silver, grades were lower as well. The Company continued to encounter significant issues with equipment availability partway into the third quarter due to the age and condition of some of the critical mining equipment in use at the mine. Due to the challenges with equipment availability, the Company was not able to maintain its projected timeline for mine development and had limited flexibility to mine alternate headings. In addition, the mill continued to experience mechanical issues that resulted in lower throughput, and when combined with the lower tonnes mined, resulted in a production shortfall. To minimize the mechanical issues and return the mine to a cash positive position, the Company engaged a third-party contract miner during the third quarter of 2025

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 3 and started to upgrade its mining fleet.

As a result, by the end of the third quarter, the Company was able to increase production from a number of production headings.

The Company believes that the mine has the potential to generate positive cash flow based on the information to date from the new Three Sisters area, as well as other zones that have been discovered near existing headings. The Company is in the process of developing access to and drill-defining these new areas. With the improvements mentioned above, the Company is expecting the remaining months of 2025 to result in positive operating income.

In 2025, the Company has been focused on improving its cash position through the issuance of debt and equity. The Company raised $2.5 million through a registered direct offering in January 2025. In September 2025, the Company closed on a second registered direct offering of $11.4 million for the sale of 25,315,954 shares of the Company’s common stock at a price of $0.45 per share. The Company issued 14,204,846 of these shares, for the fair value of approximately $6.4 million, to fully pay off the term loan received in June 2025 as a non-cash equity settlement. In February 2025, the Company sold its interest in Green Light Metals for $0.9 million in proceeds. On May 7, 2025, the Company received a tax refund of 79.6 million pesos (approximately $4.0 million) related to DDGM taxes paid in 2023. During the nine months ended September 30, 2025, the Company raised approximately $8.6 million through its At-The-Market Offering (“ATM”) Program, after deducting the agent’s commissions and other expenses.

Although the Company has significantly improved its financial position year to date, the lower production and grades from the mine through the third quarter of 2025 raise substantial doubt about the Company’s ability to continue as a going concern, as reflected by the year-to-date net losses of $24.5 million and the cash used in operations of $2.5 million. Although the Company believes that there is adequate financing in place to cover the planned underground development and equipment improvements, there can be no assurances that the Company will achieve short-term production targets and therefore may continue with liquidity concerns.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 4 PART I - FINANCIAL INFORMATION

ITEM 1. Financial Statements

GOLD RESOURCE CORPORATION

CONDENSED CONSOLIDATED INTERIM BALANCE SHEETS

(U.S. dollars in thousands, except share amounts)

(Unaudited)

|

|

As of |

|

As of |

||

|

|

September 30, |

|

December 31, |

||

|

Note |

2025 |

|

2024 |

||

ASSETS |

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

9,797 |

|

$ |

1,628 |

Accounts receivable, net |

|

|

12,939 |

|

|

2,184 |

Inventories, net |

6 |

|

7,196 |

|

|

6,940 |

Prepaid expenses and other current assets |

8 |

|

1,293 |

|

|

5,828 |

Total current assets |

|

|

31,225 |

|

|

16,580 |

Property, plant, and mine development, net |

9 |

|

132,453 |

|

|

128,389 |

Other non-current assets |

10 |

|

661 |

|

|

905 |

Total assets |

|

$ |

164,339 |

|

$ |

145,874 |

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

Accounts payable |

|

$ |

13,857 |

|

$ |

11,258 |

Mining royalty taxes payable, net |

|

|

632 |

|

|

195 |

Accrued expenses and other current liabilities |

11 |

|

3,908 |

|

|

3,031 |

Total current liabilities |

|

|

18,397 |

|

|

14,484 |

Reclamation and remediation liabilities |

13 |

|

12,494 |

|

|

10,669 |

Gold and silver stream agreements liability |

12 |

|

86,491 |

|

|

74,432 |

Deferred tax liabilities, net |

7 |

|

15,264 |

|

|

14,041 |

Contingent consideration |

15 |

|

3,501 |

|

|

3,389 |

Other non-current liabilities |

11 |

|

2,230 |

|

|

1,576 |

Total liabilities |

|

|

138,377 |

|

|

118,591 |

|

|

|

|

|

|

|

Commitments and contingencies |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

Shareholders’ equity: |

|

|

|

|

|

|

Common stock - $0.001 par value, 200,000,000 shares authorized: |

|

|

162 |

|

|

96 |

Additional paid-in capital |

|

|

138,392 |

|

|

115,319 |

Accumulated deficit |

|

|

(105,537) |

|

|

(81,077) |

Treasury stock at cost, 336,398 shares |

|

|

(5,884) |

|

|

(5,884) |

Accumulated other comprehensive loss |

|

|

(1,171) |

|

|

(1,171) |

Total shareholders’ equity |

|

|

25,962 |

|

|

27,283 |

Total liabilities and shareholders’ equity |

|

$ |

164,339 |

|

$ |

145,874 |

The accompanying notes are an integral part of these Condensed Consolidated Interim Financial Statements.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited)

5

GOLD RESOURCE CORPORATION

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF OPERATIONS

(U.S. dollars in thousands, except share and per share amounts)

(Unaudited)

|

|

For the three months ended |

|

For the nine months ended |

||||||||

|

|

September 30, |

|

September 30, |

||||||||

|

Note |

2025 |

|

2024 |

|

2025 |

|

2024 |

||||

|

|

|

|

Restated |

|

|

|

|

Restated |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales, net |

5 |

$ |

24,878 |

|

$ |

13,272 |

|

$ |

48,460 |

|

$ |

52,756 |

Cost of sales: |

|

|

|

|

|

|

|

|

|

|

|

|

Production costs |

|

|

15,613 |

|

|

17,198 |

|

|

39,179 |

|

|

51,074 |

Depreciation and amortization |

|

|

2,610 |

|

|

4,178 |

|

|

7,670 |

|

|

14,221 |

Reclamation and remediation |

|

|

434 |

|

|

566 |

|

|

1,262 |

|

|

1,892 |

Total cost of sales |

|

|

18,657 |

|

|

21,942 |

|

|

48,111 |

|

|

67,187 |

Mine gross profit (loss) |

|

|

6,221 |

|

|

(8,670) |

|

|

349 |

|

|

(14,431) |

Costs and expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

General and administrative expenses |

|

|

1,205 |

|

|

1,293 |

|

|

2,993 |

|

|

2,975 |

Mexico exploration expenses |

|

|

799 |

|

|

767 |

|

|

1,649 |

|

|

1,850 |

Michigan Back Forty Project expenses |

|

|

191 |

|

|

177 |

|

|

562 |

|

|

524 |

Stock-based compensation |

19 |

|

403 |

|

|

203 |

|

|

1,198 |

|

|

647 |

Other expense, net |

20 |

|

7,337 |

|

|

5,175 |

|

|

16,952 |

|

|

14,246 |

Total costs and expenses |

|

|

9,935 |

|

|

7,615 |

|

|

23,354 |

|

|

20,242 |

Loss before income taxes |

|

|

(3,714) |

|

|

(16,285) |

|

|

(23,005) |

|

|

(34,673) |

Income tax provision (benefit) |

7 |

|

941 |

|

|

(3,608) |

|

|

1,455 |

|

|

10,686 |

Net loss |

|

$ |

(4,655) |

|

$ |

(12,677) |

|

$ |

(24,460) |

|

$ |

(45,359) |

Net loss per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted net loss per common share |

21 |

$ |

(0.03) |

|

$ |

(0.14) |

|

$ |

(0.19) |

|

$ |

(0.50) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted |

21 |

|

142,909,014 |

|

|

93,279,750 |

|

|

129,081,618 |

|

|

91,005,507 |

The accompanying notes are an integral part of these Condensed Consolidated Interim Financial Statements.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited)

6

GOLD RESOURCE CORPORATION

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

(U.S. dollars in thousands, except share amounts)

(Unaudited)

|

|

For the three months ended September 30, 2025 and 2024 |

||||||||||||||||||

|

|

Number of |

|

Par Value of |

|

Additional Paid- |

|

Accumulated Deficit |

|

Treasury |

|

Accumulated |

|

Total |

||||||

Balance, June 30, 2024 |

|

92,629,246 |

|

$ |

93 |

|

$ |

114,049 |

|

$ |

(57,258) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

49,829 |

Stock-based compensation |

|

- |

|

|

- |

|

|

184 |

|

|

- |

|

|

- |

|

|

- |

|

|

184 |

Issuance of common stock, net of issuance costs (1) |

|

1,230,180 |

|

|

1 |

|

|

598 |

|

|

- |

|

|

- |

|

|

- |

|

|

599 |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(12,677) |

|

|

- |

|

|

- |

|

|

(12,677) |

Balance, September 30, 2024 - Restated |

|

93,859,426 |

|

$ |

94 |

|

$ |

114,831 |

|

$ |

(69,935) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

37,935 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2025 |

|

136,786,129 |

|

$ |

137 |

|

$ |

126,958 |

|

$ |

(100,882) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

19,158 |

Stock-based compensation |

|

- |

|

|

- |

|

|

72 |

|

|

- |

|

|

- |

|

|

- |

|

|

72 |

Registered Direct Offering (2) |

|

11,111,108 |

|

|

11 |

|

|

4,984 |

|

|

- |

|

|

- |

|

|

- |

|

|

4,995 |

Issuance of equity to settle the loan (2) |

|

14,204,846 |

|

|

14 |

|

|

6,378 |

|

|

- |

|

|

- |

|

|

- |

|

|

6,392 |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(4,655) |

|

|

- |

|

|

- |

|

|

(4,655) |

Balance, September 30, 2025 |

|

162,102,083 |

|

$ |

162 |

|

$ |

138,392 |

|

$ |

(105,537) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

25,962 |

| (1) | No shares of the Company’s common stock were sold through the ATM Program during the three months ended September 30, 2025. 1,230,180 shares of the Company’s common stock were sold through the ATM Program during the three months ended September 30, 2024, for net proceeds of approximately $0.6 million to the Company, after deducting the agent’s commissions and other fees. Please also see Note—16 Shareholder’s Equity in Item 1—Condensed Consolidated Interim Financial Statements and Notes (unaudited) for additional information. |

| (2) | In September 2025, the Company closed on a $11.4 million registered direct offering for the sale of 25,315,954 shares of the Company’s common stock at a price of $0.45 per share. The Company issued 14,204,846 of these shares, for the fair value of approximately $6.4 million, to fully pay off the term loan received in June 2025 as a non-cash equity settlement. |

The accompanying notes are an integral part of these Condensed Consolidated Interim Financial Statements.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited)

7

GOLD RESOURCE CORPORATION

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

(U.S. dollars in thousands, except share amounts)

(Unaudited)

|

|

For the nine months ended September 30, 2025 and 2024 |

||||||||||||||||||

|

|

Number of |

|

Par Value of |

|

Additional Paid- |

|

Accumulated Deficit |

|

Treasury |

|

Accumulated |

|

Total |

||||||

Balance, December 31, 2023 |

|

89,030,436 |

|

$ |

89 |

|

$ |

111,970 |

|

$ |

(24,576) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

80,428 |

Stock-based compensation |

|

- |

|

|

- |

|

|

463 |

|

|

- |

|

|

- |

|

|

- |

|

|

463 |

Common stock issued for vested restricted stock units |

|

196,991 |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Issuance of common stock, net of issuance costs (1) |

|

4,708,993 |

|

|

5 |

|

|

2,429 |

|

|

- |

|

|

- |

|

|

- |

|

|

2,434 |

Surrender of common stock for taxes due on vesting |

|

(76,994) |

|

|

- |

|

|

(31) |

|

|

- |

|

|

- |

|

|

- |

|

|

(31) |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(45,359) |

|

|

- |

|

|

- |

|

|

(45,359) |

Balance, September 30, 2024 - Restated |

|

93,859,426 |

|

$ |

94 |

|

$ |

114,831 |

|

$ |

(69,935) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

37,935 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2024 |

|

95,661,347 |

|

$ |

96 |

|

$ |

115,319 |

|

$ |

(81,077) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

27,283 |

Stock-based compensation |

|

- |

|

|

- |

|

|

278 |

|

|

- |

|

|

- |

|

|

- |

|

|

278 |

Common stock issued for vested restricted stock units |

|

577,529 |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Issuance of common stock, net of issuance costs (1) |

|

25,139,655 |

|

|

25 |

|

|

8,615 |

|

|

- |

|

|

- |

|

|

- |

|

|

8,640 |

Surrender of common stock for taxes due on vesting |

|

(283,642) |

|

|

- |

|

|

(93) |

|

|

- |

|

|

- |

|

|

- |

|

|

(93) |

Equity settlement of PSUs and DSUs (2) |

|

66,240 |

|

|

- |

|

|

42 |

|

|

- |

|

|

- |

|

|

- |

|

|

42 |

Registered Direct Offerings (3) |

|

26,736,108 |

|

|

27 |

|

|

7,468 |

|

|

- |

|

|

- |

|

|

- |

|

|

7,495 |

Issuance of equity to settle the loan (3) |

|

14,204,846 |

|

|

14 |

|

|

6,378 |

|

|

- |

|

|

- |

|

|

- |

|

|

6,392 |

Warrants (4) |

|

- |

|

|

- |

|

|

385 |

|

|

- |

|

|

- |

|

|

- |

|

|

385 |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(24,460) |

|

|

- |

|

|

- |

|

|

(24,460) |

Balance, September 30, 2025 |

|

162,102,083 |

|

$ |

162 |

|

$ |

138,392 |

|

$ |

(105,537) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

25,962 |

| (1) | An aggregate of 25,139,655 shares of the Company’s common stock were sold through the ATM Program during the nine months ended September 30, 2025, for proceeds of approximately $8.6 million to the Company, after deducting the agent’s commissions and other fees. 4,708,993 shares of the Company’s common stock were sold through the ATM Program during the nine months ended September 30, 2024, for proceeds of approximately $2.4 million to the Company, after deducting the agent’s commissions and other fees. Please also see Note—15 Shareholder’s Equity in Item 1—Condensed Consolidated Interim Financial Statements and Notes (unaudited) for additional information. |

| (2) | In connection with the departure of Alberto Reyes, the Company’s former Chief Operating Officer, 90,311 of performance share units (“PSUs”) held by Mr. Reyes as of the date of his separation were immediately vested and paid out to Mr. Reyes in shares of the Company’s common stock in the amount equal to the value of such PSUs to which Mr. Reyes would have been entitled as if 100% of the target performance measures related to such PSUs were achieved. The PSUs were settled by issuing 42,265 shares of common stock, with 48,066 PSUs forfeited for taxes. Additionally, 51,242 outstanding deferred share units (“DSUs”) were paid out to Mr. Reyes in shares of the Company’s common stock by issuing 23,975 common shares, with 27,267 DSUs forfeited for taxes. |

| (3) | In January 2025, the Company closed a registered direct offering of 15,625,000 shares of the Company’s common stock at a price of $0.16 per share. In September 2025, the Company closed on a second registered direct offering of $11.4 million for the sale of 25,315,954 shares of the Company’s common stock at a price of $0.45 per share. The Company issued 14,204,846 of these shares, for the fair value of approximately $6.4 million, to fully pay off the term loan received in June 2025 as a non-cash equity settlement. |

| (4) | In connection to the loan the Company received on June 26, 2025, the Company issued a common stock purchase warrant for the purchase of up to 1,500,000 shares of the Company’s common stock at an exercise price per share of $0.65. These warrants qualified for equity accounting and were valued using a Black-Scholes model. |

The accompanying notes are an integral part of these Condensed Consolidated Interim Financial Statements.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 8 CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS

GOLD RESOURCE CORPORATION

(U.S. dollars in thousands)

(Unaudited)

|

|

For the nine months ended September 30, |

||||

|

Note |

2025 |

|

2024 |

||

|

|

|

|

|

Restated |

|

Cash flows from operating activities: |

|

|

|

|

|

|

Net loss |

|

$ |

(24,460) |

|

$ |

(45,359) |

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

Deferred income tax expense |

|

|

1,205 |

|

|

10,509 |

Depreciation and amortization |

|

|

8,423 |

|

|

15,589 |

Stock-based compensation |

|

|

1,198 |

|

|

647 |

Interest on streaming liabilities |

|

|

12,059 |

|

|

9,612 |

Other operating adjustments, net |

23 |

|

2,927 |

|

|

4,446 |

Changes in operating assets and liabilities: |

|

|

|

|

|

|

Accounts receivable |

|

|

(10,755) |

|

|

(1,078) |

Inventories |

|

|

(536) |

|

|

1,185 |

Prepaid expenses and other current assets |

|

|

879 |

|

|

(246) |

Other non-current assets |

|

|

(260) |

|

|

(154) |

Accounts payable and other accrued liabilities |

|

|

2,440 |

|

|

4,011 |

Cash settled liability awards |

|

|

(33) |

|

|

(67) |

Mining royalty and income taxes payable, net |

|

|

4,453 |

|

|

(1,048) |

Net cash used in operating activities |

|

|

(2,460) |

|

|

(1,953) |

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

Capital expenditures |

|

|

(12,186) |

|

|

(6,353) |

Proceeds from the sale of investment in Green Light Metals |

|

|

854 |

|

|

1,178 |

Net cash used in investing activities |

|

|

(11,332) |

|

|

(5,175) |

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

Net proceeds from note payable |

|

|

6,114 |

|

|

- |

Proceeds from ATM Program sales, net of issuance costs |

|

|

8,640 |

|

|

2,434 |

Net proceeds from the Registered Direct Offerings |

|

|

7,495 |

|

|

- |

Other financing activities |

|

|

(138) |

|

|

(33) |

Net cash provided by financing activities |

|

|

22,111 |

|

|

2,401 |

Effect of exchange rate changes on cash and cash equivalents |

|

|

(150) |

|

|

(175) |

|

|

|

|

|

|

|

Net increase (decrease) in cash and cash equivalents |

|

|

8,169 |

|

|

(4,902) |

Cash and cash equivalents at beginning of period |

|

|

1,628 |

|

|

6,254 |

Cash and cash equivalents at end of period |

|

$ |

9,797 |

|

$ |

1,352 |

|

|

|

|

|

|

|

Supplemental Cash Flow Information |

|

|

|

|

|

|

Income and mining taxes paid |

|

$ |

(71) |

|

$ |

1,088 |

Non-cash investing or financing activities: |

|

|

|

|

|

|

Value of common shares issued for share-based compensation redemption |

|

$ |

161 |

|

$ |

49 |

Value of common shares issued to extinguish term loan |

|

$ |

6,397 |

|

$ |

- |

Balance of capital expenditures in accounts payable |

|

$ |

1,226 |

|

$ |

386 |

Balance of equipment financing |

|

$ |

457 |

|

$ |

1,041 |

The accompanying notes are an integral part of these Condensed Consolidated Interim Financial Statements.

GOLD RESOURCE CORPORATION

NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

September 30, 2025

(Unaudited)

1. Basis of Preparation of Financial Statements

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 9 The Condensed Consolidated Interim Financial Statements (“interim financial statements”) of Gold Resource Corporation and its subsidiaries (collectively, the “Company”) are unaudited and have been prepared in accordance with the rules of the Securities and Exchange Commission (“SEC”) for interim statements. Certain information and footnote disclosures required by United States Generally Accepted Accounting Principles (“U.S. GAAP”) have been condensed or omitted as permitted by such rules. However, the Company believes that the disclosures included are adequate to make the information presented not misleading. In the opinion of management, all adjustments (including normal recurring adjustments) and disclosures necessary for a fair presentation of these interim financial statements have been included. The results reported in these interim financial statements do not necessarily indicate the results that may be reported for the entire year. These interim financial statements should be read in conjunction with the audited consolidated financial statements for the year ended December 31, 2024, included in the Company’s annual report on Form 10-K (the “2024 Annual Report”). The year-end balance sheet data was derived from the audited financial statements. Unless otherwise noted, there have been no material changes to the footnotes from those accompanying the audited consolidated financial statements contained in the 2024 Annual Report.

2. Restatement of Financial Statements

The interim unaudited condensed consolidated financial statements include corrections to the three and nine months periods ended September 30, 2024, which were presented in Note 24 to the consolidated financial statements for the year ended December 31, 2024, in the Company’s 2024 Form 10-K filed on April 8, 2025. During the preparation of the consolidated financial statements for the year ended December 31, 2024, management of the Company identified that liabilities related to the Company’s Back Forty Project with respect to the Gold and Silver Stream Agreements with Osisko (the “Osisko Stream Agreements”) were incorrectly presented in the Company’s financial statements due to errors in the application of U.S. GAAP. The errors related to the calculation of interest accretion over the liabilities associated with the Osisko Stream Agreements (the “streaming liabilities”). It was determined that the streaming liabilities should be accounted for under Financial Accounting Standards Board’s Accounting Standards Codification 606, Revenue from Contracts with Customers, and that a significant financing component is present that should be accreted using the effective interest method. The resulting errors understated the streaming liabilities and net loss for all the impacted periods noted below.

The correction to the Company’s consolidated statements of operations also impacts the Company’s consolidated balance sheets, consolidated statements of changes in shareholders’ equity, consolidated statements of cash flows, and certain notes to the consolidated financial statements.

In the restated presentation, the Company also recorded previously uncorrected misstatements that were determined to be immaterial to the financial statements in prior periods.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 10 The following table presents the Company’s restatement impact in the unaudited condensed consolidated statement of operations for the three and nine months ended September 30, 2024:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS |

||||||||||||||||

|

|

For the three months ended September 30, 2024 |

|

For the nine months ended September 30, 2024 |

||||||||||||||

|

|

As Previously |

|

Restatement |

|

Restated |

|

As Previously |

|

Restatement |

|

Restated |

||||||

|

|

(U.S. dollars in thousands, except share and per share amounts) |

||||||||||||||||

Sales, net |

|

$ |

13,272 |

|

$ |

- |

|

$ |

13,272 |

|

$ |

52,756 |

|

$ |

- |

|

$ |

52,756 |

Cost of sales: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Production costs |

|

|

17,198 |

|

|

- |

|

|

17,198 |

|

|

51,074 |

|

|

- |

|

|

51,074 |

Depreciation and amortization |

|

|

4,178 |

|

|

- |

|

|

4,178 |

|

|

14,221 |

|

|

- |

|

|

14,221 |

Reclamation and remediation |

|

|

566 |

|

|

- |

|

|

566 |

|

|

1,892 |

|

|

- |

|

|

1,892 |

Total cost of sales |

|

|

21,942 |

|

|

- |

|

|

21,942 |

|

|

67,187 |

|

|

- |

|

|

67,187 |

Mine gross loss |

|

|

(8,670) |

|

|

- |

|

|

(8,670) |

|

|

(14,431) |

|

|

- |

|

|

(14,431) |

Costs and expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General and administrative expenses |

|

|

1,293 |

|

|

- |

|

|

1,293 |

|

|

2,975 |

|

|

- |

|

|

2,975 |

Mexico exploration expenses |

|

|

767 |

|

|

- |

|

|

767 |

|

|

1,850 |

|

|

- |

|

|

1,850 |

Michigan Back Forty Project expenses |

|

|

202 |

|

|

(25) |

|

|

177 |

|

|

549 |

|

|

(25) |

|

|

524 |

Stock-based compensation |

|

|

203 |

|

|

- |

|

|

203 |

|

|

647 |

|

|

- |

|

|

647 |

Other expense, net |

|

|

2,977 |

|

|

2,198 |

|

|

5,175 |

|

|

10,846 |

|

|

3,400 |

|

|

14,246 |

Total costs and expenses |

|

|

5,442 |

|

|

2,173 |

|

|

7,615 |

|

|

16,867 |

|

|

3,375 |

|

|

20,242 |

Loss before income taxes |

|

|

(14,112) |

|

|

(2,173) |

|

|

(16,285) |

|

|

(31,298) |

|

|

(3,375) |

|

|

(34,673) |

Income tax (benefit) provision |

|

|

(3,617) |

|

|

9 |

|

|

(3,608) |

|

|

10,952 |

|

|

(266) |

|

|

10,686 |

Net loss |

|

$ |

(10,495) |

|

$ |

(2,182) |

|

$ |

(12,677) |

|

$ |

(42,250) |

|

$ |

(3,109) |

|

$ |

(45,359) |

Net loss per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted net loss per common share |

|

$ |

(0.11) |

|

$ |

(0.03) |

|

$ |

(0.14) |

|

$ |

(0.46) |

|

$ |

(0.04) |

|

$ |

(0.50) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted |

|

|

93,279,750 |

|

|

- |

|

|

93,279,750 |

|

|

91,005,507 |

|

|

- |

|

|

91,005,507 |

The following table presents the Company’s restatement impact in the unaudited condensed consolidated statement of changes in shareholders’ equity for the three months ended September 30, 2024:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS' EQUITY |

||||||||||||||||||

|

|

For the three months ended September 30, 2024 |

||||||||||||||||||

|

|

Number of |

|

Par Value of |

|

Additional Paid- |

|

Retained |

|

Treasury |

|

Accumulated |

|

Total |

||||||

As Previously Reported |

|

(U.S. dollars in thousands, except share amounts) |

||||||||||||||||||

Balance, June 30, 2024 |

|

92,629,246 |

|

$ |

93 |

|

$ |

114,049 |

|

$ |

(40,066) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

67,021 |

Stock-based compensation |

|

- |

|

|

- |

|

|

184 |

|

|

- |

|

|

- |

|

|

- |

|

|

184 |

Issuance of common stock, net of issuance costs |

|

1,230,180 |

|

|

1 |

|

|

598 |

|

|

- |

|

|

- |

|

|

- |

|

|

599 |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(10,495) |

|

|

- |

|

|

- |

|

|

(10,495) |

Balance, September 30, 2024 |

|

93,859,426 |

|

$ |

94 |

|

$ |

114,831 |

|

$ |

(50,561) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

57,309 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Restatement Impacts |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2024 |

|

- |

|

$ |

- |

|

$ |

- |

|

$ |

(17,192) |

|

$ |

- |

|

$ |

- |

|

$ |

(17,192) |

Stock-based compensation |

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Issuance of common stock, net of issuance costs |

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(2,182) |

|

|

- |

|

|

- |

|

|

(2,182) |

Balance, September 30, 2024 |

|

- |

|

$ |

- |

|

$ |

- |

|

$ |

(19,374) |

|

$ |

- |

|

$ |

- |

|

$ |

(19,374) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Restated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2024 |

|

92,629,246 |

|

$ |

93 |

|

$ |

114,049 |

|

$ |

(57,258) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

49,829 |

Stock-based compensation |

|

- |

|

|

- |

|

|

184 |

|

|

- |

|

|

- |

|

|

- |

|

|

184 |

Issuance of common stock, net of issuance costs |

|

1,230,180 |

|

|

1 |

|

|

598 |

|

|

- |

|

|

- |

|

|

- |

|

|

599 |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(12,677) |

|

|

- |

|

|

- |

|

|

(12,677) |

Balance, September 30, 2024 |

|

93,859,426 |

|

$ |

94 |

|

$ |

114,831 |

|

$ |

(69,935) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

37,935 |

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 11 The following table presents the Company’s restatement impact in the unaudited condensed consolidated statement of changes in shareholders’ equity for the nine months ended September 30, 2024:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS' EQUITY |

||||||||||||||||||

|

|

For the nine months ended September 30, 2024 |

||||||||||||||||||

|

|

Number of |

|

Par Value of |

|

Additional Paid- |

|

Retained |

|

Treasury |

|

Accumulated |

|

Total |

||||||

As Previously Reported |

|

(U.S. dollars in thousands, except share amounts) |

||||||||||||||||||

Balance, December 31, 2023 |

|

89,030,436 |

|

$ |

89 |

|

$ |

111,970 |

|

$ |

(8,311) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

96,693 |

Stock-based compensation |

|

- |

|

|

- |

|

|

463 |

|

|

- |

|

|

- |

|

|

- |

|

|

463 |

Common stock issued for vested restricted stock units |

|

196,991 |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Issuance of common stock, net of issuance costs |

|

4,708,993 |

|

|

5 |

|

|

2,429 |

|

|

- |

|

|

- |

|

|

- |

|

|

2,434 |

Surrender of common stock for taxes due on vesting |

|

(76,994) |

|

|

- |

|

|

(31) |

|

|

- |

|

|

- |

|

|

- |

|

|

(31) |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(42,250) |

|

|

- |

|

|

- |

|

|

(42,250) |

Balance, September 30, 2024 |

|

93,859,426 |

|

$ |

94 |

|

$ |

114,831 |

|

$ |

(50,561) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

57,309 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Restatement Impacts |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2023 |

|

- |

|

$ |

- |

|

$ |

- |

|

$ |

(16,265) |

|

$ |

- |

|

$ |

- |

|

$ |

(16,265) |

Stock-based compensation |

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Common stock issued for vested restricted stock units |

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Issuance of common stock, net of issuance costs |

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Surrender of common stock for taxes due on vesting |

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(3,109) |

|

|

- |

|

|

- |

|

|

(3,109) |

Balance, September 30, 2024 |

|

- |

|

$ |

- |

|

$ |

- |

|

$ |

(19,374) |

|

$ |

- |

|

$ |

- |

|

$ |

(19,374) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Restated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2023 |

|

89,030,436 |

|

$ |

89 |

|

$ |

111,970 |

|

$ |

(24,576) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

80,428 |

Stock-based compensation |

|

- |

|

|

- |

|

|

463 |

|

|

- |

|

|

- |

|

|

- |

|

|

463 |

Common stock issued for vested restricted stock units |

|

196,991 |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

Issuance of common stock, net of issuance costs |

|

4,708,993 |

|

|

5 |

|

|

2,429 |

|

|

- |

|

|

- |

|

|

- |

|

|

2,434 |

Surrender of common stock for taxes due on vesting |

|

(76,994) |

|

|

- |

|

|

(31) |

|

|

- |

|

|

- |

|

|

- |

|

|

(31) |

Net loss |

|

- |

|

|

- |

|

|

- |

|

|

(45,359) |

|

|

- |

|

|

- |

|

|

(45,359) |

Balance, September 30, 2024 |

|

93,859,426 |

|

$ |

94 |

|

$ |

114,831 |

|

$ |

(69,935) |

|

$ |

(5,884) |

|

$ |

(1,171) |

|

$ |

37,935 |

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 12 The following table presents the Company’s restatement impact in the unaudited condensed consolidated statement of cash flows for the nine months ended September 30, 2024:

|

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS |

|||||||

|

For the nine months ended September 30, 2024 |

|||||||

|

As Previously |

|

Restatement |

|

Restated |

|||

|

(U.S. dollars in thousands) |

|||||||

Cash flows from operating activities: |

|

|

|

|

|

|

|

|

Net loss |

$ |

(42,250) |

|

$ |

(3,109) |

|

$ |

(45,359) |

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

|

|

Deferred income tax expense (benefit) |

|

10,775 |

|

|

(266) |

|

|

10,509 |

Depreciation and amortization |

|

15,589 |

|

|

- |

|

|

15,589 |

Stock-based compensation |

|

647 |

|

|

- |

|

|

647 |

Interest on streaming liabilities |

|

6,356 |

|

|

3,256 |

|

|

9,612 |

Other operating adjustments, net |

|

4,446 |

|

|

- |

|

|

4,446 |

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

Accounts receivable |

|

(1,078) |

|

|

- |

|

|

(1,078) |

Inventories |

|

1,185 |

|

|

- |

|

|

1,185 |

Prepaid expenses and other current assets |

|

(1,291) |

|

|

1,045 |

|

|

(246) |

Other non-current assets |

|

(154) |

|

|

- |

|

|

(154) |

Accounts payable and other accrued liabilities |

|

4,937 |

|

|

(926) |

|

|

4,011 |

Cash settled liability awards |

|

(67) |

|

|

- |

|

|

(67) |

Mining royalty and income taxes payable, net |

|

(1,048) |

|

|

- |

|

|

(1,048) |

Net cash used in operating activities |

|

(1,953) |

|

|

- |

|

|

(1,953) |

|

|

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

Capital expenditures |

|

(6,353) |

|

|

- |

|

|

(6,353) |

Proceeds from the sale of investment in Maritime |

|

1,178 |

|

|

- |

|

|

1,178 |

Net cash used in investing activities |

|

(5,175) |

|

|

- |

|

|

(5,175) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

Proceeds from the ATM sales, net of issuance costs |

|

2,434 |

|

|

- |

|

|

2,434 |

Other financing activities |

|

(33) |

|

|

- |

|

|

(33) |

Net cash provided by financing activities |

|

2,401 |

|

|

- |

|

|

2,401 |

Effect of exchange rate changes on cash and cash equivalents |

|

(175) |

|

|

- |

|

|

(175) |

|

|

|

|

|

|

|

|

|

Net decrease in cash and cash equivalents |

|

(4,902) |

|

|

- |

|

|

(4,902) |

Cash and cash equivalents at beginning of period |

|

6,254 |

|

|

- |

|

|

6,254 |

Cash and cash equivalents at end of period |

$ |

1,352 |

|

$ |

- |

|

$ |

1,352 |

|

|

|

|

|

|

|

|

|

Supplemental Cash Flow Information |

|

|

|

|

|

|

|

|

Income and mining taxes paid |

$ |

1,088 |

|

$ |

- |

|

$ |

1,088 |

Non-cash investing or financing activities: |

|

|

|

|

|

|

|

|

Value of common shares issued for RSU redemption |

$ |

49 |

|

$ |

- |

|

$ |

49 |

Balance of capital expenditures in accounts payable |

$ |

385 |

|

$ |

1 |

|

$ |

386 |

Balance of equipment financing |

$ |

1,041 |

|

$ |

- |

|

$ |

1,041 |

3. New Accounting Pronouncements

The FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvement to Income Tax Disclosures in December 2023, amending income tax disclosure requirements for the effective tax rate reconciliation and income taxes paid. The amendments in ASU 2023-09 are effective for fiscal years beginning after December 15, 2024, and are applied prospectively with retrospective application permitted. The Company is evaluating the impact this guidance will have on the disclosures in the consolidated financial statements.

In November 2024, the FASB issued ASU 2024-03, Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40) to improve the disclosures about a public business entity’s expense and provide more detailed information about the types of expenses included in certain expense captions in the consolidated financial statements. The amendments in this update are effective for annual reporting periods beginning after December

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 13 15, 2026, and interim reporting periods beginning after December 15, 2027.

Early adoption is permitted and the amendments in this update should be applied either prospectively or retrospectively. The Company is evaluating the impact this guidance will have on the disclosures in the consolidated financial statements.

4. Going Concern

In accordance with Accounting Standards Codification (“ASC”) 205-40, Going Concern, ("ASC 205-40"), the Company evaluated whether there are conditions and events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern within one year after the date on which this Quarterly Report on Form 10-Q is filed. The accompanying interim financial statements have been prepared assuming that the Company will continue as a going concern. Although the Company made some improvement in 2025, the Company’s financial position and operating results, along with the Company’s inability to achieve its production estimates through the third quarter of 2025, raise substantial doubt about the Company’s ability to continue as a going concern, as reflected by the year-to-date net losses of $24.5 million and the cash used in operations of $2.5 million. The interim financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern.

To improve its cash position, during the nine months ended September 30, 2025, the Company raised approximately $8.6 million through its ATM Program, after deducting the agent’s commissions and other expenses. The Company has raised gross proceeds of approximately $2.5 million through a registered direct offering in January. In September 2025, the Company closed on a second registered direct offering of $11.4 million for the sale of 25,315,954 shares of the Company’s common stock at a price of $0.45 per share. The Company issued 14,204,846 of these shares, for the fair value of approximately $6.4 million, to fully pay off the term loan received in June 2025 as a non-cash equity settlement, as further described in Note 14. In February 2025, the Company sold its interest in Green Light Metals for $0.9 million, and on May 7, 2025, the Company received the previously disclosed tax refund of 76 million pesos from the overpayment of Mexico taxes by DDGM in 2023, plus an inflation adjustment, for a total of 79.6 million pesos (approximately $4.0 million). In connection with the loan agreement described in Note 14, the Company has issued a common stock purchase warrant to an affiliate of one of the private investors for the purchase of up to 1,500,000 shares of the Company’s common stock at an exercise price per share of $0.65, the aggregate exercise proceeds of which may provide additional funds for the Company.

For the nine months ended September 30, 2025, the Company has raised a net total of $27.2 million through these efforts. However, there can be no assurances that the mine revenue will be sufficient to generate profits and positive cash flows from operations in the future, and the Company may be compelled to place the mine on “care and maintenance” status and cease operations if additional sources of capital is required and not available at such time.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 14 The Company derives its revenue mainly from the sale of concentrates.

5. Revenue

The following table presents the Company’s net sales for each period presented, disaggregated by source:

|

|

For the three months ended September 30, |

|

For the nine months ended September 30, |

||||||||

|

|

2025 |

|

2024 |

|

2025 |

|

2024 |

||||

|

|

(in thousands) |

|

(in thousands) |

||||||||

Doré sales, net |

|

|

|

|

|

|

|

|

|

|

|

|

Gold |

|

$ |

126 |

|

$ |

- |

|

$ |

1,213 |

|

$ |

24 |

Silver |

|

|

9 |

|

|

- |

|

|

54 |

|

|

1 |

Less: Refining charges |

|

|

(1) |

|

|

- |

|

|

(10) |

|

|

(6) |

Total doré sales, net |

|

|

134 |

|

|

- |

|

|

1,257 |

|

|

19 |

Concentrate sales |

|

|

|

|

|

|

|

|

|

|

|

|

Gold |

|

|

4,858 |

|

|

3,416 |

|

|

9,166 |

|

|

17,173 |

Silver |

|

|

17,271 |

|

|

5,424 |

|

|

29,825 |

|

|

17,332 |

Copper |

|

|

659 |

|

|

917 |

|

|

1,545 |

|

|

5,099 |

Lead |

|

|

417 |

|

|

918 |

|

|

1,481 |

|

|

3,342 |

Zinc |

|

|

1,868 |

|

|

4,045 |

|

|

6,390 |

|

|

13,108 |

Less: Treatment and refining charges |

|

|

(607) |

|

|

(1,394) |

|

|

(1,602) |

|

|

(4,410) |

Total concentrate sales, net |

|

|

24,466 |

|

|

13,326 |

|

|

46,805 |

|

|

51,644 |

Realized gain - embedded derivative, net (1) |

|

|

20 |

|

|

344 |

|

|

76 |

|

|

1,333 |

Unrealized gain (loss) - embedded derivative, net |

|

|

258 |

|

|

(398) |

|

|

322 |

|

|

(240) |

Total sales, net |

|

$ |

24,878 |

|

$ |

13,272 |

|

$ |

48,460 |

|

$ |

52,756 |

| (1) | Copper lead, and zinc are co-products. In the realized gain - embedded derivative, net, there is $51 thousand loss and $139 thousand loss related to these co-products for the three and nine months ended September 30, 2025, respectively. There is $0.2 million and $0.5 million gain, in the realized gain - embedded derivative, net, related to the co-products for both the three and nine months ended September 30, 2024, respectively. |

6. Inventories, net

At September 30, 2025 and December 31, 2024, inventories, net, consisted of the following:

|

|

As of |

|

As of |

||

|

|

September 30, |

|

December 31, |

||

|

|

2025 |

|

2024 |

||

|

|

(in thousands) |

||||

Stockpiles - underground mine |

|

$ |

340 |

|

$ |

73 |

Concentrates |

|

|

1,859 |

|

|

902 |

Doré, net |

|

|

- |

|

|

169 |

Subtotal - product inventories |

|

|

2,199 |

|

|

1,144 |

Materials and supplies (1) |

|

|

4,997 |

|

|

5,796 |

Total |

|

$ |

7,196 |

|

$ |

6,940 |

| (1) | Net of reserve for obsolescence of $1.1 million and $0.7 million as of September 30, 2025 and December 31, 2024, respectively. |

7. Income Taxes

The Company recorded an income tax expense of $1.5 million for the nine months ended September 30, 2025. For the nine months ended September 30, 2024, the Company recorded an income tax expense of $10.7 million. In accordance with applicable accounting rules, the interim provision for taxes is calculated using the estimated consolidated annual effective tax rate. The consolidated effective tax rate is a function of the combined effective tax rates for the jurisdictions in which the Company operates. Variations in the relative proportions of jurisdictional income could result in fluctuations

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 15 to the Company’s consolidated effective tax rate.

At the federal level, the Company’s income in the U.S. is taxed at 21%. Income in Mexico is taxed at 38.5% (30% income tax and 8.5% mining tax), and Canada’s income is taxed at a combined federal and provincial rate of 26.5%, which results in a consolidated effective tax rate above statutory U.S. Federal rates.

On July 4, 2025, the One Big Beautiful Bill Act (the “OBBBA”) was enacted in the U.S. The OBBBA permanently extends multiple tax provisions of the 2017 Tax Cuts and Jobs Act, as well as repeals, modifies, and introduces various other tax provisions. The legislation has multiple effective dates, with certain provisions effective in 2025 and others implemented through 2027. The Company does not anticipate the bill will have a material impact on the consolidated financial statements.

Mexico Valuation Allowance

The Company recorded a valuation allowance on all of the Mexico Income Tax net deferred tax assets in 2024 and has continued with a valuation allowance on all of the Mexico Income Tax net deferred tax assets as of September 30, 2025. In accordance with applicable accounting rules, a valuation allowance is recorded when it is more likely than not that some portion of the deferred tax assets will not be realized, after considering all available evidence, both positive and negative. The Company determined a valuation allowance on Mexico Income Tax deferred tax assets was necessary due primarily to the recent losses at the Mexico mine.

Mexico Mining Taxation

Mining entities in Mexico are subject to two mining duties, in addition to the 30% Mexico corporate income tax: (i) a “special” mining duty of 8.5%, effective January 1, 2025, of taxable income as defined under Mexican tax law (also referred to as “mining royalty tax”) on extraction activities performed by concession holders, and (ii) the “extraordinary” mining duty of 1.0%, also effective January 1, 2025, on gross revenue from the sale of gold, silver, and platinum. The mining royalty tax generally applies to earnings before income tax, depreciation, depletion, amortization, and interest. In calculating the mining royalty tax, there are no corporate deductions related to depreciable costs from operational fixed assets. However, prospecting and exploration expenses are amortized using a 10% rate in a 10-year straight line. Both duties are tax deductible for income tax purposes. As a result, the Company’s effective tax rate applicable to the Company’s Mexican operations is higher than Mexico’s statutory income tax rate.

The Company periodically transfers funds from its Mexican wholly owned subsidiary to the U.S. as dividends. Mexico requires a 10% Mexico withholding tax on all post-2013 earnings. The Company began distributing post-2013 earnings from Mexico in 2018. According to the existing U.S. – Mexico tax treaty, the dividend withholding tax between these countries is reduced to 5% if certain requirements are met. The Company determined that it had met such requirements and paid a 5% withholding tax on dividends received from Mexico, and as a result, $0.1 million in withholding taxes was paid for the nine months ended September 30, 2024. At the end of 2024, the Company reviewed the tax treaty and believes that it qualifies for a 0% tax withholding. Going forward, the Company will apply a 0% tax withholding on any dividend payments from its Mexico subsidiary. No dividends from Mexico were received by the Company for the nine months ended September 30, 2025.

In October 2023, the Company received a notification from the Mexican Tax Administration Services (“SAT”) with a sanction of 331 million pesos (approximately $18.0 million as of September 30, 2025) as the result of a 2015 tax audit that began in 2021. The 2015 tax audit performed by SAT encompassed various tax aspects, including but not limited to intercompany transactions, mining royalty tax, and extraordinary mining tax. Management is in process of disputing this tax notification and sent a letter of protest to the tax authorities along with providing all requested documentation. Management intends to pursue legal avenues of protest, including filing a lawsuit with the Mexico court system, if necessary, to ensure that these adjustments are removed. Management believes its position taken on the 2015 income tax return meets the more likely than not threshold and that as of September 30, 2025 and December 31, 2024, the Company has no liability for uncertain tax positions. If the Company were to determine there was an unrecognized tax benefit, the Company would recognize the liability and the related interest and penalties within income tax (benefit) provision.

Gold Resource Corporation—Condensed Consolidated Interim Financial Statements and Notes (Unaudited) 16 At September 30, 2025 and December 31, 2024, prepaid expenses and other current assets consisted of the following:

8. Prepaid Expenses and Other Current Assets

|

|

As of |

|

As of |

||

|

|

September 30, |

|

December 31, |

||

|

|

2025 |

|

2024 |

||

|

|

(in thousands) |

||||

Advances to suppliers |

|

$ |

56 |

|

$ |

46 |

Prepaid insurance |

|

|

684 |

|

|

1,121 |

Prepaid income tax |

|

|

- |

|

|

3,906 |

Other current assets |

|

|

553 |

|

|

755 |

Total |

|

$ |

1,293 |

|

$ |

5,828 |

Prepaid income tax