UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported): October 23, 2025

Esquire Financial Holdings, Inc.

(Exact name of the registrant as specified in its charter)

Maryland |

001-38131 |

27-5107901 |

|

(State or other jurisdiction of incorporation or organization) |

(Commission File Number) |

(IRS Employer Identification No.) |

100 Jericho Quadrangle, Suite 100 |

|

|

Jericho, New York |

|

11753 |

(Address of principal executive offices) |

|

(Zip Code) |

(516) 535-2002

(Registrant’s telephone number)

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (See General Instruction A.2. below):

☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4c) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common Stock, $0.01 par value |

|

ESQ |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02Results of Operations and Financial Condition.

On October 23, 2025, Esquire Financial Holdings, Inc. (the “Company”), the holding company for Esquire Bank, National Association (“Esquire Bank”), issued a press release announcing its earnings for the quarter ended September 30, 2025. A copy of the press release is attached as Exhibit 99.1 hereto and incorporated herein by reference.

The information contained in this Item 2.02 and Exhibit 99.1 shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liability of that section, and shall not be incorporated by reference into any filings made by the Company under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, except as expressly set forth by specific reference in such filing.

Item 7.01Regulation FD Disclosure.

Esquire Financial Holdings, Inc. (the “Company”) intends to distribute and make available to investors, and to post on its website, the written presentation attached hereto as Exhibit 99.2. The presentation is furnished in this Current Report on Form 8-K, pursuant to this Item 7.01, as Exhibit 99.2, and is incorporated herein by reference.

The information contained in this Item 7.01 and Exhibit 99.2 shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liability of that section, and shall not be incorporated by reference into any filings made by the Company under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, except as expressly set forth by specific reference in such filing.

Item 9.01Financial Statements and Exhibits.

(d) Exhibits.

Exhibit No. |

|

Description |

99.1 |

|

|

99.2 |

|

Written presentation to be distributed and made available to investors and posted |

104 |

|

Cover Page Interactive Data File (formatted as inline XBRL and contained in Exhibit 101). |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, hereunto duly authorized.

|

ESQUIRE FINANCIAL HOLDINGS, INC. |

|

|

|

|

|

|

Dated: October 23, 2025 |

By:/s/ Andrew C. Sagliocca |

|

Andrew C. Sagliocca |

|

Vice Chairman, Chief Executive Officer and President |

Exhibit 99.1

ESQUIRE FINANCIAL HOLDINGS, INC.

REPORTS THIRD QUARTER 2025 RESULTS

Strong Commercial Loan & Deposit Growth Drives Resilient Net Interest Margin & Record Earnings

Jericho, NY – October 23, 2025 – Esquire Financial Holdings, Inc. (NASDAQ: ESQ) (the “Company”), the financial holding company for Esquire Bank, National Association (“Esquire Bank” or the “Bank”), (collectively “Esquire”) today announced its operating results for the third quarter of 2025. Significant achievements and key performance metrics during the current quarter and year-to-date of 2025 include:

| ● | Net income increased $2.7 million or 23.7% to $14.1 million, or $1.62 per diluted share, in the current quarter as compared to $11.4 million, or $1.34 per diluted share, for the comparable quarter in 2024. On a linked quarter basis, net income increased $2.2 million or 18.2% when compared to $11.9 million, or $1.38 per diluted share. For the current quarter, adjusted(1) net income and diluted earnings per share were $12.8 million and $1.47, respectively, excluding certain discrete tax benefits related to share-based compensation, reducing income taxes by approximately $1.3 million and lowering the effective tax rate to 19.5%. |

| ● | Consistent industry leading returns on average assets and equity of 2.61% and 20.83%, respectively, notwithstanding our continued investment in current resources (both people and technology) to support future growth while also maintaining excess capital levels with an equity to asset ratio of 12.8%. For the current quarter, adjusted(1) returns on average assets and equity of 2.37% and 18.89%, respectively, excluding certain discrete tax benefits noted above. |

| ● | Resilient net interest margin of 6.04% in the current quarter supported by our national litigation platform growth, despite both elevated levels of average interest earning cash balances totaling $189.4 million (generated from average core deposits growth totaling $103.1 million, or 23.4% annualized, on a linked quarter basis), and declines in short-term market interest rates from their highs in the latter part of 2023. Total year-to-date revenue increased $15.4 million, or 16.8%, to $107.2 million when comparing 2025 to 2024. |

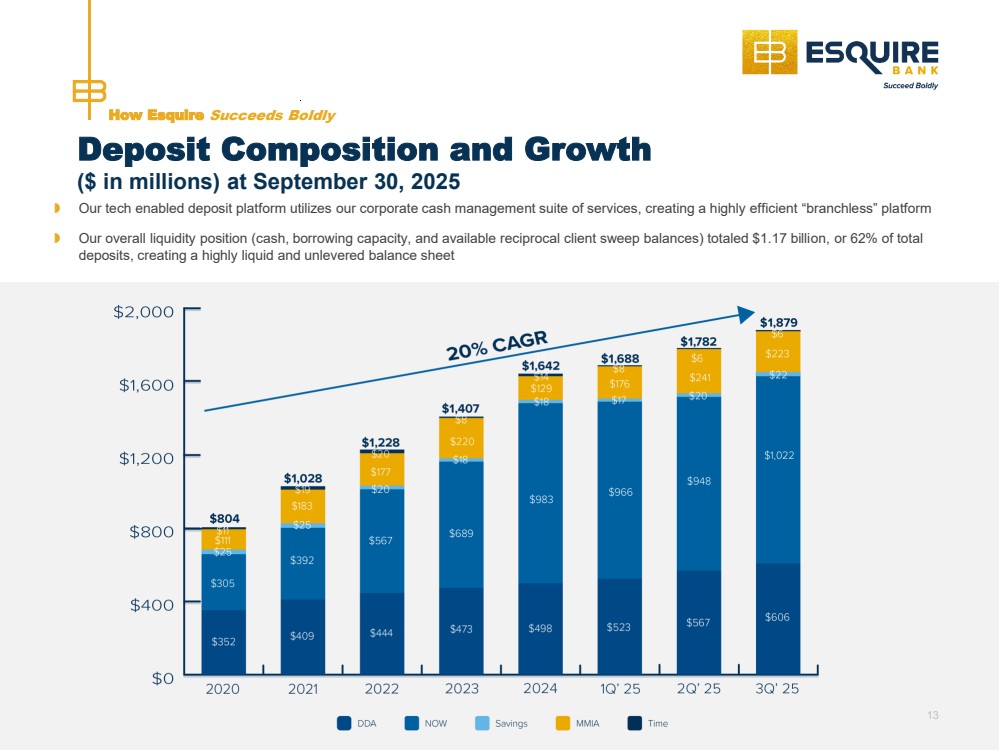

| ● | Continued strong core deposit growth totaling $97.1 million, or 22% annualized, on a linked quarter basis to $1.87 billion, comprised of low-cost commercial relationship deposits with a cost-of-funds of 1.03% (including demand deposits). Deposits grew $343.0 million, or 22%, when comparing the current quarter to the comparable quarter in 2024. Off-balance sheet sweep funds totaled $412 million, with approximately 95% available for additional on-balance sheet liquidity, while the associated administrative service payments (“ASP”) fee income totaled $731 thousand for the current quarter. Additional available liquidity, excluding the aforementioned sweeps, totaled approximately $1.1 billion. |

| ● | Loan growth on a linked quarter basis was $52.4 million, or 14% annualized, totaling $1.55 billion, despite elevated loan payoffs/paydowns of $54.8 million in the quarter while growth year over year was $249.5 million, or 19.2%. Average loan growth on a linked quarter basis was $70.1 million, or 19% annualized. Loan growth was fueled by increases in higher yielding variable rate commercial loans from our national litigation platform totaling $74.6 million, or 33% annualized, on a linked quarter basis. These commercial lending relationships have and will continue to create additional opportunities for future loan draws and core deposit growth (noninterest bearing operating or demand deposits and escrow or IOLTA accounts nationally) through our full service commercial relationship banking and tech-enabled commercial cash management platform. |

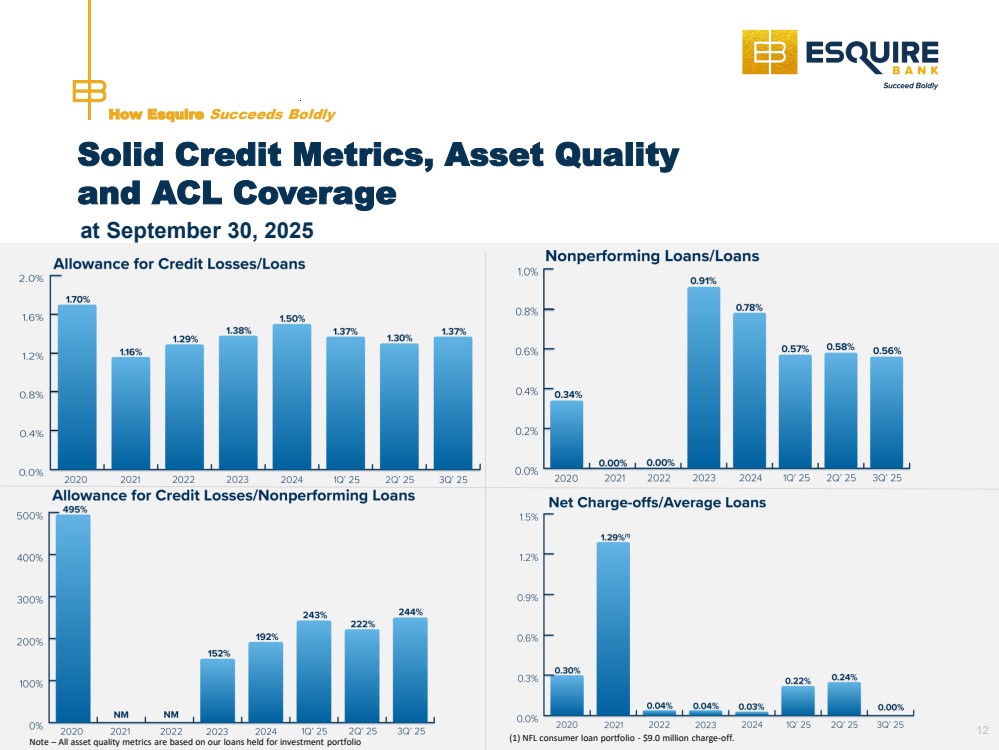

| ● | Solid credit metrics, asset quality, and reserve coverage ratios with an allowance for credit losses to loans ratio of 1.37%, nonperforming loans totaling $8.6 million, and nonperforming loans to total assets ratio of 0.40%. |

| (1) | See non-GAAP reconciliation provided at the end of this news release. |

1

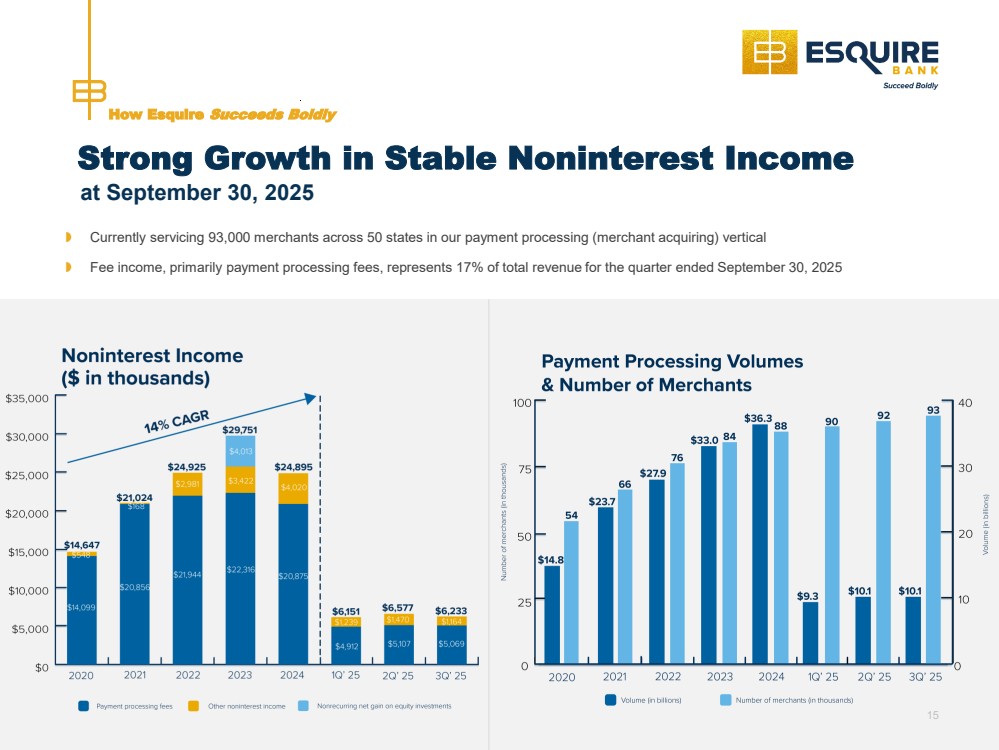

| ● | Stable and consistent noninterest income in the current quarter totaling $6.2 million, or 17% of total revenue, led by our payment processing platform with 93,000 small business clients nationally. Our tech-enabled payments platform allowed us to perform commercial treasury clearing services for $10.1 billion in credit and debit card payment volume, a 9.5% increase from the comparable quarter in 2024, across 151.8 million transactions for our small business clients. |

| ● | Strong efficiency ratio of 48.9% for the current quarter, notwithstanding our investments to support future growth, risk management and excellence in client service as well as the opening of our flagship full service banking facility in Los Angeles, California (Watt Plaza in Century City) to support our current and future clients in Southern California. |

| ● | Entered into a new headquarters lease spanning 50,000 square feet across two floors with dedicated indoor space and 16,000 square feet of outdoor space for employees, clients, and Esquire events in Jericho, NY. The new headquarters will support continued future growth and investment in resources as we execute on our long-term vision. |

| ● | Strong capital foundation with common equity tier 1 (“CET1”) and tangible common equity to tangible asset(2) (“TCE/TA”) ratios of 15.27% and 12.78%, respectively. The Bank remains well above the bank regulatory “Well Capitalized” standards. |

“With another year of industry leading performance and growth, our investment in a new headquarters will position us to attract top talent while providing our teams with a state-of-the-art facility to serve the complex and fragmented national and local verticals we operate, support future expansion, and allow us to continue to deliver exceptional client service,” stated Tony Coelho, Chairman of the Board.

“By deeply understanding and serving our key national verticals and local markets and continuously investing in our future, we've established a strong culture and foundation for sustainable growth and continued industry leadership, as reflected in our top tier performance metrics, resilient net interest margin, and strong core deposit and commercial loan growth on a national basis,” stated Andrew C. Sagliocca, Vice Chairman, Chief Executive Officer, and President.

| (2) | The Bank has no recorded intangible assets on the Statement of Financial Condition, and accordingly, GAAP common equity and GAAP assets are equal to tangible common equity and tangible assets. |

2

Third Quarter 2025 vs. 2024

Net income for the quarter ended September 30, 2025 was $14.1 million, or $1.62 per diluted share, compared to $11.4 million, or $1.34 per diluted share for the same period in 2024. Returns on average assets and equity for the current quarter were 2.61% and 20.83%, respectively, compared to 2.62% and 20.29% for the same period of 2024. Excluding a $1.3 million tax benefit related to share-based compensation, adjusted(1) net income, diluted earnings per share, return on average assets, and return on average common equity for the current quarter ended September 30, 2025 were $12.7 million, $1.47, 2.37% and 18.89%, respectively.

Net interest income increased $5.5 million, or 21.2%, to $31.3 million, due to growth in average interest earning assets totaling $389.0 million, or 23.3%, to $2.06 billion, funded with low-cost core deposits from our regional business development teams and relationship banking efforts. Our net interest margin of 6.04% decreased 12 basis points from 2024 as increases in higher yielding loans and securities were muted by elevated interest earning cash balances of $69.1 million, negatively impacting our net interest margin by approximately 12 basis points. Average loan yields increased 11 basis points to 7.98% while average loans increased $262.0 million, or 20.6%, to $1.53 billion, primarily due to commercial loan growth of $238.0 million, or 29.9%, focused in our higher yielding law firm commercial loans that grew $250.5 million, or 35.7%. Loan interest income increased $5.7 million, or 22.8%, to $30.8 million with $5.3 million related to growth in average loan volumes (substantially all commercial) and $386 thousand due to an increase in average loan rates (substantially all commercial). Average securities increased $57.9 million, or 20.7%, to $337.7 million with a securities to asset ratio of 15% at September 30, 2025. The yield on average securities increased 41 basis points to 3.81%, and securities income increased $855 thousand with $538 thousand attributable to average volume increases and $316 thousand attributable to increases in average rate. Average deposits increased $364.2 million, or 24.5%, to $1.85 billion, led by increases in litigation related escrow or IOLTA, commercial money market, and noninterest bearing commercial demand deposits totaling $215.4 million, $121.3 million, and $36.2 million, respectively. Our cost of deposits, including noninterest bearing demand deposits, increased 15 basis points to 1.03% due to changes in deposit composition coupled with increases in short-term money market rates. Our loan-to-deposit ratio was 82% at September 30, 2025.

The provision for credit losses was $1.8 million for the third quarter of 2025, a $750 thousand increase from third quarter 2024. As of September 30, 2025, our allowance to loans ratio was 1.37% as compared to 1.50% as of September 30, 2024. Based on management’s evaluation of current credit risk in our multifamily and commercial portfolios as well as increases in the general reserves considering loan growth, loan composition, and the current uncertain economic and short-term interest rate environment (including, but not limited to, the potential impact on the New York metro multifamily real estate market), management believes the allowance for credit losses is adequate at September 30, 2025.

Noninterest income totaled $6.2 million for the third quarter of 2025 as compared to $6.1 million in the same period for 2024. Payment processing income was $5.1 million for the third quarter of 2025, commensurate with the prior year quarter. Growth in payment processing income has been muted, primarily due to changes in our overall merchant risk profile and merchant composition. Payment processing volumes for the credit and debit card processing platform increased $880.3 million, or 9.5%, to $10.1 billion while transactions volume totaled 151.8 million for the current quarter. We continue to focus on the expansion of sales channels through ISOs, prudently managing risk while focusing on new merchant originations, increasing overall volumes as well as prudently managing merchant risk profiles, and expanding our technology and other resources in the payment vertical. The Company utilizes proprietary and industry leading/customized technology to ensure card brand and regulatory compliance, to support multiple processing platforms, to manage daily risk across 93,000 small business merchants in all 50 states, and to perform commercial treasury clearing services for $10.1 billion in volume across 151.8 million in transactions in the current quarter. ASP fees increased $73 thousand, or 11.1%, to $731 thousand for the third quarter of 2025. ASP fee income is directly impacted by the average balances of off-balance sheet sweep funds as well as current short-term market interest rates.

Noninterest expense increased $3.0 million, or 19.5%, to $18.4 million for the third quarter of 2025, as compared to the same period in 2024. This was primarily due to increases in employee compensation and benefits, data processing, professional and consulting services, travel and business relations, and occupancy and equipment costs. Employee compensation and benefits costs increased $1.3 million, or 13.9%, primarily due to increases in sales commissions, bonuses, year-end stock grants and related stock-based compensation, staffing needs for our Los Angeles banking facility, and the impact of year end salary and benefit increases. The increase in sales related commissions is directly related to our regional senior business development officer (“BDO”) strategy and their success in the litigation market, attracting full-service commercial banking clients nationally and directly impacting commercial lending and core-deposit growth. Data processing costs increased $582 thousand due to increases in core banking processing volumes and the continued implementation/improvement of technology supporting client relationships and lead acquisition initiatives (CRM platform, digital marketing, business development, and lending) as well as overall risk management across all platforms. Professional and consulting services costs increased $516 thousand due to continuously evaluating business development opportunities, and professional search costs related to staffing needs, primarily at our Los Angeles banking facility.

| (1) | See non-GAAP reconciliation provided at the end of this news release. |

3

Travel and business relations expenses increased $224 thousand as a result of our high touch sales efforts that complement our digital marketing efforts. Occupancy and equipment costs increased $176 thousand due to amortization of our investments in internally developed software to support our digital platform, as well as costs associated with the opening of our Los Angeles banking facility.

The Company’s efficiency ratio was 48.9% for the three months ended September 30, 2025, as compared to 48.1% in 2024, notwithstanding our continuous investment in resources (both technology and people) to support future growth, lead acquisition initiatives, excellence in client service, enhanced risk management, and costs associated with our flagship banking facility in Los Angeles.

The effective tax rate was 19.5% for the third quarter of 2025, as compared to 27.0% in the prior year quarter, resulting from certain discrete tax benefits related to the exercise of certain stock options totaling approximately $1.3 million.

Year to Date 2025 vs. 2024

Net income for the nine months ended September 30, 2025 was $37.4 million, or $4.32 per diluted share, compared to $31.9 million, or $3.78 per diluted share for the same period in 2024. Returns on average assets and equity for the current nine months were 2.46% and 19.60%, respectively, compared to 2.60% and 20.20% for the same period of 2024.

Net interest income increased $15.2 million, or 20.8%, to $88.2 million, due to growth in average interest earning assets totaling $372.8 million, or 23.5%, to $1.96 billion, funded with low-cost core deposit growth from our regional business development teams and relationship banking efforts. Our net interest margin of 6.01% decreased 13 basis points from 2024, primarily due to elevated average interest earning cash balances of $69.4 million that negatively impacted our net interest margin by approximately 15 basis points. Average loan yields increased 6 basis points to 7.89% while average loans increased $223.7 million, or 18.0%, to $1.46 billion, primarily due to commercial loan growth of $212.6 million, or 27.7%, focused in our higher yielding law firms’ commercial loans that grew $231.3 million, or 35.2%. Loan interest income increased $13.7 million, or 18.8%, to $86.4 million with $13.1 million related to growth in average loan volumes (substantially all commercial) and $545 thousand due to increases in average loan rates (substantially all commercial). Average securities increased $79.7 million, or 31.5%, to $332.9 million and securities yields increased by 61 basis points to 3.78%. Securities income increased by $3.4 million with $2.1 million attributable to average volume increases and $1.3 million attributable to increases in average rate. Average deposits increased $344.3 million, or 24.3%, to $1.76 billion, led by increases in litigation related escrow or IOLTA, money market (primarily commercial), and noninterest bearing commercial demand deposits totaling $226.5 million, $74.0 million, and $52.4 million, respectively. Our cost of deposits, including noninterest bearing demand deposits, increased 9 basis points to 0.99% due to changes in deposit composition coupled with increases in short-term money market rates. Our loan-to-deposit ratio was 82% at September 30, 2025.

The provision for credit losses was $6.8 million for the nine months ended September 30, 2025, a $3.8 million increase from the same period in 2024, driven by $6.2 million in charge-offs comprised of (1) a small business or merchant related commercial loan charge-off totaling $3.3 million ($736 thousand on nonaccrual as of September 30, 2025) in the second quarter of 2025; and (2) a multifamily loan charge-off totaling $2.9 million in the first quarter of 2025 ($7.9 million on nonaccrual as of September 30, 2025). As of September 30, 2025, our allowance to loans ratio was 1.37% as compared to 1.50% as of September 30, 2024. Based on management’s evaluation of current credit risk in our multifamily and commercial portfolios as well as increases in the general reserves considering loan growth, loan composition, and the current uncertain economic and short-term interest rate environment (including, but not limited to, the potential impact on the New York metro multifamily real estate market), management believes the allowance for credit losses is adequate at September 30, 2025.

Noninterest income increased $235 thousand, or 1.3%, to $19.0 million, in line with 2024. Payment processing income was $15.1 million, a $699 thousand decrease from 2024, primarily due to changes in our overall merchant risk profile and merchant composition. Payment processing volumes for the credit and debit card processing platform increased $2.4 billion, or 8.9%, to $29.5 billion and transactions totaled 445.1 million for the current nine months. ASP fee income increased $230 thousand to $2.3 million for the nine months ended September 30, 2025. ASP fee income is directly impacted by the average balances of off-balance sheet sweep funds as well as current short-term market interest rates. In the second quarter of 2025, we recognized a $432 thousand gain on certain equity investments.

Noninterest expense increased $7.0 million, or 15.5%, to $52.2 million for the nine months ended September 30, 2025, as compared to 2024. This increase was primarily due to increases in employee compensation and benefits, data processing, professional and consulting services, other general business operating costs, and occupancy and equipment. Employee compensation and benefits costs increased $2.9 million, or 10.4%, primarily due increases in sales commissions, bonuses, year-end stock grants and related stock-based compensation, employee benefits costs, and, to a lesser extent, the impact of year end salary increases and employee hires. The increase in sales related commissions is directly related to our regional senior BDO strategy and their success in the litigation market, attracting full-service commercial banking clients nationally and directly impacting commercial lending and core-deposit growth. Data processing costs increased $1.3 million due to increases in core banking processing volumes and the continued implementation/improvement of technology supporting client relationships and lead acquisition initiatives (CRM platform, digital marketing, business development, and lending) as well as overall risk management across all platforms. Professional and consulting services costs increased $1.3 million due to continuously evaluating business development opportunities, increased insurance and accounting costs, and costs related to staffing needs for our new Los Angeles banking facility.

4

Other operating costs increased $640 thousand due to increases in regulatory expenses and other client development costs. Occupancy and equipment costs increased $393 thousand due to amortization of internally developed software to support our digital marketing and risk management platforms and rent commencement related to our new Los Angeles banking facility. Travel and business relations expenses increased $375 thousand, resulting from our high touch sales efforts that complement our digital marketing efforts and additional travel related to the opening and associated training for our new Los Angeles banking facility.

The Company’s efficiency ratio was 48.7% for the nine months ended September 30, 2025, as compared to 49.2% in 2024, notwithstanding our continuous investment in resources (both technology and people) to support future growth, lead acquisition initiatives, excellence in client service, enhanced risk management, and the opening of our flagship Los Angeles banking facility.

The effective tax rate was 22.5% for the nine months ended September 30, 2025, as compared to 26.8% in the prior year period, resulting from certain discrete tax benefits related to share-based compensation, specifically the exercise of certain stock options during 2025.

Asset Quality

At September 30, 2025, we had two nonperforming loans totaling $8.6 million, with no exposure to commercial office and construction related borrowers, and $14.3 million in performing loans to the hospitality industry. The allowance for credit losses was $21.1 million, or 1.37% of total loans, as compared to $19.5 million, or 1.50% of total loans at September 30, 2024. The ratio of nonperforming loans to total loans and total assets was 0.56% and 0.40%, respectively. Based on management’s evaluation of current credit risk in our multifamily and commercial portfolios as well as increases in the general reserves considering loan growth, loan composition, and the current uncertain economic and short-term interest rate environment (including, but not limited to, the potential impact on the New York metro multifamily real estate market), management believes the allowance for credit losses is adequate at September 30, 2025.

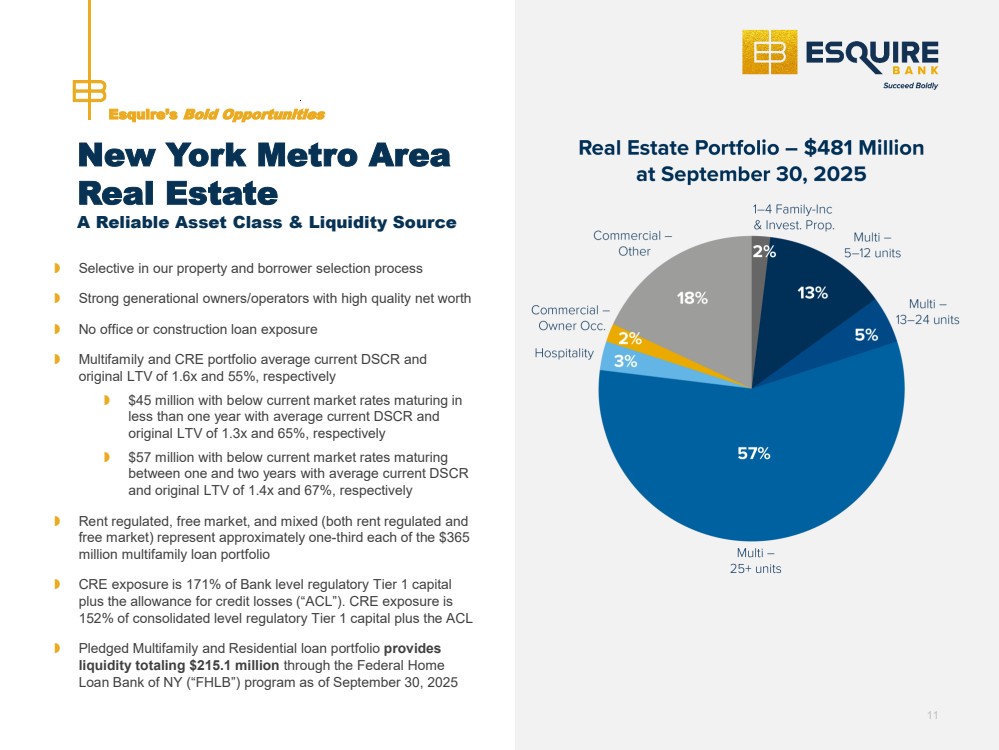

From a credit risk management perspective, the combined multifamily and CRE portfolio, excluding one nonaccrual loan, totaled $463.0 million and has a current weighted average debt service coverage ratio (“DSCR”) and an original loan-to value (“LTV”) (defined as unpaid principal balance as of September 30, 2025 divided by appraised value at origination) of approximately 1.59 and 55%, respectively. When further evaluating this population, loans with below current market rates maturing in (1) less than one year totaled $44.5 million and had a current weighted average DSCR and an original LTV of approximately 1.27 and 65%, respectively; and (2) one to two years totaled $57.3 million and had a current weighted average DSCR and an original LTV of approximately 1.43 and 67%, respectively.

Balance Sheet – September 30, 2025 vs 2024

At September 30, 2025, total assets were $2.18 billion, reflecting a $401.8 million, or 22.5% increase from September 30, 2024. This increase was primarily attributable to growth in loans totaling $249.5 million, or 19.2%, to $1.55 billion. Our higher yielding variable rate commercial loans increased $223.2 million, or 27.0%, to $1.05 billion with commercial litigation related loans increasing $265.3 million, or 36.5%, to $993.1 million. Our commercial relationship banking sales pipeline remained robust, anchored by our regional senior BDOs (supported by commercial lending, risk, and operations) located in key markets throughout the U.S. These BDOs are supported by our best-in-class technology stack including, but not limited to; our proprietary CRM system, digital marketing cloud and lending based technology built on Salesforce supporting client relationships and lead acquisition initiatives; account-based digital marketing (or “ABM”) with significant thought leadership content; and artificial intelligence (or “AI”) for advanced data analytics across our platform powering personalized and real-time ABM content to both current clients and prospective clients. Our available-for-sale securities portfolio increased $53.7 million to $265.1 million as compared to September 30, 2024, primarily due to purchases at current market interest rates totaling $102.8 million, offset by portfolio amortization of primarily lower yielding securities totaling $50.0 million. Our held-to-maturity securities portfolio totaled $62.3 million, a decrease of $8.5 million, due to portfolio amortization. The securities portfolio increased as management elected to ratably purchase short duration agency mortgage-backed securities in 2024, in light of tempering commercial real estate growth, at commensurate risk adjusted yields. Our total securities to assets ratio was 15% at September 30, 2025, enhancing our liquidity position, asset composition, and flexibility in the future.

5

The following table provides information regarding the composition of our loan portfolio for the periods presented:

|

|

September 30, |

|

|

December 31, |

|

|

September 30, |

|

|||||||||

|

|

2025 |

|

|

2024 |

|

|

2024 |

|

|||||||||

|

|

(Dollars in thousands) |

|

|||||||||||||||

Real estate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Multifamily |

|

$ |

365,309 |

|

23.6 |

% |

|

$ |

355,165 |

|

25.4 |

% |

|

$ |

350,857 |

|

27.0 |

% |

Commercial real estate |

|

|

105,634 |

|

6.8 |

|

|

|

87,038 |

|

6.2 |

|

|

|

87,544 |

|

6.8 |

|

1 – 4 family |

|

|

10,013 |

|

0.7 |

|

|

|

14,665 |

|

1.1 |

|

|

|

14,749 |

|

1.1 |

|

Total real estate |

|

|

480,956 |

|

31.1 |

|

|

|

456,868 |

|

32.7 |

|

|

|

453,150 |

|

34.9 |

|

Commercial: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Litigation related |

|

|

993,072 |

|

64.2 |

|

|

|

835,839 |

|

59.8 |

|

|

|

727,749 |

|

56.1 |

|

Other |

|

|

55,517 |

|

3.6 |

|

|

|

84,728 |

|

6.1 |

|

|

|

97,690 |

|

7.5 |

|

Total commercial |

|

|

1,048,589 |

|

67.8 |

|

|

|

920,567 |

|

65.9 |

|

|

|

825,439 |

|

63.6 |

|

Consumer |

|

|

17,181 |

|

1.1 |

|

|

|

19,339 |

|

1.4 |

|

|

|

18,874 |

|

1.5 |

|

Total loans held for investment |

|

$ |

1,546,726 |

|

100.0 |

% |

|

$ |

1,396,774 |

|

100.0 |

% |

|

$ |

1,297,463 |

|

100.0 |

% |

Deferred loan fees and unearned premiums, net |

|

|

254 |

|

|

|

|

|

247 |

|

|

|

|

|

(20) |

|

|

|

Loans, held for investment |

|

$ |

1,546,980 |

|

|

|

|

$ |

1,397,021 |

|

|

|

|

$ |

1,297,443 |

|

|

|

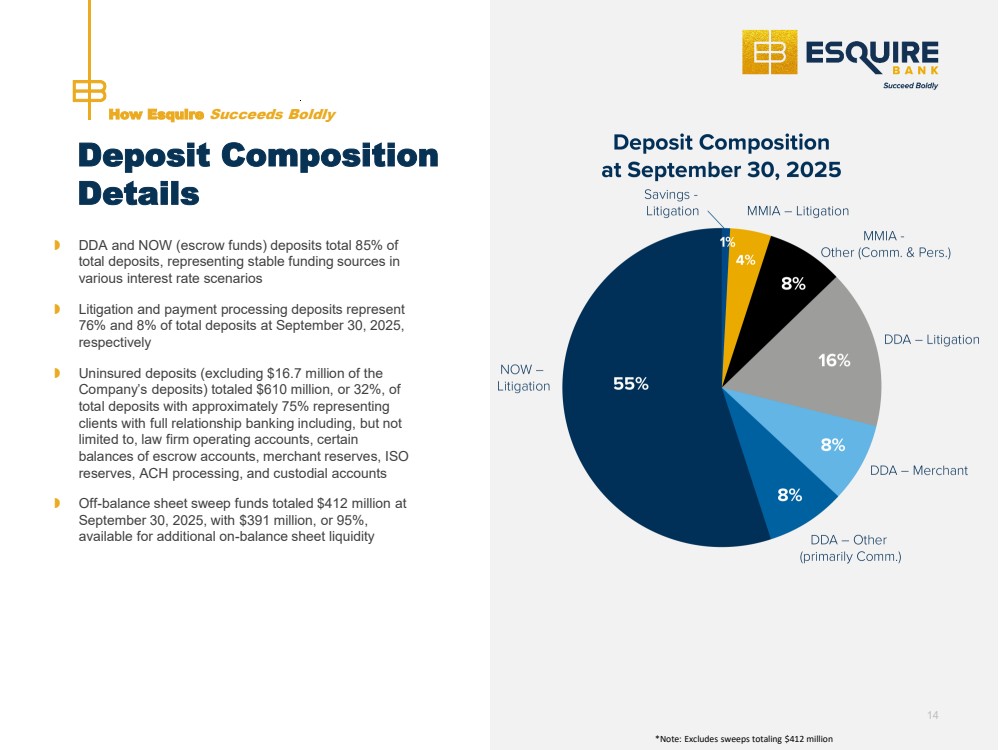

Total deposits were $1.88 billion as of September 30, 2025, a $343.0 million, or 22.3%, increase from September 30, 2024 due to a $189.9 million, or 22.9%, increase in litigation related escrow or IOLTA, a $101.6 million, or 83.6%, increase in money market deposits (primarily commercial), and a $66.1 million, or 12.3%, increase in noninterest bearing commercial demand deposits. Our deposit strategy primarily focuses on developing full service commercial banking relationships nationally with our clients through commercial lending facilities, payment processing, and other unique commercial cash management services in our two national verticals, rather than competing with other institutions on rate. Our longer duration IOLTA, escrow and settlement deposits represent $1.02 billion, or 54.2%, of total deposits. As of September 30, 2025, uninsured deposits were $610.3 million, or 32%, of our total deposits of $1.88 billion, excluding $16.7 million of the Company’s deposits held at the Bank. Approximately 75% of our uninsured deposits represent clients with full commercial relationship banking with us (i.e.-commercial loans, payment processing, and other commercial service-oriented relationships) including, but not limited to, law firm operating accounts, law firm IOLTA/escrow accounts, merchant reserves, ISO reserves, ACH processing, and custodial accounts.

Due to the nature of our larger mass tort and class action settlements related to the litigation vertical, we participate in FDIC insured sweep programs as well as treasury secured money market funds. As of September 30, 2025, off-balance sheet sweep funds totaled approximately $411.6 million, with approximately $390.6 million, or 94.9%, available to be swept on balance sheet as reciprocal client relationship deposits. Our core low-cost deposit growth and off-balance sheet client funds continue to clearly demonstrate our highly efficient, full service commercial relationships and tech-enabled cash management platform.

At September 30, 2025, we had the ability to borrow, on a secured basis, up to $459.8 million from the FHLB of New York and $48.9 million from the FRB of New York discount window. No borrowing amounts were outstanding during the third quarter of 2025. Historically, we have not leveraged our balance sheet to generate earnings and have always utilized core client deposits to fund our asset growth and related earnings.

Stockholders’ equity increased $46.7 million to $279.2 million as of September 30, 2025, primarily driven by net increases in retained earnings (net income less dividends paid to shareholders), and to a lesser extent, additional paid-in-capital due to share-based compensation and decreases in other comprehensive losses related to our available-for-sale securities portfolio.

The Bank remains well above bank regulatory “Well Capitalized” standards.

6

About Esquire Financial Holdings, Inc.

Esquire Financial Holdings, Inc. is a financial holding company headquartered in Jericho, New York, with branch offices in Jericho, New York and Los Angeles, California, as well as an administrative office in Boca Raton, Florida. Its wholly owned subsidiary, Esquire Bank, is a full-service commercial bank dedicated to serving the financial needs of the litigation industry and small businesses nationally, as well as commercial and retail customers in the New York metropolitan area. The Bank offers tailored financial and payment processing solutions to the litigation community and their clients as well as dynamic and flexible payment processing solutions to small business owners. For more information, visit www.esquirebank.com.

Cautionary Note Regarding Forward-Looking Statements

This press release includes “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 relating to future results of the Company. Forward-looking statements are subject to many risks and uncertainties, including, but not limited to: changes in business plans as circumstances warrant; changes in general economic, business and political conditions, including changes in the financial markets; and other risks detailed in the “Cautionary Note Regarding Forward-Looking Statements,” “Risk Factors” and other sections of the Company’s Annual Report on Form 10-K and Quarterly Reports on Form 10-Q as filed with the Securities and Exchange Commission. The forward-looking statements included in this press release are not a guarantee of future events, and that actual events may differ materially from those made in or suggested by the forward-looking statements. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “might,” “should,” “could,” “predict,” “potential,” “believe,” “expect,” “attribute,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “goal,” “target,” “aim,” “would,” “annualized” and “outlook,” or similar terminology. Any forward-looking statements presented herein are made only as of the date of this press release, and the Company does not undertake any obligation to update or revise any forward-looking statements to reflect changes in assumptions, the occurrence of unanticipated events, or otherwise, except as may be required by law.

Contact Information:

Eric S. Bader

Executive Vice President and Chief Operating Officer

Esquire Financial Holdings, Inc.

(516) 535-2002

eric.bader@esqbank.com

7

ESQUIRE FINANCIAL HOLDINGS, INC.

Consolidated Statement of Condition (unaudited)

(dollars in thousands except per share data)

|

|

September 30, |

|

December 31, |

|

September 30, |

|

|||

|

|

2025 |

|

2024 |

|

2024 |

|

|||

ASSETS |

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

240,759 |

|

$ |

126,329 |

|

$ |

147,663 |

|

Securities available-for-sale, at fair value |

|

|

265,132 |

|

|

241,746 |

|

|

211,460 |

|

Securities held-to-maturity, at cost |

|

|

62,288 |

|

|

68,660 |

|

|

70,794 |

|

Securities, restricted at cost |

|

|

3,173 |

|

|

3,034 |

|

|

3,034 |

|

Loans, held for investment |

|

|

1,546,980 |

|

|

1,397,021 |

|

|

1,297,443 |

|

Less: allowance for credit losses |

|

|

(21,119) |

|

|

(20,979) |

|

|

(19,451) |

|

Loans, net of allowance |

|

|

1,525,861 |

|

|

1,376,042 |

|

|

1,277,992 |

|

Premises and equipment, net |

|

|

4,408 |

|

|

2,436 |

|

|

2,610 |

|

Other assets |

|

|

82,690 |

|

|

74,256 |

|

|

68,921 |

|

Total Assets |

|

$ |

2,184,311 |

|

$ |

1,892,503 |

|

$ |

1,782,474 |

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

|

|

Demand deposits |

|

$ |

605,533 |

|

$ |

497,958 |

|

$ |

539,434 |

|

Savings, NOW and money market deposits |

|

|

1,267,850 |

|

|

1,130,174 |

|

|

982,816 |

|

Certificates of deposit |

|

|

6,057 |

|

|

14,104 |

|

|

14,145 |

|

Total deposits |

|

|

1,879,440 |

|

|

1,642,236 |

|

|

1,536,395 |

|

Other liabilities |

|

|

25,644 |

|

|

13,173 |

|

|

13,511 |

|

Total liabilities |

|

|

1,905,084 |

|

|

1,655,409 |

|

|

1,549,906 |

|

Total stockholders' equity |

|

|

279,227 |

|

|

237,094 |

|

|

232,568 |

|

Total Liabilities and Stockholders' Equity |

|

$ |

2,184,311 |

|

$ |

1,892,503 |

|

$ |

1,782,474 |

|

|

|

|

|

|

|

|

|

|

|

|

Selected Financial Data |

|

|

|

|

|

|

|

|

|

|

Common shares outstanding |

|

|

8,565,491 |

|

|

8,354,753 |

|

|

8,320,317 |

|

Book value per share |

|

$ |

32.60 |

|

$ |

28.38 |

|

$ |

27.95 |

|

Equity to assets |

|

|

12.78 |

% |

|

12.53 |

% |

|

13.05 |

% |

|

|

|

|

|

|

|

|

|

|

|

Capital Ratios (1) |

|

|

|

|

|

|

|

|

|

|

Tier 1 leverage ratio |

|

|

12.00 |

% |

|

11.70 |

% |

|

12.60 |

% |

Common equity tier 1 capital ratio |

|

|

15.27 |

|

|

14.67 |

|

|

15.39 |

|

Tier 1 capital ratio |

|

|

15.27 |

|

|

14.67 |

|

|

15.39 |

|

Total capital ratio |

|

|

16.52 |

|

|

15.92 |

|

|

16.64 |

|

|

|

|

|

|

|

|

|

|

|

|

Asset Quality |

|

|

|

|

|

|

|

|

|

|

Nonperforming loans |

|

$ |

8,646 |

|

$ |

10,940 |

|

$ |

10,940 |

|

Allowance for credit losses to total loans |

|

|

1.37 |

% |

|

1.50 |

% |

|

1.50 |

% |

Nonperforming loans to total loans |

|

|

0.56 |

|

|

0.78 |

|

|

0.84 |

|

Nonperforming assets to total assets |

|

|

0.40 |

|

|

0.58 |

|

|

0.61 |

|

Allowance to nonperforming loans |

|

|

244 |

|

|

192 |

|

|

178 |

|

| (1) | Regulatory capital ratios presented on bank-only basis. The Bank has no recorded intangible assets on the Statement of Financial Condition, and accordingly, tangible common equity is equal to common equity. |

8

ESQUIRE FINANCIAL HOLDINGS, INC.

Consolidated Income Statement (unaudited)

(dollars in thousands except per share data)

|

|

Three Months Ended |

|

Nine Months Ended |

|

|||||||||||

|

|

September 30, |

|

June 30, |

|

September 30, |

|

September 30, |

|

|||||||

|

|

2025 |

|

2025 |

|

2024 |

|

2025 |

|

2024 |

|

|||||

Interest income |

|

$ |

36,131 |

|

$ |

33,536 |

|

$ |

29,131 |

|

$ |

101,180 |

|

$ |

82,589 |

|

Interest expense |

|

|

4,792 |

|

|

4,282 |

|

|

3,273 |

|

|

12,978 |

|

|

9,546 |

|

Net interest income |

|

|

31,339 |

|

|

29,254 |

|

|

25,858 |

|

|

88,202 |

|

|

73,043 |

|

Provision for credit losses |

|

|

1,750 |

|

|

3,525 |

|

|

1,000 |

|

|

6,775 |

|

|

3,000 |

|

Net interest income after provision for credit losses |

|

|

29,589 |

|

|

25,729 |

|

|

24,858 |

|

|

81,427 |

|

|

70,043 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Payment processing fees |

|

|

5,069 |

|

|

5,107 |

|

|

5,169 |

|

|

15,088 |

|

|

15,787 |

|

Other noninterest income |

|

|

1,164 |

|

|

1,470 |

|

|

893 |

|

|

3,873 |

|

|

2,939 |

|

Total noninterest income |

|

|

6,233 |

|

|

6,577 |

|

|

6,062 |

|

|

18,961 |

|

|

18,726 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest expense: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employee compensation and benefits |

|

|

10,852 |

|

|

10,216 |

|

|

9,525 |

|

|

31,133 |

|

|

28,211 |

|

Other expenses |

|

|

7,508 |

|

|

6,846 |

|

|

5,833 |

|

|

21,037 |

|

|

16,947 |

|

Total noninterest expense |

|

|

18,360 |

|

|

17,062 |

|

|

15,358 |

|

|

52,170 |

|

|

45,158 |

|

Income before income taxes |

|

|

17,462 |

|

|

15,244 |

|

|

15,562 |

|

|

48,218 |

|

|

43,611 |

|

Income taxes |

|

|

3,405 |

|

|

3,354 |

|

|

4,202 |

|

|

10,864 |

|

|

11,706 |

|

Net income |

|

$ |

14,057 |

|

$ |

11,890 |

|

$ |

11,360 |

|

$ |

37,354 |

|

$ |

31,905 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings Per Share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

1.74 |

|

$ |

1.48 |

|

$ |

1.45 |

|

$ |

4.65 |

|

$ |

4.09 |

|

Diluted |

|

|

1.62 |

|

|

1.38 |

|

|

1.34 |

|

|

4.32 |

|

|

3.78 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Financial Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets |

|

|

2.61 |

% |

|

2.37 |

% |

|

2.62 |

% |

|

2.46 |

% |

|

2.60 |

% |

Return on average equity |

|

|

20.83 |

|

|

18.74 |

|

|

20.29 |

|

|

19.60 |

|

|

20.20 |

|

Net interest margin |

|

|

6.04 |

|

|

6.03 |

|

|

6.16 |

|

|

6.01 |

|

|

6.14 |

|

Efficiency ratio |

|

|

48.9 |

|

|

47.6 |

|

|

48.1 |

|

|

48.7 |

|

|

49.2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash dividends paid per common share |

|

$ |

0.175 |

|

$ |

0.175 |

|

$ |

0.150 |

|

$ |

0.525 |

|

$ |

0.450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average basic shares |

|

|

8,094,441 |

|

|

8,029,541 |

|

|

7,815,197 |

|

|

8,038,047 |

|

|

7,800,230 |

|

Weighted average diluted shares |

|

|

8,690,130 |

|

|

8,639,038 |

|

|

8,503,966 |

|

|

8,646,398 |

|

|

8,439,993 |

|

9

ESQUIRE FINANCIAL HOLDINGS, INC.

Consolidated Average Balance Sheets and Average Yield/Cost (unaudited)

(dollars in thousands)

|

|

Three Months Ended |

|

||||||||||||||||||||||

|

|

September 30, |

|

June 30, |

|

September 30, |

|

||||||||||||||||||

|

|

2025 |

|

2025 |

|

2024 |

|

||||||||||||||||||

|

|

Average |

|

|

|

|

Average |

|

Average |

|

|

|

|

Average |

|

Average |

|

|

|

|

Average |

|

|||

|

|

Balance |

|

Interest |

|

Yield/Cost |

|

Balance |

|

Interest |

|

Yield/Cost |

|

Balance |

|

Interest |

|

Yield/Cost |

|

||||||

INTEREST EARNING ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, held for investment |

|

$ |

1,532,484 |

|

$ |

30,839 |

|

7.98 |

% |

$ |

1,462,401 |

|

$ |

28,762 |

|

7.89 |

% |

$ |

1,270,491 |

|

$ |

25,122 |

|

7.87 |

% |

Securities, includes restricted stock |

|

|

337,705 |

|

|

3,244 |

|

3.81 |

% |

|

332,965 |

|

|

3,127 |

|

3.77 |

% |

|

279,768 |

|

|

2,389 |

|

3.40 |

% |

Interest earning cash and other |

|

|

189,418 |

|

|

2,048 |

|

4.29 |

% |

|

151,915 |

|

|

1,647 |

|

4.35 |

% |

|

120,316 |

|

|

1,620 |

|

5.36 |

% |

Total interest earning assets |

|

|

2,059,607 |

|

|

36,131 |

|

6.96 |

% |

|

1,947,281 |

|

|

33,536 |

|

6.91 |

% |

|

1,670,575 |

|

|

29,131 |

|

6.94 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NONINTEREST EARNING ASSETS |

|

|

74,791 |

|

|

|

|

|

|

|

69,289 |

|

|

|

|

|

|

|

52,008 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL AVERAGE ASSETS |

|

$ |

2,134,398 |

|

|

|

|

|

|

$ |

2,016,570 |

|

|

|

|

|

|

$ |

1,722,583 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INTEREST BEARING LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Savings, NOW, Money Market deposits |

|

$ |

1,275,061 |

|

$ |

4,739 |

|

1.47 |

% |

$ |

1,178,058 |

|

$ |

4,225 |

|

1.44 |

% |

$ |

940,920 |

|

$ |

3,129 |

|

1.32 |

% |

Time deposits |

|

|

6,092 |

|

|

52 |

|

3.39 |

% |

|

6,037 |

|

|

56 |

|

3.72 |

% |

|

12,251 |

|

|

143 |

|

4.64 |

% |

Total interest bearing deposits |

|

|

1,281,153 |

|

|

4,791 |

|

1.48 |

% |

|

1,184,095 |

|

|

4,281 |

|

1.45 |

% |

|

953,171 |

|

|

3,272 |

|

1.37 |

% |

Borrowings |

|

|

42 |

|

|

1 |

|

9.45 |

% |

|

42 |

|

|

1 |

|

9.55 |

% |

|

44 |

|

|

1 |

|

9.04 |

% |

Total interest bearing liabilities |

|

|

1,281,195 |

|

|

4,792 |

|

1.48 |

% |

|

1,184,137 |

|

|

4,282 |

|

1.45 |

% |

|

953,215 |

|

|

3,273 |

|

1.37 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NONINTEREST BEARING LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand deposits |

|

|

568,107 |

|

|

|

|

|

|

|

562,056 |

|

|

|

|

|

|

|

531,864 |

|

|

|

|

|

|

Other liabilities |

|

|

17,341 |

|

|

|

|

|

|

|

15,902 |

|

|

|

|

|

|

|

14,762 |

|

|

|

|

|

|

Total noninterest bearing liabilities |

|

|

585,448 |

|

|

|

|

|

|

|

577,958 |

|

|

|

|

|

|

|

546,626 |

|

|

|

|

|

|

Stockholders' equity |

|

|

267,755 |

|

|

|

|

|

|

|

254,475 |

|

|

|

|

|

|

|

222,742 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL AVG. LIABILITIES AND EQUITY |

|

$ |

2,134,398 |

|

|

|

|

|

|

$ |

2,016,570 |

|

|

|

|

|

|

$ |

1,722,583 |

|

|

|

|

|

|

Net interest income |

|

|

|

|

$ |

31,339 |

|

|

|

|

|

|

$ |

29,254 |

|

|

|

|

|

|

$ |

25,858 |

|

|

|

Net interest spread |

|

|

|

|

|

|

|

5.48 |

% |

|

|

|

|

|

|

5.46 |

% |

|

|

|

|

|

|

5.57 |

% |

Net interest margin |

|

|

|

|

|

|

|

6.04 |

% |

|

|

|

|

|

|

6.03 |

% |

|

|

|

|

|

|

6.16 |

% |

Deposits (including noninterest bearing demand deposits) |

|

$ |

1,849,260 |

|

$ |

4,791 |

|

1.03 |

% |

$ |

1,746,151 |

|

$ |

4,281 |

|

0.98 |

% |

$ |

1,485,035 |

|

$ |

3,272 |

|

0.88 |

% |

10

ESQUIRE FINANCIAL HOLDINGS, INC.

Consolidated Average Balance Sheets and Average Yield/Cost (unaudited)

(dollars in thousands)

|

|

Nine Months Ended September 30, |

|

||||||||||||||

|

|

2025 |

|

2024 |

|

||||||||||||

|

|

Average |

|

|

|

|

Average |

|

Average |

|

|

|

|

Average |

|

||

|

|

Balance |

|

Interest |

|

Yield/Cost |

|

Balance |

|

Interest |

|

Yield/Cost |

|

||||

INTEREST EARNING ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, held for investment |

|

$ |

1,463,667 |

|

$ |

86,411 |

|

7.89 |

% |

$ |

1,239,950 |

|

$ |

72,727 |

|

7.83 |

% |

Securities, includes restricted stock |

|

|

332,872 |

|

|

9,413 |

|

3.78 |

% |

|

253,188 |

|

|

6,017 |

|

3.17 |

% |

Interest earning cash and other |

|

|

165,824 |

|

|

5,356 |

|

4.32 |

% |

|

96,448 |

|

|

3,845 |

|

5.33 |

% |

Total interest earning assets |

|

|

1,962,363 |

|

|

101,180 |

|

6.89 |

% |

|

1,589,586 |

|

|

82,589 |

|

6.94 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NONINTEREST EARNING ASSETS |

|

|

68,370 |

|

|

|

|

|

|

|

50,439 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL AVERAGE ASSETS |

|

$ |

2,030,733 |

|

|

|

|

|

|

$ |

1,640,025 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INTEREST BEARING LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Savings, NOW, Money Market deposits |

|

$ |

1,196,256 |

|

$ |

12,748 |

|

1.42 |

% |

$ |

900,315 |

|

$ |

9,159 |

|

1.36 |

% |

Time deposits |

|

|

7,628 |

|

|

227 |

|

3.98 |

% |

|

11,667 |

|

|

384 |

|

4.40 |

% |

Total interest bearing deposits |

|

|

1,203,884 |

|

|

12,975 |

|

1.44 |

% |

|

911,982 |

|

|

9,543 |

|

1.40 |

% |

Borrowings |

|

|

42 |

|

|

3 |

|

9.55 |

% |

|

44 |

|

|

3 |

|

9.11 |

% |

Total interest bearing liabilities |

|

|

1,203,926 |

|

|

12,978 |

|

1.44 |

% |

|

912,026 |

|

|

9,546 |

|

1.40 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NONINTEREST BEARING LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand deposits |

|

|

555,235 |

|

|

|

|

|

|

|

502,851 |

|

|

|

|

|

|

Other liabilities |

|

|

16,796 |

|

|

|

|

|

|

|

14,149 |

|

|

|

|

|

|

Total noninterest bearing liabilities |

|

|

572,031 |

|

|

|

|

|

|

|

517,000 |

|

|

|

|

|

|

Stockholders' equity |

|

|

254,776 |

|

|

|

|

|

|

|

210,999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL AVG. LIABILITIES AND EQUITY |

|

$ |

2,030,733 |

|

|

|

|

|

|

$ |

1,640,025 |

|

|

|

|

|

|

Net interest income |

|

|

|

|

$ |

88,202 |

|

|

|

|

|

|

$ |

73,043 |

|

|

|

Net interest spread |

|

|

|

|

|

|

|

5.45 |

% |

|

|

|

|

|

|

5.54 |

% |

Net interest margin |

|

|

|

|

|

|

|

6.01 |

% |

|

|

|

|

|

|

6.14 |

% |

Deposits (including noninterest bearing demand deposits) |

|

$ |

1,759,119 |

|

$ |

12,975 |

|

0.99 |

% |

$ |

1,414,833 |

|

$ |

9,543 |

|

0.90 |

% |

11

ESQUIRE FINANCIAL HOLDINGS, INC.

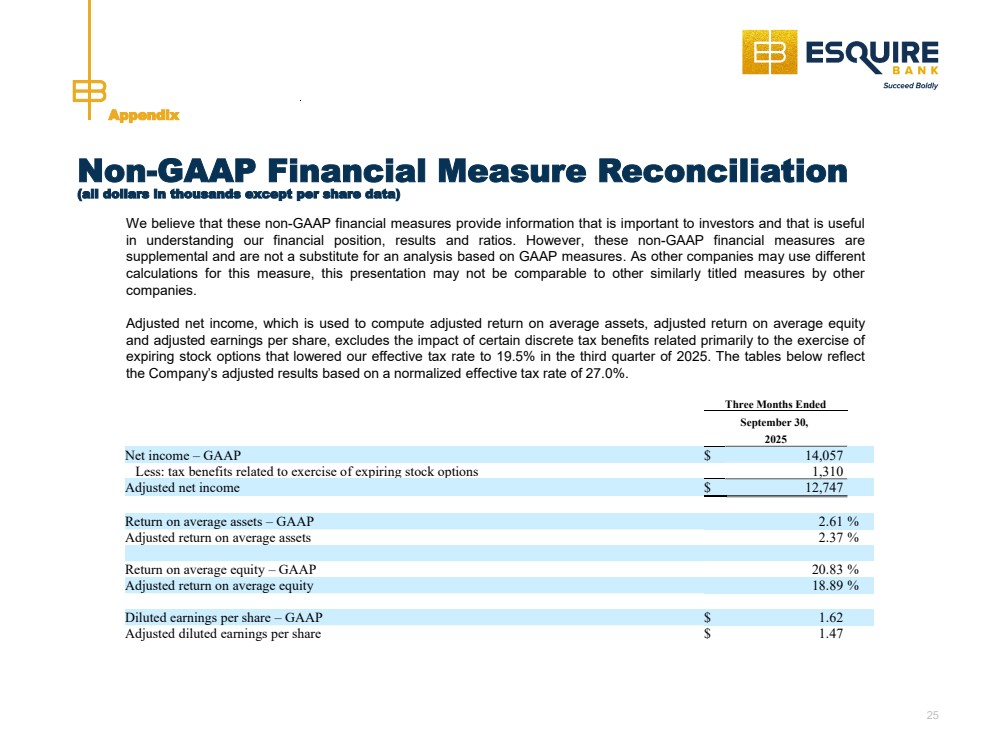

Consolidated Non-GAAP Financial Measure Reconciliation (unaudited)

(all dollars in thousands except per share data)

We believe that these non-GAAP financial measures provide information that is important to investors and that is useful in understanding our financial position, results and ratios. However, these non-GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP measures. As other companies may use different calculations for this measure, this presentation may not be comparable to other similarly titled measures by other companies.

Adjusted net income, which is used to compute adjusted return on average assets, adjusted return on average equity and adjusted earnings per share, excludes the impact of certain discrete tax benefits related primarily to the exercise of expiring stock options that lowered our effective tax rate to 19.5% in the third quarter of 2025. The tables below reflect the Company’s adjusted results based on a normalized effective tax rate of 27.0%.

|

Three Months Ended |

|

|

|

September 30, |

|

|

|

2025 |

|

|

Net income – GAAP |

$ |

14,057 |

|

Less: tax benefits related to exercise of expiring stock options |

|

1,310 |

|

Adjusted net income |

$ |

12,747 |

|

|

|

|

|

Return on average assets – GAAP |

|

2.61 |

% |

Adjusted return on average assets |

|

2.37 |

% |

|

|

|

|

Return on average equity – GAAP |

|

20.83 |

% |

Adjusted return on average equity |

|

18.89 |

% |

|

|

|

|

Diluted earnings per share – GAAP |

$ |

1.62 |

|

Adjusted diluted earnings per share |

$ |

1.47 |

|

12

|

Ensuring our Clients and Our Institution Succeed Boldly Listed as ESQ Esquire Financial Holdings, Inc. (Financial Holding Company for Esquire Bank, N.A.) 3Q 2025 Investor Presentation Exhibit 99.2 |

|

Forward Looking Disclosure This presentation contains forward-looking statements within the meaning of the federal securities laws. Forward-looking statements are not historical fact and express management’s current expectations, forecasts of future events or long-term goals and, by their nature, are subject to assumptions, risks and uncertainties, many of which are beyond the control of the Company. These statements are may be identified through the use of words or phrases such as “may,” “might,” “should,” “could,” “predict,” “potential,” “believe,” “expect,” “attribute,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “goal,” “target,” “aim,” “would,” “annualized” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. Forward-looking statements speak only as of the date they are made and are inherently subject to uncertainties and changes in circumstances, including those described under the heading “Risk Factors” in the Company’s 10-K and 10-Q, filed with the Securities and Exchange Commission (“SEC”). Forward-looking statements are not guarantees of future performance and should not be relied upon as representing management’s views as of any subsequent date. Actual results could differ materially from those indicated. The Company undertakes no obligation to update forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by law. The forward-looking statements speak as of the date of this presentation. The delivery of this presentation shall not, under any circumstances, create any implication there has been no change in the affairs of the Company after the date hereof. This presentation includes industry and market data that we obtained from periodic industry publications, third-party studies and surveys. Industry publications and surveys generally state that the information contained therein has been obtained from sources believed to be reliable. Although we believe the industry and market data to be reliable as of the date of this presentation, this information could prove to be inaccurate. Industry and market data could be wrong because of the method by which sources obtained their data and because information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. In addition, we do not know all of the assumptions regarding general economic conditions or growth that were used in preparing the forecasts from the sources relied upon or cited herein. This presentation contains financial information determined by methods other than in accordance with accounting principles generally accepted in the United States of America (“GAAP”). We believe that these non-GAAP financial measures provide information that is important to investors and that is useful in understanding our financial position, results and ratios. However, these non-GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP measures. As other companies may use different calculations for this measure, this presentation may not be comparable to other similarly titled measures by other companies. These disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. A reconciliation of the non-GAAP measures used in this presentation to the most directly comparable GAAP measures is provided in the Appendix to this presentation. 2 |

|

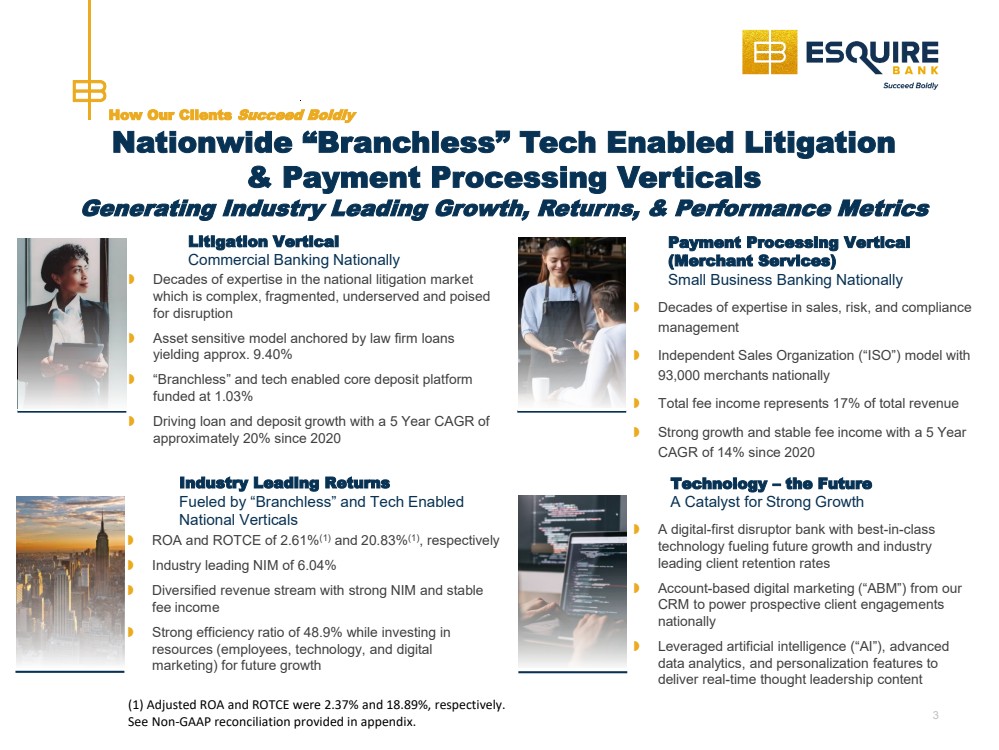

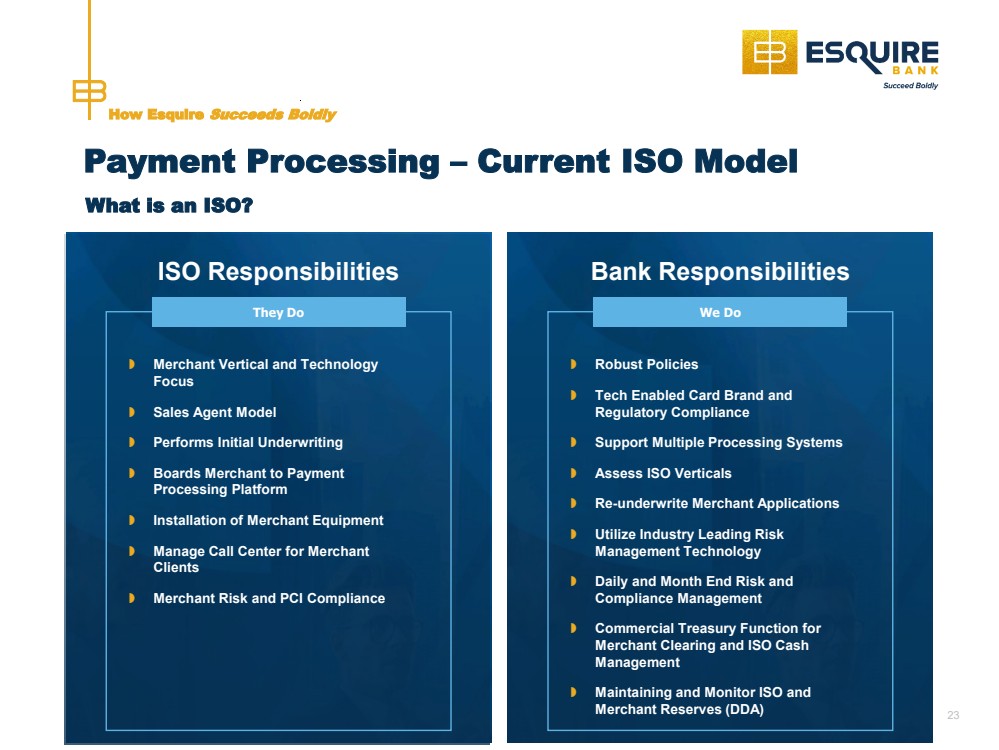

Decades of expertise in the national litigation market which is complex, fragmented, underserved and poised for disruption Asset sensitive model anchored by law firm loans yielding approx. 9.40% “Branchless” and tech enabled core deposit platform funded at 1.03% Driving loan and deposit growth with a 5 Year CAGR of approximately 20% since 2020 Decades of expertise in sales, risk, and compliance management Independent Sales Organization (“ISO”) model with 93,000 merchants nationally Total fee income represents 17% of total revenue Strong growth and stable fee income with a 5 Year CAGR of 14% since 2020 ROA and ROTCE of 2.61%(1) and 20.83%(1), respectively Industry leading NIM of 6.04% Diversified revenue stream with strong NIM and stable fee income Strong efficiency ratio of 48.9% while investing in resources (employees, technology, and digital marketing) for future growth A digital-first disruptor bank with best-in-class technology fueling future growth and industry leading client retention rates Account-based digital marketing (“ABM”) from our CRM to power prospective client engagements nationally Leveraged artificial intelligence (“AI”), advanced data analytics, and personalization features to deliver real-time thought leadership content Nationwide “Branchless” Tech Enabled Litigation & Payment Processing Verticals Generating Industry Leading Growth, Returns, & Performance Metrics Litigation Vertical Commercial Banking Nationally Industry Leading Returns Fueled by “Branchless” and Tech Enabled National Verticals Payment Processing Vertical (Merchant Services) Small Business Banking Nationally Technology – the Future A Catalyst for Strong Growth 3 How Our Clients Succeed Boldly (1) Adjusted ROA and ROTCE were 2.37% and 18.89%, respectively. See Non-GAAP reconciliation provided in appendix. |

|

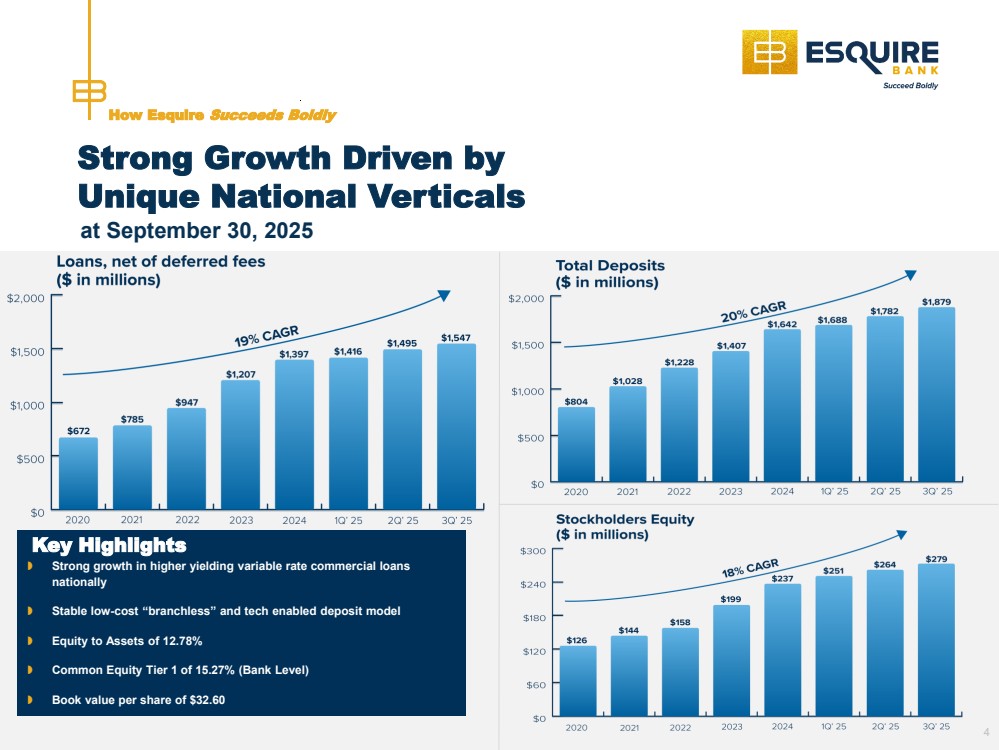

Strong Growth Driven by Unique National Verticals How Esquire Succeeds Boldly Key Highlights Strong growth in higher yielding variable rate commercial loans nationally Stable low-cost “branchless” and tech enabled deposit model Equity to Assets of 12.78% Common Equity Tier 1 of 15.27% (Bank Level) Book value per share of $32.60 4 at September 30, 2025 |

|

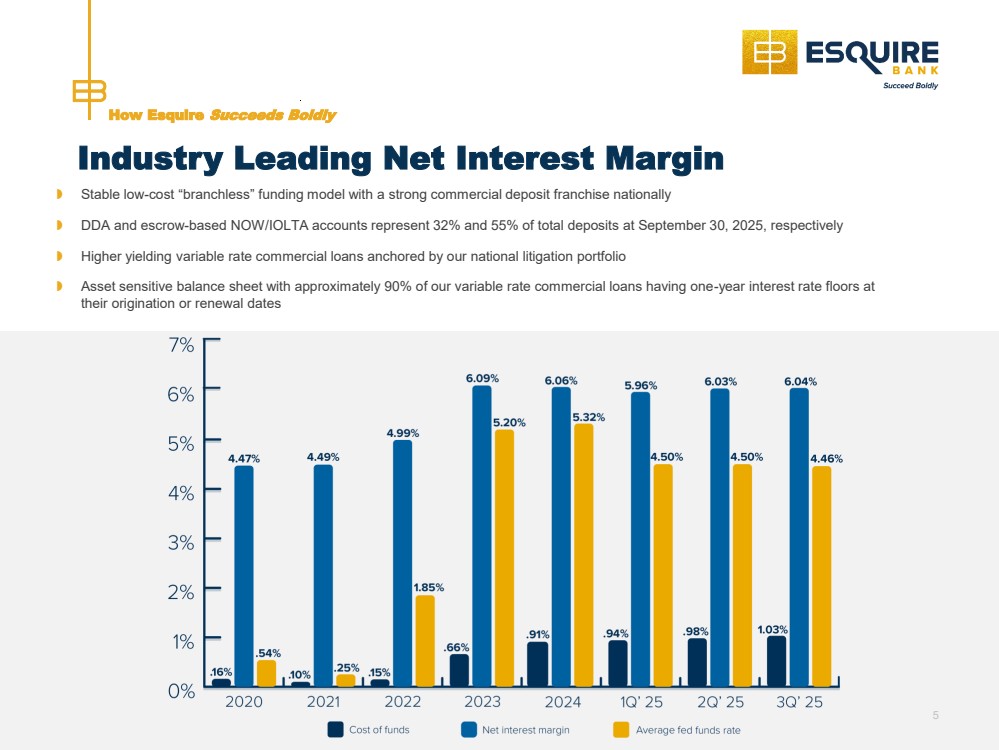

Stable low-cost “branchless” funding model with a strong commercial deposit franchise nationally DDA and escrow-based NOW/IOLTA accounts represent 32% and 55% of total deposits at September 30, 2025, respectively Higher yielding variable rate commercial loans anchored by our national litigation portfolio Asset sensitive balance sheet with approximately 90% of our variable rate commercial loans having one-year interest rate floors at their origination or renewal dates How Esquire Succeeds Boldly 5 Industry Leading Net Interest Margin |

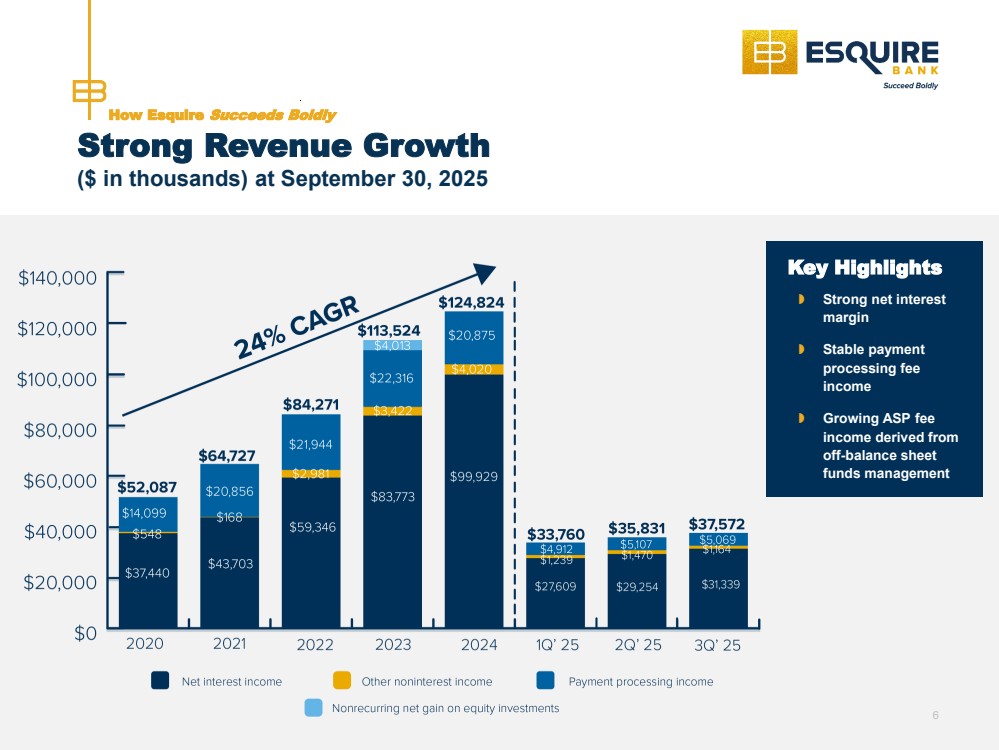

|

Strong Revenue Growth ($ in thousands) at September 30, 2025 How Esquire Succeeds Boldly 6 Key Highlights Strong net interest margin Stable payment processing fee income Growing ASP fee income derived from off-balance sheet funds management |

|

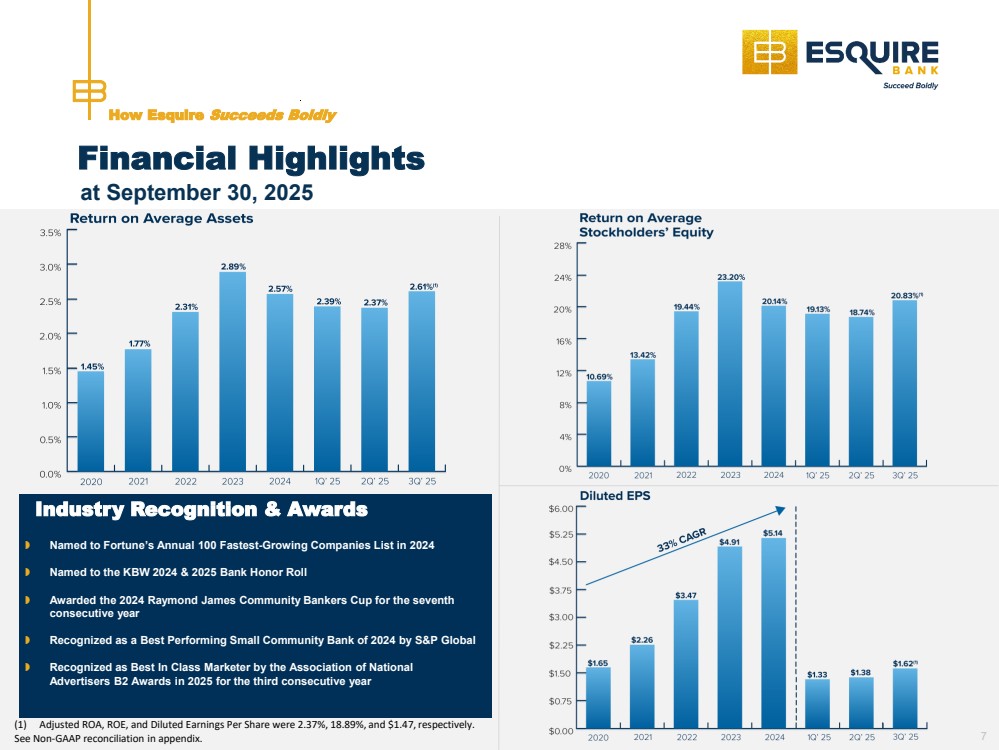

Financial Highlights How Esquire Succeeds Boldly Industry Recognition & Awards Named to Fortune’s Annual 100 Fastest-Growing Companies List in 2024 Named to the KBW 2024 & 2025 Bank Honor Roll Awarded the 2024 Raymond James Community Bankers Cup for the seventh consecutive year Recognized as a Best Performing Small Community Bank of 2024 by S&P Global Recognized as Best In Class Marketer by the Association of National Advertisers B2 Awards in 2025 for the third consecutive year 7 at September 30, 2025 (1) Adjusted ROA, ROE, and Diluted Earnings Per Share were 2.37%, 18.89%, and $1.47, respectively. See Non-GAAP reconciliation in appendix. |

|

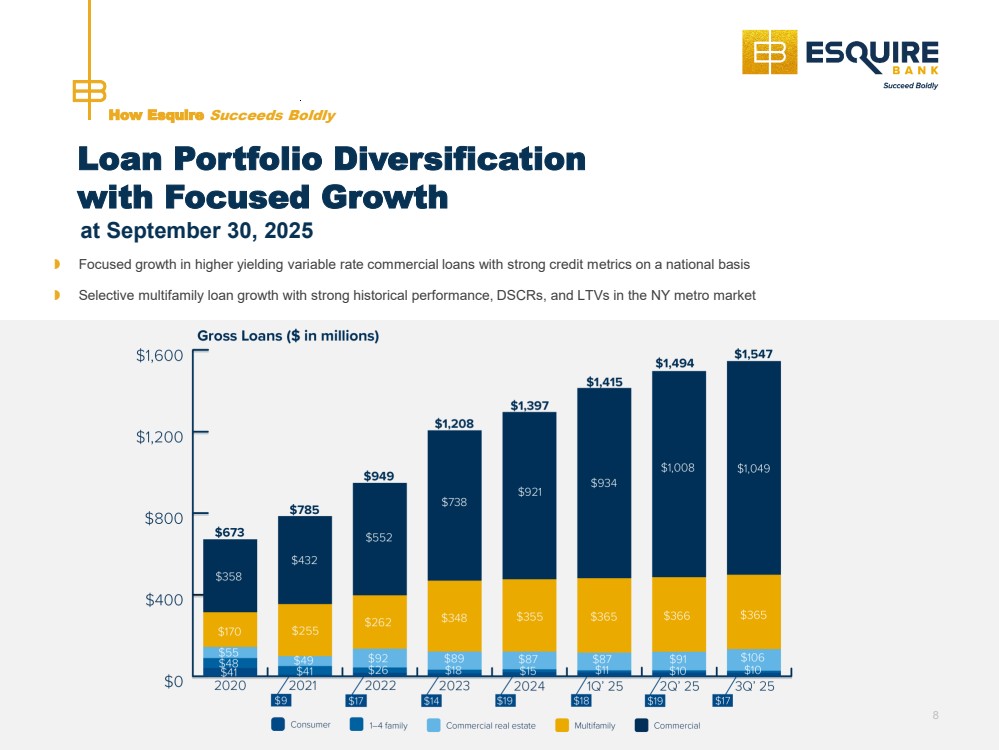

Loan Portfolio Diversification with Focused Growth Focused growth in higher yielding variable rate commercial loans with strong credit metrics on a national basis Selective multifamily loan growth with strong historical performance, DSCRs, and LTVs in the NY metro market How Esquire Succeeds Boldly 8 at September 30, 2025 |

|

Substantially all of our $1.05 billion in commercial loans are variable rate and tied to prime comprising approximately 68% of our loan portfolio Approximately 90% of our variable rate commercial loan portfolio was originated (or renewed annually) with interest rate floors in place Asset sensitive – estimated sensitivity of projected annualized net interest income (“NII”) down 100 and 200 basis point rate scenarios decreases projected NII by 5.2% and 10.9%, respectively at June 30, 2025 Loan Portfolio Diversification with Focused Growth How Esquire Succeeds Boldly 9 |

|

Commercial Litigation (Law Firm) Loans Full annual underwriting including, but not limited to: 3 years financials and tax returns (business and personal) Full contingent case inventory valuation process & collateral assignment or UCC-1 Personal guarantees for the majority of loans, including personal background checks Diversity across law firm inventories and collateral Average loan-to-collateral fee value or LTV of less than 14% Strong average DSCR (on average > 4.0x) Average draws against committed and uncommitted line-of-credit (“LOC”) and case disbursement loans of approximately 50% Weighted average interest rate of approximately 9.40% Funded with low-cost contingent law firm litigation deposits Litigation deposits to litigation loan facilities drawn is approximately 144% How Esquire Succeeds Boldly 10 |

|