UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported): October 21, 2025

AGREE REALTY CORPORATION

(Exact name of registrant as specified in its charter)

Maryland

(State or other jurisdiction of incorporation)

1-12928 |

|

38-3148187 |

(Commission file number) |

|

(I.R.S. Employer Identification No.) |

|

|

|

32301 Woodward Avenue |

|

|

Royal Oak, Michigan |

|

48073 |

(Address of principal executive offices) |

|

(Zip code) |

(Registrant’s telephone number, including area code) (248) 737-4190

Not applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Common Stock, $0.0001 par value |

ADC |

New York Stock Exchange |

Depositary Shares, each representing one- thousandth of a share of 4.25% Series A Cumulative Redeemable Preferred Stock, $0.0001 par value |

ADCPrA |

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02.Results of Operations and Financial Condition.

On October 21, 2025, Agree Realty Corporation (the “Company”) issued a press release describing its results of operations for the third quarter ended September 30, 2025, and posted an updated investor presentation to its website. The press release is furnished as Exhibit 99.1 to this report. The investor presentation is furnished as Exhibit 99.2 to this report.

The information furnished with this Item 2.02 (including Exhibits 99.1 and 99.2 under Item 9.01 below) of this Current Report on Form 8-K shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of such section, nor shall such information be deemed to be incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such a filing.

Item 9.01.Financial Statements and Exhibits.

(d)Exhibits

Exhibit |

|

Description |

99.1 |

|

|

99.2 |

|

|

104 |

|

Cover Page Interactive Data File (embedded within the Inline XBRL document). |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

AGREE REALTY CORPORATION |

|

|

|

|

|

By: |

/s/ Peter Coughenour |

|

|

Name: Peter Coughenour |

|

|

Title: Chief Financial Officer and Secretary |

|

|

|

Date: October 21, 2025 |

|

|

Exhibit 99.1

|

32301 Woodward Ave. Royal Oak, MI 48073 www.agreerealty.com FOR IMMEDIATE RELEASE |

Agree Realty Corporation Reports Third Quarter 2025 Results

Raises 2025 Investment Guidance to $1.50 Billion to $1.65 Billion

Increases 2025 AFFO Per Share Guidance to $4.31 to $4.33

Royal Oak, MI, October 21, 2025 -- Agree Realty Corporation (NYSE: ADC) (the “Company”) today announced results for the quarter ended September 30, 2025. All per share amounts included herein are on a diluted per common share basis unless otherwise stated.

Third Quarter 2025 Financial and Operating Highlights:

| ■ | Invested approximately $451 million in 110 retail net lease properties across all three external growth platforms |

| ■ | Commenced five development or Developer Funding Platform (“DFP”) projects for total committed capital of approximately $51 million |

| ■ | Net Income per share attributable to common stockholders increased 7.9% to $0.45 |

| ■ | Core Funds from Operations (“Core FFO”) per share increased 8.4% to $1.09 |

| ■ | Adjusted Funds from Operations (“AFFO”) per share increased 7.2% to $1.10 |

| ■ | Declared a monthly dividend of $0.256 per common share for September, a 2.4% year-over-year increase |

| ■ | Achieved an A- issuer rating from Fitch Ratings with a stable outlook |

| ■ | Settled 3.5 million shares of outstanding forward equity for net proceeds of approximately $252 million |

| ■ | Balance sheet positioned for growth at 3.5 times proforma net debt to recurring EBITDA; 5.1 times excluding unsettled forward equity |

| ■ | Over $1.9 billion of liquidity at quarter end including availability on the revolving credit facility, outstanding forward equity, and cash on hand |

Financial Results

Net Income Attributable to Common Stockholders

Net Income for the three months ended September 30, 2025 increased 18.2% to $50.3 million, compared to Net Income of $42.5 million for the comparable period in 2024. Net Income per share for the three months ended September 30th increased 7.9% to $0.45 compared to Net Income per share of $0.42 for the comparable period in 2024.

Net Income for the nine months ended September 30, 2025 increased 3.1% to $142.7 million, compared to Net Income of $138.4 million for the comparable period in 2024. Net Income per share for the nine months ended September 30th decreased 5.3% to $1.30 compared to Net Income per share of $1.37 for the comparable period in 2024.

Core FFO

Core FFO for the three months ended September 30, 2025 increased 18.9% to $122.4 million, compared to Core FFO of $102.9 million for the comparable period in 2024. Core FFO per share for the three months ended September 30th increased 8.4% to $1.09, compared to Core FFO per share of $1.01 for the comparable period in 2024.

Core FFO for the nine months ended September 30, 2025 increased 13.5% to $351.0 million, compared to Core FFO of $309.1 million for the comparable period in 2024. Core FFO per share for the nine months ended September 30th increased 4.3% to $3.18, compared to Core FFO per share of $3.05 for the comparable period in 2024.

AFFO

AFFO for the three months ended September 30, 2025 increased 17.5% to $123.1 million, compared to AFFO of $104.8 million for the comparable period in 2024. AFFO per share for the three months ended September 30th increased 7.2% to $1.10, compared to AFFO per share of $1.03 for the comparable period in 2024.

AFFO for the nine months ended September 30, 2025 increased 13.2% to $354.8 million, compared to AFFO of $313.3 million for the comparable period in 2024. AFFO per share for the nine months ended September 30th increased 4.0% to $3.22, compared to AFFO per share of $3.10 for the comparable period in 2024.

Dividend

In the third quarter, the Company declared monthly cash dividends of $0.256 per common share for each of July, August and September 2025. The monthly dividends declared during the third quarter reflect an annualized dividend amount of $3.072 per common share, representing a 2.4% year-over-year increase. The dividends represent payout ratios of approximately 70% of Core FFO per share and 70% of AFFO per share, respectively.

For the nine months ended September 30, 2025, the Company declared monthly cash dividends totaling $2.295 per common share, representing a 2.4% year-over-year increase. The dividends represent payout ratios of approximately 72% of Core FFO per share and 71% of AFFO per share, respectively.

Subsequent to quarter end, the Company declared a monthly cash dividend of $0.262 per common share for October 2025. The monthly dividend reflects an annualized dividend amount of $3.144 per common share, representing a 3.6% year-over-year increase. The October dividend is payable on November 14, 2025 to stockholders of record at the close of business on October 31, 2025.

Additionally, subsequent to quarter end, the Company declared a monthly cash dividend on its 4.25% Series A Cumulative Redeemable Preferred Stock of $0.08854 per depositary share, which is equivalent to $1.0625 per annum. The dividend is payable on November 3, 2025 to stockholders of record at the close of business on October 24, 2025.

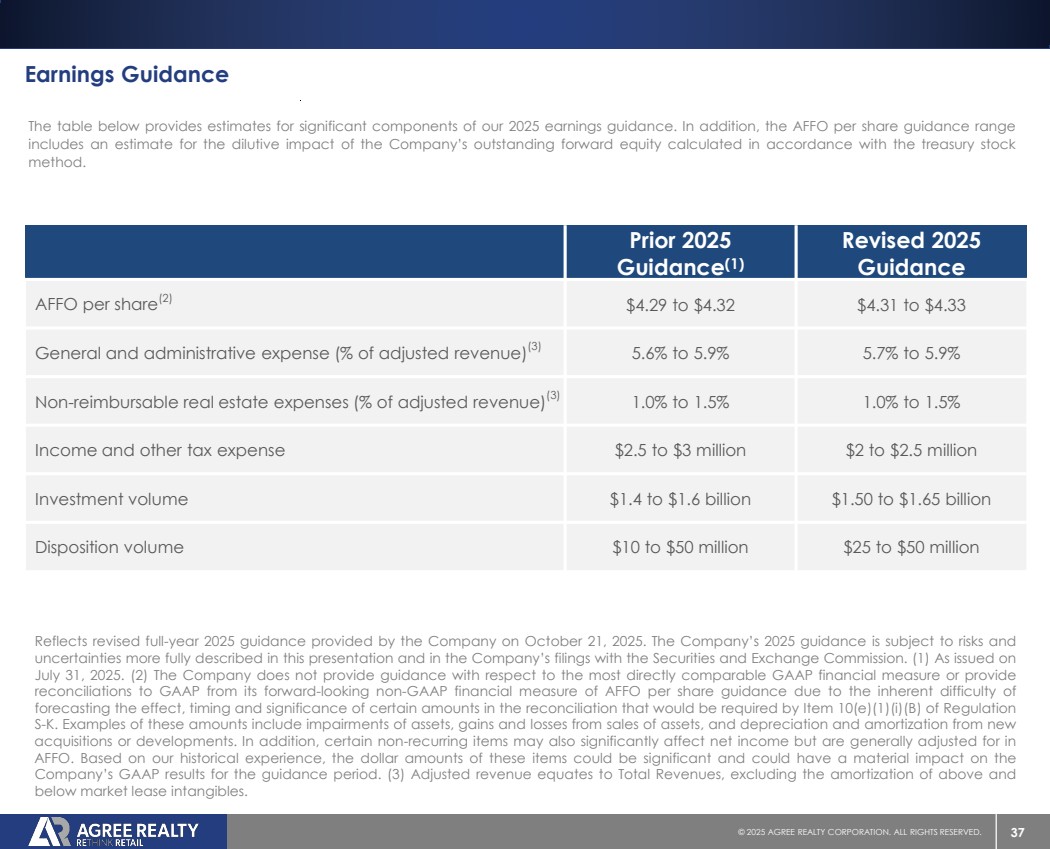

Earnings Guidance

The table below provides estimates for significant components of our 2025 earnings guidance. In addition, the AFFO per share guidance range includes an estimate for the dilutive impact of the Company's outstanding forward equity calculated in accordance with the treasury stock method.

|

|

Prior 2025 |

|

Revised 2025 |

|

|

Guidance(1) |

|

Guidance |

AFFO per share(2) |

|

$4.29 to $4.32 |

|

$4.31 to $4.33 |

General and administrative expenses (% of adjusted revenue)(3) |

|

5.6% to 5.9% |

|

5.7% to 5.9% |

Non-reimbursable real estate expenses (% of adjusted revenue)(3) |

|

1.0% to 1.5% |

|

1.0% to 1.5% |

Income and other tax expense |

|

$2.5 to $3 million |

|

$2 to $2.5 million |

Investment volume |

|

$1.4 to $1.6 billion |

|

$1.50 to $1.65 billion |

Disposition volume |

|

$10 to $50 million |

|

$25 to $50 million |

The Company’s 2025 guidance is subject to risks and uncertainties more fully described in this press release and in the Company’s filings with the Securities and Exchange Commission (the “SEC”).

| (1) | As issued on July 31, 2025. |

| (2) | The Company does not provide guidance with respect to the most directly comparable GAAP financial measure or provide reconciliations to GAAP from its forward-looking non-GAAP financial measure of AFFO per share guidance due to the inherent difficulty of forecasting the effect, timing and significance of certain amounts in the reconciliation that would be required by Item 10(e)(1)(i)(B) of Regulation S-K. Examples of these amounts include impairments of assets, gains and losses from sales of assets, and depreciation and amortization from new acquisitions or developments. In addition, certain non-recurring items may also significantly affect net income but are generally adjusted for in AFFO. Based on our historical experience, the dollar amounts of these items could be significant and could have a material impact on the Company’s GAAP results for the guidance period. |

| (3) | Adjusted revenue equates to Total Revenues, excluding the amortization of above and below market lease intangibles. |

CEO Comments

"We are very pleased with our year-to-date performance as we delivered our largest investment quarter since 2020, deploying over $450 million across our three external growth platforms,” said Joey Agree, President and Chief Executive Officer. “During the quarter, we achieved an A- issuer rating with a stable outlook from Fitch Ratings, further validating the strength of our fortress balance sheet which has total liquidity of over $1.9 billion. Given our best-in-class portfolio and robust investment pipeline, we are increasing full-year 2025 investment guidance to a range of $1.50 billion to $1.65 billion and raising 2025 AFFO per share guidance to a range of $4.31 to $4.33.”

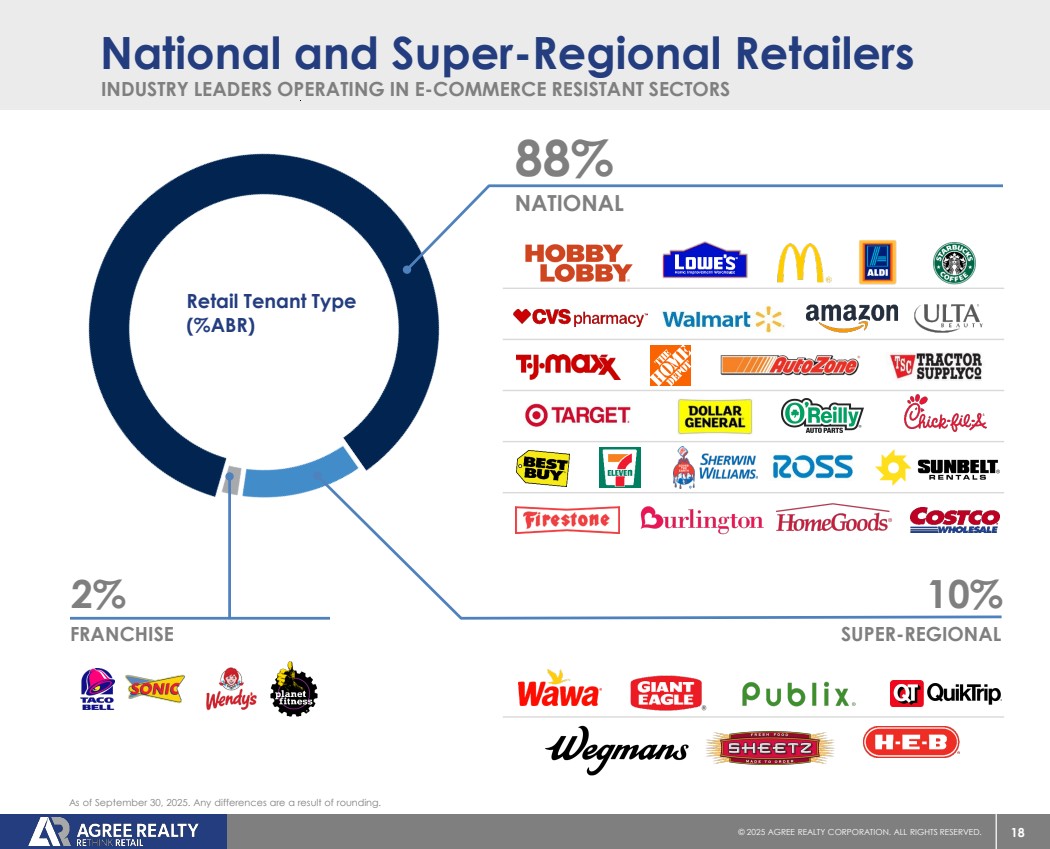

Portfolio Update

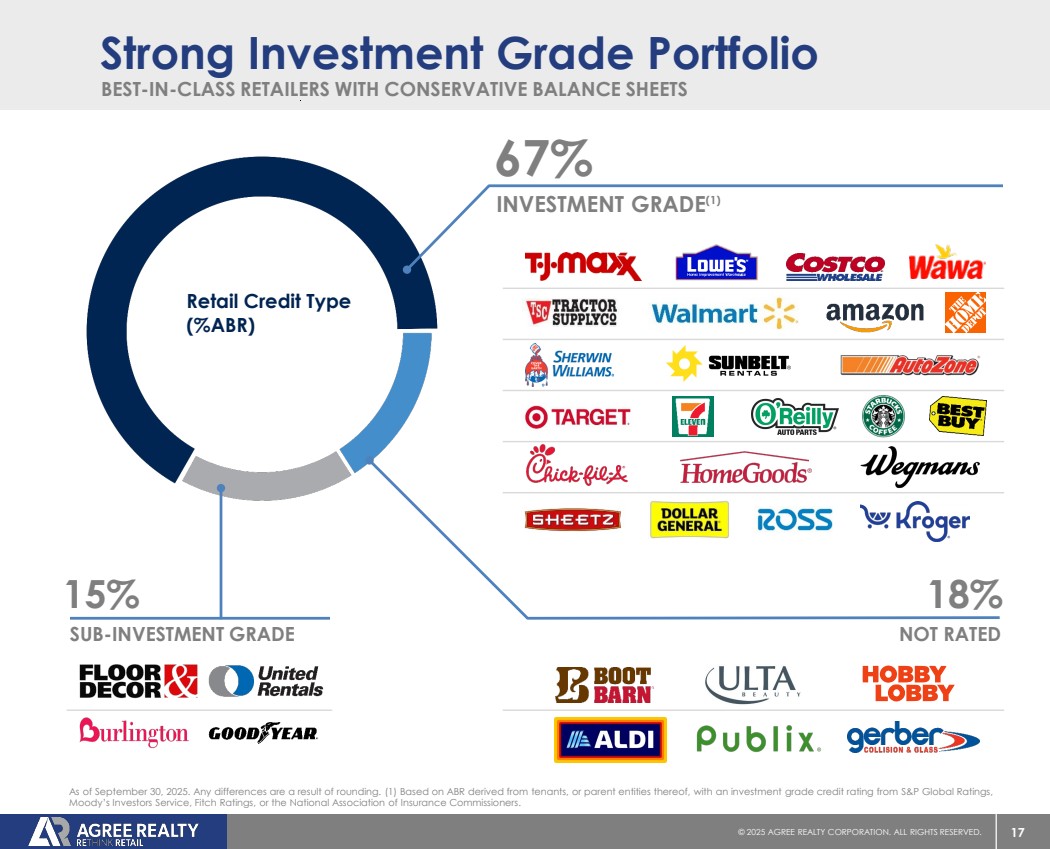

As of September 30, 2025, the Company’s portfolio consisted of 2,603 properties located in all 50 states and contained approximately 53.7 million square feet of gross leasable area. At quarter end, the portfolio was approximately 99.7% leased, had a weighted-average remaining lease term of approximately 8.0 years, and generated 66.7% of annualized base rents from investment grade retail tenants.

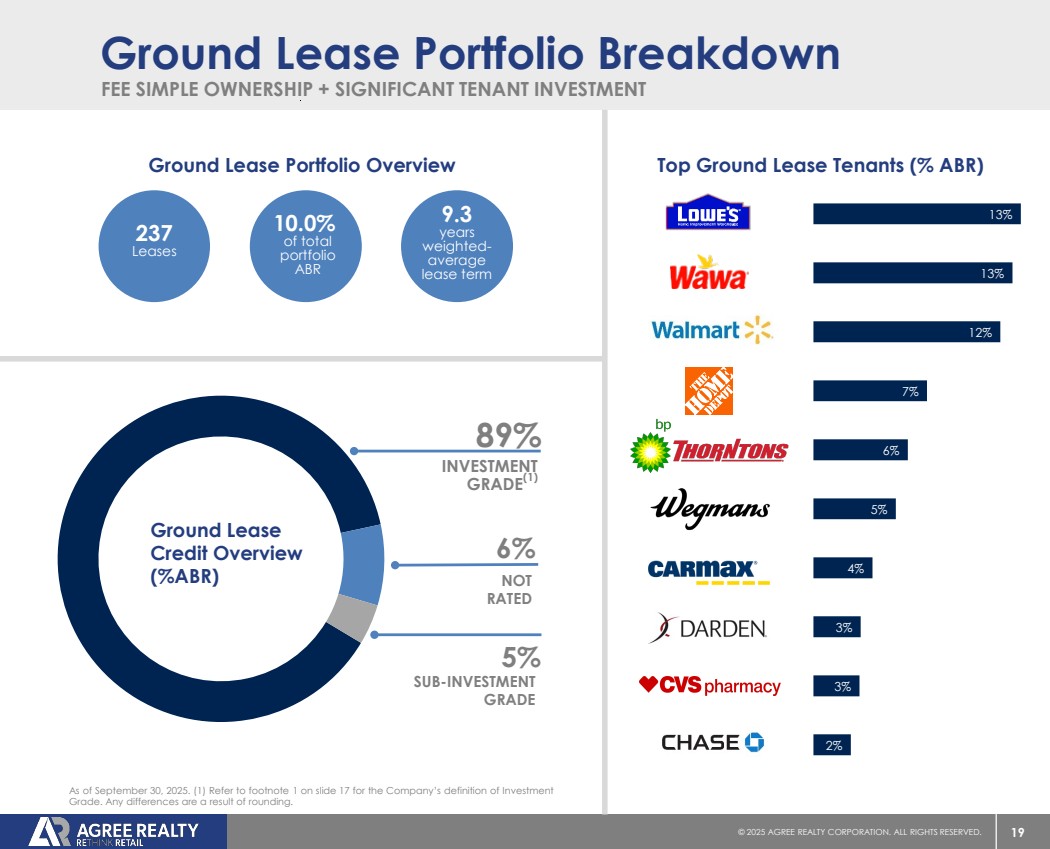

Ground Lease Portfolio

During the third quarter, the Company acquired six ground leases for an aggregate purchase price of approximately $22.5 million, representing 5.1% of annualized base rents acquired.

As of September 30, 2025, the Company’s ground lease portfolio consisted of 237 leases located in 38 states and totaled approximately 6.4 million square feet of gross leasable area. Properties ground leased to tenants represented 10.0% of annualized base rents.

At quarter end, the ground lease portfolio was fully occupied, had a weighted-average remaining lease term of approximately 9.3 years, and generated 88.5% of annualized base rents from investment grade retail tenants.

Acquisitions

Total acquisition volume for the third quarter was approximately $401.4 million and included 90 properties net leased to leading retailers operating in sectors including home improvement, auto parts, grocery stores, off-price,

farm and rural supply, convenience stores, and tire and auto service. The properties are located in 33 states and leased to tenants operating in 25 sectors.

The properties were acquired at a weighted-average capitalization rate of 7.2% and had a weighted-average remaining lease term of approximately 10.7 years. Approximately 70.0% of annualized base rents acquired were generated from investment grade retail tenants.

For the nine months ended September 30, 2025, total acquisition volume was approximately $1.1 billion. The 227 acquired properties are located in 40 states and leased to tenants who operate in 29 retail sectors. The properties were acquired at a weighted-average capitalization rate of 7.2% and had a weighted-average remaining lease term of approximately 12.0 years. Approximately 64.6% of annualized base rents were generated from investment grade retail tenants.

Dispositions

During the third quarter, the Company sold eight properties for gross proceeds of approximately $15.0 million. The dispositions were completed at a weighted-average capitalization rate of 7.4%. Notable dispositions included the Company’s only At Home located in Provo, Utah.

During the nine months ended September 30, 2025, the Company sold 13 properties for gross proceeds of approximately $23.7 million. The dispositions were completed at a weighted-average capitalization rate of 7.4%.

The Company is increasing the lower end of its full-year 2025 disposition guidance range from $10 million to $25 million, while maintaining the upper end of the range at $50 million.

Development and Developer Funding Platform

During the third quarter, the Company commenced five development or DFP projects, with total anticipated costs of approximately $50.8 million. Construction continued during the quarter on eight projects with anticipated costs totaling approximately $51.0 million. The Company completed eight projects during the quarter with total costs of approximately $61.2 million.

For the nine months ended September 30, 2025, the Company had 30 development or DFP projects completed or under construction with anticipated total costs of approximately $190.4 million. The projects are leased to leading retailers including TJX Companies, Burlington, 7-Eleven, Boot Barn, Ross Dress for Less, Five Below, Gerber Collision, and Sunbelt Rentals.

The following table presents estimated costs for the Company's active or completed development and DFP projects for the nine months ended September 30, 2025:

|

|

|

|

|

|

|

|

Anticipated |

|||

|

|

Number of |

|

Costs Funded |

|

Remaining |

|

Total Project |

|||

Quarter of Delivery |

|

Projects |

|

to Date |

|

Funding Costs |

|

Costs |

|||

Q1 2025 |

|

6 |

|

$ |

27,234 |

|

$ |

— |

|

$ |

27,234 |

Q2 2025 |

|

4 |

|

|

13,403 |

|

|

— |

|

|

13,403 |

Q3 2025 |

|

8 |

|

|

62,829 |

|

|

— |

|

|

62,829 |

Q4 2025 |

|

5 |

|

|

31,342 |

|

|

7,009 |

|

|

38,351 |

Q1 2026 |

|

2 |

|

|

12,327 |

|

|

3,124 |

|

|

15,451 |

Q2 2026 |

|

2 |

|

|

4,015 |

|

|

7,213 |

|

|

11,228 |

Q3 2026 |

|

2 |

|

|

3,948 |

|

|

14,233 |

|

|

18,181 |

Q4 2026 |

|

1 |

|

|

2,497 |

|

|

1,203 |

|

|

3,700 |

Total |

|

30 |

|

$ |

157,595 |

|

$ |

32,782 |

|

$ |

190,377 |

Development and DFP project costs are in thousands; any differences are the result of rounding. Costs Funded to Date may include adjustments related to completed projects to arrive at the correct Anticipated Total Project Costs.

Leasing Activity and Expirations

During the third quarter, the Company executed new leases, extensions or options on approximately 859,000-square feet of gross leasable area throughout the existing portfolio. Notable new leases, extensions or options included a 50,000-square foot TJ Maxx and HomeGoods combo store in Eugene, Oregon, a 27,000-square foot Burlington in Midland, Texas, and two Walmarts comprising over 310,000-square feet.

For the nine months ended September 30, 2025, the Company executed new leases, extensions or options on approximately 2.4 million square feet of gross leasable area throughout the existing portfolio.

As of September 30, 2025, the Company’s 2025 lease maturities represented 0.2% of annualized base rents. The following table presents contractual lease expirations within the Company’s portfolio as of September 30, 2025, assuming no tenants exercise renewal options:

|

|

|

|

|

|

|

Percent of |

|

|

|

|

|

|

|

|

|

Annualized |

|

Annualized |

|

Gross |

|

Percent of Gross |

Year |

|

Leases |

|

|

Base Rent (1) |

|

Base Rent |

|

Leasable Area |

|

Leasable Area |

2025 |

|

9 |

|

$ |

1,381 |

|

0.2% |

|

194 |

|

0.4% |

2026 |

|

70 |

|

|

14,990 |

|

2.1% |

|

1,548 |

|

2.9% |

2027 |

|

161 |

|

|

36,154 |

|

5.1% |

|

3,350 |

|

6.3% |

2028 |

|

182 |

|

|

47,938 |

|

6.8% |

|

4,136 |

|

7.7% |

2029 |

|

210 |

|

|

66,169 |

|

9.3% |

|

6,271 |

|

11.7% |

2030 |

|

331 |

|

|

71,143 |

|

10.1% |

|

5,875 |

|

11.0% |

2031 |

|

230 |

|

|

57,205 |

|

8.1% |

|

4,330 |

|

8.1% |

2032 |

|

247 |

|

|

52,336 |

|

7.4% |

|

3,767 |

|

7.0% |

2033 |

|

224 |

|

|

51,803 |

|

7.3% |

|

3,978 |

|

7.4% |

2034 |

|

227 |

|

|

52,089 |

|

7.4% |

|

3,490 |

|

6.5% |

Thereafter |

|

920 |

|

|

256,632 |

|

36.2% |

|

16,592 |

|

31.0% |

Total Portfolio |

|

2,811 |

|

$ |

707,840 |

|

100.0% |

|

53,531 |

|

100.0% |

The contractual lease expirations presented above exclude the effect of replacement tenant leases that had been executed as of September 30, 2025, but that had not yet commenced. Annualized Base Rent and gross leasable area (square feet) are in thousands; any differences are the result of rounding.

| (1) | Annualized Base Rent represents the annualized amount of contractual minimum rent required by tenant lease agreements as of September 30, 2025, computed on a straight-line basis. Annualized Base Rent is not, and is not intended to be, a presentation in accordance with generally accepted accounting principles (“GAAP”). The Company believes annualized contractual minimum rent is useful to management, investors, and other interested parties in analyzing concentrations and leasing activity. |

Top Tenants

The following table presents annualized base rents for all tenants that represent 1.5% or greater of the Company’s total annualized base rent as of September 30, 2025:

|

|

Annualized |

|

Percent of |

|

Tenant |

|

Base Rent(1) |

|

Annualized Base Rent |

|

Walmart |

$ |

41,155 |

|

|

5.8% |

Tractor Supply |

|

34,961 |

|

|

4.9% |

Dollar General |

|

28,437 |

|

|

4.0% |

Best Buy |

|

21,716 |

|

|

3.1% |

O'Reilly Auto Parts |

|

21,500 |

|

|

3.0% |

Kroger |

|

21,039 |

|

|

3.0% |

TJX Companies |

|

21,009 |

|

|

3.0% |

CVS |

|

20,886 |

|

|

3.0% |

Hobby Lobby |

|

20,220 |

|

|

2.9% |

Lowe's |

|

17,884 |

|

|

2.5% |

Gerber Collision |

|

17,296 |

|

|

2.4% |

7-Eleven |

|

17,181 |

|

|

2.4% |

Sunbelt Rentals |

|

16,979 |

|

|

2.4% |

Burlington |

|

15,133 |

|

|

2.1% |

Sherwin-Williams |

|

13,675 |

|

|

1.9% |

Home Depot |

|

13,553 |

|

|

1.9% |

Dollar Tree |

|

11,540 |

|

|

1.6% |

Genuine Parts Company (NAPA Auto Parts) |

|

11,420 |

|

|

1.6% |

Wawa |

|

11,111 |

|

|

1.6% |

Other(2) |

|

331,145 |

|

|

46.9% |

Total Portfolio |

$ |

707,840 |

|

|

100.0% |

Annualized Base Rent is in thousands; any differences are the result of rounding.

(1)Refer to footnote 1 on page 5 for the Company’s definition of Annualized Base Rent.

(2) Includes tenants generating less than 1.5% of Annualized Base Rent.

Retail Sectors

The following table presents annualized base rents for all the Company’s retail sectors as of September 30, 2025:

|

|

Annualized |

|

Percent of |

|

Sector |

|

Base Rent(1) |

|

Annualized Base Rent |

|

Grocery Stores |

$ |

72,940 |

|

|

10.3% |

Home Improvement |

|

62,545 |

|

|

8.8% |

Convenience Stores |

|

54,938 |

|

|

7.8% |

Tire and Auto Service |

|

54,224 |

|

|

7.6% |

Auto Parts |

|

48,088 |

|

|

6.8% |

Dollar Stores |

|

46,809 |

|

|

6.6% |

Off-Price Retail |

|

42,194 |

|

|

6.0% |

Farm and Rural Supply |

|

36,733 |

|

|

5.2% |

General Merchandise |

|

36,643 |

|

|

5.2% |

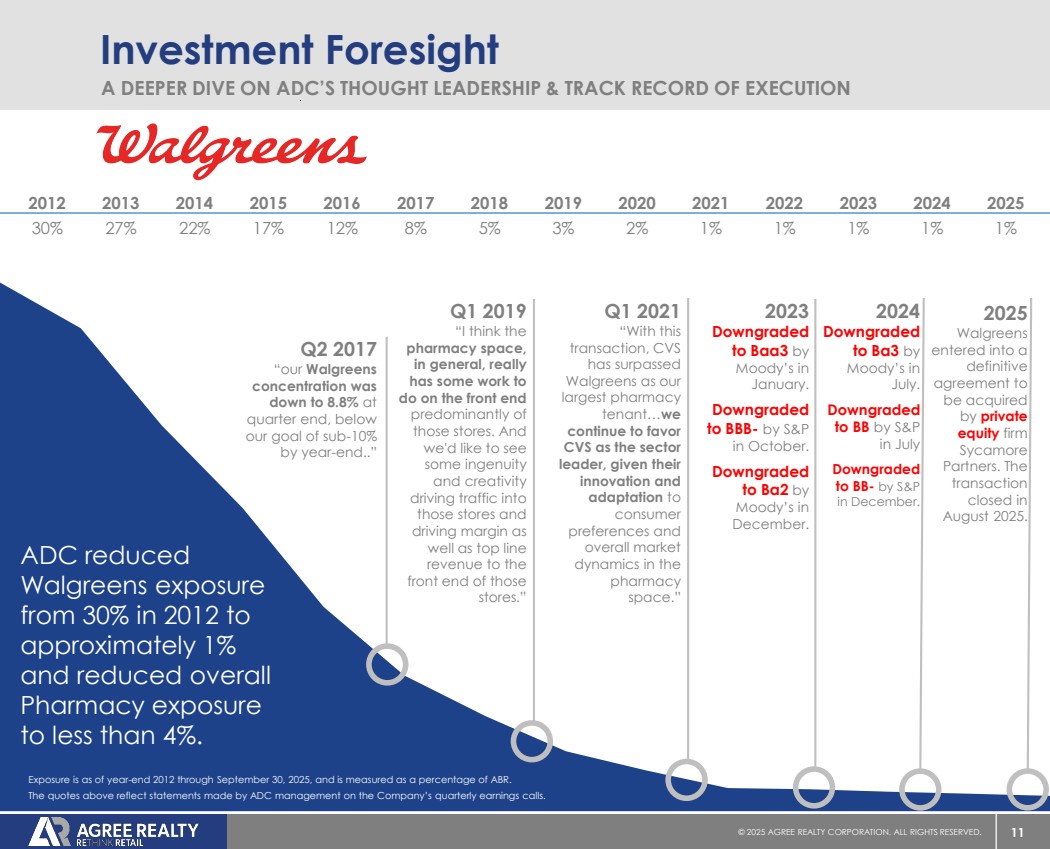

Pharmacy |

|

25,837 |

|

|

3.7% |

Consumer Electronics |

|

25,496 |

|

|

3.6% |

Crafts and Novelties |

|

22,482 |

|

|

3.2% |

Discount Stores |

|

18,598 |

|

|

2.6% |

Equipment Rental |

|

18,035 |

|

|

2.5% |

Health Services |

|

17,444 |

|

|

2.5% |

Warehouse Clubs |

|

16,823 |

|

|

2.4% |

Dealerships |

|

15,078 |

|

|

2.1% |

Restaurants - Quick Service |

|

13,886 |

|

|

2.0% |

Health and Fitness |

|

13,789 |

|

|

1.9% |

Sporting Goods |

|

11,528 |

|

|

1.6% |

Specialty Retail |

|

9,978 |

|

|

1.4% |

Financial Services |

|

8,235 |

|

|

1.2% |

Restaurants - Casual Dining |

|

6,531 |

|

|

0.9% |

Shoes |

|

4,879 |

|

|

0.7% |

Home Furnishings |

|

4,857 |

|

|

0.7% |

Pet Supplies |

|

4,468 |

|

|

0.6% |

Theaters |

|

3,976 |

|

|

0.6% |

Beauty and Cosmetics |

|

3,776 |

|

|

0.5% |

Entertainment Retail |

|

2,651 |

|

|

0.4% |

Apparel |

|

2,449 |

|

|

0.3% |

Miscellaneous |

|

1,306 |

|

|

0.2% |

Office Supplies |

|

624 |

|

|

0.1% |

Total Portfolio |

$ |

707,840 |

|

|

100.0% |

Annualized Base Rent is in thousands; any differences are the result of rounding.

Geographic Diversification

The following table presents annualized base rents for all states that represent 1.5% or greater of the Company’s total annualized base rent as of September 30, 2025:

|

|

Annualized |

|

Percent of |

|

State |

|

Base Rent(1) |

|

Annualized Base Rent |

|

Texas |

$ |

49,981 |

|

|

7.1% |

Illinois |

|

44,556 |

|

|

6.3% |

Michigan |

|

36,948 |

|

|

5.2% |

Ohio |

|

36,273 |

|

|

5.1% |

New York |

|

35,959 |

|

|

5.1% |

Pennsylvania |

|

34,520 |

|

|

4.9% |

Florida |

|

33,971 |

|

|

4.8% |

North Carolina |

|

32,519 |

|

|

4.6% |

California |

|

31,218 |

|

|

4.4% |

Georgia |

|

28,401 |

|

|

4.0% |

New Jersey |

|

24,421 |

|

|

3.5% |

Wisconsin |

|

20,038 |

|

|

2.8% |

Missouri |

|

19,818 |

|

|

2.8% |

Louisiana |

|

19,242 |

|

|

2.7% |

Virginia |

|

17,513 |

|

|

2.5% |

Mississippi |

|

16,706 |

|

|

2.4% |

South Carolina |

|

16,050 |

|

|

2.3% |

Kansas |

|

15,916 |

|

|

2.2% |

Minnesota |

|

15,578 |

|

|

2.2% |

Indiana |

|

13,994 |

|

|

2.0% |

Connecticut |

|

13,474 |

|

|

1.9% |

Tennessee |

|

13,466 |

|

|

1.9% |

Massachusetts |

|

13,004 |

|

|

1.8% |

Alabama |

|

12,591 |

|

|

1.8% |

Oklahoma |

|

10,821 |

|

|

1.5% |

Other(2) |

|

100,862 |

|

|

14.2% |

Total Portfolio |

$ |

707,840 |

|

|

100.0% |

Annualized Base Rent is in thousands; any differences are the result of rounding.

(1) Refer to footnote 1 on page 5 for the Company’s definition of Annualized Base Rent.

(2) Includes states generating less than 1.5% of Annualized Base Rent.

Capital Markets, Liquidity and Balance Sheet

Capital Markets

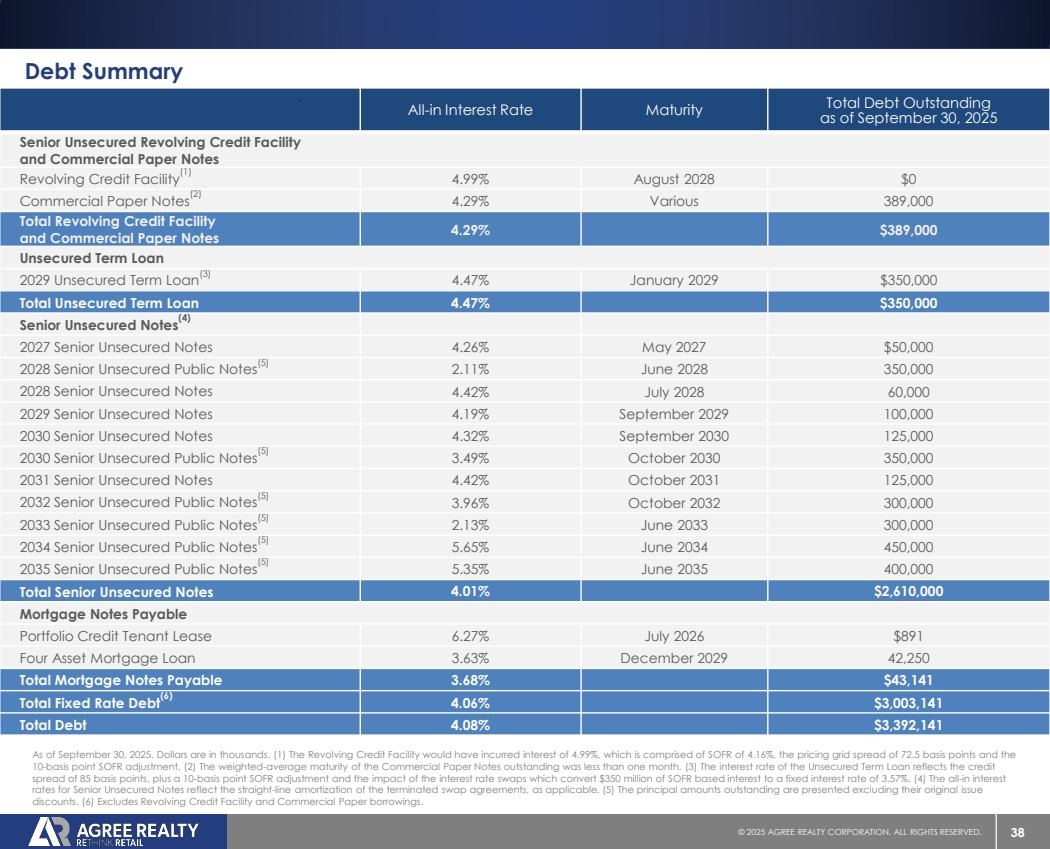

Subsequent to quarter end, the Company received commitments for an unsecured $350 million 5.5-year term loan with a 12-month delayed draw feature (the “Term Loan”). The Company anticipates closing the Term Loan in November and has entered into $350 million of forward starting swaps to fix SOFR until maturity in May 2031. Including the impact of the swaps, the interest rate on the Term Loan is fixed at 4.02% based on the Company’s current A- credit rating. The Term Loan includes an accordion option that allows the Company to request additional lender commitments up to a total of $500 million.

During the third quarter, the Company settled 3.5 million shares under existing forward sale agreements for net proceeds of $252.0 million.

The following table presents the Company’s outstanding forward equity offerings as of September 30, 2025:

|

|

|

|

|

|

|

|

|

|

|

|

Anticipated Net |

Forward Equity |

|

Shares |

|

Shares |

|

Shares |

|

|

Net Proceeds |

|

|

Proceeds |

Offerings |

|

Sold |

|

Settled |

|

Remaining |

|

|

Received |

|

|

Remaining |

Q3 2024 ATM Forward Offerings |

|

6,602,317 |

|

6,338,391 |

|

263,926 |

|

$ |

448,734,524 |

|

$ |

19,465,097 |

Q4 2024 ATM Forward Offerings |

|

739,013 |

|

— |

|

739,013 |

|

|

— |

|

|

55,007,059 |

October 2024 Forward Offering |

|

5,060,000 |

|

— |

|

5,060,000 |

|

|

— |

|

|

366,383,974 |

Q1 2025 ATM Forward Offerings |

|

2,408,201 |

|

— |

|

2,408,201 |

|

|

— |

|

|

181,169,482 |

Q2 2025 ATM Forward Offerings |

|

362,021 |

|

— |

|

362,021 |

|

|

— |

|

|

27,351,284 |

April 2025 Forward Offering |

|

5,175,000 |

|

— |

|

5,175,000 |

|

|

— |

|

|

386,733,443 |

Total Forward Equity Offerings |

|

20,346,552 |

|

6,338,391 |

|

14,008,161 |

|

$ |

448,734,524 |

|

$ |

1,036,110,339 |

Liquidity

As of September 30, 2025, the Company had total liquidity of $1.9 billion, which includes $861.0 million of availability under its revolving credit facility after adjusting for outstanding commercial paper notes and revolver borrowings, $1.0 billion of outstanding forward equity, and $16.9 million of cash on hand. The Company’s $1.25 billion revolving credit facility includes an accordion option that allows the Company to request additional lender commitments of up to a total of $2.0 billion.

Balance Sheet

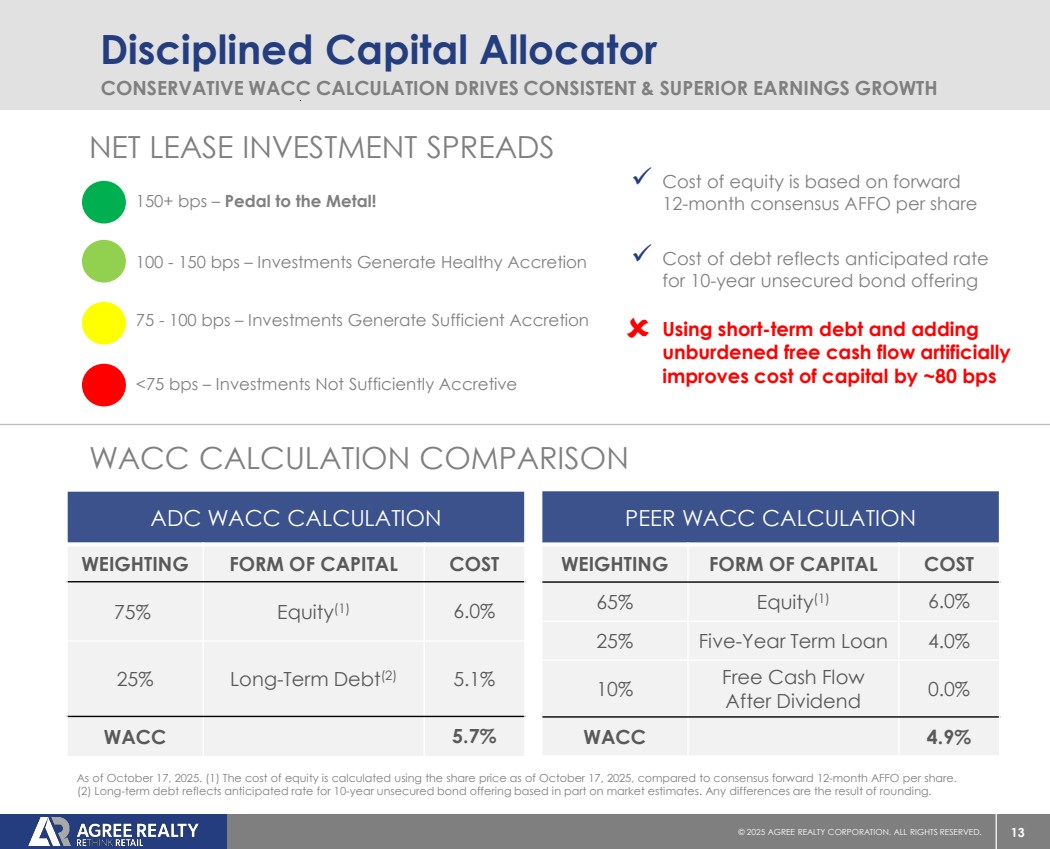

As of September 30, 2025, the Company’s net debt to recurring EBITDA was 5.1 times. The Company’s proforma net debt to recurring EBITDA was 3.5 times when deducting the $1.0 billion of anticipated net proceeds from the outstanding forward equity offerings from the Company’s net debt of $3.4 billion as of September 30, 2025. The Company’s fixed charge coverage ratio was 4.2 times at quarter end.

The Company’s total debt to enterprise value was 29.0% as of September 30, 2025. Enterprise value is calculated as the sum of net debt, the liquidation value of the Company’s preferred stock, and the market value of the Company’s outstanding shares of common stock, assuming conversion of Agree Limited Partnership (the “Operating Partnership” or “OP”) common units into common stock of the Company.

For the three months and nine months ended September 30, 2025, the Company's fully diluted weighted-average shares outstanding were 111.5 million and 109.9 million, respectively. The basic weighted-average shares outstanding for the three and nine months ended September 30, 2025 were 111.3 million and 109.4 million, respectively.

For the three months and nine months ended September 30, 2025, the Company's fully diluted weighted-average shares and units outstanding were 111.9 million and 110.2 million, respectively. The basic weighted-average shares and units outstanding for the three and nine months ended September 30, 2025 were 111.6 million and 109.7 million, respectively.

The Company’s assets are held by, and its operations are conducted through, the Operating Partnership, of which the Company is the sole general partner. As of September 30, 2025, there were 347,619 Operating Partnership common units outstanding, and the Company held a 99.7% common interest in the Operating Partnership.

Conference Call/Webcast

The Company will host its quarterly analyst and investor conference call on Wednesday, October 22, 2025 at 9:00 AM ET. To participate in the conference call, please dial (800) 715-9871 approximately ten minutes before the call begins.

Additionally, a webcast of the conference call will be available via the Company’s website. To access the webcast, visit www.agreerealty.com ten minutes prior to the start of the conference call and go to the Investors section of the website. A replay of the conference call webcast will be archived and available online through the Investors section of www.agreerealty.com.

About Agree Realty Corporation

Agree Realty Corporation is a publicly traded real estate investment trust that is RETHINKING RETAIL through the acquisition and development of properties net leased to industry-leading, omni-channel retail tenants. As of September 30, 2025, the Company owned and operated a portfolio of 2,603 properties, located in all 50 states and containing approximately 53.7 million square feet of gross leasable area. The Company’s common stock is listed on the New York Stock Exchange under the symbol “ADC”. For additional information on the Company and RETHINKING RETAIL, please visit www.agreerealty.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Company intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and includes this statement for purposes of complying with these safe harbor provisions. Forward-looking statements, which are based on certain assumptions and describe the Company’s future plans, strategies and expectations, are generally identifiable by use of the words “anticipate,” “estimate,” “should,” “expect,” “believe,” “intend,” “may,” “will,” “seek,” “could,” “project” or other similar expressions. You should not rely on forward-looking statements since they involve known and unknown risks, uncertainties and other factors which are, in some cases, beyond the Company’s control and which could materially affect the Company’s results of operations, financial condition, cash flows, performance or future achievements or events. Factors which may cause actual results to differ materially from current expectations include, but are not limited to, the factors included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2024, including those set forth under the headings “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and subsequent quarterly reports filed with the SEC. The forward-looking statements included in this press release are made as of the date hereof. Unless legally required, the Company disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events, changes in the Company’s expectations or assumptions or otherwise.

For further information about the Company’s business and financial results, please refer to the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors” sections of the Company’s SEC filings, including, but not limited to, its Annual Report on Form 10-K and Quarterly Reports on Form 10-Q, copies of which may be obtained at the Investor Relations section of the Company’s website at www.agreerealty.com.

The Company defines the “weighted-average capitalization rate” for acquisitions and dispositions as the sum of contractual fixed annual rents computed on a straight-line basis over the primary lease terms and anticipated annual net tenant recoveries, divided by the purchase and sale prices for occupied properties.

The Company defines the "all-in rate" as the interest rate that reflects the straight-line amortization of the terminated swap agreements and original issuance discount, as applicable.

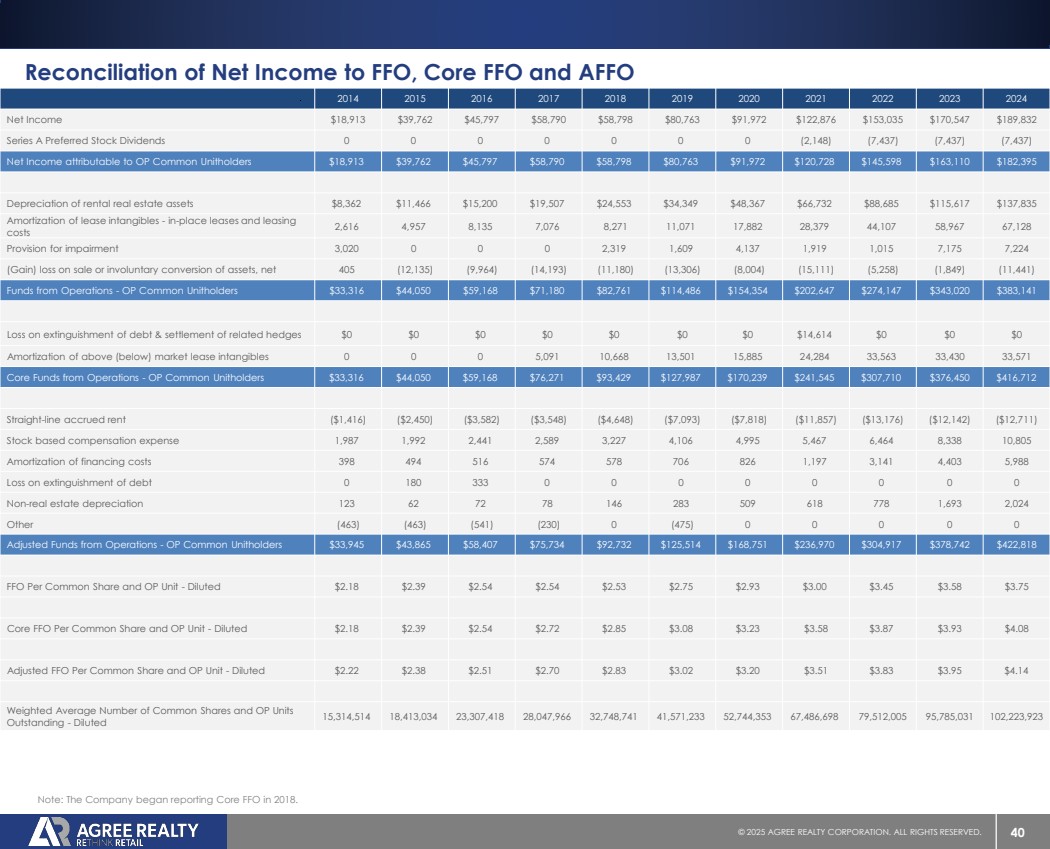

References to “Core FFO” and “AFFO” in this press release are representative of Core FFO attributable to OP common unitholders and AFFO attributable to OP common unitholders. Detailed calculations for these measures are shown in the Reconciliation of Net Income to FFO, Core FFO and Adjusted FFO table as “Core Funds From Operations – OP Common Unitholders” and “Adjusted Funds from Operations – OP Common Unitholders”.

###

Contact:

Peter Coughenour

Chief Financial Officer

Agree Realty Corporation

(248) 737-4190

Agree Realty Corporation |

Consolidated Balance Sheet |

($ in thousands, except share and per-share data) |

(Unaudited) |

|

|

September 30, |

|

December 31, |

||

|

|

2025 |

|

2024 |

||

ASSETS |

|

|

|

|

|

|

Real estate investments |

|

|

|

|

|

|

Land |

|

$ |

2,787,363 |

|

$ |

2,514,167 |

Buildings |

|

|

6,123,531 |

|

|

5,412,564 |

Less accumulated depreciation |

|

|

(677,700) |

|

|

(564,429) |

|

|

|

8,233,194 |

|

|

7,362,302 |

Property under development |

|

|

64,047 |

|

|

55,806 |

Net real estate investments |

|

|

8,297,241 |

|

|

7,418,108 |

|

|

|

|

|

|

|

Real estate held for sale, net |

|

|

706 |

|

|

— |

Cash and cash equivalents |

|

|

13,696 |

|

|

6,399 |

Cash held in escrow |

|

|

3,182 |

|

|

— |

Accounts receivable - tenants, net |

|

|

117,602 |

|

|

106,416 |

Lease intangibles, net of accumulated amortization of $546,136 and $461,419 at September 30, 2025 and December 31, 2024, respectively |

|

|

966,964 |

|

|

864,937 |

Other assets, net |

|

|

84,639 |

|

|

90,586 |

|

|

|

|

|

|

|

Total Assets |

|

$ |

9,484,030 |

|

$ |

8,486,446 |

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

Mortgage notes payable, net |

|

$ |

41,718 |

|

$ |

42,210 |

Unsecured term loan, net |

|

|

347,900 |

|

|

347,452 |

Senior unsecured notes, net |

|

|

2,583,685 |

|

|

2,237,759 |

Unsecured revolving credit facility and commercial paper notes |

|

|

389,000 |

|

|

158,000 |

Dividends and distributions payable |

|

|

29,927 |

|

|

27,842 |

Accounts payable, accrued expenses, and other liabilities |

|

|

161,782 |

|

|

116,273 |

Lease intangibles, net of accumulated amortization of $48,671 and $46,003 at September 30, 2025 and December 31, 2024, respectively |

|

|

56,777 |

|

|

46,249 |

|

|

|

|

|

|

|

Total Liabilities |

|

|

3,610,789 |

|

|

2,975,785 |

|

|

|

|

|

|

|

EQUITY |

|

|

|

|

|

|

Preferred stock, $.0001 par value per share, 4,000,000 shares authorized, 7,000 shares Series A outstanding, at stated liquidation value of $25,000 per share, at September 30, 2025 and December 31, 2024 |

|

|

175,000 |

|

|

175,000 |

Common stock, $.0001 par value, 360,000,000 and 180,000,000 shares authorized, 114,134,251 and 107,248,705 shares issued and outstanding at September 30, 2025 and December 31, 2024, respectively |

|

|

11 |

|

|

10 |

Additional paid-in-capital |

|

|

6,247,606 |

|

|

5,765,582 |

Dividends in excess of net income |

|

|

(581,162) |

|

|

(470,622) |

Accumulated other comprehensive income |

|

|

31,528 |

|

|

40,076 |

|

|

|

|

|

|

|

Total equity - Agree Realty Corporation |

|

|

5,872,983 |

|

|

5,510,046 |

Non-controlling interest |

|

|

258 |

|

|

615 |

Total Equity |

|

|

5,873,241 |

|

|

5,510,661 |

|

|

|

|

|

|

|

Total Liabilities and Equity |

|

$ |

9,484,030 |

|

$ |

8,486,446 |

Agree Realty Corporation | ||||||||||||

Consolidated Statements of Operations and Comprehensive Income | ||||||||||||

($ in thousands, except share and per-share data) | ||||||||||||

(Unaudited) | ||||||||||||

|

|

Three Months Ended |

|

Nine Months Ended |

||||||||

|

|

September 30, 2025 |

|

September 30, 2024 |

|

September 30, 2025 |

|

September 30, 2024 |

||||

Revenues |

|

|

|

|

|

|

|

|

|

|

|

|

Rental income |

|

$ |

183,191 |

|

$ |

154,292 |

|

$ |

527,701 |

|

$ |

456,139 |

Other |

|

|

31 |

|

|

40 |

|

|

208 |

|

|

222 |

Total Revenues |

|

|

183,222 |

|

|

154,332 |

|

|

527,909 |

|

|

456,361 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

Real estate taxes |

|

|

13,173 |

|

|

11,935 |

|

|

37,519 |

|

|

33,357 |

Property operating expenses |

|

|

8,243 |

|

|

6,015 |

|

|

25,040 |

|

|

19,875 |

Land lease expense |

|

|

556 |

|

|

421 |

|

|

1,592 |

|

|

1,251 |

General and administrative |

|

|

10,887 |

|

|

9,114 |

|

|

32,990 |

|

|

28,336 |

Depreciation and amortization |

|

|

61,179 |

|

|

51,504 |

|

|

175,872 |

|

|

150,421 |

Provision for impairment |

|

|

2,980 |

|

|

2,694 |

|

|

10,272 |

|

|

7,224 |

Total Operating Expenses |

|

|

97,018 |

|

|

81,683 |

|

|

283,285 |

|

|

240,464 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gain on sale of assets, net |

|

|

924 |

|

|

1,850 |

|

|

3,207 |

|

|

11,102 |

Gain (loss) on involuntary conversion, net |

|

|

132 |

|

|

(56) |

|

|

132 |

|

|

(91) |

Income from Operations |

|

|

87,260 |

|

|

74,443 |

|

|

247,963 |

|

|

226,908 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Other (Expense) Income |

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense, net |

|

|

(35,212) |

|

|

(28,942) |

|

|

(98,250) |

|

|

(79,809) |

Income and other tax expense |

|

|

(225) |

|

|

(1,077) |

|

|

(1,475) |

|

|

(3,231) |

Other income |

|

|

456 |

|

|

104 |

|

|

542 |

|

|

587 |

Net Income |

|

|

52,279 |

|

|

44,528 |

|

|

148,780 |

|

|

144,455 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Less net income attributable to non-controlling interest |

|

|

162 |

|

|

153 |

|

|

468 |

|

|

497 |

Net income attributable to Agree Realty Corporation |

|

|

52,117 |

|

|

44,375 |

|

|

148,312 |

|

|

143,958 |

Less Series A preferred stock dividends |

|

|

1,859 |

|

|

1,859 |

|

|

5,578 |

|

|

5,578 |

Net Income Attributable to Common Stockholders |

|

$ |

50,258 |

|

$ |

42,516 |

|

$ |

142,734 |

|

$ |

138,380 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income Per Share Attributable to Common Stockholders |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

0.45 |

|

$ |

0.42 |

|

$ |

1.30 |

|

$ |

1.38 |

Diluted |

|

$ |

0.45 |

|

$ |

0.42 |

|

$ |

1.30 |

|

$ |

1.37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Comprehensive Income |

|

|

|

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

52,279 |

|

$ |

44,528 |

|

$ |

148,780 |

|

$ |

144,455 |

Amortization of interest rate swaps |

|

|

(1,077) |

|

|

(739) |

|

|

(2,692) |

|

|

(2,043) |

Change in fair value and settlement of interest rate swaps |

|

|

713 |

|

|

(11,760) |

|

|

(5,884) |

|

|

3,955 |

Total comprehensive income |

|

|

51,915 |

|

|

32,029 |

|

|

140,204 |

|

|

146,367 |

Less comprehensive income attributable to non-controlling interest |

|

|

161 |

|

|

110 |

|

|

441 |

|

|

504 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Comprehensive Income Attributable to Agree Realty Corporation |

|

$ |

51,754 |

|

$ |

31,919 |

|

$ |

139,763 |

|

$ |

145,863 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average Number of Common Shares Outstanding - Basic |

|

|

111,277,316 |

|

|

100,383,207 |

|

|

109,383,735 |

|

|

100,343,493 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average Number of Common Shares Outstanding - Diluted |

|

|

111,511,615 |

|

|

101,715,311 |

|

|

109,875,336 |

|

|

100,882,858 |

Agree Realty Corporation | |||||||||||||

Reconciliation of Net Income to FFO, Core FFO and Adjusted FFO | |||||||||||||

($ in thousands, except share and per-share data) | |||||||||||||

(Unaudited) | |||||||||||||

|

|

Three Months Ended |

|

Nine Months Ended |

|||||||||

|

|

September 30, 2025 |

|

September 30, 2024 |

|

September 30, 2025 |

|

September 30, 2024 |

|||||

Reconciliation from Net Income to Funds from Operations |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

52,279 |

|

$ |

44,528 |

|

$ |

148,780 |

|

$ |

144,455 |

|

Less Series A preferred stock dividends |

|

|

1,859 |

|

|

1,859 |

|

|

5,578 |

|

|

5,578 |

|

Net income attributable to Operating Partnership common unitholders |

|

|

50,420 |

|

|

42,669 |

|

|

143,202 |

|

|

138,877 |

|

Depreciation of rental real estate assets |

|

|

40,867 |

|

|

33,941 |

|

|

116,728 |

|

|

99,438 |

|

Amortization of lease intangibles - in-place leases and leasing costs |

|

|

19,715 |

|

|

17,056 |

|

|

57,458 |

|

|

49,476 |

|

Provision for impairment |

|

|

2,980 |

|

|

2,694 |

|

|

10,272 |

|

|

7,224 |

|

(Gain) loss on sale or involuntary conversion of assets, net |

|

|

(1,056) |

|

|

(1,794) |

|

|

(3,339) |

|

|

(11,011) |

|

Funds from Operations - Operating Partnership common unitholders |

|

$ |

112,926 |

|

$ |

94,566 |

|

$ |

324,321 |

|

$ |

284,004 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amortization of above (below) market lease intangibles, net and assumed mortgage debt discount, net |

|

|

9,428 |

|

|

8,377 |

|

|

26,679 |

|

|

25,137 |

|

Core Funds from Operations - Operating Partnership common unitholders |

|

$ |

122,354 |

|

$ |

102,943 |

|

$ |

351,000 |

|

$ |

309,141 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Straight-line accrued rent |

|

|

(4,976) |

|

|

(3,332) |

|

|

(12,774) |

|

|

(9,675) |

|

Stock-based compensation expense |

|

|

3,306 |

|

|

2,780 |

|

|

9,694 |

|

|

7,993 |

|

Amortization of financing costs and original issue discounts |

|

|

1,836 |

|

|

1,871 |

|

|

5,150 |

|

|

4,359 |

|

Non-real estate depreciation |

|

|

597 |

|

|

507 |

|

|

1,686 |

|

|

1,507 |

|

Adjusted Funds from Operations - Operating Partnership common unitholders |

|

$ |

123,117 |

|

$ |

104,769 |

|

$ |

354,756 |

|

$ |

313,325 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Funds from Operations per common share and partnership unit - diluted |

|

$ |

1.01 |

|

$ |

0.93 |

|

$ |

2.94 |

|

$ |

2.81 |

|

Core Funds from Operations per common share and partnership unit - diluted |

|

$ |

1.09 |

|

$ |

1.01 |

|

$ |

3.18 |

|

$ |

3.05 |

|

Adjusted Funds from Operations per common share and partnership unit - diluted |

|

$ |

1.10 |

|

$ |

1.03 |

|

$ |

3.22 |

|

$ |

3.10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average shares and Operating Partnership common units outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

111,624,935 |

|

|

100,730,826 |

|

|

109,731,354 |

|

|

100,691,112 |

|

Diluted |

|

|

111,859,234 |

|

|

102,062,930 |

|

|

110,222,955 |

|

|

101,230,477 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional supplemental disclosure |

|

|

|

|

|

|

|

|

|

|

|

|

|

Scheduled principal repayments |

|

$ |

258 |

|

$ |

243 |

|

$ |

763 |

|

$ |

717 |

|

Capitalized interest |

|

$ |

558 |

|

$ |

425 |

|

$ |

1,497 |

|

$ |

1,126 |

|

Capitalized building improvements |

|

$ |

2,502 |

|

$ |

6,714 |

|

$ |

5,864 |

|

$ |

10,504 |

|

|

Non-GAAP Financial Measures | |||||||||||||

Agree Realty Corporation | |||

Reconciliation of Non-GAAP Financial Measures | |||

($ in thousands, except share and per-share data) | |||

(Unaudited) | |||

|

|

|

Three months ended |

|

|

|

September 30, |

|

|

|

2025 |

Mortgage notes payable, net |

|

$ |

41,718 |

Unsecured term loan, net |

|

|

347,900 |

Senior unsecured notes, net |

|

|

2,583,685 |

Unsecured revolving credit facility and commercial paper notes |

|

|

389,000 |

Total Debt per the Consolidated Balance Sheet |

|

$ |

3,362,303 |

|

|

|

|

Unamortized debt issuance costs and discounts, net |

|

|

29,838 |

Total Debt |

|

$ |

3,392,141 |

|

|

|

|

Cash and cash equivalents |

|

$ |

(13,696) |

Cash held in escrows |

|

|

(3,182) |

Net Debt |

|

$ |

3,375,263 |

|

|

|

|

Anticipated Net Proceeds from Forward Equity Offerings |

|

|

(1,036,110) |

Proforma Net Debt |

|

$ |

2,339,153 |

|

|

|

|

Net Income |

|

$ |

52,279 |

Interest expense, net |

|

|

35,212 |

Income and other tax expense |

|

|

225 |

Depreciation of rental real estate assets |

|

|

40,867 |

Amortization of lease intangibles - in-place leases and leasing costs |

|

|

19,715 |

Non-real estate depreciation |

|

|

597 |

Provision for Impairment |

|

|

2,980 |

(Gain) loss on sale or involuntary conversion of assets, net |

|

|

(1,056) |

EBITDAre |

|

$ |

150,819 |

|

|

|

|

Run-Rate Impact of Investment, Disposition and Leasing Activity |

|

|

5,601 |

Amortization of above (below) market lease intangibles, net |

|

|

9,344 |

Recurring EBITDA |

|

$ |

165,764 |

|

|

|

|

Annualized Recurring EBITDA |

|

$ |

663,056 |

|

|

|

|

Total Debt per the Consolidated Balance Sheet to Annualized Net Income |

|

|

16.2x |

|

|

|

|

Net Debt to Recurring EBITDA |

|

|

5.1x |

|

|

|

|

Proforma Net Debt to Recurring EBITDA |

|

|

3.5x |

Financial Measures

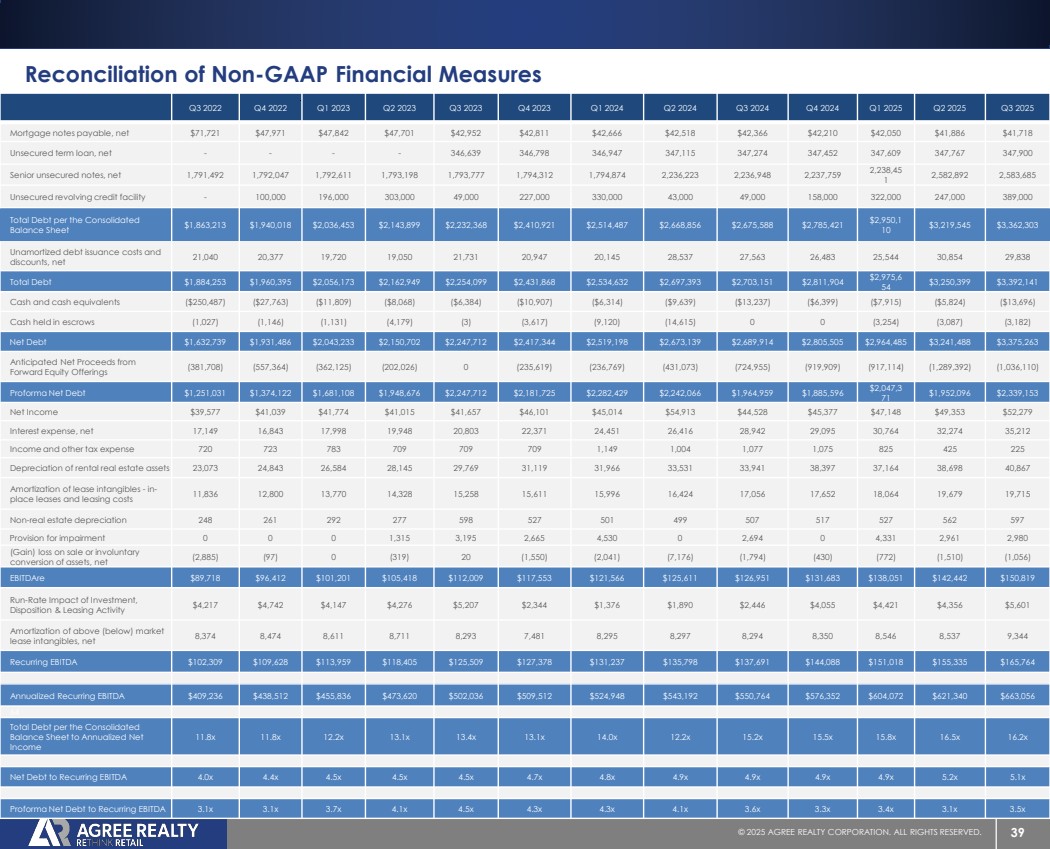

Total Debt and Net Debt

The Company defines Total Debt as debt per the consolidated balance sheet excluding unamortized debt issuance costs, original issue discounts and debt discounts. Net Debt is defined as Total Debt less cash, cash equivalents and cash held in escrows. The Company considers the non-GAAP measures of Total Debt and Net Debt to be key supplemental measures of the Company's overall liquidity, capital structure and leverage because they provide industry analysts, lenders and investors useful information in understanding our financial condition. The Company's calculation of Total Debt and Net Debt may not be comparable to Total Debt and Net Debt reported by other REITs that interpret the definitions differently than the Company. The Company presents Net Debt on both an actual and proforma basis, assuming the net proceeds of the Forward Offerings (see below) are used to pay down debt. The Company believes the proforma measure may be useful to investors in understanding the potential effect of the Forward Offerings on the Company's capital structure, its future borrowing capacity, and its ability to service its debt.

Forward Offerings

The Company has 14,008,161 shares remaining to be settled under the Forward Equity Offerings. Upon settlement, the offerings are anticipated to raise net proceeds of approximately $1.0 billion based on the applicable forward sale price as of September 30, 2025. The applicable forward sale price varies depending on the offering. The Company is contractually obligated to settle the offerings by certain dates between October 2025 and October 2026.

EBITDAre

EBITDAre is defined by Nareit to mean net income computed in accordance with GAAP, plus interest expense, income tax expense, depreciation and amortization, any gains (or losses) from sales of real estate assets and/or changes in control, any impairment charges on depreciable real estate assets, and after adjustments for unconsolidated partnerships and joint ventures. The Company considers the non-GAAP measure of EBITDAre to be a key supplemental measure of the Company's performance and should be considered along with, but not as an alternative to, net income or loss as a measure of the Company's operating performance. The Company considers EBITDAre a key supplemental measure of the Company's operating performance because it provides an additional supplemental measure of the Company's performance and operating cash flow that is widely known by industry analysts, lenders and investors. The Company’s calculation of EBITDAre may not be comparable to EBITDAre reported by other REITs that interpret the Nareit definition differently than the Company.

Recurring EBITDA

The Company defines Recurring EBITDA as EBITDAre with the addback of noncash amortization of above- and below- market lease intangibles, and after adjustments for the run-rate impact of the Company's investment and disposition activity for the period presented, as well as adjustments for non-recurring benefits or expenses. The Company considers the non-GAAP measure of Recurring EBITDA to be a key supplemental measure of the Company's performance and should be considered along with, but not as an alternative to, net income or loss as a measure of the Company's operating performance. The Company considers Recurring EBITDA a key supplemental measure of the Company's operating performance because it represents the Company's earnings run rate for the period presented and because it is widely followed by industry analysts, lenders and investors. Our Recurring EBITDA may not be comparable to Recurring EBITDA reported by other companies that have a different interpretation of the definition of Recurring EBITDA. Our ratio of net debt to Recurring EBITDA is used by management as a measure of leverage and may be useful to investors in understanding the Company’s ability to service its debt, as well as assess the borrowing capacity of the Company. Our ratio of net debt to Recurring EBITDA is calculated by taking annualized Recurring EBITDA and dividing it by our net debt per the consolidated balance sheet.

Annualized Net Income

Represents net income for the three months ended September 30, 2025, on an annualized basis.

Agree Realty Corporation | ||||||||||||

Rental Income | ||||||||||||

($ in thousands, except share and per-share data) | ||||||||||||

(Unaudited) | ||||||||||||

|

|

|

Three months ended |

|

|

Nine months ended |

||||||

|

|

|

September 30, |

|

|

September 30, |

||||||

|

|

|

2025 |

|

|

2024 |

|

|

2025 |

|

|

2024 |

Rental Income Source(1) |

|

|

|

|

|

|

|

|

|

|

|

|

Minimum rents(2) |

|

$ |

167,576 |

|

$ |

143,143 |

|

$ |

481,788 |

|

$ |

421,122 |

Percentage rents(2) |

|

|

142 |

|

|

12 |

|

|

2,254 |

|

|

1,717 |

Operating cost reimbursement(2) |

|

|

19,841 |

|

|

16,099 |

|

|

57,312 |

|

|

48,511 |

Straight-line rental adjustments(3) |

|

|

4,976 |

|

|

3,332 |

|

|

12,774 |

|

|

9,675 |

Amortization of (above) below market lease intangibles(4) |

|

|

(9,344) |

|

|

(8,294) |

|

|

(26,427) |

|

|

(24,886) |

Total Rental Income |

|

$ |

183,191 |

|

$ |

154,292 |

|

$ |

527,701 |

|

$ |

456,139 |

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) The Company adopted Financial Accounting Standards Board Accounting Standards Codification (“FASB ASC”) 842 “Leases” using the modified retrospective approach as of January 1, 2019. The Company adopted the practical expedient in FASB ASC 842 that alleviates the requirement to separately present lease and non-lease components of lease contracts. As a result, all income earned pursuant to tenant leases is reflected as one line, “Rental Income,” in the consolidated statement of operations. The purpose of this table is to provide additional supplementary detail of Rental Income. | ||||||||||||

|

OCTOBER 202 5 |

|

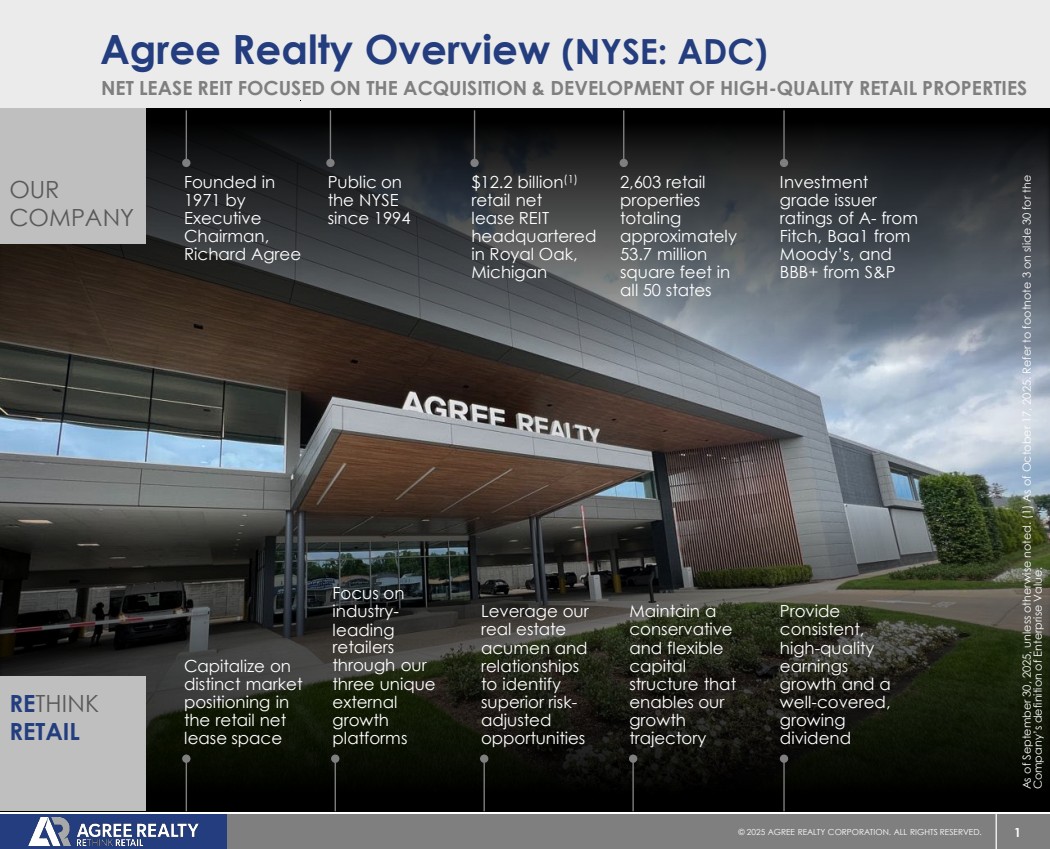

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 1 Agree Realty Overview (NYSE: ADC) OUR COMPANY NET LEASE REIT FOCUSED ON THE ACQUISITION & DEVELOPMENT OF HIGH-QUALITY RETAIL PROPERTIES Founded in 1971 by Executive Chairman, Richard Agree Public on the NYSE since 1994 $12.2 billion(1) retail net lease REIT headquartered in Royal Oak, Michigan 2,603 retail properties totaling approximately 53.7 million square feet in all 50 states Investment grade issuer ratings of A- from Fitch, Baa1 from Moody’s, and BBB+ from S&P RETHINK RETAIL Capitalize on distinct market positioning in the retail net lease space Focus on industry-leading retailers through our three unique external growth platforms Leverage our real estate acumen and relationships to identify superior risk-adjusted opportunities Maintain a conservative and flexible capital structure that enables our growth trajectory Provide consistent, high-quality earnings growth and a well-covered, growing dividend As of September 30, 2025, unless otherwise noted. (1) As of October 17, 2025. Refer to footnote 3 on slide 30 for the Company’s definition of Enterprise Value. |

|

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 2 consistency noun steadfast adherence to the same principles, course, or form [ kuh n-sis-tuh n-see ] |

|

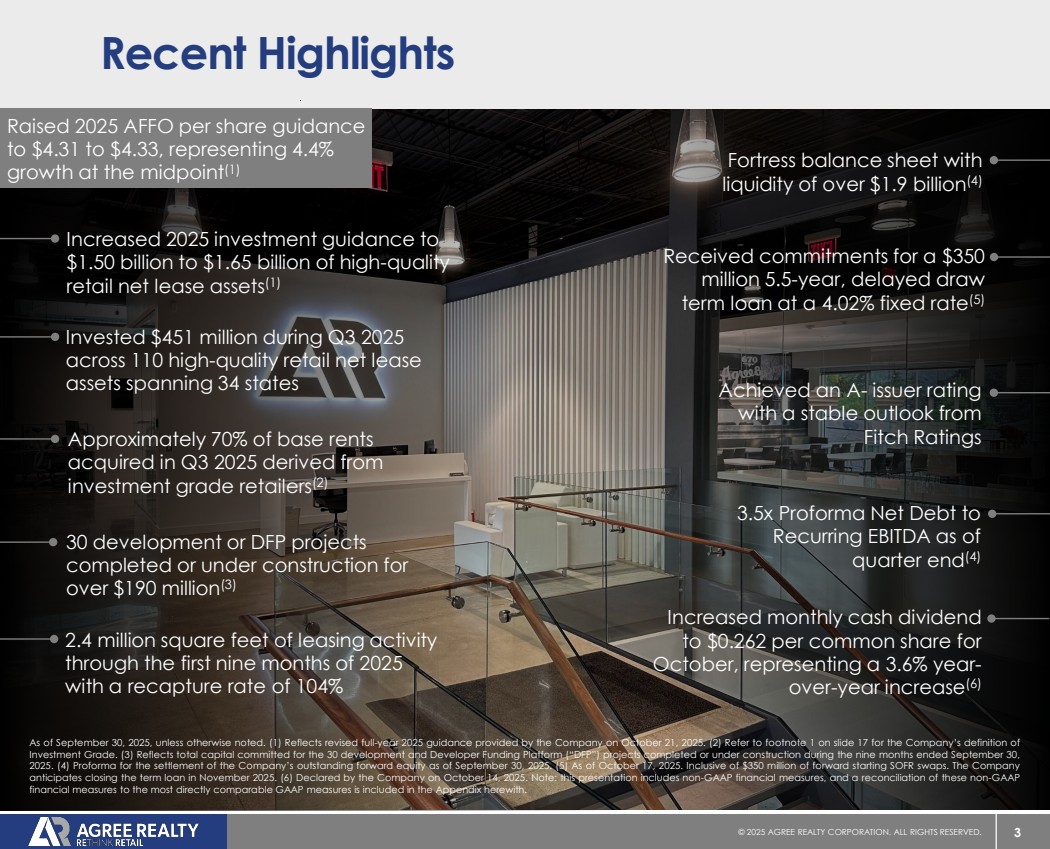

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 3 As of September 30, 2025, unless otherwise noted. (1) Reflects revised full-year 2025 guidance provided by the Company on October 21, 2025. (2) Refer to footnote 1 on slide 17 for the Company’s definition of Investment Grade. (3) Reflects total capital committed for the 30 development and Developer Funding Platform (“DFP”) projects completed or under construction during the nine months ended September 30, 2025. (4) Proforma for the settlement of the Company’s outstanding forward equity as of September 30, 2025. (5) As of October 17, 2025. Inclusive of $350 million of forward starting SOFR swaps. The Company anticipates closing the term loan in November 2025. (6) Declared by the Company on October 14, 2025. Note: this presentation includes non-GAAP financial measures, and a reconciliation of these non-GAAP financial measures to the most directly comparable GAAP measures is included in the Appendix herewith. Recent Highlights Fortress balance sheet with liquidity of over $1.9 billion(4) Raised 2025 AFFO per share guidance to $4.31 to $4.33, representing 4.4% growth at the midpoint(1) Received commitments for a $350 million 5.5-year, delayed draw term loan at a 4.02% fixed rate(5) Invested $451 million during Q3 2025 across 110 high-quality retail net lease assets spanning 34 states 3.5x Proforma Net Debt to Recurring EBITDA as of quarter end(4) Increased monthly cash dividend to $0.262 per common share for October, representing a 3.6% year-over-year increase(6) Achieved an A- issuer rating with a stable outlook from Fitch Ratings 30 development or DFP projects completed or under construction for over $190 million(3) Increased 2025 investment guidance to $1.50 billion to $1.65 billion of high-quality retail net lease assets(1) Approximately 70% of base rents acquired in Q3 2025 derived from investment grade retailers(2) 2.4 million square feet of leasing activity through the first nine months of 2025 with a recapture rate of 104% |

|

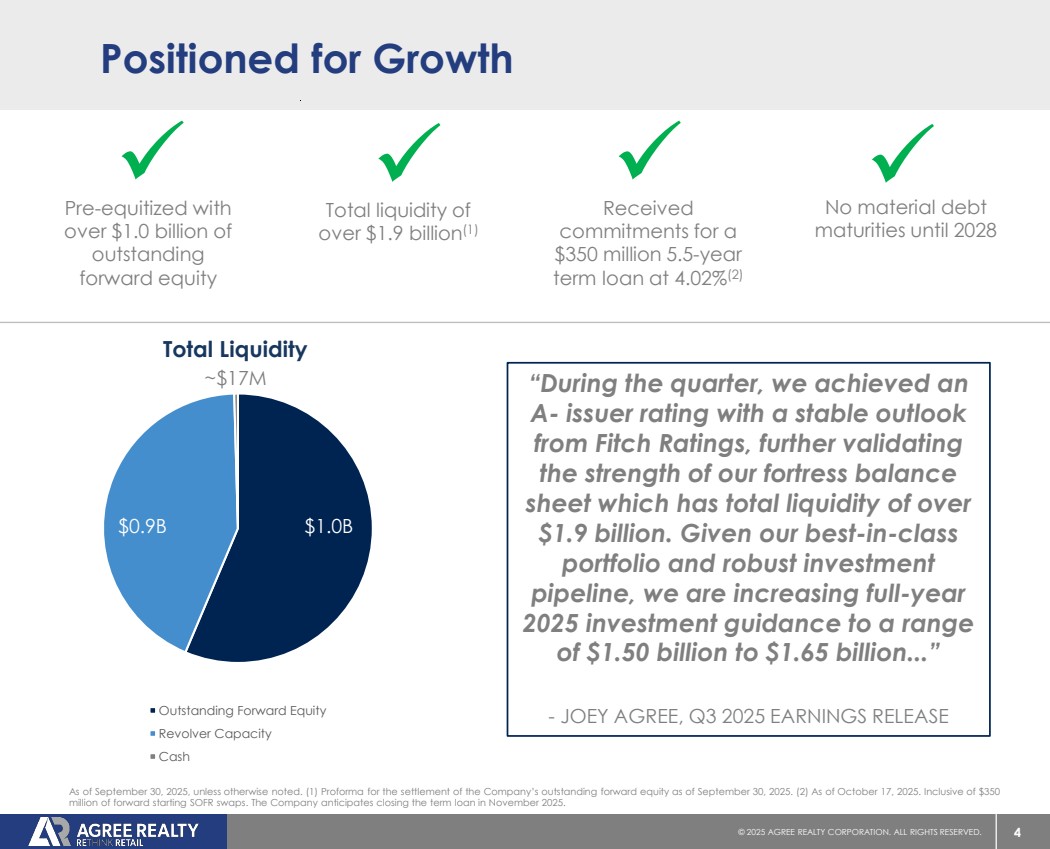

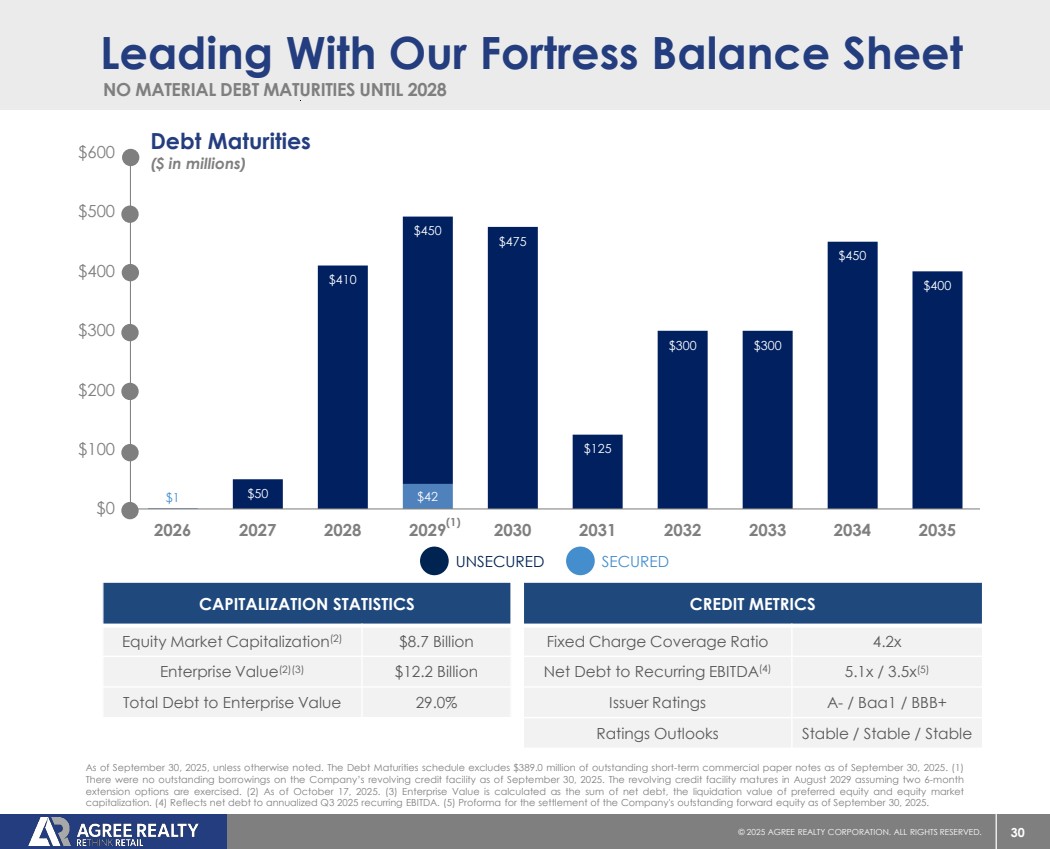

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 4 $0.9B $1.0B ~$17M Total Liquidity Outstanding Forward Equity Revolver Capacity Cash Pre-equitized with A over $1.0 billion of outstanding forward equity Total liquidity of A over $1.9 billion(1) Received A commitments for a $350 million 5.5-year term loan at 4.02%(2) No material debt A maturities until 2028 As of September 30, 2025, unless otherwise noted. (1) Proforma for the settlement of the Company’s outstanding forward equity as of September 30, 2025. (2) As of October 17, 2025. Inclusive of $350 million of forward starting SOFR swaps. The Company anticipates closing the term loan in November 2025. Positioned for Growth “During the quarter, we achieved an A- issuer rating with a stable outlook from Fitch Ratings, further validating the strength of our fortress balance sheet which has total liquidity of over $1.9 billion. Given our best-in-class portfolio and robust investment pipeline, we are increasing full-year 2025 investment guidance to a range of $1.50 billion to $1.65 billion...” - JOEY AGREE, Q3 2025 EARNINGS RELEASE |

|

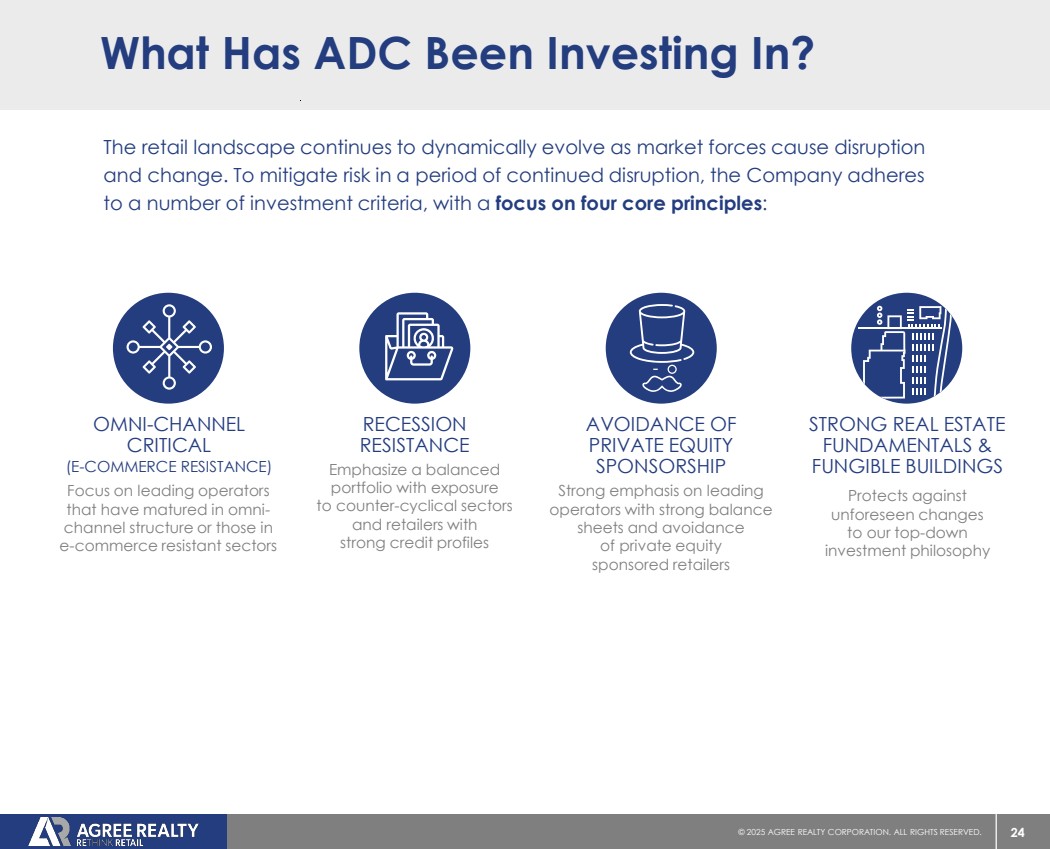

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 5 ADC’s Retail Thought Leadership Launched acquisition platform in 2010 with a focus on e-commerce resistance Launched RETHINK RETAIL campaign to challenge misperceptions about the future of brick & mortar Published proprietary ADC White Papers highlighting omnichannel retail trends Avoided or actively disposed of troubled retail sectors including theaters, pharmacy, car washes, health & fitness and entertainment retail Early identification of promising retailers: |

|

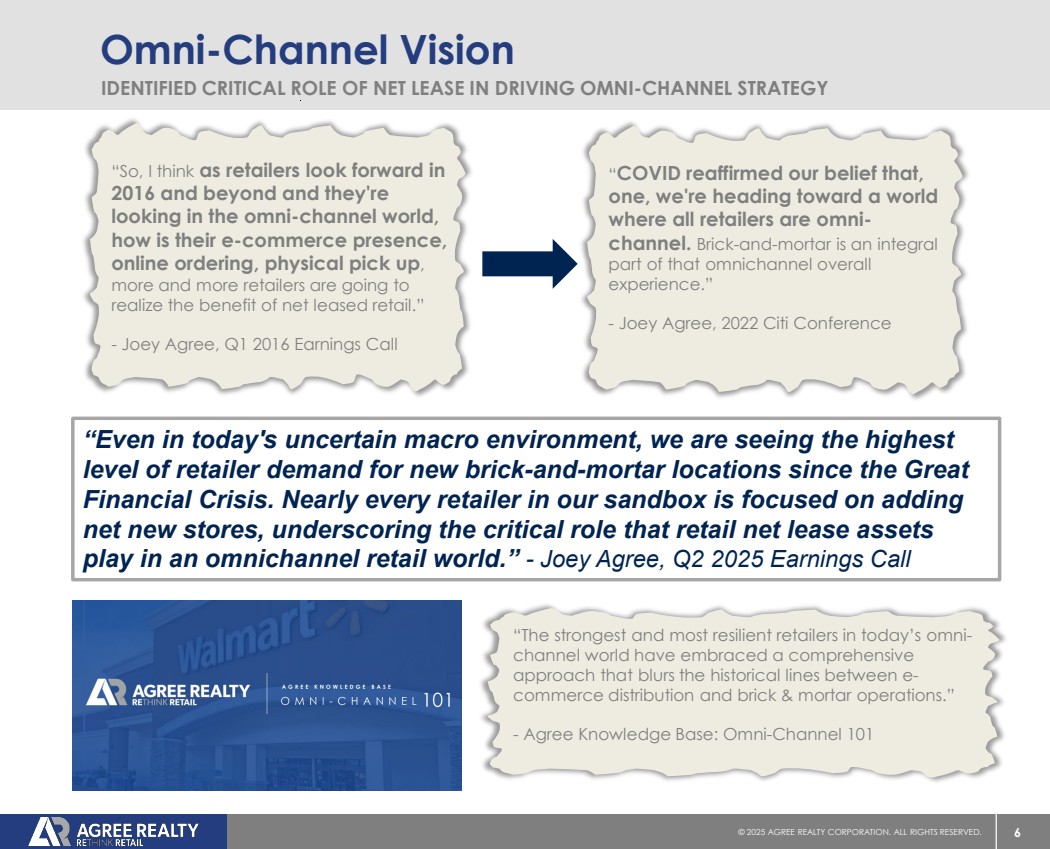

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 6 Omni-Channel Vision IDENTIFIED CRITICAL ROLE OF NET LEASE IN DRIVING OMNI-CHANNEL STRATEGY “The strongest and most resilient retailers in today’s omni-channel world have embraced a comprehensive approach that blurs the historical lines between e-commerce distribution and brick & mortar operations.” - Agree Knowledge Base: Omni-Channel 101 “Even in today's uncertain macro environment, we are seeing the highest level of retailer demand for new brick-and-mortar locations since the Great Financial Crisis. Nearly every retailer in our sandbox is focused on adding net new stores, underscoring the critical role that retail net lease assets play in an omnichannel retail world.” - Joey Agree, Q2 2025 Earnings Call “So, I think as retailers look forward in 2016 and beyond and they're looking in the omni-channel world, how is their e-commerce presence, online ordering, physical pick up, more and more retailers are going to realize the benefit of net leased retail.” - Joey Agree, Q1 2016 Earnings Call “COVID reaffirmed our belief that, one, we're heading toward a world where all retailers are omni-channel. Brick-and-mortar is an integral part of that omnichannel overall experience.” - Joey Agree, 2022 Citi Conference |

|

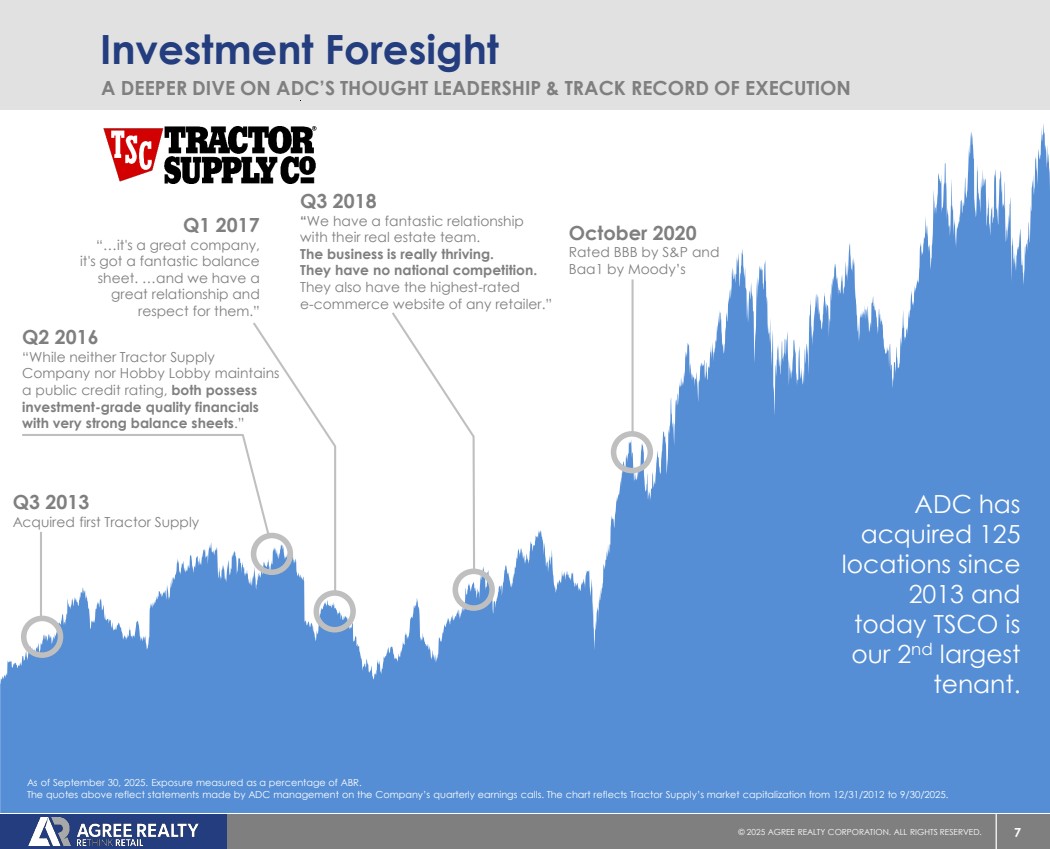

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 7 October 2020 Rated BBB by S&P and Baa1 by Moody’s Q2 2016 “While neither Tractor Supply Company nor Hobby Lobby maintains a public credit rating, both possess investment-grade quality financials with very strong balance sheets.” Q1 2017 “…it's a great company, it's got a fantastic balance sheet. …and we have a great relationship and respect for them.” Q3 2018 “We have a fantastic relationship with their real estate team. The business is really thriving. They have no national competition. They also have the highest-rated e-commerce website of any retailer.” Investment Foresight A DEEPER DIVE ON ADC’S THOUGHT LEADERSHIP & TRACK RECORD OF EXECUTION As of September 30, 2025. Exposure measured as a percentage of ABR. The quotes above reflect statements made by ADC management on the Company’s quarterly earnings calls. The chart reflects Tractor Supply’s market capitalization from 12/31/2012 to 9/30/2025. ADC has acquired 125 locations since 2013 and today TSCO is our 2nd largest tenant. Q3 2013 Acquired first Tractor Supply |

|

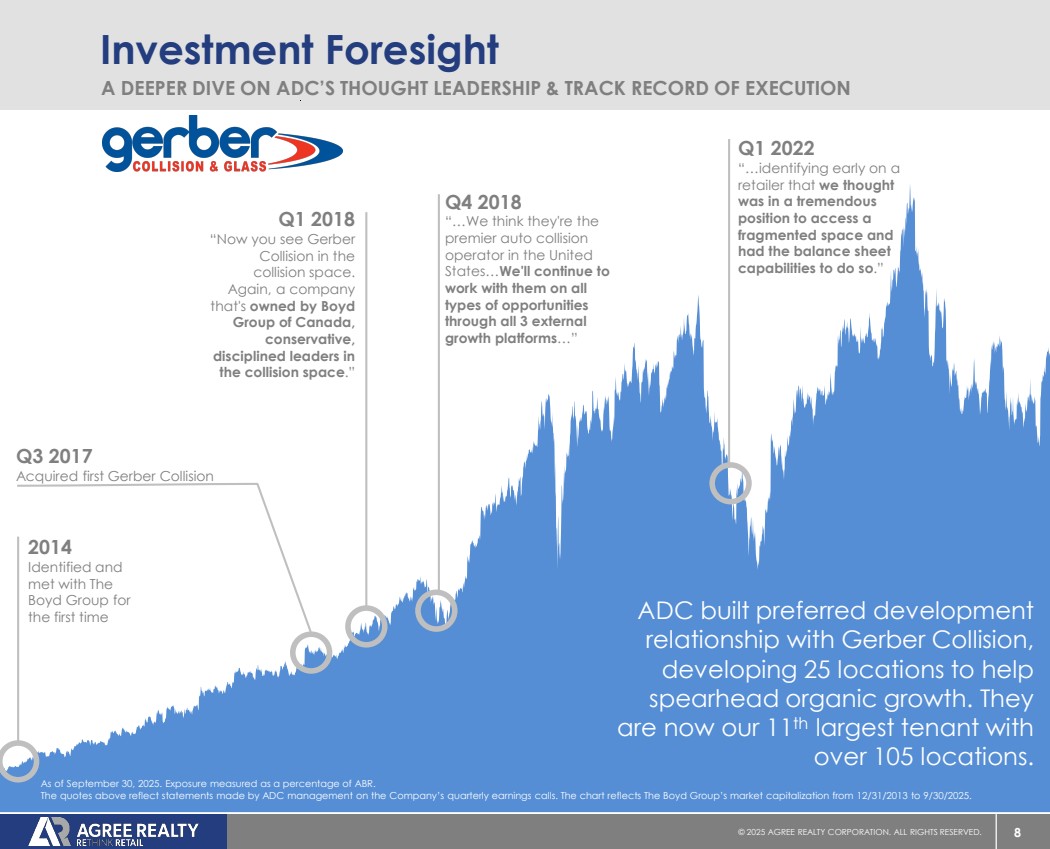

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 8 Investment Foresight A DEEPER DIVE ON ADC’S THOUGHT LEADERSHIP & TRACK RECORD OF EXECUTION Q3 2017 Acquired first Gerber Collision Q4 2018 “…We think they're the premier auto collision operator in the United States…We'll continue to work with them on all types of opportunities through all 3 external growth platforms…” Q1 2022 “…identifying early on a retailer that we thought was in a tremendous position to access a fragmented space and had the balance sheet capabilities to do so.” ADC built preferred development relationship with Gerber Collision, developing 25 locations to help spearhead organic growth. They are now our 11th largest tenant with over 105 locations. As of September 30, 2025. Exposure measured as a percentage of ABR. The quotes above reflect statements made by ADC management on the Company’s quarterly earnings calls. The chart reflects The Boyd Group’s market capitalization from 12/31/2013 to 9/30/2025. Q1 2018 “Now you see Gerber Collision in the collision space. Again, a company that's owned by Boyd Group of Canada, conservative, disciplined leaders in the collision space.” 2014 Identified and met with The Boyd Group for the first time |

|

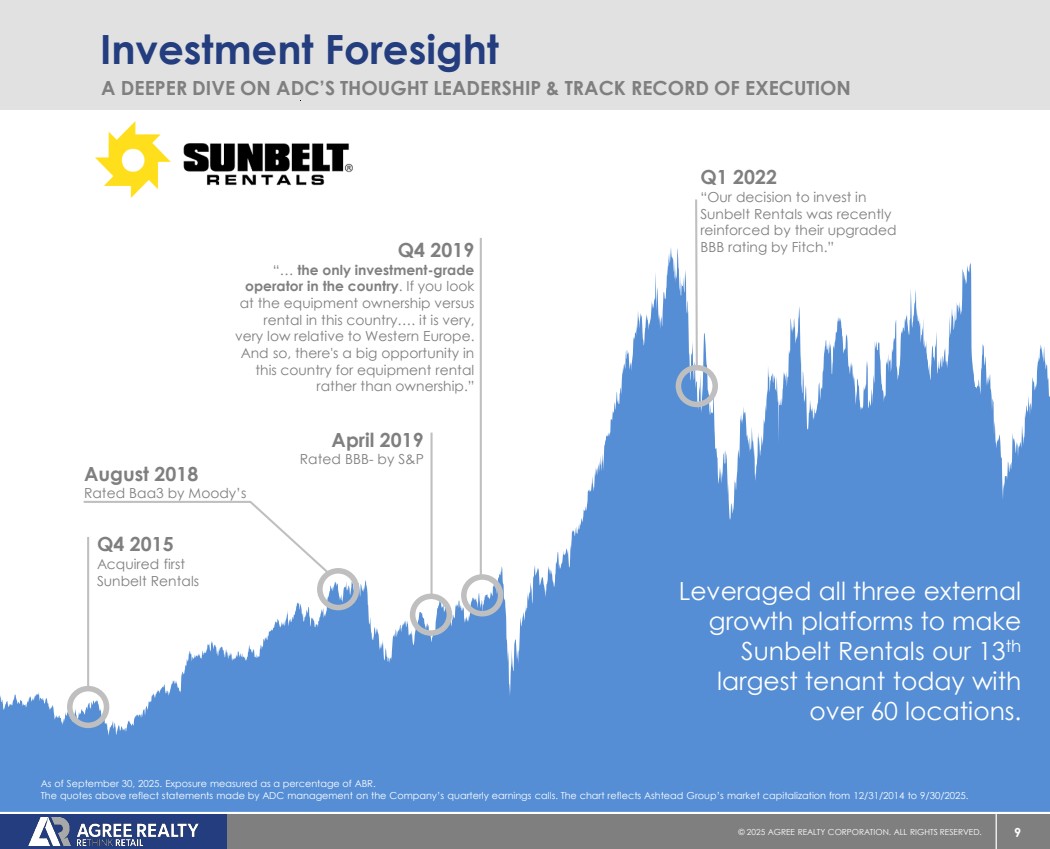

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 9 Investment Foresight A DEEPER DIVE ON ADC’S THOUGHT LEADERSHIP & TRACK RECORD OF EXECUTION Leveraged all three external growth platforms to make Sunbelt Rentals our 13th largest tenant today with over 60 locations. As of September 30, 2025. Exposure measured as a percentage of ABR. The quotes above reflect statements made by ADC management on the Company’s quarterly earnings calls. The chart reflects Ashtead Group’s market capitalization from 12/31/2014 to 9/30/2025. Q4 2015 Acquired first Sunbelt Rentals Q4 2019 “… the only investment-grade operator in the country. If you look at the equipment ownership versus rental in this country…. it is very, very low relative to Western Europe. And so, there's a big opportunity in this country for equipment rental rather than ownership.” April 2019 Rated BBB- by S&P August 2018 Rated Baa3 by Moody’s Q1 2022 “Our decision to invest in Sunbelt Rentals was recently reinforced by their upgraded BBB rating by Fitch.” |

|

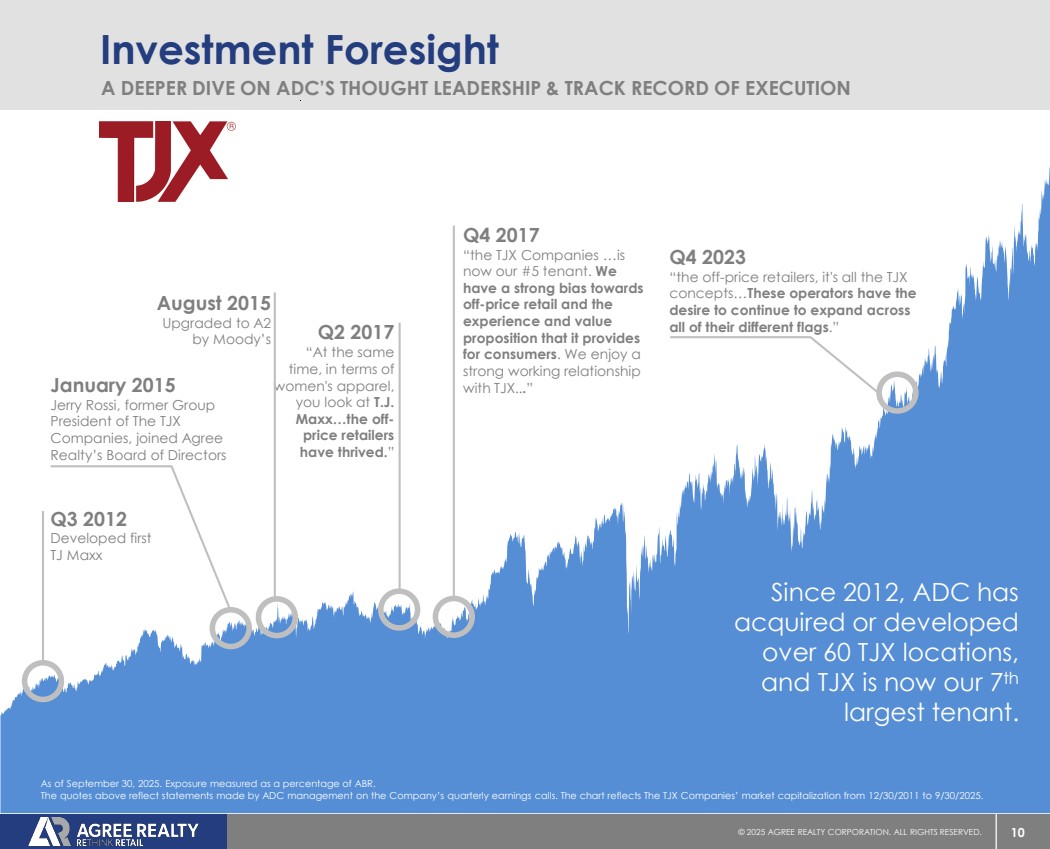

© 2025 AGREE REALTY CORPORATION. ALL RIGHTS RESERVED. 10 Investment Foresight A DEEPER DIVE ON ADC’S THOUGHT LEADERSHIP & TRACK RECORD OF EXECUTION Since 2012, ADC has acquired or developed over 60 TJX locations, and TJX is now our 7th largest tenant. As of September 30, 2025. Exposure measured as a percentage of ABR. The quotes above reflect statements made by ADC management on the Company’s quarterly earnings calls. The chart reflects The TJX Companies’ market capitalization from 12/30/2011 to 9/30/2025. Q3 2012 Developed first TJ Maxx Q4 2023 “the off-price retailers, it's all the TJX concepts…These operators have the desire to continue to expand across all of their different flags.” August 2015 Upgraded to A2 by Moody’s Q2 2017 “At the same time, in terms of women's apparel, you look at T.J. Maxx…the off-price retailers have thrived.” Q4 2017 “the TJX Companies …is now our #5 tenant. We have a strong bias towards off-price retail and the experience and value proposition that it provides for consumers. We enjoy a strong working relationship January 2015 with TJX...” Jerry Rossi, former Group President of The TJX Companies, joined Agree Realty’s Board of Directors |

|