UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of the

Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): August 4, 2025

TMC THE METALS COMPANY INC.

(Exact name of registrant as specified in its charter)

| British Columbia, Canada | 001-39281 | Not Applicable |

| (State or other jurisdiction of

incorporation) |

(Commission File Number) | (IRS Employer Identification No.) |

| 1111 West Hastings Street, 15th Floor Vancouver, British Columbia (Address of principal executive offices) |

V6E 2J3 (Zip Code) |

Registrant’s telephone number, including area code: (888) 458-3420

Not

applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) |

Name of each exchange on |

||

| TMC Common Shares without par value | TMC | The Nasdaq Stock Market LLC | ||

| Redeemable warrants, each whole warrant exercisable for one TMC Common Share, each at an exercise price of $11.50 per share | TMCWW | The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company x

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 1.01. | Entry into Material Definitive Agreement. |

On August 4, 2025, Tonga Offshore Mining Limited (“TOML”), a wholly owned subsidiary of TMC the metals company Inc. (the “Company”), entered into a revised sponsorship agreement (the “Sponsorship Agreement”) with the Kingdom of Tonga, acting through the Tonga Seabed Minerals Authority (“Tonga”), which replaces and supersedes the prior sponsorship agreement dated September 23, 2021. The Sponsorship Agreement formalizes Tonga’s continued support for TOML’s exploration activities under its exploration contract with the International Seabed Authority (“ISA”) within the TOML contract area in the Clarion-Clipperton Zone, and sets forth revised terms governing the relationship between the parties, including certain benefit entitlements to Tonga in connection with potential future commercial production by TOML or other Company subsidiaries.

Pursuant to the Sponsorship Agreement, TOML will continue to be obligated to pay Tonga a seabed mineral recovery payment based on the volume of polymetallic nodules recovered from the ISA contract area, subject to revised commercial criteria, and continuing until termination of the Sponsorship Agreement in accordance with its terms, including upon certain uncured breaches by the other party.

In connection with the Sponsorship Agreement, the Company executed a Deed of Guarantee and Indemnity (the “Deed”) in favor of Tonga, under which the Company guarantees certain financial obligations of TOML under Tongan law and the Sponsorship Agreement, and provides limited indemnification.

As further described in the Sponsorship Agreement and the Deed, on August 4, 2025, the Company issued to Tonga a warrant to purchase 1,000,000 common shares of the Company (the “Warrant”). The Warrant has an initial exercise price of $5.87 per share, becomes exercisable upon the satisfaction of certain conditions related to U.S. regulatory approvals and the Company’s commercial recovery efforts, as set forth in the Warrant, and expires five years from the date of issuance.

The foregoing descriptions of the Sponsorship Agreement, the Deed, and the Warrant do not purport to be complete and are qualified in their entirety by reference to the full text of each, copies of which are filed as Exhibits 10.1, 10.2, and 4.1, respectively, to this Current Report on Form 8-K and incorporated herein by reference.

| Item 2.03. | Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement of a Registrant |

The information set forth in Item 1.01 of this Current Report on Form 8-K is incorporated herein by reference.

| Item 7.01. | Regulation FD Disclosure. |

Strategy Event

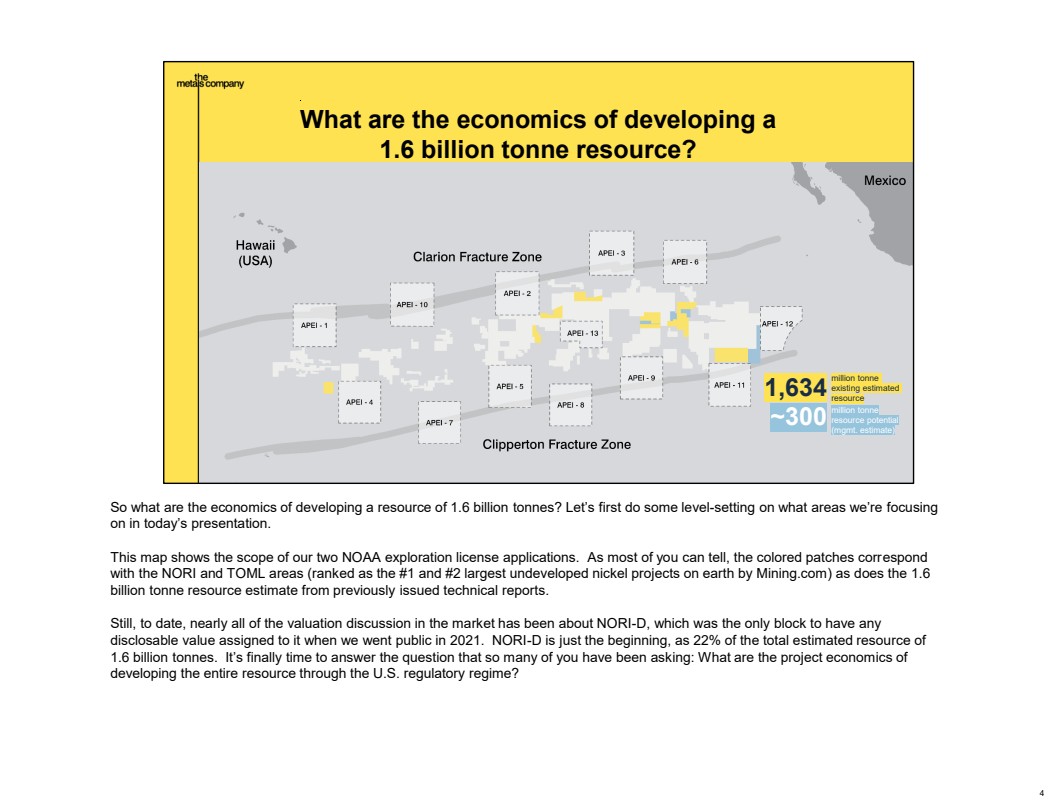

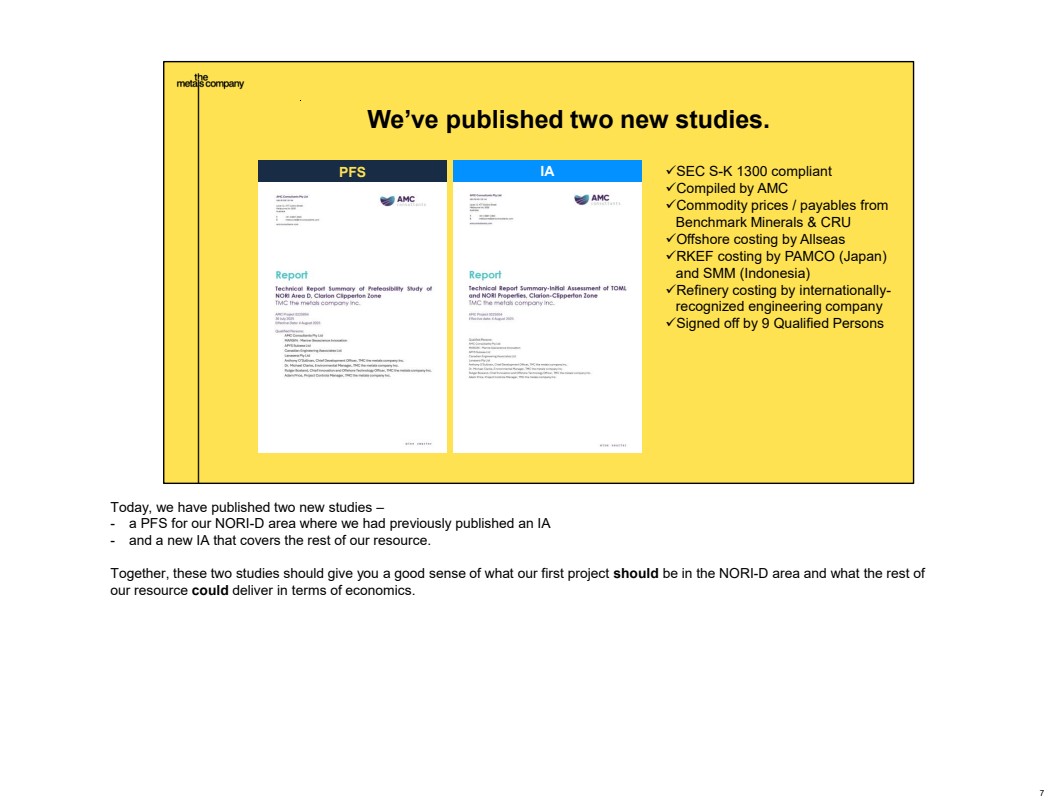

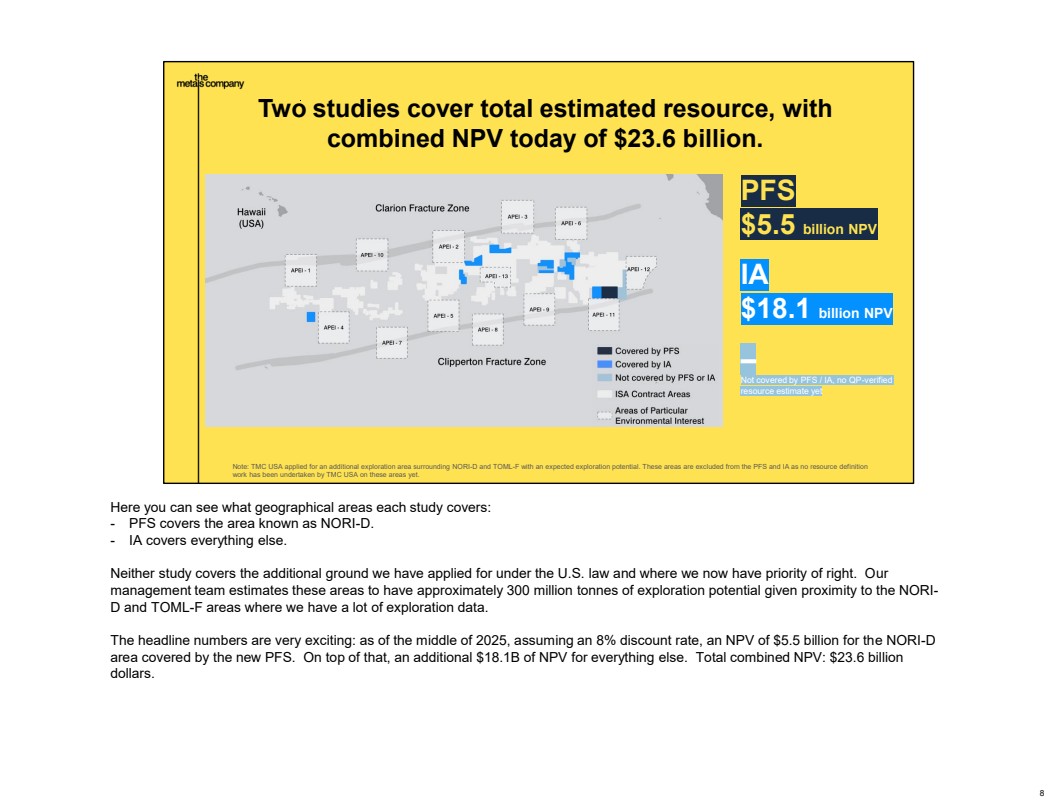

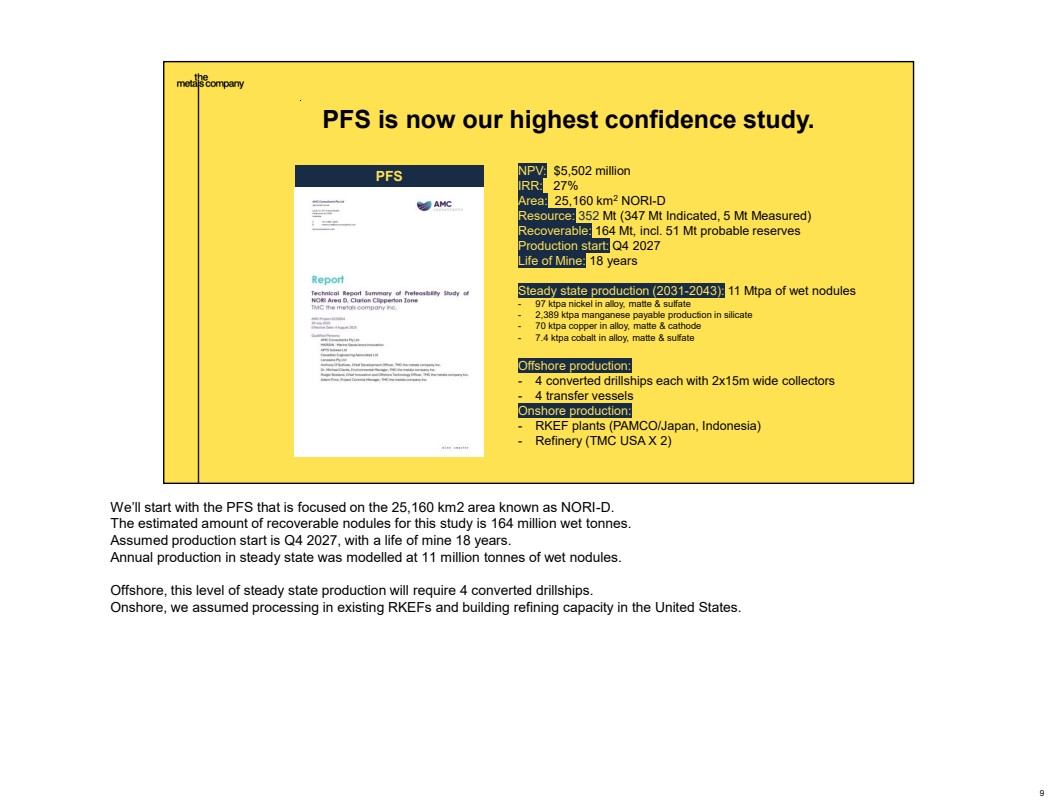

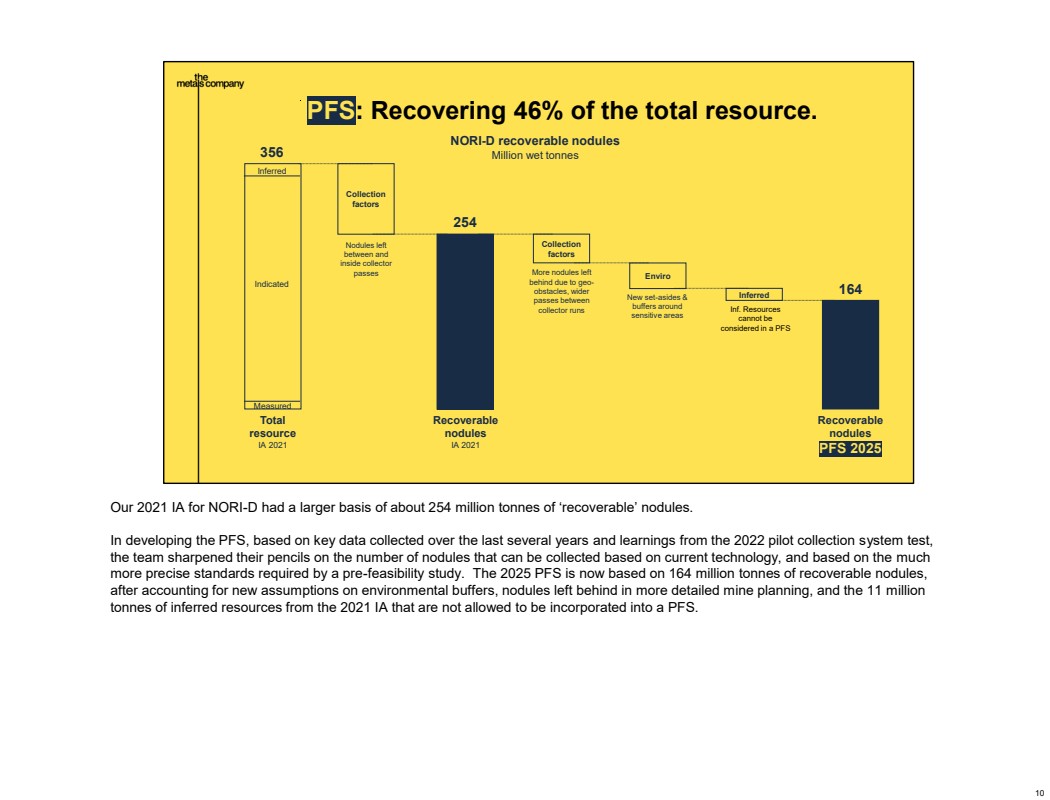

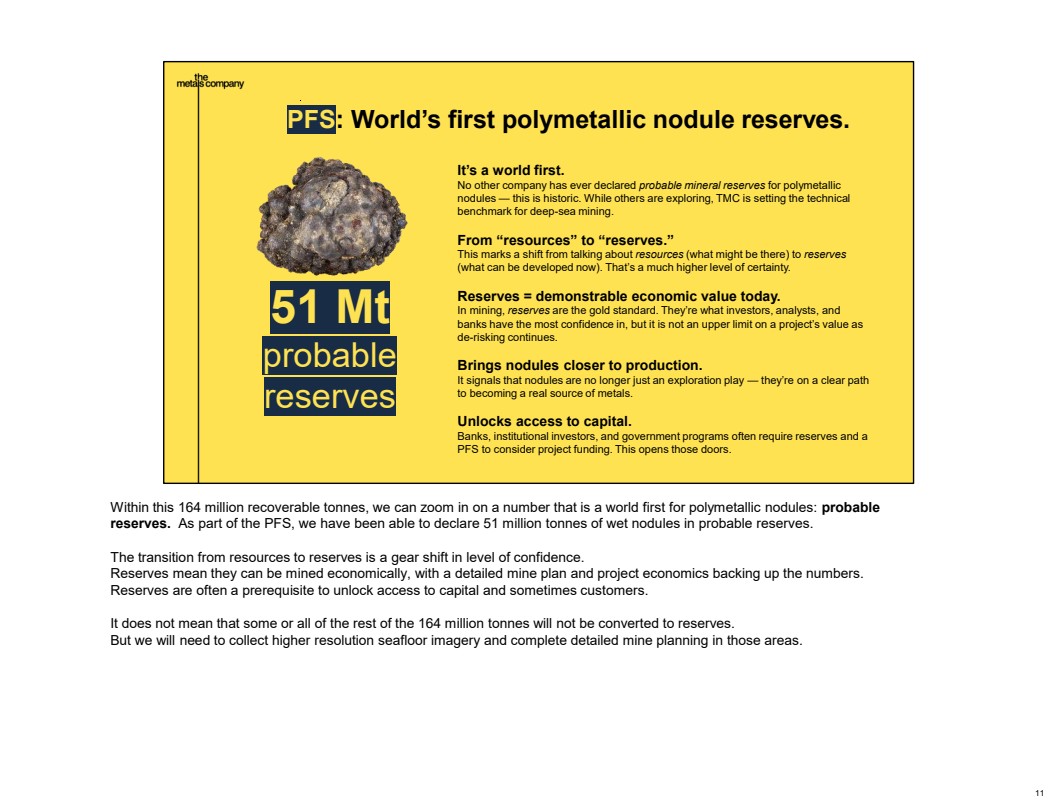

The Company will host a strategy event (the “Strategy Event”) beginning at 9:00 a.m. EDT on August 4, 2025, to discuss the release of a pre-feasibility study in a report titled S-K 1300 NORI Area D Technical Report, dated August 4, 2025, the release of an initial assessment in a report titled Technical Report Summary—Initial Assessment of TOML and NORI Properties, Clarion-Clipperton Zone, dated August 4, 2025, the Sponsorship Agreement, and other Company updates. A slideshow presentation (the “Investor Presentation”) will accompany the Strategy Event. A copy of the Investor Presentation is furnished as Exhibit 99.1 to this Current Report on Form 8-K.

The information contained in this Item 7.01, including and the Investor Presentation, is being furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, nor shall it be deemed incorporated by reference into any filing under the Securities Act of 1933, as amended, except as expressly set forth by specific reference in such a filing.

Cautionary Note Regarding Forward-Looking Statements.

Except for historical information contained in this Current Report on Form 8-K (including Exhibit 99.1), this report contains forward-looking statements which involve certain risks and uncertainties that could cause actual results to differ materially from those expressed or implied. Please refer to the cautionary statements included in the Investor Presentation, furnished as Exhibit 99.1 to this Current Report on Form 8-K.

| Item 9.01. | Financial Statements and Exhibits. |

(d) Exhibits.

| Exhibit No. | Description |

| 4.1 | Common Share Purchase Warrant, dated August 4, 2025, issued to The Kingdom of Tonga |

| 10.1† | Sponsorship Agreement, dated August 4, 2025, among The Government of The Kingdom of Tonga and Tonga Offshore Mining Limited |

| 10.2† | Deed of Guarantee and Indemnity, dated August 4, 2025, by TMC the metals company Inc. in favor of The Kingdom of Tonga |

| 99.1* | Investor Presentation |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) |

† Certain confidential portions of this Exhibit were omitted by means of marking such portions with brackets (“[***]”) because the identified confidential portions (i) are not material and (ii) is the type of information that the Company treats as private or confidential.

* The foregoing exhibit relating to Item 7.01 is intended to be furnished to, not filed with, the Securities and Exchange Commission pursuant to Regulation FD.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| TMC THE METALS COMPANY INC. | ||

| Date: August 4, 2025 | By: | /s/ Craig Shesky |

| Name: | Craig Shesky | |

| Title: | Chief Financial Officer | |

Exhibit 4.1

NEITHER THE ISSUANCE AND SALE OF THE SECURITIES REPRESENTED BY THIS WARRANT NOR THE SECURITIES INTO WHICH THESE SECURITIES ARE EXERCISABLE HAVE BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, OR APPLICABLE STATE SECURITIES LAWS. THESE SECURITIES MAY NOT BE OFFERED FOR SALE, SOLD, TRANSFERRED OR ASSIGNED (I) IN THE ABSENCE OF (A) AN EFFECTIVE REGISTRATION STATEMENT FOR THE SECURITIES UNDER THE SECURITIES ACT OF 1933, AS AMENDED, OR (B) AN OPINION OF COUNSEL TO THE HOLDER (IF REQUESTED BY THE COMPANY (AS DEFINED BELOW)), IN A FORM REASONABLY ACCEPTABLE TO THE COMPANY, THAT REGISTRATION IS NOT REQUIRED UNDER SAID ACT OR (II) UNLESS SOLD OR ELIGIBLE TO BE SOLD PURSUANT TO RULE 144 OR RULE 144A UNDER SAID ACT. THE NUMBER OF COMMON SHARES ISSUABLE UPON EXERCISE OF THIS WARRANT MAY BE LESS THAN THE AMOUNTS SET FORTH ON THE FACE HEREOF PURSUANT TO SECTION 2(a) OF THIS WARRANT.

COMMON SHARE PURCHASE WARRANT

TMC THE METALS COMPANY INC.

| Warrant Shares: 1,000,000 | Issue Date: August 4, 2025 |

THIS COMMON SHARE PURCHASE WARRANT (the “Warrant”) certifies that, for value received, The Kingdom of Tonga or its assigns (the “Holder”) is entitled, upon the terms and subject to the limitations on exercise and the conditions hereinafter set forth, at any time on or after the issue date set forth above (the “Issue Date”) and on or prior to 5:00 p.m. (New York City time) on August 4, 2033 (the “Termination Date”) but not thereafter, to subscribe for and purchase from TMC the metals company Inc., a corporation incorporated under the laws of the Province of British Columbia (the “Company”), up to one million common shares (as subject to adjustment hereunder, the “Warrant Shares”) of the Company, no par value per share (the “Common Shares”). The purchase price of one Common Share under this Warrant shall be equal to the Exercise Price (as defined below).

Section 1. Definitions. All capitalized terms used herein shall have the meaning ascribed thereto as set forth herein. As used herein:

“Continuity Conditions” shall have the meaning ascribed thereto in the Sponsorship Agreement.

“Exercise Price” means US$5.87 per Common Share, subject to adjustment as set forth in this Warrant.

“Securities Act” means the Securities Act of 1933, as amended.

“Sponsorship Agreement” means that certain Sponsorship Agreement by and among the Holder, the Tonga Seabed Minerals Authority and Tonga Offshore Mining Ltd., dated on or about the Issue Date, as the same may be amended and/or restated from time to time.

“Trading Day” means a day on which the Common Shares is traded on a Trading Market.

“Trading Market” means any of the following markets or exchanges on which the Common Shares are listed or quoted for trading on the date in question: the NYSE American, the Nasdaq Capital Market, the Nasdaq Global Market, the Nasdaq Global Select Market, the New York Stock Exchange, the OTCQB or the OTCQX (or any successors to any of the foregoing).

“Transfer Agent” means Continental Stock Transfer & Trust Company, and any successor transfer agent of the Company.

Section 2. Exercise.

a) Exercise of Warrant. Exercise of the purchase rights represented by this Warrant may be made, in whole or in part, at any time or times on or after the Issue Date, provided that the Continuity Conditions have occurred, and on or before the Termination Date by delivery to the Company of a duly executed PDF copy submitted by e-mail (or e-mail attachment) of the Notice of Exercise in the form annexed hereto (the “Notice of Exercise”). Within one (1) Trading Day following the date of exercise as aforesaid, the Holder shall deliver the aggregate Exercise Price for the Warrant Shares specified in the applicable Notice of Exercise by wire transfer to the Company. No ink-original Notice of Exercise shall be required. Notwithstanding anything herein to the contrary, the Holder shall not be required to physically surrender this Warrant to the Company until the Holder has purchased all of the Warrant Shares available hereunder and the Warrant has been exercised in full, in which case, the Holder shall surrender this Warrant to the Company for cancellation within three (3) Trading Days of the date on which the final Notice of Exercise is delivered to the Company. Partial exercises of this Warrant resulting in purchases of a portion of the total number of Warrant Shares available hereunder shall have the effect of lowering the outstanding number of Warrant Shares purchasable hereunder in an amount equal to the applicable number of Warrant Shares purchased. The Holder and the Company shall maintain records showing the number of Warrant Shares purchased and the date of such purchases. The Company shall deliver any objection to any Notice of Exercise within one (1) Trading Day of receipt of such notice. The Holder and any assignee, by acceptance of this Warrant, acknowledges and agrees that (i) by reason of the provisions of this paragraph, following the purchase of a portion of the Warrant Shares hereunder, the number of Warrant Shares available for purchase hereunder at any given time may be less than the amount stated on the face hereof, (ii) this Warrant may not be exercised in whole or in part unless and until the Continuity Conditions have occurred and (iii) this Warrant may not be “cashless” or “net” exercised.

b) Mechanics of Exercise.

i. Delivery of Warrant Shares Upon Exercise. The Company shall cause the Warrant Shares purchased hereunder to be issued by the Transfer Agent to the Holder in global form through a book-entry account maintained by the Transfer Agent (including by providing the Holder a copy of the irrevocable instructions delivered by the Company to the Transfer Agent instructing the Transfer Agent to issue the Warrant Shares to the Holder by crediting the Warrant Shares to the respective account of the Holder on the Transfer Agent’s book-entry system and confirmation from the Transfer Agent that such Warrant Shares were so issued), which Warrant Shares shall be appropriately legended in accordance with Section 4(e), in each case for the number of Warrant Shares to which the Holder is entitled pursuant to such exercise to the address specified by the Holder in the Notice of Exercise by the date that is two (2) Trading Days after receipt of the aggregate Exercise Price by the Company (such date, the “Warrant Share Delivery Date”).

ii. Delivery of New Warrants Upon Exercise. If this Warrant shall have been exercised in part, the Company shall, at the request of a Holder and upon surrender of this Warrant certificate, at the time of delivery of the Warrant Shares, deliver to the Holder a new Warrant evidencing the rights of the Holder to purchase the unpurchased Warrant Shares called for by this Warrant, which new Warrant shall in all other respects be identical with this Warrant.

iii. Rescission Rights. If the Company fails to cause the Transfer Agent to transmit to the Holder the Warrant Shares pursuant to Section 2(b)(i) by the Warrant Share Delivery Date, then the Holder will have the right to rescind such exercise.

|

|

iv. Compensation for Buy-In on Failure to Timely Deliver Warrant Shares Upon Exercise. In addition to any other rights available to the Holder, if the Company fails to cause the Transfer Agent to transmit to the Holder the Warrant Shares in accordance with the provisions of Section 2(b)(i) above pursuant to an exercise on or before the Warrant Share Delivery Date (other than a failure caused by incorrect or incomplete information provided by the Holder to the Company or the Holder’s failure to establish and maintain an account at the Transfer Agent to which the Warrant Shares may be delivered in accordance with Section 2(b)(i)), and if after such date the Holder is required by its broker to purchase (in an open market transaction or otherwise) or the Holder’s brokerage firm otherwise purchases, Common Shares to deliver in satisfaction of a sale by the Holder of the Warrant Shares which the Holder anticipated receiving upon such exercise (a “Buy-In”), then the Company shall (A) pay in cash to the Holder the amount, if any, by which (x) the Holder’s total purchase price (including brokerage commissions, if any) for the Common Shares so purchased exceeds (y) the amount obtained by multiplying (1) the number of Warrant Shares that the Company was required to deliver to the Holder in connection with the exercise at issue times (2) the price at which the sell order giving rise to such purchase obligation was executed, and (B) at the option of the Holder, either reinstate the portion of the Warrant and equivalent number of Warrant Shares for which such exercise was not honored (in which case such exercise shall be deemed rescinded) or deliver to the Holder the number of Common Shares that would have been issued had the Company timely complied with its exercise and delivery obligations hereunder. For example, if the Holder purchases Common Shares having a total purchase price of US$11,000 to cover a Buy-In with respect to an attempted exercise of Common Shares with an aggregate sale price giving rise to such purchase obligation of US$10,000, under clause (A) of the immediately preceding sentence the Company shall be required to pay the Holder US$1,000. The Holder shall provide the Company written notice indicating the amounts payable to the Holder in respect of the Buy-In and, upon request of the Company, evidence of the amount of such loss. Nothing herein shall limit a Holder’s right to pursue any other remedies available to it hereunder, at law or in equity including, without limitation, a decree of specific performance and/or injunctive relief with respect to the Company’s failure to timely deliver Common Shares upon exercise of the Warrant as required pursuant to the terms hereof.

v. No Fractional Shares or Scrip. No fractional shares or scrip representing fractional shares shall be issued upon the exercise of this Warrant. As to any fraction of a share which the Holder would otherwise be entitled to purchase upon such exercise, the Company shall round down the number of Warrant Shares issuable under this Warrant to the next whole share.

vi. Charges, Taxes and Expenses. Issuance of Warrant Shares shall be made without charge to the Holder for any issue or transfer tax or other incidental expense in respect of the issuance of such Warrant Shares, all of which taxes and expenses shall be paid by the Company, and such Warrant Shares shall be issued in the name of the Holder or in such name or names as may be directed by the Holder; provided, however, that, in the event that Warrant Shares are to be issued in a name other than the name of the Holder, this Warrant when surrendered for exercise shall be accompanied by the Assignment Form attached hereto duly executed by the Holder and the Company may require, as a condition thereto, the payment of a sum sufficient to reimburse it for any transfer tax incidental thereto. The Company shall pay all Transfer Agent fees required for same-day processing of any Notice of Exercise.

vii. Closing of Books. The Company will not close its shareholder books or records in any manner which prevents the timely exercise of this Warrant, pursuant to the terms hereof.

|

|

c) Holder’s Exercise Limitations. The Company shall not effect any exercise of this Warrant, and a Holder shall not have the right to exercise any portion of this Warrant, pursuant to Section 2 or otherwise, to the extent that after giving effect to such issuance after exercise as set forth on the applicable Notice of Exercise, the Holder (together with the Holder’s Affiliates (as defined below), and any other Persons acting as a group together with the Holder or any of the Holder’s Affiliates (such Persons, “Attribution Parties”)), would beneficially own in excess of the Beneficial Ownership Limitation (as defined below). For purposes of the foregoing sentence, the number of Common Shares beneficially owned by the Holder and its Affiliates and Attribution Parties shall include the number of Common Shares issuable upon exercise of this Warrant with respect to which such determination is being made, but shall exclude the number of Common Shares which would be issuable upon (i) exercise of the remaining, nonexercised portion of this Warrant beneficially owned by the Holder or any of its Affiliates or Attribution Parties and (ii) exercise or conversion of the unexercised or nonconverted portion of any other securities of the Company (including, without limitation, any other securities of the Company or the Subsidiaries which would entitle the holder thereof to acquire at any time Common Shares, including, without limitation, any debt, preferred share, right, option, warrant or other instrument that is at any time convertible into or exercisable or exchangeable for, or otherwise entitles the holder thereof to receive, Common Shares (“Common Share Equivalents”)) subject to a limitation on conversion or exercise analogous to the limitation contained herein beneficially owned by the Holder or any of its Affiliates or Attribution Parties. Except as set forth in the preceding sentence, for purposes of this Section 2(c), beneficial ownership shall be calculated in accordance with Section 13(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the rules and regulations promulgated thereunder, it being acknowledged by the Holder that the Company is not representing to the Holder that such calculation is in compliance with Section 13(d) of the Exchange Act and the Holder is solely responsible for any schedules required to be filed in accordance therewith. To the extent that the limitation contained in this Section 2(c) applies, the determination of whether this Warrant is exercisable (in relation to other securities owned by the Holder together with any Affiliates and Attribution Parties) and of which portion of this Warrant is exercisable shall be in the sole discretion of the Holder, and the submission of a Notice of Exercise shall be deemed to be the Holder’s determination of whether this Warrant is exercisable (in relation to other securities owned by the Holder together with any Affiliates and Attribution Parties) and of which portion of this Warrant is exercisable, in each case subject to the Beneficial Ownership Limitation, and the Company shall have no obligation to verify or confirm the accuracy of such determination and shall have no liability for exercises of the Warrant that are not in compliance with the Beneficial Ownership Limitation, except to the extent the Holder relies on the number of outstanding Common Shares that was provided by the Company. In addition, a determination as to any group status as contemplated above shall be determined in accordance with Section 13(d) of the Exchange Act and the rules and regulations promulgated thereunder, and the Company shall have no obligation to verify or confirm the accuracy of such determination and shall have no liability for exercises of the Warrant that are not in compliance with the Beneficial Ownership Limitation, except to the extent the Holder relies on the number of outstanding Common Shares that was provided by the Company. For purposes of this Section 2(c), in determining the number of outstanding Common Shares, a Holder may rely on the number of outstanding Common Shares as reflected in (A) the Company’s most recent periodic or annual report filed with the Commission, as the case may be, (B) a more recent public announcement by the Company or (C) a more recent written notice by the Company or the Transfer Agent setting forth the number of Common Shares outstanding. Upon the written or oral request of a Holder, the Company shall within one Trading Day confirm orally and in writing to the Holder the number of Common Shares then outstanding. In any case, the number of outstanding Common Shares shall be determined after giving effect to the conversion or exercise of securities of the Company, including this Warrant, by the Holder or its Affiliates or Attribution Parties since the date as of which such number of outstanding Common Shares was reported. The “Beneficial Ownership Limitation” shall be 4.99% of the number of Common Shares outstanding immediately after giving effect to the issuance of Common Shares issuable upon exercise of this Warrant. The Holder, upon notice to the Company, may increase or decrease the Beneficial Ownership Limitation provisions of this Section 2(c), provided that the Beneficial Ownership Limitation in no event exceeds 9.99% of the number of Common Shares outstanding immediately after giving effect to the issuance of Common Shares upon exercise of this Warrant held by the Holder and the provisions of this Section 2(c) shall continue to apply. Any increase in the Beneficial Ownership Limitation will not be effective until the 61st day after such notice is delivered to the Company. The provisions of this paragraph shall be construed and implemented in a manner otherwise than in strict conformity with the terms of this Section 2(c) to correct this paragraph (or any portion hereof) which may be defective or inconsistent with the intended Beneficial Ownership Limitation herein contained or to make changes or supplements necessary or desirable to properly give effect to such limitation. The limitations contained in this paragraph shall apply to a successor holder of this Warrant. If the Warrant is unexercisable as a result of the Holder’s Beneficial Ownership Limitation, no alternate consideration is owing to the Holder. As used herein, “Affiliate” means any Person (as defined below) that, directly or indirectly through one or more intermediaries, controls or is controlled by or is under common control with a Person, as such terms are used in and construed under Rule 405 under the Securities Act. As used herein, “Person” means an individual or corporation, partnership, trust, incorporated or unincorporated association, joint venture, limited liability company, joint stock company, government (or an agency or subdivision thereof) or other entity of any kind.

|

|

Section 3. Certain Adjustments.

a) Share Dividends and Splits. If the Company, at any time while this Warrant is outstanding: (i) pays a share dividend or otherwise makes a distribution or distributions on Common Shares or any other equity or equity equivalent securities payable in Common Shares (which, for avoidance of doubt, shall not include any Common Shares issued by the Company upon exercise of this Warrant), (ii) subdivides outstanding Common Shares into a larger number of shares, (iii) combines (including by way of reverse share split) outstanding Common Shares into a smaller number of shares, or (iv) issues by reclassification of the Common Shares of the Company, then in each case the Exercise Price shall be multiplied by a fraction of which the numerator shall be the number of Common Shares (excluding treasury shares, if any) outstanding immediately before such event and of which the denominator shall be the number of Common Shares outstanding immediately after such event, and the number of shares issuable upon exercise of this Warrant shall be proportionately adjusted such that the aggregate Exercise Price of this Warrant shall remain unchanged. Any adjustment made pursuant to this Section 3(a) shall become effective immediately after the record date for the determination of shareholders entitled to receive such dividend or distribution and shall become effective immediately after the effective date in the case of a subdivision, combination or re-classification.

b) Subsequent Rights Offerings. In addition to any adjustments pursuant to Section 3(a) above, if at any time the Company grants, issues or sells any Common Share Equivalents or rights to purchase shares, warrants, securities or other property pro rata to the record holders of any class of Common Shares (the “Purchase Rights”), then the Holder will be entitled to acquire, upon the terms applicable to such Purchase Rights, the aggregate Purchase Rights which the Holder could have acquired if the Holder had held the number of Common Shares acquirable upon complete exercise of this Warrant (without regard to any limitations on exercise hereof, including without limitation, the Beneficial Ownership Limitation) immediately before the date on which a record is taken for the grant, issuance or sale of such Purchase Rights, or, if no such record is taken, the date as of which the record holders of Common Shares are to be determined for the grant, issue or sale of such Purchase Rights (provided, however, that, to the extent that the Holder’s right to participate in any such Purchase Right would result in the Holder exceeding the Beneficial Ownership Limitation, then the Holder shall not be entitled to participate in such Purchase Right to such extent (or beneficial ownership of such Common Shares as a result of such Purchase Right to such extent) and such Purchase Right to such extent shall be held in abeyance for the Holder until such time, if ever, as its right thereto would not result in the Holder exceeding the Beneficial Ownership Limitation).

c) Pro Rata Distributions. Subject to compliance with applicable securities and corporate law, including the constituting documents of the Company, during such time as this Warrant is outstanding, if the Company shall declare or make any dividend or other distribution of its assets (or rights to acquire its assets) to holders of Common Shares, by way of return of capital or otherwise (including, without limitation, any distribution of cash, shares or other securities, property or options by way of a dividend, spin off, reclassification, corporate rearrangement, scheme of arrangement or other similar transaction, other than such dividends or distributions that result in an adjustment under Section 3(a) or (b)) (a “Distribution”), at any time after the issuance of this Warrant, then, in each such case, the Holder shall be entitled to receive an equivalent distribution to such Distribution, in the same form and to the equivalent extent that the Holder would have participated therein if the Holder had held the number of Common Shares acquirable upon complete exercise of this Warrant (without regard to any limitations on exercise hereof, including without limitation, the Beneficial Ownership Limitation) immediately before the date of which a record is taken for such Distribution, or, if no such record is taken, the date as of which the record holders of Common Shares are to be determined for the participation in such Distribution (provided, however, that, to the extent that the Holder's right to receive such equivalent distribution to such Distribution would result in the Holder exceeding the Beneficial Ownership Limitation, then the Holder shall not be entitled to such equivalent distribution to such Distribution to such extent (or in the beneficial ownership of any Common Shares as a result of such Distribution to such extent) and the portion of such equivalent distribution shall be held in abeyance for the benefit of the Holder until such time, if ever, as its right thereto would not result in the Holder exceeding the Beneficial Ownership Limitation).

|

|

d) Calculations. All calculations under this Section 3 shall be made to the nearest cent or the nearest 1/100th of a share, as the case may be. For purposes of this Section 3, the number of Common Shares deemed to be issued and outstanding as of a given date shall be the sum of the number of Common Shares (excluding treasury shares, if any) issued and outstanding.

e) Notice to Holder.

i. Adjustment to Exercise Price. Whenever the Exercise Price is adjusted pursuant to any provision of this Section 3, the Company shall promptly deliver to the Holder by email a notice setting forth the Exercise Price after such adjustment and any resulting adjustment to the number of Warrant Shares and setting forth a brief statement of the facts requiring such adjustment.

ii. Notice to Allow Exercise by Holder. If, while this Warrant is exercisable following the occurrence of the Continuity Conditions (A) the Company shall declare a dividend (or any other distribution on Common Shares in whatever form) on the Common Shares, (B) the Company shall declare a special nonrecurring cash dividend on or a redemption of the Common Shares, (C) the Company shall authorize the granting to all holders of the Common Shares rights or warrants to subscribe for or purchase any shares of any class or of any rights, (D) the approval of any shareholders of the Company shall be required in connection with any reclassification of the Common Shares, any consolidation or merger to which the Company (and all of its Subsidiaries, taken as a whole) is a party, any sale or transfer of all or substantially all of the assets of the Company, or any compulsory share exchange whereby the Common Shares are converted into other securities, cash or property, or (E) the Company shall authorize the voluntary or involuntary dissolution, liquidation or winding up of the affairs of the Company, then, in each case, the Company shall cause to be delivered by email to the Holder at its last email address as it shall appear upon the Warrant Register (as defined below) of the Company, at least 5 calendar days prior to the applicable record or effective date hereinafter specified, a notice stating (x) the date on which a record is to be taken for the purpose of such dividend, distribution, redemption, rights or warrants, or if a record is not to be taken, the date as of which the holders of the Common Shares of record to be entitled to such dividend, distributions, redemption, rights or warrants are to be determined or (y) the date on which such reclassification, consolidation, merger, sale, transfer or share exchange is expected to become effective or close, and the date as of which it is expected that holders of the Common Shares of record shall be entitled to exchange their Common Shares for securities, cash or other property deliverable upon such reclassification, consolidation, merger, sale, transfer or share exchange; provided that the failure to deliver such notice or any defect therein or in the delivery thereof shall not affect the validity of the corporate action required to be specified in such notice. Notwithstanding the foregoing, to the extent that any notice to be provided in this Warrant constitutes, or contains, material, non-public information regarding the Company or any of the Subsidiaries, the Company may delay such notice until such time as the Company would otherwise make a public announcement of such notice or information, whether by a Current Report on Form 8-K or otherwise. The Holder shall remain entitled to exercise this Warrant during the period commencing on the date of such notice to the effective date of the event triggering such notice except as may otherwise be expressly set forth herein.

|

|

Section 4. Transfer of Warrant.

a) Transferability. Subject to compliance with applicable laws and the restrictive legend set forth at the beginning of this Warrant, this Warrant and all rights hereunder (including, without limitation, any registration rights) are transferable, in whole or in part, upon surrender of this Warrant at the principal office of the Company or its designated agent, which may be accepted via email, together with a written assignment of this Warrant substantially in the form attached hereto duly executed by the Holder or its agent or attorney and funds sufficient to pay any transfer taxes payable upon the making of such transfer, subject to compliance with applicable securities laws. Upon such surrender and, if required, such payment, the Company shall execute and deliver a new Warrant or Warrants in the name of the assignee or assignees, as applicable, and in the denomination or denominations specified in such instrument of assignment, and shall issue to the assignor a new Warrant evidencing the portion of this Warrant not so assigned, and this Warrant shall promptly be cancelled. Notwithstanding anything herein to the contrary, the Holder shall not be required to physically surrender this Warrant to the Company unless the Holder has assigned this Warrant in full, in which case, the Holder shall surrender this Warrant to the Company within three (3) Trading Days of the date on which the Holder delivers an assignment form to the Company assigning this Warrant in full. The Warrant, if properly assigned in accordance herewith, may be exercised by a new holder for the purchase of Warrant Shares without having a new Warrant issued. Notwithstanding the foregoing, each Holder hereby covenants and agrees in favour of the Company that it will not sell, transfer or assign any Warrants or any Warrant Shares to any Canadian resident or any person for subsequent resale to a Canadian resident for a period of four months and a day after the Issue Date.

b) Warrant Register. The Company shall register this Warrant, upon records to be maintained by the Company or the Transfer Agent for that purpose (the “Warrant Register”), in the name of the record Holder hereof from time to time. The Company may deem and treat the registered Holder of this Warrant as the absolute owner hereof for the purpose of any exercise hereof or any distribution to the Holder, and for all other purposes, absent actual notice to the contrary.

c) Transfer Restrictions. If, at the time of the surrender of this Warrant in connection with any transfer of this Warrant, the transfer of this Warrant shall not be either (i) registered pursuant to an effective registration statement under the Securities Act and under applicable state securities or blue sky laws or (ii) eligible for resale without volume or manner-of-sale restrictions or current public information requirements pursuant to Rule 144, the Company may require, as a condition of allowing such transfer, that the Holder or transferee of this Warrant, as the case may be, comply with the provisions of restrictive legend set forth at the beginning of this Warrant and Section 4(e) below.

e) Representations by the Holder. The Holder, by the acceptance hereof, represents and warrants that it is acquiring this Warrant and, upon any exercise hereof, will acquire the Warrant Shares issuable upon such exercise, for its own account and not with a view to or for distributing or reselling such Warrant Shares or any part thereof in violation of the Securities Act or any applicable state securities law, except pursuant to sales registered or exempted under the Securities Act. The Holder, by the acceptance hereof, (i) acknowledges that any resale of the Warrant or the Warrant Shares in or into Canada must be exempt from, or not subject to, the requirement in Canadian securities legislation that prohibits a person or company from distributing a security without a prospectus that qualifies that distribution, and, where applicable, in compliance with or exempt from dealer registration requirements under Canadian securities legislation, and (ii) covenants that, unless permitted under applicable Canadian securities legislation, the Holder will not trade the Warrant or the Warrant Shares in Canada before the date that is four (4) months and a day after the date of this Warrant. The Holder acknowledges and agrees that, until such time as this Warrant and the Warrant Shares issuable upon exercise of this Warrant may be sold pursuant to Rule 144 without restriction, this Warrant and any such Warrant Shares, whether maintained in a book-entry system or otherwise, will bear one or more legends in substantially the form and substance as the restrictive legend set forth at the beginning of this Warrant.

Section 5. Miscellaneous.

a) No Rights as Shareholder Until Exercise; No Settlement in Cash. This Warrant does not entitle the Holder to any voting rights, dividends or other rights as a shareholder of the Company prior to the exercise hereof as set forth in Section 2(b)(i), except as expressly set forth in Section 3. In no event shall the Company be required to net cash settle an exercise of this Warrant.

|

|

b) Loss, Theft, Destruction or Mutilation of Warrant. Subject to the Articles of the Company, the Company covenants that upon receipt by the Company of evidence reasonably satisfactory to it of the loss, theft, destruction or mutilation of this Warrant or any share certificate relating to the Warrant Shares, and in case of loss, theft or destruction, of indemnity or security reasonably satisfactory to it (which, in the case of the Warrant, shall not include the posting of any bond), and upon surrender and cancellation of such Warrant or share certificate, if mutilated, the Company will make and deliver a new Warrant or share certificate of like tenor and dated as of such cancellation, in lieu of such Warrant or share certificate.

c) Trading Days (Saturdays, Sundays, Holidays, etc.). If the last or appointed day for the taking of any action or the expiration of any right required or granted herein shall not be a Trading Day, then such action may be taken or such right may be exercised on the next succeeding Trading Day.

d) Authorized Shares.

The Company covenants that, during the period the Warrant is outstanding, it will reserve from its authorized and unissued Common Shares a sufficient number of Common Shares to provide for the issuance of the Warrant Shares upon the exercise of any purchase rights under this Warrant. The Company further covenants that its issuance of this Warrant shall constitute full authority to its officers who are charged with the duty of issuing the necessary Warrant Shares upon the exercise of the purchase rights under this Warrant. The Company will take all such reasonable action as may be necessary to assure that such Warrant Shares may be issued as provided herein without violation of any applicable law or regulation, or of any requirements of the Trading Market upon which the Common Shares may be listed. The Company covenants that all Warrant Shares which may be issued upon the exercise of the purchase rights represented by this Warrant will, upon exercise of the purchase rights represented by this Warrant and payment for such Warrant Shares in accordance herewith, be duly authorized, validly issued, fully paid and nonassessable and free from all taxes, liens and charges created by the Company in respect of the issue thereof (other than taxes in respect of any transfer occurring contemporaneously with such issue).

Except and to the extent as waived or consented to by the Holder, the Company shall not by any action, including, without limitation, amending its certificate of incorporation or through any reorganization, transfer of assets, consolidation, merger, dissolution, issue or sale of securities or any other voluntary action, avoid or seek to avoid the observance or performance of any of the terms of this Warrant, but will at all times in good faith assist in the carrying out of all such terms and in the taking of all such actions as may be necessary or appropriate to protect the rights of Holder as set forth in this Warrant against impairment. Without limiting the generality of the foregoing, the Company will (i) not increase the par value of any Warrant Shares above the amount payable therefor upon such exercise immediately prior to such increase in par value, (ii) take all such action as may be necessary or appropriate in order that the Company may validly and legally issue fully paid and nonassessable Warrant Shares upon the exercise of this Warrant and (iii) use commercially reasonable efforts to obtain all such authorizations, exemptions or consents from any public regulatory body having jurisdiction thereof, as may be, necessary to enable the Company to perform its obligations under this Warrant.

Before taking any action which would result in an adjustment in the number of Warrant Shares for which this Warrant is exercisable or in the Exercise Price, the Company shall obtain all such authorizations or exemptions thereof, or consents thereto, as may be necessary from any public regulatory body or bodies having jurisdiction thereof.

|

|

e) Jurisdiction/Governing Law. All questions concerning the construction, validity, enforcement and interpretation of this Warrant shall be governed by and construed and enforced in accordance with the internal laws of the State of New York, without regard to the principles of conflicts of law thereof. Each party agrees that all legal proceedings concerning the interpretations, enforcement and defense of the transactions contemplated by this Warrant (whether brought against a party hereto or its respective affiliates, directors, officers, shareholders, partners, members, employees or agents) shall be commenced exclusively in the state and federal courts sitting in the City of New York. Each party hereby irrevocably submits to the exclusive jurisdiction of the state and federal courts sitting in the City of New York, Borough of Manhattan for the adjudication of any dispute hereunder or in connection herewith or with any transaction contemplated hereby or discussed herein (including with respect to the enforcement of any of this Warrant), and hereby irrevocably waives, and agrees not to assert in any action or proceeding, any claim that it is not personally subject to the jurisdiction of any such court, that such action or proceeding is improper or is an inconvenient venue for such proceeding. Each party hereby irrevocably waives personal service of process and consents to process being served in any such action or proceeding by mailing a copy thereof via registered or certified mail or overnight delivery (with evidence of delivery) to such party at the address in effect for notices to it under this Warrant and agrees that such service shall constitute good and sufficient service of process and notice thereof. Nothing contained herein shall be deemed to limit in any way any right to serve process in any other manner permitted by law.

f) Restrictions. The Holder acknowledges that the Warrant Shares acquired upon the exercise of this Warrant, if not registered, will have restrictions upon resale imposed by state, provincial and federal securities laws.

g) Nonwaiver and Expenses. No course of dealing or any delay or failure to exercise any right hereunder on the part of Holder shall operate as a waiver of such right or otherwise prejudice the Holder’s rights, powers or remedies. Without limiting any other provision of this Warrant, each party shall pay their own expenses incurred with respect to collecting any amounts due pursuant hereto or in otherwise enforcing any of its rights, powers or remedies hereunder.

h) Notices. Any notices, consents, waivers or other document or communications required or permitted to be given or delivered under the terms of this Warrant must be in writing and will be deemed to have been delivered: (i) upon receipt, if delivered personally; (ii) when sent, if sent by e-mail (provided that such sent e-mail is kept on file (whether electronically or otherwise) by the sending party and the sending party does not receive an automatically generated message from the recipient’s e-mail server that such e-mail could not be delivered to such recipient) and (iii) if sent by overnight courier service, one (1) Trading Day after deposit with an overnight courier service with next day delivery specified, in each case, properly addressed to the party to receive the same. If notice is given by email, a copy of such notice shall be dispatched no later than the next business day by first class mail, postage prepaid. The addresses and e-mail addresses for such communications shall be:

If to the Company:

c/o DuMoulin Black LLP

TMC the metals company Inc.

1111 West Hastings Street, 15th Floor

Vancouver, British Columbia, V6E 2J3

Attention: Chief Financial Officer

Email: craig@metals.co

With a copy (for informational purposes only) to:

Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C.

One Financial Center

Boston, MA 02111

E-mail: dtkajunski@mintz.com

Attention: Daniel Kajunski, Esq.

If to a Holder, to its address or e-mail address set forth herein or on the books and records of the Company.

Or, in each of the above instances, to such other address or e-mail address and/or to the attention of such other person as the recipient party has specified by written notice given to each other party at least five (5) days prior to the effectiveness of such change. Written confirmation of receipt (A) given by the recipient of such notice, consent, waiver or other communication or (B) provided by an overnight courier service shall be rebuttable evidence of personal service, receipt from an overnight courier service in accordance with clause (i) or (iii) above, respectively. A copy of the e-mail transmission containing the time, date and recipient e- mail address shall be rebuttable evidence of receipt by e-mail in accordance with clause (ii) above.

|

|

i) Limitation of Liability. No provision hereof, in the absence of any affirmative action by the Holder to exercise this Warrant to purchase Warrant Shares, and no enumeration herein of the rights or privileges of the Holder, shall give rise to any liability of the Holder for the purchase price of any Common Shares or as a shareholder of the Company, whether such liability is asserted by the Company or by creditors of the Company.

j) Remedies. The Holder, in addition to being entitled to exercise all rights granted by law, including recovery of damages, will be entitled to specific performance of its rights under this Warrant. The Company agrees that monetary damages would not be adequate compensation for any loss incurred by reason of a breach by it of the provisions of this Warrant and hereby agrees to waive and not to assert the defense in any action for specific performance that a remedy at law would be adequate.

k) Successors and Assigns. Subject to applicable securities laws, this Warrant and the rights and obligations evidenced hereby shall inure to the benefit of and be binding upon the successors and permitted assigns of the Company and the successors and permitted assigns of Holder. The provisions of this Warrant are intended to be for the benefit of any Holder from time to time of this Warrant and shall be enforceable by the Holder or holder of Warrant Shares.

l) Amendment. This Warrant may be modified or amended or the provisions hereof waived with the written consent of the Company and the Holder.

m) Severability. Wherever possible, each provision of this Warrant shall be interpreted in such manner as to be effective and valid under applicable law, but if any provision of this Warrant shall be prohibited by or invalid under applicable law, such provision shall be ineffective to the extent of such prohibition or invalidity, without invalidating the remainder of such provisions or the remaining provisions of this Warrant.

n) Headings. The headings used in this Warrant are for the convenience of reference only and shall not, for any purpose, be deemed a part of this Warrant.

********************

(Signature Page Follows)

|

|

IN WITNESS WHEREOF, the Company has caused this Warrant to be executed by its officer thereunto duly authorized as of the date first above indicated.

|

TMC THE METALS COMPANY INC.

|

||

| By: | /s/ Gerard Barron | |

| Name: Gerard Barron | ||

| Title: Chief Executive Officer | ||

Agreed to and accepted by:

|

THE KINGDOM OF TONGA

|

||

| By: | /s/ 'Uhilamoelangi Fasi | |

| Name: Hon. Dr. 'Uhilamoelangi Fasi | ||

|

Title: Minister for Lands, Survey & Natural Resources |

||

[Signature page to Common Share Purchase Warrant]

NOTICE OF EXERCISE

| TO: | TMC the metals company Inc. |

(1) The undersigned hereby elects to purchase ________ Warrant Shares of the Company pursuant to the terms of the attached Warrant (to be delivered only if exercised in full), and tenders herewith payment of the exercise price in full, together with all applicable transfer taxes, if any.

(2) The undersigned shall pay the aggregate Exercise Price of US$_________ for the applicable Warrant Shares to the Company in United States dollars as set forth in the attached Warrant.

(3) Please issue said Warrant Shares in the name of the undersigned or in such other name as is specified below (in the account at the Transfer Agent as specified below):

_______________________________

_______________________________

_______________________________

_______________________________

[SIGNATURE OF HOLDER]

| Name of Investing Entity: |

| Signature of Authorized Signatory of Investing Entity: |

| Name of Authorized Signatory: |

| Title of Authorized Signatory: |

| Date: |

ASSIGNMENT FORM

(To assign the foregoing Warrant, execute this form and supply required information. Do not use this form to purchase shares.)

FOR VALUE RECEIVED, the foregoing Warrant and all rights evidenced thereby are hereby assigned to (with the Holder representing and warranting that the assignment complied with all applicable laws and the restrictive legend set forth at the beginning of the foregoing Warrant):

| Name: | ||

| (Please Print) | ||

| Address: | ||

| (Please Print) | ||

| Phone Number: | ||

| Email Address: | ||

| Dated: | ||

| Holder’s Signature: | ||

| Holder’s Address: |

Exhibit 10.1

CERTAIN CONFIDENTIAL INFORMATION CONTAINED IN THIS DOCUMENT, MARKED BY [***], HAS BEEN OMITTED BECAUSE THE INFORMATION (I) IS NOT MATERIAL AND (II) WOULD LIKELY CAUSE COMPETITIVE HARM IF PUBLICLY DISCLOSED.

| Sponsorship Agreement |

| The Tonga Seabed Minerals Authority on behalf of the Government of the Kingdom of Tonga Tonga Offshore Mining Limited |

| Sponsorship Agreement |

Table of Contents

| 1. | Agreement subject to Act | 3 |

| 2. | Term | 3 |

| 3. | Sponsorship | 4 |

| 4. | Commercial Recovery Payment | 5 |

| 5. | Audit | 6 |

| 6. | Undertaking to Comply with ISA Contract Terms | 6 |

| 7. | Subcontractors | 7 |

| 8. | Training and Capacity Building | 7 |

| 9. | Applicable Taxes and Payments | 7 |

| 10. | Tongan Laws, Expropriation and Corporate Existence | 8 |

| 11. | Access to TOML Rights and Intellectual Property | 11 |

| 12. | Assignment of TOML Rights | 12 |

| 13. | Notification to TOML | 13 |

| 14. | Exploration and Exploitation Applications | 13 |

| 15. | Environmental and Safety Performance Monitoring Program | 14 |

| 16. | ESPMP Officers | 15 |

| 17. | Completion Criteria | 16 |

| 18. | Confidentiality | 16 |

| 19. | Administration Fee | 16 |

| 20. | TOML Default and State Default | 17 |

| 21. | Temporary Suspension of Activities | 18 |

| 22. | Material TOML Breach Termination | 19 |

| 23. | Material State Breach | 21 |

| 24. | Payment of a Continuity Benefit | 21 |

| 25. | Dispute Resolution | 26 |

| 26. | Authorisation to Enter Agreement | 27 |

| 27. | Governing Law & Jurisdiction | 27 |

| 28. | International Law | 28 |

| 29. | Notices | 28 |

| 30. | Entire Agreement | 29 |

| 31. | Force Majeure | 29 |

| 32. | Amendment | 30 |

| 33. | Severability of Provisions | 30 |

| 34. | Further Assurances | 30 |

| 35. | No Limitation | 30 |

| 36. | Representations and Warranties | 30 |

| 37. | Non Reliance | 31 |

| 38. | Counterparts | 31 |

| 39. | Interpretation | 31 |

| 40. | Definitions | 32 |

| Page ( |

| Date | August 4, 2025 |

| Parties | |

|

The Tonga Seabed Minerals Authority, on behalf of The Government of the Kingdom of Tonga (the “State”)

AND

Tonga Offshore Mining Limited (“TOML”) |

|

| Recitals | |

| A | TOML has the exclusive right to explore for Polymetallic Nodules in the International Seabed Area pursuant to the ISA Exploration Contract. |

| B | The State has Sponsored TOML’s Seabed Mineral Activities in the International Seabed Area pursuant to the Sponsorship Certificate, and agrees to maintain Sponsorship on the terms of this Agreement. |

| C | In consideration for the State’s continued sponsorship, TOML will make certain payments to the State in accordance with this Agreement and the Act. |

| D | During Exploitation, the Commercial Recovery Payment will be paid via the Tonga Seabed Minerals Authority to the Seabed Minerals Fund, in accordance with the Act to provide benefits to Tonga’s current and future generations in a transparent manner. |

| E | TOML currently funds community and social programs and provides training and capacity building initiatives for Tongan nationals and proposes to continue to provide such initiatives during the Exploration and Exploitation phases. |

| F | The Exploration and Exploitation will be carried out in the International Seabed Area, which is outside the sovereign jurisdiction of the State. For clarity, the State does not own the Polymetallic Nodules contained in the ISA Contract Area. Polymetallic nodule processing will also be carried out in a different national jurisdiction to the State given geographic and infrastructure constraints. |

| G | ISA Contracts are administered by the ISA, and TOML will be required to make payments to the ISA if it were to recover minerals during Exploitation. |

| Page |

| H | It is acknowledged that considerable funds will be required to be expended before any commercial Exploitation of the Polymetallic Nodules in the ISA Contract Area. The State is not making any monetary investment toward the Seabed Mineral Activities in the ISA Contract Area, and accordingly is not exposed to the risk of loss associated with such investment. |

| I | TOML undertakes that its Polymetallic Nodule Exploitation in the International Seabed Area will not directly impact on the environment in the Kingdom of Tonga and will not cause depletion of the Kingdom of Tonga’s own mineral resources. |

| J | With regard to the respective obligations and commitments under this Agreement, each of the parties covenant that it shall act in good faith and deal fairly with the other party. |

For good and valuable consideration, the Parties hereto agree to be bound by the following terms and conditions:

| 1. | Agreement subject to Act |

| 1.1 | This Agreement is issued under and subject at all times to the Act and the Regulations issued under the Act as at the date of this Agreement. If and to the extent any term and condition of this Agreement is in conflict with or inconsistent with the Act as at the date of this Agreement, the latter prevails. |

| 1.2 | Notwithstanding clause 1.1: |

the State acknowledges that the payments, contributions and benefits set out in this Agreement are done in satisfaction of any and all payments that may otherwise be payable by TOML under the Act and indemnifies TOML against any liability to make additional payments to the State other than those set out in this Agreement.

| 1.3 | Unless a contrary intention appears, terms used in this Agreement that are defined in UNCLOS, the relevant Rules of the ISA, the Act or the Regulations have the same meaning as those in UNCLOS, the relevant Rules of the ISA, the Act or the Regulations. |

| 2. | Term |

| 2.1 | This Agreement will remain in force until: |

| (a) | the Parties agree to terminate the Agreement; |

| (b) | this Agreement is terminated pursuant to clauses 10.6, 12, 22, or 23 of this Agreement. |

| Page |

| 2.2 | During the Term, and only if TOML holds an ISA Contracts, TOML shall, within [***] days of the end of each calendar year, submit a report to the Tonga Seabed Minerals Authority, containing information on its programme of activities for the previous year. Within [***] days of submitting the report, the Parties shall meet to discuss the report, as well as the performance of each of the Parties under this Agreement, to ensure the Agreement is being fulfilled as originally intended. |

| 3. | Sponsorship |

| 3.1 | The State agrees to: |

| (a) | provide and maintain Sponsorship of TOML and TOML’s Exploration and Exploitation of the ISA Contract Area (including providing Sponsorship of any future TOML’s Exploitation application(s) to the ISA) for the Term of this Agreement; and |

| (b) | do all things reasonably necessary to give effect to TOML having the full benefit of the Sponsorship, including renewing TOML’s Sponsorship Certificate where applicable, supporting any application made by TOML to the ISA for an extension to its ISA Exploration Contract, undertaking communications with, and providing documentation, certificates and undertakings to, the ISA or other regulatory body required in respect of the Sponsorship. |

| 3.2 | For clarity, the State acknowledges that the Sponsorship is provided by the State, as a signatory to UNCLOS, for the purposes of UNCLOS and the Rules of the ISA and that neither this Agreement nor Sponsorship confers on the State any rights to or in connection with: |

| (a) | the ISA Contracts; |

| (b) | the Polymetallic Nodules contained within the ISA Contract Area or recovered therefrom; or |

| (c) | any product produced from the processing of the Polymetallic Nodules. |

| 3.3 | Under its ISA Contracts, TOML will have the exclusive enjoyment and right to carry out the Exploration and Exploitation in the ISA Contract Area, and TOML may at its sole discretion deal with the title and ownership of ISA Contract Area and Polymetallic Nodules in any way. |

| 3.4 | The State recognizes that the Exploration and Exploitation within the ISA Contract Area shall require significant international financing, and the State agrees to use its best efforts to assist the TOML Group to obtain financing, including entering into agreements and providing formal documents that the lenders, investors and other third parties may reasonably require in relation to Sponsorship and the provision of regulatory certainty, however nothing herein will require or be deemed that the State has provided or guaranteed any such financing. |

| 3.5 | For the avoidance of doubt, the State is only sponsoring TOML, and is not sponsoring or responsible for the activities of any other entity in the TOML Group. |

| Page |

| 3.6 | For clarity, the Sponsorship Certificate is also referred to as a Title under the Act. |

| 4. | Commercial Recovery Payment |

| 4.1 | In exchange for the State agreeing to provide continued Sponsorship for the Term on the terms set out in this Agreement, TOML shall pay to the Tonga Seabed Minerals Authority during Payment Years a Commercial Recovery Payment (“CRP”) in accordance with this clause 4. |

| 4.2 | The CRP will be [***] per Tonne of Polymetallic Nodules Recovered from the ISA Contract Area during Payment Years. |

| 4.3 | The CRP shall be paid in arrears on or before: |

| (a) | the last day of [***], in respect of the period [***] to [***] each year; and |

| (b) | the last day of [***], in respect of the period [***] to [***] each year. |

| 4.4 | The CRP shall be adjusted (on a compounding basis) on the first day of January in each following year by the relevant factor in each following year that represents official inflation in the United States of America (“US”) using the All Items Consumer Price Index for All Urban Consumers (CPI-U) for the US City Average published from time to time by the US Department of Labour, Bureau of Labour Statistics. For example, if official inflation in the US is 3% in the 6th year of this Agreement the CRP will be increased by 3%. |

| 4.5 | No CRP or other amounts or payments will be payable by TOML to the State (except for the Administration Fee under clause 19 of this Agreement) until [***]. |

| 4.6 | Subject to clauses 10 and 19 of this Agreement, the State hereby agrees that the TOML Group will not be subject to or required to pay any taxes, payments or fees, other than those set out in this Agreement or the Act (as at the date of this Agreement), including the CRP and the taxes, payments and fees listed in clause 9. |

| 4.7 | The State hereby undertakes and affirms that at no time will the rights (and the full and peaceful enjoyment thereof) granted by it under this Agreement be discriminately derogated from or otherwise prejudiced by any Tongan Law or the action or inaction of the State, or any official thereof, or any other person whose actions or inactions are subject to the control of the Government. To the extent there is inconsistency between any future Tongan Law related to taxation or the financial terms between the State and the TOML Group, then this Agreement will govern. |

| 4.8 | In accordance with section 94 of the Act, once the CRP has been received by the Tonga Seabed Minerals Authority, the Tonga Seabed Minerals Authority will pay the funds in to the Seabed Minerals Fund, excepting any funds allocated by the Treasury to be used directly for the purposes of covering the costs of establishing the Tonga Seabed Minerals Authority and performing the functions under the Act. |

| Page |

| 5. | Audit |

| 5.1 | During the term of the ISA Contract, the State may, not more than once each calendar year, request in writing an independent audit of the amount of Polymetallic Nodules Recovered in the preceding calendar year (“Production Audit”). If the State requests a Production Audit, TOML and the State shall seek to agree on a suitably qualified and independent auditor to conduct the Production Audit. |

| 5.2 | TOML will provide the auditor with reasonable access to its records for the purpose of undertaking the Production Audit. |

| 5.3 | The Parties will require the auditor to provide a written report to the Parties on the findings of the Production Audit within [***] days of completion of the Production Audit. In the absence of manifest error, the findings of the auditor will be binding on the Parties. |

| 5.4 | If the auditor determines that a materially larger or smaller (i.e. more than 5%) amount of Polymetallic Nodules were Recovered from the ISA Contract Area in the preceding year than reflected in the CRP calculated by TOML for the year pursuant to clause 4, then within [***] of receipt of the auditor's report, TOML must recalculate in accordance with the accurate and revised figures determined by the auditor for that year the CRP under clause 4, and pay to (or deduct from future payments to) the State the difference between the CRP already paid and the CRP due under clause 4 on the basis of the revised figures. |

| 5.5 | The cost of an audit under this clause will be borne equally between the State and TOML. |

| 6. | Undertaking to Comply with ISA Contract Terms |

| 6.1 | TOML shall ensure that the Activities carried out in the International Seabed Area will be in compliance with: |

| (i) | the terms and conditions of the applicable ISA Contract that is in existence at the time and that pertains to the Activities in the International Seabed Area, including the environmental terms and conditions contained in the applicable ISA Contract; and |

| (ii) | TOML’s ISA Obligations that pertain to the Activities in the International Seabed Area. |

| 6.2 | TOML and its Subcontractors will not commit any actions, or make any omissions that would cause the State to materially breach its Sponsorship Obligations. |

| Page |

| 6.3 | The State will not commit any actions or make any omissions that would cause TOML to breach its obligations under clause 6.1 . |

| 7. | Subcontractors |

| 7.1 | Subject to the provisions of this clause, the State acknowledges and agrees that TOML may delegate to and/or contract with Subcontractors to undertake all or part of the Exploration and Exploitation. |

| 7.2 | Notwithstanding any delegation or contract to a Subcontractor, TOML: |

| (a) | remains bound by its obligations under this Agreement and the Act to carry out the Activities in accordance with TOML’s ISA Obligations, and will take reasonable and appropriate measures to ensure that the Subcontractors comply with TOML’s ISA Obligations; |

| (b) | agrees that the Exploration and Exploitation under an ISA Contract shall be carried out in accordance with TOML’s ISA Obligations and the Act, whether the Exploration or Exploitation is being carried out by TOML or a Subcontractor; and |

| (c) | is responsible to the State for any monetary damage the State suffers under UNCLOS for a breach of its Sponsorship Obligations resulting from the acts, negligence, omissions or defaults of any Subcontractor in carrying out the Activities in the International Seabed Area under TOML’s ISA Contract, as if they were the acts, negligence, omissions or defaults of TOML. |

| 7.3 | TOML shall take reasonable and appropriate measures to ensure that the Activities carried out in the International Seabed Area under an ISA Contract are executed by and under the supervision of appropriately qualified, experienced and skilled personnel. |

| 8. | Training and Capacity Building |

| 8.1 | TOML will fund and implement training and capacity building initiatives for Tongan nationals. |

| 9. | Applicable Taxes and Payments |

| 9.1 | Notwithstanding anything contained in this Agreement, TOML agrees that it will be subject to the following payments and conditions, where applicable: |

| (a) | [***]; |

| (b) | [***]; |

| (c) | [***]; |

| (d) | [***]; |

| (e) | [***]; |

| (f) | [***]; |

| Page |

| (g) | [***]; |

| (h) | [***]; |

| (i) | [***]; |

| (j) | [***], |

provided that such payments and conditions are applied on a fair and reasonable basis and are imposed on a non-discriminatory basis to all Tongan entities and nationals.

| 9.2 | The State also agrees that the payments TOML makes pursuant to this Agreement satisfy, fulfil and extinguish any obligation or liability to make any payments whatsoever under the Act. The State further indemnifies TOML against [***]. |

| 9.3 | For the avoidance of doubt, the TOML Group will not be subject to or required to pay any other Taxes for the Term, including without limitation [***]. |

| 10. | Tongan Laws, Expropriation and Corporate Existence |

| 10.1 | The State agrees and warrants that: |

| (a) | any Tongan Laws and regulations brought into effect after the Commencement Date will not interfere with or diminish TOML’s rights with respect to any ISA Contract Area, the Business or the rights arising under this Agreement and must not be a Discriminatory Change in Tongan Law, except to the extent the State has an obligation at International Law to enact or comply with such laws in order to fulfil the State’s Sponsorship Obligations; |

| (b) | to the extent that TOML or the TOML Group’s rights and obligations under this Agreement conflict with their rights and obligations under any Tongan Law, this Agreement will take precedence, and TOML and the TOML Group will be relieved of any obligations under Tongan Law to the extent that their rights and obligations conflict with Tongan Law; |

| (c) | the State will take such actions necessary to give effect to the exemptions from applicable law and tax law expressly provided in this Agreement. |

| 10.2 | Prior to bringing in any laws or regulations that are required by International Law to fulfil the State’s Sponsorship Obligations the State will provide TOML with reasonable and meaningful consultation. |

| 10.3 | The State must also notify TOML from time to time as to any applicable Tongan Law that may be brought in to effect to fulfil the State’s Sponsorship Obligations and shall provide TOML sufficient time to ensure that it is able to comply with those laws or otherwise seek dispute resolution between the Parties with regards to the application of such Tongan Law. In the event any such change comes into force and materially impacts on the financial obligations of TOML, then the parties agree to negotiate in good faith appropriate amendments to the payments contemplated to the State under this Agreement in order to maintain the same level of financial burden on TOML as of the date of execution of this Agreement. |

| Page |

| 10.4 | The State shall not impose, nor shall it permit or authorise any of its agencies or instrumentalities or any local or other authority of the State to impose any Taxes, impositions, rates or charges of any nature whatsoever on or in respect of the titles, property, or other assets, products, materials, or services used or produced by or through the Activities or by any or all of the TOML Group otherwise in the conduct of its business pursuant to the TOML Rights nor will the State take or permit to be taken by any such State authority any other discriminatory action which would deprive the TOML Group of full enjoyment of the rights granted and intended to be granted by the TOML Rights or otherwise under this Agreement. |

| 10.5 | In enacting and implementing Tongan Laws and regulations the State shall at all times accord TOML fair and equitable treatment, and will provide a stable and predictable legal framework and make decisions consistently and transparently and in accordance with the legitimate expectations of TOML and the TOML Group. |

| 10.6 | In the event there occurs any change in Tongan Laws (including without limitation provisions relating to imposts, duties, fees, charges, penalties, and Tax related legislation) after the date of this Agreement, and if upon TOML’s representation it appears that on a reasonable interpretation and application of the law it would have the effect of divesting, decreasing, or in any way limiting, reducing or withholding any rights or benefits accruing to TOML or the TOML Group under this Agreement or under current legislation, then the Parties shall, in good faith, negotiate to modify this Agreement so as to restore the economic rights and benefits of the TOML Group to a level equivalent to or as close as possible to what they would have been if such change had not occurred. If the economic rights and benefits of the TOML Group are not restored then TOML may at its election terminate this agreement. |

| 10.7 | The State will permit all bona fide monetary conversions and transfers related to the TOML Rights or the Business (including currency conversions, transfers to, by or on behalf of TOML, or any member of the TOML Group) to be made freely and without delay into and out of the Kingdom of Tonga provided the procedural laws applicable to the transfer of funds out of jurisdiction applicable to all persons are be complied with. |

| 10.8 | The State acting in good faith shall not do or cause to be done or permit any act, thing or omission whether legislative, executive or administrative which discriminates adversely and unfairly against TOML, any member of the TOML Group, the TOML Rights or the Business if it results, upon its application, in a deprivation of the full enjoyment of the rights granted or intended to be granted under this Agreement. |

| Page |

| 10.9 | The State shall accord TOML treatment no less favourable than the treatment it accords, in like situations, to other investors. |

| 10.10 | The State shall accord TOML full security and protection, including complete and unconditional legal protection. |

| 10.11 | The State shall not Expropriate, nationalize, confiscate, condemn or wrongfully possess, nor, to the extent possible, destroy, disrupt or interfere with TOML, TOML’s title to possession, TOML’s peaceful enjoyment of the TOML Rights and all property of TOML and any member of the TOML Group except against prompt adequate and effective compensation. Such compensation shall amount to the genuine value of TOML’s investment expropriated immediately before the expropriation or before the impending expropriation became public knowledge, whichever is the earlier, shall include interest at a normal commercial rate until the date of payment, shall be made without delay, be effectively realizable and be freely transferable. |

| 10.12 | In the event of any inconsistency between the provisions contained within this Agreement, the Parties agree that an interpretation of this Agreement will be preferred which gives TOML and the TOML Group the benefit of this Agreement without nationalisation or expropriation. |

| 10.13 | Provided TOML is in material compliance with this Agreement and the Companies Act, the State will take all necessary actions for the Term to ensure that the corporate existence of TOML as a body corporate duly organized and validly existing and in good standing under the laws of the State is maintained, including ensuring that all such authorisations, approvals, consents and licences are issued as may be required to enable TOML to maintain its good standing, including ensuring that certificates evidencing annual renewal of registration of incorporation are issued in a timely manner in accordance with the Companies Act. Unless TOML is in material breach of this Agreement and/or the Companies Act, the State shall ensure that no action is taken (either by the government or by any government entity or instrumentality) to interfere with the continued corporate existence and registration of TOML and such other members of the TOML Group incorporated in the State. |

| 10.14 | The State guarantees the conversion and transfer overseas of TOML earnings and savings or earnings of expatriate personnel, their Affiliates and Subcontractors, resulting from the Activities. |

| 10.15 | With respect to earnings of TOML servants or agents, and expatriate personnel, whilst the State will not place unnecessary restriction of transfer of funds legitimately earned by TOML servants or agents, and expatriate personnel, such transfers will comply with the procedural laws applicable to transfer of funds out of jurisdiction applicable to all persons. |

| Page |

| 11. | Access to TOML Rights and Intellectual Property |

| 11.1 | In accordance with the Act, the State agrees that any or all members of the TOML Group may have access by way of sharing, use, Assignment or any other manner of access to the TOML Rights and Intellectual Property or any part thereof at any time (“Access to TOML Rights and Intellectual Property”), at their sole discretion, without reason and without prior consultation, upon providing notification to the State. |