UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

or

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 001-32749

FRESENIUS MEDICAL CARE AG

(Exact name of Registrant as specified in its charter)

FRESENIUS MEDICAL CARE AG

(Translation of Registrant’s name into English)

Germany

(Jurisdiction of incorporation or organization)

Else-Kröner-Strasse 1, 61352 Bad Homburg, Germany

(Address of principal executive offices)

Olga Renkewitsch, +49 151 149 65 619, olga.renkewitsch@freseniusmedicalcare.com,

Else-Kröner-Strasse 1, 61352 Bad Homburg, Germany

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

American Depositary Shares representing ordinary shares |

|

FMS |

|

New York Stock Exchange |

Ordinary shares, no par value |

|

N/A |

|

New York Stock Exchange(1) |

| (1) | Not for trading, but only in connection with the registration of American Depositary Shares representing such shares. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Ordinary Shares, no par value: 293,413,449

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer, “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ |

Accelerated filer ☐ |

Non-accelerated filer ☐ |

|

|

Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☒

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☐ U.S. GAAP

☒ International Financial Reporting Standards as issued by the International Accounting Standards Board

☐ Other

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

☐ Item 17

☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

Table of contents

|

|

|

Page |

Introduction |

|

|

|

|

|

|

|

N/A |

6 |

||

N/A |

6 |

||

|

6 |

||

|

23 |

||

N/A |

80 |

||

|

81 |

||

|

109 |

||

|

152 |

||

|

155 |

||

|

156 |

||

|

157 |

||

|

166 |

||

|

167 |

||

|

|

|

|

N/A |

169 |

||

N/A |

Material modifications to the rights of security holders and use of proceeds |

169 |

|

|

169 |

||

|

Management’s annual report on internal control over financial reporting |

169 |

|

|

169 |

||

|

169 |

||

|

170 |

||

|

170 |

||

|

170 |

||

|

171 |

||

|

Purchase of equity securities by the issuer and affiliated purchasers |

171 |

|

|

171 |

||

|

171 |

||

N/A |

178 |

||

N/A |

Disclosure regarding foreign jurisdictions that prevent inspections |

178 |

|

|

178 |

||

|

178 |

||

|

|

|

|

N/A |

181 |

||

|

181 |

||

|

181 |

i

Certain defined terms

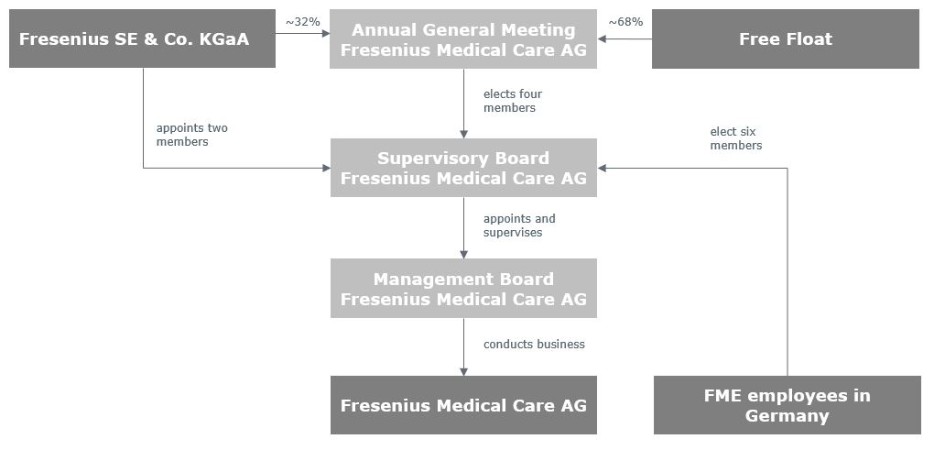

In this report, “FME AG,” or the “Company,” “we”, “us” or “our” refers to Fresenius Medical Care AG or to Fresenius Medical Care AG and its subsidiaries on a consolidated basis, as the context requires. “FMCH” and “D-GmbH” refer, respectively, to Fresenius Medical Care Holdings, Inc., the holding company for our North American operations, and to Fresenius Medical Care Deutschland GmbH, one of our German subsidiaries. In addition, “Fresenius SE” and “Fresenius SE & Co. KGaA” refer to Fresenius SE & Co. KGaA. Fresenius SE owns 94,380,382 of our shares as of February 13, 2025, 32.2% based on 293,413,449 outstanding shares, as reported herein. In this report, we use Fresenius SE to refer to that company as a partnership limited by shares, effective on and after January 28, 2011, as well as both before and after the conversion of Fresenius AG from a stock corporation under German law into a European Company (Societas Europaea) on July 13, 2007. “Management Board” and “our Management Board” refer to the members of the management board of FME AG and, except as otherwise specified, “Supervisory Board” and “our Supervisory Board” refer to the supervisory board of FME AG. “Ordinary shares” refers to the ordinary shares prior to the conversion in 2013 of our preference shares into ordinary shares. Following such conversion, we refer to our ordinary shares as “shares.”

The term “Care Enablement” refers to our Care Enablement operating segment, which is primarily engaged in the distribution of health care products and equipment and includes research and development (R&D), manufacturing, supply chain and commercial operations, as well as supporting functions, such as regulatory and quality management. The term “Care Delivery” refers to the Care Delivery operating segment, which is primarily engaged in providing services for the treatment of chronic kidney disease (CKD), end-stage renal disease (ESRD) and other extracorporeal therapies, including value and risk-based care programs. Care Delivery also includes the pharmaceutical products business and the income from equity method investees related to the sale of certain renal pharmaceuticals from Vifor Fresenius Medical Care Renal Pharma Ltd. (VFMCRP), which are used in our clinics to provide health care services to our patients. Our operating segments are determined based upon how we manage our businesses and allocate resources with responsibilities by products and services and is aligned to the financial information that is presented on a quarterly basis to the chief operating decision maker.

Our Global Medical Office (GMO), which seeks to optimize medical treatments and clinical processes within the Company and supports both Care Delivery and Care Enablement, is centrally managed and its profit and loss are allocated to the segments. Similarly, we allocate costs related primarily to headquarters’ overhead charges, including accounting and finance as well as certain human resources, legal and IT costs, as we believe that these costs are attributable to the segments and used in the allocation of resources to Care Delivery and Care Enablement. These costs are allocated at budgeted amounts, with the difference between budgeted and actual figures recorded at the corporate level. However, certain costs, which relate mainly to shareholder activities, management activities, global internal audit and the remeasurement of certain investments and virtual power purchase agreements, are not allocated to a segment but are accounted for as corporate expenses. These activities do not fulfill the definition of a segment according to IFRS 8, Operating Segments and are also reported separately as Corporate (Corporate). Financing is a corporate function which is not controlled by the operating segments. Therefore, the Company does not include interest expense relating to financing as a segment measurement. In addition, the Company does not include income taxes as we believe taxes are outside the segments’ control. See note 29 of the notes to the consolidated financial statements included in this report for a further discussion on our operating segments.

At an extraordinary general meeting (EGM) of the Company held on July 14, 2023, the shareholders of the Company approved a proposal to change the legal form of the Company from a partnership limited by shares (Kommanditgesellschaft auf Aktien – KGaA) into a stock corporation (Aktiengesellschaft – AG), (the Conversion). Upon effectiveness of the Conversion, which occurred upon registration of the Conversion with the competent commercial register on November 30, 2023, Fresenius Medical Care Management AG, the Company’s former general partner (Management AG) exited the Company, Fresenius SE & Co. KGaA (Fresenius SE) ceased to control (as defined by IFRS 10, Consolidated Financial Statements) the Company and the Company ceased to be a member of the Fresenius SE consolidated group. Following the Conversion, Fresenius SE continued to hold 32.2% of our share capital.

The abbreviations “THOUS” and “M” are used to denote the presentation of amounts in thousands and millions, respectively. All references in this report to the notes to our financial statements are to the notes to the consolidated financial statements included in this report.

1

Forward-looking statements

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act). When used in this report, the words “outlook,” “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “guidance,” “target” and similar expressions are generally intended to identify forward looking statements. Although we believe that the assumptions and expectations reflected in such forward-looking statements are reasonable, forward-looking statements are inherently subject to risks and uncertainties, many of which cannot be predicted with accuracy and some of which might not be anticipated. Additionally, subsequent events and actual results, financial and otherwise, have differed in the past and, going forward, could differ materially from those set forth in or contemplated by the forward-looking statements contained elsewhere in this report. We have based these forward-looking statements on current estimates and assumptions made to the best of our knowledge. By their nature, such forward-looking statements involve risks, uncertainties, assumptions and other factors which could cause actual results, including our financial condition and profitability, to differ materially, positively or negatively, relative to the results expressly or implicitly described in or suggested by these statements. Moreover, forward-looking estimates or predictions derived from third parties’ studies or information (which we do not independently verify) may prove to be inaccurate. Consequently, we cannot give any assurance regarding the future accuracy of the opinions set forth in this report or the actual occurrence of the projected developments described herein. In addition, even if our future results meet the expectations expressed here, those results may not be indicative of our performance in future periods.

These risks, uncertainties, assumptions, and other factors, including associated costs, could cause actual results to differ from our projected results and include, among others, the following:

| ● | changes in governmental and private payor reimbursement for our complete products and services portfolio, including the United States (U.S. or USA) Medicare reimbursement system for dialysis and other health care services, including potentially significant changes to the Patient Protection and Affordable Care Act of 2010 (Pub.L. 111-148), as amended by the Health Care and Education Reconciliation Act (Pub.L. 111-152) (collectively, ACA) that could result from the expiration of insurance premium subsidies presently available under the ACA or future efforts to revise, repeal or replace the ACA, and changes by regulators to certain reimbursement models, such as the ESRD Treatment Choices (ETC) model and the Comprehensive Kidney Care Contracting (CKCC) model, which could significantly impact performance under these models in unanticipated ways; |

| ● | our ability to accurately interpret and comply with complex current and future government regulations applicable to our business including sanctions and export control laws and regulations, laws and regulations in relation to environmental, social and governance topics, the impact of health care, tax and trade law reforms, in particular the Organisation for Economic Co-operation and Development (OECD) initiatives for the reallocation of taxation rights to market countries (Pillar one) and introduction of a global minimum tax (Pillar two) as well as potential U.S. tax reform and countermeasures to OECD Global Tax deals, antitrust and competition laws in the countries and localities in which we operate, other government regulation including, in the U.S., the federal Medicare and Medicaid Fraud and Abuse Amendments of 1977, as amended (the Anti-Kickback Statute), the False Claims Act, the federal Physician Self-Referral Law (the Stark Law), the Civil Monetary Penalty Law, the Health Insurance Portability and Accountability Act, the Health Information Technology for Economic and Clinical Health Act, the Foreign Corrupt Practices Act (FCPA), the Federal Trade Commission Non-Compete Clause Rule (which is presently subject to an injunction against enforcement), the U.S. Securities and Exchange Commission’s (SEC) climate disclosure rules (which have been stayed by the SEC pending the completion of judicial review) and (in each case) other similar state laws, as well as the Food, Drug and Cosmetic Act and, outside the U.S. (International), inter alia, the European Union (EU) Medical Device Regulation (MDR), the EU General Data Protection Regulation, the EU Taxonomy Regulation, the EU Corporate Sustainability Reporting Directive (CSRD), the EU Artificial Intelligence Act, the NIS 2 Directive (Directive (EU) 2022/2555), the German Act on Human Rights Due Diligence in Supply Chains, the EU Due Diligence Directive, the two invoice policy, “Buy China” policy, volume-based procurement policies and the Tendering and Bidding Law in China and other related local legislation as well as other comparable regulatory regimes in many of the countries where we supply health care services and/or products. |

2

In the U.S., the interpretation of these statutes and the validity of existing interpretations by the agencies that administer such statutes may be subject to increased uncertainty as a result of the U.S. Supreme Court’s opinion in Loper Bright Enterprises v. Raimondo and Relentless v. Department of Commerce, 603 U.S. (2024) (Loper) in June 2024. Loper overruled the so-called “Chevron Doctrine” under which administrative agencies were accorded significant deference in their interpretation of the statutes they administer. The Loper opinion held that the U.S. Administrative Procedure Act requires courts to “exercise their independent judgment in deciding whether an agency has acted within its statutory authority.” While the effects of the Loper decision will become apparent over the succeeding months and years, it is possible that the decision could result in additional litigation challenging regulations, guidance, and decisions issued by agencies such as the U.S. Food and Drug Administration (FDA) and the Centers for Medicare and Medicaid (CMS), concern over the enforceability of such regulations until tested in court, challenges to CMS guidance in areas such as coverage billing requirements, coding decisions, add-on payments and procedure categorization and the Medicaid Drug Rebate Program, as well as the validity of advisory opinions and safe-harbor regulations issued by the Office of Inspector General of the Department of Health and Human Services under the Anti-Kickback Statute. Such additional litigation could also result in additional uncertainty regarding such regulations and interpretations due to conflicting interpretations and rulings issued by courts in different jurisdictions. Given the uncertainty created by the Loper decision, we cannot predict its potential impact on our financial condition and results of operations at this time;

| ● | the influence of private payors (including integrated care organizations, commercial insurance and Medicare Advantage plans, also known as Medicare Part C, offered by private health insurers approved by CMS to provide their members with Medicare Part A, Part B and usually Part D benefits (Medicare Advantage or MA plans), as well as efforts by these organizations to manage costs by limiting health care benefits, narrowing their networks, reducing provider reimbursement, implementing prior authorization requirements and/or restricting options for patient funding of health insurance premiums, including efforts by employer group health plans (EGHPs) and commercial insurers to make dialysis reimbursement payments at a lower rate as a result of the U.S. Supreme Court’s ruling in Marietta Memorial Hospital Employee Health Benefit Plan, et al. v. DaVita Inc. et al. 142 S. Ct. 1968 (2022) (Marietta), particularly if the U.S. Congress fails to enact legislation that would reverse the effects of that decision; |

| ● | the impact of worldwide pandemics (for example, the severe acute respiratory syndrome coronavirus 2 and the related Coronavirus disease (COVID-19) pandemic), including, without limitation, a significant increase in mortality of patients with chronic kidney diseases as well as an increase in persons experiencing renal failure, the impacts of global viruses on our patients, caregivers, employees, suppliers, supply chain, business and operations, and consequences of economic downturns resulting from global pandemics; |

| ● | our ability to attract and retain skilled employees and risks that competition for labor, high turnover rates and meaningfully higher personnel costs as well as legislative, union, or other labor-related activities or changes have and will continue to result in significant increases in our operating costs, decreases in productivity and partial suspension of operations and to impact our ability to address additional treatments and growth recovery; |

| ● | the increase in raw material, energy, labor and other costs, including an impact from these cost increases and/or supply chain impacts on our cost savings initiatives and increases due to geopolitical conflicts in certain regions (for example, impacts related to the war between Russia and Ukraine (Ukraine War)) as well as the impact that inflation may have on a potential impairment of our goodwill, investments or other assets as noted above; |

| ● | the outcome of litigation as well as government and internal investigations; |

| ● | launch of new technology, introduction of generic or new pharmaceuticals and medical devices that compete with our products or services, advances in medical therapies, including the increased utilization of pharmaceuticals that reduce the progression of CKD and its precursors, xenotransplantation research and development and new market entrants that compete with our businesses (further information regarding the impact of certain pharmaceuticals that reduce the progression of CKD and our analysis of their impact on our cash flow projections and goodwill sensitivity assessments can be found in note 2 a) of the notes to the consolidated financial statements included in this report); |

| ● | product liability risks and the risk of recalls of our products by regulators; |

3

| ● | our ability to continue to grow our health care services and products businesses, organically and through acquisitions, including, with respect to acquisitions, the effects of increased enforcement of antitrust and competition laws, and to implement our strategy; |

| ● | the impact of currency and interest rate fluctuations, including the heightened risk of fluctuations as a result of geopolitical conflicts in certain regions, the impact of the current macroeconomic inflationary environment on interest rates and a related effect on our borrowing costs; |

| ● | volatility in the valuation of financial instruments connected to energy prices or energy production volumes (such as virtual power purchase agreements (vPPAs)), including the heightened risk of volatility as a result of geopolitical conflicts in certain regions; |

| ● | potential impairment of our goodwill, investments or other assets due to decreases in the recoverable amount of those assets relative to their book value, particularly as a result of sovereign rating agency downgrades coupled with an economic downturn in various regions or as a result of geopolitical conflicts in certain regions; |

| ● | our ability to protect our information technology systems and protected health information against cyber-attacks and to prevent other data privacy or security breaches of our data (including data held by our third party service providers), current and potential litigation arising from cybersecurity breaches and the potential effects on our reputation, customer or vendor relationships, business operations or competitiveness of any cybersecurity incidents we or our service providers may incur, as well as our ability to effectively capture efficiency goals and align with contractual and other requirements related to data offshoring activities; |

| ● | changes in our costs of purchasing and utilization patterns for pharmaceuticals and our other health care products and supplies, the inability to procure raw materials or disruptions in our supply chain; |

| ● | increases in tariffs and trade barriers that could result from withdrawal by single or multiple countries from multilateral trade agreements or the imposition of sanctions, retaliatory tariffs and other countermeasures in the wake of trade disputes and geopolitical conflicts in certain regions along with the effects of global events, political and/or governmental volatility and the influence of the U.S. political landscape and associated developments on health care systems, our patients or our business; |

| ● | collectability of our receivables, which depends primarily on the efficacy of our billing practices, the financial stability and liquidity of our governmental and private payors, services from third-party clearinghouses, customers and intermediaries as well as payor strategies to delay, dispute or thwart the collection process; |

| ● | our ability to secure contracts and achieve cost savings and desired clinical outcomes in our operations, including in our value-based care operations and other health care risk management programs in which we participate or intend to participate; |

| ● | the greater size, market power, experience and product offerings of certain competitors in certain geographic regions and business lines; |

| ● | the use of accounting estimates, judgments and accounting pronouncement interpretations in our consolidated financial statements; |

| ● | our ability to continue to achieve projected cost savings through 2025 as part of our previously announced transformation of our operating structure and steps to achieve cost savings (FME25 Program) as well as the possibility that changing or increasing responsibilities of our employees as a result of this transformation could require additional resources in the short-term; |

| ● | our ability to improve our financial performance through the divestiture of non-core and dilutive assets; and |

| ● | our ability to achieve projected price increases for our products and corresponding services. |

4

Important factors that could contribute to such differences are noted in Item 3.D, “Key Information – Risk factors,” Item 4B, “Information on the Company – Business overview,” and the notes to our audited consolidated financial statements included in this report.

Our business is also subject to other risks and uncertainties that we describe from time to time in our periodic public filings which can be accessed at the SEC website at www.sec.gov. Developments in any of these areas could cause our results to differ materially from the results that we or others have projected or may project.

The actual accounting policies, the judgments made in the selection and application of these policies, as well as the sensitivities of reported results to changes in accounting policies, assumptions and estimates, are additional factors to be considered along with our financial statements and the discussion under “Results of operations” in Item 5 below, “Operating and financial review and prospects.” For a discussion of our critical accounting policies, see note 2 of the notes to the consolidated financial statements included in this report.

We provide certain non-financial information about our efforts and performance in environmental, social, and governance (ESG) matters. This information, prepared in accordance with Sections 315b to 315c in conjunction with Sections 289c to 289e of the German Commercial Code and the EU Taxonomy Regulation, addresses key topics such as environmental sustainability, social responsibility, anti-corruption measures, and human rights and is included in our German Annual Report (Geschaeftsbericht). We voluntarily comply with CSRD requirements, which are currently not incorporated into German law, as part of providing such non-financial information. This information, included in our German Annual Report, is reviewed by an independent auditor and made available on our website under “Publications” on the “Investors” page at www.freseniusmedicalcare.com. The report, including our ESG information for 2024, will be published following the filing of our annual Form 20-F with the SEC.

Our sustainability efforts, including those on diversity, equity and inclusion, are designed to comply with any applicable laws, in particular anti-discrimination laws and other legal requirements of the various jurisdictions in which we operate. We are monitoring relevant legal developments, including early 2025 Executive Orders issued in the U.S., and will review our activities in relevant Company entities as appropriate to facilitate ongoing compliance with applicable laws, in particular anti-discrimination laws, and related risk mitigation efforts. Additionally, this Form 20-F is being filed for the fiscal year ended December 31, 2024, prior to the recent Executive Orders issued in the United States.

In referencing such ESG information and/or any other portions of our German Annual Report and furnishing our website address in this report, however, we do not intend to incorporate any content from those documents or information on our website into this report, and any information in those documents or on our website should not be considered to be part of this report, except as may be expressly set forth herein. This disclosure reflects our ongoing commitment to transparency and sustainability.

Rounding adjustments applied to individual numbers and percentages shown in this and other reports may result in these figures differing immaterially from their absolute values. Some figures (including percentages) in this report have been rounded in accordance with commercial rounding conventions. In some instances, such rounded figures and percentages may not add up to 100% or to the totals or subtotals contained in this report. Furthermore, totals and subtotals in tables may differ slightly from unrounded figures contained in this report due to rounding in accordance with commercial rounding conventions. A dash (–) indicates that no data were reported for a specific line item in the relevant financial year or period, while a zero (0) is used when the pertinent figure, after rounding, amounts to zero.

Market and industry data

Except as otherwise specified herein, all patient and market data in this report have been derived using internal estimates and publicly available information collected by our internal market analysis tools. See Item 4.B, “Information on the Company - Business Overview – Major Markets and Competitive Position.”

5

Part I

Item 1. |

Identity of directors, senior management and advisors |

Not applicable

Item 2.Offer statistics and expected timetable

Not applicable

Item 3.Key information

We conduct our business on a global basis in various currencies with major operations located in the U.S. and Germany. We prepare our consolidated financial statements utilizing the euro as our reporting currency. We have converted the balance sheets of our non-euro denominated operations into euro at the exchange rates prevailing at the balance sheet date. Revenues and expenses are translated at the annual average exchange rates for the respective period, as shown.

A summary of the spot and annual average exchange rates for the euro to U.S. dollars for the last three years is set forth below. The European Central Bank (ECB) determines such rates (Reference Rates) based on the regular daily averaging of rates between central banks within and outside the European banking system. The ECB normally publishes the Reference Rates daily around 4 p.m. Central European Time (CET).

Exchange rates |

|

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

December 31, |

|

|

|

|

|

|

|

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

2022 |

|

|

spot exchange |

|

spot exchange |

|

average exchange |

|

average exchange |

|

average exchange |

|

|

rate in € |

|

rate in € |

|

rate in € |

|

rate in € |

|

rate in € |

1 U.S. dollar |

|

0.96256 |

|

0.90498 |

|

0.92386 |

|

0.92484 |

|

0.94962 |

B. |

Capitalization and indebtedness |

Not applicable

C. |

Reasons for the offer and use of proceeds |

Not applicable

D. |

Risk factors |

Before you invest in our securities, you should be aware that the occurrence of any of the events described in the following risk factors or elsewhere in this report, and other events that we have not predicted or assessed could affect the outcome of forward-looking statements included in this report and/or have a material adverse impact on our business, financial condition and results of operations. If the events described below or other unpredicted events occur, then the trading price of our securities could decline and you may lose all or part of your investment.

Risks relating to legal and regulatory matters

We operate in a highly regulated industry such that the potential for legislative reform provides uncertainty and potential threats to our operating models and results.

The delivery of health care services and products is highly regulated in virtually every country in which we operate. Proposals for legislative reform in these countries are often introduced to improve access to care, address quality of care issues and manage costs of the health care system. In the U.S., there have been efforts to pursue significant changes to existing health care programs, including efforts to repeal or replace the ACA which, while unsuccessful to date, continue. On June 17, 2021, the U.S. Supreme Court reversed lower court rulings that declared the ACA to be unconstitutional, holding that the states and other plaintiffs in the case did not have standing to challenge the law. If future efforts to limit or repeal the ACA are successful, such efforts could have significant effects on our businesses, both positive and negative, but the outcomes are impossible to predict.

6

In October 2017, the Trump administration discontinued making cost-sharing reduction (CSR) reimbursements to insurers, arguing that Congress failed to appropriate funding. In response, many state departments of insurance either allowed or required insurers to mitigate their losses by increasing the 2018 premiums on their ACA plans. Many insurers also mitigated the impact to themselves by “silver loading,” a practice whereby the premiums for silver-level plans were increased to offset the loss of CSR payments. Silver loading may also have mitigated the impact of premium increases to some low-income consumers by increasing their premium tax credits. In 2019 and 2020, all states either permitted or required silver loading. In 2017, several insurers sued the U.S. federal government to reinstate CSR payments. On June 21, 2021, the U.S. Supreme Court denied requests from multiple insurers to review lower court decisions that held they were not entitled to full unpaid CSR payments. As a result, insurers are entitled to the unpaid CSRs, but the total amount they are owed must be offset by any excess premium tax credits received from premium increases for 2018 and beyond. The Biden administration requested appropriations for CSR payments in its fiscal year (FY) 2025 budget request. Congress did not pass appropriations bills for FY 2025 and funding is maintained at current levels under a continuing resolution that expires on March 14, 2025. As a result, a reduction in the availability of insurance through insurance exchanges established by the ACA or expiration without renewal of insurance premium subsidies presently available under the ACA could reduce the number of our commercially insured patients and shift such patients to Medicare and Medicaid. In addition, the Marietta ruling makes it easier for health plans to design plan benefits for Medicare eligible ESRD patients in a way that makes private health insurance relatively less attractive to ESRD patients and Medicare relatively more attractive. In the Marietta case, the questions presented involved whether the health plan violated the Medicare Secondary Payor Act (MSPA) by “taking into account” that plan beneficiaries are eligible for Medicare and/or by “differentiating” between the benefits that the plan offers to patients with dialysis versus others. On June 21, 2022, the U.S. Supreme Court reversed the Sixth Circuit decision and held that the EGHP for Marietta Memorial Hospital did not violate the MSPA.

Bills were introduced previously to Congress that would address the Marietta decision, but will need to be reintroduced in the current Congress. The Restore Protections for Dialysis Patients Act would restore the interpretation of the Medicare Secondary Payer Act prior to the Marietta decision and ensure that patients cannot be discriminated against because of their need for dialysis. We cannot predict whether the U.S. Congress will enact this or any other proposed legislation that would reverse the potential effects of the Marietta decision. These bills will need to be reintroduced before they are taken up in the 119th Congress which began on January 3, 2025. As Medicare and Medicaid reimbursement rates are generally lower than the reimbursement rates paid by commercial insurers, a shift of commercially insured patients to Medicare and Medicaid could have a material adverse impact on our business, financial condition and results of operations. The Marietta ruling may also result in certain EGHPs reducing the benefits offered for dialysis, which could, depending on the number of patients impacted, have a material and adverse impact on our business, financial condition and results of operation. There can be no assurance that this proposal or any other legislation to address the Marietta decision will be enacted. See “Changes in reimbursement, payor mix and/or governmental regulations for health care could materially decrease our revenues and operating profit” below.

7

Changes in reimbursement, payor mix and/or governmental regulations for health care could materially decrease our revenues and operating profit.

We receive reimbursement for our health care services from both public, government-sponsored payors and private, commercial payors. A large portion of our businesses is reimbursed by government payors, in particular the Medicare and Medicaid programs in the U.S. For the fiscal year ended December 31, 2024, approximately 18% of our consolidated revenues resulted from Medicare and Medicaid (excluding Medicare Advantage) reimbursement. The Medicare and Medicaid programs change their payment methodologies and funding from time to time in ways that are driven by changes in statute, economic conditions, and policy. For example, the Budget Control Act of 2011 (BCA) required a $1.2 trillion reduction in deficits through 2021. As a backup, if Congress could not agree on proposals to reach this target, sequestration or across-the-board spending cuts would go into effect (U.S. Sequestration). On April 1, 2013, a 2% reduction to Medicare payments took effect and continues in force. Additionally, the Statutory Pay-As-You-Go Act of 2010 (Statutory PAYGO) requires that if the Congressional Budget Office determines that Congress has passed legislation increasing the federal budget deficit, a 4% sequester cut for Medicare program payments would become effective. To date, Congress has passed legislation increasing the federal deficit on a number of occasions subsequent to the passage of Statutory PAYGO, but has always acted to prevent such sequestration from becoming effective. Spending cuts pursuant to the U.S. Sequestration have adversely affected our operating results in the past and will continue to do so. In addition, options to restructure the Medicare program in the direction of a defined contribution, “premium support” model and to shift Medicaid funding to a block grant or per capita arrangement, with greater flexibility for the states, have been proposed or considered from time to time. Changes in payment methodologies and funding or payment requirements of (without limitation) the End-Stage Renal Disease Prospective Payment System (ESRD PPS), the Physician Fee Schedule, the Clinical Laboratory Fee Schedule and the Ambulatory Surgical Center Payment System may have material effects on our operating results. We may also experience changes in the interpretation of government regulations by the courts. We have very little opportunity to influence or predict the magnitude of many of those changes. For further information regarding Medicare and Medicaid reimbursement, including new payment models proposed by executive order in July 2019 which are intended to encourage identification and earlier treatment of kidney disease as well as increased home dialysis and transplants, see Item 4B, “Information on the Company — Business Overview — Regulatory and Legal Matters — Reimbursement.”

Our patients make decisions about their insurance coverage among options that, depending on their personal circumstances and location, may include Medicare, Medicaid, Medicare Advantage plans, employer group health coverage, exchange plans and other commercial coverage. Government reimbursement programs, including Medicare and Medicaid, generally pay less than commercial insurance, and Medicare Advantage plans generally pay less than other commercial plans. In addition, we may experience higher write-offs of Medicare deductibles and other cost-sharing amounts due to secondary uninsured and underinsured patients which would result in an increase in uncollectible accounts. As a result, the payments we receive from private payors generate a substantial portion of the profits we report. For further information, see the table “U.S. patient service revenue” detailing the percentage generated from government reimbursement and private payors in the U.S. in Item 4B, “Information on the Company — Business overview.”

Any of the following events, among others, could have a material adverse impact on our business, financial condition and results of operations:

| ● | we may be subject to rejections of or reductions in reimbursement from private payors, including, for example, through their use of lower allowed charges rather than rates based on our billed charges; |

| ● | we may experience a reduction in our ability to obtain and retain commercially insured patients to utilize our health care services; |

| ● | efforts by private payors to continue to control the cost of and/or the eligibility for access to health care services, including relative to insurance products on and off the health care exchanges established by the ACA and potential efforts by employer group health plans and commercial insurers to limit benefits or reduce reimbursement for our services or eliminate reimbursement for some of our services; |

| ● | a portion of our business that is currently reimbursed by private insurers or hospitals may become reimbursed by integrated care organizations, which may use payment methodologies that reduce reimbursement for our services. There can be no assurance that we can achieve future price increases from private insurers and integrated care organizations offering private insurance coverage to our patients; |

8

| ● | if legislative or regulatory efforts or litigation to restrict or eliminate the charitable funding of patient insurance premiums are successful, our patients with coverage under publicly funded programs like Medicare may be unable to continue to pay the premiums for that coverage and may become uninsured for dialysis services. In addition, a portion of our patients who are currently covered by private insurers may be unable to continue to pay the premiums for that coverage and may become uninsured for dialysis services or may elect to transition to government funded reimbursement programs that reimburse us at lower rates for our services. See Item 4B, “Information on the Company – Business Overview – Regulatory and Legal Matters – Reimbursement – Potential changes impacting our private payors” for further information; or |

| ● | if we are unable to secure appropriate reimbursement arrangements for the pharmaceuticals we provide in our dialysis clinics, we could experience a material adverse effect on our operating results. An increased utilization of bundled pharmaceuticals, as part of the ESRD PPS, or decreases in reimbursement for pharmaceuticals outside the bundled rate may result in a material adverse impact on our results of operations. |

For further information, see Item 4B, “Information on the Company — Business Overview — Regulatory and Legal Matters — Reimbursement.”

In addition to the foregoing factors, the health care insurance industry is experiencing continuing consolidation among insurers and pharmacy benefit managers, including increasing buyer power and impacts on referral streams. Such consolidation could have a material adverse effect on our ability to negotiate favorable coverage terms and reimbursement rates.

If we do not comply with the numerous governmental regulations applicable to our business, we could suffer adverse legal consequences, including exclusion from government health care programs or termination of our authority to conduct business, any of which would result in a material decrease in our revenue; this regulatory environment also exposes us to claims and litigation, including “whistleblower” suits.

Our operations in both our health care services business and our products business are subject to extensive governmental regulation in virtually every country in which we operate. We are also subject to other laws of general applicability, including antitrust, anti-bribery and anti-corruption laws as well as sustainability requirements. The applicable regulations, which differ from country to country, cover areas that include:

| ● | regulatory approvals for products or product improvements; |

| ● | regulatory approvals and oversight of clinical and certain non-clinical R&D activities; |

| ● | the quality, safety and efficacy of medical and pharmaceutical products and supplies; |

| ● | the operation and licensure of manufacturing facilities, laboratories, dialysis clinics, ambulatory surgery centers and other health care facilities; |

| ● | product labeling, advertising and other promotion; |

| ● | accurate reporting and billing for government and third-party reimbursement, including accurate and complete medical records to support such billing and, in the U.S., the obligation to report and return overpayments within 60 days of the time that the overpayment is identified and quantified; |

| ● | the discounting of reimbursed drug and medical device products and the reporting of drug prices to government authorities; |

| ● | limits on our ability to make acquisitions or certain investments and the terms of those transactions; |

| ● | the collection, dissemination, access, use, security, protection and privacy of protected health information or other protected data, as well as requirements to report data breaches to regulatory agencies; and |

| ● | compensation of medical directors and other financial arrangements with physicians and other referral sources. |

9

Failure to comply with one or more of these laws or regulations may give rise to a number of adverse legal consequences. These include, in particular, loss or suspension of federal certifications, loss or suspension of licenses under the laws of any state or governmental authority from which we generate substantial revenues, monetary and administrative penalties, product recalls, increased costs for compliance with government orders, complete or partial exclusion from government reimbursement programs, refunds of payments received from government payors and government health care program beneficiaries due to failures to meet applicable requirements or complete or partial curtailment of our authority to conduct business. Any of these consequences could have a material adverse impact on our business, financial condition and results of operations.

Our medical devices and drug products are subject to detailed, rigorous and frequently changing regulation by numerous national, supranational, federal and state authorities. In addition, our facilities and procedures and those of our suppliers are subject to periodic inspection by various regulatory authorities which may suspend, revoke, or adversely amend the authority necessary for research, manufacture, marketing or sale of our products and those of our suppliers. We and our suppliers must incur expense and spend time and effort to ensure compliance with these complex regulations, and if such compliance is not maintained, we and our suppliers could be subject to significant adverse administrative and judicial enforcement actions in the future. These possible enforcement actions could include warning letters, injunctions, civil penalties, seizures of our products, and criminal prosecutions as well as dissemination of information to the public about such enforcement actions. These actions could result in, among other things, substantial modifications to our business practices and operations; refunds; a total or partial shutdown of production while the alleged violation is remedied; and recalls, withdrawals or suspensions of current products from the market. Any of these events, in combination or alone, could disrupt our business and have a material adverse impact on our business, financial condition and results of operations.

We operate many facilities and engage with other business associates to help carry out our health care activities. In such a widespread, global system, it is often difficult to maintain the desired level of oversight and control over the thousands of individuals employed by many affiliated companies and their business associates. We rely on our management structure, regulatory and legal resources and the effective operation of our compliance programs to direct, manage and monitor our operations, including the activities of our employees and their agents, to comply with government regulations. We cannot assure that our internal control policies and procedures will always protect us from intentional or inadvertent acts of our employees or agents that contravene our compliance policies or violate applicable laws. If employees were to deliberately, recklessly or inadvertently fail to adhere to these regulations, then our authority to conduct business could be terminated and our operations could be significantly curtailed. Any such terminations or reductions could materially reduce our revenues. If we fail to identify in our diligence process or to promptly remediate any non-compliant business practices in companies that we acquire, we could be subject to penalties, claims for repayment or other sanctions. Any such terminations or reductions could materially reduce our revenues, with a resulting material adverse impact on our business, financial condition and results of operations. See also “Risks relating to internal control and compliance — We operate in many different jurisdictions and we could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-corruption laws,” below.

By virtue of this regulatory environment, our business activities and practices are subject to extensive review by regulatory authorities and private parties, and continuing audits, subpoenas, other inquiries, claims and litigation relating to our compliance with applicable laws and regulations. We may not always be aware that an inquiry or action has begun, particularly in the case of “qui tam” or “whistleblower” actions brought by private plaintiffs under the False Claims Act, which are initially filed under seal. We are the subject of a number of governmental inquiries and civil suits by governmental and private plaintiffs. For information about certain of these pending investigations and lawsuits, see note 25 of the notes to our consolidated financial statements included in this report.

In addition, future legislative or regulatory changes could affect procedures or decision making for approving medical devices or pharmaceuticals. Any such legislation or regulations, if enacted or promulgated, could result in a delay or denial of regulatory approval for our products. If any of our products do not receive regulatory approval, or there is a delay in obtaining approval, this also could have a material adverse impact on our business, financial condition and results of operations.

Cyber-attacks or other privacy and data security incidents could disrupt our business and expose us to significant losses, liability and reputational damage.

We and our third-party service providers routinely process, store and transmit large amounts of data in our operations, including sensitive personal information as well as proprietary or confidential information relating to our business or third parties. We may be subject to breaches of the information technology security systems we use both internally and externally with third-party service providers.

10

Cyber-attacks may penetrate our and our third-party service providers’ security controls and result in the misappropriation or compromise of personal information or proprietary or confidential information, including such information which is stored or transmitted on the systems used by certain of our or their products, to create system disruptions, cause shutdowns (including disruptions to our production plants), or deploy viruses, worms, ransomware, denial-of-service attacks and other malicious software programs that attack our systems. We and our third-party service providers handle the personal information of our patients and beneficiaries, Patient Personal Data (PPD), throughout the U.S. and other parts of the world. We or our third-party service providers may experience a breach under the U.S. Health Insurance Portability and Accountability Act Privacy and Security Rules, the EU’s General Data Protection Regulation and or other similar laws (Data Protection Laws), including the following events:

| ● | impermissible use, access, or disclosure of unsecured PPD, |

| ● | a breach under Data Protection Laws when we or our business associates neglect to implement the required administrative, technical and physical safeguards of its electronic systems and devices, or |

| ● | a data breach that results in impermissible use, access or disclosure of personal identifying information of our employees, patients and beneficiaries. |

Our IT systems have been attacked in the past, resulting in certain patient data being illegally published. For information regarding our cybersecurity risk management and governance, see Item 16K. “Cybersecurity.” For information regarding litigation relating to cybersecurity incidents we experienced in 2023, see note 25 of the notes to the consolidated financial statements included in this report.

When appropriate, we have filed complaints against the unknown attackers with the relevant authorities and we contacted the patients who were affected by the illegal data publication as well as other relevant regulatory agencies and stakeholders. While there has not been any material impact to our financial condition and results of operations as a result of these attacks, future cyber-attacks against our IT systems may result in a loss of financial data or interruptions of our operations that could have a material adverse impact on our business, financial condition and results of operations in the future. The Ukraine War has increased the risk of cyber-attacks against our systems and data.

As we increase the amount of personal information or financial data that we store and share digitally, our exposure to these privacy and data breaches and cyber-attack risks increases (particularly as medical records are a high-value target), including the risk of undetected attacks, damage, loss or unauthorized disclosure or access, and the cost of attempting to protect against these risks also increases. Pursuant to recent legislation, Medicare coverage for telehealth services was extended to March 31, 2025. Commencing April 1, 2025, Medicare coverage for telehealth services will be available principally in rural areas. While the availability of telehealth services is convenient and improves access to medical care, increased reliance on, and utilization of, telemedicine for delivery of health care services could also increase the risk of privacy violations and our vulnerability to data breaches and cyber-attacks. There are no assurances that our security technologies, processes and procedures that we or our outside service providers have implemented to protect personal information and proprietary or confidential information and to build security into the design of our products will be effective. Any failure to keep our information technology systems, financial data and our patients’ and customers’ sensitive information secure from attack, damage, loss or unauthorized disclosure or access, whether as a result of our action or inaction or that of our third-party business associates or vendors that utilize and store such personal information on our behalf, could materially adversely affect our reputation and ability to continue normal operations. Additionally, such failure could expose us to mandatory public disclosure requirements, litigation and governmental enforcement proceedings, material fines, penalties and/or remediation costs, and compensatory, special, punitive and statutory damages, consent orders and other adverse actions, any of which could have a material adverse impact on our business, financial condition and results of operations.

11

If certain of our investments or value and risk-based care programs with health care organizations and health care providers are found to have violated the law, our business could be adversely affected.

A number of the dialysis clinics and health care centers that we operate are owned, or managed, by entities in which one or more hospitals, physicians or physician practice groups hold an interest. Physician owners, who are usually nephrologists, may also provide medical director services and physician owners may refer patients to those centers or other centers we own and operate or to other physicians who refer patients to those centers or other centers we own and operate. We also have arrangements with physician practices to collaborate on our value and risk-based care programs with public and private payors. In the past, certain parties have attempted to utilize our disclosure of these arrangements as the basis for qui tam proceedings under the Anti-Kickback Statute and the Stark Law. Such attempts have not been successful to date. Because our relationships with physicians are governed by the federal and state anti-kickback statutes and other state fraud and abuse laws, we have structured our arrangements to comply with many of the criteria for safe harbor protection and waivers under the Anti-Kickback Statute; however, these arrangements do not always satisfy all elements of applicable safe harbors. While we have established comprehensive compliance policies, procedures and programs to ensure ethical and compliant business operations, if one or more of our arrangements, including value and risk-based care programs, were found to be in violation of the Anti-Kickback Statute, the Stark Law, analogous state laws, or other similar laws worldwide, we could be required to restructure or terminate them. We could also be required to repay to Medicare, Medicaid as well as other federal health care program amounts pursuant to any prohibited referrals, and we could be subject to criminal and monetary penalties and exclusion from federal and state health care programs. Imposition of any of these penalties could have a material adverse impact on our business, financial condition and results of operations. See note 25 of the notes to our consolidated financial statements included in this report.

We are exposed to product liability, patent infringement and other claims which could result in significant costs and liability which we may not be able to insure on acceptable terms in the future.

Health care companies are typically subject to claims alleging negligence, product liability, breach of warranty, malpractice and other legal theories that may involve large claims and significant defense costs whether or not liability is ultimately imposed. Health care products may also be subject to recalls, statutory or regulatory shipping holds and intellectual property rights (for example patents or trademarks) infringement claims which, in addition to monetary penalties, may restrict our ability to sell or use our products. We cannot assure that such claims will not be asserted against us, or, for example, that significant adverse verdicts will not be reached against us or that large scale recalls of our products will not become necessary. In addition, the laws of some of the countries in which we operate provide legal rights to users of pharmaceutical products that could increase the risk of product liability claims. Product liability and intellectual property rights infringement claims, other actions for negligence or breach of contract and product recalls or related sanctions could result in significant costs. These costs could have a material adverse impact on our business, financial condition and results of operations.

While we have been able to obtain liability insurance in the past to partially cover our business risks, we cannot assure that such insurance will be available in the future either on acceptable terms or at all, or that our insurance carriers will not dispute their coverage obligations. In addition, FMCH, our largest subsidiary, is partially self-insured for professional, product and general liability, auto liability and worker’s compensation claims, up to pre-determined levels above which our third-party insurance applies. A successful claim for which we are self-insured or in excess of the limits of our insurance coverage could have a material adverse impact on our business, financial condition and results of operations. Liability claims, regardless of their merit or eventual outcome, also may have a material adverse effect on our business and result in a loss of customer confidence in us or our products, which could have a material adverse impact on our business, financial condition and results of operations. For information about certain of these pending investigations and lawsuits, see note 25 of the notes to our consolidated financial statements included in this report.

12

Risks relating to internal control and compliance

We operate in many different jurisdictions and we could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-corruption laws.

The U.S. FCPA and similar worldwide anti-corruption laws generally prohibit companies and their intermediaries from making improper payments to public officials for the purpose of obtaining or retaining business. Our internal policies mandate compliance with these anti-corruption laws. We operate many facilities throughout the U.S. and other parts of the world. Our widespread, global operations have thousands of persons employed by many affiliated companies, and we rely on our management structure, regulatory and legal resources and effective operation of our compliance program to direct, manage and monitor the activities of these employees and third-party intermediaries. On March 29, 2019, we entered into a non-prosecution agreement (NPA) with the U.S. Department of Justice (DOJ) and a separate agreement with the SEC in connection with its Cease and Desist Order (SEC Order) intended to resolve fully and finally the U.S. government allegations against us arising from DOJ and SEC investigations into conduct in countries outside the U.S. that violated the FCPA or other anti-bribery laws. As part of these agreements, we agreed to the appointment of an independent compliance monitor (the Monitor). On December 30, 2022, the Monitor certified to our implementation of an effective anti-corruption compliance program and submitted her final certification report on January 31, 2023. The DOJ and SEC have accepted the Monitor’s certification and the NPA and SEC Order expired on March 1, 2023 and March 29, 2023, respectively. While we continue to make significant investments in our compliance and financial controls and in our compliance, legal and financial organizations (including certain remaining recommendations of the Monitor), and are fully committed to compliance with the FCPA and other applicable anti-bribery laws, we cannot ensure that our internal control policies and procedures always will protect us from deliberate, reckless or inadvertent acts of our employees or third-party intermediaries that contravene our compliance policies or violate applicable laws. Our continued expansion, including in developing countries, could increase the risk of such violations in the future. Violations of these laws, or allegations of such violations, could disrupt our business and result in a material adverse impact on our business, financial condition and results of operations.

In 2015, we self-reported to the German prosecutor conduct with a potential nexus to Germany and continued to cooperate with government authorities in Germany in their review of the conduct that prompted our and the U.S. government investigations.

For further information, see note 25 of the notes to our consolidated financial statements included in this report.

Risks relating to our business activities and industry

If physicians and other referral sources cease referring patients to our health care service businesses and facilities or cease purchasing or prescribing our products, our revenues would decrease.

In providing services within our health care business, we depend upon patients choosing our health care facilities as the location for their care. Patients may select a facility based, in whole or in part, on the recommendation of their physician. Physicians and other clinicians typically consider a number of factors when recommending a particular dialysis facility, dialysis home program, pharmacy, physician practice, vascular surgery center, or cardiac catheterization center to an ESRD patient, including the quality of care, the competency of staff, convenient scheduling, and location and physical condition. Physicians may change their recommendations, which may result in the movement of new or existing patients to competing facilities, including facilities established by the physicians themselves. At most of our dialysis clinics and home programs, a relatively small number of physicians often account for the referral of all or a significant portion of the patient base. We have no ability to dictate these recommendations and referrals. If a significant number of physicians or other referral sources cease referring their patients to our facilities and home programs or stop purchasing or prescribing our dialysis products, this would reduce our health care revenue and could materially adversely affect our overall operations.

As a company with operations spanning around 150 countries, we face specific risks from our global operations.

We operate dialysis clinics in around 40 countries and sell a range of products and services to customers in around 150 countries. Our global operations are subject to a number of risks, including but not limited to the following:

| ● | the economic and political situation in certain countries or regions could deteriorate, become unstable, or lead to armed conflict, as exemplified by the Ukraine War; |

13

| ● | geopolitical factors could intensify fluctuations in exchange rates, currency devaluations, and/or material increases in interest rates (for example, as a reaction from central banks to high inflation), any of which could adversely affect profitability and all of which have been heightened by the Ukraine War; |

| ● | sovereign rating agency downgrades coupled with an economic downturn in various regions or as a result of geopolitical conflicts in certain regions (for example, the Ukraine War) could result in impairment of our goodwill, investments or other assets due to decreases in the recoverable amount of those assets relative to their book value; |

| ● | we could face difficulties in enforcing and collecting accounts receivable under some countries’ legal systems; |

| ● | local regulations could restrict our ability to obtain a direct ownership interest in dialysis clinics or other operations; |

| ● | some countries or economic unions may impose charges or restrictions, such as local content requirements, which restrict the importation of our products or give local manufacturers an advantage in tenders or provide large discounts to providers for certain purchases of our products; |

| ● | potential increases in tariffs and trade barriers could occur affecting both the sale of our products and importation of products and product components, including upon any withdrawal by the U.S. or other countries from multilateral trade agreements, or the imposition of sanctions, retaliatory tariffs and other countermeasures in the wake of trade disputes and geopolitical conflicts and wars in certain regions (for example the Ukraine War); |

| ● | we could experience transportation delays or interruptions or higher energy costs or energy shortages; |

| ● | growth and expansion into emerging markets could cause us difficulty due to greater regulatory barriers than in the U.S. or Western Europe, the necessity of adapting to new regulatory systems, and problems related to entering new markets with different economic, social, legal and political systems and conditions; and |

| ● | we may not prevail in competitive contract tenders. |

Any one or more of these or other factors relevant to global operations could increase our costs, reduce our revenues, or disrupt our operations, with possible material adverse impact on our business and financial condition.

Certain countries in which we market, manufacture or sell our products do not have laws which protect our intellectual property to the same degree as those in the U.S. or elsewhere and our competitors may gain market position by designing products that infringe upon our intellectual property rights. An inability to protect our intellectual property in these countries could have an adverse effect on our business, results of operations and financial condition.

14

We conduct humanitarian-related business and provide life-sustaining health care products and services directly or indirectly in sanctioned countries, such as Russia, Belarus, Iran and Syria. We believe our humanitarian-related business is permitted by applicable sanctions regimes (or, in some cases is excluded from such regimes), and in light of the humanitarian nature of our products and services and the patient communities that benefit from our products, we expect to continue such activities, provided they continue to be permissible under or excluded from applicable export controls and economic sanctions. Life-sustaining health care products are usually not subject to trade sanctions/export controls. However, as a result of the escalation of EU, U.S. and other countries’ trade sanctions targeting Russia and Belarus, certain spare parts and components for our products fall under product categories subject to restrictions. Sanctions programs often, but do not always, provide for certain exemptions or availability of licensure for medical or pharmaceutical purposes. Furthermore, product registration procedures may be affected in case technology/technical information on products or components to be submitted in such procedures is or becomes subject to export or transfer restrictions for a relevant country and in case relevant licenses cannot be obtained, which ultimately may also have an impact on marketability of affected products. At this time, we expect that such risk would mostly be limited to product registration procedures in Russia and Belarus as a result of the escalation of EU, U.S. and other countries’ trade sanctions targeting Russia and Belarus, but it may also affect Eurasian Economic Union (EAEU) product registration procedures in other EAEU member states in case these involve an information exchange with Russian/Belarusian authorities of restricted technology/technical information and in case relevant licenses cannot be obtained. A violation of applicable economic sanctions or export controls laws and regulations could subject us to enforcement actions. Possible enforcement actions vary between jurisdictions and depend on the factual circumstances of the given violation, but could include criminal penalties, imprisonment of responsible individuals, administrative or civil penalties, restricted access to certain markets and reputational harm, among others. Our internal policies and procedures may not protect us from deliberate, reckless or inadvertent acts of our employees or agents that contravene our compliance policies or violate applicable laws.

If we fail to estimate, price for and manage medical costs in an effective manner, the profitability of our value and risk-based care programs could decline and could materially and adversely affect our results of operations, financial position and cash flows.

Through our value and risk-based care programs, we assume the risk of both medical and administrative costs for certain patients in return for fixed periodic payments or potential reimbursement based on our achievement against set benchmark targets from governmental and commercial insurers. Specifically in the U.S., our participation in various value and risk-based care programs includes the CMS CKCC model and capitation, risk-based or shared savings agreements with commercial insurers in which FMCH receives fixed periodic payments against set benchmark targets to cover all or a defined portion of the medical costs of a defined population of patients. For information on the value-based programs in which we participate, see Item 4B, “Information on the Company — Business overview — Other health care services — Value and risk-based care programs.”

Our profitability in our value-based agreements and risk products depends in part upon our ability to negotiate favorable financial terms, to manage a patient’s care, to collaborate with our payor partners, to coordinate with other health care providers, to accurately document patients’ health conditions for risk adjustment, and to find cost efficient, medically appropriate sites of service for our patients. Any failure to do so would limit our ability to improve the quality of patient care and health outcomes and to reduce medically unnecessary costs, which could lead to poorer performance under value and risk-based care programs.

The reserves that we establish in connection with the operation of our value and risk-based care programs are based upon assumptions and judgments concerning a number of factors, including trends in health care costs, expenses, patient hospitalization rates and other factors. To the extent the actual claims experience is less favorable than estimated based on our underlying assumptions, our incurred losses would increase, and future earnings could be adversely affected.

CMS relied on authority granted by the ACA to implement the CKCC model and seeks to deliver better health outcomes for ESRD patients while lowering CMS’ costs. Efforts to repeal or replace the ACA, while unsuccessful to date, continue. For further information, see “We operate in a highly regulated industry such that the potential for legislative reform provides uncertainty and potential threats to our operating models and results” and Item 4B, “Information on the Company — Business Overview — Regulatory and Legal Matters — Reimbursement — Executive order-based models.”

Our sales and earnings growth depends, in part, on our ability to develop and expand our core kidney care business, efficiently manage costs and execute our portfolio optimization plan to exit non-core and dilutive assets, as well as realize anticipated cost savings within our expected timeframe.

The health care industry experiences continuing consolidation, particularly among health care providers, as well as pressure on reimbursement and increasing costs, which requires us to identify both growth opportunities and efficiencies in the way we operate. Continuing consolidation in our industry could adversely affect our ability to find suitable acquisition targets and to increase future growth and product sales.

15