UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO

RULE 13a-16 OR 15d-16 UNDER THE

SECURITIES EXCHANGE ACT OF 1934

For the month of April, 2024

Commission File Number 001-13422

AGNICO EAGLE MINES LIMITED

(Translation of registrant’s name into English)

145 King Street East, Suite 400, Toronto, Ontario M5C 2Y7

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-For Form 40-F. Form 20-F ¨ Form 40-F x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101 (b)(1): ¨

Note: Regulation S-T Rule 101 (b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101 (b)(7): ¨

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934. Yes ¨ No x

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82- .

EXHIBITS

| Exhibit No. | Exhibit Description |

| 99.1 | Press Release dated April 25, 2024 announcing the Corporation’s first quarter results |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| AGNICO EAGLE MINES LIMITED | ||

| (Registrant) | ||

| Date: 04/29/2024 | By: | /s/ Chris Vollmershausen |

| Chris Vollmershausen | ||

| Executive Vice-President, Legal, General Counsel & Corporate Secretary | ||

Exhibit 99.1

| Stock Symbol: | AEM (NYSE and TSX) |

| For further information: | Investor Relations |

| (416) 947-1212 |

(All amounts expressed in U.S. dollars unless otherwise noted)

AGNICO EAGLE REPORTS FIRST QUARTER 2024 RESULTS – STRONG QUARTERLY GOLD PRODUCTION AND COST PERFORMANCE DRIVE RECORD QUARTERLY FREE CASH FLOW; 2023 SUSTAINABILITY REPORT RELEASED

Toronto (April 25, 2024) – Agnico Eagle Mines Limited (NYSE:AEM, TSX:AEM) ("Agnico Eagle" or the "Company") today reported financial and operating results for the first quarter of 2024.

"Building on a very strong close to 2023, we are reporting our second consecutive quarter of record operating margins and record free cash flow, on the back of solid operational and cost performance. With this strong start to the year, we are well positioned to achieve our production and cost guidance for 2024," said Ammar Al-Joundi, Agnico Eagle's President and Chief Executive Officer. "During the quarter, we continued to advance our key value drivers and project pipeline, and our exploration program yielded significant results at Hope Bay, Canadian Malartic and Detour Lake. We strengthened our balance sheet in the quarter and our focus remains on capital discipline and cost control, while investing in our projects pipeline and providing returns to shareholders," added Mr. Al-Joundi.

First quarter 2024 highlights:

| · | Strong quarterly gold production – Payable gold production1 in the first quarter of 2024 was 878,652 ounces at production costs per ounce of $892, total cash costs per ounce2 of $901 and all-in sustaining costs ("AISC") per ounce3 of $1,190. Gold production in the first quarter of 2024 was led by record quarterly production at Canadian Malartic and strong production from Macassa and the Company's Nunavut operations |

1 Payable production of a mineral means the quantity of a mineral produced during a period contained in products that have been or will be sold by the Company whether such products are shipped during the period or held as inventory at the end of the period.

2 Total cash costs per ounce is a non-GAAP ratio that is not a standardized financial measure under IFRS and in this news release, unless otherwise specified, is reported on (i) a per ounce of gold production basis, and (ii) a by-product basis. For a description of the composition and usefulness of this non-GAAP measure and a reconciliation of total cash costs to production costs on both a byproduct and a co-product basis, see "Reconciliation of Non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

3 AISC per ounce is a non-GAAP ratio that is not a standardized financial measure under the IFRS and in this news release, unless otherwise specified, is reported on (i) a per ounce of gold production basis, and (ii) a by-product basis. For a description of the composition and usefulness of this non-GAAP measure and a reconciliation to production costs and for all-in sustaining costs on both a by-product and co-product basis, see "Reconciliation of Non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

| · | Record quarterly cash provided by operating activities and free cash flow – The Company reported quarterly net income of $347.2 million or $0.70 per share and adjusted net income4 of $377.5 million or $0.76 per share for the first quarter of 2024. Cash provided by operating activities was $1.57 per share ($1.56 per share before changes in non-cash working capital balances5) and free cash flow5 was $0.79 per share ($0.78 per share before changes in non-cash working capital balances5) |

| · | Strengthening investment grade balance sheet – In the first quarter of 2024, the Company increased its cash position by $186 million and reduced net debt. In addition, in March 2024, Moody's upgraded the Company's long-term issuer rating to Baa1 from Baa2 |

| · | 2024 gold production, cost and capital expenditure guidance reiterated – Expected payable gold production remains unchanged at approximately 3.35 to 3.55 million ounces in 2024, with total cash costs per ounce and AISC per ounce in 2024 unchanged at $875 to $925 and $1,200 to $1,250, respectively. Total capital expenditures (excluding capitalized exploration) for 2024 are still estimated to be between $1.6 billion to $1.7 billion |

| · | Update on key value drivers and pipeline projects |

| · | Construction of Odyssey mine at the Canadian Malartic complex progressing well – In the first quarter of 2024, ramp development continued to exceed target, reaching the first production level of East Gouldie in February 2024 and a depth of 765 metres as at March 31, 2024. Shaft sinking improved during the quarter, with an average sinking rate of 2.4 metres per day (including pre-sinking). The temporary loading pocket, previously planned at level 102, will now be built at Level 64, which is expected to provide hoisting capacity by mid-2025, six months earlier than previously planned and will provide added development and production flexibility. Surface construction is progressing as planned, with a focus on the main hoist building, phase two of the paste plant and the operational complex |

| · | Positive exploration results at Odyssey mine – Exploration drilling continues to return positive results to the east of the East Gouldie mineral resources, including 4.5 g/t gold over 30.0 metres at 1,162 metres depth and 1,060 metres east of current mineral reserves; and 3.1 g/t gold over 32.8 metres at 1,556 metres depth and 420 metres east of the lower portion of the East Gouldie mineral reserves |

| · | Detour Lake – The mill delivered a solid performance with a throughput rate of 71,451 tonnes per day ("tpd"), which was the highest for a first quarter period, demonstrating continued mill improvement year-over-year. The Company continues to evaluate underground mining scenarios at Detour Lake and expects to provide an update on the project, mill optimization efforts and ongoing exploration results in the second quarter of 2024. Exploration during the first quarter included infill drilling in the shallow portion of the West Pit Extension, with highlight intercepts of 3.9 g/t gold over 25.4 metres at 369 metres depth and 5.4 g/t gold over 16.6 metres at 307 metres depth, both at underground depths near the proposed exploration ramp |

| · | Hope Bay – Exploration drilling during the first quarter totalled 30,600 metres and returned strong results in the Patch 7 area of the Madrid deposit, including 20.8 g/t gold over 17.7 metres at 461 metres depth and 14.1 g/t gold over 16.4 metres at 480 metres depth in a cluster of high-grade intersections approximately 200 metres north of Patch 7 mineral resources |

4 Adjusted net income and adjusted net income per share are non-GAAP measures or ratios that are not standardized financial measures under IFRS. For a description of the composition and usefulness of these non-GAAP measures and a reconciliation to net income see "Reconciliation of Non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

5 Cash provided by operating activities before changes in non-cash working capital balances, free cash flow and free cash flow before changes in non-cash working capital balances are non-GAAP measures or ratios that are not standardized financial measures under IFRS. For a description of the composition and usefulness of these non-GAAP measures and a reconciliation to cash provided by operating activities see "Reconciliation of Non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

| · | 2023 Sustainability Report published – The Company continues to demonstrate its commitment to ESG performance. In 2023, the Company recorded its best safety performance in its 66-year history and maintained or improved performance across other key ESG indicators, including efficient management of water resources and increased local employment. In addition, efforts continued in 2023 to maintain a climate resilient business and meet our interim reduction target of 30% of absolute Scope 1 and 2 emissions by 2030 |

| · | Continued focus on shareholder returns – In the first quarter of 2024, a quarterly dividend of $0.40 per share has been declared and the Company repurchased 375,000 common shares for $19.9 million through its normal course issuer bid ("NCIB") |

First Quarter 2024 Results Conference Call and Webcast Tomorrow

Agnico Eagle's senior management will host a conference call on Friday, April 26, 2024 at 8:30 AM (E.D.T.) to discuss the Company's financial and operating results.

Via Webcast:

A live audio webcast of the conference call will be available on the Company's website www.agnicoeagle.com.

Via URL Entry:

To join the conference call without operator assistance, you may register and enter your phone number at https://emportal.ink/3Rvps04 to receive an instant automated call back. You can also dial direct to be entered to the call by an Operator (see "Via Telephone" details below).

Via Telephone:

For those preferring to listen by telephone, please dial 416.764.8659 or toll-free 1.888.664.6392. To ensure your participation, please call approximately five minutes prior to the scheduled start of the call.

Replay Archive:

Please dial 416.764.8677 or toll-free 1.888.390.0541, access code 505445#. The conference call replay will expire on May 26, 2024.

The webcast, along with presentation slides, will be archived for 180 days on the Company's website.

Annual Meeting

The Company will host its Annual and Special Meeting of Shareholders (the "AGM") on Friday, April 26, 2024 at 11:00 AM (E.D.T). During the AGM, management will provide an overview of the Company's activities.

The AGM will be held in person at the Arcadian Court, 401 Bay Street, Simpson Tower, 8th Floor, Toronto, Ontario, M5H 2Y4 and online at: https://meetnow.global/MFJPVMP.

For details explaining how to attend, communicate and vote virtually at the AGM please see the Company's Management Information Circular dated March 22, 2024, filed under the Company's profile on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov. Shareholders who have questions about voting their shares or attending the AGM may contact Investor Relations by phone at 416.947.1212, by toll-free phone at 1.888.822.6714 or by email at investor.relations@agnicoeagle.com or may contact the Company's strategic shareholder advisor and proxy solicitation agent, Laurel Hill Advisory Group, by phone at 1.877.452.7184 (toll free in North America), at 1.416.304.0211 (for collect calls outside of North America) or by e-mail at assistance@laurelhill.com.

First Quarter 2024 Production and Costs

Production and Cost Results Summary*

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Gold production (ounces) | 878,652 | 812,813 | ||||||

| Gold sales (ounces) | 879,063 | 787,558 | ||||||

| Production costs per ounce | $ | 892 | $ | 804 | ||||

| Total cash costs per ounce | $ | 901 | $ | 832 | ||||

| AISC per ounce | $ | 1,190 | $ | 1,125 | ||||

* Reflects Agnico Eagle's 50% interest in the Canadian Malartic complex up to and including March 30, 2023 and 100% interest thereafter.

Gold Production

Gold production increased in the first quarter of 2024 when compared to the prior-year period primarily due to additional production from the acquisition of the remaining 50% of the Canadian Malartic complex following the closing of the acquisition of the Canadian assets of Yamana Gold Inc. (the "Yamana Transaction") and higher production from the Meadowbank complex, partially offset by lower production at the Fosterville mine.

Production Costs per Ounce

Production costs per ounce increased in the first quarter of 2024 when compared to the prior-year period primarily due to higher production costs at most mine sites resulting from inflation, combined with the impact of the timing of inventory sales and lower production at the LaRonde complex, a lower build-up of ore stockpiles, lower gold production at the Detour Lake mine and the timing of inventory sales at the Meliadine mine, partially offset by higher gold production and lower production costs at the Meadowbank complex.

Total Cash Costs per Ounce

Total cash costs per ounce increased in the first quarter of 2024 when compared to the prior-year period primarily due to higher operating costs at most mine sites resulting from inflation, higher royalties arising from higher gold prices and gold production, and the impact of lower gold grades at the LaRonde complex, the Detour Lake mine and the Fosterville mine due to mining sequence, partially offset by higher gold production and lower production costs at the Meadowbank complex.

AISC per Ounce

AISC per ounce increased in the first quarter of 2024 when compared to the prior-year period due to higher total cash costs per ounce and higher sustaining capital expenditures during the period associated with the acquisition of the remaining 50% of the Canadian Malartic complex, partially offset by higher production.

AISC per ounce in the first quarter of 2024 was lower than expected primarily as a result of the deferral of certain sustaining capital expenditures at the Detour Lake mine to later in 2024. AISC per ounce is expected to be higher in the remainder 2024 as the Company still expects company-wide AISC per ounce for the full year 2024 to be in the range of $1,200 to $1,250 per ounce.

First Quarter 2024 Financial Results

Financial Results Summary

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Realized gold price ($/ounce)6 | $ | 2,062 | $ | 1,892 | ||||

| Net income ($ millions)7 | $ | 347.2 | $ | 1,816.9 | ||||

| Adjusted net income ($ millions) | $ | 377.5 | $ | 271.3 | ||||

| EBITDA ($ millions)8 | $ | 882.5 | $ | 2,272.9 | ||||

| Adjusted EBITDA ($ millions)8 | $ | 929.3 | $ | 740.4 | ||||

| Cash provided by operating activities ($ millions) | $ | 783.2 | $ | 649.6 | ||||

| Cash provided by operating activities before changes in non-cash working capital balances ($ millions) | $ | 777.1 | $ | 608.8 | ||||

| Capital expenditures9 | $ | 372.0 | $ | 341.7 | ||||

| Free cash flow ($ millions) | $ | 395.6 | $ | 264.7 | ||||

| Free cash flow before changes in non-cash working capital balances ($ millions) | $ | 389.5 | $ | 223.9 | ||||

| Net income per share (basic) | $ | 0.70 | $ | 3.87 | ||||

| Adjusted net income per share (basic) | $ | 0.76 | $ | 0.58 | ||||

| Cash provided by operating activities per share (basic) | $ | 1.57 | $ | 1.39 | ||||

| Cash provided by operating activities before changes in non-cash working capital balances per share (basic) | $ | 1.56 | $ | 1.30 | ||||

| Free cash flow per share (basic) | $ | 0.79 | $ | 0.56 | ||||

| Free cash flow before changes in non-cash working capital balances per share (basic) | $ | 0.78 | $ | 0.48 | ||||

Net Income

In the first quarter of 2024, net income was $347.2 million ($0.70 per share). This result includes the following items (net of tax): derivative losses on financial instruments of $29.2 million ($0.05 per share), net asset disposal losses of $2.6 million ($0.01 per share), foreign exchange gains of $4.5 million ($0.01 per share), and foreign currency translation losses on deferred tax liabilities and various other adjustments totaling $3.0 million ($0.01 per share).

Excluding the above items results in adjusted net income of $377.5 million or $0.76 per share for the first quarter of 2024. Included in the first quarter of 2024 net income, and not adjusted above, is a non-cash stock option expense of $4.2 million ($0.01 per share).

Net income of $347.2 million in the first quarter of 2024 decreased when compared to net income of $1,816.9 million in the prior-year period primarily due to the recognition of a $1,543.4 million remeasurement gain on the 50% of the Canadian Malartic complex that the Company owned prior to the Yamana Transaction in the prior-year period, partially offset by higher revenues from higher gold sales and higher realized gold prices in the current period.

6 Realized gold price is calculated as gold revenues from mining operations divided by the number of ounces sold.

7 For the first quarter of 2023, includes a $1.5 billion revaluation gain on the 50% interest the Company owned in the Canadian Malartic complex prior to the Yamana Transaction on March 31, 2023.

8 "EBITDA" means earnings before interest, taxes, depreciation, and amortization. EBITDA and adjusted EBITDA are non-GAAP measures or ratios that are not standardized financial measures under IFRS. For a description of the composition and usefulness of these non-GAAP measures and a reconciliation to net income see "Reconciliation of Non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

9 Includes capitalized exploration

Adjusted EBITDA

Adjusted EBITDA increased in the first quarter of 2024 when compared to the prior-year period primarily due to record operating margins10 from higher gold sales and higher realized gold prices, partially offset by higher production costs.

Cash Provided by Operating Activities

Cash provided by operating activities and cash provided by operating activities before changes in non-cash working capital balances both increased in the first quarter of 2024 when compared to the prior-year period primarily due to higher revenues from higher gold sales and higher realized gold prices, partially offset by higher production costs.

Free Cash Flow Before Changes in Non-Cash Working Capital Balances

Free cash flow before changes in non-cash working capital balances was a record in the first quarter of 2024 and increased when compared to the prior-year period primarily due to the reasons described above in respect of cash provided by operating activities, partially offset by higher capital expenditures.

10 Operating margin is a non-GAAP measure that is not a standardized measure under IFRS. For a description of the composition and usefulness of this non-GAAP measure and a reconciliation to net income see "Summary of Operations Key Performance Indicators" and "Note Regarding Certain Measures of Performance", respectively, below.

Capital Expenditures

The capital expenditures in the first quarter of 2024 were lower than forecast primarily due to the deferral of certain sustaining capital expenditures at Detour Lake mine to later in 2024. Total expected capital expenditures (including capitalized exploration) remain in line with guidance for the full year 2024.

The following table sets out a summary of capital expenditures (including sustaining capital expenditures11 and development capital expenditures11) and capitalized exploration in the first quarter of 2024.

Summary of Capital Expenditures

($ thousands)

| Capital Expenditures* | Capitalized Exploration | |||||||

| Three Months Ended | Three Months Ended | |||||||

| Mar 31, 2024 | Mar 31, 2024 | |||||||

| Sustaining Capital Expenditures | ||||||||

| LaRonde complex | $ | 22,924 | $ | 319 | ||||

| Canadian Malartic complex | 27,045 | — | ||||||

| Goldex complex | 12,053 | 738 | ||||||

| Detour Lake mine | 49,638 | — | ||||||

| Macassa mine | 10,131 | 400 | ||||||

| Meliadine mine | 17,865 | 1,337 | ||||||

| Meadowbank complex | 19,942 | — | ||||||

| Fosterville mine | 5,483 | — | ||||||

| Kittila mine | 16,064 | 450 | ||||||

| Pinos Altos mine | 4,989 | 303 | ||||||

| La India mine | 22 | — | ||||||

| Other | 329 | 575 | ||||||

| Total Sustaining Capital Expenditures | $ | 186,485 | $ | 4,122 | ||||

| Development Capital Expenditures | ||||||||

| LaRonde complex | $ | 24,089 | $ | — | ||||

| Canadian Malartic complex | 36,005 | 1,318 | ||||||

| Goldex complex | 4,131 | — | ||||||

| Detour Lake mine | 37,759 | 7,552 | ||||||

| Macassa mine | 12,146 | 8,318 | ||||||

| Meliadine mine | 18,245 | 4,086 | ||||||

| Meadowbank complex | (27 | ) | — | |||||

| Fosterville mine | 9,428 | 3,624 | ||||||

| Kittila mine | 908 | 2,131 | ||||||

| Pinos Altos mine | 646 | 4 | ||||||

| San Nicolás project | 5,371 | — | ||||||

| Other | 5,677 | — | ||||||

| Total Development Capital Expenditures | $ | 154,378 | $ | 27,033 | ||||

| Total Capital Expenditures | $ | 340,863 | $ | 31,155 | ||||

* Excludes capitalized exploration

11 Sustaining capital expenditures and development capital expenditures are non-GAAP measures that are not standardized financial measures under IFRS. For a discussion of the composition and usefulness of these non-GAAP measures and a reconciliation to additions to property, plant and mine development per the consolidated statements of cash flows, see "Reconciliation of Non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

2024 Guidance Reiterated

The Company is well positioned to achieve its 2024 gold production guidance of approximately 3.35 to 3.55 million ounces, its 2024 total cash costs per ounce guidance of $875 to $925 and its 2024 AISC per ounce guidance of $1,200 to $1,250.

Total expected capital expenditures (excluding capitalized exploration) for 2024 are still estimated to be between $1.6 billion to $1.7 billion.

Strong Cash Flow Generation Enhances Investment Grade Balance Sheet Alongside Continued Commitment to Shareholder Returns

As at March 31, 2024, the Company's long-term debt was $1,841.0 million, consistent with the prior quarter. No amounts were outstanding under the Company's unsecured revolving bank credit facility as at March 31, 2024.

Cash and cash equivalents increased by $186.0 million when compared to the prior quarter primarily due to higher cash provided by operating activities as a result of higher revenues from higher gold sales and higher realized gold prices, and lower capital expenditures.

The following table sets out the calculation of net debt12, which decreased by $188.1 million when compared to the prior quarter primarily as a result of higher cash and cash equivalents.

Net Debt Summary

($ millions)

| As at | As at | |||||||

| Mar 31, 2024 | Dec 31, 2023 | |||||||

| Current portion of long-term debt | $ | 100.0 | $ | 100.0 | ||||

| Non-current portion of long-term debt | 1,741.0 | 1,743.1 | ||||||

| Long-term debt | $ | 1,841.0 | $ | 1,843.1 | ||||

| Less: cash and cash equivalents | (524.6 | ) | (338.6 | ) | ||||

| Net debt | $ | 1,316.4 | $ | 1,504.5 | ||||

In order to maintain financial flexibility, and consistent with past practice, the Company intends to file a new base shelf prospectus in the second quarter of 2024. The Company has no present intention to offer securities pursuant to the new base shelf prospectus. The notice set out in this paragraph does not constitute an offer of any securities for sale or an offer to sell or the solicitation of an offer to buy any securities.

Credit Facility and Credit Rating

As at March 31, 2024, available liquidity under the Company's new unsecured revolving bank credit facility (as further described below) was approximately $2.0 billion, not including the uncommitted $1.0 billion accordion feature.

On February 12, 2024, the Company replaced its $1.2 billion unsecured revolving bank credit facility with a new $2.0 billion unsecured revolving bank credit facility, including an increased uncommitted accordion feature of $1.0 billion, and having a maturity date of February 12, 2029. In addition to the increased size and extended term of the new unsecured revolving bank credit facility, the new credit facility includes enhancements to its terms and conditions more in line with the Company's credit profile and improves its financial flexibility and strengthens its financial position. At the same time, the Company's $600.0 million term loan was amended to align the terms and conditions with the new unsecured revolving credit facility.

12 Net debt is a non-GAAP measure that is not a standardized financial measure under IFRS. For a description of the composition and usefulness of this non-GAAP measure and a reconciliation to long-term debt, see "Reconciliation of non-GAAP Financial Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

On March 28, 2024, Moody’s Ratings upgraded the Company’s investment grade credit rating to Baa1 with a Stable Outlook recognizing the Company’s financial strength and stability. In addition, Fitch has provided an investment grade credit rating of BBB+ (Stable Outlook). These ratings underscore the Company's strong business and credit profile, with low leverage and conservative financial policies, and recognize the benefits of the Company's size and scale and operations in favourable mining jurisdictions. The Company remains committed to maintaining a strong financial position and an investment grade balance sheet.

Hedges

Approximately 72% of the Company's remaining estimated Canadian dollar exposure for 2024 is hedged at an average floor price providing protection above 1.34 C$/US$. Approximately 25% of the Company's remaining estimated Euro exposure for 2024 is hedged at an average floor price providing protection below 1.10 US$/EUR. Approximately 69% of the Company's remaining Australian dollar exposure for 2024 is hedged at an average floor price providing protection above 1.46 A$/US$. The Company does not currently hedge its exposure to the Mexican peso. The Company's full year 2024 cost guidance is based on assumed exchange rates of 1.34 C$/US$, 1.10 US$/EUR, 1.45 A$/US$ and 16.50 MXP/US$.

Including the diesel purchased for the Company's Nunavut operations that was delivered in the 2023 sealift, approximately 46% of the Company's remaining estimated diesel exposure for 2024 is hedged at an average benchmark price of $0.72 per litre (excluding transportation and taxes), which is expected to reduce the Company's exposure to diesel price volatility in 2024. The Company's full year 2024 cost guidance is based on an assumed diesel benchmark price of $0.80 per litre (excluding transportation and taxes).

The Company will continue to monitor market conditions and anticipates continuing to opportunistically add to its operating currency and diesel hedges to strategically support its key input costs. Hedging positions are not factored into 2024 or future guidance.

Shareholder Returns

Dividend Record and Payment Dates for the Second Quarter of 2024

Agnico Eagle's Board of Directors has declared a quarterly cash dividend of $0.40 per common share, payable on June 14, 2024 to shareholders of record as of May 31, 2024. Agnico Eagle has declared a cash dividend every year since 1983.

Expected Dividend Record and Payment Dates for the 2024 Fiscal Year

| Record Date | Payment Date |

| March 1, 2024* | March 15, 2024* |

| May 31, 2024** | June 14, 2024** |

| August 30, 2024 | September 16, 2024 |

| November 29, 2024 | December 16, 2024 |

*Paid

**Declared

Normal Course Issuer Bid

In addition to the quarterly dividend, the Company believes that its NCIB provides a flexible and complementary tool as part of the Company's overall capital allocation program and that it generates value for shareholders. In the first quarter of 2024, the Company repurchased 375,000 common shares for an aggregate of $19.9 million under the NCIB. The NCIB permits the Company to purchase up to $500.0 million of its common shares subject to a maximum of 5% of its issued and outstanding common shares. Purchases under the NCIB may continue for up to one year from the commencement day on May 4, 2023.

The Company intends to seek approval from the TSX to renew the NCIB for another year on substantially the same terms. Additional details will be provided at the time of the renewal.

Dividend Reinvestment Plan

See the following link for information on the Company's dividend reinvestment plan: Dividend Reinvestment Plan

International Dividend Currency Exchange

For information on the Company's international dividend currency exchange program, please contact Computershare Trust Company of Canada by phone at 1.800.564.6253 or online at www.investorcentre.com or www.computershare.com/investor.

2023 Sustainability Report Illustrates Continued Commitment to Strong ESG Performance and Transparency

On April 25, 2024, the Company released its 2023 Sustainability Report (the "Report") which provides an update on the Company's strategy, practices and risk management approach in the key areas of health and safety, ESG and the sustainability performance of mining operations.

This marks the 15th year that the Company has produced a detailed account of its ESG performance. The Report has been prepared in accordance with the Global Reporting Initiative (GRI) Standards, is aligned with the Task Force on Climate Related Financial Disclosures (TCFD) and includes additional mining industry specific indicators from the Sustainability Accounting Standards Board (SASB) Metals and Mining disclosures and metrics.

The theme of the Report, "Global Approach, Regional Focus", reflects the Company's commitment that, as the Company expands and evolves as an organization, it remains deeply rooted in and committed to the regions in which it operates.

The Company aims to be a partner of choice within the mining industry by:

| · | Having strong ESG performance – In 2023, the Company achieved the best safety performance in its over 66-year history and maintained or improved performance across many other key ESG indicators, including zero significant environmental incidents, the efficient management of water (reducing freshwater usage per ounce of gold produced) and increased local employment and procurement |

| · | Addressing climate change and working towards net-zero by 2050 – In 2023, the Company's decarbonization efforts focused on energy efficiency, technology transition and increased renewable energy. In accordance with best practices, the Company's greenhouse gas emissions (GHG) were calculated to account for the acquisition of Canadian Malartic. The Company continues to be a low intensity gold producer and its GHG intensity per ounce of gold for all its operations are below the industry average |

| · | Being a great place to work – The Company is committed to providing a safe, diverse, inclusive and collaborative workplace for its people. In 2023, 66% of our workforce were local residents |

| · | Investing in communities – Being a trusted and valued member of the communities associated with the Company's operations remains a fundamental principle and priority for Agnico Eagle. In 2023, the Company's donations and sponsorships to local organizations in the regions it operates were approximately $16 million and the Company spent approximately $1.9 billion on locally-sourced goods and services, approximately $1 billion of which went to Indigenous businesses |

| · | Mining responsibly – The Company is committed to being a responsible miner and contributing to the sustainable development of the regions in which we operate. The Company is a long-time supporter of recognized international sustainability frameworks, including Towards Sustainable Mining (TSM), Responsible Gold Mining Principles (RGMP), the Voluntary Principles on Security and Human Rights (VPSHRs), the Conflict-Free Gold Standard and the Task Force on Climate-related Financial Disclosures |

The Company's 2023 Sustainability Report can be accessed here.

Update on Key Value Drivers and Pipeline Projects

Highlights on key value drivers (Odyssey project, Detour Lake mine and optimization of assets and infrastructure in the Abitibi region of Quebec) and the Hope Bay and San Nicolás projects are set out below. Details on certain mine expansion projects (Meliadine Phase 2 expansion and Amaruq underground) are set out in the applicable operational sections of this news release.

Odyssey Project

In the first quarter of 2024, underground development continued to exceed targets. At the main ramp, the Company achieved a lateral development rate of 167 metres per month, exceeding the target rate of 140 metres per month. The ramp reached the first production level of East Gouldie (level 75) in February 2024, ahead of schedule, and, as at March 31, 2023, the ramp was at a depth of 765 metres.

In terms of total underground development, a record 1,259 metres was achieved at the Odyssey project in March 2024. Equipment remotely tele-operated from the surface (scoops, jumbos and cable bolters) continued to drive overall development productivity gains. Autonomous trucks, tested in the first quarter of 2024, are expected to further support the development and production performance. The Company continued to develop the main ventilation system at the Odyssey project, with the completion of the future exhaust raise between levels 36 and 54.

Shaft sinking activities were more productive during the quarter. In the first quarter of 2024, the average conventional sinking rate was 1.8 metres per day, a 64% improvement when compared to the fourth quarter of 2023, and the overall sinking rate was 2.4 metres per day when factoring the pre-sinking of the shaft between levels 26 and 36. The second pre-sink leg of the shaft was extended by 20 metres and will now be between levels 54 and 66. The pre-sinking of this leg is expected to be completed in the second quarter of 2024. As at March 31, 2024, the shaft had reached a depth of approximately 452 metres. The Company still expects to complete excavation of the shaft in 2027.

The temporary loading station, previously planned at level 102, will now be built at level 64. The service hoist that will be connected to the temporary loading pocket will support the transportation of people, materials and waste to and from Level 64. The change in design is expected to provide several advantages: (i) the loading station will be developed and built from the ramp rather than from the shaft, which is expected to simplify and accelerate the construction and lower the costs; (ii) the temporary loading station and service hoist are now expected to be operational by mid-2025, six months earlier than previously planned; and (iii) the hoisting capacity is expected to increase from 2,000 tpd to 3,500 tpd as a result of the shorter hoisting cycle, which is expected to reduce the haul truck requirement in years 2025 to 2027. Level 64 is also where the ramps to the East Gouldie, Odyssey North and Odyssey South deposits are planned to connect.

Surface construction progressed as planned and on budget in the first quarter of 2024. Key areas of focus included the main hoist building, phase 2 of the paste plant to expand capacity to 20,000 tpd and the operational complex. At the main hoist building, the installation of the interior architecture, the HVAC and main electrical systems is ongoing. The mechanical and electrical components for the service hoists were delivered and the hoist concrete foundation was completed in the first quarter of 2024. The conceptual engineering for the paste plant expansion is expected to be completed in the second quarter of 2024. The bids for the construction of the operational complex were received and the selected turnkey contractor is expected to mobilize on site in the third quarter of 2024. The construction of the operational complex is expected to be completed by the end of 2025.

Exploration drilling at the Odyssey mine totalled 29,395 metres during the first quarter of 2024 with 11 drill rigs in operation.

At the East Gouldie deposit, gold mineralization continued to be intersected outside of the current mineral resource envelope with highlight hole MEX23-309 returning 4.5 g/t gold over 30.0 metres at 1,162 metres depth, including 8.0 g/t gold over 6.5 metres at 1,156 metres depth, in an intersection located 1,060 metres east of current mineral reserves. In an intersection located 420 metres east of the lower portion of the East Gouldie mineral reserves, hole MEX23-310Z returned 3.1 g/t gold over 32.8 metres at 1,556 metres depth, including 6.5 g/t gold over 4.8 metres at 1,558 metres depth. In the western extension of the East Gouldie mineralized envelope, hole MEX23-304W intersected 3.3 g/t gold over 14.6 metres at 1,246 metres depth and approximately 240 metres west of the East Gouldie inferred mineral resources.

These holes demonstrate the potential to add inferred mineral resources laterally to the east and to the west at East Gouldie with further drilling into these extensions of mineralization.

Selected recent drill intercepts from the Odyssey mine are set out in the table and composite longitudinal section below.

| Drill hole | From (metres) |

To (metres) |

Depth of midpoint below surface (metres) |

Estimated true width (metres) |

Gold grade (g/t) (uncapped) |

Gold grade (g/t) (capped)* |

||||||||||||||||||

| MEX23-304W | 1,559.5 | 1,575.1 | 1,246 | 14.6 | 3.3 | 3.3 | ||||||||||||||||||

| MEX23-309 | 1,618.0 | 1,651.1 | 1,162 | 30.0 | 4.5 | 4.5 | ||||||||||||||||||

| including | 1,622.1 | 1,629.2 | 1,156 | 6.5 | 8.0 | 8.0 | ||||||||||||||||||

| MEX23-310Z | 1,837.0 | 1,871.9 | 1,556 | 32.8 | 3.1 | 3.1 | ||||||||||||||||||

| including | 1,854.5 | 1,860.3 | 1,558 | 4.8 | 6.5 | 6.5 | ||||||||||||||||||

*Results from East Gouldie use a capping factor of 20 g/t gold In the first quarter of 2024, the mill continued to show improved performance when compared to the prior year period.

[Odyssey mine – Composite Longitudinal Section]

Detour Lake Mine

The throughput rate was approximately 71,451 tpd, the highest for a first quarter period when mill operations can be affected by the colder temperatures. During the quarter, the process optimization initiatives remained focused on optimizing grinding efficiency and on improving the load balance between the SAG mills and the ball mills.

New instrumentation was installed in the SAG mill (known as "mill slicer"), which is expected to improve the control of the load balance between the SAG mills and the ball mills. These instruments are already in use at the Goldex and Canadian Malartic mills. Trials with new screen panel and grate configuration for the SAG discharge were carried out during the quarter and additional trials are planned in the second and third quarters of 2024. New liners for the secondary crushers were also tested during the quarter and yielded favourable results in terms of lifespan which should help reduce downtime at the secondary crushers. Further testing of these liners is planned in the second and third quarters of 2024. Other initiatives that are expected to improve mill throughput in 2024 include the installation of a ball mill discharge grizzly in one of the lines and the scalping screens.

The Company still expects the mill to reach a throughput rate of approximately 76,700 tpd (equivalent to an annualized rate of approximately 28 million tonnes per annum) by the end of 2024.

In the first quarter of 2024, the Company continued to advance an internal evaluation of underground mining scenarios and expects to provide an update on the project in the second quarter of 2024. With the update, the Company will present the proposed next steps to de-risk and optimize the project.

Exploration drilling at Detour Lake during the first quarter totalled 58,000 metres in the West Pit and West Pit Extension with a focus on infill drilling in the shallow portion of the West Pit Extension at underground depths immediately west of the West Pit mineral resources and near the potential exploration ramp for the Underground Project.

Recent highlights from infill drilling include: hole DLM23-818 returning 3.9 g/t gold over 25.4 metres at 369 metres depth, approximately 200 metres west of the West Pit mineral resource; hole DLM23-775 returning 5.4 g/t gold over 16.6 metres at 307 metres depth, approximately 350 metres west of the West Pit mineral resource; and hole DLM23-805 returning 3.4 g/t gold over 29.4 metres at 562 metres depth, approximately 750 metres west of the West Pit mineral resource.

Selected recent drill intercepts from the Detour Lake mine are set out in the table, plan map and composite longitudinal section below.

| Drill hole | From (metres) |

To (metres) |

Depth of midpoint below surface (metres) |

Estimated true width (metres) |

Gold grade (g/t) (uncapped)* |

|||||||||||||||

| DLM23-775 | 343.0 | 361.0 | 307 | 16.6 | 5.4 | |||||||||||||||

| DLM24-805 | 645.0 | 678.0 | 562 | 29.4 | 3.4 | |||||||||||||||

| including | 660.8 | 664.1 | 563 | 2.9 | 15.1 | |||||||||||||||

| DLM24-818 | 405.9 | 436.2 | 369 | 25.4 | 3.9 | |||||||||||||||

| including | 432.0 | 436.2 | 380 | 3.5 | 15.3 | |||||||||||||||

*Results from Detour Lake are uncapped.

[Detour Lake – Plan Map and Composite Longitudinal Section]

Optimization of Other Assets and Infrastructure in the Abitibi Region

At Macassa, the development of the Amalgamated Kirkland ("AK") deposit is on track for initial production in the fourth quarter of 2024. At Upper Beaver, the Company is concluding a trade-off analysis on processing options and expects to provide an update of the project and next steps at mid-year 2024. At Wasamac, the Company continues to advance its stakeholder engagement initiatives, while assessing the optimal mining rate and processing options.

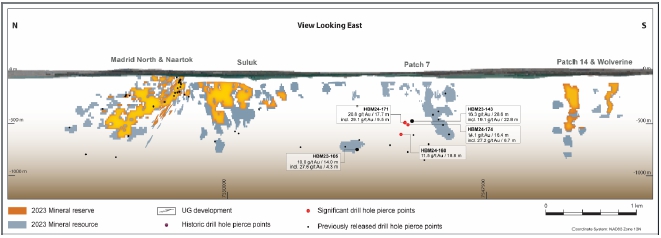

Hope Bay – Step-Out Drilling Continues to Extend Madrid's High-Grade Patch 7 Zone at Depth and Laterally

Exploration drilling at Hope Bay during the first quarter of 2024 totalled 30,600 metres and returned strong results in the Gap area between the Patch 7 and Suluk zones of the Madrid deposit.

Drilling targeted an area in Patch 7 between previously reported hole HBM23-143, which intersected 16.3 g/t gold over 28.6 metres at 445 metres depth (see the news release dated February 15, 2024, with the depth value revised in this new release), and hole HBM23-105, which intersected 10.0 g/t gold over 14.0 metres at 677 metres depth (see the news release dated July 26, 2023).

Recent highlights from this area include hole HBM24-171, which intersected 20.8 g/t gold over 17.7 metres at 461 metres depth, including 29.1 g/t gold over 9.5 metres at 466 metres depth, 90 metres north and down-dip from hole HBM23-143; and hole HBM-174, which intersected 14.1 g/t gold over 16.4 metres at 480 metres depth, including 27.2 g/t gold over 6.7 metres at 476 metres depth, 66 metres north and down-dip from hole HBM23-143.

At greater depth, hole HBM24-160 intersected 11.5 g/t gold over 18.8 metres at 573 metres depth, 165 metres north and down-dip from hole HBM23-143, demonstrating the continuity of potentially economic mineralization between holes HBM24-160 and HBM23-143 over at least 165 metres.

With this emerging new mineralized area so far showing grades and thicknesses greater than average for the Madrid deposit, the Company's objective is to intensify drilling in this area for the rest of the year as this area could have a positive impact on mining scenarios for potential project redevelopment.

Selected recent drill intercepts from the Madrid deposit are set out in the table and composite longitudinal section below.

| Drill hole | From (metres) |

To (metres) |

Depth of midpoint below surface (metres) |

Estimated true width (metres) |

Gold grade (g/t) (uncapped) |

Gold grade (g/t) (capped)* |

||||||||||||||||||

| HBM23-105** | 815.0 | 839.5 | 677 | 14.0 | 14.5 | 10.0 | ||||||||||||||||||

| including | 830.5 | 838.0 | 682 | 4.3 | 42.3 | 27.6 | ||||||||||||||||||

| HBM23-143** | 560.4 | 594.0 | 445 | 28.6 | 17.6 | 16.3 | ||||||||||||||||||

| including | 560.4 | 587.2 | 443 | 22.8 | 20.8 | 19.1 | ||||||||||||||||||

| HBM24-160 | 672.4 | 712.5 | 573 | 18.8 | 11.7 | 11.5 | ||||||||||||||||||

| HBM24-171 | 547.0 | 580.0 | 461 | 17.7 | 25.0 | 20.8 | ||||||||||||||||||

| including | 560.0 | 577.8 | 466 | 9.5 | 37.0 | 29.1 | ||||||||||||||||||

| HBM24-174 | 589.5 | 613.4 | 480 | 16.4 | 18.7 | 14.1 | ||||||||||||||||||

| including | 591.1 | 600.8 | 476 | 6.7 | 38.7 | 27.2 | ||||||||||||||||||

*Results from Madrid deposit at Hope Bay use a capping factor of 50 g/t gold.

**Previously released, with the depth values for hole HBM23-143 revised in this news release.

[Madrid Deposit at Hope Bay – Composite Longitudinal Section]

San Nicolás Copper Project

In January 2024, Minas de San Nicolás submitted their MIA-R permit application (Environmental Impact Assessment) and continued engagement with government and stakeholders in support of permit review. In addition, the Minas de San Nicolás team continued to advance feasibility study work, with plans to initiate detailed engineering in the first half of 2025. Project approval would be expected to follow, subject to receipt of permits and the results of the feasibility study.

ABITIBI REGION, QUEBEC

LaRonde Complex – Automation Initiatives at LZ5 Continue to Yield Higher Productivity; Gold Production Affected by Lower Grades

| LaRonde Complex – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 680 | 707 | ||||||

| Tonnes of ore milled per day | 7,473 | 7,867 | ||||||

| Gold grade (g/t) | 3.41 | 3.72 | ||||||

| Gold production (ounces) | 68,364 | 79,607 | ||||||

| Production costs per tonne (C$) | $ | 187 | $ | 118 | ||||

| Minesite costs per tonne (C$)13 | $ | 158 | $ | 157 | ||||

| Production costs per ounce | $ | 1,383 | $ | 778 | ||||

| Total cash costs per ounce of gold produced | $ | 1,065 | $ | 958 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production decreased when compared to the prior-year period primarily due to lower volumes of ore milled and lower gold grades as expected under the mining sequence |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne increased when compared to the prior-year period primarily due to stockpile consumption, higher underground maintenance costs and the lower volumes of ore milled in the current period. Production costs per ounce increased when compared to the prior-year period primarily due to the same reasons as for the higher production costs per tonne, the timing of inventory sales and lower gold grades |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne increased when compared to the prior-year period primarily due to lower volumes of ore milled in the current period. Total cash costs per ounce increased when compared to the prior-year period primarily due to lower gold grades |

Highlights

| · | The Company continued its automation initiatives at LaRonde Zone 5 ("LZ5"), improving overall productivity and increasing the production rate to 3,500 tpd in the quarter, compared to approximately 3,300 tpd in 2023. Starting in the first quarter of 2024, the Friday night shift was converted from manual to automated operation. All development and production activities on Friday, Saturday and Sunday night shifts are now done remotely from surface, which resulted in approximately 19% of the tonnage mined in automated mode in the first quarter of 2024 |

| · | Production from the 11-3 Zone at the LaRonde mine ramped up as planned, contributing over 105,000 tonnes in the first quarter of 2024. The 11-3 Zone is expected to continue to add additional flexibility to the LaRonde mine production plan |

| · | The LZ5 processing facility was placed on care and maintenance during the third quarter of 2023 and is on track to restart in the third quarter of 2024. During the downtime, the Company is overhauling the facility's leach tanks. Ore from LZ5 will continue to be processed at the LaRonde mill until the restart of the LZ5 processing facility, which is expected early in the second half of 2024 |

13 Minesite costs per tonne is a non-GAAP measure that is not standardized under IFRS and is reported on a per tonne of ore milled basis. For a description of the composition and usefulness of this non-GAAP measure and a reconciliation to production costs see "Reconciliation of Non-GAAP Performance Measures" and "Note Regarding Certain Measures of Performance", respectively, below.

| · | At the LaRonde processing facility, the focus remained on improving mill recoveries by optimizing the blending of ore from the LaRonde mine, 11-3 Zone, LZ5, Goldex and Akasaba West |

| · | The LaRonde complex received certification under the International Cyanide Management Code during the first quarter of 2024 |

Canadian Malartic Complex – Record Quarterly Gold Production Driven by Higher Tonnage Milled and Higher Gold Grades from Odyssey; Odyssey Ramp Development Reached the Top of the East Gouldie Deposit

| Canadian Malartic Complex – Operating Statistics* | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 5,173 | 4,524 | ||||||

| Tonnes of ore milled per day | 56,846 | 50,267 | ||||||

| Gold grade (g/t) | 1.21 | 1.19 | ||||||

| Gold production* (ounces) | 186,906 | 80,685 | ||||||

| Production costs per tonne (C$) | $ | 33 | $ | 34 | ||||

| Minesite costs per tonne (C$) | $ | 42 | $ | 39 | ||||

| Production costs per ounce | $ | 677 | $ | 710 | ||||

| Total cash costs per ounce | $ | 850 | $ | 794 | ||||

* Gold production reflects Agnico Eagle's 50% interest in the Canadian Malartic complex up to and including March 30, 2023 and 100% interest thereafter. Tonnage of ore milled is reported on a 100% basis for both periods.

Gold Production

| · | First Quarter of 2024 – Gold production increased when compared to the prior-year period primarily due to the increase in the Company's ownership percentage between periods from 50% to 100% as a result of the Yamana Transaction, which closed on March 31, 2023, as well as higher throughput and gold grades |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne decreased when compared to the prior-year period primarily due to higher volume of ore milled. Production costs per ounce decreased when compared to the prior-year period due to lower production costs per tonne and higher gold grades |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne increased when compared to the prior-year period primarily due to the consumption of stockpiles during the quarter, partially offset by higher volume of ore milled. Total cash costs per ounce increased when compared to the prior-year period primarily due to higher minesite costs per tonne, partially offset by higher gold grades |

Highlights

| · | At the Barnat pit, good equipment availability and productivity, together with mining areas with softer ultramafic ore, drove solid operational performance despite challenging weather conditions |

| · | At Odyssey South, the mining rate and production were slightly below plan at approximately 3,300 tpd and 17,700 ounces of gold, respectively. The waste generated from the pre-sinking of the shaft between levels 54 to 66 and the raise bore from levels 36 to 54 impacted the ore and waste haulage by ramp. The underground operations are expected to gain additional flexibility in the second quarter of 2024, with the start of a second mining front and the addition of four 65 tonnes haulage trucks |

| · | Stope reconciliation at Odyssey South remains positive, primarily from the contribution of the internal zones, which resulted in approximately 16% more gold ounces produced than anticipated |

| · | Mill throughput continued to be above plan due to softer rock conditions. High mill throughput, high gold grades resulting from the contribution from Odyssey and higher mill recoveries than planned resulted in record quarterly production at the Canadian Malartic complex |

| · | At the Canadian Malartic pit, the Company continued the construction of the central berm (approximately 74% complete) in preparation for in-pit tailings disposal, which is scheduled to start in mid-2024 |

| · | In the first quarter of 2024 at the Odyssey mine, ramp development continued to exceed targets, with the ramp reaching the first production level of East Gouldie (level 75) in February 2024. An update on the Odyssey project development, construction and exploration highlights is set out in the Update on Key Value Drivers and Pipeline Projects section above |

Goldex Complex – Akasaba West Project Achieves Commercial Production; Initial Production from Deep 2 Zone on Track for Second Quarter

Commercial production was achieved at the Akasaba West project on February 1, 2024. The ore from Akasaba is hauled and processed at the Goldex mill. The Goldex mine and the Akasaba mine now form the Goldex complex.

| Goldex Complex – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 760 | 698 | ||||||

| Tonnes of ore milled per day | 8,352 | 7,756 | ||||||

| Gold grade (g/t) | 1.64 | 1.73 | ||||||

| Gold production (ounces) | 34,388 | 34,023 | ||||||

| Production costs per tonne (C$) | $ | 59 | $ | 54 | ||||

| Minesite costs per tonne (C$) | $ | 60 | $ | 52 | ||||

| Production costs per ounce | $ | 965 | $ | 818 | ||||

| Total cash costs per ounce | $ | 948 | $ | 810 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production increased when compared to the prior-year period primarily due to higher throughput as a result of the additional production from Akasaba West, partially offset by lower gold grades |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne increased when compared to the prior-year period primarily due to higher underground production costs, higher open pit mining costs associated with the Akasaba West deposit and higher milling costs, partially offset by higher volume of ore milled. Production costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for production costs per tonne as well as lower gold grades |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne increased when compared to the prior-year period due to the same reasons outlined above for the higher production costs per tonne. Total cash costs per ounce increased when compared to the prior-year period due to higher minesite costs per tonne and lower gold grades |

Highlights

| · | Akasaba West is expected to provide additional production flexibility to the Goldex complex, contributing approximately 1,750 tpd grading 0.84 g/t of gold and 0.48% of copper to the Goldex processing facility, while the underground mine is now expected to contribute approximately 7,000 tpd |

| · | In the first quarter of 2024, production from South Zone Sector 3 contributed approximately 1,000 tpd as planned, providing higher gold grades and additional flexibility for the mining operations |

| · | The development of the Deep 2 Zone continued to advance as planned and initial production is expected in the second quarter of 2024 |

ABITIBI REGION, ONTARIO

Detour Lake – Record Quarterly Tonnes Mined; Continued Mill Improvement Year-Over-Year ; Gold Production Affected by Lower Grades and Lower Mill Recovery

| Detour Lake Mine – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 6,502 | 6,397 | ||||||

| Tonnes of ore milled per day | 71,451 | 71,078 | ||||||

| Gold grade (g/t) | 0.82 | 0.86 | ||||||

| Gold production (ounces) | 150,751 | 161,857 | ||||||

| Production costs per tonne (C$) | $ | 27 | $ | 24 | ||||

| Minesite costs per tonne (C$) | $ | 27 | $ | 26 | ||||

| Production costs per ounce | $ | 875 | $ | 704 | ||||

| Total cash costs per ounce | $ | 871 | $ | 771 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production decreased when compared to the prior-year period primarily due to lower gold grades as expected under the mining sequence and lower mill recovery due to abnormal chipping of grinding media affecting grinding efficiency |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne increased when compared to the prior-year period due to higher milling and mining costs and a lower stockpile build-up in the current period, partially offset by a higher volume of ore processed. Production costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for production costs per tonne as well as lower gold grades |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne increased when compared to the prior-year period due to the same reasons outlined above for the higher production costs per tonne. Total cash costs per ounce increased when compared to the prior-year period due to lower gold grades and higher minesite costs per tonne |

Highlights

| · | In the first quarter of 2024, the open pit set a record of quarterly tonnes mined, despite unseasonably warm and variable winter conditions affecting operating conditions in the pit. Improvements in truck utilization drove higher truck productivity |

| · | In the first quarter of 2024, the mill throughput rate was approximately 71,451 tpd, which was the highest for a first quarter period, demonstrating continued mill improvement year-over-year. This solid performance was achieved despite challenges with abnormal chipping of grinding media in the SAG mill which affected throughput and grinding efficiency and resulted in lower mill recovery. The Company is working with its suppliers to resolve the issue and further optimize the grinding efficiency in the SAG mill. The introduction of new grinding media in mid-March 2024 yielded favourable results and further testing is scheduled in the second quarter of 2024 |

| · | The expansion of the mine maintenance shops to support increased mining rates and a larger production fleet is ongoing. All long lead items have been ordered and construction commenced in the first quarter of 2024. The new mining service facility is expected to be completed in 2025 |

| · | An upgrade of the 230kV main substation is planned to improve the power quality at the mine and improve the site readiness for potential projects such as the Detour Lake underground and mill expansion. Approximately 95% of the engineering was completed as at March 31, 2024. The upgrades related to power quality are expected to be completed in 2024 and those related to improving site readiness for future projects are expected in 2025 |

| · | An update on the mill expansion work, the advancement of the underground evaluation and exploration results is set out in the Update on Key Value Drivers and Pipeline Projects section above |

Macassa – Record Quarterly Mill Throughput; Strong Operational Performance Driven by Higher Productivity from Continued Workforce Ramp-Up and Improved Equipment Availability

| Macassa Mine – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 134 | 87 | ||||||

| Tonnes of ore milled per day | 1,473 | 967 | ||||||

| Gold grade (g/t) | 16.27 | 23.32 | ||||||

| Gold production (ounces) | 68,259 | 64,115 | ||||||

| Production costs per tonne (C$) | $ | 483 | $ | 589 | ||||

| Minesite costs per tonne (C$) | $ | 493 | $ | 585 | ||||

| Production costs per ounce | $ | 698 | $ | 592 | ||||

| Total cash costs per ounce | $ | 711 | $ | 604 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production increased when compared to the prior-year period primarily due to higher throughput as a result of increased productivity from a larger workforce and improved equipment availability and the addition of ore sourced from the Near Surface deposit, partially offset by lower gold grades |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne decreased when compared to the prior-year period due to the higher volume of ore milled in the current period, partially offset by higher underground development and mining costs. Production costs per ounce increased when compared to the prior-year period due to lower gold grades, partially offset by lower production costs per tonne |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne decreased when compared to the prior-year period due to the same reasons outlined above for the lower production costs per tonne. Total cash costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for the higher production costs per ounce |

Highlights

| · | During the first quarter of 2024, Macassa continued to demonstrate sustained productivity gains with the highest quarterly gold production achieved since its acquisition by the Company, driven by record quarterly volume skipped and record quarterly mill throughput |

| · | In the first quarter of 2024, realized gold grades were higher than plan primarily due to accelerated development of a higher grade cut and fill area, which was originally planned to be mined in the second half of 2024 |

| · | The commissioning of the ventilation system upgrade was completed in the first quarter of 2024 with both surface fans reaching required operating capacity |

| · | At the Portal (ramp access to the Near Surface and AK deposits), production from long hole stopes in the Near Surface deposit continued in the first quarter of 2024, while the development of the AK deposit is on-track for initial production in the fourth quarter of 2024 |

| · | Exploration drilling at Macassa during the first quarter totalled 42,900 metres with highlights that included hole 58-1018 returning 33.6 g/t gold over 3.3 metres at 2,150 metres depth in an eastern extension of the Main Break Zone; and infill hole KLAK-273 returning 11.8 g/t gold over 5.0 metres at 342 metres depth in the shallow eastern extension of the AK deposit |

NUNAVUT

Meliadine Mine – Record Monthly Throughput and Ore Haulage Performance in January 2024

| Meliadine Mine – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 496 | 476 | ||||||

| Tonnes of ore milled per day | 5,451 | 5,300 | ||||||

| Gold grade (g/t) | 6.24 | 6.12 | ||||||

| Gold production (ounces) | 95,725 | 90,467 | ||||||

| Production costs per tonne (C$) | $ | 254 | $ | 228 | ||||

| Minesite costs per tonne (C$) | $ | 245 | $ | 239 | ||||

| Production costs per ounce | $ | 976 | $ | 897 | ||||

| Total cash costs per ounce | $ | 942 | $ | 937 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production increased when compared to the prior-year period primarily due to higher throughput as result of strong operational performance at the mine and mill and gold grades as expected under the mining sequence |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne increased when compared to the prior-year period primarily due to higher open pit volumes mined, partially offset by the higher volume of ore milled in the current period. Production costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for production costs per tonne as well as timing of inventory sales, partially offset by higher gold grades |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne increased when compared to the prior-year period due to the same reasons outlined above for production costs per tonne. Total cash costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for production costs per ounce |

Highlights

| · | Both the open pit and the underground mine performed above plan in the first quarter of 2024, with the underground mine showing significant improvement and achieving record volumes hauled in January 2024 following underground optimization initiatives. The processing plant also continued to demonstrate overall strong performance, with record monthly volume processed in January 2024 of 191,000 tonnes |

| · | The mill expansion project remains on-track for completion in mid-2024. The key focus areas in the first quarter of 2024 were the commissioning of the filter press and equipment installation, the installation of the leach tanks and agitators at the carbon in leach process and the mechanical, piping and electrical work at the secondary grinding circuit. With the commissioning of the Phase 2 mill expansion, the processing rate ramp-up is expected to increase throughput to 6,000 tpd by year-end 2024 |

| · | Construction was completed on the Western ventilation intake and the system is expected to enter into production in the second quarter of 2024 |

| · | During the quarter, the Company submitted a proposal to the Nunavut Water Board to amend the current Type A Water license to include tailings, water and waste management infrastructure at the Pump, F-Zone, Wesmeg and Discovery deposits. In January 2024, the Company received confirmation from the Nunavut Planning Commission that no review was required from the Nunavut Impact Review Board (NIRB) and that the new water license amendment process could be initiated. The Company expects permits to be received in the fourth quarter of 2024 |

| · | Exploration drilling at Meliadine during the first quarter totalled 24,500 metres, highlighted by significant high-grade intersections in the Wesmeg and Wesmeg North deep extension to the east, demonstrated by hole M23-3732B returning 10.2 g/t gold over 5.8 metres in Wesmeg's Lode 625 at 349 metres depth and hole ML300-10340-D11 returning 11.1 g/t gold over 3.6 metres in Wesmeg North's Lode 972 at 401 metres depth and 6.1 g/t gold over 7.4 metres in Wesmeg's Lode 625 at 467 metres depth |

Meadowbank Complex – Record Quarterly Mill Throughput

| Meadowbank Complex – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 1,071 | 983 | ||||||

| Tonnes of ore milled per day | 11,769 | 10,922 | ||||||

| Gold grade (g/t) | 4.09 | 3.91 | ||||||

| Gold production (ounces) | 127,774 | 111,110 | ||||||

| Production costs per tonne (C$) | $ | 143 | $ | 176 | ||||

| Minesite costs per tonne (C$) | $ | 151 | $ | 174 | ||||

| Production costs per ounce | $ | 893 | $ | 1,170 | ||||

| Total cash costs per ounce | $ | 937 | $ | 1,134 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production increased when compared to the prior-year period primarily due to higher gold grades as expected under the mine plan and higher throughput as operations in the prior-year period were affected by unplanned downtime at the SAG mill |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne decreased when compared to the prior-year period due to a higher volume of ore milled and a build-up in stockpiles, partially offset by the lower deferred stripping adjustment in the current period. Production costs per ounce decreased when compared to the prior-year period due to higher gold grades and lower production costs per tonne |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne decreased when compared to the prior-year period due to the same reasons outlined above for the lower production costs per tonne. Total cash costs per ounce decreased when compared to the prior-year period due to the same reasons outlined above for the lower production costs per ounce |

Highlights

| · | The open pit operation continued to deliver solid haulage performance during the first quarter of 2024, with reduced weather delays also contributing to the positive production results. Gold production continued to benefit from positive reconciliation on ore tonnage |

| · | The underground operation achieved its strongest quarter, setting quarterly performance records for the cemented rock fill, production drilling and development in the first quarter of 2024. This was accomplished through continued productivity gains that demonstrated sustained improvement through the full mining cycle and increased adherence and compliance to plan |

| · | Stripping for the IVR pit push-back, which was approved in the fourth quarter of 2023, commenced in the first quarter of 2024 |

AUSTRALIA

Fosterville – Quarterly Gold Production in Line with Plan; Work on Ventilation Upgrade Continues to Advance

| Fosterville Mine – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 172 | 148 | ||||||

| Tonnes of ore milled per day | 1,890 | 1,644 | ||||||

| Gold grade (g/t) | 10.51 | 18.55 | ||||||

| Gold production (ounces) | 56,569 | 86,558 | ||||||

| Production costs per tonne (A$) | $ | 301 | $ | 367 | ||||

| Minesite costs per tonne (A$) | $ | 275 | $ | 343 | ||||

| Production costs per ounce | $ | 595 | $ | 423 | ||||

| Total cash costs per ounce | $ | 537 | $ | 396 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production decreased when compared to the prior-year period primarily due to the lower gold grades as expected under the mining sequence and as a result of lower than expected gold grades in a high grade Swan stope mined, partially offset by higher throughput |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne decreased when compared to the prior-year period due to lower mining and royalty costs and higher volume of ore milled. Production costs per ounce increased when compared to the prior-year period due to lower gold grades, partially offset by the lower mining and royalty costs and the weaker Australian dollar relative to the U.S. dollar |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne decreased when compared to the prior-year period due to the same reasons outlined above for the lower production costs per tonne. Total cash costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for the higher production costs per ounce |

Highlights

| · | With the completion of the key underground development associated with the ventilation upgrade in the fourth quarter of 2023, the mine ramped up its production activities and exceeded volume targets in the first quarter of 2024 |

| · | The higher ore volume mined drove the strong operating performance of the processing facility, with throughput exceeding plan. The Company continues to focus on productivity gains and cost control at the mine and the mill to maximize throughput and reduce unit costs |

| · | The Company is currently advancing an upgrade of the primary ventilation system to sustain the mining rate in the Lower Phoenix zones in future years. In the first quarter of 2024, the Company continued the excavation of the ventilation raises and the project is progressing as planned at approximately 25% completion. The Company expects the project to be completed by early 2025 |

FINLAND

Kittila – Annual Autoclave Maintenance Completed as Planned; Gold Production on Target; Positive Exploration Results Continue to Demonstrate Expansion Potential of Main Zone and Sisar Zone

| Kittila Mine – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 482 | 496 | ||||||

| Tonnes of ore milled per day | 5,297 | 5,511 | ||||||

| Gold grade (g/t) | 4.31 | 4.73 | ||||||

| Gold production (ounces) | 54,581 | 63,692 | ||||||

| Production costs per tonne (EUR) | € | 113 | € | 98 | ||||

| Minesite costs per tonne (EUR) | € | 112 | € | 98 | ||||

| Production costs per ounce | $ | 1,082 | $ | 837 | ||||

| Total cash costs per ounce | $ | 1,070 | $ | 806 | ||||

Gold Production

| · | First Quarter of 2024 – Gold production decreased when compared to the prior-year period primarily due to lower gold grades as expected under the mining sequence, lower throughput as a result of the planned annual maintenance of the autoclave and lower gold recoveries as a result of higher sulphur and organic carbon content |

Production Costs

| · | First Quarter of 2024 – Production costs per tonne increased when compared to the prior-year period due to the lower volume of ore milled, higher mill maintenance costs, higher contractor costs for waste haulage and increased mining royalty costs, partially offset by lower underground mining development costs. Production costs per ounce increased when compared to the prior-year period due to lower gold grades and higher production costs per tonne |

Minesite and Total Cash Costs

| · | First Quarter of 2024 – Minesite costs per tonne increased when compared to the prior-year period due to the same reasons outlined above for the higher production costs per tonne. Total cash costs per ounce increased when compared to the prior-year period due to the same reasons outlined above for the higher production costs per ounce |

Highlights

| · | A ten-day planned shutdown for the autoclave and other mill maintenance was completed in the first quarter of 2024. Mill throughput was on target, however, recovery was lower than plan due to high carbon and sulfur content in the ore, affecting gold production. Trial tests were completed to reduce the organic carbon which yielded positive results, and the mill showed improved recovery towards the end of the first quarter of 2024 |

| · | Exploration at Kittila during the first quarter continued to demonstrate the expansion potential of both the Main Zone and Sisar Zone to the north and near the bottom of the shaft. In the Roura area at depth, hole ROD23-701C returned 10.5 g/t gold over 3.1 metres in the Sisar Zone at 1,834 metres depth, approximately 200 metres below current mineral resources, showing the potential of this area which is open at depth and to the north |

MEXICO

Pinos Altos – Solid Performance at Reyna de Plata Pit Drives Quarterly Production

| Pinos Altos Mine – Operating Statistics | Three Months Ended March 31, |

|||||||

| 2024 | 2023 | |||||||

| Tonnes of ore milled (thousands of tonnes) | 426 | 364 | ||||||

| Tonnes of ore milled per day | 4,681 | 4,044 | ||||||

| Gold grade (g/t) | 1.89 | 2.16 | ||||||

| Gold production (ounces) | 24,725 | 24,134 | ||||||

| Production costs per tonne | $ | 78 | $ | 90 | ||||

| Minesite costs per tonne | $ | 94 | $ | 90 | ||||

| Production costs per ounce | $ | 1,351 | $ | 1,364 | ||||

| Total cash costs per ounce | $ | 1,348 | $ | 1,116 | ||||