UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 40-F

[Check one]

☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

OR | ||

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13(a) or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

For the fiscal year ended December 31, 2023 |

Commission File Number 001-13382 |

KINROSS GOLD CORPORATION

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English (if applicable))

Province of Ontario, Canada

(Province or other jurisdiction of incorporation or organization)

1041

(Primary Standard Industrial Classification Code Number (if applicable))

650430083

(I.R.S. Employer Identification Number (if applicable))

25 York Street, 17th Floor, Toronto, Ontario, Canada M5J 2V5 (416) 365-5123

(Address and telephone number of Registrant’s principal executive offices)

Martin D. Litt

Secretary

Kinross Gold U.S.A., Inc.

5075 S. Syracuse Street,

Suite 800,

Denver, Colorado,

80237

Telephone: (303) 802-1445

(Name, address (including zip code) and telephone number (including area code)

of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common stock, no par value |

|

KGC |

|

New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

For annual reports, indicate by check mark the information filed with this Form:

☒ Annual information form |

|

☒ Audited annual financial statements |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2023, there were 1,227,837,974 common shares and no preferred shares outstanding.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging Growth Company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

NOTE FOR U.S. READERS ON CANADA/U.S. REPORTING DIFFERENCES

We are permitted, under a multi-jurisdictional disclosure system adopted by the United States, to prepare this annual report on Form 40-F in accordance with Canadian disclosure requirements, which are different from those of the United States. We prepare our consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board, including the report of the independent registered public accounting firm with respect thereto. Consequently, our financial statements may not be comparable to those prepared by U.S. companies. Our Annual Information Form dated March 27, 2024 and Management’s Discussion and Analysis, together with our audited consolidated financial statements and notes thereto as at December 31, 2023 and 2022 and for the years then ended, are filed under cover of this form as exhibits 99.1, 99.2 and 99.3, respectively.

Our common shares are listed on the Toronto Stock Exchange and the New York Stock Exchange. There are certain differences between the corporate governance practices applicable to us and those applicable to U.S. companies under the New York Stock Exchange listing standards. A summary of the significant differences can be found at http://www.kinross.com/about/governance/default.aspx.

DISCLOSURE CONTROLS AND PROCEDURES

We maintain disclosure controls and procedures designed to ensure that information required to be disclosed in reports filed under the U.S. Securities Exchange Act of 1934, as amended, (the “Exchange Act”) is recorded, processed, summarized and reported within the appropriate time periods and that such information is accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate, to allow for timely disclosures regarding required disclosure. In designing and evaluating the disclosure controls and procedures, we recognize that any disclosure controls and procedures, no matter how well conceived or operated, can only provide reasonable, not absolute, assurance that the objectives of the control system are met, and management is required to exercise its judgment in evaluating the cost-benefit relationship of possible controls and procedures.

As required by Rule 13a-15(b) under the Exchange Act, we conducted an evaluation, under the supervision and with the participation of our management, including the Chief Executive Officer and the Chief Financial Officer, of the effectiveness of the design and operation of our disclosure controls and procedures as of December 31, 2023, the end of the period covered by this annual report on Form 40-F. Based on that evaluation, the Chief Executive Officer and Chief Financial Officer concluded that, as of December 31, 2023, the design and operation of the Company’s disclosure controls and procedures provide reasonable assurance that they are effective.

MANAGEMENT’S ANNUAL REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

Management is responsible for establishing and maintaining adequate internal control over financial reporting, as defined in Rules 13a-15(f) of the Exchange Act. As of December 31, 2023, Kinross’ management evaluated the effectiveness of its internal control over financial reporting. In making this assessment, management used the criteria specified in Internal Control - Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on that evaluation, the Chief Executive Officer and the Chief Financial Officer have concluded that Kinross’ internal control over financial reporting was effective as of December 31, 2023 and no material weaknesses in Kinross’s internal control over financial reporting were discovered.

The Company is required to provide an auditor’s attestation report on its internal control over financial reporting for the fiscal year ended December 31, 2023. In this annual report on Form 40-F, the Company’s independent registered public accounting firm, KPMG LLP, has provided its opinion as to the effectiveness of the Company’s internal control over financial reporting as of December 31, 2023. KPMG has also audited the Company’s financial statements included in this annual report on Form 40-F and issued a report thereon.

ATTESTATION OF REPORT OF INDEPENDENT AUDITOR

The attestation report of KPMG LLP is included in the Report of Independent Registered Public Accounting Firm that accompanies Kinross’ audited consolidated financial statements for the year ended December 31, 2023 included as exhibit 99.3 to this annual report on Form 40-F.

CHANGES IN INTERNAL CONTROL OVER FINANCIAL REPORTING

There have been no changes to our system of internal control over financial reporting for the year ended December 31, 2023 that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

AUDIT AND RISK COMMITTEE

The audit and risk committee of our Board of Directors is comprised of four directors: Glenn A. Ives, chairman, Kerry D. Dyte, Elizabeth D. McGregor and David A. Scott. Each of the members of the audit and risk committee is “independent” as that term is defined in the listing standards of the New York Stock Exchange. The board of directors has determined that Mr. Ives, and Ms. McGregor each qualify as an “audit committee financial expert” as such term is defined in paragraph 8(b) of General Instructions B to Form 40-F. Information concerning Mr. Ives’, Mr. Dyte’s, Ms. McGregor’s and Mr. Scott’s relevant education and experience is included in the biographical information contained in the Company’s Annual Information Form included as exhibit 99.1 to the annual report on Form 40-F. The Securities and Exchange Commission has indicated that the designation of a person as an audit committee financial expert does not make such person an “expert” for any purpose, impose any duties, obligations or liabilities on such person that are greater than those imposed generally on members of the audit and risk committee and the board of directors who do not carry this designation, or affect the duties, obligations or liability of any other member of the audit and risk committee or board of directors.

CODE OF ETHICS

The Code of Business Conduct and Ethics may be viewed at the Company’s website at www.kinross.com under “About – Corporate Governance” and is available in print to any shareholder upon written request to the Company’s Corporate Secretary. Any amendments to the Code of Business Conduct and Ethics, including a description of such amendment, will be posted to the Company’s website within five business days following the date of the amendment.

The Company did not grant any waivers under its Code of Business Conduct and Ethics during 2023.

PRINCIPAL ACCOUNTANT FEES AND SERVICES

Our independent registered public accounting firm is KPMG LLP, Toronto, ON, Canada, Auditor Firm ID: 85.

We paid the following fees to our independent registered public accounting firm during the last two fiscal years:

|

2023 |

2022 |

Audit Fees |

C$4,853,000 |

C$4,423,000 |

Audit-Related Fees |

C$230,000 |

C$203,000 |

Tax Fees |

nil |

C$2,000 |

All Other Fees1 |

C$444,000 |

C$109,000 |

Audit-related fees include fees related primarily to translation services and pension plan audits. Tax fees were for tax compliance and advisory services. “All Other Fees” includes amounts for services related to other non-audit services, which include assurance over the Company's sustainability reporting.

The audit and risk committee is required to approve all services provided by our principal auditor. All audit services, audit-related services, tax services, and other services provided during the year ended December 31, 2023 were pre-approved by the audit and risk committee which concluded that the provision of such services by KPMG LLP was compatible with the maintenance of that firm’s independence in the conduct of its auditing functions.

OFF-BALANCE SHEET ARRANGEMENTS

Our off-balance sheet arrangements are disclosed in Kinross’ Management’s Discussion and Analysis included as exhibit 99.2 under the captions “Liquidity and Capital Resources” and “Risk Analysis” and under Note 11, “Long-Term Debt and Credit Facilities”, under Note 13, “Provisions”, and under Note 19, “Commitments and Contingencies” to Kinross’ audited consolidated financial statements for the year ended December 31, 2023 included as exhibit 99.3 to this annual report on Form 40-F.

CONTRACTUAL OBLIGATIONS

The contractual obligations of the Company are disclosed in Kinross’ Management’s Discussion and Analysis included as exhibit 99.2 under the caption “Liquidity and Capital Resources – Contractual Obligations and Commitments”, and under Note 11, “Long-Term Debt and Credit Facilities” and under Note 19, “Commitments and Contingencies” to Kinross’ audited consolidated financial statements for the year ended December 31, 2023 included as exhibit 99.3 to this annual report on Form 40-F.

On June 26, 2023, Kinross announced an offering of US$500 million aggregate principal amount of 6.250% senior notes due 2033. The notes are senior unsecured obligations of Kinross and are unconditionally and irrevocably guaranteed by certain of Kinross’ wholly-owned subsidiaries that are also guarantors under Kinross’ senior unsecured credit agreements. The offering was completed on July 5, 2023. Kinross used the net proceeds, along with available cash on hand, to repay its $500.0 million aggregate principal amount of 5.950% senior notes due March 15, 2024 (the “2024 Notes”). On August 10, 2023, Kinross redeemed all of the outstanding 2024 Notes.

MINE SAFETY DISCLOSURE

Information concerning mine safety violations and other regulatory matters required by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act and paragraph (16) of General Instruction B to Form 40-F is included in exhibit 99.5 of this annual report on Form 40-F.

| 1. | “All Other Fees” includes C$415,000 in 2023 related to sustainability assurance work (2022 - C$81,000). |

SAFE HARBOR FOR FORWARD-LOOKING STATEMENTS

Cautionary Statement on Forward-Looking Information

All statements, other than statements of historical fact, contained or incorporated by reference in this annual report on Form 40-F including, but not limited to, any information as to the future financial or operating performance of Kinross, constitute “forward-looking information” or “forward-looking statements” within the meaning of certain securities laws, including the provisions of the Securities Act (Ontario) and the provisions for “safe harbor” under the United States Private Securities Litigation Reform Act of 1995 and are based on expectations, estimates and projections as of the date of this annual report on Form 40-F. Forward-looking statements contained in this annual report on Form 40-F, include, but are not limited to, statements with respect to our guidance for production, cost guidance, including production costs of sales, all-in sustaining cost of sales, and capital expenditures; statements with respect to our guidance for cash flow and attributable free cash flow; the declaration, payment and sustainability of the Company’s dividends; identification of additional resources and reserves or the conversion of resources to reserves; the Company’s liquidity; greenhouse gas reduction initiatives and targets; the implementation and effectiveness of the Company’s ESG or Climate Change strategy; the schedules budgets, and forecast economics for the Company’s development projects; budgets for and future prospects for exploration, development and operation at the Company’s operations and projects, including the Great Bear project; potential mine life extensions at the Company’s operations; the Company’s balance sheet and liquidity outlook, as well as references to other possible events including, the future price of gold and silver, costs of production, operating costs; price inflation; capital expenditures, costs and timing of the development of projects and new deposits, estimates and the realization of such estimates (such as mineral or gold reserves and resources or mine life), success of exploration, development and mining, currency fluctuations, capital requirements, project studies, government regulation, permit applications, environmental risks and proceedings, and resolution of pending litigation. The words “additional”, “advance”, “anticipate”, “assumption”, “believe”, “budget”, “consideration”, “continue”, “develop”, “enhancement”, “estimates”, “expand”, “expects”, “explore”, “extend”, “forecast”, “goal”, “focus”, “forward”, “future”, “guidance”, “indicate”, “initiative”, “intend”, “measures”, “opportunity”, “optimize”, “outlook”, “phase”, “plan”, “possible”, “potential”, “priority”, “proceeding”, “progress”, “project”, “prospect”, “prospective”, “schedule”, “seek”, “study”, “target”, or variations of or similar such words and phrases or statements that certain actions, events or results may, could, should or will be achieved, received or taken, or will occur or result and similar such expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by Kinross as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The estimates, models and assumptions of Kinross referenced, contained or incorporated by reference in this annual report on Form 40-F, which may prove to be incorrect, include, but are not limited to, the various assumptions set forth herein and in our Management’s Discussion and Analysis (“MD&A”) for the year ended December 31, 2023 and in our Annual Information Form (“AIF”) for the year ended December 31, 2023, as well as: (1) there being no significant disruptions affecting the operations of the Company, whether due to extreme weather events (including, without limitation, excessive snowfall, excessive or lack of rainfall, in particular, the potential for further production curtailments at Paracatu resulting from insufficient rainfall and the operational challenges at Fort Knox and Bald Mountain resulting from excessive rainfall or snowfall, which can impact costs and/or production) and other or related natural disasters, labour disruptions (including but not limited to strikes or workforce reductions), supply disruptions, power disruptions, damage to equipment, pit wall slides or otherwise; (2) permitting, development, operations and production from the Company’s operations and development projects being consistent with Kinross’ current expectations including, without limitation: the maintenance of existing permits and approvals and the timely receipt of all permits and authorizations necessary for the operation of Tasiast; water and power supply and continued operation of the tailings reprocessing facility at Paracatu; permitting of the Great Bear project (including the consultation process with Indigenous groups), permitting and development of the Lobo-Marte project; in each case in a manner consistent with the Company’s expectations; and the successful completion of exploration consistent with the Company’s expectations at the Company’s projects; (3) political and legal developments in any jurisdiction in which the Company operates being consistent with its current expectations including, without limitation, restrictions or penalties imposed, or actions taken, by any government, including but not limited to amendments to the mining laws, and potential power rationing and tailings facility regulations in Brazil (including those related to financial assurance requirements), potential amendments to water laws and/or other water use restrictions and regulatory actions in Chile, new dam safety regulations, potential amendments to minerals and mining laws and energy levies laws, new regulations relating to work permits, potential amendments to customs and mining laws (including but not limited to amendments to the VAT) and the potential application of the tax code in Mauritania, potential amendments to and enforcement of tax laws in Mauritania (including, but not limited to, the interpretation, implementation, application and enforcement of any such laws and amendments thereto), potential third party legal challenges to existing permits, and the impact of any trade tariffs being consistent with Kinross’ current expectations; (4) the completion of studies, including scoping studies, preliminary economic assessments, pre-feasibility or feasibility studies, on the timelines currently expected and the results of those studies being consistent with Kinross’ current expectations; (5) the exchange rate between the Canadian dollar, Brazilian real, Chilean peso, Mauritanian ouguiya and the U.S.

dollar being approximately consistent with current levels; (6) certain price assumptions for gold and silver; (7) prices for diesel, natural gas, fuel oil, electricity and other key supplies being approximately consistent with the Company’s expectations; (8) attributable production and cost of sales forecasts for the Company meeting expectations; (9) the accuracy of the current mineral reserve and mineral resource estimates of the Company and Kinross’ analysis thereof being consistent with expectations (including but not limited to ore tonnage and ore grade estimates), future mineral resource and mineral reserve estimates being consistent with preliminary work undertaken by the Company, mine plans for the Company’s current and future mining operations, and the Company’s internal models; (10) labour and materials costs increasing on a basis consistent with Kinross’ current expectations; (11) the terms and conditions of the legal and fiscal stability agreements for Tasiast being interpreted and applied in a manner consistent with their intent and Kinross’ expectations and without material amendment or formal dispute (including without limitation the application of tax, customs and duties exemptions and royalties); (12) asset impairment potential; (13) the regulatory and legislative regime regarding mining, electricity production and transmission (including rules related to power tariffs) in Brazil being consistent with Kinross’ current expectations; (14) access to capital markets, including but not limited to maintaining our current credit ratings consistent with the Company’s current expectations; (15) potential direct or indirect operational impacts resulting from infectious diseases or pandemics; (16) changes in national and local government legislation or other government actions, including the Canadian federal impact assessment regime; (17) litigation, regulatory proceedings and audits, and the potential ramifications thereof, being concluded in a manner consistent with the Corporation’s expectations (including without limitation litigation in Chile relating to the alleged damage of wetlands and the scope of any remediation plan or other environmental obligations arising therefrom); (18) the Company’s financial results, cash flows and future prospects being consistent with Company expectations in amounts sufficient to permit sustained dividend payments; and (19) the impacts of detected pit wall instability at Round Mountain and Bald Mountain being consistent with the Company’s expectations. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not limited to: the inaccuracy of any of the foregoing assumptions; fluctuations in the currency markets; fluctuations in the spot and forward price of gold or certain other commodities (such as fuel and electricity); price inflation of goods and services; changes in the discount rates applied to calculate the present value of net future cash flows based on country-specific real weighted average cost of capital; changes in the market valuations of peer group gold producers and the Company, and the resulting impact on market price to net asset value multiples; changes in various market variables, such as interest rates, foreign exchange rates, gold or silver prices and lease rates, or global fuel prices, that could impact the mark-to-market value of outstanding derivative instruments and ongoing payments/receipts under any financial obligations; risks arising from holding derivative instruments (such as credit risk, market liquidity risk and mark-to-market risk); changes in national and local government legislation, taxation (including but not limited to income tax, advance income tax, stamp tax, withholding tax, capital tax, tariffs, value-added or sales tax, capital outflow tax, capital gains tax, windfall or windfall profits tax, production royalties, excise tax, customs/import or export taxes/duties, asset taxes, asset transfer tax, property use or other real estate tax, together with any related fine, penalty, surcharge, or interest imposed in connection with such taxes), controls, policies and regulations; the security of personnel and assets; political or economic developments in Canada, the United States, Chile, Brazil, Mauritania or other countries in which Kinross does business or may carry on business; business opportunities that may be presented to, or pursued by, us; our ability to successfully integrate acquisitions and complete divestitures; operating or technical difficulties in connection with mining, development or refining activities; employee relations; litigation or other claims against, or regulatory investigations and/or any enforcement actions, administrative orders or sanctions in respect of the Company (and/or its directors, officers, or employees) including, but not limited to, securities class action litigation in Canada and/or the United States, environmental litigation or regulatory proceedings or any investigations, enforcement actions and/or sanctions under any applicable anti-corruption, international sanctions and/or anti-money laundering laws and regulations in Canada, the United States or any other applicable jurisdiction; the speculative nature of gold exploration and development including, but not limited to, the risks of obtaining and maintaining necessary licenses and permits; diminishing quantities or grades of reserves; adverse changes in our credit ratings; and contests over title to properties, particularly title to undeveloped properties. In addition, there are risks and hazards associated with the business of gold exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion losses (and the risk of inadequate insurance, or the inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can directly or indirectly affect, and could cause, Kinross’ actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, Kinross, including but not limited to resulting in an impairment charge on goodwill and/or assets. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements are provided for the purpose of providing information about management’s expectations and plans relating to the future. All of the forward-looking statements made or incorporated by reference in this annual report on Form 40-F, including but not limited to the “Risk Factors” section of our 2023 AIF and in the “Risk Analysis” section of our most recently filed MD&A, are qualified by this cautionary statement and those made in our other filings with the securities regulators of Canada and the United States including, but not limited to, the cautionary statements made in the “Risk Factors” section of our 2023 AIF and the “Risk Analysis” section of our MD&A for the year ended December 31, 2023. These factors are not intended to represent a complete list of the factors that could affect Kinross. Kinross disclaims any intention or obligation to update or revise any forward-looking statements or to explain any material difference between subsequent actual events and such forward looking statements, except to the extent required by applicable law.

UNDERTAKING AND CONSENT TO SERVICE OF PROCESS

Registrant undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

ADDITIONAL INFORMATION

Additional information relating to our company, including our audited consolidated financial statements as at December 31, 2023 and 2022, and for each of the years then ended, together with the accompanying Management’s Discussion and Analysis and the 2023 Annual Information Form can be found on SEDAR+ (www.sedarplus.ca), on EDGAR (www.sec.gov) or on our website at www.kinross.com. The information found on, or otherwise accessible through, our website is not incorporated by reference into, nor does it form a part of, this annual report on Form 40-F or any other document that we file with the SEC. Upon the written request of any shareholder, Kinross will provide a copy of this annual report on Form 40-F, including the audited financial statements, Management’s Discussion and Analysis, and the Annual Information Form included as exhibits hereto. Written requests for such information should be directed to Investor Relations, Kinross Gold Corporation, 25 York Street, 17th Floor, Toronto, Ontario, Canada M5J 2V5, toll free 1-866-561-3636 or info@kinross.com.

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Registrant certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

|

KINROSS GOLD CORPORATION |

|

|

|

|

|

|

|

March 27, 2024 |

By |

/s/ Andrea S. Freeborough |

|

|

Andrea S. Freeborough |

|

|

Executive Vice President & |

|

|

Chief Financial Officer |

EXHIBIT INDEX

Exhibit |

|

Description |

97.1 |

|

|

|

|

|

99.1 |

|

Annual Information Form for Kinross Gold Corporation dated March 27, 2024 |

|

|

|

99.2 |

|

|

|

|

|

99.3 |

|

|

|

|

|

99.4 |

|

Consent of KPMG LLP, independent registered public accounting firm for Kinross Gold Corporation |

|

|

|

99.5 |

|

|

|

|

|

99.6 |

|

Consent of Nicos Pfeiffer to being named as a qualified person |

|

|

|

99.7 |

|

Certification of the Principal Executive Officer pursuant to Rule 13a – 14(a) |

|

|

|

99.8 |

|

Certification of the Chief Financial Officer pursuant to Rule 13a – 14(a) |

|

|

|

99.9 |

|

|

|

|

|

99.10 |

|

|

|

|

|

|

|

* This information is furnished and not filed for purposes of Section 11 and 12 of the Securities Act of 1933 and Section 18 of the Securities Exchange Act of 1934. |

|

|

|

101 |

|

Interactive Data File (formatted as Inline XBRL) |

|

|

|

104 |

|

Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101) |

EXHIBIT 97.1

KINROSS GOLD CORPORATION

COMPENSATION RECOUPMENT POLICY

Approved by:

Board of Directors – November 8, 2023

1.0Purpose

This Compensation Recoupment Policy (the “Policy”) provides for the recoupment by Kinross Gold Corporation (the “Company”) of Incentive Compensation (as defined herein) in the event of a Financial Restatement and has been adopted in compliance with the requirements of Section 10D of the Securities Exchange Act of 1934 and the listing standards of the New York Stock Exchange (the “Exchange”) and applies while the Company continues to have a class of securities listed on the Exchange.

A person who becomes subject to this Policy remains subject to this Policy even if the person ceases to be an Executive Officer or an employee of the Group.

2.0Definitions

For purposes of this Policy:

“Board” means the board of directors of the Company.

“Committee” means the Human Resources and Compensation Committee of the Board or, in the absence of such committee, a majority of independent directors serving on the Board.

“Executive Officer” means, with respect to the Company, (i) its president, (ii) its principal financial officer, (iii) its principal accounting officer (or if there is no such accounting officer, its controller), (iv) any vice- president in charge of a principal business unit, division or function (such as sales, administration or finance), (v) any other officer who performs a policy-making function for the Company (including any officer of the Group if they perform policy-making functions for the Company), and (vi) any other person who performs similar policy-making functions for the Company.

“Financial Reporting Measure” means any (i) measure that is determined and presented in accordance with the accounting principles used in preparing the Company’s financial statements, (ii) stock price, (iii) total shareholder return, and (iv) any measures that are derived wholly or in part from any measure referenced in (i), (ii) or (iii). Such measures need not be presented within the Company’s financial statements or included in a filing with the U.S. Securities and Exchange Commission to constitute a Financial Reporting Measure.

“Financial Restatement” means an accounting restatement of any of the interim quarterly or annual consolidated financial statements of the Company due to the material non-compliance of the Company with any financial reporting requirement under securities laws, including any required accounting restatement to correct:

(a) |

an error in previously issued financial statements that is material to the previously issued financial statements, or |

(b) |

that would result in a material misstatement if the error were corrected in the current period or left uncorrected in the current period, |

but does not include (1) an out-of-period adjustment (i.e., the correction of an immaterial error in previously- issued financial statements, provided that such correction is immaterial to the current period), (2) an accounting restatement pursuant to an order issued by an applicable securities regulatory authority (provided such order is unrelated to any material non-compliance of the Company with any financial reporting requirement under securities laws), (3) the retrospective application of a change in accounting principles, (4) the retrospective revision to reportable segment information due to a change in the structure of the Company’s internal organization, (5) a retrospective reclassification due to a discontinued operation, (6) the retrospective application of a change in reporting entity, such as from a reorganization of entities under common control, (7) retrospective adjustments to provisional amounts in connection with a prior business combination, and (8) retrospective revision for stock splits, stock dividends, or other changes in the Company’s capital structure.

“Group” means, collectively, the Company, its parent(s) and all of its subsidiaries.

“Incentive Compensation” means any compensation that is:

(a) |

granted, earned, or vested based wholly or in part upon the attainment of a Financial Reporting Measure; or |

(b) |

determined based on (or otherwise calculated by reference to) compensation in (a) above. |

“Received”, with respect to Incentive Compensation, occurs in the Company’s fiscal period during which the Financial Reporting Measure specified in the Incentive Compensation award is attained, even if the grant or payment of the Incentive Compensation occurs after the end of that period.

“Recoupment Amount” means the amount determined under Subsection 4.1 of this Policy.

“Recoupment Period” means the three fiscal years completed immediately preceding any applicable Restatement Date, plus any transition period (that results from a change in the Company’s fiscal year) within or immediately following those three completed fiscal years, provided that a transition period between the last day of the Company’s previous fiscal year end and the first day of its new fiscal year that comprises a period of nine (9) to twelve (12) months would be deemed a completed fiscal year.

“Restatement Date” has the meaning set out in Section 3.0 of this Policy.

3.0When is Incentive Compensation Subject to Recoupment?

In the event of a Financial Restatement, Incentive Compensation shall be subject to recoupment under this Policy as of the date (the “Restatement Date”) which is the earlier to occur of:

(a) |

the date the Board, a committee of the Board, or the officer or officers of the Company authorized to take such action if Board action is not required, concludes, or reasonably should have concluded, that the Company is required to prepare a Financial Restatement; or |

(b) |

the date a court, regulator, or other legally authorized body directs the Company to prepare a Financial Restatement. |

Notwithstanding the foregoing, recoupment will not apply to Incentive Compensation Received (i) by a person prior to October 2, 2023, (ii) prior to the date the person became an Executive Officer, or (iii) by a person if they were not an Executive Officer during the performance period applicable to such Incentive Compensation.

4.0Recoupment Process for Incentive Compensation

4.1 |

Determination of Recoupment Amount |

Subject to Subsection 4.3, the “Recoupment Amount” shall be the amount by which the Incentive Compensation Received by the Executive Officer during the Recoupment Period exceeds the amount the Executive Officer would have Received during that period had it been determined based on the restated amounts in the Financial Restatement, measured on a before-tax basis, as determined by the Committee. Where the Recoupment Amount is not subject to mathematical recalculation directly from the information in the Financial Restatement (such as if it is based on stock price or total shareholder return), then (i) the amount will be based on a reasonable estimate of the effect of the Financial Restatement on the applicable Financial Reporting Measure, (ii) the Company will maintain documentation related to that determination, and (iii) the Company will provide such documentation to the Exchange.

4.2 |

Procedure for Recoupment |

The Company will reasonably promptly recover the Recoupment Amount. The Committee shall determine, in its sole discretion and subject to applicable law, the method for recovery of any Recoupment Amount, which to the fullest extent permitted by applicable law may include any one or more of the following:

(a) |

withholding, forfeiting and/or cancelling the Incentive Compensation of the individual; and/or |

(b) |

cancelling or setting-off against planned future grants of Incentive Compensation; and/or |

(c) |

requiring repayment of Incentive Compensation amounts previously received by the individual. |

Except as set forth in Subsection 4.3 below, the Company may not accept an amount that is less than the Recoupment Amount in satisfaction of the Executive Officer’s obligations under this Policy.

To the extent that an Executive Officer has already reimbursed the Company for any Recoupment Amount received under any duplicative recovery obligations established by the Company or applicable law, such reimbursed amount shall be credited to the Recoupment Amount that is subject to recovery under this Policy.

4.3 |

Exceptions to Recoupment Requirement |

Notwithstanding anything to the contrary in this Policy, the Company may elect not to recover some or all of the Recoupment Amount to the extent the Committee determines that recovery would be impracticable and one or more of the following conditions, and any other requirements of applicable law, are met:

(a) |

the direct expense paid to a third party to assist in enforcing the Policy would exceed the Recoupment Amount, and the Company (i) has made a reasonable attempt to recover the Recoupment Amount, (ii) documented such attempt, and (iii) provided such documentation to the Exchange; |

(b) |

recovery of the Recoupment Amount by the Company would violate applicable laws in Canada that were adopted prior to November 28, 2022, and the Company (i) has obtained an opinion of Canadian counsel that recovery would result in a violation of such laws and (ii) has provided such opinion to the Exchange; or |

(c) |

recovery of the Recoupment Amount would likely cause an otherwise tax-qualified retirement plan, under which benefits are broadly available to employees of the Company, to fail to meet the requirements of Sections 401(a)(13) or 411(a) of the U.S. Internal Revenue Code of 1986, as amended. |

5.0General

This Policy and the remedies available under this Policy are in addition to any other action, remedy or other claim or cause of action available to the Company against the applicable Executive Officer under applicable law, up to and including termination of employment and/or legal action for, among other things, breach of fiduciary duty.

6.0Prohibition on Indemnification

Notwithstanding any provision of the Articles or By-laws of the Company or of any agreement between the Company and an employee, employees are not entitled to be indemnified for any Incentive Compensation which is subject to recoupment under this Policy or any taxes previously paid or other costs associated with the receipt of such Incentive Compensation or application of this Policy and no employee will be entitled to any compensation or damages in respect of any portion of any Incentive Compensation which is recouped pursuant to this Policy.

Recoupment under this Policy shall not be considered to be or give rise to an event or action of the Company constituting “good reason” for resignation (or any similar concept) under any agreement, incentive plan or award of the Company.

7.0Administration

The Committee shall administer this Policy and may make all determinations under it, and all such determinations will be final and binding on all interested parties.

Subject to Section 10D of the Securities Exchange Act of 1934 and the listing standards of the Exchange, as applicable, this Policy may be terminated or amended at any time by the Board.

8.0Effective Date

This Policy was first approved by the Board on November 8, 2023.

Exhibit 99.1

KINROSS GOLD CORPORATION

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2023

Dated March 27, 2024

|

Page |

3 |

|

5 |

|

9 |

|

9 |

|

10 |

|

11 |

|

11 |

|

12 |

|

12 |

|

13 |

|

14 |

|

14 |

|

15 |

|

24 |

|

24 |

|

31 |

|

38 |

|

38 |

|

39 |

|

39 |

|

40 |

|

41 |

|

42 |

|

43 |

|

44 |

|

58 |

|

59 |

|

61 |

|

63 |

|

64 |

|

65 |

|

70 |

|

72 |

|

72 |

|

72 |

|

73 |

|

73 |

|

74 |

|

74 |

|

77 |

|

77 |

|

85 |

IMPORTANT NOTICE

ABOUT INFORMATION IN THIS ANNUAL INFORMATION FORM

Unless specifically stated otherwise in this Annual Information Form:

| ● | all dollar amounts are in U.S. dollars unless expressly stated otherwise; |

| ● | information is presented as of December 31, 2023, unless expressly stated otherwise; and |

| ● | references to “Kinross”, the “Company”, “its”, “our” and “we”, or related terms, refer to Kinross Gold Corporation or Kinross Gold Corporation and/or one or more or all of its subsidiaries, as may be applicable in the context. |

All statements, other than statements of historical fact, contained or incorporated by reference in this Annual Information Form (“AIF”) including, but not limited to, any information as to the future financial or operating performance of Kinross, constitute “forward-looking information” or “forward-looking statements” within the meaning of certain securities laws, including the provisions of the Securities Act (Ontario) and the provisions for “safe harbor” under the United States Private Securities Litigation Reform Act of 1995 and are based on expectations, estimates and projections as of the date of this AIF. Forward-looking statements contained in this AIF, include, but are not limited to, statements with respect to our guidance for production, cost guidance, including production costs of sales, all-in sustaining cost of sales, and capital expenditures; statements with respect our guidance for production, cost guidance, including production costs of sales, all-in sustaining cost of sales, and capital expenditures; statements with respect to our guidance for cash flow and attributable free cash flow; the declaration, payment and sustainability of the Company’s dividends; identification of additional resources and reserves or the conversion of resources to reserves; the Company’s liquidity; greenhouse gas reduction initiatives and targets; the implementation and effectiveness of the Company’s ESG or Climate Change strategy; the schedules budgets, and forecast economics for the Company’s development projects; budgets for and future prospects for exploration, development and operation at the Company’s operations and projects, including the Great Bear project; potential mine life extensions at the Company’s operations; the Company’s balance sheet and liquidity outlook, as well as references to other possible events including, the future price of gold and silver, costs of production, operating costs; price inflation; capital expenditures, costs and timing of the development of projects and new deposits, estimates and the realization of such estimates (such as mineral or gold reserves and resources or mine life), success of exploration, development and mining, currency fluctuations, capital requirements, project studies, government regulation, permit applications, environmental risks and proceedings, and resolution of pending litigation. The words “additional”, “advance”, “anticipate”, “assumption”, “believe”, “budget”, “consideration”, “continue”, “develop”, “enhancement”, “estimates”, “expand”, “expects”, “explore”, “extend”, “forecast”, “goal”, “focus”, “forward”, “future”, “guidance”, “indicate”, “initiative”, “intend”, “measures”, “opportunity”, “optimize”, “outlook”, “phase”, “plan”, “possible”, “potential”, “priority”, “proceeding”, “progress”, “project”, “prospect”, “prospective”, “schedule”, “seek”, “study”, “target”, or variations of or similar such words and phrases or statements that certain actions, events or results may, could, should or will be achieved, received or taken, or will occur or result and similar such expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by Kinross as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The estimates, models and assumptions of Kinross referenced, contained or incorporated by reference in this AIF, which may prove to be incorrect, include, but are not limited to, the various assumptions set forth herein and in our Management’s Discussion and Analysis (“MD&A”) for the year ended December 31, 2023, as well as: there being no significant disruptions affecting the operations of the Company, whether due to extreme weather events (including, without limitation, excessive snowfall, excessive or lack of rainfall, in particular, the potential for further production curtailments at Paracatu resulting from insufficient rainfall and the operational challenges at Fort Knox and Bald Mountain resulting from excessive rainfall or snowfall, which can impact costs and/or production) and other or related natural disasters, labour disruptions (including but not limited to strikes or workforce reductions), supply disruptions, power disruptions, damage to equipment, pit wall slides or otherwise; (2) permitting, development, operations and production from the Company’s operations and development projects being consistent with Kinross’ current expectations including, without limitation: the maintenance of existing permits and approvals and the timely receipt of all permits and authorizations necessary for the operation of Tasiast; water and power supply and continued operation of the tailings reprocessing facility at Paracatu; permitting of the Great Bear project (including the consultation process with Indigenous groups), permitting and development of the Lobo-Marte project; in each case in a manner consistent with the Company’s expectations; and the successful completion of exploration consistent with the Company’s expectations at the Company’s projects; (3) political and legal developments in any jurisdiction in which the Company operates being consistent with its current expectations including, without limitation, restrictions or penalties imposed, or actions taken, by any government, including but not limited to amendments to the mining laws, and potential power rationing and tailings facility regulations in Brazil (including those related to financial assurance requirements), potential amendments to water laws and/or other water use restrictions and regulatory actions in Chile, new dam safety regulations, potential amendments to minerals and mining laws and energy levies laws, new regulations relating to work permits, potential amendments to customs and mining laws (including but not limited to amendments to the value added tax “VAT”) and the potential application of the tax code in Mauritania, potential amendments to and enforcement of tax laws in Mauritania (including, but not limited to, the interpretation, Kinross Gold Corporation was initially created in May 1993 by the amalgamation of CMP Resources Ltd., Plexus Resources Corporation, and 1021105 Ontario Corp.

3

implementation, application and enforcement of any such laws and amendments thereto), potential third party legal challenges to existing permits, and the impact of any trade tariffs being consistent with Kinross’ current expectations; (4) the completion of studies, including scoping studies, preliminary economic assessments, pre-feasibility or feasibility studies, on the timelines currently expected and the results of those studies being consistent with Kinross’ current expectations; (5) the exchange rate between the Canadian dollar, Brazilian real, Chilean peso, Mauritanian ouguiya and the U.S. dollar being approximately consistent with current levels; (6) certain price assumptions for gold and silver; (7) prices for diesel, natural gas, fuel oil, electricity and other key supplies being approximately consistent with the Company’s expectations; (8) attributable production and cost of sales forecasts for the Company meeting expectations; (9) the accuracy of the current mineral reserve and mineral resource estimates of the Company and Kinross’ analysis thereof being consistent with expectations (including but not limited to ore tonnage and ore grade estimates), future mineral resource and mineral reserve estimates being consistent with preliminary work undertaken by the Company, mine plans for the Company’s current and future mining operations, and the Company’s internal models; (10) labour and materials costs increasing on a basis consistent with Kinross’ current expectations; (11) the terms and conditions of the legal and fiscal stability agreements for Tasiast being interpreted and applied in a manner consistent with their intent and Kinross’ expectations and without material amendment or formal dispute (including without limitation the application of tax, customs and duties exemptions and royalties); (12) asset impairment potential; (13) the regulatory and legislative regime regarding mining, electricity production and transmission (including rules related to power tariffs) in Brazil being consistent with Kinross’ current expectations; (14) access to capital markets, including but not limited to maintaining our current credit ratings consistent with the Company’s current expectations; (15) potential direct or indirect operational impacts resulting from infectious diseases or pandemics; (16) changes in national and local government legislation or other government actions, including the Canadian federal impact assessment regime; (17) litigation, regulatory proceedings and audits, and the potential ramifications thereof, being concluded in a manner consistent with the Corporation’s expectations (including without limitation litigation in Chile relating to the alleged damage of wetlands and the scope of any remediation plan or other environmental obligations arising therefrom); (18) the Company’s financial results, cash flows and future prospects being consistent with Company expectations in amounts sufficient to permit sustained dividend payments; and (19) the impacts of detected pit wall instability at Round Mountain and Bald Mountain being consistent with the Company’s expectations. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not limited to: the inaccuracy of any of the foregoing assumptions; fluctuations in the currency markets; fluctuations in the spot and forward price of gold or certain other commodities (such as fuel and electricity); price inflation of goods and services; changes in the discount rates applied to calculate the present value of net future cash flows based on country-specific real weighted average cost of capital; changes in the market valuations of peer group gold producers and the Company, and the resulting impact on market price to net asset value multiples; changes in various market variables, such as interest rates, foreign exchange rates, gold or silver prices and lease rates, or global fuel prices, that could impact the mark-to-market value of outstanding derivative instruments and ongoing payments/receipts under any financial obligations; risks arising from holding derivative instruments (such as credit risk, market liquidity risk and mark-to-market risk); changes in national and local government legislation, taxation (including but not limited to income tax, advance income tax, stamp tax, withholding tax, capital tax, tariffs, value-added or sales tax, capital outflow tax, capital gains tax, windfall or windfall profits tax, production royalties, excise tax, customs/import or export taxes/duties, asset taxes, asset transfer tax, property use or other real estate tax, together with any related fine, penalty, surcharge, or interest imposed in connection with such taxes), controls, policies and regulations; the security of personnel and assets; political or economic developments in Canada, the United States, Chile, Brazil, Mauritania or other countries in which Kinross does business or may carry on business; business opportunities that may be presented to, or pursued by, us; our ability to successfully integrate acquisitions and complete divestitures; operating or technical difficulties in connection with mining, development or refining activities; employee relations; litigation or other claims against, or regulatory investigations and/or any enforcement actions, administrative orders or sanctions in respect of the Company (and/or its directors, officers, or employees) including, but not limited to, securities class action litigation in Canada and/or the United States, environmental litigation or regulatory proceedings or any investigations, enforcement actions and/or sanctions under any applicable anti-corruption, international sanctions and/or anti-money laundering laws and regulations in Canada, the United States or any other applicable jurisdiction; the speculative nature of gold exploration and development including, but not limited to, the risks of obtaining and maintaining necessary licenses and permits; diminishing quantities or grades of reserves; adverse changes in our credit ratings; and contests over title to properties, particularly title to undeveloped properties. In addition, there are risks and hazards associated with the business of gold exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion losses (and the risk of inadequate insurance, or the inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can directly or indirectly affect, and could cause, Kinross’ actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, Kinross, including but not limited to resulting in an impairment charge on goodwill and/or assets. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements are provided for the purpose of providing information about management’s expectations and plans relating to the future. All of the forward-looking statements made in this AIF, including but not limited to the “Risk Factors” section hereof, are qualified by this cautionary statement and those made in our other filings with the securities regulators of Canada and the United States including, but not limited to, the cautionary statements made in the “Risk Analysis” section of our MD&A for the year ended December 31, 2023. These factors are not intended to represent a complete list of the factors that could affect Kinross. Kinross disclaims any intention or obligation to update or revise any forward-looking statements or to explain any material difference between subsequent actual events and such forward-looking statements, except to the extent required by applicable law.

4

In December 2000, Kinross amalgamated with LT Acquisition Inc.; in January 2005, Kinross amalgamated with its wholly-owned subsidiary, TVX Gold Inc. (“TVX”); in January 2006, it amalgamated with its wholly-owned subsidiary, Echo Bay Mines Ltd. (“Echo Bay”); and in January 2011, it amalgamated with Underworld Resources Inc. Kinross is the continuing entity resulting from these amalgamations. Kinross is governed by the Business Corporations Act (Ontario) and its registered and principal offices are located at 25 York Street, 17th Floor, Toronto, Ontario, M5J 2V5.

Each of Kinross’ mining operations is a separate business unit. Operations are overseen by a general manager, employed by Kinross or the applicable foreign subsidiary, who reports to the Company’s Chief Operating Officer. Global exploration strategies, corporate financing, tax, additional technical support services, hedging and acquisition strategies are managed centrally. Execution of site/regional operations and exploration strategies is managed locally. Kinross’ enterprise risk management programs are subject to overview by its Audit and Risk Committee of the Board of Directors (as defined below).

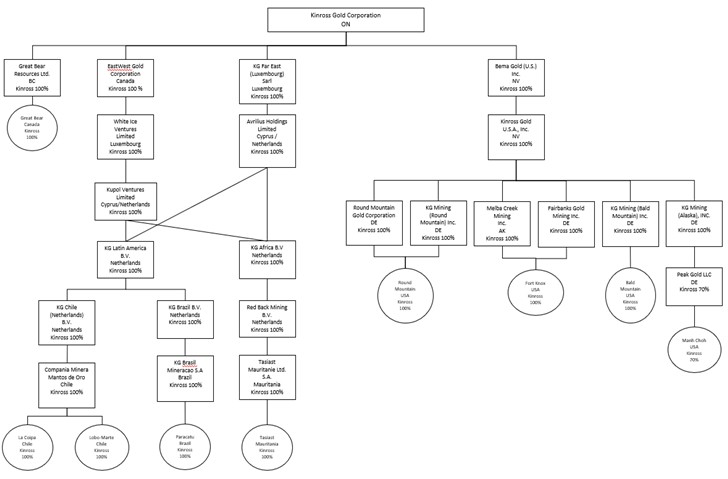

A significant portion of Kinross’ business is carried on through subsidiaries. A chart showing the names of the significant subsidiaries of Kinross, as of December 31, 2023, is set out below. All subsidiaries are 100% owned (directly or indirectly) unless otherwise noted.

5

Subsidiary Governance and Internal Controls

Kinross has systems of governance, internal control over financial consolidation and reporting, and disclosure controls and procedures that apply at all levels of the Company and its subsidiaries, including those that operate in emerging markets. These systems are overseen by the Company’s board of directors (the “Board of Directors”) and are implemented by the Company’s senior management, and the senior management of its subsidiaries. The relevant features of these systems include:

Control over Subsidiaries. All of the Company’s subsidiaries are wholly-owned or controlled unless otherwise noted. Operations are overseen by a general manager employed by Kinross or the applicable foreign subsidiary, who reports to the Company’s Chief Operating Officer. Each of the subsidiaries legally owns or controls its operating assets, and the subsidiaries’ operational decisions are localized. Kinross, as the ultimate sole shareholder, has internal policies and systems in place which provide it with visibility into the operations of its subsidiaries, including its subsidiaries operating in emerging markets, and the Company’s management team is responsible for monitoring the activities of the subsidiaries.

Further, the board of directors (or similar governing body) of each subsidiary is appointed by the shareholders of such subsidiary. Directors (or those holding similar positions) may be replaced at any time by a written resolution of the shareholders (or equivalent corporate action under applicable law). Through its corporate structure, Kinross has the power to directly or indirectly appoint and replace the board members of each wholly owned subsidiary1, including those operating in emerging markets. The boards of directors (or similar governing bodies under applicable law) of Kinross’ subsidiaries (including those operating in emerging markets) act with regard to their respective fiduciary duties in the interests of the respective subsidiaries and in accordance with applicable corporate procedures, and are also accountable to Kinross and its Board of Directors and senior management.

With respect to the bank accounts of subsidiaries, Kinross has internal controls that require each of the Company’s subsidiaries to notify the Company’s treasury team before opening or closing any bank accounts. Kinross’ treasury team is also responsible for generally monitoring the activity within all such bank accounts on an ongoing basis via a web-based global treasury management system and/or web-based account access provided by the applicable financial institution to the extent available.

Strategic Direction. While the operations of each of the Company’s subsidiaries are managed locally, certain exploration strategies, external corporate financing, tax governance, additional technical support services, hedging and acquisition strategies are established centrally by the Company’s management, and, on consideration, implemented accordingly by senior management of applicable subsidiaries under the oversight of their respective boards of directors. Each operating subsidiary is responsible for the development and execution of its own risk management programs based on the enterprise risk management process established by the Company. The subsidiaries report a summary of their respective risk registers to the Company’s management on a quarterly basis which is then aggregated and summarized for reporting to the Audit and Risk Committee of the Board of Directors.

Financial Reporting. Kinross prepares its consolidated financial statements and the financial information presented in its Management’s Discussion & Analysis (“MD&A”) on a quarterly and annual basis in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”), which includes financial information and disclosures from its subsidiaries. The Company has internal controls over the preparation of its financial statements and other financial disclosures to provide reasonable assurance that its financial reporting is reliable and that the quarterly and annual financial statements and the financial information presented in its MD&A are being prepared in accordance with IFRS and applicable securities laws. These internal controls include the following:

| (a) | The Company receives quarterly reporting packages from its key operating subsidiaries including financial information and disclosures required to complete the Company’s consolidated financial statements and MD&A. Those responsible for the finance function of the Company’s subsidiaries report to the Company’s management, and the Company’s management has direct access to relevant financial information and finance personnel of the subsidiaries. |

1 Kinross has the power to appoint and replace two of the three members of the Management Committee at Peak Gold, LLC. Our joint venture partner Contango ORE, Inc. has the power to appoint and replace the third member of the Management Committee.

7

| (b) | All public disclosure documents and financial statements released by the Company relating to the Company and its subsidiaries containing material information are reviewed by senior management and approved by the Company’s disclosure committee before such material is disclosed. The disclosure committee is comprised of the Chief Financial Officer, the Chief Operating Officer and the Chief Legal Officer. With respect to quarterly reporting, including consolidated financial statements and MD&A, the disclosure committee meets to review and discuss all information prior to public disclosure. A summary of such meeting is provided to the Audit and Risk Committee by the Chief Financial Officer. The disclosure committee also receives a report on quarterly and annual sub-certifications received from senior management responsible for direct oversight of the operations of each operating subsidiary. |

| (c) | The primary responsibility of the Audit and Risk Committee is to oversee the Company’s financial reporting process on behalf of the Board of Directors of Kinross and to report the results of its activities to the Board of Directors. |

| (d) | The Audit and Risk Committee is also responsible for providing assistance to the Board of Directors in fulfilling its risk oversight responsibilities. The Audit and Risk Committee assesses the Company’s risk tolerance, the overall process for identifying the Company’s principal business and operational risks and the implementation of appropriate measures to manage and disclose such risks. |

| (e) | The Audit and Risk Committee reviews the Company’s quarterly and annual consolidated financial statements and MD&A and meets with senior management to discuss quarterly results, including accounting, disclosure and internal control matters. The Audit and Risk Committee recommends the quarterly and annual consolidated financial statements and MD&A to the Company’s Board of Directors for approval. |

| (f) | The Audit and Risk Committee receives confirmation from the Chief Executive Officer and Chief Financial Officer as to the matters addressed in the quarterly and annual certifications required under National Instrument 52-109 – Certification of Disclosure in Issuer’s Annual and Interim Filings. This confirmation is obtained from the quarterly CFO Report which provides a summary of management’s assessment and evaluation of internal control over financial reporting and disclosures control and procedures. |

| (g) | The Audit and Risk Committee periodically assesses and evaluates the adequacy of the procedures in place for the review of the Company’s public disclosure of financial information extracted or derived from the Company’s financial statements, other than the annual and interim consolidated financial statements and related notes, MD&A, earnings releases and the AIF. |

Pursuant to regulations adopted by the U.S. Securities and Exchange Commission, under the Sarbanes-Oxley Act of 2002 and those of the Canadian Securities Administrators, Kinross’ management evaluates the effectiveness of the design and operation of the Company’s disclosure controls and procedures and internal control over financial reporting. This evaluation is done under the supervision of, and with the participation of, the Company’s Chief Executive Officer and Chief Financial Officer.

These systems of corporate governance, internal control over financial reporting and disclosure controls and procedures are designed to enable, among other things, Kinross to have access to all material information about its subsidiaries, including those operating in emerging markets.

Fund Transfers from the Company’s Subsidiaries

Certain of the Company’s subsidiaries have a long history of operating in emerging markets. As noted in the Three-Year History section in this AIF, other than the period between March 2022 and the date of the divestiture of Kinross' Russian operations in June 2022, Kinross has not had any material issues with respect to transferring funds from, to or within emerging markets. Sanctions imposed by the United States, Canada and the European Union in response to Russia’s invasion of Ukraine and counter sanctions enacted by the Russian Federation, prevented certain of the Company’s subsidiaries from transferring funds out of the Russian Federation and placed limitations on the Company’s ability to transfer funds into the Russian Federation after February 2022 in order to remain compliant with all applicable laws. In all other countries that Kinross operates in, funds are transferred to, from or among Kinross’ subsidiaries pursuant to a variety of methods which include the following: chargeback of costs undertaken on behalf of the subsidiaries via intercompany invoices; advances and repayment of intercompany loans and related interest expenses; capital contributions; equity purchases; returns of capital and dividend declaration/payment by the subsidiaries. The method of transfer is dependent on the operational, financing or other arrangement established amongst Kinross and/or its applicable subsidiaries.

8

All fund transfers from Kinross’ subsidiaries are in compliance with applicable law.

Records Management of the Company’s Subsidiaries

As required by applicable law, original copies of all corporate records are required to be maintained in the language of, and stored at the offices of, each subsidiary in the jurisdiction of incorporation. However, where practical, a duplicate set of corporate records for certain subsidiaries is maintained at Kinross’ head office in Toronto. Kinross also maintains a web-based global entity management system for recording such corporate information and documents which is regularly monitored and updated by Kinross’ corporate secretarial team and/or the regional legal teams.

GENERAL DEVELOPMENT OF THE BUSINESS

Kinross is principally engaged in the mining and processing of gold and, as a by-product, silver ore and the exploration for, and the acquisition of, gold bearing properties in Canada, the United States, Brazil, Chile, Mauritania and Finland. The principal products of Kinross are gold and silver produced in the form of doré that is shipped to refineries for final processing.

Kinross’ strategy is to increase shareholder value through increases in precious metal reserves, net asset value, production, long-term cash flow and earnings per share. Kinross’ strategy also consists of optimizing the performance, and therefore, the value, of existing operations, investing in quality exploration and development projects and acquiring new potentially accretive properties and projects.

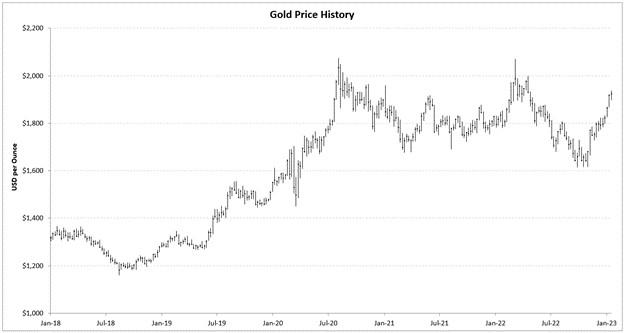

Kinross’ operations and mineral reserves are impacted by, among other things, changes in metal prices. The average gold price for 2023 based on the London Bullion Market Association PM Benchmark was $1,941.00 per ounce ($1,800.00 per ounce during 2022). Kinross used a gold price of $1,400.00 per ounce at the end of 2023 to estimate mineral reserves.

Kinross’ estimated proven and probable mineral reserves as at December 31, 2023, was 22.8 Moz. of gold and 23.7 Moz. of silver.

9

On June 1, 2021, Kinross redeemed all of its outstanding 5.125% Senior Notes due September 1, 2021, which had an aggregate principal amount of $500.0 million.

On June 16, 2021, Kinross announced the temporary suspension of mill operations at its Tasiast mine in Mauritania due to a fire that occurred on June 15, 2021. On November 10, 2021, Kinross announced that mill operations had re-started at its Tasiast mine at costs below original estimates. Kinross has received a total of $167.1 million in insurance recoveries in respect of the fire.

On July 15, 2021, Kinross announced it had signed a definitive agreement with the Government of Mauritania ("Government") with respect to its Tasiast mine and the primary exploitation permit held by Tasiast Mauritanie Limited S.A. ("TMLSA"), which includes the following key terms: (i) the continuation of tax exemptions on fuel duties2, (ii) the repayment by the Government to Kinross of approximately $40 million in outstanding VAT refunds3, (iii) the payment by the Company to the Government of $10 million to resolve disputed matters2, (iv) the introduction of an updated escalating royalty structure2 tied to the gold price that aligns with current Mauritanian mining legislation and is comparable to other royalties in the region, and (v) the nomination of two observers by the Government to the Board of Directors of the Kinross subsidiary operating the Tasiast mine.

On December 8, 2021, Kinross announced that it had entered into a definitive agreement with Great Bear Resources Ltd. (“Great Bear”) to acquire all of the issued and outstanding shares of Great Bear through a plan of arrangement (the “Arrangement”) and the acquisition was officially completed on February 24, 2022. Kinross agreed to an upfront payment of approximately $1.4 billion (C$1.8 billion), representing C$29.00 per Great Bear common share paid through a combination of cash and Kinross common shares. The arrangement also includes payment of contingent consideration in the form of a contingent value right that may be exchanged for 0.1330 of a Kinross common share per Great Bear common share, representing further potential consideration of approximately $46.0 million (C$58.2 million). The contingent consideration has a ten-year term and will be payable in connection with Kinross’ public announcement of commercial production at the Great Bear project, provided that at least 8.5 million gold ounces of mineral reserves and measured and indicated mineral resources are disclosed.

On March 7, 2022, Kinross entered into a new $1.0 billion term loan that will mature on March 7, 2025, has no mandatory amortization payments, and has a flexible repayment schedule. Kinross used the proceeds from such term loan to repay amounts drawn under its $1.5 billion revolving credit facility in connection with the closing of its acquisition of Great Bear Resources Ltd.

On April 5, 2022, Kinross announced that it had entered into a definitive agreement with the Highland Gold Mining group of companies (“Highland Gold”) and its affiliates to sell 100% of its Russian assets for total consideration of $680.0 million in cash. Following a review of the transaction by the Russian Sub-commission of the Control of Foreign Investments, which approved the transaction for a purchase price not exceeding $340.0 million, the parties adjusted the total consideration to $340.0 million in cash, with $300.0 million due on closing and $40.0 million due on the one year-anniversary of closing the transaction. The transaction closed on June 15, 2022 and all proceeds have been received.

On April 25, 2022, Kinross announced that it had entered into a sale agreement with Asante Gold Corporation (“Asante”) to sell its 90% interest in the Chirano mine in Ghana for a total consideration of $225.0 million in cash and shares. The transaction closed on August 10, 2022. In accordance with the sale agreement, the Company received $60.0 million in cash and 34,962,584 Asante shares on closing, with the remaining cash consideration to be paid across several payments due between February and May 2023 totaling $55.0 million plus interest, and $36.9 million due on each of the one-year and two-year anniversaries of closing. On February 10, 2023, Kinross and Asante amended the sale agreement in respect of the deferred payment consideration of $55.0 million due on February 10, 2023. Under the amended agreement, the receivable accrues interest at a rate of prime plus 5% until payment is received. In addition, the Company received 5.0 million Asante warrants, valued at $2.5 million, on closing of the amended agreement. During the year ended December 31, 2023, the Company received $5.0 million in respect of the deferred payment consideration. The total deferred consideration is secured through pledges by Asante of equity interests in certain acquired entities holding an indirect interest in the Chirano mine.

2 The fuel tax exemption and updated royalty structure were effective on July 1, 2020.

3 The VAT refund payments are scheduled over a five-year period.

10

On August 4, 2022, the Company amended its $1.5 billion revolving credit facility to extend the maturity by two years to August 4, 2027.

On September 19, 2022, Kinross announced an enhanced share buyback program. On September 29, 2022, Kinross received approval from the Toronto Stock Exchange to increase its normal course issuer bid (“NCIB”) program. Under the amended NCIB program, the Company was authorized to purchase up to 10% of the Company’s public float. On August 4, 2023 the Company announced that its NCIB program had been renewed for another year covering the period starting on August 9, 2023 and ending on August 8, 2024.