UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 40-F

◻ REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES

EXCHANGE ACT OF 1934

OR

⌧ ANNUAL REPORT PURSUANT TO SECTION 13 (a) OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

For the fiscal year ended December 31, 2023

Commission file number: 001-13422

AGNICO EAGLE MINES LIMITED

(Exact name of Registrant as specified in its charter)

Ontario, Canada |

|

1040 |

|

98-0357066 |

|

(Province of other jurisdiction of incorporation or organization) |

|

(Primary Standard Industrial Classification Code Number) |

|

(I.R.S. Employer Identification Number) |

145 King Street East, Suite 400

Toronto, Ontario, Canada M5C 2Y7

(416) 947-1212

(Address and telephone number of Registrant's principal executive offices)

Davies Ward Phillips & Vineberg LLP

900 Third Avenue, 24th Floor, New York, New York 10022

Attention: Jeffrey Nadler

(212) 588-5505

(Name, address (including zip code) and telephone number (including area code) of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Common Shares, without par value |

|

AEM |

|

New York Stock Exchange |

(Title of each class) |

|

(Trading Symbol(s)) |

|

(Name of each exchange on which registered) |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

For annual reports, indicate by check mark the information filed with this Form:

⌧ Annual information form ⌧ Audited annual financial statements

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

497,299,441 Common Shares as of December 31, 2023

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ⌧ No ◻

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Yes ⌧ No ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging growth company ◻

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ◻

† The term "new or revised financial accounting standard" refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ⌧

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ◻ Agnico Eagle Mines Limited (“Agnico Eagle” or the “Company”) is a Canadian issuer eligible to file its annual report pursuant to Section 13 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), on Form 40-F pursuant to the multi-jurisdictional disclosure system of the Exchange Act (the “MJDS”).

EXPLANATORY NOTE

The Company is a “foreign private issuer” as defined in Rule 405 under the Securities Act of 1933, as amended. Equity securities of the Company are accordingly exempt from Sections 14(a), 14(b), 14(c), 14(f) and 16 of the Exchange Act pursuant to Rule 3a12-3.

FORWARD-LOOKING INFORMATION

This Annual Report on Form 40-F and the exhibits attached hereto (this “Form 40-F”) contain “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995. These statements relate to, among other things, the Company’s plans, objectives, expectations, estimates, beliefs, strategies and intentions and can generally be identified by the use of words such as “anticipate”, “believe”, “budget”, “could”, “estimate”, “expect”, “forecast”, “intend”, “likely”, “may”, “plan”, “project”, “schedule”, “should”, “target”, “will”, “would” or other variations of these terms or similar words. Forward-looking statements in this Form 40-F include, but are not limited to, the following:

| ● | the Company’s outlook for 2024 and future periods, including estimates of metal production, ore grades, ore tonnage, recovery rates, project timelines, drilling results, life of mine, total cash costs per ounce, all-in sustaining costs per ounce, minesite costs per tonne, other expenses, cash flows; |

| ● | statements regarding future earnings and the sensitivity of earnings to gold and other metal prices; |

| ● | anticipated levels or trends for prices of gold and by-product metals mined by the Company or for exchange rates between currencies in which capital is raised, revenue is generated or expenses are incurred by the Company; |

| ● | estimates of future capital expenditures, exploration expenditures, development expenditures and other cash needs, and expectations as to the funding thereof; |

| ● | estimated timing and conclusions of studies, analyses and evaluations undertaken by the Company or others; |

| ● | statements regarding the projected exploration, development and exploitation of ore deposits, including estimates of the timing of such exploration, development and production or decisions with respect thereto; |

| ● | estimates of mineral reserves and mineral resources and their sensitivities to gold prices and other factors, ore grades and mineral recoveries and statements regarding anticipated future exploration results; |

| ● | anticipated timing of events at the Company’s mines, mine development projects and exploration projects; |

| ● | methods by which ore will be extracted or processed; |

| ● | estimates of future costs and other liabilities for environmental remediation; |

| ● | statements concerning expansion projects, mill throughput, optimization and projected exploration, including costs and other estimates upon which such projections are based; |

| ● | statements regarding the Company's ability to obtain the necessary permits and authorizations in connection with its current or proposed operations and the anticipated timing thereof; |

| ● | statements regarding the sufficiency of the Company's cash resources; |

| ● | statements regarding anticipated legislation and regulations, including with respect to climate change, and estimates of the impact thereof on the Company; |

| ● | other anticipated trends with respect to the Company’s capital resources and results of operations; and |

| ● | statements regarding the impact of pandemics and other health emergencies, and measures taken to reduce the spread of such pandemics or other health emergencies on the Company’s future operations and business. |

Forward-looking statements are necessarily based upon a number of factors and assumptions that, while considered reasonable by Agnico Eagle as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The factors and assumptions of Agnico Eagle upon which the forward-looking statements in this Form 40-F are based, and which may prove to be incorrect, include the assumptions set out elsewhere in this Form 40-F as well as: that there are no significant disruptions affecting Agnico Eagle’s operations, whether due to labour disruptions, supply disruptions, damage to equipment, natural or man-made occurrences, pandemics, mining or milling issues, political changes, title issues, community protests, including by First Nations groups, or otherwise; that permitting, development, expansion and the ramp up of operations at each of Agnico Eagle’s mines, mine development projects and exploration projects proceed on a basis consistent with expectations and that Agnico Eagle does not change its exploration or development plans relating to such projects; that the exchange rates between the Canadian dollar, Euro, Australian dollar, Mexican peso and the U.S. dollar will be approximately consistent with current levels or as set out in this Form 40-F and the Company’s management discussion and analysis for the year ended December 31, 2023 (the “Annual MD&A”); that prices for gold, silver, zinc and copper will be consistent with Agnico Eagle’s expectations; that prices for key mining and construction supplies, including labour costs, remain consistent with Agnico Eagle’s expectations; that production meets expectations; that Agnico Eagle’s current estimates of mineral reserves, mineral resources, mineral grades and mineral recoveries are accurate; that there are no material delays in the timing for completion of development projects; that seismic activity at the Company’s operations at LaRonde, Goldex and other properties is as expected by the Company; that the Company’s current plans to optimize production are successful; and that there are no material variations in the current tax and regulatory environments that affect Agnico Eagle; and that governments, the Company or others do not take measures in response to pandemics or other health emergencies or otherwise that, individually or in the aggregate, materially affect the Company’s ability to operate its business; that measures taken in connection with pandemics or other health emergencies do not affect productivity; that measures taken relating to, or other effects of a pandemic or other health emergency do not affect the Company’s ability to obtain necessary supplies and deliver them to its mine sites.

The forward-looking statements in this Form 40-F reflect the Company’s views as at the date hereof and involve known and unknown risks, uncertainties and other factors which could cause the actual results, performance or achievements of the Company or industry results to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, the risk factors set out under “Risk Factors” on page 74 of the Company’s annual information form for the year ended December 31, 2023, which is filed as Exhibit 99.1 to this Form 40-F and incorporated by reference herein (the “AIF”). Given these uncertainties, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date made. Except as otherwise required by law, the Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any such statements to reflect any change in the Company’s expectations or any change in events, conditions or circumstances on which any such statement is based. This Form 40-F contains information regarding anticipated total cash costs per ounce, all-in sustaining costs per ounce, minesite costs per tonne sustaining capital expenditures and development capital expenditures and operating margin in respect of the Company or at certain of the Company’s mines and mine development projects. The Company believes that these generally accepted industry measures are realistic indicators of operating performance and are useful in allowing year over year comparisons. Investors are cautioned that this information may not be suitable for other purposes.

CURRENCY

Agnico Eagle presents its consolidated financial statements in United States dollars. All dollar amounts in this Form 40-F are stated in United States dollars (“U.S. dollars”, “$” or “US$”), except where otherwise indicated. On March 18, 2024, the exchange rate (based on the daily average exchange rate as reported by the Bank of Canada) for U.S. dollars into Canadian dollars (“C$”) was US$1.00 equals C$1.3541.

NOTES TO INVESTORS REGARDING THE USE OF MINERAL RESOURCES

The mineral reserve and mineral resource estimates contained in this Form 40-F have been prepared in accordance with the Canadian Security Administrators’ (“CSA”) National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”).

Effective February 25, 2019, the SEC’s disclosure requirements and policies for mining properties are more closely aligned with current industry and global regulatory practices and standards, including NI 43-101. However, Canadian issuers that report in the United States using the MJDS, such as Agnico Eagle, may still use NI 43-101 rather than the SEC’s disclosure requirements when using the SEC’s MJDS registration statement and annual report forms. Accordingly, mineral reserve and mineral resource information contained or incorporated by reference herein may not be comparable to similar information disclosed by U.S. companies.

Investors are cautioned that while the SEC now recognizes “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources”, investors should not assume that any part or all of the mineral deposits in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. These terms have a great amount of uncertainty as to their economic and legal feasibility. Accordingly, investors are cautioned not to assume that any “measured mineral resources”, “indicated mineral resources”, or “inferred mineral resources” that the Company reports in this Form 40-F are or will be economically or legally mineable.

Further, “inferred mineral resources” have a great amount of uncertainty as to their existence and as to their economic and legal feasibility. It cannot be assumed that any part or all of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian regulations, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in limited circumstances. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists, or is or will ever be economically or legally mineable.

The mineral reserve and mineral resource data contained or incorporated by reference herein are estimates, and no assurance can be given that the anticipated tonnages and grades will be achieved or that the indicated level of recovery will be realized. The Company does not include equivalent gold ounces for by-product metals contained in mineral reserves in its calculation of contained ounces and mineral reserves are not reported as a subset of mineral resources. See “Mineral Reserves and Mineral Resources” in the AIF for additional information.

NOTE TO INVESTORS CONCERNING CERTAIN MEASURES OF PERFORMANCE

This Form 40-F presents certain financial performance measures, including “total cash costs per ounce”, “all-in sustaining costs per ounce”, “minesite costs per tonne”, “adjusted net income”, “adjusted net income per share”, “realized prices”, “sustaining capital expenditures”, “development capital expenditures” and “operating margin” that are not standardized measures under International Financial Reporting Standards (“IFRS”). These measures may not be comparable to similar measures reported by other gold producers. For a reconciliation of these measures to the most directly comparable financial information presented in the consolidated financial statements prepared in accordance with IFRS, and for an explanation of how management uses these measures and why management believes them to be useful to investors, please see the Company’s management’s discussion and analysis for the year ended December 31, 2023, which is filed as Exhibit 99.3 to this Form 40-F and incorporated by reference herein (the “Annual MD&A”). The Company believes that these generally accepted industry measures are realistic indicators of operating performance and are useful in allowing year over year comparisons. However, these non-IFRS measures should be considered together with other data prepared in accordance with IFRS, and these measures, taken by themselves, are not necessarily indicative of operating costs or cash flow measures prepared in accordance with IFRS. This Form 40-F also contains information as to estimated future total cash costs per ounce, all-in sustaining costs per ounce and minesite costs per tonne. The estimates of total cash costs per ounce, all-in sustaining costs per ounce and minesite costs per tonne are based upon the total cash costs per ounce, all-in sustaining costs per ounce and minesite costs per tonne that the Company expects to incur to mine gold at its projects and, consistent with the reconciliation of these actual costs referred to above, do not include production costs attributable to accretion expense and other asset retirement costs, which will vary over time as each project is developed and mined. It is therefore not practicable to reconcile these forward-looking non-IFRS financial measures to the most comparable IFRS measure.

DISCLOSURE CONTROLS AND PROCEDURES

The Company’s management, with the participation of the Company’s Chief Executive Officer and Chief Financial Officer, evaluated the effectiveness of the Company’s disclosure controls and procedures as of December 31, 2023 pursuant to Rule 13a-15 under the Exchange Act. In designing and evaluating the disclosure controls and procedures, management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the desired control objectives. In addition, the design of disclosure controls and procedures must reflect the fact that there are resource constraints and that management is required to apply its judgment in evaluating the benefits of possible controls and procedures relative to their costs.

Based on such evaluation, the Company’s Chief Executive Officer and Chief Financial Officer concluded that, as of December 31, 2023, the Company’s disclosure controls and procedures were designed at a reasonable assurance level and were effective to provide reasonable assurance that information the Company is required to disclose in reports that the Company files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in SEC rules and forms, and that such information is accumulated and communicated to the Company’s management, including the Company’s Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

MANAGEMENT’S ANNUAL REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

Management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting. Internal control over financial reporting is a process designed by, or under the supervision of, the Company’s Chief Executive Officer and Chief Financial Officer and effected by the Company’s board of directors (the “Board”), management and other personnel to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

The Company’s management, including the Company’s Chief Executive Officer and Chief Financial Officer, assessed the effectiveness of the Company’s internal control over financial reporting as of December 31, 2023. In making this assessment, the Company’s management used the criteria set out by the Committee of Sponsoring Organizations of the Treadway Commission in Internal Control — Integrated Framework (2013). Based upon its assessment, management concluded that, as of December 31, 2023, the Company’s internal control over financial reporting was effective.

Ernst & Young LLP, an independent registered public accounting firm, has audited the Annual Financial Statements and has included its attestation report on management’s assessment of the Company’s internal control over financial reporting, which is found on page 2 of the Annual Financial Statements.

The Company will continue to periodically review its disclosure controls and procedures and internal control over financial reporting and may make modifications from time to time as considered necessary or desirable.

ATTESTATION REPORT OF THE REGISTERED PUBLIC ACCOUNTING FIRM

Ernst & Young LLP’s attestation report on management’s assessment of the Company’s internal control over financial reporting is found on page 6 of the Annual Financial Statements.

CHANGES IN INTERNAL CONTROL OVER FINANCIAL REPORTING

Management regularly reviews its system of internal control over financial reporting and makes changes to the Company’s processes and systems to improve controls and increase efficiency, while ensuring that the Company maintains an effective internal control environment. Changes may include such activities as implementing new, more efficient systems, consolidating activities, and migrating processes.

During the year ended December 31, 2023, there have been no changes in the Company’s internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting

NOTICES PURSUANT TO REGULATION BTR

The Company did not send any notices required by Rule 104 of Regulation BTR during the year ended December 31, 2023 concerning any equity security subject to a blackout period under Rule 101 of Regulation BTR.

IDENTIFICATION OF THE AUDIT COMMITTEE

The Board has a separately-designated standing Audit Committee established in accordance with Section 3(a)(58)(A) of the Exchange Act. The Audit Committee is composed of Mr. Jeffrey Parr (Chair), Mr. J. Merfyn Roberts and Mr. Jamie Sokalsky, as described under “Audit Committee — Composition of the Audit Committee” on page 99 of the AIF.

AUDIT COMMITTEE FINANCIAL EXPERT

The Board has determined that the Company has at least one “audit committee financial expert” (as defined in paragraph (8) of General Instruction B to Form 40-F) and that Mr. Jeffrey Parr, Mr. J. Merfyn Roberts and Mr. Jamie Sokalsky are the Company’s “audit committee financial experts” serving on the Audit Committee of the Board. Each of the Audit Committee financial experts is “independent” under applicable listing standards.

PRINCIPAL ACCOUNTANT FEES AND SERVICES

Ernst & Young LLP, Toronto, Canada, PCAOB ID No. 1263, served as the Company’s independent public accountant for each of the fiscal years in the two-year period ended December 31, 2023. For a description of the total amount billed to the Company by Ernst & Young LLP for services performed in the last two fiscal years by category of service (audit fees, audit-related fees, tax fees and all other fees), see “Audit Committee — External Auditor Service Fees” on page 100 of the AIF. No audit-related fees, tax fees or other non-audit fees were approved by the Audit Committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

AUDIT COMMITTEE PRE-APPROVAL POLICIES AND PROCEDURES

For a description of the pre-approval policies and procedures of the Company’s Audit Committee, see “Audit Committee — Pre-Approval Policies and Procedures” on page 100 of the AIF.

CODE OF ETHICS

The Company has a “code of ethics” (as defined in paragraph (9) of General Instruction B to Form 40-F) that applies to its Chief Executive Officer, Chief Financial Officer, principal accounting officer, controller and persons performing similar functions. The Company’s Code of Business Conduct and Ethics is available on the Company’s website at www.agnicoeagle.com or, without charge, upon request from the Corporate Secretary, Agnico Eagle Mines Limited, Suite 400, 145 King Street East, Toronto, Ontario M5C 2Y7 (telephone 416-947-1212).

On July 26, 2023, the Company’s Code of Business Conduct and Ethics was amended with effect from July 26, 2023 to add (i) an addendum concerning conflicts of interests and transparency, (ii) a summary section to the Company’s Code of Business Conduct and Ethics and (iii) references to the Company’s workplace violence, harassment and discrimination policy. In addition to these changes, certain technical, administrative and other non-substantive amendments were made to the Company’s Code of Business Conduct and Ethics. An amended version of the Company’s Code of Business Conduct and Ethics, which reflects the revisions described above, is filed as Exhibit 99.14 to this Form 40-F.

Except as described above, during the fiscal year ended December 31, 2023 there have not been any amendments to, or waivers of, including implicit waivers of, any provision of the Company’s Code of Business Conduct and Ethics which is applicable to the Company’s Chief Executive Officer, Chief Financial Officer, principal accounting officer or controller, or persons performing similar functions and that relates to any element of the code of ethics definition enumerated in paragraph (9)(b) of General Instruction B to Form 40-F.

OFF-BALANCE SHEET ARRANGEMENTS

The Company does not have any off-balance sheet arrangements (as defined in paragraph (11) of General Instruction B to Form 40-F) that have or are reasonably likely to have a current or future effect on the Company’s financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to investors.

CONTRACTUAL OBLIGATIONS

For tabular disclosure of the Company’s contractual obligations, see page 27 of the Annual MD&A under the heading “Liquidity and Capital Resources — Contractual Obligations”.

MINE SAFETY DISCLOSURE

Not applicable.

CORPORATE GOVERNANCE

The Company is subject to a variety of corporate governance guidelines and requirements enacted by the Toronto Stock Exchange (the ”TSX”), the Canadian securities regulatory authorities, the New York Stock Exchange (the ”NYSE”) and the SEC. The Company is listed on the NYSE and, although the Company is not required to comply with most of the NYSE corporate governance requirements to which the Company would be subject if it were a U.S. corporation, the Company’s governance practices differ from those required of U.S. domestic issuers in only the following respects. The NYSE rules for U.S. domestic issuers require shareholder approval of all equity compensation plans (as defined in the NYSE rules) regardless of whether new issuances, treasury shares or shares that the Company has purchased in the open market are used. The TSX rules require shareholder approval of share compensation arrangements involving new issuances of shares, and of certain amendments to such arrangements, but do not require such approval if the compensation arrangements involve only shares purchased in the open market. The NYSE rules for U.S. domestic issuers also require shareholder approval of certain transactions or series of related transactions that result in the issuance of common shares, or securities convertible into or exercisable for common shares, that have, or will have upon issuance, voting power equal to or in excess of 20% of the voting power outstanding prior to the transaction or if the issuance of common shares, or securities convertible into or exercisable for common shares, are, or will be upon issuance, equal to or in excess of 20% of the number of common shares outstanding prior to the transaction. The TSX rules require shareholder approval of acquisition transactions resulting in dilution in excess of 25%. The TSX also has broad general discretion to require shareholder approval in connection with any issuances of listed securities. The Company complies with the TSX rules described in this paragraph.

RECOVERY OF ERRONEOUSLY AWARDED COMPENSATION

The Company has adopted a compensation recovery policy, most recently amended effective July 26, 2023 (referred to as the “Executive Compensation Clawback Policy”) as required by NYSE listing standards and pursuant to Rule 10D-1 of the Exchange Act. The Executive Compensation Clawback Policy is filed as Exhibit 97 to this Form 40-F. At no time during or after the fiscal year ended December 31, 2023 (as of the date of this Form 40-F), was the Company required to prepare an accounting restatement that required recovery of erroneously awarded compensation pursuant to the Executive Compensation Clawback Policy and, as of December 31, 2023, there was no outstanding balance of erroneously awarded compensation to be recovered from the application of the Executive Compensation Clawback Policy to a prior restatement.

DISCLOSURE PURSUANT TO SECTION 13(r) OF THE EXCHANGE ACT

In accordance with Section 13(r) of the Exchange Act, the Company is required to include certain disclosures in its periodic reports if it or any of its affiliates knowingly engaged in certain specified activities during the period covered by the report. Neither the Company nor its affiliates have knowingly engaged in any transaction or dealing reportable under Section 13(r) of the Exchange Act during the year ended December 31, 2023.

UNDERTAKING

Agnico Eagle undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the SEC staff, and to furnish promptly, when requested to do so by the SEC staff, information relating to: the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

CONSENT TO SERVICE OF PROCESS

Any change to the name or address of the Company’s agent for service shall be communicated promptly to the SEC by amendment to the Form F-X referencing the file number of the Company.

INCORPORATION BY REFERENCE

This Form 40-F, which includes the exhibits filed herewith (other than the section of the AIF entitled “Ratings”), is incorporated by reference into the Company’s Registration Statements on Form F-3 (File No. 333-271854) and Form S-8 (File Nos. 333-130339 and 333-152004).

EXHIBIT INDEX

Exhibit |

|

Description |

97 |

|

|

99.1 |

|

Annual Information Form of the Company for the year ended December 31, 2023 |

99.2 |

|

|

99.3 |

|

Management’s Discussion and Analysis for the year ended December 31, 2023 |

99.4 |

|

|

99.5 |

|

|

99.6 |

|

|

99.7 |

|

|

99.8 |

|

|

99.9 |

|

|

99.10 |

|

|

99.11 |

|

|

99.12 |

|

|

99.13 |

|

|

99.14 |

|

|

101.INS |

|

XBRL Instance |

101.SCH |

|

XBRL Taxonomy Extension Schema |

101.CAL |

|

XBRL Taxonomy Extension Calculation Linkbase |

101.DEF |

|

XBRL Taxonomy Extension Definition Linkbase |

101.LAB |

|

XBRL Taxonomy Extension Label Linkbase |

101.PRE |

|

XBRL Taxonomy Extension Presentation Linkbase |

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Company certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

Toronto, Canada |

|

AGNICO EAGLE MINES LIMITED |

|

March 22, 2024 |

|

|

|

|

|

by |

/s/ Jamie Porter |

|

|

|

|

|

|

|

Jamie Porter |

|

|

|

Executive Vice-President, Finance and |

|

|

|

Chief Financial Officer |

Exhibit 97

AGNICO EAGLE MINES LIMITED

EXECUTIVE INCENTIVE COMPENSATION RECOUPMENT POLICY

I. |

INTRODUCTION |

1. |

Purpose |

The board of directors (the “Board”) of Agnico Eagle Mines Limited (together with its affiliates, the “Corporation”) believes that it is in the best interests of the Corporation to adopt this executive compensation clawback policy (the “Policy”) to enhance the Corporation’s alignment with good compensation governance practices and to assist the Corporation in managing its reputation and compensation related risk. Among other things, this Policy is intended to comply with (i) Section 304 of the United States Sarbanes-Oxley Act of 2002 (see Part II below) and (ii) Section 10D of the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), Rule 10D-1 promulgated under the Exchange Act (“Rule 10D-1”) and Section 303A.14 of the New York Stock Exchange Listed Corporation Manual (the “NYSE Listing Standards”) (see Part III below).

2. |

Authority |

Except as specifically set forth herein, the Policy shall be administered by the Compensation Committee of the Board of Directors (the “Administrator”). The Administrator is authorized to interpret and construe the Policy and to make all determinations necessary, appropriate or advisable for the administration of the Policy. Any determinations made by the Administrator shall be final and binding on all affected individuals.

In the administration of the Policy, the Administrator is authorized and directed to consult with the full Board or such other committees of the Board as may be necessary or appropriate as to matters within the scope of such other committee’s responsibility and authority. Subject to any limitation at applicable law, the Administrator may authorize and empower any officer or employee of the Corporation to take any and all actions necessary or appropriate to carry out the purpose and intent of the Policy (other than with respect to any recovery under the Policy involving such officer or employee).

3. |

Amendment; Termination |

The Board may amend, modify, supplement, rescind or replace all or any portion of the Policy at any time and from time to time in its discretion, and shall amend the Policy as it deems necessary to comply with applicable law or any rules or standards adopted by a securities exchange on which the Corporation’s securities are listed.

4. |

Severability |

If any provision of the Policy or its application shall be adjudicated to be invalid, illegal or unenforceable in any respect, such invalidity, illegality or unenforceability shall not affect any other provisions of the Policy, and the invalid, illegal or unenforceable provisions shall be deemed amended to the minimum extent necessary to render any such provision or application enforceable.

5. |

Other Recoupment Rights |

The Board intends that the Policy shall be applied to the fullest extent permitted by law. Any right of recoupment under the Policy is in addition to, and not in lieu of, any other remedies or rights of recoupment that may be available to the Corporation under applicable law, rules or regulations with respect to the claw back or recoupment of erroneously awarded compensation or pursuant to the terms of any employment agreement, equity award agreement, or similar agreement. To the extent that the Corporation, the Board, or any committee of the Board is required to comply with any such laws, rules or regulations, the Policy shall be read to incorporate such requirements to the extent applicable.

6. |

Other Claims |

Nothing contained in the Policy, and no recoupment or recovery as contemplated by the Policy, shall limit any claims, damages or other legal remedies the Corporation or any of its affiliates may have against any person arising out of or resulting from any actions or omissions by such person.

7. |

Absence of Conflicts |

Subject to Section 5(b) of Part III of the Policy, the application of the Policy by the Administrator may result in recoupment of compensation pursuant to Part II or Part III of the Policy or both Part II and Part III of the Policy, as determined to be necessary, appropriate and advisable.

8. |

Successors |

The Policy shall be binding and enforceable against all persons subject thereto and their beneficiaries, heirs, executors, administrators or other legal representatives.

9. |

Disclosure Requirements |

The Corporation shall file all disclosures with respect to the Policy required by applicable laws and regulations, including applicable rules of the United States Securities and Exchange Commission (“SEC”).

II. |

SARBANES-OXLEY CLAWBACK |

Part II of the Policy is designed to comply with, and shall be interpreted in a manner consistent with, the provisions of Section 304 of the United States Sarbanes-Oxley Act of 2002.

1. |

Definitions |

As used in this Part II of the Policy, the following capitalized terms have the meanings set out below:

"Executives" means each officer or employee of the Corporation at the level of "Executive Vice President" or above, including, without limitation, the Executive Chair, the Chief Executive and Chief Financial Officer, and "Executive" means any one of the Executives.

"Incentive Compensation" means compensation relating to the achievement of financial or performance goals or similar conditions, any award or payment under the Corporation's annual incentive plan or long term incentive plan and any bonus payment, stock options, performance share unit, restricted share unit or other award of equity based compensation whether vesting is based on the achievement of performance conditions, the passage of time or both.

"Overcompensation Amount" has the meaning set out below in Section 3 of Part II of this Policy.

"Part II Effective Date" means January 1, 2015.

"Restatement" means an accounting restatement or the correction of a material error due to the Corporation's material non-compliance with any applicable financial reporting requirement, other than as a result of a change or amendment in accounting principles or securities laws.

"Restatement Date" means the date upon which the Corporation is required to prepare a Restatement.

"Wrongful Conduct" shall mean fraud, gross negligence or intentional misconduct.

2. |

Application |

Part II of the Policy applies to all persons who are or become Executives on or after the Part II Effective Date and applies to all Incentive Compensation awarded, granted or paid to an Executive on or after the Part II Effective Date. The right of recoupment survives the cessation of an Executive's employment in such capacity.

3. |

Determination of Overcompensation Amounts |

If (i) the Corporation is required to prepare a Restatement; or (ii) the Board determines that an Executive has engaged in Wrongful Conduct, the Board will review all Incentive Compensation paid or granted to Executives on the basis of having met or exceeded specific performance targets for performance periods during the time period covered by the Restatement or in which the Wrongful Conduct occurred, as applicable. Any determination made by the Board under Part II of the Policy shall be final, binding and conclusive on all parties.

To the extent permitted by applicable law and taking into account all factors considered relevant by the Board in its sole discretion, the Board may seek to recoup Incentive Compensation paid or granted to any current or former Executive in the three (3) year period preceding the date of the Restatement or the Wrongful Conduct, if and to the extent that (i) the amount or the granting of Incentive Compensation was calculated based upon the achievement of certain financial results or performance targets that were subsequently reduced or otherwise determined not to have been properly achieved due to a Restatement or the Wrongful Conduct, and (ii) the amount or the granting of Incentive Compensation that would have been paid or granted to the Executive had the financial results been properly reported or the performance targets been properly determined would have been lower than the amount actually paid or granted (the difference between the amounts determined in (i) and (ii) being the "Overcompensation Amount").

4. |

Recoupment of Overcompensation Amounts |

To the extent that an Executive received an Overcompensation Amount, the Board shall be entitled:

(a)to the extent the Overcompensation Amount has been paid, transferred or otherwise made available to the Executive, require, by written demand, the Executive to reimburse the Corporation for all or part of the Overcompensation Amount;

(b)to the extent the Overcompensation Amount has not been paid, transferred or otherwise made available to the Executive by the Corporation, the right of the Executive to the Overcompensation Amount shall be immediately forfeited by the Executive and/or cancelled by the Corporation, to the extent required such that, if recalculated following such forfeiture or cancellation, the Overcompensation Amount is equal to zero; and

(c)to the extent the Overcompensation Amount is not immediately recovered upon demand from the Executive, or forfeited and/or cancelled, require any compensation owing by the Corporation to the Executive including any salary or any unvested or unexercised Incentive Compensation, be immediately withheld and/or irrevocably cancelled by the Corporation to compensate for the Overcompensation Amount or any unrecovered portion thereof, and to bring any other actions against the Executive which they may deem necessary or advisable to recover the Overcompensation Amount.

The Corporation may recover the Overcompensation Amount from the Executive (i) in the case of a Restatement, for three years from the Restatement Date, and (ii) in the case of Wrongful Conduct, if the Wrongful Conduct has been discovered by the Corporation within 36 months from the date on which the Wrongful Conduct occurred. Recoupment of Overcompensation Amounts under Part II of the Policy shall be initiated by the Corporation at the request of the Board, and all amounts recoverable or payable hereunder shall be paid to the Corporation or as otherwise directed by the Board.

5. |

Effective Date of Part II of the Policy |

This Part II of the Policy is intended to replace the Agnico Eagle Mines Limited Executive Incentive Compensation Recoupment Policy, as of March 2021, and shall apply to all Incentive Compensation awarded, granted or paid to an Executive on or after January 1, 2015.

III. |

DODD-FRANK CLAWBACK |

Part III of the Policy is intended to comply with, and shall be interpreted to be consistent with, Section 10D of the Exchange Act, Rule 10D-1 and Section 303A.14 of the NYSE Listing Standards.

1. |

Definitions |

As used in this Part III of the Policy, the following capitalized terms have the meanings set out below:

“Accounting Restatement” means an accounting restatement due to the material noncompliance of the Corporation with any financial reporting requirement under securities laws, including any required accounting restatement to correct an error in previously issued financial statements that is material to the previously issued financial statements (a “Big R” restatement), or that would result in a material misstatement if the error were corrected in the current period or left uncorrected in the current period (a “little r” restatement).

“Applicable Period” means the three completed fiscal years immediately preceding the date on which the Corporation is required to prepare an Accounting Restatement, as well as any transition period (that results from a change in the Corporation’s fiscal year) within or immediately following those three completed fiscal years (except that a transition period that comprises a period of at least nine months shall count as a completed fiscal year).

The “date on which the Corporation is required to prepare an Accounting Restatement” is the earlier to occur of (a) the date the Board, a committee of the Board, or the officer or officers of the Corporation authorized to take such action (if Board action is not required) concludes, or reasonably should have concluded, that the Corporation is required to prepare an Accounting Restatement or (b) the date a court, regulator or other legally authorized body directs the Corporation to prepare an Accounting Restatement, in each case regardless of if or when the restated financial statements are filed.

“Erroneously Awarded Compensation” has the meaning set forth in Section 4 of this Part III of the Policy.

“Executives” means the Corporation’s current and former executive chair, president, chief executive officer, principal financial officer, principal accounting officer (or, if there is no such accounting officer, the controller), any vice-president of the Corporation in charge of a principal business unit, division or function (such as sales, administration or finance), any other executive who performs a policy-making function, or any other person who performs similar policy-making functions for the Corporation, as determined by the Administrator in accordance with the definition of executive officer set forth in Rule 10D-1 and the NYSE Listing Standards.

“Financial Reporting Measure” means measures that are determined and presented in accordance with the accounting principles used by the Corporation in preparing its financial statements, and all other measures that are derived wholly or in part from such measures. Share price and total shareholder return (and any measures that are derived wholly or in part from share price or total shareholder return) shall, for purposes of this Part III of the Policy, be considered Financial Reporting Measures. For the avoidance of doubt, a Financial Reporting Measure need not be presented within the Corporation’s financial statements or included in a filing with any securities regulatory authority, including the SEC.

“Incentive-Based Compensation” means any compensation that is granted, earned or vested based wholly or in part upon the attainment of a Financial Reporting Measure.

Incentive-Based Compensation is “received” for purposes of this Part III of the Policy in the Corporation’s fiscal period during which the Financial Reporting Measure specified in the Incentive-Based Compensation award is attained, even if the payment or grant of such Incentive-Based Compensation occurs after the end of that period.

2. |

Covered Executives; Incentive-Based Compensation |

Part III of the Policy applies to Incentive-Based Compensation received by an Executive (i) after beginning services as an Executive; (ii) if the Executive served as an Executive at any time during the performance period for such Incentive-Based Compensation; and (iii) while the Corporation has (or had) a class of securities listed on the New York Stock Exchange (“NYSE”) or any other U.S. national securities exchange.

3. |

Recoupment of Erroneously Awarded Compensation in the Event of an Accounting Restatement |

If the Corporation is required to prepare an Accounting Restatement, the Corporation shall promptly recoup the amount of any Erroneously Awarded Compensation received by any Executive during the Applicable Period as calculated pursuant to Section 4 of this Part III of the Policy.

4. |

Erroneously Awarded Compensation: Amount Subject to Recovery |

The amount of Erroneously Awarded Compensation subject to recovery under this Part III of the Policy, as determined by the Administrator, is the amount of Incentive-Based Compensation received by the Executive that exceeds the amount of Incentive Based-Compensation that would have been received by the Executive had it been determined based on the restated amounts.

Erroneously Awarded Compensation shall be computed by the Administrator without regard to any taxes paid by the Executive in respect of the Erroneously Awarded Compensation.

For Incentive-Based Compensation based on share price or total shareholder return, where the amount of Erroneously Awarded Compensation is not subject to mathematical recalculation directly from the information in the applicable Accounting Restatement:

(a) |

the Administrator shall determine the amount of Erroneously Awarded Compensation based on a reasonable estimate of the effect of the Accounting Restatement on the share price or total shareholder return upon which the Incentive-Based Compensation was received; and |

(b) |

the Corporation shall maintain documentation of the determination of that reasonable estimate and provide such documentation to the NYSE. |

5. |

Method of Recoupment |

(a) |

The Administrator shall have discretion to determine the appropriate means of recouping Erroneously Awarded Compensation based on the particular facts and circumstances. Notwithstanding the foregoing, except as set forth in Section 6 of this Part III of the Policy, in |

no event may the Corporation accept an amount that is less than the amount of Erroneously Awarded Compensation in satisfaction of an Executive’s obligations hereunder.

(b) |

To the extent that the Executive reimburses the Corporation for any Incentive-Based Compensation received that constitutes Erroneously Awarded Compensation under any duplicative recovery obligation established by the Corporation in the Policy or otherwise, or pursuant to applicable law, any such reimbursed amount may be credited to the amount of Erroneously Awarded Compensation that is subject to recovery under this Part III of the Policy. |

(c) |

To the extent that an Executive fails to repay all Erroneously Awarded Compensation to the Corporation when due, the Corporation shall take all actions reasonable and appropriate to recover such Erroneously Awarded Compensation from the applicable Executive. The applicable Executive shall be required to reimburse the Corporation for any and all expenses reasonably incurred (including legal fees) by the Corporation in recovering such Erroneously Awarded Compensation in accordance with the immediately preceding sentence. |

6. |

Exceptions to Recovery |

The Corporation will recover Erroneously Awarded Compensation in compliance with this Part III of the Policy unless any of the following conditions are met and the Administrator determines that recovery would be impracticable:

(a) |

The direct expense paid to a third party to assist in enforcing this Part III of the Policy would exceed the amount to be recovered. Before concluding that it would be impracticable to recover any amount of Erroneously Awarded Compensation based on the expense of enforcement, the Corporation must make a reasonable attempt to recover such Erroneously Awarded Compensation, document such reasonable attempt(s) to recover, and provide that documentation to the NYSE. |

(b) |

Recovery would violate applicable Canadian federal or provincial law (provided that law was adopted prior to November 28, 2022). Before concluding that it would be impracticable to recover any amount of Erroneously Awarded Compensation based on violation of Canadian federal or provincial law, the Corporation shall obtain an opinion of Canadian counsel, acceptable to the NYSE, that recovery would result in such a violation, and must provide such opinion to the NYSE. |

(c) |

Recovery would likely cause an otherwise tax-qualified retirement plan, under which benefits are broadly available to employees of the Corporation, to fail to meet the requirements of Section 401(a)(13) or 411(a) of the United States Internal Revenue Code and the regulations thereunder. |

7. |

No indemnification of Executives |

The Corporation shall not insure or indemnify any Executive against (i) the loss of any Erroneously Awarded Compensation that is repaid, returned or recovered pursuant to the terms of this Part III of the Policy, or (ii) any claims relating to the Corporation’s enforcement of its rights under this Part III of the Policy. The Corporation shall not enter into any agreement that exempts any Incentive-Based Compensation that is granted, paid or awarded to an Executive from the application of this Part III of the Policy or that waives the Corporation’s right to recovery of any

Erroneously Awarded Compensation, and this Part III of the Policy shall supersede any such agreement (whether entered into before, on or after the Effective Date of this Part III of the Policy).

8. |

Effective Date; Retroactive Application |

Part III of the Policy shall be effective as of October 2, 2023 (the “Part III Effective Date”). The terms of Part III of the Policy shall apply to any Incentive-Based Compensation that is received by Executives on or after the Part III Effective Date, even if such Incentive-Based Compensation was approved, awarded, granted or paid to Executives prior to the Part III Effective Date. Without limiting the generality of Section 5 of this Part III of the Policy, and subject to applicable law, the Administrator may affect recovery under this Part III of the Policy from any amount of compensation approved, awarded, granted, payable or paid to the Executive prior to, on or after the Part III Effective Date.

[TO BE SIGNED BY AGNICO EXECUTIVES:]

Acknowledgment of the Agnico Eagle Mining Limited Executive Incentive Compensation Recoupment Policy

I, the undersigned, agree and acknowledge that I have read, and that I am fully bound by, and subject to, all of the terms and conditions of the Agnico Eagle Mining Limited Executive Incentive Compensation Recoupment Policy (as such policy may be amended, restated, supplemented or otherwise modified from time to time, the “Policy”). Any capitalized terms used in this Acknowledgment without definition shall have the meaning set forth in the Policy.

If there is any inconsistency between the Policy and the terms of any employment agreement to which I am a party, or the terms of any compensation plan, program or agreement under which any compensation has been granted, awarded, earned or paid, the terms of the Policy shall govern. If it is determined by the Administrator that any amounts granted, awarded, earned or paid to me must be forfeited or reimbursed to the Corporation, I will promptly take any action necessary to effectuate such forfeiture and/or reimbursement.

By: |

|

|

|

[Name] |

|

|

[Title] |

|

Date: |

|

|

![[MISSING IMAGE: lg_agnicoeagle-bw.jpg]](/disclosures/0001104659-24-037982/asset?file=lg_agnicoeagle-bw.jpg&lang=en)

| | | | | | | | |

| | | |

Page

|

| |||

| INTRODUCTORY NOTES | | | | | ii | | |

| | | | | ii | | | |

| | | | | ii | | | |

| | | | | iv | | | |

| | | | | iv | | | |

| | | | | v | | | |

| SELECTED FINANCIAL DATA | | | | | 1 | | |

| GLOSSARY OF SELECTED MINING TERMS | | | | | 2 | | |

| CORPORATE STRUCTURE | | | | | 3 | | |

| DESCRIPTION OF THE BUSINESS | | | | | 5 | | |

| GENERAL DEVELOPMENT OF THE BUSINESS | | | | | 7 | | |

| OPERATIONS & PRODUCTION | | | | | 12 | | |

| | | | | 12 | | | |

| | | | | 54 | | | |

| | | | | 55 | | | |

| | | | | 69 | | | |

| | | | | 69 | | | |

| | | | | 70 | | | |

| | | | | 70 | | | |

| | | | | 71 | | | |

| | | | | 71 | | | |

| | | | | 72 | | | |

| | | | | 73 | | | |

| RISK FACTORS | | | | | 74 | | |

| DIVIDENDS | | | | | 93 | | |

| | | | | | | | |

| | | |

Page

|

| |||

| DESCRIPTION OF CAPITAL STRUCTURE | | | | | 93 | | |

| RATINGS | | | | | 93 | | |

| MARKET FOR SECURITIES | | | | | 94 | | |

| | | | | 95 | | | |

| | | | | 95 | | | |

| | | | | 97 | | | |

| | | | | 97 | | | |

| | | | | 98 | | | |

| | | | | 98 | | | |

| | | | | 99 | | | |

| AUDIT COMMITTEE | | | | | 99 | | |

| | | | | 99 | | | |

| | | | | 100 | | | |

| | | | | 100 | | | |

| | | | | 100 | | | |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | | | | | 101 | | |

| | | | | 101 | | | |

| TRANSFER AGENT AND REGISTRAR | | | | | 101 | | |

| MATERIAL CONTRACTS | | | | | 101 | | |

| INTERESTS OF EXPERTS | | | | | 103 | | |

| ADDITIONAL INFORMATION | | | | | 104 | | |

| SCHEDULE “A” AUDIT COMMITTEE CHARTER OF THE COMPANY | | | | | A-1 | | |

| | | | | B-1 | | | |

| | | |

Year Ended December 31,

|

| |||||||||||||||||||||||||||

| | | |

2023

|

| |

2022

|

| |

2021

|

| |

2020

|

| |

2019

|

| |||||||||||||||

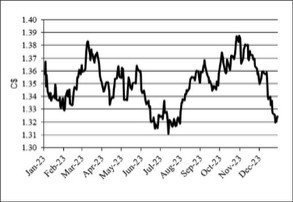

| High | | | | | 1.3875 | | | | | | 1.3858 | | | | | | 1.2942 | | | | | | 1.4496 | | | | | | 1.3600 | | |

| Low | | | | | 1.3128 | | | | | | 1.2451 | | | | | | 1.2040 | | | | | | 1.2718 | | | | | | 1.2988 | | |

| End of Period | | | | | 1.3226 | | | | | | 1.3544 | | | | | | 1.2678 | | | | | | 1.2732 | | | | | | 1.2988 | | |

| Average | | | | | 1.3497 | | | | | | 1.3013 | | | | | | 1.2535 | | | | | | 1.3415 | | | | | | 1.3269 | | |

| | | |

2024

|

| |

2023

|

| ||||||||||||||||||||||||||||||||||||

| | | |

March

(to March 18) |

| |

February

|

| |

January

|

| |

December

|

| |

November

|

| |

October

|

| |

September

|

| |||||||||||||||||||||

| High | | | | | 1.3582 | | | | | | 1.3574 | | | | | | 1.3522 | | | | | | 1.3599 | | | | | | 1.3875 | | | | | | 1.3871 | | | | | | 1.3674 | | |

| Low | | | | | 1.3472 | | | | | | 1.3404 | | | | | | 1.3316 | | | | | | 1.3205 | | | | | | 1.3581 | | | | | | 1.3591 | | | | | | 1.3423 | | |

| End of Period | | | | | 1.3541 | | | | | | 1.3570 | | | | | | 1.3397 | | | | | | 1.3226 | | | | | | 1.3582 | | | | | | 1.3871 | | | | | | 1.3520 | | |

| Average | | | | | 1.3520 | | | | | | 1.3501 | | | | | | 1.3425 | | | | | | 1.3431 | | | | | | 1.3709 | | | | | | 1.3717 | | | | | | 1.3535 | | |

| | | |

Year Ended December 31,

|

| |||||||||||||||||||||||||||

| | | |

2023

|

| |

2022

|

| |

2021*

|

| |

2020

|

| |

2019

|

| |||||||||||||||

| | | |

(in thousands of U.S. dollars, other than share and per share information)

|

| |||||||||||||||||||||||||||

| Income Statement Data | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Revenues from mining operations | | | | | 6,626,909 | | | | | | 5,741,162 | | | | | | 3,869,625 | | | | | | 3,138,113 | | | | | | 2,494,892 | | |

| Production | | | | | 2,933,263 | | | | | | 2,643,321 | | | | | | 1,773,121 | | | | | | 1,424,152 | | | | | | 1,247,705 | | |

| Exploration and corporate development | | | | | 215,781 | | | | | | 271,117 | | | | | | 152,514 | | | | | | 113,492 | | | | | | 104,779 | | |

| Amortization of property, plant and mine development | | | | | 1,491,771 | | | | | | 1,094,691 | | | | | | 738,129 | | | | | | 631,101 | | | | | | 546,057 | | |

| General and administrative | | | | | 208,451 | | | | | | 220,861 | | | | | | 142,003 | | | | | | 116,288 | | | | | | 120,987 | | |

| Impairment loss on equity securities | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | |

| (Gain) Loss on derivative financial instruments | | | | | -68,432 | | | | | | 90,692 | | | | | | 11,103 | | | | | | -107,873 | | | | | | -17,124 | | |

| Finance costs | | | | | 130,087 | | | | | | 82,935 | | | | | | 92,042 | | | | | | 95,134 | | | | | | 105,082 | | |

| Other expenses (income) | | | | | 63,557 | | | | | | 130,891 | | | | | | 21,742 | | | | | | 48,234 | | | | | | -13,169 | | |

| Environmental remediation | | | | | 2,712 | | | | | | 10,417 | | | | | | 576 | | | | | | 27,540 | | | | | | 2,804 | | |

| Foreign currency translation (gain) loss | | | | | -328 | | | | | | -16,081 | | | | | | 5,672 | | | | | | 22,480 | | | | | | 4,850 | | |

| Care and maintenance | | | | | 47,392 | | | | | | 41,895 | | | | | | — | | | | | | — | | | | | | — | | |

| Income (loss) before income and mining taxes | | | | | 2,359,069 | | | | | | 1,115,423 | | | | | | 932,723 | | | | | | 767,565 | | | | | | 738,742 | | |

| Income and mining taxes expense | | | | | 417,762 | | | | | | 445,174 | | | | | | 370,778 | | | | | | 255,958 | | | | | | 265,576 | | |

| Net income (loss) for the year | | | | | 1,941,307 | | | | | | 670,249 | | | | | | 561,945 | | | | | | 511,607 | | | | | | 473,166 | | |

| Net income (loss) per share – basic | | | | | 3.97 | | | | | | 1.53 | | | | | | 2.31 | | | | | | 2.12 | | | | | | 2.00 | | |

| Net income (loss) per share – diluted | | | | | 3.95 | | | | | | 1.53 | | | | | | 2.30 | | | | | | 2.10 | | | | | | 1.99 | | |

| Weighted average number of common shares outstanding – basic | | | | | 488,722,676 | | | | | | 437,678,131 | | | | | | 243,707,991 | | | | | | 241,508,347 | | | | | | 236,933,791 | | |

| Weighted average number of common shares outstanding – diluted | | | | | 489,912,686 | | | | | | 438,533,089 | | | | | | 244,732,372 | | | | | | 243,072,085 | | | | | | 238,229,593 | | |

| Cash dividends declared per common share | | | | | 1.6 | | | | | | 1.6 | | | | | | 1.4 | | | | | | 0.95 | | | | | | 0.55 | | |

| Balance Sheet Data (at end of period) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Property, plant and mine development | | | | | 21,221,905 | | | | | | 18,459,400 | | | | | | 7,675,595 | | | | | | 7,325,418 | | | | | | 7,003,665 | | |

| Total assets | | | | | 28,684,949 | | | | | | 23,494,808 | | | | | | 10,216,090 | | | | | | 9,614,755 | | | | | | 8,789,885 | | |

| Long-term debt | | | | | 1,843,086 | | | | | | 1,342,070 | | | | | | 1,565,223 | | | | | | 1,565,241 | | | | | | 1,724,108 | | |

| Reclamation provision | | | | | 1,073,504 | | | | | | 901,836 | | | | | | 729,996 | | | | | | 667,053 | | | | | | 439,801 | | |

| Net assets | | | | | 19,422,915 | | | | | | 16,241,345 | | | | | | 5,999,771 | | | | | | 5,683,213 | | | | | | 5,111,514 | | |

| Common shares | | | | | 18,334,869 | | | | | | 16,251,221 | | | | | | 5,863,512 | | | | | | 5,751,479 | | | | | | 5,589,352 | | |

| Shareholders’ equity | | | | | 19,422,915 | | | | | | 16,241,345 | | | | | | 5,999,771 | | | | | | 5,683,213 | | | | | | 5,111,514 | | |

| Total common shares outstanding | | | | | 497,299,441 | | | | | | 456,465,296 | | | | | | 245,001,857 | | | | | | 242,884,314 | | | | | | 239,619,035 | | |

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

1

|

|

| |

2

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

3

|

|

![[MISSING IMAGE: fc_miningterms-bwlr.jpg]](/disclosures/0001104659-24-037982/asset?file=fc_miningterms-bwlr.jpg&lang=en)

| |

4

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| | | |

Date of

Acquisition(1) |

| |

Date of

Commencement of Construction(1) |

| |

Date of achieving

Commercial Production(1) |

| |

Estimated

Mine Life(2) |

|

|

LaRonde mine

|

| |

1992

|

| |

1985

|

| |

1988

|

| |

2034

|

|

|

LaRonde Zone 5 mine

|

| |

2003

|

| |

2017

|

| |

June 2018

|

| |

2032

|

|

| Canadian Malartic Complex(3) | | |

June 2014

|

| |

n/a

|

| |

n/a

|

| |

2042

|

|

| Goldex mine(4) | | |

December 1993

|

| |

July 2012

|

| |

October 2013

|

| |

2031

|

|

| Meadowbank Complex(5) | | |

April 2007

|

| |

Pre-April 2007

|

| |

March 2010

|

| |

2028

|

|

|

Meliadine mine

|

| |

July 2010

|

| |

2017

|

| |

May 2019

|

| |

2032

|

|

| Detour Lake mine(6) | | |

February 2022

|

| |

n/a

|

| |

n/a

|

| |

2052

|

|

| Macassa mine(6) | | |

February 2022

|

| |

n/a

|

| |

n/a

|

| |

2030

|

|

|

Kittila mine

|

| |

November 2005

|

| |

June 2006

|

| |

May 2009

|

| |

2035

|

|

| Fosterville mine(6) | | |

February 2022

|

| |

n/a

|

| |

n/a

|

| |

2033

|

|

|

Pinos Altos mine

|

| |

March 2006

|

| |

August 2007

|

| |

November 2009

|

| |

2028

|

|

|

La India mine

|

| |

November 2011

|

| |

September 2012

|

| |

February 2014

|

| |

2024

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

5

|

|

| |

6

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| | | |

2021 Capital Expenditures(1)

(thousands of $) |

| |||||||||||||||||||||

| | | | | | | | | | | | | | | |

Capitalized Exploration

|

| |||||||||

| | | |

Sustaining

|

| |

Development

|

| |

Sustaining

|

| |

Non-sustaining

|

| ||||||||||||

| LaRonde Complex | | | | | 72,749 | | | | | | 45,914 | | | | | | – | | | | | | 10,699 | | |

| Canadian Malartic Complex (50%) | | | | | 28,582 | | | | | | 14,668 | | | | | | 2,435 | | | | | | 4,005 | | |

| Goldex mine | | | | | 37,312 | | | | | | 77,175 | | | | | | 5,320 | | | | | | – | | |

| Kittila mine | | | | | 48,917 | | | | | | 5,820 | | | | | | – | | | | | | 3,823 | | |

| Meadowbank Complex (including Amaruq) | | | | | 48,446 | | | | | | 168,291 | | | | | | 1,895 | | | | | | 5,993 | | |

| Meliadine mine | | | | | 39,109 | | | | | | 6,969 | | | | | | 5,051 | | | | | | 913 | | |

| Pinos Altos mine | | | | | 21,615 | | | | | | 23,777 | | | | | | 601 | | | | | | – | | |

| La India mine | | | | | 10,000 | | | | | | 9,383 | | | | | | 117 | | | | | | – | | |

| Other | | | | | – | | | | | | 11,105 | | | | | | – | | | | | | 866 | | |

| Total Capital Expenditures | | | | | 414,963 | | | | | | 416,257 | | | | | | 17,580 | | | | | | 26,299 | | |

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

7

|

|

| | | |

2022 Capital Expenditures(1)

(thousands of $) |

| |||||||||||||||||||||

| | | | | | | | | | | | | | | |

Capitalized Exploration

|

| |||||||||

| | | |

Sustaining

|

| |

Development

|

| |

Sustaining

|

| |

Non-sustaining

|

| ||||||||||||

| LaRonde Complex | | | | $ | 100,111 | | | | | $ | 72,020 | | | | | | 2,068 | | | | | | – | | |

| Canadian Malartic Complex (50%) | | | | | 69,137 | | | | | | 115,997 | | | | | | – | | | | | | 12,554 | | |

| Goldex mine | | | | | 23,480 | | | | | | 35,136 | | | | | | 1,645 | | | | | | 3,944 | | |

| Detour Lake mine | | | | | 214,060 | | | | | | 148,672 | | | | | | – | | | | | | 31,400 | | |

| Fosterville mine | | | | | 56,131 | | | | | | 9,876 | | | | | | 213 | | | | | | 28,492 | | |

| Kittila mine | | | | | 43,803 | | | | | | 50,315 | | | | | | 4,996 | | | | | | 2,449 | | |

| Macassa mine | | | | | 29,393 | | | | | | 70,468 | | | | | | 905 | | | | | | 21,707 | | |

| Meadowbank Complex (including Amaruq) | | | | | 86,435 | | | | | | 53,393 | | | | | | – | | | | | | – | | |

| Meliadine mine | | | | | 58,485 | | | | | | 90,859 | | | | | | 3,601 | | | | | | 2,949 | | |

| Pinos Altos mine | | | | | 25,664 | | | | | | 26,749 | | | | | | 837 | | | | | | – | | |

| La India mine | | | | | 8,955 | | | | | | 6,129 | | | | | | 8 | | | | | | – | | |

| Other | | | | | 3,291 | | | | | | 16,289 | | | | | | 328 | | | | | | 3,956 | | |

| Total Capital Expenditures | | | | $ | 718,945 | | | | | $ | 695,903 | | | | | $ | 14,601 | | | | | $ | 107,451 | | |

| |

8

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| | | |

2023 Capital Expenditures(1)

(thousands of $) |

| |||||||||||||||||||||

| | | | | | | | | | | | | | | |

Capitalized Exploration

|

| |||||||||

| | | |

Sustaining

|

| |

Development

|

| |

Sustaining

|

| |

Non-sustaining

|

| ||||||||||||

| LaRonde Complex | | | | $ | 81,043 | | | | | $ | 68,930 | | | | | $ | 2,038 | | | | | $ | – | | |

| Canadian Malartic Complex(2) | | | | | 91,028 | | | | | | 160,513 | | | | | | – | | | | | | 9,447 | | |

| Goldex mine(3) | | | | | 25,908 | | | | | | 56,977 | | | | | | 1,295 | | | | | | 2,459 | | |

| Detour Lake mine | | | | | 249,765 | | | | | | 140,388 | | | | | | – | | | | | | 32,515 | | |

| Fosterville mine | | | | | 33,751 | | | | | | 33,575 | | | | | | 895 | | | | | | 19,218 | | |

| Kittila mine | | | | | 47,355 | | | | | | 26,410 | | | | | | 2,184 | | | | | | 5,053 | | |

| Macassa mine | | | | | 43,333 | | | | | | 75,125 | | | | | | 1,696 | | | | | | 26,105 | | |

| Meadowbank Complex | | | | | 121,653 | | | | | | 80 | | | | | | – | | | | | | – | | |

| Meliadine mine | | | | | 67,947 | | | | | | 106,953 | | | | | | 7,328 | | | | | | 11,927 | | |

| Pinos Altos mine | | | | | 28,449 | | | | | | 4,196 | | | | | | 1,692 | | | | | | 1,101 | | |

| Other | | | | | 247 | | | | | | 11,449 | | | | | | – | | | | | | 840 | | |

| Total Capital Expenditures | | | | $ | 790,479 | | | | | $ | 684,596 | | | | | $ | 17,128 | | | | | $ | 108,665 | | |

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

9

|

|

| | | |

2024 Capital Expenditures (Expected)(1)

(thousands of $) |

| |||||||||||||||||||||||||||

| | | |

Capital Expenditures

|

| |

Capitalized Exploration

|

| ||||||||||||||||||||||||

| | | |

Sustaining

|

| |

Development

|

| |

Sustaining

|

| |

Non-sustaining

|

| |

Total

|

| |||||||||||||||

| LaRonde Complex | | | | $ | 86,100 | | | | | $ | 68,200 | | | | | $ | 2,300 | | | | | $ | – | | | | |

$

|

156,600

|

| |

| Canadian Malartic Complex | | | | | 135,900 | | | | | | 167,500 | | | | | | – | | | | | | 7,100 | | | | |

|

310,500

|

| |

| Goldex mine | | | | | 52,800 | | | | | | 7,700 | | | | | | 2,900 | | | | | | – | | | | |

|

63,400

|

| |

| Detour Lake mine | | | | | 274,800 | | | | | | 201,100 | | | | | | – | | | | | | 20,300 | | | | |

|

496,200

|

| |

| Macassa mine | | | | | 59,400 | | | | | | 97,800 | | | | | | 2,100 | | | | | | 32,900 | | | | |

|

192,200

|

| |

| Meliadine mine | | | | | 70,200 | | | | | | 82,400 | | | | | | 5,500 | | | | | | 13,200 | | | | |

|

171,300

|

| |

| Meadowbank Complex | | | | | 94,000 | | | | | | – | | | | | | – | | | | | | – | | | | |

|

94,000

|

| |

| Fosterville mine | | | | | 35,800 | | | | | | 41,100 | | | | | | – | | | | | | 11,000 | | | | |

|

87,900

|

| |

| Kittila mine | | | | | 87,200 | | | | | | 2,900 | | | | | | 1,900 | | | | | | 5,400 | | | | |

|

97,400

|

| |

| Pinos Altos mine | | | | | 19,800 | | | | | | 15,400 | | | | | | 1,800 | | | | | | 500 | | | | |

|

37,500

|

| |

| San Nicolas project | | | | | – | | | | | | 17,000 | | | | | | – | | | | | | – | | | | |

|

17,000

|

| |

| Other | | | | | – | | | | | | 35,900 | | | | | | – | | | | | | 1,700 | | | | |

|

37,600

|

| |

| Total Capital Expenditures | | | | $ | 916,000 | | | | | $ | 737,000 | | | | | $ | 16,500 | | | | | $ | 92,100 | | | | | $ | 1,761,600 | | |

| |

10

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

11

|

|

| |

12

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

![[MISSING IMAGE: mp_larondecomplex-4c.jpg]](/disclosures/0001104659-24-037982/asset?file=mp_larondecomplex-4c.jpg&lang=en)

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

13

|

|

![[MISSING IMAGE: mp_abitibiregionproperti-4c.jpg]](/disclosures/0001104659-24-037982/asset?file=mp_abitibiregionproperti-4c.jpg&lang=en)

![[MISSING IMAGE: mp_surfacelaronde-4c.jpg]](/disclosures/0001104659-24-037982/asset?file=mp_surfacelaronde-4c.jpg&lang=en)

| |

14

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

15

|

|

| | | | | | |

Copper

Concentrate 2,578 tonnes produced |

| |

Zinc

Concentrate 7,702 tonnes produced |

| | | | | | | ||||||

| | | |

Head

Grades |

| |

Grade

|

| |

Recovery

|

| |

Grade

|

| |

Recovery

|

| |

Overall

Metal Recoveries |

| |

Payable

Production |

|

|

Gold

|

| |

3.83 g/t

|

| |

321.2

|

| |

59.37%

|

| |

24.08 g/t

|

| |

4.30%

|

| |

93.59%

|

| |

306,648 oz

|

|

|

Silver

|

| |

9.12 g/t

|

| |

768.3

|

| |

45.98%

|

| |

147.54 g/t

|

| |

9.76%

|

| |

85.73%

|

| |

587,556 oz

|

|

|

Copper

|

| |

0.13%

|

| |

18.62%

|

| |

80.78%

|

| |

–

|

| |

–

|

| |

80.78%

|

| |

2,578 t

|

|

|

Zinc

|

| |

0.44%

|

| |

3.58%

|

| |

4.42%

|

| |

52.88%

|

| |

76.77%

|

| |

76.77%

|

| |

7,702 t

|

|

| |

16

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

17

|

|

| |

18

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

19

|

|

| |

20

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

![[MISSING IMAGE: mp_surfacemalarticmine-4c.jpg]](/disclosures/0001104659-24-037982/asset?file=mp_surfacemalarticmine-4c.jpg&lang=en)

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

21

|

|

| | | |

Head

Grade |

| |

Overall

Metal Recovery |

| |

Payable

Production |

|

| Gold | | |

1.17 g/t

|

| |

92.8%

|

| |

603,955 oz

|

|

| Silver | | |

0.80 g/t

|

| |

72.3%

|

| |

310,494 oz

|

|

| |

22

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

23

|

|

| |

24

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

| |

25

|

|

| |

26

|

| |

AGNICO EAGLE

ANNUAL INFORMATION FORM

|

|