UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section

13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (date of earliest event reported): March 12, 2024

Enviva Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 001-37363 | 46-4097730 | ||

(State or other jurisdiction of incorporation) |

(Commission File Number) | (I.R.S. Employer Identification No.) |

| 7272

Wisconsin Ave. Suite 1800 Bethesda, MD |

20814 | |

| (Address of principal executive offices) | (Zip code) |

(301) 657-5560

(Registrant’s telephone number, including area code)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock | EVA | New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2).

Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 1.01. | Entry Into Material Definitive Agreement. |

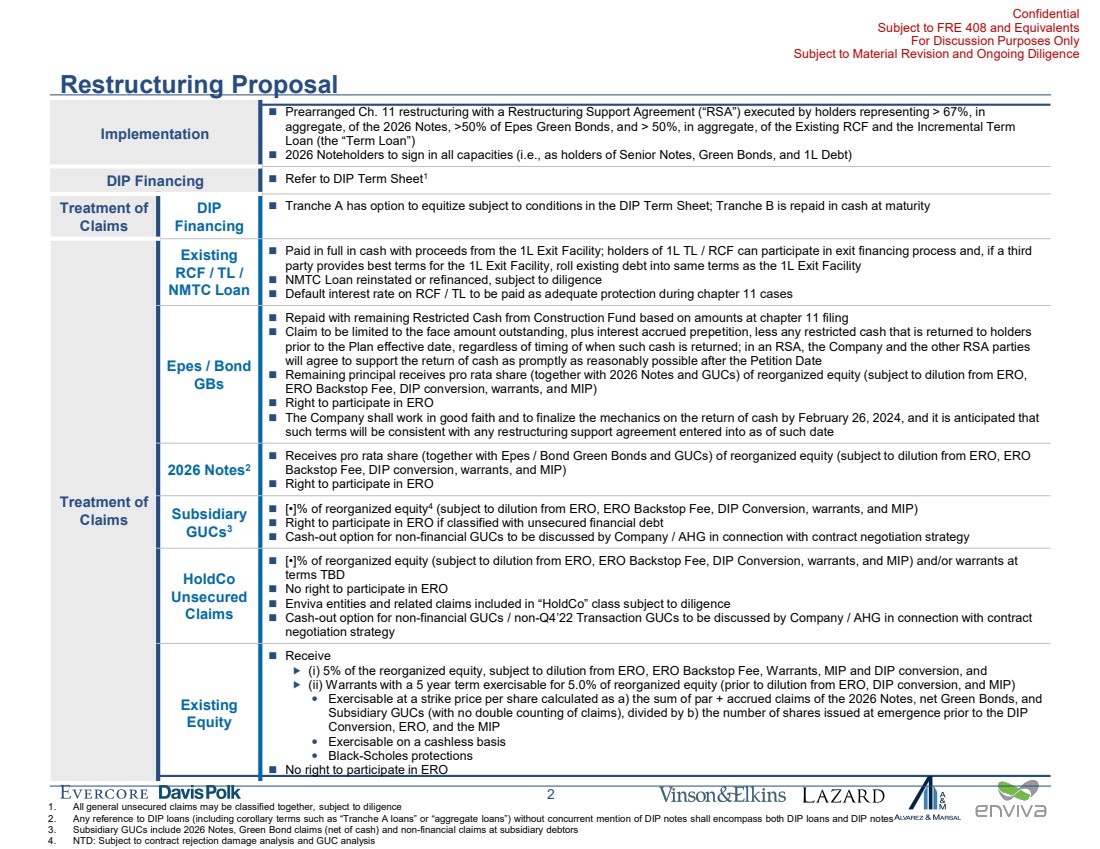

Restructuring Support Agreement

On March 12, 2024 (the “Petition Date”), Enviva Inc., a Delaware corporation (the “Company”), entered into a Restructuring Support Agreement (including any term sheets attached thereto, the “RSA”) with (i) certain subsidiaries of the Company listed on Schedule 1 of the RSA (together with the Company, the “Company RSA Parties”), (ii) certain participating holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders of the Company’s outstanding 6.5% Senior Notes due 2026 (the “2026 Notes” and the holders thereof, the “2026 Noteholders”), (iii) certain participating holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders, whether as record holders or participants, of loans or commitments under the Company’s senior secured credit facility (the “Senior Secured Credit Facility” and the lenders thereunder, the “Credit Facility Lenders”), (iv) certain participating holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders of Exempt Facilities Revenue Bonds (Enviva Inc. Project), Series 2022 (Green Bonds) issued by the Industrial Development Authority of Sumter County, Alabama (the “Epes Green Bonds” and the holders thereof, the “Epes Bondholders”), and (v) certain participating holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders of Exempt Facilities Revenue Bonds (Enviva Inc.), Series 2022 (Green Bonds) issued by Mississippi Business Finance Corporation (the “Bond Green Bonds” and the holders thereof, the “Bond Bondholders,” and together with the 2026 Noteholders, the Credit Facility Lenders, and the Epes Bondholders, the “Restructuring Support Parties”).

Under the terms of the RSA, the Restructuring Support Parties have agreed to support a restructuring of the Company RSA Parties under a Chapter 11 plan of reorganization (the “Plan”) to be proposed in accordance with the terms as set forth in the RSA, including the term sheet attached as Exhibit A thereto (the “RSA Term Sheet”), which terms include that, subject to the RSA:

| · | Senior Secured Credit Facility claims will be repaid in full in connection with consummation of the Plan; |

| · | Epes Green Bonds claims and Bond Green Bonds claims (in each case, net of paydown with remaining restricted cash), the 2026 Notes claims, and general unsecured claims against certain subsidiary Debtors (as defined below) will receive a pro rata share of reorganized equity (in amounts to be determined in connection with the Plan and subject to dilution as provided for in the RSA Term Sheet); |

| · | General unsecured claims against certain HoldCo Debtors (as defined in the RSA) will receive reorganized equity and/or warrants (in amounts to be determined in connection with the Plan and subject to dilution as provided for in the RSA Term Sheet); and |

| · | Existing equity holders will receive 5% of the initial reorganized equity and warrants for an additional 5% of reorganized equity (in each case, subject to dilution as provided for in the RSA Term Sheet). |

The Company RSA Parties also entered into a Restructuring Support Agreement (the “Bond MS RSA”) with certain Bond Bondholders comprising a majority of Bond Green Bonds outstanding and the Bond Green Bonds Trustee (as defined in the Bond MS RSA). Under the Bond MS RSA, the Company agrees, among other obligations described in the term sheet attached as Exhibit A thereto, to promptly seek court approval of a settlement with the Bond Bondholders party thereto, whereby the Company RSA Parties will consent to the partial redemption of the Bond Green Bonds via the release of certain funds currently held by the Bond Green Bonds Trustee. In exchange, the Bond Green Bondholders and the Bond Green Bonds Trustee both agree, among other obligations described in the term sheet attached to the Bond MS RSA as Exhibit A thereto, and subject to any rights granted thereunder, to support the Plan.

The foregoing descriptions of the RSA and the Bond MS RSA do not purport to be complete and are qualified in their entirety by reference to the full text of the RSA and the Bond MS RSA, respectively, which are filed as Exhibit 10.1 and Exhibit 10.2, respectively, to this Current Report on Form 8-K (the “Current Report”) and are incorporated herein by reference.

| Item 1.03. | Bankruptcy or Receivership. |

On the Petition Date, the Company and certain subsidiaries of the Company (collectively, the “Debtors”) filed voluntary petitions (“Bankruptcy Petitions”) for reorganization under Chapter 11 of Title 11 of the United States Code (“Bankruptcy Code”) in the United States Bankruptcy Court for the Eastern District of Virginia (“Bankruptcy Court”). The Company also filed motions with the Bankruptcy Court seeking joint administration of the Chapter 11 Cases under the caption In re Enviva Inc., et al., Case No. 24-10453 (the “Chapter 11 Cases”). The Company will continue to operate its businesses as “debtors-in-possession” under the jurisdiction of the Bankruptcy Court and under the provisions of the Bankruptcy Code and orders of the Bankruptcy Court. The Company expects to continue to operate in the ordinary course throughout the Chapter 11 process without material disruption to vendors, suppliers, and partners.

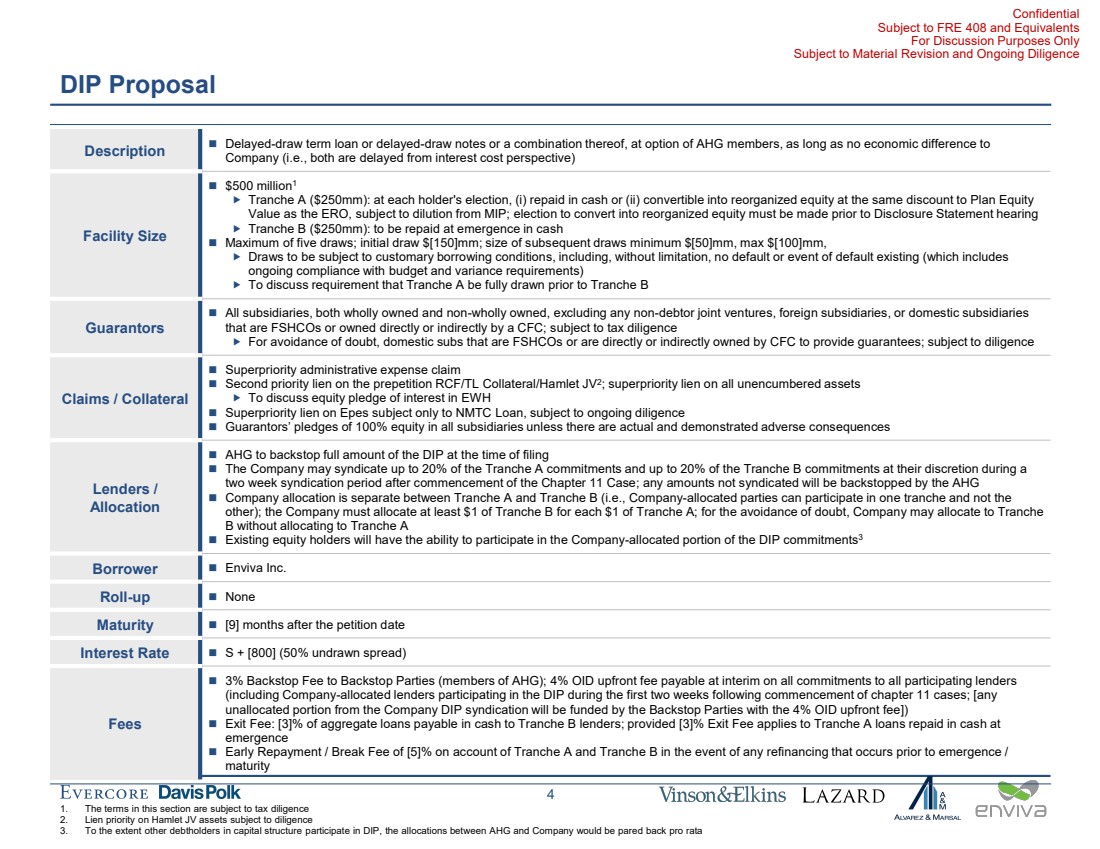

The Debtors will seek approval from the Bankruptcy Court to enter into a multi-tranche, delayed-draw, debtor-in-possession (“DIP”) credit and note purchase agreement (the “DIP Facility Agreement”), consisting of loans and notes in an aggregate principal amount of $500,000,000 from lenders and noteholders under the DIP facility (the “DIP Creditors”), of which $150,000,000 will be available immediately upon entry of an interim order, and the remainder of which will be available through additional draws, in each case subject to and upon the date of entry of a final order. A portion of the commitments under the DIP Facility Agreement will be allocated by the Company to eligible stockholders in accordance with a syndication process that is subject to Bankruptcy Court approval.

Subject to approval by the Bankruptcy Court, the proceeds of the loans and notes under the DIP Facility Agreement will be used to pay the Debtors’ operating expenses, help fund the completion of certain construction projects, and pay other fees, expenses, and other expenditures of the Debtors to be set forth in rolling budgets prepared as part of the Chapter 11 Cases, which shall be subject to approval by the DIP Creditors. Closing of the DIP Facility Agreement is contingent on the satisfaction of customary conditions, including receipt of an order by the Bankruptcy Court approving the DIP Facility Agreement.

In addition, the Debtors filed a motion (“NOL Motion”) seeking entry of an interim and final order establishing certain procedures and restrictions with respect to the direct or indirect purchase, disposition, or other transfer of the Company’s common stock (“Common Stock”) (including declarations of worthlessness with respect to such Common Stock) (such procedures, “Stock Procedures”), and seeking related relief, in order to preserve and protect the potential value of the Debtors’ net operating losses (“NOLs”) and certain other tax attributes of the Debtors (together with the NOLs, “Tax Attributes”).

If approved, the Stock Procedures would restrict transactions involving, and require notices of the holdings of and proposed transactions by, any person or group of persons that is or, as a result of a proposed transaction, would become, a Substantial Stockholder of Common Stock or declarations of worthlessness involving, and require notices of holdings of, any person or group of persons that is a 50-percent shareholder. For purposes of the Stock Procedures, a “Substantial Stockholder” is any person that beneficially owns at least 3,360,328 shares of Common Stock (representing approximately 4.5% of all issued and outstanding shares of Common Stock) and a “50-percent shareholder” is any person that would be a “50-percent shareholder” (within the meaning of section 382(g)(4)(D) of the Internal Revenue Code of 1986, as amended (the “Tax Code”)) with respect to its beneficial ownership of Common Stock if such person claimed a worthlessness deduction under section 165 of the Tax Code with respect to such Common Stock at any time on or after the Petition Date.

The NOL Motion and Stock Procedures are available on the docket of the Chapter 11 Cases, which can be accessed via PACER at https://www.pacer.gov. The Company also requested authority to employ Kurtzman Carson Consultants LLC (“KCC”) as its claims and notice agent. If approved, the NOL Motion and Stock Procedures and additional information about the Chapter 11 Cases would also be available for free on the website maintained for the Company by KCC, located at www.kccllc.net/enviva or by calling (888) 249-2695 (U.S. / Canada) or +1 (310) 751-2601 (international).

| Item 2.02. | Results of Operations and Financial Condition. |

To the extent applicable, the disclosures in Item 7.01 below are incorporated herein by reference.

| Item 2.04 | Triggering Events that Accelerate or Increase a Direct Financial Obligation or an Obligation Under an Off-Balance Sheet Arrangement. |

The filing of the Bankruptcy Petitions described above constitutes an event of default and acceleration under each of the following debt instruments (the “Debt Instruments”):

| · | Indenture, dated as of December 9, 2019, by and among the Company (as successor to Enviva Partners, LP), Enviva Partners Finance Corp., each of the guarantors party thereto, and Wilmington Savings Fund Society, FSB (as successor to Wilmington Trust, N.A.), as trustee. | |

| · | Amended and Restated Credit Agreement, dated as of October 18, 2018 (as amended, restated, amended and restated, supplemented, or otherwise modified from time to time), by and among the Company, Enviva, LP, each of the guarantors party thereto, the lenders party thereto, and Ankura Trust Company, LLC, as Administrative Agent and as Collateral Agent, and the other parties thereto; | |

| · | Indenture of Trust (as amended, restated, modified, supplemented, or replaced from time to time), dated as of July 1, 2022, by and between The Industrial Development Authority of Sumter County and Wilmington Trust, N.A., as trustee; | |

| · | Loan and Guaranty Agreement, dated effective as of July 15, 2022, by and among The Industrial Development Authority of Sumter County, the Company, and certain of its subsidiaries; | |

| · | Indenture of Trust (as amended, restated, modified, supplemented, or replaced from time to time), dated as of November 1, 2022, by and between Mississippi Business Finance Corporation and Wilmington Trust, N.A., as trustee; | |

| · | Loan and Guaranty Agreement, dated effective as of November 22, 2022, by and among Mississippi Business Finance Corporation, the Company, and certain of its subsidiaries; | |

| · | Loan Agreement, dated as of June 27, 2022, by and among Enviva Pellets Epes, LLC, the lenders party thereto, and the Company; and | |

| · | Loan Agreement, dated as of June 27, 2022, by and between Enviva Pellets Epes Finance Company, LLC and United Bank. |

The Debt Instruments provide that as a result of the Bankruptcy Petitions, the principal and interest due thereunder shall be immediately due and payable. However, any efforts to enforce such payment obligations under the Debt Instruments will be automatically stayed as a result of the Bankruptcy Petitions, and the creditors’ rights of enforcement in respect of the Debt Instruments will be subject to the applicable provisions of the Bankruptcy Code and orders of the Bankruptcy Court.

The information under Item 1.03 is incorporated herein by reference.

| Item 7.01 | Regulation FD Disclosure. |

Press Release

On March 12, 2024, the Company issued a press release announcing the commencement of the Chapter 11 Cases and its entry into the RSA, a copy of which is attached as Exhibit 99.1 to this Current Report and incorporated herein by reference.

Cleansing Material

Prior to the Petition Date and in connection with discussions with certain of its debt holders, the Company entered into confidentiality agreements (collectively, the “NDAs”) with certain of the Restructuring Support Parties pursuant to which the Company agreed, limited to the extent necessary, to publicly disclose certain information, including certain material non-public information (the “Cleansing Materials”), upon the occurrence of certain events set forth in the NDAs. The Company is furnishing the Cleansing Materials as Exhibit 99.2 to this Current Report in satisfaction of its obligations under the NDAs.

The Cleansing Materials are based solely on certain information made available to the Company as of the date of the Cleansing Materials and were not prepared with a view toward public disclosure. The Cleansing Materials should not be relied upon by any party for any reason. The Cleansing Materials should not be relied upon as a reliable prediction of future events. Neither the Company nor any third party has made or makes any representation to any person regarding the accuracy of any Cleansing Materials or undertakes any obligation to publicly update the Cleansing Materials to reflect circumstances existing after the date when the Cleansing Materials were prepared or conveyed or to reflect the occurrence of future events.

The Cleansing Materials contain the Company’s preliminary estimates of certain financial results for the three months ended December 31, 2023, the fiscal year ended December 31, 2023, and the three months ended March 31, 2024, based on currently available information. The Company has not yet finalized its results for these periods, and its consolidated financial statements as of and for the year ended December 31, 2023 and the three months ended December 31, 2023 and March 31, 2024, respectively, are not currently available. The Company’s actual results remain subject to the completion of the year-end and quarter-end closing processes, which includes review by management and the Company’s board of directors (the “Board”), including the audit committee of the Board. While carrying out such procedures, the Company may identify items that require it to make adjustments to the preliminary estimates of its results set forth in the Cleansing Materials. As a result, the Company’s actual results could be materially different from those set forth in the Cleansing Materials. Additionally, the Company’s estimates are forward-looking statements based solely on information available to it as of the date of the Cleansing Materials and may differ materially from actual results. Therefore, a reader should not rely on these preliminary estimates of the Company’s results. The preliminary estimates of the Company’s results included in the Cleansing Materials have been prepared by, and are the responsibility of, the Company’s management. The Company’s independent auditors have not audited, reviewed, or compiled such preliminary estimates of the Company’s results. Accordingly, Ernst & Young LLP expresses no opinion or any other form of assurance with respect thereto. The preliminary estimates of certain financial results presented in the Cleansing Materials should not be considered a substitute for actual results.

The information furnished under Item 7.01 of this Current Report, including the accompanying Exhibits 99.1 and 99.2, shall not be deemed to be “filed” for the purposes of Section 18 of the Securities Exchange Act of 1923, as amended (the “Exchange Act”), or otherwise subject to the liability of such section, nor shall such information be deemed to be incorporated by reference in any filing by the Company under the Securities Act of 1933, as amended, or the Exchange Act, regardless of the general incorporation language of such filing, except as specifically stated in such filing.

Cautionary Statements

This Current Report includes “forward-looking statements” within the meaning of federal securities laws. Such forward-looking statements are subject to a number of risks and uncertainties, many of which are beyond the Company’s control. These risks include, but are not limited to: (i) the Company’s ability to successfully complete a restructuring under Chapter 11; (ii) potential adverse effects of the Chapter 11 Cases on the Company’s liquidity and results of operations (including the availability of operating capital during the pendency of Chapter 11 Cases); (iii) the Company’s ability to obtain timely approval by the Court with respect to the motions filed in the Chapter 11 Cases; (iv) objections to the Company’s restructuring process, DIP financing, or other pleadings filed that could protract the Chapter 11 Cases; (v) employee attrition and the Company’s ability to retain senior management and other key personnel due to distractions and uncertainties associated with the Chapter 11 Cases, including the Company’s ability to provide adequate compensation and benefits during the Chapter 11 Cases; (vi) the Company’s ability to maintain relationships with vendors, customers, employees, and other third parties and regulatory authorities as a result of the Chapter 11 Cases; (vii) the DIP financing and other financing arrangements; (viii) the effects of the Bankruptcy Petitions on the Company and on the interests of various constituents, including the Company’s stockholders; (ix) the length of time that the Company will operate under Chapter 11 protection and the continued availability of operating capital during the pendency of the proceedings; (x) risks associated with third-party motions in the Chapter 11 Cases, which may interfere with the ability to consummate a restructuring; (xi) the Company’s consummation of a restructuring; (xii) increased administrative and legal costs related to the Chapter 11 process and other litigation and inherent risks involved in a bankruptcy process; (xiii) the Company’s ability to continue funding operations through the Chapter 11 bankruptcy process; (xiv) the Company’s ability to continue as a going concern; (xv) the Company’s ability to successfully execute cost-reduction and productivity initiatives on the anticipated timeline or at all; (xvi) the outcome and timing of the Company’s comprehensive review; (xvii) impairment of goodwill, intangible assets, and other long-lived assets; (xviii) risks related to the Company’s indebtedness, including the levels and maturity date of such indebtedness; (xix) potential liability resulting from pending or future litigation, investigations, or claims; (xx) changes to the Company’s leadership and management team; and (xxi) governmental actions and actions by other third parties that are beyond the Company’s control. All statements included in this Current Report, other than historical facts, are forward-looking statements. All forward-looking statements speak only as of the date of this Current Report. Although the Company believes that the plans, intentions, and expectations reflected in or suggested by the forward-looking statements are reasonable, there is no assurance that these plans, intentions, or expectations will be achieved. Therefore, actual outcomes and results could differ materially from what is expressed, implied, or forecast in such statements.

| Item 9.01. | Financial Statements and Exhibits. |

Exhibits.

SIGNATURES

Pursuant to the requirements of the Exchange Act, the registrant has duly caused this Current Report to be signed on its behalf by the undersigned hereunto duly authorized.

| ENVIVA INC. | ||

| Date: March 13, 2024 | By: | /s/ Jason E. Paral |

| Name: | Jason E. Paral | |

| Title: | Executive Vice President, General Counsel, and Secretary | |

Exhibit 10.1

THIS RESTRUCTURING SUPPORT AGREEMENT DOES NOT CONSTITUTE, AND SHALL NOT BE DEEMED TO BE, AN OFFER OF SECURITIES OR A SOLICITATION OF THE ACCEPTANCE OR REJECTION OF A CHAPTER 11 PLAN FOR PURPOSES OF SECTIONS 1125 AND 1126 OF THE BANKRUPTCY CODE. ANY SUCH OFFER OR SOLICITATION WILL COMPLY WITH ALL APPLICABLE SECURITIES LAWS AND/OR PROVISIONS OF THE BANKRUPTCY CODE. NOTHING CONTAINED IN THIS RESTRUCTURING SUPPORT AGREEMENT SHALL BE AN ADMISSION OF FACT OR LIABILITY OR, UNTIL THE OCCURRENCE OF THE RSA EFFECTIVE DATE ON THE TERMS DESCRIBED HEREIN, DEEMED BINDING ON ANY OF THE PARTIES HERETO.

THIS RESTRUCTURING SUPPORT AGREEMENT DOES NOT PURPORT TO SUMMARIZE ALL OF THE TERMS, CONDITIONS, REPRESENTATIONS, WARRANTIES, AND OTHER PROVISIONS WITH RESPECT TO THE TRANSACTIONS DESCRIBED HEREIN, WHICH TRANSACTIONS WILL BE SUBJECT TO THE COMPLETION OF DEFINITIVE DOCUMENTATION INCORPORATING THE TERMS SET FORTH HEREIN, AND THE CLOSING OF ANY TRANSACTION SHALL BE SUBJECT TO THE TERMS AND CONDITIONS SET FORTH IN SUCH DEFINITIVE DOCUMENTATION AND THE APPROVAL RIGHTS OF THE PARTIES SET FORTH HEREIN AND IN SUCH DEFINITIVE DOCUMENTATION.

ENVIVA INC.

RESTRUCTURING SUPPORT AGREEMENT

March 12, 2024

This Restructuring Support Agreement (together with the exhibits and schedules attached hereto, as each may be amended, restated, supplemented, or otherwise modified from time to time in accordance with the terms hereof, this “Agreement”),1 dated as of March 12, 2024, is entered into by and among the following parties:

| (i) | Enviva Inc. and those certain subsidiaries of Enviva Inc. listed on Schedule 1 hereto (such subsidiaries and Enviva Inc. each a “Debtor” and, collectively, the “Debtors”); |

| (ii) | the undersigned holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders, of the senior notes issued pursuant to that certain Indenture, dated as of December 9, 2019, among Enviva Partners, LP and Enviva Partners Finance Corp., as issuers, each of the guarantors party thereto, and Wilmington Savings Fund Society, FSB, as trustee (in such capacity, the “2026 Notes Indenture Trustee”) (as amended, restated, modified, supplemented, or replaced from time to time prior to the Petition Date, the “2026 Notes Indenture”), for the 6.500% senior notes due 2026 (the “2026 Notes,” and the claims against the Debtors on account thereof, the “2026 Notes Claims”) (such holders, together with their respective successors and permitted assigns and any subsequent holder of 2026 Notes that may become in accordance with Section 12 and/or Section 13 hereof signatory hereto, collectively, the “Consenting 2026 Noteholders”); |

| 1 | Unless otherwise noted, capitalized terms used but not immediately defined herein shall have the meanings ascribed to them at a later point in this Agreement or in the Term Sheet (as defined herein), as applicable. |

| (iii) | the undersigned holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders, whether as record holders or participants, of loans or commitments (the “Senior Secured Credit Facility Loans”) under that certain Amended and Restated Credit Agreement dated as of October 18, 2018 (as amended, restated, modified, supplemented, or replaced from time to time prior to the Petition Date, the “Senior Secured Credit Agreement,” and the claims arising thereunder, the “Senior Secured Credit Facility Claims”) among Enviva Inc., as administrative borrower, Enviva LP, as subsidiary borrower, Ankura Trust Company, LLC, as administrative agent and collateral agent (in such capacity, the “Senior Secured Credit Facility Agent”), and the lenders party thereto from time to time (such lenders, together with their respective successors and permitted assigns and any subsequent lender that may become in accordance with Section 12 and/or Section 13 hereof signatory hereto, collectively, the “Consenting Senior Secured Credit Facility Lenders”); |

| (iv) | (A) the undersigned holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders, of Exempt Facilities Revenue Bonds (Enviva Inc. Project), Series 2022 (Green Bonds) (the “Epes Green Bonds,” and the claims against the Debtors on account thereof, the “Epes Green Bonds Claims”) issued by the Industrial Development Authority of Sumter County, Alabama (the “Epes Green Bonds Issuer”) pursuant to that certain Indenture of Trust, dated as of July 1, 2022, between Epes Green Bonds Issuer and Wilmington Trust, N.A., as trustee (the “Epes Green Bonds Trustee”) (such holders, together with their respective successors and permitted assigns and any subsequent holder of Epes Green Bonds that may become in accordance with Section 12 and/or Section 13 hereof signatory hereto, collectively, the “Consenting Epes Green Bondholders”); and |

| (v) | (A) the undersigned holders or beneficial holders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or beneficial holders, of Exempt Facilities Revenue Bonds, (Enviva Inc.), Series 2022 (Green Bonds) (the “Bond Green Bonds,” and, the claims against the Debtors on account of the Bond Green Bonds, the “Bond Green Bonds Claims” and, the Bond Green Bonds Claims together with the Epes Green Bonds Claims, the “Green Bonds Claims”2 and, the Green Bonds Claims together with the 2026 Notes Claims and the Senior Secured Credit Facility Claims, the “Company Claims/Interests”) issued by Mississippi Business Finance Corporation (the “Bond Green Bonds Issuer”) pursuant to that certain Indenture of Trust, dated as of November 1, 2022, between Bond Green Bonds Issuer and Wilmington Trust, N.A., as trustee (the “Bond Green Bonds Trustee”) (such holders, together with their respective successors and permitted assigns and any subsequent holder of Bond Green Bonds that may become in accordance with Section 12 and/or Section 13 hereof signatory hereto, collectively, the “Consenting Bond Green Bondholders,” and collectively with the Consenting Epes Green Bondholders, the “Consenting Green Bondholders” and, together with the Consenting 2026 Noteholders and the Consenting Senior Secured Credit Facility Lenders, the “Restructuring Support Parties”). |

| 2 | For the avoidance of doubt, any reference herein to the principal amount of Green Bonds Claims as of the RSA Effective Date shall, upon the consummation of either the Epes Bond Settlement or the MS Bond Settlement (each as defined herein), as applicable, refer to the adjusted principal amount of the applicable Green Bonds Claims after the consummation of the applicable Settlement. |

This Agreement collectively refers to the Debtors and the Restructuring Support Parties as the “Parties” and each individually as a “Party.”

RECITALS

WHEREAS, as of the date hereof, the Consenting 2026 Noteholders, in the aggregate, hold, or are investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of beneficial owner(s) that hold, approximately 95% of the aggregate outstanding principal amount of the 2026 Notes;

WHEREAS, as of the date hereof, the Consenting Senior Secured Credit Facility Lenders, in the aggregate, hold, or are investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of beneficial owner(s) that hold, approximately 72% of the aggregate outstanding principal amount of Senior Secured Credit Facility Loans;

WHEREAS, as of the date hereof, the Consenting Epes Green Bondholders, in the aggregate, hold, or are investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of beneficial owner(s) that hold, approximately 78% of the aggregate outstanding principal amount of the Epes Green Bonds;

WHEREAS, as of the date hereof, the Consenting Bond Green Bondholders, in the aggregate, hold, or are investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of beneficial owner(s) that hold, approximately 45% of the aggregate outstanding principal amount of the Bond Green Bonds; and

WHEREAS, the Debtors and the Restructuring Support Parties have, in good faith and at arms’ length, negotiated certain restructuring transactions (the “Restructuring”) with respect to the Debtors on the terms set forth in this Agreement and as specified in the restructuring term sheet attached hereto as Exhibit A (as may be amended, restated, supplemented, or otherwise modified from time to time in accordance herewith, the “Term Sheet”) and incorporated herein by reference pursuant to Section 2 hereof, which will be implemented through jointly administered voluntary cases commenced by the Debtors (the “Chapter 11 Cases”) under chapter 11 of title 11 of the United States Code, 11 U.S.C. §§ 101–1532 (as amended, the “Bankruptcy Code”), in the United States Bankruptcy Court for the Eastern District of Virginia (the “Bankruptcy Court”), pursuant to the Plan3, which will be filed by the Debtors in the Chapter 11 Cases in accordance with the Milestones set forth in Section 4 of this Agreement.

| 3 | “Plan” means the joint plans of reorganization for each of the Debtors under chapter 11 of the Bankruptcy Code on the terms and subject to the conditions set forth herein, including in the Term Sheet. |

NOW, THEREFORE, in consideration of the promises, mutual covenants, and agreements set forth herein, and for other good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, each of the Parties, intending to be legally bound, hereby agrees as follows:

AGREEMENT

1. RSA Effective Date. This Agreement shall become effective, and the obligations contained herein shall become binding upon the Parties, upon the first date (such date, the “RSA Effective Date”) that this Agreement has been executed by all of the following: (i) each Debtor; (ii) the holders4 of at least one-half of the aggregate outstanding principal amount of Senior Secured Credit Facility Claims; (iii) the holders of at least two-thirds of the aggregate outstanding principal amount of 2026 Notes Claims; (iv) the holders of at least 45% of the aggregate outstanding principal amount of Bond Green Bonds Claims; (v) the holders of at least two-thirds of the aggregate outstanding principal amount of Epes Green Bonds Claims; provided that the RSA Effective Date with respect to any Joining Party shall be the date that such Joining Party executes a Joinder Agreement; and (vi) the Forbearance Agreements5 shall be in full force and effect and the Debtors shall be in full compliance therewith.

2. Exhibits and Schedules Incorporated by Reference. Each of the exhibits attached hereto and any schedules to such exhibits (collectively, the “Exhibits and Schedules”) is expressly incorporated herein and made a part of this Agreement, and all references to this Agreement shall include the Exhibits and Schedules. In the event of any inconsistency between this Agreement (without reference to the Exhibits and Schedules) and the Exhibits and Schedules, this Agreement (without reference to the Exhibits and Schedules) shall govern.

| 4 | References to “holder” or “lender” herein shall include holders or lenders or beneficial holders (including participants) or lenders, investment advisors, sub-advisors, or managers of funds and/or accounts that are holders or lenders, or beneficial holders (including participants) or lenders, as applicable. For purposes of this Agreement, including in connection with determining requisite consent thresholds, termination thresholds, the occurrence of the RSA Effective Date, covenants, and representations and warranties with respect to holdings of Company Claims/Interests, holdings of Company Claims/Interests shall include any executed but unsettled trades and any Company Claims/Interests beneficially held by the applicable party. Any covenants or representations and warranties with respect to voting shall be satisfied with respect to any unsettled trades by using commercially reasonable efforts to exercise all rights such Restructuring Support Party has to cause and direct the applicable holder of such Company Claims/Interests to vote. |

| 5 | “Forbearance Agreements” means, collectively, (i) the forbearance agreement dated as of February 16, 2024, between Enviva Inc. and certain of its subsidiaries more particularly detailed therein, as debtors and the holders or investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of holders, of the senior notes issued pursuant to that certain Indenture dated as of December 9, 2019, as requisite creditors, (ii) the forbearance agreement dated as of February 16, 2024, between Enviva Inc. and certain of its subsidiaries more particularly detailed therein, as debtors and the holders, or investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of holders, of loans or commitments under that certain Amended and Restated Credit Agreement, dated as of October 18, 2018, as requisite creditors, and (iii) the forbearance agreement dated as of February 16, 2024, between Enviva Inc. and certain of its subsidiaries more particularly detailed therein, as debtors and the holders or investment advisors, sub-advisors, or managers of discretionary accounts or funds acting on behalf of holders, of Exempt Facilities Revenue Bonds (Enviva Inc. Project), Series 2022 (Green Bonds) issued by the Industrial Development Authority of Sumter County, as requisite creditors. |

3. Definitive Documentation.

| (a) | The definitive documents and agreements governing the Restructuring (each, including all amendments, modifications and supplements thereto, a “Definitive Document” and collectively, the “Definitive Documentation”) shall include: |

| (i) | the Plan and all exhibits thereto (including the compilation of documents and forms of documents, schedules, and exhibits to the Plan that will be filed by the Debtors with the Bankruptcy Court in accordance with this Agreement (the “Plan Supplement”), including the exhibit to the Plan Supplement that will set forth the material components of the transactions that are required to effectuate the Restructuring contemplated by this Agreement and the Plan Supplement, including any “restructuring steps memo,” “tax steps memo” or other document describing steps to be taken and the related tax considerations in connection with the Restructuring (the “Restructuring Transactions Exhibit”)); |

| (ii) | the confirmation order with respect to the Plan (the “Confirmation Order”) and any pleadings in support of entry thereof; |

| (iii) | the order with respect to the Disclosure Statement (the “Disclosure Statement Order”) (including the Disclosure Statement and Solicitation Motion (as defined herein)); |

| (iv) | the solicitation materials with respect to the Plan, including the disclosure statement (and all exhibits thereto) with respect to the Plan (the “Disclosure Statement”) (collectively, the “Solicitation Materials”); |

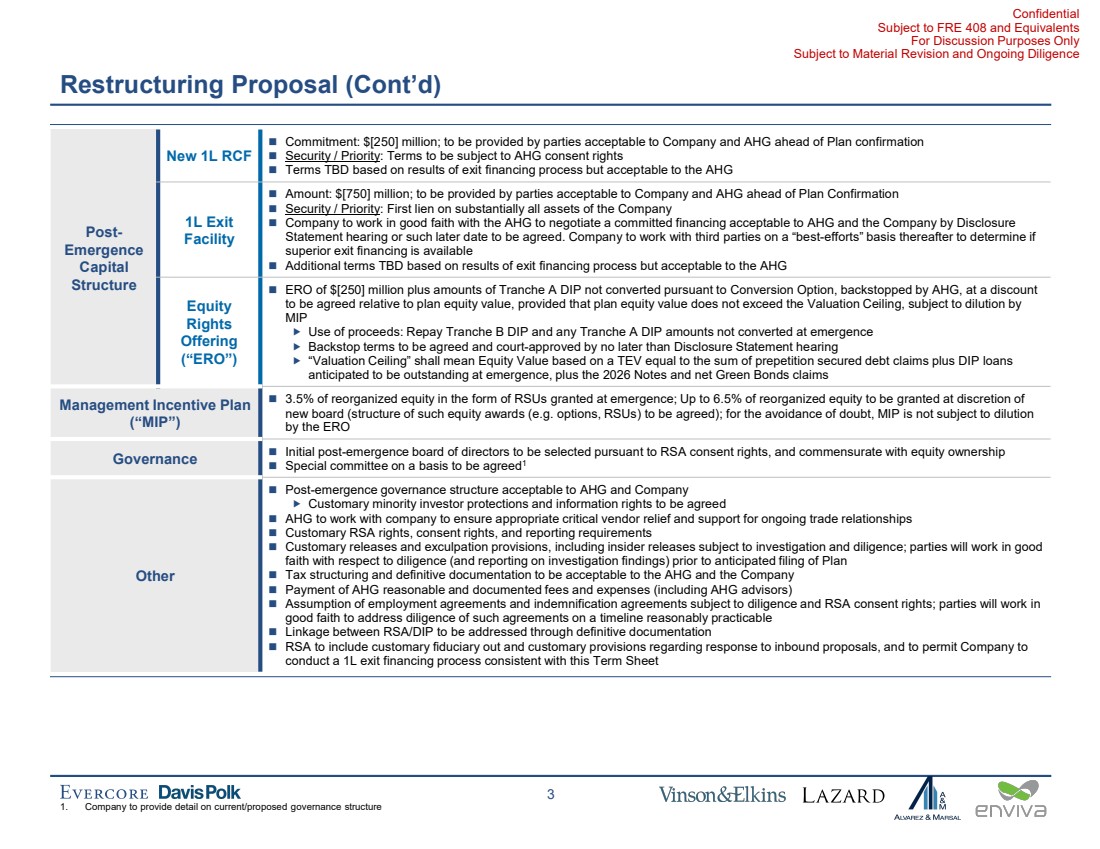

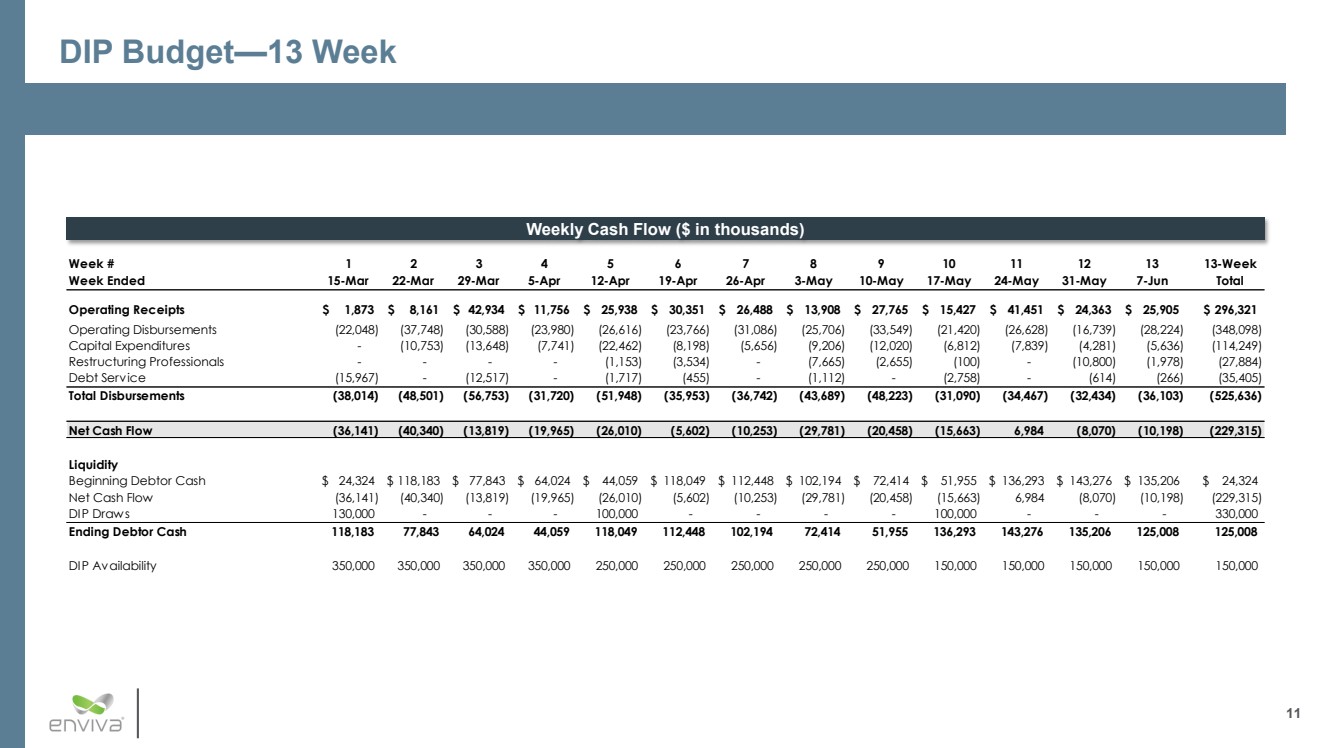

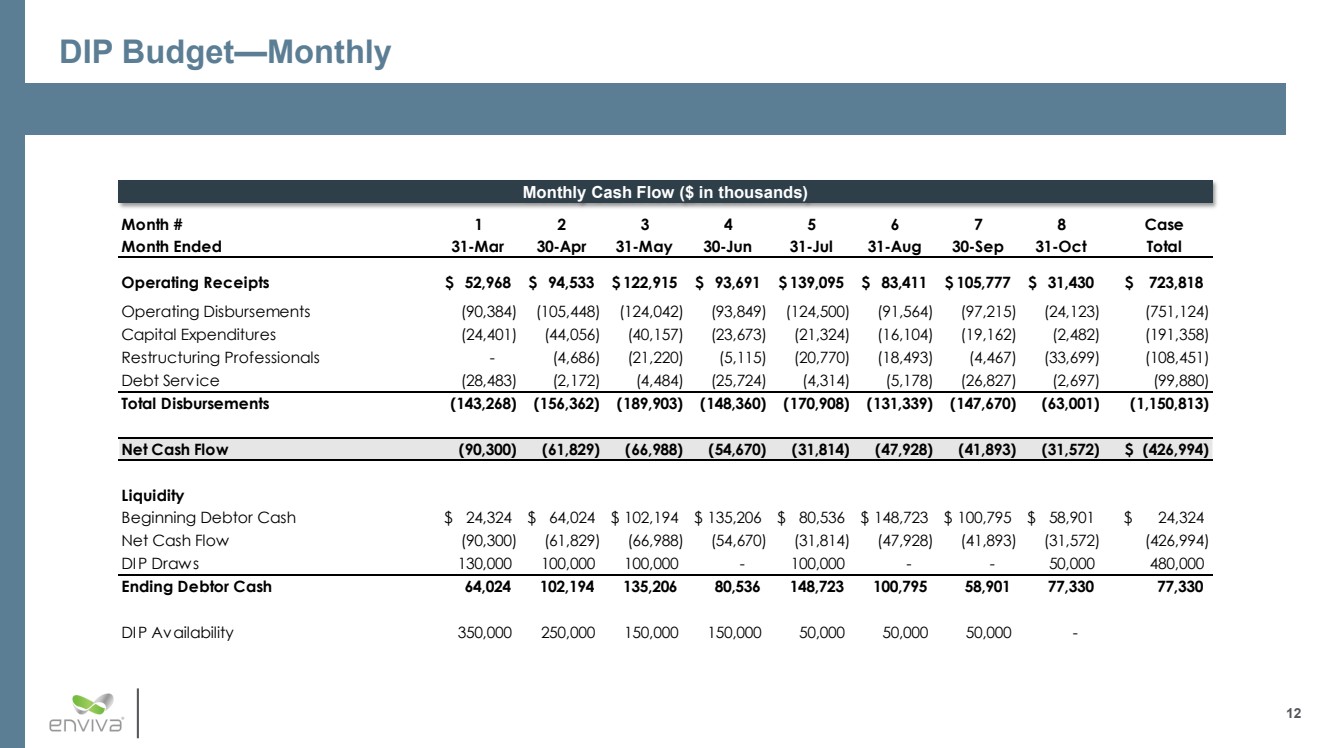

| (v) | (A) the interim order authorizing, among other things, the Debtors to use cash collateral and obtain debtor-in-possession financing (the “Interim DIP Order”), (B) the final order authorizing, among other things, the Debtors to use cash collateral and obtain debtor-in-possession financing (the “Final DIP Order” and, together with the Interim DIP Order, the “DIP Orders”), and (C) the debtor-in-possession credit agreement and note purchase agreement (the “DIP Facility Agreement”) and all related documentation, including any budget (the “DIP Budget”) or term sheet (the “DIP Term Sheet”) related thereto, regarding the debtor-in-possession financing including any equity conversion processes or mechanisms relating thereto (collectively, the “DIP Financing Documents” and, such financing, the “DIP Financing”); |

| (vi) | all documentation related to any exit financing for the Restructuring (collectively, the “Exit Financing Documents”); |

| (vii) | all documentation related to the new money rights offering, which will be offered pursuant to section 1145 of the Bankruptcy Code and/or any other applicable law, including, without limitation, under section 4(a)(2) of the Securities Act (the “Rights Offering”), including the order authorizing the Debtors to enter into the Backstop Agreement (the “Backstop Approval Order”) and the procedures for the implementation of the Rights Offering (the “Rights Offering Procedures”) (collectively with the Backstop Agreement, the “Rights Offering Documents”); |

| (viii) | the backstop agreement with respect to the Rights Offering (the “Backstop Agreement”); |

| (ix) | any “key employee” retention or incentive plan and any motion, declaration or order related thereto; |

| (x) | all “first day” motions, applications, and other documents that any Debtor intends to file with the Bankruptcy Court and seeks to have heard on an expedited basis at the “first-day hearing” in the Chapter 11 Cases and any proposed orders related thereto; |

| (xi) | all documentation addressing or relating to the MS Bond Settlement (as defined herein) (the “MS Bond Settlement Documents”) and/or the Epes Bond Settlement (as defined herein) (the “Epes Bond Settlement Documents”); |

| (xii) | any other material documents, agreements, motions, pleadings, supplements, briefs, applications, orders, and other filings with the Bankruptcy Court, including any term sheets in respect thereof related to any of the foregoing or as may be reasonably necessary or advisable to implement the Restructuring; and |

| (xiii) | to the extent not included, any motions and related proposed orders, or amendment or modification of any order, related to each of the above. |

| (b) | The Definitive Documentation identified in Section 3(a) not executed or in a form attached to this Agreement will, after the RSA Effective Date, remain subject to negotiation and completion. The Definitive Documentation, including all amendments and modifications thereto and including all forms thereof filed with the Bankruptcy Court, shall contain terms, conditions, representations, warranties, and covenants consistent with the terms of this Agreement and shall be at all times in form and substance reasonably acceptable to (i) the Debtors and (ii) the Consenting 2026 Noteholders holding at least one-half in dollar amount of the aggregate outstanding principal amount of the 2026 Notes Claims held by all Consenting 2026 Noteholders at the time of such consent (the “Majority Consenting 2026 Noteholders”); provided, that, without limiting the foregoing, (A) the Plan, the Plan Supplement, the DIP Orders, the DIP Facility Agreement, the Backstop Agreement, the Backstop Approval Order and the Confirmation Order shall be in form and substance acceptable to the Debtors and the Majority Consenting 2026 Noteholders; (B) (x) the MS Bond Settlement Documents and (y) any other Definitive Document to the extent related to or concerning the Plan treatment of the Bond Green Bonds to the extent materially and adversely inconsistent with this Agreement (including as may be amended), shall, in each case, be reasonably acceptable to the Debtors and the Consenting Bond Green Bondholders holding at least one-half in dollar amount of the aggregate outstanding principal amount of the Bond Green Bonds Claims held by all Consenting Bond Green Bondholders at the time of such consent (the “Majority Consenting Bond Green Bondholders”); (C) (x) the Epes Bond Settlement Documents and (y) any other Definitive Document to the extent related to or concerning the Plan treatment of the Epes Green Bonds to the extent materially and adversely inconsistent with this Agreement (including as may be amended), shall, in each case, be reasonably acceptable to the Debtors and the Consenting Epes Green Bondholders holding at least one-half in dollar amount of the aggregate outstanding principal amount of the Epes Green Bonds Claims held by all Consenting Epes Green Bondholders at the time of such consent (the “Majority Consenting Epes Green Bondholders”); and (D) any Definitive Document, to the extent related to or concerning (x) the use of prepetition cash collateral, adequate protection or stipulations and findings relating to the Senior Secured Credit Facility Claims, (y) the Plan treatment of the Senior Secured Credit Facility Claims to the extent materially and adversely inconsistent with this Agreement (including as may be amended) and (z) the Exit Financing Documents (solely to the extent the Senior Secured Credit Facility Claims convert to obligations under such Exit Financing) shall be reasonably acceptable to the Debtors and the Consenting Senior Secured Credit Facility Lenders holding at least one-half in dollar amount of the aggregate outstanding principal amount of the Senior Secured Credit Facility Claims held by all Consenting Senior Secured Credit Facility Lenders at the time of such consent (the “Majority Consenting Senior Secured Credit Facility Lenders”); provided further, that any provision of any Definitive Document setting out allocations of the DIP Financing or any backstop of the Rights Offering or Exit Financing shall be acceptable to the Debtors and the ad hoc group of those holders of Company Claims/Interests, including the 2026 Notes Claims (the “Ad Hoc Group”) represented by Davis Polk & Wardwell LLP (“Davis Polk”), as legal counsel, and Evercore Group L.L.C. (“Evercore”), as financial advisor, in connection with the Restructuring (collectively, the “Ad Hoc Group Advisors”). |

| (c) | For the avoidance of doubt, any reference in this Agreement to a Definitive Document or other instrument shall be construed to include the attendant consent rights set forth herein, and failure to explicitly refer to such consent rights when referencing or defining a Definitive Document or instrument shall not impair such rights. |

4. Milestones. As provided in and subject to Section 6, the Debtors shall implement the Restructuring on the following timeline (each deadline, a “Milestone”):6

| (a) | no later than March 12, 2024 at 11:59 p.m. (prevailing Eastern Time), the Debtors shall commence the Chapter 11 Cases by filing petitions for relief under chapter 11 of the Bankruptcy Code with the Bankruptcy Court (such filing date, the “Petition Date”); |

| (b) | no later than one calendar day after the Petition Date, the Debtors shall file with the Bankruptcy Court a motion seeking entry of the DIP Orders; |

| (c) | no later than seven calendar days after the Petition Date, the Debtors shall have obtained entry by the Bankruptcy Court of the Interim DIP Order; |

| (d) | no later than 14 calendar days after the Petition Date, the Debtors shall file with the Bankruptcy Court a motion seeking entry of an order setting a date as the deadline for submitting any claim (as defined in section 101(5) of the Bankruptcy Code, a “Claim”) against the Debtors (other than administrative and government Claims) (such order, the “Bar Date Order”); |

| (e) | no later than 35 calendar days after the Petition Date, the Debtors shall have obtained entry by the Bankruptcy Court of the Final DIP Order; |

| (f) | no later than 45 calendar days after the Petition Date, the Debtors shall file with the Bankruptcy Court a motion seeking rejection of the Rejected Customer Contracts7; |

| (g) | no later than 90 calendar days after the Petition Date, the Debtors shall deliver to the Ad Hoc Group an initial draft of their revised long-term business plan; |

| (h) | no later than 100 calendar days after the Petition Date, the Debtors shall have entered into definitive documentation in respect of all renegotiated Customer Contracts8; provided that the Milestone in this Section 4(h) may be extended if the Debtors, in their sole discretion, and in consultation with the Ad Hoc Group, determine that continuing good faith negotiations in respective of any Customer Contract is in the best interest of the Debtors and their Estates9; |

| (i) | no later than 115 calendar days after the Petition Date, the Debtors shall deliver to the Ad Hoc Group their revised long-term business plan; |

| 6 | In computing any period of time prescribed or allowed under this Agreement, the provisions of Federal Rule of Bankruptcy Procedure 9006(a) shall apply. |

| 7 | “Rejected Customer Contracts” means the initial Customer Contracts (as defined below) that the Debtors will file a motion seeking to reject in the Chapter 11 Cases. |

| 8 | “Customer Contracts” means the contracts for the sale of wood pellets between a Debtor and a Customer. |

| 9 | “Estates” means the estates of the Debtors created under section 541 of the Bankruptcy Code upon the commencement of each Debtor’s Chapter 11 Case and all property acquired by each Debtor after the Petition Date and before the Effective Date. |

| (j) | no later than 120 calendar days after the Petition Date, the Debtors shall file with the Bankruptcy Court: (i) the Plan; (ii) the Disclosure Statement; (iii) a motion (the “Disclosure Statement and Solicitation Motion”) seeking, among other things, (A) approval of the Disclosure Statement, (B) approval of procedures for soliciting, receiving, and tabulating votes on the Plan and for filing objections to the Plan, (C) approval of the Solicitation Materials, and (D) to schedule the hearing to consider final approval of the Disclosure Statement and confirmation of the Plan; (iv) a motion seeking approval of the Backstop Agreement; and (v) a motion seeking approval of the Rights Offering Procedures; |

| (k) | no later than 150 calendar days after the Petition Date, the Bankruptcy Court shall have entered (i) the Disclosure Statement Order and (ii) the Backstop Approval Order; |

| (l) | no later than five calendar days after entry of the Disclosure Statement Order, the Debtors shall have commenced a solicitation of votes to accept or reject the Plan in accordance with the order approving the Disclosure Statement and Solicitation Motion; |

| (m) | no later than 185 calendar days after the Petition Date, the Bankruptcy Court shall have entered the Confirmation Order; and |

| (n) | no later than 205 calendar days after the Petition Date, the Debtors shall have consummated the transactions contemplated by the Plan (the date of such consummation, the “Effective Date”), it being understood that the satisfaction or waiver of the conditions precedent to the Effective Date (as set forth in the Plan) are conditions precedent to the occurrence of the Effective Date. |

Each of the Milestones may be extended or waived with the express prior written consent of the Majority Consenting 2026 Noteholders.

5. Commitment of Restructuring Support Parties. Each Restructuring Support Party shall (severally and not jointly), solely so long as it remains the holder of or with power and/or authority to bind any of its applicable Company Claims/Interests, from the RSA Effective Date until the occurrence of a Termination Date (as defined in Section 10) applicable to such Restructuring Support Party:

| (a) | support and use commercially reasonable efforts to cooperate with the Debtors to take all actions reasonably necessary to obtain approval of the DIP Financing and consummate the Restructuring in accordance with the Plan, in each case on the terms and conditions of this Agreement and the Term Sheet; |

| (b) | vote (or, to the extent of any applicable legal entitlements, instruct its proxy or other relevant person to vote) each of its Company Claims/Interests now or hereafter acquired by such Restructuring Support Party (or for which such Restructuring Support Party now or hereafter has voting control over), for so long as it remains the holder thereof, to accept the Plan in accordance with the applicable procedures set forth in the Disclosure Statement and the Solicitation Materials, as approved by the Bankruptcy Court, and timely return a duly-executed ballot in connection therewith; |

| (c) | to the extent that it is permitted to elect whether to opt out of (or opt in to) any releases to be provided under the Plan, elect not to opt out of (or elect to opt in to) such releases; |

| (d) | not withdraw, amend, or revoke (or cause to be withdrawn, amended, or revoked) its consent, waiver, subscription, or vote with respect to the Restructuring or the Plan; provided, however, that the consent, waiver, subscription, or vote of a Restructuring Support Party shall be immediately deemed void ab initio upon the occurrence of a Termination Date with respect to such Restructuring Support Party in accordance with the terms hereof and such Restructuring Support Party shall have a reasonable opportunity to cast a vote; |

| (e) | use commercially reasonable efforts to provide any applicable consents as may be necessary or required to effectuate the Restructuring as set forth herein, in the Term Sheet and in the Definitive Documentation (in each case without limiting or superseding any consent rights herein or in any such documents); |

| (f) | (i) in the case of the Consenting Senior Secured Credit Facility Lenders, give any reasonable notice, order, instruction, or direction to the Senior Secured Credit Facility Agent necessary to give effect to the Restructuring (including the DIP Financing), and not give any notice, order, instruction, or direction to the Senior Secured Credit Facility Agent to take any action inconsistent with such Consenting Senior Secured Credit Facility Lender’s obligations under this Agreement; (ii) in the case of the Consenting 2026 Noteholders, give any reasonable notice, order, instruction, or direction to the 2026 Notes Indenture Trustee necessary to give effect to the Restructuring (including the DIP Financing), and not give any notice, order, instruction, or direction to the 2026 Notes Indenture Trustee to take any action inconsistent with such Consenting 2026 Noteholder’s obligations under this Agreement; and (iii) in the case of the Consenting Green Bondholders, give any reasonable notice, order, instruction, or direction to the Epes Green Bonds Trustee and/or the Bond Green Bonds Trustee, as applicable, necessary to give effect to the Restructuring (including the DIP Financing), and not give any notice, order, instruction, or direction to the Epes Green Bonds Trustee and/or the Bond Green Bonds Trustee, as applicable, to take any action inconsistent with such Consenting Green Bondholders’ obligations under this Agreement; provided that nothing herein shall abrogate or reduce any consent rights of any Restructuring Support Party under the DIP Orders or other DIP Financing Documents or the ability of any Restructuring Support Party to enforce any rights or remedies under the DIP Orders or DIP Financing Documents or cause or direct enforcement of such rights, including in connection with any termination or default by the Debtors thereunder; |

| (g) | (i) provide reasonable support and cooperation to the Debtors in connection with the Debtors’ process of negotiating modifications to certain Customer Contracts with key customers of the Debtors (the “Customers”), it being understood that (x) the Debtors’ efforts shall be undertaken in consultation with the Ad Hoc Group and Ad Hoc Group Advisors and in a manner consistent with the terms and conditions of the Restructuring and (y) any agreements and/or modifications to agreements involving the Debtors and the Customers shall be subject to the applicable consent rights set forth herein and in the Definitive Documents; and (ii) not engage with the Customers regarding the Restructuring or the negotiations described in the foregoing clause (i) without the prior written consent of the Debtors (such consent not to be unreasonably withheld), so long as nothing herein shall prohibit the Ad Hoc Group from engaging with any party in interest that has appeared or otherwise engaged in the Chapter 11 Cases or restrict any communications by the Ad Hoc Group Advisors, in each case, with respect to the Restructuring; provided further that, in connection with the foregoing, the Ad Hoc Group and Ad Hoc Group Advisors shall, as reasonably practicable, consult with the Debtors and their advisors and provide advance notice in connection with initiating any such discussions with Customers; |

| (h) | support and not oppose, delay or impede the Debtors’ negotiation, prosecution and implementation of the MS Bond Settlement and the Epes Bond Settlement; provided, however, that nothing set forth in this sub-clause 5(h) is intended to impose any cost on any Party other than as may be set forth in the MS Bond Settlement or the Epes Bond Settlement; |

| (i) | not object to, delay, impede, or take any action that is inconsistent with, or is intended to interfere with, the acceptance, implementation, or consummation of the Restructuring (including the DIP Financing); |

| (j) | engage in good faith negotiations with the Debtors regarding potential modifications or alternatives that do not negatively impact the economic or legal terms, rights or recoveries of the Restructuring Support Parties (relative to the terms and conditions set forth in the Term Sheet) in the event that the DIP Financing is not approved on the terms set forth in the Term Sheet and upon the Debtors’ reasonable request; |

| (k) | negotiate in good faith upon reasonable request of the Debtors any modifications to the Restructuring that improve the tax efficiency of the Restructuring or are otherwise necessary to address any legal, financial, or structural impediment that may prevent the consummation of the Restructuring (in each case to the extent such modifications can be implemented without any material adverse effect on any members of the Ad Hoc Group or the Restructuring); |

| (l) | negotiate in good faith and, to the extent agreed in accordance with the terms of this Agreement, use commercially reasonable efforts to execute (as applicable) and implement the Definitive Documentation to which it is required to be a party; |

| (m) | support and not object to, delay, impede, or take any other action, whether direct or indirect, inconsistent with the Restructuring (including the entry by the Bankruptcy Court of the DIP Orders and the execution and implementation thereof), or propose, file, support, or vote for, seek, solicit, pursue, initiate, assist, join in, participate in the formulation of, or enter into negotiations with any entity regarding any restructuring, workout, Alternative Transaction, Alternative Transaction Proposal, or chapter 11 plan for any of the Debtors other than the Restructuring and the Plan (but without limiting consent, approval, or termination rights provided in this Agreement and the Definitive Documentation); and |

| (n) | not object to or otherwise seek to hinder the Debtors’ retention of and payment to Lazard Frères & Co. LLC (“Lazard”) of the fees and expenses set forth in the engagement letter, dated as of January 25, 2024, and amended as of February 27, 2024, among Lazard, Vinson & Elkins LLP, and Enviva Inc., as modified and supplemented pursuant to that certain agreement communicated by email among Lazard, Vinson & Elkins LLP, Enviva Inc., and the Ad Hoc Group Advisors on March 12, 2024, and, in each case, any application seeking approval of or court order approving the same. |

Notwithstanding anything contained in this Agreement, nothing in this Agreement and neither a vote to accept the Plan by any Restructuring Support Party nor the acceptance of the Plan by any Restructuring Support Party shall (i) be construed to prohibit any Restructuring Support Party from contesting whether any matter, fact, or thing is a breach of, or is inconsistent with, this Agreement or the Definitive Documentation, or exercising rights or remedies reserved herein or therein, (ii) be construed to limit any Restructuring Support Party’s rights under any applicable indenture, credit agreement, other loan document, and/or applicable law or to prohibit any Restructuring Support Party from appearing as a party-in-interest in any matter to be adjudicated in the Chapter 11 Cases, so long as, from the RSA Effective Date until the occurrence of a Termination Date, such appearance and the positions advocated in connection therewith are not materially inconsistent with this Agreement and are not for the purpose of hindering, delaying, or preventing the consummation of the Restructuring, (iii) impair or waive the rights of any Restructuring Support Party to assert or raise any objection permitted under (A) this Agreement in connection with any hearing on confirmation of the Plan or in the Bankruptcy Court or (B) under the DIP Orders or DIP Financing Documents, (iv) prevent any Restructuring Support Party from enforcing this Agreement or contesting whether any matter, fact, or thing is a breach of, or is inconsistent with, this Agreement, (v) be construed to prohibit any Restructuring Support Party from, either itself or through any representatives or agents, soliciting, initiating, negotiating, facilitating, proposing, continuing or responding to any proposal to purchase or sell Company Claims/Interests, so long as such Restructuring Support Party complies with Section 13 hereof; (vi) obligate a Restructuring Support Party to deliver a vote to support the Plan or prohibit a Restructuring Support Party from changing such vote, in each case from and after the Termination Date as to such Restructuring Support Party (other than pursuant to Section 10); (vii) affect the ability of any Restructuring Support Party to consult with any other Restructuring Support Party, the Debtors, or any other party in interest in the Chapter 11 Cases (including any official committee and the United States Trustee), subject to sub-paragraph (g) of this Section 5; (viii) be construed to prohibit or limit any Restructuring Support Party from taking or directing any action relating to maintenance, protection or preservation of any collateral, provided that such action is not materially inconsistent with this Agreement; (ix) prohibit any Restructuring Support Party from taking any other action that is not inconsistent with this Agreement, the Restructuring or any Definitive Document; (x) require any Consenting Senior Secured Credit Facility Lender to breach or potentially breach any participation agreement relating to the Senior Secured Credit Facility Loans to which such Consenting Senior Secured Credit Facility Lender is a party; (xi) require any Restructuring Support Party to incur any costs or provide any entity with any indemnity in connection with this Agreement and/or the Restructuring except as may be agreed in the Definitive Documentation; or (xii) be construed to be a binding commitment on the part of any Restructuring Support Party to provide any financing, funding or any other similar funding commitments relating to the Restructuring, including with respect to the DIP Financing, the Exit Financing, the Rights Offering, or any backstop to the foregoing, except to the extent such Restructuring Support Party agrees, pursuant to a Definitive Document, to provide such financing, funding or other funding commitment.

6. Commitment of the Debtors. Each of the Debtors agrees to, and agrees to cause each of its direct and indirect subsidiaries to:

| (a) | (i) (A) support and use commercially reasonable efforts to take all steps reasonably necessary and desirable to complete the Restructuring set forth in the Plan and this Agreement, (B) negotiate in good faith, and, to the extent agreed in accordance with the terms of this Agreement, execute and implement (to the extent the Debtors are required to be a party) all Definitive Documentation that is subject to negotiation as of the RSA Effective Date, (C) use commercially reasonable efforts to complete the Restructuring set forth in the Plan in accordance with each Milestone set forth in Section 4 of this Agreement, and (D) obtain, file, submit, or register any and all required governmental, regulatory, and third-party approvals that are necessary or required for the implementation or consummation of the Restructuring or approval by the Bankruptcy Court of the Definitive Documentation, and (ii) shall not undertake any action inconsistent with the adoption and implementation of the Plan and the confirmation thereof; |

| (b) | timely file a formal objection to any motion, pleading, application, adversary proceeding or cause of action filed with the Bankruptcy Court by a third party seeking the entry of an order (i) directing the appointment of a trustee or examiner (with expanded powers beyond those set forth in section 1106(a)(3) and (4) of the Bankruptcy Code), (ii) converting the Chapter 11 Cases to cases under chapter 7 of the Bankruptcy Code, (iii) dismissing the Chapter 11 Cases, (iv) modifying or terminating the Debtors’ exclusive right to file and/or solicit acceptances of a plan of reorganization, as applicable or (v) for relief that (y) is inconsistent with this Agreement or any Definitive Document in any material respect or (z) would or would reasonably be expected to frustrate the purposes of this Agreement or any Definitive Document, including by preventing consummation of the Restructuring; |

| (c) | oppose, object to and timely file a formal written response in opposition to any objection filed with the Bankruptcy Court by any person with respect to the Restructuring, the DIP Financing or any Definitive Document (provided that the Debtors and the Ad Hoc Group Advisors may agree that no written response is required with respect to certain objections); |

| (d) | not solicit proposals or offers for any chapter 11 plan or restructuring transaction (including, for the avoidance of doubt, a transaction premised on an asset sale under section 363 of the Bankruptcy Code) other than the Restructuring (an “Alternative Transaction” and any inquiry, proposal, offer, bid, indication of interest, or term sheet with respect to an Alternative Transaction, whether written or oral, an “Alternative Transaction Proposal”) received from a party other than the Restructuring Support Parties; provided, however, that, notwithstanding the foregoing, the Debtors and their respective directors, officers, employees, investment bankers, attorneys, accountants, consultants, and other advisors or representatives, and in the case of any Debtor that is a wholly owned direct or indirect subsidiary of Enviva Inc., any manager or member of such Debtor, shall have the right, consistent with their fiduciary duties, to (i) consider, respond to, and discuss unsolicited Alternative Transaction Proposals received by any Debtor; (ii) provide access to nonpublic information concerning the Debtors to any person or entity that: (A) provides an unsolicited Alternative Transaction Proposal; (B) executes and delivers to the Debtors a customary confidentiality agreement, which shall be in form and substance no less restrictive than the confidentiality agreement between the Debtors and the Ad Hoc Group, and otherwise acceptable to the Debtors; and (C) requests such information; (iii) maintain or continue discussions or negotiations with respect to any unsolicited Alternative Transaction Proposals (including, for the avoidance of doubt, any unsolicited Alternative Transaction Proposal that was proposed to the Debtors prior to the RSA Effective Date); and (iv) enter into or continue discussions or preliminary negotiations with holders of Company Claims/Interests (including any Restructuring Support Party), any other party in interest in the Chapter 11 Cases (including any official committee and the United States Trustee), or any other entity regarding an Alternative Transaction or an Alternative Transaction Proposal; provided, further, that if any Debtor receives an Alternative Transaction Proposal or an update thereto, then such Debtor shall, within one (1) business day of receiving such Alternative Transaction Proposal, provide the Ad Hoc Group Advisors with all documentation (with redactions as reasonably necessary) received in connection with such Alternative Transaction Proposal (or, if such Alternative Transaction Proposal was not made in writing, a reasonably detailed summary of such Alternative Transaction Proposal), including, as permitted, the identity of the person or group of persons involved and reasonable updates as to the status and progress of such Alternative Transaction Proposal, and such Debtor shall respond promptly to reasonable information requests and questions from the Ad Hoc Group Advisors relating to such Alternative Transaction Proposal; provided, further, that if the board of directors or board of managers, as applicable, of any Debtor determines, in the exercise of its fiduciary duties, to pursue an Alternative Transaction Proposal that is not acceptable to the Majority Consenting 2026 Noteholders, including by making any written or oral proposal or counterproposal (other than discussions contemplated by the foregoing sub-clause (d)(iv)) with respect thereto, the Debtors shall provide written notice (with email being sufficient) to counsel to the Ad Hoc Group within two (2) business days following such determination and prior to make any such proposal or counterproposal (an “Alternative Transaction Proposal Notice”), and the Required Consenting 2026 Noteholders (as defined herein) shall have the right to terminate this Agreement pursuant to the terms hereof upon receipt of such Alternative Transaction Proposal Notice; |

| (e) | promptly (but in any event within two (2) business days) provide written notice to counsel to the Ad Hoc Group of (i) the occurrence of any event of which the Debtors have actual knowledge, or believe is likely, which occurrence or failure would, or would be likely to cause (A) any condition precedent or covenant contained in this Agreement or in any Definitive Document not to occur or become impossible to satisfy, or (B) a material breach by any Debtor of any undertaking, commitment or covenant of such Debtor set forth in this Agreement or the existence of an inaccuracy in any material respect in a representation or warranty of any Debtor as of the RSA Effective Date that would trigger, including with the delivery of notice and/or the passage of time, a right hereunder to cause a Consenting 2026 Noteholder Termination Event, (ii) the receipt of any written notice from any governmental authority or third party alleging that the consent of such party is or may be required in connection with the transactions contemplated by the Restructuring, (iii) receipt of any written notice of any proceeding commenced or, to the actual knowledge of the Debtors, threatened against the Debtors relating to or involving or otherwise affecting in any material respect the transactions contemplated by this Agreement or the Restructuring, or (iv) a failure of the Debtors to comply in any material respect with a covenant or agreement to be complied with or by it hereunder or under any Definitive Document; |

| (f) | unless the Debtors have received prior written consent from the Majority Consenting 2026 Noteholders, operate the business of each of the Debtors in the ordinary course (other than changes in the operations resulting from or relating to the Restructuring or the filing of the Chapter 11 Cases) and consistent with past practice, the DIP Budget, and in a manner that is materially consistent with this Agreement and the business plan of the Debtors; |

| (g) | as reasonably requested with reasonable notice by the Majority Consenting 2026 Noteholders (which, in each case, may be through the Ad Hoc Group Advisors), (i) cause management and advisors of the Debtors to inform and/or confer with the Ad Hoc Group Advisors as to: (A) the status and progress of the Restructuring, including, without limitation, progress in relation to the negotiations of the Definitive Documentation, (B) the status of obtaining any necessary or desirable authorizations (including any consents) with respect to the Restructuring from each Restructuring Support Party, any competent judicial body, governmental authority, banking, taxation, supervisory, or regulatory body or any stock exchange and (C) operational and financial performance matters (including liquidity), collateral matters, contract negotiation and lease matters, and the general status of ongoing operations, (ii) shall provide the Ad Hoc Group Advisors with all information related to the Debtors, its properties and business, or any transaction; provided, however, that to the extent such diligence information is designated as professional eyes only, such diligence information shall be provided to the Ad Hoc Group Advisors, and the Debtors and their advisors shall act reasonably and in good faith to ensure that the maximal amount of such information that can be provided to the Ad Hoc Group pursuant to the terms of any non-disclosure agreements then in effect between Enviva and such Restructuring Support Parties is so provided (and the Debtors shall work in good faith to enter into or renew non-disclosure agreements with members of the Ad Hoc Group and/or the Ad Hoc Group Advisors as reasonably necessary or appropriate); and (iii) hold calls on a weekly basis (or with such other frequency as may be reasonably agreed) for the Chief Executive Officer of Enviva Inc. to provide updates to members of the Ad Hoc Group regarding the business operations and finances of the Debtors and the progress of the Chapter 11 Cases and the Restructuring, provided that any financial advisor and/or investment banker of the Debtors and the Ad Hoc Group may also participate in such update calls; |

| (h) | pay all fees and expenses in accordance with Section 15 of this Agreement as and when due; |

| (i) | not file or seek authority to file any motion, pleading, or Definitive Documentation with the Bankruptcy Court or any other court (including any modifications or amendments thereof) that, in whole or in part, is not consistent with this Agreement or the Plan; |

| (j) | comply with each Milestone; |

| (k) | not consummate or enter into a definitive agreement evidencing any merger, consolidation, disposition of material assets, acquisition of material assets, or similar transaction, pay any dividend, or incur any indebtedness for borrowed money, in each case outside the ordinary course of business, in each case other than: (i) the Restructuring or (ii) with the prior consent of the Majority Consenting 2026 Noteholders; |

| (l) | timely (i) pursue Bankruptcy Court approval and implementation of the MS Bond Settlement10 and (ii) negotiate, document and pursue Bankruptcy Court approval of a settlement with the Consenting Epes Green Bondholders providing for the release of cash from trust accounts in respect of the Epes Green Bonds on substantially similar terms to the MS Bond Settlement (inclusive of process milestones providing for such settlement to be prosecuted and implemented on the same timeline as the MS Bond Settlement, or such other timeline as has been agreed to by the Consenting Epes Green Bondholders) (the “Epes Bond Settlement”); provided that, in connection with the MS Bond Settlement, the Epes Bond Settlement and the other Definitive Documents, the amounts paid from the Debtors’ Estates to the advisors acting on behalf of trustees and/or holders of Green Bonds Claims (including, without limitation, Perella Weinberg Partners L.P. as financial advisor and Kramer Levin Naftalis & Frankel LLP as legal advisor) shall not at any time during and/or at emergence of the Chapter 11 Cases exceed the aggregate professional fees cap agreed as communicated by email among the Debtors and the Ad Hoc Group Advisors on March 12, 2024 (and the amounts paid may be less than such limits); |

| 10 | “MS Bond Settlement” means that certain settlement by and among the Debtors and certain holders of Bond Green Bonds Claims concerning the return of funds held by the trustee for the Bond Green Bonds to the holders of the Bond Green Bonds Claims, as set forth in that certain MS Bond term sheet, dated as of February 15, 2024, by and among the Debtors and certain holders of Bond Green Bonds Claims. |

| (m) | provide all consents within each Debtors’ power that are necessary or appropriate to elevate any participation interests in any Senior Secured Credit Facility Loans held by any Restructuring Support Party to record positions held by assignment; |

| (n) | not object to, delay, impede, or take any other action that is inconsistent with, or is intended to interfere with, consummation of the Restructuring or is barred by this Agreement; |

| (o) | negotiate in good faith upon reasonable request of the Ad Hoc Group any supplements or modifications to the Restructuring that (i) improve the tax efficiency of the Restructuring or are otherwise necessary to address any legal, financial, or structural impediment that may prevent the consummation of the Restructuring (in each case to the extent such modifications can be implemented without any material adverse effect on such Debtor or the Restructuring) and/or (ii) are intended to minimize go-forward costs for the reorganized Debtors with respect to any potential litigation cost exposure that may survive the consummation of the Restructuring; |

| (p) | except to the extent required by this Agreement or otherwise required to consummate the Restructuring or with the consent of the Ad Hoc Group, not take any action or inaction that would cause a change to the tax classification, for United States federal income tax purposes, of any Debtor; and |

| (q) | to the extent any legal or structural impediment arises that would prevent, hinder, or delay the consummation of the Restructuring, agrees to take all steps reasonably necessary and desirable, including to negotiate in good faith with respect to appropriate additional or alternative provisions, to address any such impediment, in each case, in a manner reasonably acceptable to the Majority Consenting 2026 Noteholders. |

For the avoidance of doubt, nothing in this Section 6 shall be construed to limit or affect in any way (y) any Restructuring Support Party’s rights under this Agreement, including upon the occurrence of any Termination Event, or (z) the Debtors’ ability to engage in marketing efforts, discussions, and/or negotiations with any party regarding exit debt financing consistent with the Term Sheet and the terms hereof.

Notwithstanding anything to the contrary herein, any board of directors, board of managers, director or officer of any Debtor and, in the case of any Debtor that is a wholly owned direct or indirect subsidiary of Enviva Inc., any manager or member of such Debtor (in its capacity as such, each a “Debtor Agent”) shall be permitted to take or refrain from taking any action to the extent such Debtor Agent determines, in good faith and based upon advice of outside legal counsel, that taking such action, or refraining from taking such action, as applicable, is reasonably required to comply with its fiduciary duties, and may take (or refrain from taking) such action; provided that this provision shall not limit (x) any other obligation herein to provide notice to any other Party or (y) any Party’s right to terminate this Agreement pursuant to the terms hereof, including, without limitation, as a result of any breach of this Agreement resulting from a determination of the type made in this paragraph.

7. Restructuring Support Party Termination Events

| (a) | Individual Restructuring Support Party Termination Events. Any Restructuring Support Party shall have the right, but not the obligation, upon written notice to the Debtors and counsel to the Consenting 2026 Noteholders, to terminate the obligations of such Restructuring Support Party under this Agreement upon the occurrence of any of the following events (each, an “Individual Restructuring Support Party Termination Events”), in which case this Agreement shall terminate solely with respect to such terminating Restructuring Support Party; provided that such right to terminate shall be deemed waived if not exercised by the applicable Restructuring Support Party within five (5) business days of such Restructuring Support Party becoming aware of the underlying facts or circumstances giving rise to such Individual Restructuring Support Party Termination Event: |