UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report

of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16

under the Securities Exchange Act of 1934

For the month of February 2024

Commission File Number 001-11444

| MAGNA INTERNATIONAL INC. |

| (Exact Name of Registrant as specified in its Charter) |

| 337 Magna Drive, Aurora, Ontario, Canada L4G 7K1 |

| (Address of principal executive office) |

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☐ Form 40-F ☒ Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

SIGNATURES

| MAGNA INTERNATIONAL INC. | ||||

| (Registrant) | ||||

| Date: | February 23, 2024 | |||

| By: | /s/ “Bassem Shakeel” | |||

| Bassem A. Shakeel, | ||||

| Vice-President, Associate General Counsel and Corporate Secretary | ||||

EXHIBITS

| Exhibit 99.3 | Consent of Deloitte LLP |

Exhibit 99.1

MAGNA INTERNATIONAL INC.

Management’s Discussion and Analysis of Results of Operations and Financial Position

Unless otherwise noted, all amounts in this Management’s Discussion and Analysis of Results of Operations and Financial Position [“MD&A”] are in U.S. dollars and all tabular amounts are in millions of U.S. dollars, except per share figures, which are in U.S. dollars. When we use the terms “we”, “us”, “our” or “Magna”, we are referring to Magna International Inc. and its subsidiaries and jointly controlled entities, unless the context otherwise requires.

This MD&A should be read in conjunction with the audited consolidated financial statements for the year ended December 31, 2023 included in our 2023 Annual Report to Shareholders.

This MD&A may contain statements that are forward looking. Refer to the “Forward-Looking Statements” section in this MD&A for a more detailed discussion of our use of forward-looking statements.

This MD&A has been prepared as at February 22, 2024.

HIGHLIGHTS

INDUSTRY PRODUCTION ENVIRONMENT

| • | Global light vehicle production increased 8% in 2023, including increases of 9%, 11%, and 8% in North America, Europe, and China, respectively. | |

| • | North American light vehicle production was negatively impacted by the UAW labour strikes at certain customers during the third and fourth quarters of 2023. |

SALES & EARNINGS

| • | Total sales increased 13% to a record $42.8 billion, primarily reflecting higher global vehicle production, the launch of new programs, and the acquisition of Veoneer Active Safety [“Veoneer AS”], partially offset by the negative impact of lost vehicle production as a result of the UAW labour strikes at certain customers during the third and fourth quarters of 2023. |

| • | Diluted earnings per share were $4.23 and adjusted diluted earnings per share(1) were $5.49 in 2023. Adjusted diluted earnings per share increased $1.25 compared to 2022 primarily reflecting earnings on higher sales, including higher margins due to the impact of operational excellence and cost initiatives, and productivity and efficiency improvements. These factors were partially offset by higher launch, engineering, and other costs associated with new assembly business, the negative impact of the UAW labour strikes, the net unfavourable impact of commercial items, lower amortization of the initial value of public company securities, higher launch costs associated with new manufacturing business, and the impact of acquisitions, net of divestitures. |

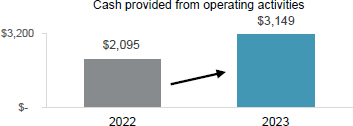

CASH & INVESTMENTS

| • | Cash generated from operating activities was $3.1 billion, compared to $2.1 billion in 2022, largely reflecting an increase in net income and generation of cash from operating assets and liabilities in 2023 compared to an investment in operating assets and liabilities in 2022. |

| • | We continued to invest in our business, including: |

| • | $2.5 billion for fixed assets; |

| • | $562 million in investment and other asset spending; and |

| • | $1.5 billion for acquisitions and business combinations, and public and private equity investments, including the acquisition of Veoneer AS. |

| • | We paid dividends of $522 million in 2023. |

| • | Our Board of Directors increased our quarterly dividend to $0.475 per share, our 14th consecutive year of dividend increases. |

| • | We raised $2 billion in debt, comprised of Senior Notes and $400 million in a delayed-draw Term Loan, fund the acquisition of Veoneer AS, invest in megatrend areas, and refinance €550 million in Senior Notes that came due in 2023. |

STRATEGIC UPDATES

| • | Active Safety – we further advanced our position in Active Safety, including: | |

| • | Completing the acquisition of Veoneer AS, broadening our active safety portfolio with complementary products, customers, geographies, engineering and software resources; | |

| • | Launching our innovative, Gen5 front camera module system on a high-volume program for a European-based global OEM, and winning further front camera module volume on the program for an additional region. | |

| • | Electrification – we continued to strengthen our business in electrification, including through: | |

| • | Winning two additional integrated e-drive programs for global OEMs, one based in North America and one in Europe; | |

| • | Launching primary and secondary e-drives on a battery electric vehicle program for a new customer; | |

| • | Launching a first-to-market modular eDecoupling unit to support multiple battery electric vehicle programs for | |

| a German premium OEM; | ||

| • | Winning significant new awards for battery enclosures on multiple OEM programs. | |

| • | Sustainability – we committed to sustainability and environmental stewardship by submitting net-zero emission targets for validation by the Science Based Targets initiative, with a goal to achieve this target by 2050, and meet our near-term Scope 1, 2 and 3 targets by 2030. | |

Magna International Inc. Annual Report 2023

OVERVIEW

OUR BUSINESS(2)

Magna is more than one of the world’s largest suppliers in the automotive space. We are a mobility technology company built to innovate, with a global, entrepreneurial-minded team of over 179,000(3) employees across 342 manufacturing operations and 104 product development, engineering and sales centres spanning 28 countries. With 65+ years of expertise, our ecosystem of interconnected products combined with our complete vehicle expertise uniquely positions us to advance mobility in an expanded transportation landscape. For further information about Magna (NYSE:MGA; TSX:MG), please visit www.magna.com or follow us on social.

1 Adjusted diluted earnings per share is a Non-GAAP financial measure. Refer to the section “Use of Non-GAAP Measures”.

2 Manufacturing operations, product development, engineering and sales centres include certain operations accounted for under the equity method.

3 Number of employees includes over 166,000 employees at our wholly owned or controlled entities and over 13,000 employees at operations accounted for under the equity method.

FORWARD-LOOKING STATEMENTS

Certain statements in this MD&A may constitute “forward-looking information” or “forward-looking statements” (collectively, “forward-looking statements”). Any such forward-looking statements are intended to provide information about management’s current expectations and plans and may not be appropriate for other purposes. Forward-looking statements may include financial and other projections, as well as statements regarding our future plans, strategic objectives or economic performance, or the assumptions underlying any of the foregoing, and other statements that are not recitations of historical fact. We use words such as “may”, “would”, “could”, “should”, “will”, “likely”, “expect”, “anticipate”, “believe”, “intend”, “plan”, “aim”, “forecast”, “outlook”, “project”, “estimate”, “target” and similar expressions suggesting future outcomes or events to identify forward-looking statements.

Forward-looking statements in this document include, but are not limited to, statements relating to achievement of our near term emissions reductions target and 2050 net zero target.

Forward-looking statements are based on information currently available to us and are based on assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances. While we believe we have a reasonable basis for making any such forward-looking statements, they are not a guarantee of future performance or outcomes. Whether actual results and developments conform to our expectations and predictions is subject to a number of risks, assumptions, and uncertainties, many of which are beyond our control, and the effects of which can be difficult to predict, including the risk factors which are described later in this MD&A.

INDUSTRY TRENDS

Our operating results are primarily dependent on the levels of North American, European, and Chinese car and light truck production by our customers. While we supply systems and components to every major original equipment manufacturer [“OEM”], we do not supply systems and components for every vehicle, nor is the value of our content consistent from one vehicle to the next. As a result, customer and program mix relative to market trends, as well as the value of our content on specific vehicle production programs, are also important drivers of our results.

Ordinarily, OEM production volumes are aligned with vehicle sales levels and thus affected by changes in such levels. Aside from vehicle sales levels, production volumes are typically impacted by a range of factors, including: general economic and political conditions; labour disruptions; free trade arrangements; tariffs; relative currency values; commodities prices; supply chains and infrastructure; availability and relative cost of skilled labour; regulatory considerations, including those related to environmental emissions and safety standards; and other factors.

Overall vehicle sales levels are significantly affected by changes in consumer confidence levels, which may in turn be impacted by consumer perceptions and general trends related to the job, housing, and stock markets, as well as other macroeconomic and political factors. Other factors which typically impact vehicle sales levels and thus production volumes include: vehicle affordability; interest rates and/or availability of credit; fuel and energy prices; relative currency values; regulatory restrictions on use of vehicles in certain megacities; government subsidies to consumers for the purchase of low- and zero-emission vehicles; and other factors.

While the foregoing economic, political, and other factors are part of the general context in which the global automotive industry operates, there were a number of significant industry trends that impacted us during 2023, including:

| • | elevated inflation in all markets in which we operate; |

| • | price increases and surcharges from sub-suppliers impacted by inflationary pressures; |

| • | targeted labour strikes by UAW members against certain Ford, General Motors and Stellantis facilities in the U.S.; |

| • | supply chain disruptions, including continued impact from the global shortage of semiconductor chips that has materially affected global automotive production volumes since 2020; and |

| • | operational inefficiencies as a result of our production lines being stopped/restarted unexpectedly. |

We continue to implement a business strategy which is rooted in our best assessment as to the rate and direction of change in the automotive industry, including with respect to trends related to vehicle electrification and advanced driver assistance systems, as well as future mobility business models. Our short and medium-term operational success, as well as our ability to create long-term value through our business strategy, are subject to a number of risks and uncertainties which are discussed later in this MD&A.

Magna International Inc. Annual Report 2023

USE OF NON-GAAP FINANCIAL MEASURES

In addition to results presented in accordance with accounting principles generally accepted in the United States of America [“U.S. GAAP”], this report includes the use of Adjusted earnings before interest and taxes [“Adjusted EBIT”], Adjusted EBIT as a percentage of sales, Adjusted diluted earnings per share, and Adjusted Return on Invested Capital [collectively, the “Non-GAAP Measures”]. We believe these Non-GAAP financial measures provide additional information that is useful to investors in understanding our underlying performance and trends through the same financial measures employed by our management. Readers should be aware that Non-GAAP Measures have no standardized meaning under U.S. GAAP and accordingly may not be comparable to the calculation of similar measures by other companies. We believe that Adjusted EBIT, Adjusted EBIT as a percentage of sales, Adjusted diluted earnings per share and Adjusted Return on Invested Capital provide useful information to our investors for measuring our operational performance as they exclude certain items that are not reflective of ongoing operating profit and facilitate a comparison with prior periods. The presentation of any Non-GAAP Measures should not be considered in isolation or as a substitute for our related financial results prepared in accordance with U.S. GAAP. Non-GAAP financial measures are presented together with the most directly comparable U.S. GAAP financial measure, and a reconciliation to the most directly comparable U.S. GAAP financial measure, can be found in the “Non-GAAP Financial Measures Reconciliation” section of this MD&A.

During 2023, we revised our calculations of Adjusted EBIT, Adjusted diluted earnings per share and Adjusted Return on Invested Capital to exclude the amortization of acquired intangible assets. The historical presentation of these Non-GAAP measures within this MD&A has also been updated to reflect the revised calculations. Refer to the “Non-GAAP Financial Measures Reconciliation” section of this MD&A for further information.

RESULTS OF OPERATIONS

AVERAGE FOREIGN EXCHANGE

| 2023 | 2022 | Change | ||||||||||

| 1 Canadian dollar equals U.S. dollars | 0.742 | 0.769 | -4 | % | ||||||||

| 1 euro equals U.S. dollars | 1.082 | 1.053 | +3 | % | ||||||||

| 1 Chinese renminbi equals U.S. dollars | 0.141 | 0.149 | -5 | % | ||||||||

The preceding table reflects the average foreign exchange rates between the most common currencies in which we conduct business and our U.S. dollar reporting currency.

The results of operations for which the functional currency is not the U.S. dollar are translated into U.S. dollars using the average exchange rates for the relevant period. Throughout this MD&A, reference is made to the impact of translation of foreign operations on reported U.S. dollar amounts where relevant.

Our results can also be affected by the impact of movements in exchange rates on foreign currency transactions (such as raw material purchases or sales denominated in foreign currencies). However, as a result of hedging programs employed by us, foreign currency transactions in the current period have not been fully impacted by movements in exchange rates. We record foreign currency transactions at the hedged rate where applicable.

Finally, foreign exchange gains and losses on revaluation and/or settlement of monetary items denominated in a currency other than an operation’s functional currency impact reported results. These gains and losses are recorded in selling, general and administrative expense.

LIGHT VEHICLE PRODUCTION VOLUMES

Our operating results are mostly dependent on light vehicle production in the regions reflected in the table below:

Light Vehicle Production Volumes (thousands of units)

| 2023 | 2022 | Change | ||||||||||

| North America | 15,589 | 14,280 | +9 | % | ||||||||

| Europe | 17,481 | 15,802 | +11 | % | ||||||||

| China | 28,581 | 26,363 | +8 | % | ||||||||

| Other | 27,577 | 26,107 | +6 | % | ||||||||

| Global | 89,228 | 82,552 | +8 | % | ||||||||

Global light vehicle production increased 8% in 2023, largely reflecting the rebalancing of supply chains in 2023 compared to the significant industry production disruptions during 2022 caused by global semiconductor chip shortages.

RESULTS OF OPERATIONS – FOR THE YEAR ENDED DECEMBER 31, 2023

SALES

Sales increased 13% or $4.96 billion to $42.80 billion for 2023 compared to $37.84 billion for 2022 primarily due to:

| • | the launch of new programs during or subsequent to 2022; |

| • | higher global light vehicle production; |

| • | acquisitions, net of divestitures, subsequent to 2022, which increased sales by $814 million; and |

| • | customer price increases to recover certain higher production input costs. |

These factors were partially offset by:

| • | the negative impact of lost vehicle production as a result of the UAW labour strikes at certain customers during 2023, which decreased sales by approximately $325 million; |

| • | the net weakening of foreign currencies against the U.S. dollar, which decreased reported U.S. dollar sales by $91 million; and |

| • | net customer price concessions subsequent to 2022. |

COST OF GOODS SOLD

| 2023 | 2022 | Change | ||||||||||

| Material | $ | 26,309 | $ | 23,388 | $ | 2,921 | ||||||

| Direct labour | 3,164 | 2,791 | 373 | |||||||||

| Overhead | 7,712 | 7,009 | 703 | |||||||||

| Cost of goods sold | $ | 37,185 | $ | 33,188 | $ | 3,997 | ||||||

Cost of goods sold increased $4.00 billion to $37.19 billion for 2023 compared to $33.19 billion for 2022, primarily due to:

| • | higher material, direct labour and overhead associated with higher sales; |

| • | acquisitions, net of divestitures, subsequent to 2022; |

| • | higher launch, engineering and other costs associated with new assembly business; |

| • | commercial items in 2023 and 2022, which had a net unfavourable impact on a year over year basis; |

| • | higher pre-operating costs incurred at new facilities; and |

| • | higher net production input costs, including for labour, partially offset by lower prices for energy, certain commodities and freight. |

These factors were partially offset by:

| • | productivity and efficiency improvements, including lower costs at certain previously underperforming facilities; |

| • | the net weakening of foreign currencies against the U.S. dollar, which decreased reported U.S. dollar costs of goods sold by $44 million; and |

| • | the impact of operational excellence and cost initiatives. |

DEPRECIATION

Depreciation increased $63 million to $1.44 billion for 2023 compared to $1.37 billion for 2022 primarily due to increased capital deployed at new and existing facilities to support the launch of programs, and acquisitions, net of divestitures, subsequent to 2022, partially offset by the end of production of certain programs.

AMORTIZATION OF ACQUIRED INTANGIBLE ASSETS

Amortization of acquired intangible assets increased $42 million to $88 million for 2023 compared to $46 million for 2022 primarily due to the acquisition of Veoneer AS during the second quarter of 2023.

Magna International Inc. Annual Report 2023

SELLING, GENERAL AND ADMINISTRATIVE [“SG&A”]

SG&A expense increased $390 million to $2.05 billion for 2023 compared to $1.66 billion for 2022, primarily as a result of:

| • | higher labour and benefit costs; |

| • | commercial items in 2023 and 2022, which had a net unfavourable impact on a year over year basis; |

| • | acquisitions, net of divestitures, subsequent to 2022; |

| • | higher incentive compensation; |

| • | higher investments in research, development and new mobility; |

| • | higher restructuring costs; |

| • | higher costs to accelerate our operational excellence initiatives; and |

| • | higher pre-operating costs incurred at new facilities. |

These factors were partially offset by lower provisions against certain accounts receivable and other balances.

INTEREST EXPENSE, NET

During 2023, we recorded net interest expense of $156 million compared to $81 million for 2022. The $75 million increase was primarily a result of interest expense on the $1.6 billion of Senior Notes issued during the first quarter of 2023, interest expense on the Term Loan entered into during the first quarter of 2023, interest expense on higher short-term borrowings and higher interest rates. These factors we partially offset by higher interest income earned on cash and investments due to higher interest rates.

EQUITY INCOME

Equity income increased $23 million to $112 million for 2023 compared to $89 million for 2022, primarily as a result of earnings on higher sales at certain equity-accounted entities, and acquisitions subsequent to 2022, partially offset by higher launch costs, and higher production input costs, net of customer recoveries.

OTHER EXPENSE, NET

| 2023 | 2022 | |||||||

| Investments (1) | $ | 201 | $ | 221 | ||||

| Restructuring (2) | 148 | 22 | ||||||

| Veoneer AS transaction costs (3) | 23 | — | ||||||

| Impairments and loss on sale of operations in Russia (4) | 16 | 376 | ||||||

| Loss on sale of business (5) | — | 58 | ||||||

| Impairments (6) | — | 26 | ||||||

| Other expense, net | $ | 388 | $ | 703 | ||||

|

(1) |

Investments |

| 2023 | 2022 | |||||||

| Revaluation of public company warrants | $ | 110 | $ | 173 | ||||

| Non-cash impairment charges (i) | 90 | — | ||||||

| Revaluation of public and private equity investments | 1 | 49 | ||||||

| Net gain on sale of public equity investments | — | (1 | ) | |||||

| Other expense, net | 201 | 221 | ||||||

| Tax effect | (28 | ) | (53 | ) | ||||

| Net loss attributable to Magna | $ | 173 | $ | 168 | ||||

| (i) | The non-cash impairment charges relate to impairments of private equity investments and related long-term receivables within Other assets. |

| (2) | Restructuring |

During 2023, we recorded restructuring charges of $117 million [$97 million after tax] in our Power & Vision segment, and $31 million [$27 million after tax] in our Body Exteriors & Structures segment, respectively.

For the year ended December 31, 2022, we recorded restructuring charges of $22 million [$22 million after tax] in our Power & Vision segment.

| (3) | Veoneer AS transaction costs |

During 2023, we incurred $23 million [$22 million after tax] of transaction costs relating to our acquisition of Veoneer AS. Refer to Note 7, “Business Combinations”, to the consolidated financial statements included in this Report.

| (4) | Impairments and loss on sale of operations in Russia |

During 2023, we completed the sale of all of our investments in Russia which resulted in a loss of $16 million [$16 million after tax] including a net cash outflow of $23 million.

During 2022, we recorded a $376 million [$361 million after tax] impairment charge related to our investment in Russia as a result of the expected lack of future cashflows and the uncertainties connected with the Russian economy. This included net asset impairments of $173 million and a $203 million reserve against the related foreign currency translation losses that were included in accumulated other comprehensive loss. The net asset impairments consisted of $163 million and $10 million in our Body Exteriors & Structures and Seating Systems segments, respectively.

| (5) | Loss on sale of business |

During 2022, we entered into an agreement to sell a European Power & Vision operation. Under the terms of the arrangement, we were contractually obligated to provide the buyer with up to $42 million of funding, resulting in a loss of $58 million [$57 million after tax]. During the first quarter of 2023, we completed the sales of this operation which resulted in a net cash outflow of $25 million.

| (6) | Impairments |

During 2022, we recorded impairment charges of $22 million [$21 million after tax] in our Body Exteriors & Structures segment and $4 million [$3 million after tax] in our Power & Vision segment, respectively.

INCOME FROM OPERATIONS BEFORE INCOME TAXES

Income from operations before income taxes was $1.61 billion for 2023 compared to $878 million for 2022. The $728 million increase was a result of the following changes, each as discussed above:

| 2023 | 2022 | Change | ||||||||||

| Sales | $ | 42,797 | $ | 37,840 | $ | 4,957 | ||||||

| Costs and expenses | ||||||||||||

| Cost of goods sold | 37,185 | 33,188 | 3,997 | |||||||||

| Depreciation | 1,436 | 1,373 | 63 | |||||||||

| Amortization of acquired intangible assets | 88 | 46 | 42 | |||||||||

| Selling, general & administrative | 2,050 | 1,660 | 390 | |||||||||

| Interest expense, net | 156 | 81 | 75 | |||||||||

| Equity income | (112 | ) | (89 | ) | (23 | ) | ||||||

| Other expense, net | 388 | 703 | (315 | ) | ||||||||

| Income from operations before income taxes | $ | 1,606 | $ | 878 | $ | 728 | ||||||

INCOME TAXES

| 2023 | 2022 | |||||||||||||||

| Income taxes as reported | $ | 320 | 19.9 | % | $ | 237 | 27.0 | % | ||||||||

| Tax effect on Other expense, net and Amortization of acquired intangible assets | 70 | (1.2 | ) | 79 | (7.6 | ) | ||||||||||

| Adjustments to Deferred Tax Valuation Allowances | 47 | 2.3 | 29 | 1.8 | ||||||||||||

| $ | 437 | 21.0 | % | $ | 345 | 21.2 | % | |||||||||

We released valuation allowances against certain deferred tax assets in South America and North America during 2023 and in Europe during 2022 [“Adjustments to Deferred Tax Valuation Allowances”].

Excluding the tax effect on Other expense, net and Amortization of acquired intangible assets, as well as the Adjustments to Deferred Tax Valuation Allowances our effective income tax rate decreased to 21.0% for 2023 compared to 21.2% for 2022 primarily due to lower losses not benefitted in Europe and higher non-taxable foreign exchange adjustments recognized for U.S. GAAP purposes. These factors were partially offset by lower favourable changes in our reserves for uncertain tax positions and a change in mix of earnings.

Magna International Inc. Annual Report 2023

INCOME ATTRIBUTABLE TO NON-CONTROLLING INTERESTS

Income attributable to non-controlling interests was $73 million for 2023 compared to $49 million for 2022. This $24 million increase was primarily due to higher net income at our non-wholly owned operations in China.

NET INCOME ATTRIBUTABLE TO MAGNA INTERNATIONAL INC.

Net income attributable to Magna International Inc. was $1.213 billion for 2023 compared to $592 million for 2022. This $621 million increase was as a result of an increase in income from operations before income taxes of $728 million partially offset by increases in income taxes and income attributable to non-controlling interests of $83 million and $24 million, respectively.

EARNINGS PER SHARE

| 2023 | 2022 | % Change | ||||||||||

| Earnings per Common Share | ||||||||||||

| Basic | $ | 4.24 | $ | 2.04 | + 108 | % | ||||||

| Diluted | $ | 4.23 | $ | 2.03 | + 108 | % | ||||||

| Weighted average number of Common Shares outstanding (millions) | ||||||||||||

| Basic | 286.2 | 290.4 | - 1 | % | ||||||||

| Diluted | 286.6 | 291.2 | - 2 | % | ||||||||

| Adjusted diluted earnings per share | $ | 5.49 | $ | 4.24 | + 29 | % | ||||||

Diluted earnings per share was $4.23 for 2023 compared to $2.03 for 2022. The $2.20 increase was substantially a result of higher net income attributable to Magna International Inc., as discussed above, and a decrease in the weighted average number of diluted shares outstanding during 2023. The decrease in the weighted average number of diluted shares outstanding was primarily due to the purchase and cancellation of Common Shares, during or subsequent to 2022, pursuant to our normal course issuer bids.

Other expense, net, and the Amortization of acquired intangible assets, each after tax, and Adjustments to Deferred Tax Valuation Allowances negatively impacted diluted earnings per share by $1.26 in 2023 and $2.21 in 2022, respectively, as discussed. Adjusted diluted earnings per share, as reconciled in the "Non-GAAP Financial Measures Reconciliation" section, was $5.49 for 2023 compared to $4.24 for 2022, an increase of $1.25.

NON-GAAP PERFORMANCE MEASURES - FOR THE YEAR ENDED DECEMBER 31, 2023

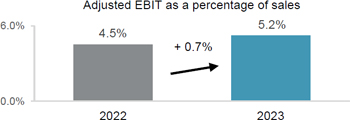

ADJUSTED EBIT AS A PERCENTAGE OF SALES

The table below shows the change in Magna's Sales and Adjusted EBIT by segment and the impact each segment's changes have on Magna's Adjusted EBIT as a percentage of sales for 2023 compared to 2022:

| Sales | Adjusted EBIT |

Adjusted EBIT as a percentage of sales |

||||||||||

| 2022 | $ | 37,840 | $ | 1,708 | 4.5 | % | ||||||

| Increase (decrease) related to: | ||||||||||||

| Body Exteriors & Structures | 1,507 | 452 | + 0.9 | % | ||||||||

| Power & Vision | 2,444 | 166 | + 0.1 | % | ||||||||

| Seating Systems | 778 | 114 | + 0.2 | % | ||||||||

| Complete Vehicles | 317 | (111 | ) | - 0.3 | % | |||||||

| Corporate and Other | (89 | ) | (91 | ) | - 0.2 | % | ||||||

| 2023 | $ | 42,797 | $ | 2,238 | 5.2 | % | ||||||

Adjusted EBIT as a percentage of sales increased to 5.2% for 2023 compared to 4.5% for 2022 primarily due to:

| • | earnings on higher sales including higher margins as a result of the impact of operational excellence and cost initiatives; |

| • | productivity and efficiency improvements, including lower costs at certain previously underperforming facilities; and |

| • | lower provisions against certain accounts receivable and other balances. |

These factors were partially offset by:

| • | higher launch, engineering and other costs associated with new assembly business; |

| • | acquisitions, net of divestitures, subsequent to 2022; |

| • | commercial items in 2023 and 2022, which had a net unfavourable impact on a year over year basis; |

| • | the negative impact of the UAW labour strikes during the third and fourth quarters of 2023; |

| • | higher launch costs associated with new manufacturing business; |

| • | lower amortization of the initial value of public company securities; |

| • | higher pre-operating costs incurred at new facilities; |

| • | lower scrap steel and aluminum recoveries; and |

| • | higher investments in research, development and new mobility. |

Magna International Inc. Annual Report 2023

ADJUSTED RETURN ON INVESTED CAPITAL

Adjusted Return on Invested Capital increased to 10.0% for 2023 compared to 8.5% for 2022 as a result of an increase in Adjusted After-tax operating profits partially offset by higher Average Invested Capital.

Average Invested Capital increased $1.85 billion to $17.77 billion for 2023 compared to $15.92 billion for 2022, primarily due to:

| • | the acquisition of Veoneer AS during 2023; |

| • | average investment in fixed assets in excess of our average depreciation expense on fixed assets; and |

| • | an increase in average operating assets and liabilities. |

These factors were partially offset by:

| • | the impairment of our Russian assets recorded during 2022; |

| • | lower net investments in public and private equity companies and public company warrants; and |

| • | the net weakening of foreign currencies against the U.S. dollar. |

SEGMENT ANALYSIS

We are a global automotive supplier that has complete vehicle engineering and contract manufacturing expertise, as well as product capabilities which include body, chassis, exterior, seating, powertrain, active driver assistance, electronics, mechatronics, mirrors, lighting and roof systems. We also have electronic and software capabilities across many of these areas.

Our reporting segments are: Body Exteriors & Structures; Power & Vision; Seating Systems; and Complete Vehicles.

| Sales | Adjusted EBIT | |||||||||||||||||||||||

| 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||

| Body Exteriors & Structures | $ | 17,511 | $ | 16,004 | $ | 1,507 | $ | 1,304 | $ | 852 | $ | 452 | ||||||||||||

| Power & Vision | 14,305 | 11,861 | 2,444 | 668 | 502 | 166 | ||||||||||||||||||

| Seating Systems | 6,047 | 5,269 | 778 | 218 | 104 | 114 | ||||||||||||||||||

| Complete Vehicles | 5,538 | 5,221 | 317 | 124 | 235 | (111 | ) | |||||||||||||||||

| Corporate and Other | (604 | ) | (515 | ) | (89 | ) | (76 | ) | 15 | (91 | ) | |||||||||||||

| Total reportable segments | $ | 42,797 | $ | 37,840 | $ | 4,957 | $ | 2,238 | $ | 1,708 | $ | 530 | ||||||||||||

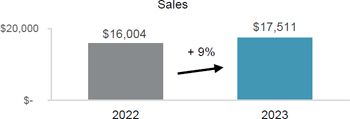

BODY EXTERIORS & STRUCTURES

| 2023 | 2022 | Change | ||||||||||||||

| Sales | $ | 17,511 | $ | 16,004 | $ | 1,507 | +9 | % | ||||||||

| Adjusted EBIT | $ | 1,304 | $ | 852 | $ | 452 | +53 | % | ||||||||

| Adjusted EBIT as a percentage of sales | 7.4 | % | 5.3 | % | +2.1 | % | ||||||||||

Sales – Body Exteriors & Structures

Sales increased 9% or $1.51 billion to $17.51 billion for 2023 compared to $16.00 billion for 2022, primarily due to:

| • | the launch of programs during or subsequent to 2022, including the: |

| • | Honda CR-V; |

| • | Ford F-Series Super Duty; |

| • | BMW X1 and |

| • | Rivian R1S & R1T; |

| • | higher global light vehicle production; and |

| • | customer price increases to recover certain higher production input costs. |

These factors were partially offset by:

| • | the negative impact of lost vehicle production as a result of the UAW labour strikes at certain customers during 2023, which decreased sales by approximately $200 million; |

| • | the net weakening of foreign currencies against the U.S. dollar, which decreased reported U.S. dollar sales by $99 million; |

| • | lower sales as a result of the substantial idling of our Russian facilities; and |

| • | net customer price concessions subsequent to 2022. |

Magna International Inc. Annual Report 2023

Adjusted EBIT and Adjusted EBIT as a percentage of sales – Body Exteriors & Structures

Adjusted EBIT increased $452 million to $1,304 million for 2023 compared to $852 million for 2022 and Adjusted EBIT as a percentage of sales increased to 7.4% from 5.3%. These increases were primarily due to:

| • | earnings on higher sales including higher margins due to the impact of operational excellence and cost initiatives; |

| • | productivity and efficiency improvements, including lower costs at certain previously underperforming facilities; |

| • | commercial items in 2023 and 2022, which had a net favourable impact on a year over year basis; and |

| • | lower provisions against certain accounts receivable and other balances. |

These factors were partially offset by:

| • | the negative impact of the UAW labour strikes during the third and fourth quarters of 2023; |

| • | higher restructuring costs; |

| • | higher launch costs; |

| • | higher pre-operating costs incurred at new facilities; |

| • | lower scrap steel and aluminum recoveries; and |

| • | the net weakening of foreign currencies against the U.S. dollar, which had a $19 million unfavourable impact on reported U.S. dollar Adjusted EBIT. |

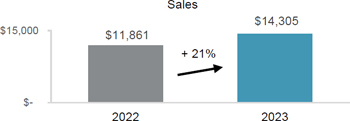

POWER & VISION

| 2023 | 2022 | Change | ||||||||||||||

| Sales | $ | 14,305 | $ | 11,861 | $ | 2,444 | + 21 | % | ||||||||

| Adjusted EBIT | $ | 668 | $ | 502 | $ | 166 | + 33 | % | ||||||||

| Adjusted EBIT as a percentage of sales | 4.7 | % | 4.2 | % | + 0.5 | % | ||||||||||

Sales – Power & Vision

Sales increased 21% or $2.44 billion to $14.31 billion for 2023 compared to $11.86 billion for 2022, primarily due to:

| • | the launch of programs during or subsequent to 2022, including the: |

| • | BMW X1 & iX1; |

| • | Chery Tiggo 9; |

| • | Chery Arrizo 8; and |

| • | Fisker Ocean; |

| • | acquisitions, net of divestitures, subsequent to 2022, which increased sales by $820 million; |

| • | higher global light vehicle production; and |

| • | customer price increases to recover certain higher production input costs. |

These factors were partially offset by:

| • | the negative impact of lost vehicle production as a result of the UAW labour strikes at certain customers during 2023, which decreased sales by approximately $80 million; |

| • | the net weakening of foreign currencies against the U.S. dollar, which decreased reported U.S. dollar sales by $47 million; and |

| • | net customer price concessions subsequent to 2022. |

Adjusted EBIT and Adjusted EBIT as a percentage of sales – Power & Vision

Adjusted EBIT increased $166 million to $668 million for 2023 compared to $502 million for 2022 and Adjusted EBIT as a percentage of sales increased to 4.7% from 4.2%. These increases were primarily due to:

| • | earnings on higher sales including higher margins due to the impact of operational excellence and cost initiatives; |

| • | customer recoveries net of higher production input costs, including for certain commodities, energy, and freight, partially offset by higher prices for labour; |

| • | cost savings and efficiencies realized, including as a result of restructuring actions taken; |

| • | higher equity income; and |

| • | lower net warranty costs of $15 million. |

These factors were partially offset by:

| • | commercial items in 2023 and 2022, which had a net unfavourable impact on a year over year basis; |

| • | acquisitions, net of divestitures, subsequent to 2022; |

| • | the negative impact of the UAW labour strikes during the third and fourth quarters of 2023; and |

| • | the net weakening of foreign currencies against the U.S. dollar, which had a $20 million unfavourable impact on reported U.S. dollar Adjusted EBIT. |

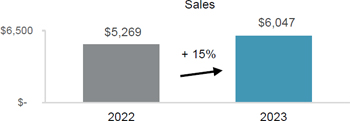

SEATING SYSTEMS

| 2023 | 2022 | Change | ||||||||||||||

| Sales | $ | 6,047 | $ | 5,269 | $ | 778 | + 15 | % | ||||||||

| Adjusted EBIT | $ | 218 | $ | 104 | $ | 114 | + 110 | % | ||||||||

| Adjusted EBIT as a percentage of sales | 3.6 | % | 2.0 | % | + 1.6 | % | ||||||||||

Magna International Inc. Annual Report 2023

Sales – Seating Systems

Sales increased 15% or $778 million to $6.05 billion for 2023 compared to $5.27 billion for 2022, primarily due to:

| • | the launch of programs during or subsequent to 2022, including the: |

| • | Nissan Frontier; |

| • | Geely Boyue L; |

| • | Changan Oshan Z6; and |

| • | BMW XM; |

| • | higher global light vehicle production; and |

| • | customer price increases to recover certain higher production input costs. |

These factors were partially offset by:

| • | the net weakening of foreign currencies against the U.S. dollar, which decreased reported U.S. dollar sales by $50 million; |

| • | the negative impact of lost vehicle production as a result of the UAW labour strikes at certain customers during 2023, which decreased sales by approximately $45 million; and |

| • | net customer price concessions subsequent to 2022. |

Adjusted EBIT and Adjusted EBIT as a percentage of sales – Seating Systems

Adjusted EBIT increased $114 million to $218 million for 2023 compared to $104 million for 2022 and Adjusted EBIT as a percentage of sales increased to 3.6% from 2.0%. These increases were primarily due to:

| • | earnings on higher sales including higher margins due to the impact of operational excellence and cost initiatives; |

| • | productivity and efficiency improvements, including lower costs at certain previously underperforming facilities; and |

| • | commercial items in 2023 and 2022, which had a net favourable impact on a year over year basis. |

These factors were partially offset by:

| • | higher production input costs net of customer recoveries, including for labour and certain commodities; |

| • | higher launch costs; |

| • | the negative impact of the UAW labour strikes during the third and fourth quarters of 2023; |

| • | higher net foreign exchange losses, primarily due to the weakening of the Argentine peso against the U.S. dollar; |

| • | lower equity income; and |

| • | the net weakening of foreign currencies against the U.S. dollar, which had a $5 million unfavourable impact on reported U.S. dollar Adjusted EBIT. |

COMPLETE VEHICLES

| 2023 | 2022 | Change | ||||||||||||||

| Complete Vehicle Assembly Volumes (thousands of units)(i) | 105.1 | 112.2 | (7.1 | ) | - 6 | % | ||||||||||

| Sales | $ | 5,538 | $ | 5,221 | $ | 317 | + 6 | % | ||||||||

| Adjusted EBIT | $ | 124 | $ | 235 | $ | (111 | ) | - 47 | % | |||||||

| Adjusted EBIT as a percentage of sales | 2.2 | % | 4.5 | % | - 2.3 | % | ||||||||||

| (i) | Vehicles produced at our Complete Vehicle operations are included in Europe Light Vehicle Production volumes. |

Sales – Complete Vehicles

Sales increased 6% or $317 million to $5.54 billion for 2023 compared to $5.22 billion for 2022. The increase in sales was primarily due to favourable program mix and a $109 million increase in reported U.S. dollar sales as a result of the strengthening of the euro against the U.S. dollar partially offset by lower assembly volumes, including the end of production of the BMW 5-Series.

Adjusted EBIT and Adjusted EBIT as a percentage of sales – Complete Vehicles

Adjusted EBIT decreased $111 million to $124 million for 2023 compared to $235 million for 2022 and Adjusted EBIT as a percentage of sales decreased to 2.2% from 4.5%. These decreases were primarily due to:

| • | higher launch, engineering and other costs associated with new assembly business; |

| • | commercial items in 2023 and 2022, which had a net unfavourable impact on a year over year basis; and |

| • | lower earnings on lower assembly volumes, net of contractual fixed cost recoveries on certain programs. |

These factors were partially offset by higher earnings due to favourable program mix.

CORPORATE AND OTHER

Adjusted EBIT was a loss of $76 million for 2023 compared to income of $15 million for 2022. The $91 million decrease was primarily the result of:

| • | lower amortization of the initial value of public company securities; |

| • | higher incentive and stock-based compensation; |

| • | higher investments in research, development and new mobility; |

| • | higher labour and benefit costs; and |

| • | higher costs to accelerate our operational excellence initiatives. |

These factors were partially offset by an increase in fees received from our divisions and net transactional foreign exchange gains in 2023 compared to net transactional foreign exchange losses in 2022.

Magna International Inc. Annual Report 2023

FINANCIAL CONDITION, LIQUIDITY AND CAPITAL RESOURCES

OPERATING ACTIVITIES

| 2023 | 2022 | Change | ||||||||||

| Net income | $ | 1,286 | $ | 641 | ||||||||

| Items not involving current cash flows | 1,642 | 1,776 | ||||||||||

| 2,928 | 2,417 | $ | 511 | |||||||||

| Changes in operating assets and liabilities | 221 | (322 | ) | 543 | ||||||||

| Cash provided from operating activities | $ | 3,149 | $ | 2,095 | $ | 1,054 | ||||||

Cash provided from operating activities

Comparing 2023 to 2022, cash provided from operating activities increased $1.05 billion primarily as a result of:

| • | a $4.98 billion increase in cash received from customers; |

| • | higher dividends received from equity investments of $84 million; and |

| • | a $28 million decrease in cash taxes. |

These factors were partially offset by:

| • | a $2.84 billion increase in cash paid for materials and overhead; |

| • | a $1.08 billion increase in cash paid for labour; and |

| • | a $75 million increase in cash interest paid. |

Changes in operating assets and liabilities

During 2023, we generated $221 million from operating assets and liabilities primarily consisting of:

| • | a $637 million increase in other accrued liabilities; and |

| • | a $501 million increase in accounts payable. |

These factors were partially offset by:

| • | a $687 million increase in production and other receivables; and |

| • | a $246 million increase in tooling investment for current and upcoming program launches. |

INVESTING ACTIVITIES

| 2023 | 2022 | Change | ||||||||||

| Fixed asset additions | $ | (2,500 | ) | $ | (1,681 | ) | ||||||

| Increase in investments, other assets and intangible assets | (562 | ) | (455 | ) | ||||||||

| Increase in public and private equity investments | (11 | ) | (29 | ) | ||||||||

| Fixed assets, investments, other assets and intangible assets additions | (3,073 | ) | (2,165 | ) | ||||||||

| Proceeds from dispositions | 122 | 124 | ||||||||||

| Net cash (outflow) inflow from disposal of facilities | (48 | ) | 6 | |||||||||

| Acquisitions | (1,504 | ) | (3 | ) | ||||||||

| Cash used for investing activities | $ | (4,503 | ) | $ | (2,038 | ) | $ | (2,465 | ) | |||

Cash used for investing activities in 2023 was $2.47 billion higher compared to 2022. The change between 2023 and 2022 was primarily due to the acquisition of Veoneer AS and a $908 million increase in cash used for fixed assets and other assets.

During the fourth quarter of 2022, we entered into an agreement to sell a European Power & Vision operation in early 2023. During the first quarter of 2023, we completed the sale of this operation which resulted in a net cash outflow of $25 million.

In addition, during the third quarter of 2023, we completed the sale of all of our investments in Russia resulting in a net cash outflow of $23 million.

FINANCING ACTIVITIES

| 2023 | 2022 | Change | ||||||||||

| Issues of debt | $ | 2,083 | $ | 54 | ||||||||

| Increase in short-term borrowings | 487 | 11 | ||||||||||

| Issue of Common Shares on exercise of stock options | 20 | 8 | ||||||||||

| Contributions to subsidiaries by non-controlling interests | 11 | 5 | ||||||||||

| Tax withholdings on vesting of equity awards | (11 | ) | (15 | ) | ||||||||

| Repurchase of Common Shares | (13 | ) | (780 | ) | ||||||||

| Dividends paid to non-controlling interest | (74 | ) | (46 | ) | ||||||||

| Dividends paid | (522 | ) | (514 | ) | ||||||||

| Repayments of debt | (644 | ) | (456 | ) | ||||||||

| Cash provided from (used for) financing activities | $ | 1,337 | $ | (1,733 | ) | $ | 3,070 | |||||

During the first quarter of 2023, we issued the following Senior Notes [the “Senior Notes”]:

| Amount in USD at | ||||||

| Issuance Date | Issuance Date | Maturity Date | ||||

| Cdn$350 million Senior Notes at 4.950% | March 10, 2023 | $258 million | January 31, 2031 | |||

| €550 million Senior Notes at 4.375% | March 17, 2023 | $591 million | March 17, 2032 | |||

| $300 million Senior Notes at 5.980% | March 21, 2023 | $300 million | March 21, 2026 | |||

| $500 million Senior Notes at 5.500% | March 21, 2023 | $500 million | March 21, 2033 |

The total cash proceeds received from the Senior Note issuances was $1,637 million, which consisted of $1,649 million of Senior Notes less debt issuance costs of $12 million.

The

Senior Notes are unsecured obligations and do not include any financial covenants. We may redeem the Senior Notes in whole or in part

at any time, and from time to time, at specified redemption prices determined in accordance with the terms of the indenture governing

the Senior Notes. Refer to Note 16, “Debt” of our audited consolidated financial statements for the

year ended December 31, 2023.

Magna International Inc. Annual Report 2023

On March 6, 2023, we entered into a syndicated, unsecured, delayed draw term loan [the “Term Loan”] with a 3-year tranche of $800 million and 5-year tranche of $600 million. During the second quarter of 2023, we drew $100 million from the 3-year tranche and $300 million from the 5-year tranche of the Term Loan. The amounts are drawn in advances of 1,3 or 6-month loans and may be rolled over until the end of the 3- and 5-year terms. The remaining balance of the facility was subsequently cancelled.

Short-term borrowings increased $487 million in 2023 primarily due to the issuance of Commercial Paper.

Cash dividends paid per Common Share were $1.84 for 2023 compared to $1.80 for 2022.

FINANCING RESOURCES

| 2023 | 2022 | Change | ||||||||||

| Liabilities | ||||||||||||

| Short-term borrowings | $ | 511 | $ | 8 | ||||||||

| Long-term debt due within one year | 819 | 654 | ||||||||||

| Current portion of operating lease liabilities | 399 | 276 | ||||||||||

| Long-term debt | 4,175 | 2,847 | ||||||||||

| Operating lease liabilities | 1,319 | 1,288 | ||||||||||

| $ | 7,223 | $ | 5,073 | $ | 2,150 | |||||||

Financial liabilities increased $2.15 billion to $7.22 billion as at December 31, 2023 primarily as a result of the $1.64 billion issuance of Senior Notes during the first quarter of 2023, a $400 million increase in the Term Loan, and the issuance of $509 million of commercial paper in the fourth quarter of 2023. These increases were offset by a $569 million repayment of Senior Notes.

CASH RESOURCES

In 2023, our cash resources remain unchanged at $1.2 billion, primarily as a result of cash provided from operating and financing activities being offset by cash used for investing activities, as discussed above. In addition to our cash resources at December 31, 2023, we had term and operating lines of credit totaling $4.1 billion, of which $3.0 billion was unused and available.

On March 6, 2023, we entered into a Term Loan with a 3-year tranche of $800 million and a 5-year tranche of $600 million. During the second quarter of 2023, we drew $100 million from the 3-year tranche and $300 million from the 5-year tranche. The remaining balance of the facility was subsequently cancelled.

On April 27, 2023, we amended our $2.7 billion syndicated revolving credit facility, including to: (i) extend the maturity date from June 24, 2027 to June 24, 2028, and (ii) cancel the $150 million Asian tranche and allocate the equivalent amount to the Canadian tranche. As of December 31, 2023, we have had limited borrowing under this credit facility.

On May 26, 2023, we extended the maturity date of our $800 million 364-day syndicated revolving credit facility from June 24, 2023 to June 24, 2024. As of December 31, 2023, we have not borrowed any funds under this credit facility.

MAXIMUM NUMBER OF SHARES ISSUABLE

The following table presents the maximum number of shares that would be outstanding if all of the outstanding options at February 22, 2024 were exercised:

| Common Shares | 286,866,376 | |||

| Stock options (i) | 5,572,829 | |||

| 292,439,205 |

| (i) | Options

to purchase Common Shares are exercisable by the holder in accordance with the vesting provisions

and upon payment of the exercise price as may be determined from time to time pursuant to

our stock option plans. |

CONTRACTUAL OBLIGATIONS

A purchase obligation is defined as an agreement to purchase goods or services that is enforceable and legally binding on us and that specifies all significant terms, including: fixed or minimum quantities to be purchased; fixed, minimum or variable price provisions; and the approximate timing of the transaction. Consistent with our customer obligations, substantially all of our purchases are made under purchase orders with our suppliers which are requirements based and accordingly do not specify minimum quantities. Other long-term liabilities are defined as long-term liabilities that are recorded on our consolidated balance sheet. Based on this definition, the following table includes only those contracts which include fixed or minimum obligations.

At December 31, 2023, we had contractual obligations requiring annual payments as follows:

| 2024 | 2025- 2026 |

2027- 2028 |

Thereafter | Total | ||||||||||||||||

| Operating leases | $ | 326 | $ | 535 | $ | 401 | $ | 779 | $ | 2,041 | ||||||||||

| Long-term debt | 819 | 1,101 | 967 | 2,125 | 5,012 | |||||||||||||||

| Unconditional purchase obligations: | ||||||||||||||||||||

| Materials and services | 5,151 | 576 | 424 | 45 | 6,196 | |||||||||||||||

| Capital | 1,011 | 199 | 63 | 12 | 1,285 | |||||||||||||||

| Total contractual obligations | $ | 7,307 | $ | 2,411 | $ | 1,855 | $ | 2,961 | $ | 14,534 | ||||||||||

Our unfunded obligation with respect to employee future benefit plans, which have been actuarially determined, was $550 million at December 31, 2023. These obligations are as follows:

| Pension Liability |

Retirement Liability |

Termination and Long Service Arrangements |

Total | |||||||||||||

| Projected benefit obligation | $ | 511 | $ | 21 | $ | 445 | $ | 977 | ||||||||

| Less plan assets | (427 | ) | — | — | (427 | ) | ||||||||||

| Unfunded amount | $ | 84 | $ | 21 | $ | 445 | $ | 550 | ||||||||

Foreign Currency Activities

Our North American operations negotiate sales contracts with OEMs for payment in U.S. dollars, Canadian dollars and Mexican pesos. Materials and equipment are purchased in various currencies depending upon competitive factors, including relative currency values. Our North American operations use labour and materials which are paid for in U.S. dollars, Canadian dollars and Mexican pesos. Our Mexican operations generally use the U.S. dollar as the functional currency.

Our European operations negotiate sales contracts with OEMs for payment principally in euros. Our European operations’ material, equipment and labour are paid for principally in euros and U.S. dollars.

Our Asian operations negotiate sales contracts with OEMs for payment principally in Chinese renminbi. Our Asian operations’ material, equipment and labour are paid for principally in Chinese renminbi.

We employ hedging programs, primarily through the use of foreign exchange forward contracts, in an effort to manage our foreign exchange exposure, which arises when manufacturing facilities have committed to the delivery of products for which the selling price or material purchases have been quoted in foreign currencies and for labour in countries where the local currency is not the divisions’ functional currency. These commitments represent our contractual obligations to deliver products over the duration of the product programs, which can last a number of years. The amount and timing of the forward contracts will be dependent upon a number of factors, including anticipated production delivery schedules and anticipated production costs, which may be paid in the foreign currency. Despite these measures, significant long-term fluctuations in relative currency values, in particular a significant change in the relative values of the U.S. dollar, Canadian dollar, euro, Chinese renminbi or Mexican peso, could have an adverse effect on our profitability and financial condition (as discussed throughout this MD&A).

Magna International Inc. Annual Report 2023

NON-GAAP FINANCIAL MEASURES RECONCILIATION

During 2023, we revised our calculations of Adjusted EBIT, Adjusted diluted earnings per share and Adjusted Return on Invested Capital to exclude the amortization of acquired intangible assets. Revenue generated from acquired intangible assets is included within revenue in determining net income attributable to Magna. We believe that excluding the amortization of acquired intangible assets from these Non-GAAP measures helps management and investors in understanding our underlying performance and improves comparability between our segmented results of operations and our peers.

The historical presentation of these Non-GAAP measures within this MD&A has also been updated to reflect the revised calculations.

The reconciliation of Non-GAAP financial measures is as follows:

ADJUSTED EBIT

| 2023 | 2022 | |||||||

| Net income | $ | 1,286 | $ | 641 | ||||

| Add : | ||||||||

| Amortization of acquired intangible assets | 88 | 46 | ||||||

| Interest expense, net | 156 | 81 | ||||||

| Other expense, net | 388 | 703 | ||||||

| Income taxes | 320 | 237 | ||||||

| Adjusted EBIT | $ | 2,238 | $ | 1,708 | ||||

ADJUSTED EBIT AS A PERCENTAGE OF SALES

| 2023 | 2022 | |||||||

| Sales | $ | 42,797 | $ | 37,840 | ||||

| Adjusted EBIT | $ | 2,238 | $ | 1,708 | ||||

| Adjusted EBIT as a percentage of sales | 5.2 | % | 4.5 | % | ||||

ADJUSTED DILUTED EARNINGS PER SHARE

| 2023 | 2022 | |||||||

| Net income attributable to Magna International Inc. | $ | 1,213 | $ | 592 | ||||

| Add (deduct): | ||||||||

| Amortization of acquired intangible assets | 88 | 46 | ||||||

| Other expense, net | 388 | 703 | ||||||

| Tax effect on Amortization of acquired intangible assets and Other expense, net | (70 | ) | (79 | ) | ||||

| Adjustments to Deferred Tax Valuation Allowances | (47 | ) | (29 | ) | ||||

| Adjusted net income attributable to Magna International Inc. | $ | 1,572 | $ | 1,233 | ||||

| Diluted weighted average number of Common Shares outstanding during the period (millions) | 286.6 | 291.2 | ||||||

| Adjusted diluted earnings per share | $ | 5.49 | $ | 4.24 | ||||

ADJUSTED RETURN ON INVESTED CAPITAL

Adjusted Return on Invested Capital is calculated as Adjusted After-tax operating profits divided by Average Invested Capital for the period. Average Invested Capital for the twelve month period is averaged on a five-fiscal quarter basis.

| 2023 | 2022 | |||||||

| Net Income | $ | 1,286 | $ | 641 | ||||

| Add (deduct): | ||||||||

| Interest expense, net | 156 | 81 | ||||||

| Amortization of acquired intangible assets | 88 | 46 | ||||||

| Other expense, net | 388 | 703 | ||||||

| Tax effect on Interest expense, net, Amortization of acquired intangible assets and Other expense, net | (102 | ) | (96 | ) | ||||

| Adjustments to Deferred Tax Valuation Allowances | (47 | ) | (29 | ) | ||||

| Adjusted After-tax operating profits | $ | 1,769 | $ | 1,346 | ||||

| 2023 | 2022 | |||||||

| Total Assets | $ | 32,255 | $ | 27,789 | ||||

| Excluding: | ||||||||

| Cash and cash equivalents | (1,198 | ) | (1,234 | ) | ||||

| Deferred tax assets | (621 | ) | (491 | ) | ||||

| Less Current Liabilities | (13,234 | ) | (10,998 | ) | ||||

| Excluding: | ||||||||

| Short-term borrowing | 511 | 8 | ||||||

| Long-term debt due within one year | 819 | 654 | ||||||

| Current portion of operating lease liabilities | 399 | 276 | ||||||

| Invested Capital | $ | 18,931 | $ | 16,004 | ||||

| 2023 | 2022 | |||||||

| Adjusted After-tax operating profits | $ | 1,769 | $ | 1,346 | ||||

| Average Invested Capital | $ | 17,771 | $ | 15,924 | ||||

| Adjusted Return on Invested Capital | 10.0 | % | 8.5 | % | ||||

Magna International Inc. Annual Report 2023

SIGNIFICANT ACCOUNTING POLICIES AND CRITICAL ACCOUNTING ESTIMATES

Our significant accounting policies are more fully described in Note 2, “Significant Accounting Policies”, to the consolidated financial statements included in this Report. The preparation of the audited consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses and the related disclosure of contingent assets and liabilities, as of the date of the consolidated financial statements. These estimates and assumptions are based on our historical experience, and various other assumptions we believe to be reasonable in the circumstances. Since these estimates and assumptions are subject to an inherent degree of uncertainty, actual results in these areas may differ significantly from our estimates.

We believe the following critical accounting policies and estimates affect the more subjective or complex judgements and estimates used in the preparation of our consolidated financial statements and accompanying notes. Management has discussed the development and selection of the following critical accounting policies with the Audit Committee of the Board of Directors, and the Audit Committee has reviewed our disclosure relating to critical accounting policies in this MD&A.

BUSINESS COMBINATIONS

We allocate the purchase price of an acquired business to its identifiable assets and liabilities based on estimated fair values at the date of the acquisition. The excess of the purchase price over the amount allocated to the assets and liabilities, if any, is recorded as goodwill.

Our purchase price allocation methodology contains uncertainties because it requires management to make assumptions and to apply judgement to estimate the fair value of assets acquired and liabilities assumed. When determining the fair values of assets acquired and liabilities assumed, management makes significant estimates and assumptions and engages outside appraisal firms to assist in the fair value determination of identifiable intangible assets and any other significant assets or liabilities. We adjust the preliminary purchase price allocation, as necessary, up to one year after acquisition closing date as we obtain more information regarding assets acquired and liabilities assumed.

Unanticipated events or circumstances may occur which could affect the accuracy of our fair value estimates, including assumptions regarding industry economic factors and business strategies. Accordingly, there can be no assurance that the estimates, assumptions, and values reflected in the valuations will be realized, and actual results could vary.

REVENUE RECOGNITION - COMPLETE VEHICLE ASSEMBLY ARRANGEMENTS

Our complete vehicle assembly contracts with customers are complex and often include promises to transfer multiple products and services, some of which may be implicitly contracted. Each good or service is evaluated to determine whether it represents a distinct performance obligation, and whether it should be characterized as revenue or as a reimbursement of costs incurred. The total transaction price is then allocated to the distinct performance obligations based on the expected cost plus a margin approach and recognized as revenue.

Significant interpretation and judgment is sometimes required to determine the appropriate accounting for these contracts including: (i) combining contracts that may impact the allocation of the transaction price between products and services; (ii) determining whether performance obligations are considered distinct and are required to be accounted for separately or combined; and (iii) the allocation of the transaction price to each distinct performance obligation and determining when to recognize revenue.

IMPAIRMENT ASSESSMENTS – GOODWILL, LONG-LIVED ASSETS, AND EQUITY METHOD INVESTMENTS

We review goodwill at the reporting unit level for impairment in the fourth quarter of each year or more frequently if events or changes in circumstances indicate that goodwill might be impaired. Goodwill impairment is assessed by comparing the fair value of a reporting unit to the underlying carrying value of the reporting unit’s net assets, including goodwill. If a reporting unit’s carrying amount exceeds its fair value, an impairment is recognized based on that difference. The fair value of a reporting unit is determined using the estimated discounted future cash flows of the reporting unit.

In addition to our review of goodwill, we evaluate fixed assets and other long-lived assets for impairment whenever indicators of impairment exist. Indicators of impairment include the bankruptcy of a significant customer or the early termination, loss, renegotiation of the terms of, significant volume decrease in, or delay in the implementation of, any significant production contract. If the sum of the future cash flows expected to result from the asset, undiscounted and without interest charges, is less than the carrying amount of the asset, an asset impairment may be recognized in the consolidated financial statements. The amount of impairment to be recognized is calculated by subtracting the fair value of the asset from the carrying amount of the asset.

As of December 31, 2023, we had equity method investments of $987 million. We monitor our investments for indicators of other-than-temporary declines in value on an ongoing basis in accordance with U.S. GAAP. If we determine that an other-than-temporary decline in value has occurred, we recognize an impairment loss, which is measured as the difference between the book value and the fair value of the investment.

We believe that the impairment assessments for goodwill, long-lived assets, and equity method investments contain “critical accounting estimates” because: (i) they are subject to significant measurement uncertainty and are susceptible to change as management is required to make forward-looking assumptions regarding the impact of improvement plans on current operations, in-sourcing and other new business opportunities, program pricing and cost assumptions on current and future business, the timing of new program launches and future forecasted production volumes; and (ii) any resulting impairment loss could have a material impact on our consolidated net income and on the amount of assets reported in our consolidated balance sheet.

WARRANTY

We record product warranty costs, which include product liability and recall costs. Under most customer agreements, we only account for existing or probable claims on product default issues when amounts related to such issues are probable and reasonably estimable. Under certain complete vehicle assembly, powertrain systems, and electronics contracts, we record an estimate of future warranty-related costs based on the terms of the specific customer agreements and/or the Company’s warranty experience.

Product liability and recall provisions are established based on our best estimate of the amounts necessary to settle existing claims. These estimates typically require assumptions from management regarding: the number of units that may be returned; the cost of the product being replaced; labour to remove and replace the defective part; and the customer’s administrative costs relating to the recall. In making this estimate, judgement is also required as to the ultimate negotiated sharing of the cost between us, the customer and, in some cases a supplier. Where applicable, insurance recoveries related to such provisions are also recorded.

We monitor warranty activity on an ongoing basis and revise our best estimate as necessary. Due to the uncertainty and potential volatility of the factors contributing to developing estimates of the amounts necessary to settle existing claims, actual product liability costs could be materially different from our best estimate.

INCOME TAXES

The determination of our tax liabilities involves dealing with uncertainties in the application of complex tax laws. Significant judgement and estimates are required in determining our provision for income taxes, deferred tax assets and liabilities, and liabilities for unrecognized tax benefits. We recognize tax benefits from uncertain tax positions only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such positions are then measured based on the largest benefit that has a greater than 50% likelihood of being realized upon ultimate settlement.

At December 31, 2023, we had gross unrecognized tax benefits of $220 million excluding interest and penalties, of which $188 million, if recognized, would affect our effective tax rate. The gross unrecognized tax benefits differ from the amount that would affect our effective tax rate due primarily to the impact of the valuation allowances on deferred tax assets.

Deferred tax assets and liabilities are recognized for the estimated future tax effects attributable to temporary differences between financial statement carrying value of existing assets and liabilities and their respective tax bases and tax loss and credit carryforwards. Deferred tax assets and liabilities are measured using the enacted tax rates and laws that will be in effect when the differences are expected to reverse. Accounting standards require that we assess whether valuation allowances should be established or maintained against our deferred income tax assets, based on consideration of all available evidence, using a “more-likely-than-not” standard. The factors used to assess the likelihood of realization are: history of losses, forecasts of future pre-tax income and tax planning strategies that could be implemented to realize the deferred tax assets. On a quarterly basis, we evaluate the realizability of deferred tax assets by assessing our valuation allowances and by adjusting the amount of such allowances as necessary. We use tax planning strategies to realize deferred tax assets in order to avoid the potential loss of these tax benefits. Changes in our estimates, due to unforeseen events or otherwise, could have a material impact on our financial condition and results of operations. Refer to Note 12, “Income Taxes” of the notes to the consolidated financial statements for additional information.

EMPLOYEE FUTURE BENEFIT PLANS

The determination of the obligation and expense for defined benefit pension, termination and long service arrangements and other post-retirement benefits, such as retiree healthcare and medical benefits, is dependent on the selection of certain assumptions used by actuaries in calculating such amounts. Those assumptions include, among others, the discount rate, expected long-term rate of return on plan assets and rates of increase in compensation costs. Actual results that differ from the assumptions used are accumulated and amortized over future periods and therefore impact the recognized expense in future periods. Significant changes in assumptions or significant plan amendments could materially affect our future employee benefit obligations and future expense.

Magna International Inc. Annual Report 2023

At December 31, 2023, we had past service costs and actuarial experience losses of $116 million included in accumulated other comprehensive income that will be amortized to future employee benefit expense over the expected average remaining service life of employees or over the expected average life expectancy of retired employees, depending on the status of the plan.

COMMITMENTS AND CONTINGENCIES

From time to time, we may be contingently liable for litigation, legal and/or regulatory actions and proceedings and other claims. Refer to Note 23, “Contingencies” of our audited consolidated financial statements for the year ended December 31, 2023.

For a discussion of risk factors relating to legal and other claims/actions against us, refer to “Item 5. Risk Factors” in our Annual Information Form and Annual Report on Form 40-F, each in respect of the year ended December 31, 2023.

CONTROLS AND PROCEDURES

DISCLOSURE CONTROLS AND PROCEDURES

Disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended [the “Exchange Act”]), are designed to ensure that material information required to be disclosed in reports filed or submitted under the Exchange Act is recorded, processed, summarized and reported on a timely basis, and that such information is accumulated and communicated to senior management, including the Company’s Chief Executive Officer and Chief Financial Officer, as appropriate, to enable them to make timely decisions regarding required disclosure of such information. We have conducted an evaluation of our disclosure controls and procedures as of December 31, 2023, under the supervision, and with the participation of our Chief Executive Officer and our Chief Financial Officer. Based on this evaluation, our Chief Executive Officer and our Chief Financial Officer have concluded that our disclosure controls and procedures (as this term is defined in the rules adopted by Canadian securities regulatory authorities and the United States Securities and Exchange Commission [“SEC”]) are effective as of December 31, 2023.

MANAGEMENT’S ANNUAL REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

Internal control over financial reporting is a process designed to provide reasonable, but not absolute, assurance regarding the reliability of financial reporting and preparation of financial statements for external purposes in accordance with U.S. GAAP. Our management is responsible for establishing and maintaining adequate internal control over financial reporting. Due to its inherent limitations, internal control over financial reporting may not prevent or detect misstatements on a timely basis. Additionally, projections of any evaluation of the effectiveness of internal control over financial reporting to future periods are subject to the risk that the controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. Our management used the Committee of Sponsoring Organizations of the Treadway Commission [“COSO”] Internal Control-Integrated Framework (2013) to evaluate the effectiveness of internal control over financial reporting.

On June 1, 2023, we completed the acquisition of 100% of the common shares of Veoneer AS. As permitted by securities rules and regulations, we have excluded Veoneer AS from our evaluation of internal controls over financial reporting as of December 31, 2023. The excluded Veoneer AS assets constituted 4% of our total assets as of December 31, 2023, and 2% of our sales for the year then ended.

Based on this evaluation, our Chief Executive Officer and our Chief Financial Officer have assessed the effectiveness of our internal control over financial reporting and concluded that, as at December 31, 2023, such internal control over financial reporting is effective. The Company’s internal control over financial reporting as of December 31, 2023, has been audited by Deloitte LLP, an Independent Registered Public Accounting Firm, who also audited the Company’s consolidated financial statements for the year ended December 31, 2023. Deloitte LLP expressed an unqualified opinion on the effectiveness of the Company’s internal control over financial reporting. This report precedes our audited consolidated financial statements for the year ended December 31, 2023.

CHANGES IN INTERNAL CONTROLS OVER FINANCIAL REPORTING

Other than the addition of Veoneer AS operations to our internal control over financial reporting, there have been no changes in our internal controls over financial reporting that occurred during 2023 that have materially affected or are reasonably likely to materially affect, our internal control over financial reporting. We are currently integrating Veoneer AS into our operations, compliance programs, and internal control process.

RISK FACTORS

Our short and medium-term operational success, as well as our ability to create long-term value through our business strategy, are subject to risks and uncertainties. The following are the more significant risks:

MACROECONOMIC, GEOPOLITICAL AND OTHER RISKS

| • | Inflationary Pressures: We continue to experience elevated inflation in all markets in which we operate, with higher commodity, energy, labour, freight, and other production input pricing expected to persist in 2024. While many of these input price increases will moderate over time, the increases in wage levels we are currently experiencing are likely to have a longer-term effect on our cost structure. Additionally, we may continue to experience price increases or surcharges from sub-suppliers in connection with the inflationary pressures they face. The inability to offset inflationary price increases, including through recoveries from our customers, modifications to our products, continuous improvement actions or otherwise, could have a material adverse effect on our profitability. |

| • | Interest Rates: Increasing global inflation rates have spurred a cycle of monetary policy tightening, including through central bank increases to key short term lending rates. The availability and cost of credit are both factors affecting consumer confidence, which is a critical driver of vehicle sales and thus automotive production. A material, sustained decrease in consumer demand for vehicles could result in further reductions to vehicle production from levels assumed in our business plan, which could have a material adverse effect on our profitability and financial condition. Higher interest rates will have an adverse effect on our borrowing costs and, if prolonged, could have an adverse effect on our profitability. |