UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934

| Date of Report (Date of earliest event reported) | November 9, 2023 |

| Associated Banc-Corp |

| (Exact name of registrant as specified in its charter) |

| Wisconsin | 001-31343 | 39-1098068 |

| (State or other jurisdiction of incorporation) | (Commission File Number) |

(IRS Employer Identification No.) |

| 433 Main Street, Green Bay, Wisconsin | 54301 |

| (Address of principal executive offices) | (Zip code) |

| Registrant’s telephone number, including area code | (920) 491-7500 |

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

¨ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

¨ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

¨ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

¨ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) |

Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | ASB | The New York Stock Exchange |

| Depositary Shrs, each representing 1/40th intrst in a shr of 5.875% Non-Cum. Perp Pref Stock, Srs E | ASB PrE | The New York Stock Exchange |

| Depositary Shrs, each representing 1/40th intrst in a shr of 5.625% Non-Cum. Perp Pref Stock, Srs F | ASB PrF | The New York Stock Exchange |

| 6.625% Fixed-Rate Reset Subordinated Notes due 2033 | ASBA | The New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 7.01 Regulation FD Disclosure. |

| Associated Banc-Corp (the “Company”) is furnishing herewith as Exhibit 99.1 a strategic update presentation providing detailed information regarding the strategic update described under Item 8.01 of this current report on Form 8-K. |

| Item 8.01. Other Events. |

|

On November 9, 2023, the Company announced plans for the next phase of the Company’s people-led, digitally enabled strategic plan. These plans include a series of investments in people, products and technology intended to grow and remix the loan portfolio, accelerate core customer deposit growth.

The press release issued by the Company on November 9, 2023 relating to the announcement described above is attached hereto as Exhibit 99.2 and is incorporated herein by reference. |

| Item 9.01. Financial Statements and Exhibits. |

| (d) Exhibits |

| 99.1 | Strategic Update Presentation dated November 9, 2023 |

| 99.2 | Press Release dated November 9, 2023 |

| 104 | Cover Page Interactive Data File the cover page XBRL tags are embedded within the Inline XBRL document |

| SIGNATURES | |

| Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized. | |

| Associated Banc-Corp | |

| (Registrant) | |

| Date: November 9, 2023 | By: /s/ Randall J. Erickson |

| Randall J. Erickson | |

| Executive Vice President, General Counsel and Corporate Secretary | |

Exhibit 99.1

November 9, 2023 Strategic Update Presentation Associated Banc - Corp 1 Forward - Looking Statements Important note regarding forward - looking statements: Statements made in this presentation which are not purely historical are forward - looking statements, as defined in the Private Securities Litigation Reform Act of 1995.

This includes any statements regarding management’s plans, objectives, or goals for future operations, products or services, and forecasts of its revenues, earnings, or other measures of performance. Such forward - looking statements may be identified by the use of words such as “believe,” “expect,” “anticipate,” “plan,” “estimate,” “should,” “will,” “intend,” "target,“ “outlook,” “project,” “guidance,” or simila r expressions. Forward - looking statements are based on current management expectations and, by their nature, are subject to risks and uncertainties. Actual results may differ materially from those contained in the forward - looking statements. Factors which may cause actual results to differ materially from those contained in such forward - looking statements include those identified in the Company’s most recent Form 10 - K and subsequent Form 10 - Qs and other SEC filings, and such factors are incorporated herein by reference. Trademarks: All trademarks, service marks, and trade names referenced in this material are official trademarks and the property of their respective owners. Presentation: Within the charts and tables presented, certain segments, columns and rows may not sum to totals shown due to rounding. Non - GAAP Measures: This presentation includes certain non - GAAP financial measures. These non - GAAP measures are provided in addition to, and not as substitutes for, measures of our financial performance determined in accordance with GAAP. Our calculation of these non - GAAP measures may not be comparable to similarly titled measures of other companies due to potential differences between companies in the method of calculation. As a result, the use of these non - GAAP measures has limitations and should not be considered superior to, in isolation from, or as a substitute for, related GAAP measures. Reconciliations of these non - GAAP financial measures to the most directly comparable GAAP financial measures can be found at the end of this presentation.

Our Foundation

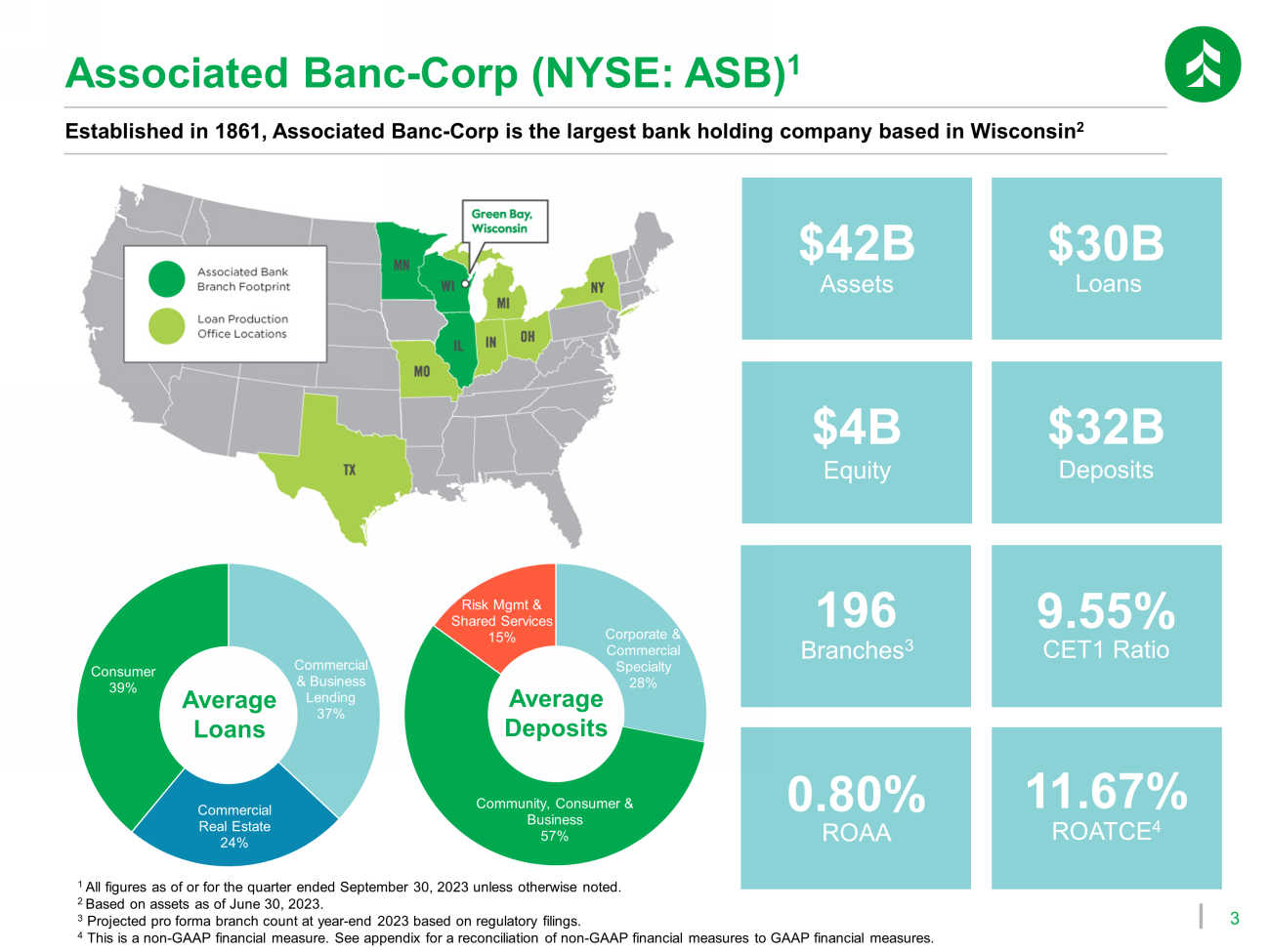

3 Commercial & Business Lending 37% Commercial Real Estate 24% Consumer 39% Corporate & Commercial Specialty 28% Community, Consumer & Business 57% Risk Mgmt & Shared Services 15% Established in 1861, Associated Banc - Corp is the largest bank holding company based in Wisconsin 2 Associated Banc - Corp (NYSE: ASB) 1 $42B Assets $30B Loans $4B Equity $32B Deposits Average Loans Average Deposits 1 All figures as of or for the quarter ended September 30, 2023 unless otherwise noted. 2 Based on assets as of June 30, 2023. 3 Projected pro forma branch count at year - end 2023 based on regulatory filings. 4 This is a non - GAAP financial measure. See appendix for a reconciliation of non - GAAP financial measures to GAAP financial measur es.

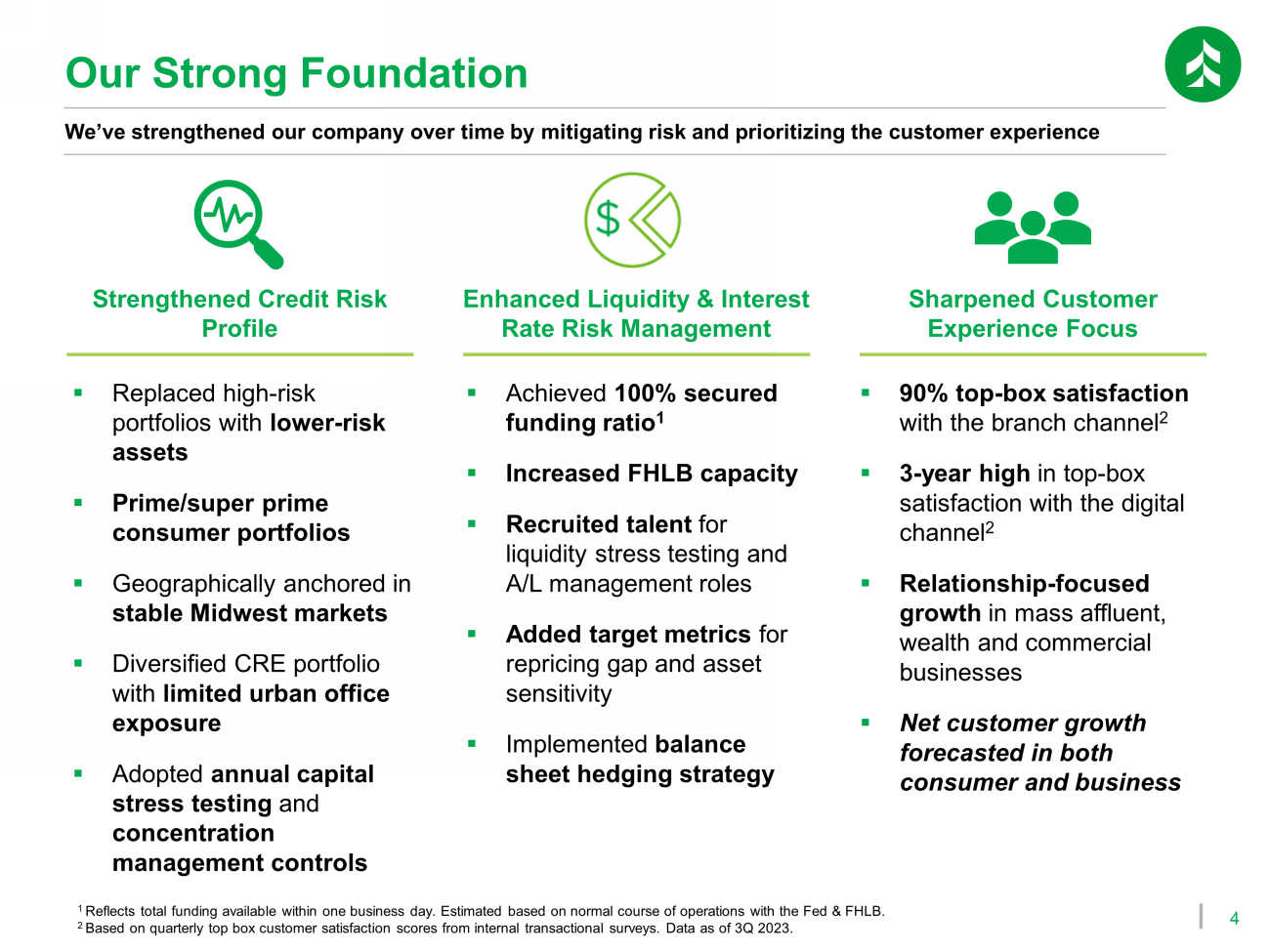

11.67% ROATCE 4 196 Branches 3 9.55% CET1 Ratio 0.80% ROAA 4 Our Strong Foundation We’ve strengthened our company over time by mitigating risk and prioritizing the customer experience Strengthened Credit Risk Profile Enhanced Liquidity & Interest Rate Risk Management Sharpened Customer Experience Focus ▪ Replaced high - risk portfolios with lower - risk assets ▪ Prime/super prime consumer portfolios ▪ Geographically anchored in stable Midwest markets ▪ Diversified CRE portfolio with limited urban office exposure ▪ Adopted annual capital stress testing and concentration management controls ▪ Achieved 100% secured funding ratio 1 ▪ Increased FHLB capacity ▪ Recruited talent for liquidity stress testing and A/L management roles ▪ Added target metrics for repricing gap and asset sensitivity ▪ Implemented balance sheet hedging strategy ▪ 90% top - box satisfaction with the branch channel 2 ▪ 3 - year high in top - box satisfaction with the digital channel 2 ▪ Relationship - focused growth in mass affluent, wealth and commercial businesses ▪ Net customer growth forecasted in both consumer and business 1 Reflects total funding available within one business day. Estimated based on normal course of operations with the Fed & FHLB. 2 Based on quarterly top box customer satisfaction scores from internal transactional surveys. Data as of 3Q 2023.

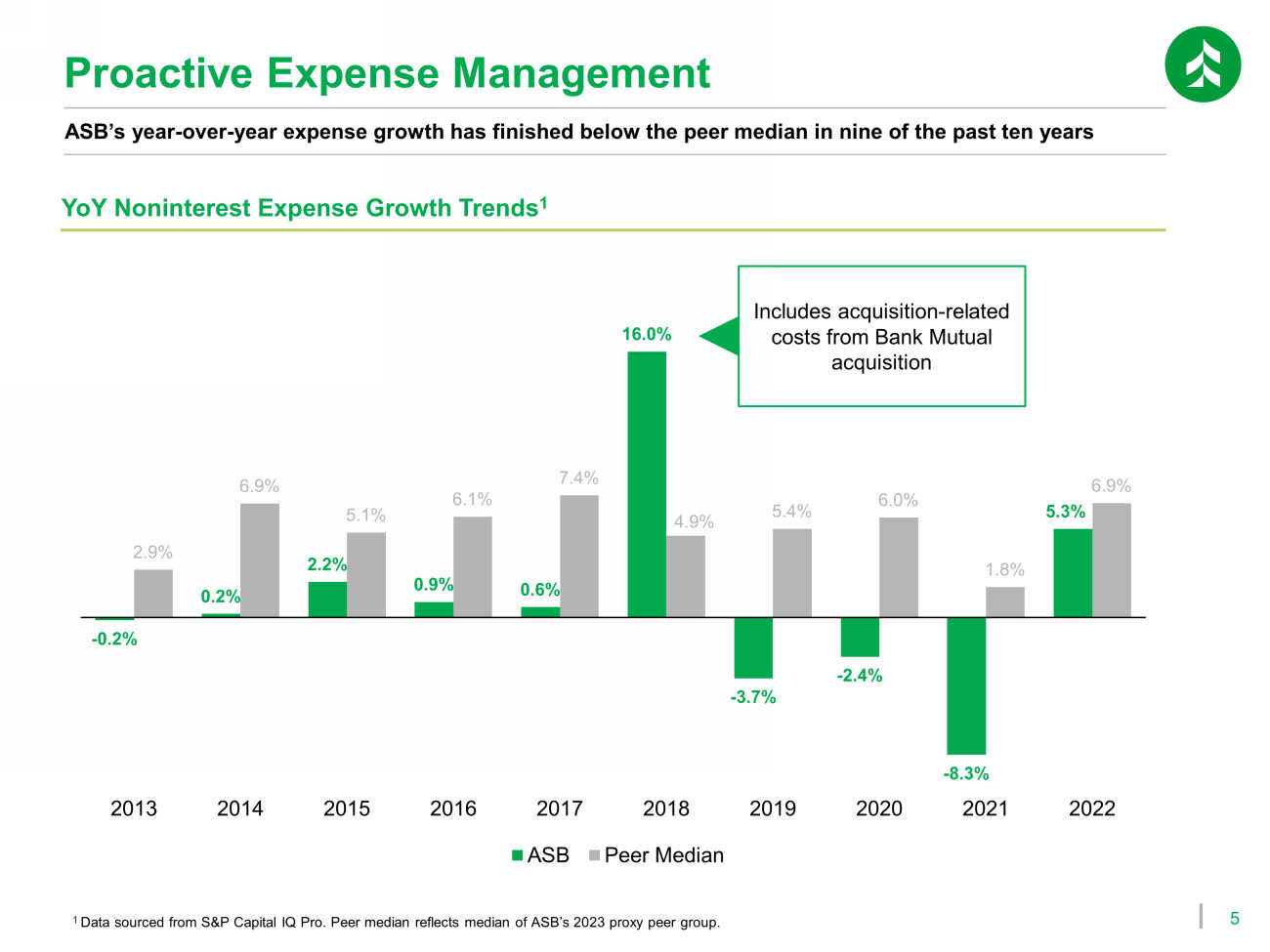

5 Proactive Expense Management ASB’s year - over - year expense growth has finished below the peer median in nine of the past ten years 1 Data sourced from S&P Capital IQ Pro . Peer median reflects median of ASB’s 2023 proxy peer group. YoY Noninterest Expense Growth Trends 1 - 0.2% 0.2% 2.2% 0.9% 0.6% 16.0% - 3.7% - 2.4% - 8.3% 5.3% 2.9% 6.9% 5.1% 6.1% 7.4% 4.9% 5.4% 6.0% 1.8% 6.9% 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 ASB Peer Median Includes acquisition - related costs from Bank Mutual acquisition Strategic Plan Phase 1 Launched September 2021

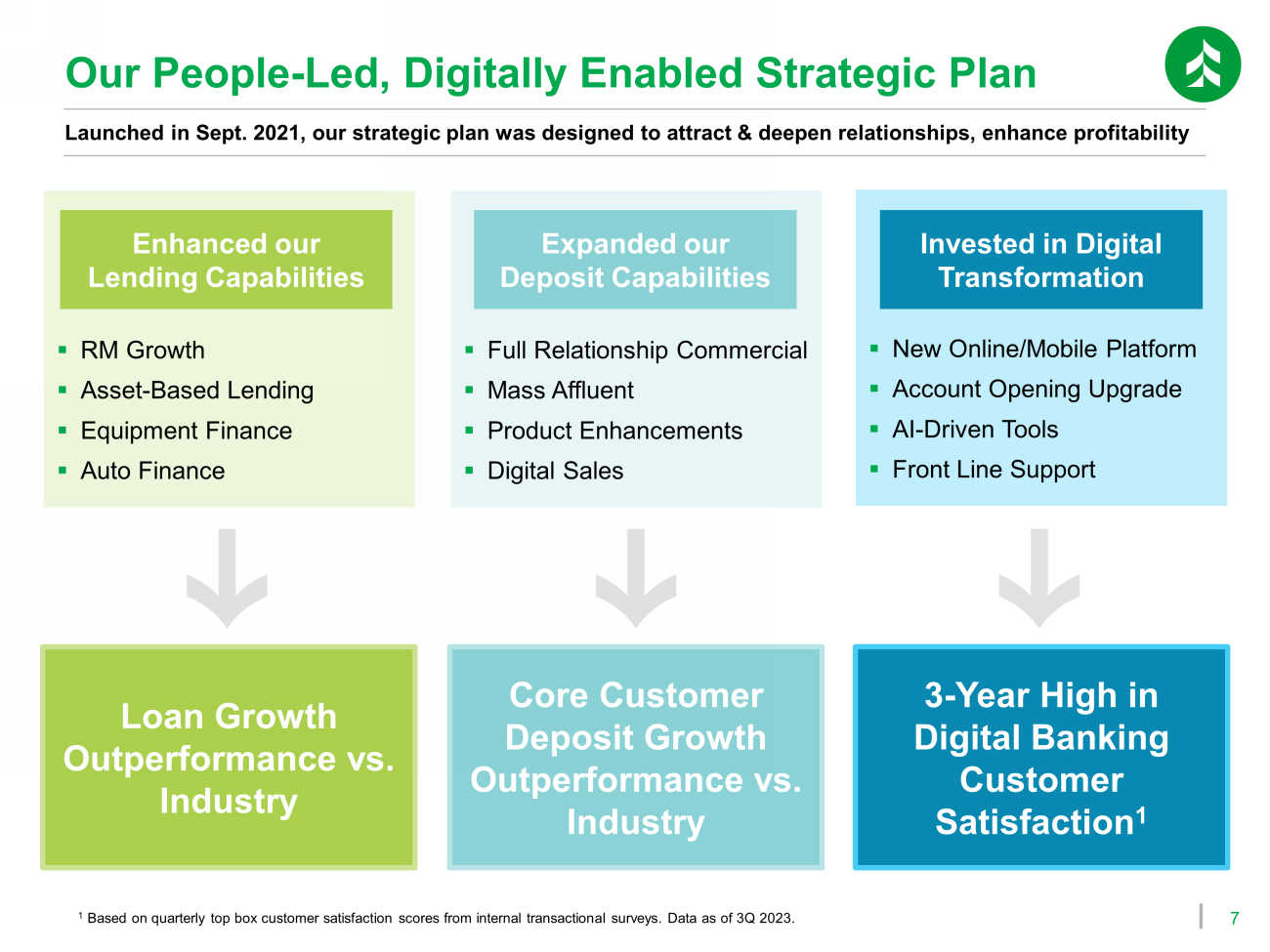

7 Our People - Led, Digitally Enabled Strategic Plan Launched in Sept. 2021, our strategic plan was designed to attract & deepen relationships, enhance profitability ▪ RM Growth ▪ Asset - Based Lending ▪ Equipment Finance ▪ Auto Finance ▪ Full Relationship Commercial ▪ Mass Affluent ▪ Product Enhancements ▪ Digital Sales ▪ New Online/Mobile Platform ▪ Account Opening Upgrade ▪ AI - Driven Tools ▪ Front Line Support Enhanced our Lending Capabilities Expanded our Deposit Capabilities Invested in Digital Transformation Loan Growth Outperformance vs. Industry Core Customer Deposit Growth Outperformance vs. Industry 3 - Year High in Digital Banking Customer Satisfaction 1 1 Based on quarterly top box customer satisfaction scores from internal transactional surveys. Data as of 3Q 2023.

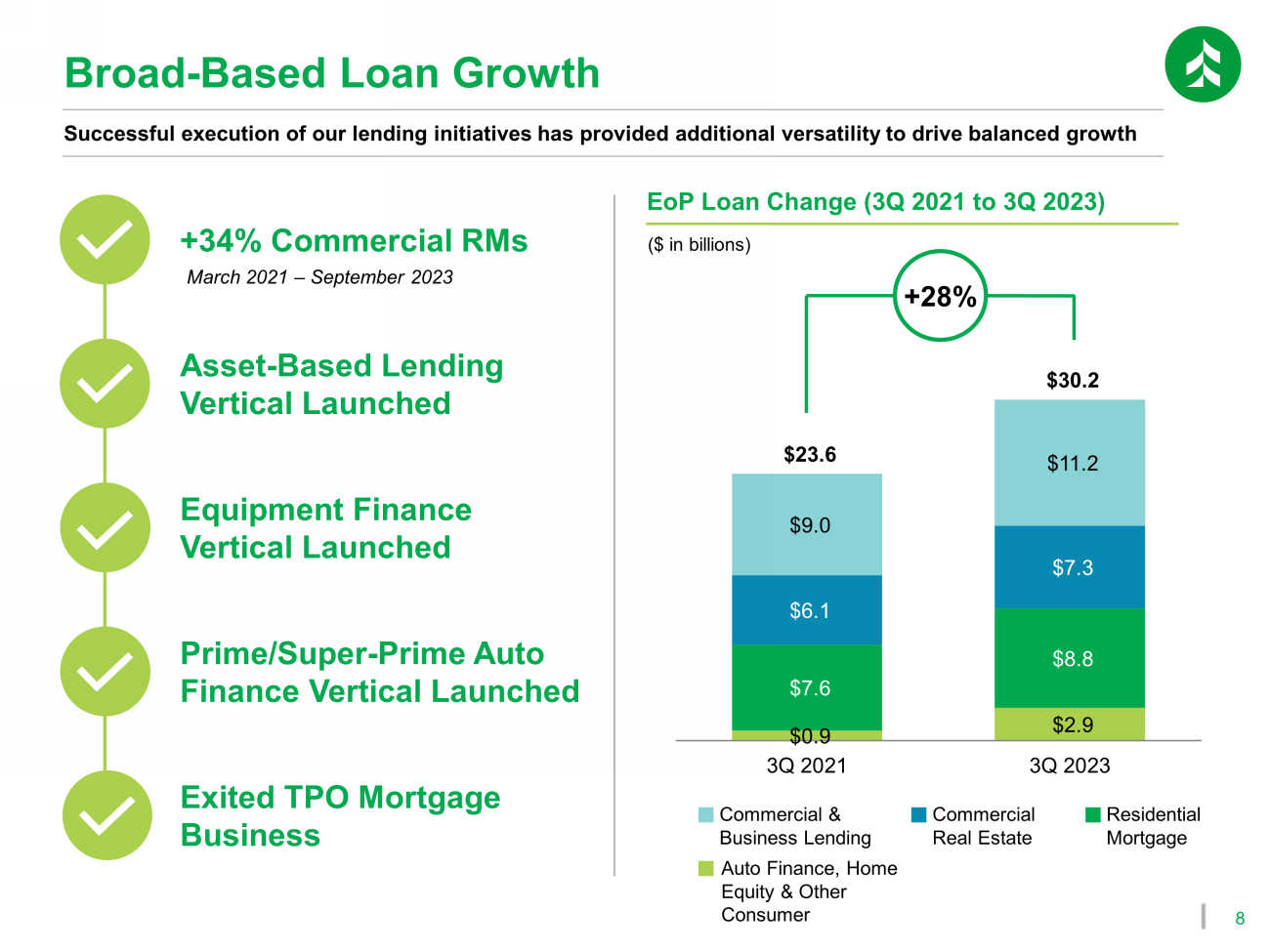

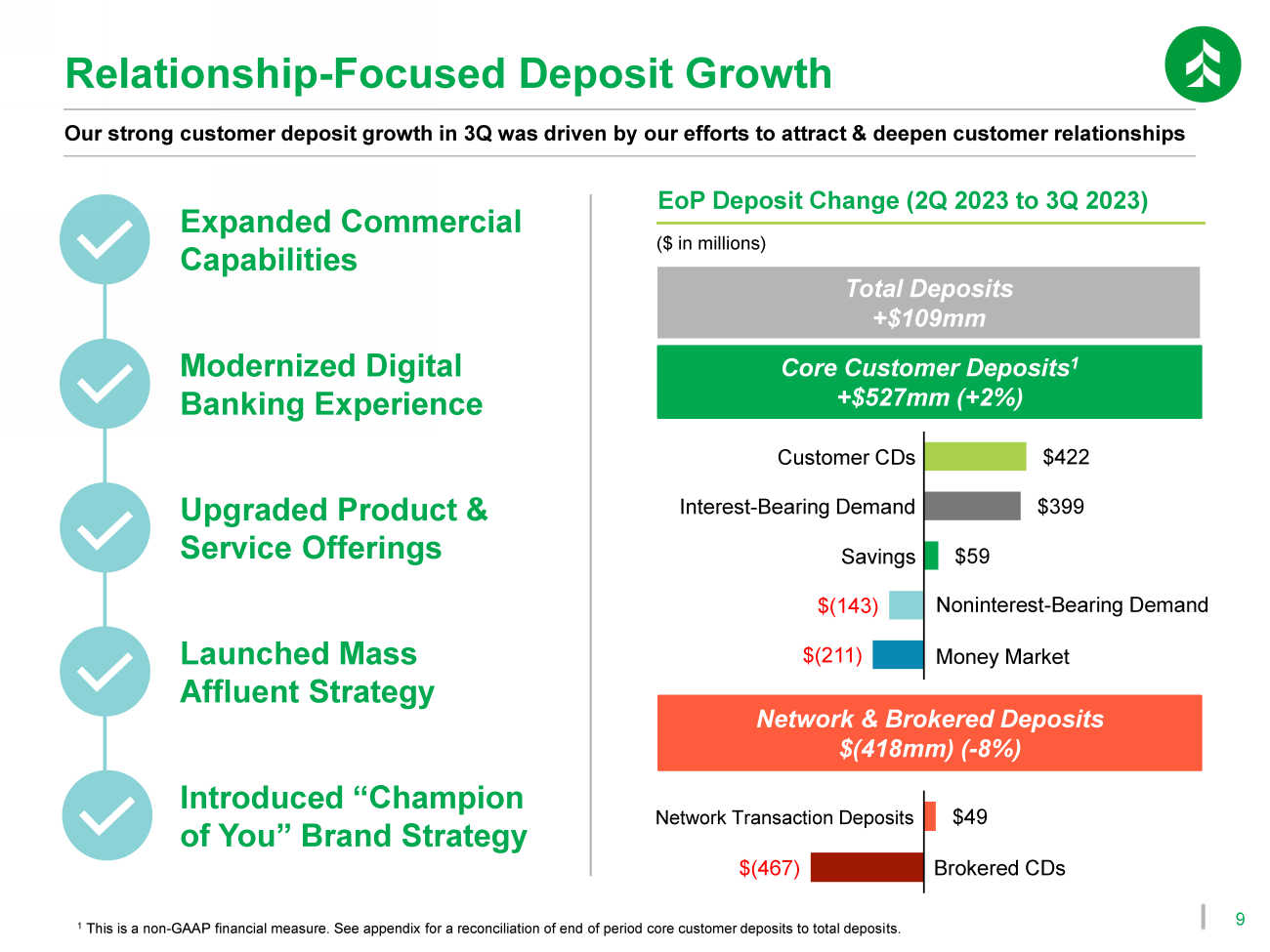

8 Successful execution of our lending initiatives has provided additional versatility to drive balanced growth Broad - Based Loan Growth EoP Loan Change (3Q 2021 to 3Q 2023) Asset - Based Lending Vertical Launched Equipment Finance Vertical Launched Prime/Super - Prime Auto Finance Vertical Launched Exited TPO Mortgage Business +34% Commercial RMs March 2021 – September 2023 ($ in billions) Auto Finance, Home Equity & Other Consumer $0.9 $2.9 $7.6 $8.8 $6.1 $7.3 $9.0 $11.2 $23.6 $30.2 3Q 2021 3Q 2023 Commercial & Business Lending Commercial Real Estate Residential Mortgage +28% 9 Our strong customer deposit growth in 3Q was driven by our efforts to attract & deepen customer relationships Relationship - Focused Deposit Growth Modernized Digital Banking Experience Upgraded Product & Service Offerings Launched Mass Affluent Strategy Introduced “Champion of You” Brand Strategy Expanded Commercial Capabilities 1 This is a non - GAAP financial measure.

See appendix for a reconciliation of end of period core customer deposits to total deposi ts.

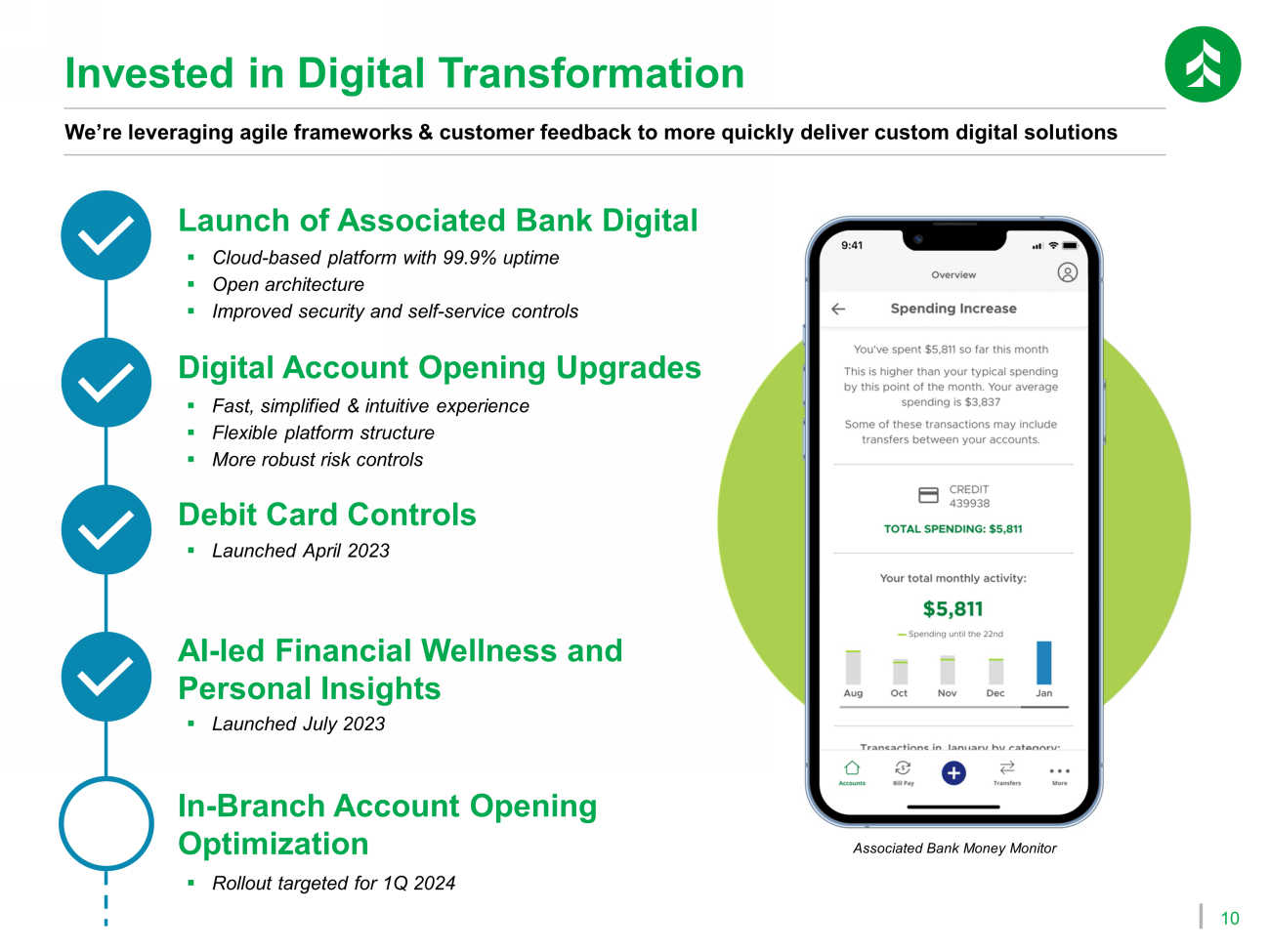

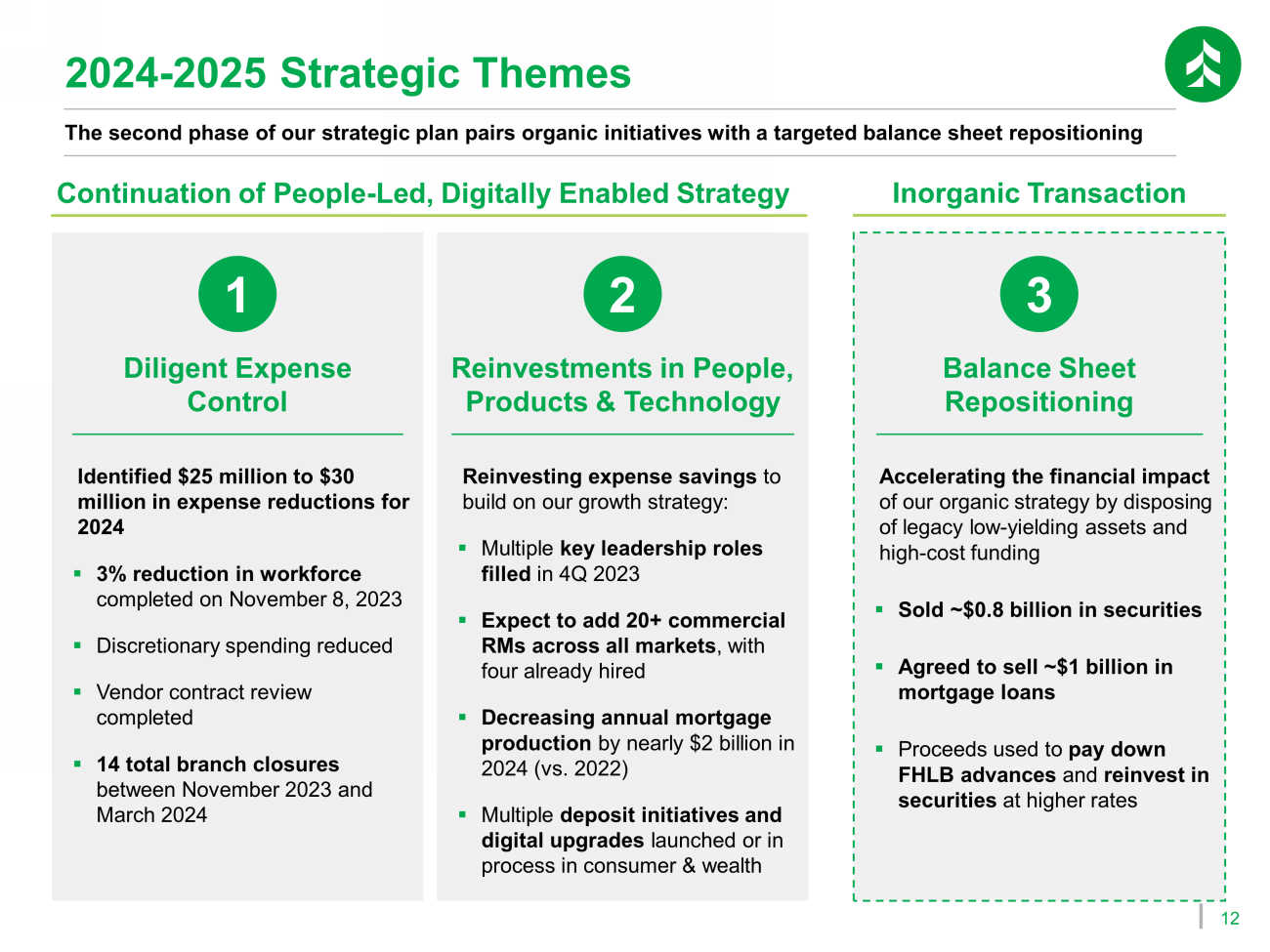

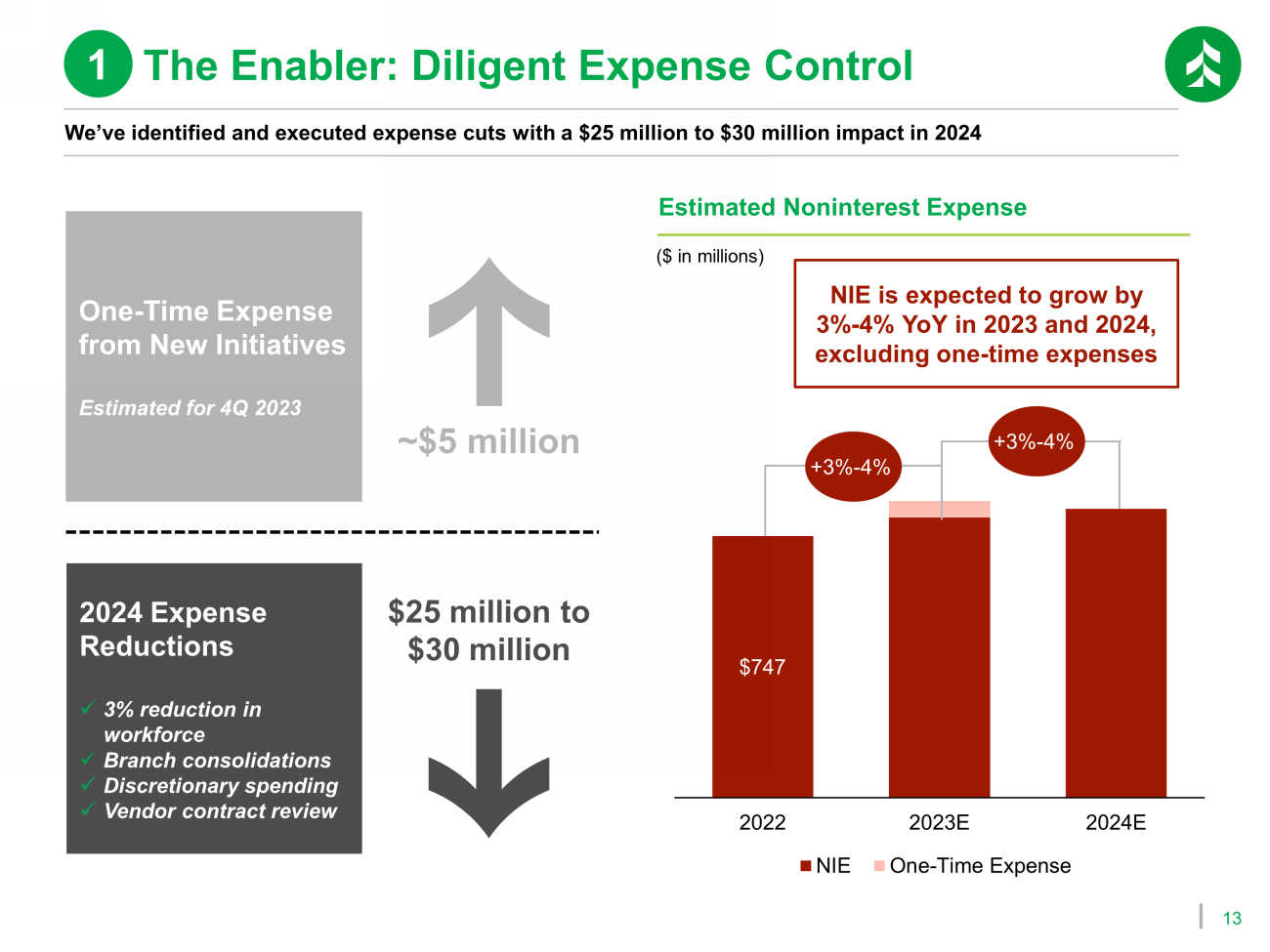

EoP Deposit Change (2Q 2023 to 3Q 2023) ($ in millions) $(211) $(143) $59 $399 $422 Custome r CDs Money Market Interest - Bearing Demand $(467) $49 Network Transaction Deposits Noninterest - Bearing Demand Brokered CDs Savings Core Customer Deposits 1 +$527mm (+2%) Network & Brokered Deposits $(418mm) ( - 8%) Total Deposits +$109mm 10 We’re leveraging agile frameworks & customer feedback to more quickly deliver custom digital solutions Invested in Digital Transformation Launch of Associated Bank Digital Debit Card Controls AI - led Financial Wellness and Personal Insights Digital Account Opening Upgrades ▪ Cloud - based platform with 99.9% uptime ▪ Open architecture ▪ Improved security and self - service controls ▪ Fast, simplified & intuitive experience ▪ Flexible platform structure ▪ More robust risk controls In - Branch Account Opening Optimization ▪ Launched April 2023 ▪ Launched July 2023 Associated Bank Money Monitor ▪ Rollout targeted for 1Q 2024 12 2024 - 2025 Strategic Themes The second phase of our strategic plan pairs organic initiatives with a targeted balance sheet repositioning Identified $25 million to $30 million in expense reductions for 2024 ▪ 3% reduction in workforce completed on November 8, 2023 ▪ Discretionary spending reduced ▪ Vendor contract review completed ▪ 14 total branch closures between November 2023 and March 2024 Reinvesting expense savings to build on our growth strategy: ▪ Multiple key leadership roles filled in 4Q 2023 ▪ Expect to add 20+ commercial RMs across all markets , with four already hired ▪ Decreasing annual mortgage production by nearly $2 billion in 2024 (vs.

Our Next Chapter

2022) ▪ Multiple deposit initiatives and digital upgrades launched or in process in consumer & wealth Diligent Expense Control Accelerating the financial impact of our organic strategy by disposing of legacy low - yielding assets and high - cost funding ▪ Sold ~$0.8 billion in securities ▪ Agreed to sell ~$1 billion in mortgage loans ▪ Proceeds used to pay down FHLB advances and reinvest in securities at higher rates Balance Sheet Repositioning Inorganic Transaction Continuation of People - Led, Digitally Enabled Strategy Reinvestments in People, Products & Technology 1 2 3 13 One - Time Expense from New Initiatives Estimated for 4Q 2023 We’ve identified and executed expense cuts with a $25 million to $30 million impact in 2024 The Enabler: Diligent Expense Control Estimated Noninterest Expense $747 2022 2023E 2024E NIE One-Time Expense NIE is expected to grow by 3% - 4% YoY in 2023 and 2024, excluding one - time expenses +3% - 4% +3% - 4% ($ in millions) 2024 Expense Reductions x 3% reduction in workforce x Branch consolidations x Discretionary spending x Vendor contract review ~$5 million $25 million to $30 million 1

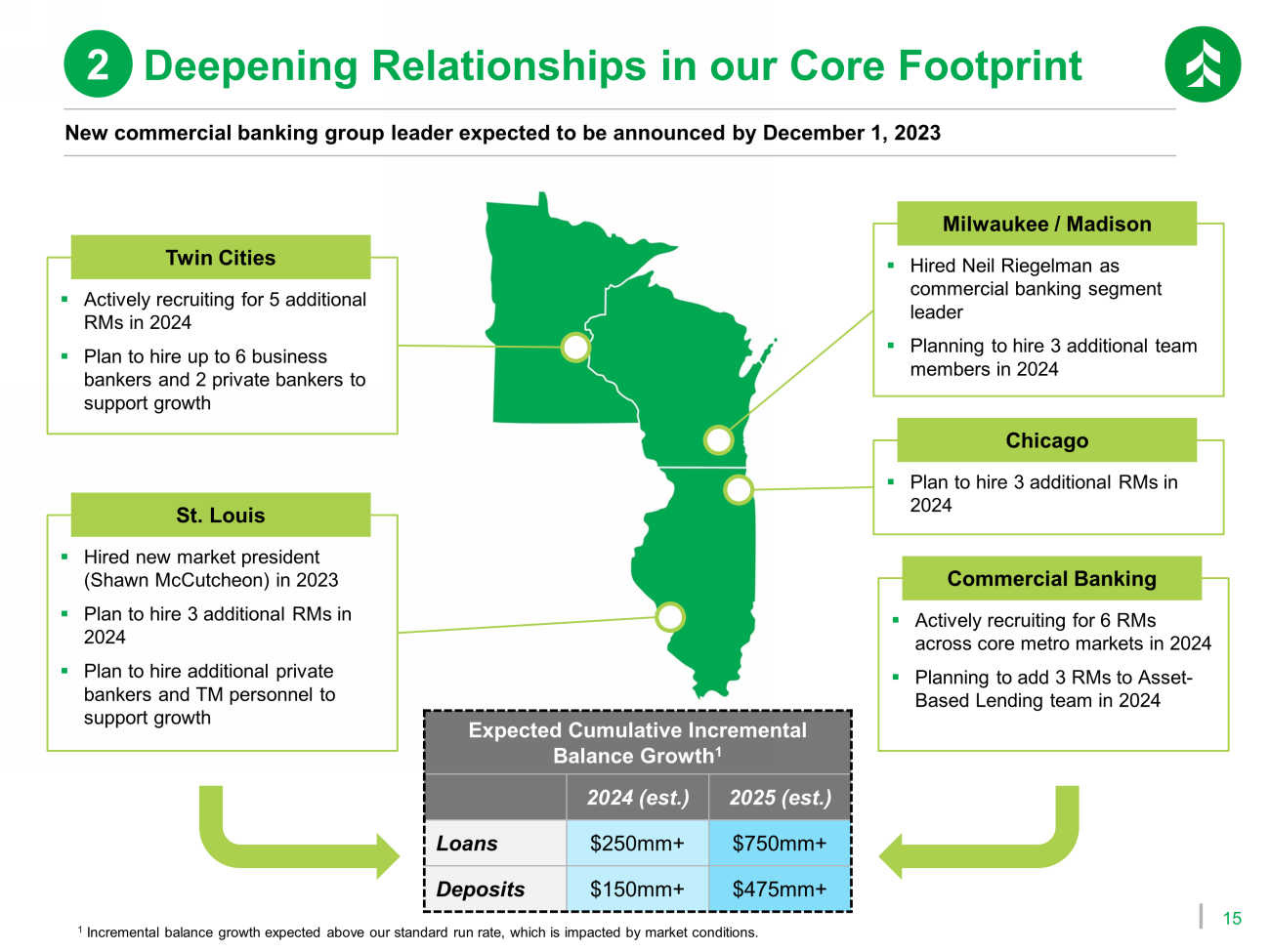

14 Attracting and retaining high - quality talent continues to be a key driver of our strategic plan Private Wealth Commercial Banking Business Banking ▪ Jayne Hladio joined the bank as president of private wealth ▪ With over 30 years of experience, Hladio is expected to play an influential role in advancing private wealth, mass affluent and digital strategies ▪ Neil Riegelman joined the bank as our commercial banking segment leader in Milwaukee and Madison ▪ With over 20 years of experience, Riegelman is expected to oversee relationship development ▪ Expect to hire 20+ commercial RMs across all markets by 2025, with four already hired ▪ New commercial banking group leader reporting to John Utz expected to be announced by December 1st ▪ Gus Hernandez transitioned to the role of SVP, director of business banking ▪ With over 35 years of experience, Hernandez brings a unique skillset bridging our retail, small business and commercial strategies Neil Riegelman Jayne Hladio Gus Hernandez Moves Already Made in 4Q 2023 Bolstering Talent in Key Areas 2 15 ▪ Actively recruiting for 6 RMs across core metro markets in 2024 ▪ Planning to add 3 RMs to Asset - Based Lending team in 2024 New commercial banking group leader expected to be announced by December 1, 2023 ▪ Hired Neil Riegelman as commercial banking segment leader ▪ Planning to hire 3 additional team members in 2024 Milwaukee / Madison ▪ Actively recruiting for 5 additional RMs in 2024 ▪ Plan to hire up to 6 business bankers and 2 private bankers to support growth Twin Cities ▪ Hired new market president (Shawn McCutcheon) in 2023 ▪ Plan to hire 3 additional RMs in 2024 ▪ Plan to hire additional private bankers and TM personnel to support growth St. Louis Commercial Banking Expected Cumulative Incremental Balance Growth 1 2024 (est.) 2025 (est.) Loans $250mm+ $750mm+ Deposits $150mm+ $475mm+ Deepening Relationships in our Core Footprint 2 ▪ Plan to hire 3 additional RMs in 2024 Chicago 1 Incremental balance growth expected above our standard run rate, which is impacted by market conditions.

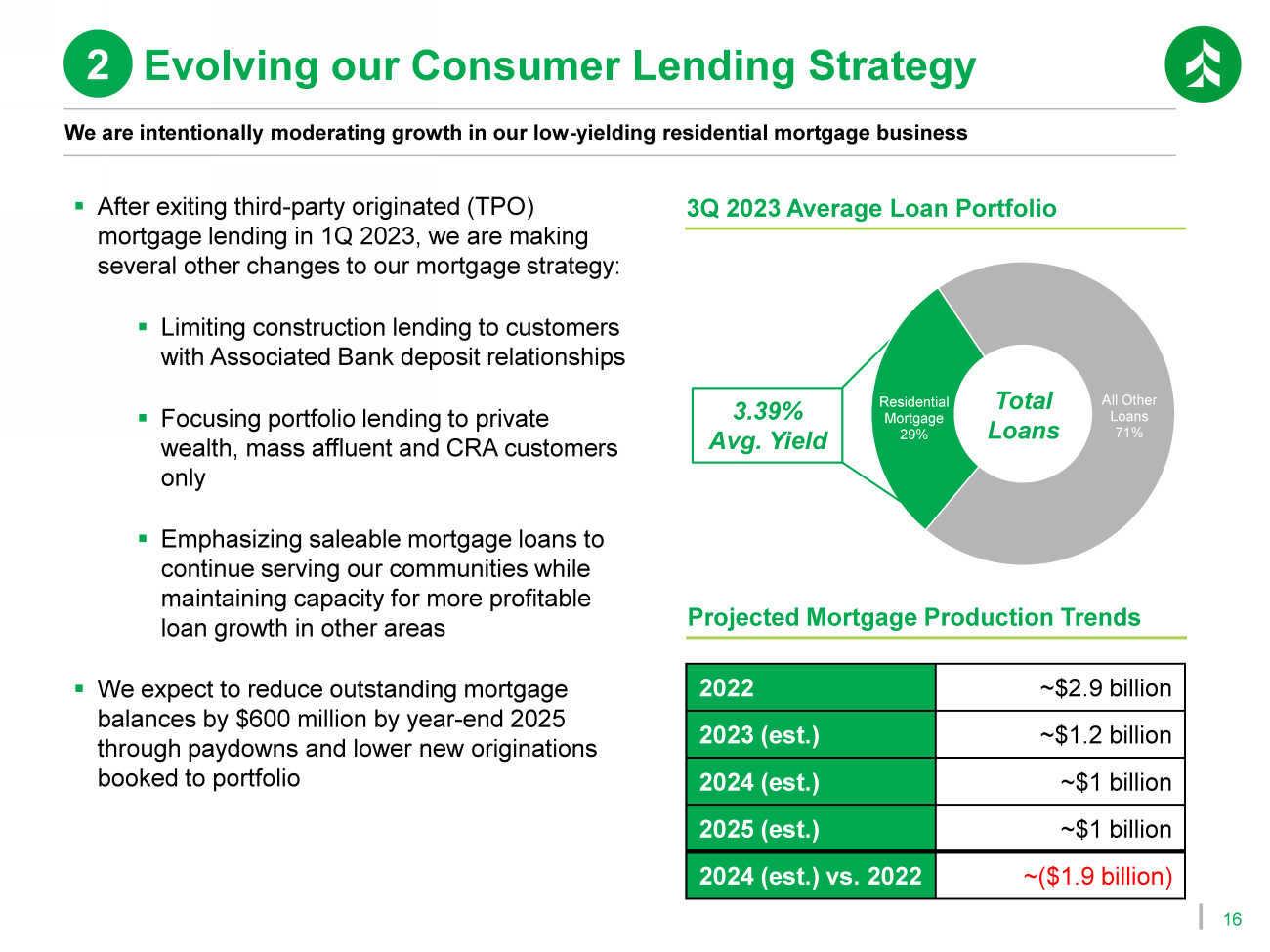

16 All Other Loans 71% Residential Mortgage 29% 0 Total Loans We are intentionally moderating growth in our low - yielding residential mortgage business Projected Mortgage Production Trends 2022 ~$2.9 billion 2023 (est.) ~$1.2 billion 2024 (est.) ~$1 billion 2025 (est.) ~$1 billion 2024 (est.) vs. 2022 ~($1.9 billion) 3Q 2023 Average Loan Portfolio ▪ After exiting third - party originated (TPO) mortgage lending in 1Q 2023, we are making several other changes to our mortgage strategy: ▪ Limiting construction lending to customers with Associated Bank deposit relationships ▪ Focusing portfolio lending to private wealth, mass affluent and CRA customers only ▪ Emphasizing saleable mortgage loans to continue serving our communities while maintaining capacity for more profitable loan growth in other areas ▪ We expect to reduce outstanding mortgage balances by $600 million by year - end 2025 through paydowns and lower new originations booked to portfolio 3.39% Avg.

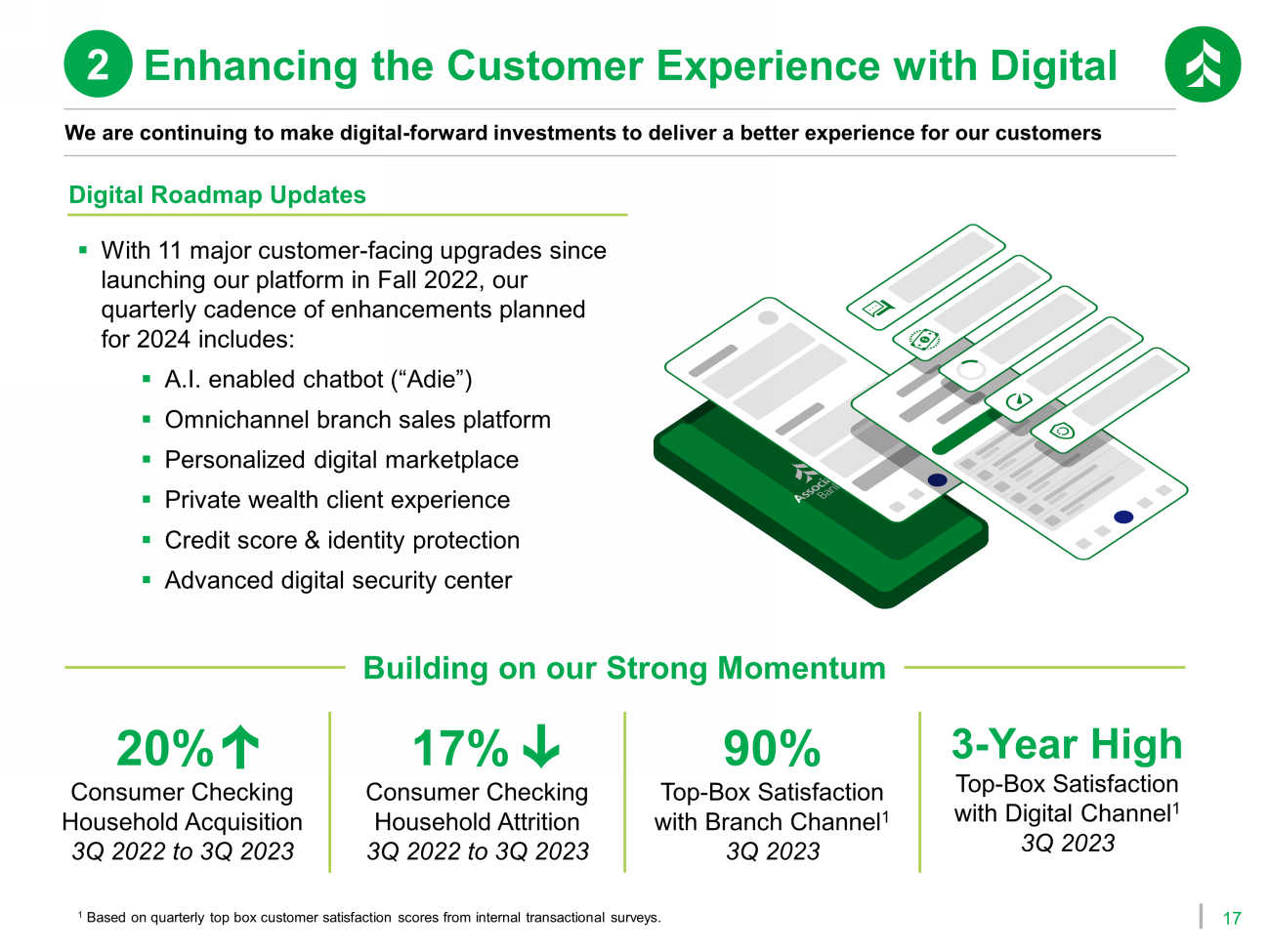

Yield Evolving our Consumer Lending Strategy 2 17 20% Consumer Checking Household Acquisition 3Q 2022 to 3Q 2023 17% Consumer Checking Household Attrition 3Q 2022 to 3Q 2023 90% Top - Box Satisfaction with Branch Channel 1 3Q 2023 3 - Year High Top - Box Satisfaction with Digital Channel 1 3Q 2023 We are continuing to make digital - forward investments to deliver a better experience for our customers 1 Based on quarterly top box customer satisfaction scores from internal transactional surveys. Building on our Strong Momentum ▪ With 11 major customer - facing upgrades since launching our platform in Fall 2022, our quarterly cadence of enhancements planned for 2024 includes: ▪ A.I.

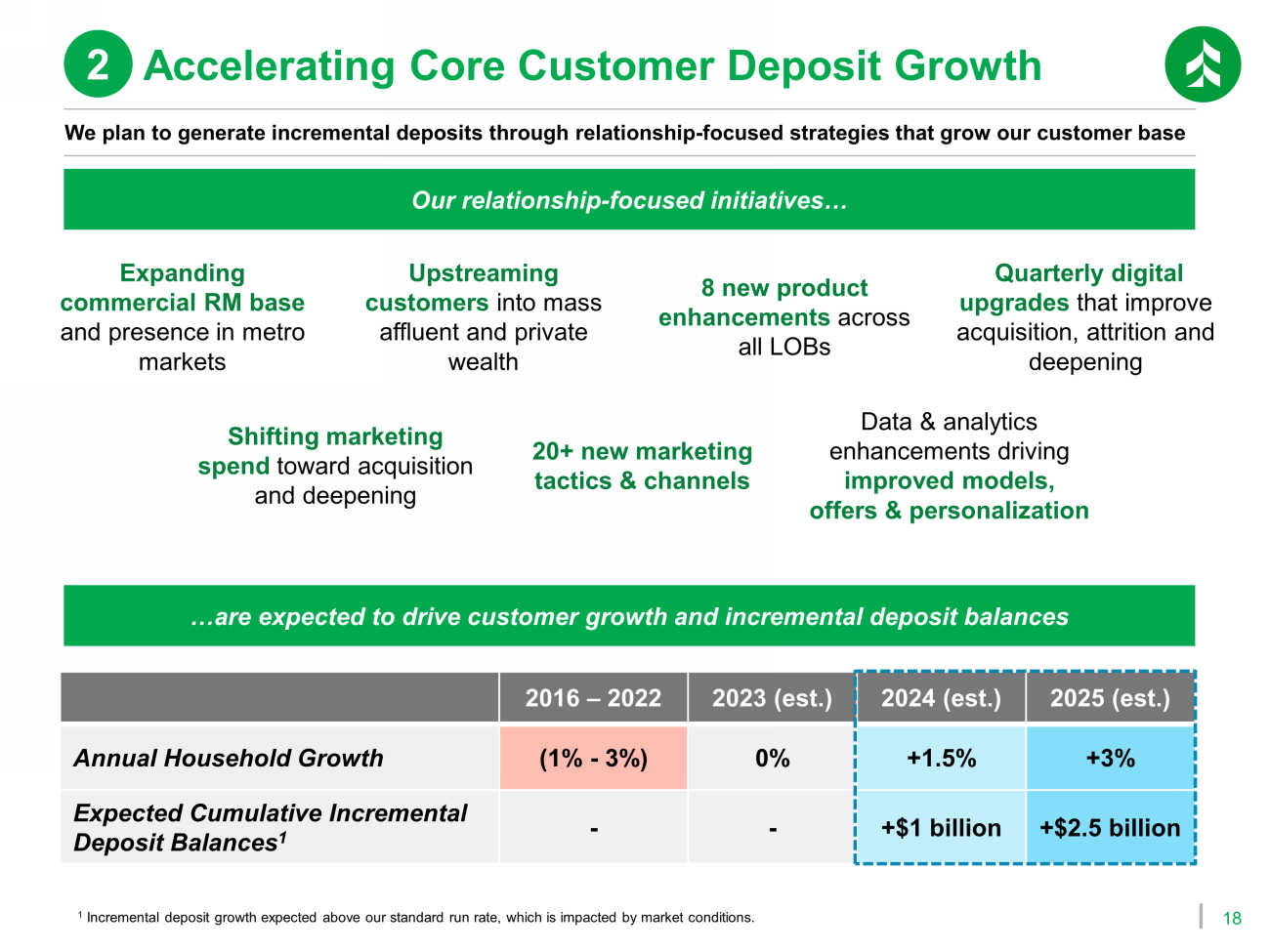

enabled chatbot (“Adie”) ▪ Omnichannel branch sales platform ▪ Personalized digital marketplace ▪ Private wealth client experience ▪ Credit score & identity protection ▪ Advanced digital security center Digital Roadmap Updates Enhancing the Customer Experience with Digital 2 18 We plan to generate incremental deposits through relationship - focused strategies that grow our customer base Expanding commercial RM base and presence in metro markets Upstreaming customers into mass affluent and private wealth 8 new product enhancements across all LOBs Our relationship - focused initiatives… …are expected to drive customer growth and incremental deposit balances Quarterly digital upgrades that improve acquisition, attrition and deepening Shifting marketing spend toward acquisition and deepening 20+ new marketing tactics & channels Data & analytics enhancements driving improved models, offers & personalization 2016 – 2022 2023 (est.) 2024 (est.) 2025 (est.) Annual Household Growth (1% - 3%) 0% +1.5% +3% Expected Cumulative Incremental Deposit Balances 1 - - +$1 billion +$2.5 billion Accelerating Core Customer Deposit Growth 2 1 Incremental deposit growth expected above our standard run rate, which is impacted by market conditions.

19 Our organic plan builds on our momentum while adhering to the foundational strengths that got us here Expected Benefits of Organic Plan Transitions our Balance Sheet into Higher Return Businesses Creates an Earnings Tailwind by Consistently Growing our Customer Base Maintains our Strong Foundation of Expense Discipline and Investment Decisioning Retains a Disciplined Credit Approach by Growing in Existing Businesses Funds our Balance Sheet ▪ Cumulative incremental deposit balance growth 1 of $2.5 billion by year - end 2025 ▪ Cumulative incremental commercial loan growth 1 of $750 million by year - end 2025 ▪ Reduction of $600 million in outstanding mortgage loans by year - end 2025 ▪ Run rate of 3% customer household growth by 2025 1 Incremental balance growth expected above our standard run rate, which is impacted by market conditions.

Balance Sheet Repositioning Transaction

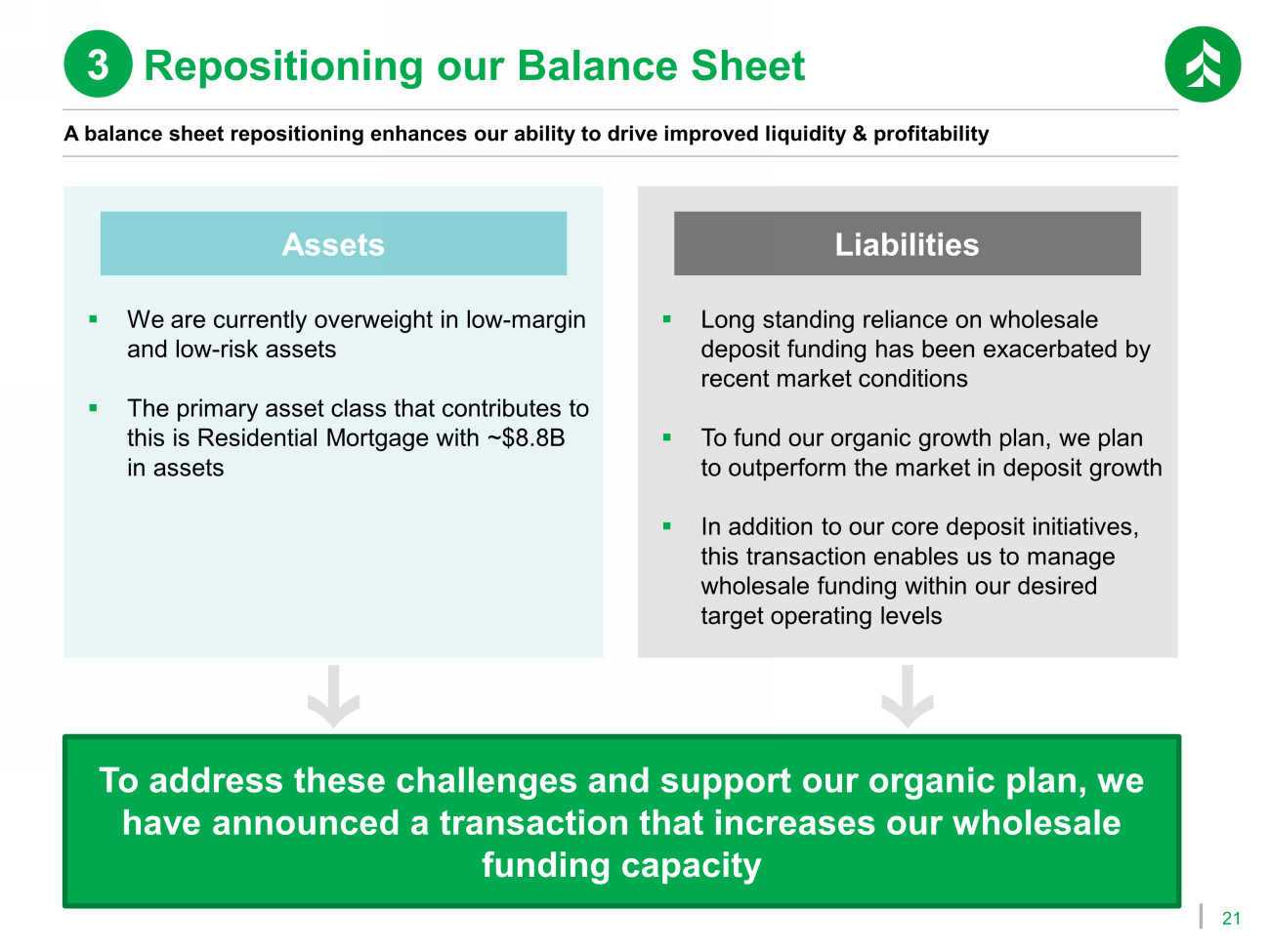

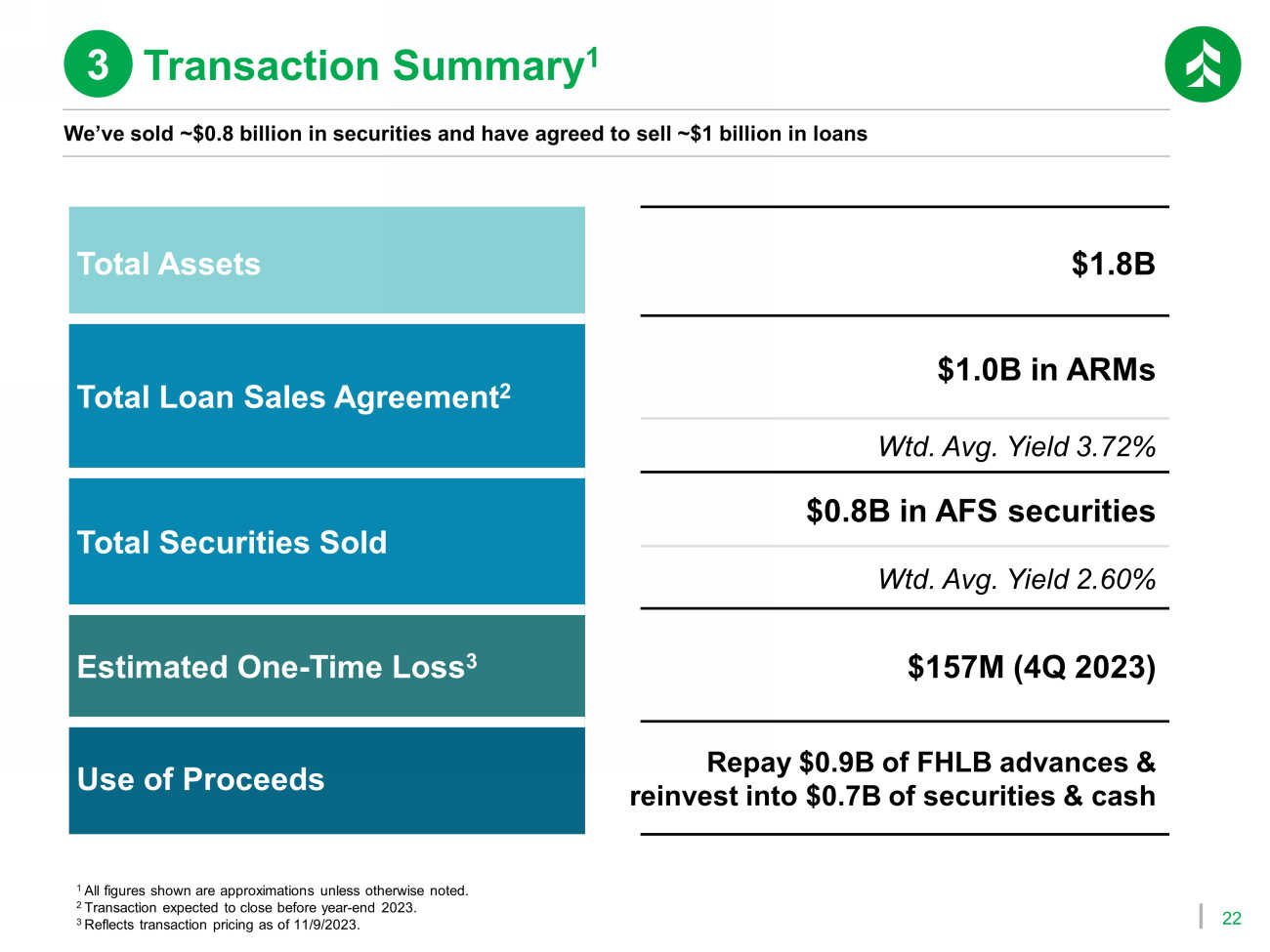

21 A balance sheet repositioning enhances our ability to drive improved liquidity & profitability ▪ We are currently overweight in low - margin and low - risk assets ▪ The primary asset class that contributes to this is Residential Mortgage with ~$8.8B in assets Assets ▪ Long standing reliance on wholesale deposit funding has been exacerbated by recent market conditions ▪ To fund our organic growth plan, we plan to outperform the market in deposit growth ▪ In addition to our core deposit initiatives, this transaction enables us to manage wholesale funding within our desired target operating levels Liabilities To address these challenges and support our organic plan, we have announced a transaction that increases our wholesale funding capacity Repositioning our Balance Sheet 3 22 1 All figures shown are approximations unless otherwise noted.

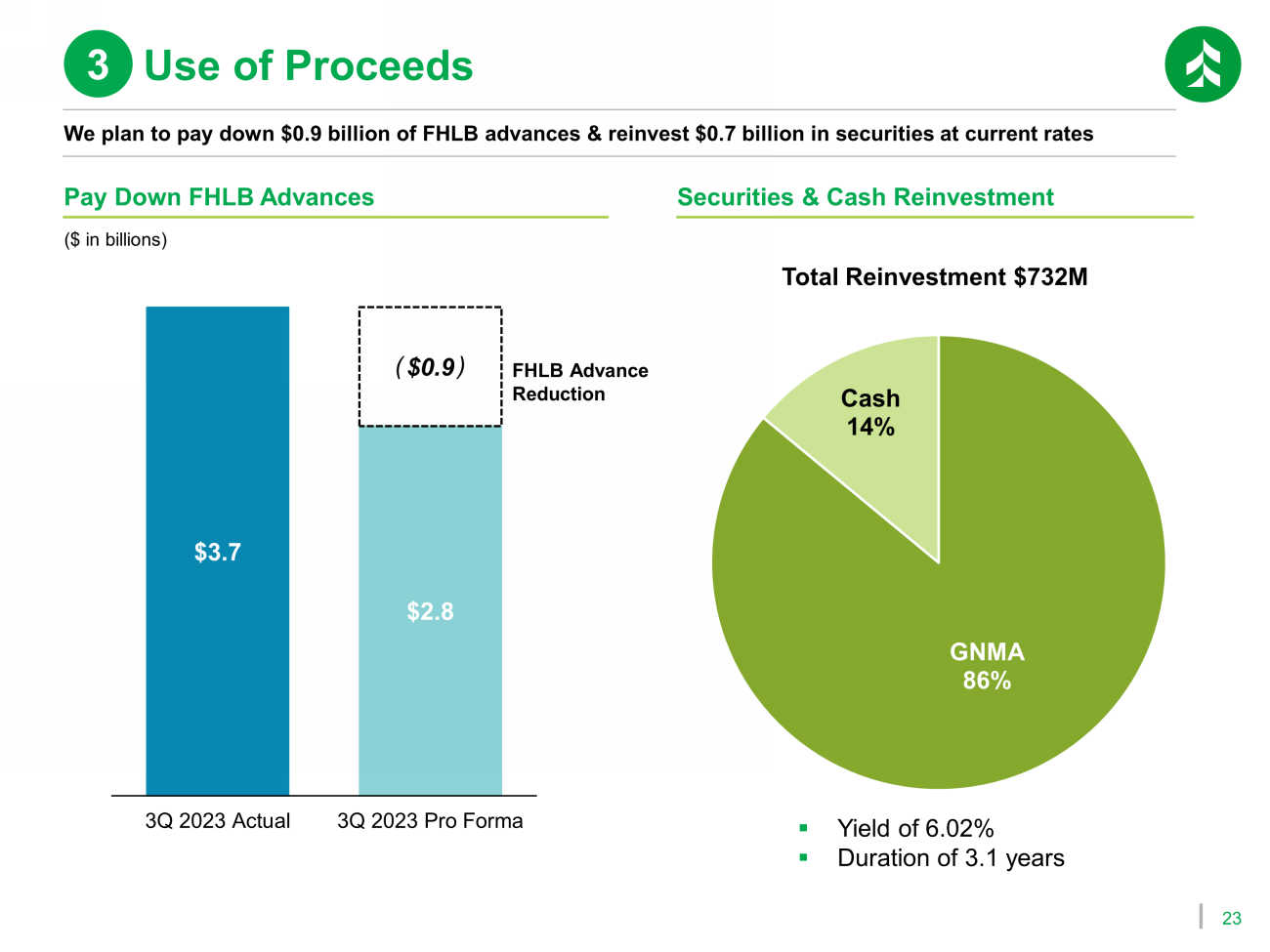

2 Transaction expected to close before year - end 2023. 3 Reflects transaction pricing as of 11/9/2023. We’ve sold ~$0.8 billion in securities and have agreed to sell ~$1 billion in loans Total Assets $1.8B Total Loan Sales Agreement 2 $1.0B in ARMs Wtd. Avg. Yield 3.72% Total Securities Sold $0.8B in AFS securities Wtd. Avg. Yield 2.60% Estimated One - Time Loss 3 $157M (4Q 2023) Use of Proceeds Repay $0.9B of FHLB advances & reinvest into $0.7B of securities & cash Transaction Summary 1 3 23 We plan to pay down $0.9 billion of FHLB advances & reinvest $0.7 billion in securities at current rates $3.7 $2.8 $0.9 3Q 2023 Actual 3Q 2023 Pro Forma FHLB Advance Reduction Pay Down FHLB Advances Securities & Cash Reinvestment GNMA 86% Cash 14% Total Reinvestment $732M ( ) ($ in billions) Use of Proceeds 3 ▪ Yield of 6.02% ▪ Duration of 3.1 years

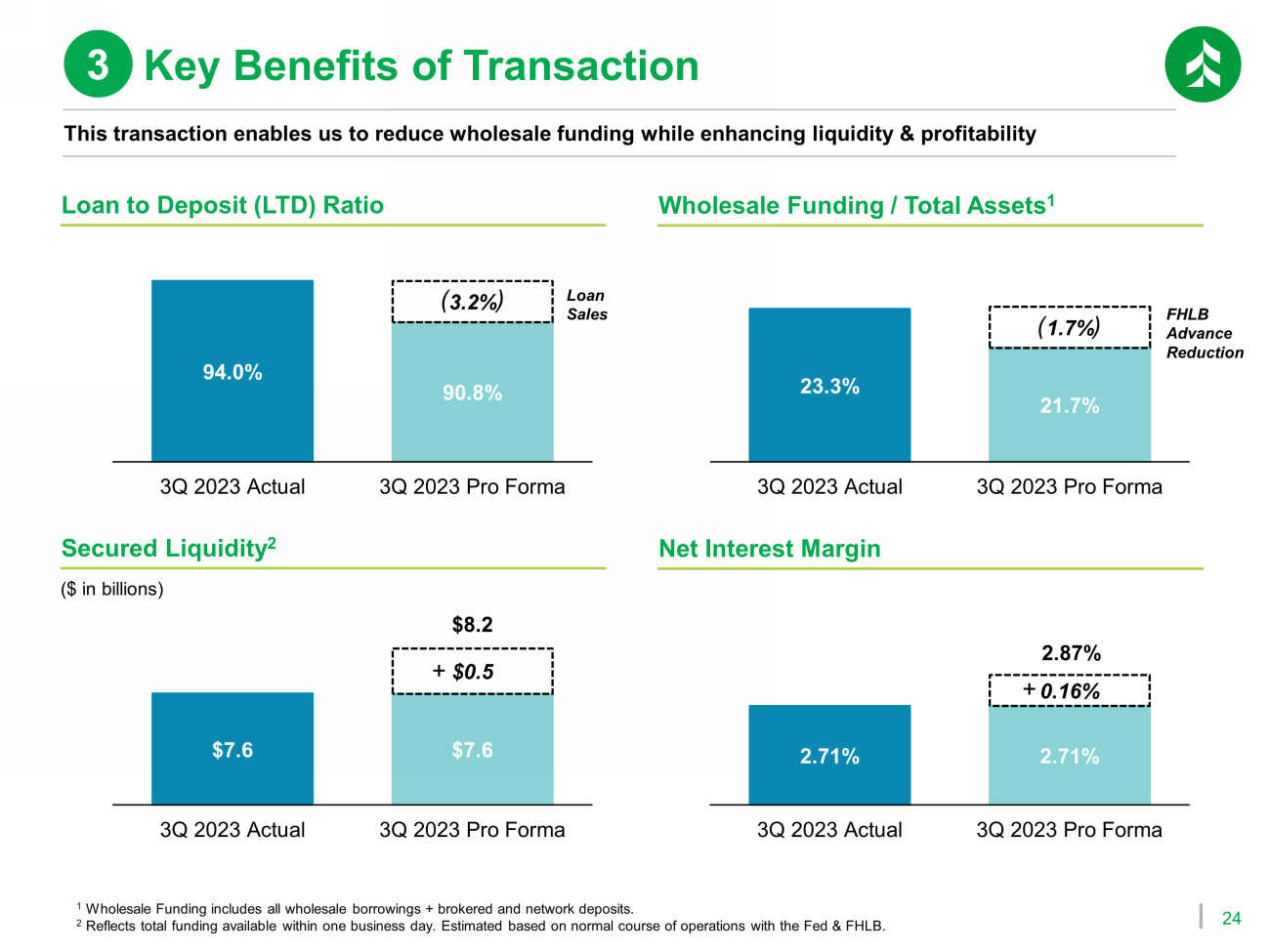

24 94.0% 90.8% 3.2% 3Q 2023 Actual 3Q 2023 Pro Forma 2.71% 2.71% 0.16% 2.87% 3Q 2023 Actual 3Q 2023 Pro Forma 1 Wholesale Funding includes all wholesale borrowings + brokered and network deposits. 2 Reflects total funding available within one business day. Estimated based on normal course of operations with the Fed & FHLB.

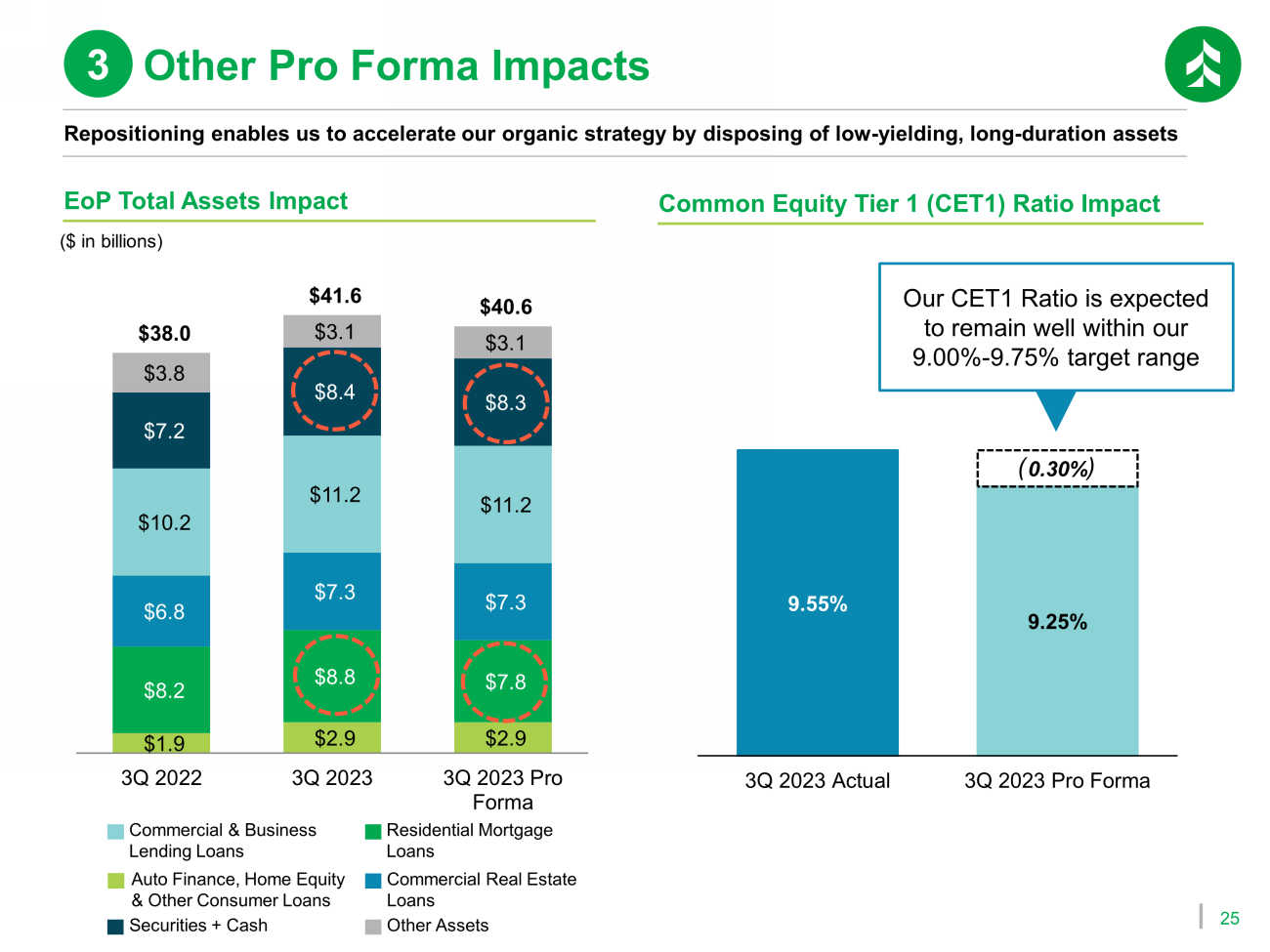

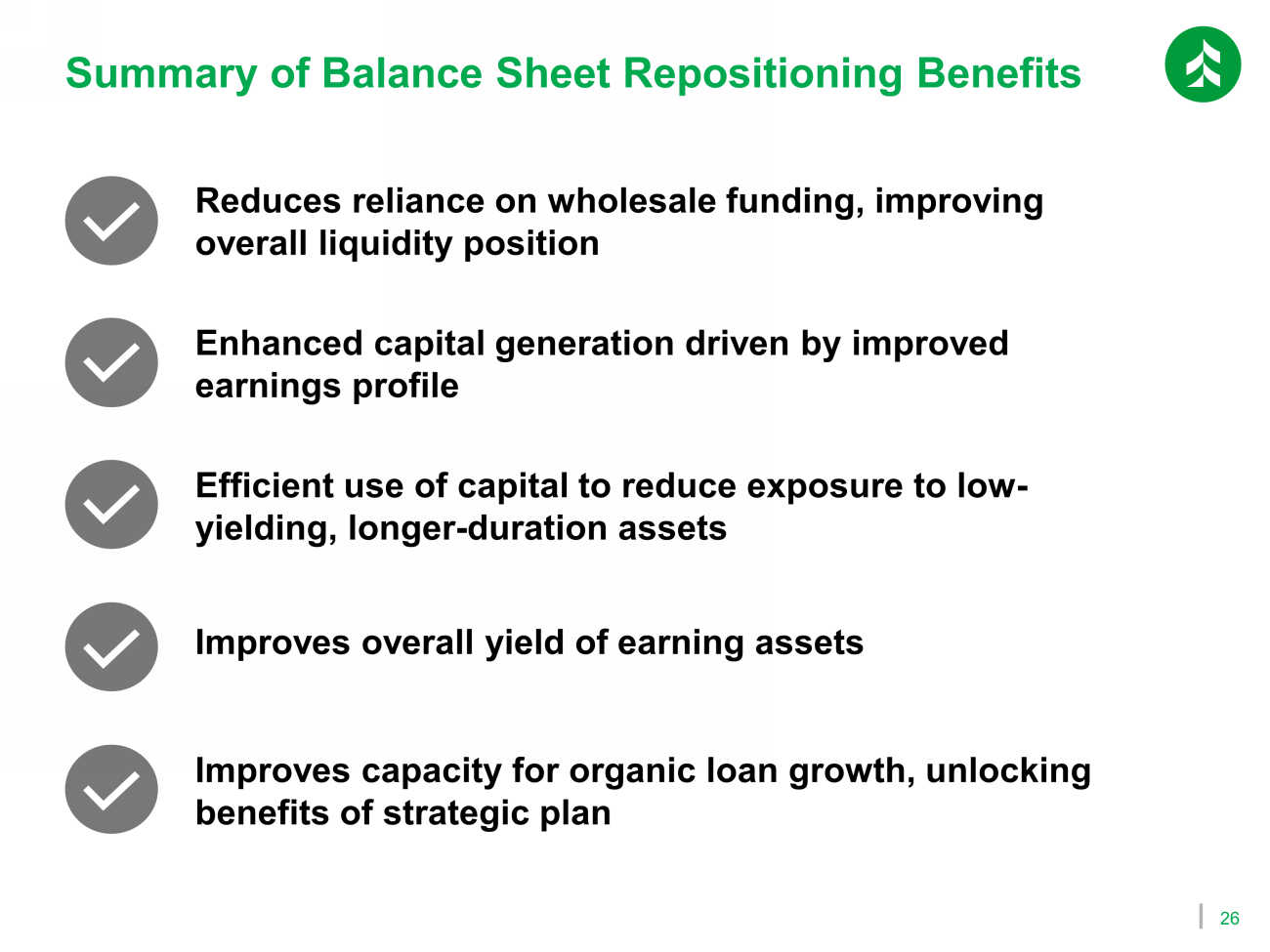

23.3% 21.7% 1.7% 3Q 2023 Actual 3Q 2023 Pro Forma Loan Sales Loan to Deposit (LTD) Ratio Wholesale Funding / Total Assets 1 FHLB Advance Reduction $7.6 $7.6 $0.5 $8.2 3Q 2023 Actual 3Q 2023 Pro Forma Secured Liquidity 2 Net Interest Margin ( ) ( ) + + ($ in billions) This transaction enables us to reduce wholesale funding while enhancing liquidity & profitability Key Benefits of Transaction 3 25 $1.9 $2.9 $2.9 $8.2 $8.8 $7.8 $6.8 $7.3 $7.3 $10.2 $11.2 $11.2 $7.2 $8.4 $8.3 $3.8 $3.1 $3.1 $38.0 $41.6 $40.6 3Q 2022 3Q 2023 3Q 2023 Pro Forma Repositioning enables us to accelerate our organic strategy by disposing of low - yielding, long - duration assets EoP Total Assets Impact ($ in billions) Commercial & Business Lending Loans Commercial Real Estate Loans Residential Mortgage Loans Auto Finance, Home Equity & Other Consumer Loans Other Assets Securities + Cash Other Pro Forma Impacts 3 Common Equity Tier 1 (CET1) Ratio Impact 9.55% 9.25% 0.30% 3Q 2023 Actual 3Q 2023 Pro Forma ( ) Our CET1 Ratio is expected to remain well within our 9.00% - 9.75% target range 26 Summary of Balance Sheet Repositioning Benefits Improves capacity for organic loan growth, unlocking benefits of strategic plan Reduces reliance on wholesale funding, improving overall liquidity position Enhanced capital generation driven by improved earnings profile Efficient use of capital to reduce exposure to low - yielding, longer - duration assets Improves overall yield of earning assets

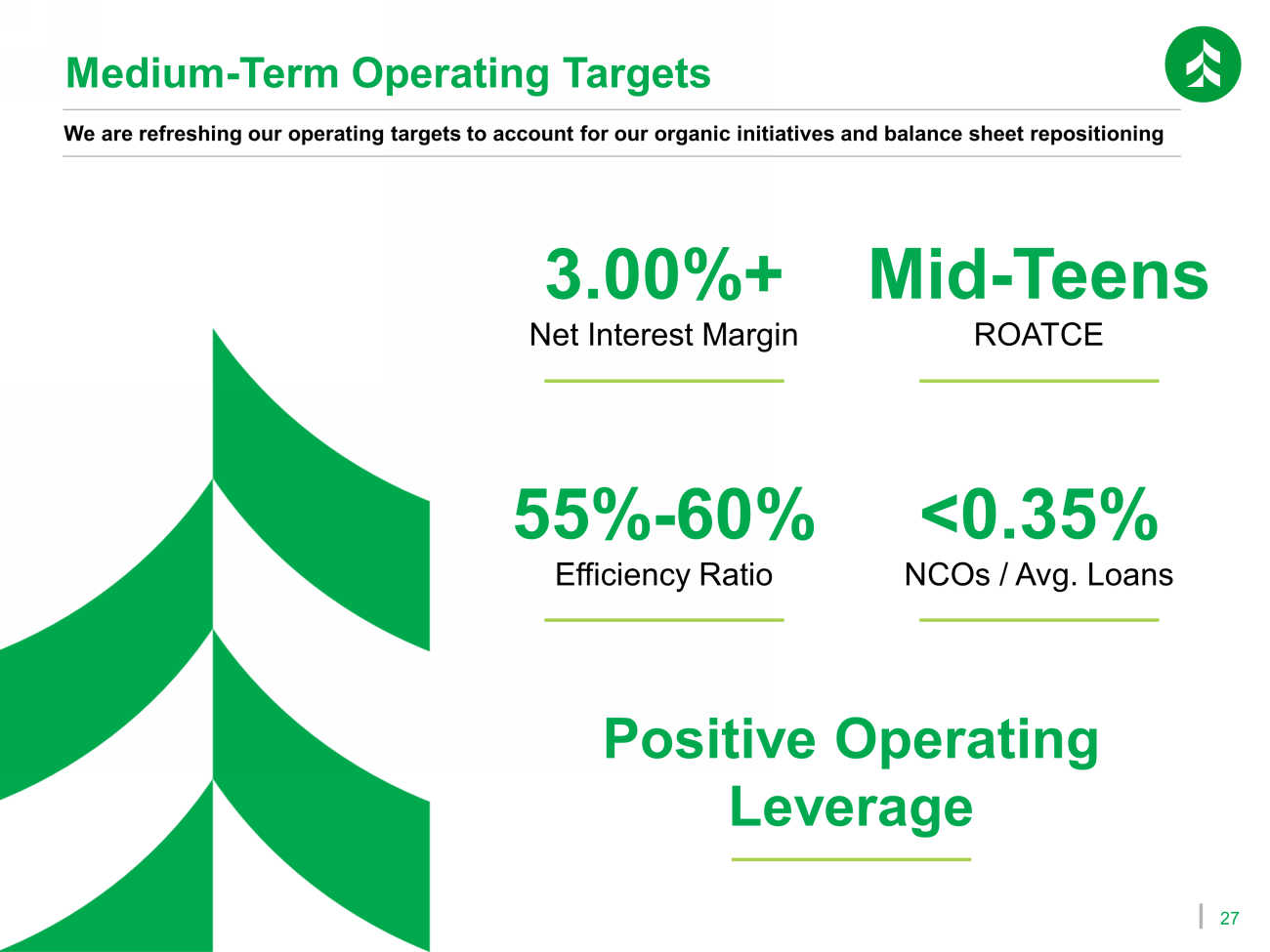

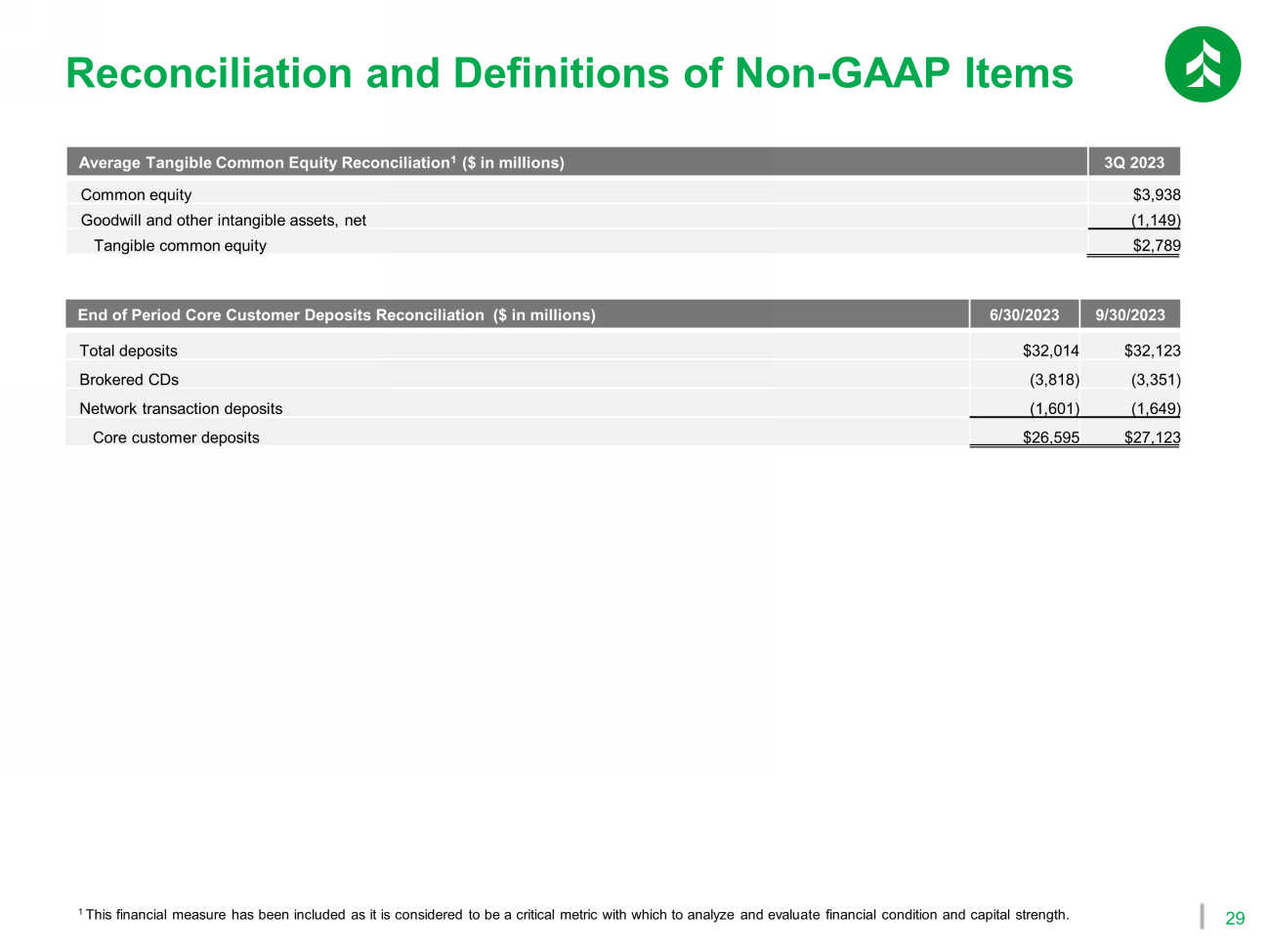

27 Medium - Term Operating Targets 3.00%+ Net Interest Margin Mid - Teens ROATCE 55% - 60% Efficiency Ratio <0.35% NCOs / Avg. Loans We are refreshing our operating targets to account for our organic initiatives and balance sheet repositioning Positive Operating Leverage 29 Reconciliation and Definitions of Non - GAAP Items 1 This financial measure has been included as it is considered to be a critical metric with which to analyze and evaluate finan cia l condition and capital strength.

Appendix

End of Period Core Customer Deposits Reconciliation ($ in millions) 6/30/2023 9/30/2023 Total deposits $32,014 $32,123 Brokered CDs (3,818) (3,351) Network transaction deposits (1,601) (1,649) Core customer deposits $26,595 $27,123 Average Tangible Common Equity Reconciliation 1 ($ in millions) 3Q 2023 Common equity $3,938 Goodwill and other intangible assets, net (1,149) Tangible common equity $2,789

Exhibit 99.2

News Release

Media Contact: Jennifer Kaminski

Vice President | Public Relations Senior Manager

920-491-7576 | Jennifer.Kaminski@AssociatedBank.com

Investor Contact: Ben McCarville

Vice President | Director of Investor Relations

920-491-7059 | Ben.McCarville@AssociatedBank.com

Associated Bank executing next phase of strategic plan

GREEN BAY, Wis. – November 9, 2023 – Associated Banc-Corp (NYSE: ASB) today announced plans for the next phase of the Company’s people-led, digitally enabled strategic plan. These plans include a series of investments in people, products and technology intended to grow and remix the loan portfolio, accelerate core customer deposit growth, and deliver a better banking experience for customers.

“Since launching the first phase of our strategic plan in 2021, we’ve steadily executed on our plans to drive high-quality loan growth, expand our deposit capabilities and transform the digital experience for our customers,” said President and CEO Andy Harmening. “These efforts have resulted in strong balance sheet expansion, and better positioned us to attract, deepen and retain customer relationships. While we continue to benefit from these initial efforts, we also plan to capitalize on our momentum through the next phase of our strategic plan. Already underway, this plan accelerates our efforts to attract and deepen relationships, enhance our return profile and drive improved shareholder returns over time. We look forward to sharing updates on our progress in 2024 and beyond.”

Bolstering Talent to Foster Relationships and Balance Sheet Growth

Associated today announced further investments in talent to sharpen the Company’s focus on relationships and drive incremental loan and deposit growth.

| · | The Company is expanding its commercial middle market team with plans to hire over 20 additional relationship managers in focus markets such as Milwaukee, Madison, Chicago, Twin Cities and St. Louis. |

o Neil Riegelman joined Associated in October as SVP, commercial banking segment leader. Riegelman brings more than 20 years of experience to Associated Bank. Having served in progressive commercial banking roles with BMO Harris Bank since 2005, he most recently held the position of managing director and team lead for commercial banking in Wisconsin. In his new role, Riegelman will oversee relationship development strategies in Milwaukee and Madison.

| o | Associated’s Gus Hernandez has been appointed to the role of SVP, director of business banking. In his new role, he is responsible for business banking sales, product management and credit functions across the Company’s major metropolitan markets, including Milwaukee, Madison, Chicago and the Twin Cities. With approximately 35 years of banking experience, Hernandez is well-positioned to bridge Associated’s retail, small business and commercial middle market strategies. He is also expected to lead the Company’s efforts to add business bankers across the footprint. |

| o | A new commercial banking group leader reporting to head of corporate banking John Utz is also expected to be announced by December 1, 2023. |

| · | Associated has also advanced its private wealth strategy by hiring Jayne Hladio as EVP, president of private wealth in October. A Midwest banking leader, Hladio brings more than 30 years of market expertise to Associated. After serving a 12-year career at U.S. Bank, ultimately leading as national wealth management executive across 26 states, she most recently served as President of Midland Wealth Management and Midland Trust Co. Hladio will play an influential role in advancing the Company’s private wealth and mass affluent strategies. |

| · | As the Company looks to broaden and grow its loan portfolio, Associated also announced several adjustments to the Company’s consumer lending strategy. These adjustments are expected to decrease reliance on low-yielding portfolio mortgage loans and maintain capacity for more profitable growth in other areas. Key strategic changes include: |

| o | Limiting construction lending to customers with Associated Bank deposit relationships |

| o | Reducing portfolio lending to private wealth, mass affluent and CRA customers only |

| o | Emphasizing the sale of conforming mortgage loans to continue fully serving our communities while maintaining capacity for more profitable loan growth in other areas |

Leveraging Talent, Products and Services to Drive Core Customer Deposit Growth

Following the successful launch of several deposit gathering initiatives over the past 24 months, the Company is focused on accelerating core customer deposit relationships to decrease reliance on higher-cost network and brokered funding sources. In addition to bolstering talent in key business units, the Company is leveraging customer feedback to deliver targeted product and service enhancements and supporting these efforts with customer acquisition-focused marketing and branding.

| · | The planned 20+ new commercial relationship managers will be focused on attracting and deepening whole customer relationships including loans, deposits, treasury management and other services. |

| · | Associated also plans to dedicate additional resources to grow the mass affluent segment, which is expected to attract and deepen high-value customer relationships and create upstream opportunities into private wealth. |

| · | To drive growth in consumer and small business households, Associated plans to release several key product enhancements including early pay, automated savings and credit score monitoring. These enhancements will be supported by the Company’s customer acquisition-focused brand strategy. |

Continued Execution on Associated’s Digital Roadmap

Following the successful launch of a new digital banking platform in September of 2022, Associated has leveraged agile delivery to execute 11 major customer-facing upgrades. This work has contributed to double-digit percentage increases in customer acquisition, double-digit percentage decreases in customer attrition, and multi-year highs in digital banking customer satisfaction. To build on this momentum, the Company has continued to make digital-forward investments and expects to deliver a quarterly cadence of feature and functionality upgrades. In 2024, planned initiatives include:

| · | An A.I. enabled chatbot, |

| · | An omnichannel branch sales platform, |

| · | A personalized digital marketplace, |

| · | Credit score and identity protection functionality, and |

| · | An enhanced digital banking experience for private wealth clients |

Funding Investments with Diligent Expense Control

In keeping with the Company’s strategy, a cross-functional team has reviewed Associated’s expense structure in partnership with a third-party consultant to identify cost saves and reinvest into the Company’s growth initiatives. Through these efforts, the Company has identified $25 million to $30 million in noninterest expense reductions for 2024. Expense reductions are primarily comprised of FTE reductions, branch consolidations and decreased discretionary spending. In connection with these expense reduction initiatives, the Company expects to incur a one-time charge of approximately $5 million in severance and other expenses in the fourth quarter of 2023.

After fully implementing these expense reductions and reinvestments, Associated’s noninterest expense is expected to grow by between 3% and 4% in both 2023 and 2024, excluding the one-time expenses anticipated in the fourth quarter of 2023.

Balance Sheet Repositioning

To accelerate the financial impacts of the Associated’s organic growth strategy, the Company also announced today a balance sheet repositioning transaction.

| · | Under the terms of the transaction, Associated Bank has sold approximately $0.8 billion of investment securities and has agreed to sell approximately $1 billion in mortgage loans, generally in single-product relationships. The sale of the mortgage loans is expected to close by year-end 2023. |

| · | The transaction is expected to result in an after-tax loss of approximately $157 million which will cause the Company to report a net loss for the fourth quarter of 2023. |

The transaction is expected to significantly increase Associated’s wholesale funding capacity by paying down FHLB advances and other high-cost funding, while also removing low-yielding assets from the books. The Company has also chosen to reinvest over $700 million into investment securities at current rates and cash.

Associated Bank management intends to provide additional details on its strategic plan and initiatives in a conference call for investors and analysts at 5:00 p.m. Central Time (CT) today, November 9, 2023. Interested parties can access the live webcast of the call through the Investor Relations section of the Company’s website, http://investor.associatedbank.com. Parties may also dial into the call at 877-407-8037 (domestic) or 201-689-8037 (international) and request the Associated Banc-Corp strategic update call. An accompanying slide presentation will be available on the Company’s website just prior to the call. An audio archive of the webcast will be available on the Company’s website approximately fifteen minutes after the call is over.

An investor presentation has been filed as a Form 8-K with the Securities and Exchange Commission and can be accessed via Associated Banc-Corp’s website at http://investor.associatedbank.com.

# # #

ABOUT ASSOCIATED BANC-CORP

Associated Banc-Corp (NYSE: ASB) has total assets of $42 billion and is the largest bank holding company based in Wisconsin. Headquartered in Green Bay, Wisconsin, Associated is a leading Midwest banking franchise, offering a full range of financial products and services from more than 200 banking locations serving more than 100 communities throughout Wisconsin, Illinois and Minnesota. The Company also operates loan production offices in Indiana, Michigan, Missouri, New York, Ohio and Texas. Associated Bank, N.A. is an Equal Housing Lender, Equal Opportunity Lender and Member FDIC. More information about Associated Banc-Corp is available at www.associatedbank.com.

FORWARD-LOOKING STATEMENTS

Statements made in this document which are not purely historical are forward-looking statements, as defined in the Private Securities Litigation Reform Act of 1995. This includes any statements regarding management’s plans, objectives, or goals for future operations, products or services, and forecasts of its revenues, earnings, or other measures of performance. Such forward-looking statements may be identified by the use of words such as “believe,” “expect,” “anticipate,” “plan,” “estimate,” “should,” “will,” “intend,” “target,” “outlook,” “project,” “guidance,” or similar expressions. Forward-looking statements are based on current management expectations and, by their nature, are subject to risks and uncertainties. Actual results may differ materially from those contained in the forward-looking statements. Factors which may cause actual results to differ materially from those contained in such forward-looking statements include those identified in the Company’s most recent Form 10-K and subsequent SEC filings. Such factors are incorporated herein by reference.