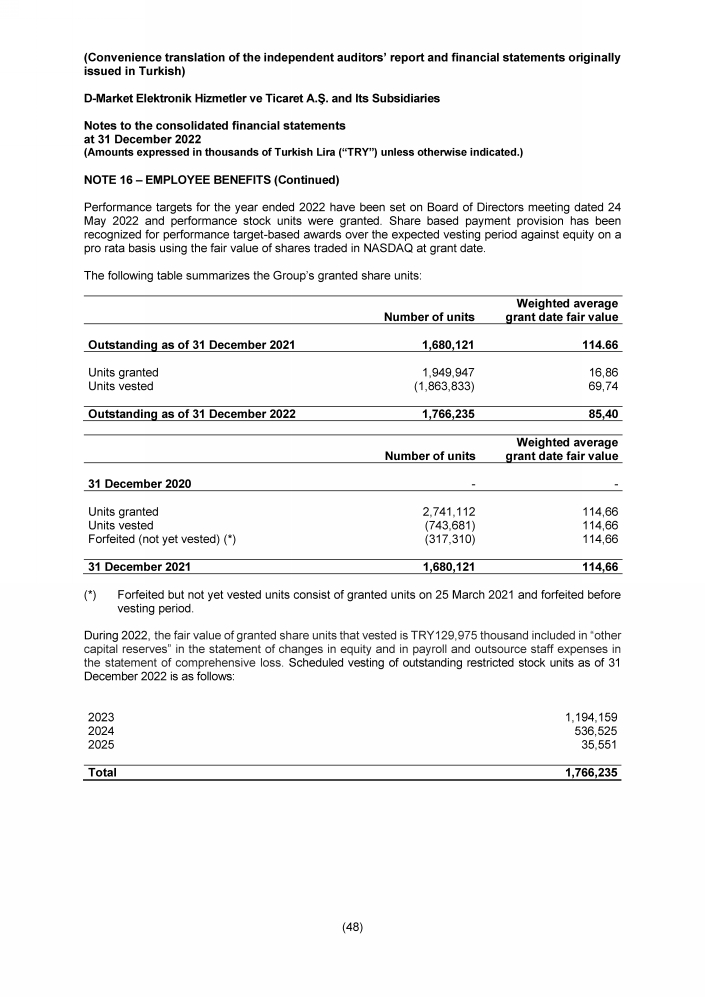

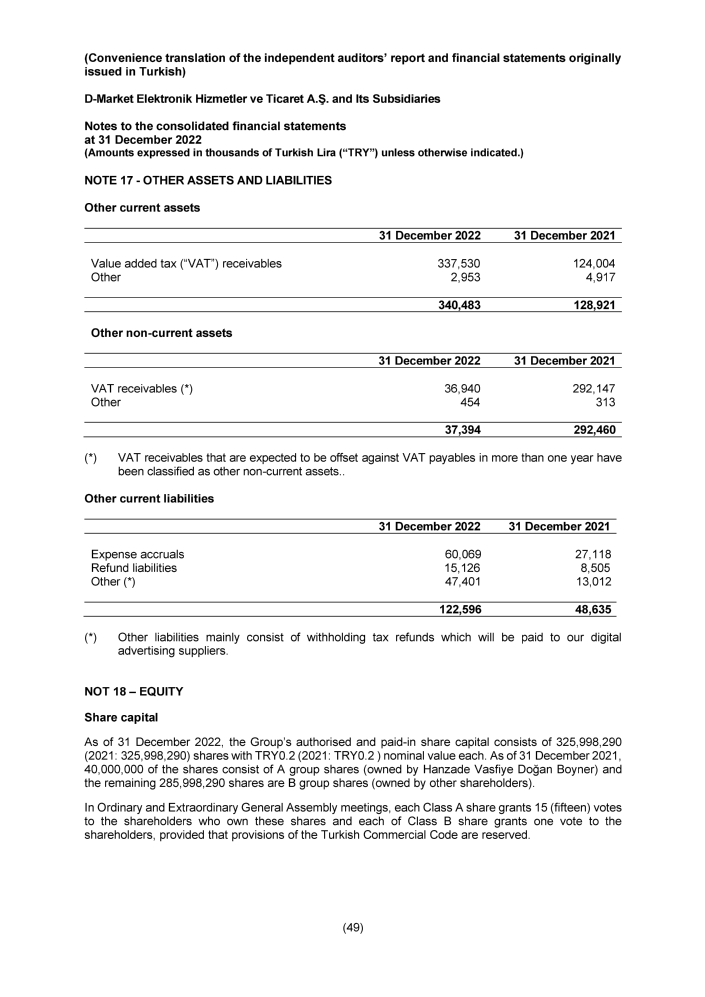

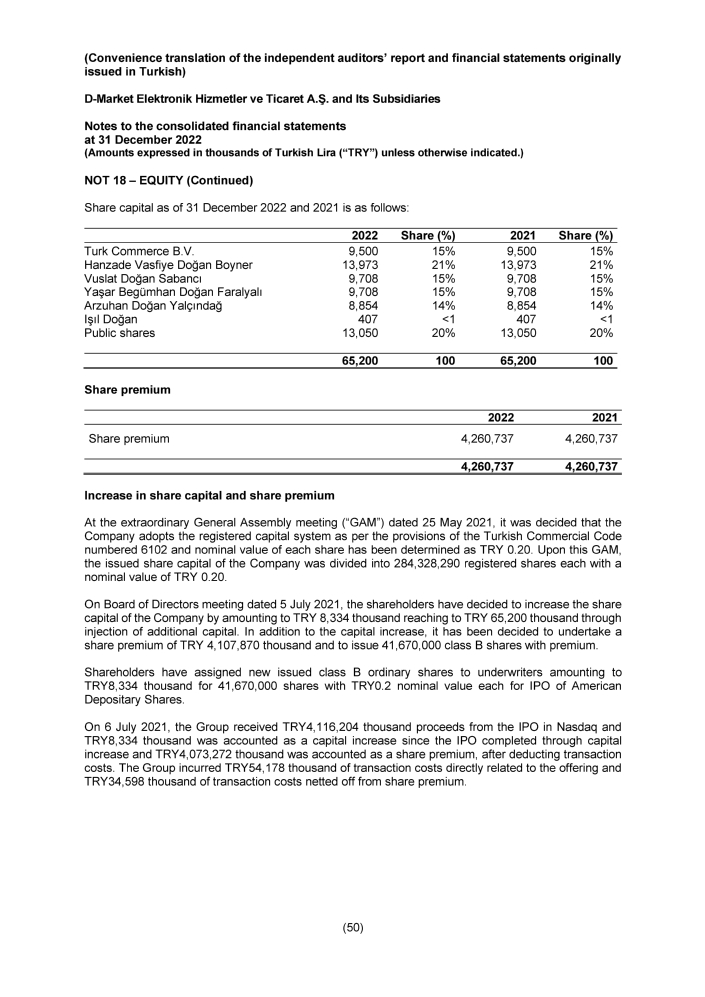

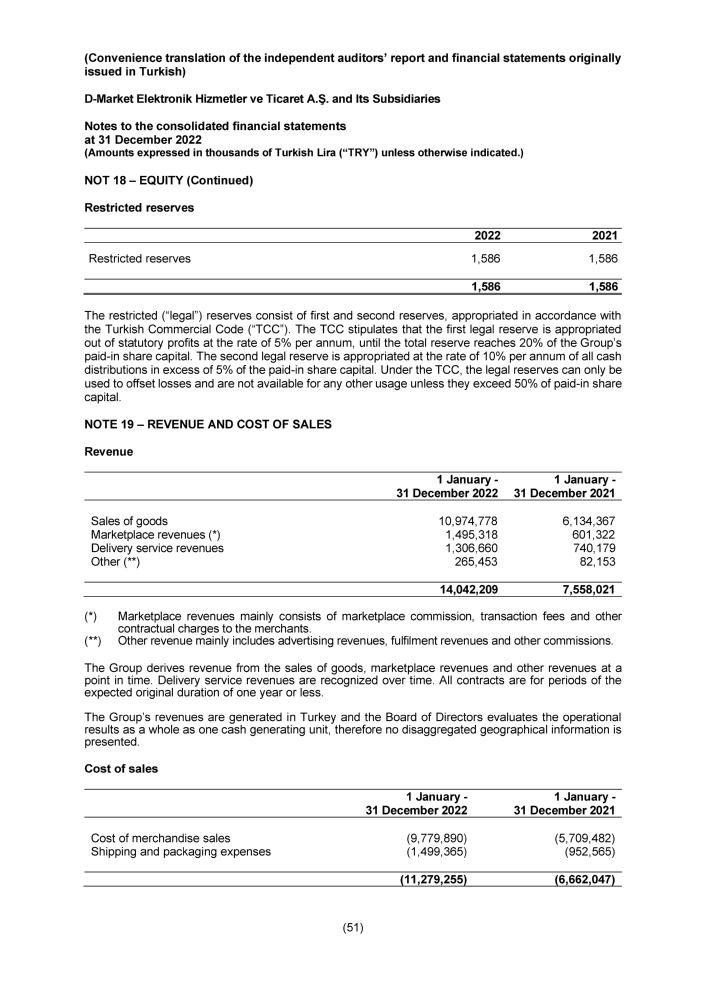

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

Date of Report: July 27, 2023

Commission File Number: 001-40553

D-MARKET Elektronik Hizmetler ve Ticaret Anonim Şirketi

(Exact Name of registrant as specified in its charter)

D-MARKET

Electronic Services & Trading

(Translation of Registrant‘s Name into English)

Kuştepe Mahallesi Mecidiyeköy Yolu

Cad. no: 12 Kule 2 K2

Şişli-Istanbul, Türkiye

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F x Form 40-F ¨

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| D-MARKET ELECTRONIC SERVICES & TRADING | ||

| July 27, 2023 | By: | /s/ NİLHAN GÖKÇETEKİN |

| Name: | Nilhan Gökçetekin | |

| Title: | Chief Executive Officer | |

| By: | /s/ H. KORHAN ÖZ | |

| Name: | H. Korhan Öz | |

| Title: | Chief Financial Officer |

EXHIBITS

Exhibit 99.1

Hepsiburada Announces 2022 Annual General Assembly

ISTANBUL, July 27, 2023 - D-MARKET Electronic Services & Trading (d/b/a “Hepsiburada”) (NASDAQ: HEPS) (the “Company”), a leading Turkish e-commerce platform, will hold its 2022 Annual General Assembly on Friday, August 25, 2023 at 11:00 İstanbul time at the Company’s headquarters at Kuştepe Mahallesi, Mecidiyeköy Yolu Caddesi, No:12 Trump Towers Kule:2 Şişli, İstanbul.

Holders of the Company’s American Depositary Shares (the “ADSs”) who wish to exercise their voting rights for the underlying shares must act through the depositary of the Company’s ADS program, The Bank of New York Mellon.

The agenda of the Annual General Assembly consists of the following items in accordance with the relevant provisions of the Turkish Commercial Code (the “TCC”) and the Regulation on Principles and Procedures for General Assembly Meetings of Joint Stock Companies and Ministry Representatives in Such Meetings (the “Regulation”) governing the agenda of ordinary general assembly meetings:

| 1. | Opening of the meeting and election of the General Assembly Meeting Chairmanship; |

| 2. | Authorization of the General Assembly Meeting Chairmanship to sign the minutes of the meeting; |

| 3. | Reading and discussion of the Board of Director’s annual report for 2022 and reading of the independent auditor’s report, as stipulated in the Regulation on Principles and Procedures for General Assembly Meetings of Joint Stock Companies and Ministry Representatives to be Present at These Meetings (the “Regulation”); |

| 4. | Reading, discussion, and ratification of the financial statements for the 2022 accounting period, as specified in the Regulation; |

| 5. | Release of the members of the Board of Directors for all their respective business, transactions and activities for the 2022 accounting period, as specified in the Regulation; |

| 6. | Decision on the Company’s profit for the 2022 accounting period, the use of the profit, the proportions of the profit and earnings shares to be distributed, as specified in the Regulation; |

| 7. | Decision on the salary, honorarium, bonus, and premium to be paid to the members of the Board of Directors in their capacity as such and, as applicable, in their capacity as members of committees for the year 2023 under Article 394 of the TCC and the Regulation; |

| 8. | Approval of the appointment of Mr. Stefan Gross-Selbeck, who was appointed by the Board of Directors pursuant to Article 363 of the TCC as an independent member of the Board of Directors to fill a seat vacated due to the resignation of Mr. Cemal Ahmet Bozer, as specified in the TCC and the Regulation; |

| 9. | Appointment of the members of the Board of Directors and determination of their terms of office; |

| 10. | Appointment of the independent auditor for the 2023 accounting period, as specified in the Regulation; |

| 11. | Consent of members of the Board of Directors for the commercial activities and transactions referred to in Article 395 and Article 396 of the TCC; |

| 12. | Approval of the renewal of the directors’ and officers’ insurance policy; |

| 13. | Determination of the upper limit for the aid and donations to be made until the next Ordinary General Assembly meeting of the Company as 2 per thousands of the total net assets of the Company and approval of the authorization of the Board of Directors within this context; |

| 14. | Approval of the granting of Company’s Class B shares that can be represented by ADSs (American Depositary Shares) within the scope of the Incentive Plan (HAPP), the main framework and conditions of which were established under the decision of the Company’s Board of Directors dated 24 March 2021 and numbered 2021/13, to senior executives, key employees, consultants, managers and members of the Board of Directors, as determined by the resolution of the Board of Directors dated 27 February 2023 and numbered 2023/03; |

| 15. | Approval of the Revised Incentive Plan under which shares may be granted to senior executives, key employees, consultants, managers and members of the Board of Directors as set forth in the resolution of the Board of Directors dated 24 April 2023 and numbered 2023/10; |

| 16. | Determining the procedures and principles of the authorization to the Board of Directors to repurchase a portion of the Company’s ADSs traded on Nasdaq, pursuant to the applicable laws of the United States by complying with the requirements and limitations in applicable law, for the purpose of granting shares of the Company that can be represented by ADS to those senior executives, key employees, consultants, managers and members of the Board of Directors, within the scope of the Revised Incentive Plan approved with the decision of the Board of Directors dated 24 April 2023 and numbered 2023/10; |

| 17. | Determination of the procedures and principles of the authorization to be given to the members of the Board of Directors for the repurchase of ADSs representing Class B shares of the Company from the publicly traded portion, as specified in Article 16 of the Agenda above, in accordance with the provisions of Article 379 et seq. of the TCC; |

| 18. | Approval of the Remuneration Policy for the members of the Board of Directors and managers of the Company; |

| 19. | Closing. |

Explanatory notes on the agenda items along with the copies of certain materials related to the Annual General Assembly will be made available on the Company’s investor relations website https://investors.hepsiburada.com/ as of July 27, 2023.

About Hepsiburada

Hepsiburada is a leading e-commerce technology platform in Türkiye, connecting over 57 million members with approximately 180 million stock keeping units across over 30 product categories. Hepsiburada provides goods and services through its hybrid model combining first-party direct sales (1P model) and a third-party marketplace (3P model) with over 100,000 merchants.

With its vision of leading the digitalization of commerce, Hepsiburada acts as a reliable, innovative and purpose-led companion in consumers’ daily lives. Hepsiburada’s e-commerce platform provides a broad ecosystem of capabilities for merchants and consumers including: last-mile delivery and fulfilment services, advertising services, on-demand grocery delivery services, and payment solutions offered through Hepsipay, Hepsiburada’s payment companion and Buy-Now-Pay-Later solutions provider. HepsiGlobal offers a selection from international merchants through its inbound arm while outbound operations aim to enable merchants in Türkiye to make cross-border sales.

Since its founding in 2000, Hepsiburada has been purpose-led, leveraging its digital capabilities to develop the role of women in the Turkish economy. Hepsiburada started the “Technology Empowerment for Women Entrepreneurs” programme in 2017, which has supported over 43,000 female entrepreneurs throughout Türkiye to reach millions of customers with their products.

Investor Relations Contact

ir@hepsiburada.com

Media Contact

corporatecommunications@hepsiburada.com

Exhibit 99.2

Annual General Meeting of Shareholders of D-Market Electronic Services & Trading Date: August 25, 2023 See Voting Instruction On Reverse Side. Please make your marks like this: Use pen only Please refer below and to the other side of the card for a description of the matters submitted to the Annual Shareholders’ Meeting of August 25, 2023 Agenda: 1. Opening of the meeting and election of the General Assembly Meeting Chairmanship, 2. Authorization of the General Assembly Meeting Chairmanship to sign the minutes of the meeting, 3. Reading and discussion of the Board of Director’s annual report for 2022 and reading of the independent auditor’s report, as stipulated in the Regulation on Principles and Procedures for General Assembly Meetings of Joint Stock Companies and Ministry Representatives to be Present at These Meetings (the “Regulation”), 4. Reading, discussion, and ratification of the financial statements for the 2022 accounting period, as specified in the Regulation, 5. Release of the members of the Board of Directors for all their respective business, transactions and activities for the 2022 accounting period, as specified in the Regulation, 6. Decision on the Company’s profit for the 2022 accounting period, the use of the profit, the proportions of the profit and earnings shares to be distributed, as specified in the Regulation, 7. Decision on the salary, honorarium, bonus, and premium to be paid to the members of the Board of Directors in their capacity as such and, as applicable, in their capacity as members of committees for the year 2023 under Article 394 of the TCC and the Regulation, 8. Approval of the appointment of Mr. Stefan Gross-Selbeck, who was appointed by the Board of Directors pursuant to Article 363 of the TCC as an independent member of the Board of Directors to fill a seat vacated due to the resignation of Mr. Cemal Ahmet Bozer, as specified in the TCC and the Regulation, 9. Appointment of the members of the Board of Directors and determination of their terms of office, 10. Appointment of the independent auditor for the 2023 accounting period, as specified in the Regulation, 11. Consent of members of the Board of Directors for the commercial activities and transactions referred to in Article 395 and Article 396 of the TCC, 12. Approval of the renewal of the directors and officers’ insurance policy, 13. Determination of the upper limit for the aid and donations to be made until the next Ordinary General Assembly meeting of the Company as 2 per thousands of the total net assets of the Company and approval of the authorization of the Board of Directors within this context, 14. Approval of the granting of Company’s Class B shares that can be represented by ADSs (American Depositary Shares) within the scope of the Incentive Plan (HAPP), the main framework and conditions of which were established under the decision of the Company’s Board of Directors dated 24 March 2021 and numbered 2021/13, to senior executives, key employees, consultants, managers and members of the Board of Directors, as determined by the resolution of the Board of Directors dated 27 February 2023 and numbered 2023/03, 15. Approval of the Revised Incentive Plan under which shares may be granted to senior executives, key employees, consultants, managers and members of the Board of Directors as set forth in the resolution of the Board of Directors dated 24 April 2023 and numbered 2023/10, 16. Determining the procedures and principles of the authorization to the Board of Directors to repurchase a portion of the Company’s ADSs traded on Nasdaq, pursuant to the applicable laws of the United States by complying with the requirements and limitations in applicable law, for the purpose of granting shares of the Company that can be represented by ADS to those senior executives, key employees, consultants, managers and members of the Board of Directors, within the scope of the Revised Incentive Plan approved with the decision of the Board of Directors dated 24 April 2023 and numbered 2023/10, 17. Determination of the procedures and principles of the authorization to be given to the members of the Board of Directors for the repurchase of ADSs representing Class B shares of the Company from the publicly traded portion, as specified in Article 16 of the Agenda above, in accordance with the provisions of Article 379 et seq. of the TCC, 18. Approval of the Remuneration Policy for the members of the Board of Directors and managers of the Company, 19. Closing.Authorized Signatures - This section must be completed for your instructions to be executed.For AgainstAnnual General Meeting of Shareholders of D-Market Electronic Services & Trading to be held August 25, 2023 For Holders as of July 26, 2023MAIL • Mark, sign and date your Voting Instruction Form. • Detach your Voting Instruction Form. • Return your Voting Instruction Form in the postage-paid envelope provided.All votes must be received prior to 12:00 p.m. (NY City Time) on August 18, 2023.PROXY TABULATOR FOR D-MARKET ELECTRONIC SERVICES & TRADING P.O. BOX 8016 CARY, NC 27512-9903EVENT # CLIENT #Please Sign Here Please Date AbovePlease Sign Here Please Date AboveCopyright © 2023 Mediant Communications Inc. All Rights Reserved

D-Market Electronic Services & Trading Instructions to The Bank of New York Mellon, as Depositary (Must be received prior to 12:00 p.m. (NY City Time) on August 18, 2023) The undersigned registered holder of American Depositary Receipts hereby requests and instructs The Bank of New York Mellon, as Depositary, to endeavor, in so far as practicable, to vote or cause to be voted the amount of shares or other Deposited Securities represented by such Receipt of D-Market Electronic Services & Trading registered in the name of the undersigned on the books of the Depositary as of the close of business July 26, 2023 at the Annual General Meeting of D-Market Electronic Services & Trading to be held on August 25, 2023 in Istanbul. NOTES: 1. Please direct the Depositary how it is to vote by placing X in the appropriate box opposite the resolution.(Continued and to be marked, dated and signed, on the other side)

Exhibit 99.3

D-MARKET ELEKTRONİK HİZMETLER VE TİCARET A.Ş.

(D-MARKET ELECTRONIC SERVICES AND TRADING)

EXPLANATORY NOTES ON THE AGENDA AND

INFORMATION ABOUT THE ANNUAL GENERAL

ASSEMBLY OF THE SHAREHOLDERS OF D-MARKET

TO BE HELD ON AUGUST 25, 2023

Shareholders in D-Market Elektronik Hizmetler ve Ticaret A.Ş. (the “Company”) (“D-Market Shareholders”) are invited to attend the Annual General Assembly Meeting of Shareholders (the “General Assembly”) for the year 2022 to be held on August 25, 2023, at 11.00 (local time) at Kuştepe Mahallesi Mecidiyeköy Yolu Caddesi No:12 Trump Towers Kule:2 Kat:2 Şişli/İstanbul.

Agenda of the General Assembly and Other Information

| 1. | Opening of the meeting and election of the General Assembly Meeting Chairmanship |

In accordance with the “Turkish Commercial Code” no. 6102 (“TCC”), the “Regulation on the Principles and Procedures for General Assembly Meetings of Joint Stock Companies and the Representatives of the Ministry Attending Such Meetings” (“Regulation”), D-Market’s Articles of Association and the “Internal Directive on the Working Principles of the General Assembly”, the Chairmanship of the General Assembly shall be elected by the D-Market Shareholders.

| 2. | Authorization of the General Assembly Meeting Chairmanship to sign the minutes of the meeting |

In accordance with the TCC and the Regulation, the D-Market Shareholders attending the General Assembly shall vote to authorize the Chairmanship to keep minutes of the General Assembly and sign them.

| 3. | Reading and discussion of the Board of Director’s annual report for 2022 and reading of the independent auditor’s report, as stipulated in the Regulation on Principles and Procedures for General Assembly Meetings of Joint Stock Companies and Ministry Representatives to be Present at These Meetings (the “Regulation”) |

In accordance with the provisions of the TCC, D-Market Shareholders may obtain the Company’s Annual Report (D-Market Elektronik Hizmetler ve Ticaret A.Ş. 2022 Annual Report) prepared by the Board of Directors from the Company’s headquarters free of charge or download from https://investors.hepsiburada.com/ at least 15 days before the General Assembly Meeting. Additionally, D-Market Shareholders may obtain the independent auditors’ report prepared by Güney Bağımsız Denetim ve Serbest Muhasebeci Mali Müşavirlik A.Ş. (Ernst and Young) from the Company headquarters free of charge or from https://investors.hepsiburada.com/ at least 15 days before the General Assembly Meeting. There are no issues to be voted on.

| 4. | Reading, discussion, and ratification of the financial statements for the 2022 accounting period, as specified in the Regulation |

According to Article 28 of D-Market’s Articles of Association, D-Market’s accounting period starts on the first day of January and ends on the last day of December. Within this framework, the financial statements of the Company for the period between January 1, 2022 and December 31, 2022 shall be read and submitted for the approval of the D-Market Shareholders attending the General Assembly. D-Market Shareholders may obtain these documents from the Company’s headquarters or from https://investors.hepsiburada.com/ website at least 15 days before the General Assembly Meeting.

| 5. | Release of the members of the Board of Directors for all their respective business, transactions and activities for the 2022 accounting period, as specified in the Regulation |

As per the provisions of the TCC, release of the members of the Board of Directors from liability for their business, transactions and activities in connection with their service on the Board of Directors for the 2022 financial year shall be submitted for the approval of the D-Market Shareholders attending the General Assembly.

| 6. | Decision on the Company’s profit for the 2022 accounting period, the use of the profit, the proportions of the profit and earnings shares to be distributed, as specified in the Regulation |

In view of there not having been any profit for the fiscal year ended December 31, 2022, according to the statement of comprehensive loss of the Company for that period, the Board of Directors proposes to the D-Market Shareholders attending the General Assembly to approve its determination not to distribute any dividend.

| 7. | Decision on the salary, honorarium, bonus, and premium to be paid to the members of the Board of Directors in their capacity as such and, as applicable, in their capacity as members of committees for the year 2023 under Article 394 of the TCC and the Regulation |

The Board of Directors proposes that the D-Market Shareholders attending the General Assembly approve the following salary, honorarium, bonus, and premium to be paid to the members of the Board of Directors due to their independent membership of the Board of Directors and committees:

| • | 100,000 USD annual gross payment to independent board members |

| • | 20,000 USD annual gross payment to chairpersons of the committees |

| • | 10,000 USD annual gross payment to the other independent members of the committees |

Remuneration for the Chairperson and board members due to their membership of the Board of Directors and Committees* will be decided in line with Article 394 of the TCC and Article 15 of D-Market’s Articles of Association.

| 8. | Approval of the appointment of Mr. Stefan Gross-Selbeck, who was appointed by the Board of Directors pursuant to Article 363 of the TCC as an independent member of the Board of Directors to fill a seat vacated due to the resignation of Mr. Cemal Ahmet Bozer, as specified in the TCC and the Regulation |

* Committee: Audit Committee, Corporate Governance Committee and Risk Committee.

The resume of Mr. Stefan Gross-Selbeck is as below:

Dr. Stefan Gross-Selbeck joined our Board of Directors in January 2023 as an independent board member. Dr. Gross-Selbeck has over twenty years of experience in senior leadership roles including as a CEO and held a number of board memberships. Dr. Gross-Selbeck is a Senior Partner and Managing Director of the Boston Consulting Group and has since January 2023 been serving as Global Topic Leader Climate Technologies. Dr. Gross-Selbeck previously served as the Global Managing Partner of BCG Digital Ventures, the corporate venture arm of Boston Consulting Group and as Managing Partner for their European operations. Prior to joining BCG Digital Ventures in 2014, Dr. Gross-Selbeck served as CEO of New Work SE (formerly known as XING AG), a leading social network for professionals in Europe, between 2009 and 2013. He also had different management roles at eBay, ProSiebenSat1 and Boston Consulting Group GmbH. Dr. Gross-Selbeck is a member of the advisory boards of the German Startup Association and several ventures built by BCG Digital Ventures.

| 9. | Appointment of the members of the Board of Directors and determination of their terms of office |

The D-Market Shareholders attending the General Assembly shall vote on the appointment of the current members of the Board of Directors and determination of their terms of office.

| 10. | Appointment of the independent auditor for the 2023 accounting period, as specified in the Regulation |

The D-Market Shareholders attending the General Assembly shall vote on the appointment of PwC Bağımsız Denetim ve Serbest Muhasebeci Mali Müşavirlik A.Ş. (PwC) as auditor of the fiscal year 2023 accounts, as per the proposal of the Board of Directors and the Audit Committee.

| 11. | Consent of members of the Board of Directors for the commercial activities and transactions referred to in Article 395 and Article 396 of the TCC |

Article 395 of the Turkish Commercial Code titled “Prohibition of Carrying Out Transactions with the Company, Borrowing Money to the Company” provides that members of the board of directors may not carry out any transactions with the company on their own behalf or on behalf of others without obtaining authorization from the general assembly. It further stipulates that members of the board of directors who are not shareholders of the company and relatives of the members of the board of directors who are not shareholders of the company as listed in Article 393 may not borrow cash from the company and that the company cannot provide sureties, guarantees and collaterals for these persons, cannot assume responsibility, and cannot take over their debts.

In accordance with Article 396 of the Turkish Commercial Code entitled “Prohibition on Competing”, which states empowerment of members of the board of directors, in connection with carrying out an activity which is a commercial transaction falling under the scope of the company’s business either on their own or on a third party’s account as well as becoming a partner with unlimited liability at a company that is engaged in the same type of commercial transactions is required and, board members may engage in transactions described in Article 396 only with the approval of the majority of the shareholders attending the general assembly.

In line with these provisions, such authorizations for the members of the Board of Directors for 2023 shall be submitted to the consent of the D-Market Shareholders attending the General Assembly.

| 12. | Approval of the renewal of the directors’ and officers’ insurance policy |

Further details regarding the directors’ and officers’ liability insurance policy can be found on page 141 of the Company’s annual report on Form 20-F, accessible via the below link.

https://hepsiburada.gcs-web.com/static-files/8ca14b71-e8c7-4131-bf2c-d8d8a6b30c94?auth_token=df23ffe8-8292-49b7-99e5-21225fac63b4

| 13. | Determination of the upper limit for the aid and donations to be made until the next Ordinary General Assembly meeting of the Company as 2 per thousands of the total net assets of the Company and approval of the authorization of the Board of Directors within this context |

The upper limit of 0.2 per cent of the total net assets of the Company for the aid and donations to be made until the next ordinary (i.e. annual) General Assembly meeting of shareholders as approved by the Board of Directors shall be submitted to the approval of the shareholders attending the General Assembly.

| 14. | Approval of the granting of Company’s Class B shares that can be represented by ADSs (American Depositary Shares) within the scope of the Incentive Plan (HAPP), the main framework and conditions of which were established under the decision of the Company’s Board of Directors dated 24 March 2021 and numbered 2021/13, to senior executives, key employees, consultants, managers and members of the Board of Directors, as determined by the resolution of the Board of Directors dated 27 February 2023 and numbered 2023/03 |

Further details regarding the Incentive Plan (HAPP) can be found on pages 129 and 130 of the Company’s annual report on Form 20-F, accessible via the below link.

https://hepsiburada.gcs-web.com/static-files/8ca14b71-e8c7-4131-bf2c-d8d8a6b30c94?auth_token=df23ffe8-8292-49b7-99e5-21225fac63b4

| 15. | Approval of the Revised Incentive Plan under which shares may be granted to senior executives, key employees, consultants, managers and members of the Board of Directors as set forth in the resolution of the Board of Directors dated 24 April 2023 and numbered 2023/10 |

Further details regarding the Revised Incentive Plan (HAPP) can be found on pages 129 et seq. of, and Exhibit 4.4. to, the Company’s annual report on Form 20-F, accessible via the below link.

https://hepsiburada.gcs-web.com/static-files/8ca14b71-e8c7-4131-bf2c-d8d8a6b30c94?auth_token=df23ffe8-8292-49b7-99e5-21225fac63b4

| 16. | Determining the procedures and principles of the authorization to the Board of Directors to repurchase a portion of the Company’s ADSs traded on Nasdaq, pursuant to the applicable laws of the United States by complying with the requirements and limitations in applicable law, for the purpose of granting shares of the Company that can be represented by ADS to those senior executives, key employees, consultants, managers and members of the Board of Directors, within the scope of the Revised Incentive Plan approved with the decision of the Board of Directors dated 24 April 2023 and numbered 2023/10 |

The D-Market Shareholders attending the General Assembly shall vote on the determination on the procedures and principles of the authorization to the Board of Directors to repurchase a portion of the Company’s ADSs traded on Nasdaq. The purpose of the repurchase is to grant shares of the Company that can be represented by ADS to those senior executives, key employees, consultants, managers and members of the Board of Directors, within the scope of the Revised Incentive Plan.

| 17. | Determination of the procedures and principles of the authorization to be given to the members of the Board of Directors for the repurchase of ADSs representing Class B shares of the Company from the publicly traded portion, as specified in Article 16 of the Agenda above, in accordance with the provisions of Article 379 et seq. of the TCC |

Pursuant the Article 379 of the Turkish Commercial Code, the Company may acquire its own shares in an amount not exceeding one tenth of its registered or issued capital. To repurchase its shares, the Company should comply with the following conditions:

| (i) | the board of directors of the Company should adopt a resolution with respect to the share repurchase and request the authorization of the general assembly, |

| (ii) | the general assembly should adopt a resolution authorizing the board of directors to repurchase the Company’s shares and the authorization should be valid for a maximum period of 5 years and specify the nominal value of shares, the total nominal value of shares and the lower and upper limits of the price that may be paid, |

| (iii) | after deducting the value of shares to be repurchased, the remaining net assets of the Company should be at least the sum of the registered or issued capital and the reserves that are not allowed to be distributed in accordance with the Turkish Commercial Code and the Company’s articles of association, |

| (iv) | the committed capital for the shares to be repurchased must be paid, and |

| (v) | the share repurchase must comply with all relevant provisions of the Turkish Commercial Code. |

In this context, the determination of the procedures and principles of the authorization to be given to the members of the Board of Directors for the repurchase of ADSs representing Class B shares of the Company from the publicly traded portion by the Company shall be submitted to the approval of the D-Market Shareholders attending the General Assembly.

The D-Market Shareholders attending the General Assembly shall vote on authorizing the Board of Directors for the repurchase of the Company’s ADSs representing Class B shares of the Company from the publicly traded portion in accordance with the provisions of the Turkish Commercial Code Article 379 et seq. in one or more transactions. The following procedures and principles for the authorization of the Board of Directors in relation to the transactions concerning the repurchase of ADSs representing Class B shares of the Company shall be submitted to the approval of the D-Market Shareholders attending the General Assembly:

| (i) | the amount of capital represented by the ADSs representing Class B shares of the Company to be repurchased shall not exceed 10% of the issued capital of the Company, |

| (ii) | the transactions shall not exceed the upper limit of 6,500,000 ADSs representing Class B shares (with a total nominal value of TRY 1,300,000 and a nominal value of TRY 0.20 for each share) of the Company, |

| (iii) | the authorisation period shall be 2 years, and |

| (iv) | the lower and upper limit that can be paid for the repurchase of ADSs representing Class B shares of the Company shall be determined. |

| 18. | Approval of the Remuneration Policy for the members of the Board of Directors and managers of the Company |

The Remuneration Policy for the members of the Board of Directors and managers of the Company, as amended, shall be submitted to the approval of the D-Market Shareholders attending the General Assembly. The revised version of the policy will be published on the Company’s investor relations website, which can be accessed via the following link: https://investors.hepsiburada.com/en/governance/governance-documents

| 19. | Closing |

There are no issues to be voted on under Item 19 of the Agenda.

|

hepsiburada D-MARKET ELEKTRONiK HiZMETLER • VE TICARET A.~. 2022 ANNUAL REPORT 0 ;1/p |

|

11) GENERAL INFORMATION I.a) Fiscal period to which the report relates: This Annual Report ("Annual Report") is in relation to the activities of D-Market Elektronik Hizmetler ve Ticaret A.$. (hereinafter referred to as "D-Market" or the "Company") and its subsidiaries (hereinafter collectively referred to as the "Group") for the year 2022. l.b) Corporate name of the Company, trade register number, communication information in relation to headquarters and, if any, its branches and, if any, its website address: Corporate Name Trade Registry Office Trade Registry Number Address : D-Market Elektronik Hizmetler ve Ticaret A.$. : Istanbul : 436165 : Ku§tepe Mah. Mecidiyekoy Yolu Cad. No:12 Kat: 2 Phone Kule 2 34387 $i§li / Istanbul : 212 705 68 00 Fax : 212 397 26 08 Corporate Website : investors.hepsiburada.com The branches of the Company are listed below: Branch Telephone D-Market Elektronik Hizmetler ve Ticaret 0212 705 68 00 Anonim $irketi Trump Towers Branch D-Market Elektronik Hizmetler ve Ticaret 0549 438 05 53 Anonim $irketi Sancaktepe Branch D-Market Elektronik Hizmetler ve Ticaret 0549 831 40 59 Anonim $irketi Izmir Torbah Branch D-Market Elektronik Hizmetler ve Ticaret 0549 438 15 77 Anonim $irketi Ankara Kazan Branch D-Market Elektronik Hizmetler ve Ticaret 0549 826 33 35 Anonim $irketi Diyarbak1r Yeni§ehir Branch D-Market Elektronik Hizmetler ve Ticaret 0549 438 18 53 Anonim $irketi Adana Seyhan Branch D-Market Elektronik Hizmetler ve Ticaret 0549 836 10 55 Anonim $irketi Erzurum Aziziye Branch D-Market Elektronik Hizmetler ve Ticaret 0549 827 18 69 Anonim $irketi Gebze Branch D-Market Elektronik Hizmetler ve Ticaret Anonim $irketi Istanbul Tuzla Branch 0536 067 08 53 Address Ku§tepe Mah. Mecidiyekby Yolu Cad. No:12 Kat: 2 Kule:2 34387 $i§li, Istanbul Meclis Mah, Bogazici Cad, Seheryeli Sk, No: 1, Karsan Plaza Sancaktepe, Istanbul Kaz1m Karabekir Mah. Bekir Saydam Cad. No:76 D.No:1 Torbal1 , Izmir Saray Mah. 221 . Sk. No:6 Kazan, Ankara Oc;:kuyu Mah. Mir Cebeli 1. Sk. No:5 Merkez, Yeni§ehir-Diyarbak1r Zeytinli Mahallesi Turhan Cemal Beriker Bulvan No.623 Seyhan, Adana <;iftlik Mahallesi, Tepe Mevkii, Ada:11202 Parsel:815 Yakutiye, Erzurum Inonu Mah. Farabi Cad. No:3 Gebze Guzeller OSB Gebze, Kocaeli Istanbul Deri Organize Sanayi Bolgesi, Dolap Cad. No:3 K-2 Ozel Parse! Tuzla, Istanbul The Company was established in April 2000 and it currently operates as a retail website (www.hepsiburada.com) offering its customers a wide selection of merchandise including electronics and non-electronics (including books, sports, toys, kids and baby products, cosmetics, furniture, etc.) As of 31 December 2022, the shareholders of D-Market are the members of Dogan Family, TurkCommerce B.V and The Bank of New York Mellon. 1 |

|

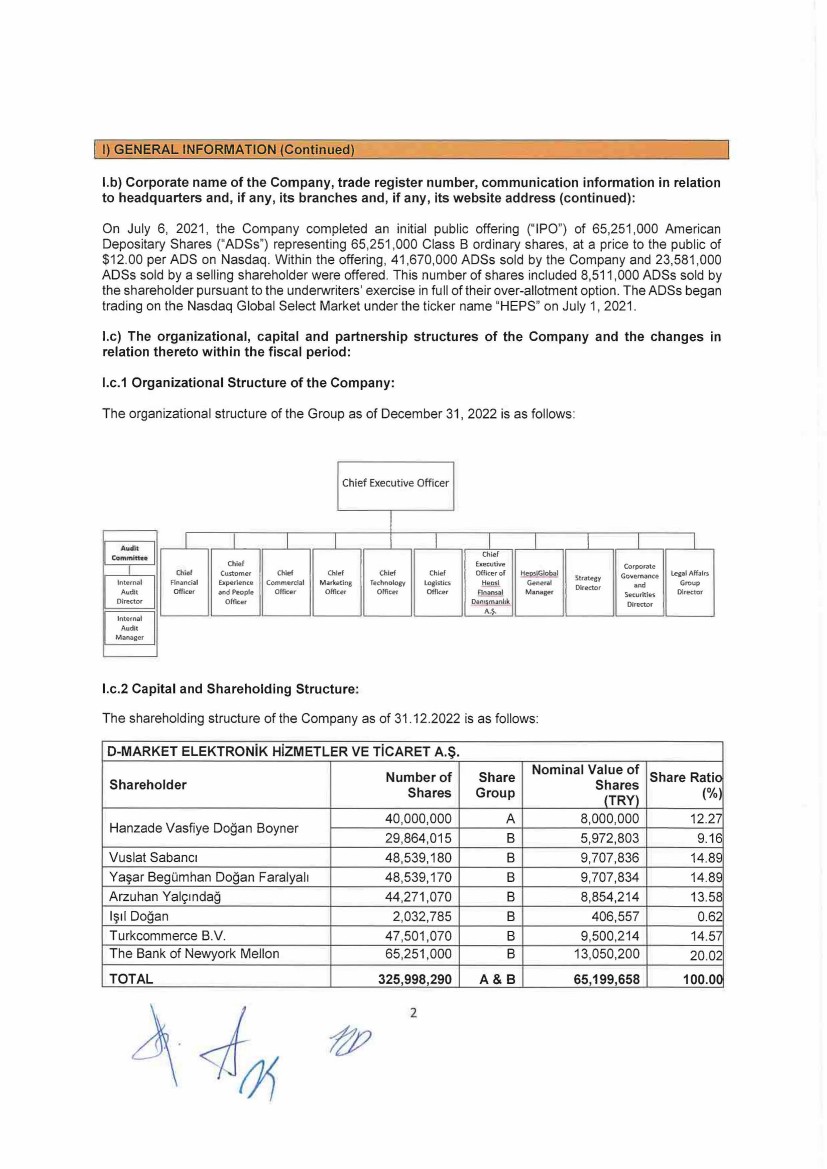

I t) GENERAL INFORMATION (Continued) l.b) Corporate name of the Company, trade register number, communication information in relation to headquarters and, if any, its branches and, if any, its website address (continued): On July 6, 2021 , the Company completed an initial public offering ("IPO") of 65,251 ,000 American Depositary Shares ("ADSs") representing 65,251,000 Class B ordinary shares, at a price to the public of $12.00 per ADS on Nasdaq. Within the offering, 41,670,000 ADSs sold by the Company and 23,581,000 ADSs sold by a selling shareholder were offered. This number of shares included 8,511,000 ADSs sold by the shareholder pursuant to the underwriters' exercise in full of their over-allotment option. The ADSs began trading on the Nasdaq Global Select Market under the ticker name "HEPS" on July 1, 2021 . l.c) The organizational, capital and partnership structures of the Company and the changes in relation thereto within the fiscal period: l.c.1 Organizational Structure of the Company: The organizational structure of the Group as of December 31 , 2022 is as follows : Chief Executive Officer I Audll I I I I I I I I I I Commlth• Chief Chief Executive Corporate I O,iof Customer Chle-f Chief Chle-f Chief Officer of HepslGlobal Governance Legal Affalr.s Internal Financial Experience Commercial Marketing Technology Logistics ~ General Strategy Group Director and Audit Officer and People Officer Officer Officer Officer Flnanul Manager Securities Director Director Officer Dam manltk Director A~. Internal Audit Manager l.c.2 Capital and Shareholding Structure: The shareholding structure of the Company as of 31 .12.2022 is as follows: D-MARKET ELEKTRONiK HiZMETLER VE TiCARET A.~. Number of Share Nominal Value of Share Ratic Shareholder Shares Shares Group (TRY) (%) Hanzade Vasfiye Dogan Boyner 40,000,000 A 8,000,000 12.27 29,864,015 B 5,972,803 9.16 Vuslat Sabanci 48,539,180 B 9,707,836 14.89 Ya§iar Beg0mhan Dogan Faralyal1 48,539,170 B 9,707,834 14.89 Arzuhan Yalc;:indag 44,271,070 B 8,854,214 13.58 l§ill Dogan 2,032,785 B 406,557 0.62 Turkcommerce B.V. 47,501,070 B 9,500,214 14.57 The Bank of Newyork Mellon 65,251 ,000 B 13,050,200 20.02 TOTAL 325,998,290 A&B 65,199,658 100.00 2 |

|

I) GENERAL INFORMATION (Continued) l.c.2 Capital and Shareholding Structure (continued): At the extraordinary General Assembly meeting ("GAM") dated 25 May 2021, it was decided that the Company adopts the registered capital system as per the provisions of the Turkish Commercial Code ("TCC") numbered 6102 and nominal value of each share has been determined as TRY 0.20. Upon this GAM, the issued share capital of the Company was divided into 284,328,290 registered shares each with a nominal value of TRY 0.20. At the Board of Directors meeting dated 5 July 2021, the Board of Directors decided to increase the share capital of the Company by amounting to TRY 8,334,000 reaching TRY 65,199,658 through injection of additional capital. In addition to the capital increase, it has been decided to undertake a share premium of TRY 4,107,870,000 and to issue 41,670,000 class B shares with premium. Board of Directors allocated newly issued class B ordinary shares with a total nominal value of TRY 8,334,000 for 41,670,000 shares with TRY 0.2 nominal value each to underwriters for IPO of American Depositary Shares. Le) Statements in relation to the privileged shares and the voting rights of the shares: By means of the Extraordinary General Assembly Resolution dated 25.05.2021, the Articles of Association of the Company were amended, and the right of privilege was granted to shareholders of Group A. At the Ordinary and Extraordinary General Assembly meetings, Group A shares have been granted 15 (fifteen each) voting rights, and the Group B shares have been granted 1 (one) vote each save for the provisions of the TCC. Information on the privilege in the Company as of 31.12.2022 in the Articles of Association is presented below. TRANSFER OF SHARES ARTICLE 7 Transfer of Class B shares is unrestricted, provided that the relevant articles of the Turkish Commercial Code and provisions of these articles of association are reserved. However, Class A shares may be transferred within the framework of the arrangements provided in article titled "Elimination of Share Classes Partially or Completely and Privileged Votes" of these articles of association. PARTIAL OR FULL TERMINATION OF SHARE CLASSES AND PRIVILEGED VOTES ARTICLE 7/A A. Events Fully Eliminating Privileged Shares Except for the Permitted Transactions defined in section (D) of this article, in following events, the privileged voting afforded to Class A shares under these articles of association shall automatically terminate, to the extent permitted by the provisions of the Turkish Commercial Code and other legislation, without revival afterwards. In any case, if these situations occur, the articles of association hereby shall be amended and share classes and references to share classes shall be removed in the first general assembly meeting to be held thereupon: a. 180 days following the transaction that leads to the shares (including both privileged Class A shares and ordinary Class B shares) held by the shareholders who owns Class A shares falls below 7.5% of the total paid-in capital of the Company b. In the event that the shareholder who owns Class A shares is a real person, 180 days after the date of legal documentation of this person's or people's (i) death or (ii) permanent mental incapacity due to health reasons; c. 1 (one) calendar year after all duties and titles are terminated, in the event that the shareholder who owns Class A shares is a real person, this person or these people (a) resign from the Board of Directors of the Company, (b) do not become a candidate for the Company's board of directors and (c) in case the conditions of ceasing to hold any employment or consultancy position at the Company are fulfilled together and if this situation is not corrected within 1 (one) calendar year wholly and solely with their own will; 3 |

|

11) GENERAL INFORMATION (Continued) I.,;,) Statements in relation to the privileged shares and the voting rights of the shares (continued): B. General Time Limit Regarding the Privileged Shares Notwithstanding occurrence or non-occurrence of the events set forth under (a) to (c) above in section (A) of this article hereinabove, on the 20th anniversary of the date on which the Company's shares or other securities representing the Company's capital start to be traded in any stock exchange, the voting privilege afforded to all Class A shares existing as of such date, shall automatically terminate, to the extent permitted by the provisions of the Turkish Commercial Code and other legislation, without revival afterwards, In any case, if these situations occur, the articles of association hereby shall be amended and share classes and references to share classes shall be removed in the first general assembly meeting to be held thereupon. PARTIAL OR FULL TERMINATION OF SHARE CLASSES AND PRIVILEGED VOTES ARTICLE 7/A (Continued) C. Events Partially Eliminating Privileged Shares Except for the Permitted Transactions defined in section (D) of this article, in following events, the privileged voting afforded to Class A shares under these articles of association shall automatically terminate, to the extent permitted by the provisions of the Turkish Commercial Code and other legislation, without revival afterwards. In any case, if these situations occur, the articles of association hereby shall be amended and share classes and references to share classes shall be removed in the first general assembly meeting to be held thereupon: a. Except for the cases included in the scope of "Permitted Transactions" below, in the event that Class A shares are transferred to any third real or legal person, as of the date of this transfer, only in relation to the transferred shares; and b. Upon application of the shareholders who owns Class A shares to the Central Registry Agency of Turkey (Merkezi Kay1t Kurulu~u Anonim $irketi) or a substitute institution to convert such shares to tradable form in the stock exchange for any reason including for sale thereof in the stock exchange or subjecting the same to collateral and only in relation to the transferred shares. D. Permitted Transactions However, in case of occurrence of Permitted Transactions, even if they are within the scope of the transactions stated under the above headings (A), (B) and (C) of this article, Class A shares may be transferred without being converted to Class B shares. Below transactions are "Permitted Transactions": a. Legal or arbitrary transfer transactions to be made by the shareholder who owns Class A shares to his or her first or second degree relatives; and b. Transactions whereby Class A shares are transferred to a domestic or overseas legal entity whose management is controlled by the immediate blood relatives or second degree relatives of the shareholder who owns Class A shares. CAPITAL INCREASE AND DECREASE ARTICLE 8 The Company's share capital may be increased or decreased when necessary, within the framework of the provisions of the Turkish Commercial Code. Bonus shares issued in capital increases through bonus issues shall be distributed to the existing shareholders as of the date of the increase pro rata to their shares. Unless otherwise determined, in capital increases to be made, Class A shares shall be issued in return for the Class A shares and Class B shares shall be issued in return for the Class B shares. In paid capital increase, in relation to Class A shares, if the owners of the said shares do not exercise their right to acquire new shares, only the relevant Class A shares shall automatically be converted to Class B shares. 4 |

|

[ 1) GENERAL INFORMATION (Continued) l.c) Statements in relation to the privileged shares and the voting rights of the shares (continued): VOTING RIGHT AND APPOINTMENT OF PROXY ARTICLE 23 In Ordinary and Extraordinary General Assembly meetings, each Class A share grants 15 (fifteen) votes to the shareholders who owns these shares and each of Class B share grants one vote to the shareholders, provided that provisions of the Turkish Commercial Code are reserved. In the General Assembly meetings, votes are cast openly. However, a ballot can be held upon request of the shareholders who owns at least 1/20 of the capital represented in the meeting. Le) Statements in relation to the privileged shares and the voting rights of the shares (continued): AMENDMENT IN ARTICLES OF ASSOCIATION ARTICLE 26 Amendments to the articles of association shall be decided in the general assembly to be called in line with the provisions of the Turkish Commercial Code and the Articles of Association, within the framework of provisions of the Turkish Commercial Code and the articles of association. The amendments to the articles of association must be registered and announced . Amendments to the articles of association shall bind third parties after registration thereof. In case the amendment of the articles of association is subject to the permission of the Ministry of Trade or another public institution or organization, the draft amendments to the articles of association, which are not approved by the mentioned public institutions or organizations, cannot be included in the agenda of the general assembly and cannot be discussed. Pursuant to the provisions of Article 454 of the Turkish Commercial Code, if the decision of the general assembly on amendment of the articles of association is of a nature that violates the rights of privileged shareholders of Class A shares, this decision shall be made in a special meeting to be held by Class A shareholders, unless approved by a decision they will take within the framework of the provisions of the relevant legislation, it is not applicable. l.d) Information on the management organ, senior management and the number of employees: l.d.1 Board of Directors: The Members of the Board of Directors as at 31 December 2022 are as follows: Hanzade Vasfiye Dogan BOYNER (Chairman of the Board of Directors) Erman KALKANDELEN (Deputy Chairman of the Board of Directors) Vuslat SABANCI T olga BABALI Mehmet Murat EMiRDAG Ahmet Fad1I ASHABOGLU (Independent Board Member) Tayfun BAYAZIT (Independent Board Member) Hali! Gem KARAKA$ (Independent Board Member) Cerna! Ahmet BOZER<1l (Independent Board Member) (1) Cemal Ahmet Bazer resigned from the board of directors with the decision of the board of directors dated 2 January 2023 and Dr. Stefan Gross-Selbeck was appointed as an independent board member on the same date. 5 |

|

Hanzade Vasfiye Dogan Boyner Committee Memberships: None Hanzade Vasfiye Dogan Boyner is our founder and has served as the Chair of our Board of Directors since she founded Hepsiburada in 2000. Ms. Dogan is an experienced entrepreneur and leader of e-commerce and technology businesses as well as blue-chip companies. In 2002, Ms. Dogan founded Nesine, one of TOrkiye's leading sports betting platforms, and currently holds the position of chairwoman. From 2003 to 2007, Ms. Dogan was the chairwoman of Dogan Publishing, Turkiye's largest publishing company in terms of circulation at the time. From 2006 to 2010, Ms. Dogan was first a board member and then the chairwoman of Petrol Ofisi, Turkiye's main fuel-products distribution company and second largest corporation by revenue throughout that period. Ms. Dogan is the founding board member and served as the Vice-Chairwoman of Global Relations Forum between 2009 and 2020. She has been a member of the Brookings Institute Board of Trustees since 2014. Ms. Dogan is a regular participant at the World Economic Forum and a Committee Member of the Digital Platforms and Ecosystems Initiative. Between 2012 and 2022, Ms. Dogan served as the chairwoman of the Aydin Dogan Foundation, a not-for-profit organization with a social mobility mission and currently serves as a board member. Ms. Dogan holds a Bachelor's degree in Economics from the London School of Economics and a Master of Business Administration from Columbia University where she continues to serve as a member of the Business School Board of Overseers. Erman Ka/kandelen Committee Memberships: None Erman Kalkandelen has served as a member of our board since August 2020. Mr. Kalkandelen currently serves as the CEO and Chairman of Franklin Templeton Turkey. Mr. Kalkandelen previously co-managed the Templeton Emerging Market Small Cap strategy. He is currently heading the private equity practice of Franklin Templeton in TOrkiye and CEE and focusing mainly on the technology industry. He is a member of the board of directors of Netlog Lojistik, Gozde Giri§im and Gozde Tech Ventures, Fibabanka, $ok Marketler, Bleckmann, Penta Teknoloji and Bizim Toptan. Mr. Kalkandelen holds a Master of Business Administration, with honors, from Sabanci University. During his MBA, he also studied strategic management at the Warrington School of Business Management, Florida University and graduated with honors from the Labor Economics Department of the Political Sciences Faculty, Ankara University. Vus/at Sabanci Committee Memberships: None Vuslat Sabanci has been a member of our board of directors since 2020. Ms. Sabanci has over twenty years of experience in publishing and media. From 2004 to 2008, she served as the CEO of Hurriyet Publishing, Turkiye's foremost newspaper group, and as publisher from 2008 to 2018, during which time Hurriyet became a widely read and influential newspaper and Turkiye's largest digital content company. Prior to joining Hurriyet, Ms. Sabanci worked at The New York Times and The Wall Street Journal. Ms. Sabanci founded Hurriyet Emlak, one of Turkiye's leading real estate websites in 2016, and has been chairwoman since 2019. Ms. Sabanci sits on the board of a number of companies, including Dogan Group. Ms. Sabanci is a lifetime honorary board member of the International Press Institute (IPI) and serves on the Advisory Board of Columbia University's Global Centers, as well as on the Columbia Global Leadership Council. In 2006, Ms. Sabanci received UN Grand Award for outstanding achievement for her social justice campaigns. She is Vice President of the not-for-profit Aydin Dogan Foundation and a founding board member of Turkish Businesswomen Association and the not-for-profit organization Endeavor Turkiye. ff(} 6 |

|

Ms. Sabanci holds a Bachelor's degree in Economics from Bilkent University and completed her graduate studies in International Media and Communications at Columbia University's School of International and Public Affairs. Taiga Baba/1 Committee Memberships: Risk Committee, Corporate Governance Committee Taiga Babali has been a member of our board of directors since May 2021. Since 2008, he has held several management roles in Dogan Holding and related companies in the Dogan Group and, between August 2017 and March 2023, Mr. Babal1 served as a Board member of Dogan Holding, with responsibility for financial and operational management. He continues to serve as a board member in a number of Dogan Group companies. Prior to joining the Dogan Group, Mr. Baba!, worked for the Tax Inspection Board and Revenue Administration at the Ministry of Finance of Ti.irkiye from 1998 to 2008. Mr. Babali holds a Bachelor's degree in Economics from Gazi University, Ankara, and is certified as a Sworn-in Certified Public Accountant and an Independent Auditor. Mehmet Murat Emirdag Committee Memberships: None Mehmet Murat Emirdag served as our Chief Executive Officer (CEO) from February 1, 2019 until December 31, 2022 and is currently a member of our board of directors. Prior to Hepsiburada, Mr. Emirdag hel,d different executive and management roles at leading companies such as lnstacart, Zynga, Microsoft and Unilever. Mr. Emirdag holds a Master of Business Administration from Columbia Business School and holds degrees in Chemical Engineering and Mechanical Engineering from Bosphorus University in Istanbul. Ahmet Fad1/ Ashabog/u Committee Memberships: Audit Committee, Corporate Governance Committee, Risk Committee (Chairman) Ahmet Fadtl Ashaboglu joined our board of directors in May 2022 as an independent board member. He began his career as a Research Assistant at MIT in 1994, followed by various positions in capital markets within UBS Warburg, New York (1996-1999). After serving as a management consultant at McKinsey & Company, New York (1999-2003), Ahmet Fad1I Ashaboglu moved back to Ti.irkiye and joined Koc;: Holding as Finance Group Coordinator in 2003. He was appointed as Group Chief Financial Officer at Koc;: Holding in 2006 and served in that position until April 2022. Ahmet Fad1I Ashaboglu is currently a board member of Mavi, Yap, Kredi Bank, Koc;: Financial Services, Koc;: Finansman, Sirena Marine and DP Eurasia N.V. Ahmet Fad1I Ashaboglu holds a BSc degree from Tufts University and a Master of Science degree from Massachusetts Institute of Technology (MIT), both in Mechanical Engineering. Tayfun Bayaz1t Committee Memberships: Audit Committee (Chairman), Risk Committee Tayfun Bayaz1t has been a member of our board of directors since July 2021 as an independent board member. After having received a BS degree in Mechanical Engineering (1980) and an MBA from Columbia University, New York, (Finance and International Business - 1983), Mr. BayazIt started his banking career at Citibank in 1983. He subsequently worked in executive positions within <;ukurova Group for 13 consecutive years (Yap, Kredi as Senior EVP and Executive Committee Member, Interbank as CEO, Banque de Commerce et de Placements S.A. Switzerland as President and CEO). In 1999, he was appointed as Vice Chairman of 7 fl£) |

|

Dogan Holding and an Executive Director of D11?bank. In 2001, he assumed the CEO position at D11?bank. In 2003, he was also appointed Chairman and was requested to remain as CEO of Fortis TOrkiye and the region in July 2005 after its acquisition. Subsequently, he was elected as Chairman of Fortis in 2006. Mr. BayazIt came back to Yap, Kredi in 2007 (at which time Yap, Kredi was owned by a joint venture of the UniCredit and the Kor;: Group) as CEO and two years later he was elected as Chairman. He served as chairman of all Yap, Kredi subsidiaries including Yap, Kredi Sigorta (property and casualty insurance) and Yap, Kredi Emeklilik (private pension and life) for 4 years. Yap, Kredi was the fourth largest high street bank in T0rkiye with subsidiaries in Holland, Bahrain and Russia, actively involved in mortgage lending among other individual banking activities with a strong digital focus. Mr. BayazIt left this post in August 2011 to set up his own firm "Bayazit Consulting Services." He was then elected as the Country Chairman for MarshMcLennan Group (Marsh, Mercer and Oliver Wyman exist in T0rkiye) in September 2012 and serves on the board of directors of MLP Care (healthcare) and Coca Cola lcecek (bottling and distribution) as an independent director. He is also a board member at Aydem Enerji and Boyner companies. He is a member of TUSIAD (Turkish Industrialists and Business Association) High Advisory Board and takes an active role in other non-governmental organizations such as the World Resources Institute, Corporate Governance Association of TOrkiye. He is a member of the board of trustees of Bosphorus University and Turkish Education Volunteers Foundation. Hali/ Gem Karaka§ Committee Memberships: Audit Committee, Corporate Governance Committee (Chairman) Dr. Halil Cem Karakai? joined our board of directors in May 2022 as an independent board member. Dr. Karakai? is an industrial restructuring leader in global snacking industry. He has led large scale restructuring and growth programs in biscuit and chocolate industries building and rationalizing several dozen manufacturing plants around the world as well as leading omni-channel market entry programs. Latest, Dr. Karakai? was the founding CEO of Pladis, the largest European biscuit player and one of the largest snacking companies globally. Prior to that Dr. Karakai? held CEO and CFO roles in Y1ld1z Group and Erdemir Group of T0rkiye. Dr. Karakai? is the executive chairman of Aran Ard Teoranta and Rudi's Organic, the fastest growing European and North American free-from bakery players. Dr. Karakai? has a Bachelor's degree in management from Middle East Technical University, Master's degree in business administration in finance from Massachusetts Institute of Technology and a Doctorate degree in finance from Istanbul University. Gema! Ahmet Bozer<1 ! Committee Memberships: Audit Committee, Corporate Governance Committee, Risk Committee (Chairman) ( 2! Cemal Ahmet Bazer became a member of our board of directors in 2016. Mr. Bazer started his career at DeVry Institute of Technology in 1983 as an Assistant Professor. He joined the audit firm Coopers & Lybrand in Atlanta in 1985, serving in a variety of audit, consultancy and management roles. He later joined Coca-Cola and served in financial roles from 1990 to 1997. In 1994, he took a leadership role at Coca-Cola Bottlers of Turkey (now Coca-Cola lcecek) as Chief Financial Officer and became its Managing Director, reporting to a board of JV partners. Returning to Coca-Cola in 2000 as Division President, Eurasia, he soon assumed Middle East responsibilities, and in 2007 became Group President for Eurasia. In 2008 Mr. Bozer was named Group President & COO, Eurasia & Africa, where he led business activities in 90 countries and in 2012, he was named as President of Coca-Cola International in more than 200 countries/territories. Mr. Bazer has a Bachelor's degree in Management from the Middle East Technical University, Ankara, and a Master's degree in Business in Information Systems from Georgia State. While at Coopers & Lybrand Mr. Bozer became a Certified Public Accountant. (1) Cemal Ahmet Bazer resigned from the board of directors with the decision of the board of directors dated 2 January 2023 and Dr. Stefan Gross-Selbeck was appointed as an independent board member on the same date. 8 |

|

(2) Cemal Ahmet Bozer resigned from his roles in Corporate Governance Committee, Risk Committee and Audit Committee effective as of June 24, 2022. Committees of the Board of Directors We have three committees reporting to the Board of Directors, namely (1) Audit Committee, (2) Risk Committee and (3) Corporate Governance Committee. All members of these committees operate to fulfill the requirements of the U.S. Securities and Exchange Commission - SEC, U.S. Nasdaq, TCC and Turkish capital markets legislation. Members of the Committees of the Board Directors as well as their duties and responsibilities are as follows: (1) Audit Committee: The Audit Committee assists our Board in its responsibilities for (i) the integrity of our financial statements, (ii) the qualifications and independence of our statutory auditors, (iii) oversight of our independent auditors' performance and our internal audit function, and (iv) compliance with legal and regulatory requirements, as well as environmental and social responsibilities. Members of the Audit Committee as of December 31, 2022, are as follows: Tayfun BAYAZIT (Chairman) Ahmet Fad1I ASHABOGLU (Member) Halil Cem KARAKA$ (Member) Cemal Ahmet Bazer and Halil Korhan Oz resigned from their roles in the Audit Committee effective as of June 24, 2022. Ah met Fad1I Ashaboglu and Halil Cem Karaka~ have been appointed to the Audit Commitee as of the same date. (2) Risk Committee: The Risk Committee is responsible for early identification of risks that pose a threat to the existence, development and continuity of our Company. It reviews Hepsiburada's risk management policies at least once a year. Members of the Risk Committee as of December 31, 2022 are as follows: Ahmet Fad1I ASHABOGLU (Chairman) Tayfun BAYAZIT (Member) Taiga BABALI (Member) Cerna! Ahmet Bazer resigned from his role in the Risk Committee effective as of June 24, 2022. Ahmet Fad1l Ashaboglu has been appointed to the Risk Commitee as of the same date. (3) Corporate Governance Committee: The Corporate Governance Committee periodically reviews whether the corporate governance principles are applied by our Board of Directors and makes recommendations to the Board of Directors on corporate governance issues. The Committee also fulfills the functions of the Nomination and Remuneration Committee, which advises the board on nomination and remuneration policies for the board and executives. Members of the Corporate Governance Committee as of December 31, 2022 are as follows: Halil Cem KARAKA$ (Chairman) Ahmet Fad1l ASHABOGLU (Member) Taiga BABALI (Member) Cemal Ahmet Bazer and Tayfun Bayaz1t resigned from their roles in the Corporate Governance Committee effective as of June 24, 2022. Ahmet Fad1I Ashaboglu and Halil Cem Karaka~ have been appointed to the Corporate Governance Commitee as of the same date. 9 |

|

l.d.2 Senior Management: Except for the members of the Company's Board of Directors, those who are conferred the authority and responsibility to plan, manage and control the activities of the Group directly or indirectly by the Board of Directors are defined as "senior management". The names and titles of the Company Group Heads as at 31 December 2022 are listed below: Hepsiburada CEO Hepsiburada CFO Hepsiburada Chief Human Resources Officer Hepsiburada Chief Commercial Officer Hepsiburada Chief Information Officer Hepsiburada Chief Marketing Officer Hepsiburada Chief Technology Officer Hepsiburada Chief Logistics Officer Hepsi Finansal CEO Mehmet Murat EMIRDAG( 1) Halil Korhan OZ Esra BEYZADEOGLLJ( 2) Murat B0YOMEZ<3) Gurkan CO$KUNER(4) Ender OZG0N<3) Alexey SHEVENKOV Mehmethan YALLAGOZ Erkin AYDIN (1) As of 1 January 2023, Nilhan Onal Gokr;etekin was appointed as the Chief Executive Officer of the Company. (2) As of 2 January 2023, Esra Beyzadeoglu's title has been updated as Chief Customer Experience and Human Resources Officer and her responsibilities have been expanded to include customer experience and customer service functions . (3) Murat Buyumez, has taken a leave of absence from his position between May 2, 2023 and September 21 , 2023. Mr. Murat Buyumez is expected to take a new position in the Company as Chief Investment Officer effective on his return. As of May 2, 2023, the Company's Chief Marketing Officer, Ender Ozgun, has assumed the responsibilities of the Chief Commercial Officer, in addition to his existing roles. (4) As of 31 December 2022, Gurkan Co~kuner resigned from his position. During the period, the following changes occurred in the senior management team: • On June 1, 2022, Erkin Aydin was appointed as the Chief Executive Officer of Hepsi Financial. • On July 22, 2022, Nilhan Onal Gokr;etekin was appointed as the Chief Executive Officer of the Company, effective from January 1, 2023. Our former Chief Executive Officer Murat Emirdag will continue to be a Member of the Board of Directors. l.d.3 Number of Personnel: As of 31.12.2022, the Group has 3,834 employees. (31.12.2021 : 3,789) l.e) Information about the transactions made by the members of the management body with the Company on behalf of themselves or someone else within the framework of the authorization given by the general assembly of the Company and their activities within the scope of the prohibition of competition: As stated in TCC, it is permitted to authorize the members of the Board of Directors to carry out, on their own behalf or on behalf of others, any commercial transaction that falls within the scope of the Company's business, and to become a partner with unlimited liability in a company which is engaged in the same type ~-qf IX 10 |

|

of commercial business, as specified in Article 396 of the TCC. The members of the Company's Board of Directors serve as members of the Board of Directors of some other Dogan Group companies, including those having similar fields of activity with our Company, and of the companies in which Franklin Templeton Turkey has a shareholding and in 2022, there were no significant transactions requiring information in this context. ) RENUMERATION PROVIDED TO THE MEMBERS OF THE BOARD OF DIRECTORS AND SENIOR MANAGEMENT All rights, benefits and remuneration provided to the members of the Board of Directors are determined every year at the Group General Assembly. Except for the independent members of the Board of Directors, no "attendance fee" is paid to the members of the Board of Directors, and the executive Members of the Board of Directors may also receive monthly salaries, bonuses and related fringe benefits for their duties in the Company. The total amount of financial benefits such as salaries, bonuses, share-based payments, health insurance, communication and transportation provided to the Group's senior management consisting of Members of the Board of Directors, General Managers, Group Presidents and directors are disclosed in Note 26 Related Party Disclosures in the notes to the consolidated financial statements prepared in accordance with Turkish Accounting Standards/Turkish Financial Reporting Standards ("TAS/TFRS") for the period ended December 31, 2022. The Company does not provide any guarantees such as loans, credits and personal loans to any Member of the Board of Directors and executives and guarantees such as sureties in their favor. f111) RESEARCH AND DEVELOPMENT ACTIVITIES In 2022, the Group's website and application development costs amount to TRY 519,626 thousand. The Group's research and development activities are carried out at our two R&D Centers, located in Istanbul and certified by the Turkish Ministry of Industry, and Technology. Our projects encompass a wide range including recommendation engines, search engines, customer personalization, payment systems, as well as fraud prevention. Along with our existing trademarks and pending trademark filings, certain components of our website and mobile applications, including the design, codes, website and mobile application contents, images, software integrations and interfaces are under copyright protection under relevant copyright regulations. As of December 31, 2022, we held three patents in Ti.irkiye as D-Market and one patent as D-Fast. As of the same date, we also had nine pending patent applications as D-Market and six pending patent applications as D-Fast. As of December 31, 2022, we had approximately 867 employees dedicated to technology operations and 59 product function teams dedicated to a particular technology product. Our research and development centres cooperate with Turkey's leading universities, making the Group attractive for technological talents and engineers. IV) THE COMPANY'S ACTIVITIES AND SIGNIFICANT DEVELOPMENTS IN RELATION TO THE ACTIVITIES IV.a) Information on investments made by the Group in the related accounting period: In 2022, the Group purchased fixtures and fittings amounting to TRY 130,760 thousand, vehicles amounting to TRY 33,721 thousand and spent TRY 12,316 thousand on leasehold improvements within the scope of warehouse renovations and warehouse investments. The total purchase price of software and rights purchased by the Group amounts to TRY 69,579 thousand. fg7 11 |

|

IV) THE COMPANY'S ACTIVITIES AND SIGNIFICANT DEVELOPMENTS IN RELATION TO THE ACTIVITIES (continued) IV.b) Information on the Group's internal control system and internal audit activities and the Board of Directors' opinion on this matter: The Group has manual and automated internal control systems in place against financial and operational risks. The efficiency of internal controls is regularly reviewed and new control points are included in the process when necessary. The Internal Audit Department, which reports directly to the Board of Directors and the Audit Committee, is responsible for carrying out audit activities across the Group and its subsidiaries in accordance with International Standards for the Professional Practice of Internal Auditing and reporting the findings to the Audit Committee. Audit activities mainly consist of operational (technology and business processes) audits performed within the framework of annual risk-based audit plans and compliance audits with Article 404 of the Sarbanes Oxley Act. Operational audit activities are performed in accordance with the annual audit plan prepared based on the risk-based audit approach. Through these audits, the Internal Audit function assesses the effectiveness of the Company's risk management, control and corporate governance processes, assures the Board of Directors and the Audit Committee on these processes, and helps the Company achieve its objectives. Within the scope of compliance with Section 404 of the Sarbanes Oxley Act, audit activities are carried out within the framework of the annual plan to provide assurance on the existence, adequacy and effective operation of the internal control structure established in the Group and Group Companies whose financial statements are consolidated. All stages of the audit activities carried out within the scope of compliance with the aforementioned article, starting from the planning stage to the follow-up and finalization of the internal control deficiencies and actions identified, are regularly reported to the Audit Committee, the Chief Executive Officer and the Chief Financial Officer. The Internal Audit Department also performs a consultancy function on current issues and matters requested by the management. The Internal Audit mechanism operates with a risk-based audit approach. In this framework, possible functional and organizational risks are constantly reviewed. The main input of the audit activities is the risk analyses resulting from these studies. The Group has also established an Internal Control and Compliance Department. This team, which is tasked with ensuring that all existing business processes and newly established processes are operated with controls to minimize risks, reports periodically to the Chief Financial Officer and the Audit, Risk and Corporate Governance Committees of the Board of Directors. IV.c) Information on the Company's direct or indirect subsidiaries and their shareholding rates: Information regarding the direct and indirect subsidiaries of D-Market is presented below: 12 |

|

IV) THE COMPANY'S ACTIVITIES AND SIGNIFICANT DEVELOPMENTS IN RELATION TO THE ACTIVITIES (Continued) 1) D Fast Dag1tim Hizmetleri ve Lojistik A.$. ("D-Fast") D FAST DAGITIM HiZMETLERi VE LOJiSTiK A.$. Shareholders Number of Shares Share Amount Share Ratio(%) (TRY) D-MARKET ELEKTRONiK 222,329,299 222,329,299.00 HiZMETLER VE TiCARET A.$. 100.00 TOTAL 222,329,299 222,329,299.00 100.00 D-Fast was established on February 26, 2016 and operates as a cargo and logistics company that provides last-mile delivery services to the customers of Hepsiburada and other e-commerce websites with which it has an agreement. As of December 31 , 2022, D-Fast provides services in 81 provinces. 2) D Odeme Elektronik Para ve Odeme Hizmetleri A.$. ("D-Odeme") D ODEME ELEKTRONiK PARA VE ODEME HiZMETLERi A.$. Shareholders Number of Shares Share Amount (TRY) Share Ratio(%) D-MARKET ELEKTRONiK 196,535,857 196,535,857.00 100.00 HiZMETLER VE TiCARET A.$. TOTAL 196,535,857 196,535,857.00 100.00 D-Odeme was established on June 4, 2015 and provides payment services intermediation and e-money services. D-Odeme obtained an operating license from the Banking Regulation and Supervision Agency on February 20, 2016. D-Odeme carried out its first payment services transaction on June 15, 2016. D-Odeme launched the Hepsipay wallet, a digital wallet product integrated into the Hepsiburada's platform, in June 2021 . Operating as Hepsiburada's payment gateway, D-Odeme enables its customers to pay with their e-money account balances and registered cards . 13 |

|

IV) THE COMPANY'S ACTIVITIES AND SIGNIFICANT DEVELOPMENTS IN RELATION TO THE ACTIVITIES (Continued) IV.c) Information on the Company's direct or indirect subsidiaries and their shareholding rates (continued): 3) Hepsi Finansal Dam!?manhk A.$. ("Hepsi Finansal") HEPSi FiNANSAL DANl$MANLIK A.$. Shareholders Number of Share Amount Share Ratio(%) Shares (TRY) D-MARKET ELEKTRONIK 49,000,000 49,000,000.00 100.00 HiZMETLER VE TiCARET A.$. TOTAL 49,000,000 49,000,000.00 100.00 Established on December 1, 2021, Hepsi Finansal plans to operate as a holding company for the Group's financial technology operations and aims to provide financial solutions to Hepsiburada's customers. Hepsi Finansal is the main shareholder of Doruk Finansman A.$. (the current trade name of the company is "Hepsi Finansman A.$."), which was acquired in February 2022. 4) Hepsi Finansman A.$. ("Hepsi Finansman") HEPSi FiNANSMAN A.$. Shareholders Number of Share Amount Share Ratio(%) Shares (TRY) HEPSI FINANSAL 50,000 50,000,000.00 100.00 DANl$MANLIK A.$. TOTAL 50,000 50,000,000.00 100.00 Doruk Finansman A.$.'s trade name has been changed to Hepsi Finansman A.$. as published in the trade registry gazette dated January 9, 2023 and numbered 10743. As of December 31, 2022 Hepsi Finansman has not yet begun its credit operations for a new portfolio. It carries out collection operations of the portfolio acquired from Doruk Finansman A.$. IV.c) Information on the Group's own shares acquired: The Group did not acquire its own shares during the period. IV.d) Explanations regarding the private audit and public audit conducted during the accounting period: The examination initiated by the Tax Office in July 2020 for the years 2018 and 2019 of the Company was completed in 2022. As a result of the examination, the Company paid an additional tax of TRY 282,582. IV.e) Information about the lawsuits filed against the Group that may affect the financial status and operations of the Company and their possible outcomes: On September 28, 2021, a class action lawsuit before the Supreme Court of the State of New York ("State Court") was filed against the Company and various other defendants. On October 21, 2021 , a separate class action lawsuit was filed against the Company and various other defendants before the Federal Court for the Southern District of New York ("Federal Court"). Both lawsuits allege that the Company made false ~) <Ztx 14 |

|

IV) THE COMPANY'S ACTIVITIES AND SIGNIFICANT DEVELOPMENTS IN RELATION TO THE ACTIVITIES (Continued) IV.e) Information about the lawsuits filed against the Group that may affect the financial status and operations of the Company and their possible outcomes (continued): and/or incomplete statements and violated applicable laws in the Registration Statement and Prospectus issued in connection with the Company's U.S. initial public offering. Lawsuits are currently pending. Opinions on the possible legal and financial risks regarding the course and possible outcomes of these lawsuits were obtained from expert and leading law firms in the United States of America and from financial advisors who are also experts in their fields . These opinions were of the view that discontinuation and termination of these lawsuits through settlement would save our Company from a major financial burden. In this context, within the scope of the decision of our Board of Directors numbered 2022/30 and dated November 10, 2022, in line with the opinions of the relevant expert legal and financial advisors, it was decided to settle with the counterparties of the lawsuits. In this regard, a mediation process was initiated for the final settlement of both lawsuits that would lead to eliminating the uncertainties, costs and risks of long-term, complex proceedings and saving time, effort and costs created by class actions, without any admission of liability or fault and following the negotiations led by an experienced mediator in the field, the plaintiff and defendant parties agreed on a binding settlement term sheet on December 2, 2022. Accordingly, the Company agreed to pay TRY 260,375 thousand (USO 13,900 thousand) to fully settle both lawsuits. Concerning USO 3,975 thousand of the USO 13,900 thousand, a binding contribution term sheet was signed on December 5, 2022, providing that the Company will receive a contribution payment from TurkCommerce B.V., another defendant who sold shares during the public offering, subject to certain preconditions. In this respect, the Company has provided a provision amounting to TRY 260,375 thousand (USO 13,900 thousand) in its consolidated financial statements as of December 31, 2022. Regarding both lawsuits, the settlement agreement prepared by the plaintiff and defendant parties was signed and submitted to the preliminary approval of the Federal Court in March. In its preliminary approval decision of April 20, 2023, the Federal Court held that the settlement agreement concluded between the parties: (i) was concluded by sufficiently informed parties, after protracted negotiations, and on an arm's length basis, under the direction of an experienced mediator; (ii) eliminates the risks to the parties in the event of continued litigation; (iii) does not constitute an unfairly preferential treatment in favor of the plaintiffs or certain segments of the settlement class; (iv) does not result in excessive fees to plaintiffs' counsel; (v) appears to fall within an acceptable range for possible approval and is sufficiently equitable, reasonable and fair to require notice to settlement class members. Additional information on the settlement process and the settlement agreement is provided in this Annual Report's Section 8 titled "other matters", subparagraph 9. More detailed information is provided in the consolidated financial statements prepared in accordance with TAS/TFRS for the period ended December 31 , 2022, at Note 15. IV.f) Explanations on administrative or judicial sanctions imposed on the Group and the members of the management body due to practices contrary to the provisions of the legislation: There are no significant administrative or judicial sanctions imposed on the Group and the members of the management body due to practices contrary to the provisions of the legislation. More detailed information is provided in the consolidated financial statements prepared in accordance with TAS/TFRS for the period ended December 31, 2022, at Note 15. IV.g) Information and evaluations on whether the targets set in the previous periods have been achieved, whether the resolutions of the general assembly have been fulfilled, and if the targets have not been achieved or the resolutions have not been fulfilled, the reasons thereof: The Ordinary General Assembly Meeting of the Company for the year 2021 was held on 24.06.2022 at the Company headquarters. At the said Ordinary General Assembly Meeting, the meeting quorum was met with ~ 0,82~ esolutions were adop::d by open ; IA |

|