UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 40-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2023 | Commission File Number: 001-31965 |

| TASEKO MINES LIMITED | |||

| (Exact name of Registrant as specified in its charter) | |||

| British Columbia | 1040 | Not Applicable | |

| (Province or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code) |

(I.R.S. Employer Identification No.) |

|

|

12

th

Floor - 1040 West Georgia Street

Vancouver, British Columbia Canada V6E 4H1 (778) 373-4533 |

|||

| (Address and telephone number of Registrant's principal executive offices) | |||

|

Corporation Service Company

Suite 400, 2711 Centerville Road Wilmington, Delaware 19808 (800) 927-9800 |

|||

| (Name, address (including zip code) and telephone number (including area code) of agent for service in the United States) |

|||

Securities registered or to be registered pursuant to section 12(b) of the Act:

| Title Of Each Class | Name Of Each Exchange On Which Registered |

| Common Shares, no par value | NYSE American |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

For annual reports, indicate by check mark the information filed with this Form:

☒ Annual Information Form ☒ Audited Annual Financial Statements

Indicate the number of outstanding shares of each of the Registrant's classes of capital or common stock as of the close of the period covered by the annual report: 289,999,596 Common Shares as of December 31, 2023

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the

Exchange Act.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term "new or revised financial accounting standard" refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

| Auditor Name: KPMG LLP | Auditor Location: Vancouver, Canada | Auditor Firm ID: 85 |

- 2 -

INTRODUCTORY INFORMATION

Taseko Mines Limited (the "Company" or "Taseko") is a Canadian public company whose common shares are listed on the Toronto Stock Exchange, London Stock Exchange, and the NYSE American Exchange (the "NYSE American"). Taseko is a "foreign private issuer" as defined in Rule 3b-4 under Securities Exchange Act of 1934, as amended (the "Exchange Act"), and is eligible to file this annual report on Form 40-F (the "Annual Report") pursuant to the multi-jurisdictional disclosure system (the "MJDS").

PRINCIPAL DOCUMENTS

The following documents that are filed as exhibits to this annual report are incorporated by reference herein:

CAUTIONARY NOTE TO UNITED STATES INVESTORS CONCERNING

ESTIMATES OF RESERVES AND MEASURED, INDICATED AND INFERRED RESOURCES

As a British Columbia corporation and a "reporting issuer" under Canadian securities laws, the Company is required to provide disclosure regarding its mineral properties in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. In accordance with NI 43-101, the Company uses the terms mineral reserves and resources as they are defined in accordance with the CIM Definition Standards on mineral reserves and resources (the "CIM Definition Standards") adopted by the Canadian Institute of Mining, Metallurgy and Petroleum.

The SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the United States Securities and Exchange Commission (the "SEC") under the U.S. Exchange Act. These amendments became effective February 25, 2019 (the "SEC Modernization Rules"). The SEC Modernization Rules have replaced the historical property disclosure requirements for mining registrants that were included in SEC Industry Guide 7 ("Guide 7"), which have been rescinded. The Company is not required to provide disclosure on its mineral properties under the SEC Modernization Rules as the Company is presently a "foreign issuer" under the U.S. Exchange Act and entitled to file continuous disclosure reports with the SEC under the MJDS Disclosure System between Canada and the United States.

The SEC Modernization Rules include the adoption of terms describing mineral reserves and mineral resources that are substantially similar to the corresponding terms under the CIM Definition Standards. As a result of the adoption of the SEC Modernization Rules, SEC will now recognize estimates of "measured mineral resources", "indicated mineral resources" and "inferred mineral resources". In addition, the SEC has amended its definitions of "proven mineral reserves" and "probable mineral reserves" to be substantially similar to the corresponding CIM Definitions.

- 3 -

United States investors are cautioned that while the above terms are substantially similar to CIM Definitions, there are differences in the definitions under the SEC Modernization Rules and the CIM Definition Standards. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as "proven reserves", "probable reserves", "measured mineral resources", "indicated mineral resources" and "inferred mineral resources" under NI 43-101 would be the same had the Company prepared the reserve or resource estimates under the standards adopted under the SEC Modernization Rules.

United States investors are also cautioned that while the SEC will now recognize "measured mineral resources", "indicated mineral resources" and "inferred mineral resources", investors should not to assume that any part or all of the mineralization in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. Mineralization described using these terms has a greater amount of uncertainty as to their existence and feasibility than mineralization that has been characterized as reserves. Accordingly, investors are cautioned not to assume that any "measured mineral resources", "indicated mineral resources", or "inferred mineral resources" that the Company reports are or will be economically or legally mineable.

Further, "inferred resources" have a greater amount of uncertainty as to their existence and as to whether they can be mined legally or economically. Therefore, United States investors are also cautioned not to assume that all or any part of the inferred resources exist. In accordance with Canadian rules, estimates of "inferred mineral resources" cannot form the basis of feasibility or other economic studies, except in limited circumstances where permitted under NI 43-101.

For the above reasons, information contained in this Annual Report and the documents incorporated by reference herein containing descriptions of our mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

NOTE TO UNITED STATES READERS REGARDING DIFFERENCES

BETWEEN UNITED STATES AND CANADIAN REPORTING PRACTICES

International Financial Reporting Standards

The Company is permitted under the MJDS to prepare this Annual Report in accordance with Canadian disclosure requirements, which are different from those of the United States.

The Company's Audited Consolidated Financial Statements that are incorporated by reference into this Registration Statement have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board (the "IASB").

DISCLOSURE CONTROLS AND PROCEDURES

Disclosure Controls and Procedures

Disclosure controls and procedures are defined in Rule 13a-15(e) under the Exchange Act to mean controls and other procedures of an issuer that are designed to ensure that information required to be disclosed by the issuer in the reports that it files or submits under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC's rules and forms and includes, without limitation, controls and procedures designed to ensure that such information is accumulated and communicated to the issuer's management, including its principal executive and principal financial officers, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure.

- 4 -

Management's Evaluation of Disclosure Controls and Procedures

As of the end of the period covered by this report, our management carried out an evaluation, with the participation of our Chief Executive Officer and Chief Financial Officer, of the effectiveness of our disclosure controls and procedures. Based upon that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that, as of the end of the period covered by this report, our disclosure controls and procedures, as defined in Rule 13a-15(e), were effective as at December 31, 2023.

See "Internal and Disclosure Controls Over Financial Reporting" on page 32 of the MD&A incorporated herein by reference.

INTERNAL CONTROLS OVER FINANCIAL REPORTING

Internal Control over Financial Reporting

Internal control over financial reporting is defined in Rule 13a-15(f) and 15d-15(f) of the Exchange Act as a process designed by, or under the supervision of, the issuer's principal executive and principal financial officers and effected by the issuer's board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles and includes those policies and procedures that:

• pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company;

• provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and

• provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the company's assets that may have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness of internal control over financial reporting to future periods are subject to risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Management's Report on Internal Control Over Financial Reporting

Management is responsible for establishing and maintaining adequate internal control over financial reporting (as such term is defined in Rule 13a-15(f) of the Exchange Act) for the Company.

With the participation of the CEO and CFO, management carried out an evaluation of the Company's internal control over financial reporting as of December 31, 2023. In making this evaluation, the Company's management used the framework established in Internal Control-Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). Based upon this evaluation, management concluded that the Company's internal control over financial reporting was effective as of December 31, 2023.

- 5 -

A copy of management's report on the effectiveness of our internal controls is included under "Management's Report on Internal Control Over Financial Reporting" on page 3 of our Audited Consolidated Financial Statements incorporated herein by reference.

Attestation Report of the Registered Public Accounting Firm

The Company is required to provide an attestation report of the Company's independent registered public accounting firm on internal control over financial reporting as of December 31, 2023. In this report, the Company's auditor, KPMG LLP, must state its opinion as to the effectiveness of the Company's internal control over financial reporting as of December 31, 2023. KPMG LLP has audited the Company's internal controls over financial reporting and has issued an attestation report on the Company's internal control over financial reporting as of December 31, 2023 which is included in our Audited Consolidated Financial Statements incorporated herein by reference.

No Changes in Internal Control Over Financial Reporting

There were no changes in the Company's internal control over financial reporting that occurred during the period covered by this Annual Report that have materially affected, or are reasonably likely to affect, the Company's internal control over financial reporting.

NOTICES PURSUANT TO REGULATION BTR

The Company did not send any notices required by Rule 104 of Regulation BTR during the year ended December 31, 2023 concerning any equity security subject to a blackout period under Rule 101 of Regulation BTR.

AUDIT AND RISK COMMITTEE

The disclosure provided under "Composition of Audit and Risk Committee" on page 124 of our AIF is incorporated herein by reference. The Company's Board of Directors has established a separately-designated Audit and Risk Committee of the Board in accordance with Section 3(a)(58)(A) of the Exchange Act. The Board has determined that each of the members of the Audit Committee is independent as determined under Rule 10A-3 of the Exchange Act and Section 803 of the NYSE American LLC Company Guide.

AUDIT AND RISK COMMITTEE FINANCIAL EXPERT

The Company's Board of Directors has determined that Peter Mitchell and Ron Thiessen, members of the Audit and Risk Committee of the Board, are audit committee financial experts (as that term is defined in Item 407 of Regulation S-K under the Exchange Act) and are independent directors under applicable laws and regulations and the requirements of the NYSE American Exchange.

PRINCIPAL ACCOUNTANT FEES AND SERVICES

The disclosure provided under "Principal Accountant Fees and Services" on page 125 of our AIF is incorporated herein by reference. This disclosure includes the fees paid by the Company to KPMG LLP (PCAOB ID: 85) of Vancouver, British Columbia, Canada for professional services rendered during each of the years ended December 31, 2023 and 2022.

- 6 -

AUDIT AND RISK COMMITTEE PRE-APPROVAL POLICIES AND PROCEDURES

The disclosure provided under "Audit and Risk Committee-Pre-Approval Policies and Procedures" on page 126 of our AIF is incorporated herein by reference.

OFF-BALANCE SHEET ARRANGEMENTS

The Company has not entered into any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company's financial condition, changes in financial condition, revenues, expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

CONTRACTUAL OBLIGATIONS

The disclosures provided under "Commitments and contingencies" on page 21 of our MD&A is incorporated herein by reference.

CODE OF ETHICS

The disclosure provided under "Code of Ethics" on page 125 of our AIF is incorporated herein by reference.

During the Company's fiscal year ended December 31, 2023, the Company did not (i) substantively amend its Code of Ethics or (ii) grant a waiver, including any implicit waiver, from any provision of its Code of Ethics with respect to any of the directors, executive officers or employees subject to it.

NYSE AMERICAN CORPORATE GOVERNANCE

The Company is subject to corporate governance requirements prescribed under applicable Canadian securities laws, rule and policies. The Company is also subject to corporate governance requirements prescribed by the listing standards of the NYSE American, and the rules and regulations promulgated by the SEC under the Exchange Act (including those applicable rules and regulations mandated by the Sarbanes-Oxley Act of 2002).

Section 110 of the NYSE American company guide permits NYSE American to consider the laws, customs and practices of foreign issuers in relaxing certain NYSE American listing criteria, and to grant exemptions from NYSE American listing criteria based on these considerations. A company seeking relief under these provisions is required to provide written certification from independent local counsel that the non-complying practice is not prohibited by home country law. A description of the significant ways in which the Company's governance practices differ from those followed by domestic companies pursuant to NYSE American standards is contained on the Company's website at www.tasekomines.com (under the ESG / Corporate Governance and Code of Ethics tab).

The Company's governance practices also differ from those followed by U.S. domestic companies pursuant to NYSE American listing standards in the following manner:

Board Meetings

Section 802(c) of the NYSE American Company Guide requires that the Board of Directors hold meetings on at least a quarterly basis. The Board of Directors of the Company is not required to meet on a quarterly basis under the laws of the Province of British Columbia.

- 7 -

Solicitation of Proxies

NYSE American requires the solicitation of proxies and delivery of proxy statements for all shareholder meetings, and requires that these proxies shall be solicited pursuant to a proxy statement that conforms to applicable SEC proxy rules. Since the Company is a foreign private issuer, the equity securities of the Company are exempt from the proxy rules set forth in Sections 14(a), 14(b), 14(c) and 14(f) of the Exchange Act. The Company solicits proxies in accordance with applicable rules and regulations in Canada.

Shareholders Approval for Dilutive Private Placement Financings

Section 713 of the NYSE American Company Guide requires that the Company obtain the approval of its shareholders for share issuances equal to 20 percent or more of presently outstanding shares for a price which is less than the greater of book or market value of the shares. This requirement does not apply to public offerings. There is no such requirement under British Columbia law or under the Company's home stock exchange rules (Toronto Stock Exchange ("TSX")) unless the dilutive financing:

(i) materially affects control of the issuer;

(ii) provides consideration to insiders in the aggregate of 10% or greater of the issuer's market capitalization or outstanding shares, or a non-diluted basis, where certain conditions are met; and

(iii) is in respect of private placement or an acquisition where the issuer will issue shares in excess of 25% of its presently outstanding shares, on a non-diluted basis.

The Company will seek a waiver from NYSE American's section 713 requirements should a dilutive private placement financing trigger the NYSE American shareholders' approval requirement in circumstances where the same financing does not trigger such a requirement under British Columbia law or under the TSX rules.

The Company believes that there are otherwise no significant differences between its corporate governance policies and those required to be followed by United States domestic issuers listed on the NYSE American. In particular, in addition to having a separate Audit and Risk Committee, the Company's Board of Directors has established a separately-designated Compensation Committee that materially meets the requirements for a compensation committee under section 805 of the NYSE American Company Guide, as currently in force.

Copies of the Company's corporate governance materials are available on the Company's website at www.tasekomines.com (under the ESG / Corporate Governance & Code of Ethics tab). In addition, the Company is required by National Instrument 58-101 of the Canadian Securities Administrators, Disclosure of Corporate Governance Practices, to describe its practices and policies with regard to corporate governance in management information circulars that are furnished to the Company's shareholders in connection with annual meetings of shareholders. Information on the Company's website is not incorporated by reference herein.

MINE SAFETY DISCLOSURE

Pursuant to Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 ("Dodd-Frank Act"), issuers that are operators, or that have a subsidiary that is an operator, of a coal or other mine in the United States are required to disclose in their periodic reports filed with the SEC information regarding specified health and safety violations, orders and citations, related assessments and legal actions, and mining-related fatalities under the regulation of the Federal Mine Safety and Health Administration under the Federal Mine Safety and Health Act of 1977.

- 8 -

The Company's operations in the United States were not subject to regulation by the Federal Mine Safety and Health Administration under the Federal Mine Safety and Health Act of 1977 during the fiscal year ended December 31, 2023.

UNDERTAKING

The Registrant undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

CONSENT TO SERVICE OF PROCESS

The Company previously filed an Appointment of Agent for Service of Process and Undertaking on Form F-X signed by the Company and its agent for service of process with respect to the class of securities in relation to which the obligation to file this annual report arises.

- 9 -

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Company certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Date: March 27, 2024 | TASEKO MINES LIMITED | |

| By: | /s/ Bryce Hamming | |

| Bryce Hamming | ||

| Chief Financial Officer | ||

- 10 -

EXHIBIT INDEX

(1) Filed as an exhibit to this Annual Report on Form 40-F

POLICY FOR THE RECOVERY OF ERRONEOUSLY AWARDED INCENTIVE

BASED COMPENSATION (the "Recovery Policy")

1. GENERAL PROVISIONS

1.1 Purpose

This Recovery Policy has been adopted by resolution of the Board (as hereinafter defined) in accordance with certain listing standards of the NYSE American stock exchange mandated by Rule 10D-1 (as hereinafter defined), to facilitate reasonably prompt recovery by the Company of the amount of any Incentive-Based Compensation that is deemed to have been erroneously awarded in the event that the Company is required to restate its financial statements due to material non-compliance with any financial reporting requirement under relevant Securities Laws (as hereinafter defined).

1.2 Definitions

In this Recovery Policy, the following terms will have the following meanings:

(a) "Accounting Restatement" means an accounting restatement due to material noncompliance of the Company with any financial reporting requirement under the Securities Laws, including any required accounting restatement to correct an error in previously issued financial statements that is material to the previously issued financial statements, or that would result in a material misstatement if the error were corrected in the current period or left uncorrected in the current period;

(b) "Board" means the Board of Directors of the Company;

(c) "Canadian Securities Laws" means all applicable securities laws of each of the provinces of Canada in which the Company is a "reporting issuer", and the respective rules and regulations made and forms prescribed under such laws, together with all applicable published instruments, policy statements, blanket orders, rulings and notices adopted by the securities regulatory authorities in such provinces;

(d) "Company" means Taseko Mines Limited;

(e) "Compensation Committee" means the Compensation Committee of the Board;

(f) "Effective Date" means the effective date of this Recovery Policy, being the 31 day of October, 2023;

(g) "Erroneously Awarded Incentive-Based Compensation" means that portion of any Incentive-Based Compensation that has been paid to an Executive Officer and is recoverable under Section 4.1 of this Recovery Policy, as such Erroneously Awarded Incentive-Based Compensation is determined under this Recovery Policy; (h) "Exchange Act" means the United States Securities Exchange Act of 1934, as amended;

(i) "Executive Officer" means any individual deemed to be an "executive officer" of the Company under Rule 10D-1. For the avoidance of doubt, the identification of an executive officer for purposes of this Recovery Policy shall include each executive officer who is or was identified pursuant to Item 401(b) of Regulation S-K or Item 6.A of Form 20-F, as applicable, as well as the principal financial officer and principal accounting officer (or, if there is no principal accounting officer, the controller).

(j) "Financial Reporting Measures" means any measures that are determined and presented in accordance with the accounting principles used in preparing the Company's financial statements, and any measures derived wholly or in part from such measures whether or not the measure is presented within the financial statements or included in a filing with the SEC. For greater certainty, stock price and TSR are included in the definition of Financial Reporting Measures;

(k) "Incentive-Based Compensation" means any compensation that is granted, earned or vested based wholly or in part upon the attainment of a Financial Reporting Measure;

(l) "MJDS" means the United States/Canada multi-jurisdictional disclosure system;

(m) "NYSE American" means the NYSE American LLC:

(n) "Received" means, in the context of Incentive-Based Compensation, the actual or deemed receipt in the Company's fiscal period during which the Financial Reporting Measure specified in the Incentive-Based Compensation is attained, even if the payment or grant of the Incentive-Based Compensation occurs after the end of that period;

(o) "Recovery Period" has the meaning set forth in Section 4.4;

(p) "Recovery Policy" means this policy for the recovery of erroneously awarded executive compensation;

(q) "Rule 10D-1" means Rule 10D-1 adopted by the SEC under the Exchange Act;

(r) "SEC" means the United States Securities and Exchange Commission;

(s) "SEC Final Release" means the final release no. 34-96159 of the SEC entitled "Listing Standards of Recovery of Erroneously Awarded Compensation" in respect of the adoption of Rule 10D-1 pursuant to the requirements of Section 10D of the Exchange Act; (t) "Securities Laws" means the Exchange Act and the U.S. Securities Act and, to the extent that the Company has filed any of its financial statements with the SEC under the Exchange Act in reliance on the MJDS, Canadian Securities Laws;

(u) "TSR" means total shareholder return; and

(v) "U.S. Securities Act" means the United States Securities Act of 1933, as amended;

2. ADMINISTRATION

2.1 Administration

This Recovery Policy will be administered by the Compensation Committee which will be empowered to, with consideration of applicable Securities Laws,

(a) interpret and administer this Recovery Policy;

(b) make determinations as to whether any Incentive-Based Compensation that has been Received by the current and former Executive Officers of the Company constitutes Erroneously Awarded Incentive-Based Compensation in the event of an Accounting Restatement;

(c) take action to enforce on behalf of the Company any recovery of any Erroneously Awarded Incentive-Based Compensation pursuant to the provisions of this Recovery Policy, and

(d) make any other determinations that the Compensation Committee deems necessary or desirable to give effect to the objectives of this Recovery Policy, and

(e) periodically review legislative developments that may have an impact on this Recovery Policy, and report to the Board any recommendations.

2.2 Interpretations

This Recovery Policy is intended to be a "Recovery Policy" for the purposes of Section 811 of the NYSE American Company Manual and will be interpreted by the Compensation Committee consistent with the SEC's interpretation of Rule 10D-1, including the guidance of the SEC set forth in the SEC Final Release and any other applicable law, regulation, rule or interpretation of the SEC or NYSE American promulgated or issued in connection therewith. This Recovery Policy is in addition to the requirements of Section 304 of the Sarbanes-Oxley Act of 2002 that are applicable to the Company's chief executive officer and chief financial officer.

2.3 Compliance

The Compensation Committee may require that any employment agreement, offer letter, compensation plan, equity award agreement, or any other agreement entered into on or after the Effective Date require an Executive Officer to agree to abide by the terms of this Recovery Policy. Further, the Compensation Committee may required each Executive Officer to acknowledge this Recovery Policy through execution of the form of acknowledgement attached hereto as Exhibit 1 (or such other form as approved from time-to-time by the Compensation Committee).

3. SCOPE AND INTERPRETATION OF THIS RECOVERY POLICY

3.1 Effective Period

This Recovery Policy will be applied to all Incentive Based Compensation that is Received by an Executive Officer on or after the Effective Date.

3.2 Scope of Executive Officers Subject to Recovery Policy

The Compensation Committee will determine from time-to-time the individuals that are deemed to be subject to the Recovery Policy by virtue of being considered an Executive Officer of the Company under Rule 10D-1.

3.3 Scope of Accounting Restatements Subject to Recovery Policy

The Accounting Restatements that will trigger the obligation to recover Erroneously Awarded Incentive-Based Compensation will include any restatement of any of the financial statements of the Company filed with the SEC under the Exchange Act to correct an error in previously issued financial statements that is material to the previously issued financial statements, or that would result in a material misstatement if the error were corrected in the current period or left uncorrected in the current period. For clarity, Accounting Restatements include for the purposes of this Recovery Policy both:

(a) big "R" restatements, being restatements to correct an error material to previously issued financial statements, and

(b) little "r" restatements, being restatements to correct errors that were not material to those previously issued financial statements, but would result in a material misstatement if (i) the errors were left uncorrected in the current report or (ii) the error correction was recognized in the current period.

3.4 Determination of When Incentive-Based Compensation is Received

Incentive-Based Compensation will be deemed Received in the fiscal period during which the Financial Reporting Measure specified in the Incentive-Based Compensation award was attained, even if the payment or grant occurs after the end of that period.

4. RECOVERY OF ERRONEOUSLY AWARDED INCENTIVE-BASED COMPENSATION

4.1 Recovery

In that event that the Company is required to prepare an Accounting Restatement, the Company will reasonably promptly take action to recover the amount of any Erroneously Awarded Incentive-Based Compensation that has been Received by each applicable Executive Officer:

(a) after beginning services as an Executive Officer;

(b) who served as Executive Officer at any time during the performance period for that Incentive-Based Compensation;

(c) while the Company has a class of securities listed on NYSE American (or another national securities exchange in the United States or Nasdaq); and

(d) during the three completed fiscal years immediately preceding the date on which the Company was required to prepare the Accounting Statement, as this three year period is determined under Section 4.4 below.

4.2 No Fault Basis

Recovery will be required on a "no fault" basis, without regard to whether an Executive Officer engaged in any misconduct or whether the Executive Officer was responsible for the erroneous financial statements that led to the Accounting Restatement.

4.3 Trigger for Recovery of Erroneously Award Compensation

The date on which the Company is deemed to be required to prepare an Accounting Statement for the purposes of determining the Recovery Period under Section 4.1 will be the earlier to occur of:

(a) the date that the Board or a committee of the Board concludes, or reasonably should have concluded that the Company, is required to prepare an Accounting Restatement, or

(b) the date that a court, regulator or other legally authorized body directs the Company to prepare an Accounting Restatement.

4.4 Determination of Recovery Period

The recovery period for the determination of Erroneously Awarded Incentive-Based Compensation (the "Recovery Period") will determined as the three completed fiscal years immediately preceding the date that the Company is required to prepare an Accounting Restatement, as that date is determined under Section 4.3. In the event of a change in the financial year of the Company, the Recovery Period will also include any transition period that results from a change in the Company's fiscal year within or immediately following those three completed fiscal years, provided that a transition period between the last day of the Company's previous fiscal year end and the first day of its new fiscal year that comprises a period of nine to 12 months would be deemed a completed fiscal year.

4.5 Scope of Incentive Based Compensation Subject to Recovery

Recovery will be made against each current and former Executive Officer who has Received Incentive-Based Compensation during the three year Recovery Period to the extent that such Incentive-Based Compensation is determined to be Erroneously Awarded Incentive-Based Compensation. Recovery of Incentive-Based Compensation received while an individual was serving in a non-executive capacity prior to becoming an Executive Officer is not subject to this Recovery Policy and recovery will not be required. An award of incentive-based compensation granted to an individual before the individual becomes an Executive Officer will be subject to this Recovery Policy, so long as the Incentive-Based Compensation was received by the individual at any time during the performance period after beginning service as an Executive Officer.

4.6 Determination of Amount of Erroneously Awarded Compensation

The amount of any Erroneously Awarded Incentive-Based Compensation to be recovered under Section 4.1 will be determined as follows for each applicable Executive Officer:

(a) the amount of Incentive-Based Compensation that has been Received by the Executive Officer during the Recovery Period to which this Recovery Policy applies, less

(b) the amount of the Incentive-Based Compensation that would have been received in respect of the Recovery Period had the Incentive-Based Compensation been determined based on the restated amount.

4.7 Compensation Based on Stock Price.

Erroneously Awarded Incentive-Based Compensation will include any Incentive-Based Compensation that was based on stock price or TSR to the extent that the Incentive-Based Compensation was inaccurate as a result of the Accounting Restatement. For Incentive-Based Compensation based on stock price or TSR, where the amount of Erroneously Awarded Incentive-Based Compensation is not subject to mathematical recalculation directly from the information in the Accounting Restatement:

(a) the amount must be based on a reasonable estimate of the effect of the Accounting Restatement on the stock price or TSR upon which the Incentive-Based Compensation was received, and

(b) the amount of the Incentive-Based Compensation that would have been received in respect of the Recovery Period had the Incentive-Based Compensation been determined based on the restated amount.

4.8 Notice

The Compensation Committee shall promptly notify each Executive Officer with a written notice containing the amount of any Erroneously Awarded Compensation and a demand for repayment or return of such compensation.

4.9 No Deduction for Taxes

The amount of any Erroneously Awarded Incentive-Based Compensation will be computed without regard to any taxes paid by the Executive Officer.

4.10 No Duplication

To the extent that the Executive Officer has already reimbursed the Company for any Erroneously Awarded Compensation Received under any duplicative recovery obligations established by the Company or applicable law, it shall be appropriate for any such reimbursed amount to be credited to the amount of Erroneously Awarded Compensation that is subject to recovery under this Recovery Policy.

4.11 No Requirement for Additional Compensation

Notwithstanding anything in this Recovery Policy, in no event will the Company be required to award any Executive Officer an additional payment or other compensation if the Accounting Restatement would have resulted in the grant, payment or vesting of Incentive-Based Compensation that is greater than the Incentive-Based Compensation actually received by the affected Executive Officer. The recovery of Erroneously Awarded Incentive-Based Compensation is not dependent on if or when the restatement is filed.

5. REPORTING

5.1 Reporting of Erroneously Award Compensation

In the event of an Accounting Restatement pursuant to which the Compensation Committee has considered whether recovery of any Erroneously Awarded Incentive-Based Compensation is required, the Compensation Committee will prepare a report to management of the Company detailing the information required to be reported by the Company with respect to such Accounting Restatement on the Form 40-F or other form of annual report to be filed by the Company under the Exchange Act for the fiscal year in which the Accounting Restatement occurred and in any other filing required to be made by the Company under Securities Laws.

5.2 Documentation

The Compensation Committee will maintain documentation as to the determination of the amount of any Erroneously Awarded Incentive-Based Compensation, including any reasonable estimates made during the calculation process, and any efforts undertaken to recover Erroneously Awarded Incentive-Based Compensation. The Company will provide this information to NYSE American upon its request.

Without limiting the above, the Company will comply will all disclosure, documentation and records requirements relating to this Recovery Policy under Section 10D of the Exchange Act, the NYSE American Company Guide and the filings required to be made by the Company under the Exchange Act.

6. ENFORCEMENT OF RECOVERY

6.1 Requirement to Recover

Upon a determination by the Compensation Committee that the Company is obligated to recover Erroneously Awarded Incentive-Based Compensation under Section 4.1, the Company will take steps to recover such Erroneously Awarded Incentive-Based Compensation other than in circumstances where each of (a) and (b) below apply:

(a) one of the following circumstances exists:

(i) the direct expense paid to a third party to assist in enforcing this Recovery Policy would exceed the amount to be recovered, provided that before concluding that it would be impracticable to recover any amount of Erroneously Awarded Incentive-Based Compensation based on expense of enforcement, the Company has made a reasonable attempt to recover such Erroneously Awarded Incentive-Based Compensation and documented such reasonable attempt(s) to recover (which documentation will be provided to NYSE American at the request of NYSE American);

(ii) recovery would violate British Columbia or Canadian law where that law was adopted prior to November 28, 2022, provided that the Company has obtained an opinion of its Canadian counsel, in a form acceptable to NYSE American, that recovery would result in such a violation, and such opinion is provided to NYSE American; or

(iii) recovery would likely cause an otherwise tax-qualified retirement plan, under which benefits are broadly available to employees of the registrant, to fail to meet the requirements of 26 U.S.C. 401(a)(13) or 26 U.S.C. 411(a) and regulations thereunder; and (b) the Compensation Committee, or a majority of the independent directors of the Board, has made a determination that recovery would be impracticable.

6.2 Deferred Payment Plans

The Compensation Committee may consider the establishment of a deferred payment where recovery is required from an Executive Officer and where the deferred payment plan allows the Executive Officer to repay the Erroneously Awarded Incentive-Based Compensation as soon as possible without unreasonable economic hardship to the Executive Officer, depending on the facts and circumstances; provided that any such deferred payment plan shall be narrowly tailored to the Erroneously Awarded Incentive-Based Compensation being recovered so as not to constitute a personal loan to the Executive Officer that is prohibited by Section 13(k) of the Exchange Act.

6.3 Recovery of Costs

If an Executive Officer fails to repay all Erroneously Awarded Incentive-Based Compensation when due, the Company will take all actions reasonable and appropriate to recover the Erroneously Awarded Incentive-Based Compensation from the Executive Officer, and in that case the Executive Officer will be required to reimburse the Company for all reasonable expenses incurred in recovering the Erroneously Awarded Incentive-Based Compensation from the Executive Officer.

6.4 Other Legal Remedies

Any right of recovery under this Recovery Policy is in addition to, and not in lieu of, any other remedies or rights of recovery that may be available to the Company under applicable law, regulation or rule, or under the terms of any similar policy or agreement in any employment agreement, offer letter, compensation plan, equity award agreement, or similar agreement and any other legal remedies available to the Company.

This Recovery Policy does not preclude the Company from taking any other action to enforce an Executive Officer's obligations to the Company or limit any other remedies that the Company may have available to it and any other actions that the Company may take, including termination of employment, institution of civil proceedings, or reporting of any misconduct to appropriate government authorities.

7. PROHIBITION ON INDEMNIFICATION

7.1 Prohibition on Indemnification

The Company shall not be permitted to indemnify or insure any Executive Officer against (i) the loss of any Erroneously Awarded Compensation that is repaid, returned or recovered pursuant to the terms of this Policy, or (ii) any claims relating to the Company's enforcement of its rights under this Recovery Policy. Further, the Company shall not enter into any agreement that exempts any Incentive-based Compensation that is granted, paid or awarded to an Executive Officer from the application of this Recovery Policy or that waives the Company's right to recovery of any Erroneously Awarded Compensation, and this Recovery Policy shall supersede any such agreement (whether entered into before, on or after the Effective Date of this Recovery Policy).

7.2 Insurance

The Company will not purchase or pay or reimburse any Executive Officer for any insurance policy to cover losses incurred by any Executive Officer under this Recovery Policy.

7.3 Other Recovery Rights

This Recovery Policy shall be binding and enforceable against all Executive Officers and, to the extent required by applicable law or guidance from the SEC or NYSE American, their beneficiaries, heirs, executors, administrators or other legal representatives. The Compensation Committee intends that this Policy will be applied to the fullest extent required by applicable law. Any employment agreement, equity award agreement, compensatory plan or any other agreement or arrangement with an Executive Officer shall be deemed to include, as a condition to the grant of any benefit thereunder, an agreement by the Executive Officer to abide by the terms of this Recovery Policy. Any right of recovery under this Recovery Policy is in addition to, and not in lieu of, any other remedies or rights of recovery that may be available to the Company under applicable law, regulation or rule or pursuant to the terms of any policy of the Company or any provision in any employment agreement, equity award agreement, compensatory plan, agreement or other arrangement.

8. AUTHORITY OF THE COMPENSATION COMMITTEE

8.1 Engagement of Professional Advisors

In addition to any authority provided under its charter, the Compensation Committee will have the authority to engage and retain independent legal counsel, independent accounting advisors and any outside professional advisor that it determines necessary to carry out its duties, at the expense of the Company, without the Board's approval and at any time, and has the authority to determine any such advisor's fees and other retention terms.

8.2 Oversight

In the event that the Company is required to recover any Erroneously Awarded Incentive-Based Compensation under this Recovery Policy, such recovery efforts will be undertaken with the supervision of the office of the General Counsel under oversight of the Compensation Committee, provided that Compensation Committee will directly supervise such efforts in the event of that the General Counsel is an Executive Officer who is subject to recovery.

8.3 Review

The Compensation Committee will periodically review legislative developments, regulatory initiatives, and similar matters relating to Canadian Securities Laws and Securities Laws that may have an impact on this Recovery Policy, and report to the Board any recommendations it may have concerning the Recovery Policy.

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2023

AS AT MARCH 27, 2024

Table of Contents

Figures

| Figure 1: Location of Taseko's Properties | 16 |

Appendix A

| Audit and Risk Committee Charter |

Introductory Notes

Forward-Looking Statements

This Annual Information Form ("AIF"), including the documents incorporated by reference, contains forward-looking statements and forward-looking information (collectively referred to as "forward-looking statements") which may not be based on historical fact, including without limitation statements regarding our expectations in respect of future financial position, business strategy, future production, reserve potential, feasibility of development projects, exploration drilling, exploitation activities, events or developments that we expect to take place in the future, projected costs and plans and objectives, financial capacity to complete anticipated development projects, and anticipated effects of changes in taxation levels on the value of development projects. Often, but not always, forward-looking statements can be identified by the use of the words "believes", "may", "plan", "will", "estimate", "scheduled", "continue", "anticipates", "intends", "expects", "aim" and similar expressions.

Such statements reflect our current views with respect to future events and are subject to risks and uncertainties. These statements are necessarily based upon a number of estimates and assumptions that are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. Many factors could cause our actual results, performance or achievements to be materially different from any future results, performance, or achievements that may be expressed or implied by such forward-looking statements, including, among others:

- 3 -

- 4 -

Such information is included, among other places, in this AIF under the headings "Taseko's Business" and "Risk Factors".

Should one or more of these risks and uncertainties materialize, or should underlying factors or assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements. Material factors or assumptions involved in developing forward-looking statements include, without limitation, that:

- 5 -

- 6 -

These factors should be considered carefully and you are cautioned not to place undue reliance on any forward-looking statements. You are also cautioned that the foregoing list of risk factors is not exhaustive and it is recommended that you carefully read the more complete discussion of risks and uncertainties facing the Company included under "Risk Factors" in this AIF.

Although we believe that the expectations conveyed by the forward-looking statements are reasonable based on the information available to Taseko on the date such statements were made, no assurances can be given as to future results, approvals or achievements. The forward-looking statements contained in this AIF are expressly qualified by this cautionary statement. Taseko disclaims any duty to update any of the forward-looking statements to conform such statements to actual results or to changes in Taseko's expectations except as otherwise required by applicable law.

Additional Financial Information

Additional information regarding Taseko is available in the audited consolidated financial statements, together with the auditor's report thereon, and MD&A for the Company for the year ended December 31, 2023. The financial statements are available for review on the System for Electronic Document Analysis and Retrieval ("SEDAR+") website at www.sedarplus.ca. All financial information in this AIF is prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board and expressed in Canadian dollars.

Non-GAAP Performance Measures

This AIF may include the following non-GAAP performance measures: (i) total operating costs and site operating costs, net of by-product credits; (ii) total site costs; (iii) adjusted net income (loss) and adjusted EPS; (iv) adjusted EBITDA; and (v) earnings from mining operations before depletion and amortization; and (vi) site operating costs per ton milled. These measures may differ from those used by, and may not be comparable to such measures as reported by, other issuers. The Company believes that these measures are commonly used by certain investors, in conjunction with conventional IFRS measures, to enhance their understanding of the Company's performance. These measures have been derived from the Company's financial statements and applied on a consistent basis. See "Non-GAAP Performance Measures" in our MD&A for the year ended December 31, 2023 for a reconciliation of these measures to the most directly comparable IFRS measure.

Currency and Metric Equivalents

The Company's accounts are maintained in Canadian dollars and all dollar amounts herein are expressed in Canadian dollars unless otherwise indicated.

- 7 -

The following factors for converting Imperial measurements into metric equivalents are provided:

| To Convert from Imperial | To Metric | Multiply by |

| acres | hectares | 0.405 |

| feet | metres | 0.305 |

| miles | kilometres | 1.609 |

| tons (2,000 pounds) | tonnes | 0.907 |

| ounces (troy)/ton | grams/tonne | 34.286 |

Abbreviations

In this AIF, the following capitalized terms have the defined meanings set forth below:

| 2023 MD&A | Our Management's Discussion and Analysis for the year ended December 31, 2023 dated March 7, 2024. |

| ASCu | The weight percentage of copper per unit weight of rock that is readily acid soluble, including native copper. |

| ADEQ | Arizona Department of Environmental Quality. |

| APP and TAPP | Aquifer Protection Permit and Temporary Aquifer Protection Permit. |

| Common Shares | The Company's common shares without par value, being the only class or kind of the Company's authorized capital. |

| Carbonatite Deposit | Carbonatite deposits are igneous rocks largely consisting of the carbonate minerals calcite and dolomite, which contain the niobium mineral pyrochlore, rare earth minerals or copper sulphide minerals. |

| Concentrator | A type of mineral processing facility that converts raw ore from the mine into a metal concentrate that can then be sold to a smelter for further processing. |

| EPA | U.S. Environmental Protection Agency. |

| Epithermal Deposit | A mineral deposit formed at low temperature (50 to 200°C), usually within one kilometre of the earth's surface, often as structurally controlled veins. |

| Florence Copper | The Florence Copper mine, an ISCR copper mine to be developed by the Company in Florence, Arizona |

- 8 -

| Flotation | Flotation is a method of mineral separation whereby, after crushing and grinding ore, froth created in a slurry by a variety of reagents causes some finely crushed minerals to float to the surface where they are skimmed off. |

| Gibraltar | The Gibraltar Mine, an open-pit copper mine located near Williams Lake, British Columbia. |

| IFRS | International Financial Reporting Standards as issued by the International Accounting Standards Board. |

| ISCR | In-situ copper recovery. |

| LSE | The London Stock Exchange being one of the three stock exchanges (together with the NYSE American and TSX) on which the Common Shares are listed. |

| Mineral Deposit | A deposit of mineralization, which may or may not be ore. |

| Mineral Symbols | Ag - silver; Au - gold; Cu - copper; Pb - lead; Zn - zinc; Mo - molybdenum; and Nb - niobium. |

| NSR | Net smelter return, a general proxy for the gross value of metals derived from concentrates delivered to a smelter for refining. |

| NYSE American | The NYSE American, being one of the three stock exchanges (together with the LSE and TSX) on which the Common Shares are listed. |

| PLS | Pregnant leach solutions containing copper. |

| PTF | The production test facility, a 24-well ISCR operation designed to prove the feasibility of extracting copper at Florence Copper using in-situ mining methods. |

| Porphyry Deposit | A type of mineral deposit in which ore minerals are widely disseminated, generally of low grade but large tonnage. |

| Semi-autogenous Grinding ("SAG") | SAG mills are essentially autogenous mills, but utilize grinding balls to aid in grinding like in a ball mill. A SAG mill is generally used as a primary or first stage grinding solution. |

- 9 -

| Solvent Extraction/ Electrowinning ("SX/EW") | Solvent extraction is the technique of transferring a solute from one solution to another; for example, when copper oxide is dissolved into solution, copper becomes the solute. Electrowinning is the process in which an electric current flow between a pair of electrodes (anode & cathode) in a solution containing metal ions (electrolyte). Metal is deposited on the cathode in accordance with the metal's ability to gain or lose electrons. Since ion deposition is selective, the cathode product is generally high grade and requires little further refining. |

| Taseko or the Company | Taseko Mines Limited, including its subsidiaries, unless the context requires otherwise. |

| TSX | The Toronto Stock Exchange, being one of the three stock exchanges (together with the LSE and NYSE American) on which the Company's Common Shares are listed. |

| UIC | Underground Injection Control permit. |

Resource and Reserve Categories (Classifications) Used in this AIF.

The discussion of mineral deposit classifications in this AIF adheres to the resource/reserve definitions and classification criteria developed by the Canadian Institute of Mining, Metallurgy and Petroleum (the "CIM Council") as required reporting standards in Canada and in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). Estimated mineral resources fall into two broad categories dependent on whether their economic viability has been established and these are namely "resources" (economic viability not established) and "reserves" (viable economic production is feasible). Resources are sub-divided into categories depending on the confidence level of the estimate based on level of detail of sampling and geological understanding of the deposit. The categories, from lowest confidence to highest confidence, are inferred resource, indicated resource and measured resource. Similarly, reserves are sub-divided by order of confidence into probable (lowest) and proven (highest). These classifications can be more particularly described as follows in accordance with the CIM Definition Standards on Mineral Resources and Reserves (the "2014 CIM Standards") adopted by the CIM Council on May 10, 2014:

A "Feasibility Study" is a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable modifying factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate, at the time of reporting, that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a pre-feasibility study.

- 10 -

A "Mineral Resource" is a concentration or occurrence of solid material of economic interest in or on the Earth's crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

An "Inferred Mineral Resource" is that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply, but not verify geological, and grade or quality continuity. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

An "Indicated Mineral Resource" is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource and may only be converted to a Probable Mineral Reserve.

A "Measured Mineral Resource" is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated Mineral Resource or an Inferred Mineral Resource. It may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve.

A "Mineral Reserve" is the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The U.S. Securities and Exchange Commission require permits in hand or their issuance imminent to classify mineralized material as reserves.

- 11 -

A "Pre-Feasibility study" is a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the modifying factors and the evaluation of any other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the mineral resource may be converted to a mineral reserve at the time of reporting. A pre-feasibility is at a lower confidence level than a feasibility study.

A "Probable Mineral Reserve" is the economically mineable part of an Indicated Mineral Resource, and in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve.

A "Proven Mineral Reserve" is the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the Modifying Factors.

"Modifying Factors" are considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

Cautionary Note to United States Investors Concerning Estimates of Reserves and Measured, Indicated and Inferred Resources

The disclosure in this AIF, including the documents incorporated by reference herein, uses terms that comply with reporting standards in Canada in accordance with NI 43-101 and the 2014 CIM Standards. NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all reserve and resource estimates contained in or incorporated by reference in this AIF have been prepared in accordance with NI 43-101 and the 2014 CIM Standards.

The U.S. Security and Exchange Commission ("SEC") has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC under the U.S. Exchange Act, effective February 25, 2019 (the "SEC Modernization Rules"). The SEC Modernization Rules replaced the historical property disclosure requirements for mining registrants that were included in SEC Industry Guide 7.

The SEC Modernization Rules include the adoption of definitions of terms, which are "substantially similar" to the corresponding terms under the 2014 CIM Standards that are presented above under "Resource and Reserve Categories (Classifications) Used in this AIF".

- 12 -

We are not required to provide disclosure on our mineral properties under the SEC Modernization Rules as we are presently a "foreign issuer" under the U.S. Exchange Act and entitled to file continuous disclosure reports with the SEC under the Multijurisdictional Disclosure System ("MJDS") between Canada and the United States. Accordingly, we are entitled to provide disclosure on our mineral properties in accordance with NI 43-101 disclosure standards and 2014 CIM Standards. However, if we either cease to be a "foreign issuer" or cease to be able to or entitled to file reports under the MJDS, then we will be required to provide disclosure on our mineral properties under the SEC Modernization Rules. Accordingly, United States investors are cautioned that the disclosure that we provide on our mineral properties in this AIF and under our continuous disclosure obligations under the U.S. Exchange Act may be different from the disclosure that we would otherwise be required to provide as a U.S. domestic issuer or a non-MJDS foreign issuer under the SEC Modernization Rules.

United States investors are cautioned that while the above terms under the SEC Modernization Rules are "substantially similar" to 2014 CIM Standards, there are differences in the definitions under the SEC Modernization Rules and the 2014 CIM Standards. Accordingly, there is no assurance any resources and reserves that we may report as "measured mineral resources", "indicated mineral resources" and "inferred mineral resources" and "proven mineral reserves" and "probable mineral reserves" under NI 43-101 would be the same had we prepared these estimates under the standards adopted under the SEC Modernization Rules.

United States investors are also cautioned that while the SEC now recognizes "measured mineral resources", "indicated mineral resources" and "inferred mineral resources", investors should not assume that any part or all of the mineral deposits in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. Mineralization described by these terms has a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Accordingly, investors are cautioned not to assume that any "measured mineral resources", "indicated mineral resources", or "inferred mineral resources" that we report in this AIF are or will be economically or legally mineable.

Further, "inferred resources" have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. Therefore, United States investors are also cautioned not to assume that all or any part of the inferred resources exist. In accordance with Canadian rules, estimates of "inferred mineral resources" cannot form the basis of feasibility or other economic studies, except in limited circumstances where permitted under NI 43-101.

For the above reasons, information contained in this AIF and the documents incorporated by reference herein containing descriptions of our mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

- 13 -

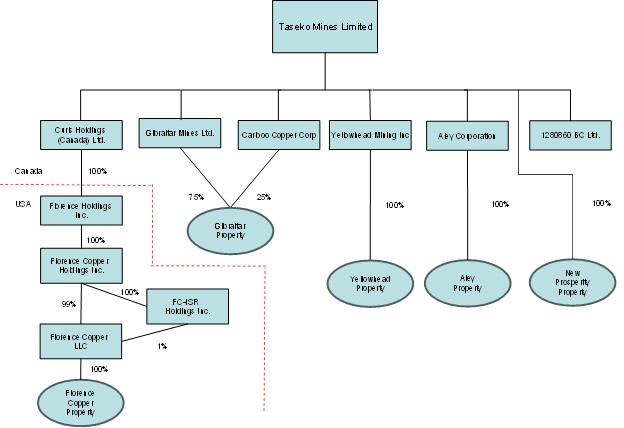

Corporate Structure

Taseko Mines Limited was incorporated on April 15, 1966, pursuant to the Company Act (British Columbia). This corporate legislation was superseded in 2004 by the British Columbia Business Corporations Act which is now the corporate law statute that governs us. Our registered office is located at Suite 1500, 1055 West Georgia Street, Vancouver, British Columbia, V6E 4N7, and our head office is located at Suite 1200, 1040 West Georgia Street, Vancouver, British Columbia, V6E 4H1.

The following is a list of the Company's principal subsidiaries:

| Subsidiary | Jurisdiction of Incorporation | Ownership |

| Gibraltar Mines Ltd. 1 | British Columbia | 100% |

| Cariboo Copper Corporation 2 | British Columbia | 100% |

| Curis Holdings (Canada) Ltd. 3 | British Columbia | 100% |

| Florence Holdings Inc. 3 | Nevada, USA | 100% |

| Florence Copper Holdings Inc. 3 | Nevada, USA | 100% |

| FC-ISR Holdings Inc. 3 | Nevada, USA | 100% |

| Florence Copper LLC 3 | Nevada, USA | 100% |

| Yellowhead Mining Inc. | British Columbia | 100% |

| Aley Corporation | Canada | 100% |

1.Taseko owns 100% of Gibraltar Mines Ltd., which owns 75% of the Gibraltar Joint Venture.

2.Taseko owns 100% of Cariboo Copper Corporation, which owns 25% of the Gibraltar Joint Venture. Taseko acquired 50% share ownership of Cariboo Copper Corporation on March 15, 2023 and acquired the remaining 50% on March 25, 2024.

3.Taseko owns 100% of Curis Holdings (Canada) Ltd., which owns 100% of Florence Holdings Inc., which owns 100% of Florence Copper Holdings Inc., which owns 99% of Florence Copper LLC and 100% of FC-ISR Holdings Inc. (which holds the remaining 1% of Florence Copper LLC).

- 14 -

Gibraltar Joint Venture

On March 31, 2010, we established an unincorporated joint venture ("JV") between Gibraltar Mines Ltd., and Cariboo Copper Corp. ("Cariboo") over the Gibraltar copper and molybdenum mine (the "Gibraltar Mine" or "Gibraltar"), whereby Cariboo acquired a 25% interest in the Gibraltar Mine and we retained a 75% interest with Gibraltar Mines Ltd. Under the related Joint Venture Formation Agreement ("JVFA"), the Company contributed to the Joint Venture substantially all assets and obligations pertaining to the Gibraltar Mine, and Cariboo paid the Company $187 million to obtain its 25% interest in the JV. Gibraltar Mines Ltd. continued to be the operator of the Gibraltar Mine under the Joint Venture Operating Agreement (the "JVOA") which is filed at www.sedarplus.ca. Cariboo was originally a Japanese consortium jointly owned by Sojitz Corporation ("Sojitz") (50%), Dowa Metals & Mining Co., Ltd. ("Dowa") (25%) and Furukawa Co., Ltd. ("Furukawa") (25%).

On March 15, 2023, the Company acquired Sojitz Corporation's 50% interest in Cariboo giving Taseko a further 12.5% indirect interest in Gibraltar, bringing its total effective interest to 87.5%.

On March 25, 2024, the Company purchased the remaining 50% interest in Cariboo from Dowa and Furukawa, bringing its total interest in Cariboo to 100% and therefore its total effective interest in Gibraltar to 100% as of the date of this AIF.

- 15 -

Taseko's Business

Taseko is a British Columbia incorporated copper mining company, headquartered in Vancouver, Canada, and listed on the TSX, the NYSE American and the LSE.

Our principal operating asset is our wholly-owned Gibraltar Mine, a large copper mine located in central British Columbia. We are also currently constructing our 100% owned Florence Copper mine in Arizona, which is expected to commence copper production in the fourth quarter of 2025. Florence Copper is expected to be a low-cost copper producer and also one of the greenest sources of copper globally. In addition, we have several wholly-owned advanced-stage development projects. The location of our properties in British Columbia, Canada, and the Florence Copper property in Arizona, United States are shown in the map below.

Taseko's mineral properties are summarized in the table below.

| Project/Mine | Ownership Interest | Location | Principal Mineralization |

| Gibraltar Mine | 100% | British Columbia | Copper/ Molybdenum/ Silver |

| Florence Copper | 100% | Arizona, USA | Copper |

| Yellowhead | 100% | British Columbia | Copper/ Gold/ Silver |

| New Prosperity | 100% | British Columbia | Copper/ Gold |

| Aley | 100% | British Columbia | Niobium |

- 16 -

The map below highlights the location of our mineral properties:

Figure 1: Location of Taseko's Properties

Gibraltar

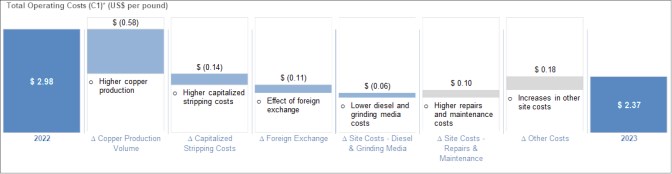

Gibraltar produced 123 million pounds of copper and 1.2 million pounds of molybdenum in 2023. Gibraltar has an expected mine life of at least 21 years remaining based on Proven and Probable Sulphide Mineral Reserves of 645 million tons at a grade of 0.25% copper as of December 31, 2023.

Between 2006 and 2013, we invested over C$800 million to expand and modernize the mine and original ore concentrator, add a second ore concentrator and make other production improvements at the Gibraltar Mine. Following this period of investment and mine expansion, Gibraltar has achieved a stable level of operations with an ore processing capacity of 85,000 tons per day, which makes Gibraltar the second largest open pit copper mine in Canada.

Going forward, our focus is on continued stable operations at Gibraltar with further improvements to operating practices to reduce unit costs. Average annual copper production over the remaining mine life is expected to be approximately 130 million pounds.

- 17 -

Florence Copper

Florence Copper is currently under construction and first copper production is expected in the fourth quarter of 2025. The commercial operation at Florence Copper will have a production capacity of 85 million pounds of copper annually over a 22 year mine life, and is expected to be in the lowest quartile of producers on the global copper cost curve based on current construction and operating cost projections. Construction activities for the commercial facility have been ramping up in early 2024, following the issuance of the final UIC by the EPA in October 2023.

Florence Copper production will utilize an ISCR copper recovery process to produce a high-quality copper cathode. Since 2018, we have operated a PTF at the Florence Copper site which has successfully demonstrated the ISCR process. Over one million pounds of copper cathode were produced and sold from the PTF operation during its 18-month production phase, and the results of the PTF test work were incorporated into an updated technical report published in March 2023.

The Company acquired Florence Copper in 2014 for US$70 million and has invested over US$250 million in the project up to December 31, 2023. Based on the 2023 Florence Copper Technical Report, the remaining cost to complete construction of the commercial ISCR facility at Florence Copper is estimated to be approximately US$232 million (based on third quarter 2022 cost estimates).

As of December 31, 2023, the Company has available liquidity of $176 million (including cash and equivalents and an undrawn Credit Facility of US$60 million). The Company has also completed project financings and obtained commitments for an additional US$150 million to fund the construction of Florence Copper, including a US$50 million copper metal stream agreement with Mitsui & Co. (USA) ("Mitsui"), a US$50 million royalty with Taurus Mining Royalty Fund L.P. ("Taurus") registered on title and a credit commitment for a US$50 million first lien project debt facility from a commercial bank (with an accordion feature for an additional US$25 million). Details of our available liquidity and the committed financing facilities for Florence Copper are provided in the discussion below under "Description of Capital Structure - Indebtedness and Other Financing Arrangements - Florence Copper" and in our 2023 MD&A.

Other Development Projects

Our other development projects ("Other Development Projects") include the Yellowhead copper project (the "Yellowhead Copper Project"), the New Prosperity gold and copper project (the "New Prosperity Project") and the Aley niobium project (the "Aley Project").