| Maryland | 1-12993 | 95-4502084 | ||||||||||||

| (State or other jurisdiction of incorporation) |

(Commission File Number) | (I.R.S. Employer Identification No.) | ||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Common Stock, $.01 par value per share | ARE |

New York Stock Exchange | ||||||

| ALEXANDRIA REAL ESTATE EQUITIES, INC. | ||||||||||||||

| July 25, 2022 | By: | /s/ Joel S. Marcus | ||||||||||||

| Joel S. Marcus | ||||||||||||||

| Executive Chairman | ||||||||||||||

| By: | /s/ Peter M. Moglia | |||||||||||||

| Peter M. Moglia | ||||||||||||||

| Co-Chief Executive Officer and Co-Chief Investment Officer |

||||||||||||||

| By: | /s/ Stephen A. Richardson | |||||||||||||

| Stephen A. Richardson | ||||||||||||||

| Co-Chief Executive Officer | ||||||||||||||

| By: | /s/ Dean A. Shigenaga | |||||||||||||

| Dean A. Shigenaga | ||||||||||||||

| President and Chief Financial Officer | ||||||||||||||

|

|||||

| Table of Contents | |||||

June 30, 2022 | |||||

| EARNINGS PRESS RELEASE | Page | Page | ||||||||||||

Second Quarter Ended June 30, 2022 Financial and Operating Results

|

||||||||||||||

Guidance |

||||||||||||||

| SUPPLEMENTAL INFORMATION | Page | Page | ||||||||||||

| External Growth / Investments in Real Estate | ||||||||||||||

New Class A Development and Redevelopment Properties: |

||||||||||||||

| Internal Growth | ||||||||||||||

| Balance Sheet Management | ||||||||||||||

| Definitions and Reconciliations | ||||||||||||||

Alexandria Real Estate Equities, Inc. All Rights Reserved. © 2022 |

xviii |

|||||||

| Key highlights | |||||||||||||||||||||||

| Operating results | 2Q22 | 2Q21 | 1H22 | 1H21 | |||||||||||||||||||

| Total revenues: | |||||||||||||||||||||||

| In millions | $ | 643.8 | $ | 509.6 | $ | 1,258.8 | $ | 989.5 | |||||||||||||||

| Growth | 26.3 | % | 27.2 | % | |||||||||||||||||||

| Net income attributable to Alexandria’s common stockholders – diluted | |||||||||||||||||||||||

| In millions | $ | 269.3 | $ | 380.6 | $ | 118.5 | $ | 388.5 | |||||||||||||||

| Per share | $ | 1.67 | $ | 2.61 | $ | 0.74 | $ | 2.74 | |||||||||||||||

Funds from operations attributable to Alexandria’s common stockholders – diluted, as adjusted |

|||||||||||||||||||||||

| In millions | $ | 338.8 | $ | 282.3 | $ | 663.4 | $ | 545.2 | |||||||||||||||

| Per share | $ | 2.10 | $ | 1.93 | $ | 4.15 | $ | 3.84 | |||||||||||||||

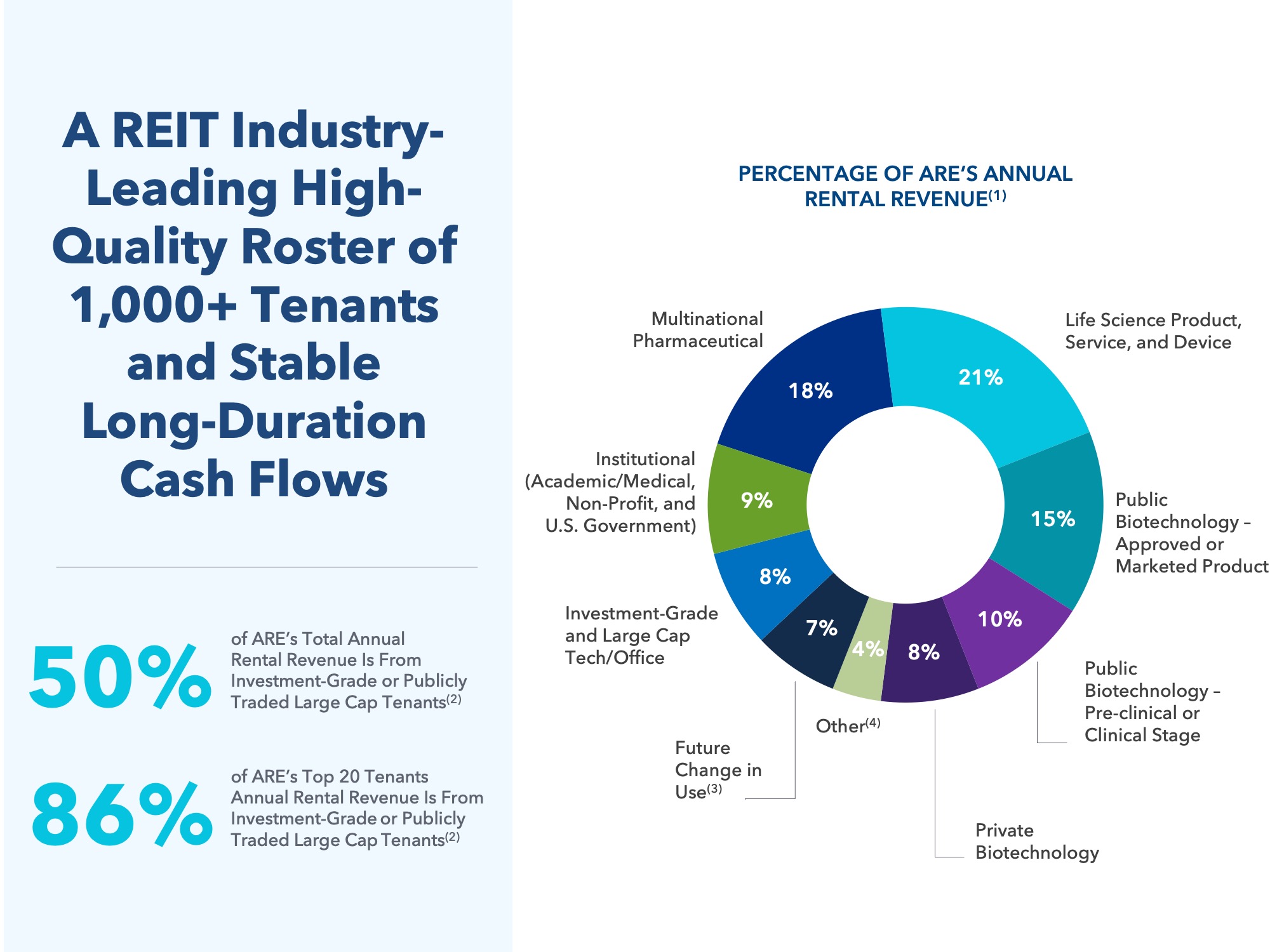

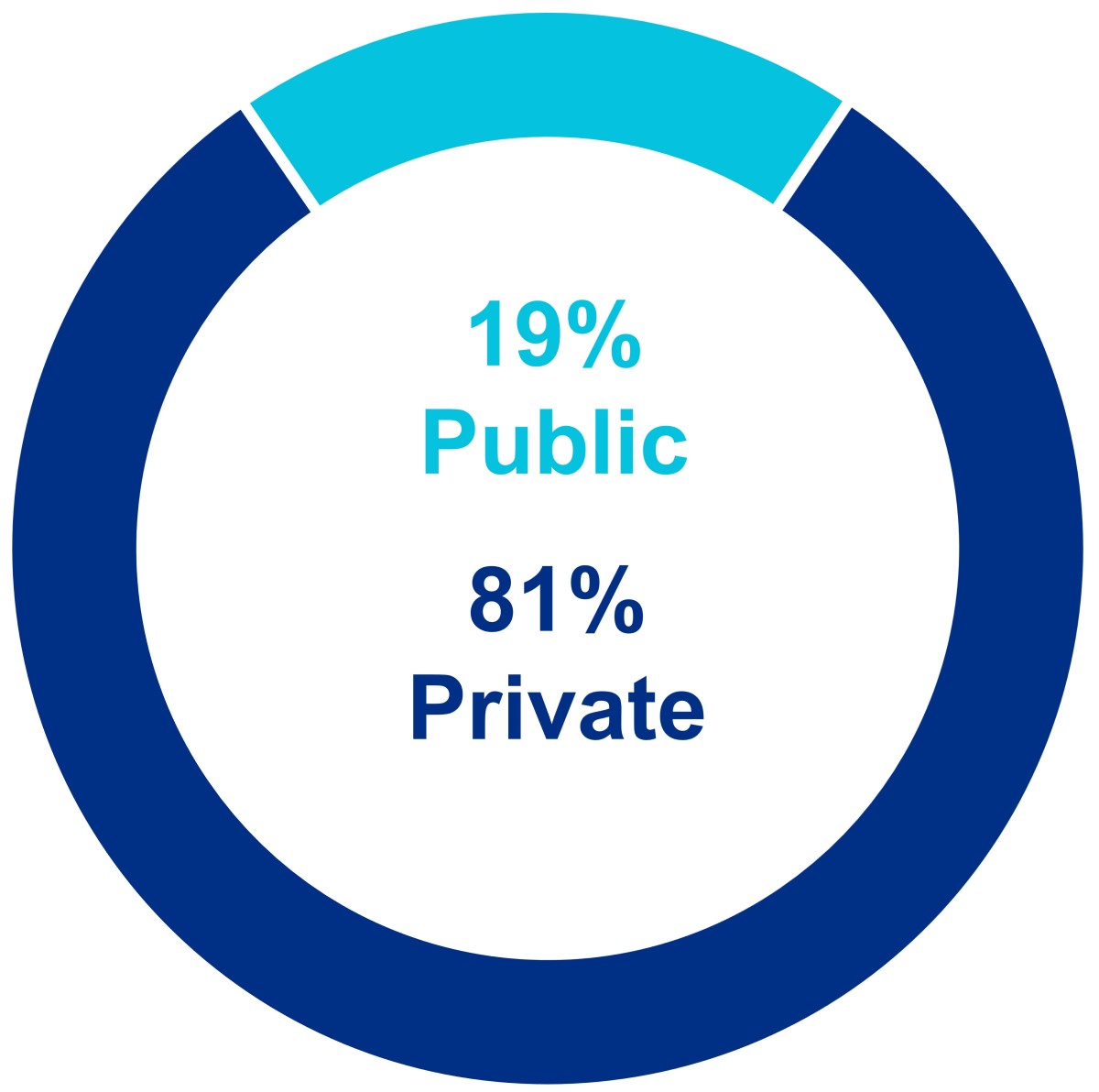

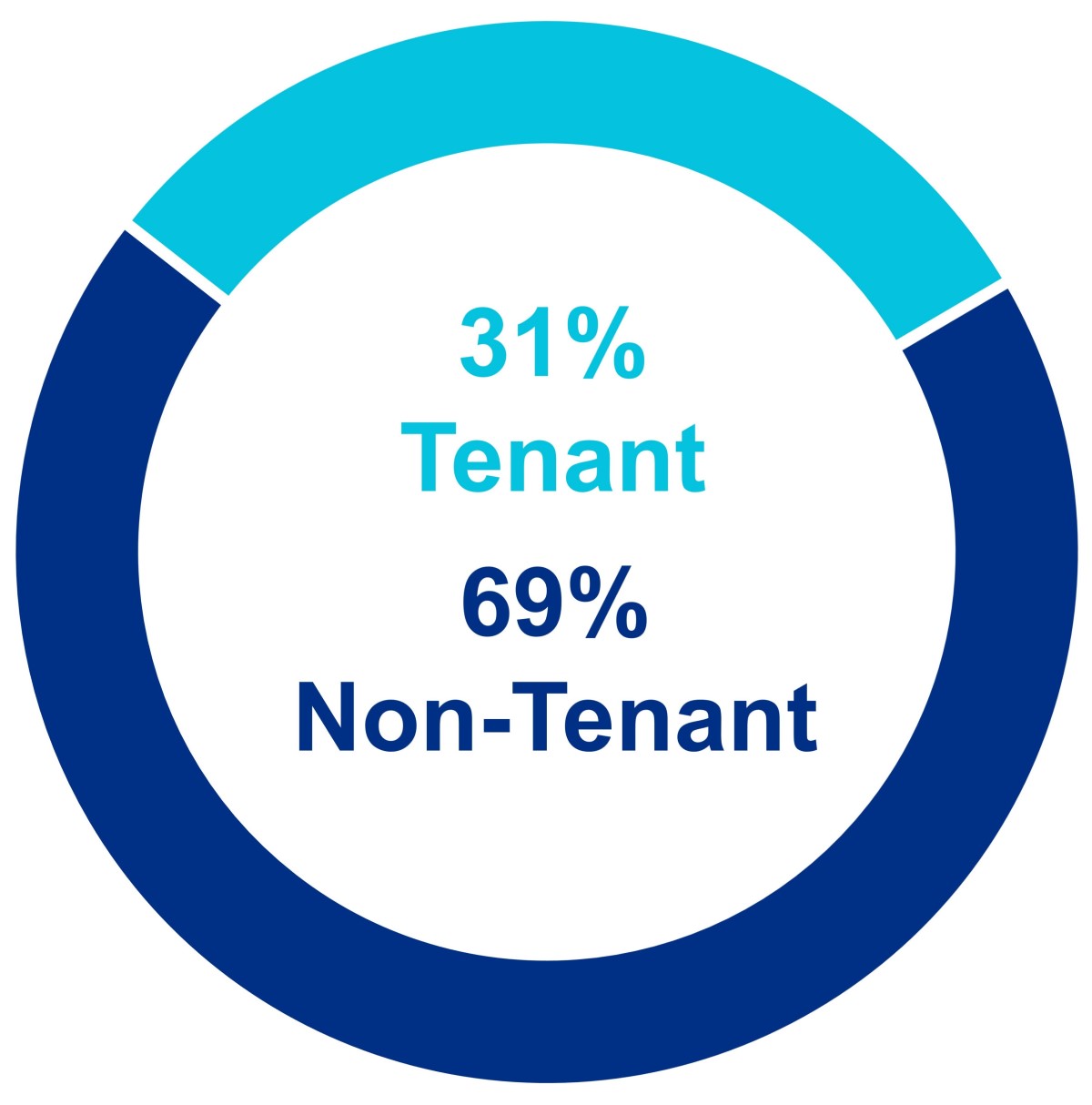

| Percentage of total annual rental revenue in effect from investment-grade or publicly traded large cap tenants | 50 | % | ||||||||||||

| Sustained strength in tenant collections: | ||||||||||||||

Tenant receivables as of June 30, 2022 |

$ | 7.1 | million | |||||||||||

July tenant rent and receivables collected as of July 25, 2022 |

99.9 | % | ||||||||||||

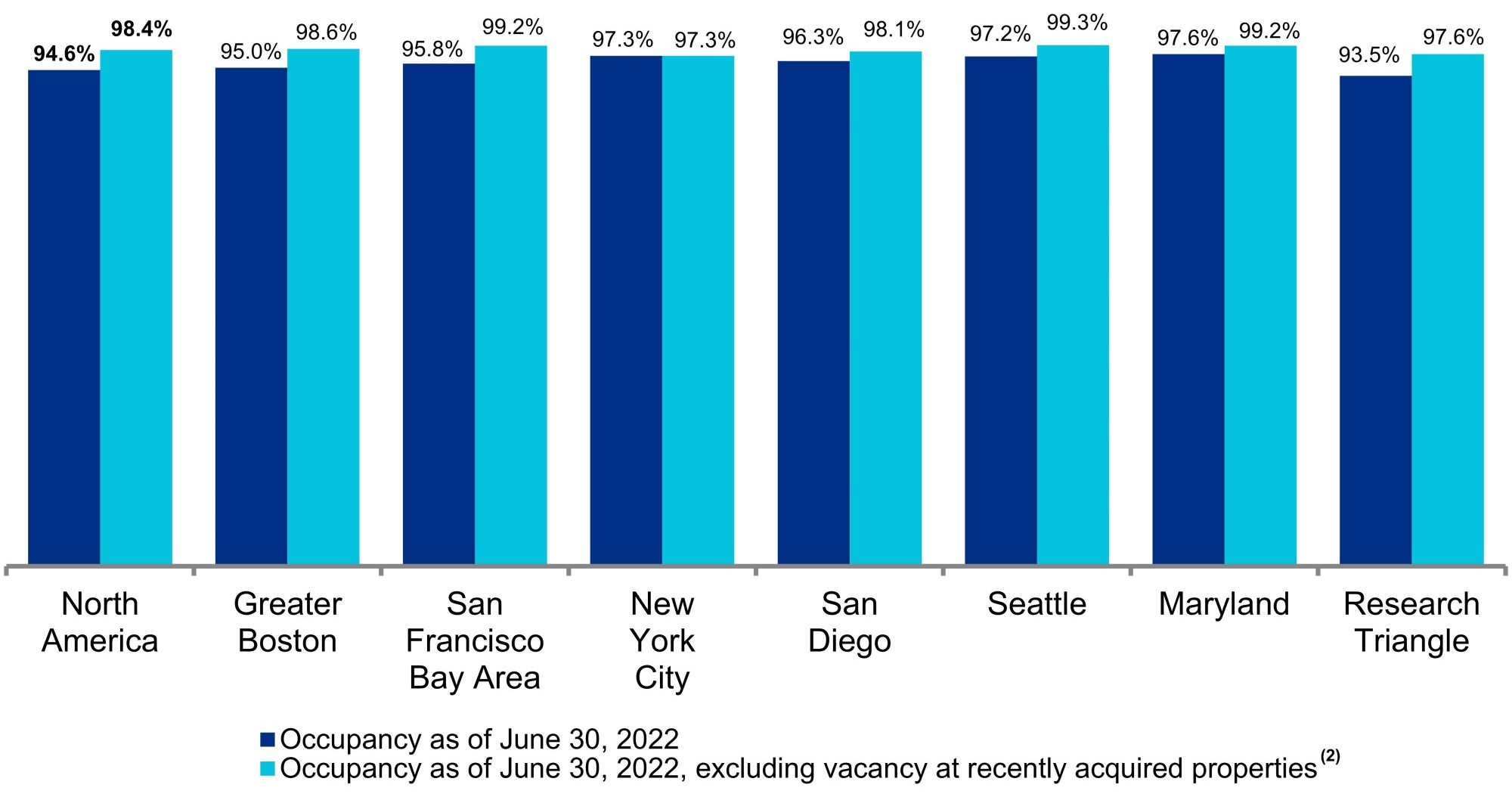

| Occupancy of operating properties in North America | 94.6 | % | ||||||||||||

| Occupancy of operating properties in North America (excluding vacancy at recently acquired properties) | 98.4 | % | (1) |

|||||||||||

| Operating margin | 70 | % | ||||||||||||

| Adjusted EBITDA margin | 70 | % | ||||||||||||

| Weighted-average remaining lease term: | ||||||||||||||

| All tenants | 7.1 | years | ||||||||||||

| Top 20 tenants | 10.2 | years | ||||||||||||

| 2Q22 | 1H22 | |||||||||||||

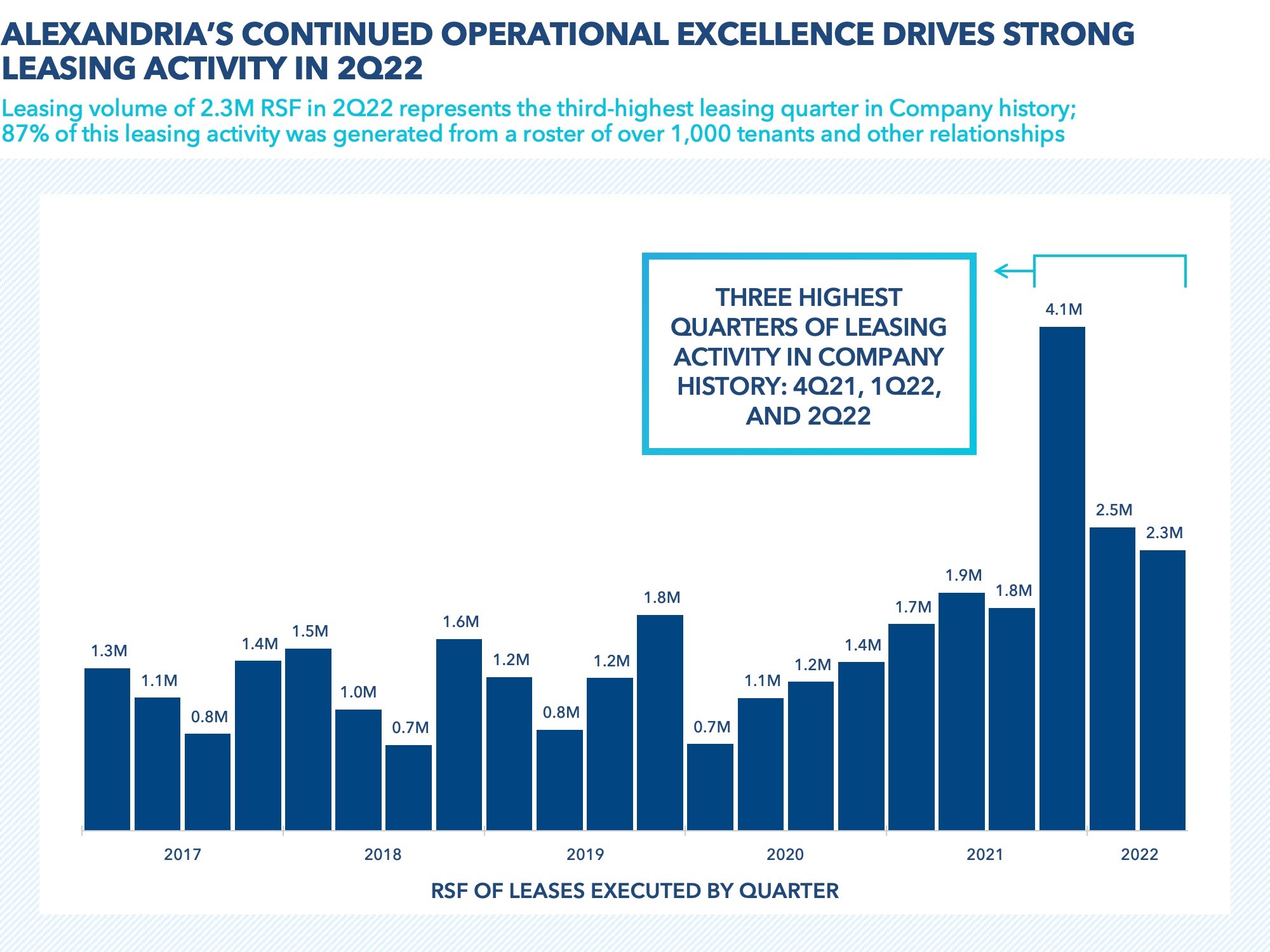

| Total leasing activity – RSF | 2,279,758 | 4,743,196 | ||||||||||||

| Leasing of development and redevelopment space – RSF | 916,436 | 2,356,132 | ||||||||||||

| Lease renewals and re-leasing of space: | ||||||||||||||

| RSF (included in total leasing activity above) | 1,087,082 | 1,951,159 | ||||||||||||

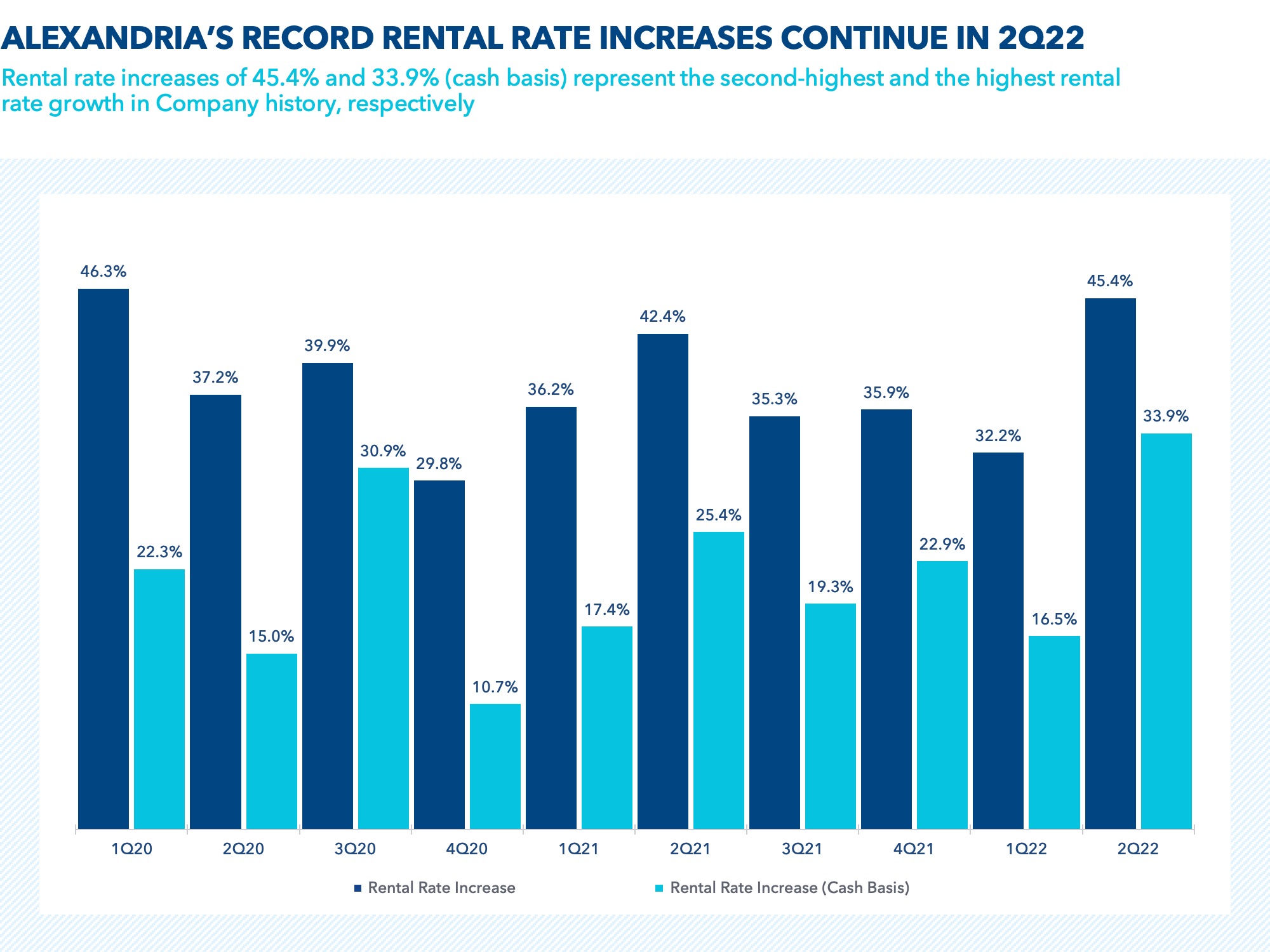

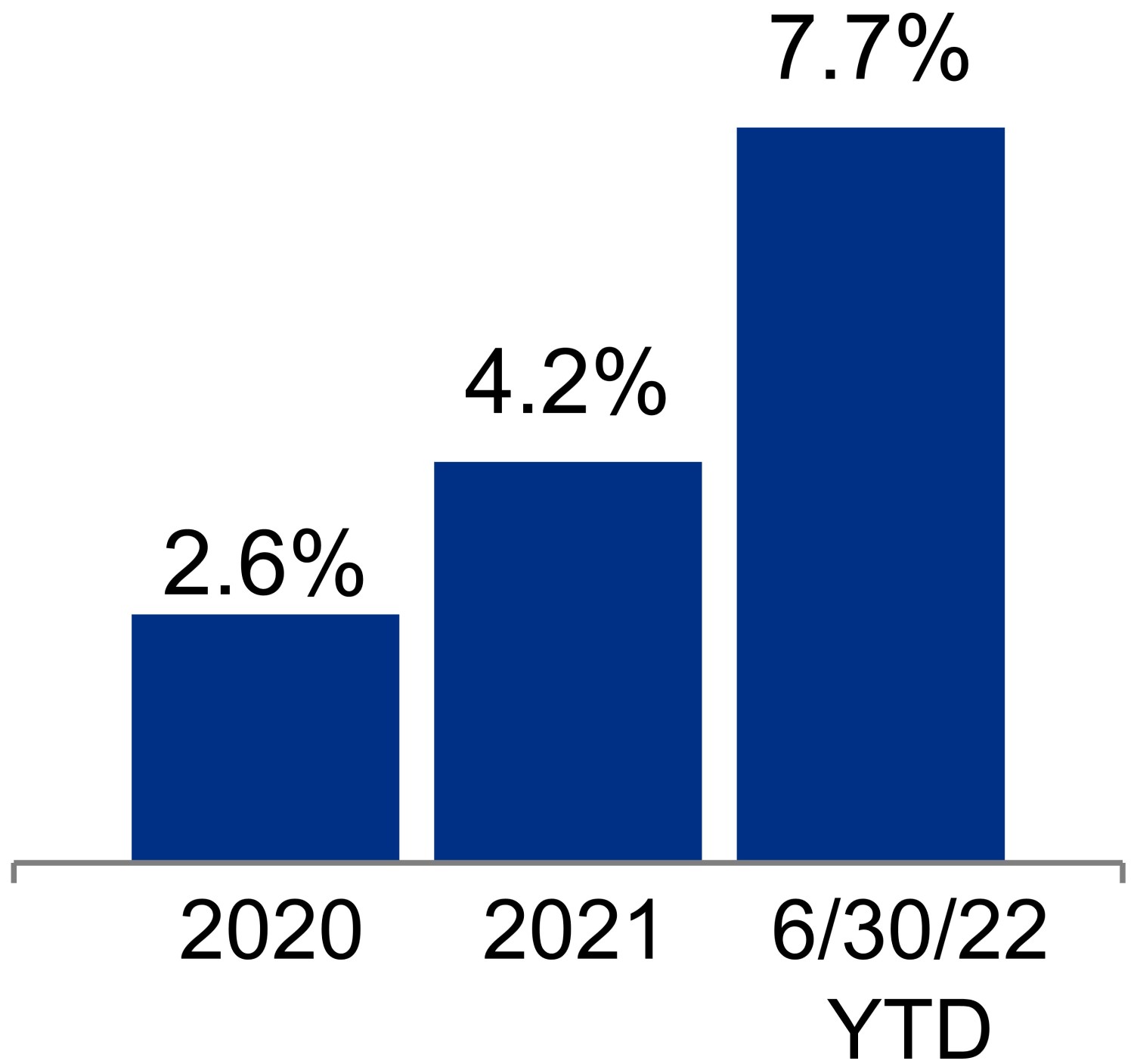

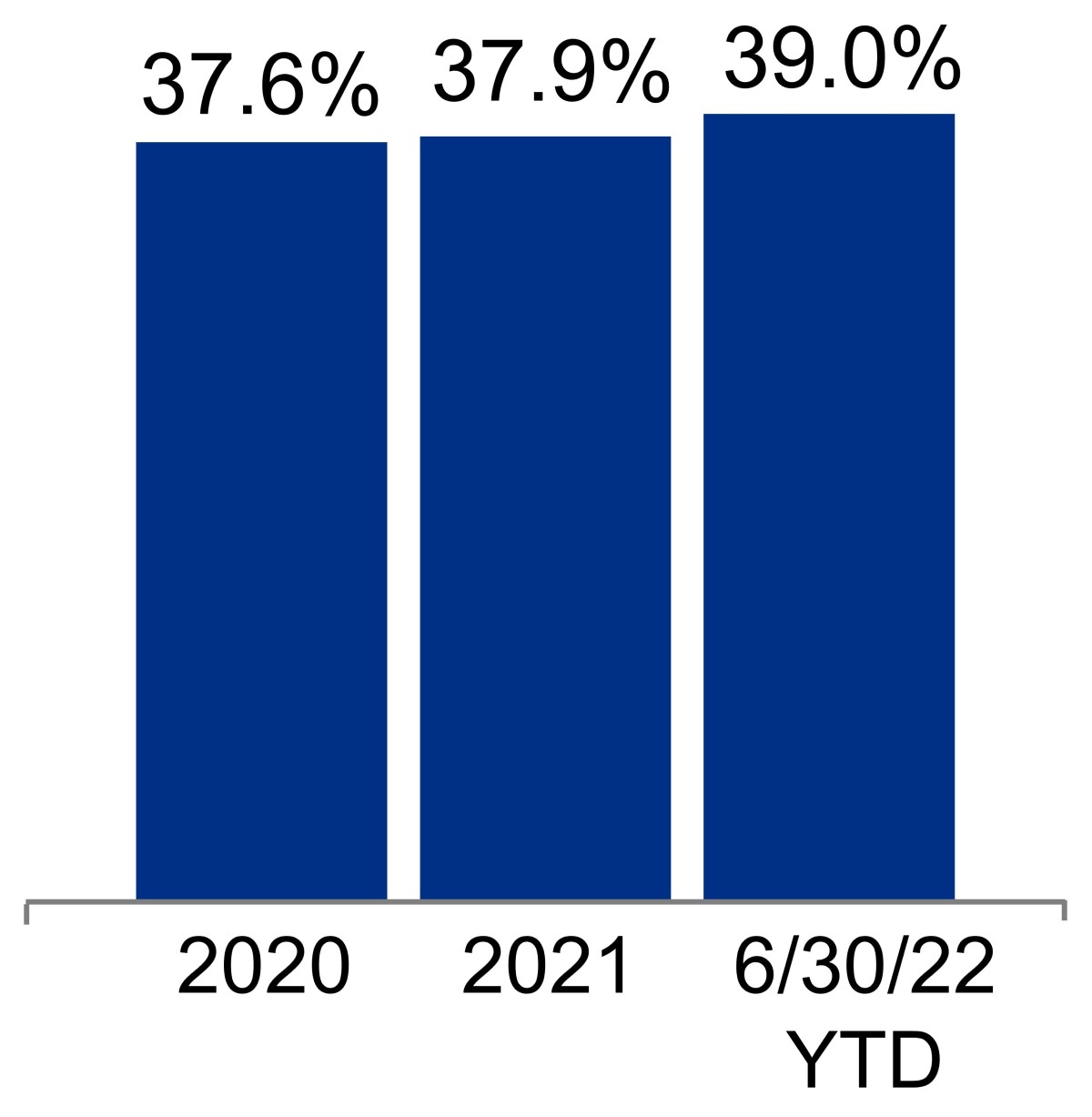

| Rental rate increases | 45.4% | 39.0% | ||||||||||||

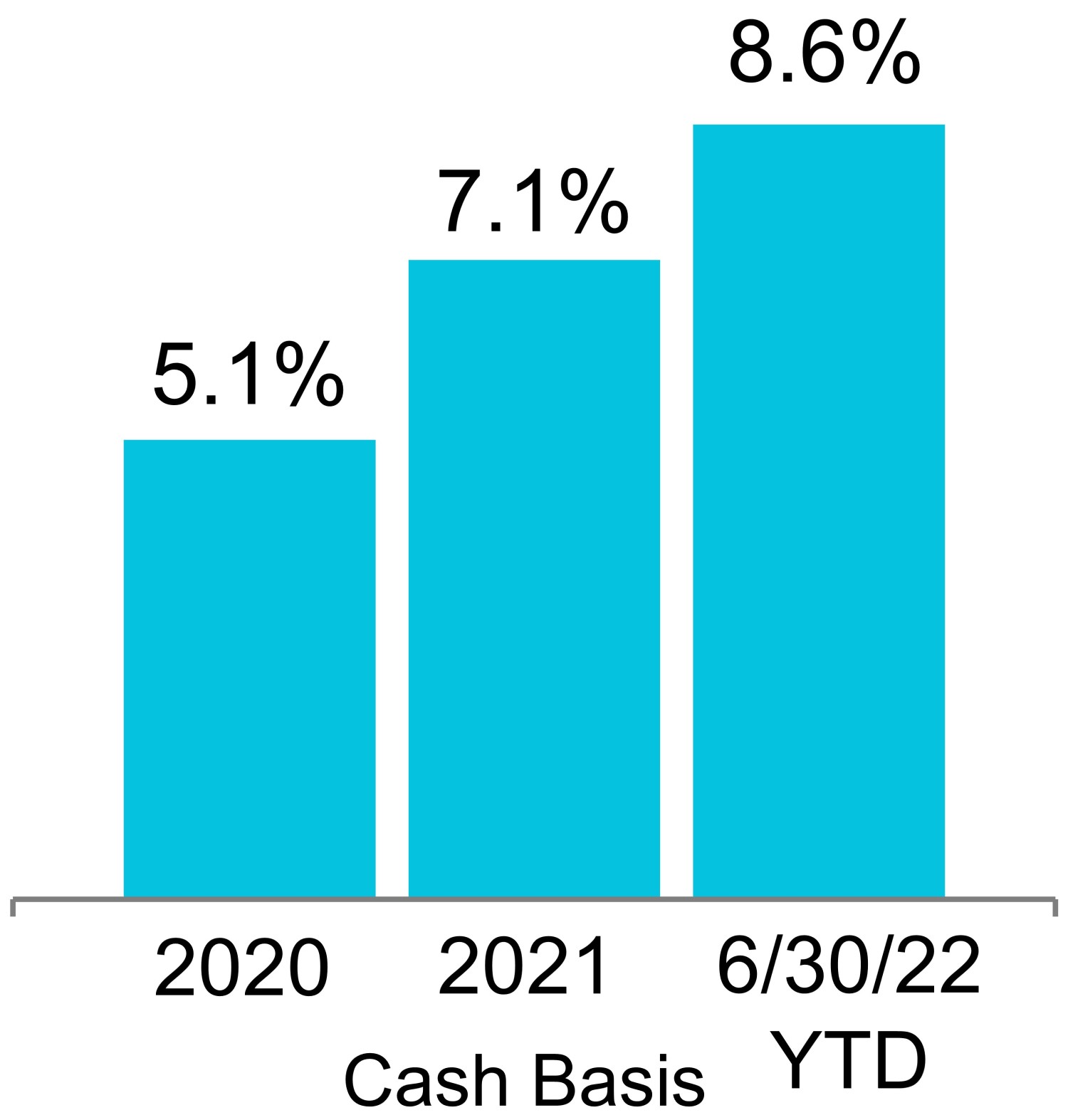

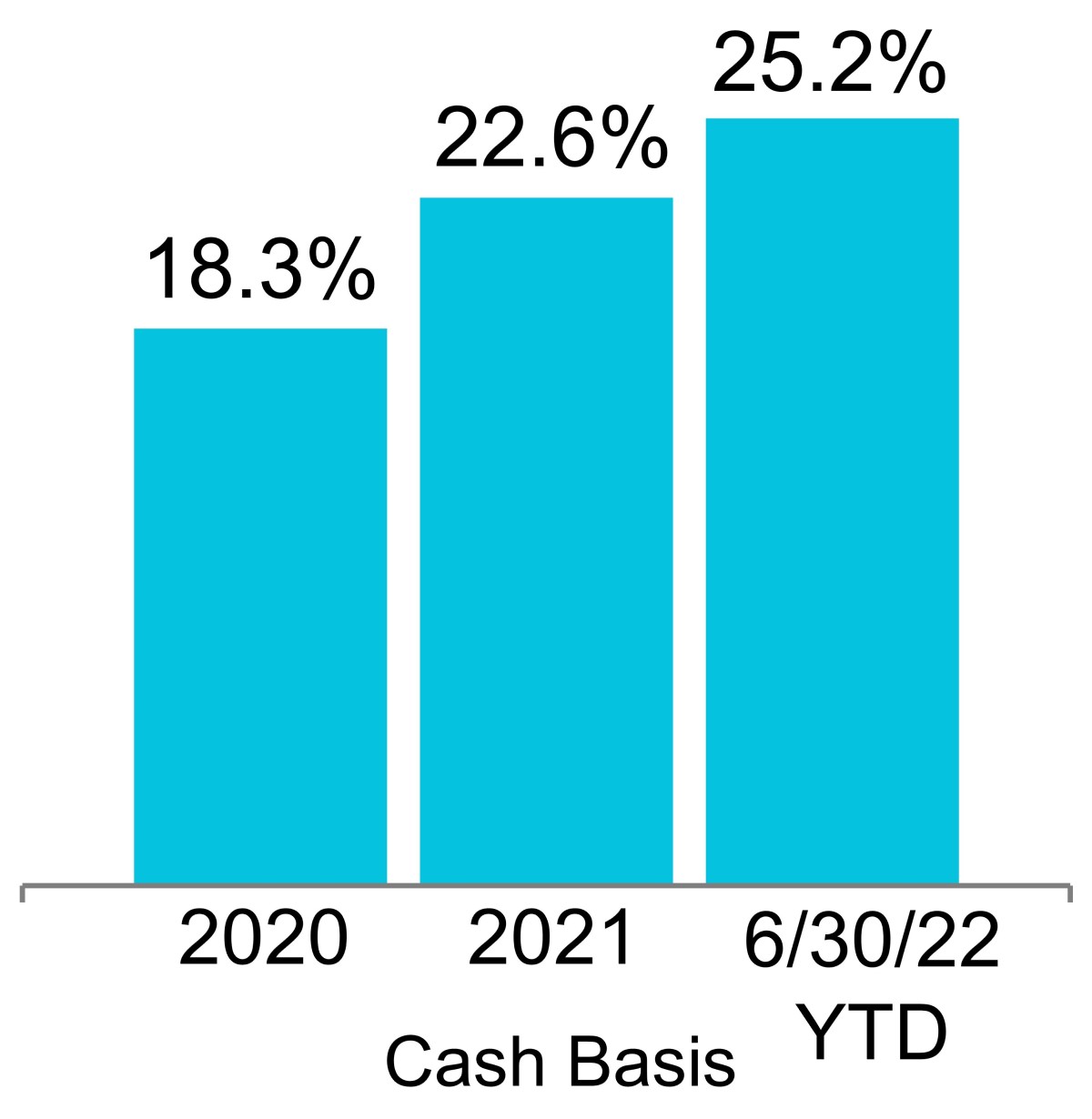

| Rental rate increases (cash basis) | 33.9% | 25.2% | ||||||||||||

|

|||||

Second Quarter Ended June 30, 2022 Financial and Operating Results (continued) | |||||

June 30, 2022 | |||||

| Key items included in net income attributable to Alexandria’s common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||

(In millions, except per share amounts) |

Amount | Per Share – Diluted | Amount | Per Share – Diluted | |||||||||||||||||||||||||||||||||||||||||||

| 2Q22 | 2Q21 | 2Q22 | 2Q21 | 1H22 | 1H21 | 1H22 | 1H21 | ||||||||||||||||||||||||||||||||||||||||

| Unrealized (losses) gains on non-real estate investments | $ | (68.1) | $ | 244.0 | $ | (0.42) | $ | 1.67 | $ | (331.6) | $ | 197.8 | $ | (2.07) | $ | 1.39 | |||||||||||||||||||||||||||||||

| Significant realized gains on non-real estate investments | — | 34.8 | — | 0.24 | — | 57.7 | — | 0.41 | |||||||||||||||||||||||||||||||||||||||

| Gain on sales of real estate | 214.2 | — | 1.33 | — | 214.2 | 2.8 | 1.34 | 0.02 | |||||||||||||||||||||||||||||||||||||||

| Impairment of real estate | — | (4.9) | — | (0.03) | — | (10.1) | — | (0.07) | |||||||||||||||||||||||||||||||||||||||

| Loss on early extinguishment of debt | (3.3) | — | (0.02) | — | (3.3) | (67.3) | (0.02) | (0.47) | |||||||||||||||||||||||||||||||||||||||

Total |

$ | 142.8 | $ | 273.9 | $ | 0.89 | $ | 1.88 | $ | (120.7) | $ | 180.9 | $ | (0.75) | $ | 1.28 | |||||||||||||||||||||||||||||||

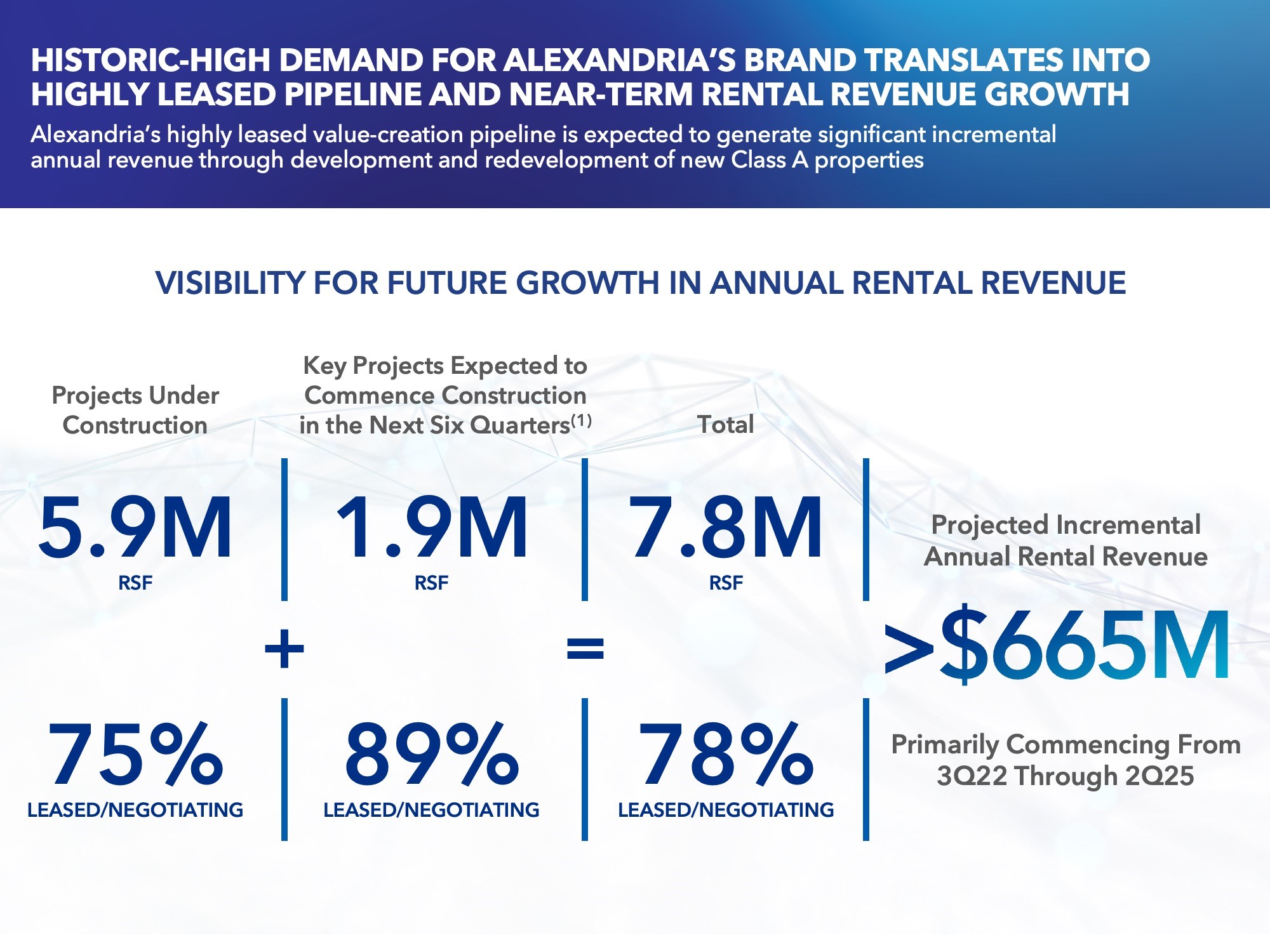

| Value-creation pipeline of new Class A development and redevelopment projects as a percentage of gross assets | 2Q22 | |||||||

Under construction projects 75% leased/negotiating |

10% | |||||||

Pre-leased/negotiating near-term projects expected to commence construction in the next six quarters 89% leased/negotiating |

1% | |||||||

Income-producing/potential cash flows/covered land play(1) |

8% | |||||||

| Land | 2% | |||||||

|

|||||

Second Quarter Ended June 30, 2022 Financial and Operating Results (continued) | |||||

June 30, 2022 | |||||

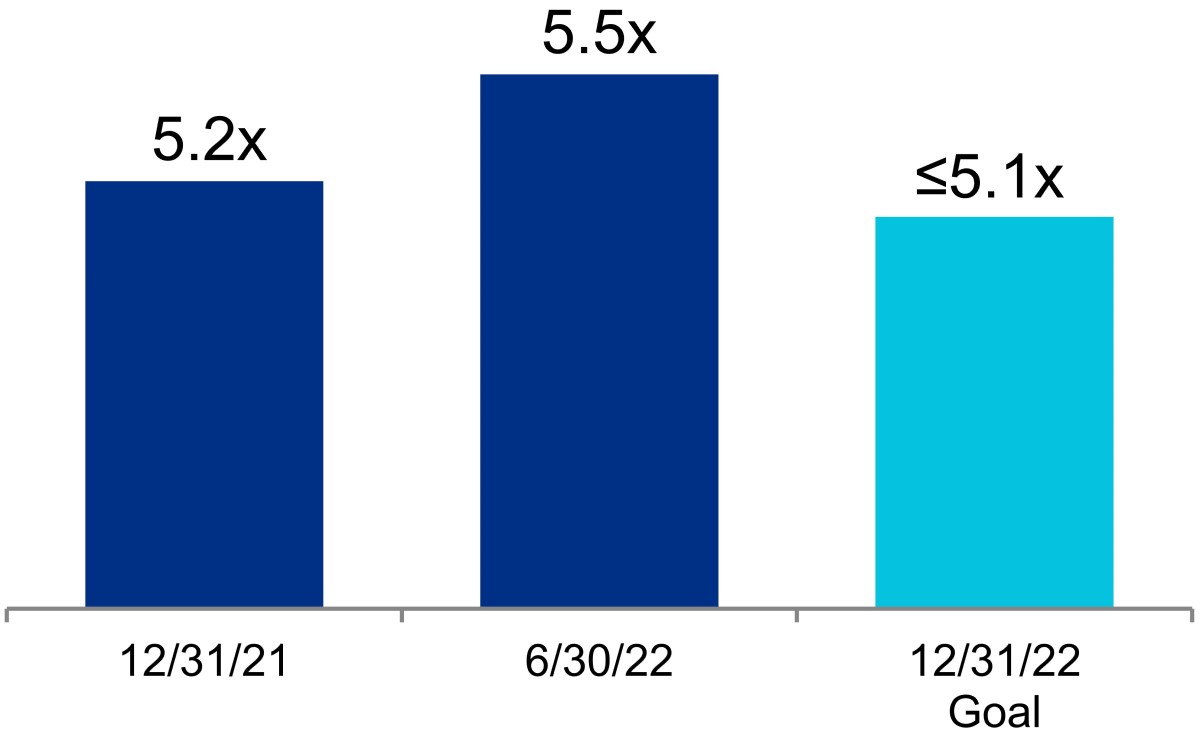

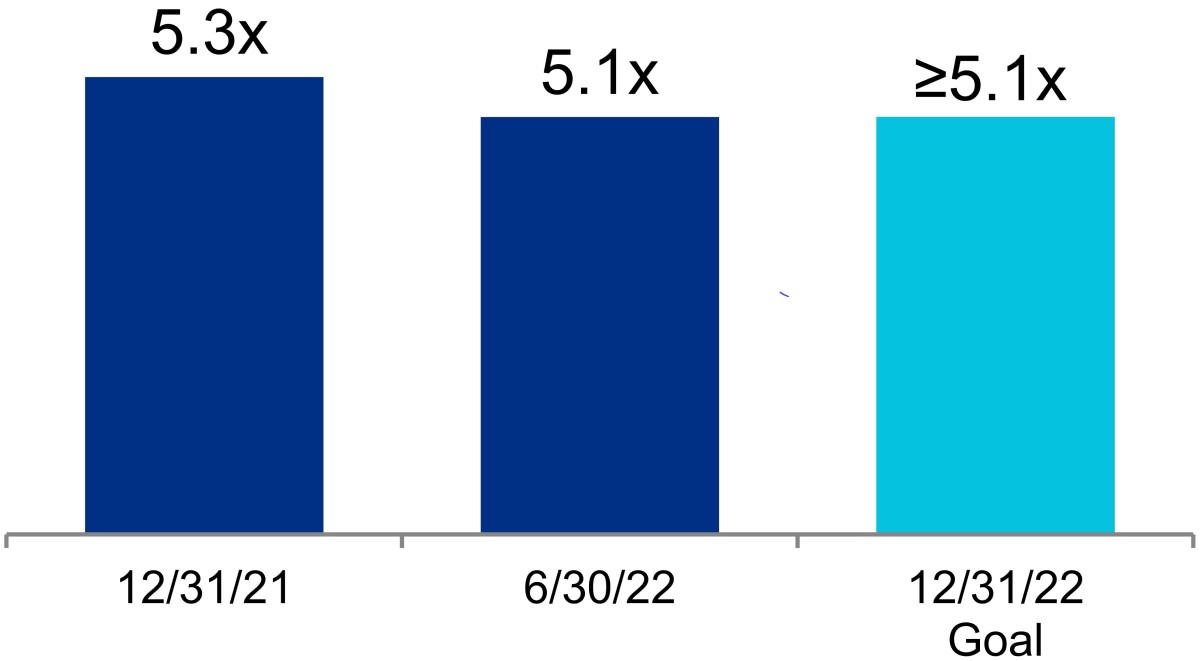

| 2Q22 | Goal | |||||||||||||||||||||||||

| Quarter | Trailing | 4Q22 | ||||||||||||||||||||||||

| Annualized | 12 Months | Annualized | ||||||||||||||||||||||||

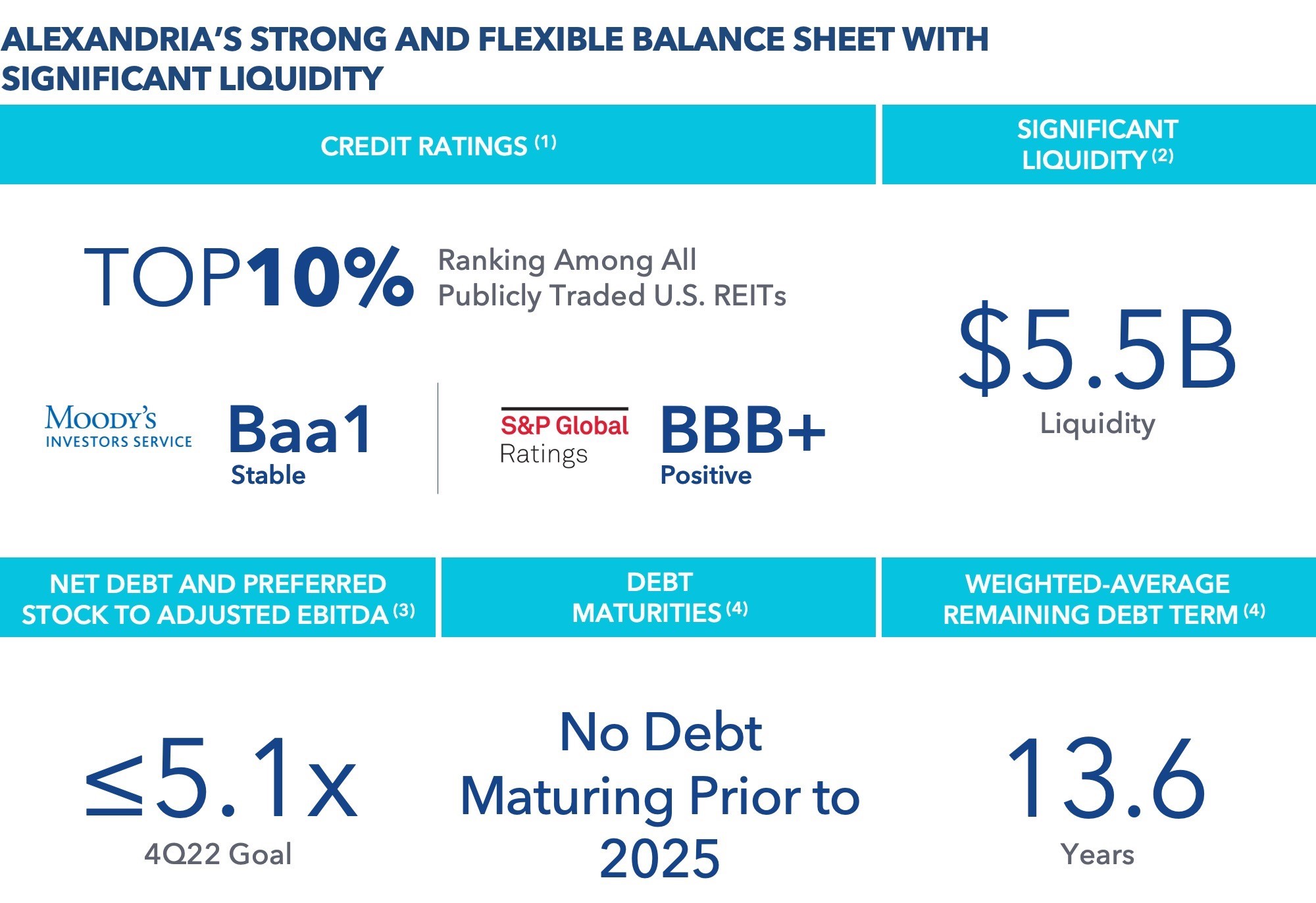

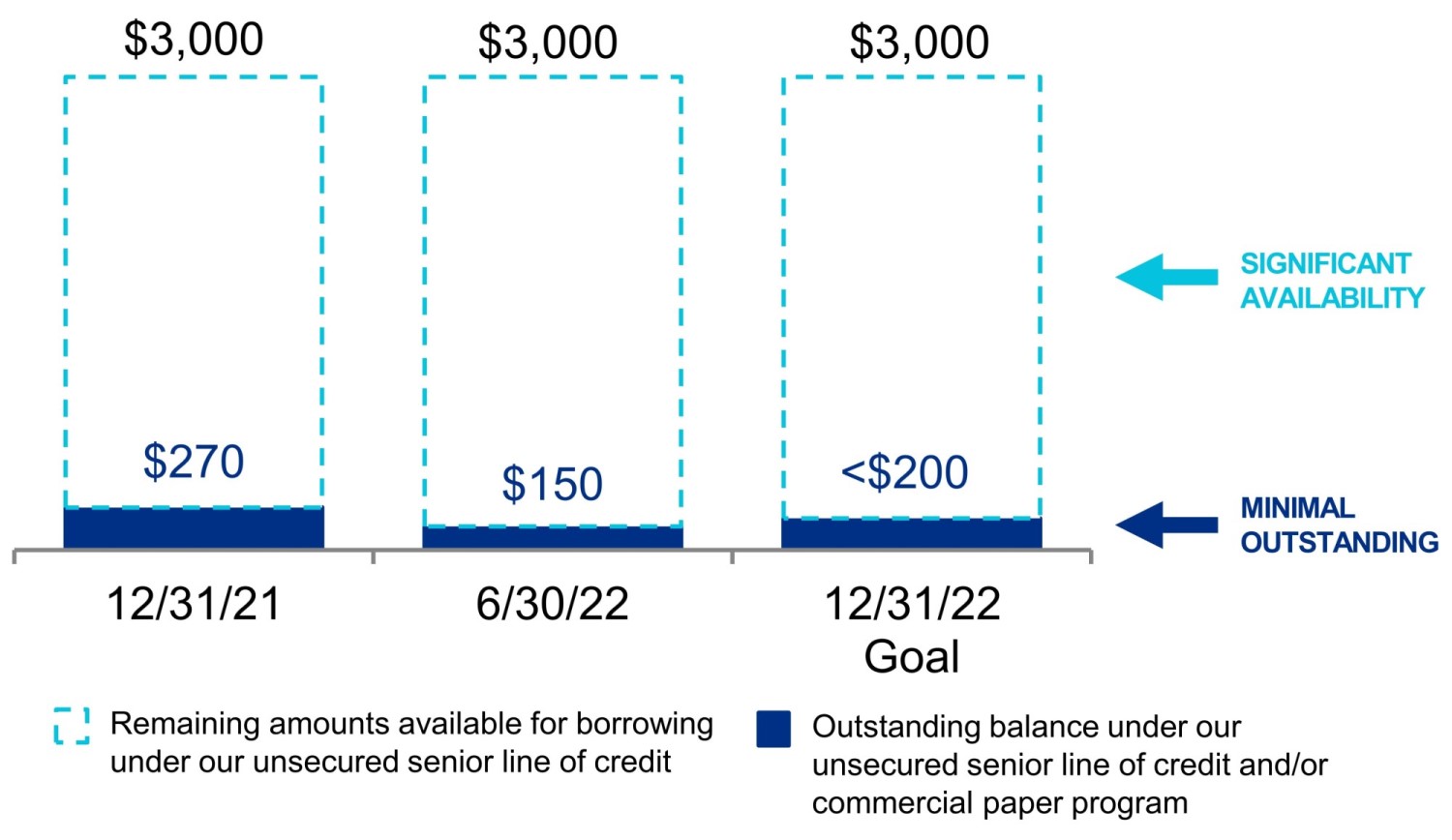

| Net debt and preferred stock to Adjusted EBITDA | 5.5x | 5.9x | Less than or equal to 5.1x | |||||||||||||||||||||||

| Fixed-charge coverage ratio | 5.1x | 5.1x | Greater than or equal to 5.1x | |||||||||||||||||||||||

| Acquisitions | |

||||

June 30, 2022 | |||||

| (Dollars in thousands) | |||||

| Property | Submarket/Market | Date of Purchase |

Number of Properties | Operating Occupancy |

Square Footage | Purchase Price | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Acquisitions With Development/Redevelopment Opportunities(1) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Future Development | Operating With Future Development/ Redevelopment | Operating(2) |

Operating | Total(3) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Completed in 1Q22 | 29 | 91 | % | 4,617,991 | 2,668,494 | 451,760 | — | 7,306,305 | $ | 1,840,717 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Completed in 2Q22: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

One Hampshire Street(4) |

Cambridge/Inner Suburbs/ Greater Boston

|

6/23/22 | 1 | 100 | % | — | 88,591 | — | — | 88,591 | 140,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | Various | Various | 2 | 76 | 869,000 | 109,557 | — | — | 978,557 | 140,146 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | 87 | % | 869,000 | 198,148 | (5) |

— | (5) |

— | (5) |

1,067,148 | 280,146 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Completed in July 2022 | 9,561 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2,130,424 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Pending(6) |

Various | 3Q22 | 275,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | 244,576 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 acquisitions (midpoint) | $ | 2,650,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2022 guidance range(7) |

$2,550,000 – $2,750,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dispositions and Sales of Partial Interest | |

||||

June 30, 2022 | |||||

| (Dollars in thousands) | |||||

| Capitalization Rate (Cash Basis) |

Sales Price per RSF | Gain or Consideration in Excess of Book Value | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Property | Submarket/Market | Date of Sale | Interest Sold | RSF | Capitalization Rate | Sales Price | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Completed 1H22: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 100 Binney Street | Cambridge/Inner Suburbs/Greater Boston | 3/30/22 | 70 | % | 432,931 | 3.6 | % | 3.5 | % | $ | 713,228 | (1) |

$ | 2,353 | $ | 413,615 | (2) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 300 Third Street | Cambridge/Inner Suburbs/Greater Boston | 6/27/22 | 70 | % | 131,963 | 4.6 | % | 4.3 | % | 166,485 | (1) |

$ | 1,802 | 113,020 | (2) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

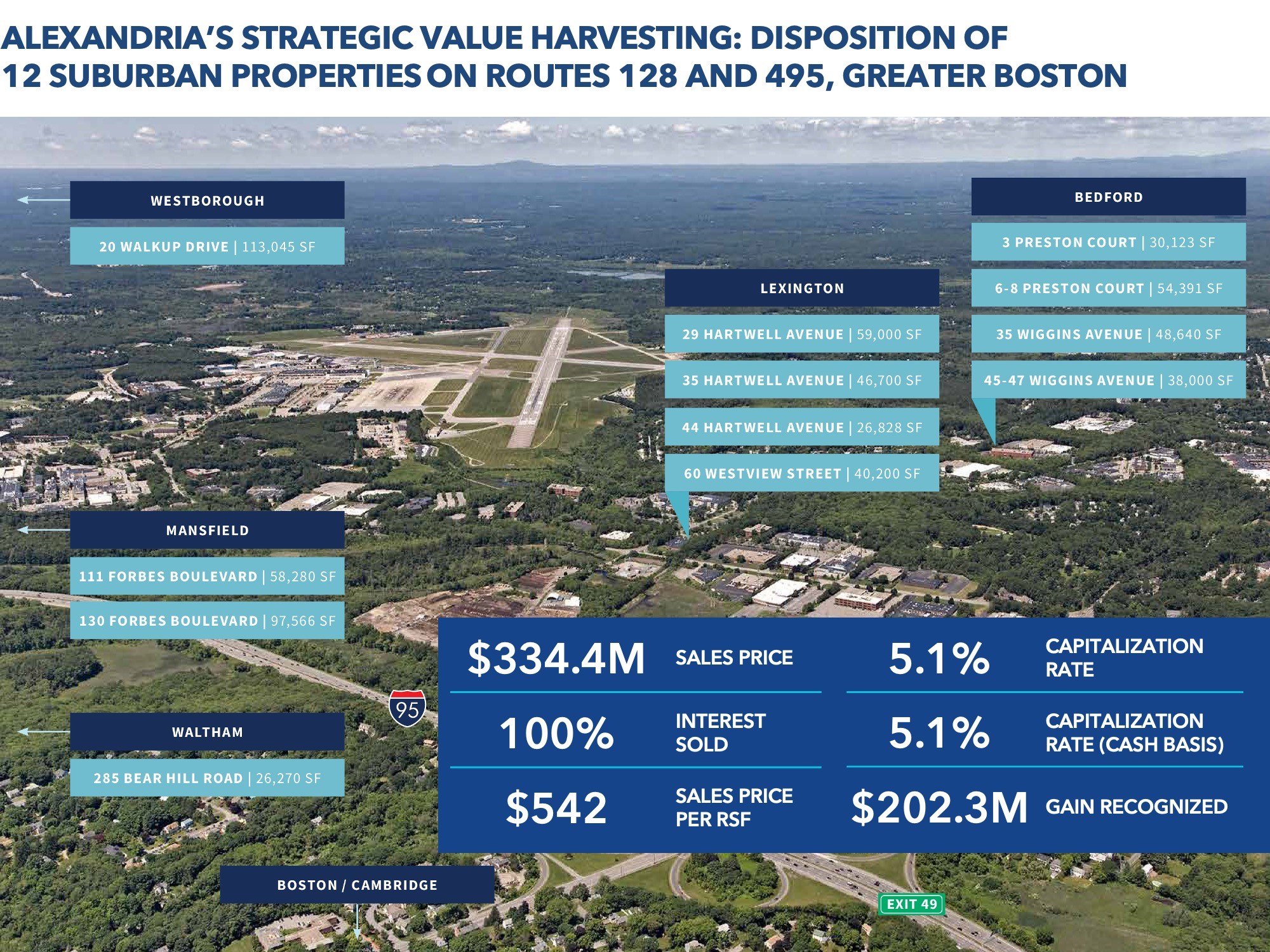

| Alexandria Park at 128, 285 Bear Hill Road, 111 and 130 Forbes Boulevard, and 20 Walkup Drive | Route 128 and Route 495/Greater Boston | 6/8/22 | 100 | % | 617,043 | 5.1 | % | 5.1 | % | 334,397 | $ | 542 | 202,325 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | N/A | N/A | 47,800 | N/A | 11,895 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1,261,910 | $ | 740,855 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Completed in July 2022: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1450 Owens Street | Mission Bay/San Francisco Bay Area | 7/1/22 | 20 | % | (3) |

191,000 | N/A | N/A | 25,039 | (1) |

N/A | $ | 10,083 | (2) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1,286,949 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Pending | San Diego | 3Q22 | TBD | TBD | 140,000 | – | 160,000 | TBD | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | TBD | TBD | TBD | 588,051 | TBD | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 dispositions (midpoint) | $ | 2,025,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 guidance range | $1,450,000 – $2,600,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Guidance | |

||||

June 30, 2022 | |||||

| (Dollars in millions) | |||||

| 2022 Guidance | |||||||||||||||||||||||||||||

| Reduction in uses of capital | Reduction | Summary of key changes in guidance | As of 7/25/22 | As of 4/25/22 | |||||||||||||||||||||||||

| Construction | $285 | EPS, FFO per share, and FFO per share, as adjusted | Refer to page 7 |

||||||||||||||||||||||||||

| Acquisitions | $350 | Same property net operating income increase | 6.0% to 8.0% | 5.9% to 7.9% | |||||||||||||||||||||||||

| Same property net operating income increase (cash basis) | 6.8% to 8.8% | 6.5% to 8.5% | |||||||||||||||||||||||||||

| General and administrative expenses | $172 to $180 | $168 to $176 | |||||||||||||||||||||||||||

| As of 7/25/22 | |||||||||||||||||||||||||||||||||||||||||||||||

Key Sources and Uses of Capital |

Range | Midpoint | Certain Completed Items |

As of 4/25/22 Midpoint |

Key Changes to Midpoint | ||||||||||||||||||||||||||||||||||||||||||

| Sources of capital: | |||||||||||||||||||||||||||||||||||||||||||||||

| Net cash provided by operating activities after dividends | $ | 275 | $ | 325 | $ | 300 | $ | 300 | |||||||||||||||||||||||||||||||||||||||

| Net incremental debt | 1,361 | 561 | 961 | See below | 950 | ||||||||||||||||||||||||||||||||||||||||||

Dispositions and sales of partial interest (refer to page 5) |

1,450 | 2,600 | 2,025 | $ | 1,287 | 1,950 | $ | 75 | |||||||||||||||||||||||||||||||||||||||

| Common equity | 2,364 | 2,364 | 2,364 | $ | 2,364 | (1) |

2,750 | $ | (386) | ||||||||||||||||||||||||||||||||||||||

| Total sources of capital | $ | 5,450 | $ | 5,850 | $ | 5,650 | $ | 5,950 | |||||||||||||||||||||||||||||||||||||||

| Uses of capital: | |||||||||||||||||||||||||||||||||||||||||||||||

| Construction | $ | 2,900 | $ | 3,100 | $ | 3,000 | $ | 2,950 | $ | 50 | |||||||||||||||||||||||||||||||||||||

Acquisitions (refer to page 4) |

2,550 | 2,750 | 2,650 | $ | 2,130 | 3,000 | $ | (350) | |||||||||||||||||||||||||||||||||||||||

Total uses of capital |

$ | 5,450 | $ | 5,850 | $ | 5,650 | $ | 5,950 | |||||||||||||||||||||||||||||||||||||||

Incremental debt (included above): |

|||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of unsecured senior notes payable | $ | 1,800 | $ | 1,800 | $ | 1,800 | $ | 1,800 | $ | 1,800 | |||||||||||||||||||||||||||||||||||||

| Repayments of secured notes payable | (195) | (195) | (195) | $ | (195) | (195) | |||||||||||||||||||||||||||||||||||||||||

| Unsecured senior line of credit, commercial paper, and other | (44) | (744) | (394) | (655) | |||||||||||||||||||||||||||||||||||||||||||

Incremental cash expected to be held at December 31, 2022(2) |

(200) | (300) | (250) | — | $ | (250) | |||||||||||||||||||||||||||||||||||||||||

| Net incremental debt | $ | 1,361 | $ | 561 | $ | 961 | $ | 950 | |||||||||||||||||||||||||||||||||||||||

| Guidance (continued) | |

||||

June 30, 2022 | |||||

| (Dollars in millions, except per share amounts) | |||||

Projected 2022 Earnings per Share and Funds From Operations per Share Attributable to Alexandria’s Common Stockholders – Diluted |

|||||||||||||||||||||||||||||

| As of 7/25/22 | As of 4/25/22 | ||||||||||||||||||||||||||||

Earnings per share(1) |

$2.14 to $2.20 | $1.08 to $1.18 | |||||||||||||||||||||||||||

| Depreciation and amortization of real estate assets | 5.50 | 5.65 | |||||||||||||||||||||||||||

| Gain on sales of real estate | (1.34) | — | |||||||||||||||||||||||||||

| Allocation to unvested restricted stock awards | (0.02) | (0.02) | |||||||||||||||||||||||||||

Funds from operations per share(2) |

$6.28 to $6.34 | $6.71 to $6.81 | |||||||||||||||||||||||||||

| Unrealized losses on non-real estate investments | 2.07 | 1.67 | |||||||||||||||||||||||||||

Loss on early extinguishment of debt(3) |

0.02 | 0.02 | |||||||||||||||||||||||||||

Acceleration of stock compensation due to executive officer resignation(4) |

0.04 | — | |||||||||||||||||||||||||||

| Allocation to unvested restricted stock awards | (0.02) | (0.02) | |||||||||||||||||||||||||||

| Other | (0.01) | (0.05) | |||||||||||||||||||||||||||

Funds from operations per share, as adjusted(1) |

$8.38 to $8.44 | $8.33 to $8.43 | |||||||||||||||||||||||||||

| Midpoint | $8.41 | $8.38 | |||||||||||||||||||||||||||

| As of 7/25/22 | As of 4/25/22 | ||||||||||||||||||||||||||||

Key Assumptions |

Low | High | Low | High | |||||||||||||||||||||||||

Occupancy percentage in North America as of December 31, 2022 |

95.2% | 95.8% | 95.2% | 95.8% | |||||||||||||||||||||||||

Lease renewals and re-leasing of space: |

|||||||||||||||||||||||||||||

Rental rate increases |

30.0% | 35.0% | 30.0% | 35.0% | |||||||||||||||||||||||||

Rental rate increases (cash basis) |

18.0% | 23.0% | 18.0% | 23.0% | |||||||||||||||||||||||||

Same property performance: |

|||||||||||||||||||||||||||||

Net operating income increase |

6.0% | 8.0% | 5.9% | 7.9% | |||||||||||||||||||||||||

Net operating income increase (cash basis) |

6.8% | 8.8% | 6.5% | 8.5% | |||||||||||||||||||||||||

Straight-line rent revenue(5) |

$ | 144 | $ | 154 | $ | 154 | $ | 164 | |||||||||||||||||||||

General and administrative expenses(4) |

$ | 172 | $ | 180 | $ | 168 | $ | 176 | |||||||||||||||||||||

Capitalization of interest |

$ | 269 | $ | 279 | $ | 269 | $ | 279 | |||||||||||||||||||||

Interest expense |

$ | 90 | $ | 100 | $ | 90 | $ | 100 | |||||||||||||||||||||

| Key Credit Metrics | As of 7/25/22 | As of 4/25/22 | ||||||||||||

Net debt and preferred stock to Adjusted EBITDA – 4Q22 annualized |

Less than or equal to 5.1x | Less than or equal to 5.1x | ||||||||||||

Fixed-charge coverage ratio – 4Q22 annualized |

Greater than or equal to 5.1x | Greater than or equal to 5.1x | ||||||||||||

|

|||||

| Earnings Call Information and About the Company | |||||

June 30, 2022 | |||||

| Consolidated Statements of Operations | |

||||

June 30, 2022 | |||||

| (Dollars in thousands, except per share amounts) | |||||

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||||||||||||||||||||

| 6/30/22 | 3/31/22 | 12/31/21 | 9/30/21 | 6/30/21 | 6/30/22 | 6/30/21 | ||||||||||||||||||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||||||||||||||||||||

| Income from rentals | $ | 640,959 | $ | 612,554 | $ | 574,656 | $ | 546,527 | $ | 508,371 | $ | 1,253,513 | $ | 987,066 | ||||||||||||||||||||||||||||||

| Other income | 2,805 | 2,511 | 2,267 | 1,232 | 1,248 | 5,316 | 2,402 | |||||||||||||||||||||||||||||||||||||

| Total revenues | 643,764 | 615,065 | 576,923 | 547,759 | 509,619 | 1,258,829 | 989,468 | |||||||||||||||||||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||||||||||||||

| Rental operations | 196,284 | 181,328 | 175,717 | 165,995 | 143,955 | 377,612 | 281,843 | |||||||||||||||||||||||||||||||||||||

| General and administrative | 43,397 | 40,931 | 41,654 | 37,931 | 37,880 | 84,328 | 71,876 | |||||||||||||||||||||||||||||||||||||

| Interest | 24,257 | 29,440 | 34,862 | 35,678 | 35,158 | 53,697 | 71,625 | |||||||||||||||||||||||||||||||||||||

| Depreciation and amortization | 242,078 | 240,659 | 239,254 | 210,842 | 190,052 | 482,737 | 370,965 | |||||||||||||||||||||||||||||||||||||

| Impairment of real estate | — | — | — | 42,620 | 4,926 | — | 10,055 | |||||||||||||||||||||||||||||||||||||

| Loss on early extinguishment of debt | 3,317 | — | — | — | — | 3,317 | 67,253 | |||||||||||||||||||||||||||||||||||||

| Total expenses | 509,333 | 492,358 | 491,487 | 493,066 | 411,971 | 1,001,691 | 873,617 | |||||||||||||||||||||||||||||||||||||

| Equity in earnings of unconsolidated real estate joint ventures | 213 | 220 | 3,018 | 3,091 | 2,609 | 433 | 6,146 | |||||||||||||||||||||||||||||||||||||

| Investment (loss) income | (39,481) | (240,319) | (112,884) | 67,084 | 304,263 | (279,800) | 305,277 | |||||||||||||||||||||||||||||||||||||

| Gain (loss) on sales of real estate | 214,219 | — | 124,226 | (435) | — | 214,219 | 2,779 | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | 309,382 | (117,392) | 99,796 | 124,433 | 404,520 | 191,990 | 430,053 | |||||||||||||||||||||||||||||||||||||

| Net income attributable to noncontrolling interests | (37,168) | (32,177) | (24,901) | (21,286) | (19,436) | (69,345) | (36,848) | |||||||||||||||||||||||||||||||||||||

| Net income (loss) attributable to Alexandria Real Estate Equities, Inc.’s stockholders | 272,214 | (149,569) | 74,895 | 103,147 | 385,084 | 122,645 | 393,205 | |||||||||||||||||||||||||||||||||||||

Net income attributable to unvested restricted stock awards |

(2,934) | (2,081) | (2,098) | (1,883) | (4,521) | (4,134) | (4,663) | |||||||||||||||||||||||||||||||||||||

| Net income (loss) attributable to Alexandria Real Estate Equities, Inc.’s common stockholders | $ | 269,280 | $ | (151,650) | $ | 72,797 | $ | 101,264 | $ | 380,563 | $ | 118,511 | $ | 388,542 | ||||||||||||||||||||||||||||||

| Net income (loss) per share attributable to Alexandria Real Estate Equities, Inc.’s common stockholders: | ||||||||||||||||||||||||||||||||||||||||||||

| Basic | $ | 1.67 | $ | (0.96) | $ | 0.47 | $ | 0.67 | $ | 2.61 | $ | 0.74 | $ | 2.74 | ||||||||||||||||||||||||||||||

| Diluted | $ | 1.67 | $ | (0.96) | $ | 0.47 | $ | 0.67 | $ | 2.61 | $ | 0.74 | $ | 2.74 | ||||||||||||||||||||||||||||||

| Weighted-average shares of common stock outstanding: | ||||||||||||||||||||||||||||||||||||||||||||

| Basic | 161,412 | 158,198 | 153,464 | 150,854 | 145,825 | 159,814 | 141,596 | |||||||||||||||||||||||||||||||||||||

| Diluted | 161,412 | 158,198 | 154,307 | 151,561 | 146,058 | 159,814 | 141,896 | |||||||||||||||||||||||||||||||||||||

| Dividends declared per share of common stock | $ | 1.18 | $ | 1.15 | $ | 1.15 | $ | 1.12 | $ | 1.12 | $ | 2.33 | $ | 2.21 | ||||||||||||||||||||||||||||||

| Consolidated Balance Sheets | |

||||

June 30, 2022 | |||||

| (In thousands) | |||||

| 6/30/22 | 3/31/22 | 12/31/21 | 9/30/21 | 6/30/21 | ||||||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||

| Investments in real estate | $ | 27,952,931 | $ | 27,100,009 | $ | 24,980,669 | $ | 23,071,514 | $ | 21,692,385 | ||||||||||||||||||||||

| Investments in unconsolidated real estate joint ventures | 37,587 | 38,456 | 38,483 | 321,737 | 323,622 | |||||||||||||||||||||||||||

| Cash and cash equivalents | 420,258 | 775,060 | 361,348 | 325,872 | 323,876 | |||||||||||||||||||||||||||

| Restricted cash | 97,404 | 95,106 | 53,879 | 42,182 | 33,697 | |||||||||||||||||||||||||||

| Tenant receivables | 7,069 | 7,570 | 7,379 | 7,749 | 6,710 | |||||||||||||||||||||||||||

| Deferred rent | 905,699 | 881,743 | 839,335 | 816,219 | 781,600 | |||||||||||||||||||||||||||

| Deferred leasing costs | 498,434 | 484,184 | 402,898 | 329,952 | 321,005 | |||||||||||||||||||||||||||

| Investments | 1,657,461 | 1,661,101 | 1,876,564 | 2,046,878 | 1,999,283 | |||||||||||||||||||||||||||

| Other assets | 1,667,210 | 1,801,027 | 1,658,818 | 1,596,615 | 1,536,672 | |||||||||||||||||||||||||||

| Total assets | $ | 33,244,053 | $ | 32,844,256 | $ | 30,219,373 | $ | 28,558,718 | $ | 27,018,850 | ||||||||||||||||||||||

| Liabilities, Noncontrolling Interests, and Equity | ||||||||||||||||||||||||||||||||

| Secured notes payable | $ | 24,986 | $ | 208,910 | $ | 205,198 | $ | 198,758 | $ | 227,984 | ||||||||||||||||||||||

| Unsecured senior notes payable | 10,096,462 | 10,094,337 | 8,316,678 | 8,314,851 | 8,313,025 | |||||||||||||||||||||||||||

| Unsecured senior line of credit and commercial paper | 149,958 | — | 269,990 | 749,978 | 299,990 | |||||||||||||||||||||||||||

Accounts payable, accrued expenses, and other liabilities |

2,317,940 | 2,172,692 | 2,210,410 | 2,149,450 | 1,825,387 | |||||||||||||||||||||||||||

| Dividends payable | 192,571 | 187,701 | 183,847 | 173,560 | 170,647 | |||||||||||||||||||||||||||

| Total liabilities | 12,781,917 | 12,663,640 | 11,186,123 | 11,586,597 | 10,837,033 | |||||||||||||||||||||||||||

| Commitments and contingencies | ||||||||||||||||||||||||||||||||

| Redeemable noncontrolling interests | 9,612 | 9,612 | 9,612 | 11,681 | 11,567 | |||||||||||||||||||||||||||

Alexandria Real Estate Equities, Inc.’s stockholders’ equity: |

||||||||||||||||||||||||||||||||

Common stock |

1,615 | 1,614 | 1,580 | 1,532 | 1,507 | |||||||||||||||||||||||||||

| Additional paid-in capital | 17,149,571 | 16,934,094 | 16,195,256 | 14,727,735 | 14,194,023 | |||||||||||||||||||||||||||

| Accumulated other comprehensive loss | (11,851) | (5,727) | (7,294) | (6,029) | (4,508) | |||||||||||||||||||||||||||

| Alexandria Real Estate Equities, Inc.’s stockholders’ equity | 17,139,335 | 16,929,981 | 16,189,542 | 14,723,238 | 14,191,022 | |||||||||||||||||||||||||||

| Noncontrolling interests | 3,313,189 | 3,241,023 | 2,834,096 | 2,237,202 | 1,979,228 | |||||||||||||||||||||||||||

| Total equity | 20,452,524 | 20,171,004 | 19,023,638 | 16,960,440 | 16,170,250 | |||||||||||||||||||||||||||

Total liabilities, noncontrolling interests, and equity |

$ | 33,244,053 | $ | 32,844,256 | $ | 30,219,373 | $ | 28,558,718 | $ | 27,018,850 | ||||||||||||||||||||||

| Funds From Operations and Funds From Operations per Share | |

||||

June 30, 2022 | |||||

| (In thousands) | |||||

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||||||||||||||||||||

| 6/30/22 | 3/31/22 | 12/31/21 | 9/30/21 | 6/30/21 | 6/30/22 | 6/30/21 | ||||||||||||||||||||||||||||||||||||||

| Net income (loss) attributable to Alexandria’s common stockholders | $ | 269,280 | $ | (151,650) | $ | 72,797 | $ | 101,264 | $ | 380,563 | $ | 118,511 | $ | 388,542 | ||||||||||||||||||||||||||||||

| Depreciation and amortization of real estate assets | 238,565 | 237,160 | 234,979 | 205,436 | 186,498 | 475,725 | 364,218 | |||||||||||||||||||||||||||||||||||||

Noncontrolling share of depreciation and amortization from consolidated real estate JVs |

(26,418) | (23,681) | (21,265) | (17,871) | (16,301) | (50,099) | (31,744) | |||||||||||||||||||||||||||||||||||||

Our share of depreciation and amortization from unconsolidated real estate JVs |

934 | 955 | 3,058 | 3,465 | 4,135 | 1,889 | 7,211 | |||||||||||||||||||||||||||||||||||||

| (Gain) loss on sales of real estate | (214,219) | — | (124,226) | 435 | — | (214,219) | (2,779) | |||||||||||||||||||||||||||||||||||||

Impairment of real estate – rental properties |

— | — | — | 18,602 | 1,754 | — | 6,883 | |||||||||||||||||||||||||||||||||||||

Allocation to unvested restricted stock awards |

— | — | — | (1,472) | (2,191) | — | (4,427) | |||||||||||||||||||||||||||||||||||||

Funds from operations attributable to Alexandria’s common stockholders – diluted(1) |

268,142 | 62,784 | 165,343 | 309,859 | 554,458 | 331,807 | 727,904 | |||||||||||||||||||||||||||||||||||||

| Unrealized losses (gains) on non-real estate investments | 68,128 | 263,433 | 139,716 | 14,432 | (244,031) | 331,561 | (197,780) | |||||||||||||||||||||||||||||||||||||

| Significant realized gains on non-real estate investments | — | — | — | (52,427) | (34,773) | — | (57,692) | |||||||||||||||||||||||||||||||||||||

Impairment of real estate |

— | — | — | 24,018 | 3,172 | — | 3,172 | |||||||||||||||||||||||||||||||||||||

Loss on early extinguishment of debt |

3,317 | — | — | — | — | 3,317 | 67,253 | |||||||||||||||||||||||||||||||||||||

Allocation to unvested restricted stock awards |

(778) | (1,604) | (1,432) | 149 | 3,428 | (3,264) | 2,382 | |||||||||||||||||||||||||||||||||||||

| Funds from operations attributable to Alexandria’s common stockholders – diluted, as adjusted | $ | 338,809 | $ | 324,613 | $ | 303,627 | $ | 296,031 | $ | 282,254 | $ | 663,421 | $ | 545,239 | ||||||||||||||||||||||||||||||

| Funds From Operations and Funds From Operations per Share (continued) | |

||||

June 30, 2022 | |||||

| (In thousands, except per share amounts) | |||||

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||||||||||||||||||||

| 6/30/22 | 3/31/22 | 12/31/21 | 9/30/21 | 6/30/21 | 6/30/22 | 6/30/21 | ||||||||||||||||||||||||||||||||||||||

| Net income (loss) per share attributable to Alexandria’s common stockholders – diluted | $ | 1.67 | $ | (0.96) | $ | 0.47 | $ | 0.67 | $ | 2.61 | $ | 0.74 | $ | 2.74 | ||||||||||||||||||||||||||||||

Depreciation and amortization of real estate assets |

1.32 | 1.36 | 1.40 | 1.26 | 1.19 | 2.68 | 2.39 | |||||||||||||||||||||||||||||||||||||

| Gain on sales of real estate | (1.33) | — | (0.80) | — | — | (1.34) | (0.02) | |||||||||||||||||||||||||||||||||||||

| Impairment of real estate – rental properties | — | — | — | 0.12 | 0.01 | — | 0.05 | |||||||||||||||||||||||||||||||||||||

Allocation to unvested restricted stock awards |

— | — | — | (0.01) | (0.01) | — | (0.03) | |||||||||||||||||||||||||||||||||||||

Funds from operations per share attributable to Alexandria’s common stockholders – diluted |

1.66 | 0.40 | 1.07 | 2.04 | 3.80 | 2.08 | 5.13 | |||||||||||||||||||||||||||||||||||||

| Unrealized losses (gains) on non-real estate investments | 0.42 | 1.67 | 0.91 | 0.10 | (1.67) | 2.07 | (1.39) | |||||||||||||||||||||||||||||||||||||

| Significant realized gains on non-real estate investments | — | — | — | (0.35) | (0.24) | — | (0.41) | |||||||||||||||||||||||||||||||||||||

| Impairment of real estate | — | — | — | 0.16 | 0.02 | — | 0.02 | |||||||||||||||||||||||||||||||||||||

Loss on early extinguishment of debt |

0.02 | — | — | — | — | 0.02 | 0.47 | |||||||||||||||||||||||||||||||||||||

Allocation to unvested restricted stock awards |

— | (0.02) | (0.01) | — | 0.02 | (0.02) | 0.02 | |||||||||||||||||||||||||||||||||||||

Funds from operations per share attributable to Alexandria’s common stockholders – diluted, as adjusted |

$ | 2.10 | $ | 2.05 | $ | 1.97 | $ | 1.95 | $ | 1.93 | $ | 4.15 | $ | 3.84 | ||||||||||||||||||||||||||||||

| Weighted-average shares of common stock outstanding for calculation of: | ||||||||||||||||||||||||||||||||||||||||||||

| Earnings per share – diluted | 161,412 | 158,198 | 154,307 | 151,561 | 146,058 | 159,814 | 141,896 | |||||||||||||||||||||||||||||||||||||

| Funds from operations, diluted, per share | 161,412 | 158,209 | 154,307 | 151,561 | 146,058 | 159,814 | 141,896 | |||||||||||||||||||||||||||||||||||||

| Funds from operations, diluted, as adjusted, per share | 161,412 | 158,209 | 154,307 | 151,561 | 146,058 | 159,814 | 141,896 | |||||||||||||||||||||||||||||||||||||

|

|||||

| Company Profile | |||||

June 30, 2022 | |||||

| EXECUTIVE MANAGEMENT TEAM | ||||||||

| Joel S. Marcus | Peter M. Moglia | |||||||

| Executive Chairman & Founder | Co-Chief Executive Officer & Co-Chief Investment Officer |

|||||||

| Dean A. Shigenaga | Stephen A. Richardson | |||||||

| President & Chief Financial Officer | Co-Chief Executive Officer | |||||||

| Daniel J. Ryan | Hunter L. Kass | |||||||

| Co-Chief Investment Officer & Regional Market Director – San Diego | Executive Vice President – Regional Market Director – Greater Boston | |||||||

| John H. Cunningham | Lawrence J. Diamond | |||||||

| Executive Vice President – Regional Market Director – New York City | Co-Chief Operating Officer & Regional Market Director – Maryland | |||||||

| Vincent R. Ciruzzi | Joseph Hakman | |||||||

| Chief Development Officer | Co-Chief Operating Officer & Chief Strategic Transactions Officer |

|||||||

| Jackie B. Clem | Marc E. Binda | |||||||

| General Counsel & Secretary | Executive Vice President – Finance & Treasurer |

|||||||

| Andres R. Gavinet | Gary D. Dean | |||||||

| Chief Accounting Officer | Executive Vice President – Real Estate Legal Affairs |

|||||||

| Terezia C. Nemeth | Onn C. Lee | |||||||

| Executive Vice President – Regional Market Director – San Francisco Bay Area |

Executive Vice President – Accounting |

|||||||

| Kristina A. Fukuzaki-Carlson | Madeleine T. Alsbrook | |||||||

| Executive Vice President – Business Operations |

Executive Vice President – Talent Management |

|||||||

|

|||||

| Investor Information | |||||

June 30, 2022 | |||||

| Corporate Headquarters | New York Stock Exchange Trading Symbol | Information Requests | |||||||||||||||

| 26 North Euclid Avenue | Common stock: ARE | Phone: | (626) 578-0777 | ||||||||||||||

| Pasadena, California 91101 | Email: | corporateinformation@are.com | |||||||||||||||

| Website: | www.are.com | ||||||||||||||||

| Equity Research Coverage | ||

Alexandria is currently covered by the following research analysts. This list may be incomplete and is subject to change as firms initiate or discontinue coverage of our company. Please note that any opinions, estimates, or forecasts regarding our historical or predicted performance made by these analysts are theirs alone and do not represent opinions, estimates, or forecasts of Alexandria or our management. Alexandria does not by our reference or distribution of the information below imply our endorsement of or concurrence with any opinions, estimates, or forecasts of these analysts. Interested persons may obtain copies of analysts’ reports on their own as we do not distribute these reports. Several of these firms may, from time to time, own our stock and/or hold other long or short positions in our stock and may provide compensated services to us. | ||

| Bank of America Merrill Lynch | Citigroup Global Markets Inc. | JMP Securities | RBC Capital Markets | |||||||||||||||||

| Jamie Feldman | Michael Bilerman / Michael Griffin | Aaron Hecht | Michael Carroll | |||||||||||||||||

| (646) 855-5808 | (212) 816-1383 / (212) 816-5871 | (415) 835-3963 | (440) 715-2649 | |||||||||||||||||

| Berenberg Capital Markets | Evercore ISI | J.P. Morgan Securities LLC | Robert W. Baird & Co. Incorporated | |||||||||||||||||

| Connor Siversky | Sheila McGrath / Wendy Ma | Anthony Paolone / Ray Zhong | David Rodgers / Nicholas Thillman | |||||||||||||||||

| (646) 949-9037 | (212) 497-0882 / (212) 497-0870 | (212) 622-6682 / (212) 622-5411 | (216) 737-7341 / (414) 298-5053 | |||||||||||||||||

| BTIG, LLC | Green Street | Mizuho Securities USA LLC | SMBC Nikko Securities America, Inc. | |||||||||||||||||

| Tom Catherwood / John Nickodemus | Daniel Ismail / Dylan Burzinski | Vikram Malhotra / Georgi Dinkov | Richard Anderson / Jay Kornreich | |||||||||||||||||

| (212) 738-6140 / (212) 738-6050 | (949) 640-8780 / (949) 640-8780 | (212) 282-3827 / (617) 352-1721 | (646) 521-2351 / (646) 424-3202 | |||||||||||||||||

| CFRA | ||||||||||||||||||||

| Kenneth Leon | ||||||||||||||||||||

| (646) 517-2552 | ||||||||||||||||||||

| Fixed Income Coverage | Rating Agencies | |||||||||||||||||||

| Barclays Capital Inc. | Stifel Financial Corp. | Moody’s Investors Service | S&P Global Ratings | |||||||||||||||||

| Srinjoy Banerjee | Thierry Perrein | (212) 553-0376 | Fernanda Hernandez / Michael Souers | |||||||||||||||||

| (212) 526-3521 | (646) 376-5303 | (212) 438-1347 / (212) 438-2508 | ||||||||||||||||||

| J.P. Morgan Securities LLC | ||||||||||||||||||||

| Mark Streeter / Ian Snyder | ||||||||||||||||||||

| (212) 834-5086 / (212) 834-3798 | ||||||||||||||||||||

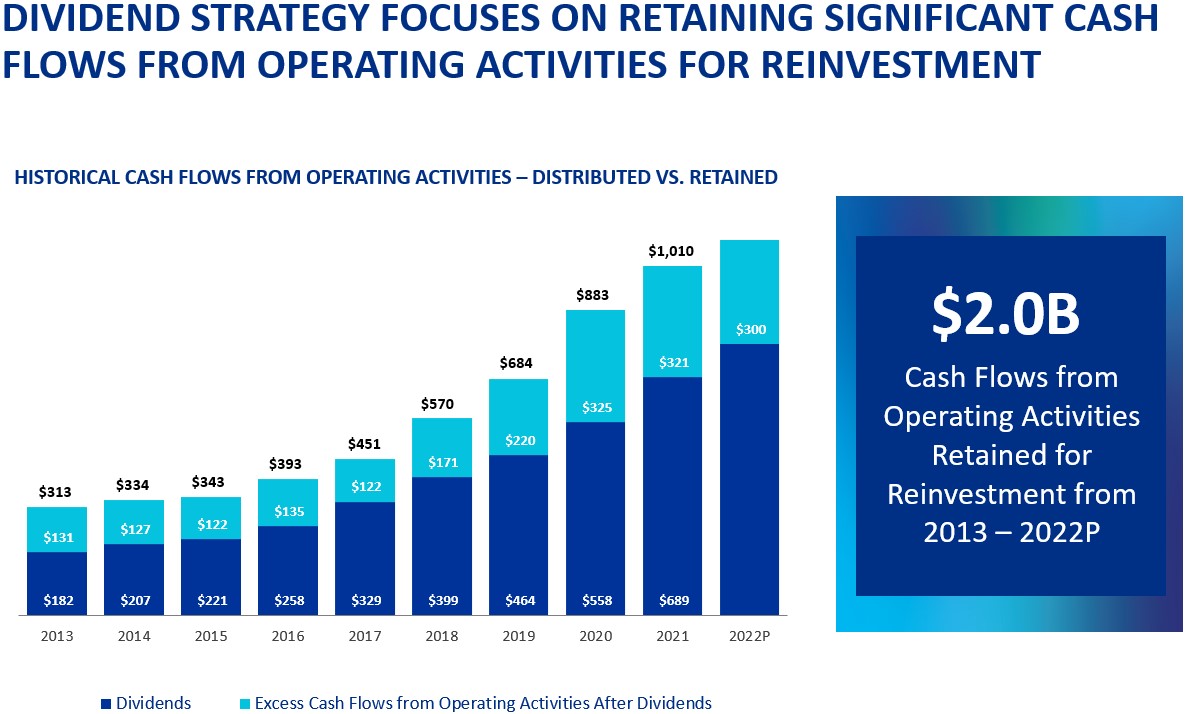

| Financial and Asset Base Highlights | |

||||

June 30, 2022 | |||||

| (Dollars in thousands, except per share amounts) | |||||

| Three Months Ended (unless stated otherwise) | ||||||||||||||||||||||||||||||||

| 6/30/22 | 3/31/22 | 12/31/21 | 9/30/21 | 6/30/21 | ||||||||||||||||||||||||||||

Selected financial data from consolidated financial statements and related information |

||||||||||||||||||||||||||||||||

Rental revenues |

$ | 485,067 | $ | 469,537 | $ | 435,637 | $ | 415,918 | $ | 396,804 | ||||||||||||||||||||||

Tenant recoveries |

$ | 155,892 | $ | 143,017 | $ | 139,019 | $ | 130,609 | $ | 111,567 | ||||||||||||||||||||||

| General and administrative expenses | $ | 43,397 | $ | 40,931 | $ | 41,654 | $ | 37,931 | $ | 37,880 | ||||||||||||||||||||||

|

General and administrative expenses as a percentage of net operating income –

trailing 12 months

|

9.8% | 10.0% | 10.2% | 10.1% | 9.8% | |||||||||||||||||||||||||||

| Operating margin | 70% | 71% | 70% | 70% | 72% | |||||||||||||||||||||||||||

Adjusted EBITDA margin |

70% | 71% | 71% | 71% | 73% | |||||||||||||||||||||||||||

Adjusted EBITDA – quarter annualized |

$ | 1,797,488 | $ | 1,734,956 | $ | 1,631,244 | $ | 1,557,652 | $ | 1,483,576 | ||||||||||||||||||||||

Adjusted EBITDA – trailing 12 months |

$ | 1,680,335 | $ | 1,601,857 | $ | 1,517,838 | $ | 1,442,929 | $ | 1,371,586 | ||||||||||||||||||||||

Net debt at end of period |

$ | 9,832,722 | $ | 9,514,256 | $ | 8,442,115 | $ | 8,960,645 | $ | 8,550,339 | ||||||||||||||||||||||

| Net debt and preferred stock to Adjusted EBITDA – quarter annualized | 5.5x | 5.5x | 5.2x | 5.8x | 5.8x | |||||||||||||||||||||||||||

| Net debt and preferred stock to Adjusted EBITDA – trailing 12 months | 5.9x | 5.9x | 5.6x | 6.2x | 6.2x | |||||||||||||||||||||||||||

| Total debt and preferred stock at end of period | $ | 10,271,406 | $ | 10,303,247 | $ | 8,791,866 | $ | 9,263,587 | $ | 8,840,999 | ||||||||||||||||||||||

| Gross assets at end of period | $ | 37,304,589 | $ | 36,795,922 | $ | 33,990,614 | $ | 32,173,158 | $ | 30,480,630 | ||||||||||||||||||||||

| Total debt and preferred stock to gross assets at end of period | 28% | 28% | 26% | 29% | 29% | |||||||||||||||||||||||||||

Fixed-charge coverage ratio – quarter annualized |

5.1x | 5.1x | 5.3x | 5.1x | 4.9x | |||||||||||||||||||||||||||

Fixed-charge coverage ratio – trailing 12 months |

5.1x | 5.1x | 5.0x | 4.8x | 4.6x | |||||||||||||||||||||||||||

Unencumbered net operating income as a percentage of total net operating income |

100% | 97% | 97% | 97% | 97% | |||||||||||||||||||||||||||

Closing stock price at end of period |

$ | 145.03 | $ | 201.25 | $ | 222.96 | $ | 191.07 | $ | 181.94 | ||||||||||||||||||||||

Common shares outstanding (in thousands) at end of period |

161,456 | 161,408 | 158,044 | 153,284 | 150,708 | |||||||||||||||||||||||||||

Total equity capitalization at end of period |

$ | 23,415,970 | $ | 32,483,420 | $ | 35,237,463 | $ | 29,287,880 | $ | 27,419,791 | ||||||||||||||||||||||

Total market capitalization at end of period |

$ | 33,687,376 | $ | 42,786,667 | $ | 44,029,329 | $ | 38,551,467 | $ | 36,260,790 | ||||||||||||||||||||||

Dividend per share – quarter/annualized |

$1.18/$4.72 | $1.15/$4.60 | $1.15/$4.60 | $1.12/$4.48 | $1.12/$4.48 | |||||||||||||||||||||||||||

Dividend payout ratio for the quarter |

56% | 57% | 60% | 58% | 60% | |||||||||||||||||||||||||||

Dividend yield – annualized |

3.3% | 2.3% | 2.1% | 2.3% | 2.5% | |||||||||||||||||||||||||||

Amounts related to operating leases: |

||||||||||||||||||||||||||||||||

| Operating lease liabilities at end of period | $ | 412,535 | $ | 405,818 | $ | 434,745 | $ | 371,538 | $ | 371,905 | ||||||||||||||||||||||

Rent expense |

$ | 7,924 | $ | 7,718 | $ | 7,124 | $ | 6,228 | $ | 6,213 | ||||||||||||||||||||||

Capitalized interest |

$ | 68,202 | $ | 57,763 | $ | 44,078 | $ | 43,185 | $ | 43,492 | ||||||||||||||||||||||

Weighted-average interest rate for capitalization of interest during the period |

3.56% | 3.26% | 3.22% | 3.30% | 3.47% | |||||||||||||||||||||||||||

| Financial and Asset Base Highlights (continued) | |

||||

June 30, 2022 | |||||

| (Dollars in thousands, except annual rental revenue per occupied RSF amounts) | |||||

| Three Months Ended (unless stated otherwise) | ||||||||||||||||||||||||||||||||

| 6/30/22 | 3/31/22 | 12/31/21 | 9/30/21 | 6/30/21 | ||||||||||||||||||||||||||||

| Amounts included in funds from operations and non-revenue-enhancing capital expenditures | ||||||||||||||||||||||||||||||||

Straight-line rent revenue |

$ | 27,362 | $ | 42,025 | $ | 25,942 | $ | 33,918 | $ | 27,903 | ||||||||||||||||||||||

Amortization of acquired below-market leases |

$ | 16,760 | $ | 13,915 | $ | 15,737 | $ | 13,664 | $ | 13,267 | ||||||||||||||||||||||

| Straight-line rent expense on ground leases | $ | 354 | $ | 416 | $ | 301 | $ | 58 | $ | 248 | ||||||||||||||||||||||

Stock compensation expense |

$ | 14,340 | $ | 14,028 | $ | 14,253 | $ | 9,728 | $ | 12,242 | ||||||||||||||||||||||

Amortization of loan fees |

$ | 3,236 | $ | 3,103 | $ | 2,911 | $ | 2,854 | $ | 2,859 | ||||||||||||||||||||||

| Amortization of debt (discounts) premiums | $ | (267) | $ | 424 | $ | 502 | $ | 498 | $ | 465 | ||||||||||||||||||||||

Non-revenue-enhancing capital expenditures: |

||||||||||||||||||||||||||||||||

Building improvements |

$ | 4,199 | $ | 4,110 | $ | 4,027 | $ | 3,901 | $ | 3,669 | ||||||||||||||||||||||

Tenant improvements and leasing commissions |

$ | 24,562 | $ | 27,791 | $ | 109,516 | $ | 16,409 | $ | 47,439 | ||||||||||||||||||||||

Operating statistics and related information (at end of period) |

||||||||||||||||||||||||||||||||

Number of properties – North America |

436 | 446 | 414 | 407 | 381 | |||||||||||||||||||||||||||

RSF – North America (including development and redevelopment projects under construction) |

46,934,653 | 47,364,067 | 43,670,737 | 43,044,195 | 40,076,883 | |||||||||||||||||||||||||||

Total square feet – North America |

74,087,636 | 74,185,859 | 66,970,705 | 63,858,780 | 58,108,390 | |||||||||||||||||||||||||||

| Annual rental revenue per occupied RSF – North America | $ | 50.80 | $ | 49.42 | $ | 48.65 | $ | 47.73 | $ | 48.65 | ||||||||||||||||||||||

| Occupancy of operating properties – North America | 94.6% | 94.7% | 94.0% | 94.4% | 94.3% | |||||||||||||||||||||||||||

| Occupancy of operating properties – North America (excluding vacancy at recently acquired properties) | 98.4% | (1) |

98.6% | 98.7% | 98.5% | 98.1% | ||||||||||||||||||||||||||

| Occupancy of operating and redevelopment properties – North America | 89.0% | 88.9% | 88.5% | 89.6% | 90.1% | |||||||||||||||||||||||||||

Weighted-average remaining lease term (in years) |

7.1 | 7.3 | 7.5 | 7.4 | 7.5 | |||||||||||||||||||||||||||

Total leasing activity – RSF |

2,279,758 | 2,463,438 | 4,094,174 | 1,810,630 | 1,933,838 | |||||||||||||||||||||||||||

Lease renewals and re-leasing of space – change in average new rental rates over expiring rates: |

||||||||||||||||||||||||||||||||

Rental rate increases |

45.4% | 32.2% | 35.9% | 35.3% | 42.4% | |||||||||||||||||||||||||||

| Rental rate increases (cash basis) | 33.9% | 16.5% | 22.9% | 19.3% | 25.4% | |||||||||||||||||||||||||||

| RSF (included in total leasing activity above) | 1,087,082 | 864,077 | 1,947,727 | 671,775 | 1,472,713 | |||||||||||||||||||||||||||

Same property – percentage change over comparable quarter from prior year: |

||||||||||||||||||||||||||||||||

| Net operating income increase | 7.5% | 7.6% | 5.0% | 3.0% | 3.7% | |||||||||||||||||||||||||||

| Net operating income increase (cash basis) | 10.2% | 7.3% | 7.5% | 7.1% | 7.8% | |||||||||||||||||||||||||||

|

|||||

| High-Quality, Diverse, and Innovative Tenants | |||||

June 30, 2022 | |||||

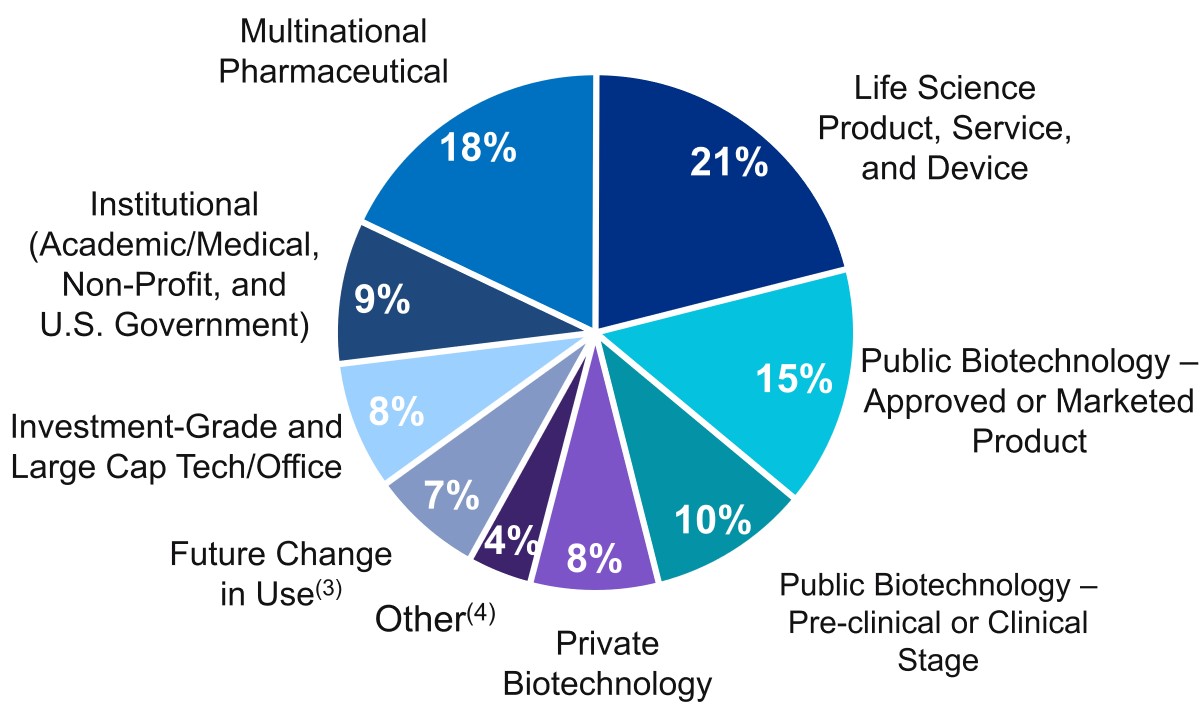

| Investment-Grade or Publicly Traded Large Cap Tenants |

Industry Mix of 1,000+ Tenants |

||||||||||||||||

|

|||||||||||||||||

| 50% | |||||||||||||||||

of ARE’s Total Annual Rental Revenue(1) |

|||||||||||||||||

| Long-Duration Lease Terms | |||||||||||||||||

| 7.1 Years | |||||||||||||||||

Weighted-Average Remaining Term(2) |

|||||||||||||||||

Percentage of ARE’s Annual Rental Revenue(1) |

|||||||||||||||||

|

|||||

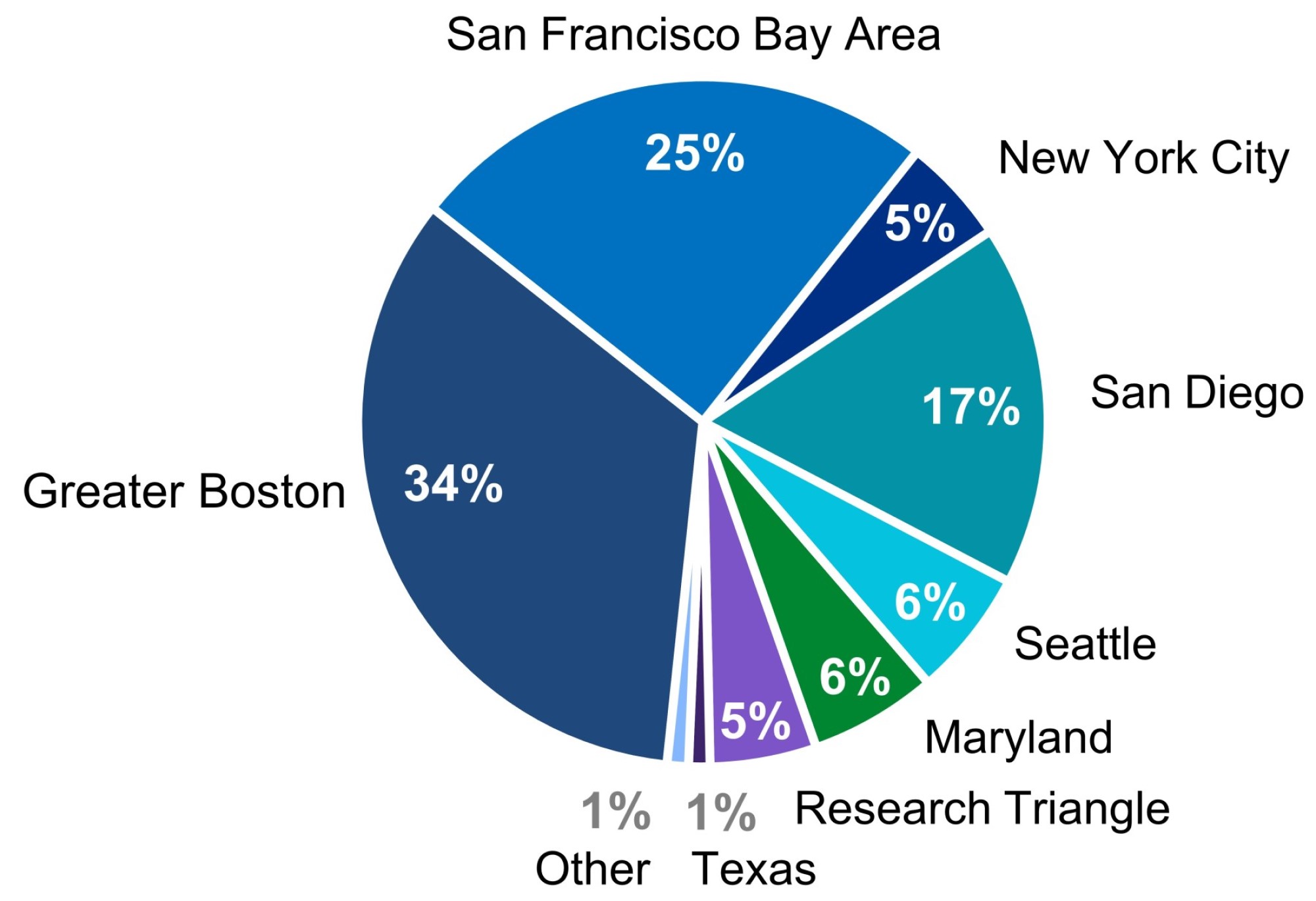

| Class A Properties in AAA Locations | |||||

June 30, 2022 | |||||

| Industry-Leading Tenant Roster |

AAA Locations | |||||||||||||

|

||||||||||||||

| 86% | ||||||||||||||

| of ARE’s Top 20 Tenants | ||||||||||||||

Annual Rental Revenue(1) |

||||||||||||||

| Is From Investment-Grade | ||||||||||||||

| or Publicly Traded Large Cap Tenants | ||||||||||||||

Percentage of ARE’s Annual Rental Revenue(2) |

||||||||||||||

|

|||||

| Occupancy | |||||

June 30, 2022 | |||||

Solid Historical Occupancy(1) |

Occupancy Across Key Locations | |||||||||||||

|

||||||||||||||

| 96% | ||||||||||||||

| Over 10 Years | ||||||||||||||

As of June 30, 2022 |

Percentage of Vacancy Leased/Negotiating RSF | ||||||||||||||||||||||||||||||||||

| Vacant RSF |

Operating Properties Occupancy Impact | ||||||||||||||||||||||||||||||||||

| Property | Market/Submarket | Region | North America | ||||||||||||||||||||||||||||||||

| Intersection Campus | Texas/Austin | 159,638 | 9.6 | % | 0.4 | % | 100 | % | |||||||||||||||||||||||||||

| 601 and 611 Gateway Boulevard | San Francisco Bay Area/South San Francisco | 153,596 | 1.8 | % | 0.4 | 46 | |||||||||||||||||||||||||||||

Alexandria Center® for Life Science – Durham |

Research Triangle/Research Triangle | 128,387 | 3.6 | % | 0.3 | 53 | |||||||||||||||||||||||||||||

| 275 Grove Street | Greater Boston/Route 128 | 124,240 | 1.2 | % | 0.3 | — | (3) |

||||||||||||||||||||||||||||

Alexandria Center® for Life Science – Fenway |

Greater Boston/Fenway | 89,458 | 0.8 | % | 0.2 | 20 | |||||||||||||||||||||||||||||

| Other acquisitions | Various | 909,833 | N/A | 2.2 | 24 | ||||||||||||||||||||||||||||||

| 1,565,152 | 3.8 | % | 34 | % | |||||||||||||||||||||||||||||||

|

|||||

| Key Operating Metrics | |||||

June 30, 2022 | |||||

| Historical Same Property Net Operating Income Growth |

Favorable Lease Structure(1) |

|||||||||||||||||||||||||||||||

|

|

Strategic Lease Structure by Owner and Operator of Collaborative Life Science, Agtech, and Technology Campuses |

||||||||||||||||||||||||||||||

| Increasing cash flows | ||||||||||||||||||||||||||||||||

|

Percentage of leases containing

annual rent escalations

|

97% | |||||||||||||||||||||||||||||||

| Stable cash flows | ||||||||||||||||||||||||||||||||

|

Percentage of triple

net leases

|

91% | |||||||||||||||||||||||||||||||

| Lower capex burden | ||||||||||||||||||||||||||||||||

|

Percentage of leases providing for the

recapture of capital expenditures

|

94% | |||||||||||||||||||||||||||||||

| Historical Rental Rate Growth: Renewed/Re-Leased Space |

Margins(2) |

|||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||

| Operating | Adjusted EBITDA | |||||||||||||||||||||||||||||||

| 70% | 70% | |||||||||||||||||||||||||||||||

| Same Property Performance | |

||||

June 30, 2022 | |||||

| (Dollars in thousands) | |||||

| June 30, 2022 | June 30, 2022 | |||||||||||||||||||||||||||||||

Same Property Financial Data |

Three Months Ended | Six Months Ended | Same Property Statistical Data |

Three Months Ended | Six Months Ended | |||||||||||||||||||||||||||

Percentage change over comparable period from prior year: |

Number of same properties |

287 | 266 | |||||||||||||||||||||||||||||

Net operating income increase |

7.5% | 7.7% | Rentable square feet |

28,897,189 | 27,008,468 | |||||||||||||||||||||||||||

Net operating income increase (cash basis) |

10.2% | 8.6% | Occupancy – current-period average |

95.9% | 95.8% | |||||||||||||||||||||||||||

Operating margin |

71% | 71% | Occupancy – same-period prior-year average |

94.5% | 94.6% | |||||||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | $ Change | % Change | 2022 | 2021 | $ Change | % Change | |||||||||||||||||||||||||||||||||||||||||||

| Income from rentals: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Same properties | $ | 378,130 | $ | 350,577 | $ | 27,553 | 7.9 | % | $ | 708,840 | $ | 656,182 | $ | 52,658 | 8.0 | % | ||||||||||||||||||||||||||||||||||

| Non-same properties | 106,937 | 46,227 | 60,710 | 131.3 | 245,764 | 110,855 | 134,909 | 121.7 | ||||||||||||||||||||||||||||||||||||||||||

| Rental revenues | 485,067 | 396,804 | 88,263 | 22.2 | 954,604 | 767,037 | 187,567 | 24.5 | ||||||||||||||||||||||||||||||||||||||||||

| Same properties | 124,693 | 101,088 | 23,605 | 23.4 | 235,108 | 196,835 | 38,273 | 19.4 | ||||||||||||||||||||||||||||||||||||||||||

| Non-same properties | 31,199 | 10,479 | 20,720 | 197.7 | 63,801 | 23,194 | 40,607 | 175.1 | ||||||||||||||||||||||||||||||||||||||||||

| Tenant recoveries | 155,892 | 111,567 | 44,325 | 39.7 | 298,909 | 220,029 | 78,880 | 35.8 | ||||||||||||||||||||||||||||||||||||||||||

| Income from rentals | 640,959 | 508,371 | 132,588 | 26.1 | 1,253,513 | 987,066 | 266,447 | 27.0 | ||||||||||||||||||||||||||||||||||||||||||

| Same properties | 193 | 134 | 59 | 44.0 | 324 | 209 | 115 | 55.0 | ||||||||||||||||||||||||||||||||||||||||||

| Non-same properties | 2,612 | 1,114 | 1,498 | 134.5 | 4,992 | 2,193 | 2,799 | 127.6 | ||||||||||||||||||||||||||||||||||||||||||

| Other income | 2,805 | 1,248 | 1,557 | 124.8 | 5,316 | 2,402 | 2,914 | 121.3 | ||||||||||||||||||||||||||||||||||||||||||

| Same properties | 503,016 | 451,799 | 51,217 | 11.3 | 944,272 | 853,226 | 91,046 | 10.7 | ||||||||||||||||||||||||||||||||||||||||||

| Non-same properties | 140,748 | 57,820 | 82,928 | 143.4 | 314,557 | 136,242 | 178,315 | 130.9 | ||||||||||||||||||||||||||||||||||||||||||

| Total revenues | 643,764 | 509,619 | 134,145 | 26.3 | 1,258,829 | 989,468 | 269,361 | 27.2 | ||||||||||||||||||||||||||||||||||||||||||

| Same properties | 147,045 | 120,686 | 26,359 | 21.8 | 271,903 | 228,963 | 42,940 | 18.8 | ||||||||||||||||||||||||||||||||||||||||||

| Non-same properties | 49,239 | 23,269 | 25,970 | 111.6 | 105,709 | 52,880 | 52,829 | 99.9 | ||||||||||||||||||||||||||||||||||||||||||

| Rental operations | 196,284 | 143,955 | 52,329 | 36.4 | 377,612 | 281,843 | 95,769 | 34.0 | ||||||||||||||||||||||||||||||||||||||||||

| Same properties | 355,971 | 331,113 | 24,858 | 7.5 | 672,369 | 624,263 | 48,106 | 7.7 | ||||||||||||||||||||||||||||||||||||||||||

| Non-same properties | 91,509 | 34,551 | 56,958 | 164.9 | 208,848 | 83,362 | 125,486 | 150.5 | ||||||||||||||||||||||||||||||||||||||||||

| Net operating income | $ | 447,480 | $ | 365,664 | $ | 81,816 | 22.4 | % | $ | 881,217 | $ | 707,625 | $ | 173,592 | 24.5 | % | ||||||||||||||||||||||||||||||||||

Net operating income – same properties |

$ | 355,971 | $ | 331,113 | $ | 24,858 | 7.5 | % | $ | 672,369 | $ | 624,263 | $ | 48,106 | 7.7 | % | ||||||||||||||||||||||||||||||||||

| Straight-line rent revenue | (15,859) | (22,214) | 6,355 | (28.6) | (41,101) | (41,360) | 259 | (0.6) | ||||||||||||||||||||||||||||||||||||||||||

| Amortization of acquired below-market leases | (9,875) | (9,338) | (537) | 5.8 | (14,063) | (14,365) | 302 | (2.1) | ||||||||||||||||||||||||||||||||||||||||||

Net operating income – same properties (cash basis) |

$ | 330,237 | $ | 299,561 | $ | 30,676 | 10.2 | % | $ | 617,205 | $ | 568,538 | $ | 48,667 | 8.6 | % | ||||||||||||||||||||||||||||||||||

| Leasing Activity | |

||||

June 30, 2022 | |||||

| (Dollars per RSF) | |||||

| Three Months Ended | Six Months Ended | Year Ended | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| June 30, 2022 | June 30, 2022 | December 31, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Including Straight-Line Rent |

Cash Basis | Including Straight-Line Rent |

Cash Basis | Including Straight-Line Rent |

Cash Basis | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Leasing activity: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Renewed/re-leased space(1) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Rental rate changes |

45.4% | (2) |

33.9% | (2) |

39.0% | 25.2% | 37.9% | 22.6% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

New rates |

$54.34 | $52.31 | $56.61 | $54.47 | $59.00 | $55.60 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Expiring rates |

$37.36 | $39.07 | $40.73 | $43.50 | $42.80 | $45.36 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

RSF |

1,087,082 | 1,951,159 | 4,614,040 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Tenant improvements/leasing commissions |

$22.54 | $26.83 | $41.05 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Weighted-average lease term |

5.2 years | 4.8 years | 6.3 years | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Developed/redeveloped/previously vacant space leased(3) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

New rates |

$76.69 | $68.39 | $79.72 | $70.20 | $78.52 | $69.42 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

RSF |

1,192,676 | 2,792,037 | 4,902,261 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Weighted-average lease term |

12.7 years | 12.9 years | 11.2 years | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Leasing activity summary (totals): |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

New rates |

$66.03 | $60.72 | $70.21 | $63.73 | $69.05 | $62.72 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

RSF |

2,279,758 | 4,743,196 | (4) |

9,516,301 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Weighted-average lease term |

9.1 years | 9.5 years | 8.8 years | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Lease expirations(1) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Expiring rates |

$34.82 | $36.26 | $38.15 | $38.30 | $41.53 | $43.70 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| RSF | 1,572,185 | 3,094,767 | 5,747,192 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||

| Contractual Lease Expirations | |||||

June 30, 2022 | |||||

| Year | RSF | Percentage of Occupied RSF |

Annual Rental Revenue (per RSF)(1) |

Percentage of Total Annual Rental Revenue |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | (2) |

987,720 | 2.6 | % | $ | 51.62 | 2.6 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 3,897,615 | 10.1 | % | $ | 44.39 | 9.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2024 | 3,444,777 | 8.9 | % | $ | 45.38 | 8.1 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2025 | 3,488,483 | 9.0 | % | $ | 48.77 | 8.8 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2026 | 2,515,497 | 6.5 | % | $ | 50.94 | 6.6 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2027 | 2,671,591 | 6.9 | % | $ | 53.50 | 7.4 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2028 | 3,782,340 | 9.8 | % | $ | 49.10 | 9.6 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2029 | 2,345,066 | 6.1 | % | $ | 58.28 | 7.1 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2030 | 2,486,008 | 6.4 | % | $ | 56.28 | 7.3 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2031 | 3,034,985 | 7.9 | % | $ | 52.91 | 8.3 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Thereafter | 9,987,771 | 25.8 | % | $ | 48.39 | 25.2 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Market |

2022 Contractual Lease Expirations (in RSF) |

Annual Rental Revenue

(per RSF)(1)

|

2023 Contractual Lease Expirations (in RSF) |

Annual Rental Revenue

(per RSF)(1)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Leased | Negotiating/ Anticipating |

Targeted for

Development/

Redevelopment(3)

|

Remaining

Expiring

Leases(4)

|

Total(2) |

Leased | Negotiating/ Anticipating |

Targeted for

Development/

Redevelopment(3)

|

Remaining Expiring Leases |

Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Greater Boston | 36,379 | — | 48,793 | 118,677 | 203,849 | $ | 75.06 | 110,943 | 80,506 | 323,110 | 637,785 | 1,152,344 | $ | 57.53 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| San Francisco Bay Area | — | 74,992 | — | 60,622 | 135,614 | 44.87 | 15,711 | 160,622 | 250,000 | 338,410 | 764,743 | 59.11 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New York City | — | — | — | 24,303 | 24,303 | N/A | — | — | — | 85,055 | 85,055 | N/A | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| San Diego | 165,146 | — | 34,715 | 91,376 | 291,237 | 47.45 | 6,619 | 10,563 | 269,048 | 699,206 | 985,436 | 26.62 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Seattle | — | 7,566 | 50,552 | 41,087 | 99,205 | 13.67 | — | — | 110,885 | 266,752 | 377,637 | 25.19 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maryland | 34,001 | 21,241 | — | 59,988 | 115,230 | 22.95 | — | 74,054 | — | 218,233 | 292,287 | 28.18 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Research Triangle | — | — | — | 30,855 | 30,855 | 35.48 | — | 81,956 | — | 126,941 | 208,897 | 32.40 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Texas | 65,188 | — | — | — | 65,188 | 24.89 | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Canada | — | 14,590 | — | — | 14,590 | 34.66 | — | 13,321 | — | — | 13,321 | 29.99 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-cluster/other markets | — | — | — | 7,649 | 7,649 | 82.26 | — | — | — | 17,895 | 17,895 | 68.01 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | 300,714 | 118,389 | 134,060 | 434,557 | 987,720 | $ | 51.62 | 133,273 | 421,022 | 953,043 | 2,390,277 | 3,897,615 | $ | 44.39 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Percentage of expiring leases |

30 | % | 12 | % | 14 | % | 44 | % | 100 | % | 3 | % | 11 | % | 24 | % | 62 | % | 100 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Top 20 Tenants | |

||||

June 30, 2022 | |||||

| (Dollars in thousands, except average market cap amounts) | |||||

| Tenant | Remaining Lease Term(1) (in years) |

Aggregate RSF |

Annual Rental Revenue(1) |

Percentage of Aggregate Annual Rental Revenue(1) |

Investment-Grade Credit Ratings |

Average Market Cap(1)

(in billions)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Moody’s | S&P | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | Bristol-Myers Squibb Company | 6.4 | 919,292 | $ | 67,575 | 3.5 | % | A2 | A+ | $ | 146.4 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | Eli Lilly and Company | 7.0 | 733,781 | 48,836 | 2.5 | A2 | A+ | $ | 252.5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | Moderna, Inc. | 15.1 | 878,933 | 48,777 | 2.5 | — | — | $ | 98.2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | Sanofi | 6.3 | 490,154 | 42,284 | 2.2 | A1 | AA | $ | 129.6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | Takeda Pharmaceutical Company Limited | 7.5 | 549,760 | 37,399 | 1.9 | Baa2 | BBB+ | $ | 47.3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6 | Illumina, Inc. | 8.1 | 891,495 | 36,196 | 1.9 | Baa3 | BBB | $ | 57.0 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 7 | 2seventy bio, Inc.(2) |

11.2 | 312,805 | 33,617 | 1.7 | — | — | $ | 0.5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 8 | Novartis AG | 6.1 | 447,831 | 30,582 | 1.6 | A1 | AA- | $ | 211.3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 9 | TIBCO Software Inc. | 4.7 | (3) |

292,013 | 28,537 | 1.5 | — | — | $ | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 10 | Uber Technologies, Inc. | 60.2 | (4) |

1,009,188 | 27,677 | 1.4 | — | — | $ | 71.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 11 | Roche | 7.0 | 416,833 | 26,541 | 1.4 | Aa3 | AA | $ | 326.1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12 | Merck & Co., Inc. | 10.4 | 339,344 | 21,889 | 1.1 | A1 | A+ | $ | 204.3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 13 | Maxar Technologies | 3.5 | (5) |

478,000 | 21,803 | 1.1 | — | — | $ | 2.2 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 14 | Massachusetts Institute of Technology | 6.5 | 257,626 | 21,165 | 1.1 | Aaa | AAA | $ | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 15 | The Children's Hospital Corporation | 14.3 | 269,816 | 20,066 | 1.0 | Aa2 | AA | $ | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 16 | New York University | 9.4 | 203,500 | 19,241 | 1.0 | Aa2 | AA- | $ | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 17 | Pfizer Inc. | 3.0 | 416,996 | 17,742 | 0.9 | A2 | A+ | $ | 276.2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 18 | Apple Inc. | 2.9 | 604,382 | 17,512 | 0.9 | Aaa | AA+ | $ | 2,560.6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 19 | United States Government | 7.6 | 315,908 | 17,491 | 0.9 | Aaa | AA+ | $ | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 20 | Alphabet Inc. | 4.7 | 354,304 | 16,985 | 0.9 | Aa2 | AA+ | $ | 1,775.6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total/weighted-average |

10.2 | (4) |

10,181,961 | $ | 601,915 | 31.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Summary of Properties and Occupancy | |

||||

June 30, 2022 | |||||

| (Dollars in thousands, except per RSF amounts) | |||||

Market |

RSF | Number of Properties | Annual Rental Revenue | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating | Development | Redevelopment | Total | % of Total | Total | % of Total | Per RSF | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Greater Boston |

10,654,420 | 1,887,038 | 1,300,281 | 13,841,739 | 29 | % | 85 | $ | 661,389 | 34 | % | $ | 65.33 | ||||||||||||||||||||||||||||||||||||||||||||||

| San Francisco Bay Area | 8,678,996 | 230,592 | 300,010 | 9,209,598 | 20 | 72 | 477,206 | 25 | 61.26 | ||||||||||||||||||||||||||||||||||||||||||||||||||

New York City |

1,204,461 | — | 65,558 | 1,270,019 | 3 | 5 | 96,228 | 5 | 82.14 | ||||||||||||||||||||||||||||||||||||||||||||||||||

San Diego |

8,000,319 | 229,094 | — | 8,229,413 | 18 | 102 | 331,296 | 17 | 42.98 | ||||||||||||||||||||||||||||||||||||||||||||||||||

Seattle |

2,813,803 | 311,631 | 213,976 | 3,339,410 | 7 | 46 | 108,333 | 6 | 39.60 | ||||||||||||||||||||||||||||||||||||||||||||||||||

Maryland |

3,427,753 | 282,000 | 122,856 | 3,832,609 | 8 | 50 | 111,204 | 6 | 33.79 | ||||||||||||||||||||||||||||||||||||||||||||||||||

Research Triangle |

3,550,170 | 329,718 | 376,871 | 4,256,759 | 9 | 42 | 94,291 | 5 | 28.41 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Texas | 1,668,718 | — | 201,499 | 1,870,217 | 4 | 14 | 36,884 | 1 | 28.20 | ||||||||||||||||||||||||||||||||||||||||||||||||||

Canada |

614,028 | — | — | 614,028 | 1 | 7 | 11,190 | — | 23.74 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-cluster/other markets | 412,128 | — | — | 412,128 | 1 | 12 | 14,415 | 1 | 45.58 | ||||||||||||||||||||||||||||||||||||||||||||||||||

Properties held for sale |

58,733 | — | — | 58,733 | — | 1 | 428 | — | N/A | ||||||||||||||||||||||||||||||||||||||||||||||||||

| North America | 41,083,529 | 3,270,073 | 2,581,051 | 46,934,653 | 100 | % | 436 | $ | 1,942,864 | 100 | % | $ | 50.80 | ||||||||||||||||||||||||||||||||||||||||||||||

| 5,851,124 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Properties | Operating and Redevelopment Properties | |||||||||||||||||||||||||||||||||||||

| Market | 6/30/22 | 3/31/22 | 6/30/21 | 6/30/22 | 3/31/22 | 6/30/21 | ||||||||||||||||||||||||||||||||

| Greater Boston | 95.0 | % | (1) |

95.4 | % | 95.5 | % | 84.7 | % | 85.0 | % | 91.0 | % | |||||||||||||||||||||||||

| San Francisco Bay Area | 95.8 | 95.6 | 94.0 | 92.6 | 92.4 | 92.9 | ||||||||||||||||||||||||||||||||

| New York City | 97.3 | (2) |

98.4 | 99.4 | 92.2 | 91.9 | 90.1 | |||||||||||||||||||||||||||||||

| San Diego | 96.3 | 94.2 | 93.8 | 96.3 | 92.7 | 92.3 | ||||||||||||||||||||||||||||||||

| Seattle | 97.2 | 97.9 | 97.6 | 90.4 | 91.0 | 90.2 | ||||||||||||||||||||||||||||||||

| Maryland | 97.6 | (3) |

100.0 | 98.9 | 94.2 | 96.4 | 90.3 | |||||||||||||||||||||||||||||||

| Research Triangle | 93.5 | 93.6 | 92.8 | 84.5 | 85.5 | 84.1 | ||||||||||||||||||||||||||||||||

| Texas | 78.4 | N/A | N/A | 69.9 | N/A | N/A | ||||||||||||||||||||||||||||||||

| Subtotal | 95.1 | 95.7 | 95.2 | 89.3 | 89.8 | 90.9 | ||||||||||||||||||||||||||||||||

| Canada | 76.8 | 76.5 | 77.0 | 76.8 | 76.5 | 77.0 | ||||||||||||||||||||||||||||||||

| Non-cluster/other markets | 76.7 | 80.4 | 46.0 | 76.7 | 75.7 | 46.0 | ||||||||||||||||||||||||||||||||

| North America | 94.6 | % | (4) |

94.7 | % | 94.3 | % | 89.0 | % | 88.9 | % | 90.1 | % | |||||||||||||||||||||||||

| Property Listing | |

||||

June 30, 2022 | |||||

| (Dollars in thousands) | |||||

Market / Submarket / Address |

RSF |

Number of Properties | Annual Rental Revenue | Occupancy Percentage |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating | Operating and Redevelopment | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating | Development | Redevelopment | Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Greater Boston | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cambridge/Inner Suburbs | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: Alexandria Center® at Kendall Square |

2,369,854 | — | 403,892 | 2,773,746 | 11 | $ | 185,373 | 98.9 | % | 84.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

50(2), 60(2), 75/125(2), 100(2), and 225(2) Binney Street, 161 and 215 First Street, 150 Second Street, 300 Third Street(2), 11 Hurley Street, and One Rogers Street |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: Alexandria Center® at One Kendall Square |

903,777 | 462,100 | — | 1,365,877 | 12 | 83,028 | 97.7 | 97.7 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| One Kendall Square – Buildings 100, 200, 300, 400, 500, 600/700, 1400, 1800, and 2000, 325 and 399 Binney Street, and One Hampshire Street | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: Alexandria Technology Square® |

1,181,635 | — | — | 1,181,635 | 7 | 114,427 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

100, 200, 300, 400, 500, 600, and 700 Technology Square |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mega Campus: The Arsenal on the Charles | 772,557 | 248,018 | 100,108 | 1,120,683 | 13 | 44,134 | 94.8 | 84.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 311, 321, and 343 Arsenal Street, 300, 400, and 500 North Beacon Street, 1, 2, 3, and 4 Kingsbury Avenue, and 100, 200, and 400 Talcott Avenue |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mega Campus: 480 Arsenal Way and 500 and 550 Arsenal Street | 495,127 | — | — | 495,127 | 3 | 23,014 | 98.3 | 98.3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

99 Coolidge Avenue(2) |

— | 320,809 | — | 320,809 | 1 | — | N/A | N/A | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

640 Memorial Drive |

225,504 | — | — | 225,504 | 1 | 15,551 | 82.1 | 82.1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 780 and 790 Memorial Drive | 99,658 | — | — | 99,658 | 2 | 9,168 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 167 Sidney Street and 99 Erie Street | 54,549 | — | — | 54,549 | 2 | 4,028 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

79/96 13th Street (Charlestown Navy Yard) |

25,309 | — | — | 25,309 | 1 | 797 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Cambridge/Inner Suburbs |

6,127,970 | 1,030,927 | 504,000 | 7,662,897 | 53 | 479,520 | 97.8 | 90.4 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fenway | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: Alexandria Center® for Life Science – Fenway |

927,499 | 510,116 | — | 1,437,615 | 2 | 59,172 | 90.4 | 90.4 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

401 Park Drive and 201 Brookline Avenue(2) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Seaport Innovation District | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

5 and 15(2) Necco Street |

95,400 | 345,995 | — | 441,395 | 2 | 6,331 | 86.6 | 86.6 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mega Campus: 380 and 420 E Street | 195,506 | — | — | 195,506 | 2 | 4,472 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Seaport Innovation District | 290,906 | 345,995 | — | 636,901 | 4 | 10,803 | 95.6 | 95.6 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Route 128 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mega Campus: One Upland Road, 100 Tech Drive, and One Investors Way | 706,988 | — | — | 706,988 | 4 | 29,059 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 19, 225, and 235 Presidential Way | 585,022 | — | — | 585,022 | 3 | 13,508 | 99.9 | 99.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reservoir Woods | 312,845 | — | 202,428 | 515,273 | 3 | 15,469 | 100.0 | 60.7 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 40, 50, and 60 Sylvan Road | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

275 Grove Street |

509,702 | — | — | 509,702 | 3 | 17,253 | 75.6 | 75.6 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

225, 266, and 275 Second Avenue |

329,005 | — | — | 329,005 | 3 | 18,461 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 840 Winter Street | 28,230 | — | 139,984 | 168,214 | 1 | 1,239 | 100.0 | 16.8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

100 Beaver Street |

82,330 | — | — | 82,330 | 1 | 5,110 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Route 128 | 2,554,122 | — | 342,412 | 2,896,534 | 18 | 100,099 | 95.1 | 83.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | 753,923 | — | 453,869 | 1,207,792 | 8 | 11,795 | 77.5 | 48.3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Greater Boston |

10,654,420 | 1,887,038 | 1,300,281 | 13,841,739 | 85 | $ | 661,389 | 95.0 | % | 84.7 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

(1)Refer to “New Class A development and redevelopment properties: summary of pipeline” and to “Mega campus” in the “Definitions and reconciliations” of this Supplemental Information for additional details.

(2)We own a partial interest in this property through a real estate joint venture. Refer to “Joint venture financial information” of this Supplemental Information for additional details.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Property Listing (continued) | |

||||

June 30, 2022 | |||||

| (Dollars in thousands) | |||||

Market / Submarket / Address |

RSF |

Number of Properties | Annual Rental Revenue | Occupancy Percentage |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating | Operating and Redevelopment | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating | Development | Redevelopment | Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| San Francisco Bay Area | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mission Bay | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Mega Campus: Alexandria Center® for Science and Technology –

Mission Bay(1)

|

2,015,177 | — | — | 2,015,177 | 9 | $ | 96,014 | 99.9 | % | 99.9 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

1455(2), 1515(2), 1655, and 1725 Third Street, 409 and 499 Illinois Street, 1500 and 1700 Owens Street, and 455 Mission Bay Boulevard South |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mission Bay | 2,015,177 | — | — | 2,015,177 | 9 | 96,014 | 99.9 | 99.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South San Francisco | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: Alexandria Technology Center® – Gateway(1) |

1,114,890 | 230,592 | 300,010 | 1,645,492 | 12 | 53,869 | 85.0 | 67.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

600(2), 601, 611, 630(2), 650(2), 651, 681, 685, 701, 751, 901(2), and 951(2)

Gateway Boulevard

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: 213(1), 249, 259, 269, and 279 East Grand Avenue |

919,704 | — | — | 919,704 | 5 | 48,951 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mega Campus: 1122 and 1150 El Camino Real | 725,172 | — | — | 725,172 | 2 | 13,081 | 97.6 | 97.6 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Alexandria Center® for Life Science – South San Francisco |

504,551 | — | — | 504,551 | 3 | 36,750 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 201 Haskins Way and 400 and 450 East Jamie Court | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

500 Forbes Boulevard(1) |

155,685 | — | — | 155,685 | 1 | 10,680 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

7000 Shoreline Court |

139,709 | — | — | 139,709 | 1 | 8,657 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

341 and 343 Oyster Point Boulevard |

108,208 | — | — | 108,208 | 2 | 6,788 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

849/863 Mitten Road/866 Malcolm Road |

103,857 | — | — | 103,857 | 1 | 4,829 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South San Francisco | 3,771,776 | 230,592 | 300,010 | 4,302,378 | 27 | 183,605 | 95.1 | 88.1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Greater Stanford | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Mega Campus: Alexandria Center® for Life Science – San Carlos |

739,192 | — | — | 739,192 | 9 | 49,745 | 95.3 | 95.3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 825, 835, 960, and 1501-1599 Industrial Road | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Alexandria Stanford Life Science District |

703,742 | — | — | 703,742 | 9 | 63,683 | 98.9 | 98.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3160, 3165, 3170, and 3181 Porter Drive and 3301, 3303, 3305, 3307, and 3330 Hillview Avenue | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

3825 and 3875 Fabian Way |

478,000 | — | — | 478,000 | 2 | 21,802 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3412, 3420, 3440, 3450, and 3460 Hillview Avenue | 338,751 | — | — | 338,751 | 5 | 21,133 | 73.8 | 73.8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2100, 2200, 2300, and 2400 Geng Road | 194,648 | — | — | 194,648 | 4 | 9,302 | 79.2 | 79.2 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2475 and 2625/2627/2631 Hanover Street and 1450 Page Mill Road | 194,503 | — | — | 194,503 | 3 | 18,012 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2425 Garcia Avenue/2400/2450 Bayshore Parkway |

99,208 | — | — | 99,208 | 1 | 4,257 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Shoreway Science Center |

82,462 | — | — | 82,462 | 2 | 5,322 | 100.0 | 100.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

75 and 125 Shoreway Road |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

3350 West Bayshore Road |