| Illinois | 001-35077 | 36-3873352 | ||||||||||||||||||

| (State or other jurisdiction of Incorporation) | (Commission File Number) | (I.R.S. Employer Identification No.) |

||||||||||||||||||

9700 W. Higgins Road, Suite 800 |

Rosemont | Illinois | 60018 | |||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

| ☐ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) | ||||

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) | ||||

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) | ||||

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) | ||||

| Title of Each Class | Ticker Symbol | Name of Each Exchange on Which Registered | ||||||

| Common Stock, no par value | WTFC | The Nasdaq Global Select Market | ||||||

Depositary Shares, Each Representing a 1/1,000th Interest in a Share of |

WTFCN | The Nasdaq Global Select Market | ||||||

| 7.875% Fixed-Rate Reset Non-Cumulative Perpetual Preferred Stock, Series F, no par value | ||||||||

| Exhibit | |||||

| WINTRUST FINANCIAL CORPORATION (Registrant) |

||||||||

| By: | /s/ David L. Stoehr | |||||||

| David L. Stoehr Executive Vice President and Chief Financial Officer |

||||||||

| Exhibit | |||||

| FOR IMMEDIATE RELEASE | October 20, 2025 | |||||||

*On May 22, 2025, the Company completed the issuance of $425 million of Series F Preferred Stock. The issuance was in contemplation of redeeming $412.5 million of Series D and Series E Preferred Stock that was expected to reprice at rates higher than existing market rates. The Series D and Series E Preferred Stock were redeemed on July 15, 2025.

*On May 22, 2025, the Company completed the issuance of $425 million of Series F Preferred Stock. The issuance was in contemplation of redeeming $412.5 million of Series D and Series E Preferred Stock that was expected to reprice at rates higher than existing market rates. The Series D and Series E Preferred Stock were redeemed on July 15, 2025.

|

% or (1)

basis point (bp) change from

2nd Quarter

2025

|

% or basis point (bp) change from 3rd Quarter 2024 |

||||||||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||||||||

| (Dollars in thousands, except per share data) | Sep 30, 2025 | Jun 30, 2025 | Sep 30, 2024 | ||||||||||||||||||||||||||||||||

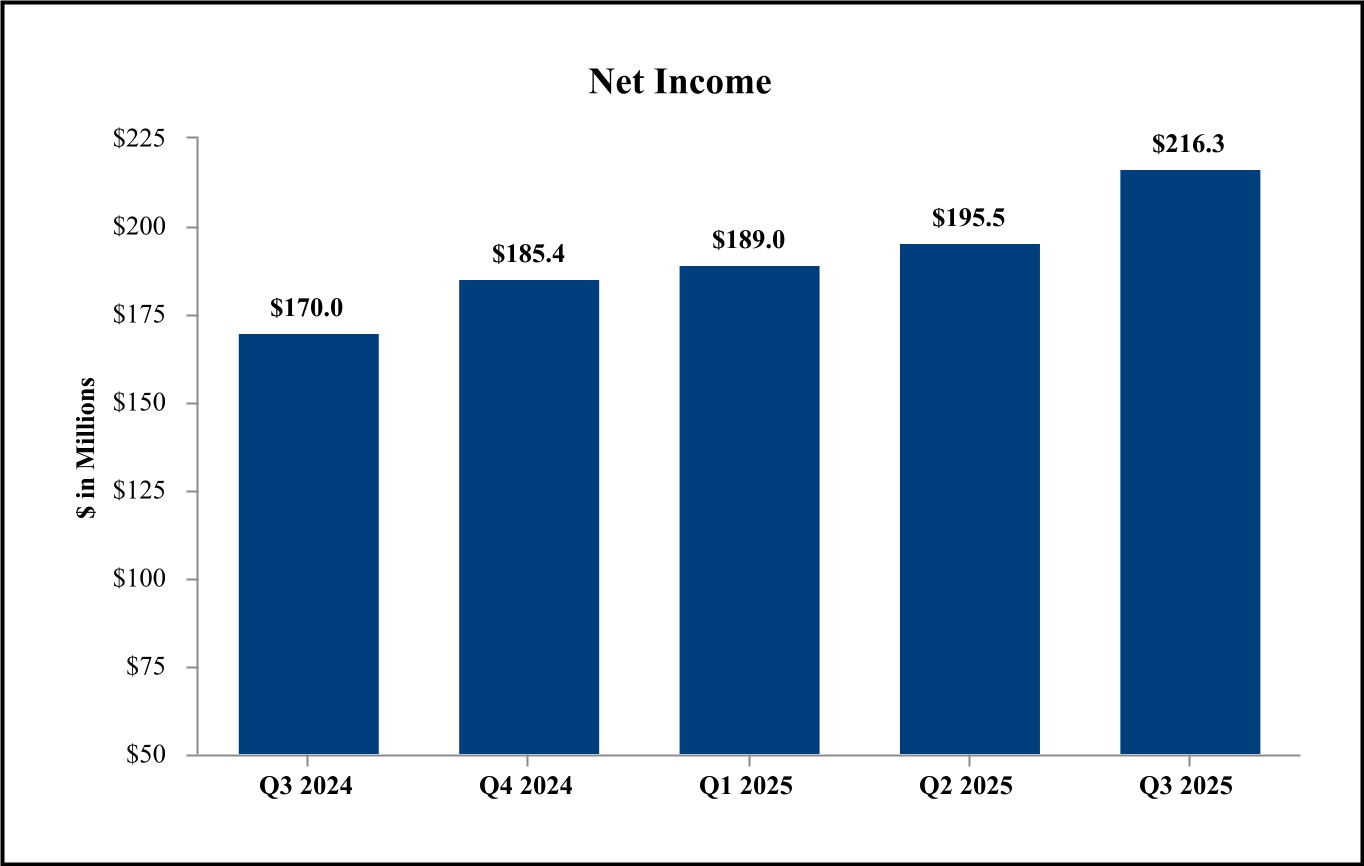

| Net income | $ | 216,254 | $ | 195,527 | $ | 170,001 | 11 | % | 27 | % | |||||||||||||||||||||||||

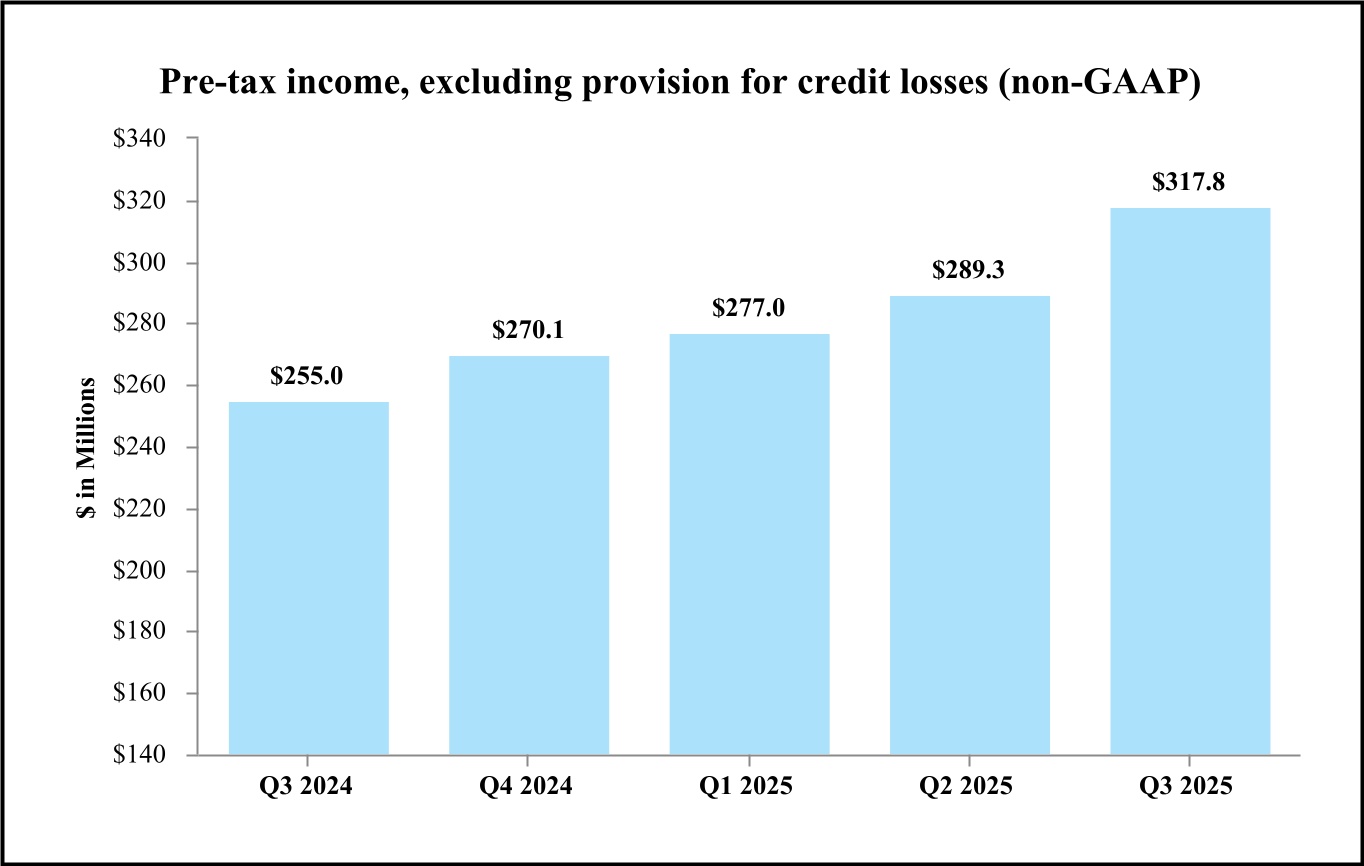

Pre-tax income, excluding provision for credit losses (non-GAAP) (2) |

317,809 | 289,322 | 255,043 | 10 | 25 | ||||||||||||||||||||||||||||||

| Net income per common share – Diluted | 2.78 | 2.78 | 2.47 | — | 13 | ||||||||||||||||||||||||||||||

| Cash dividends declared per common share | 0.50 | 0.50 | 0.45 | — | 11 | ||||||||||||||||||||||||||||||

Net revenue (3) |

697,837 | 670,783 | 615,730 | 4 | 13 | ||||||||||||||||||||||||||||||

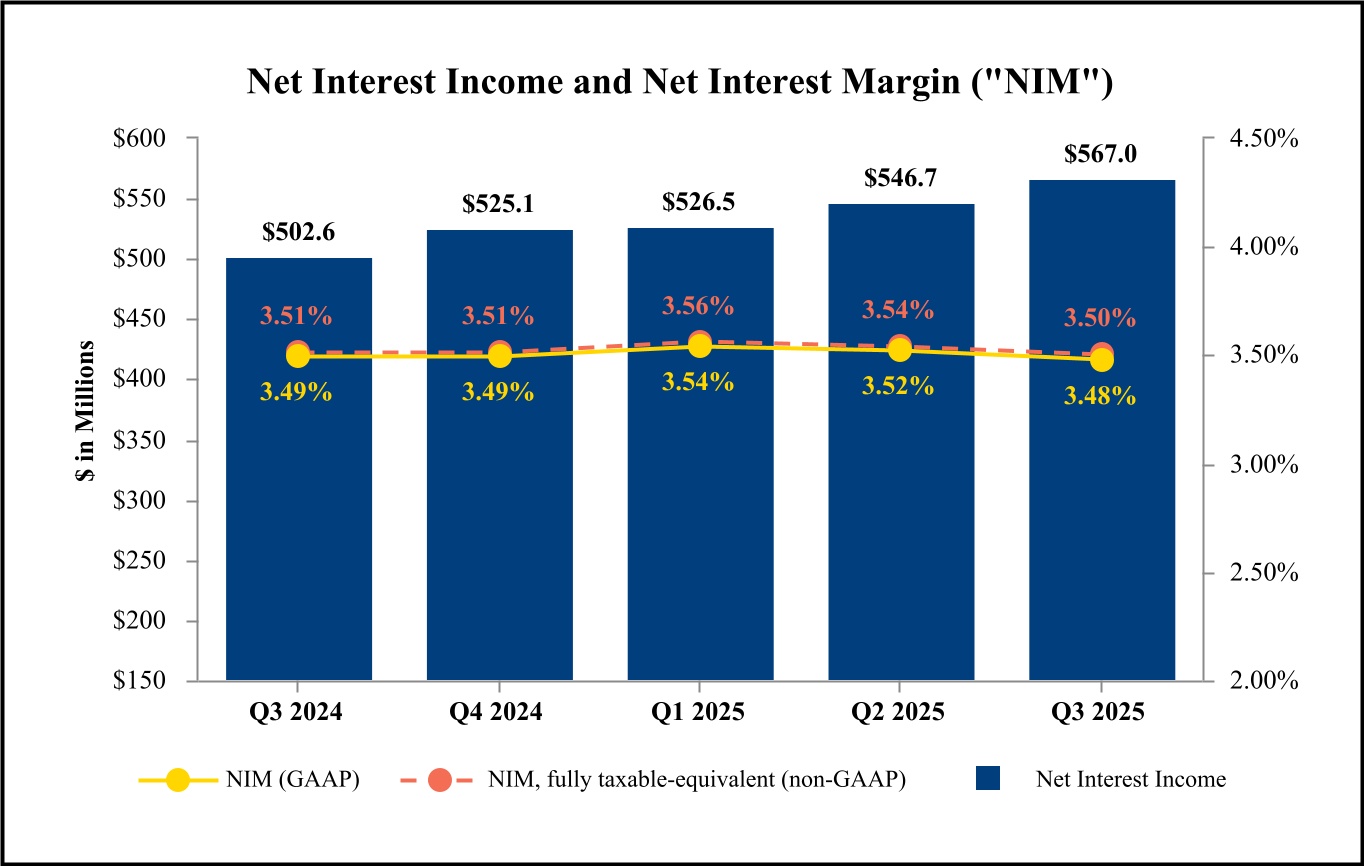

| Net interest income | 567,010 | 546,694 | 502,583 | 4 | 13 | ||||||||||||||||||||||||||||||

| Net interest margin | 3.48 | % | 3.52 | % | 3.49 | % | (4) | bps | (1) | bps | |||||||||||||||||||||||||

Net interest margin – fully taxable-equivalent (non-GAAP) (2) |

3.50 | 3.54 | 3.51 | (4) | (1) | ||||||||||||||||||||||||||||||

Net overhead ratio (4) |

1.45 | 1.57 | 1.62 | (12) | (17) | ||||||||||||||||||||||||||||||

| Return on average assets | 1.26 | 1.19 | 1.11 | 7 | 15 | ||||||||||||||||||||||||||||||

| Return on average common equity | 11.58 | 12.07 | 11.63 | (49) | (5) | ||||||||||||||||||||||||||||||

Return on average tangible common equity (non-GAAP) (2) |

13.74 | 14.44 | 13.92 | (70) | (18) | ||||||||||||||||||||||||||||||

| At end of period | |||||||||||||||||||||||||||||||||||

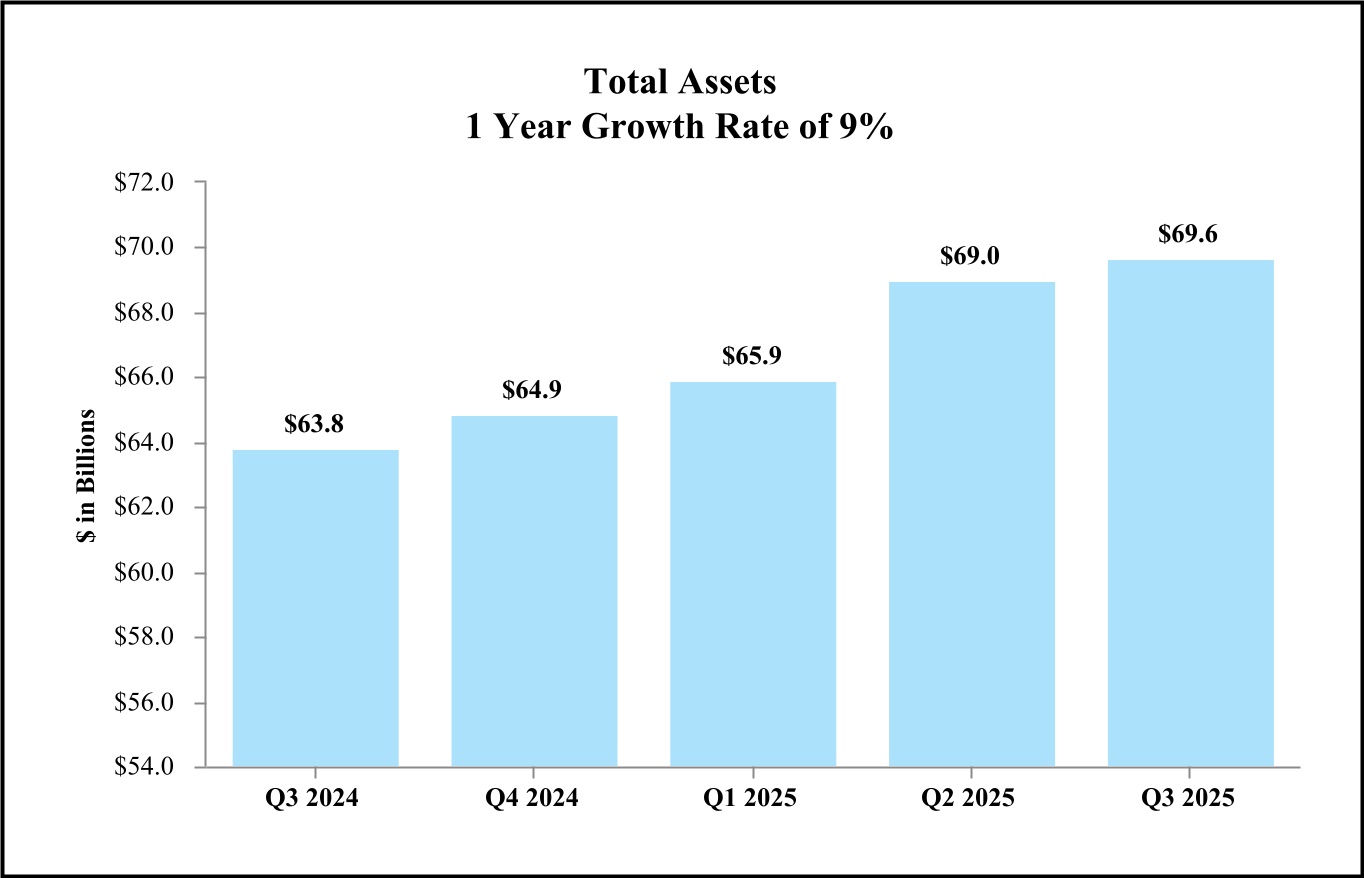

| Total assets | $ | 69,629,638 | $ | 68,983,318 | $ | 63,788,424 | 4 | % | 9 | % | |||||||||||||||||||||||||

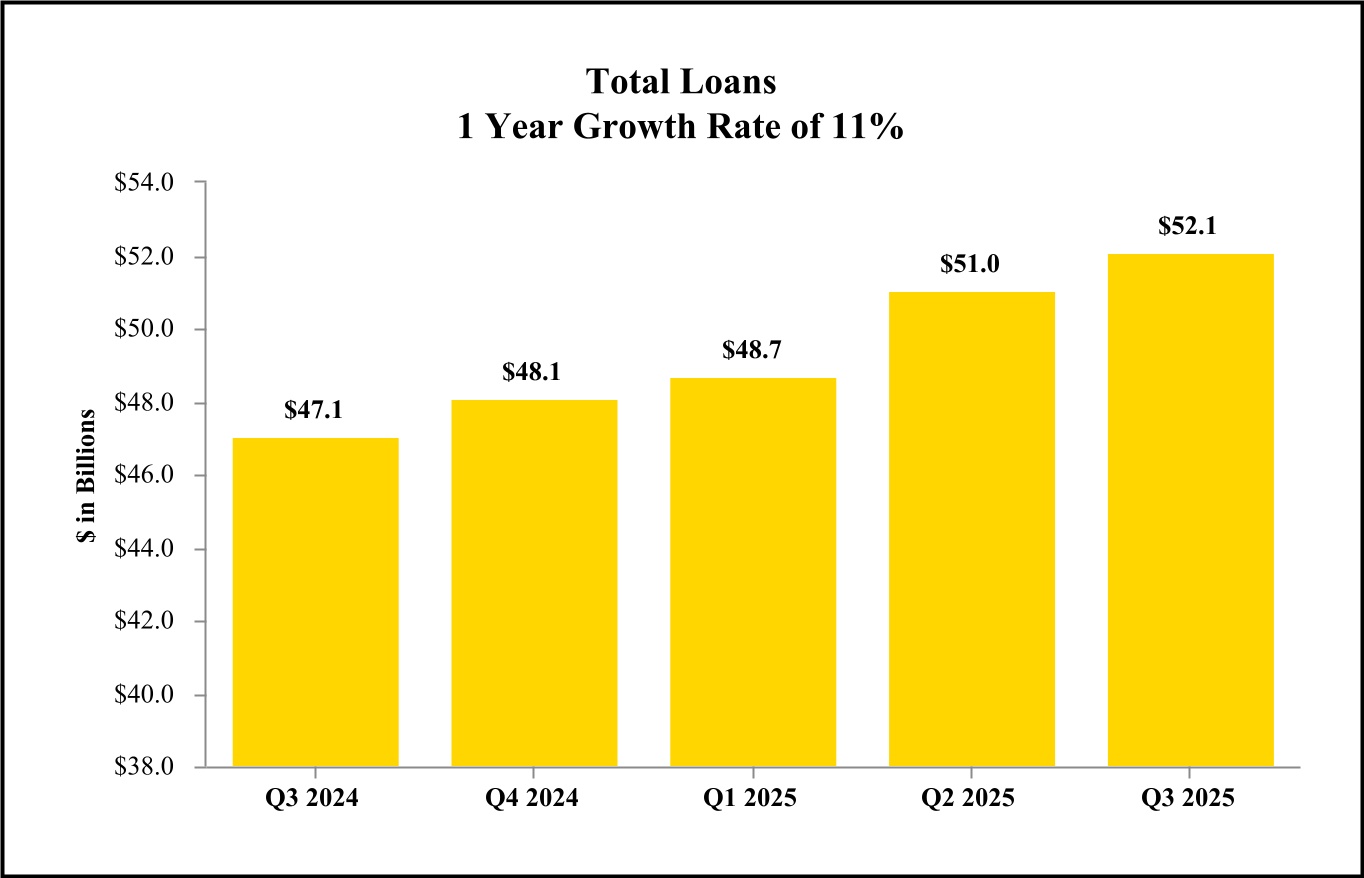

Total loans (5) |

52,063,482 | 51,041,679 | 47,067,447 | 8 | 11 | ||||||||||||||||||||||||||||||

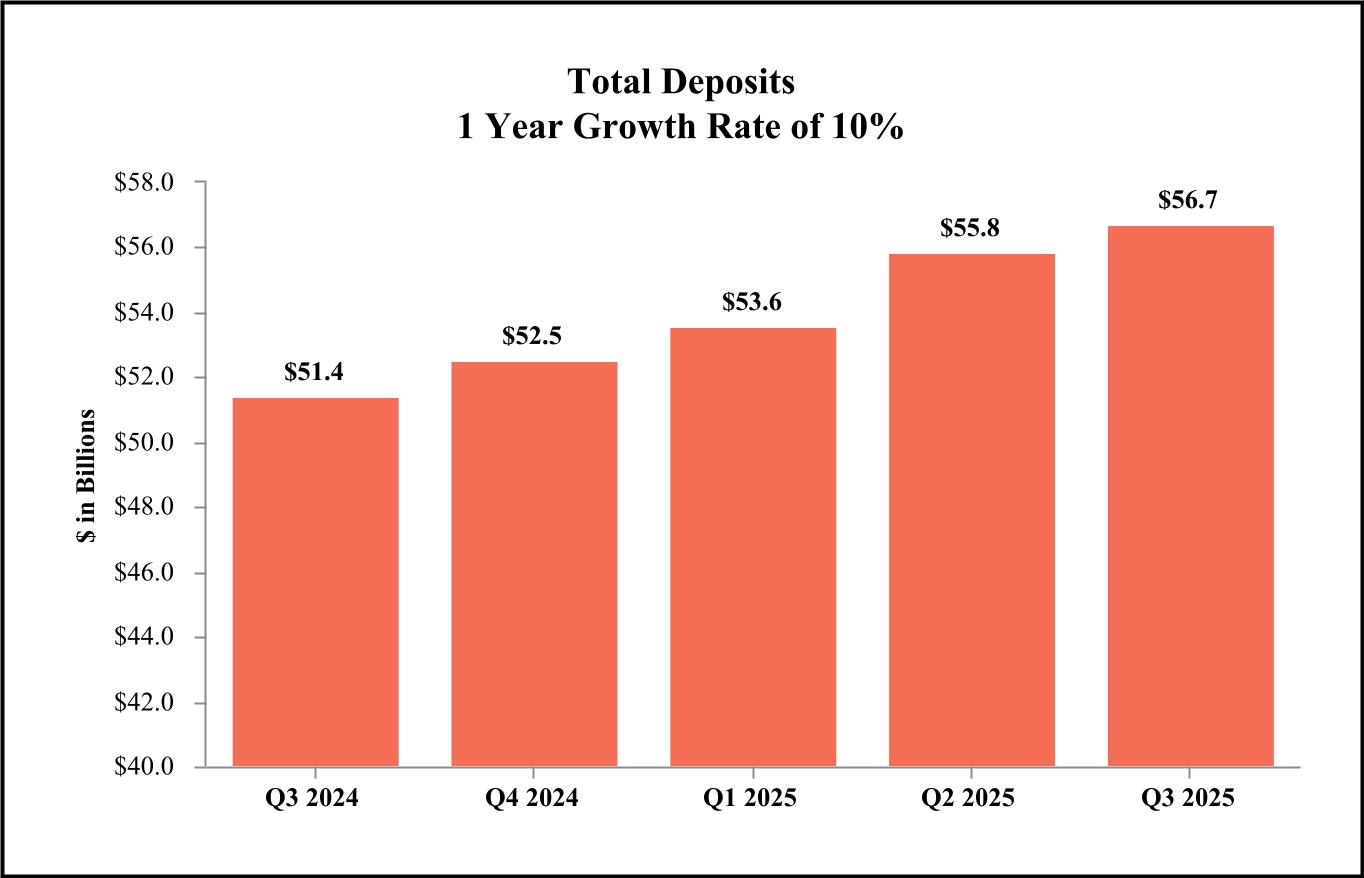

| Total deposits | 56,711,381 | 55,816,811 | 51,404,966 | 6 | 10 | ||||||||||||||||||||||||||||||

| Total shareholders’ equity | 7,045,757 | 7,225,696 | 6,399,714 | (10) | 10 | ||||||||||||||||||||||||||||||

| Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands, except per share data) | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | Sep 30, 2025 | Sep 30, 2024 | ||||||||||||||||||||||||||||||||||

| Selected Financial Condition Data (at end of period): | |||||||||||||||||||||||||||||||||||||||||

| Total assets | $ | 69,629,638 | $ | 68,983,318 | $ | 65,870,066 | $ | 64,879,668 | $ | 63,788,424 | |||||||||||||||||||||||||||||||

Total loans (1) |

52,063,482 | 51,041,679 | 48,708,390 | 48,055,037 | 47,067,447 | ||||||||||||||||||||||||||||||||||||

| Total deposits | 56,711,381 | 55,816,811 | 53,570,038 | 52,512,349 | 51,404,966 | ||||||||||||||||||||||||||||||||||||

| Total shareholders’ equity | 7,045,757 | 7,225,696 | 6,600,537 | 6,344,297 | 6,399,714 | ||||||||||||||||||||||||||||||||||||

| Selected Statements of Income Data: | |||||||||||||||||||||||||||||||||||||||||

| Net interest income | $ | 567,010 | $ | 546,694 | $ | 526,474 | $ | 525,148 | $ | 502,583 | $ | 1,640,178 | $ | 1,437,387 | |||||||||||||||||||||||||||

Net revenue (2) |

697,837 | 670,783 | 643,108 | 638,599 | 615,730 | 2,011,728 | 1,812,261 | ||||||||||||||||||||||||||||||||||

| Net income | 216,254 | 195,527 | 189,039 | 185,362 | 170,001 | 600,820 | 509,683 | ||||||||||||||||||||||||||||||||||

Pre-tax income, excluding provision for credit losses (non-GAAP) (3) |

317,809 | 289,322 | 277,018 | 270,060 | 255,043 | 884,149 | 778,076 | ||||||||||||||||||||||||||||||||||

| Net income per common share – Basic | 2.82 | 2.82 | 2.73 | 2.68 | 2.51 | 8.37 | 7.79 | ||||||||||||||||||||||||||||||||||

| Net income per common share – Diluted | 2.78 | 2.78 | 2.69 | 2.63 | 2.47 | 8.25 | 7.67 | ||||||||||||||||||||||||||||||||||

| Cash dividends declared per common share | 0.50 | 0.50 | 0.50 | 0.45 | 0.45 | 1.50 | 1.35 | ||||||||||||||||||||||||||||||||||

| Selected Financial Ratios and Other Data: | |||||||||||||||||||||||||||||||||||||||||

| Performance Ratios: | |||||||||||||||||||||||||||||||||||||||||

| Net interest margin | 3.48 | % | 3.52 | % | 3.54 | % | 3.49 | % | 3.49 | % | 3.51 | % | 3.52 | % | |||||||||||||||||||||||||||

Net interest margin – fully taxable-equivalent (non-GAAP) (3) |

3.50 | 3.54 | 3.56 | 3.51 | 3.51 | 3.53 | 3.54 | ||||||||||||||||||||||||||||||||||

| Non-interest income to average assets | 0.76 | 0.76 | 0.74 | 0.71 | 0.74 | 0.75 | 0.86 | ||||||||||||||||||||||||||||||||||

| Non-interest expense to average assets | 2.21 | 2.32 | 2.32 | 2.31 | 2.36 | 2.28 | 2.38 | ||||||||||||||||||||||||||||||||||

Net overhead ratio (4) |

1.45 | 1.57 | 1.58 | 1.60 | 1.62 | 1.53 | 1.52 | ||||||||||||||||||||||||||||||||||

| Return on average assets | 1.26 | 1.19 | 1.20 | 1.16 | 1.11 | 1.22 | 1.17 | ||||||||||||||||||||||||||||||||||

| Return on average common equity | 11.58 | 12.07 | 12.21 | 11.82 | 11.63 | 11.94 | 12.52 | ||||||||||||||||||||||||||||||||||

Return on average tangible common equity (non-GAAP) (3) |

13.74 | 14.44 | 14.72 | 14.29 | 13.92 | 14.28 | 14.69 | ||||||||||||||||||||||||||||||||||

| Average total assets | $ | 68,303,036 | $ | 65,840,345 | $ | 64,107,042 | $ | 63,594,105 | $ | 60,915,283 | $ | 66,098,845 | $ | 58,014,347 | |||||||||||||||||||||||||||

| Average total shareholders’ equity | 6,955,543 | 6,862,040 | 6,460,941 | 6,418,403 | 5,990,429 | 6,761,319 | 5,628,346 | ||||||||||||||||||||||||||||||||||

| Average loans to average deposits ratio | 92.5 | % | 93.0 | % | 92.3 | % | 91.9 | % | 93.8 | % | 92.6 | % | 94.5 | % | |||||||||||||||||||||||||||

| Period-end loans to deposits ratio | 91.8 | 91.4 | 90.9 | 91.5 | 91.6 | ||||||||||||||||||||||||||||||||||||

| Common Share Data at end of period: | |||||||||||||||||||||||||||||||||||||||||

| Market price per common share | $ | 132.44 | $ | 123.98 | $ | 112.46 | $ | 124.71 | $ | 108.53 | |||||||||||||||||||||||||||||||

| Book value per common share | 98.87 | 95.43 | 92.47 | 89.21 | 90.06 | ||||||||||||||||||||||||||||||||||||

Tangible book value per common share (non-GAAP) (3) |

85.39 | 81.86 | 78.83 | 75.39 | 76.15 | ||||||||||||||||||||||||||||||||||||

| Common shares outstanding | 66,961,209 | 66,937,732 | 66,919,325 | 66,495,227 | 66,481,543 | ||||||||||||||||||||||||||||||||||||

| Other Data at end of period: | |||||||||||||||||||||||||||||||||||||||||

| Common equity to assets ratio | 9.5 | % | 9.3 | % | 9.4 | % | 9.1 | % | 9.4 | % | |||||||||||||||||||||||||||||||

Tangible common equity ratio (non-GAAP) (3) |

8.3 | 8.0 | 8.1 | 7.8 | 8.1 | ||||||||||||||||||||||||||||||||||||

Tier 1 leverage ratio (5) |

9.5 | 10.2 | 9.6 | 9.4 | 9.6 | ||||||||||||||||||||||||||||||||||||

| Risk-based capital ratios: | |||||||||||||||||||||||||||||||||||||||||

Tier 1 capital ratio (5) |

10.9 | 11.5 | 10.8 | 10.7 | 10.6 | ||||||||||||||||||||||||||||||||||||

Common equity tier 1 capital ratio (5) |

10.2 | 10.0 | 10.1 | 9.9 | 9.8 | ||||||||||||||||||||||||||||||||||||

Total capital ratio (5) |

12.4 | 13.0 | 12.5 | 12.3 | 12.2 | ||||||||||||||||||||||||||||||||||||

Allowance for credit losses (6) |

$ | 454,586 | $ | 457,461 | $ | 448,387 | $ | 437,060 | $ | 436,193 | |||||||||||||||||||||||||||||||

| Allowance for loan and unfunded lending-related commitment losses to total loans | 0.87 | % | 0.90 | % | 0.92 | % | 0.91 | % | 0.93 | % | |||||||||||||||||||||||||||||||

| Number of: | |||||||||||||||||||||||||||||||||||||||||

| Bank subsidiaries | 16 | 16 | 16 | 16 | 16 | ||||||||||||||||||||||||||||||||||||

| Banking offices | 208 | 208 | 208 | 205 | 203 | ||||||||||||||||||||||||||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | |||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | ||||||||||||||||||||||||||||

| (In thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | |||||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||

| Cash and due from banks | $ | 565,406 | $ | 695,501 | $ | 616,216 | $ | 452,017 | $ | 725,465 | ||||||||||||||||||||||

| Federal funds sold and securities purchased under resale agreements | 63 | 63 | 63 | 6,519 | 5,663 | |||||||||||||||||||||||||||

| Interest-bearing deposits with banks | 3,422,452 | 4,569,618 | 4,238,237 | 4,409,753 | 3,648,117 | |||||||||||||||||||||||||||

| Available-for-sale securities, at fair value | 5,274,124 | 4,885,715 | 4,220,305 | 4,141,482 | 3,912,232 | |||||||||||||||||||||||||||

| Held-to-maturity securities, at amortized cost | 3,438,406 | 3,502,186 | 3,564,490 | 3,613,263 | 3,677,420 | |||||||||||||||||||||||||||

| Trading account securities | — | — | — | 4,072 | 3,472 | |||||||||||||||||||||||||||

| Equity securities with readily determinable fair value | 63,445 | 273,722 | 270,442 | 215,412 | 125,310 | |||||||||||||||||||||||||||

| Federal Home Loan Bank and Federal Reserve Bank stock | 282,755 | 282,087 | 281,893 | 281,407 | 266,908 | |||||||||||||||||||||||||||

| Brokerage customer receivables | — | — | — | 18,102 | 16,662 | |||||||||||||||||||||||||||

| Mortgage loans held-for-sale, at fair value | 333,883 | 299,606 | 316,804 | 331,261 | 461,067 | |||||||||||||||||||||||||||

| Loans, net of unearned income | 52,063,482 | 51,041,679 | 48,708,390 | 48,055,037 | 47,067,447 | |||||||||||||||||||||||||||

| Allowance for loan losses | (386,622) | (391,654) | (378,207) | (364,017) | (360,279) | |||||||||||||||||||||||||||

| Net loans | 51,676,860 | 50,650,025 | 48,330,183 | 47,691,020 | 46,707,168 | |||||||||||||||||||||||||||

| Premises, software and equipment, net | 775,425 | 776,324 | 776,679 | 779,130 | 772,002 | |||||||||||||||||||||||||||

| Lease investments, net | 301,000 | 289,768 | 280,472 | 278,264 | 270,171 | |||||||||||||||||||||||||||

| Accrued interest receivable and other assets | 1,614,674 | 1,610,025 | 1,598,255 | 1,739,334 | 1,721,090 | |||||||||||||||||||||||||||

| Receivable on unsettled securities sales | 978,209 | 240,039 | 463,023 | — | 551,031 | |||||||||||||||||||||||||||

| Goodwill | 797,639 | 798,144 | 796,932 | 796,942 | 800,780 | |||||||||||||||||||||||||||

| Other acquisition-related intangible assets | 105,297 | 110,495 | 116,072 | 121,690 | 123,866 | |||||||||||||||||||||||||||

| Total assets | $ | 69,629,638 | $ | 68,983,318 | $ | 65,870,066 | $ | 64,879,668 | $ | 63,788,424 | ||||||||||||||||||||||

| Liabilities and Shareholders’ Equity | ||||||||||||||||||||||||||||||||

| Deposits: | ||||||||||||||||||||||||||||||||

| Non-interest-bearing | $ | 10,952,146 | $ | 10,877,166 | $ | 11,201,859 | $ | 11,410,018 | $ | 10,739,132 | ||||||||||||||||||||||

| Interest-bearing | 45,759,235 | 44,939,645 | 42,368,179 | 41,102,331 | 40,665,834 | |||||||||||||||||||||||||||

| Total deposits | 56,711,381 | 55,816,811 | 53,570,038 | 52,512,349 | 51,404,966 | |||||||||||||||||||||||||||

| Federal Home Loan Bank advances | 3,151,309 | 3,151,309 | 3,151,309 | 3,151,309 | 3,171,309 | |||||||||||||||||||||||||||

| Other borrowings | 579,328 | 625,392 | 529,269 | 534,803 | 647,043 | |||||||||||||||||||||||||||

| Subordinated notes | 298,536 | 298,458 | 298,360 | 298,283 | 298,188 | |||||||||||||||||||||||||||

| Junior subordinated debentures | 253,566 | 253,566 | 253,566 | 253,566 | 253,566 | |||||||||||||||||||||||||||

| Payable on unsettled securities sales | — | 39,105 | — | — | — | |||||||||||||||||||||||||||

| Accrued interest payable and other liabilities | 1,589,761 | 1,572,981 | 1,466,987 | 1,785,061 | 1,613,638 | |||||||||||||||||||||||||||

| Total liabilities | 62,583,881 | 61,757,622 | 59,269,529 | 58,535,371 | 57,388,710 | |||||||||||||||||||||||||||

| Shareholders’ Equity: | ||||||||||||||||||||||||||||||||

| Preferred stock | 425,000 | 837,500 | 412,500 | 412,500 | 412,500 | |||||||||||||||||||||||||||

| Common stock | 67,042 | 67,025 | 67,007 | 66,560 | 66,546 | |||||||||||||||||||||||||||

| Surplus | 2,521,306 | 2,495,637 | 2,494,347 | 2,482,561 | 2,470,228 | |||||||||||||||||||||||||||

| Treasury stock | (9,150) | (9,156) | (9,156) | (6,153) | (6,098) | |||||||||||||||||||||||||||

| Retained earnings | 4,356,367 | 4,200,923 | 4,045,854 | 3,897,164 | 3,748,715 | |||||||||||||||||||||||||||

| Accumulated other comprehensive loss | (314,808) | (366,233) | (410,015) | (508,335) | (292,177) | |||||||||||||||||||||||||||

| Total shareholders’ equity | 7,045,757 | 7,225,696 | 6,600,537 | 6,344,297 | 6,399,714 | |||||||||||||||||||||||||||

| Total liabilities and shareholders’ equity | $ | 69,629,638 | $ | 68,983,318 | $ | 65,870,066 | $ | 64,879,668 | $ | 63,788,424 | ||||||||||||||||||||||

| Three Months Ended | Nine Months Ended | |||||||||||||||||||||||||||||||||||||

| (Dollars in thousands, except per share data) | Sep 30, 2025 |

Jun 30, 2025 |

Mar 31, 2025 |

Dec 31, 2024 |

Sep 30, 2024 |

Sep 30, 2025 | Sep 30, 2024 | |||||||||||||||||||||||||||||||

| Interest income | ||||||||||||||||||||||||||||||||||||||

| Interest and fees on loans | $ | 832,140 | $ | 797,997 | $ | 768,362 | $ | 789,038 | $ | 794,163 | $ | 2,398,499 | $ | 2,254,316 | ||||||||||||||||||||||||

| Mortgage loans held-for-sale | 4,757 | 4,872 | 4,246 | 5,623 | 6,233 | 13,875 | 15,813 | |||||||||||||||||||||||||||||||

| Interest-bearing deposits with banks | 34,992 | 34,317 | 36,766 | 46,256 | 32,608 | 106,075 | 68,997 | |||||||||||||||||||||||||||||||

| Federal funds sold and securities purchased under resale agreements | 75 | 276 | 179 | 53 | 277 | 530 | 313 | |||||||||||||||||||||||||||||||

| Investment securities | 86,426 | 78,053 | 72,016 | 67,066 | 69,592 | 236,495 | 209,049 | |||||||||||||||||||||||||||||||

| Trading account securities | — | — | 11 | 6 | 11 | 11 | 42 | |||||||||||||||||||||||||||||||

| Federal Home Loan Bank and Federal Reserve Bank stock | 5,444 | 5,393 | 5,307 | 5,157 | 5,451 | 16,144 | 14,903 | |||||||||||||||||||||||||||||||

| Brokerage customer receivables | — | — | 78 | 302 | 269 | 78 | 663 | |||||||||||||||||||||||||||||||

| Total interest income | 963,834 | 920,908 | 886,965 | 913,501 | 908,604 | 2,771,707 | 2,564,096 | |||||||||||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||||||||||||||

| Interest on deposits | 355,846 | 333,470 | 320,233 | 346,388 | 362,019 | 1,009,549 | 997,254 | |||||||||||||||||||||||||||||||

| Interest on Federal Home Loan Bank advances | 26,007 | 25,724 | 25,441 | 26,050 | 26,254 | 77,172 | 73,099 | |||||||||||||||||||||||||||||||

| Interest on other borrowings | 6,887 | 6,957 | 6,792 | 7,519 | 9,013 | 20,636 | 26,961 | |||||||||||||||||||||||||||||||

| Interest on subordinated notes | 3,717 | 3,735 | 3,714 | 3,733 | 3,712 | 11,166 | 14,384 | |||||||||||||||||||||||||||||||

| Interest on junior subordinated debentures | 4,367 | 4,328 | 4,311 | 4,663 | 5,023 | 13,006 | 15,011 | |||||||||||||||||||||||||||||||

| Total interest expense | 396,824 | 374,214 | 360,491 | 388,353 | 406,021 | 1,131,529 | 1,126,709 | |||||||||||||||||||||||||||||||

| Net interest income | 567,010 | 546,694 | 526,474 | 525,148 | 502,583 | 1,640,178 | 1,437,387 | |||||||||||||||||||||||||||||||

| Provision for credit losses | 21,768 | 22,234 | 23,963 | 16,979 | 22,334 | 67,965 | 84,068 | |||||||||||||||||||||||||||||||

| Net interest income after provision for credit losses | 545,242 | 524,460 | 502,511 | 508,169 | 480,249 | 1,572,213 | 1,353,319 | |||||||||||||||||||||||||||||||

| Non-interest income | ||||||||||||||||||||||||||||||||||||||

| Wealth management | 37,188 | 36,821 | 34,042 | 38,775 | 37,224 | 108,051 | 107,452 | |||||||||||||||||||||||||||||||

| Mortgage banking | 24,451 | 23,170 | 20,529 | 20,452 | 15,974 | 68,150 | 72,761 | |||||||||||||||||||||||||||||||

| Service charges on deposit accounts | 19,825 | 19,502 | 19,362 | 18,864 | 16,430 | 58,689 | 46,787 | |||||||||||||||||||||||||||||||

| Gains (losses) on investment securities, net | 2,972 | 650 | 3,196 | (2,835) | 3,189 | 6,818 | 233 | |||||||||||||||||||||||||||||||

| Fees from covered call options | 5,619 | 5,624 | 3,446 | 2,305 | 988 | 14,689 | 7,891 | |||||||||||||||||||||||||||||||

| Trading gains (losses), net | 172 | 151 | (64) | (113) | (130) | 259 | 617 | |||||||||||||||||||||||||||||||

| Operating lease income, net | 15,466 | 15,166 | 15,287 | 15,327 | 15,335 | 45,919 | 43,383 | |||||||||||||||||||||||||||||||

| Other | 25,134 | 23,005 | 20,836 | 20,676 | 24,137 | 68,975 | 95,750 | |||||||||||||||||||||||||||||||

| Total non-interest income | 130,827 | 124,089 | 116,634 | 113,451 | 113,147 | 371,550 | 374,874 | |||||||||||||||||||||||||||||||

| Non-interest expense | ||||||||||||||||||||||||||||||||||||||

| Salaries and employee benefits | 219,668 | 219,541 | 211,526 | 212,133 | 211,261 | 650,735 | 604,975 | |||||||||||||||||||||||||||||||

| Software and equipment | 35,027 | 36,522 | 34,717 | 34,258 | 31,574 | 106,266 | 88,536 | |||||||||||||||||||||||||||||||

| Operating lease equipment | 10,409 | 10,757 | 10,471 | 10,263 | 10,518 | 31,637 | 32,035 | |||||||||||||||||||||||||||||||

| Occupancy, net | 20,809 | 20,228 | 20,778 | 20,597 | 19,945 | 61,815 | 58,616 | |||||||||||||||||||||||||||||||

| Data processing | 11,329 | 12,110 | 11,274 | 10,957 | 9,984 | 34,713 | 28,779 | |||||||||||||||||||||||||||||||

| Advertising and marketing | 19,027 | 18,761 | 12,272 | 13,097 | 18,239 | 50,060 | 48,715 | |||||||||||||||||||||||||||||||

| Professional fees | 7,465 | 9,243 | 9,044 | 11,334 | 9,783 | 25,752 | 29,303 | |||||||||||||||||||||||||||||||

| Amortization of other acquisition-related intangible assets | 5,196 | 5,580 | 5,618 | 5,773 | 4,042 | 16,394 | 6,322 | |||||||||||||||||||||||||||||||

| FDIC insurance | 11,418 | 10,971 | 10,926 | 10,640 | 10,512 | 33,315 | 35,478 | |||||||||||||||||||||||||||||||

| Other real estate owned (“OREO”) expenses, net | 262 | 505 | 643 | 397 | (938) | 1,410 | (805) | |||||||||||||||||||||||||||||||

| Other | 39,418 | 37,243 | 38,821 | 39,090 | 35,767 | 115,482 | 102,231 | |||||||||||||||||||||||||||||||

| Total non-interest expense | 380,028 | 381,461 | 366,090 | 368,539 | 360,687 | 1,127,579 | 1,034,185 | |||||||||||||||||||||||||||||||

| Income before taxes | 296,041 | 267,088 | 253,055 | 253,081 | 232,709 | 816,184 | 694,008 | |||||||||||||||||||||||||||||||

| Income tax expense | 79,787 | 71,561 | 64,016 | 67,719 | 62,708 | 215,364 | 184,325 | |||||||||||||||||||||||||||||||

| Net income | $ | 216,254 | $ | 195,527 | $ | 189,039 | $ | 185,362 | $ | 170,001 | $ | 600,820 | $ | 509,683 | ||||||||||||||||||||||||

| Preferred stock dividends | 13,295 | 6,991 | 6,991 | 6,991 | 6,991 | 27,277 | 20,973 | |||||||||||||||||||||||||||||||

| Preferred stock redemption | 14,046 | — | — | — | — | 14,046 | — | |||||||||||||||||||||||||||||||

| Net income applicable to common shares | $ | 188,913 | $ | 188,536 | $ | 182,048 | $ | 178,371 | $ | 163,010 | $ | 559,497 | $ | 488,710 | ||||||||||||||||||||||||

| Net income per common share - Basic | $ | 2.82 | $ | 2.82 | $ | 2.73 | $ | 2.68 | $ | 2.51 | $ | 8.37 | $ | 7.79 | ||||||||||||||||||||||||

| Net income per common share - Diluted | $ | 2.78 | $ | 2.78 | $ | 2.69 | $ | 2.63 | $ | 2.47 | $ | 8.25 | $ | 7.67 | ||||||||||||||||||||||||

| Cash dividends declared per common share | $ | 0.50 | $ | 0.50 | $ | 0.50 | $ | 0.45 | $ | 0.45 | $ | 1.50 | $ | 1.35 | ||||||||||||||||||||||||

| Weighted average common shares outstanding | 66,952 | 66,931 | 66,726 | 66,491 | 64,888 | 66,871 | 62,743 | |||||||||||||||||||||||||||||||

| Dilutive potential common shares | 1,028 | 888 | 923 | 1,233 | 1,053 | 945 | 934 | |||||||||||||||||||||||||||||||

| Average common shares and dilutive common shares | 67,980 | 67,819 | 67,649 | 67,724 | 65,941 | 67,816 | 63,677 | |||||||||||||||||||||||||||||||

% Growth From (1) |

|||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 |

Sep 30, 2024 | Jun 30, 2025 (2) |

Sep 30, 2024 | ||||||||||||||||||||||||||||

| Balance: | |||||||||||||||||||||||||||||||||||

| Mortgage loans held-for-sale, excluding early buy-out exercised loans guaranteed by U.S. government agencies | $ | 211,360 | $ | 192,633 | $ | 181,580 | $ | 189,774 | $ | 314,693 | 39 | % | (33) | % | |||||||||||||||||||||

| Mortgage loans held-for-sale, early buy-out exercised loans guaranteed by U.S. government agencies | 122,523 | 106,973 | 135,224 | 141,487 | 146,374 | 58 | (16) | ||||||||||||||||||||||||||||

| Total mortgage loans held-for-sale | $ | 333,883 | $ | 299,606 | $ | 316,804 | $ | 331,261 | $ | 461,067 | 45 | % | (28) | % | |||||||||||||||||||||

| Core loans: | |||||||||||||||||||||||||||||||||||

| Commercial | |||||||||||||||||||||||||||||||||||

| Commercial and industrial | $ | 7,135,083 | $ | 7,028,247 | $ | 6,871,206 | $ | 6,867,422 | $ | 6,774,683 | 6 | % | 5 | % | |||||||||||||||||||||

| Asset-based lending | 1,588,522 | 1,663,693 | 1,701,962 | 1,611,001 | 1,709,685 | (18) | (7) | ||||||||||||||||||||||||||||

| Municipal | 804,986 | 771,785 | 798,646 | 826,653 | 827,125 | 17 | (3) | ||||||||||||||||||||||||||||

| Leases | 2,834,563 | 2,757,331 | 2,680,943 | 2,537,325 | 2,443,721 | 11 | 16 | ||||||||||||||||||||||||||||

| Commercial real estate | |||||||||||||||||||||||||||||||||||

| Residential construction | 60,923 | 59,027 | 55,849 | 48,617 | 73,088 | 13 | (17) | ||||||||||||||||||||||||||||

| Commercial construction | 2,273,545 | 2,165,263 | 2,086,797 | 2,065,775 | 1,984,240 | 20 | 15 | ||||||||||||||||||||||||||||

| Land | 323,685 | 304,827 | 306,235 | 319,689 | 346,362 | 25 | (7) | ||||||||||||||||||||||||||||

| Office | 1,578,208 | 1,601,208 | 1,641,555 | 1,656,109 | 1,675,286 | (6) | (6) | ||||||||||||||||||||||||||||

| Industrial | 2,912,547 | 2,824,889 | 2,677,555 | 2,628,576 | 2,527,932 | 12 | 15 | ||||||||||||||||||||||||||||

| Retail | 1,478,861 | 1,452,351 | 1,402,837 | 1,374,655 | 1,404,586 | 7 | 5 | ||||||||||||||||||||||||||||

| Multi-family | 3,306,597 | 3,200,578 | 3,091,314 | 3,125,505 | 3,193,339 | 13 | 4 | ||||||||||||||||||||||||||||

| Mixed use and other | 1,684,841 | 1,683,867 | 1,652,759 | 1,685,018 | 1,588,584 | 0 | 6 | ||||||||||||||||||||||||||||

| Home equity | 484,202 | 466,815 | 455,683 | 445,028 | 427,043 | 15 | 13 | ||||||||||||||||||||||||||||

| Residential real estate | |||||||||||||||||||||||||||||||||||

| Residential real estate loans for investment | 4,019,046 | 3,814,715 | 3,561,417 | 3,456,009 | 3,252,649 | 21 | 24 | ||||||||||||||||||||||||||||

| Residential mortgage loans, early buy-out eligible loans guaranteed by U.S. government agencies | 75,088 | 80,800 | 86,952 | 114,985 | 92,355 | (28) | (19) | ||||||||||||||||||||||||||||

| Residential mortgage loans, early buy-out exercised loans guaranteed by U.S. government agencies | 49,736 | 53,267 | 36,790 | 41,771 | 43,034 | (26) | 16 | ||||||||||||||||||||||||||||

| Total core loans | $ | 30,610,433 | $ | 29,928,663 | $ | 29,108,500 | $ | 28,804,138 | $ | 28,363,712 | 9 | % | 8 | % | |||||||||||||||||||||

| Niche loans: | |||||||||||||||||||||||||||||||||||

| Commercial | |||||||||||||||||||||||||||||||||||

| Franchise | $ | 1,298,140 | $ | 1,286,265 | $ | 1,262,555 | $ | 1,268,521 | $ | 1,191,686 | 4 | % | 9 | % | |||||||||||||||||||||

| Mortgage warehouse lines of credit | 1,204,661 | 1,232,530 | 1,019,543 | 893,854 | 750,462 | (9) | 61 | ||||||||||||||||||||||||||||

| Community Advantage - homeowners association | 537,696 | 526,595 | 525,492 | 525,446 | 501,645 | 8 | 7 | ||||||||||||||||||||||||||||

| Insurance agency lending | 1,140,691 | 1,120,985 | 1,070,979 | 1,044,329 | 1,048,686 | 7 | 9 | ||||||||||||||||||||||||||||

| Premium Finance receivables | |||||||||||||||||||||||||||||||||||

| U.S. property & casualty insurance | 7,502,901 | 7,378,340 | 6,486,663 | 6,447,625 | 6,253,271 | 7 | 20 | ||||||||||||||||||||||||||||

| Canada property & casualty insurance | 863,391 | 944,836 | 753,199 | 824,417 | 878,410 | (34) | (2) | ||||||||||||||||||||||||||||

| Life insurance | 8,758,553 | 8,506,960 | 8,365,140 | 8,147,145 | 7,996,899 | 12 | 10 | ||||||||||||||||||||||||||||

| Consumer and other | 147,016 | 116,505 | 116,319 | 99,562 | 82,676 | 104 | 78 | ||||||||||||||||||||||||||||

| Total niche loans | $ | 21,453,049 | $ | 21,113,016 | $ | 19,599,890 | $ | 19,250,899 | $ | 18,703,735 | 6 | % | 15 | % | |||||||||||||||||||||

| Total loans, net of unearned income | $ | 52,063,482 | $ | 51,041,679 | $ | 48,708,390 | $ | 48,055,037 | $ | 47,067,447 | 8 | % | 11 | % | |||||||||||||||||||||

| % Growth From | ||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | Sep 30, 2025 |

Jun 30, 2025 |

Mar 31, 2025 |

Dec 31, 2024 |

Sep 30, 2024 |

Jun 30, 2025 (1) |

Sep 30, 2024 | |||||||||||||||||||||||||||||||

| Balance: | ||||||||||||||||||||||||||||||||||||||

| Non-interest-bearing | $ | 10,952,146 | $ | 10,877,166 | $ | 11,201,859 | $ | 11,410,018 | $ | 10,739,132 | 3 | % | 2 | % | ||||||||||||||||||||||||

| NOW and interest-bearing demand deposits | 6,710,919 | 6,795,725 | 6,340,168 | 5,865,546 | 5,466,932 | (5) | 23 | |||||||||||||||||||||||||||||||

Wealth management deposits (2) |

1,600,735 | 1,595,764 | 1,408,790 | 1,469,064 | 1,303,354 | 1 | 23 | |||||||||||||||||||||||||||||||

| Money market | 20,270,382 | 19,556,041 | 18,074,733 | 17,975,191 | 17,713,726 | 14 | 14 | |||||||||||||||||||||||||||||||

| Savings | 6,758,743 | 6,659,419 | 6,576,251 | 6,372,499 | 6,183,249 | 6 | 9 | |||||||||||||||||||||||||||||||

| Time certificates of deposit | 10,418,456 | 10,332,696 | 9,968,237 | 9,420,031 | 9,998,573 | 3 | 4 | |||||||||||||||||||||||||||||||

| Total deposits | $ | 56,711,381 | $ | 55,816,811 | $ | 53,570,038 | $ | 52,512,349 | $ | 51,404,966 | 6 | % | 10 | % | ||||||||||||||||||||||||

| Mix: | ||||||||||||||||||||||||||||||||||||||

| Non-interest-bearing | 19 | % | 19 | % | 21 | % | 22 | % | 21 | % | ||||||||||||||||||||||||||||

| NOW and interest-bearing demand deposits | 12 | 12 | 12 | 11 | 11 | |||||||||||||||||||||||||||||||||

Wealth management deposits (2) |

3 | 3 | 3 | 3 | 3 | |||||||||||||||||||||||||||||||||

| Money market | 36 | 35 | 34 | 34 | 34 | |||||||||||||||||||||||||||||||||

| Savings | 12 | 12 | 12 | 12 | 12 | |||||||||||||||||||||||||||||||||

| Time certificates of deposit | 18 | 19 | 18 | 18 | 19 | |||||||||||||||||||||||||||||||||

| Total deposits | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||||||||||||||||||||

| (Dollars in thousands) | Total Time Certificates of Deposit |

Weighted-Average Rate of Maturing Time Certificates of Deposit |

||||||||||||

| 1-3 months | $ | 4,450,481 | 3.83 | % | ||||||||||

| 4-6 months | 3,165,121 | 3.72 | ||||||||||||

| 7-9 months | 1,489,181 | 3.64 | ||||||||||||

| 10-12 months | 973,156 | 3.79 | ||||||||||||

| 13-18 months | 196,146 | 3.13 | ||||||||||||

| 19-24 months | 79,669 | 3.00 | ||||||||||||

| 24+ months | 64,702 | 3.00 | ||||||||||||

| Total | $ | 10,418,456 | 3.74 | % | ||||||||||

| Average Balance for three months ended, | ||||||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | ||||||||||||||||||||||||||||

| (In thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | |||||||||||||||||||||||||||

Interest-bearing deposits with banks, securities purchased under resale agreements and cash equivalents (1) |

$ | 3,276,683 | $ | 3,308,199 | $ | 3,520,048 | $ | 3,934,016 | $ | 2,413,728 | ||||||||||||||||||||||

Investment securities (2) |

9,377,930 | 8,801,560 | 8,409,735 | 8,090,271 | 8,276,576 | |||||||||||||||||||||||||||

FHLB and FRB stock (3) |

282,338 | 282,001 | 281,702 | 271,825 | 263,707 | |||||||||||||||||||||||||||

Liquidity management assets (4) |

$ | 12,936,951 | $ | 12,391,760 | $ | 12,211,485 | $ | 12,296,112 | $ | 10,954,011 | ||||||||||||||||||||||

Other earning assets (4) (5) |

— | — | 13,140 | 20,528 | 17,542 | |||||||||||||||||||||||||||

| Mortgage loans held-for-sale | 295,365 | 310,534 | 286,710 | 378,707 | 376,251 | |||||||||||||||||||||||||||

Loans, net of unearned income (4) (6) |

51,403,566 | 49,517,635 | 47,833,380 | 47,153,014 | 45,920,586 | |||||||||||||||||||||||||||

Total earning assets (4) |

$ | 64,635,882 | $ | 62,219,929 | $ | 60,344,715 | $ | 59,848,361 | $ | 57,268,390 | ||||||||||||||||||||||

| Allowance for loan and investment security losses | (410,681) | (398,685) | (375,371) | (367,238) | (383,736) | |||||||||||||||||||||||||||

| Cash and due from banks | 495,292 | 478,707 | 476,423 | 470,033 | 467,333 | |||||||||||||||||||||||||||

| Other assets | 3,582,543 | 3,540,394 | 3,661,275 | 3,642,949 | 3,563,296 | |||||||||||||||||||||||||||

Total assets |

$ | 68,303,036 | $ | 65,840,345 | $ | 64,107,042 | $ | 63,594,105 | $ | 60,915,283 | ||||||||||||||||||||||

| NOW and interest-bearing demand deposits | $ | 6,687,292 | $ | 6,423,050 | $ | 6,046,189 | $ | 5,601,672 | $ | 5,174,673 | ||||||||||||||||||||||

| Wealth management deposits | 1,604,142 | 1,552,989 | 1,574,480 | 1,430,163 | 1,362,747 | |||||||||||||||||||||||||||

| Money market accounts | 19,431,021 | 18,184,754 | 17,581,141 | 17,579,395 | 16,436,111 | |||||||||||||||||||||||||||

| Savings accounts | 6,723,325 | 6,578,698 | 6,479,444 | 6,288,727 | 6,096,746 | |||||||||||||||||||||||||||

| Time deposits | 10,319,719 | 9,841,702 | 9,406,126 | 9,702,948 | 9,598,109 | |||||||||||||||||||||||||||

| Interest-bearing deposits | $ | 44,765,499 | $ | 42,581,193 | $ | 41,087,380 | $ | 40,602,905 | $ | 38,668,386 | ||||||||||||||||||||||

FHLB advances (3) |

3,151,310 | 3,151,310 | 3,151,309 | 3,160,658 | 3,178,973 | |||||||||||||||||||||||||||

| Other borrowings | 614,892 | 593,657 | 582,139 | 577,786 | 622,792 | |||||||||||||||||||||||||||

| Subordinated notes | 298,481 | 298,398 | 298,306 | 298,225 | 298,135 | |||||||||||||||||||||||||||

| Junior subordinated debentures | 253,566 | 253,566 | 253,566 | 253,566 | 253,566 | |||||||||||||||||||||||||||

Total interest-bearing liabilities |

$ | 49,083,748 | $ | 46,878,124 | $ | 45,372,700 | $ | 44,893,140 | $ | 43,021,852 | ||||||||||||||||||||||

| Non-interest-bearing deposits | 10,791,709 | 10,643,798 | 10,732,156 | 10,718,738 | 10,271,613 | |||||||||||||||||||||||||||

| Other liabilities | 1,472,036 | 1,456,383 | 1,541,245 | 1,563,824 | 1,631,389 | |||||||||||||||||||||||||||

| Equity | 6,955,543 | 6,862,040 | 6,460,941 | 6,418,403 | 5,990,429 | |||||||||||||||||||||||||||

Total liabilities and shareholders’ equity |

$ | 68,303,036 | $ | 65,840,345 | $ | 64,107,042 | $ | 63,594,105 | $ | 60,915,283 | ||||||||||||||||||||||

Net free funds/contribution (7) |

$ | 15,552,134 | $ | 15,341,805 | $ | 14,972,015 | $ | 14,955,221 | $ | 14,246,538 | ||||||||||||||||||||||

| Net Interest Income for three months ended, | ||||||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | ||||||||||||||||||||||||||||

| (In thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | |||||||||||||||||||||||||||

| Interest income: | ||||||||||||||||||||||||||||||||

| Interest-bearing deposits with banks, securities purchased under resale agreements and cash equivalents | $ | 35,067 | $ | 34,593 | $ | 36,945 | $ | 46,308 | $ | 32,885 | ||||||||||||||||||||||

| Investment securities | 87,101 | 78,733 | 72,706 | 67,783 | 70,260 | |||||||||||||||||||||||||||

FHLB and FRB stock (1) |

5,444 | 5,393 | 5,307 | 5,157 | 5,451 | |||||||||||||||||||||||||||

Liquidity management assets (2) |

$ | 127,612 | $ | 118,719 | $ | 114,958 | $ | 119,248 | $ | 108,596 | ||||||||||||||||||||||

Other earning assets (2) |

— | — | 92 | 310 | 282 | |||||||||||||||||||||||||||

| Mortgage loans held-for-sale | 4,757 | 4,872 | 4,246 | 5,623 | 6,233 | |||||||||||||||||||||||||||

Loans, net of unearned income (2) |

834,294 | 800,197 | 770,568 | 791,390 | 796,637 | |||||||||||||||||||||||||||

| Total interest income | $ | 966,663 | $ | 923,788 | $ | 889,864 | $ | 916,571 | $ | 911,748 | ||||||||||||||||||||||

| Interest expense: | ||||||||||||||||||||||||||||||||

| NOW and interest-bearing demand deposits | $ | 40,448 | $ | 37,517 | $ | 33,600 | $ | 31,695 | $ | 30,971 | ||||||||||||||||||||||

| Wealth management deposits | 8,415 | 8,182 | 8,606 | 9,412 | 10,158 | |||||||||||||||||||||||||||

| Money market accounts | 169,831 | 155,890 | 146,374 | 159,945 | 167,382 | |||||||||||||||||||||||||||

| Savings accounts | 38,844 | 37,637 | 35,923 | 38,402 | 42,892 | |||||||||||||||||||||||||||

| Time deposits | 98,308 | 94,244 | 95,730 | 106,934 | 110,616 | |||||||||||||||||||||||||||

| Interest-bearing deposits | $ | 355,846 | $ | 333,470 | $ | 320,233 | $ | 346,388 | $ | 362,019 | ||||||||||||||||||||||

FHLB advances (1) |

26,007 | 25,724 | 25,441 | 26,050 | 26,254 | |||||||||||||||||||||||||||

| Other borrowings | 6,887 | 6,957 | 6,792 | 7,519 | 9,013 | |||||||||||||||||||||||||||

| Subordinated notes | 3,717 | 3,735 | 3,714 | 3,733 | 3,712 | |||||||||||||||||||||||||||

| Junior subordinated debentures | 4,367 | 4,328 | 4,311 | 4,663 | 5,023 | |||||||||||||||||||||||||||

| Total interest expense | $ | 396,824 | $ | 374,214 | $ | 360,491 | $ | 388,353 | $ | 406,021 | ||||||||||||||||||||||

| Less: Fully taxable-equivalent adjustment | (2,829) | (2,880) | (2,899) | (3,070) | (3,144) | |||||||||||||||||||||||||||

Net interest income (GAAP) (3) |

567,010 | 546,694 | 526,474 | 525,148 | 502,583 | |||||||||||||||||||||||||||

| Fully taxable-equivalent adjustment | 2,829 | 2,880 | 2,899 | 3,070 | 3,144 | |||||||||||||||||||||||||||

Net interest income, fully taxable-equivalent (non-GAAP) (3) |

$ | 569,839 | $ | 549,574 | $ | 529,373 | $ | 528,218 | $ | 505,727 | ||||||||||||||||||||||

| Net Interest Margin for three months ended, | ||||||||||||||||||||||||||||||||

| Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 |

Dec 31, 2024 | Sep 30, 2024 |

||||||||||||||||||||||||||||

| Yield earned on: | ||||||||||||||||||||||||||||||||

| Interest-bearing deposits with banks, securities purchased under resale agreements and cash equivalents | 4.25 | % | 4.19 | % | 4.26 | % | 4.68 | % | 5.42 | % | ||||||||||||||||||||||

| Investment securities | 3.68 | 3.59 | 3.51 | 3.33 | 3.38 | |||||||||||||||||||||||||||

FHLB and FRB stock (1) |

7.65 | 7.67 | 7.64 | 7.55 | 8.22 | |||||||||||||||||||||||||||

| Liquidity management assets | 3.91 | % | 3.84 | % | 3.82 | % | 3.86 | % | 3.94 | % | ||||||||||||||||||||||

| Other earning assets | — | — | 2.84 | 6.01 | 6.38 | |||||||||||||||||||||||||||

| Mortgage loans held-for-sale | 6.39 | 6.29 | 6.01 | 5.91 | 6.59 | |||||||||||||||||||||||||||

| Loans, net of unearned income | 6.44 | 6.48 | 6.53 | 6.68 | 6.90 | |||||||||||||||||||||||||||

| Total earning assets | 5.93 | % | 5.96 | % | 5.98 | % | 6.09 | % | 6.33 | % | ||||||||||||||||||||||

| Rate paid on: | ||||||||||||||||||||||||||||||||

| NOW and interest-bearing demand deposits | 2.40 | % | 2.34 | % | 2.25 | % | 2.25 | % | 2.38 | % | ||||||||||||||||||||||

| Wealth management deposits | 2.08 | 2.11 | 2.22 | 2.62 | 2.97 | |||||||||||||||||||||||||||

| Money market accounts | 3.47 | 3.44 | 3.38 | 3.62 | 4.05 | |||||||||||||||||||||||||||

| Savings accounts | 2.29 | 2.29 | 2.25 | 2.43 | 2.80 | |||||||||||||||||||||||||||

| Time deposits | 3.78 | 3.84 | 4.13 | 4.38 | 4.58 | |||||||||||||||||||||||||||

| Interest-bearing deposits | 3.15 | % | 3.14 | % | 3.16 | % | 3.39 | % | 3.72 | % | ||||||||||||||||||||||

| FHLB advances | 3.27 | 3.27 | 3.27 | 3.28 | 3.29 | |||||||||||||||||||||||||||

| Other borrowings | 4.44 | 4.70 | 4.73 | 5.18 | 5.76 | |||||||||||||||||||||||||||

| Subordinated notes | 4.94 | 5.02 | 5.05 | 4.98 | 4.95 | |||||||||||||||||||||||||||

| Junior subordinated debentures | 6.83 | 6.85 | 6.90 | 7.32 | 7.88 | |||||||||||||||||||||||||||

| Total interest-bearing liabilities | 3.21 | % | 3.20 | % | 3.22 | % | 3.44 | % | 3.75 | % | ||||||||||||||||||||||

Interest rate spread (2) (3) |

2.72 | % | 2.76 | % | 2.76 | % | 2.65 | % | 2.58 | % | ||||||||||||||||||||||

| Less: Fully taxable-equivalent adjustment | (0.02) | (0.02) | (0.02) | (0.02) | (0.02) | |||||||||||||||||||||||||||

Net free funds/contribution (4) |

0.78 | 0.78 | 0.80 | 0.86 | 0.93 | |||||||||||||||||||||||||||

Net interest margin (GAAP) (3) |

3.48 | % | 3.52 | % | 3.54 | % | 3.49 | % | 3.49 | % | ||||||||||||||||||||||

| Fully taxable-equivalent adjustment | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | |||||||||||||||||||||||||||

Net interest margin, fully taxable-equivalent (non-GAAP) (3) |

3.50 | % | 3.54 | % | 3.56 | % | 3.51 | % | 3.51 | % | ||||||||||||||||||||||

|

Average Balance

for nine months ended,

|

Interest

for nine months ended,

|

Yield/Rate

for nine months ended,

|

|||||||||||||||||||||||||||

| (Dollars in thousands) | Sep 30, 2025 | Sep 30, 2024 |

Sep 30, 2025 | Sep 30, 2024 | Sep 30, 2025 | Sep 30, 2024 | |||||||||||||||||||||||

Interest-bearing deposits with banks, securities purchased under resale agreements and cash equivalents (1) |

$ | 3,367,419 | $ | 1,720,387 | $ | 106,605 | $ | 69,310 | 4.23 | % | 5.38 | % | |||||||||||||||||

Investment securities (2) |

8,866,621 | 8,276,711 | 238,540 | 210,834 | 3.60 | 3.40 | |||||||||||||||||||||||

FHLB and FRB stock (3) |

282,016 | 249,375 | 16,144 | 14,903 | 7.65 | 7.98 | |||||||||||||||||||||||

Liquidity management assets (4) (5) |

$ | 12,516,056 | $ | 10,246,473 | $ | 361,289 | $ | 295,047 | 3.86 | % | 3.85 | % | |||||||||||||||||

Other earning assets (4) (5) (6) |

4,332 | 15,966 | 92 | 715 | 2.84 | 5.98 | |||||||||||||||||||||||

| Mortgage loans held-for-sale | 297,568 | 338,061 | 13,875 | 15,813 | 6.23 | 6.25 | |||||||||||||||||||||||

Loans, net of unearned income (4) (5) (7) |

49,597,938 | 43,963,779 | 2,405,059 | 2,261,341 | 6.48 | 6.87 | |||||||||||||||||||||||

Total earning assets (5) |

$ | 62,415,894 | $ | 54,564,279 | $ | 2,780,315 | $ | 2,572,916 | 5.96 | % | 6.30 | % | |||||||||||||||||

| Allowance for loan and investment security losses | (395,041) | (368,713) | |||||||||||||||||||||||||||

| Cash and due from banks | 483,543 | 450,899 | |||||||||||||||||||||||||||

| Other assets | 3,594,449 | 3,367,882 | |||||||||||||||||||||||||||

Total assets |

$ | 66,098,845 | $ | 58,014,347 | |||||||||||||||||||||||||

| NOW and interest-bearing demand deposits | $ | 6,387,859 | $ | 5,279,697 | $ | 111,565 | $ | 98,586 | 2.34 | % | 2.49 | % | |||||||||||||||||

| Wealth management deposits | 1,577,312 | 1,467,886 | 25,203 | 30,913 | 2.14 | 2.81 | |||||||||||||||||||||||

| Money market accounts | 18,405,748 | 15,398,045 | 472,095 | 460,466 | 3.43 | 3.99 | |||||||||||||||||||||||

| Savings accounts | 6,594,716 | 5,923,205 | 112,404 | 123,026 | 2.28 | 2.77 | |||||||||||||||||||||||

| Time deposits | 9,859,196 | 8,435,172 | 288,282 | 284,263 | 3.91 | 4.50 | |||||||||||||||||||||||

| Interest-bearing deposits | $ | 42,824,831 | $ | 36,504,005 | $ | 1,009,549 | $ | 997,254 | 3.15 | % | 3.65 | % | |||||||||||||||||

| Federal Home Loan Bank advances | 3,151,310 | 3,002,228 | 77,172 | 73,099 | 3.27 | 3.25 | |||||||||||||||||||||||

| Other borrowings | 597,016 | 612,627 | 20,636 | 26,961 | 4.62 | 5.88 | |||||||||||||||||||||||

| Subordinated notes | 298,396 | 381,813 | 11,166 | 14,384 | 5.00 | 5.03 | |||||||||||||||||||||||

| Junior subordinated debentures | 253,566 | 253,566 | 13,006 | 15,011 | 6.86 | 7.91 | |||||||||||||||||||||||

Total interest-bearing liabilities |

$ | 47,125,119 | $ | 40,754,239 | $ | 1,131,529 | $ | 1,126,709 | 3.21 | % | 3.69 | % | |||||||||||||||||

| Non-interest-bearing deposits | 10,722,772 | 10,041,972 | |||||||||||||||||||||||||||

| Other liabilities | 1,489,635 | 1,589,790 | |||||||||||||||||||||||||||

| Equity | 6,761,319 | 5,628,346 | |||||||||||||||||||||||||||

Total liabilities and shareholders’ equity |

$ | 66,098,845 | $ | 58,014,347 | |||||||||||||||||||||||||

Interest rate spread (5) (8) |

2.75 | % | 2.61 | % | |||||||||||||||||||||||||

| Less: Fully taxable-equivalent adjustment | (8,608) | (8,820) | (0.02) | (0.02) | |||||||||||||||||||||||||

Net free funds/contribution (9) |

$ | 15,290,775 | $ | 13,810,040 | 0.78 | 0.93 | |||||||||||||||||||||||

Net interest income/margin (GAAP) (5) |

$ | 1,640,178 | $ | 1,437,387 | 3.51 | % | 3.52 | % | |||||||||||||||||||||

| Fully taxable-equivalent adjustment | 8,608 | 8,820 | 0.02 | 0.02 | |||||||||||||||||||||||||

Net interest income/margin, fully taxable-equivalent (non-GAAP) (5) |

$ | 1,648,786 | $ | 1,446,207 | 3.53 | % | 3.54 | % | |||||||||||||||||||||

| Static Shock Scenario | +200 Basis Points | +100 Basis Points | -100 Basis Points | -200 Basis Points | ||||||||||||||||||||||

| Sep 30, 2025 | (2.3) | % | (0.8) | % | 0.0 | % | (0.4) | % | ||||||||||||||||||

| Jun 30, 2025 | (1.5) | (0.4) | (0.2) | (1.2) | ||||||||||||||||||||||

| Mar 31, 2025 | (1.8) | (0.6) | (0.2) | (1.2) | ||||||||||||||||||||||

| Dec 31, 2024 | (1.6) | (0.6) | (0.3) | (1.5) | ||||||||||||||||||||||

| Sep 30, 2024 | 1.2 | 1.1 | 0.4 | (0.9) | ||||||||||||||||||||||

| Ramp Scenario | +200 Basis Points | +100 Basis Points | -100 Basis Points | -200 Basis Points | |||||||||||||||||||

| Sep 30, 2025 | (0.2) | % | (0.1) | % | 0.1 | % | (0.1) | % | |||||||||||||||

| Jun 30, 2025 | 0.0 | 0.0 | (0.1) | (0.4) | |||||||||||||||||||

| Mar 31, 2025 | 0.2 | 0.2 | (0.1) | (0.5) | |||||||||||||||||||

| Dec 31, 2024 | (0.2) | (0.0) | 0.0 | (0.3) | |||||||||||||||||||

| Sep 30, 2024 | 1.6 | 1.2 | 0.7 | 0.5 | |||||||||||||||||||

| Loans repricing or contractual maturity period | |||||||||||||||||||||||||||||

| As of September 30, 2025 | One year or less |

From one to five years |

From five to fifteen years | After fifteen years | Total | ||||||||||||||||||||||||

| (In thousands) | |||||||||||||||||||||||||||||

| Commercial | |||||||||||||||||||||||||||||

| Fixed rate | $ | 465,635 | $ | 3,851,843 | $ | 2,154,642 | $ | 17,113 | $ | 6,489,233 | |||||||||||||||||||

| Variable rate | 10,054,366 | 743 | — | — | 10,055,109 | ||||||||||||||||||||||||

| Total commercial | $ | 10,520,001 | $ | 3,852,586 | $ | 2,154,642 | $ | 17,113 | $ | 16,544,342 | |||||||||||||||||||

| Commercial real estate | |||||||||||||||||||||||||||||

| Fixed rate | $ | 771,993 | $ | 2,629,379 | $ | 358,703 | $ | 68,729 | $ | 3,828,804 | |||||||||||||||||||

| Variable rate | 9,779,638 | 10,700 | 65 | — | 9,790,403 | ||||||||||||||||||||||||

| Total commercial real estate | $ | 10,551,631 | $ | 2,640,079 | $ | 358,768 | $ | 68,729 | $ | 13,619,207 | |||||||||||||||||||

| Home equity | |||||||||||||||||||||||||||||

| Fixed rate | $ | 9,470 | $ | 464 | $ | — | $ | 13 | $ | 9,947 | |||||||||||||||||||

| Variable rate | 474,255 | — | — | — | 474,255 | ||||||||||||||||||||||||

| Total home equity | $ | 483,725 | $ | 464 | $ | — | $ | 13 | $ | 484,202 | |||||||||||||||||||

| Residential real estate | |||||||||||||||||||||||||||||

| Fixed rate | $ | 17,018 | $ | 4,563 | $ | 70,142 | $ | 1,040,869 | $ | 1,132,592 | |||||||||||||||||||

| Variable rate | 117,542 | 736,051 | 2,157,685 | — | 3,011,278 | ||||||||||||||||||||||||

| Total residential real estate | $ | 134,560 | $ | 740,614 | $ | 2,227,827 | $ | 1,040,869 | $ | 4,143,870 | |||||||||||||||||||

| Premium finance receivables - property & casualty | |||||||||||||||||||||||||||||

| Fixed rate | $ | 8,275,798 | $ | 90,494 | $ | — | $ | — | $ | 8,366,292 | |||||||||||||||||||

| Variable rate | — | — | — | — | — | ||||||||||||||||||||||||

| Total premium finance receivables - property & casualty | $ | 8,275,798 | $ | 90,494 | $ | — | $ | — | $ | 8,366,292 | |||||||||||||||||||

| Premium finance receivables - life insurance | |||||||||||||||||||||||||||||

| Fixed rate | $ | 255,894 | $ | 140,954 | $ | 4,000 | $ | — | $ | 400,848 | |||||||||||||||||||

| Variable rate | 8,357,705 | — | — | — | 8,357,705 | ||||||||||||||||||||||||

| Total premium finance receivables - life insurance | $ | 8,613,599 | $ | 140,954 | $ | 4,000 | $ | — | $ | 8,758,553 | |||||||||||||||||||

| Consumer and other | |||||||||||||||||||||||||||||

| Fixed rate | $ | 65,657 | $ | 8,660 | $ | 1,045 | $ | 853 | $ | 76,215 | |||||||||||||||||||

| Variable rate | 70,801 | — | — | — | 70,801 | ||||||||||||||||||||||||

| Total consumer and other | $ | 136,458 | $ | 8,660 | $ | 1,045 | $ | 853 | $ | 147,016 | |||||||||||||||||||

| Total per category | |||||||||||||||||||||||||||||

| Fixed rate | $ | 9,861,465 | $ | 6,726,357 | $ | 2,588,532 | $ | 1,127,577 | $ | 20,303,931 | |||||||||||||||||||

| Variable rate | 28,854,307 | 747,494 | 2,157,750 | — | 31,759,551 | ||||||||||||||||||||||||

| Total loans, net of unearned income | $ | 38,715,772 | $ | 7,473,851 | $ | 4,746,282 | $ | 1,127,577 | $ | 52,063,482 | |||||||||||||||||||

Less: Existing cash flow hedging derivatives (1) |

(5,650,000) | ||||||||||||||||||||||||||||

| Total loans repricing or maturing in one year or less, adjusted for cash flow hedging activity | $ | 33,065,772 | |||||||||||||||||||||||||||

| Variable Rate Loan Pricing by Index: | |||||||||||||||||||||||||||||

SOFR tenors (2) |

$ | 20,295,819 | |||||||||||||||||||||||||||

12- month CMT (3) |

7,284,381 | ||||||||||||||||||||||||||||

| Prime | 3,083,193 | ||||||||||||||||||||||||||||

| Fed Funds | 768,000 | ||||||||||||||||||||||||||||

| Other U.S. Treasury tenors | 191,629 | ||||||||||||||||||||||||||||

| Other | 136,529 | ||||||||||||||||||||||||||||

| Total variable rate | $ | 31,759,551 | |||||||||||||||||||||||||||

| Basis Point (bp) Change in | |||||||||||||||||||||||

| 1-month SOFR |

12- month CMT | Prime | |||||||||||||||||||||

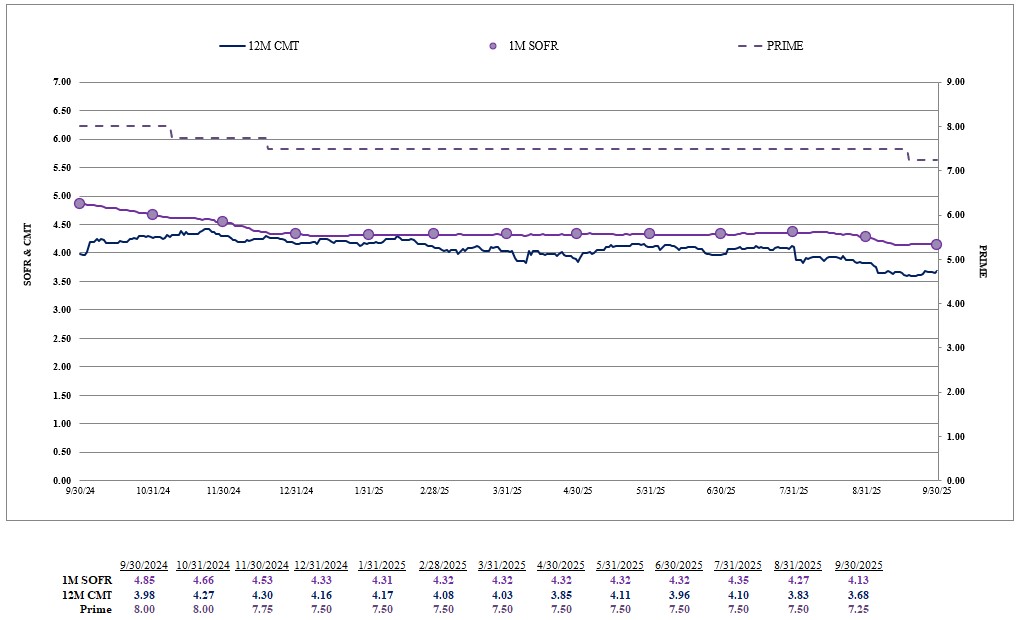

| Third Quarter 2025 | (19) | bps | (28) | bps | (25) | bps | |||||||||||||||||

| Second Quarter 2025 | — | (7) | — | ||||||||||||||||||||

| First Quarter 2025 | (1) | (13) | — | ||||||||||||||||||||

| fourth quarter 2024 | (52) | 18 | (50) | ||||||||||||||||||||

| Third Quarter 2024 | (49) | (111) | (50) | ||||||||||||||||||||

| Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | Sep 30, | Sep 30, | |||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | 2025 | 2024 | ||||||||||||||||||||||||||||||||||

| Allowance for credit losses at beginning of period | $ | 457,461 | $ | 448,387 | $ | 437,060 | $ | 436,193 | $ | 437,560 | $ | 437,060 | $ | 427,612 | |||||||||||||||||||||||||||

| Provision for credit losses - Other | 21,768 | 22,234 | 23,963 | 16,979 | 6,787 | 67,965 | 68,521 | ||||||||||||||||||||||||||||||||||

| Provision for credit losses - Day 1 on non-PCD assets acquired during the period | — | — | — | — | 15,547 | — | 15,547 | ||||||||||||||||||||||||||||||||||

| Initial allowance for credit losses recognized on PCD assets acquired during the period | — | — | — | — | 3,004 | — | 3,004 | ||||||||||||||||||||||||||||||||||

| Other adjustments | (88) | 180 | 4 | (187) | 30 | 96 | (20) | ||||||||||||||||||||||||||||||||||

| Charge-offs: | |||||||||||||||||||||||||||||||||||||||||

| Commercial | 21,597 | 6,148 | 9,722 | 5,090 | 22,975 | 37,467 | 43,774 | ||||||||||||||||||||||||||||||||||

| Commercial real estate | 144 | 5,711 | 454 | 1,037 | 95 | 6,309 | 21,090 | ||||||||||||||||||||||||||||||||||

| Home equity | 27 | 111 | — | — | — | 138 | 74 | ||||||||||||||||||||||||||||||||||

| Residential real estate | 26 | — | — | 114 | — | 26 | 61 | ||||||||||||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 6,860 | 6,346 | 7,114 | 13,301 | 7,790 | 20,320 | 24,214 | ||||||||||||||||||||||||||||||||||

| Premium finance receivables - life insurance | 18 | — | 12 | — | 4 | 30 | 4 | ||||||||||||||||||||||||||||||||||

| Consumer and other | 174 | 179 | 147 | 189 | 154 | 500 | 398 | ||||||||||||||||||||||||||||||||||

| Total charge-offs | 28,846 | 18,495 | 17,449 | 19,731 | 31,018 | 64,790 | 89,615 | ||||||||||||||||||||||||||||||||||

| Recoveries: | |||||||||||||||||||||||||||||||||||||||||

| Commercial | 1,449 | 1,746 | 929 | 775 | 649 | 4,124 | 2,078 | ||||||||||||||||||||||||||||||||||

| Commercial real estate | 241 | 10 | 12 | 172 | 30 | 263 | 151 | ||||||||||||||||||||||||||||||||||

| Home equity | 104 | 30 | 216 | 194 | 101 | 350 | 165 | ||||||||||||||||||||||||||||||||||

| Residential real estate | 1 | 2 | 136 | 0 | 5 | 139 | 15 | ||||||||||||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 2,459 | 3,335 | 3,487 | 2,646 | 3,436 | 9,281 | 8,613 | ||||||||||||||||||||||||||||||||||

| Premium finance receivables - life insurance | — | — | — | — | 41 | — | 54 | ||||||||||||||||||||||||||||||||||

| Consumer and other | 37 | 32 | 29 | 19 | 21 | 98 | 68 | ||||||||||||||||||||||||||||||||||

| Total recoveries | 4,291 | 5,155 | 4,809 | 3,806 | 4,283 | 14,255 | 11,144 | ||||||||||||||||||||||||||||||||||

| Net charge-offs | (24,555) | (13,340) | (12,640) | (15,925) | (26,735) | (50,535) | (78,471) | ||||||||||||||||||||||||||||||||||

| Allowance for credit losses at period end | $ | 454,586 | $ | 457,461 | $ | 448,387 | $ | 437,060 | $ | 436,193 | $ | 454,586 | $ | 436,193 | |||||||||||||||||||||||||||

| Annualized net charge-offs (recoveries) by category as a percentage of its own respective category’s average: | |||||||||||||||||||||||||||||||||||||||||

| Commercial | 0.49 | % | 0.11 | % | 0.23 | % | 0.11 | % | 0.61 | % | 0.28 | % | 0.41 | % | |||||||||||||||||||||||||||

| Commercial real estate | (0.00) | 0.17 | 0.01 | 0.03 | 0.00 | 0.06 | 0.23 | ||||||||||||||||||||||||||||||||||

| Home equity | (0.06) | 0.07 | (0.20) | (0.18) | (0.10) | (0.06) | (0.03) | ||||||||||||||||||||||||||||||||||

| Residential real estate | 0.00 | (0.00) | (0.02) | 0.01 | 0.00 | (0.00) | 0.00 | ||||||||||||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 0.20 | 0.16 | 0.20 | 0.59 | 0.24 | 0.19 | 0.30 | ||||||||||||||||||||||||||||||||||

| Premium finance receivables - life insurance | 0.00 | — | 0.00 | — | 0.00 | 0.00 | (0.00) | ||||||||||||||||||||||||||||||||||

| Consumer and other | 0.40 | 0.44 | 0.45 | 0.63 | 0.63 | 0.43 | 0.54 | ||||||||||||||||||||||||||||||||||

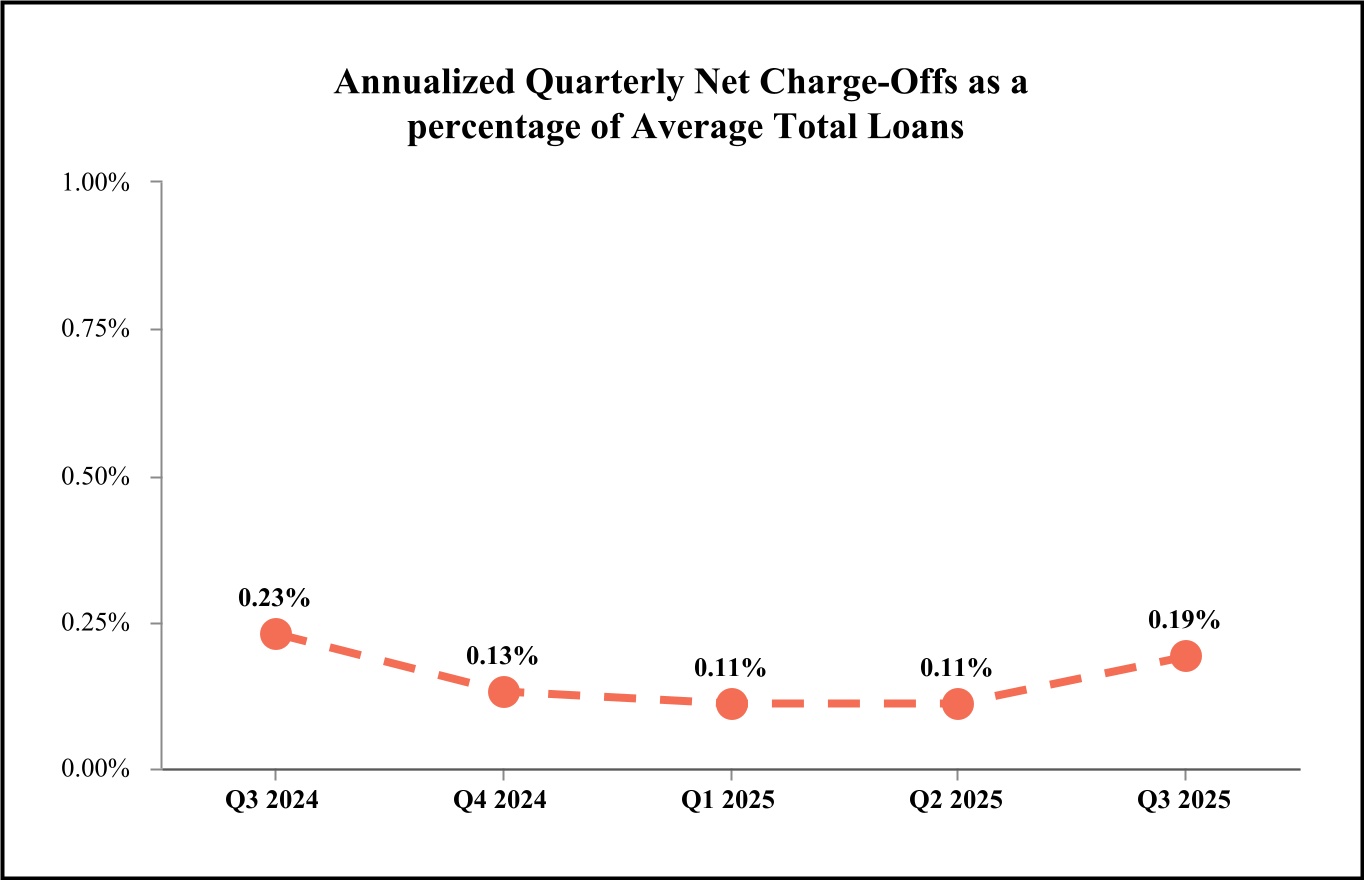

| Total loans, net of unearned income | 0.19 | % | 0.11 | % | 0.11 | % | 0.13 | % | 0.23 | % | 0.14 | 0.24 | % | ||||||||||||||||||||||||||||

| Loans at period end | $ | 52,063,482 | $ | 51,041,679 | $ | 48,708,390 | $ | 48,055,037 | $ | 47,067,447 | |||||||||||||||||||||||||||||||

| Allowance for loan losses as a percentage of loans at period end | 0.74 | % | 0.77 | % | 0.78 | % | 0.76 | % | 0.77 | % | |||||||||||||||||||||||||||||||

| Allowance for loan and unfunded lending-related commitment losses as a percentage of loans at period end | 0.87 | 0.90 | 0.92 | 0.91 | 0.93 | ||||||||||||||||||||||||||||||||||||

| Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | Sep 30, | Sep 30, | |||||||||||||||||||||||||||||||||||

| (In thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | 2025 | 2024 | ||||||||||||||||||||||||||||||||||

| Provision for loan losses - Other | $ | 19,610 | $ | 26,607 | $ | 26,826 | $ | 19,852 | $ | 6,782 | $ | 73,043 | $ | 78,052 | |||||||||||||||||||||||||||

| Provision for credit losses - Day 1 on non-PCD assets acquired during the period | — | — | — | — | 15,547 | — | 15,547 | ||||||||||||||||||||||||||||||||||

| Provision for unfunded lending-related commitments losses - Other | 2,160 | (4,325) | (2,852) | (2,851) | 17 | (5,017) | (9,663) | ||||||||||||||||||||||||||||||||||

| Provision for held-to-maturity securities losses | (2) | (48) | (11) | (22) | (12) | (61) | 132 | ||||||||||||||||||||||||||||||||||

| Provision for credit losses | $ | 21,768 | $ | 22,234 | $ | 23,963 | $ | 16,979 | $ | 22,334 | $ | 67,965 | $ | 84,068 | |||||||||||||||||||||||||||

| Allowance for loan losses | $ | 386,622 | $ | 391,654 | $ | 378,207 | $ | 364,017 | $ | 360,279 | |||||||||||||||||||||||||||||||

| Allowance for unfunded lending-related commitments losses | 67,569 | 65,409 | 69,734 | 72,586 | 75,435 | ||||||||||||||||||||||||||||||||||||

| Allowance for loan losses and unfunded lending-related commitments losses | 454,191 | 457,063 | 447,941 | 436,603 | 435,714 | ||||||||||||||||||||||||||||||||||||

| Allowance for held-to-maturity securities losses | 395 | 398 | 446 | 457 | 479 | ||||||||||||||||||||||||||||||||||||

| Allowance for credit losses | $ | 454,586 | $ | 457,461 | $ | 448,387 | $ | 437,060 | $ | 436,193 | |||||||||||||||||||||||||||||||

| As of Sep 30, 2025 | As of Jun 30, 2025 | As of Mar 31, 2025 | |||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | Recorded Investment |

Calculated Allowance |

% of its category’s balance |

Recorded Investment |

Calculated Allowance |

% of its category’s balance |

Recorded Investment |

Calculated Allowance |

% of its category’s balance |

||||||||||||||||||||||||||||||||||||||

| Commercial | $ | 16,544,342 | $ | 189,476 | 1.15 | % | $ | 16,387,431 | $ | 194,568 | 1.19 | % | $ | 15,931,326 | $ | 201,183 | 1.26 | % | |||||||||||||||||||||||||||||

| Commercial real estate: | |||||||||||||||||||||||||||||||||||||||||||||||

| Construction and development | 2,658,153 | 78,765 | 2.96 | 2,529,117 | 75,936 | 3.00 | 2,448,881 | 71,388 | 2.92 | ||||||||||||||||||||||||||||||||||||||

| Non-construction | 10,961,054 | 151,712 | 1.38 | 10,762,893 | 148,422 | 1.38 | 10,466,020 | 138,622 | 1.32 | ||||||||||||||||||||||||||||||||||||||

| Total commercial real estate | $ | 13,619,207 | $ | 230,477 | 1.69 | % | $ | 13,292,010 | $ | 224,358 | 1.69 | % | $ | 12,914,901 | $ | 210,010 | 1.63 | % | |||||||||||||||||||||||||||||

| Total commercial and commercial real estate | $ | 30,163,549 | $ | 419,953 | 1.39 | % | $ | 29,679,441 | $ | 418,926 | 1.41 | % | $ | 28,846,227 | $ | 411,193 | 1.43 | % | |||||||||||||||||||||||||||||

| Home equity | 484,202 | 9,229 | 1.91 | 466,815 | 9,221 | 1.98 | 455,683 | 9,139 | 2.01 | ||||||||||||||||||||||||||||||||||||||

| Residential real estate | 4,143,870 | 12,013 | 0.29 | 3,948,782 | 11,455 | 0.29 | 3,685,159 | 10,652 | 0.29 | ||||||||||||||||||||||||||||||||||||||

| Premium finance receivables | |||||||||||||||||||||||||||||||||||||||||||||||

| Property and casualty insurance | 8,366,292 | 11,187 | 0.13 | 8,323,176 | 15,872 | 0.19 | 7,239,862 | 15,310 | 0.21 | ||||||||||||||||||||||||||||||||||||||

| Life insurance | 8,758,553 | 762 | 0.01 | 8,506,960 | 740 | 0.01 | 8,365,140 | 729 | 0.01 | ||||||||||||||||||||||||||||||||||||||

| Consumer and other | 147,016 | 1,047 | 0.71 | 116,505 | 849 | 0.73 | 116,319 | 918 | 0.79 | ||||||||||||||||||||||||||||||||||||||

| Total loans, net of unearned income | $ | 52,063,482 | $ | 454,191 | 0.87 | % | $ | 51,041,679 | $ | 457,063 | 0.90 | % | $ | 48,708,390 | $ | 447,941 | 0.92 | % | |||||||||||||||||||||||||||||

Total core loans (1) |

$ | 30,610,433 | $ | 408,780 | 1.34 | % | $ | 29,928,663 | $ | 409,826 | 1.37 | % | $ | 29,108,500 | $ | 397,664 | 1.37 | % | |||||||||||||||||||||||||||||

Total niche loans (1) |

21,453,049 | 45,411 | 0.21 | 21,113,016 | 47,237 | 0.22 | 19,599,890 | 50,277 | 0.26 | ||||||||||||||||||||||||||||||||||||||

| (In thousands) | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | |||||||||||||||||||||||||||

| Loan Balances: | ||||||||||||||||||||||||||||||||

| Commercial | ||||||||||||||||||||||||||||||||

| Nonaccrual | $ | 66,577 | $ | 80,877 | $ | 70,560 | $ | 73,490 | $ | 63,826 | ||||||||||||||||||||||

| 90+ days and still accruing | — | — | 46 | 104 | 20 | |||||||||||||||||||||||||||

| 60-89 days past due | 12,190 | 34,855 | 15,243 | 54,844 | 32,560 | |||||||||||||||||||||||||||

| 30-59 days past due | 36,136 | 45,103 | 97,397 | 92,551 | 46,057 | |||||||||||||||||||||||||||

| Current | 16,429,439 | 16,226,596 | 15,748,080 | 15,353,562 | 15,105,230 | |||||||||||||||||||||||||||

| Total commercial | $ | 16,544,342 | $ | 16,387,431 | $ | 15,931,326 | $ | 15,574,551 | $ | 15,247,693 | ||||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||||||||||||||

| Nonaccrual | $ | 28,202 | $ | 32,828 | $ | 26,187 | $ | 21,042 | $ | 42,071 | ||||||||||||||||||||||

| 90+ days and still accruing | — | — | — | — | 225 | |||||||||||||||||||||||||||

| 60-89 days past due | 14,119 | 11,257 | 6,995 | 10,521 | 13,439 | |||||||||||||||||||||||||||

| 30-59 days past due | 83,055 | 51,173 | 83,653 | 30,766 | 48,346 | |||||||||||||||||||||||||||

| Current | 13,493,831 | 13,196,752 | 12,798,066 | 12,841,615 | 12,689,336 | |||||||||||||||||||||||||||

| Total commercial real estate | $ | 13,619,207 | $ | 13,292,010 | $ | 12,914,901 | $ | 12,903,944 | $ | 12,793,417 | ||||||||||||||||||||||

| Home equity | ||||||||||||||||||||||||||||||||

| Nonaccrual | $ | 1,295 | $ | 1,780 | $ | 2,070 | $ | 1,117 | $ | 1,122 | ||||||||||||||||||||||

| 90+ days and still accruing | — | — | — | — | — | |||||||||||||||||||||||||||

| 60-89 days past due | 246 | 138 | 984 | 1,233 | 1,035 | |||||||||||||||||||||||||||

| 30-59 days past due | 2,294 | 2,971 | 3,403 | 2,148 | 2,580 | |||||||||||||||||||||||||||

| Current | 480,367 | 461,926 | 449,226 | 440,530 | 422,306 | |||||||||||||||||||||||||||

| Total home equity | $ | 484,202 | $ | 466,815 | $ | 455,683 | $ | 445,028 | $ | 427,043 | ||||||||||||||||||||||

| Residential real estate | ||||||||||||||||||||||||||||||||

Early buy-out loans guaranteed by U.S. government agencies (1) |

$ | 124,824 | $ | 134,067 | $ | 123,742 | $ | 156,756 | $ | 135,389 | ||||||||||||||||||||||

| Nonaccrual | 28,942 | 28,047 | 22,522 | 23,762 | 17,959 | |||||||||||||||||||||||||||

| 90+ days and still accruing | — | — | — | — | — | |||||||||||||||||||||||||||

| 60-89 days past due | 8,829 | 8,954 | 1,351 | 5,708 | 6,364 | |||||||||||||||||||||||||||

| 30-59 days past due | 95 | 38 | 38,943 | 18,917 | 2,160 | |||||||||||||||||||||||||||

| Current | 3,981,180 | 3,777,676 | 3,498,601 | 3,407,622 | 3,226,166 | |||||||||||||||||||||||||||

| Total residential real estate | $ | 4,143,870 | $ | 3,948,782 | $ | 3,685,159 | $ | 3,612,765 | $ | 3,388,038 | ||||||||||||||||||||||

| Premium finance receivables - property & casualty | ||||||||||||||||||||||||||||||||

| Nonaccrual | $ | 24,512 | $ | 30,404 | $ | 29,846 | $ | 28,797 | $ | 36,079 | ||||||||||||||||||||||

| 90+ days and still accruing | 13,006 | 14,350 | 18,081 | 16,031 | 18,235 | |||||||||||||||||||||||||||

| 60-89 days past due | 23,527 | 25,641 | 19,717 | 19,042 | 18,740 | |||||||||||||||||||||||||||

| 30-59 days past due | 38,133 | 29,460 | 39,459 | 68,219 | 30,204 | |||||||||||||||||||||||||||

| Current | 8,267,114 | 8,223,321 | 7,132,759 | 7,139,953 | 7,028,423 | |||||||||||||||||||||||||||

| Total Premium finance receivables - property & casualty | $ | 8,366,292 | $ | 8,323,176 | $ | 7,239,862 | $ | 7,272,042 | $ | 7,131,681 | ||||||||||||||||||||||

| Premium finance receivables - life insurance | ||||||||||||||||||||||||||||||||

| Nonaccrual | $ | — | $ | — | $ | — | $ | 6,431 | $ | — | ||||||||||||||||||||||

| 90+ days and still accruing | — | 327 | 2,962 | — | — | |||||||||||||||||||||||||||

| 60-89 days past due | 34,016 | 11,202 | 10,587 | 72,963 | 10,902 | |||||||||||||||||||||||||||

| 30-59 days past due | 34,506 | 34,403 | 29,924 | 36,405 | 74,432 | |||||||||||||||||||||||||||

| Current | 8,690,031 | 8,461,028 | 8,321,667 | 8,031,346 | 7,911,565 | |||||||||||||||||||||||||||

| Total Premium finance receivables - life insurance | $ | 8,758,553 | $ | 8,506,960 | $ | 8,365,140 | $ | 8,147,145 | $ | 7,996,899 | ||||||||||||||||||||||

| Consumer and other | ||||||||||||||||||||||||||||||||

| Nonaccrual | $ | 38 | $ | 41 | $ | 18 | $ | 2 | $ | 2 | ||||||||||||||||||||||

| 90+ days and still accruing | 60 | 184 | 98 | 47 | 148 | |||||||||||||||||||||||||||

| 60-89 days past due | 49 | 61 | 162 | 59 | 22 | |||||||||||||||||||||||||||

| 30-59 days past due | 159 | 175 | 542 | 882 | 264 | |||||||||||||||||||||||||||

| Current | 146,710 | 116,044 | 115,499 | 98,572 | 82,240 | |||||||||||||||||||||||||||

| Total consumer and other | $ | 147,016 | $ | 116,505 | $ | 116,319 | $ | 99,562 | $ | 82,676 | ||||||||||||||||||||||

| Total loans, net of unearned income | ||||||||||||||||||||||||||||||||

Early buy-out loans guaranteed by U.S. government agencies (1) |

$ | 124,824 | $ | 134,067 | $ | 123,742 | $ | 156,756 | $ | 135,389 | ||||||||||||||||||||||

| Nonaccrual | 149,566 | 173,977 | 151,203 | 154,641 | 161,059 | |||||||||||||||||||||||||||

| 90+ days and still accruing | 13,066 | 14,861 | 21,187 | 16,182 | 18,628 | |||||||||||||||||||||||||||

| 60-89 days past due | 92,976 | 92,108 | 55,039 | 164,370 | 83,062 | |||||||||||||||||||||||||||

| 30-59 days past due | 194,378 | 163,323 | 293,321 | 249,888 | 204,043 | |||||||||||||||||||||||||||

| Current | 51,488,672 | 50,463,343 | 48,063,898 | 47,313,200 | 46,465,266 | |||||||||||||||||||||||||||

| Total loans, net of unearned income | $ | 52,063,482 | $ | 51,041,679 | $ | 48,708,390 | $ | 48,055,037 | $ | 47,067,447 | ||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | |||||||||||||||||||||||||

| (Dollars in thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | ||||||||||||||||||||||||

| Loans past due greater than 90 days and still accruing: | |||||||||||||||||||||||||||||

| Commercial | $ | — | $ | — | $ | 46 | $ | 104 | $ | 20 | |||||||||||||||||||

| Commercial real estate | — | — | — | — | 225 | ||||||||||||||||||||||||

| Home equity | — | — | — | — | — | ||||||||||||||||||||||||

| Residential real estate | — | — | — | — | — | ||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 13,006 | 14,350 | 18,081 | 16,031 | 18,235 | ||||||||||||||||||||||||

| Premium finance receivables - life insurance | — | 327 | 2,962 | — | — | ||||||||||||||||||||||||

| Consumer and other | 60 | 184 | 98 | 47 | 148 | ||||||||||||||||||||||||

| Total loans past due greater than 90 days and still accruing | 13,066 | 14,861 | 21,187 | 16,182 | 18,628 | ||||||||||||||||||||||||

| Non-accrual loans: | |||||||||||||||||||||||||||||

| Commercial | 66,577 | 80,877 | 70,560 | 73,490 | 63,826 | ||||||||||||||||||||||||

| Commercial real estate | 28,202 | 32,828 | 26,187 | 21,042 | 42,071 | ||||||||||||||||||||||||

| Home equity | 1,295 | 1,780 | 2,070 | 1,117 | 1,122 | ||||||||||||||||||||||||

| Residential real estate | 28,942 | 28,047 | 22,522 | 23,762 | 17,959 | ||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 24,512 | 30,404 | 29,846 | 28,797 | 36,079 | ||||||||||||||||||||||||

| Premium finance receivables - life insurance | — | — | — | 6,431 | — | ||||||||||||||||||||||||

| Consumer and other | 38 | 41 | 18 | 2 | 2 | ||||||||||||||||||||||||

| Total non-accrual loans | 149,566 | 173,977 | 151,203 | 154,641 | 161,059 | ||||||||||||||||||||||||

| Total non-performing loans: | |||||||||||||||||||||||||||||

| Commercial | 66,577 | 80,877 | 70,606 | 73,594 | 63,846 | ||||||||||||||||||||||||

| Commercial real estate | 28,202 | 32,828 | 26,187 | 21,042 | 42,296 | ||||||||||||||||||||||||

| Home equity | 1,295 | 1,780 | 2,070 | 1,117 | 1,122 | ||||||||||||||||||||||||

| Residential real estate | 28,942 | 28,047 | 22,522 | 23,762 | 17,959 | ||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 37,518 | 44,754 | 47,927 | 44,828 | 54,314 | ||||||||||||||||||||||||

| Premium finance receivables - life insurance | — | 327 | 2,962 | 6,431 | — | ||||||||||||||||||||||||

| Consumer and other | 98 | 225 | 116 | 49 | 150 | ||||||||||||||||||||||||

| Total non-performing loans | $ | 162,632 | $ | 188,838 | $ | 172,390 | $ | 170,823 | $ | 179,687 | |||||||||||||||||||

| Other real estate owned | 24,832 | 23,615 | 22,625 | 23,116 | 13,682 | ||||||||||||||||||||||||

| Total non-performing assets | $ | 187,464 | $ | 212,453 | $ | 195,015 | $ | 193,939 | $ | 193,369 | |||||||||||||||||||

| Total non-performing loans by category as a percent of its own respective category’s period-end balance: | |||||||||||||||||||||||||||||

| Commercial | 0.40 | % | 0.49 | % | 0.44 | % | 0.47 | % | 0.42 | % | |||||||||||||||||||

| Commercial real estate | 0.21 | 0.25 | 0.20 | 0.16 | 0.33 | ||||||||||||||||||||||||

| Home equity | 0.27 | 0.38 | 0.45 | 0.25 | 0.26 | ||||||||||||||||||||||||

| Residential real estate | 0.70 | 0.71 | 0.61 | 0.66 | 0.53 | ||||||||||||||||||||||||

| Premium finance receivables - property & casualty | 0.45 | 0.54 | 0.66 | 0.62 | 0.76 | ||||||||||||||||||||||||

| Premium finance receivables - life insurance | — | 0.00 | 0.04 | 0.08 | — | ||||||||||||||||||||||||

| Consumer and other | 0.07 | 0.19 | 0.10 | 0.05 | 0.18 | ||||||||||||||||||||||||

| Total loans, net of unearned income | 0.31 | % | 0.37 | % | 0.35 | % | 0.36 | % | 0.38 | % | |||||||||||||||||||

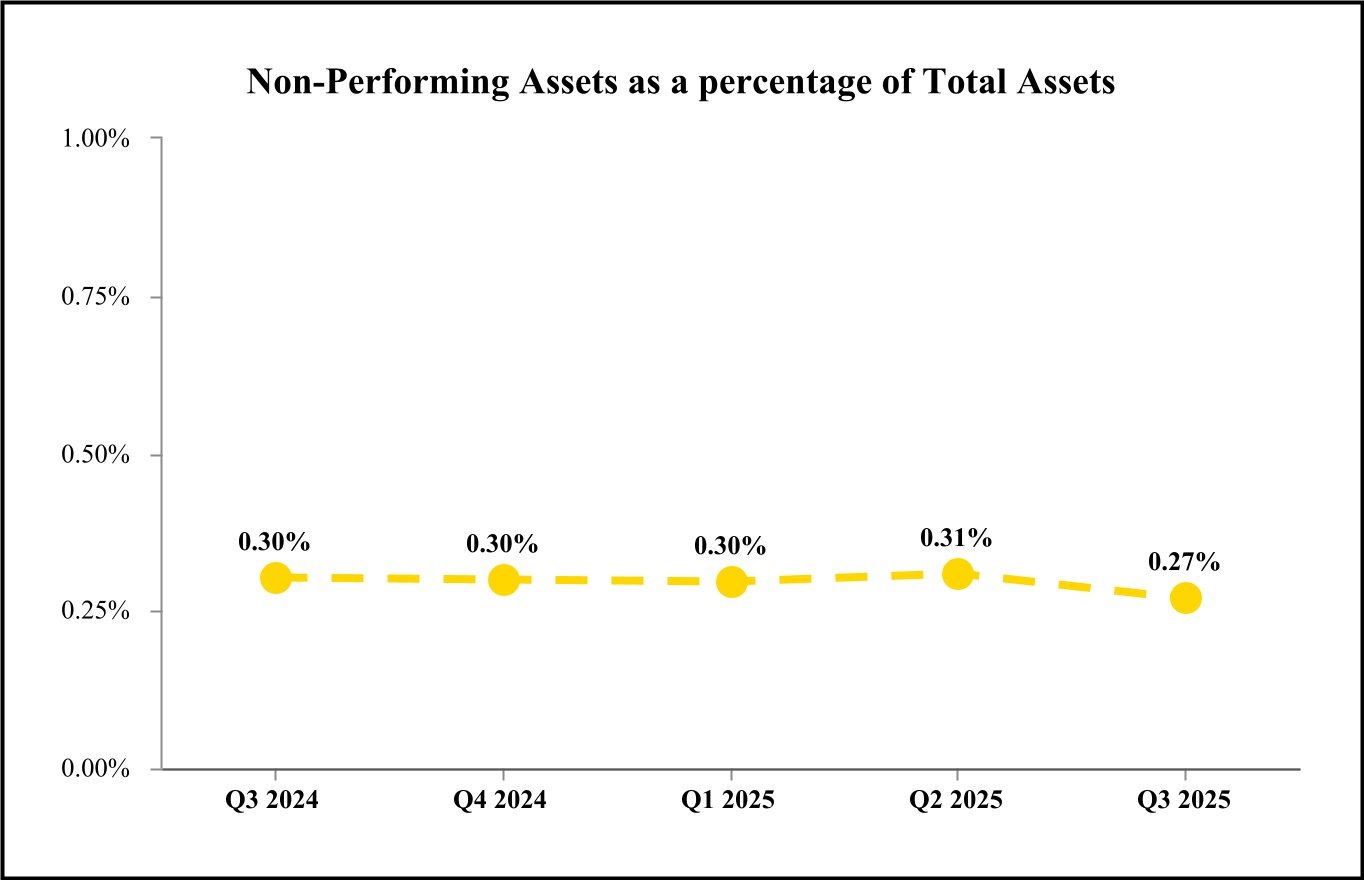

| Total non-performing assets as a percentage of total assets | 0.27 | % | 0.31 | % | 0.30 | % | 0.30 | % | 0.30 | % | |||||||||||||||||||

| Allowance for loan losses and unfunded lending-related commitments losses as a percentage of non-accrual loans | 303.67 | % | 262.71 | % | 296.25 | % | 282.33 | % | 270.53 | % | |||||||||||||||||||

| Three Months Ended | Nine Months Ended | |||||||||||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | Sep 30, | Sep 30, | ||||||||||||||||||||||||||||||||

| (In thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | 2025 | 2024 | |||||||||||||||||||||||||||||||

| Balance at beginning of period | $ | 188,838 | $ | 172,390 | $ | 170,823 | $ | 179,687 | $ | 174,251 | $ | 170,823 | $ | 139,030 | ||||||||||||||||||||||||

| Additions from becoming non-performing in the respective period | 34,805 | 48,651 | 27,721 | 30,931 | 42,335 | 111,177 | 119,853 | |||||||||||||||||||||||||||||||

| Additions from assets acquired in the respective period | — | — | — | — | 189 | — | 189 | |||||||||||||||||||||||||||||||

| Return to performing status | (3,399) | (6,896) | (1,207) | (1,108) | (362) | (11,502) | (1,764) | |||||||||||||||||||||||||||||||

| Payments received | (28,052) | (5,602) | (15,965) | (12,219) | (10,894) | (49,619) | (28,841) | |||||||||||||||||||||||||||||||

| Transfer to OREO or other assets | (348) | (2,247) | — | (17,897) | (3,680) | (2,595) | (12,006) | |||||||||||||||||||||||||||||||

| Charge-offs, net | (21,526) | (11,734) | (8,600) | (5,612) | (21,211) | (41,860) | (43,694) | |||||||||||||||||||||||||||||||

| Net change for premium finance receivables | (7,686) | (5,724) | (382) | (2,959) | (941) | (13,792) | 6,920 | |||||||||||||||||||||||||||||||

| Balance at end of period | $ | 162,632 | $ | 188,838 | $ | 172,390 | $ | 170,823 | $ | 179,687 | $ | 162,632 | $ | 179,687 | ||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | |||||||||||||||||||||||||

| (In thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | ||||||||||||||||||||||||

| Balance at beginning of period | $ | 23,615 | $ | 22,625 | $ | 23,116 | $ | 13,682 | $ | 19,731 | |||||||||||||||||||

| Disposals/resolved | — | — | — | (8,545) | (9,729) | ||||||||||||||||||||||||

| Transfers in at fair value, less costs to sell | 1,217 | 1,315 | — | 17,979 | 3,680 | ||||||||||||||||||||||||

| Fair value adjustments | — | (325) | (491) | — | — | ||||||||||||||||||||||||

| Balance at end of period | $ | 24,832 | $ | 23,615 | $ | 22,625 | $ | 23,116 | $ | 13,682 | |||||||||||||||||||

| Period End | |||||||||||||||||||||||||||||

| (In thousands) | Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | ||||||||||||||||||||||||

| Balance by Property Type: | 2025 | 2025 | 2025 | 2024 | 2024 | ||||||||||||||||||||||||

| Residential real estate | $ | — | $ | — | $ | — | $ | — | $ | — | |||||||||||||||||||

| Commercial real estate | 24,832 | 23,615 | 22,625 | 23,116 | 13,682 | ||||||||||||||||||||||||

| Total | $ | 24,832 | $ | 23,615 | $ | 22,625 | $ | 23,116 | $ | 13,682 | |||||||||||||||||||

| Three Months Ended |

Q3 2025 compared to

Q2 2025

|

Q3 2025 compared to

Q3 2024

|

|||||||||||||||||||||||||||||||||||||||||||||

| Sep 30, | Jun 30, | Mar 31, | Dec 31, | Sep 30, | |||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | 2025 | 2025 | 2025 | 2024 | 2024 | $ Change | % Change | $ Change | % Change | ||||||||||||||||||||||||||||||||||||||

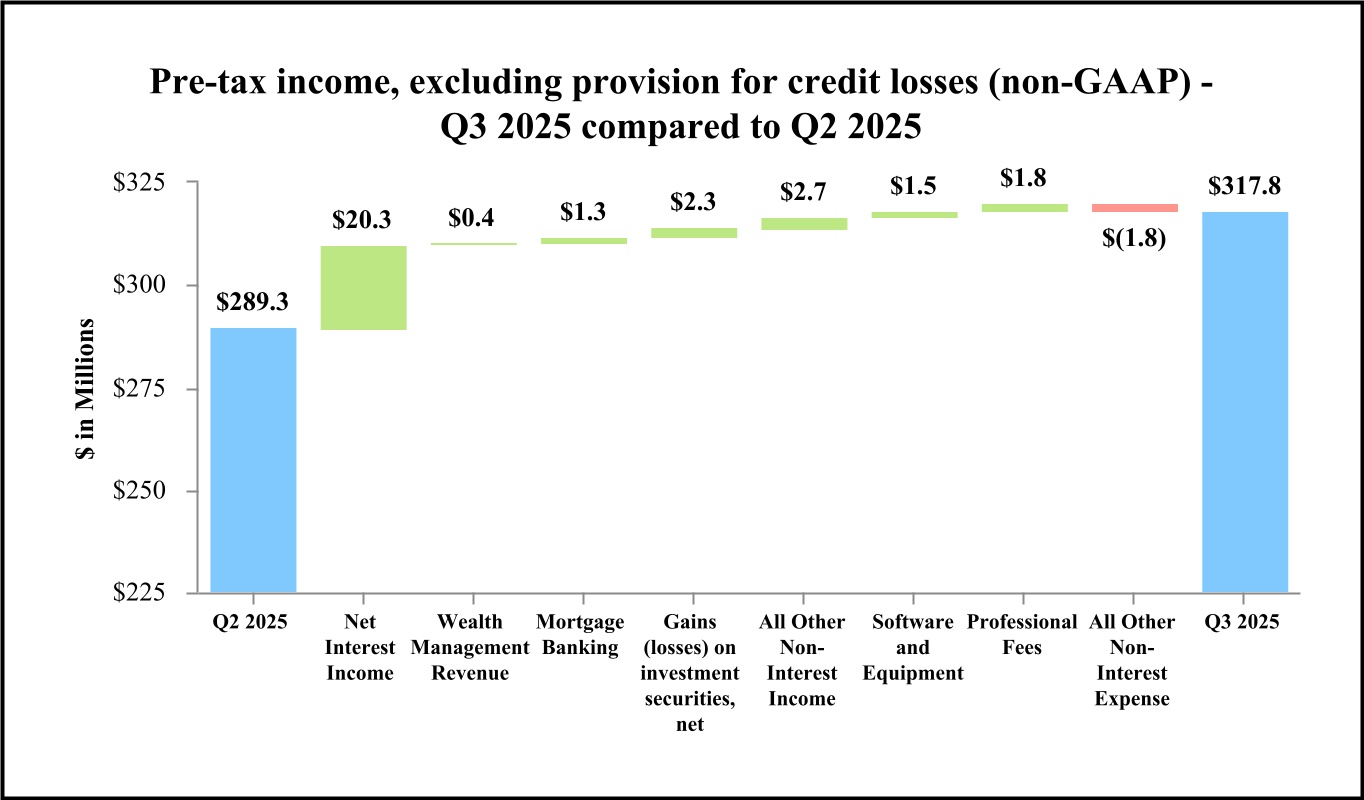

| Brokerage | $ | 4,426 | $ | 4,212 | $ | 4,757 | $ | 5,328 | $ | 6,139 | $ | 214 | 5 | % | $ | (1,713) | (28) | % | |||||||||||||||||||||||||||||

| Trust and asset management | 32,762 | 32,609 | 29,285 | 33,447 | 31,085 | 153 | 0 | 1,677 | 5 | ||||||||||||||||||||||||||||||||||||||

| Total wealth management | 37,188 | 36,821 | 34,042 | 38,775 | 37,224 | 367 | 1 | (36) | 0 | ||||||||||||||||||||||||||||||||||||||

| Mortgage banking | 24,451 | 23,170 | 20,529 | 20,452 | 15,974 | 1,281 | 6 | 8,477 | 53 | ||||||||||||||||||||||||||||||||||||||

| Service charges on deposit accounts | 19,825 | 19,502 | 19,362 | 18,864 | 16,430 | 323 | 2 | 3,395 | 21 | ||||||||||||||||||||||||||||||||||||||

| Gains (losses) on investment securities, net | 2,972 | 650 | 3,196 | (2,835) | 3,189 | 2,322 | NM | (217) | (7) | ||||||||||||||||||||||||||||||||||||||

| Fees from covered call options | 5,619 | 5,624 | 3,446 | 2,305 | 988 | (5) | 0 | 4,631 | NM | ||||||||||||||||||||||||||||||||||||||

| Trading gains (losses), net | 172 | 151 | (64) | (113) | (130) | 21 | 14 | 302 | NM | ||||||||||||||||||||||||||||||||||||||

| Operating lease income, net | 15,466 | 15,166 | 15,287 | 15,327 | 15,335 | 300 | 2 | 131 | 1 | ||||||||||||||||||||||||||||||||||||||

| Other: | |||||||||||||||||||||||||||||||||||||||||||||||

| Interest rate swap fees | 3,909 | 3,010 | 2,269 | 3,360 | 2,914 | 899 | 30 | 995 | 34 | ||||||||||||||||||||||||||||||||||||||

| BOLI | 1,591 | 2,257 | 796 | 1,236 | 1,517 | (666) | (30) | 74 | 5 | ||||||||||||||||||||||||||||||||||||||

| Administrative services | 1,240 | 1,315 | 1,393 | 1,347 | 1,450 | (75) | (6) | (210) | (14) | ||||||||||||||||||||||||||||||||||||||

| Foreign currency remeasurement (losses) gains | (416) | 658 | (183) | (682) | 696 | (1,074) | NM | (1,112) | NM | ||||||||||||||||||||||||||||||||||||||

| Changes in fair value on EBOs and loans held-for-investment | 1,452 | 172 | 383 | 129 | 518 | 1,280 | NM | 934 | NM | ||||||||||||||||||||||||||||||||||||||

| Early pay-offs of capital leases | 519 | 400 | 768 | 514 | 532 | 119 | 30 | (13) | (2) | ||||||||||||||||||||||||||||||||||||||

| Miscellaneous | 16,839 | 15,193 | 15,410 | 14,772 | 16,510 | 1,646 | 11 | 329 | 2 | ||||||||||||||||||||||||||||||||||||||

| Total Other | 25,134 | 23,005 | 20,836 | 20,676 | 24,137 | 2,129 | 9 | 997 | 4 | ||||||||||||||||||||||||||||||||||||||

| Total Non-Interest Income | $ | 130,827 | $ | 124,089 | $ | 116,634 | $ | 113,451 | $ | 113,147 | $ | 6,738 | 5 | % | $ | 17,680 | 16 | % | |||||||||||||||||||||||||||||

| Nine Months Ended | Q3 2025 compared to Q3 2024 |

|||||||||||||||||||

| Sep 30, | Sep 30, | |||||||||||||||||||

| (Dollars in thousands) | 2025 | 2024 | $ Change | % Change | ||||||||||||||||

| Brokerage | $ | 13,395 | $ | 17,283 | $ | (3,888) | (22) | % | ||||||||||||

| Trust and asset management | 94,656 | 90,169 | 4,487 | 5 | ||||||||||||||||

| Total wealth management | 108,051 | 107,452 | 599 | 1 | ||||||||||||||||

| Mortgage banking | 68,150 | 72,761 | (4,611) | (6) | ||||||||||||||||

| Service charges on deposit accounts | 58,689 | 46,787 | 11,902 | 25 | ||||||||||||||||

| Gains on investment securities, net | 6,818 | 233 | 6,585 | NM | ||||||||||||||||

| Fees from covered call options | 14,689 | 7,891 | 6,798 | 86 | ||||||||||||||||

| Trading gains, net | 259 | 617 | (358) | (58) | ||||||||||||||||

| Operating lease income, net | 45,919 | 43,383 | 2,536 | 6 | ||||||||||||||||

| Other: | ||||||||||||||||||||

| Interest rate swap fees | 9,188 | 9,134 | 54 | 1 | ||||||||||||||||

| BOLI | 4,644 | 4,519 | 125 | 3 | ||||||||||||||||

| Administrative services | 3,948 | 3,989 | (41) | (1) | ||||||||||||||||

| Foreign currency remeasurement gains (losses) | 59 | (620) | 679 | NM | ||||||||||||||||

| Changes in fair value on EBOs and loans held-for-investment | 2,007 | 683 | 1,324 | NM | ||||||||||||||||

| Early pay-offs of capital leases | 1,687 | 1,355 | 332 | 25 | ||||||||||||||||

| Miscellaneous | 47,442 | 76,690 | (29,248) | (38) | ||||||||||||||||

| Total Other | 68,975 | 95,750 | (26,775) | (28) | ||||||||||||||||

| Total Non-Interest Income | $ | 371,550 | $ | 374,874 | $ | (3,324) | (1) | % | ||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| (Dollars in thousands) | Sep 30, 2025 |

Jun 30, 2025 |

Mar 31, 2025 |

Dec 31, 2024 |

Sep 30, 2024 |

||||||||||||||||||||||||

| Originations: | |||||||||||||||||||||||||||||

| Retail originations | $ | 505,793 | $ | 523,759 | $ | 348,468 | $ | 483,424 | $ | 527,408 | |||||||||||||||||||

| Veterans First originations | 137,600 | 157,787 | 111,985 | 176,914 | 239,369 | ||||||||||||||||||||||||

| Total originations for sale (A) | $ | 643,393 | $ | 681,546 | $ | 460,453 | $ | 660,338 | $ | 766,777 | |||||||||||||||||||

| Originations for investment | 351,012 | 422,926 | 217,177 | 355,119 | 218,984 | ||||||||||||||||||||||||

| Total originations | $ | 994,405 | $ | 1,104,472 | $ | 677,630 | $ | 1,015,457 | $ | 985,761 | |||||||||||||||||||

| As a percentage of originations for sale: | |||||||||||||||||||||||||||||