UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

OR

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to _______

Commission File Number 1-37816

ALCOA CORPORATION

(Exact name of registrant as specified in its charter)

|

Delaware (State or other jurisdiction of incorporation or organization) |

|

81-1789115 (I.R.S. Employer Identification No.) |

|

|

|

|

201 Isabella Street, Suite 500, Pittsburgh, Pennsylvania (Address of principal executive offices) |

|

15212-5858 (Zip Code) |

(Registrant’s telephone number, including area code): 412-315-2900

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common Stock, par value $0.01 per share |

|

AA |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☒ |

|

Accelerated filer |

☐ |

Non-accelerated filer |

☐ |

|

Smaller reporting company |

☐ |

Emerging growth company |

☐ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of the registrant’s voting stock held by non-affiliates at June 28, 2024 was approximately $7.1 billion, based on the closing price per share of Common Stock on June 28, 2024 of $39.78 as reported on the New York Stock Exchange.

Indicate the number of shares outstanding of each of the registrant’s classes of stock, as of the latest practicable date.

Title or Class |

|

Outstanding Shares as of February 14, 2025 |

Common Stock, par value $0.01 per share |

|

258,884,337 |

Series A Convertible Preferred Stock, par value $0.01 per share |

|

4,041,989 |

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference certain information from the registrant’s Definitive Proxy Statement for its 2025 Annual Meeting of Stockholders to be filed pursuant to Regulation 14A.

TABLE OF CONTENTS

|

|

|

Page |

|

|

|

|

Item 1. |

|

1 |

|

Item 1A. |

|

16 |

|

Item 1B. |

|

30 |

|

Item 1C. |

|

31 |

|

Item 2. |

|

32 |

|

Item 3. |

|

45 |

|

Item 4. |

|

46 |

|

|

|

|

|

Item 5. |

|

47 |

|

Item 6. |

|

48 |

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

49 |

Item 7A. |

|

71 |

|

Item 8. |

|

72 |

|

Item 9. |

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

135 |

Item 9A. |

|

135 |

|

Item 9B. |

|

135 |

|

Item 9C. |

|

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

135 |

|

|

|

|

Item 10. |

|

135 |

|

Item 11. |

|

136 |

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

136 |

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

136 |

Item 14. |

|

136 |

|

|

|

|

|

Item 15. |

|

137 |

|

Item 16. |

|

140 |

|

|

|

141 |

Note on Incorporation by Reference

In this Form 10-K, selected items of information and data are incorporated by reference to portions of Alcoa Corporation’s Definitive Proxy Statement for its 2025 Annual Meeting of Stockholders (Proxy Statement), which will be filed with the Securities and Exchange Commission within 120 days after the end of Alcoa Corporation’s fiscal year ended December 31, 2024. Unless otherwise provided herein, any reference in this Form 10-K to disclosures in the Proxy Statement shall constitute incorporation by reference of only that specific disclosure into this Form 10-K.

PART I

Item 1. Business.

(dollars in millions, except per-share amounts, average realized prices, and average cost amounts)

The Company

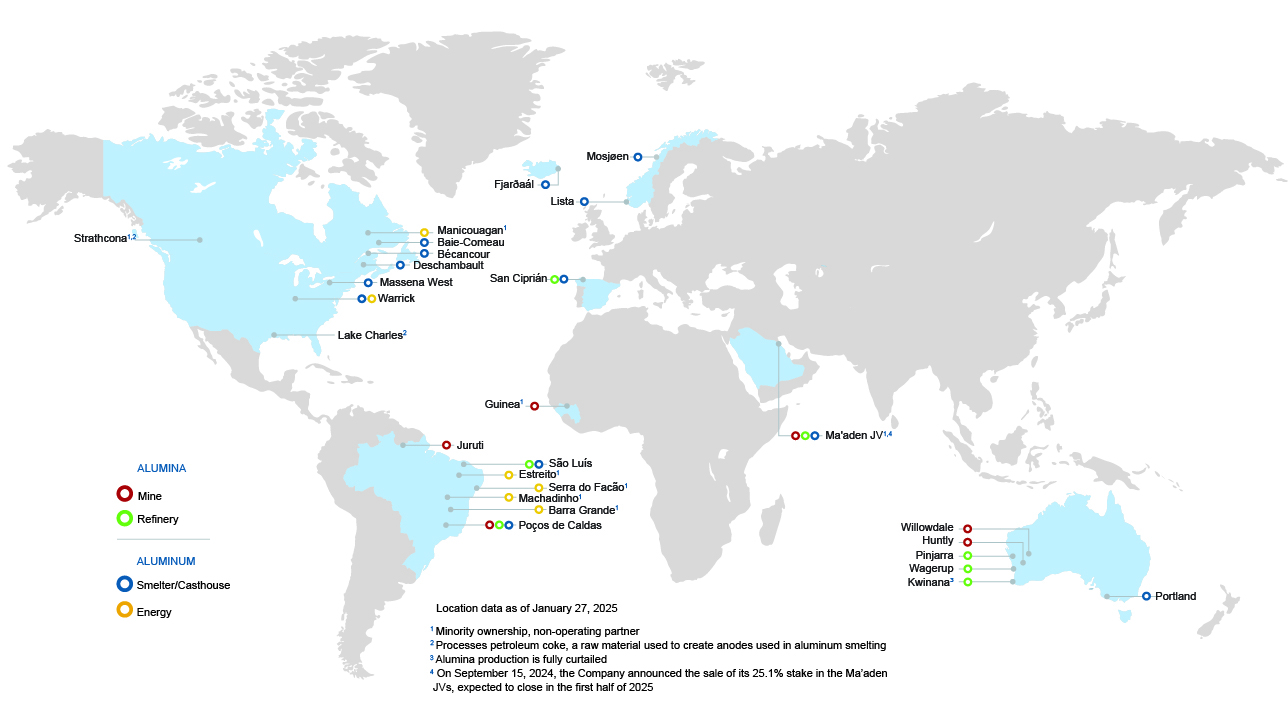

Alcoa Corporation, a Delaware corporation (Alcoa or the Company), is active in all aspects of the upstream aluminum industry with bauxite mining, alumina refining, and aluminum smelting and casting. The Company has direct and indirect ownership of 26 operating locations across nine countries on six continents.

The Company’s operations are comprised of two reportable business segments: Alumina and Aluminum. The Alumina segment primarily consists of the Company’s bauxite mines and alumina refineries, which generally includes the mining of bauxite and other aluminous ores, as well as the refining, production, and sale of smelter grade and non-metallurgical alumina. The Aluminum segment consists of the Company’s aluminum smelting and casting operations along with most of the Company’s energy production assets.

On August 1, 2024, Alcoa completed the acquisition of Alumina Limited, which primarily consisted of the acquisition of Alumina Limited’s noncontrolling interest in the Alcoa World Alumina and Chemicals (AWAC) joint venture (described below). Prior to the acquisition, the Alumina segment primarily consisted of a series of affiliated operating entities held in AWAC. Upon completion of the acquisition by Alcoa, Alumina Limited and, as a result, the operations held by the AWAC joint venture, became wholly-owned by Alcoa Corporation.

Aluminum, as an element, is abundant in the earth’s crust, but a multi-step process is required to manufacture finished aluminum metal. Aluminum metal is produced by refining alumina oxide from bauxite into alumina, which is then smelted into aluminum and can be cast into many shapes and forms.

Alcoa smelts and casts aluminum in various shapes and sizes for global customers, including developing and creating various alloy combinations for specific applications.

Aluminum metal is a commodity traded on the London Metal Exchange (LME) and priced daily. Additionally, alumina is subject to market pricing through the Alumina Price Index (API), which is calculated by the Company based on the weighted average of a prior month’s daily spot prices published by the following three indices: CRU Metallurgical Grade Alumina Price, Platts Metals Daily Alumina PAX Price, and FastMarkets Metal Bulletin Non-Ferrous Metals Alumina Index. As a result, the prices of both aluminum and alumina are subject to significant volatility and, therefore, influence the operating results of Alcoa.

Alcoa Corporation became an independent, publicly traded company on November 1, 2016, following its separation (the Separation Transaction) from its former parent company, Alcoa Inc. References herein to “ParentCo” refer to Alcoa Inc. and its consolidated subsidiaries through October 31, 2016, at which time it was renamed Arconic Inc. and since has been subsequently renamed Howmet Aerospace Inc.

1

Business Strategy

Alcoa's business strategy is designed to create stockholder value while aligning with our purpose, vision, and values.

Over the past five years, the Company has made significant progress in reducing complexity and optimizing its portfolio of mining, refining, and smelting assets. In 2024, Alcoa safely curtailed the Kwinana alumina refinery in Australia, acquired Alumina Limited and subsequently benefited from the increased alumina exposure, and announced the sale of its 25.1% ownership in the Saudi Arabia joint venture. In the near term, Alcoa will focus on maintaining operational stability while strategically managing its portfolio to maximize profitability and value creation, including advancing Australia mine approvals, improving the long-term outlook for the San Ciprián operations (Spain), and completing the Alumar smelter (Brazil) restart while maintaining operational stability.

To strengthen our competitive position, Alcoa has identified priorities that address both immediate and long-term opportunities:

Achieving Safety Performance and Operational Excellence

Building a High-Performance Culture

Disciplined Capital Allocation

Targeted Growth

With an emphasis on safety, operational excellence, and continuous improvement, Alcoa’s portfolio of assets is well positioned to deliver stockholder value across business cycles. By following disciplined capital allocation and making pragmatic growth investments, the Company is prepared to adapt and thrive in an evolving industry landscape.

See Part II Item 7 of this Form 10-K in Management’s Discussion and Analysis of Financial Condition and Results of Operations under caption Business Update for more information.

2

Joint Ventures

Saudi Arabia Joint Venture

In December 2009, Alcoa entered into a joint venture with the Saudi Arabian Mining Company (Ma’aden), which was formed by the government of Saudi Arabia to develop its mineral resources and create a fully integrated aluminum complex in Saudi Arabia. Ma’aden is listed on the Saudi Stock Exchange (Tadawul). The joint venture complex includes a bauxite mine with estimated capacity of 5 million dry metric tons per year; an alumina refinery with a capacity of 1.8 million metric tons per year (mtpy); and an aluminum smelter with a capacity of 804,000 mtpy.

The joint venture is currently comprised of two entities: the Ma’aden Bauxite and Alumina Company (MBAC) and the Ma’aden Aluminium Company (MAC). Ma’aden owns a 74.9% interest in the joint venture. Alcoa owns a 25.1% interest in MAC, which holds the smelter; AWAC, which became wholly-owned by Alcoa upon its completion of the Alumina Limited acquisition, holds a 25.1% interest in MBAC, which holds the mine and refinery. The refinery and smelter are located within the Ras Al Khair industrial zone on the east coast of Saudi Arabia.

On September 15, 2024, Alcoa entered into a share purchase and subscription agreement with Ma’aden, pursuant to which Alcoa agreed to sell its full ownership interest of 25.1% in the Saudi Arabia joint venture, comprised of MBAC and MAC, to Ma’aden in exchange for issuance by Ma’aden of approximately 86 million shares and $150 in cash. The shares of Ma’aden will be subject to transfer and sale restrictions, including a restriction requiring Alcoa to hold its Ma’aden shares for a minimum of three years, with one-third of the shares becoming transferable after each of the third, fourth, and fifth anniversaries of closing of the transaction. The transaction is subject to regulatory approvals, approval by Ma’aden’s shareholders, and other customary closing conditions and is expected to close in the first half of 2025.

ELYSIS

ELYSISTM Limited Partnership (ELYSIS) is between wholly-owned subsidiaries of Alcoa (48.235%) and Rio Tinto Alcan Inc. (Rio Tinto) (48.235%), respectively, and Investissement Québec (3.53%), a company wholly-owned by the Government of Québec, Canada. The purpose of ELYSIS is to advance larger scale development and commercialization of its patent-protected technology that eliminates direct greenhouse gas emissions from the traditional aluminum smelting process and, instead, emits oxygen. Alcoa first developed the inert anode technology for the aluminum smelting process that served as the basis for the formation of ELYSIS in 2018. Development scale quantities of aluminum produced by ELYSIS have been sold for commercial purposes, including to Ball Corporation for its low-carbon aluminum cup launched at the World Economic Forum in Davos, Switzerland and to Nexans, producing the world’s first cable containing metal from this breakthrough technology. Further progress on ELYSIS technology was announced in 2024 with Rio Tinto’s plans to launch the first industrial-scale demonstration of the breakthrough technology, which includes 10 ELYSIS smelting pots operating at 100 kiloamperes (kA), a size similar to those operating at smaller-scale commercial smelters. Alcoa has the right to purchase up to 40 percent of the metal produced from the demonstration, allowing for Alcoa customers to benefit from ELYSIS’s carbon-free electrolytic process early in the technology development cycle. The target for first production is by 2027.

Alcoa World Alumina and Chemicals (AWAC)

On August 1, 2024, Alcoa completed the acquisition of all of the ordinary shares of Alumina Limited (Alumina Shares) through a wholly-owned subsidiary, AAC Investments Australia 2 Pty Ltd. At acquisition, Alumina Limited, a company previously listed on the Australian Securities Exchange, held a 40% ownership interest in the AWAC joint venture.

Under the Scheme Implementation Deed entered into in March 2024, as amended in May 2024, holders of Alumina Shares received 0.02854 Alcoa CHESS Depositary Interests (CDIs) for each Alumina Share (the Agreed Ratio), except that i) holders of Alumina Shares represented by American Depositary Shares, each of which represented 4 Alumina Shares, received 0.02854 shares of Alcoa common stock and ii) a certain shareholder received, for certain of their Alumina Shares, 0.02854 shares of Alcoa non-voting convertible preferred stock. The Alcoa CDIs are quoted on the Australian Stock Exchange.

At closing, Alumina Shares outstanding of 2,760,056,014 and 141,625,403 were exchanged for 78,772,422 and 4,041,989 shares of Alcoa common stock and Alcoa preferred stock, respectively. Based on Alcoa’s closing share price as of July 31, 2024, the Agreed Ratio implied a value of A$1.45 per Alumina Share and aggregate purchase consideration of approximately $2,700 for Alumina Limited.

3

The transaction consisted in substance of the acquisition of Alumina Limited’s noncontrolling interest in AWAC, the assumption of Alumina Limited’s indebtedness, the recognition of deferred tax assets primarily related to Alumina Limited’s prior net operating losses and the tax allocation of the fixed asset valuation to individual assets, and the acquisition of cash and other current liabilities. The transaction was accounted for as an equity transaction where net assets acquired and transaction costs were reflected as an increase to Additional capital.

Prior to Alcoa’s acquisition of Alumina Limited, Alcoa Corporation and Alumina Limited owned 60% and 40%, respectively, of AWAC, an unincorporated global joint venture consisting of a number of affiliated entities that own, operate, or have an interest in bauxite mines and alumina refineries, as well as an aluminum smelter, in seven countries. The scope of AWAC generally includes the mining of bauxite and other aluminous ores; the refining, production, and sale of smelter grade and non-metallurgical alumina; and the production of certain primary aluminum products. Upon completion of the acquisition on August 1, 2024, Alumina Limited and, as a result, the operations held by the AWAC joint venture, became wholly-owned by Alcoa Corporation.

AWAC Operations

In 2024, AWAC entities’ assets included the following interests:

Others

The Company is party to several other joint ventures and consortia. See additional details within each business segment discussion below.

The Aluminerie de Bécancour Inc. (ABI) smelter is a joint venture between Alcoa and Rio Tinto located in Bécancour, Québec. Alcoa owns 74.95% of the joint venture through its 50% equity investment in Pechiney Reynolds Quebec, Inc., which owns a 50.1% share of the smelter, and two wholly-owned Canadian subsidiaries, which own 49.9% of the smelter. Rio Tinto owns the remaining 25.05% interest in the joint venture through its 50% ownership in Pechiney Reynolds Quebec, Inc.

CBG is a joint venture between Boké Investment Company (51%) and the Government of Guinea (49%) for the operation of a bauxite mine in the Boké region of Guinea. Boké Investment Company is owned 100% by Halco (Mining) Inc.; Alcoa World Alumina LLC (AWA LLC) holds a 45% interest in Halco (Mining) Inc. AWA LLC is part of the AWAC group of companies, which became wholly-owned by Alcoa upon its completion of the Alumina Limited acquisition.

On April 30, 2022, Alcoa completed the sale of its investment in Mineração Rio Do Norte (MRN) for proceeds of $10. An additional $30 in cash could be paid to the Company in the future if certain post-closing conditions related to future MRN mine development are satisfied. Related to this transaction, the Company recorded an asset impairment of $58 in the first quarter of 2022 in Restructuring and other charges, net on the Statement of Consolidated Operations. In addition, the Company entered into several bauxite offtake agreements with South32 Minerals S.A. (South32) to provide bauxite supply for existing long-term supply contracts.

Alumar is an unincorporated joint venture for the operation of a refinery, smelter, and casthouse in Brazil. The refinery is owned by AWAB (39.96%), Rio Tinto (10%), Alcoa Alumínio (14.04%), and South32 (36%). AWAB is part of the AWAC group of companies, which became wholly-owned by Alcoa upon its completion of the Alumina Limited acquisition. With respect to Rio Tinto and South32, the named company or an affiliate thereof holds the interest. The smelter and casthouse are owned by Alcoa Alumínio (60%) and South32 (40%).

4

Strathcona calciner is a joint venture between affiliates of Alcoa and Rio Tinto located in Alberta, Canada. Calcined coke is used as a raw material in aluminum smelting. The calciner is owned by Alcoa (39%) and Rio Tinto (61%).

Hydropower

Machadinho Hydro Power Plant (HPP) is a consortium located on the Pelotas River in southern Brazil in which the Company has a 27.3% ownership interest through Alcoa Alumínio. The remaining ownership interests are held by unrelated third parties.

Barra Grande HPP is a joint venture located on the Pelotas River in southern Brazil in which the Company has a 42.2% ownership interest through Alcoa Alumínio. The remaining ownership interests are held by unrelated third parties.

Estreito HPP is a consortium between Alcoa Alumínio, through Estreito Energia S.A. (25.5%) and unrelated third parties located on the Tocantins River, northern Brazil.

Serra do Facão HPP is a joint venture between Alcoa Alumínio (35%) and unrelated third parties located on the Sao Marcos River, central Brazil.

Manicouagan Power Limited Partnership (Manicouagan) is a joint venture between affiliates of Alcoa and Hydro-Québec. Manicouagan owns and operates the 335 megawatt McCormick hydroelectric project, which is located on the Manicouagan River in the Province of Québec, Canada. Alcoa owns 40% of the joint venture.

Alumina

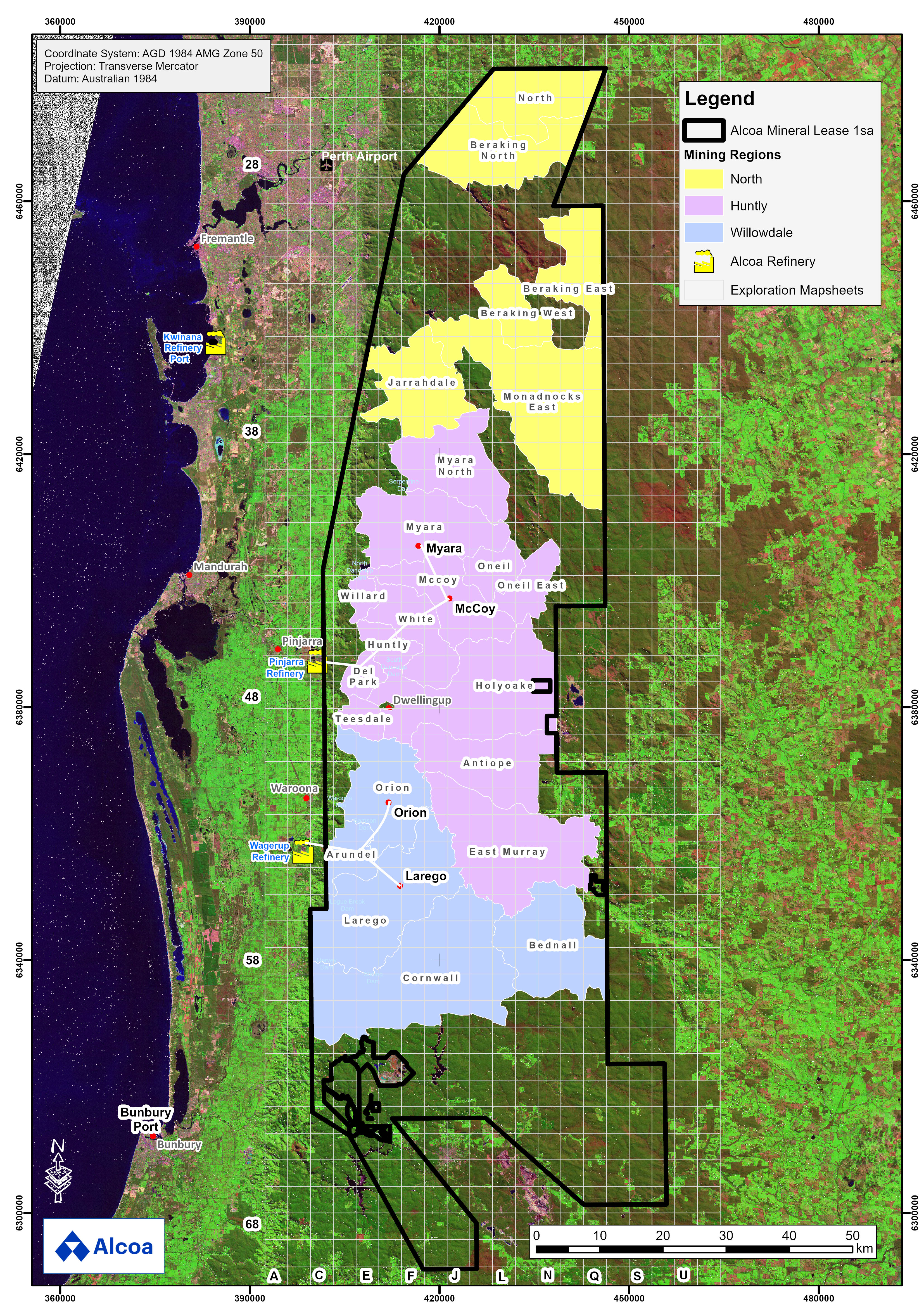

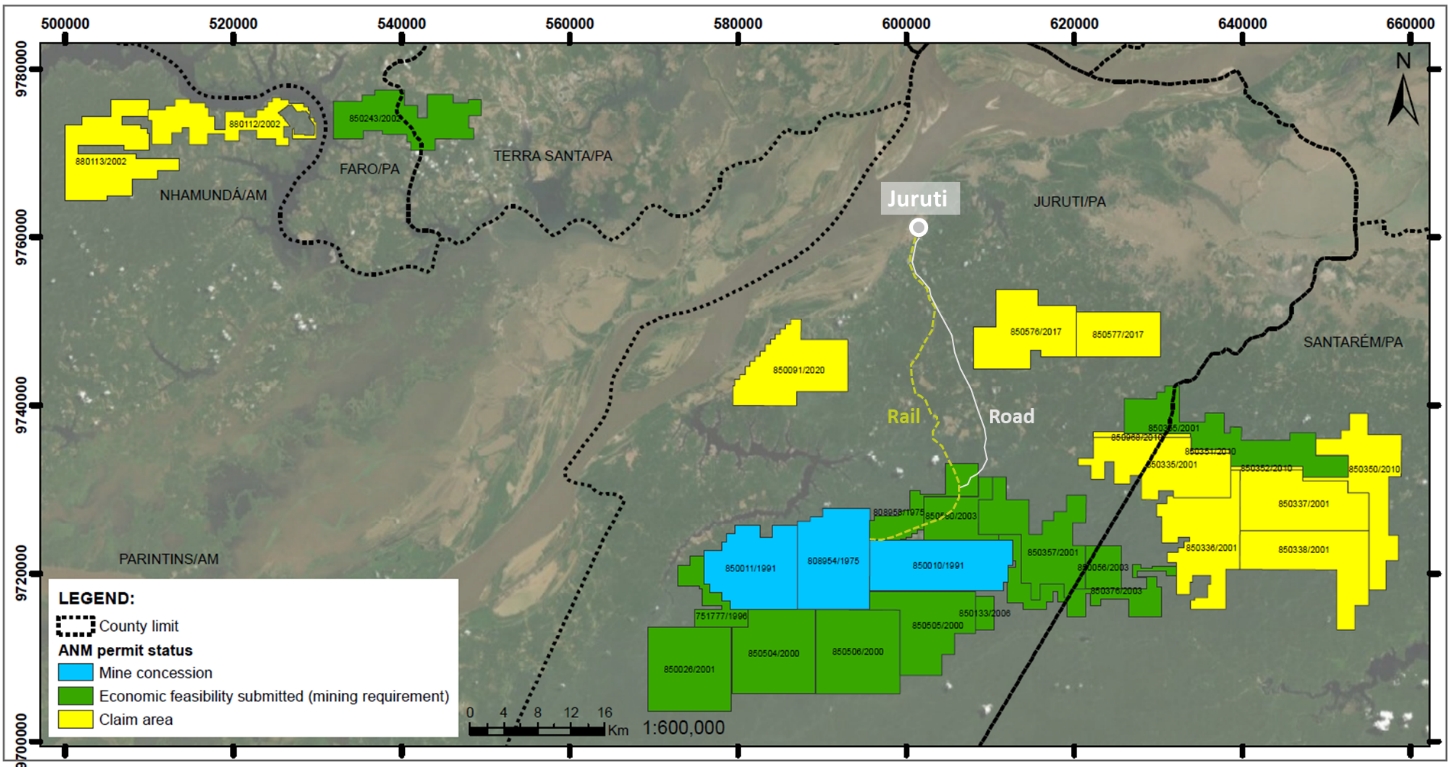

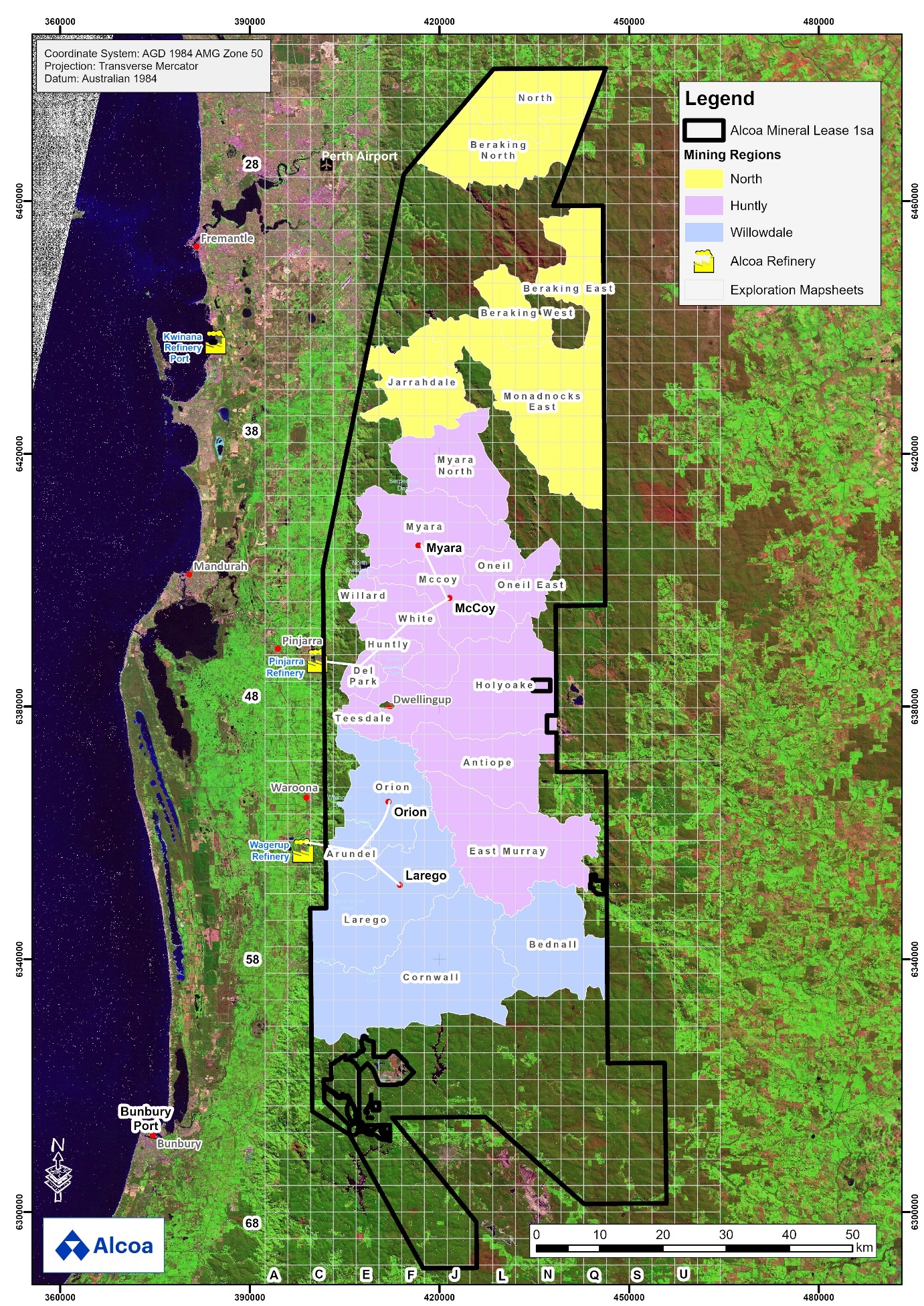

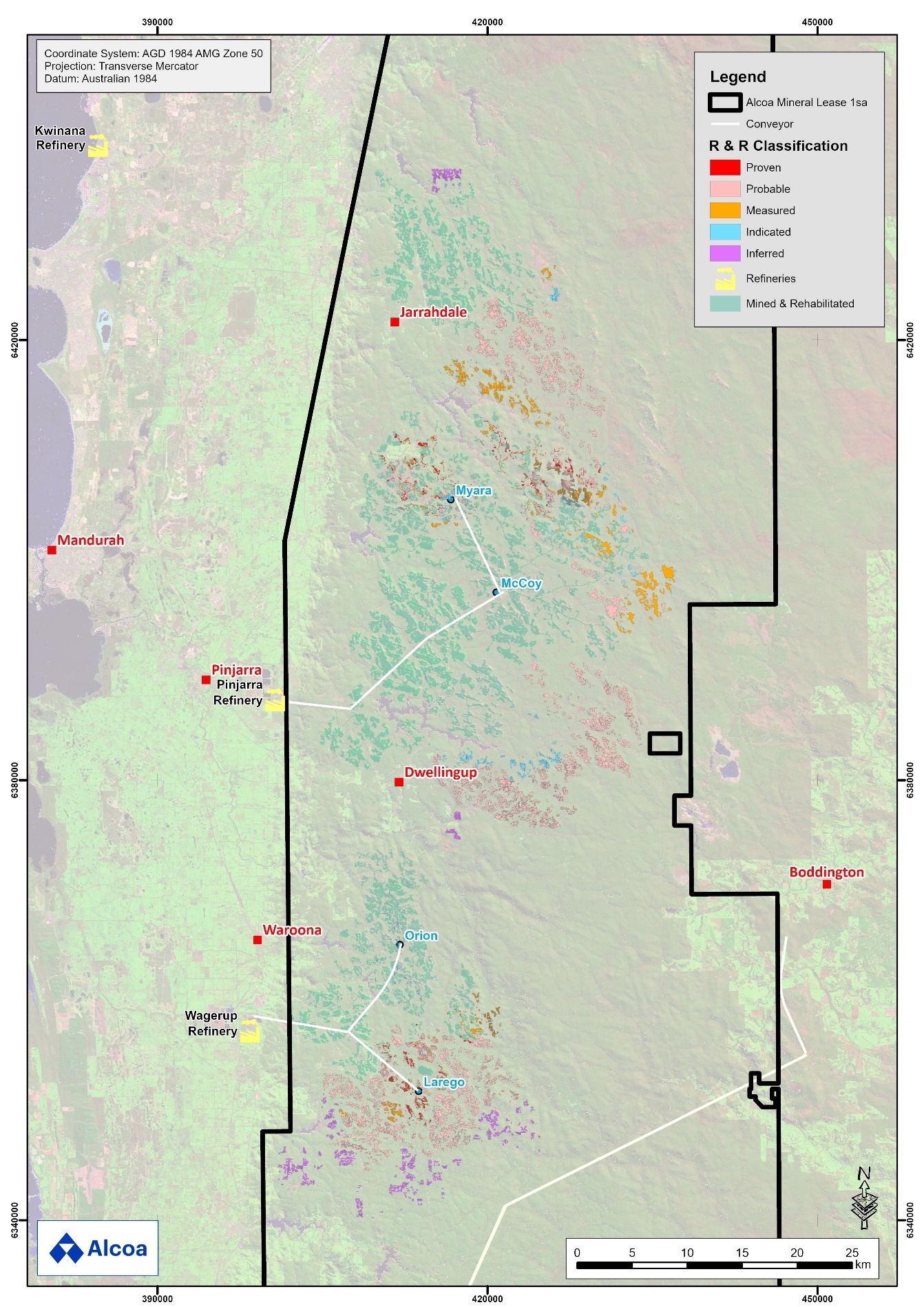

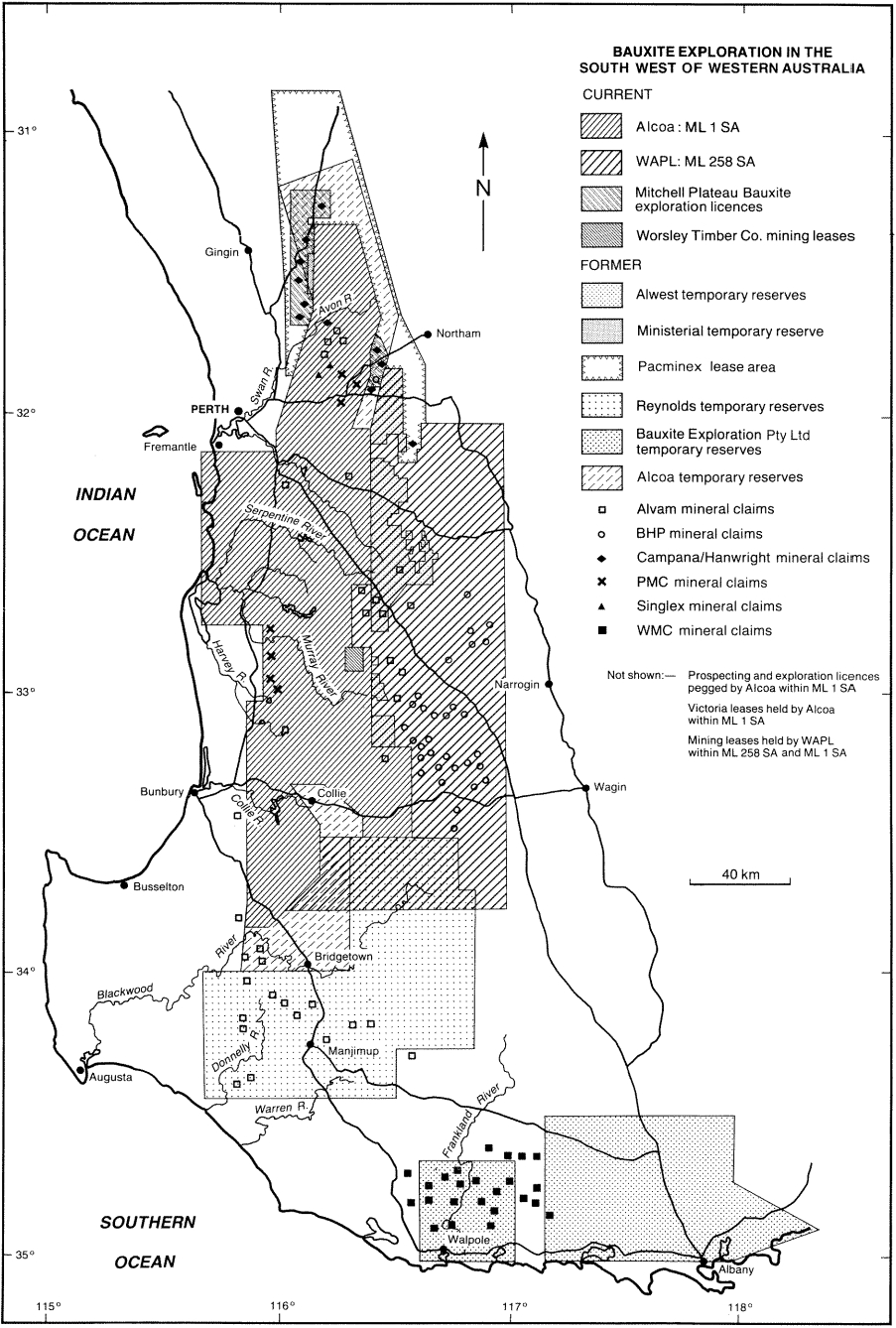

This segment consists of the Company’s worldwide refining system, including the mining of bauxite, which is then refined into alumina, a compound of aluminum and oxygen that is the raw material used by smelters to produce aluminum metal. Bauxite is the principal raw material used to produce alumina and contains various aluminum hydroxide minerals, the most important of which are gibbsite and boehmite. Bauxite is refined into alumina using the Bayer process. The Company obtains bauxite from its own resources as well as through long-term and short-term contracts and mining leases. Tons of bauxite are reported on a zero-moisture basis in millions of dry metric tons (mdmt) unless otherwise stated.

Alcoa’s alumina sales are made to customers globally and are typically priced by reference to published spot market prices. The Company produces smelter grade alumina and non-metallurgical grade alumina. The Company’s largest customer for smelter grade alumina is its own aluminum smelters, which in 2024 accounted for approximately 32 percent of its total alumina shipments. A small portion of the alumina (non-metallurgical grade) is sold to third-party customers who process it into industrial chemical products. This segment also includes Alcoa's 25.1% share of MBAC. In September 2024, Alcoa entered into a share purchase and subscription agreement with Ma’aden, pursuant to which Alcoa agreed to sell its full ownership interest of 25.1% in the Saudi Arabia joint venture. See Part II Item 7 of this Form 10-K in Management’s Discussion and Analysis of Financial Condition and Results of Operations under caption Business Update for more information.

In 2024, Alcoa-operated mines, mines operated by partnerships in which Alcoa has equity interests, and bauxite offtake agreements supplied 85 percent of bauxite volume to Alcoa refineries and the remaining 15 percent was sold to third-party customers. Alcoa-operated mines produced 33.7 mdmt of bauxite and mines operated by partnerships produced 4.6 mdmt of bauxite on a proportional equity basis, for a total Company bauxite production of 38.3 mdmt.

On April 30, 2022, Alcoa completed the sale of its investment in MRN. The Company entered into several bauxite offtake agreements with South32 to provide bauxite supply for existing long-term supply contracts.

Based on the terms of its bauxite supply contracts, the amount of bauxite Alcoa purchases from its minority-owned joint ventures, MRN (until its sale in April 2022) and CBG, differ from its proportional equity in those mines. Therefore, in 2024, Alcoa had access to 41.3 mdmt of production from its portfolio of bauxite interests and bauxite offtake and supply agreements and sold 6.4 mdmt of bauxite to third parties; 34.9 mdmt of bauxite was delivered to Alcoa refineries.

The Company primarily sells alumina through contracts containing two pricing components: (1) the API price basis and (2) a negotiated adjustment basis that takes into account various factors, including freight, quality, customer location, and market conditions, as well as through fixed price spot sales. In 2024, approximately 95 percent of the Company’s smelter grade alumina shipments to third parties were sold on an adjusted API price or fixed price spot basis.

Information regarding the Company’s bauxite mining properties and bauxite mineral resources and reserves is included in Part 1 Item 2 of this Form 10-K.

5

Alcoa’s alumina refining facilities and its worldwide alumina capacity stated in metric tons per year (mtpy) as of December 31, 2024 are shown in the following table:

Country |

|

Facility |

|

Nameplate |

|

|

Alcoa |

|

||

Australia (AofA) |

|

Kwinana |

|

|

2,190 |

|

|

|

2,190 |

|

|

|

Pinjarra |

|

|

4,700 |

|

|

|

4,700 |

|

|

|

Wagerup |

|

|

2,879 |

|

|

|

2,879 |

|

Brazil |

|

Poços de Caldas |

|

|

390 |

|

|

|

390 |

|

|

|

São Luís (Alumar) |

|

|

3,860 |

|

|

|

2,084 |

|

Spain |

|

San Ciprián |

|

|

1,600 |

|

|

|

1,600 |

|

TOTAL |

|

|

|

|

15,619 |

|

|

|

13,843 |

|

Equity Interests: |

|

|

|

|

|

|

|

|

||

Country |

|

Facility |

|

Nameplate |

|

|

Alcoa |

|

||

Saudi Arabia |

|

Ras Al Khair (MBAC) |

|

|

1,800 |

|

|

|

452 |

|

As of December 31, 2024, Alcoa had approximately 3,204,000 mtpy of idle capacity relative to total Alcoa consolidated capacity of 13,843,000 mtpy. The idle capacity includes: 2,190,000 mtpy at the Kwinana refinery, 800,000 mtpy at the San Ciprián refinery, and 214,000 mtpy at the Poços de Caldas facility.

In October 2024, the Company completed its five-year strategic portfolio review to improve cost positioning, or curtail, close, or divest 4 million metric tons of refining capacity. The Company exceeded its target for refining capacity with the decision to curtail the Kwinana refinery in January 2024. The Company continues to evaluate assets for opportunities for improvement to remain profitable throughout business cycles.

In June 2024, the Company completed the full curtailment of the Kwinana refinery, as planned, which was announced in January 2024. As of March 2024, the refinery had approximately 780 employees and this number was reduced to approximately 250 through the fourth quarter of 2024 to manage certain processes that are expected to continue until about the fourth quarter of 2025. At that time, the employee number will be further reduced to approximately 50. In addition to the employees separating as a result of the curtailment, approximately 290 employees have terminated through the productivity program announced in the third quarter of 2023 or redeployed to other Alcoa operations.

In 2022, production at the San Ciprián refinery was reduced to approximately 50 percent of the 1.6 million metric tons of annual capacity to mitigate the financial impact of high natural gas costs. In October 2024, Alcoa announced that it is progressing toward entering into a strategic partnership with IGNIS Equity Holdings, SL (IGNIS EQT), the majority shareholder in the IGNIS Group of Companies, a vertically integrated energy company based in Spain, to support the continued operation of the San Ciprián complex. Alcoa would continue as the managing operator of the San Ciprián operations, with IGNIS EQT holding 25 percent ownership. In January 2025, the Company, the Spanish national and Xunta regional governments, and IGNIS EQT signed a memorandum of understanding (MoU) that outlines a process for the parties to work cooperatively toward the common objective of improving the long-term outlook for the San Ciprián operations and focuses on the key areas of cooperation.

6

Aluminum

This segment currently consists of (i) the Company’s worldwide smelting and casthouse system and (ii) a portfolio of energy assets in Brazil, Canada, and the United States. The smelting operations produce molten primary aluminum, which is then formed by the casting operations into either common alloy ingot (e.g., t-bar, sow, standard ingot) or into value add ingot products (e.g., foundry, billet, rod, and slab). The energy assets supply power to external customers in Brazil and the United States, as well as internal customers in the Aluminum segment (Baie-Comeau (Canada) smelter and Warrick (Indiana) smelter) and, to a lesser extent, the Alumina segment (Brazilian refineries). This segment also includes Alcoa’s 25.1% share of MAC, the smelting joint venture company in Saudi Arabia. In September 2024, Alcoa entered into a share purchase and subscription agreement with Ma’aden, pursuant to which Alcoa agreed to sell its full ownership interest of 25.1% in the Saudi Arabia joint venture. See Part II Item 7 of this Form 10-K in Management’s Discussion and Analysis of Financial Condition and Results of Operations under caption Business Update for more information.

Smelting and Casting Operations

Contracts for primary aluminum vary widely in duration, from multi-year supply contracts to spot purchases. Pricing for primary aluminum products is typically comprised of three components: (i) the published LME aluminum price for commodity grade P1020 aluminum, (ii) the published regional premium applicable to the delivery locale, and (iii) a negotiated product premium that accounts for factors such as shape and alloy.

Alcoa’s primary aluminum facilities and its global smelting capacity stated in metric tons per year (mtpy) as of December 31, 2024 are shown in the following table:

Country |

|

Facility |

|

Nameplate |

|

|

Alcoa |

|

||

Australia |

|

Portland |

|

|

358 |

|

|

|

197 |

|

Brazil |

|

Poços de Caldas2 |

|

N/A |

|

|

N/A |

|

||

|

|

São Luís (Alumar) |

|

|

447 |

|

|

|

268 |

|

Canada |

|

Baie Comeau, Québec |

|

|

324 |

|

|

|

324 |

|

|

|

Bécancour, Québec |

|

|

467 |

|

|

|

350 |

|

|

|

Deschambault, Québec |

|

|

287 |

|

|

|

287 |

|

Iceland |

|

Fjarðaál |

|

|

351 |

|

|

|

351 |

|

Norway |

|

Lista |

|

|

95 |

|

|

|

95 |

|

|

|

Mosjøen |

|

|

200 |

|

|

|

200 |

|

Spain |

|

San Ciprián |

|

|

228 |

|

|

|

228 |

|

United States |

|

Massena West, NY |

|

|

130 |

|

|

|

130 |

|

|

|

Evansville, IN (Warrick) |

|

|

215 |

|

|

|

215 |

|

TOTAL |

|

|

|

|

3,102 |

|

|

|

2,645 |

|

Equity Interests: |

|

|

|

|

|

|

|

|

||

Country |

|

Facility |

|

Nameplate |

|

|

Alcoa |

|

||

Saudi Arabia |

|

Ras Al Khair (MAC) |

|

|

804 |

|

|

|

202 |

|

As of December 31, 2024, Alcoa had approximately 374,000 mtpy of idle smelting capacity relative to total Alcoa consolidated capacity of 2,645,000 mtpy. The idle capacity includes: 214,000 mtpy at the San Ciprián smelter, 54,000 mtpy at the Warrick smelter, 42,000 mtpy at the Alumar smelter, 33,000 mtpy at the Portland smelter, and 31,000 mtpy at the Lista smelter.

7

In October 2024, the Company completed its five-year strategic portfolio review to improve cost positioning, or curtail, close, or divest 1.5 million metric tons of smelting capacity. The Company reached approximately 93 percent of its target for smelting capacity with the decision to restart capacity at the Warrick smelter completed in the first quarter 2024. The Company continues to evaluate assets for opportunities for improvement to be profitable throughout business cycles.

During 2024, the Company maintained the controlled pace for the restart of the Alumar smelter in São Luís, Brazil and continued actions to improve the smelter's overall performance. The site was operating at approximately 84 percent of the site’s total annual capacity of 268,000 mtpy (Alcoa share) as of December 31, 2024.

In the fourth quarter of 2024, the Company completed the restart of 16,000 mtpy of previously curtailed capacity at the Portland smelter in Australia that began in the fourth quarter of 2023. The site was operating at approximately 83 percent of the site’s total annual capacity of 197,000 mtpy (Alcoa share) as of December 31, 2024.

In the first quarter of 2024, the Company completed the restart of 54,000 mtpy of capacity at the Warrick smelter (Indiana) that began in the fourth quarter of 2023.

The San Ciprián smelter was curtailed in January 2022, as a result of an agreement with the workers’ representatives in December 2021. In February 2023, under the terms of an amended viability agreement, Alcoa agreed to a phased restart of the smelter beginning in January 2024, to operate an initial complement of approximately 6 percent of total pots, to restart all pots by October 1, 2025 and to maintain 75 percent of the annual capacity of 228,000 mtpy from October 1, 2025 until the end of 2026. In March 2024, the Company completed the restart of approximately 6 percent of total pots at the San Ciprián smelter. In October 2024, Alcoa announced that it is progressing toward entering into a strategic partnership with IGNIS EQT to support the continued operation of the San Ciprián complex. Alcoa would continue as the managing operator of the San Ciprián operations, with IGNIS EQT holding 25 percent ownership. In January 2025, the Company, the Spanish national and Xunta regional governments, and IGNIS EQT signed an MoU that outlines a process for the parties to work cooperatively toward the common objective of improving the long-term outlook for the San Ciprián operations and focuses on the key areas of cooperation.

Energy Facilities and Sources

In 2024, energy comprised approximately 24 percent of the Company’s total alumina refining production costs and electric power comprised approximately 22 percent of the Company’s primary aluminum production costs.

Electricity markets are regional and are limited by physical and regulatory constraints, including the physical inability to transport electricity efficiently over long distances, the design of the electric grid, including interconnections, and the regulatory structure imposed by various federal and state entities.

Electricity contracts may be short-term (real-time or day ahead) or years in duration, and contracts can be executed for immediate delivery or years in advance. Pricing may be fixed, indexed to an underlying fuel source or other index such as LME, cost-based, or based on regional market pricing. In 2024, Alcoa generated approximately 10 percent of the power used at its smelters worldwide and generally purchased the remainder under long-term arrangements.

The following table sets forth the electricity generation capacity and 2024 generation of facilities in which Alcoa Corporation has an ownership interest. See also the Joint Ventures section above.

Country |

|

Facility |

|

Alcoa Corporation Consolidated |

|

|

2024 Generation |

|

||

Brazil |

|

Barra Grande |

|

|

150 |

|

|

|

1,315,259 |

|

|

|

Estreito |

|

|

155 |

|

|

|

1,360,074 |

|

|

|

Machadinho |

|

|

126 |

|

|

|

1,105,950 |

|

|

|

Serra do Facão |

|

|

60 |

|

|

|

525,600 |

|

Canada |

|

Manicouagan |

|

|

133 |

|

|

|

1,164,467 |

|

United States |

|

Warrick |

|

|

657 |

|

|

|

2,838,977 |

|

TOTAL |

|

|

|

|

1,281 |

|

|

|

8,310,327 |

|

The figures in this table are presented in megawatts (MW) and megawatt hours (MWh), respectively.

8

Each facility listed above generates hydroelectric power except the Warrick facility, which generates substantially all of the power used by the Warrick smelting facility from the co-located Warrick power plant using coal purchased from third parties at nearby coal reserves. In 2024, Alcoa ceased using coal from the Alcoa-owned Liberty Mine, which was operated by a third-party coal company. In 2024, approximately 31 percent of the generation from the Warrick power plant was sold into the market under its current operating permits. Alcoa Power Generating Inc., a subsidiary of the Company, also owns certain Federal Energy Regulatory Commission (FERC)-regulated transmission assets in Indiana, Tennessee, New York, and Washington.

The consolidated capacity of the Brazilian energy facilities shown above in MW is the assured energy, representing approximately 53 percent of hydropower plant nominal capacity. The Brazilian hydroelectric facilities produce energy which is transmitted across the national grid to Alcoa’s refineries in Brazil and the excess generation capacity is sold into the market.

Below is an overview of our external energy for our smelters and refineries.

|

External Energy Source |

|

Region |

Electricity |

Natural Gas |

North America |

Québec, Canada Alcoa’s smelter located in Baie-Comeau, Québec, purchases approximately 25 percent of its electricity needs from Manicouagan Power Limited Partnership under an agreement that expires in February 2036. Otherwise, all electricity consumed by the three smelters in Québec is purchased under contracts with Hydro-Québec that expire on December 31, 2029. The Baie-Comeau contract has an automatic renewal through February 2036.

Massena, New York (Massena West) The Massena West smelter in New York purchases power from the New York Power Authority (NYPA) pursuant to a contract between Alcoa and NYPA that expires in March 2026.

|

Alcoa generally procures natural gas on a competitive bid basis from a variety of sources, including natural gas producers and independent gas marketers. Contract pricing for gas is typically based on a published industry index such as the New York Mercantile Exchange (NYMEX). |

Australia |

Portland This smelter purchases power from the National Electricity Market (NEM) variable spot market in the state of Victoria and has fixed-for-floating swap contracts with AGL Hydro Partnership, Origin Energy Electricity Limited, and Alinta Energy CEA Trading Pty Ltd, for a combined 587 MW that expire on June 30, 2026.

In August 2023 and September 2024, the smelter entered into nine-year fixed-for-floating swap contracts with AGL Hydro Partnership for a combined 587 MW effective July 1, 2026.

Each of these swap contracts manage exposure to the variable energy rates from the NEM spot market under long-term power purchase agreements, which may include purchases of power from renewable energy sources.

|

Western Australia AofA uses gas to co-generate steam and electricity for its alumina refining processes at the Kwinana (see below), Pinjarra, and Wagerup refineries, and to fuel the calcination furnaces at each site.

The Kwinana refinery was fully curtailed in June 2024, and the Company is evaluating alternatives to resell, swap or redeploy the gas secured for the Kwinana refinery.

Prior to 2022, AofA secured a significant portion of gas supplies through 2032. On a combined basis, these gas supply arrangements are expected to cover approximately 90 percent of the Pinjarra and Wagerup refineries’ gas requirements through 2027, with decreasing percentages thereafter through 2032.

In 2024, AofA contracted for a portion of the additional gas supplies required starting in 2028 for a 10-year period.

|

9

|

External Energy Source |

|

Region |

Electricity |

Natural Gas |

Europe |

San Ciprián, Spain Since March 2024, when Alcoa completed the restart of approximately 6 percent of capacity, the San Ciprián smelter has been exposed to the electricity spot market.

In 2022, Alcoa entered into two long-term power purchase agreements (PPAs) with renewable energy providers that are expected to supply up to 50 percent of the smelter's power needs at its full capacity. The supply of energy will continue to depend on the permitting and development of the windfarms included in the PPAs.

In October 2024, Alcoa announced that it is progressing toward entering into a strategic partnership with IGNIS EQT to support the continued operation of the San Ciprián complex. Alcoa would continue as the managing operator of the San Ciprián operations, with IGNIS EQT holding 25 percent ownership. In January 2025, the Company, the Spanish national and Xunta regional governments, and IGNIS EQT signed an MoU that outlines a process for the parties to work cooperatively toward the common objective of improving the long-term outlook for the San Ciprián operations and focuses on the key areas of cooperation.

Mosjøen, Norway Alcoa has several long-term power purchase agreements securing approximately 80 percent of the necessary power for the smelter through 2035. The remaining power at the smelter is purchased at spot rates.

Lista, Norway Alcoa had several power purchase agreements securing approximately 90 percent of the necessary power for the smelter through 2024, and has a power purchase agreement securing approximately 80 percent of the necessary power for the smelter for 2025 through 2027. The remaining power at the smelter is purchased at spot rates.

Financial compensation of the indirect carbon emissions costs passed through in the electricity bill is received in accordance with European Union (EU) Commission Guidelines and the Norwegian compensation regime. Beginning in 2024, 40 percent of the compensation is conditional on decarbonization investment by Alcoa in Norway. Complying with the additional condition can be achieved over multiple years, but not later than 2034. Compensation received for approved decarbonization investment is expected to be recognized over the useful lives of the related assets.

Iceland Landsvirkjun, the Icelandic national power company, supplies competitively priced electricity from a hydroelectric facility to the smelter under a 40-year power contract, which expires in 2047 with a price renegotiation effective from 2028.

|

Spain The San Ciprián refinery has been operating at 50 percent of its capacity since the third quarter of 2022.

The San Ciprián refinery has access to an adequate supply at Spanish (PVB) spot gas rates.

|

10

|

External Energy Source |

|

Region |

Electricity |

Natural Gas |

South America |

Alumar The Alumar smelter was operating at 84 percent of the site’s total annual capacity of 268,000 mtpy (Alcoa share) as of December 31, 2024, following the restart that was announced in September 2021.

The Alumar smelter purchases power under several long-term power purchase agreements that expire in 2038. Long-term power secured is from renewable sources. |

|

Sources and Availability of Raw Materials

The Company believes that the raw materials necessary to its business are and will continue to be available and that the sources and availability of such raw materials are currently adequate. Generally, materials are purchased from third-party suppliers under competitively priced supply contracts or bidding arrangements. Substantially all of the raw materials required to manufacture our products are available from more than one supplier. Some sources of these raw materials are located in countries that may be subject to unstable political and economic conditions, which could disrupt supply or affect the price of these materials.

Certain raw materials, such as caustic soda and calcined petroleum coke, may be subject to significant price volatility which could impact our financial results.

Alcoa sources bauxite from its own resources and believes its present sources of bauxite on a global basis are sufficient to meet the forecasted requirements of its alumina refining operations for the foreseeable future.

Certain alumina refineries generate electricity through the digestor process that meets or exceeds their power needs, while others purchase electricity from third-party suppliers.

For each metric ton (mt) of alumina produced, Alcoa consumes the following amounts of the identified raw material inputs (approximate range across relevant facilities):

Raw Material |

|

Units |

|

Consumption per mt of Alumina |

Bauxite |

|

mt |

|

2.2 – 4.0 |

Caustic soda |

|

kg |

|

80 – 130 |

Electricity |

|

MWh |

|

0.17 to 0.30 total consumed |

Fuel oil and natural gas |

|

GJ |

|

6 – 10.5 |

Lime (CaO) |

|

kg |

|

6 – 50 |

For each metric ton of aluminum produced, Alcoa consumes the following amounts of the identified raw material inputs (approximate range across relevant facilities):

Raw Material |

|

Units |

|

Consumption per mt of Primary Aluminum |

Alumina |

|

mt |

|

1.91 – 1.94 |

Aluminum fluoride |

|

kg |

|

12.2 – 27.2 |

Calcined petroleum coke |

|

mt |

|

0.26 – 0.40 |

Cathode blocks |

|

mt |

|

0.003 – 0.007 |

Electricity |

|

MWh |

|

13.27 – 16.77 |

Liquid pitch |

|

mt |

|

0.08 – 0.12 |

Natural gas |

|

mcf |

|

2.1 – 4.9 |

Certain aluminum we produce includes alloying materials. Because of the number of different types of elements that can be used to produce various alloys, providing a range of such elements would not be meaningful. With the exception of a very small number of internally used products, Alcoa produces its aluminum alloys in adherence to an Aluminum Association (of which Alcoa is an active member) standard, which uses a specific designation system to identify alloy types. In general, each alloy type has a major alloying element other than aluminum but will also include lesser amounts of other constituents.

11

Competition

Alcoa is subject to highly competitive conditions in all aspects of the aluminum supply chain in which it competes. Our business segments operate in key markets globally, and we are able to meet customer demand in North America, South America, Europe, the Middle East, Australia, China, and other parts of Asia.

We compete with a variety of both U.S. and non-U.S. companies in all major markets across the aluminum supply chain. Competitors include bauxite miners who supply to the third-party bauxite market, alumina suppliers, commodity traders, aluminum producers, and producers of alternative materials such as steel, titanium, copper, carbon fiber, composites, plastic, and glass.

With the Sustana brand, including EcoDura aluminum (recycled content), EcoLum aluminum (low carbon), and EcoSource alumina (also low carbon), the Company is well positioned to compete with others.

Alumina

We are the largest alumina producer outside of China and the largest supplier of third-party alumina outside of China. The alumina market is global and highly competitive, with many active suppliers, producers, and commodity traders. The majority of our product is sold in the form of smelter grade alumina. Our main competitors in the third-party alumina market are Aluminum Corporation of China, South32, Hangzhou Jinjiang Group, Rio Tinto, and Norsk Hydro ASA. In recent years, there has been significant growth in alumina refining in China and Indonesia.

Key factors influencing competition in the alumina market include cost position, price, reliability of bauxite supply, quality, and proximity to customers and end markets. We had an average cost position in the first quartile of global alumina production in 2024, as determined by CRU independent commodity intelligence. Increased production costs in 2024 caused by lower bauxite grades in Australia could place Alumina in the second quartile until new mine regions are accessed. Our refineries are strategically located near low-cost bauxite mines, which provide a long-term supply of bauxite to our refineries. Our alumina refineries include sophisticated refining technology to maximize efficiency with the bauxite grades from these internal mines.

We are among the world’s largest bauxite miners. The majority of bauxite mined globally is converted to alumina for the production of aluminum. In 2024, Alcoa-operated mines, mines operated by partnerships, and bauxite offtake agreements supplied approximately 85 percent of bauxite volume to Alcoa refineries and approximately 15 percent of Alcoa’s bauxite shipments were sold to third-party customers.

Our principal competitors in the third-party bauxite market include Rio Tinto and multiple suppliers from Guinea, Australia, and Brazil, among other countries. We compete largely based on bauxite quality, price, and logistics, as well as strategically located long-term bauxite resources in Brazil and Guinea, which is home to the world’s largest reserves of high-quality metallurgical grade bauxite.

Aluminum

In our Aluminum segment, competition is dependent upon the type of product we are selling.

The market for primary aluminum is global, and demand for aluminum varies widely from region to region. We compete with commodity traders, such as Glencore, Trafigura, J. Aron and Gerald Group, and aluminum producers, such as Emirates Global Aluminum, Norsk Hydro ASA, Rio Tinto, Century Aluminum, and Vedanta Aluminum Ltd.

Several of the most critical competitive factors in our industry are product quality, production costs (including source, reliability of supply, and cost of energy), price, access and proximity to raw materials, customers and end markets, timeliness of delivery, customer service (including technical support), product innovation, and breadth of offerings. Where aluminum products compete with other materials, the characteristics of aluminum are also a significant factor, particularly its light weight, strength, and recyclability.

The strength of our position in the primary aluminum market is largely attributable to: our integrated supply chain and regional presence in key markets, primarily North America and Europe; long-term energy arrangements; the ability of our casthouses to provide customers with a diverse product portfolio in terms of shapes and alloys, while meeting high product quality standards; and low carbon footprint for the majority of our production, as approximately 87 percent of the aluminum smelting portfolio operated by the Company was powered by renewable (primarily hydropower) energy sources in 2024. Renewable energy is derived from natural processes that are replenished constantly, such as sunlight, wind, and hydropower. The Company intends to continue to focus on optimizing value add product capacity utilization.

12

Patents, Trade Secrets, and Trademarks

The Company believes that its domestic and international patent, trade secret, and trademark assets provide it with a competitive advantage. The Company’s rights under its intellectual property, as well as the technology and products made and sold under them, are important to the Company as a whole and, to varying degrees, important to each business segment. Alcoa’s business as a whole is not, however, materially dependent on any single patent, trade secret or trademark. As a result of product development and technological advancement, the Company continues to pursue patent protection in jurisdictions throughout the world. As of December 31, 2024, Alcoa’s worldwide patent portfolio consisted of approximately 360 granted patents and approximately 200 pending patent applications. The Company also has a number of domestic and international registered trademarks that have significant recognition within the markets that are served, including the name “Alcoa” and the Alcoa symbol. Patents may exist for 20 years from filing date, and trademarks may have an indefinite life based upon continued use.

Government Regulations and Environmental Matters

Alcoa’s global operations subject it to compliance with various types of government laws, regulations, permits, and other requirements which often provide discretion to government authorities and could be interpreted, applied, or modified in ways to make the Company’s operations or compliance activities more costly. These laws and regulations include those relating to safety and health, environmental protection and compliance, tailings management, data privacy and security, anti-corruption, human rights, competition, and trade, such as tariffs or other import or export restrictions that may increase the cost of raw material or cross-border shipments and impact our ability to do business with certain countries or individuals. Though we cannot predict the collective potential adverse impact of the expanding body of laws, regulations, and interpretations, we believe that we are in compliance with such laws and regulations in all material respects and do not expect that continued compliance with such regulations will have a material effect upon capital expenditures, earnings, or our competitive position. For a discussion of the risks associated with certain applicable laws and regulations, see Part I Item 1A of this Form 10-K.

Environmental

Alcoa is subject to extensive federal, state/provincial, and local environmental laws and regulations and other requirements in the U.S. and abroad, including those relating to the release or discharge of materials into the air, water, and soil; waste management, pollution prevention measures; the generation, storage, handling, use, transportation, and disposal of hazardous materials; and the exposure of persons to hazardous materials.

Alcoa is committed to the Global Industry Standard on Tailings Management (GISTM), an integrated approach to the management and operations of our tailings storage facilities to enhance the safety of these facilities. In August 2023, Alcoa’s impoundments with very high or extreme consequence classification were audited by an independent third party and assessed as in conformance with GISTM as required by the International Council on Mining and Metals Conformance Protocol. This represents the first phase of implementation with lower consequence impoundment conformance required by August 2025.

Additionally, we are and may become subject to various laws and regulations related to the disclosures of emissions, the impact of climate change to our business, and plans to reduce such emissions. Recent laws and regulations pertaining to climate change and greenhouse gas emissions have been implemented or are being considered. In addition, as regulators and investors increasingly focus on climate change and other sustainability issues, we are subject to new disclosure frameworks and regulations. For example, the EU adopted the European Sustainability Reporting Standards (ESRS) and the Corporate Sustainability Reporting Directive (CSRD) that will require disclosure of the risks and opportunities arising from social and environmental issues and the impact of companies’ activities on people and the environment. The CSRD applies not only to local operations in the EU, but under certain circumstances, to global companies with operations in the EU. The CSRD is applicable to Alcoa operations for 2025 with reporting in 2026. Further, in 2024 Australia passed legislation to mandate climate-related financial disclosures applicable to Alcoa effective for 2025 with reporting in 2026. We continue to monitor the development and implementation of such laws and regulations and continue to assess the extent of potential disclosures or other reporting requirements.

We maintain remediation and reclamation plans for various sites, and we manage environmental assessments and cleanups at approximately 60 locations, which include currently owned or operated facilities and adjoining properties, previously owned or operated facilities and adjoining properties, and waste sites, such as U.S. Superfund (Comprehensive Environmental Response, Compensation and Liability Act (CERCLA)) sites. In 2024, capital expenditures for new or expanded facilities for environmental control were $131 and approximately $170 is expected in 2025. See Part II Item 8 of this Form 10-K in Note S to the Consolidated Financial Statements under caption Contingencies for additional information.

13

Safety and Health

We are subject to a broad range of foreign, federal, state, and local laws and regulations relating to occupational health and safety, and our safety program includes measures required for compliance. We have incurred, and will continue to incur, capital expenditures to meet our health and safety compliance requirements, as well as to continually improve our safety systems.

For a discussion of the risks associated with certain applicable laws and regulations, see Part I Item 1A of this Form 10-K.

Human Capital Resources

Our core values – Act with Integrity, Operate with Excellence, Care for People, and Lead with Courage – guide us as a company, including our approach to human capital management. We believe that our people are our greatest asset. The success and growth of our business depend in large part on our ability to attract, develop, and retain talented, qualified, and highly skilled employees at all levels of our organization, including the individuals who comprise our global workforce, our executive officers, and other key personnel.

Alcoa's vision is to provide trusting workplaces that are safe, respectful, and inclusive and that reflect the communities in which we operate. Our aim is to build a more inclusive culture where employees feel valued, empowered, and respected. We continue to execute against our strategy, which is driven by our three pillars: (i) strengthen foundations; (ii) build awareness; and, (iii) drive accountability.

Our Company policies, including the Code of Conduct and Ethics, Harassment and Bullying Free Workplace Policy, and EHS Vision, Values, Mission, and Policy, support our mission to advance our Company culture and core values. Alcoa maintains a Human Rights Policy that applies globally to the Company, its partnerships, and other business associates, which incorporates international human rights principles encompassed in the Universal Declaration of Human Rights, the International Labor Organization’s Declaration on Fundamental Principles and Rights at Work, the United Nations Global Compact, and the United Nations Guiding Principles on Business and Human Rights.

The safety and health of our employees, contractors, temporary workers, and visitors are top priorities and key to our ability to attract and retain talent. We aspire to consistently work safely across our locations. We integrate our temporary workers, contractors, and visitors into our safety programs and data. We strive to foster a culture of hazard and risk awareness, speaking up and proactive incident reporting, and knowledge sharing.

Our safety programs and systems are designed to prevent loss of life and serious injury at our locations and include rigorous safety standards and controls, periodic risk-based audits, a formal and standardized process for investigating fatal and serious injury incidents (including potential incidents), management of critical risks and safety hazards, and efforts to eliminate hazards or implement controls to prevent and mitigate risks. We have operating standards based on human performance, which teach employees how to anticipate and recognize situations where errors are likely to occur, which help enable us to predict, reduce, manage, and prevent fatalities and injuries.

As of December 31, 2024, Alcoa had approximately 13,900 employees in 17 countries. As of December 31, 2024, women comprised approximately 20 percent of our global workforce. Approximately 10,300 of our global employees are covered by collective bargaining agreements with certain unions and varying expiration dates, including approximately 1,000 employees in the U.S., 1,900 employees in Europe, 1,400 employees in Canada, 3,500 employees in South America, and 2,500 employees in Australia.

The three collective bargaining agreements with le Syndicat des Métallos (FTQ) representing about 1,000 hourly employees at the Bécancour smelter in Québec, Canada expires on July 19, 2025. ABI is preparing to negotiate new collective bargaining agreements.

14

Available Information

The Company’s internet website address is https://www.alcoa.com. Alcoa makes available free of charge on or through its website its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the Securities and Exchange Commission (the SEC). These documents can be accessed on the investor relations portion of our website, https://www.alcoa.com/investors. This information can also be found on the SEC’s internet website, https://www.sec.gov. The information on the Company’s website is included as an inactive textual reference only and is not a part of, or incorporated by reference in, this Annual Report on Form 10-K.

Dissemination of Company Information

Alcoa Corporation intends to make future announcements regarding Company developments and financial performance through its website, https://www.alcoa.com, as well as through press releases, filings with the SEC, conference calls, media broadcasts, and webcasts.

Information about our Executive Officers

The names, ages, positions, and areas of responsibility of the executive officers of the Company as of February 14, 2025, are listed below.

William F. Oplinger, 58, has served as President and Chief Executive Officer of Alcoa Corporation since September 24, 2023. Mr. Oplinger served as Executive Vice President and Chief Operations Officer of the Company from February 2023 until his appointment as President and Chief Executive Officer. From November 2016 through January 2023, Mr. Oplinger was Executive Vice President and Chief Financial Officer of the Company. Prior to this, Mr. Oplinger served as Executive Vice President and Chief Financial Officer of ParentCo from April 1, 2013 to November 2016. Mr. Oplinger joined ParentCo in 2000, and through 2013 held key corporate positions in financial analysis and planning and also served as Director of Investor Relations. Mr. Oplinger also held principal positions in the ParentCo’s Global Primary Products division, including as Controller, Operational Excellence Director, Chief Financial Officer, and Chief Operating Officer.

Molly S. Beerman, 61, has served as Executive Vice President and Chief Financial Officer of Alcoa Corporation since February 1, 2023. Prior to this, Ms. Beerman was Senior Vice President and Controller of the Company from November 2019 through January 2023 and Vice President and Controller from December 2016 through October 2019. Ms. Beerman was Director, Global Shared Services Strategy and Solutions from November to December 2016. In 2016, Ms. Beerman held a consulting role with the Finance Department of ParentCo. From 2012 to 2015, Ms. Beerman served as Vice President, Finance and Administration for a non-profit organization focused on community issues. Prior to that, Ms. Beerman was employed by ParentCo from 2001 to 2012, having held several roles in the finance function and eventually becoming the director of global procurement center of excellence from 2008 to 2012. Ms. Beerman is a certified public accountant.

Renato Bacchi, 48, has served as Executive Vice President and Chief Commercial Officer of Alcoa Corporation since August 1, 2023. He leads the Company’s sales and trading, marketing, supply chain, commercial operations, and procurement and oversees the Company’s global energy assets and innovation and technology programs. Mr. Bacchi was Executive Vice President and Chief Strategy and Innovation Officer of Alcoa Corporation from February 2023 to August 2023. Previously, he was Executive Vice President and Chief Strategy Officer from February 2022 through January 2023, Senior Vice President and Treasurer from November 2019 through January 2022, and Vice President and Treasurer from November 2016 through October 2019. Prior to the Separation Transaction, Mr. Bacchi served as the Assistant Treasurer of ParentCo from October 2014 through October 2016 and the Director, Corporate Treasury from 2012 to 2014. Prior to this time, Mr. Bacchi held various roles of increasing responsibility in areas including finance, strategy, procurement, energy and sales. Mr. Bacchi joined ParentCo in Brazil in 1997.

Nicol A. Gagstetter, 46, has served as Executive Vice President and Chief External Affairs Officer of Alcoa Corporation since October 1, 2023. Ms. Gagstetter is responsible for global external affairs, communications, and sustainability, and she oversees the Alcoa Foundation. Ms. Gagstetter was the Global Head of Environment and Social, Copper Industrial Assets at Glencore International AG, a commodity trading and mining company, from August 2021 through September 2023. Ms. Gagstetter was a Senior Marketing Manager at Rio Tinto, a metals and mining company, from 2018 to 2021, and she previously held a variety of leadership roles and positions across external affairs, sustainability, and marketing in Rio Tinto’s Commercial, Minerals, and Copper groups from 2008 to 2018.

15

Andrew Hastings, 50, has served as Executive Vice President and General Counsel of Alcoa Corporation since September 1, 2023. Mr. Hastings has overall responsibility for the Company’s global legal, compliance, governance, and security matters. Prior to joining the Company, Mr. Hastings was Senior Vice President and General Counsel at Lundin Mining Corporation, a mine owner and operator, from February 2019 through August 2023. Previously, Mr. Hastings held progressive legal and commercial roles at Barrick Gold Corporation, a mining company, most recently as Vice President, Joint Venture Governance from May 2018 to February 2019.

Tammi A. Jones, 45, has served as Executive Vice President and Chief Human Resources Officer of Alcoa Corporation since April 1, 2020. Ms. Jones oversees all aspects of human resources management, including talent and recruitment, compensation and benefits, inclusion, training and development, and labor relations. Ms. Jones served as Vice President, Compensation and Benefits of Alcoa Corporation from January 2019 through March 2020 and was the Director, Organizational Effectiveness from April 2017 to December 2018. From April 2015 through March 2017, Ms. Jones served as Human Resources Director, Aluminum (at ParentCo until the Separation Transaction), and she served as Human Resources Director for ParentCo Wheels and Transportation Products from April 2013 to April 2015. Ms. Jones joined ParentCo in 2006 and held a variety of human resource positions at ParentCo, including Human Resources Director, Europe Building & Construction and Human Resources Director, UK and Ireland in ParentCo’s Building and Construction Systems division.

Matthew T. Reed, 52, has served as Executive Vice President and Chief Operations Officer of Alcoa Corporation since January 1, 2024. Mr. Reed is responsible for the daily operations of the Company’s global bauxite, alumina, aluminum, and transformation assets. Mr. Reed was previously Vice President Operations, Australia and President, Alcoa of Australia from June 2023, when he joined the Company, through December 2023. Prior to joining Alcoa, Mr. Reed was the Operations Executive (Chief Operations Officer) of OZ Minerals Limited, a mining company based in South Australia, from September 2021 through May 2023. He was General Manager, Projects at OZ Minerals Limited from January 2021 through August 2021. Previously, Mr. Reed was the Executive Managing Director (Chief Operating Officer) at SIMEC Mining, a mining company based in South Australia, from September 2017 through December 2020.

Item 1A. Risk Factors.

There are inherent risks associated with Alcoa’s business and industry. In addition to the factors discussed elsewhere in this report, the following risks and uncertainties could have a material adverse effect on our business, financial condition, or results of operations, including causing Alcoa’s actual results to differ materially from those projected in any forward-looking statements. Although the risks are organized by heading, and each risk is described separately, many of the risks are interrelated. While we believe we have identified and discussed below the key risk factors affecting our business, there may be additional risks and uncertainties that are not presently known to Alcoa or that Alcoa currently deems immaterial that also may materially adversely affect us in future periods. See Part II Item 7 of this Form 10-K in Management’s Discussion and Analysis of Financial Condition and Results of Operations under the caption Forward-Looking Statements.

Industry and Global Market Risks

The aluminum industry and aluminum end-use markets are highly cyclical and are influenced by several factors, including global economic conditions, the Chinese market, and overall consumer confidence.

The nature of the industries in which our customers operate causes demand for our products to be cyclical, creating potential uncertainty regarding future profitability. The demand for aluminum is sensitive to, and impacted by, demand for the finished goods manufactured by our customers in industries, such as the commercial construction, transportation, and automotive industries, which may change as a result of factors beyond our control. The demand for aluminum is also highly correlated to economic growth, and we could be adversely affected by large or sudden shifts in the global inventory of aluminum and the resulting market price impacts.

We believe the long-term prospects for aluminum and aluminum products are positive; however, we are unable to predict the future course of industry variables or the strength of the global economy and the effects of government intervention. Our business, financial condition, and results of operations may be materially affected by the conditions in the global economy generally, including inflationary and recessionary conditions, and in global capital markets, including in the end markets and geographic regions in which we and our customers operate. Many of the markets in which our customers participate are also cyclical in nature and experience significant fluctuations in demand for their products based on economic and geopolitical conditions, consumer demand, raw material and energy costs, foreign exchange rates, and government actions. Many of these factors are beyond our control.

16

The Chinese market is a significant source of global demand for, and supply of, commodities, including aluminum. Chinese production rates of aluminum, both from new construction and installed smelting capacity, can fluctuate based on Chinese government policy, such as the level of enforcement of production capacity limits and/or licenses and environmental policies. In addition, industry overcapacity, a sustained slowdown in Chinese aluminum demand, or a significant slowdown in other markets, that is not offset by decreases in supply of aluminum or increased aluminum demand in emerging economies, such as India, Brazil, and several Southeast Asian countries, could have an adverse effect on the global supply and demand for aluminum and aluminum prices. Also, changes in the aluminum market can cause changes in the alumina and bauxite markets, which could also materially affect our business, financial condition, or results of operations. As a result of these factors, our profitability is subject to significant fluctuation.

A decline in consumer and business confidence and spending, severe reductions in the availability and cost of credit, and volatility in the capital and credit markets could adversely affect the business and economic environment in which we operate and the profitability of our business. We are also exposed to risks associated with the creditworthiness of our suppliers and customers. If the availability of credit to fund or support the continuation and expansion of our customers’ business operations is curtailed or if the cost of that credit is increased, the resulting inability of our customers or of their customers to either access credit or absorb the increased cost of that credit could adversely affect our business by reducing our sales or by increasing our exposure to losses from uncollectible customer accounts. These conditions and a disruption of the credit markets could also result in financial instability of some of our suppliers and customers. The consequences of such adverse effects could include the interruption of production at the facilities of our customers, the reduction, delay or cancellation of customer orders, delays or interruptions of the supply of raw materials we purchase, and bankruptcy of customers, suppliers, or other creditors. Any of these events could adversely affect our business, financial condition, and results of operations.

We have in the past and could in the future be materially adversely affected by volatility and declines in aluminum and alumina demand and prices, including global, regional, and product-specific prices, or by significant changes in production costs which are linked to LME or other commodities.

The overall price of primary aluminum consists of several components: (i) the underlying base metal component, which is typically based on quoted prices from the LME; (ii) the regional premium, which comprises the incremental price over the base LME component that is associated with the physical delivery of metal to a particular region (e.g., the Midwest premium for metal sold in the United States); and (iii) the product premium, which represents the incremental price for receiving physical metal in a particular shape (e.g., foundry, billet, slab, rod, etc.) and/or alloy. Each of the above three components has its own drivers of variability.

The LME price volatility is typically driven by macroeconomic factors (including geopolitical instability), global supply and demand of aluminum (including expectations for growth, contraction, and the level of global inventories), and trading activity of financial investors. In 2024, LME cash prices reached a high of $2,695 per metric ton in May 2024 and a low of $2,110 per metric ton in January 2024.

While global inventories remained at historically low levels in 2024, high inventories could lead to a reduction in the price of aluminum and declines in the LME price have had a negative impact on our business, financial condition, and results of operations. Regional premiums tend to vary based on the supply of and demand for metal in a particular region, associated transportation costs, and import tariffs. Product premiums generally are a function of supply and demand for a given primary aluminum shape and alloy combination in a particular region. Periods of industry overcapacity may also result in a weak aluminum pricing environment.

A sustained weak LME aluminum pricing environment, deterioration in LME aluminum prices, or a decrease in regional premiums or product premiums could have a material adverse effect on our business, financial condition, or results of operations. Similarly, our operating results are affected by significant changes in key costs of production that are linked to LME or other commodities.

Most of our alumina contracts contain two pricing components: (1) the API price basis and (2) a negotiated adjustment basis that takes into account various factors, including freight, quality, customer location, and market conditions. Because the API component can exhibit significant volatility due to market exposure, revenues associated with our alumina operations are exposed to market pricing.

Market-driven balancing of global aluminum supply and demand may be disrupted by non-market forces.

In response to market-driven factors relating to the global supply and demand of aluminum and alumina, including energy prices and environmental policies, other industry producers have independently undertaken to reduce or increase production. Changes in production may be delayed or impaired by the ability to secure, or the terms of long-term contracts, to buy energy or raw materials.

17