UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the quarterly period ended September 30, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the transition period from to .

Commission File No. 001-36276

ULTRAGENYX PHARMACEUTICAL INC.

(Exact name of registrant as specified in its charter)

Delaware |

|

|

27-2546083 |

(State or other jurisdiction of incorporation or organization) |

|

|

(I.R.S. Employer Identification No.) |

60 Leveroni Court |

|

94949 |

(Address of principal executive offices) |

|

(Zip Code) |

(415) 483-8800

(Registrant’s telephone number, including area code)

Not Applicable

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

Common Stock, $0.001 par value |

RARE |

The Nasdaq Global Select Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☑ NO ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). YES ☑ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☑ |

|

Accelerated filer |

|

☐ |

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

☐ |

|

|

|

|

Emerging growth company |

|

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☑

As of October 30, 2023, the registrant had 82,114,350 shares of common stock issued and outstanding.

ULTRAGENYX PHARMACEUTICAL INC.

FORM 10-Q FOR THE QUARTER ENDED SEPTEMBER 30, 2023

INDEX

|

|

|

|

|

|

Page |

|

|

|

|

|

||

|

1 |

|||||

|

|

|

|

|

||

Part I – |

|

|

|

|||

|

|

|

|

|

|

|

|

|

Item 1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

Item 2. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

22 |

|

|

|

|

|

|

|

|

|

Item 3. |

|

|

34 |

|

|

|

|

|

|

|

|

|

|

Item 4. |

|

|

35 |

|

|

|

|

|

|

||

Part II – |

|

|

|

|||

|

|

|

|

|

|

|

|

|

Item 1. |

|

|

36 |

|

|

|

|

|

|

|

|

|

|

Item 1A. |

|

|

36 |

|

|

|

|

|

|

|

|

|

|

Item 2. |

|

|

72 |

|

|

|

|

|

|

|

|

|

|

Item 3. |

|

|

72 |

|

|

|

|

|

|

|

|

|

|

Item 4. |

|

|

72 |

|

|

|

|

|

|

|

|

|

|

Item 5. |

|

|

72 |

|

|

|

|

|

|

|

|

|

|

Item 6. |

|

|

73 |

|

|

|

|

|

|

|

|

|

|

|

|

|

74 |

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q, or the Quarterly Report, contains forward-looking statements that involve risks and uncertainties. We make such forward-looking statements pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. All statements other than statements of historical facts contained in this Quarterly Report are forward-looking statements. In some cases, you can identify forward-looking statements by words such as “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “will,” “would,” or the negative of these words, or other comparable terminology. These forward-looking statements include, but are not limited to, statements about:

Any forward-looking statements in this Quarterly Report reflect our current views with respect to future events or to our future financial performance and involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by these forward-looking statements. Factors that may cause actual results to differ materially from current expectations include, among other things, those discussed under Part II, Item 1A. Risk Factors and elsewhere in this Quarterly Report. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Except as required by law, we assume no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future.

1

This Quarterly Report also contains estimates, projections, and other information concerning our industry, our business, and the markets for certain diseases, including data regarding the estimated size of those markets, and the incidence and prevalence of certain medical conditions. Information that is based on estimates, forecasts, projections, market research, or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained such industry, business, market, and other data from reports, research surveys, studies, and similar data prepared by market research firms and other third parties, industry, medical and general publications, government data, and similar sources.

2

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

ULTRAGENYX PHARMACEUTICAL INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)

(In thousands, except share amounts)

|

September 30, |

|

|

December 31, |

|

||

|

2023 |

|

|

2022 |

|

||

ASSETS |

|

||||||

Current assets: |

|

|

|

|

|

||

Cash and cash equivalents |

$ |

72,575 |

|

|

$ |

132,944 |

|

Marketable debt securities |

|

369,519 |

|

|

|

614,818 |

|

Accounts receivable, net |

|

79,263 |

|

|

|

40,445 |

|

Inventory |

|

31,802 |

|

|

|

26,766 |

|

Prepaid expenses and other current assets |

|

46,029 |

|

|

|

68,926 |

|

Total current assets |

|

599,188 |

|

|

|

883,899 |

|

Property, plant, and equipment, net |

|

296,811 |

|

|

|

259,726 |

|

Equity investments |

|

4,039 |

|

|

|

5,531 |

|

Marketable debt securities |

|

82,071 |

|

|

|

148,970 |

|

Right-of-use assets |

|

26,427 |

|

|

|

25,961 |

|

Intangible assets, net |

|

157,302 |

|

|

|

160,105 |

|

Goodwill |

|

44,406 |

|

|

|

44,406 |

|

Other assets |

|

27,896 |

|

|

|

16,846 |

|

Total assets |

$ |

1,238,140 |

|

|

$ |

1,545,444 |

|

LIABILITIES AND STOCKHOLDERS' EQUITY |

|

||||||

Current liabilities: |

|

|

|

|

|

||

Accounts payable |

$ |

33,357 |

|

|

$ |

43,274 |

|

Accrued liabilities |

|

178,622 |

|

|

|

204,678 |

|

Contract liabilities |

|

— |

|

|

|

1,479 |

|

Lease liabilities |

|

12,067 |

|

|

|

11,779 |

|

Liabilities for sales of future royalties |

|

29,932 |

|

|

|

— |

|

Total current liabilities |

|

253,978 |

|

|

|

261,210 |

|

Lease liabilities |

|

34,555 |

|

|

|

19,814 |

|

Deferred tax liabilities |

|

31,667 |

|

|

|

31,667 |

|

Liabilities for sales of future royalties |

|

875,996 |

|

|

|

875,439 |

|

Other liabilities |

|

10,230 |

|

|

|

4,820 |

|

Total liabilities |

|

1,206,426 |

|

|

|

1,192,950 |

|

Stockholders’ equity: |

|

|

|

|

|

||

Preferred stock — 25,000,000 shares authorized; nil outstanding as of September 30, 2023 and |

|

— |

|

|

|

— |

|

Common stock — 250,000,000 shares authorized; 72,174,307 and 70,197,297 shares issued |

|

72 |

|

|

|

70 |

|

Treasury stock, at cost, 8,444 and nil shares held as of September 30, 2023 and December 31, 2022, respectively |

|

(381 |

) |

|

|

— |

|

Deferred compensation obligation |

|

381 |

|

|

|

— |

|

Additional paid-in capital |

|

3,298,357 |

|

|

|

3,140,019 |

|

Accumulated other comprehensive loss |

|

(2,244 |

) |

|

|

(6,573 |

) |

Accumulated deficit |

|

(3,264,471 |

) |

|

|

(2,781,022 |

) |

Total stockholders’ equity |

|

31,714 |

|

|

|

352,494 |

|

Total liabilities and stockholders’ equity |

$ |

1,238,140 |

|

|

$ |

1,545,444 |

|

See accompanying notes.

3

ULTRAGENYX PHARMACEUTICAL INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(In thousands, except share and per share amounts)

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

2023 |

|

|

2022 |

|

|

2023 |

|

|

2022 |

|

||||

Revenues: |

|

|

|

|

|

|

|

|

|

|

|

||||

Product sales |

$ |

42,349 |

|

|

$ |

32,503 |

|

|

$ |

128,757 |

|

|

$ |

90,019 |

|

Royalty revenue |

|

55,703 |

|

|

|

5,373 |

|

|

|

106,916 |

|

|

|

15,634 |

|

Collaboration and license |

|

— |

|

|

|

52,827 |

|

|

|

71,184 |

|

|

|

154,328 |

|

Total revenues |

|

98,052 |

|

|

|

90,703 |

|

|

|

306,857 |

|

|

|

259,981 |

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

||||

Cost of sales |

|

10,987 |

|

|

|

8,631 |

|

|

|

33,158 |

|

|

|

23,001 |

|

Research and development |

|

157,245 |

|

|

|

237,297 |

|

|

|

487,892 |

|

|

|

534,981 |

|

Selling, general and administrative |

|

74,917 |

|

|

|

69,841 |

|

|

|

232,966 |

|

|

|

205,290 |

|

Total operating expenses |

|

243,149 |

|

|

|

315,769 |

|

|

|

754,016 |

|

|

|

763,272 |

|

Loss from operations |

|

(145,097 |

) |

|

|

(225,066 |

) |

|

|

(447,159 |

) |

|

|

(503,291 |

) |

Interest income |

|

5,881 |

|

|

|

3,483 |

|

|

|

18,135 |

|

|

|

4,876 |

|

Change in fair value of equity investments |

|

(1,419 |

) |

|

|

(1,626 |

) |

|

|

(1,492 |

) |

|

|

(21,139 |

) |

Non-cash interest expense on liabilities for sales of future royalties |

|

(17,665 |

) |

|

|

(14,505 |

) |

|

|

(48,676 |

) |

|

|

(27,141 |

) |

Other expense |

|

(699 |

) |

|

|

(1,105 |

) |

|

|

(2,380 |

) |

|

|

(1,746 |

) |

Loss before income taxes |

|

(158,999 |

) |

|

|

(238,819 |

) |

|

|

(481,572 |

) |

|

|

(548,441 |

) |

Provision for income taxes |

|

(650 |

) |

|

|

(6,287 |

) |

|

|

(1,877 |

) |

|

|

(7,147 |

) |

Net loss |

$ |

(159,649 |

) |

|

$ |

(245,106 |

) |

|

$ |

(483,449 |

) |

|

$ |

(555,588 |

) |

Net loss per share, basic and diluted |

$ |

(2.23 |

) |

|

$ |

(3.50 |

) |

|

$ |

(6.81 |

) |

|

$ |

(7.96 |

) |

Weighted-average shares used in computing net loss per share, |

|

71,664,493 |

|

|

|

70,054,173 |

|

|

|

70,987,801 |

|

|

|

69,834,037 |

|

See accompanying notes.

4

ULTRAGENYX PHARMACEUTICAL INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(Unaudited)

(In thousands)

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

2023 |

|

|

2022 |

|

|

2023 |

|

|

2022 |

|

||||

Net loss |

$ |

(159,649 |

) |

|

$ |

(245,106 |

) |

|

$ |

(483,449 |

) |

|

$ |

(555,588 |

) |

Other comprehensive income (loss): |

|

|

|

|

|

|

|

|

|

|

|

||||

Foreign currency translation adjustments |

|

(249 |

) |

|

|

(420 |

) |

|

|

188 |

|

|

|

(1,211 |

) |

Unrealized gain (loss) on available-for-sale securities |

|

1,103 |

|

|

|

(888 |

) |

|

|

4,141 |

|

|

|

(7,607 |

) |

Other comprehensive income (loss): |

|

854 |

|

|

|

(1,308 |

) |

|

|

4,329 |

|

|

|

(8,818 |

) |

Total comprehensive loss |

$ |

(158,795 |

) |

|

$ |

(246,414 |

) |

|

$ |

(479,120 |

) |

|

$ |

(564,406 |

) |

See accompanying notes.

5

ULTRAGENYX PHARMACEUTICAL INC.

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(Unaudited)

(In thousands, except share amounts)

|

|

Common Stock |

|

|

Additional |

|

|

Accumulated |

|

|

Accumulated |

|

|

Treasury |

|

|

Deferred Compensation |

|

|

Total |

|

|||||||||||

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Income (Loss) |

|

|

Deficit |

|

|

Stock |

|

|

Obligation |

|

|

Equity |

|

||||||||

Balance as of June 30, 2023 |

|

|

71,465,424 |

|

|

$ |

71 |

|

|

$ |

3,236,879 |

|

|

$ |

(3,098 |

) |

|

$ |

(3,104,822 |

) |

|

$ |

(381 |

) |

|

$ |

381 |

|

|

$ |

129,030 |

|

Issuance of common stock in connection with |

|

|

611,282 |

|

|

|

1 |

|

|

|

24,791 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

24,792 |

|

Stock-based compensation |

|

|

|

|

|

— |

|

|

|

36,245 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

36,245 |

|

|

Issuance of common stock under |

|

|

97,601 |

|

|

|

— |

|

|

|

442 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

442 |

|

Other comprehensive income |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

854 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

854 |

|

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(159,649 |

) |

|

|

— |

|

|

|

— |

|

|

|

(159,649 |

) |

Balance as of September 30, 2023 |

|

|

72,174,307 |

|

|

$ |

72 |

|

|

$ |

3,298,357 |

|

|

$ |

(2,244 |

) |

|

$ |

(3,264,471 |

) |

|

$ |

(381 |

) |

|

$ |

381 |

|

|

$ |

31,714 |

|

|

|

Common Stock |

|

|

Additional |

|

|

Accumulated |

|

|

Accumulated |

|

|

Treasury |

|

|

Deferred Compensation |

|

|

Total |

|

|||||||||||

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Income (Loss) |

|

|

Deficit |

|

|

Stock |

|

|

Obligation |

|

|

Equity |

|

||||||||

Balance as of December 31, 2022 |

|

|

70,197,297 |

|

|

$ |

70 |

|

|

$ |

3,140,019 |

|

|

$ |

(6,573 |

) |

|

$ |

(2,781,022 |

) |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

352,494 |

|

Issuance of common stock in connection with |

|

|

1,175,584 |

|

|

|

1 |

|

|

|

53,298 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

53,299 |

|

Stock-based compensation |

|

|

|

|

|

— |

|

|

|

100,780 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

100,780 |

|

|

Issuance of common stock under |

|

|

801,426 |

|

|

|

1 |

|

|

|

4,260 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

4,261 |

|

Deferred compensation |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(381 |

) |

|

|

381 |

|

|

|

— |

|

Other comprehensive income |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

4,329 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

4,329 |

|

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(483,449 |

) |

|

|

— |

|

|

|

— |

|

|

|

(483,449 |

) |

Balance as of September 30, 2023 |

|

|

72,174,307 |

|

|

$ |

72 |

|

|

$ |

3,298,357 |

|

|

$ |

(2,244 |

) |

|

$ |

(3,264,471 |

) |

|

$ |

(381 |

) |

|

$ |

381 |

|

|

$ |

31,714 |

|

|

|

Common Stock |

|

|

Additional |

|

|

Accumulated |

|

|

Accumulated |

|

|

Treasury |

|

|

Deferred Compensation |

|

|

Total |

|

|||||||||||

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Income (Loss) |

|

|

Deficit |

|

|

Stock |

|

|

Obligation |

|

|

Equity |

|

||||||||

Balance as of June 30, 2022 |

|

|

70,010,398 |

|

|

$ |

70 |

|

|

$ |

3,071,000 |

|

|

$ |

(8,914 |

) |

|

$ |

(2,384,083 |

) |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

678,073 |

|

Stock-based compensation |

|

|

— |

|

|

|

— |

|

|

|

36,096 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

36,096 |

|

Issuance of common stock under |

|

|

69,379 |

|

|

|

— |

|

|

|

1,074 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

1,074 |

|

Other comprehensive loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(1,308 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(1,308 |

) |

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(245,106 |

) |

|

|

— |

|

|

|

— |

|

|

|

(245,106 |

) |

Balance as of September 30, 2022 |

|

|

70,079,777 |

|

|

$ |

70 |

|

|

$ |

3,108,170 |

|

|

$ |

(10,222 |

) |

|

$ |

(2,629,189 |

) |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

468,829 |

|

6

|

|

Common Stock |

|

|

Additional |

|

|

Accumulated |

|

|

Accumulated |

|

|

Treasury |

|

|

Deferred Compensation |

|

|

Total |

|

|||||||||||

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Income (Loss) |

|

|

Deficit |

|

|

Stock |

|

|

Obligation |

|

|

Equity |

|

||||||||

Balance as of December 31, 2021 |

|

|

69,344,998 |

|

|

$ |

69 |

|

|

$ |

2,997,497 |

|

|

$ |

(1,404 |

) |

|

$ |

(2,073,601 |

) |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

922,561 |

|

Stock-based compensation |

|

|

— |

|

|

|

— |

|

|

|

101,862 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

101,862 |

|

Issuance of common stock under |

|

|

734,779 |

|

|

|

1 |

|

|

|

8,811 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

8,812 |

|

Other comprehensive loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(8,818 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(8,818 |

) |

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(555,588 |

) |

|

|

— |

|

|

|

— |

|

|

|

(555,588 |

) |

Balance as of September 30, 2022 |

|

|

70,079,777 |

|

|

$ |

70 |

|

|

$ |

3,108,170 |

|

|

$ |

(10,222 |

) |

|

$ |

(2,629,189 |

) |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

468,829 |

|

See accompanying notes.

7

ULTRAGENYX PHARMACEUTICAL INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(In thousands)

|

Nine Months Ended September 30, |

|

|||||

|

2023 |

|

|

2022 |

|

||

Operating activities: |

|

|

|

|

|

||

Net loss |

$ |

(483,449 |

) |

|

$ |

(555,588 |

) |

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

||

Stock-based compensation |

|

101,483 |

|

|

|

101,022 |

|

Acquired in-process research and development |

|

— |

|

|

|

75,234 |

|

Amortization of (discount) premium on marketable debt securities, net |

|

(8,894 |

) |

|

|

4,349 |

|

Depreciation and amortization |

|

17,788 |

|

|

|

13,263 |

|

Change in fair value of equity investments |

|

1,492 |

|

|

|

21,139 |

|

Non-cash royalty revenue |

|

(42,695 |

) |

|

|

(15,634 |

) |

Non-cash interest expense on liabilities for sales of future royalties |

|

48,676 |

|

|

|

27,141 |

|

Other |

|

3,102 |

|

|

|

564 |

|

Changes in operating assets and liabilities: |

|

|

|

|

|

||

Accounts receivable |

|

(23,790 |

) |

|

|

(2,973 |

) |

Inventory |

|

(4,974 |

) |

|

|

(5,496 |

) |

Prepaid expenses and other assets |

|

16,584 |

|

|

|

558 |

|

Accounts payable, accrued, and other liabilities |

|

(14,746 |

) |

|

|

52,416 |

|

Contract liabilities |

|

(1,479 |

) |

|

|

(6,118 |

) |

Net cash used in operating activities |

|

(390,902 |

) |

|

|

(290,123 |

) |

Investing activities: |

|

|

|

|

|

||

Purchase of property, plant, and equipment |

|

(42,667 |

) |

|

|

(89,153 |

) |

Acquisition, net of cash acquired |

|

— |

|

|

|

(75,391 |

) |

Purchase of marketable debt securities |

|

(304,789 |

) |

|

|

(416,161 |

) |

Proceeds from sale of marketable debt securities |

|

47,520 |

|

|

|

82,966 |

|

Proceeds from maturities of marketable debt securities |

|

582,230 |

|

|

|

407,926 |

|

Payment for intangible asset |

|

(2,500 |

) |

|

|

(30,000 |

) |

Other |

|

(4,777 |

) |

|

|

(240 |

) |

Net cash provided by (used in) investing activities |

|

275,017 |

|

|

|

(120,053 |

) |

Financing activities: |

|

|

|

|

|

||

Proceeds from the sale of future royalties, net |

|

— |

|

|

|

490,950 |

|

Proceeds from the issuance of common stock in connection with at-the-market offering, net |

|

53,299 |

|

|

|

— |

|

Proceeds from the issuance of common stock under equity plan awards, net of tax |

|

4,261 |

|

|

|

8,812 |

|

Other |

|

(28 |

) |

|

|

(436 |

) |

Net cash provided by financing activities |

|

57,532 |

|

|

|

499,326 |

|

Effect of exchange rate changes on cash |

|

(641 |

) |

|

|

(2,427 |

) |

Net increase (decrease) in cash, cash equivalents and restricted cash |

|

(58,994 |

) |

|

|

86,723 |

|

Cash, cash equivalents and restricted cash at beginning of period |

|

137,601 |

|

|

|

309,585 |

|

Cash, cash equivalents and restricted cash at end of period |

$ |

78,607 |

|

|

$ |

396,308 |

|

|

|

|

|

|

|

||

Supplemental disclosures of non-cash information: |

|

|

|

|

|

||

Acquired lease liabilities arising from obtaining right-of-use assets and property, plant, and equipment |

$ |

23,360 |

|

|

$ |

1,168 |

|

Stock-based compensation capitalized into ending inventory |

$ |

2,562 |

|

|

$ |

619 |

|

Costs of PP&E included in AP, accrued, and other liabilities |

$ |

1,427 |

|

|

$ |

20,435 |

|

Non-cash interest expense on liabilities for sales of future royalties capitalized during the year into ending property, plant and equipment |

$ |

9,430 |

|

|

$ |

7,820 |

|

See accompanying notes.

8

ULTRAGENYX PHARMACEUTICAL INC.

Notes to Condensed Consolidated Financial Statements

1. Organization

Ultragenyx Pharmaceutical Inc., or the Company, is a biopharmaceutical company incorporated in Delaware.

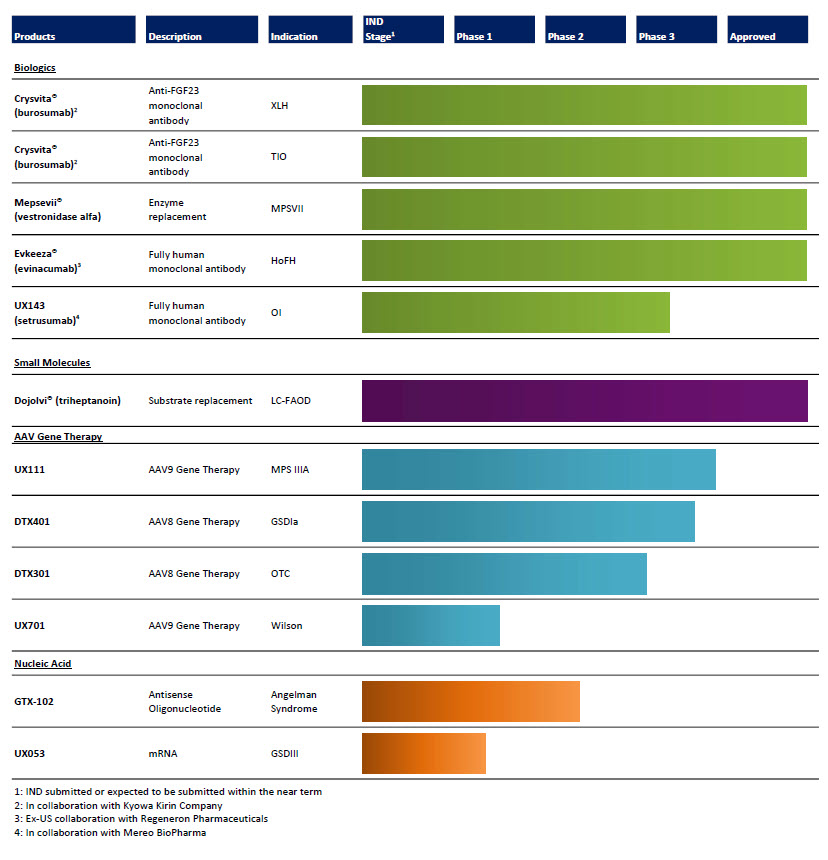

The Company is focused on the identification, acquisition, development, and commercialization of novel products for the treatment of serious rare and ultrarare genetic diseases. The Company operates as one reportable segment and has four commercially approved products.

Crysvita® (burosumab) is approved in the United States, or U.S., the European Union, or EU, and certain other regions for the treatment of X-linked hypophosphatemia, or XLH, in adult and pediatric patients one year of age and older. Crysvita is also approved in the U.S. and certain other regions for the treatment of fibroblast growth factor 23, or FGF23,-related hypophosphatemia in tumor-induced osteomalacia, or TIO, associated with phosphaturic mesenchymal tumors that cannot be curatively resected or localized in adults and pediatric patients 2 years of age and older.

Mepsevii® (vestronidase alfa) is approved in the U.S., the EU and certain other regions, as the first medicine for the treatment of children and adults with mucopolysaccharidosis VII, or MPS VII, also known as Sly syndrome.

Dojolvi® (triheptanoin) is approved in the U.S. and certain other regions for the treatment of pediatric and adult patients severely affected by long-chain fatty acid oxidation disorders, or LC-FAOD.

Evkeeza® (evinacumab) is approved in the U.S. and the European Economic Area, or EEA, for the treatment of homozygous familial hypercholesterolemia, or HoFH. The Company has exclusive rights to commercialize Evkeeza® (evinacumab) outside of the U.S.

In addition to the approved products, the Company has the following ongoing clinical development programs:

The Company has sustained operating losses and expects such annual losses to continue over the next several years. The Company’s ultimate success depends on the outcome of its research and development and commercialization activities. Through September 30, 2023, the Company has relied primarily on its sale of equity securities, its revenues from commercial products, its sale of future royalties, and strategic collaboration arrangements to finance its operations. The Company expects it will need to raise additional capital to fully implement its business plans through the issuance of equity, borrowings, or strategic alliances with partner companies. However, if such financing is not available at adequate levels, the Company would need to reevaluate its operating plans.

2. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited Condensed Consolidated Financial Statements include the accounts of the Company and its wholly-owned subsidiaries and have been prepared in accordance with U.S. generally accepted accounting principles, or GAAP, for interim financial information and in accordance with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X.

9

Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. The unaudited interim Condensed Consolidated Financial Statements have been prepared on the same basis as the annual financial statements. In the opinion of management, the accompanying unaudited Condensed Consolidated Financial Statements reflect all adjustments (consisting only of normal recurring adjustments) considered necessary for a fair presentation. These financial statements should be read in conjunction with the audited financial statements and notes thereto for the preceding fiscal year contained in the Company’s Annual Report on Form 10-K filed on February 17, 2023, or Annual Report, with the United States Securities and Exchange Commission, or the SEC.

The results of operations for the three and nine months ended September 30, 2023 are not necessarily indicative of the results to be expected for the year ending December 31, 2023. The Condensed Consolidated Balance Sheet as of December 31, 2022 has been derived from audited financial statements at that date, but does not include all of the information required by GAAP for complete financial statements.

Use of Estimates

The accompanying Condensed Consolidated Financial Statements have been prepared in accordance with GAAP. The preparation of the Condensed Consolidated Financial Statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent liabilities and the reported amounts of expenses in the Condensed Consolidated Financial Statements and the accompanying notes. On an ongoing basis, management evaluates its estimates, including those related to clinical trial accruals, fair value of assets and liabilities, income taxes, stock-based compensation, revenue recognition, and the liabilities for sales of future royalties. Management bases its estimates on historical experience and on various other market-specific and relevant assumptions that management believes to be reasonable under the circumstances. Actual results could differ from those estimates.

Cash, Cash Equivalents and Restricted Cash

Restricted cash primarily consists of money market accounts used as collateral for the Company’s obligations under its facility leases. The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported within the Condensed Consolidated Balance Sheets that sum to the total of the same such amounts shown in the Condensed Consolidated Statement of Cash Flows (in thousands):

|

September 30, |

|

|||||

|

2023 |

|

|

2022 |

|

||

Cash and cash equivalents |

$ |

72,575 |

|

|

$ |

391,651 |

|

Restricted cash included in prepaid expenses and |

|

1,976 |

|

|

|

517 |

|

Restricted cash included in other assets |

|

4,056 |

|

|

|

4,140 |

|

Total cash, cash equivalents, and restricted cash |

$ |

78,607 |

|

|

$ |

396,308 |

|

Credit Losses

The Company is exposed to credit losses primarily through receivables from customers and collaborators and through its available-for-sale debt securities. For trade receivables and other instruments, the Company uses a forward-looking expected loss model that generally results in the earlier recognition of allowances for losses. For available-for-sale debt securities with unrealized losses, the losses are recognized as allowances rather than as reductions in the amortized cost of the securities.

The Company’s expected loss allowance methodology for the receivables is developed using historical collection experience, current and future economic market conditions, a review of the current aging status and financial condition of the entities. Specific allowance amounts are established to record the appropriate allowance for customers that have a higher probability of default. Balances are written off when determined to be uncollectible. The Company’s expected loss allowance methodology for the debt securities is developed by reviewing the extent of the unrealized loss, the size, term, geographical location, and industry of the issuer, the issuers’ credit ratings and any changes in those ratings, as well as reviewing current and future economic market conditions and the issuers’ current status and financial condition. There were no material credit losses recorded for receivables and available-for-sale debt securities for the three and nine months ended September 30, 2023 and 2022.

10

Revenue Recognition

Product Sales

The Company sells its approved products through a limited number of distributors. Under ASC 606, revenue from product sales is recognized at the point in time when the delivery is made and when title and risk of loss transfers to these distributors. The Company also recognizes revenue from sales of certain products on a “named patient” basis, which are allowed in certain countries prior to the commercial approval of the product. Prior to recognizing revenue, the Company makes estimates of the transaction price, including any variable consideration that is subject to a constraint. Amounts of variable consideration are included in the transaction price to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur and when the uncertainty associated with the variable consideration is subsequently resolved. Product sales are recorded net of estimated government-mandated rebates and chargebacks, estimated product returns, and other deductions.

Provisions for returns and other adjustments are provided for in the period the related revenue is recorded, as estimated by management. These reserves are based on estimates of the amounts earned or to be claimed on the related sales and are reviewed periodically and adjusted as necessary. The Company’s estimates of government mandated rebates, chargebacks, estimated product returns, and other deductions depends on the identification of key customer contract terms and conditions, as well as estimates of sales volumes to different classes of payors. If actual results vary, the Company may need to adjust these estimates, which could have a material effect on earnings in the period of the adjustment.

Collaboration, License, and Royalty Revenue

The Company has certain license and collaboration agreements that are within the scope of Accounting Standards Codification, or ASC, 808, Collaborative Agreements, which provides guidance on the presentation and disclosure of collaborative arrangements. Generally, the classification of the transactions under the collaborative arrangements is determined based on the nature of contractual terms of the arrangement, along with the nature of the operations of the participants. The Company records its share of collaboration revenue, net of transfer pricing related to net sales in the period in which such sales occur, if the Company is considered as an agent in the arrangement. The Company is considered an agent when the collaboration partner controls the product before transfer to the customers and has the ability to direct the use of and obtain substantially all of the remaining benefits from the product. Funding received related to research and development services and commercialization costs is generally classified as a reduction of research and development expenses and selling, general and administrative expenses, respectively, in the Condensed Consolidated Statements of Operations, because the provision of such services for collaborative partners are not considered to be part of the Company’s ongoing major or central operations.

In order to record collaboration revenue, the Company utilizes certain information from its collaboration partners, including revenue from the sale of the product, associated reserves on revenue, and costs incurred for development and sales activities. For the periods covered in the financial statements presented, there have been no material changes to prior period estimates of revenues and expenses.

The Company also records royalty revenues under certain of the Company’s license or collaboration agreements in exchange for license of intellectual property. If the Company does not have any future performance obligations for these license or collaboration agreements, royalty revenue is recorded as the underlying sales occur.

The Company sold the right to receive certain royalty payments from net sales of Crysvita in certain territories to RPI Finance Trust, or RPI, an affiliate of Royalty Pharma, and to OCM LS23 Holdings LP, an investment vehicle for Ontario Municipal Employees Retirement System, or OMERS, as further described in “Note 8 Liabilities for Sales of Future Royalties”. The Company records the royalty revenue from the net sales of Crysvita in the applicable territories on a prospective basis as royalty revenue in the Condensed Consolidated Statements of Operations over the term of the applicable arrangement.

The terms of the Company’s collaboration and license agreements may contain multiple performance obligations, which may include licenses and research and development activities. The Company evaluates these agreements under ASC 606, Revenue from Contracts with Customers, or ASC 606, to determine the distinct performance obligations. The Company analogizes to ASC 606 for the accounting for distinct performance obligations for which there is a customer relationship. Prior to recognizing revenue, the Company makes estimates of the transaction price, including variable consideration that is subject to a constraint. Amounts of variable consideration are included in the transaction price to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur and when the uncertainty associated with the variable consideration is subsequently resolved. Total consideration may include nonrefundable upfront license fees, payments for research and development activities, reimbursement of certain third-party costs, payments based upon the achievement of specified milestones, and royalty payments based on product sales derived from the collaboration.

If there are multiple distinct performance obligations, the Company allocates the transaction price to each distinct performance obligation based on its relative standalone selling price. The standalone selling price is generally determined based on the prices charged to customers or using expected cost-plus margin.

11

The Company estimates the efforts needed to complete the performance obligations and recognizes revenue by measuring the progress towards complete satisfaction of the performance obligations using input measures.

Deferred Compensation Plan

The Company maintains a nonqualified deferred compensation plan whereby certain employees and members of the board of directors are able to defer certain equity awards and other compensation. Amounts deferred are invested into various mutual funds. The plan complies with the provisions of Section 409A of the Internal Revenue Code. All of the various mutual funds held in the plan are classified as trading securities and recorded at fair value in other non-current assets in the Condensed Consolidated Balance Sheets with changes in fair value recognized as earnings in the period they occur. The corresponding liability for the plan is included in other non-current liabilities in the Condensed Consolidated Balance Sheets. Certain equity awards deferred under the plan are required to be settled through the issuance of Company stock. These awards are recorded as treasury stock and deferred compensation obligation within stockholders’ equity.

3. Financial Instruments

Financial assets and liabilities are recorded at fair value. The carrying amount of certain financial instruments, including cash and cash equivalents, accounts receivable, accounts payable and accrued liabilities approximate fair value due to their relatively short maturities. Assets and liabilities recorded at fair value on a recurring basis in the balance sheets are categorized based upon the level of judgment associated with the inputs used to measure their fair values. Fair value is defined as the exchange price that would be received for an asset or an exit price that would be paid to transfer a liability in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. The authoritative guidance on fair value measurements establishes a three-tier fair value hierarchy for disclosure of fair value measurements as follows:

Level 1—Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date;

Level 2—Inputs are observable, unadjusted quoted prices in active markets for similar assets or liabilities, unadjusted quoted prices for identical or similar assets or liabilities in markets that are not active, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the related assets or liabilities; and

Level 3—Unobservable inputs that are significant to the measurement of the fair value of the assets or liabilities that are supported by little or no market data.

The Company determines the fair value of its equity investment in Solid Biosciences Inc., or Solid, by using the quoted market prices, which are Level 1 fair value measurements.

The following tables set forth the fair value of the Company’s financial assets remeasured on a recurring basis based on the three-tier fair value hierarchy (in thousands):

|

September 30, 2023 |

|

|||||||||||||

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

|

||||

Money market funds |

$ |

34,222 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

34,222 |

|

Certificates of deposit and time deposit |

|

— |

|

|

|

13,844 |

|

|

|

— |

|

|

|

13,844 |

|

Corporate bonds |

|

— |

|

|

|

142,398 |

|

|

|

— |

|

|

|

142,398 |

|

Commercial paper |

|

— |

|

|

|

46,175 |

|

|

|

— |

|

|

|

46,175 |

|

Asset-backed securities |

|

— |

|

|

|

5,826 |

|

|

|

— |

|

|

|

5,826 |

|

U.S. Government Treasury and agency securities |

|

66,437 |

|

|

|

186,910 |

|

|

|

— |

|

|

|

253,347 |

|

Investment in Solid common stock |

|

1,315 |

|

|

|

— |

|

|

|

— |

|

|

|

1,315 |

|

Other |

|

— |

|

|

|

9,890 |

|

|

|

— |

|

|

|

9,890 |

|

Total |

$ |

101,974 |

|

|

$ |

405,043 |

|

|

$ |

— |

|

|

$ |

507,017 |

|

12

|

December 31, 2022 |

|

|||||||||||||

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

|

||||

Money market funds |

$ |

102,847 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

102,847 |

|

Certificates of deposit and time deposit |

|

— |

|

|

|

25,972 |

|

|

|

— |

|

|

|

25,972 |

|

Corporate bonds |

|

— |

|

|

|

427,598 |

|

|

|

— |

|

|

|

427,598 |

|

Commercial paper |

|

— |

|

|

|

135,393 |

|

|

|

— |

|

|

|

135,393 |

|

Asset-backed securities |

|

— |

|

|

|

11,980 |

|

|

|

— |

|

|

|

11,980 |

|

U.S. Government Treasury and agency securities |

|

27,645 |

|

|

|

129,345 |

|

|

|

— |

|

|

|

156,990 |

|

Debt securities in government-sponsored entities |

|

— |

|

|

|

15,855 |

|

|

|

— |

|

|

|

15,855 |

|

Investment in Solid common stock |

|

2,807 |

|

|

|

— |

|

|

|

— |

|

|

|

2,807 |

|

Other |

|

— |

|

|

|

4,575 |

|

|

|

— |

|

|

|

4,575 |

|

Total |

$ |

133,299 |

|

|

$ |

750,718 |

|

|

$ |

— |

|

|

$ |

884,017 |

|

4. Balance Sheet Components

Cash Equivalents and Marketable Debt Securities

The fair values of cash equivalents and marketable debt securities classified as available-for-sale securities consisted of the following (in thousands):

|

September 30, 2023 |

|

||||||||||||||

|

|

|

|

|

Gross Unrealized |

|

|

|

|

|||||||

|

|

Amortized |

|

|

Gains |

|

|

Losses |

|

|

Estimated |

|

||||

Money market funds |

|

$ |

34,222 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

34,222 |

|

Certificates of deposit and time deposit |

|

|

13,844 |

|

|

|

— |

|

|

|

— |

|

|

|

13,844 |

|

Corporate bonds |

|

|

143,261 |

|

|

|

39 |

|

|

|

(902 |

) |

|

|

142,398 |

|

Commercial paper |

|

|

46,175 |

|

|

|

— |

|

|

|

— |

|

|

|

46,175 |

|

Asset-backed securities |

|

|

5,844 |

|

|

|

— |

|

|

|

(18 |

) |

|

|

5,826 |

|

U.S. Government Treasury and agency securities |

|

|

254,053 |

|

|

|

1 |

|

|

|

(707 |

) |

|

|

253,347 |

|

Total |

|

$ |

497,399 |

|

|

$ |

40 |

|

|

$ |

(1,627 |

) |

|

$ |

495,812 |

|

|

December 31, 2022 |

|

||||||||||||||

|

|

|

|

|

Gross Unrealized |

|

|

|

|

|||||||

|

|

Amortized |

|

|

Gains |

|

|

Losses |

|

|

Estimated |

|

||||

Money market funds |

|

$ |

102,847 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

102,847 |

|

Certificates of deposit and time deposit |

|

|

25,972 |

|

|

|

— |

|

|

|

— |

|

|

|

25,972 |

|

Corporate bonds |

|

|

432,211 |

|

|

|

87 |

|

|

|

(4,700 |

) |

|

|

427,598 |

|

Commercial paper |

|

|

135,393 |

|

|

|

— |

|

|

|

— |

|

|

|

135,393 |

|

Asset-backed securities |

|

|

12,002 |

|

|

|

— |

|

|

|

(22 |

) |

|

|

11,980 |

|

U.S. Government Treasury and agency securities |

|

|

157,933 |

|

|

|

320 |

|

|

|

(1,263 |

) |

|

|

156,990 |

|

Debt securities in government-sponsored entities |

|

|

16,005 |

|

|

|

— |

|

|

|

(150 |

) |

|

|

15,855 |

|

Total |

|

$ |

882,363 |

|

|

$ |

407 |

|

|

$ |

(6,135 |

) |

|

$ |

876,635 |

|

At September 30, 2023, the remaining contractual maturities of available-for-sale securities were less than three years. There have been no significant realized gains or losses on available-for-sale securities for the periods presented. For investments with unrealized losses, the Company does not intend to sell the investments and it is not more likely than not that the Company will be required to sell the investments before recovery of their amortized cost basis.

13

Inventory

Inventory consists of the following (in thousands):

|

|

September 30, |

|

|

December 31, |

|

||

|

|

2023 |

|

|

2022 |

|

||

Work-in-process |

|

$ |

19,173 |

|

|

$ |

17,486 |

|

Finished goods |

|

|

12,629 |

|

|

|

9,280 |

|

Total inventory |

|

$ |

31,802 |

|

|

$ |

26,766 |

|

Accrued Liabilities

Accrued liabilities consist of the following (in thousands):

|

|

September 30, |

|

|

December 31, |

|

||

|

|

2023 |

|

|

2022 |

|

||

Research, clinical study, and manufacturing expenses |

|

$ |

51,520 |

|

|

$ |

73,558 |

|

Payroll and related expenses |

|

|

76,300 |

|

|

|

78,938 |

|

Other |

|

|

50,802 |

|

|

|

52,182 |

|

Total accrued liabilities |

|

$ |

178,622 |

|

|

$ |

204,678 |

|

5. Revenue

The following table disaggregates total revenues from external customers by product sales, royalty revenue, and collaboration and license revenue (in thousands):

|

Three Months Ended |

|

|

Nine Months Ended |

|

||||||||||

|

September 30, |

|

|

September 30, |

|

||||||||||

|

2023 |

|

|

2022 |

|

|

2023 |

|

|

2022 |

|

||||

Product sales: |

|

|

|

|

|

|

|

|

|

|

|

||||

Crysvita |

$ |

19,200 |

|

|

$ |

13,184 |

|

|

$ |

57,318 |

|

|

$ |

34,980 |

|

Mepsevii |

|

5,633 |

|

|

|

6,045 |

|

|

|

22,552 |

|

|

|

15,839 |

|

Dojolvi |

|

16,553 |

|

|

|

13,274 |

|

|

|

47,347 |

|

|

|

39,200 |

|

Evkeeza |

|

963 |

|

|

|

— |

|

|

|

1,540 |

|

|

|

— |

|

Total product sales |

|

42,349 |

|

|

|

32,503 |

|

|

|

128,757 |

|

|

|

90,019 |

|

Crysvita royalty revenue |

|

55,703 |

|

|

|

5,373 |

|

|

|

106,916 |

|

|

|

15,634 |

|

Collaboration and license revenue: |

|

|

|

|

|

|

|

|

|

|

|

||||

Crysvita collaboration revenue in profit- |

|

— |

|

|

|

51,348 |

|

|

|

69,705 |

|

|

|

148,121 |

|

Daiichi Sankyo |

|

— |

|

|

|

1,479 |

|

|

|

1,479 |

|

|

|

6,207 |

|

Total collaboration and license revenue |

|

— |

|

|

|

52,827 |

|

|

|

71,184 |

|

|

|

154,328 |

|

Total revenues |

$ |

98,052 |

|

|

$ |

90,703 |

|

|

$ |

306,857 |

|

|

$ |

259,981 |

|

The following table disaggregates total revenues based on geographic location (in thousands):

|

Three Months Ended |

|

|

Nine Months Ended |

|

||||||||||

|

September 30, |

|

|

September 30, |

|

||||||||||

|

2023 |

|

|

2022 |

|

|

2023 |

|

|

2022 |

|

||||

North America |

$ |

67,811 |

|

|

$ |

67,012 |

|

|

$ |

214,232 |

|

|

$ |

196,257 |

|

Latin America |

|

17,229 |

|

|

|

14,119 |

|

|

|

59,096 |

|

|

|

36,449 |

|

Europe |

|

13,012 |

|

|

|

8,411 |

|

|

|

32,351 |

|

|

|

26,114 |

|

Japan |

|

— |

|

|

|

1,161 |

|

|

|

1,178 |

|

|

|

1,161 |

|

Total revenues |

$ |

98,052 |

|

|

$ |

90,703 |

|

|

$ |

306,857 |

|

|

$ |

259,981 |

|

14

The following table presents changes in the contract liabilities (in thousands):

|

Nine Months Ended September 30, |

|

|||||

|

2023 |

|

|

2022 |

|

||

Balance of contract liabilities at beginning of period |

$ |

1,479 |

|

|

$ |

9,076 |

|

Additions |

|

— |

|

|

|

89 |

|

Deductions |

|

(1,479 |

) |

|

|

(6,207 |

) |

Balance of contract liabilities at end of period, net |

$ |

— |

|

|

$ |

2,958 |

|

See Note 7 for additional details on contract liabilities activities.

The Company’s largest accounts receivable balance was from a collaboration partner and accounted for 68% and 68% of the total accounts receivable balance as of September 30, 2023 and December 31, 2022, respectively.

6. GeneTx Acquisition

In August 2019, the Company entered into a Program Agreement and a Unitholder Option Agreement with GeneTx Biotherapeutics LLC, or GeneTx, to collaborate on the development of GeneTx’s GTX-102, an ASO for the treatment of Angelman syndrome. Pursuant to the terms of the Unitholder Option Agreement, the Company made an upfront payment of $20.0 million for an exclusive option to acquire GeneTx, which was exercisable any time prior to 30 days following FDA acceptance of the Investigational New Drug Application, or IND, for GTX-102. Pursuant to the agreement, upon acceptance of the IND, which occurred in January 2020, the Company elected to extend the option period by paying an option extension payment of $25.0 million during the quarter ended March 31, 2020, which was recorded as an in-process research and development expense. In April 2022, the parties entered into an amendment to the Unitholder Option Agreement, or the Amendment, which provided the Company with an additional, earlier option to acquire GeneTx for an option exercise price of $75.0 million based on the earlier of receipt of interim data in the Phase 1/2 study or a specified date, such option, the Interim Option.

In July 2022, the Company exercised the Interim Option to acquire GeneTx and entered into a Unit Purchase Agreement, or the Purchase Agreement, pursuant to which the Company purchased all the outstanding units of GeneTx. In accordance with the terms of the Purchase Agreement, the Company paid the option exercise price of $75.0 million and an additional $15.6 million to acquire the outstanding cash of GeneTx, and adjustments for working capital and transaction expenses of $0.6 million, for a total purchase consideration of $91.2 million. Additionally, the Company may make payments of up to $190.0 million upon the achievement of certain milestones, including up to $30.0 million in milestone payments upon achievement of the earlier of initiation of a Phase 3 clinical study or product approvals in Canada and the U.K., up to $85.0 million in additional regulatory approval milestones for the achievement of U.S. and EU product approvals, and up to $75.0 million in commercial milestone payments based on annual worldwide net product sales. In addition, the Company will also pay tiered mid- to high single-digit percentage royalties based on licensed product annual net sales. If the Company receives and resells an FDA priority review voucher, or PRV, in connection with a new drug application approval, GeneTx is entitled to receive a portion of proceeds from the sale or a cash payment from the Company if the Company choses to retain the PRV.

The transaction was accounted as an asset acquisition, as substantially all of the fair value of the gross assets acquired was concentrated in a single identifiable in-process research and development intangible asset. Prior to the achievement of certain development and regulatory milestones, the acquired in-process research and development intangible asset has not yet reached technological feasibility and has no alternative future use. Accordingly, the Company recorded the acquisition price of $75.0 million, net of cash and working capital acquired, as in-process research and development expense during the year ended December 31, 2022.

7. License and Research Agreements

Kyowa Kirin Co., Ltd.

In August 2013, the Company entered into a collaboration and license agreement with Kyowa Kirin Co., Ltd., or KKC (formerly Kyowa Hakko Kirin Co., Ltd. or KHK). Under the terms of this collaboration and license agreement, as amended, the Company and KKC collaborate on the development and commercialization of Crysvita in the field of orphan diseases in the U.S. and Canada, or the profit-share territory, and in the European Union, United Kingdom, and Switzerland, or the European territory, and the Company has the right to develop and commercialize such products in the field of orphan diseases in Mexico and Central and South America, or Latin America.

15

Development Activities

In the field of orphan diseases, and except for ongoing studies being conducted by KKC, the Company was the lead party for development activities in the profit-share territory and in the European territory until the applicable transition date. The Company shared the costs for development activities in the profit-share territory and the European territory conducted pursuant to the development plan before the applicable transition date equally with KKC. In April 2023, which was the transition date for the profit-share territory, KKC became the lead party and is responsible for the costs of the development activities. However, the Company will continue to share the costs of the studies commenced prior to the applicable transition date equally with KKC.

The collaboration and license agreements are within the scope of ASC 808, which provides guidance on the presentation and disclosure of collaborative arrangements.

Collaboration and Royalty Revenue for Sales in the Profit-share Territory

The Company and KKC shared commercial responsibilities and profits in the profit-share territory until April 2023. Under the collaboration agreement, KKC manufactured and supplied Crysvita for commercial use in the profit-share territory and charged the Company a transfer price of 30% of net sales. The transfer price on these sales was 35% prior to December 31, 2022. The remaining profit or loss after supply costs from commercializing products in the profit-share territory was shared between the Company and KKC on a 50/50 basis until April 2023. In April 2023, commercialization responsibilities for Crysvita in the profit-share territory transitioned to KKC and KKC assumed responsibility for the commercialization of Crysvita in the territory at and after April 2023. Thereafter, the Company is entitled to receive a tiered double-digit revenue share from the mid-20% range up to a maximum rate of 30%.

In September 2022, the Company entered into an amendment to the collaboration agreement which clarified the scope of increased participation by KKC in support of the Company’s commercial activities prior to April 2023 and granted the Company the right to continue to support KKC in commercial field activities in the U.S. through April 2024, subject to the limitations and conditions set forth in the amendment. As a result, the Company will continue to support commercial field and marketing efforts through a cost share arrangement through April 2024, subject to the limits and conditions set forth in the amendment. After April 2024, the Company’s rights to promote Crysvita in the U.S. will be limited to medical geneticists and the Company will solely bear its expenses for the promotion of Crysvita in the profit-share territory.

As KKC is the principal in the sale transaction with the customer, the Company recognizes a pro-rata share of collaboration revenue, net of transfer pricing, in the period the sale occurs. The Company concluded that its portion of KKC’s sales in the profit-share territory prior to April 2023 was analogous to a royalty and therefore recorded its share as collaboration revenue, similar to a royalty. Starting in April 2023, the Company began to record the royalty revenue as the underlying sales occur.

In July 2022, the Company sold to OMERS its right to receive 30% of the future royalty payments due to the Company based on net sales of Crysvita in the U.S. and Canada, subject to a cap, beginning in April 2023, as further described in Note 8. The Company records this revenue as royalty revenue.

Royalty Revenue for Sales in the European Territory

KKC has the commercial responsibility for Crysvita in the European territory. In December 2019, the Company sold its right to receive royalty payments based on sales in the European territory to Royalty Pharma, effective January 1, 2020, as further described in “Note 8. Liabilities for Sales of Future Royalties.” Prior to the Company’s sale of the royalty, the Company received a royalty of up to 10% on net sales in the European territory, which was recognized as the underlying sales occur. The Company records this revenue as royalty revenue.

Product Revenue for Sales in Other Territories

The Company is responsible for commercializing Crysvita in Latin America and Turkey. The Company is considered the principal in these territories as the Company controls the product before it is transferred to the customer. Accordingly, the Company records revenue on a gross basis for the sale of Crysvita once the product is delivered and the risk and title of the product is transferred to the distributor. KKC has the option to assume responsibility for commercialization efforts in Turkey from the Company, after a certain minimum period.

Under the collaboration agreement, KKC manufactures and supplies Crysvita, which is purchased by the Company for sales in Latin American territories and charges the Company a transfer price of 30% of net sales. The transfer price on these sales was 35% prior to December 31, 2022. The Company also pays to KKC a low single-digit royalty on net sales in Latin America.

Total Crysvita revenue was as follows (in thousands):

16

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

2023 |

|

|

2022 |

|

|

2023 |

|

|

2022 |

|

||||

Revenue in profit-share territory: |

|

|

|

|

|

|

|

|

|

|

|

||||

Collaboration revenue |

$ |

— |

|

|

$ |

51,348 |

|

|

$ |

69,705 |

|

|

$ |

148,121 |

|

Royalty revenue |

|

35,160 |

|

|

|

— |

|

|

|

64,221 |

|

|

|

— |

|

Non-cash royalty revenue |

|

15,070 |

|

|

|

— |

|

|

|

27,524 |

|

|

|

— |

|

Total revenue in profit-share territory |

|

50,230 |

|

|

|

51,348 |

|

|