Document

FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of April, 2025

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

BANCO SANTANDER, S.A.

________________________

TABLE OF CONTENTS

|

|

|

|

|

|

|

|

|

|

|

Item 1. January - March 2025 Financial Report |

|

Index

This report was approved by the board of directors on 29 April 2025, following a favourable report from the audit committee. Important information regarding this report can be found on pages 90 and 91.

Key consolidated data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| BALANCE SHEET (EUR million) |

Mar-25 |

Dec-24 |

% |

|

Mar-24 |

% |

Dec-24 |

| Total assets |

1,845,177 |

|

1,837,081 |

|

0.4 |

|

|

1,800,006 |

|

2.5 |

|

1,837,081 |

|

| Loans and advances to customers |

1,064,416 |

|

1,054,069 |

|

1.0 |

|

|

1,049,533 |

|

1.4 |

|

1,054,069 |

|

| Customer deposits |

1,081,894 |

|

1,055,936 |

|

2.5 |

|

|

1,044,453 |

|

3.6 |

|

1,055,936 |

|

| Total funds |

1,386,326 |

|

1,348,422 |

|

2.8 |

|

|

1,315,779 |

|

5.4 |

|

1,348,422 |

|

| Total equity |

110,514 |

|

107,327 |

|

3.0 |

|

|

105,025 |

|

5.2 |

|

107,327 |

|

| Note: total funds includes customer deposits, mutual funds, pension funds and managed portfolios. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INCOME STATEMENT (EUR million) |

Q1'25 |

Q4'24 |

% |

|

Q1'24 |

% |

2024 |

| Net interest income |

11,378 |

|

11,986 |

|

(5.1) |

|

|

11,983 |

|

(5.0) |

|

46,668 |

|

| Total income |

15,537 |

|

16,026 |

|

(3.1) |

|

|

15,045 |

|

3.3 |

|

61,876 |

|

|

|

|

|

|

|

|

|

| Net operating income |

9,048 |

|

9,254 |

|

(2.2) |

|

|

8,498 |

|

6.5 |

|

35,842 |

|

|

|

|

|

|

|

|

|

| Profit before tax |

5,187 |

|

4,600 |

|

12.8 |

|

|

4,583 |

|

13.2 |

|

19,027 |

|

| Profit attributable to the parent |

3,402 |

|

3,265 |

|

4.2 |

|

|

2,852 |

|

19.3 |

|

12,574 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EPS, PROFITABILITY AND EFFICIENCY (%) 1 |

Q1'25 |

Q4'24 |

% |

|

Q1'24 |

% |

2024 |

| EPS (euros) |

0.21 |

|

0.20 |

|

5.8 |

|

|

0.17 |

|

26.1 |

|

0.77 |

|

| RoE |

13.4 |

|

13.3 |

|

|

|

11.9 |

|

|

13.0 |

|

| RoTE |

16.6 |

|

16.6 |

|

|

|

14.9 |

|

|

16.3 |

|

| RoTE (post-AT1) |

15.8 |

|

15.7 |

|

|

|

14.1 |

|

|

15.5 |

|

| RoA |

0.81 |

|

0.78 |

|

|

|

0.69 |

|

|

0.76 |

|

| RoRWA |

2.34 |

|

2.27 |

|

|

|

1.96 |

|

|

2.18 |

|

Efficiency ratio 2 |

41.8 |

|

42.3 |

|

|

|

42.6 |

|

|

41.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNDERLYING INCOME STATEMENT 2 (EUR million) |

Q1'25 |

Q4'24 |

% |

|

Q1'24 |

% |

2024 |

| Net interest income |

11,378 |

|

11,986 |

|

(5.1) |

|

|

11,983 |

|

(5.0) |

|

46,668 |

|

| Total income |

15,537 |

|

16,026 |

|

(3.1) |

|

|

15,380 |

|

1.0 |

|

62,211 |

|

|

|

|

|

|

|

|

|

| Net operating income |

9,048 |

|

9,254 |

|

(2.2) |

|

|

8,833 |

|

2.4 |

|

36,177 |

|

|

|

|

|

|

|

|

|

| Profit before tax |

5,187 |

|

4,600 |

|

12.8 |

|

|

4,583 |

|

13.2 |

|

19,027 |

|

| Profit attributable to the parent |

3,402 |

|

3,265 |

|

4.2 |

|

|

2,852 |

|

19.3 |

|

12,574 |

|

| Changes in constant euros: |

|

|

|

|

|

| Q1'25 / Q4'24: NII: -5.6%; Total income: -3.5%; Net operating income: -2.8%; Profit before tax: +12.4%; Attributable profit: +4.2%. |

| Q1'25 / Q1'24: NII: -1.7%; Total income: +4.8%; Net operating income: +6.9%; Profit before tax: +17.5%; Attributable profit: +23.9%. |

|

|

|

Note: for Argentina and any grouping which includes it, the variations in constant euros have been calculated considering the Argentine peso exchange rate on the last working day for each of the periods presented. Additionally, from Q2 2024 onwards for the Argentine peso, we apply an alternative exchange rate that better reflects the evolution of inflation (we continue to apply the official ARS exchange rate to all prior periods). For further information, see the 'Alternative performance measures' section in the appendix to this report. Certain figures contained in this report, have been subject to rounding to enhance their presentation. Accordingly, in certain instances, the sum of the numbers in a column or a row in tables contained in this report may not conform exactly to the total figure given for that column or row.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SOLVENCY (%) |

Mar-25 |

Dec-24 |

|

|

Mar-24 |

|

Dec-24 |

| Phased-in CET1 ratio |

12.9 |

|

12.8 |

|

|

|

12.3 |

|

|

12.8 |

|

| Phased-in total capital ratio |

17.2 |

|

17.4 |

|

|

|

16.6 |

|

|

17.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CREDIT QUALITY (%)1 |

Q1'25 |

Q4'24 |

|

|

Q1'24 |

|

2024 |

Cost of risk 2, 3 |

1.14 |

|

1.15 |

|

|

|

1.20 |

|

|

1.15 |

|

| NPL ratio |

2.99 |

|

3.05 |

|

|

|

3.10 |

|

|

3.05 |

|

| NPL coverage ratio |

65.7 |

|

64.8 |

|

|

|

66.1 |

|

|

64.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| MARKET CAPITALIZATION AND SHARES |

Mar-25 |

Dec-24 |

% |

|

Mar-24 |

% |

Dec-24 |

| Shares (millions) |

15,152 |

|

15,152 |

|

0.0 |

|

|

15,826 |

|

(4.3) |

|

15,152 |

|

| Number of shareholders |

3,435,876 |

|

3,485,134 |

|

(1.4) |

|

|

3,584,294 |

|

(4.1) |

3,485,134 |

|

| Share price (euros) |

6.196 |

|

4.465 |

|

38.8 |

|

|

4.522 |

|

37.0 |

|

4.465 |

|

| Market capitalization (EUR million) |

93,885 |

|

67,648 |

|

38.8 |

|

|

71,555 |

|

31.2 |

|

67,648 |

|

| Tangible book value per share (euros) |

5.46 |

|

5.24 |

|

|

|

4.86 |

|

|

5.24 |

|

| Price / Tangible book value per share (X) |

1.13 |

|

0.85 |

|

|

|

0.93 |

|

|

0.85 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CUSTOMERS (thousands) |

Mar-25 |

Dec-24 |

% |

|

Mar-24 |

% |

Dec-24 |

| Total customers |

174,769 |

|

172,537 |

|

1.3 |

|

|

165,752 |

|

5.4 |

172,537 |

|

| Active customers |

104,179 |

|

103,262 |

|

0.9 |

|

|

100,092 |

|

4.1 |

|

103,262 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Digital customers |

60,651 |

|

59,317 |

|

2.2 |

|

|

55,305 |

|

9.7 |

59,317 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| OTHER DATA |

Mar-25 |

Dec-24 |

% |

|

Mar-24 |

% |

Dec-24 |

|

|

|

|

|

|

|

|

| Number of employees |

207,137 |

|

206,753 |

|

0.2 |

|

|

211,141 |

|

(1.9) |

|

206,753 |

|

| Number of branches |

7,910 |

|

8,011 |

|

(1.3) |

|

|

8,405 |

|

(5.9) |

|

8,011 |

|

|

|

|

|

|

|

| 1. |

|

| 2. |

In addition to financial information prepared in accordance with International Financial Reporting Standards (IFRS) and derived from our consolidated financial statements, this report contains certain financial measures that constitute alternative performance measures (APMs) as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority (ESMA) on 5 October 2015, and other non-IFRS measures, including the figures related to “underlying” results, which do not include factors that are outside the ordinary course of our business, or have been reclassified within the underlying income statement. Further details are provided in the 'Alternative performance measures' section of the appendix to this report. For further details on the APMs and non-IFRS measures used, including their definition or a reconciliation between any applicable management indicators and the financial data presented in the annual consolidated financial statements prepared under IFRS, please see our 2024 Annual Financial Report, published in the CNMV on 28 February 2025, our 20-F report for the year ending 31 December 2024 filed with the SEC in the United States on 28 February 2025 as well as the 'Alternative performance measures' section of the appendix to this report.

|

|

|

|

|

| 3. |

Allowances for loan-loss provisions over the last 12 months / Average loans and advances to customers over the last 12 months. |

OUR BUSINESS MODEL

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CUSTOMER FOCUS |

Building a digital bank with branches |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

→ We continue to build a digital bank with branches, with a multichannel offering to fulfil all our customers' financial needs. |

|

|

175 mn |

|

104 mn |

|

|

|

total customers |

|

active customers |

|

|

|

|

|

|

|

|

|

|

| SCALE |

Global and in-market scale |

|

|

|

|

|

|

|

|

|

|

→ Our global and in-market scale helps us to improve our local banks' profitability, adding value and network benefits.

→ Our activities are organized under five global businesses: Retail & Commercial Banking (Retail), Digital Consumer Bank (Consumer), Corporate & Investment Banking (CIB), Wealth Management & Insurance (Wealth) and Payments.

→ Our five global businesses support value creation based on the profitable growth and operational leverage that ONE Santander provides.

|

|

|

|

|

|

|

|

|

|

|

|

| DIVERSIFICATION |

Business, geographical and balance sheet |

|

|

|

|

|

|

|

|

|

→ Well-balanced diversification between businesses and markets with a solid and simple balance sheet that gives us recurrent net operating income with low volatility and more predictable results. |

Our corporate culture

The Santander Way remains unchanged to continue to deliver for all our stakeholders.

|

|

|

|

|

|

|

|

|

|

|

|

|

Our purpose |

|

|

|

|

|

|

To help people and businesses prosper |

|

|

|

|

|

Our aim |

|

|

|

|

|

To be the best open financial services platform, by acting responsibly and earning the lasting loyalty of our people, customers, shareholders and communities |

|

|

|

|

|

Our how |

|

|

|

|

|

Everything we do should be Simple, Personal and Fair |

|

|

|

|

GROUP FINANCIAL INFORMATION

General background

Grupo Santander's operating environment in Q1 2025 was characterized by a moderate global economic slowdown, with falling interest rates and a decline in inflation across most of our footprint. Labour markets continued to have relatively low unemployment rates across most of our countries. Geopolitical and commercial tensions have increased and there has been greater volatility in global financial markets. Looking ahead, and with the information available to date on the events that have occurred in the second quarter (trade tensions and market volatility), these trends could intensify.

|

|

|

|

|

|

|

|

|

|

|

|

Country |

GDP Change1 |

Economic performance |

|

Eurozone |

+1.2% |

Economic activity was weak in Q1 2025, reflected in confidence indicators which remained at low levels. Inflation fell to 2.2% in March. Although it seemed in March that the ECB would pause interest rate cuts, in April it reduced rates again to 2.25% due to the greater uncertainty regarding global trade and concerns over economic growth. |

|

Spain |

+3.4% |

The Spanish economy has begun 2025 positively, albeit less so than in previous quarters. This points to solid growth, though more contained in the year as a whole, driven by internal demand. The labour market remains strong, with the number of people enrolled in social security at record levels. Inflation fell to 2.3% in March, with a moderation in services prices. |

|

United Kingdom |

+1.5% |

Economic indicators up to March suggest a generalized improvement in activity before the change in US trade policy and the impact of the new taxes in early April. The labour market cooled, although the unemployment rate remains at very low levels (4.4% in January), and wage pressures remain (5.9% year-on-year growth in February). The annual inflation rate fell to 2.6% in March and core inflation declined to 3.5%. Despite expected pressure on inflation, we expect the Bank of England will cut rates from 4.50% to 4.25% in May. |

|

Portugal |

+2.9% |

Strong GDP growth in Q4 2024 has given the economy a boost for 2025. Consumption remained robust during the first quarter of the year. Employment increased and the unemployment rate remained low (6.4% in February). Headline and core inflation moderated to 1.9% in March, but a rebound is expected during the year due to increased activity and consumption. |

|

Poland |

+3.4% |

The outlook for 2025 is for growth around 3.5%, supported by internal demand which should offset weakness in the external sector, having registered average growth of 3% in 2024. The labour market remained strong, with unemployment at record lows (5.3% in March). The slowdown in wages improved inflation expectations for 2025 and annual inflation was stable at 4.9% in March. The central bank, having held interest rates at 5.75% in April, could start a cycle of interest rate cuts from May. |

|

United States |

+2.5% |

After strong growth in the second half of 2024, economic growth slowed in Q1 2025. The labour market remained relatively strong and inflation remained around 3%. Uncertainty regarding tariff policies is affecting the market expectations. The Fed held interest rates due to the risk of higher inflation and lower economic growth. |

|

Mexico |

+0.5% |

The economy weakened further between late 2024 and early 2025, affected by global uncertainty which is delaying investment and consumption decisions. The labour market remained resilient, albeit with signs of softening. The annual inflation rate moderated to 3.8% in March and core inflation stood at 3.6%. The central bank has continued to cut the official rate, by 50 bps per meeting, to 9% in March and suggested further cuts in the future. |

|

Brazil |

+3.6% |

Significant economic momentum continued in Q1 2025, with growth exceeding 3.5% driven by private consumption and a very low unemployment rate (below 7%). The annual inflation rate rebounded to 5.5% in March and medium-term expectations remained above target. In Q1 2025, the central bank continued the cycle of interest rate hikes it began in September 2024, with two 100 bp increases to 14.25%, and suggested that there will be more, albeit smaller, increases. |

|

Chile |

+4.0% |

After a strong Q4 2024, the economy slowed in Q1 2025, driven by temporary factors which should dissipate as the year goes on. Inflation remains high (4.9% in March) it is expected to moderate rapidly in the second half of the year and converge to the 3% target in early 2026. The central bank paused the rate-cutting cycle it had been implementing in the past two years and left the official interest rate at 5% in Q1 2025, while setting a cautious tone for the future that suggests rate stability in the coming months. |

|

Argentina |

+2.1% |

The economy consolidated its recovery in Q1 2025 and inflation, although elevated, fell further with monthly rates below 3%. The IMF approved a new USD 20 billion plan with the country in April. The funds will serve to recapitalize the central bank and should help Argentina re-establish access to international capital markets. The central bank lifted the fixed exchange rate regime, allowing it to float freely between 1,000-1,400 ARS/USD. |

1.Year-on-year changes for Q4 2024.

|

|

|

|

|

|

|

|

|

|

|

|

| Highlights of the period: Main figures |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1'25 ATTRIBUTABLE PROFIT |

|

|

EUR 3,402 mn |

|

|

|

|

|

|

|

|

+4% in euros |

/Q4'24 |

|

|

+4% in constant euros |

|

|

|

|

|

|

|

|

+19% in euros |

/Q1'24 |

|

|

+24% in constant euros |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RoTE (post-AT1) |

|

|

|

|

|

|

|

|

15.8% |

|

|

+172 bps |

/ Q1 2024 |

|

|

Note: RoTE (pre-AT1): 16.6% (+164 bps / Q1'24). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VOLUMES AND INCOME |

|

|

Loan and advances to customers |

Customer funds |

|

|

+1% |

+5% |

|

|

Net interest income |

Net fee income |

|

|

-2% |

+9% |

|

|

Note: YoY changes in constant euros and Argentina in current euros. |

|

|

|

|

|

|

|

|

EFFICIENCY |

|

|

-0.8pp |

|

|

|

|

|

|

|

|

|

|

COST OF RISK |

|

|

-6bps |

|

|

|

|

|

|

|

|

|

|

CET11 |

|

| +0.3pp |

+0.1pp |

|

|

|

uIn Q1 2025, profit attributable to the parent was EUR 3,402 million, a new record for the fourth consecutive quarter, having increased 4% compared to Q4 2024. In constant euros, profit also rose 4%, driven by lower costs. Positive net fee income performance and resilient net interest income in the current interest rate environment, excluding Argentina.

uAttributable profit increased 19% compared to Q1 2024. In constant euros, profit rose 24% boosted by the positive total income performance, with a solid contribution from net fee income, and costs, which grew by less than revenue and declined in real terms.

Additionally, the year-on-year comparison was favoured by the temporary levy on revenue earned in Spain which was recorded in full in Q1 2024 compared to the quarterly accrual of the banking tax expected for 2025. If we accrue the 2024 temporary levy, distributing the charge in line with the treatment of the tax in 2025, profit would increase by 13% year-on-year in constant euros.

uBy business, strong year-on-year profit growth across all global businesses, with most of them rising double digits.

uThese results reflect an excellent start to the year and put us on track to meet our 2025 targets.

uProfitability improved strongly year-on-year. RoTE (post-AT1) stood at 15.8% in Q1 2025, compared to 14.1% in the same period of 2024.

uSustained earnings per share growth, increasing 26% year-on-year to EUR 21.5 cents, boosted by the positive trends in profit and the share buybacks executed in the last 12 months.

uIn terms of business volumes, growth of customer funds continued to outpace loans and advances to customers as we continued to focus on active capital management, disciplined capital allocation and profitable growth.

Gross loans and advances to customers (excluding reverse repos) rose 1% year-on-year in constant euros, supported by increases in all global businesses' portfolios except Retail, where they fell slightly.

Customer funds (customer deposits excluding repos plus mutual funds) increased 5% year-on-year in constant euros, underpinned by double-digit growth in mutual funds and a rise in deposits (supported by increases in most global businesses), mainly due to demand deposits.

uIn the new interest rate environment, total income increased 1% in euros (+5% in constant euros) in line with the target we established for 2025. Of note was the positive net interest income performance, as excluding Argentina (strongly impacted by the sharp fall in interest rates) net interest income increased 4% in constant euros, with most global businesses growing. Higher customer activity and network benefits were reflected in net fee income (+4%, +9% in constant euros), growing in most global businesses except Consumer.

uThe structural changes we have implemented to move towards a simpler and more integrated model through ONE Transformation continued to contribute to better costs, efficiency gains and profitable growth. Costs decreased 1% in current euros, in line with our 2025 year-end target. The efficiency ratio improved 0.8 pp year-on-year to 41.8% driven mainly by Retail and Payments.

uCredit quality remains robust, supported by the positive overall macroeconomic environment and employment across our footprint. The NPL ratio improved 10 bps year-on-year to 2.99%. Total loan-loss reserves reached EUR 22,980 million, resulting in an NPL coverage ratio of 66%.

uThe Group's cost of risk improved 6 bps year-on-year to 1.14%, in line with our target for 2025. In Retail, the cost of risk improved to 0.91%, and in Consumer, the ratio was practically stable at controlled levels (2.14%). Retail and Consumer accounted for more than 80% of the Group's net loan-loss provisions.

uAs at end March 2025, the CET1 ratio stood at 12.9%, having increased 0.1 pp quarter-on-quarter, supported by +33 bps of organic generation, mainly resulting from gross profit generation (+53 bps) which amply offset RWA growth in the quarter, and +12 bps in markets and others. The ratio was impacted by a 27 bp deduction for the accrual of shareholder remuneration against profit earned in Q1 2025, in line with our 50% payout target2, and 8 bps in regulatory charges.

1.Dec-24 ratio on a fully-loaded basis (as published in the Q4 2024 Financial Report), excluding the transitory treatment of IFRS 9 and the CRR2. Mar-25 ratio on phased-in basis, calculated in accordance with the transitory treatment of the CRR.

2.In line with our current ordinary shareholder remuneration policy of approximately 50% of the Group's reported profit (excluding non-cash, non-capital ratios impact items), divided approximately equally between cash dividends and share buybacks. The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SHAREHOLDER REMUNERATION |

|

|

EUR million |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

+19% |

higher than cash dividends against 2023 results |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TNAVps + CASH DPS |

|

|

|

|

|

|

|

|

n Cash DPS: €10.0 cents |

|

|

+14.5% |

|

|

|

/ Mar-24 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

uOn 4 April 2025, the ordinary general shareholders’ meeting approved a final cash dividend charged against 2024 results in the gross amount of EUR 11.00 cents per share entitled to dividends cash that will be paid from 2 May 2025. Including the interim cash dividend paid in November 2024 (EUR 10.00 cents), the total cash dividend per share paid against 2024 results will be EUR 21.00 cents, around 19% more than the dividends paid against 2023 results.

uThese dividends are complemented by two share buyback programmes. The first has already been completed for a total of EUR 1,525 million, and the second started on 6 February 2025 after having been approved by the board of directors and having obtained the required regulatory authorization, for a maximum amount of EUR 1,587 million. Following the completion of this second programme, the Group will have repurchased 14% of its outstanding shares since we began our buybacks in 2021.

uAfter both actions have been carried out, total shareholder remuneration against 2024 results is therefore expected to be around EUR 6.3 billion, 13% higher than the remuneration against 2023 results, distributed approximately equally between cash dividends and share buybacks. On 5 February 2025, we announced that the board of directors intends to return up to EUR 10 billion to our shareholders through share buybacks corresponding to 2025 and 2026 results as well as to distribute excesses of our capital1.

uAs at March 2025, TNAV was EUR 5.46, +4.2% quarter-on-quarter. Including the first dividend charged against 2024 results, TNAV per share + dividend per share increased 14.5% year-on-year.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# OF CUSTOMERS (Mar-25) |

|

|

Total customers: |

175 |

mn |

|

|

|

|

|

|

|

Active customers: |

104 |

mn |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

uOur efforts to simplify and improve our product offering and service quality are reflected in an increase of 9 million customers year-on-year, bringing our total customers to 175 million. We have 104 million active customers, up 4 million year-on-year.

uThe volume of transactions per active customer rose 6% year-on-year in Q1 2025.

uWe continue to focus on delivering great customer experience and improving our service quality, ranking in the top 3 in NPS2 in seven of our markets.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contribution to Group revenue 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail |

|

50% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Consumer |

|

21% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CIB |

|

14% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Wealth |

|

6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Payments |

|

9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 2025 data. Year-on-year changes in constant euros

uIn Retail, double-digit attributable profit growth to EUR 1,902 million, driven by a 2% rise in total income, boosted by the positive trends in net fee income and by the structural cost improvements (-1%) stemming from our transformation efforts, with controlled provisions (+2%).

uThe efficiency improved 1.3 pp to 39.4% and cost of risk also improved to 0.91%. RoTE (post-AT1) increased to 17.6%.

uIn Consumer, attributable profit grew to EUR 492 million, with a good performance in total income (+2%), supported by net interest income and by lower provisions (-1%) due to DCB US.

uThe efficiency ratio stood at 41.9%, cost of risk was stable at controlled levels (2.14%) and RoTE (post-AT1) was 9.7%.

uIn CIB, attributable profit reached a new quarterly record of EUR 806 million, with double-digit growth driven by total income, supported by net fee income, especially in Global Transaction Banking.

uThe efficiency ratio stood at 42.9%. RoTE (post-AT1) improved 3.1 pp to 21.6%.

uIn Wealth, attributable profit amounted to EUR 471 million, also rising double-digits, driven by net fee income (greater activity) and higher revenue from our joint ventures in Insurance, more than offsetting the impact of interest rates on net interest income and higher costs, reflecting our investments in key initiatives such as reinforcing Private Banking teams.

uThe efficiency ratio improved 1.4 pp to 36.5% and RoTE (post-AT1) was 68.0%.

uIn Payments, attributable profit reached EUR 126 million, boosted by double-digit growth in net interest income and fees, with costs flat, partially offset by higher provisions in Cards in Brazil and Mexico, in part due to portfolio growth.

uCost of risk was 7.52%. In PagoNxt, EBITDA margin reached 28.6% (+11.6 pp year-on-year).

1.This share buyback target includes i) buybacks that are part of the existing shareholder remuneration policy, and ii) additional buybacks following the publication of annual results to distribute year-end excesses of CET1 capital.

2.Net Promoter Score, internal benchmark of individual customers' satisfaction audited by Stiga/Deloitte in H2 2024.

3.As % of total operating areas, excluding the Corporate Centre.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statutory income statement |

|

|

|

|

|

|

|

|

Grupo Santander results

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Grupo Santander. Summarized income statement |

| EUR million |

|

|

|

|

|

|

|

|

|

|

|

Change |

|

|

Change |

|

Q1'25 |

Q4'24 |

% |

|

|

Q1'24 |

% |

|

| Net interest income |

11,378 |

|

11,986 |

|

(5.1) |

|

|

|

11,983 |

|

(5.0) |

|

|

Net fee income1 |

3,369 |

|

3,344 |

|

0.7 |

|

|

|

3,240 |

|

4.0 |

|

|

Gains or losses on financial assets and liabilities and exchange differences2 |

678 |

|

780 |

|

(13.1) |

|

|

|

623 |

|

8.8 |

|

|

| Dividend income |

88 |

|

130 |

|

(32.3) |

|

|

|

93 |

|

(5.4) |

|

|

| Share of results of entities accounted for using the equity method |

168 |

|

214 |

|

(21.5) |

|

|

|

123 |

|

36.6 |

|

|

Other operating income/expenses (net)3 |

(144) |

|

(428) |

|

(66.4) |

|

|

|

(1,017) |

|

(85.8) |

|

|

| Total income |

15,537 |

|

16,026 |

|

(3.1) |

|

|

|

15,045 |

|

3.3 |

|

|

| Operating expenses |

(6,489) |

|

(6,772) |

|

(4.2) |

|

|

|

(6,547) |

|

(0.9) |

|

|

| Administrative expenses |

(5,635) |

|

(5,948) |

|

(5.3) |

|

|

|

(5,719) |

|

(1.5) |

|

|

| Staff costs |

(3,532) |

|

(3,770) |

|

(6.3) |

|

|

|

(3,594) |

|

(1.7) |

|

|

| Other general administrative expenses |

(2,103) |

|

(2,178) |

|

(3.4) |

|

|

|

(2,125) |

|

(1.0) |

|

|

| Depreciation and amortization |

(854) |

|

(824) |

|

3.6 |

|

|

|

(828) |

|

3.1 |

|

|

| Provisions or reversal of provisions |

(621) |

|

(1,362) |

|

(54.4) |

|

|

|

(633) |

|

(1.9) |

|

|

| Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net) |

(3,156) |

|

(3,120) |

|

1.2 |

|

|

|

(3,134) |

|

0.7 |

|

|

|

|

|

|

|

|

|

|

|

| Impairment on other assets (net) |

(102) |

|

(192) |

|

(46.9) |

|

|

|

(129) |

|

(20.9) |

|

|

| Gains or losses on non-financial assets and investments, net |

2 |

|

(4) |

|

— |

|

|

|

2 |

|

— |

|

|

| Negative goodwill recognized in results |

23 |

|

— |

|

— |

|

|

|

— |

|

— |

|

|

| Gains or losses on non-current assets held for sale not classified as discontinued operations |

(7) |

|

24 |

|

— |

|

|

|

(21) |

|

(66.7) |

|

|

| Profit or loss before tax from continuing operations |

5,187 |

|

4,600 |

|

12.8 |

|

|

|

4,583 |

|

13.2 |

|

|

| Tax expense or income from continuing operations |

(1,446) |

|

(1,037) |

|

39.4 |

|

|

|

(1,468) |

|

(1.5) |

|

|

| Profit from the period from continuing operations |

3,741 |

|

3,563 |

|

5.0 |

|

|

|

3,115 |

|

20.1 |

|

|

| Profit or loss after tax from discontinued operations |

— |

|

— |

|

— |

|

|

|

— |

|

— |

|

|

| Profit for the period |

3,741 |

|

3,563 |

|

5.0 |

|

|

|

3,115 |

|

20.1 |

|

|

| Profit attributable to non-controlling interests |

(339) |

|

(298) |

|

13.8 |

|

|

|

(263) |

|

28.9 |

|

|

| Profit attributable to the parent |

3,402 |

|

3,265 |

|

4.2 |

|

|

|

2,852 |

|

19.3 |

|

|

|

|

|

|

|

|

|

|

|

| EPS (euros) |

0.21 |

|

0.20 |

|

5.8 |

|

|

|

0.17 |

|

26.1 |

|

|

| Diluted EPS (euros) |

0.21 |

|

0.20 |

|

5.8 |

|

|

|

0.17 |

|

26.0 |

|

|

|

|

|

|

|

|

|

|

|

| Memorandum items: |

|

|

|

|

|

|

|

|

| Average total assets |

1,855,729 |

|

1,834,476 |

|

1.2 |

|

|

|

1,804,334 |

|

2.8 |

|

|

| Average stockholders' equity |

101,501 |

|

97,952 |

|

3.6 |

|

|

|

96,308 |

|

5.4 |

|

|

|

|

|

|

|

|

| Note: the summarized income statement groups some lines of the consolidated statutory income statement on page 88 as follows: |

1.‘Commission income’ and ‘Commission expense’. |

2.‘Gain or losses on financial assets and liabilities not measured at fair value through profit or loss, net’; ‘Gain or losses on financial assets and liabilities held for trading, net’; ‘Gains or losses on non-trading financial assets and liabilities mandatorily at fair value through profit or loss’; ‘Gain or losses on financial assets and liabilities measured at fair value through profit or loss, net’; ‘Gain or losses from hedge accounting, net’; and ‘Exchange differences, net’. |

3.‘Other operating income’; ‘Other operating expenses’; ’Income from insurance and reinsurance contracts’; and ‘Expenses from insurance and reinsurance contracts’. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statutory income statement |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STATUTORY INCOME STATEMENT |

|

|

|

|

|

Results performance compared to Q1 2024

In Q1 2025, profit attributable to the parent totalled EUR 3,402 million, reaching a new quarterly record for the fourth quarter in a row, supported by the good performance of our global businesses.

Compared to the EUR 2,852 million recorded in Q1 2024, profit attributable to the parent in Q1 2025 was 19% higher year-on-year.

This year-on-year comparison is favoured by the temporary levy on revenue earned in Spain (EUR 335 million) which was recorded in full in Q1 2024. This compares to EUR 87 million in Q1 2025, corresponding to the quarterly accrual of the tax on revenue expected in Spain for the year.

If we accrue the 2024 temporary levy, distributing the charge equally between the four quarters of the year in line with the treatment of the tax in 2025, profit would increase 10% year-on-year. This growth was supported by the good performance in total income, mainly in net fee income, and lower operating expenses, reflecting our progress in transformation, with a slight increase in provisions in line with credit portfolio growth.

Total income

Total income amounted to EUR 15,537 million, up 3% year-on-year.

•Net interest income (NII) totalled EUR 11,378 million, 5% lower than Q1 2024, mainly due to the impact from the sharp fall in interest rates in Argentina (which are at the lowest levels since 2018) on all businesses, especially Retail and CIB.

Excluding Argentina, net interest income was flat as the good performance in Consumer, due to good margin management and higher volumes, and in CIB and Payments, due to increased activity, offset the slight fall in Retail, as well as declines in Wealth and the Corporate Centre, impacted by the new interest rate environment.

|

|

|

|

|

|

| Net interest income |

| EUR million |

•Net fee income amounted to EUR 3,369 million, up 4% compared to Q1 2024, due to the good performance in all businesses. Of particular note were the increases in CIB, supported by Global Transaction Banking and Global Banking, boosted by our US Banking Build-Out (US BBO) initiative, in Wealth, due to the good performances in Private Banking and Santander Asset Management, and in Payments, boosted by higher activity. On the other hand, net fee income in Consumer fell slightly, as DCB Europe was impacted by new insurance regulation in Germany.

|

|

|

|

|

|

| Net fee income |

| EUR million |

•Gains or losses on financial assets and liabilities and exchange differences reached EUR 678 million (EUR 623 million in Q1 2024) due to the higher results in Retail and the Corporate Centre due to a lower impact from currency hedges.

•Dividend income was EUR 88 million (EUR 93 million in Q1 2024).

•Income from companies accounted for by the equity method reached EUR 168 million, compared to EUR 123 million in Q1 2024.

•Other operating income recorded a loss of EUR 144 million, compared to a EUR 1,017 million loss in Q1 2024, which was strongly affected by the larger hyperinflation adjustment in Argentina and the temporary levy on revenue earned in Spain, which was recorded in full in Q1 2024 (EUR 335 million).

In summary, a resilient performance in total income, which exceeded EUR 15 billion for the fifth consecutive quarter, reflecting our diversification and global scale, despite the impact of the new interest rate environment on net interest income.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statutory income statement |

|

|

|

|

|

|

|

|

Operating expenses

Operating expenses in Q1 2025 amounted to EUR 6,489 million, 1% lower year-on-year, reflecting our progress in transformation.

Our cost management continued to focus on structurally improving our efficiency and, as a result, we remain as one of the most efficient banks in the world.

We continued to drive our business transformation plan, ONE Transformation, across our footprint, reflected in greater operational leverage and better commercial dynamics.

|

|

|

|

|

|

| Operating expenses |

| EUR million |

Provisions or reversal of provisions

Provisions (net of provisions reversals) amounted to EUR 621 million. In Q1 2024, this line totalled EUR 633 million.

Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net)

Impairment or reversal of impairment on financial assets not measured at fair value through profit or loss (net) was EUR 3,156 million, relatively stable year-on-year (EUR 3,134 million in Q1 2024).

Credit quality indicators remained robust, supported by our risk management and the resilience of the labour markets across our footprint.

Impairment on other assets (net)

The impairment on other assets (net) was EUR 102 million. In Q1 2024, the impairment on other assets totalled EUR 129 million.

Gains or losses on non-financial assets and investments (net)

Net gains on non-financial assets and investments were EUR 2 million in Q1 2025. In Q1 2024, net gains were also EUR 2 million.

Negative goodwill recognized in results

In Q1 2025, negative goodwill recognized in results was EUR 23 million relating to the acquisition of CrediScotia Financiera from Scotiabank to expand Consumer's presence in Peru. There was no negative goodwill recorded in Q1 2024.

Gains or losses on non-current assets held for sale not classified as discontinued operations

This item, which mainly includes impairment of foreclosed assets recorded and the sale of properties acquired upon foreclosure, recorded a EUR 7 million loss in Q1 2025 (EUR 21 million loss in Q1 2024).

Profit before tax

Profit before tax was EUR 5,187 million in Q1 2025, up 13% year-on-year, supported by the solid performance in net fee income, our cost discipline and the impact of recording the temporary levy on revenue earned in Spain in full in Q1 2024 (EUR 335 million) in the other operating income line.

Income tax

Total income tax amounted to EUR 1,446 million which includes EUR 87 million corresponding to the quarterly accrual of the tax on revenue expected in Spain for the year. In Q1 2024, income tax was EUR 1,468 million.

Profit attributable to non-controlling interests

Profit attributable to non-controlling interests amounted to EUR 339 million (EUR 263 million in Q1 2024).

Profit attributable to the parent

Profit attributable to the parent rose to a new record at EUR 3,402 million in Q1 2025, compared to EUR 2,852 million in the same period in 2024, 19% higher year-on-year.

These results do not fully reflect the underlying business performance due to the different accounting of the aforementioned temporary levy in 2024 and tax in 2025.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Underlying income statement |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNDERLYING INCOME STATEMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

→ Fourth consecutive quarter of record profit boosted by solid performance in our global businesses.

→ Efficiency improvement and profitable growth, supported by the operational leverage resulting from ONE Transformation.

→ Risk indicators were robust, supported by good risk management and low unemployment.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attributable profit |

|

RoTE (post-AT1) |

RoRWA |

|

|

|

EUR 3,402 million |

+19% in euros |

|

15.8% |

2.34% |

|

|

|

+24% in constant euros |

|

+1.7 pp |

+0.4 pp |

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: changes vs. Q1 2024. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Results performance compared to Q1 2024

The Group presents, both at the total Group level and for each of the business units, the changes in euros registered in the income statement, as well as variations excluding the exchange rate effect (i.e. in constant euros, except for Argentina and any grouping which includes it), understanding that the latter provide a better analysis of the Group’s management. For further information, see the

'Alternative performance measures' section in the appendix to this report.

At the Group level, exchange rates had a negative impact of 3.8 pp on total income and a positive impact of 2.9 pp on administrative expenses and amortizations, mainly due to the depreciation of the Brazilian real and the Mexican peso.

To better understand the business trends, we reclassified certain items under some headings of the underlying income statement. These items explain the differences between the statutory and underlying income statements. There was only one reclassification in Q1 2024:

•The impact of the temporary levy on revenue earned in Spain totalling EUR 335 million in Q1 2024, which was reclassified from total income to other gains (losses) and provisions.

As profit was not affected by results that fell outside the ordinary course of our business, no amount was recorded in the net capital gains and provisions line in Q1 2025 or in Q1 2024 and so both profit attributable to the parent and underlying profit attributable to the parent were the same; EUR 3,402 million in Q1 2025 and EUR 2,852 million in Q1 2024. This represents a 19% year-on-year increase,+24% in constant euros.

This year-on-year comparison is favoured by the temporary levy on revenue earned in Spain (EUR 335 million) which was recorded in full in Q1 2024. This compares to EUR 87 million in Q1 2025, corresponding to the quarterly accrual of the tax on revenue expected in Spain for the year. If we accrue the 2024 temporary levy, distributing the charge equally between the four quarters of the year in line with the treatment of the tax in 2025, profit increases 10% year-on-year (+13% in constant euros). This growth was supported by the good performance in net fee income, and our effort to reduce administrative expenses and amortizations, with net loan-loss provisions and cost of risk at controlled levels.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Summarized underlying income statement |

| EUR million |

|

|

|

|

|

|

|

|

|

|

|

Change |

|

|

Change |

|

Q1'25 |

Q4'24 |

% |

% excl. FX |

|

Q1'24 |

% |

% excl. FX |

| Net interest income |

11,378 |

|

11,986 |

|

(5.1) |

(5.6) |

|

11,983 |

|

(5.0) |

(1.7) |

| Net fee income |

3,369 |

|

3,344 |

|

0.7 |

0.3 |

|

3,240 |

|

4.0 |

8.7 |

Gains (losses) on financial transactions 1 |

678 |

|

780 |

|

(13.1) |

(12.3) |

|

623 |

|

8.8 |

10.8 |

| Other operating income |

112 |

|

(84) |

|

— |

— |

|

(466) |

|

— |

— |

| Total income |

15,537 |

|

16,026 |

|

(3.1) |

(3.5) |

|

15,380 |

|

1.0 |

4.8 |

| Administrative expenses and amortizations |

(6,489) |

|

(6,772) |

|

(4.2) |

(4.5) |

|

(6,547) |

|

(0.9) |

2.0 |

| Net operating income |

9,048 |

|

9,254 |

|

(2.2) |

(2.8) |

|

8,833 |

|

2.4 |

6.9 |

| Net loan-loss provisions |

(3,161) |

|

(3,114) |

|

1.5 |

0.6 |

|

(3,125) |

|

1.2 |

7.2 |

| Other gains (losses) and provisions |

(700) |

|

(1,540) |

|

(54.5) |

(55.0) |

|

(1,125) |

|

(37.8) |

(36.5) |

| Profit before tax |

5,187 |

|

4,600 |

|

12.8 |

12.4 |

|

4,583 |

|

13.2 |

17.5 |

| Tax on profit |

(1,446) |

|

(1,037) |

|

39.4 |

38.0 |

|

(1,468) |

|

(1.5) |

2.7 |

| Profit from continuing operations |

3,741 |

|

3,563 |

|

5.0 |

4.9 |

|

3,115 |

|

20.1 |

24.5 |

| Net profit from discontinued operations |

— |

|

— |

|

— |

|

— |

|

|

— |

|

— |

|

— |

|

| Consolidated profit |

3,741 |

|

3,563 |

|

5.0 |

4.9 |

|

3,115 |

|

20.1 |

24.5 |

| Non-controlling interests |

(339) |

|

(298) |

|

13.8 |

12.4 |

|

(263) |

|

28.9 |

30.6 |

| Net capital gains and provisions |

— |

|

— |

|

— |

— |

|

— |

|

— |

— |

| Profit attributable to the parent |

3,402 |

|

3,265 |

|

4.2 |

4.2 |

|

2,852 |

|

19.3 |

23.9 |

Underlying profit attributable to the parent 2 |

3,402 |

|

3,265 |

|

4.2 |

4.2 |

|

2,852 |

|

19.3 |

23.9 |

|

|

|

|

|

|

|

|

|

1. Includes exchange differences.

2. Excludes net capital gains and provisions.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Underlying income statement |

|

|

|

|

|

|

|

|

Total income amounted to EUR 15,537 million, up slightly compared to Q1 2024 (+1% year-on-year). In constant euros, total income rose 5% year-on-year, as follows:

•Net interest income (NII) performed well, considering the current interest rate environment, but fell 2% year-on-year mainly due to the strong impact of the interest rate decline in Argentina. Excluding Argentina, NII rose 4%.

By business:

•In Retail (-2%), NII performance reflected the impact of Argentina, where interest rates reached their lowest levels since 2018. Excluding it, NII rose 4%, due to good performances in Chile, the UK, Mexico and Poland.

•In Consumer, NII rose 2% supported by our good margin management and also by volumes growth in DCB Europe.

•In CIB, NII decreased 5%, mainly due to the impact from Argentina. Excluding it, NII grew 12% driven by the strong increase in Global Markets.

•In Wealth, NII declined 16%, especially in Private Banking, impacted by the less favourable interest rate environment, despite higher volumes.

•In Payments, NII rose 15%, with growth in both Cards, mainly in Mexico and Brazil due to volumes increase, and PagoNxt, due to higher activity.

|

|

|

|

|

|

| Net interest income |

| EUR million |

|

constant euros |

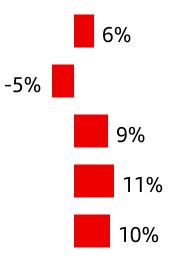

•Net fee income grew 9% year-on-year driven by widespread growth across all businesses except Consumer. By business:

•In Retail, net fee income increased 7%, supported by insurance, mutual funds and transactional fees.

•In Consumer, net fee income fell 3%, despite strong growth in the US (auto fees), mainly due to DCB Europe, which was impacted by new insurance regulation in Germany.

•In CIB, it increased 11%, driven by the three business lines, especially due to Global Transaction Banking (GTB) and Global Banking, backed by our US Banking Build-Out (US BBO) initiative.

•In Wealth, net fee income rose 16%, with strong growth in Private Banking and Asset Management due to good commercial activity.

•In Payments, net fee income rose 13% boosted by both PagoNxt (Ebury and Getnet) and Cards (driven by interchange fees in Latin America).

This positive net fee income performance keeps us on track to achieve our mid-high single digit growth target for 2025.

|

|

|

|

|

|

| Net fee income |

| EUR million |

|

constant euros |

•Gains on financial transactions rose 11%, boosted by higher results in Retail, mainly due to Brazil and Spain, and the Corporate Centre, due to a lower impact from foreign currency hedges. This good performance more than offset lower results in CIB, despite higher activity in Global Markets, as this activity was concentrated in more NII and fee based products.

•Other operating income in Q1 2025 registered a positive result compared to a negative result in Q1 2024, driven by a less negative impact from the hyperinflation adjustment in Argentina.

This positive revenue performance keeps us on track to achieve our 2025 target of reaching a revenue level of EUR 62 billion in the year, similar to the revenue recorded in 2024.

|

|

|

|

|

|

| Total income |

| EUR million |

|

constant euros |

Administrative expenses and amortizations in Q1 2025 totalled EUR 6,489 million, down 1% year-on-year, reflecting our transformation progress and in line with our 2025 target to reduce costs in euro terms. In real terms (excluding the impact of average inflation, and in constant euros), they were also 1% lower year-on-year.

Our cost management continued to focus on structurally improving our efficiency. As a result, we remain one of the most efficient banks in the world with an efficiency ratio of 41.8%, having improved 80 bps year-on-year.

We continued to progress with our business transformation plan, ONE Transformation, reflected in greater operational leverage and better business dynamics. We continued to create simpler and leaner structures. As part of our simplification, in Q1 2025 we announced the

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Underlying income statement |

|

|

|

|

|

|

|

|

dissolution of the regional structures, having fulfilled their mission to support the transition to the global operating model.

By business and in constant euros:

•In Retail, costs were down 1%, -4% in real terms (i.e. excluding inflation), reflecting our transformation efforts through the simplification and the implementation of our global platform. The efficiency ratio improved 1.3 pp year-on-year to 39.4%.

•In Consumer, costs rose 3% year-on-year. In real terms, they were flat as our transformation savings offset our investments in leasing and check-out lending platforms and in Openbank. The efficiency ratio stood at 41.9% (+0.8 pp year-on-year).

•In CIB, costs increased 9%, +6% in real terms, due to our investments in our transformation initiatives. The efficiency ratio was 42.9%, maintaining a leading position among peers.

•In Wealth, costs rose 10%. In real terms, they increased 7%, reflecting our investments to reinforce Private Banking teams and new capabilities to address the increase in commercial activity. The efficiency ratio improved 1.4 pp year-on-year to 36.5%.

•In Payments, costs were stable, declining 3% in real terms, supported by our efforts to control costs, with good performances in both PagoNxt and Cards. The efficiency ratio stood at 43.9%, an improvement of 4.5 pp year-on-year.

|

|

|

|

|

|

| Operating expenses |

| EUR million |

|

constant euros |

Net operating income in Q1 2025 grew 2% year-on-year (+7% in constant euros), reaching EUR 9,048 million.

|

|

|

|

|

|

| Net operating income |

| EUR million |

|

constant euros |

Net loan-loss provisions in Q1 2025 amounted to EUR 3,161 million, up 1% year-on-year. In constant euros, they increased 7% due to higher provisions in Payments (impacted by strong credit portfolio growth in Cards, macro outlook and regulatory changes in models in Brazil and model updates in Mexico due to the macro environment) and higher provisions in the Corporate Centre to accelerate NPL ratio reductions, improving the Group's credit quality.

The cost of risk stood at 1.14%, in line with the Group’s 2025 target.

|

|

|

|

|

|

| Net loan-loss provisions |

| EUR million |

|

constant euros |

Other gains (losses) and provisions had a loss of EUR 700 million, versus a EUR 1,125 million loss in Q1 2024. This reduction was mainly explained by the temporary levy on revenue earned in Spain (EUR 335 million) which was recorded in full in Q1 2024 but also due to the good performance in most global businesses.

Total income tax amounted EUR 1,446 million, 1% lower than in Q1 2024 (+3% in constant euros). Included in Q1 2025 is the EUR 87 million charge corresponding to the quarterly accrual of the tax on revenue expected in Spain for the year.

Profit attributable to the parent in Q1 2025 was EUR 3,402 million, 19% more than in Q1 2024 (+24% in constant euros).

|

|

|

|

|

|

| Profit attributable to the parent |

| EUR million |

|

constant euros |

RoTE (post-AT1) in Q1 2025 stood at 15.8% (14.1% in Q1 2024), on track to achieve our 2025 target of 16.5%. RoRWA was 2.34% (1.96% in Q1 2024) and earnings per share stood at EUR 0.21 (EUR 0.17 in Q1 2024).

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Underlying income statement |

|

|

|

|

|

|

|

|

Underlying results performance compared to the previous quarter

Underlying profit attributable to the parent and profit attributable to the parent were both the same in Q1 2025, at EUR 3,402 million, and in Q4 2024, at EUR 3,265 million, as profit in neither period was affected by results outside the ordinary course of our business.

Compared to Q4 2024, profit in Q1 2025 increased 4%, driven by good performances in operating expenses and provisions.

The quarter-on-quarter comparison was greatly affected by the impact of the exchange rate on Argentina's results in Q4 2024. For further information, see the

'Alternative performance measures' section in the appendix to this report. Additionally, profit in Q4 2024 was impacted by the provision for potential complaints related to motor finance dealer commissions in the UK.

In constant euros, profit increased 4%, by line:

•Total income remained above EUR 15 billion. However, it decreased 4%, heavily affected by the impact of the exchange rate on Argentina's results in Q4 2024. By line:

•Net interest income decreased 6%, strongly affected by the exchange rate effect on Argentina's results in Q4 2024. Excluding Argentina, NII was stable, as increases in CIB (+8%) and Payments (+6%) from higher activity, offset a worse performance in Retail (-1%), mainly in Brazil due to the negative sensitivity of its balance sheet to interest rate hikes.

•Net fee income was stable quarter-on-quarter. Excluding Argentina, it increased 4%, driven by growth in most countries in Retail and the good performance in CIB and Wealth, which offset the decline in Consumer (new insurance regulation in Germany) and Payments, affected by the seasonality of the last quarter in the year in both PagoNxt and Cards.

•Gains on financial transactions fell 12%, mainly affected by worse performance in the Corporate Centre related to FX hedges, partially offset by higher results in CIB, driven by Global Markets.

•Operating expenses in Q1 2025 declined 5% quarter-on-quarter (-2% excluding Argentina), underpinned by the good performance in all global businesses except Consumer, where costs were strongly affected by the new Openbank launches, and Payments, due to PagoNxt's platform investments.

•Net loan-loss provisions were fairly stable, supported by the significant improvement in DCB US, due to a good underlying performance and some seasonality in Q4, offsetting higher provisions mainly in the Corporate Centre to accelerate NPL ratio reductions, improving the Group's credit quality.

•Other gains (losses) and provisions recorded a EUR 700 million loss in Q1 2025, compared to a EUR 1,540 million loss in Q4 2024, which was impacted by the aforementioned provision for potential complaints related to motor finance dealer commissions in the UK.

Grupo Santander balance sheet

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Grupo Santander. Condensed balance sheet |

| EUR million |

|

|

|

|

|

|

|

|

Change |

|

| Assets |

Mar-25 |

Mar-24 |

Absolute |

% |

Dec-24 |

| Cash, cash balances at central banks and other demand deposits |

166,948 |

|

174,161 |

|

(7,213) |

|

(4.1) |

|

192,208 |

|

| Financial assets held for trading |

243,348 |

|

209,589 |

|

33,759 |

|

16.1 |

|

230,253 |

|

| Debt securities |

91,215 |

|

71,983 |

|

19,232 |

|

26.7 |

|

82,646 |

|

| Equity instruments |

16,739 |

|

19,805 |

|

(3,066) |

|

(15.5) |

|

16,636 |

|

| Loans and advances to customers |

28,979 |

|

18,722 |

|

10,257 |

|

54.8 |

|

26,591 |

|

| Loans and advances to central banks and credit institutions |

50,440 |

|

39,146 |

|

11,294 |

|

28.9 |

|

40,280 |

|

| Derivatives |

55,975 |

|

59,933 |

|

(3,958) |

|

(6.6) |

|

64,100 |

|

Financial assets designated at fair value through profit or loss1 |

13,647 |

|

14,919 |

|

(1,272) |

|

(8.5) |

|

14,045 |

|

| Loans and advances to customers |

5,513 |

|

6,474 |

|

(961) |

|

(14.8) |

|

5,652 |

|

| Loans and advances to central banks and credit institutions |

407 |

|

455 |

|

(48) |

|

(10.5) |

|

408 |

|

| Other (debt securities an equity instruments) |

7,727 |

|

7,990 |

|

(263) |

|

(3.3) |

|

7,985 |

|

| Financial assets at fair value through other comprehensive income |

94,873 |

|

84,183 |

|

10,690 |

|

12.7 |

|

89,898 |

|

| Debt securities |

81,279 |

|

73,638 |

|

7,641 |

|

10.4 |

|

76,558 |

|

| Equity instruments |

2,401 |

|

1,916 |

|

485 |

|

25.3 |

|

2,193 |

|

| Loans and advances to customers |

10,848 |

|

8,282 |

|

2,566 |

|

31.0 |

|

10,784 |

|

| Loans and advances to central banks and credit institutions |

345 |

|

347 |

|

(2) |

|

(0.6) |

|

363 |

|

| Financial assets measured at amortized cost |

1,221,296 |

|

1,207,699 |

|

13,597 |

|

1.1 |

|

1,203,707 |

|

| Debt securities |

127,891 |

|

112,589 |

|

15,302 |

|

13.6 |

|

120,949 |

|

| Loans and advances to customers |

1,019,076 |

|

1,016,055 |

|

3,021 |

|

0.3 |

|

1,011,042 |

|

| Loans and advances to central banks and credit institutions |

74,329 |

|

79,055 |

|

(4,726) |

|

(6.0) |

|

71,716 |

|

| Investments in subsidiaries, joint ventures and associates |

7,460 |

|

7,685 |

|

(225) |

|

(2.9) |

|

7,277 |

|

| Tangible assets |

30,822 |

|

34,229 |

|

(3,407) |

|

(10.0) |

|

32,087 |

|

| Intangible assets |

19,150 |

|

19,910 |

|

(760) |

|

(3.8) |

|

19,259 |

|

| Goodwill |

13,510 |

|

14,028 |

|

(518) |

|

(3.7) |

|

13,438 |

|

| Other intangible assets |

5,640 |

|

5,882 |

|

(242) |

|

(4.1) |

|

5,821 |

|

Other assets2 |

47,633 |

|

47,631 |

|

2 |

|

— |

|

48,347 |

|

| Total assets |

1,845,177 |

|

1,800,006 |

|