United States

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): February 1, 2024

ATLANTIC UNION BANKSHARES CORPORATION

(Exact name of registrant as specified in its charter)

Virginia |

001-39325 |

54-1598552 |

(State or other jurisdiction |

(Commission |

(I.R.S. Employer |

of incorporation) |

File Number) |

Identification No.) |

|

|

|

4300 Cox Road

Glen Allen, Virginia 23060

(Address of principal executive offices, including Zip Code)

Registrant’s telephone number, including area code: (804) 633-5031

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common Stock, par value $1.33 per share |

|

AUB |

|

New York Stock Exchange |

Depositary Shares, Each Representing a 1/400th Interest in a Share of 6.875% Perpetual Non-Cumulative Preferred Stock, Series A |

|

AUB.PRA |

|

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. |

☐ |

Item 7.01 Regulation FD Disclosure.

Attached as Exhibit 99.1 is a handout containing information that certain members of Atlantic Union Bankshares Corporation (the “Company”) management will use during meetings with investors, analysts, and other interested parties to assist their understanding of the Company from time to time during the first quarter of 2024. Other presentations and related materials will be made available as they are presented. This handout is also available under the Presentations link in the Investor Relations section of the Company’s website at http://investors.atlanticunionbank.com. Exhibit 99.1 is incorporated by reference into this Item 7.01.

The information disclosed in or incorporated by reference into this Item 7.01, including Exhibit 99.1, is furnished and shall not be deemed filed for purposes of Section 18 of the Securities Exchange Act of 1934.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits.

Exhibit No. |

|

Description of Exhibit |

99.1 |

|

Atlantic Union Bankshares Corporation investor presentation. |

104 |

|

Cover Page Interactive Data File – the cover page iXBRL tags are embedded within the Inline XBRL document |

1

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

ATLANTIC UNION BANKSHARES CORPORATION |

||

|

|

|

|

|

|

|

|

|

|

|

|

Date: February 1, 2024 |

By: |

/s/ Robert M. Gorman |

|

|

|

Robert M. Gorman |

|

|

|

Executive Vice President and |

|

|

|

Chief Financial Officer |

|

|

|

|

|

2

|

Investor Presentation NYSE: AUB February – March 2024 |

|

2 Forward Looking Statements This presentation and statements by our management may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are statements that include, without limitation, statements on slides entitled "Q4 2023 Highlights and FY 2023 Highlights,“ “Loan and Deposit Betas,” and “Financial Outlook,” statements regarding our strategic priorities, liquidity and capital management strategies, expectations related to our business, financial, and operating results, including our deposit base and funding, the impact of changes in economic conditions, the impact of our cost saving measures, our securities portfolio restructuring, or changes in asset quality, and statements that include, other projections, predictions, expectations, or beliefs about future events or results, including our ability to meet our top tier financial targets, or otherwise are not statements of historical fact. Such forward-looking statements are based on certain assumptions as of the time they are made, and are inherently subject to known and unknown risks, uncertainties, and other factors, some of which cannot be predicted or quantified, that may cause actual results, performance, achievements, or trends to be materially different from those expressed or implied by such forward-looking statements. Such statements are often characterized by the use of qualified words (and their derivatives) such as “expect,” “believe,” “estimate,” “plan,” “project,” “anticipate,” “intend,” “will,” “may,” “view,” “opportunity,” “potential,” “continue,” “confidence,” “should,” or words of similar meaning or other statements concerning opinions or judgments of our management about future events. Although we believe that our expectations with respect to forward-looking statements are based on reasonable assumptions within the bounds of our existing knowledge of our business and operations, there can be no assurance that actual future results, performance, or achievements of, or trends affecting, us will not differ materially from any projected future results, performance, achievements or trends expressed or implied by such forward-looking statements. Actual future results, performance, achievements or trends may differ materially from historical results or those anticipated depending on a variety of factors, including, but not limited to the effects of or changes in: • market interest rates and their related impacts on macroeconomic conditions, customer and client behavior, our funding costs and our loan and securities portfolios; • inflation and its impacts on economic growth and customer and client behavior; • adverse developments in the financial industry, such as bank failures, responsive measures to mitigate and manage such developments, related supervisory and regulatory actions and costs, and related impacts on customer behavior; • the sufficiency of liquidity; • general economic and financial market conditions, in the United States generally and particularly in the markets in which we operate and which our loans are concentrated, including the effects of declines in real estate values, an increase in unemployment levels and slowdowns in economic growth; • our failure to close our proposed merger with American National Bankshares Inc. (“American National”) when expected or at all because required regulatory approvals and other conditions to closing are not received or satisfied on a timely basis or at all, and the risk that any regulatory approvals may result in the imposition of conditions that could adversely affect the combined company or the expected benefits of the merger; • the occurrence of any event, change or circumstance that could give rise to the right of either party to terminate the merger agreement between the Company and American National; • any change in the purchase accounting assumptions used regarding the American National assets acquired and liabilities assumed to determine the fair value and credit marks, particularly in light of the current interest rate environment; • the risks that the anticipated benefits of the proposed merger, including cost savings and strategic gains, are not realized when expected or at all; • the proposed merger may be more expensive or take longer to complete than anticipated, including as a result of unexpected factors or events, and may divert management’s attention from ongoing business operations and opportunities; • potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the proposed merger; • government monetary and fiscal policies, including policies of the U.S. Treasury and the Federal Reserve; • the quality or composition of our loan or investment portfolios and changes therein; • demand for loan products and financial services in our market areas; • our ability to manage our growth or implement our growth strategy; • the effectiveness of expense reduction plans; • the introduction of new lines of business or new products and services; • our ability to recruit and retain key employees; • real estate values in our lending area; • changes in accounting principles, standards, rules, and interpretations, and the related impact on our financial statements; • an insufficient ACL or volatility in the ACL resulting from the CECL methodology, either alone or as that may be affected by inflation, changing interest rates, or other factors; • our liquidity and capital positions; • concentrations of loans secured by real estate, particularly commercial real estate; • the effectiveness of our credit processes and management of our credit risk; • our ability to compete in the market for financial services and increased competition from fintech companies; • technological risks and developments, and cyber threats, attacks, or events; • operational, technological, cultural, regulatory, legal, credit, and other risks associated with the exploration, consummation and integration of potential future acquisitions, whether involving stock or cash considerations; • the potential adverse effects of unusual and infrequently occurring events, such as weather-related disasters, terrorist acts, geopolitical conflicts or public health events, and of governmental and societal responses thereto; these potential adverse effects may include, without limitation, adverse effects on the ability of our borrowers to satisfy their obligations to us, on the value of collateral securing loans, on the demand for our loans or our other products and services, on supply chains and methods used to distribute products and services, on incidents of cyberattack and fraud, on our liquidity or capital positions, on risks posed by reliance on third-party service providers, on other aspects of our business operations and on financial markets and economic growth; • performance by our counterparties or vendors; • deposit flows; • the availability of financing and the terms thereof; • the level of prepayments on loans and mortgage-backed securities; • legislative or regulatory changes and requirements; • actual or potential claims, damages, and fines related to litigation or government actions, which may result in, among other things, additional costs, fines, penalties, restrictions on our business activities, reputational harm, or other adverse consequences; • the effects of changes in federal, state or local tax laws and regulations; • any event or development that would cause us to conclude that there was an impairment of any asset, including intangible assets, such as goodwill; and • other factors, many of which are beyond our control. Please also refer to such other factors as discussed throughout Part I, Item 1A. “Risk Factors” and Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of our Annual Report on Form 10-K for the year ended December 31, 2022, Part II, Item 1A. Risk Factors in our Quarterly Reports on Form 10-Q, and related disclosures in other filings, which have been filed with the U.S. Securities and Exchange Commission (“SEC”) and are available on the SEC’s website at www.sec.gov. All risk factors and uncertainties described herein and therein should be considered in evaluating forward-looking statements, and all of the forward-looking statements are expressly our businesses or operations. Readers are cautioned not to rely too heavily on the forward-looking statements, and undue reliance should not be placed on such forward-looking statements. Forward-looking statements speak only as of the date they are made. We do not intend or assume any obligation to update, revise or clarify any forward-looking statements that may be made from time to time by or on behalf of the Company, whether as a result of new information, future events or otherwise. |

|

3 Additional Information Non-GAAP Financial Measures This presentation contains certain financial information determined by methods other than in accordance with generally accepted accounting principles in the United States (“GAAP”). These non-GAAP financial measures are a supplement to GAAP, which is used to prepare the Company’s financial statements, and should not be considered in isolation or as a substitute for comparable measures calculated in accordance with GAAP. In addition, the Company’s non-GAAP financial measures may not be comparable to non-GAAP financial measures of other companies. The Company uses the non-GAAP financial measures discussed herein in its analysis of the Company’s performance. The Company’s management believes that these non-GAAP financial measures provide additional understanding of ongoing operations, enhance comparability of results of operations with prior periods, show the effects of significant gains and charges in the periods presented without the impact of items or events that may obscure trends in the Company’s underlying performance, or show the potential effects of accumulated other comprehensive income (or AOCI) or unrealized losses on securities on the Company's capital. Please see “Reconciliation of Non-GAAP Disclosures” at the end of this presentation for a reconciliation to the nearest GAAP financial measure. No Offer or Solicitation This presentation does not constitute an offer to sell or a solicitation of an offer to buy any securities. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933, as amended, and no offer to sell or solicitation of an offer to buy shall be made in any jurisdiction in which such offer, solicitation or sale would be unlawful. About Atlantic Union Bankshares Corporation Headquartered in Richmond, Virginia, Atlantic Union Bankshares Corporation (NYSE: AUB) is the holding company for Atlantic Union Bank. Atlantic Union Bank has 109 branches and 123 ATMs located throughout Virginia, and in portions of Maryland and North Carolina as of December 31, 2023. Certain non-bank financial services affiliates of Atlantic Union Bank include: Atlantic Union Equipment Finance, Inc., which provides equipment financing; Atlantic Union Financial Consultants, LLC, which provides brokerage services; and Union Insurance Group, LLC, which offers various lines of insurance products. |

|

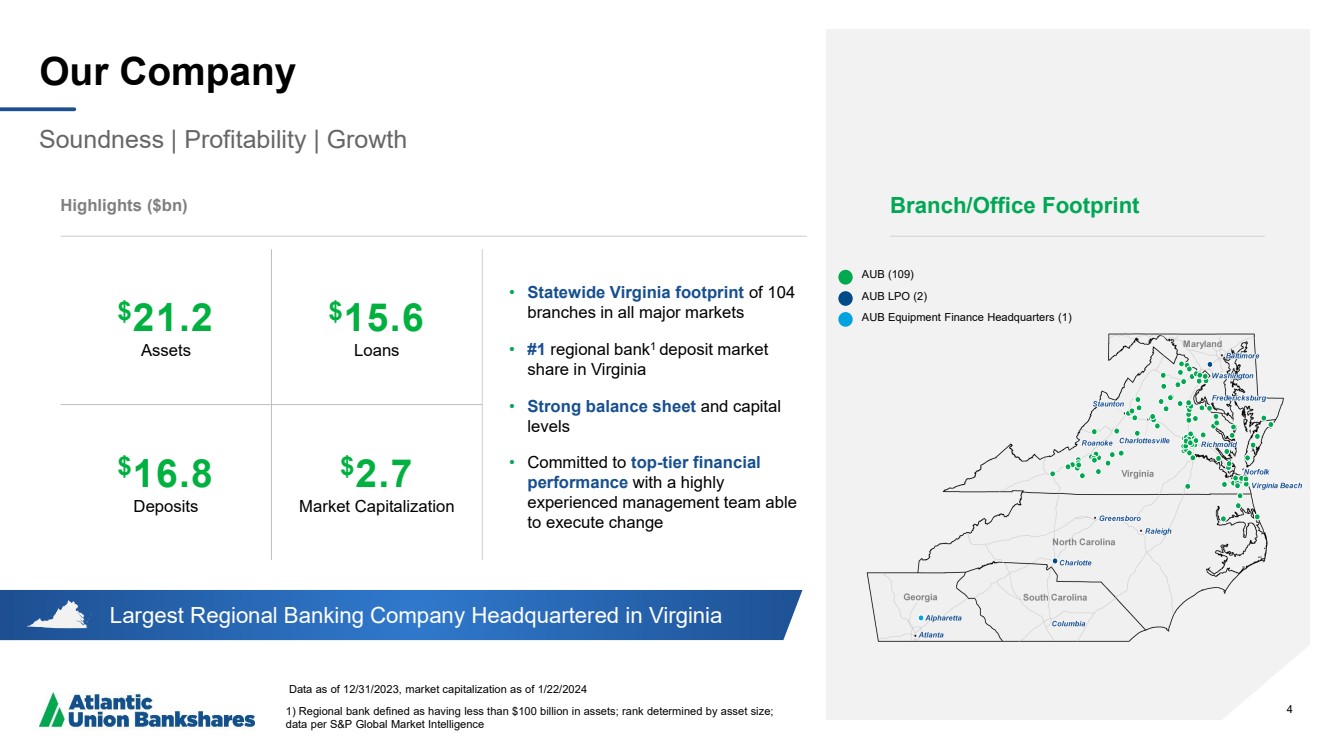

4 Largest Regional Banking Company Headquartered in Virginia Our Company Soundness | Profitability | Growth Data as of 12/31/2023, market capitalization as of 1/22/2024 1) Regional bank defined as having less than $100 billion in assets; rank determined by asset size; data per S&P Global Market Intelligence Highlights ($bn) • Statewide Virginia footprint of 104 branches in all major markets • #1 regional bank1 deposit market share in Virginia • Strong balance sheet and capital levels • Committed to top-tier financial performance with a highly experienced management team able to execute change 4 $21.2 Assets $15.6 Loans $16.8 Deposits $2.7 Market Capitalization Branch/Office Footprint AUB (109) AUB LPO (2) AUB Equipment Finance Headquarters (1) |

|

5 Our Shareholder Value Proposition Leading Regional Presence Dense, uniquely valuable presence across attractive markets Financial Strength Solid balance sheet & capital levels Attractive Financial Profile Solid dividend yield & payout ratio with earnings upside Strong Growth Potential Organic & acquisition opportunities Peer-Leading Performance Committed to top-tier financial performance |

|

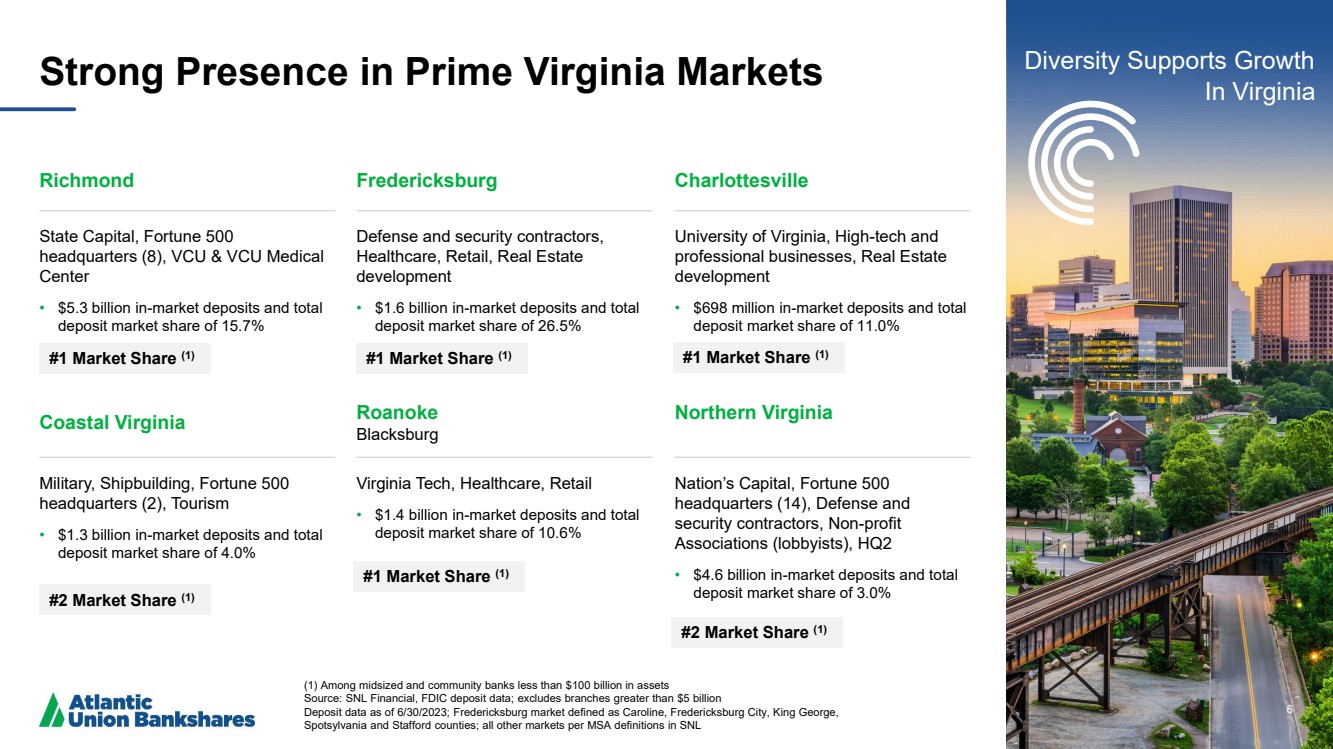

6 Strong Presence in Prime Virginia Markets (1) Among midsized and community banks less than $100 billion in assets Source: SNL Financial, FDIC deposit data; excludes branches greater than $5 billion Deposit data as of 6/30/2023; Fredericksburg market defined as Caroline, Fredericksburg City, King George, Spotsylvania and Stafford counties; all other markets per MSA definitions in SNL 6 Coastal Virginia Military, Shipbuilding, Fortune 500 headquarters (2), Tourism • $1.3 billion in-market deposits and total deposit market share of 4.0% Roanoke Blacksburg Virginia Tech, Healthcare, Retail • $1.4 billion in-market deposits and total deposit market share of 10.6% Northern Virginia Nation’s Capital, Fortune 500 headquarters (14), Defense and security contractors, Non-profit Associations (lobbyists), HQ2 • $4.6 billion in-market deposits and total deposit market share of 3.0% Diversity Supports Growth In Virginia Richmond State Capital, Fortune 500 headquarters (8), VCU & VCU Medical Center • $5.3 billion in-market deposits and total deposit market share of 15.7% Fredericksburg Defense and security contractors, Healthcare, Retail, Real Estate development • $1.6 billion in-market deposits and total deposit market share of 26.5% Charlottesville University of Virginia, High-tech and professional businesses, Real Estate development • $698 million in-market deposits and total deposit market share of 11.0% #1 Market Share (1) #2 Market Share (1) #2 Market Share (1) #1 Market Share (1) #1 Market Share (1) #1 Market Share (1) |

|

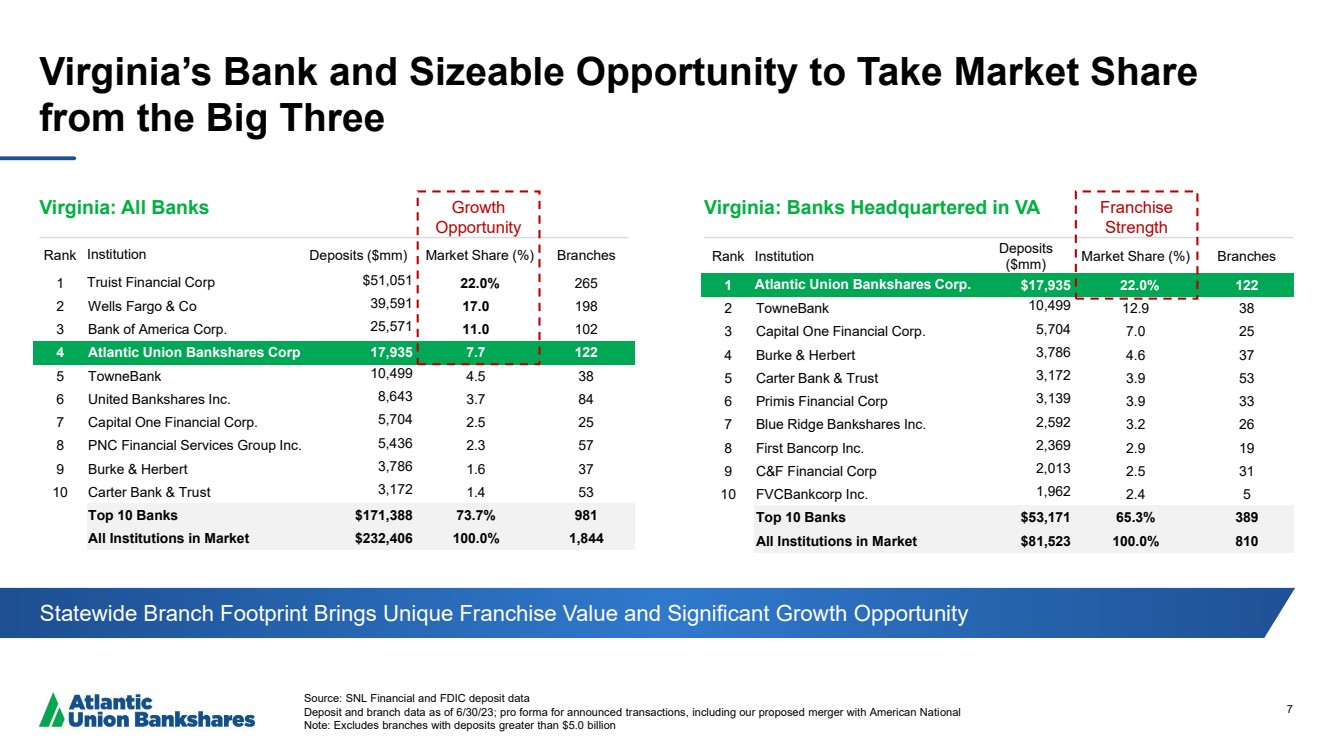

7 Virginia’s Bank and Sizeable Opportunity to Take Market Share from the Big Three Source: SNL Financial and FDIC deposit data Deposit and branch data as of 6/30/23; pro forma for announced transactions, including our proposed merger with American National Note: Excludes branches with deposits greater than $5.0 billion Virginia: All Banks Virginia: Banks Headquartered in VA Rank Institution Deposits ($mm) Market Share (%) Branches 1 Truist Financial Corp $51,051 22.0% 265 2 Wells Fargo & Co 39,591 17.0 198 3 Bank of America Corp. 25,571 11.0 102 4 Atlantic Union Bankshares Corp 17,935 7.7 122 5 TowneBank 10,499 4.5 38 6 United Bankshares Inc. 8,643 3.7 84 7 Capital One Financial Corp. 5,704 2.5 25 8 PNC Financial Services Group Inc. 5,436 2.3 57 9 Burke & Herbert 3,786 1.6 37 10 Carter Bank & Trust 3,172 1.4 53 Top 10 Banks $171,388 73.7% 981 All Institutions in Market $232,406 100.0% 1,844 Rank Institution Deposits ($mm) Market Share (%) Branches 1 Atlantic Union Bankshares Corp. $17,935 22.0% 122 2 TowneBank 10,499 12.9 38 3 Capital One Financial Corp. 5,704 7.0 25 4 Burke & Herbert 3,786 4.6 37 5 Carter Bank & Trust 3,172 3.9 53 6 Primis Financial Corp 3,139 3.9 33 7 Blue Ridge Bankshares Inc. 2,592 3.2 26 8 First Bancorp Inc. 2,369 2.9 19 9 C&F Financial Corp 2,013 2.5 31 10 FVCBankcorp Inc. 1,962 2.4 5 Top 10 Banks $53,171 65.3% 389 All Institutions in Market $81,523 100.0% 810 Statewide Branch Footprint Brings Unique Franchise Value and Significant Growth Opportunity Growth Opportunity Franchise Strength |

|

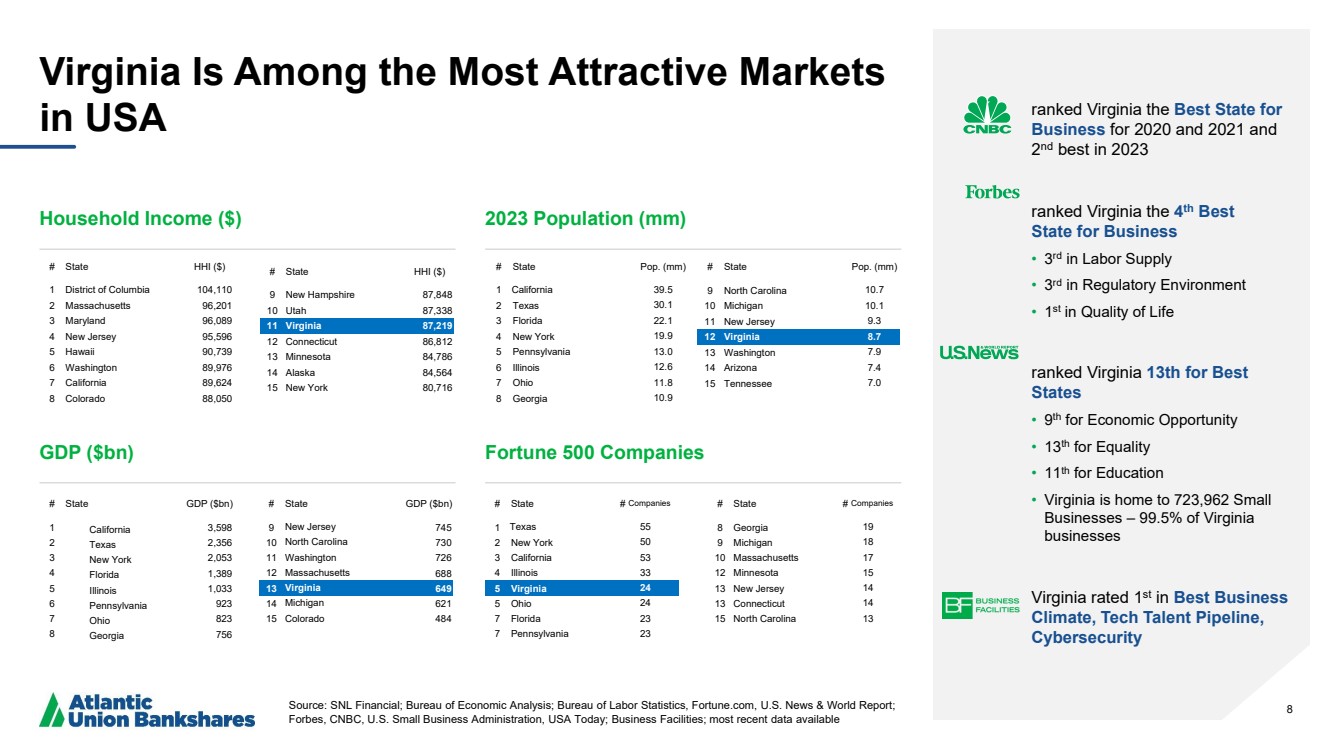

8 Virginia Is Among the Most Attractive Markets in USA Source: SNL Financial; Bureau of Economic Analysis; Bureau of Labor Statistics, Fortune.com, U.S. News & World Report; Forbes, CNBC, U.S. Small Business Administration, USA Today; Business Facilities; most recent data available ranked Virginia the Best State for Business for 2020 and 2021 and 2 nd best in 2023 ranked Virginia the 4 th Best State for Business • 3 rd in Labor Supply • 3 rd in Regulatory Environment • 1 st in Quality of Life ranked Virginia 13th for Best States • 9 th for Economic Opportunity • 13th for Equality • 11th for Education • Virginia is home to 723,962 Small Businesses – 99.5% of Virginia businesses Virginia rated 1st in Best Business Climate, Tech Talent Pipeline, Cybersecurity # State # Companies 1 Texas 55 2 New York 50 3 California 53 4 Illinois 33 5 Virginia 24 5 Ohio 24 7 Florida 23 7 Pennsylvania 23 # State Pop. (mm) 1 California 39.5 2 Texas 30.1 3 Florida 22.1 4 New York 19.9 5 Pennsylvania 13.0 6 Illinois 12.6 7 Ohio 11.8 8 Georgia 10.9 # State HHI ($) 1 District of Columbia 104,110 2 Massachusetts 96,201 3 Maryland 96,089 4 New Jersey 95,596 5 Hawaii 90,739 6 Washington 89,976 7 California 89,624 8 Colorado 88,050 # State GDP ($bn) 1 California 3,598 2 Texas 2,356 3 New York 2,053 4 Florida 1,389 5 Illinois 1,033 6 Pennsylvania 923 7 Ohio 823 8 Georgia 756 Household Income ($) 2023 Population (mm) # State Pop. (mm) 9 North Carolina 10.7 10 Michigan 10.1 11 New Jersey 9.3 12 Virginia 8.7 13 Washington 7.9 14 Arizona 7.4 15 Tennessee 7.0 # State HHI ($) 9 New Hampshire 87,848 10 Utah 87,338 11 Virginia 87,219 12 Connecticut 86,812 13 Minnesota 84,786 14 Alaska 84,564 15 New York 80,716 GDP ($bn) Fortune 500 Companies # State # Companies 8 Georgia 19 9 Michigan 18 10 Massachusetts 17 12 Minnesota 15 13 New Jersey 14 13 Connecticut 14 15 North Carolina 13 # State GDP ($bn) 9 New Jersey 745 10 North Carolina 730 11 Washington 726 12 Massachusetts 688 13 Virginia 649 14 Michigan 621 15 Colorado 484 |

|

9 Q4 2023 and FY 2023 Highlights Loan and Deposit Growth • 9.1% annualized loan growth in Q4 2023 and 8.2% for FY 2023 • 0.7% annualized deposit growth in Q4 2023 and 5.6% for FY 2023 • Line of Credit Utilization increased modestly from Q3 2023 Asset Quality • Q4 2023 net charge-offs at 3 bps annualized and net charge-offs of 5 bps for FY 2023 Positioning for Long Term • In 2023, restructured the Company’s securities portfolio by ~$500mm in February/March and ~$200mm in the third quarter to improve go-forward earnings trajectory • Lending pipelines down moderately • Granular growing deposit base • Focus on organic growth and performance of the core banking franchise Differentiated Client Experience • Responsive, strong and capable alternative to large national banks, while competitive with and more capable than smaller banks Operating Leverage Focus • ~2.8% adjusted revenue growth1 year over year • ~1.8% adjusted operating noninterest expense increase1 year over year • Adjusted operating leverage1 of ~1.0% year over year • Took strategic actions to reduce expenses in Q2 Capitalize on Strategic Opportunities • Announced intention to acquire American National Bankshares and expect to close in the first quarter of 2024 9 1 For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures.”’ Adjusted operating leverage is for the full year 2023 compared to the full year 2022. |

|

10 Caring Working together toward common goals, acting with kindness, respect and a genuine concern for others. Courageous Speaking openly, honestly and accepting our challenges and mistakes as opportunities to learn and grow. Committed Driven to help our clients, Teammates and company succeed, doing what is right and accountable for our actions. Our Core Values Culture — HOW we come together and interact as a team to accomplish our business and societal goals. Diversity, Equity, Inclusion, and Belonging Statement Atlantic Union Bank embraces diversity of thought and identity to better serve our stakeholders and achieve our purpose. We commit to cultivating a welcoming workplace where Teammate and customer perspectives are valued and respected. |

|

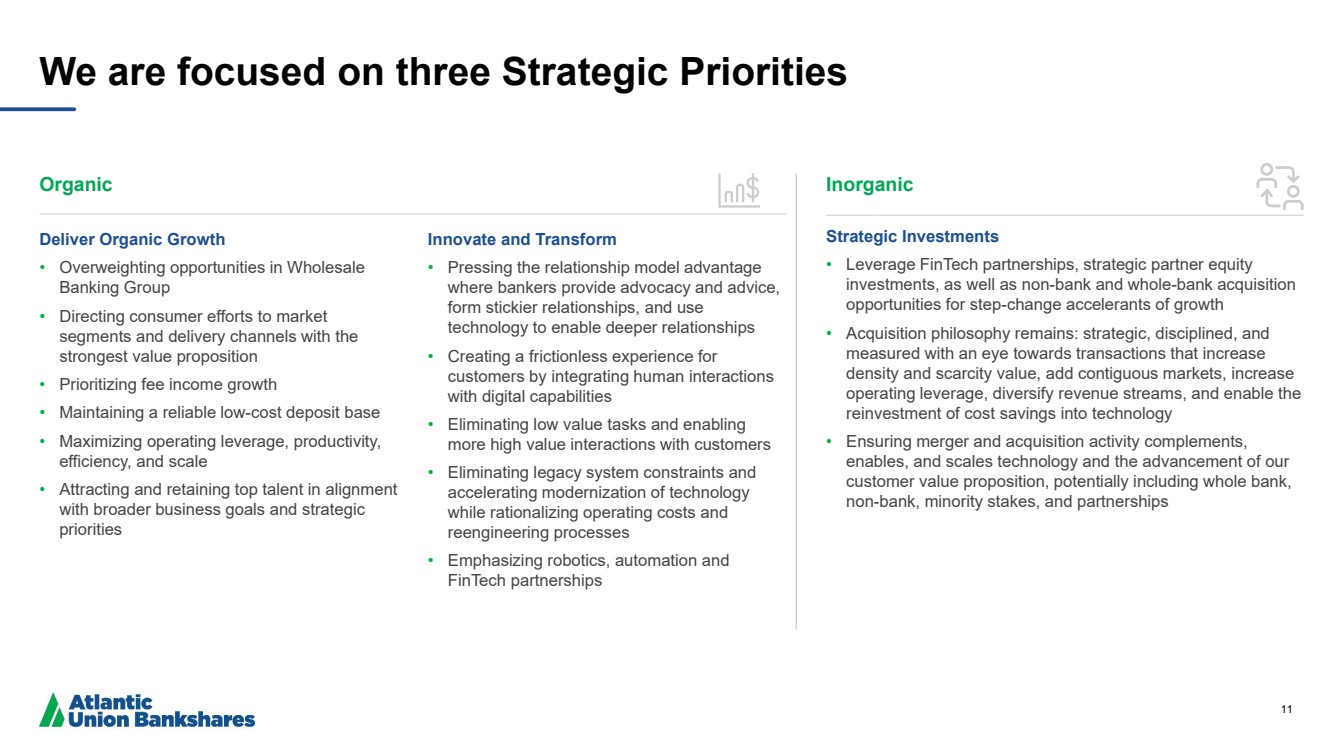

11 We are focused on three Strategic Priorities Organic Deliver Organic Growth • Overweighting opportunities in Wholesale Banking Group • Directing consumer efforts to market segments and delivery channels with the strongest value proposition • Prioritizing fee income growth • Maintaining a reliable low-cost deposit base • Maximizing operating leverage, productivity, efficiency, and scale • Attracting and retaining top talent in alignment with broader business goals and strategic priorities Innovate and Transform • Pressing the relationship model advantage where bankers provide advocacy and advice, form stickier relationships, and use technology to enable deeper relationships • Creating a frictionless experience for customers by integrating human interactions with digital capabilities • Eliminating low value tasks and enabling more high value interactions with customers • Eliminating legacy system constraints and accelerating modernization of technology while rationalizing operating costs and reengineering processes • Emphasizing robotics, automation and FinTech partnerships Inorganic Strategic Investments • Leverage FinTech partnerships, strategic partner equity investments, as well as non-bank and whole-bank acquisition opportunities for step-change accelerants of growth • Acquisition philosophy remains: strategic, disciplined, and measured with an eye towards transactions that increase density and scarcity value, add contiguous markets, increase operating leverage, diversify revenue streams, and enable the reinvestment of cost savings into technology • Ensuring merger and acquisition activity complements, enables, and scales technology and the advancement of our customer value proposition, potentially including whole bank, non-bank, minority stakes, and partnerships |

|

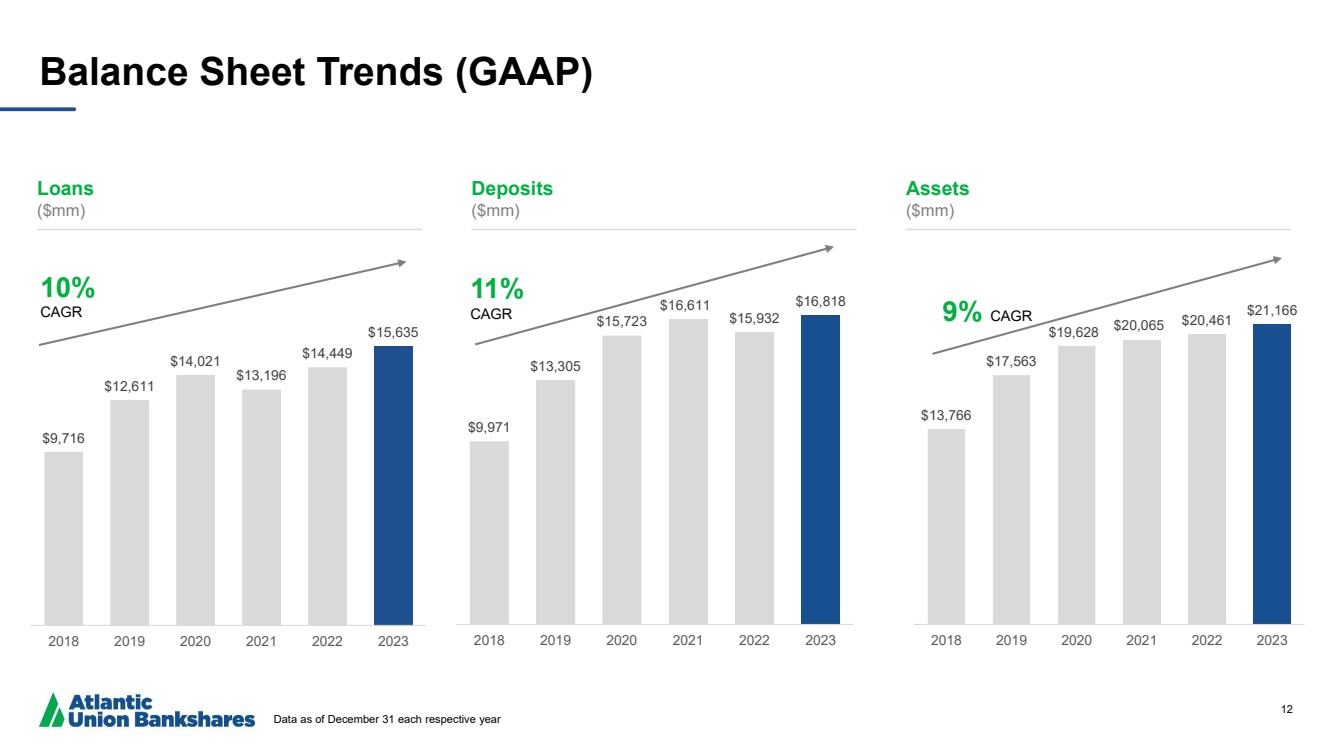

12 $9,971 $13,305 $15,723 $16,611 $15,932 $16,818 2018 2019 2020 2021 2022 2023 11% CAGR Balance Sheet Trends (GAAP) Data as of December 31 each respective year Loans ($mm) Deposits ($mm) Assets ($mm) 10% CAGR $13,766 $17,563 $19,628 $20,065 $20,461 $21,166 2018 2019 2020 2021 2022 2023 9% CAGR $9,716 $12,611 $14,021 $13,196 $14,449 $15,635 2018 2019 2020 2021 2022 2023 |

|

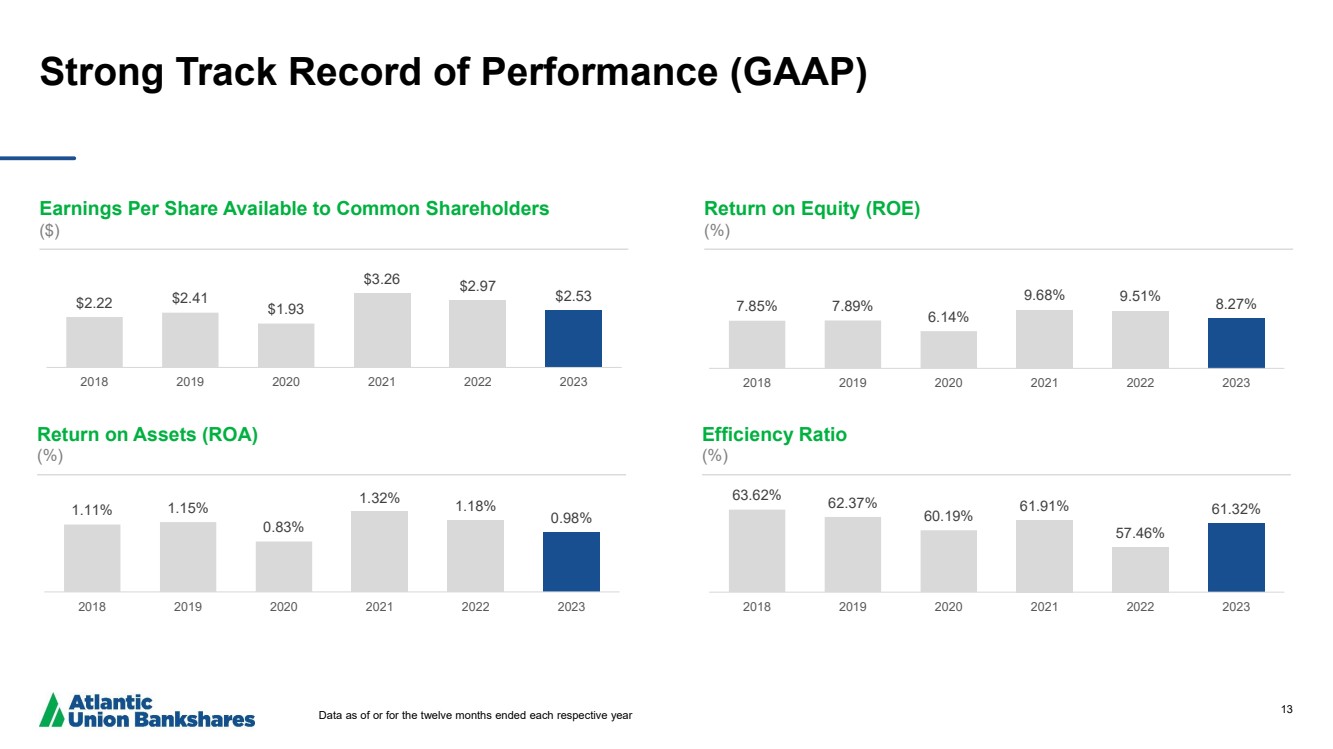

13 Strong Track Record of Performance (GAAP) Earnings Per Share Available to Common Shareholders ($) Return on Equity (ROE) (%) Return on Assets (ROA) (%) Efficiency Ratio (%) $2.22 $2.41 $1.93 $3.26 $2.97 $2.53 2018 2019 2020 2021 2022 2023 7.85% 7.89% 6.14% 9.68% 9.51% 8.27% 2018 2019 2020 2021 2022 2023 63.62% 62.37% 60.19% 61.91% 57.46% 61.32% 2018 2019 2020 2021 2022 2023 1.11% 1.15% 0.83% 1.32% 1.18% 0.98% 2018 2019 2020 2021 2022 2023 Data as of or for the twelve months ended each respective year |

|

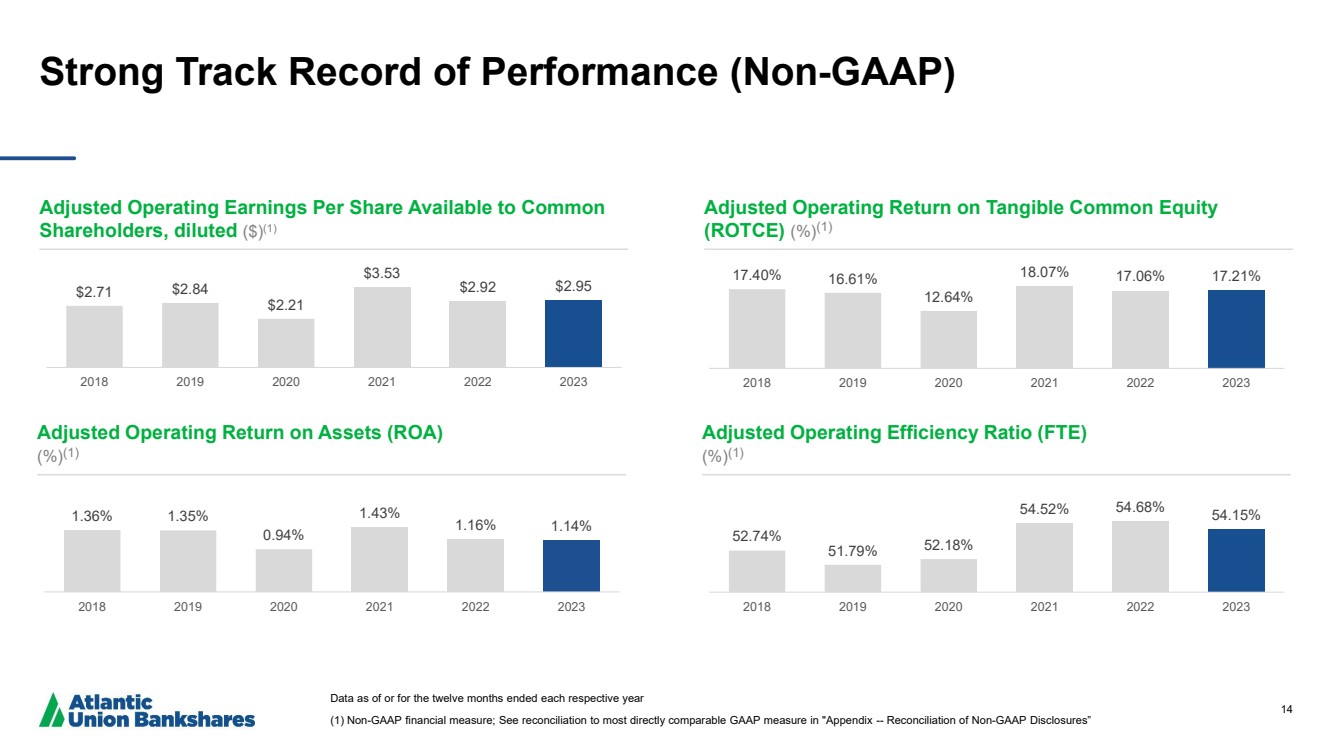

14 Strong Track Record of Performance (Non-GAAP) Data as of or for the twelve months ended each respective year (1) Non-GAAP financial measure; See reconciliation to most directly comparable GAAP measure in "Appendix -- Reconciliation of Non-GAAP Disclosures” Adjusted Operating Earnings Per Share Available to Common Shareholders, diluted ($)(1) Adjusted Operating Return on Tangible Common Equity (ROTCE) (%)(1) Adjusted Operating Return on Assets (ROA) (%)(1) Adjusted Operating Efficiency Ratio (FTE) (%)(1) $2.71 $2.84 $2.21 $3.53 $2.92 $2.95 2018 2019 2020 2021 2022 2023 17.40% 16.61% 12.64% 18.07% 17.06% 17.21% 2018 2019 2020 2021 2022 2023 52.74% 51.79% 52.18% 54.52% 54.68% 54.15% 2018 2019 2020 2021 2022 2023 1.36% 1.35% 0.94% 1.43% 1.16% 1.14% 2018 2019 2020 2021 2022 2023 |

|

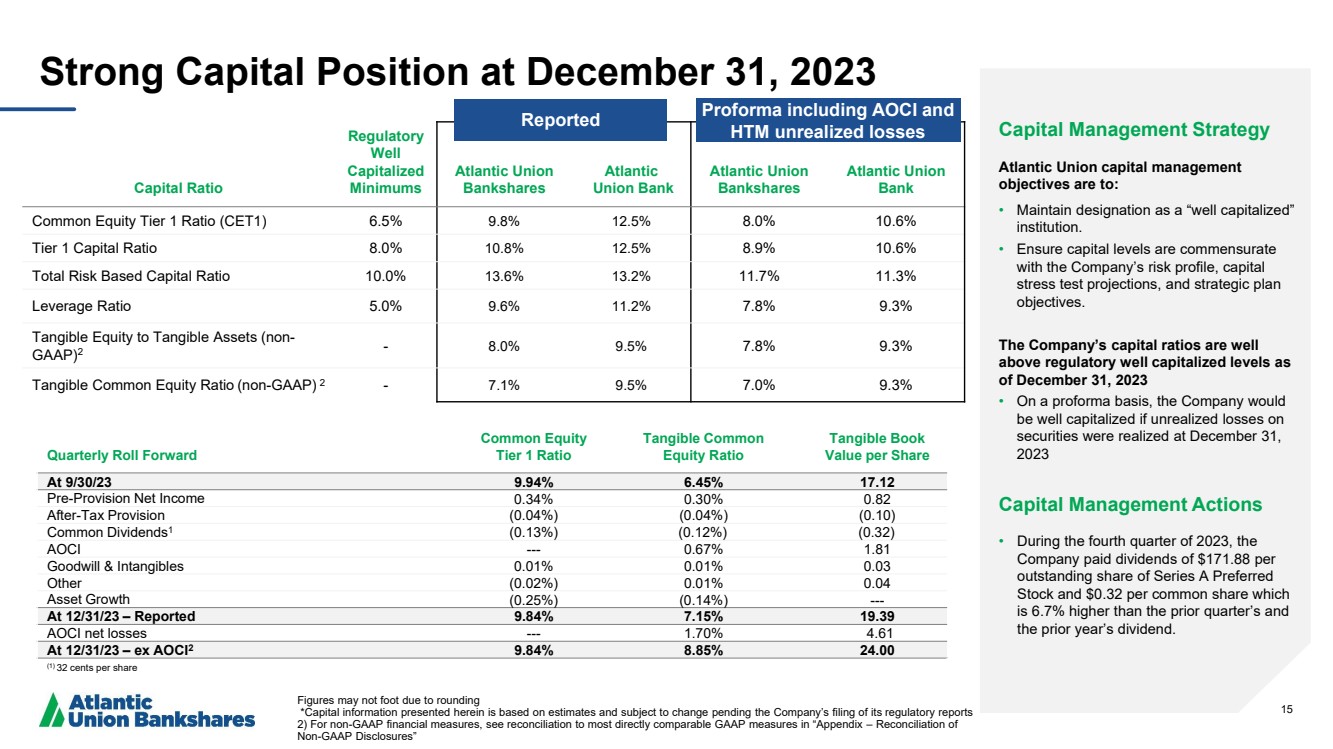

15 Capital Ratio Regulatory Well Capitalized Minimums Atlantic Union Bankshares Atlantic Union Bank Atlantic Union Bankshares Atlantic Union Bank Common Equity Tier 1 Ratio (CET1) 6.5% 9.8% 12.5% 8.0% 10.6% Tier 1 Capital Ratio 8.0% 10.8% 12.5% 8.9% 10.6% Total Risk Based Capital Ratio 10.0% 13.6% 13.2% 11.7% 11.3% Leverage Ratio 5.0% 9.6% 11.2% 7.8% 9.3% Tangible Equity to Tangible Assets (non-GAAP)2 - 8.0% 9.5% 7.8% 9.3% Tangible Common Equity Ratio (non-GAAP) 2 - 7.1% 9.5% 7.0% 9.3% Strong Capital Position at December 31, 2023 Figures may not foot due to rounding *Capital information presented herein is based on estimates and subject to change pending the Company’s filing of its regulatory reports 2) For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” Capital Management Strategy Atlantic Union capital management objectives are to: • Maintain designation as a “well capitalized” institution. • Ensure capital levels are commensurate with the Company’s risk profile, capital stress test projections, and strategic plan objectives. The Company’s capital ratios are well above regulatory well capitalized levels as of December 31, 2023 • On a proforma basis, the Company would be well capitalized if unrealized losses on securities were realized at December 31, 2023 Capital Management Actions • During the fourth quarter of 2023, the Company paid dividends of $171.88 per outstanding share of Series A Preferred Stock and $0.32 per common share which is 6.7% higher than the prior quarter’s and the prior year’s dividend. Quarterly Roll Forward Common Equity Tier 1 Ratio Tangible Common Equity Ratio Tangible Book Value per Share At 9/30/23 9.94% 6.45% 17.12 Pre-Provision Net Income 0.34% 0.30% 0.82 After-Tax Provision (0.04%) (0.04%) (0.10) Common Dividends1 (0.13%) (0.12%) (0.32) AOCI --- 0.67% 1.81 Goodwill & Intangibles 0.01% 0.01% 0.03 Other (0.02%) 0.01% 0.04 Asset Growth (0.25%) (0.14%) --- At 12/31/23 – Reported 9.84% 7.15% 19.39 AOCI net losses --- 1.70% 4.61 At 12/31/23 – ex AOCI2 9.84% 8.85% 24.00 (1) 32 cents per share Reported Proforma including AOCI and HTM unrealized losses |

|

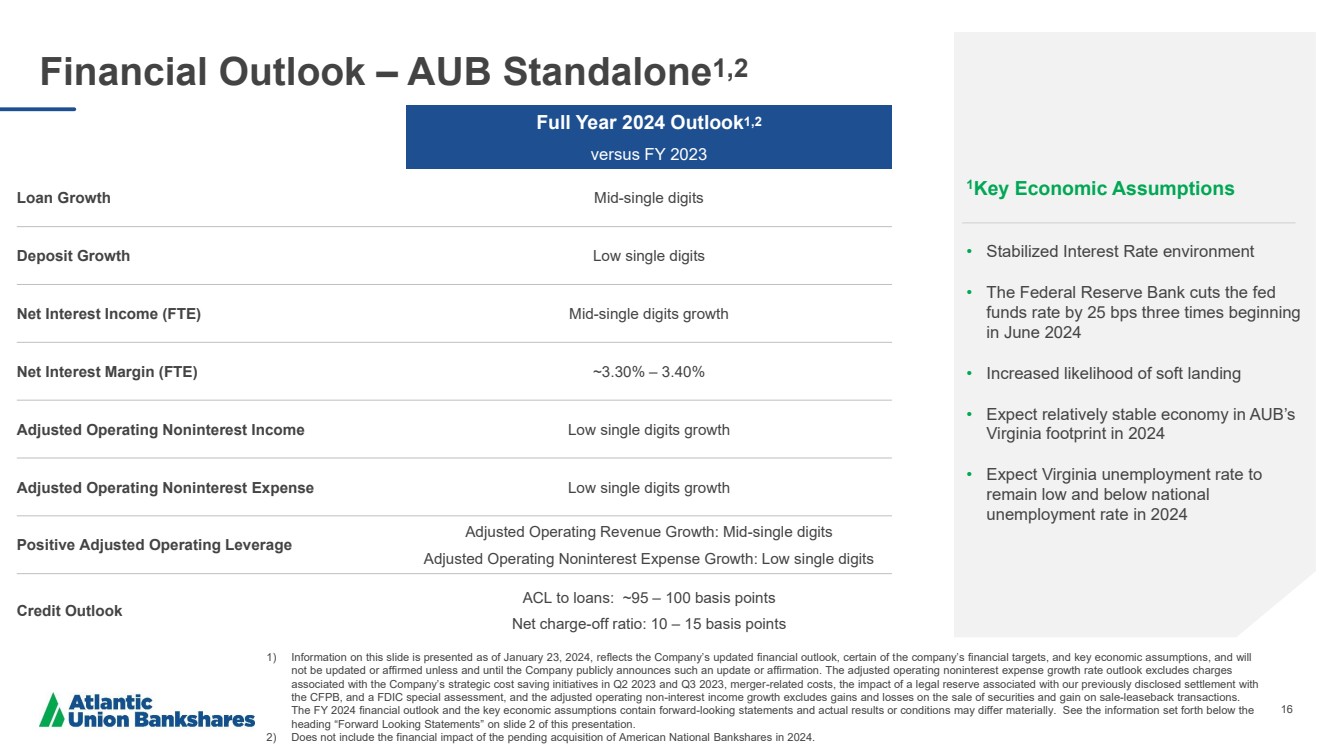

16 Financial Outlook – AUB Standalone1,2 1Key Economic Assumptions • Stabilized Interest Rate environment • The Federal Reserve Bank cuts the fed funds rate by 25 bps three times beginning in June 2024 • Increased likelihood of soft landing • Expect relatively stable economy in AUB’s Virginia footprint in 2024 • Expect Virginia unemployment rate to remain low and below national unemployment rate in 2024 Full Year 2024 Outlook1,2 versus FY 2023 Loan Growth Mid-single digits Deposit Growth Low single digits Net Interest Income (FTE) Mid-single digits growth Net Interest Margin (FTE) ~3.30% – 3.40% Adjusted Operating Noninterest Income Low single digits growth Adjusted Operating Noninterest Expense Low single digits growth Positive Adjusted Operating Leverage Adjusted Operating Revenue Growth: Mid-single digits Adjusted Operating Noninterest Expense Growth: Low single digits Credit Outlook ACL to loans: ~95 – 100 basis points Net charge-off ratio: 10 – 15 basis points 1) Information on this slide is presented as of January 23, 2024, reflects the Company’s updated financial outlook, certain of the company’s financial targets, and key economic assumptions, and will not be updated or affirmed unless and until the Company publicly announces such an update or affirmation. The adjusted operating noninterest expense growth rate outlook excludes charges associated with the Company’s strategic cost saving initiatives in Q2 2023 and Q3 2023, merger-related costs, the impact of a legal reserve associated with our previously disclosed settlement with the CFPB, and a FDIC special assessment, and the adjusted operating non-interest income growth excludes gains and losses on the sale of securities and gain on sale-leaseback transactions. The FY 2024 financial outlook and the key economic assumptions contain forward-looking statements and actual results or conditions may differ materially. See the information set forth below the heading “Forward Looking Statements” on slide 2 of this presentation. 2) Does not include the financial impact of the pending acquisition of American National Bankshares in 2024. |

|

17 Appendix |

|

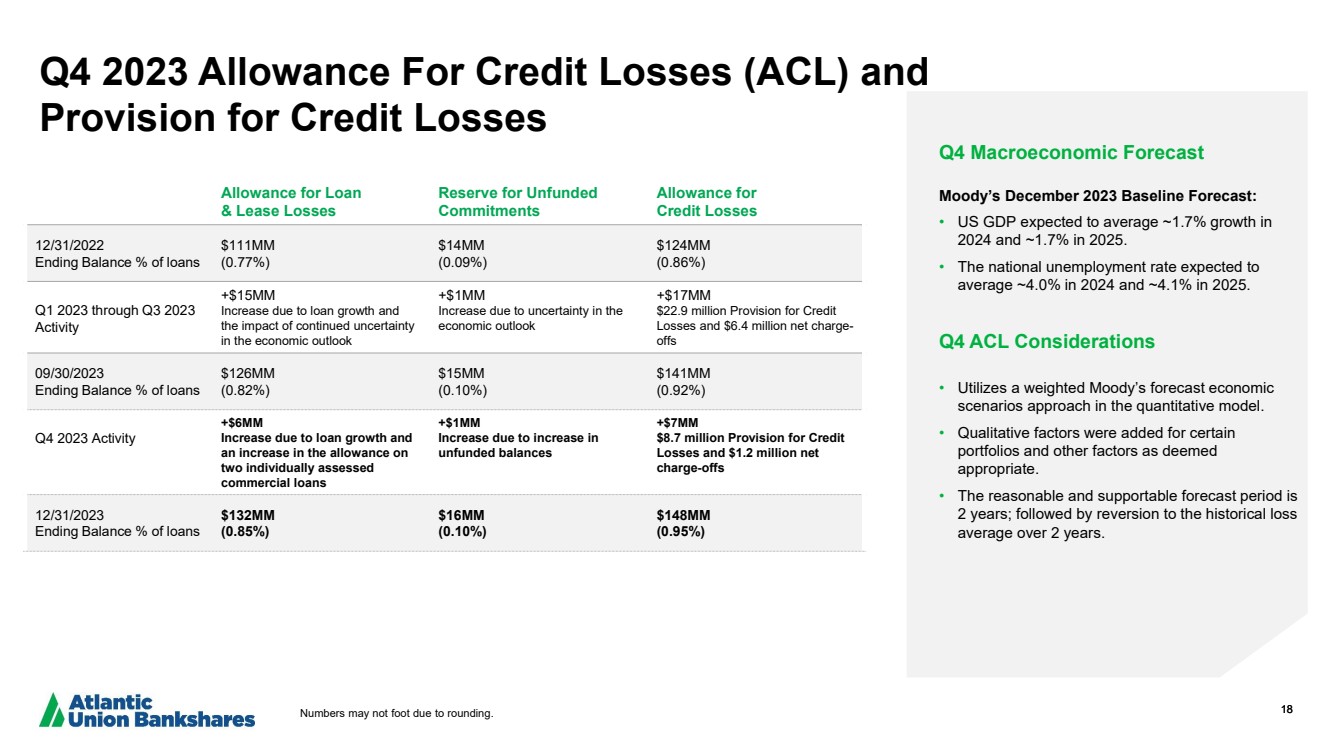

18 Q4 2023 Allowance For Credit Losses (ACL) and Provision for Credit Losses Q4 Macroeconomic Forecast Moody’s December 2023 Baseline Forecast: • US GDP expected to average ~1.7% growth in 2024 and ~1.7% in 2025. • The national unemployment rate expected to average ~4.0% in 2024 and ~4.1% in 2025. Q4 ACL Considerations • Utilizes a weighted Moody’s forecast economic scenarios approach in the quantitative model. • Qualitative factors were added for certain portfolios and other factors as deemed appropriate. • The reasonable and supportable forecast period is 2 years; followed by reversion to the historical loss average over 2 years. Allowance for Loan & Lease Losses Reserve for Unfunded Commitments Allowance for Credit Losses 12/31/2022 Ending Balance % of loans $111MM (0.77%) $14MM (0.09%) $124MM (0.86%) Q1 2023 through Q3 2023 Activity +$15MM Increase due to loan growth and the impact of continued uncertainty in the economic outlook +$1MM Increase due to uncertainty in the economic outlook +$17MM $22.9 million Provision for Credit Losses and $6.4 million net charge-offs 09/30/2023 Ending Balance % of loans $126MM (0.82%) $15MM (0.10%) $141MM (0.92%) Q4 2023 Activity +$6MM Increase due to loan growth and an increase in the allowance on two individually assessed commercial loans +$1MM Increase due to increase in unfunded balances +$7MM $8.7 million Provision for Credit Losses and $1.2 million net charge-offs 12/31/2023 Ending Balance % of loans $132MM (0.85%) $16MM (0.10%) $148MM (0.95%) Numbers may not foot due to rounding. |

|

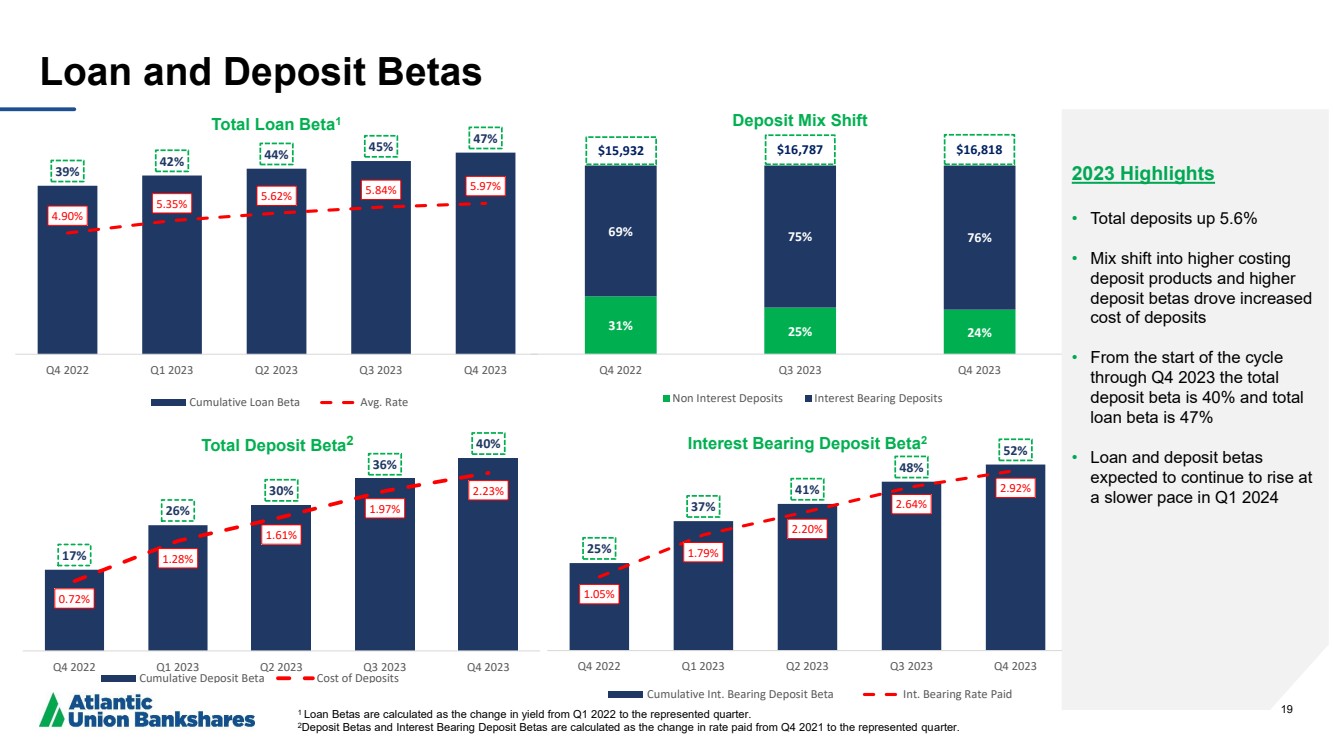

19 25% 37% 41% 48% 52% 1.05% 1.79% 2.20% 2.64% 2.92% Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Interest Bearing Deposit Beta2 Cumulative Int. Bearing Deposit Beta Int. Bearing Rate Paid 31% 25% 24% 69% 75% 76% Q4 2022 Q3 2023 Q4 2023 Deposit Mix Shift Non Interest Deposits Interest Bearing Deposits $15,932 $16,787 $16,818 Loan and Deposit Betas 2023 Highlights • Total deposits up 5.6% • Mix shift into higher costing deposit products and higher deposit betas drove increased cost of deposits • From the start of the cycle through Q4 2023 the total deposit beta is 40% and total loan beta is 47% • Loan and deposit betas expected to continue to rise at a slower pace in Q1 2024 1 Loan Betas are calculated as the change in yield from Q1 2022 to the represented quarter. 2Deposit Betas and Interest Bearing Deposit Betas are calculated as the change in rate paid from Q4 2021 to the represented quarter. 17% 26% 30% 36% 40% 0.72% 1.28% 1.61% 1.97% 2.23% Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Total Deposit Beta2 Cumulative Deposit Beta Cost of Deposits 39% 42% 44% 45% 47% 4.90% 5.35% 5.62% 5.84% 5.97% Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Total Loan Beta1 Cumulative Loan Beta Avg. Rate |

|

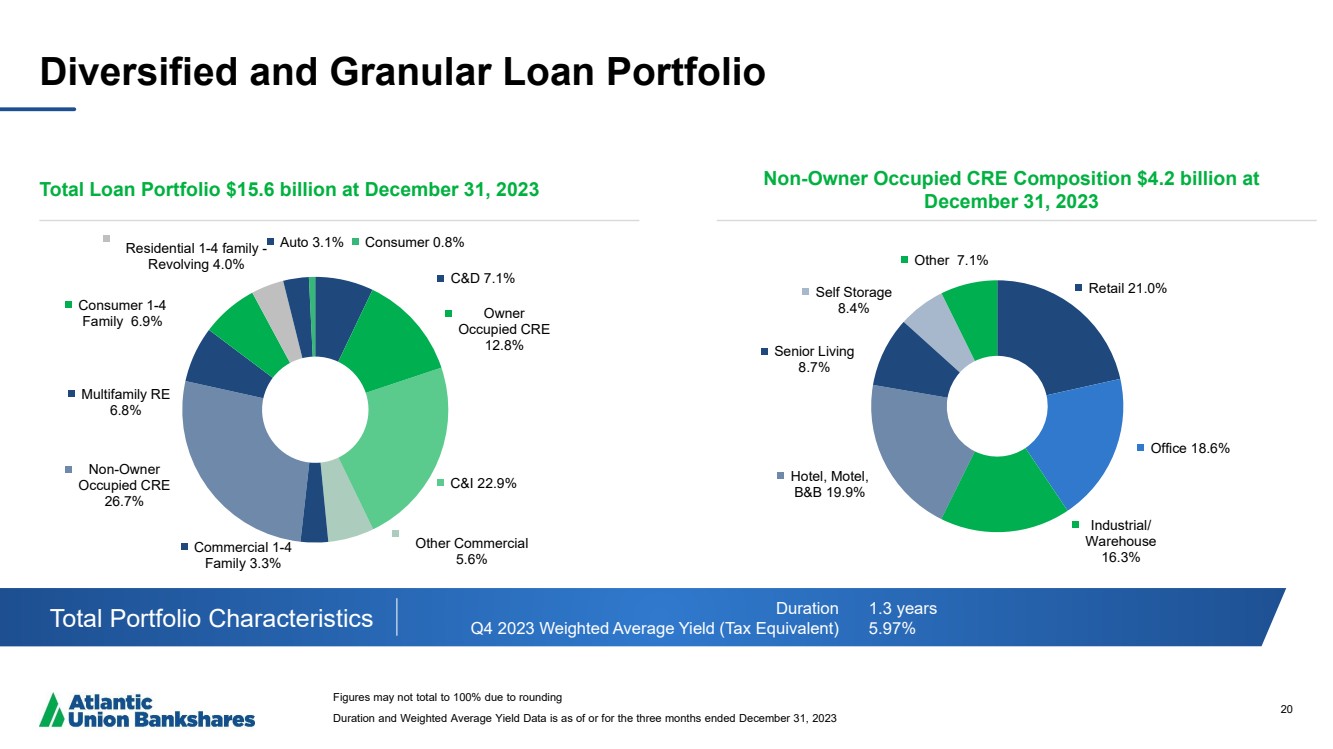

20 Diversified and Granular Loan Portfolio Total Loan Portfolio $15.6 billion at December 31, 2023 Non-Owner Occupied CRE Composition $4.2 billion at December 31, 2023 Total Portfolio Characteristics Duration Q4 2023 Weighted Average Yield (Tax Equivalent) 1.3 years 5.97% Figures may not total to 100% due to rounding Duration and Weighted Average Yield Data is as of or for the three months ended December 31, 2023 C&D 7.1% Owner Occupied CRE 12.8% C&I 22.9% Other Commercial 5.6% Commercial 1-4 Family 3.3% Non-Owner Occupied CRE 26.7% Multifamily RE 6.8% Consumer 1-4 Family 6.9% Residential 1-4 family - Revolving 4.0% Auto 3.1% Consumer 0.8% Retail 21.0% Office 18.6% Industrial/ Warehouse 16.3% Hotel, Motel, B&B 19.9% Senior Living 8.7% Self Storage 8.4% Other 7.1% |

|

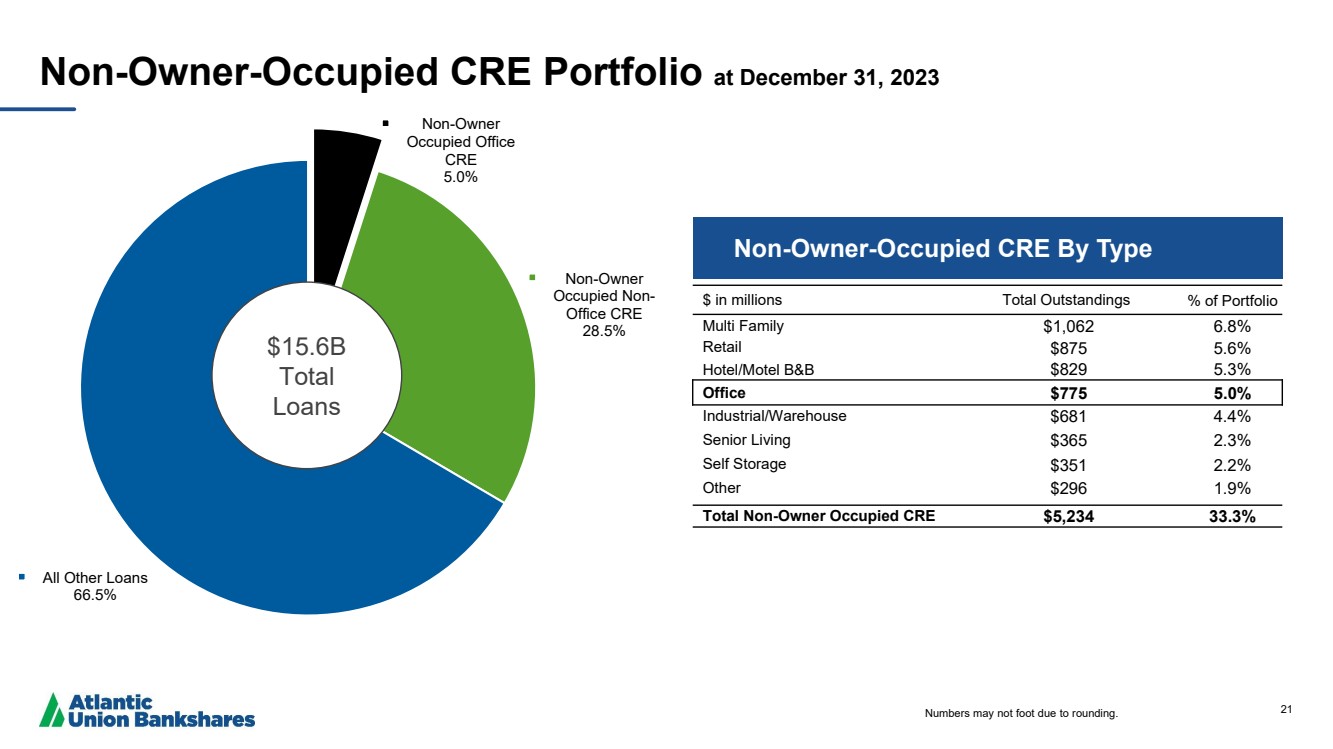

21 Non-Owner Occupied Office CRE 5.0% Non-Owner Occupied Non-Office CRE 28.5% All Other Loans 66.5% Non-Owner-Occupied CRE Portfolio at December 31, 2023 $ in millions Total Outstandings % of Portfolio Multi Family $1,062 6.8% Retail $875 5.6% Hotel/Motel B&B $829 5.3% Office $775 5.0% Industrial/Warehouse $681 4.4% Senior Living $365 2.3% Self Storage $351 2.2% Other $296 1.9% Total Non-Owner Occupied CRE $5,234 33.3% $15.6B Total Loans Non-Owner-Occupied CRE By Type Numbers may not foot due to rounding. |

|

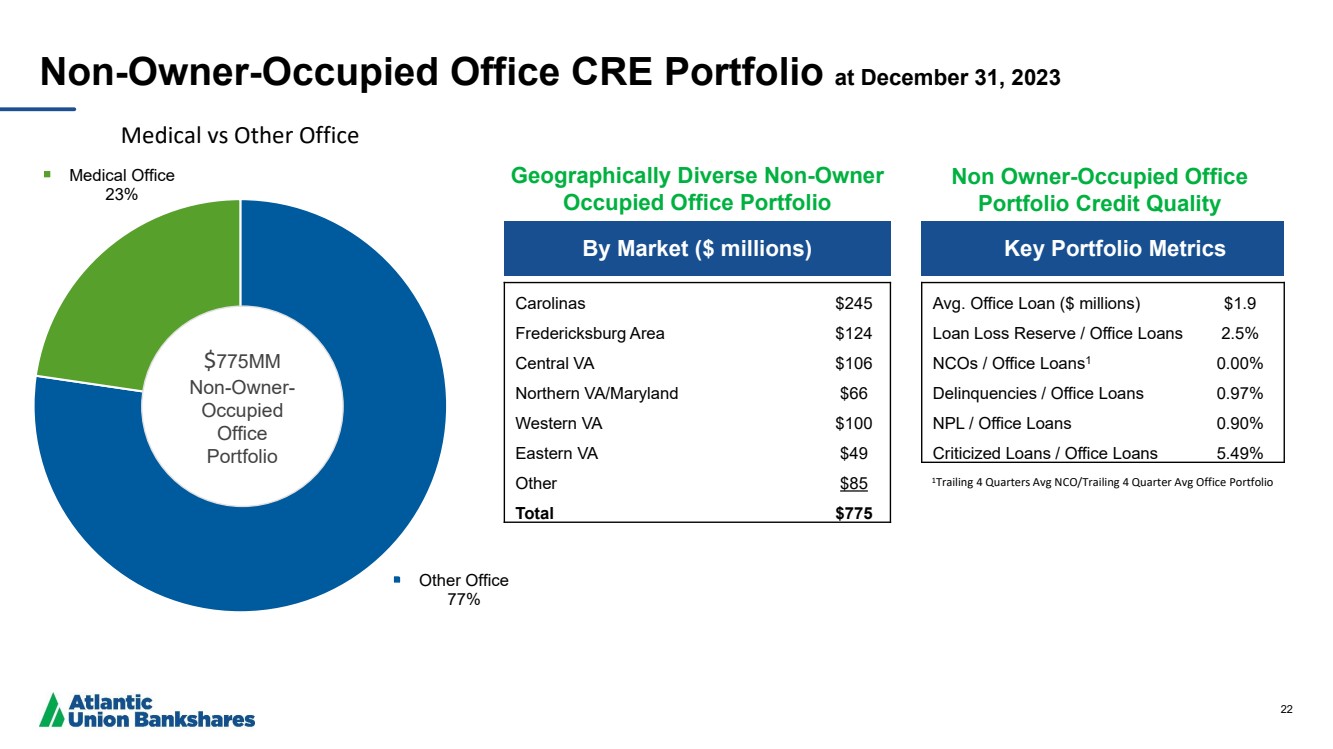

22 Other Office 77% Medical Office 23% Medical vs Other Office By Market ($ millions) Key Portfolio Metrics Carolinas $245 Fredericksburg Area $124 Central VA $106 Northern VA/Maryland $66 Western VA $100 Eastern VA $49 Other $85 Total $775 Avg. Office Loan ($ millions) $1.9 Loan Loss Reserve / Office Loans 2.5% NCOs / Office Loans1 0.00% Delinquencies / Office Loans 0.97% NPL / Office Loans 0.90% Criticized Loans / Office Loans 5.49% Non-Owner-Occupied Office CRE Portfolio at December 31, 2023 $775MM Non-Owner-Occupied Office Portfolio Non Owner-Occupied Office Portfolio Credit Quality Geographically Diverse Non-Owner Occupied Office Portfolio 1Trailing 4 Quarters Avg NCO/Trailing 4 Quarter Avg Office Portfolio |

|

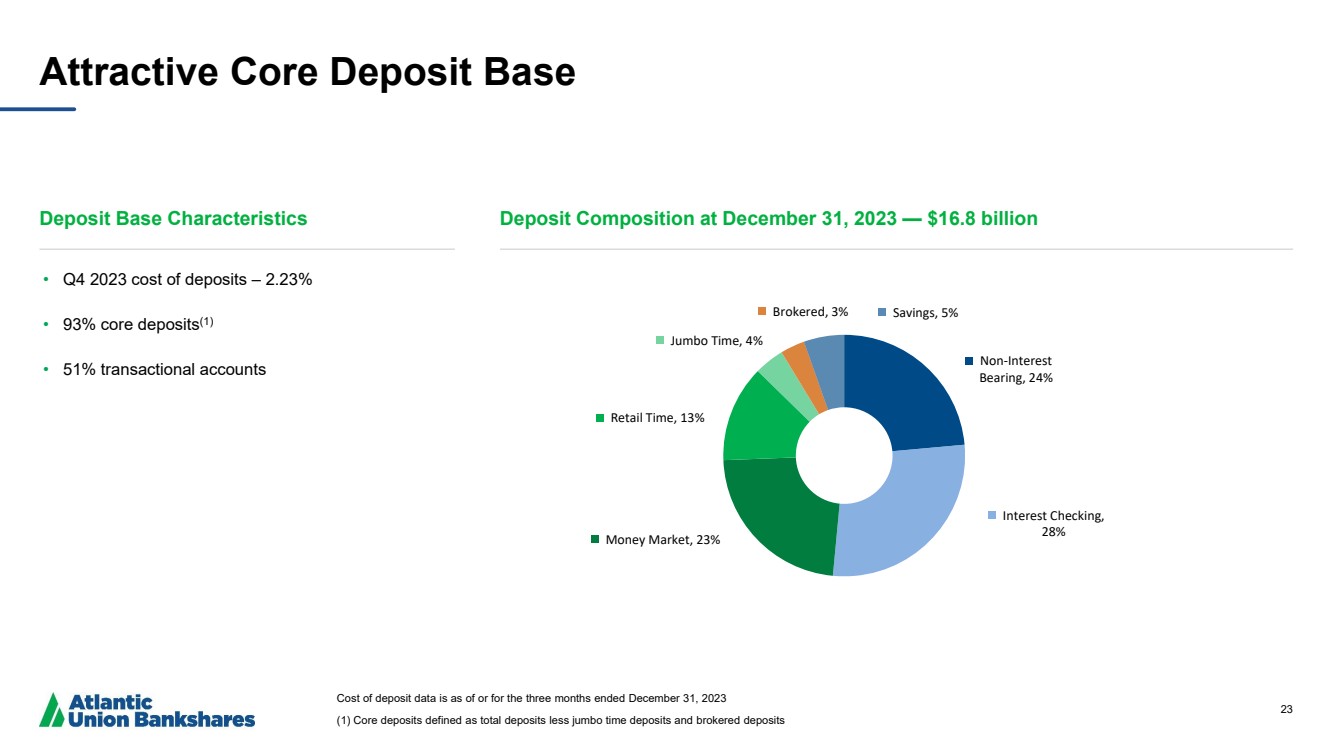

23 Attractive Core Deposit Base Deposit Base Characteristics Deposit Composition at December 31, 2023 — $16.8 billion Cost of deposit data is as of or for the three months ended December 31, 2023 (1) Core deposits defined as total deposits less jumbo time deposits and brokered deposits • Q4 2023 cost of deposits – 2.23% • 93% core deposits(1) • 51% transactional accounts Non-Interest Bearing, 24% Interest Checking, 28% Money Market, 23% Retail Time, 13% Jumbo Time, 4% Brokered, 3% Savings, 5% |

|

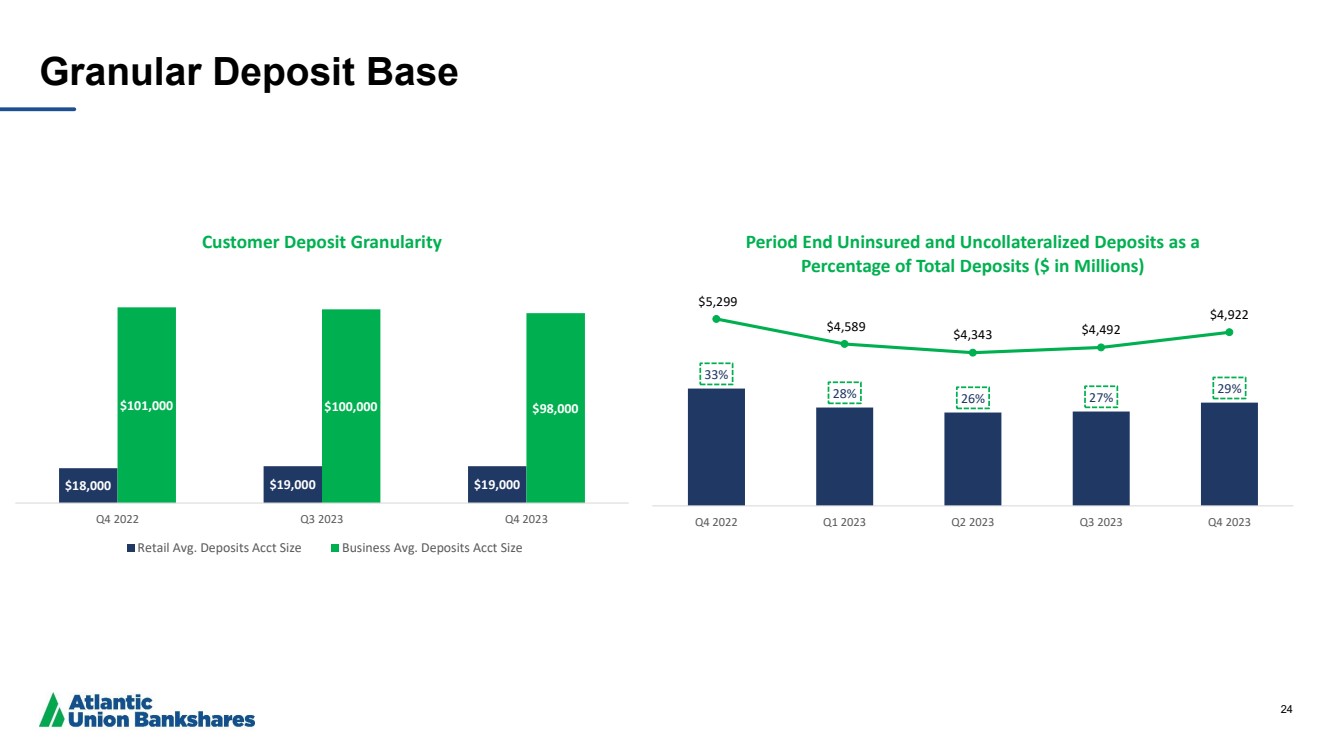

24 Granular Deposit Base 33% 28% 26% 27% 29% $5,299 $4,589 $4,343 $4,492 $4,922 Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Period End Uninsured and Uncollateralized Deposits as a Percentage of Total Deposits ($ in Millions) $18,000 $19,000 $19,000 $101,000 $100,000 $98,000 Q4 2022 Q3 2023 Q4 2023 Customer Deposit Granularity Retail Avg. Deposits Acct Size Business Avg. Deposits Acct Size |

|

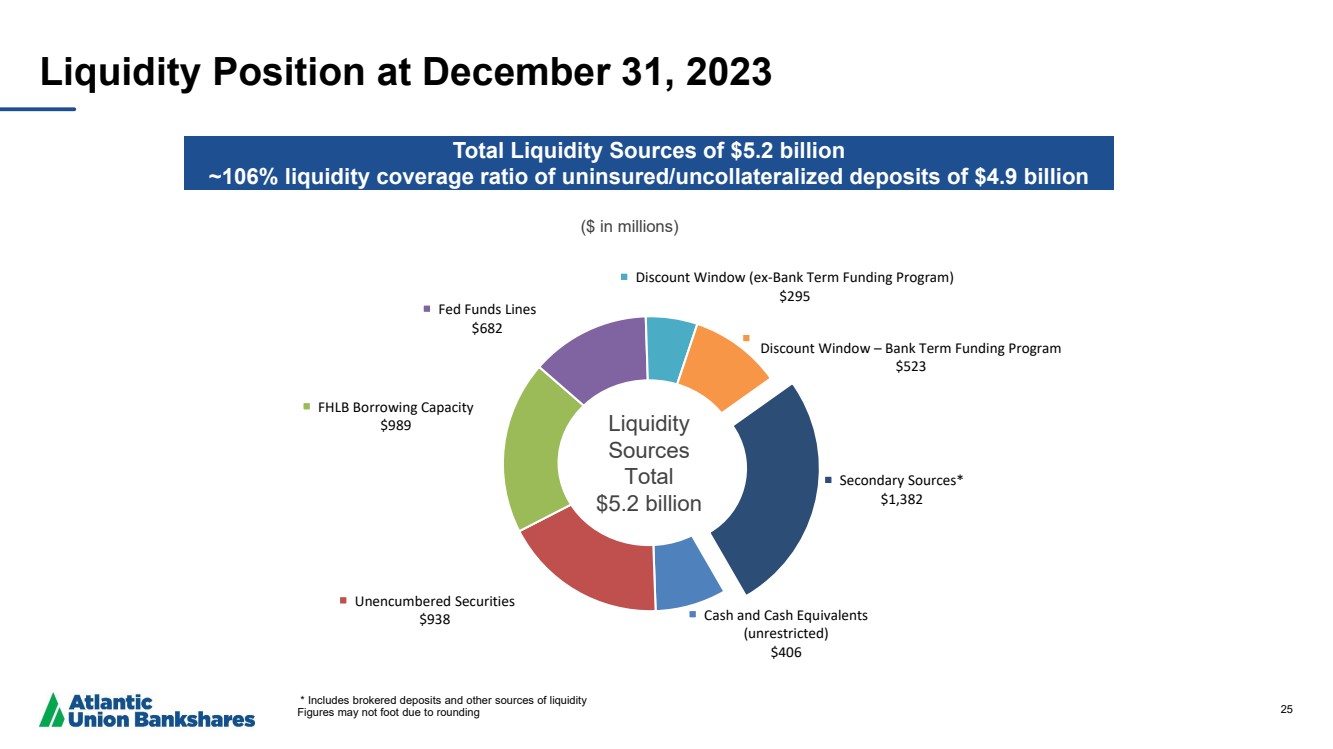

25 Cash and Cash Equivalents (unrestricted) $406 Unencumbered Securities $938 FHLB Borrowing Capacity $989 Fed Funds Lines $682 Discount Window (ex-Bank Term Funding Program) $295 Discount Window – Bank Term Funding Program $523 Secondary Sources* $1,382 ($ in millions) Liquidity Position at December 31, 2023 Total Liquidity Sources of $5.2 billion ~106% liquidity coverage ratio of uninsured/uncollateralized deposits of $4.9 billion * Includes brokered deposits and other sources of liquidity Figures may not foot due to rounding Liquidity Sources Total $5.2 billion |

|

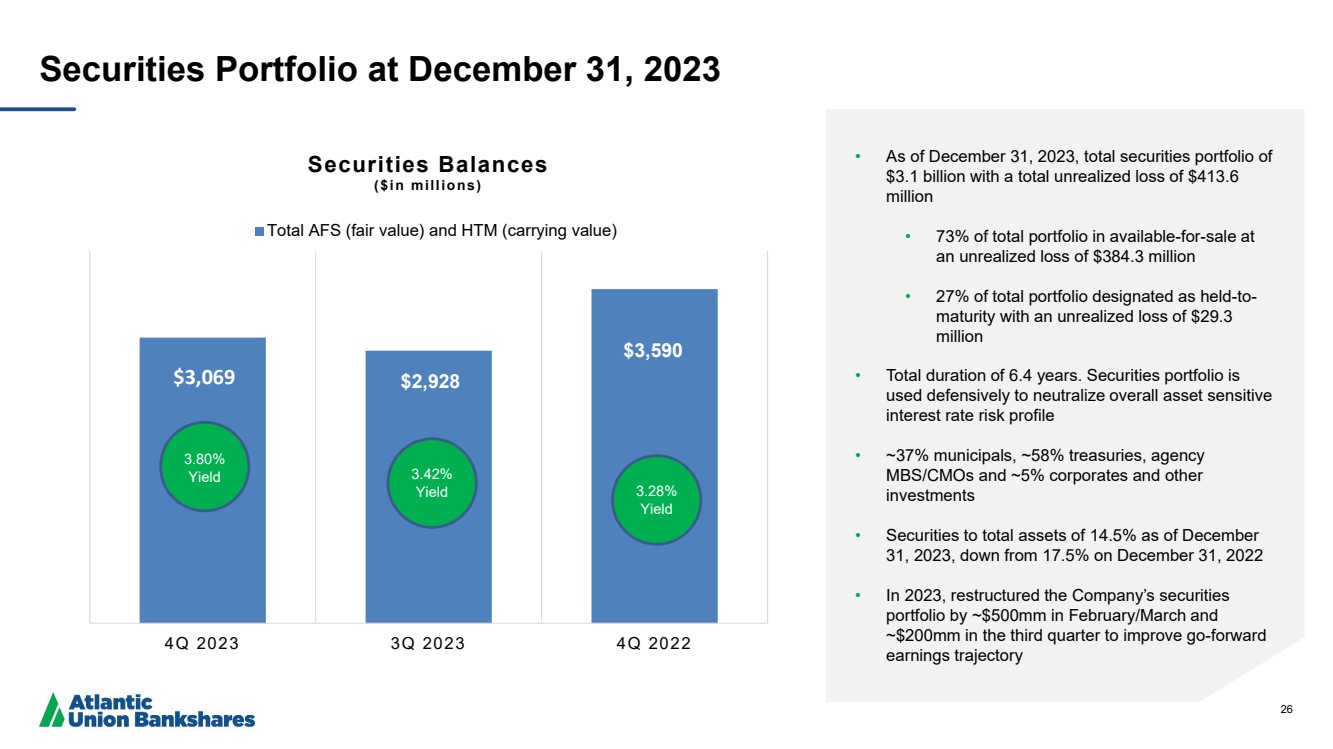

26 Securities Portfolio at December 31, 2023 • As of December 31, 2023, total securities portfolio of $3.1 billion with a total unrealized loss of $413.6 million • 73% of total portfolio in available-for-sale at an unrealized loss of $384.3 million • 27% of total portfolio designated as held-to-maturity with an unrealized loss of $29.3 million • Total duration of 6.4 years. Securities portfolio is used defensively to neutralize overall asset sensitive interest rate risk profile • ~37% municipals, ~58% treasuries, agency MBS/CMOs and ~5% corporates and other investments • Securities to total assets of 14.5% as of December 31, 2023, down from 17.5% on December 31, 2022 • In 2023, restructured the Company’s securities portfolio by ~$500mm in February/March and ~$200mm in the third quarter to improve go-forward earnings trajectory $3,032 $3,069 4Q 2023 3Q 2023 4Q 2022 Securities Balances ($in millions) Total AFS (fair value) and HTM (carrying value) 3.80% Yield 3.28% Yield 3.42% Yield $2,928 $3,590 $3,069 |

|

27 Reconciliation of Non-GAAP Disclosures The Company has provided supplemental performance measures on a tax-equivalent, tangible, operating, adjusted, or pre-tax pre-provision basis. These non-GAAP financial measures are a supplement to GAAP, which is used to prepare the Company’s financial statements, and should not be considered in isolation or as a substitute for comparable measures calculated in accordance with GAAP. In addition, the Company’s non-GAAP financial measures may not be comparable to non-GAAP financial measures of other companies. The Company uses the non-GAAP financial measures discussed herein in its analysis of the Company’s performance. The Company’s management believes that these non-GAAP financial measures provide additional understanding of ongoing operations, enhance comparability of results of operations with prior periods and show the effects of significant gains and charges in the periods presented without the impact of items or events that may obscure trends in the Company’s underlying performance. |

|

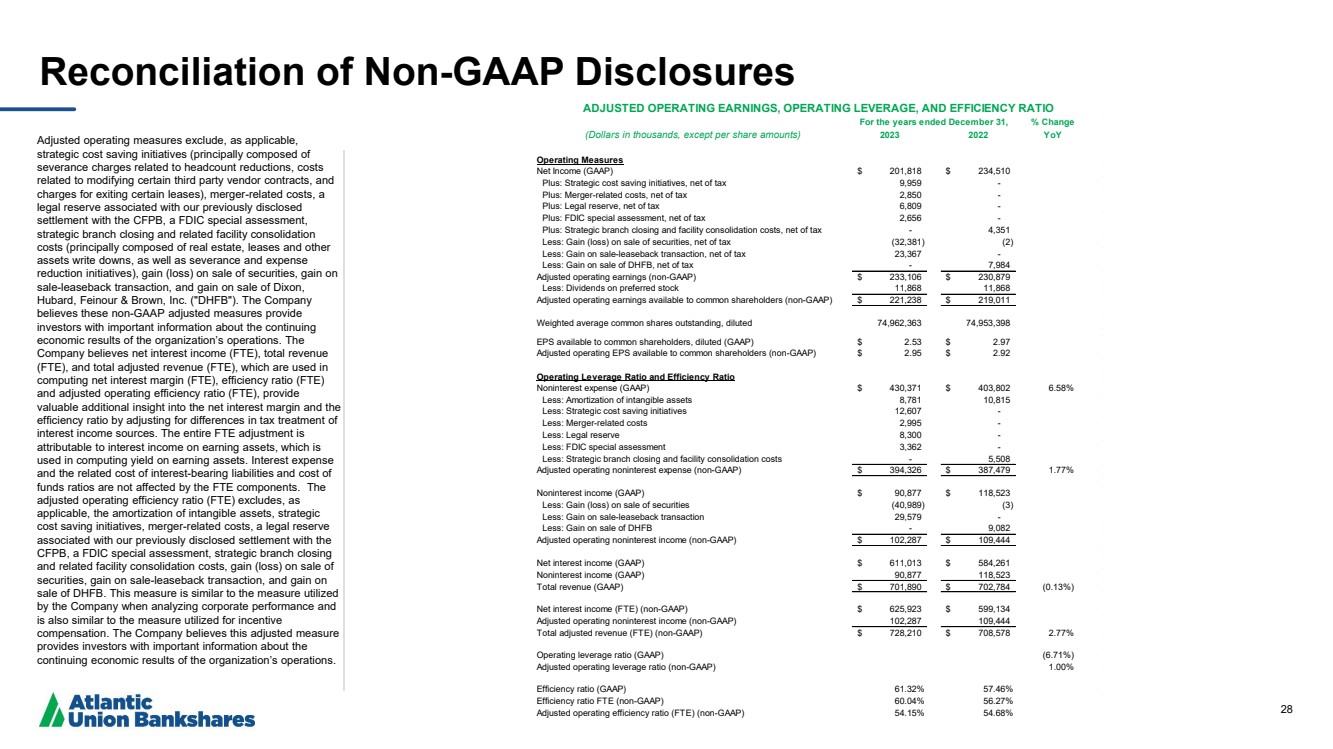

28 Reconciliation of Non -GAAP Disclosures Adjusted operating measures exclude, as applicable, strategic cost saving initiatives (principally composed of severance charges related to headcount reductions, costs related to modifying certain third party vendor contracts, and charges for exiting certain leases), merger -related costs, a legal reserve associated with our previously disclosed settlement with the CFPB, a FDIC special assessment, strategic branch closing and related facility consolidation costs (principally composed of real estate, leases and other assets write downs, as well as severance and expense reduction initiatives), gain (loss) on sale of securities, gain on sale -leaseback transaction, and gain on sale of Dixon, Hubard, Feinour & Brown, Inc. ("DHFB"). The Company believes these non -GAAP adjusted measures provide investors with important information about the continuing economic results of the organization’s operations. The Company believes net interest income (FTE), total revenue (FTE), and total adjusted revenue (FTE), which are used in computing net interest margin (FTE), efficiency ratio (FTE) and adjusted operating efficiency ratio (FTE), provide valuable additional insight into the net interest margin and the efficiency ratio by adjusting for differences in tax treatment of interest income sources. The entire FTE adjustment is attributable to interest income on earning assets, which is used in computing yield on earning assets. Interest expense and the related cost of interest -bearing liabilities and cost of funds ratios are not affected by the FTE components. The adjusted operating efficiency ratio (FTE) excludes, as applicable, the amortization of intangible assets, strategic cost saving initiatives, merger -related costs, a legal reserve associated with our previously disclosed settlement with the CFPB, a FDIC special assessment, strategic branch closing and related facility consolidation costs, gain (loss) on sale of securities, gain on sale -leaseback transaction, and gain on sale of DHFB. This measure is similar to the measure utilized by the Company when analyzing corporate performance and is also similar to the measure utilized for incentive compensation. The Company believes this adjusted measure provides investors with important information about the continuing economic results of the organization’s operations. % Change (Dollars in thousands, except per share amounts) 2023 2022 YoY Operating Measures Net Income (GAAP) $ 201,818 $ 234,510 Plus: Strategic cost saving initiatives, net of tax 9,959 - Plus: Merger-related costs, net of tax 2,850 - Plus: Legal reserve, net of tax 6,809 - Plus: FDIC special assessment, net of tax 2,656 - Plus: Strategic branch closing and facility consolidation costs, net of tax - 4,351 Less: Gain (loss) on sale of securities, net of tax (32,381) (2) Less: Gain on sale-leaseback transaction, net of tax 23,367 - Less: Gain on sale of DHFB, net of tax - 7,984 Adjusted operating earnings (non-GAAP) $ 233,106 $ 230,879 Less: Dividends on preferred stock 11,868 11,868 Adjusted operating earnings available to common shareholders (non-GAAP) $ 221,238 $ 219,011 Weighted average common shares outstanding, diluted 74,962,363 74,953,398 EPS available to common shareholders, diluted (GAAP) $ 2.53 $ 2.97 Adjusted operating EPS available to common shareholders (non-GAAP) $ 2.95 $ 2.92 Operating Leverage Ratio and Efficiency Ratio Noninterest expense (GAAP) $ 430,371 $ 403,802 6.58% Less: Amortization of intangible assets 8,781 10,815 Less: Strategic cost saving initiatives 12,607 - Less: Merger-related costs 2,995 - Less: Legal reserve 8,300 - Less: FDIC special assessment 3,362 - Less: Strategic branch closing and facility consolidation costs - 5,508 Adjusted operating noninterest expense (non-GAAP) $ 394,326 $ 387,479 1.77% Noninterest income (GAAP) $ 90,877 $ 118,523 Less: Gain (loss) on sale of securities (40,989) (3) Less: Gain on sale-leaseback transaction 29,579 - Less: Gain on sale of DHFB - 9,082 Adjusted operating noninterest income (non-GAAP) $ 102,287 $ 109,444 Net interest income (GAAP) $ 611,013 $ 584,261 Noninterest income (GAAP) 90,877 118,523 Total revenue (GAAP) $ 701,890 $ 702,784 (0.13%) Net interest income (FTE) (non-GAAP) $ 625,923 $ 599,134 Adjusted operating noninterest income (non-GAAP) 102,287 109,444 Total adjusted revenue (FTE) (non-GAAP) $ 728,210 $ 708,578 2.77% Operating leverage ratio (GAAP) (6.71%) Adjusted operating leverage ratio (non-GAAP) 1.00% Efficiency ratio (GAAP) 61.32% 57.46% Efficiency ratio FTE (non-GAAP) 60.04% 56.27% Adjusted operating efficiency ratio (FTE) (non-GAAP) 54.15% 54.68% ADJUSTED OPERATING EARNINGS, OPERATING LEVERAGE, AND EFFICIENCY RATIO For the years ended December 31, |

|

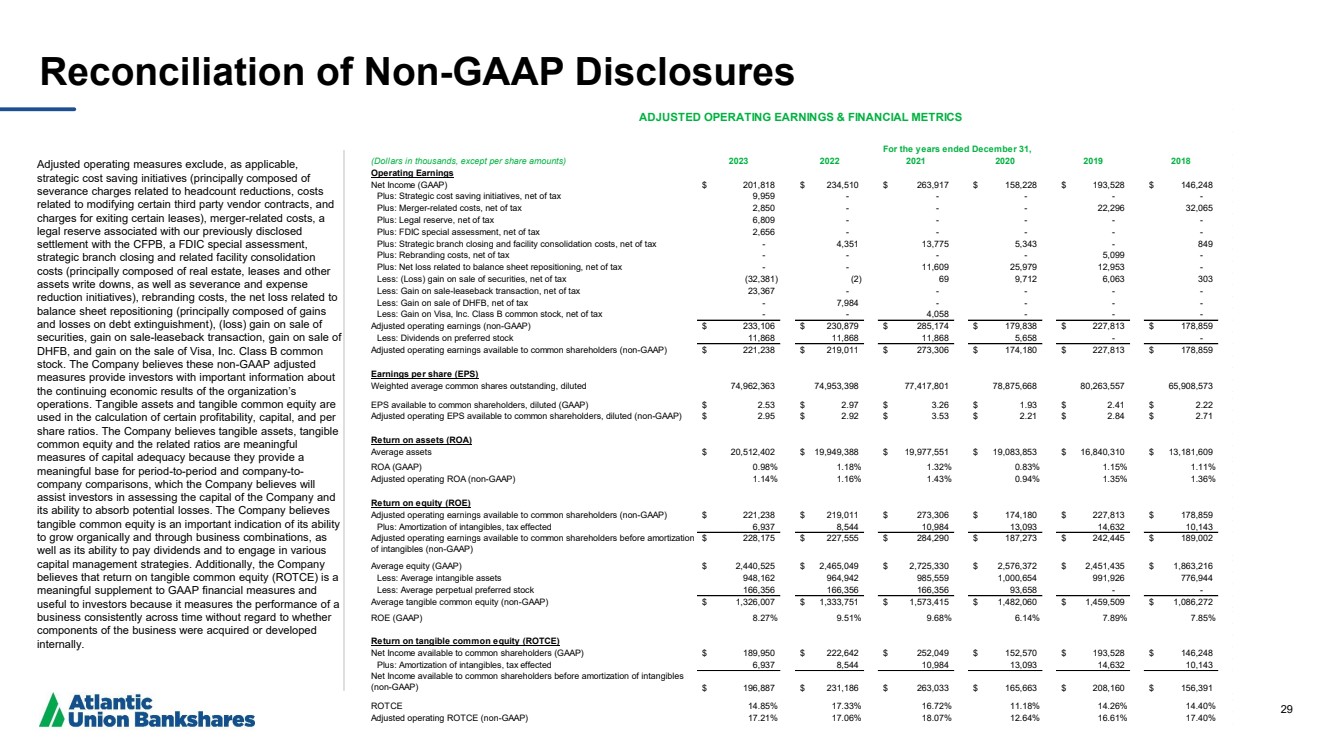

29 Reconciliation of Non -GAAP Disclosures Adjusted operating measures exclude, as applicable, strategic cost saving initiatives (principally composed of severance charges related to headcount reductions, costs related to modifying certain third party vendor contracts, and charges for exiting certain leases), merger -related costs, a legal reserve associated with our previously disclosed settlement with the CFPB, a FDIC special assessment, strategic branch closing and related facility consolidation costs (principally composed of real estate, leases and other assets write downs, as well as severance and expense reduction initiatives), rebranding costs, the net loss related to balance sheet repositioning (principally composed of gains and losses on debt extinguishment), (loss) gain on sale of securities, gain on sale -leaseback transaction, gain on sale of DHFB, and gain on the sale of Visa, Inc. Class B common stock. The Company believes these non -GAAP adjusted measures provide investors with important information about the continuing economic results of the organization’s operations. Tangible assets and tangible common equity are used in the calculation of certain profitability, capital, and per share ratios. The Company believes tangible assets, tangible common equity and the related ratios are meaningful measures of capital adequacy because they provide a meaningful base for period -to -period and company -to - company comparisons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses. The Company believes tangible common equity is an important indication of its ability to grow organically and through business combinations, as well as its ability to pay dividends and to engage in various capital management strategies. Additionally, the Company believes that return on tangible common equity (ROTCE) is a meaningful supplement to GAAP financial measures and useful to investors because it measures the performance of a business consistently across time without regard to whether components of the business were acquired or developed internally. (Dollars in thousands, except per share amounts) 2023 2022 2021 2020 2019 2018 Operating Earnings Net Income (GAAP) $ 201,818 $ 234,510 $ 263,917 $ 158,228 $ 193,528 $ 146,248 Plus: Strategic cost saving initiatives, net of tax 9,959 - - - - - Plus: Merger-related costs, net of tax 2,850 - - - 22,296 32,065 Plus: Legal reserve, net of tax 6,809 - - - - - Plus: FDIC special assessment, net of tax 2,656 - - - - - Plus: Strategic branch closing and facility consolidation costs, net of tax - 4,351 13,775 5,343 - 849 Plus: Rebranding costs, net of tax - - - - 5,099 - Plus: Net loss related to balance sheet repositioning, net of tax - - 11,609 25,979 12,953 - Less: (Loss) gain on sale of securities, net of tax (32,381) (2) 69 9,712 6,063 303 Less: Gain on sale-leaseback transaction, net of tax 23,367 - - - - - Less: Gain on sale of DHFB, net of tax - 7,984 - - - - Less: Gain on Visa, Inc. Class B common stock, net of tax - - 4,058 - - - Adjusted operating earnings (non-GAAP) $ 233,106 $ 230,879 $ 285,174 $ 179,838 $ 227,813 $ 178,859 Less: Dividends on preferred stock 11,868 11,868 11,868 5,658 - - Adjusted operating earnings available to common shareholders (non-GAAP) $ 221,238 $ 219,011 $ 273,306 $ 174,180 $ 227,813 $ 178,859 Earnings per share (EPS) Weighted average common shares outstanding, diluted 74,962,363 74,953,398 77,417,801 78,875,668 80,263,557 65,908,573 EPS available to common shareholders, diluted (GAAP) $ 2.53 $ 2.97 $ 3.26 $ 1.93 $ 2.41 $ 2.22 Adjusted operating EPS available to common shareholders, diluted (non-GAAP) $ 2.95 $ 2.92 $ 3.53 $ 2.21 $ 2.84 $ 2.71 Return on assets (ROA) Average assets $ 20,512,402 $ 19,949,388 $ 19,977,551 $ 19,083,853 $ 16,840,310 $ 13,181,609 ROA (GAAP) 0.98% 1.18% 1.32% 0.83% 1.15% 1.11% Adjusted operating ROA (non-GAAP) 1.14% 1.16% 1.43% 0.94% 1.35% 1.36% Return on equity (ROE) Adjusted operating earnings available to common shareholders (non-GAAP) $ 221,238 $ 219,011 $ 273,306 $ 174,180 $ 227,813 $ 178,859 Plus: Amortization of intangibles, tax effected 6,937 8,544 10,984 13,093 14,632 10,143 Adjusted operating earnings available to common shareholders before amortization of intangibles (non-GAAP) $ 228,175 $ 227,555 $ 284,290 $ 187,273 $ 242,445 $ 189,002 Average equity (GAAP) $ 2,440,525 $ 2,465,049 $ 2,725,330 $ 2,576,372 $ 2,451,435 $ 1,863,216 Less: Average intangible assets 948,162 964,942 985,559 1,000,654 991,926 776,944 Less: Average perpetual preferred stock 166,356 166,356 166,356 93,658 - - Average tangible common equity (non-GAAP) $ 1,326,007 $ 1,333,751 $ 1,573,415 $ 1,482,060 $ 1,459,509 $ 1,086,272 ROE (GAAP) 8.27% 9.51% 9.68% 6.14% 7.89% 7.85% Return on tangible common equity (ROTCE) Net Income available to common shareholders (GAAP) $ 189,950 $ 222,642 $ 252,049 $ 152,570 $ 193,528 $ 146,248 Plus: Amortization of intangibles, tax effected 6,937 8,544 10,984 13,093 14,632 10,143 Net Income available to common shareholders before amortization of intangibles (non-GAAP) $ 196,887 $ 231,186 $ 263,033 $ 165,663 $ 208,160 $ 156,391 ROTCE 14.85% 17.33% 16.72% 11.18% 14.26% 14.40% Adjusted operating ROTCE (non-GAAP) 17.21% 17.06% 18.07% 12.64% 16.61% 17.40% ADJUSTED OPERATING EARNINGS & FINANCIAL METRICS For the years ended December 31, |

|

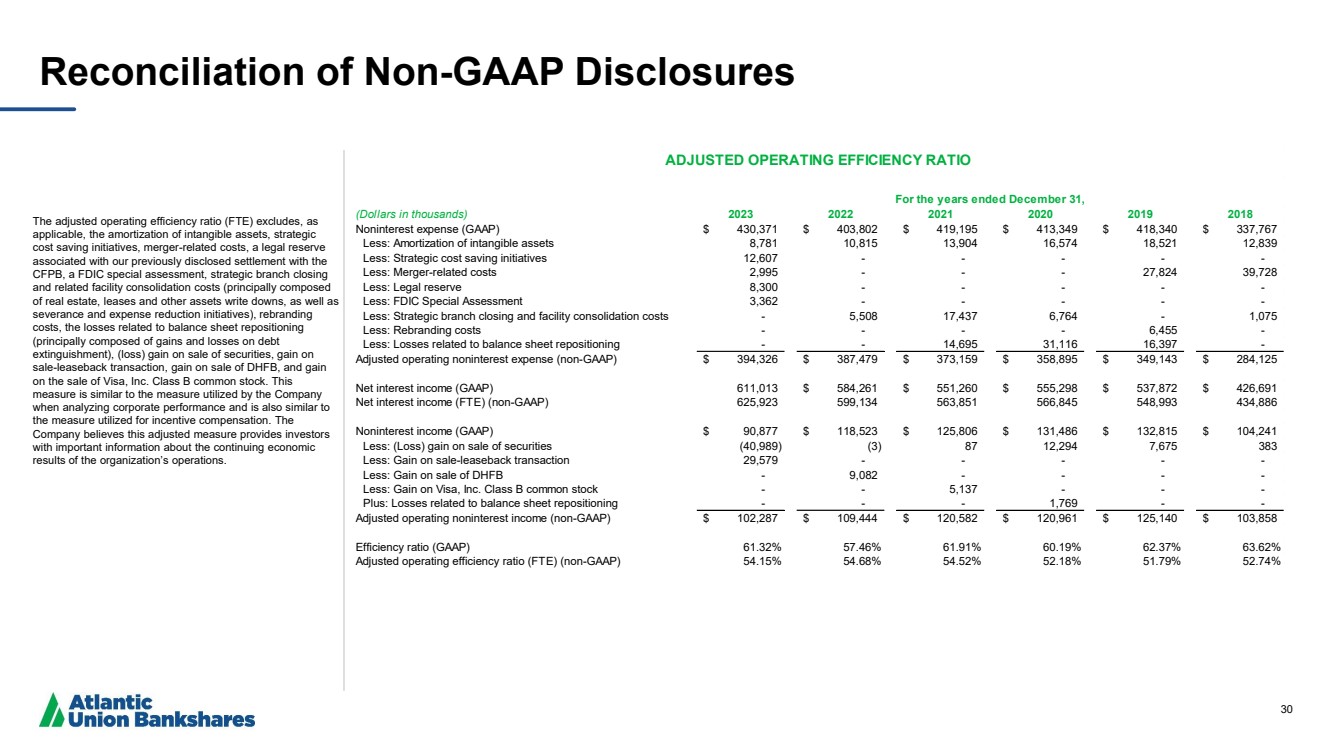

30 Reconciliation of Non-GAAP Disclosures The adjusted operating efficiency ratio (FTE) excludes, as applicable, the amortization of intangible assets, strategic cost saving initiatives, merger-related costs, a legal reserve associated with our previously disclosed settlement with the CFPB, a FDIC special assessment, strategic branch closing and related facility consolidation costs (principally composed of real estate, leases and other assets write downs, as well as severance and expense reduction initiatives), rebranding costs, the losses related to balance sheet repositioning (principally composed of gains and losses on debt extinguishment), (loss) gain on sale of securities, gain on sale-leaseback transaction, gain on sale of DHFB, and gain on the sale of Visa, Inc. Class B common stock. This measure is similar to the measure utilized by the Company when analyzing corporate performance and is also similar to the measure utilized for incentive compensation. The Company believes this adjusted measure provides investors with important information about the continuing economic results of the organization’s operations. (Dollars in thousands) 2023 2022 2021 2020 2019 2018 Noninterest expense (GAAP) $ 430,371 $ 403,802 $ 419,195 $ 413,349 $ 418,340 $ 337,767 Less: Amortization of intangible assets 8,781 10,815 13,904 16,574 18,521 12,839 Less: Strategic cost saving initiatives 12,607 - - - - - Less: Merger-related costs 2,995 - - - 27,824 39,728 Less: Legal reserve 8,300 - - - - - Less: FDIC Special Assessment 3,362 - - - - - Less: Strategic branch closing and facility consolidation costs - 5,508 17,437 6,764 - 1,075 Less: Rebranding costs - - - - 6,455 - Less: Losses related to balance sheet repositioning - - 14,695 31,116 16,397 - Adjusted operating noninterest expense (non-GAAP) $ 394,326 $ 387,479 $ 373,159 $ 358,895 $ 349,143 $ 284,125 Net interest income (GAAP) 611,013 $ 584,261 $ 551,260 $ 555,298 $ 537,872 $ 426,691 Net interest income (FTE) (non-GAAP) 625,923 599,134 563,851 566,845 548,993 434,886 Noninterest income (GAAP) $ 90,877 $ 118,523 $ 125,806 $ 131,486 $ 132,815 $ 104,241 Less: (Loss) gain on sale of securities (40,989) (3) 87 12,294 7,675 383 Less: Gain on sale-leaseback transaction 29,579 - - - - - Less: Gain on sale of DHFB - 9,082 - - - - Less: Gain on Visa, Inc. Class B common stock - - 5,137 - - - Plus: Losses related to balance sheet repositioning - - - 1,769 - - Adjusted operating noninterest income (non-GAAP) $ 102,287 $ 109,444 $ 120,582 $ 120,961 $ 125,140 $ 103,858 Efficiency ratio (GAAP) 61.32% 57.46% 61.91% 60.19% 62.37% 63.62% Adjusted operating efficiency ratio (FTE) (non-GAAP) 54.15% 54.68% 54.52% 52.18% 51.79% 52.74% ADJUSTED OPERATING EFFICIENCY RATIO For the years ended December 31, |

|

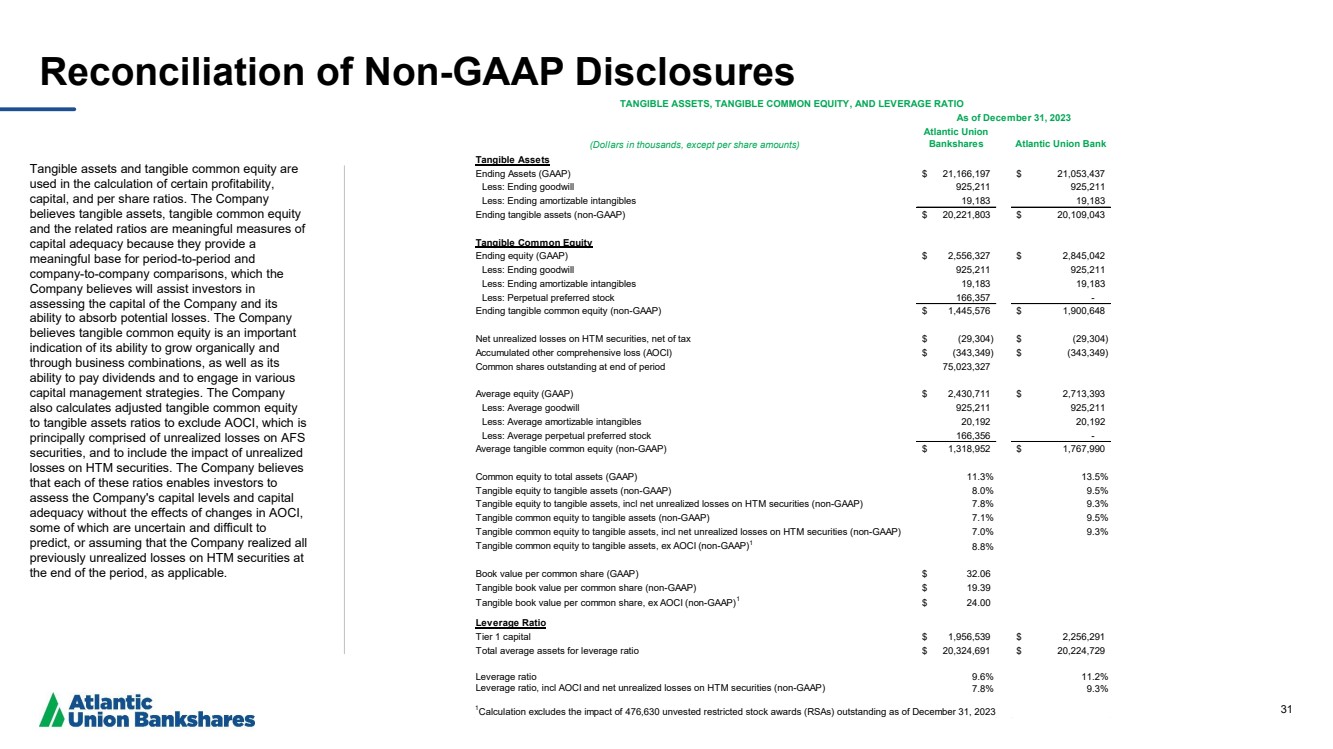

31 Reconciliation of Non-GAAP Disclosures Tangible assets and tangible common equity are used in the calculation of certain profitability, capital, and per share ratios. The Company believes tangible assets, tangible common equity and the related ratios are meaningful measures of capital adequacy because they provide a meaningful base for period-to-period and company-to-company comparisons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses. The Company believes tangible common equity is an important indication of its ability to grow organically and through business combinations, as well as its ability to pay dividends and to engage in various capital management strategies. The Company also calculates adjusted tangible common equity to tangible assets ratios to exclude AOCI, which is principally comprised of unrealized losses on AFS securities, and to include the impact of unrealized losses on HTM securities. The Company believes that each of these ratios enables investors to assess the Company's capital levels and capital adequacy without the effects of changes in AOCI, some of which are uncertain and difficult to predict, or assuming that the Company realized all previously unrealized losses on HTM securities at the end of the period, as applicable. (Dollars in thousands, except per share amounts) Atlantic Union Bankshares Atlantic Union Bank Tangible Assets Ending Assets (GAAP) $ 21,166,197 $ 21,053,437 Less: Ending goodwill 925,211 925,211 Less: Ending amortizable intangibles 19,183 19,183 Ending tangible assets (non-GAAP) $ 20,221,803 $ 20,109,043 Tangible Common Equity Ending equity (GAAP) $ 2,556,327 $ 2,845,042 Less: Ending goodwill 925,211 925,211 Less: Ending amortizable intangibles 19,183 19,183 Less: Perpetual preferred stock 166,357 - Ending tangible common equity (non-GAAP) $ 1,445,576 $ 1,900,648 Net unrealized losses on HTM securities, net of tax $ (29,304) $ (29,304) Accumulated other comprehensive loss (AOCI) $ (343,349) $ (343,349) Common shares outstanding at end of period 75,023,327 Average equity (GAAP) $ 2,430,711 $ 2,713,393 Less: Average goodwill 925,211 925,211 Less: Average amortizable intangibles 20,192 20,192 Less: Average perpetual preferred stock 166,356 - Average tangible common equity (non-GAAP) $ 1,318,952 $ 1,767,990 Less: Perpetual preferred stock Common equity to total assets (GAAP) 11.3% 13.5% Tangible equity to tangible assets (non-GAAP) 8.0% 9.5% Tangible equity to tangible assets, incl net unrealized losses on HTM securities (non-GAAP) 7.8% 9.3% Tangible common equity to tangible assets (non-GAAP) 7.1% 9.5% Tangible common equity to tangible assets, incl net unrealized losses on HTM securities (non-GAAP) 7.0% 9.3% Tangible common equity to tangible assets, ex AOCI (non-GAAP)1 8.8% Book value per common share (GAAP) $ 32.06 Tangible book value per common share (non-GAAP) $ 19.39 Tangible book value per common share, ex AOCI (non-GAAP)1 $ 24.00 Leverage Ratio Tier 1 capital $ 1,956,539 $ 2,256,291 Total average assets for leverage ratio $ 20,324,691 $ 20,224,729 Leverage ratio 9.6% 11.2% Leverage ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 7.8% 9.3% TANGIBLE ASSETS, TANGIBLE COMMON EQUITY, AND LEVERAGE RATIO As of December 31, 2023 1Calculation excludes the impact of 476,630 unvested restricted stock awards (RSAs) outstanding as of December 31, 2023 |

|

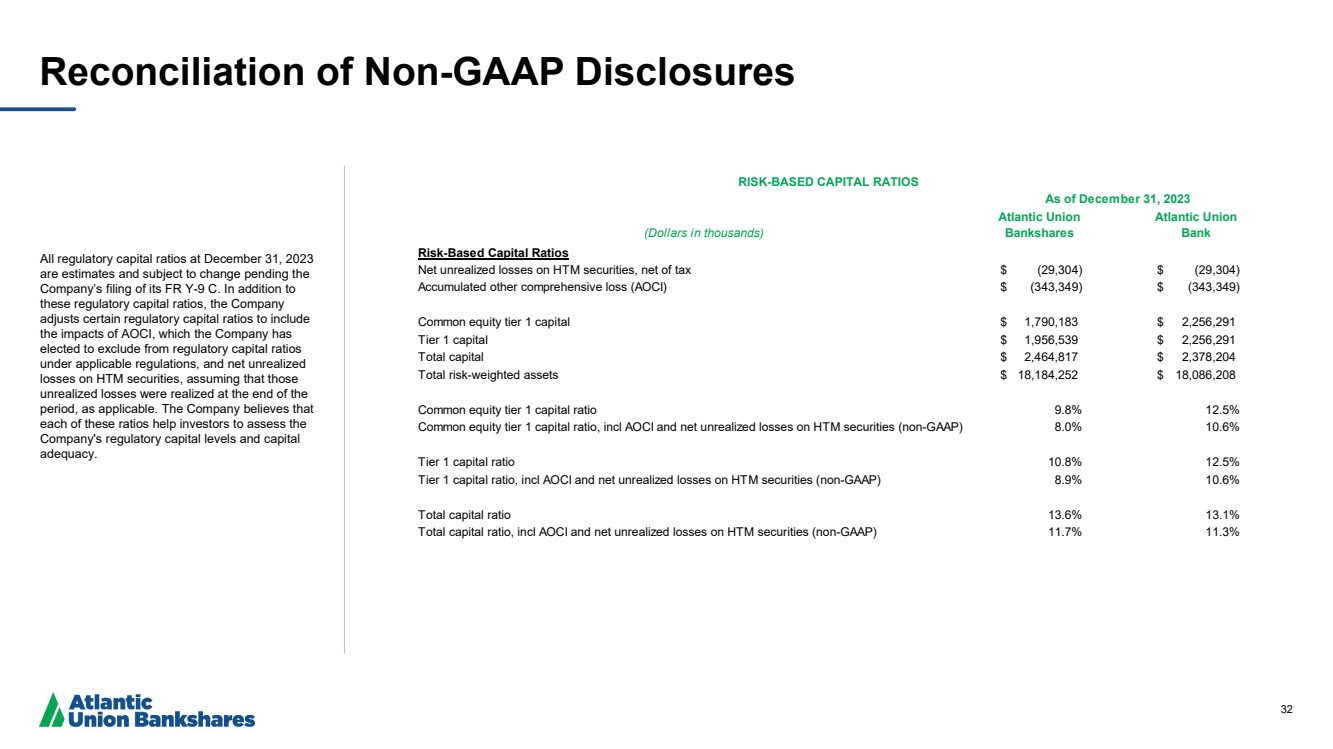

32 Reconciliation of Non-GAAP Disclosures All regulatory capital ratios at December 31, 2023 are estimates and subject to change pending the Company’s filing of its FR Y-9 C. In addition to these regulatory capital ratios, the Company adjusts certain regulatory capital ratios to include the impacts of AOCI, which the Company has elected to exclude from regulatory capital ratios under applicable regulations, and net unrealized losses on HTM securities, assuming that those unrealized losses were realized at the end of the period, as applicable. The Company believes that each of these ratios help investors to assess the Company's regulatory capital levels and capital adequacy. (Dollars in thousands) Atlantic Union Bankshares Atlantic Union Bank Risk-Based Capital Ratios Net unrealized losses on HTM securities, net of tax $ (29,304) $ (29,304) Accumulated other comprehensive loss (AOCI) $ (343,349) $ (343,349) Common equity tier 1 capital $ 1,790,183 $ 2,256,291 Tier 1 capital $ 1,956,539 $ 2,256,291 Total capital $ 2,464,817 $ 2,378,204 Total risk-weighted assets $ 18,184,252 $ 18,086,208 Common equity tier 1 capital ratio 9.8% 12.5% Common equity tier 1 capital ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 8.0% 10.6% Tier 1 capital ratio 10.8% 12.5% Tier 1 capital ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 8.9% 10.6% Total capital ratio 13.6% 13.1% Total capital ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 11.7% 11.3% RISK-BASED CAPITAL RATIOS As of December 31, 2023 |