UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): July 29, 2025

Camping World Holdings, Inc.

(Exact Name of Registrant as Specified in its Charter)

Delaware |

|

001-37908 |

|

81-1737145 |

(State or Other Jurisdiction of Incorporation) |

|

(Commission File Number) |

|

(IRS Employer Identification No.) |

|

2 Marriott Dr. (Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code (847) 808-3000 |

Not applicable

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425).

☐Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12).

☐Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)).

☐Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)).

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Class A Common Stock, |

CWH |

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02. Results of Operations and Financial Condition.

On July 29, 2025, Camping World Holdings, Inc. (the “Company”) announced its financial results for the three and six months ended June 30, 2025. The full text of the press release issued in connection with the announcement is furnished as Exhibit 99.1 to this Current Report on Form 8-K.

The information in this Item 2.02 of this Current Report on Form 8-K (including Exhibit 99.1) shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference in such a filing.

Item 7.01. Regulation FD Disclosure.

Beginning July 29, 2025, the Company plans to meet with investors and analysts where it expects to discuss sales trends in the Company’s business and industry, as well as a general business update. The presentation materials that will be used in these meetings are furnished hereto as Exhibit 99.2 and are incorporated herein by reference.

The information in Item 7.01 of this Current Report on Form 8-K, including Exhibit 99.2 hereto, shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to the liabilities of that Section, nor shall it be deemed to be incorporated by reference into any filing of the Company under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference in such filing.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits

Exhibit 99.1 relating to Item 2.02 and Exhibit 99.2 relating to Item 7.01 shall be deemed to be furnished, and not filed:

Exhibit No. Description

Exhibit 99.1 |

Exhibit 99.2 |

Exhibit 104 |

Cover Page Interactive Data File - the cover page XBRL tags are embedded within the Inline XBRL document |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

CAMPING WORLD HOLDINGS, INC. |

|

|

|

|

|

|

|

|

By: |

/s/ Thomas E. Kirn |

|

Name: |

Thomas E. Kirn |

|

Title: |

Chief Financial Officer |

Date: July 29, 2025

Exhibit 99.1

Camping World Holdings, Inc. Reports Second Quarter 2025 Results, Grows Net Income and Adjusted EBITDA by More Than 30% Driven by Strong Cost Execution and All-Time Quarterly Volume Record of Over 45,000 Units, Momentum Continues Through July

LINCOLNSHIRE, IL – July 29, 2025 (BUSINESS WIRE) -- Camping World Holdings, Inc. (NYSE: CWH) (the “Company” or “CWH”), the World’s Largest Recreational Vehicle Dealer, today reported results for the second quarter ended June 30, 2025.

Marcus Lemonis, Chairman and Chief Executive Officer of CWH stated, “I am unbelievably pleased with our Company’s financial performance in the quarter, driven by volume, margin performance and aggressive cost controls. We continue to surgically manage our inventory to find volume and gross profit opportunities leveraging our new and used supply chains, our contract manufacturing relationships, our sophisticated data analytics, and the strength of our balance sheet to put the right inventory on the ground at the right time and the right price. Our nimbleness is a true testament to the differentiation and durability of our model.”

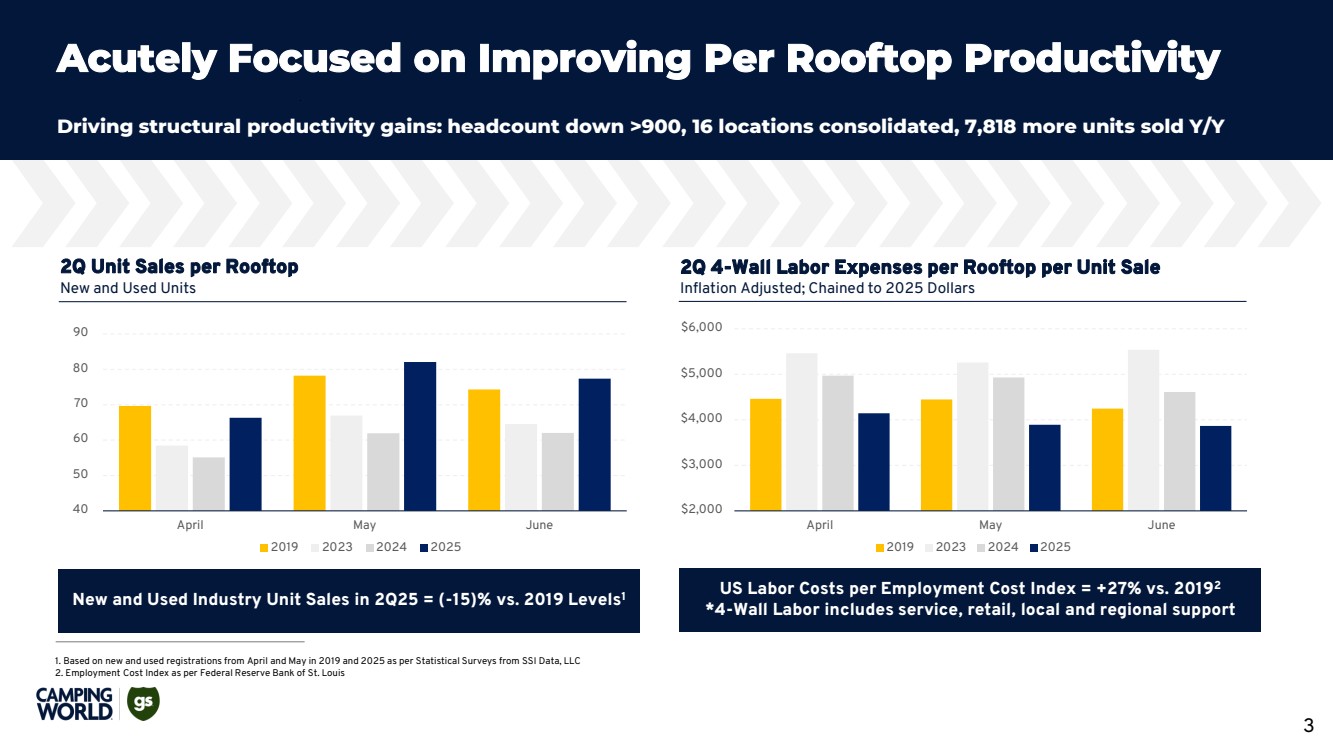

Mr. Lemonis continued, “We have made structural changes to our fixed costs compared to last year, reducing our headcount by over 900, consolidating 16 locations, and selling 7,818 more units; meaningfully improving our per-rooftop productivity and proving we can adapt to the near-term ASP contribution margin environment in new vehicles.”

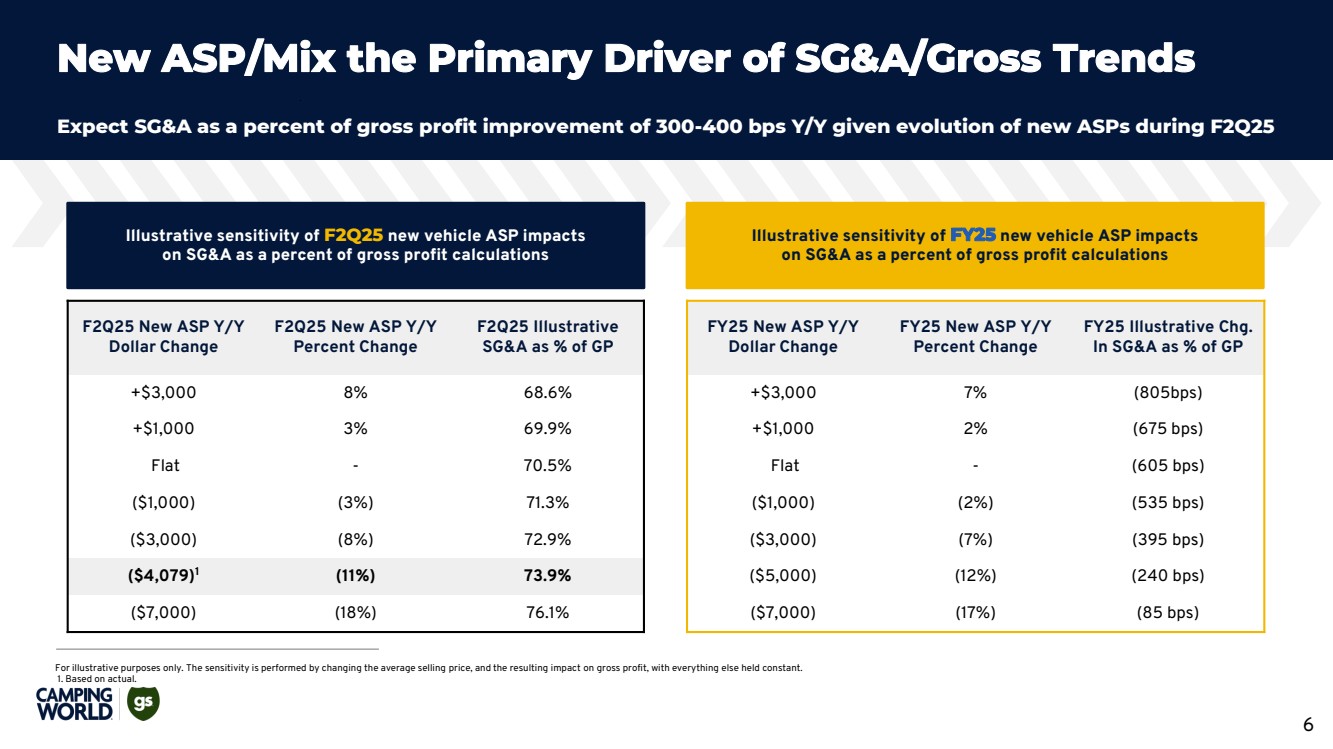

Matthew Wagner, President of CWH commented, “Our same store unit growth trends July month-to-date are tracking up high-teens percent on used vehicles and up high-singles on new vehicles compared to the prior year, both in line on a multi-year basis with our second quarter performance. Our guideposts for the full year remain largely unchanged, although our new unit volume is now expected to be higher, growing in excess of high-singles compared to the prior year. New vehicle ASP is expected to improve seasonally in the third and fourth quarter but could be lower by 10-12% for the full year compared to the prior year. Despite this drop in ASP we are expecting to accomplish 300-400 basis points of improvement in SG&A as a percentage of gross profit(1), recognizing that this efficiency will improve further as ASPs rebound.”

Tom Kirn, Chief Financial Officer of CWH commented, “We expect cash flow to benefit from the passage of the One Big Beautiful Bill Act through the immediate deductibility of floorplan interest expense on travel trailers and fifth wheels. We estimate annual cash tax savings of $15 to $20 million in 2025 and expect to prioritize debt paydown and deleveraging activities with those savings. Including payments in July 2025, we’ve paid down debt by over $75 million in total since October of last year.”

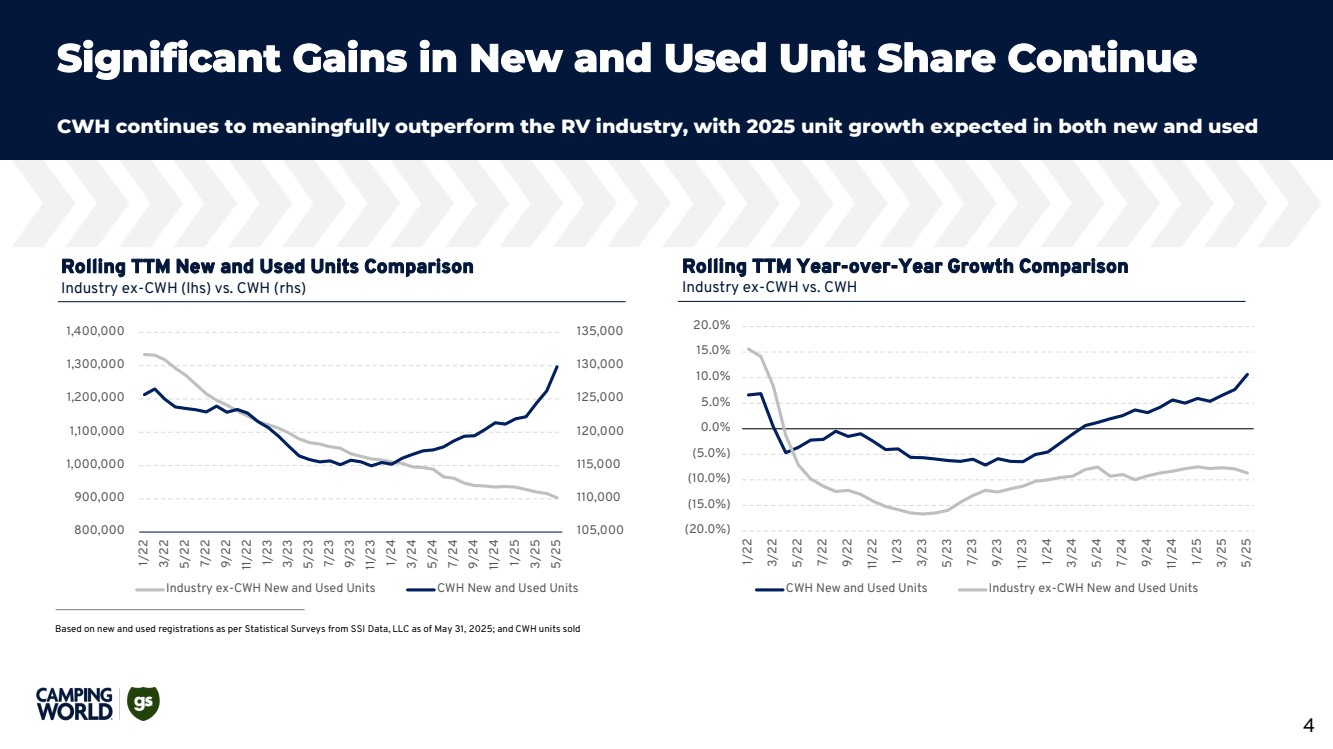

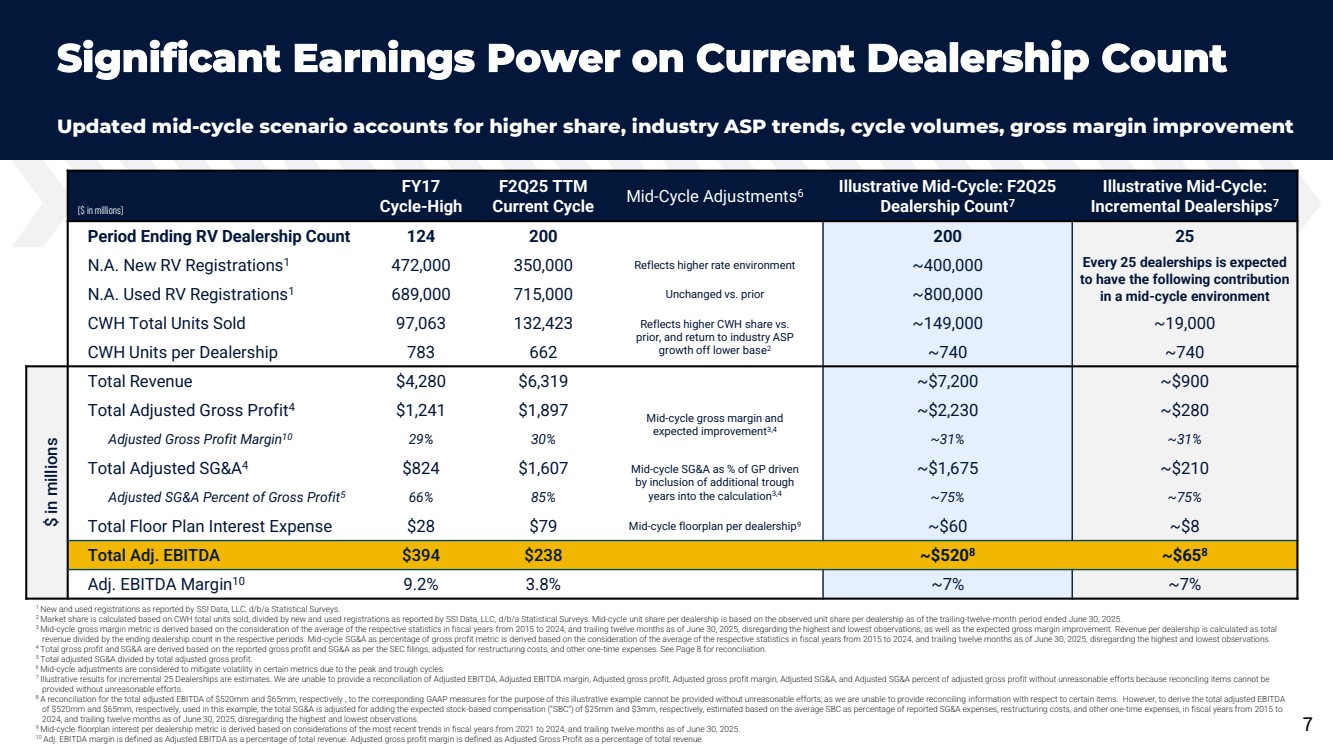

Mr. Lemonis concluded, “We enter the second half more confident than ever in our mid-cycle earnings power scenario of over $500 million of adjusted EBITDA based on today’s store count(2), particularly as the Company’s per rooftop productivity accelerates, resulting in better earnings, better leverage, and a greater willingness to explore new market expansion opportunities. Given results year-to-date, we believe that more upside exists in the 15% new and used combined market share goal we set last year, with 20% plus emerging as a realistic medium-term goal. The team also set an internal mandate to accelerate gross margin by 100 basis points, further bolstering our confidence in the earnings power of our business model.”

Please refer to the Company’s investor presentation slide deck, dated July 2025, on the Investor Relations website at http://investor.campingworld.com for more detailed information on second quarter 2025 results.

Second Quarter-over-Quarter Operating Highlights

| ● | Revenue was $2.0 billion for the second quarter, an increase of $169.4 million, or 9.4%. |

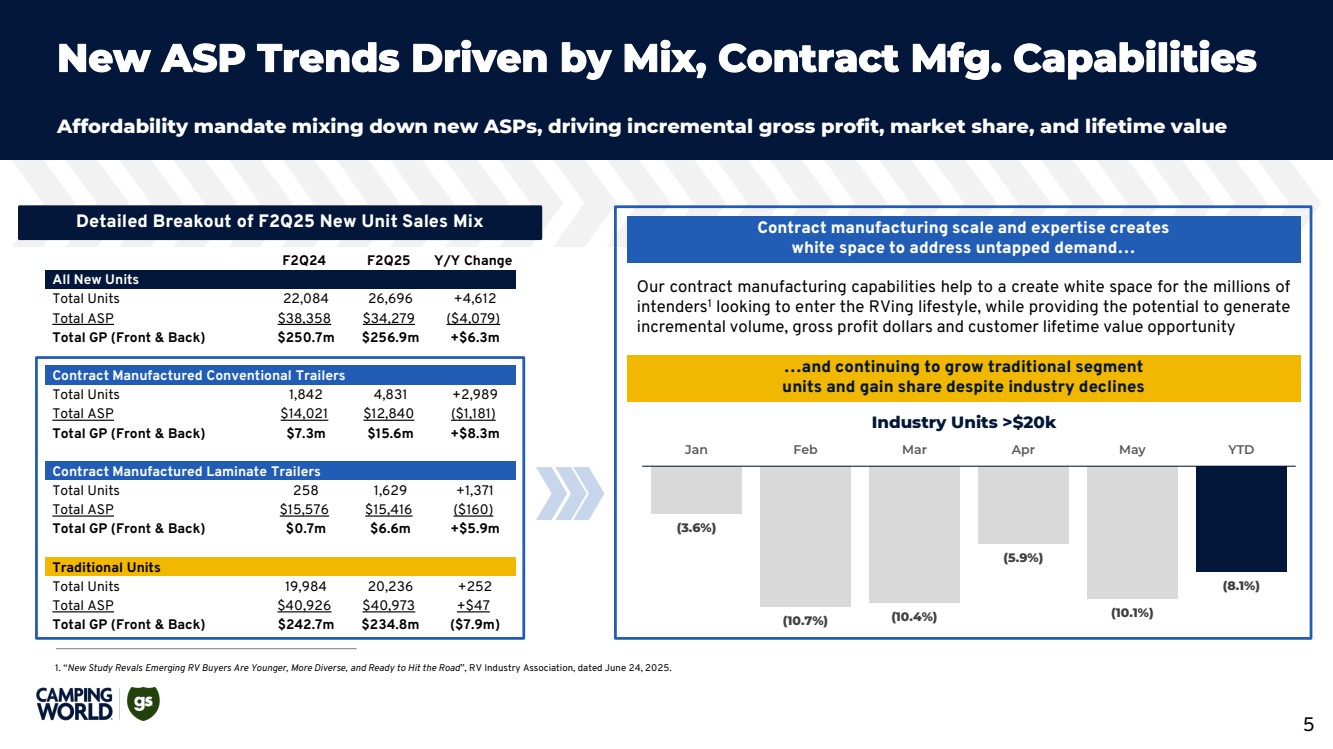

| ● | New vehicle revenue was $915.1 million for the second quarter, an increase of $68.0 million, or 8.0%, and new vehicle unit sales were 26,696 units, an increase of 4,612 units, or 20.9%. Used vehicle revenue was $572.3 million for the second quarter, an increase of $91.5 million, or 19.0%, and used vehicle unit |

1

| sales were 18,906 units, an increase of 3,206 units, or 20.4%. Combined new and used vehicle unit sales were 45,602, an increase of 7,818 units, or 20.7%. |

| ● | Average selling price of new vehicles sold decreased 10.6% and average selling price of used vehicles sold decreased 1.2%. |

| ● | Same store new vehicle unit sales increased 22.2% for the second quarter and same store used vehicle unit sales increased 20.8%. Combined same store new and used vehicle unit sales increased 21.6%. |

| ● | New vehicle gross margin was 13.8%, a decrease of 149 basis points, driven primarily by the 10.6% decrease in the average selling price per new vehicle sold, partially offset by a 9.1% reduction in the average cost per new vehicle sold. Used vehicle gross margin was 20.5%, an increase of 149 basis points, primarily due to a 3.0% decrease in the average cost per unit sold, partially offset by the 1.2% lower average selling price. |

| ● | Products, service and other revenue was $222.9 million, a decrease of $13.1 million, or 5.5%, driven primarily by a reallocation of service labor toward used inventory reconditioning and the divestiture of our RV furniture business in May 2024. Products, service and other gross margin was 47.8%, an increase of 411 basis points, driven by the divestiture of the RV furniture business, which had negative gross margins for the three months ended June 30, 2024, and increased sales volume of our higher-margin aftermarket part assortment. |

| ● | Gross profit was $592.3 million, an increase of $44.6 million, or 8.1%, and total gross margin was 30.0%, a decrease of 34 basis points. The gross profit increase was mainly driven by the $25.9 million higher used vehicle gross profit from the increase in used vehicle unit sales and gross margin as discussed above and $22.2 million increased finance and insurance, net (“F&I”) gross profit largely from the 20.7% increase in combined new and used vehicle unit sales and new F&I offerings. The gross margin decrease was primarily from higher roadside assistance claim costs that drove the 777 basis point decrease in Good Sam Services and Plans gross margin to 59.5%, which was mostly offset by improvements for used vehicles and products, service and other discussed above. |

| ● | Selling, general and administrative expenses (“SG&A”) were $437.5 million, an increase of $17.8 million, or 4.2%. This increase was primarily driven by a $7.5 million increase in employee cash compensation costs, a $3.0 million increase in employee stock-based compensation (“SBC”) expense, $2.9 million of additional advertising expenses, and an additional $3.3 million for other outside service providers. SG&A Excluding SBC(3) was $429.1 million, an increase of $14.8 million, or 3.6%. |

| ● | Floor plan interest expense was $21.0 million, a decrease of $6.8 million, or 24.5%, as a result of lower interest rates and lower principal balances. Other interest expense, net was $30.8 million, a decrease of $5.3 million, or 14.7%, as a result of lower interest rates and, to a lesser extent, lower principal balances. |

| ● | Net income was $57.5 million for the second quarter of 2025, an improvement of $34.1 million, or 145.7%. Adjusted EBITDA(3) was $142.2 million, an increase of $36.6 million, or 34.7%. |

| ● | Diluted earnings per share of Class A common stock was $0.48, an improvement of $0.26, or 118.2%. Adjusted earnings per share – diluted(3) of Class A common stock was $0.57, an improvement of $0.19, or 50.0%. |

| ● | The total number of our store locations was 201 as of June 30, 2025, a net decrease of 14 store locations from June 30, 2024, or 6.5%, which included the consolidation of 16 store locations to improve the overall cost efficiency of the remaining store locations. |

| (1) | Refers to a comparison to the baseline of SG&A as a percentage of gross profit of 86.2% as calculated from the $1.6 billion of SG&A and $1.8 billion total of gross profit for the year ended December 31, 2024. |

| (2) | See the investor presentation, dated July 29, 2025, as an exhibit to Form 8-K filed with the Securities and Exchange Commission (“SEC”) on July 29, 2025 and available on the Company’s Investor Relations website at http://investor.campingworld.com. |

| (3) | Adjusted earnings per share – diluted, Adjusted EBITDA, and SG&A Excluding SBC are non-GAAP measures. For a reconciliation of these non-GAAP measures to the most directly comparable GAAP measures, see the “Non-GAAP Financial Measures” section later in this press release. |

2

Revisions to Prior Period Condensed Consolidated Financial Statements

Subsequent to the issuance of the Company's condensed consolidated financial statements for the three and six months ended June 30, 2024, the Company's management identified prior period misstatements related to the measurement of the realizable portion of the Company’s outside basis difference deferred tax asset in CWGS Enterprises, LLC (“CWGS, LLC”), including the associated valuation allowance. As a result, deferred tax assets, net, additional paid-in capital, and income tax benefit (expense) as of and for the years ended December 31, 2023 and 2022 were revised in the Company’s Annual Report on Form 10-K for the year ended December 31, 2024 filed with the SEC on February 28, 2025. The misstatements impacted the beginning balances of deferred taxes, net, additional paid-in capital, and retained earnings, which have been revised from the amounts previously reported as of June 30, 2024. The Company evaluated the materiality of these errors, both qualitatively and quantitatively, and determined the effect of these revisions was not material to the previously issued financial statements.

The following table presents the effect of the immaterial misstatements on the Company’s consolidated balance sheet for the period indicated:

|

|

As of June 30, 2024 |

|||||||

($ in thousands) |

|

As Previously Reported |

|

Adjustment |

|

As Revised |

|||

Deferred tax assets, net |

|

$ |

150,105 |

|

$ |

43,768 |

|

$ |

193,873 |

Total assets |

|

|

4,962,108 |

|

|

43,768 |

|

|

5,005,876 |

Additional paid-in capital |

|

|

100,076 |

|

|

33,385 |

|

|

133,461 |

Retained earnings |

|

|

161,434 |

|

|

10,383 |

|

|

171,817 |

Total stockholders' equity attributable to Camping World Holdings, Inc. |

|

|

105,894 |

|

|

43,768 |

|

|

149,662 |

Total stockholders' equity |

|

|

166,637 |

|

|

43,768 |

|

|

210,405 |

Total liabilities and stockholders' equity |

|

|

4,962,108 |

|

|

43,768 |

|

|

5,005,876 |

Earnings Conference Call and Webcast Information

A conference call to discuss the Company’s second quarter 2025 financial results is scheduled for July 30, 2025, at 7:30 am Central Time. Investors and analysts can participate on the conference call by dialing 1-844-826-3035 (international callers please dial 1-412-317-5195) and using conference ID# 10201490. Interested parties can also listen to a live webcast or replay of the conference call by logging on to the Investor Relations section on the Company’s website at http://investor.campingworld.com. Presentation materials are available at http://investor.campingworld.com. The replay of the conference call webcast and presentation materials will be available on the investor relations website for approximately 90 days.

Presentation

This press release presents historical results for the periods presented for the Company and its subsidiaries, which are presented in accordance with accounting principles generally accepted in the United States (“GAAP”), unless noted as a non-GAAP financial measure. The Company is the sole managing member of CWGS, LLC, with sole voting power in and control of the management of CWGS, LLC. As of June 30, 2025, the Company owned 61.1% of CWGS, LLC. Accordingly, the Company consolidates the financial results of CWGS, LLC and reports a non-controlling interest in its consolidated financial statements. Unless otherwise indicated, all financial comparisons in this press release compare our financial results for the second quarter ended June 30, 2025 to our financial results from the second quarter ended June 30, 2024.

About Camping World Holdings, Inc.

Camping World Holdings, Inc., headquartered in Lincolnshire, IL, (together with its subsidiaries) is the world’s largest retailer of RVs and related products and services. Through Camping World and Good Sam brands, our vision is to build a business that makes RVing and other outdoor adventures fun and easy. We strive to build long-term value for our customers, employees, and stockholders by combining a unique and comprehensive assortment of RV products and services with a national network of RV dealerships, service centers and customer support centers along with the industry’s most extensive online presence and a highly trained and knowledgeable team of associates serving our customers, the RV lifestyle, and the communities in which we operate.

3

We also believe that our Good Sam organization and family of highly specialized services and plans, including roadside assistance, protection plans and insurance, uniquely enables us to connect with our customers as stewards of an outdoor and recreational lifestyle. With RV sales and service locations in 44 states, Camping World has grown to become the prime destination for everything RV. For more information, visit www.CampingWorld.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including, without limitation, statements about macroeconomic and industry trends, inventory strategy, reductions in SG&A, accelerating profitability improvement, gross margin improvement, variability in average selling prices, competitive positioning, business plans and goals, future growth of our operations, anticipated effects of new federal legislation, anticipated debt paydown and deleveraging activities, market share goals, and future financial results and position. These forward-looking statements are based on management’s current expectations.

These statements are neither promises nor guarantees, but involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to, the following: general economic conditions, including inflation, interest rates and tariffs; the availability of financing to us and our customers; fuel shortages, high prices for fuel or changes in energy sources; the success of our manufacturers; changes in consumer preferences; competition in our industry; risks related to acquisitions, new store openings and expansion into new markets; our failure to maintain the strength and value of our brands; our ability to manage our inventory; fluctuations in our same store sales; the cyclical and seasonal nature of our business; our dependence on the availability of adequate capital and risks related to our debt; our ability to execute and achieve the expected benefits of our cost cutting initiatives; our reliance on our fulfillment and distribution centers; impacts from natural disasters, including pandemics and health crises; our dependence on our relationships with third party suppliers and lending institutions; risks associated with selling goods manufactured abroad; our ability to retain senior executives and attract and retain other qualified employees; risks associated with leasing substantial amounts of space; risks associated with our private brand offerings; we may incur asset impairment charges for goodwill, intangible assets or other long-lived assets; tax risks; our private brand offerings exposing us to various risks; regulatory risks; data privacy and cybersecurity risks; risks related to our intellectual property; the impact of ongoing or future lawsuits against us and certain of our officers and directors; risks related to climate change and other environmental, social and governance matters; and risks related to our organizational structure.

These and other important factors discussed under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2024, as updated by our Quarterly Reports on Form 10-Q and our other reports filed with the SEC, could cause actual results to differ materially from those indicated by the forward-looking statements made in this press release. Any such forward-looking statements represent management’s estimates as of the date of this press release. While we may elect to update such forward-looking statements at some point in the future, we disclaim any obligation to do so, even if subsequent events cause our views to change, except as required under applicable law. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

Future declarations of quarterly dividends, if any, are subject to the determination and discretion of the Company’s Board of Directors based on its consideration of various factors, including the Company’s results of operations, financial condition, level of indebtedness, anticipated capital requirements, contractual restrictions, restrictions in its debt agreements, restrictions under applicable law, receipt of excess tax distributions from CWGS, LLC, its business prospects and other factors that the Company’s Board of Directors may deem relevant.

We intend to use our official Facebook, X (formerly known as Twitter), and Instagram accounts, each at the handle @CampingWorld, as well as the investor page of our website, investor.campingworld.com, as a distribution channel of material information about the Company and for complying with our disclosure obligations under Regulation FD. The information we post through these social media channels and on our investor webpage may be deemed material.

4

Accordingly, investors should subscribe to these accounts and our investor alerts, in addition to following our press releases, SEC filings, public conference calls and webcasts. These social media channels may be updated from time to time.

5

Camping World Holdings, Inc. and Subsidiaries

Consolidated Statements of Operations (unaudited)

(In Thousands Except Per Share Amounts)

|

|

Three Months Ended |

|

Six Months Ended |

||||||||

|

|

June 30, |

|

June 30, |

||||||||

|

|

2025 |

|

2024 |

|

2025 |

|

2024 |

||||

Revenue: |

|

|

|

|

|

|

|

|

|

|

|

|

Good Sam Services and Plans |

|

$ |

54,213 |

|

$ |

52,548 |

|

$ |

100,421 |

|

$ |

98,229 |

RV and Outdoor Retail |

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

915,106 |

|

|

847,105 |

|

|

1,536,538 |

|

|

1,503,191 |

Used vehicles |

|

|

572,271 |

|

|

480,774 |

|

|

994,622 |

|

|

818,459 |

Products, service and other |

|

|

222,890 |

|

|

235,947 |

|

|

387,882 |

|

|

413,841 |

Finance and insurance, net |

|

|

201,198 |

|

|

179,016 |

|

|

349,865 |

|

|

314,470 |

Good Sam Club |

|

|

10,270 |

|

|

11,115 |

|

|

20,144 |

|

|

22,332 |

Subtotal |

|

|

1,921,735 |

|

|

1,753,957 |

|

|

3,289,051 |

|

|

3,072,293 |

Total revenue |

|

|

1,975,948 |

|

|

1,806,505 |

|

|

3,389,472 |

|

|

3,170,522 |

Costs applicable to revenue (exclusive of depreciation and amortization shown separately below): |

|

|

|

|

|

|

|

|

|

|

|

|

Good Sam Services and Plans |

|

|

21,947 |

|

|

17,192 |

|

|

39,668 |

|

|

32,375 |

RV and Outdoor Retail |

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

788,873 |

|

|

717,650 |

|

|

1,325,232 |

|

|

1,282,689 |

Used vehicles |

|

|

455,239 |

|

|

389,601 |

|

|

799,200 |

|

|

668,134 |

Products, service and other |

|

|

116,412 |

|

|

132,933 |

|

|

201,151 |

|

|

234,608 |

Good Sam Club |

|

|

1,222 |

|

|

1,470 |

|

|

2,338 |

|

|

2,660 |

Subtotal |

|

|

1,361,746 |

|

|

1,241,654 |

|

|

2,327,921 |

|

|

2,188,091 |

Total costs applicable to revenue |

|

|

1,383,693 |

|

|

1,258,846 |

|

|

2,367,589 |

|

|

2,220,466 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross profit (exclusive of depreciation and amortization shown separately below): |

|

|

|

|

|

|

|

|

|

|

|

|

Good Sam Services and Plans |

|

|

32,266 |

|

|

35,356 |

|

|

60,753 |

|

|

65,854 |

RV and Outdoor Retail |

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

126,233 |

|

|

129,455 |

|

|

211,306 |

|

|

220,502 |

Used vehicles |

|

|

117,032 |

|

|

91,173 |

|

|

195,422 |

|

|

150,325 |

Products, service and other |

|

|

106,478 |

|

|

103,014 |

|

|

186,731 |

|

|

179,233 |

Finance and insurance, net |

|

|

201,198 |

|

|

179,016 |

|

|

349,865 |

|

|

314,470 |

Good Sam Club |

|

|

9,048 |

|

|

9,645 |

|

|

17,806 |

|

|

19,672 |

Subtotal |

|

|

559,989 |

|

|

512,303 |

|

|

961,130 |

|

|

884,202 |

Total gross profit |

|

|

592,255 |

|

|

547,659 |

|

|

1,021,883 |

|

|

950,056 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

Selling, general, and administrative |

|

|

437,489 |

|

|

419,676 |

|

|

824,934 |

|

|

791,149 |

Depreciation and amortization |

|

|

23,419 |

|

|

20,032 |

|

|

45,963 |

|

|

39,322 |

Long-lived asset impairment |

|

|

— |

|

|

4,584 |

|

|

620 |

|

|

10,411 |

Lease termination |

|

|

(107) |

|

|

40 |

|

|

(107) |

|

|

40 |

Loss (gain) on sale or disposal of assets |

|

|

1,185 |

|

|

7,945 |

|

|

(638) |

|

|

9,530 |

Total operating expenses |

|

|

461,986 |

|

|

452,277 |

|

|

870,772 |

|

|

850,452 |

Income from operations |

|

|

130,269 |

|

|

95,382 |

|

|

151,111 |

|

|

99,604 |

Other expense |

|

|

|

|

|

|

|

|

|

|

|

|

Floor plan interest expense |

|

|

(20,989) |

|

|

(27,799) |

|

|

(39,295) |

|

|

(55,681) |

Other interest expense, net |

|

|

(30,836) |

|

|

(36,153) |

|

|

(61,367) |

|

|

(72,247) |

Other expense, net |

|

|

(2,600) |

|

|

(81) |

|

|

(2,758) |

|

|

(175) |

Total other expense |

|

|

(54,425) |

|

|

(64,033) |

|

|

(103,420) |

|

|

(128,103) |

Income (loss) before income taxes |

|

|

75,844 |

|

|

31,349 |

|

|

47,691 |

|

|

(28,499) |

Income tax (expense) benefit |

|

|

(18,321) |

|

|

(7,935) |

|

|

(14,850) |

|

|

1,107 |

Net income (loss) |

|

|

57,523 |

|

|

23,414 |

|

|

32,841 |

|

|

(27,392) |

Less: net income (loss) attributable to non-controlling interests |

|

|

(27,307) |

|

|

(13,643) |

|

|

(14,905) |

|

|

14,856 |

Net income (loss) attributable to Camping World Holdings, Inc. |

|

$ |

30,216 |

|

$ |

9,771 |

|

$ |

17,936 |

|

$ |

(12,536) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings (loss) per share of Class A common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

0.48 |

|

$ |

0.22 |

|

$ |

0.29 |

|

$ |

(0.28) |

Diluted |

|

$ |

0.48 |

|

$ |

0.22 |

|

$ |

0.28 |

|

$ |

(0.28) |

Weighted average shares of Class A common stock outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

62,610 |

|

|

45,093 |

|

|

62,571 |

|

|

45,070 |

Diluted |

|

|

62,747 |

|

|

45,244 |

|

|

102,661 |

|

|

45,070 |

6

Camping World Holdings, Inc. and Subsidiaries

Supplemental Data (unaudited)

|

|

Three Months Ended June 30, |

|

Increase |

|

|

Percent |

||||||

|

|

2025 |

|

2024 |

|

(decrease) |

|

|

Change |

||||

Unit sales |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

26,696 |

|

|

22,084 |

|

|

4,612 |

|

|

|

20.9% |

Used vehicles |

|

|

18,906 |

|

|

15,700 |

|

|

3,206 |

|

|

|

20.4% |

Total |

|

|

45,602 |

|

|

37,784 |

|

|

7,818 |

|

|

|

20.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average selling price |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

34,279 |

|

$ |

38,358 |

|

$ |

(4,079) |

|

|

|

(10.6%) |

Used vehicles |

|

|

30,269 |

|

|

30,623 |

|

|

(354) |

|

|

|

(1.2%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Same store unit sales(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

24,360 |

|

|

19,936 |

|

|

4,424 |

|

|

|

22.2% |

Used vehicles |

|

|

17,528 |

|

|

14,509 |

|

|

3,019 |

|

|

|

20.8% |

Total |

|

|

41,888 |

|

|

34,445 |

|

|

7,443 |

|

|

|

21.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Same store revenue(1) ($ in 000s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

833,171 |

|

$ |

768,687 |

|

$ |

64,484 |

|

|

|

8.4% |

Used vehicles |

|

|

525,573 |

|

|

448,019 |

|

|

77,554 |

|

|

|

17.3% |

Products, service and other |

|

|

179,017 |

|

|

186,445 |

|

|

(7,428) |

|

|

|

(4.0%) |

Finance and insurance, net |

|

|

186,659 |

|

|

163,615 |

|

|

23,044 |

|

|

|

14.1% |

Total |

|

$ |

1,724,420 |

|

$ |

1,566,766 |

|

$ |

157,654 |

|

|

|

10.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average gross profit per unit |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

4,729 |

|

$ |

5,862 |

|

$ |

(1,133) |

|

|

|

(19.3%) |

Used vehicles |

|

|

6,190 |

|

|

5,807 |

|

|

383 |

|

|

|

6.6% |

Finance and insurance, net per vehicle unit |

|

|

4,412 |

|

|

4,738 |

|

|

(326) |

|

|

|

(6.9%) |

Total vehicle front-end yield(2) |

|

|

9,747 |

|

|

10,577 |

|

|

(830) |

|

|

|

(7.8%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross margin |

|

|

|

|

|

|

|

|

|

|

|

|

|

Good Sam Services and Plans |

|

|

59.5% |

|

|

67.3% |

|

|

(777) |

bps |

|

|

|

New vehicles |

|

|

13.8% |

|

|

15.3% |

|

|

(149) |

bps |

|

|

|

Used vehicles |

|

|

20.5% |

|

|

19.0% |

|

|

149 |

bps |

|

|

|

Products, service and other |

|

|

47.8% |

|

|

43.7% |

|

|

411 |

bps |

|

|

|

Finance and insurance, net |

|

|

100.0% |

|

|

100.0% |

|

|

unch |

|

|

|

|

Good Sam Club |

|

|

88.1% |

|

|

86.8% |

|

|

133 |

bps |

|

|

|

Subtotal RV and Outdoor Retail |

|

|

29.1% |

|

|

29.2% |

|

|

(7) |

bps |

|

|

|

Total gross margin |

|

|

30.0% |

|

|

30.3% |

|

|

(34) |

bps |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail locations |

|

|

|

|

|

|

|

|

|

|

|

|

|

RV dealerships |

|

|

200 |

|

|

211 |

|

|

(11) |

|

|

|

(5.2%) |

RV service & retail centers |

|

|

1 |

|

|

4 |

|

|

(3) |

|

|

|

(75.0%) |

Total |

|

|

201 |

|

|

215 |

|

|

(14) |

|

|

|

(6.5%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RV and Outdoor Retail inventories ($ in 000s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

1,330,965 |

|

$ |

1,477,510 |

|

$ |

(146,545) |

|

|

|

(9.9%) |

Used vehicles |

|

|

536,665 |

|

|

349,843 |

|

|

186,822 |

|

|

|

53.4% |

Products, parts, accessories and misc. |

|

|

193,232 |

|

|

186,758 |

|

|

6,474 |

|

|

|

3.5% |

Total RV and Outdoor Retail inventories |

|

$ |

2,060,862 |

|

$ |

2,014,111 |

|

$ |

46,751 |

|

|

|

2.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vehicle inventory per location ($ in 000s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicle inventory per dealer location |

|

$ |

6,655 |

|

$ |

7,002 |

|

$ |

(347) |

|

|

|

(5.0%) |

Used vehicle inventory per dealer location |

|

|

2,683 |

|

|

1,658 |

|

|

1,025 |

|

|

|

61.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vehicle inventory turnover(3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicle inventory turnover |

|

|

1.9 |

|

|

1.6 |

|

|

0.2 |

|

|

|

14.5% |

Used vehicle inventory turnover |

|

|

3.3 |

|

|

3.3 |

|

|

(0.0) |

|

|

|

(0.3%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other data |

|

|

|

|

|

|

|

|

|

|

|

|

|

Active Customers(4) |

|

|

4,221,642 |

|

|

4,762,376 |

|

|

(540,734) |

|

|

|

(11.4%) |

Good Sam Club members (5) |

|

|

1,662,653 |

|

|

1,880,126 |

|

|

(217,473) |

|

|

|

(11.6%) |

Service bays (6) |

|

|

2,809 |

|

|

2,877 |

|

|

(68) |

|

|

|

(2.4%) |

Finance and insurance gross profit as a % of total vehicle revenue |

|

|

13.5% |

|

|

13.5% |

|

|

5 |

bps |

|

|

n/a |

Same store locations |

|

|

178 |

|

|

n/a |

|

|

n/a |

|

|

|

n/a |

7

|

|

Six Months Ended June 30, |

|

Increase |

|

|

Percent |

||||||

|

|

2025 |

|

2024 |

|

(decrease) |

|

|

Change |

||||

Unit sales |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

43,422 |

|

|

38,966 |

|

|

4,456 |

|

|

|

11.4% |

Used vehicles |

|

|

32,845 |

|

|

26,394 |

|

|

6,451 |

|

|

|

24.4% |

Total |

|

|

76,267 |

|

|

65,360 |

|

|

10,907 |

|

|

|

16.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average selling price |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

35,386 |

|

$ |

38,577 |

|

$ |

(3,191) |

|

|

|

(8.3%) |

Used vehicles |

|

|

30,282 |

|

|

31,009 |

|

|

(727) |

|

|

|

(2.3%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Same store unit sales(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

|

39,835 |

|

|

35,657 |

|

|

4,178 |

|

|

|

11.7% |

Used vehicles |

|

|

30,395 |

|

|

24,542 |

|

|

5,853 |

|

|

|

23.8% |

Total |

|

|

70,230 |

|

|

60,199 |

|

|

10,031 |

|

|

|

16.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Same store revenue(1) ($ in 000s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

1,410,789 |

|

$ |

1,382,134 |

|

$ |

28,655 |

|

|

|

2.1% |

Used vehicles |

|

|

918,061 |

|

|

763,872 |

|

|

154,189 |

|

|

|

20.2% |

Products, service and other |

|

|

314,183 |

|

|

331,245 |

|

|

(17,062) |

|

|

|

(5.2%) |

Finance and insurance, net |

|

|

326,001 |

|

|

291,581 |

|

|

34,420 |

|

|

|

11.8% |

Total |

|

$ |

2,969,034 |

|

$ |

2,768,832 |

|

$ |

200,202 |

|

|

|

7.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average gross profit per unit |

|

|

|

|

|

|

|

|

|

|

|

|

|

New vehicles |

|

$ |

4,866 |

|

$ |

5,659 |

|

$ |

(793) |

|

|

|

(14.0%) |

Used vehicles |

|

|

5,950 |

|

|

5,695 |

|

|

255 |

|

|

|

4.5% |

Finance and insurance, net per vehicle unit |

|

|

4,587 |

|

|

4,811 |

|

|

(224) |

|

|

|

(4.7%) |

Total vehicle front-end yield(2) |

|

|

9,920 |

|

|

10,485 |

|

|

(565) |

|

|

|

(5.4%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross margin |

|

|

|

|

|

|

|

|

|

|

|

|

|

Good Sam Services and Plans |

|

|

60.5% |

|

|

67.0% |

|

|

(654) |

bps |

|

|

|

New vehicles |

|

|

13.8% |

|

|

14.7% |

|

|

(92) |

bps |

|

|

|

Used vehicles |

|

|

19.6% |

|

|

18.4% |

|

|

128 |

bps |

|

|

|

Products, service and other |

|

|

48.1% |

|

|

43.3% |

|

|

483 |

bps |

|

|

|

Finance and insurance, net |

|

|

100.0% |

|

|

100.0% |

|

|

unch |

|

|

|

|

Good Sam Club |

|

|

88.4% |

|

|

88.1% |

|

|

31 |

bps |

|

|

|

Subtotal RV and Outdoor Retail |

|

|

29.2% |

|

|

28.8% |

|

|

44 |

bps |

|

|

|

Total gross margin |

|

|

30.1% |

|

|

30.0% |

|

|

18 |

bps |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other data |

|

|

|

|

|

|

|

|

|

|

|

|

|

Finance and insurance gross profit as a % of total vehicle revenue |

|

|

13.8% |

|

|

13.5% |

|

|

28 |

bps |

|

|

n/a |

Same store locations |

|

|

178 |

|

|

n/a |

|

|

n/a |

|

|

|

n/a |

unch – unchanged

bps – basis points

n/a – not applicable

| (1) | Our same store revenue and units calculations for a given period include only those stores that were open both at the end of the corresponding period and at the beginning of the preceding fiscal year. |

| (2) | Front end yield is calculated as gross profit from new vehicles, used vehicles and finance and insurance (net), divided by combined new and used vehicle unit sales. |

| (3) | Inventory turnover is calculated as vehicle costs applicable to revenue over the last twelve months divided by the average quarterly ending vehicle inventory over the last twelve months. |

| (4) | An Active Customer is a customer who has transacted with us in any of the eight most recently completed fiscal quarters prior to the date of measurement. |

| (5) | Excludes Good Sam Club members under the free basic plan, which was introduced in November 2023 and provides for limited participation in the loyalty point program without access to the remaining member benefits. |

| (6) | A service bay is a fully-constructed bay dedicated to service, installation, and collision offerings. |

8

Camping World Holdings, Inc. and Subsidiaries

Consolidated Balance Sheets (unaudited)

(In Thousands Except Per Share Amounts)

|

|

June 30, |

|

December 31, |

|

June 30, |

|||

|

|

2025 |

|

2024 |

|

2024 |

|||

Assets |

|

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

118,084 |

|

$ |

208,422 |

|

$ |

23,743 |

Contracts in transit |

|

|

163,767 |

|

|

61,222 |

|

|

165,033 |

Accounts receivable, net |

|

|

137,822 |

|

|

120,412 |

|

|

128,938 |

Inventories |

|

|

2,061,160 |

|

|

1,821,837 |

|

|

2,014,444 |

Prepaid expenses and other assets |

|

|

57,974 |

|

|

58,045 |

|

|

68,220 |

Assets held for sale |

|

|

15,202 |

|

|

1,350 |

|

|

8,418 |

Total current assets |

|

|

2,554,009 |

|

|

2,271,288 |

|

|

2,408,796 |

|

|

|

|

|

|

|

|

|

|

Property and equipment, net |

|

|

910,052 |

|

|

846,760 |

|

|

856,308 |

Operating lease assets |

|

|

716,020 |

|

|

739,352 |

|

|

760,143 |

Deferred tax assets, net |

|

|

211,435 |

|

|

215,140 |

|

|

193,873 |

Intangible assets, net |

|

|

17,602 |

|

|

19,469 |

|

|

21,354 |

Goodwill |

|

|

748,561 |

|

|

734,023 |

|

|

731,015 |

Other assets |

|

|

34,168 |

|

|

37,245 |

|

|

34,387 |

Total assets |

|

$ |

5,191,847 |

|

$ |

4,863,277 |

|

$ |

5,005,876 |

Liabilities and stockholders' equity |

|

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

|

Accounts payable |

|

$ |

283,450 |

|

$ |

145,346 |

|

$ |

260,390 |

Accrued liabilities |

|

|

182,581 |

|

|

118,557 |

|

|

187,120 |

Deferred revenues |

|

|

94,041 |

|

|

92,124 |

|

|

99,045 |

Current portion of operating lease liabilities |

|

|

65,488 |

|

|

61,993 |

|

|

62,795 |

Current portion of finance lease liabilities |

|

|

19,514 |

|

|

7,044 |

|

|

7,335 |

Current portion of Tax Receivable Agreement liability |

|

|

1,700 |

|

|

— |

|

|

12,277 |

Current portion of long-term debt |

|

|

23,023 |

|

|

23,275 |

|

|

24,082 |

Notes payable – floor plan, net |

|

|

1,280,102 |

|

|

1,161,713 |

|

|

1,296,352 |

Other current liabilities |

|

|

79,167 |

|

|

70,900 |

|

|

80,343 |

Total current liabilities |

|

|

2,029,066 |

|

|

1,680,952 |

|

|

2,029,739 |

|

|

|

|

|

|

|

|

|

|

Operating lease liabilities, net of current portion |

|

|

734,083 |

|

|

764,113 |

|

|

788,613 |

Finance lease liabilities, net of current portion |

|

|

128,598 |

|

|

131,004 |

|

|

134,538 |

Tax Receivable Agreement liability, net of current portion |

|

|

148,672 |

|

|

150,372 |

|

|

137,589 |

Revolving line of credit |

|

|

— |

|

|

— |

|

|

31,885 |

Long-term debt, net of current portion |

|

|

1,483,470 |

|

|

1,493,318 |

|

|

1,513,986 |

Deferred revenues |

|

|

63,337 |

|

|

63,642 |

|

|

66,981 |

Other long-term liabilities |

|

|

88,042 |

|

|

94,927 |

|

|

92,140 |

Total liabilities |

|

|

4,675,268 |

|

|

4,378,328 |

|

|

4,795,471 |

Commitments and contingencies |

|

|

|

|

|

|

|

|

|

Stockholders' equity: |

|

|

|

|

|

|

|

|

|

Preferred stock, par value $0.01 per share – 20,000 shares authorized; none issued and outstanding |

|

|

— |

|

|

— |

|

|

— |

Class A common stock, par value $0.01 per share – 250,000 shares authorized; 62,649, 62,502 and 49,571 shares issued, respectively, and 62,649, 62,502 and 45,115 shares outstanding, respectively |

|

|

626 |

|

|

625 |

|

|

496 |

Class B common stock, par value $0.0001 per share – 75,000 shares authorized; 39,466 shares issued and outstanding |

|

|

4 |

|

|

4 |

|

|

4 |

Class C common stock, par value $0.0001 per share – 0.001 share authorized, issued and outstanding |

|

|

— |

|

|

— |

|

|

— |

Additional paid-in capital |

|

|

205,383 |

|

|

193,692 |

|

|

133,461 |

Treasury stock, at cost; 4,456 shares at June 30, 2024 |

|

|

— |

|

|

— |

|

|

(156,116) |

Retained earnings |

|

|

134,525 |

|

|

132,241 |

|

|

171,817 |

Total stockholders' equity attributable to Camping World Holdings, Inc. |

|

|

340,538 |

|

|

326,562 |

|

|

149,662 |

Non-controlling interests |

|

|

176,041 |

|

|

158,387 |

|

|

60,743 |

Total stockholders' equity |

|

|

516,579 |

|

|

484,949 |

|

|

210,405 |

Total liabilities and stockholders' equity |

|

$ |

5,191,847 |

|

$ |

4,863,277 |

|

$ |

5,005,876 |

9

Camping World Holdings, Inc. and Subsidiaries

Summary of Consolidated Statements of Cash Flows (unaudited)

(In Thousands)

|

|

Six Months Ended June 30, |

||||

|

|

2025 |

|

2024 |

||

|

|

|

|

|

|

|

Net cash (used in) provided by operating activities |

|

$ |

(44,595) |

|

$ |

84,341 |

|

|

|

|

|

|

|

Investing activities |

|

|

|

|

|

|

Purchases of property and equipment |

|

|

(49,696) |

|

|

(48,553) |

Proceeds from sale of property and equipment |

|

|

2,966 |

|

|

3,583 |

Purchases of real property |

|

|

(72,386) |

|

|

(1,243) |

Proceeds from the sale of real property |

|

|

9,843 |

|

|

31,195 |

Purchases of businesses, net of cash acquired |

|

|

(81,154) |

|

|

(62,323) |

Proceeds from divestiture of business |

|

|

10,349 |

|

|

19,957 |

Purchases of intangible assets |

|

|

— |

|

|

(142) |

Proceeds from sale of intangible assets |

|

|

— |

|

|

2,595 |

Net cash used in investing activities |

|

|

(180,078) |

|

|

(54,931) |

|

|

|

|

|

|

|

Financing activities |

|

|

|

|

|

|

Proceeds from long-term debt |

|

|

— |

|

|

55,624 |

Payments on long-term debt |

|

|

(12,537) |

|

|

(57,351) |

Net proceeds (payments) on notes payable – floor plan, net |

|

|

168,108 |

|

|

(19,160) |

Borrowings on revolving line of credit |

|

|

— |

|

|

43,000 |

Payments on revolving line of credit |

|

|

— |

|

|

(32,000) |

Payments on finance leases |

|

|

(3,637) |

|

|

(3,682) |

Payments on sale-leaseback arrangement |

|

|

(102) |

|

|

(97) |

Payment of debt issuance costs |

|

|

— |

|

|

(876) |

Payments of stock offering costs |

|

|

(572) |

|

|

— |

Dividends on Class A common stock |

|

|

(15,652) |

|

|

(11,274) |

Proceeds from exercise of stock options |

|

|

— |

|

|

51 |

RSU shares withheld for tax |

|

|

(1,175) |

|

|

(754) |

Distributions to holders of LLC common units |

|

|

(98) |

|

|

(18,795) |

Net cash provided by (used in) financing activities |

|

|

134,335 |

|

|

(45,314) |

|

|

|

|

|

|

|

Decrease in cash and cash equivalents |

|

|

(90,338) |

|

|

(15,904) |

Cash and cash equivalents at beginning of the period |

|

|

208,422 |

|

|

39,647 |

Cash and cash equivalents at end of the period |

|

$ |

118,084 |

|

$ |

23,743 |

10

Earnings (Loss) Per Share

Basic earnings (loss) per share of Class A common stock is computed by dividing net income (loss) attributable to Camping World Holdings, Inc. by the weighted-average number of shares of Class A common stock outstanding during the period. Diluted earnings (loss) per share of Class A common stock is computed by dividing net income (loss) attributable to Camping World Holdings, Inc. by the weighted-average number of shares of Class A common stock outstanding adjusted to give effect to potentially dilutive securities.

The following table sets forth reconciliations of the numerators and denominators used to compute basic and diluted earnings (loss) per share of Class A common stock (unaudited):

|

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

||||||||

(In thousands except per share amounts) |

|

2025 |

|

2024 |

|

2025 |

|

2024 |

||||

Numerator: |

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

|

$ |

57,523 |

|

$ |

23,414 |

|

$ |

32,841 |

|

$ |

(27,392) |

Less: net income (loss) attributable to non-controlling interests |

|

|

(27,307) |

|

|

(13,643) |

|

|

(14,905) |

|

|

14,856 |

Net income (loss) attributable to Camping World Holdings, Inc. — basic |

|

$ |

30,216 |

|

$ |

9,771 |

|

$ |

17,936 |

|

$ |

(12,536) |

Add: reallocation of net income (loss) attributable to non-controlling interests from the assumed dilutive effect of stock options and RSUs |

|

|

27 |

|

|

19 |

|

|

— |

|

|

— |

Add: reallocation of net income (loss) attributable to non-controlling interests from the assumed redemption of common units of CWGS, LLC for Class A common stock |

|

|

— |

|

|

— |

|

|

11,049 |

|

|

— |

Net income (loss) attributable to Camping World Holdings, Inc. — diluted |

|

$ |

30,243 |

|

$ |

9,790 |

|

$ |

28,985 |

|

$ |

(12,536) |

Denominator: |

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average shares of Class A common stock outstanding — basic |

|

|

62,610 |

|

|

45,093 |

|

|

62,571 |

|

|

45,070 |

Dilutive restricted stock units |

|

|

137 |

|

|

151 |

|

|

195 |

|

|

— |

Dilutive common units of CWGS, LLC that are convertible into Class A common stock |

|

|

— |

|

|

— |

|

|

39,895 |

|

|

— |

Weighted-average shares of Class A common stock outstanding — diluted |

|

|

62,747 |

|

|

45,244 |

|

|

102,661 |

|

|

45,070 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings (loss) per share of Class A common stock — basic |

|

$ |

0.48 |

|

$ |

0.22 |

|

$ |

0.29 |

|

$ |

(0.28) |

Earnings (loss) per share of Class A common stock — diluted |

|

$ |

0.48 |

|

$ |

0.22 |

|

$ |

0.28 |

|

$ |

(0.28) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average anti-dilutive securities excluded from the computation of diluted earnings (loss) per share of Class A common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

Stock options to purchase Class A common stock |

|

|

151 |

|

|

186 |

|

|

153 |

|

|

188 |

Restricted stock units |

|

|

1,892 |

|

|

1,037 |

|

|

1,684 |

|

|

1,980 |

Common units of CWGS, LLC that are convertible into Class A common stock |

|

|

39,895 |

|

|

40,045 |

|

|

— |

|

|

40,045 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average contingently issuable shares excluded from the computation of diluted loss per share of Class A common stock since all necessary conditions had not been satisfied: |

|

|

|

|

|

|

|

|

|

|

|

|

Performance stock units |

|

|

750 |

|

|

— |

|

|

750 |

|

|

— |

Non-GAAP Financial Measures

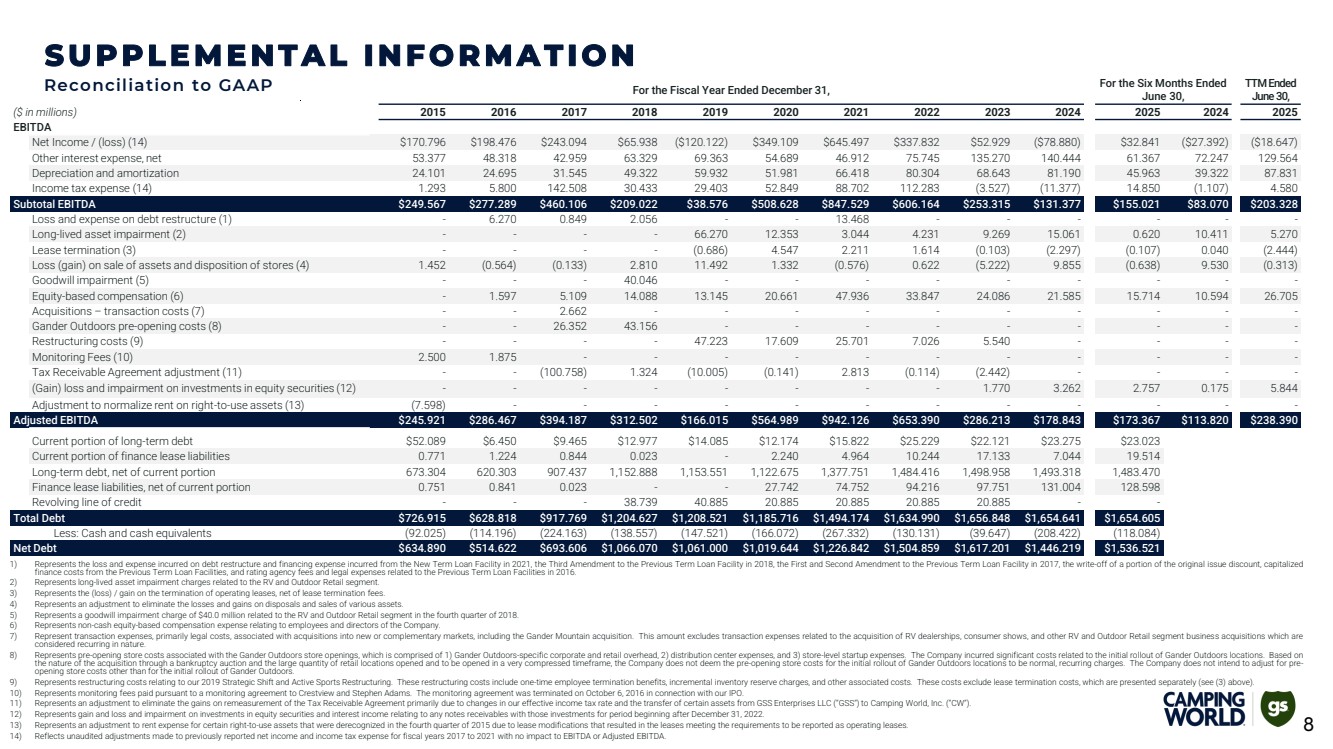

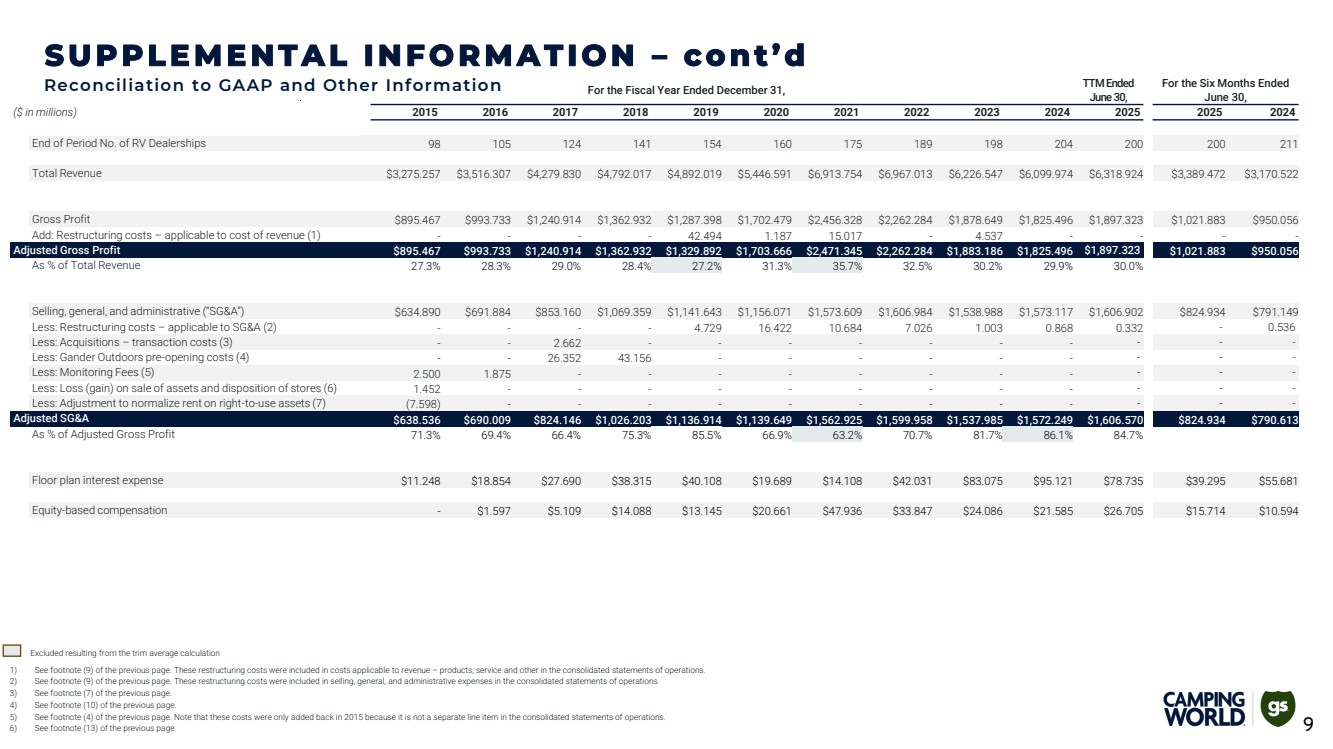

To supplement our condensed consolidated financial statements, which are prepared and presented in accordance with accounting principles generally accepted in the United States (“GAAP”), we use the following non-GAAP financial measures: EBITDA; Adjusted EBITDA; Adjusted EBITDA Margin; Adjusted Net Income (Loss) Attributable to Camping World Holdings, Inc. – Basic; Adjusted Net Income (Loss) Attributable to Camping World Holdings, Inc. – Diluted; Adjusted Earnings (Loss) Per Share – Basic; Adjusted Earnings (Loss) Per Share – Diluted; and SG&A Excluding SBC (collectively the "Non-GAAP Financial Measures"). We believe that these Non-GAAP Financial Measures, when used in conjunction with GAAP financial measures, provide useful information about operating results, enhance the overall understanding of past financial performance and future prospects, and allow for greater transparency with respect to the key metrics we use in our financial and operational decision making. Certain of these Non-GAAP Financial Measures are also frequently used by analysts, investors and other interested parties to evaluate companies in the Company’s industry and are used by management to evaluate our operating performance, to evaluate the effectiveness of strategic initiatives and for planning purposes. By providing these Non-GAAP Financial Measures, together with reconciliations, we believe we are enhancing investors’ understanding of our business and our results of operations, as well as assisting investors in evaluating how well we are executing our strategic initiatives. In addition, our Senior Secured Credit Facilities use Adjusted EBITDA, as calculated for our subsidiary CWGS Group, LLC, to measure our compliance with covenants such as the consolidated leverage ratio.

11

The Non-GAAP Financial Measures have limitations as analytical tools, and the presentation of this financial information is not intended to be considered in isolation or as a substitute for, or superior to, the financial information prepared and presented in accordance with GAAP. They should not be construed as an inference that the Company’s future results will be unaffected by any items adjusted for in these Non-GAAP Financial Measures. In evaluating these Non-GAAP Financial Measures, it is reasonable to expect that certain of these items will occur in future periods. However, we believe these adjustments are appropriate because the amounts recognized can vary significantly from period to period, do not directly relate to the ongoing operations of our business and complicate comparisons of our internal operating results and operating results of other companies over time. Each of the normal recurring adjustments and other adjustments described in this section and in the reconciliation tables below help management with a measure of our core operating performance over time by removing items that are not related to day-to-day operations.

Our earnings call on July 30, 2025 may present guidance that includes Adjusted EBITDA. A full reconciliation of the forecasted Adjusted EBITDA to its most-directly comparable GAAP metric cannot be provided without unreasonable efforts due to the inherent difficulty in forecasting and quantifying with reasonable accuracy significant items required for the reconciliations.

The Non-GAAP Financial Measures that we use are not necessarily comparable to similarly titled measures used by other companies due to different methods of calculation.

EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin

We define “EBITDA” as net income (loss) before other interest expense, net (excluding floor plan interest expense), provision for income tax expense (benefit) and depreciation and amortization. We define “Adjusted EBITDA” as EBITDA further adjusted for the impact of certain noncash and other items that we do not consider in our evaluation of ongoing operating performance. These items include, among other things, long-lived asset impairment, gains and losses on sale or disposal of assets, net, SBC, losses and gains and/or impairment on investments in equity securities, lease termination costs, and other unusual or one-time items. We define “Adjusted EBITDA Margin” as Adjusted EBITDA as a percentage of total revenue. We caution investors that amounts presented in accordance with our definitions of EBITDA, Adjusted EBITDA, and Adjusted EBITDA Margin may not be comparable to similar measures disclosed by our competitors, because not all companies and analysts calculate EBITDA, Adjusted EBITDA, and Adjusted EBITDA Margin in the same manner. We present EBITDA, Adjusted EBITDA, and Adjusted EBITDA Margin because we consider them to be important supplemental measures of our performance and believe they are frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. Management believes that investors’ understanding of our performance is enhanced by including these Non-GAAP Financial Measures as a reasonable basis for comparing our ongoing results of operations.

12

The following table reconciles EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin to the most directly comparable GAAP financial performance measures (unaudited):

|

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

|

||||||||

($ in thousands) |

|

2025 |

|

2024 |

|

2025 |

|

2024 |

|

||||

EBITDA and Adjusted EBITDA: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

|

$ |

57,523 |

|

$ |

23,414 |

|

$ |

32,841 |

|

$ |

(27,392) |

|

Other interest expense, net |

|

|

30,836 |

|

|

36,153 |

|

|

61,367 |

|

|

72,247 |

|

Depreciation and amortization |

|

|

23,419 |

|

|

20,032 |

|

|

45,963 |

|

|

39,322 |

|

Income tax expense (benefit) |

|

|

18,321 |

|

|

7,935 |

|

|

14,850 |

|

|

(1,107) |

|

Subtotal EBITDA |

|

|

130,099 |

|

|

87,534 |

|

|

155,021 |

|

|

83,070 |

|

Long-lived asset impairment (a) |

|

|

— |

|

|

4,584 |

|

|

620 |

|

|

10,411 |

|

Loss (gain) on sale or disposal of assets, net (b) |

|

|

1,185 |

|

|

7,945 |

|

|

(638) |

|

|

9,530 |

|

SBC (c) |

|

|

8,444 |

|

|

5,397 |

|

|

15,714 |

|

|

10,594 |

|

Loss and/or impairment on investments in equity securities (d) |

|

|

2,600 |

|

|

81 |

|

|

2,757 |

|

|

175 |

|

Lease termination (e) |

|

|

(107) |

|

|

40 |

|

|

(107) |

|

|

40 |

|

Adjusted EBITDA |

|

$ |

142,221 |

|

$ |

105,581 |

|

$ |

173,367 |

|

$ |

113,820 |

|

|

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

|||||

(as percentage of total revenue) |

|

2025 |

|

2024 |

|

2025 |

|

2024 |

|

Adjusted EBITDA margin: |

|

|

|

|

|

|

|

|

|

Net income (loss) margin |

|

2.9% |

|

1.3% |

|

1.0% |

|

|

(0.9%) |

Other interest expense, net |

|

1.6% |

|

2.0% |

|

1.8% |

|

|

2.3% |

Depreciation and amortization |

|

1.2% |

|

1.1% |

|

1.4% |

|

|

1.2% |

Income tax expense (benefit) |

|

0.9% |

|

0.4% |

|

0.4% |

|

|

(0.0%) |

Subtotal EBITDA margin |

|

6.6% |

|

4.8% |

|

4.6% |

|

|

2.6% |

Long-lived asset impairment (a) |

|

— |

|

0.3% |

|

0.0% |

|

|

0.3% |

Loss (gain) on sale or disposal of assets, net (b) |

|

0.1% |

|

0.4% |

|

(0.0%) |

|

|

0.3% |

SBC (c) |

|

0.4% |

|

0.3% |

|

0.5% |

|

|

0.3% |

Loss and/or impairment on investments in equity securities (d) |

|

0.1% |

|

0.0% |

|

0.1% |

|

|

0.0% |

Lease termination (e) |

|

(0.0%) |

|

0.0% |

|

(0.0%) |

|

|

0.0% |

Adjusted EBITDA margin |

|

7.2% |

|

5.8% |

|

5.1% |

|

|

3.6% |

|

Three Months Ended |

|

TTM Ended |

|||||||||||

|

June 30, |

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|||||

($ in thousands) |

2025 |

|

2025 |

|

2024 |

|

2024 |

|

2025 |

|||||

Adjusted EBITDA: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

$ |

57,523 |

|

$ |

(24,682) |

|

$ |

(59,544) |

|

$ |

8,056 |

|

$ |

(18,647) |

Other interest expense, net |

|

30,836 |

|

|

30,531 |

|

|

32,320 |

|

|

35,877 |

|

|

129,564 |

Depreciation and amortization |

|

23,419 |

|

|

22,544 |

|

|

21,285 |

|

|

20,583 |

|

|

87,831 |

Income tax expense (benefit) |

|

18,321 |

|

|

(3,471) |

|

|

(8,221) |

|

|

(2,049) |

|

|

4,580 |

Subtotal EBITDA |

|

130,099 |

|

|

24,922 |

|

|

(14,160) |

|

|

62,467 |

|

|

203,328 |

Long-lived asset impairment (a) |

|

— |

|

|

620 |

|

|

2,706 |

|

|

1,944 |

|

|

5,270 |

Loss (gain) on sale or disposal of assets, net (b) |

|

1,185 |

|

|

(1,823) |

|

|

330 |

|

|

(5) |

|

|