UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 40-F

|

|

|

☐ |

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

|

|

|

☑ |

|

ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2024 Commission File Number: 001-35297

FORTUNA MINING CORP.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English (if applicable))

British Columbia, Canada

(Province or other jurisdiction of incorporation or organization)

|

|

|

|

|

|

1040 |

|

N/A |

|

(Primary Standard Industrial Classification Code Number (if applicable)) |

|

(I.R.S. Employer Identification Number (if applicable)) |

1111 Melville Street, Suite 820

Vancouver, British Columbia V6E 3V6, Canada

604-484-4085

(Address and telephone number of Registrant’s principal executive offices)

Puglisi & Associates

850 Library Ave., Suite 204

Newark, DE 19711

302-738-6680

(Name, address (including zip code) and telephone number (including area code)

of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

|

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Common Shares |

FSM |

New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

For annual reports, indicate by check mark the information filed with this Form:

☑ Annual information form ☑ Audited annual financial statements

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

There were 306,587,630 common shares with no par value outstanding as of December 31, 2024.

Indicate by check mark whether the Registrant: (1) has filed all reports to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days.

Yes ☑ No ◻

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Yes ☑ No ◻

Indicate by check mark whether the Registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant Section 13(a) of the Exchange Act.

◻

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

DISCLOSURE REGARDING CONTROLS AND PROCEDURES

Disclosure Controls and Procedures.

Disclosure controls and procedures are defined in Rule 13a-15(e) and Rule 15d-15(e) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) as those controls and procedures designed to ensure that information required to be disclosed in the annual filings and interim filings and other reports filed or submitted by Fortuna Mining Corp. (formerly called Fortuna Silver Mines Inc.) (the “Company”) under the Exchange Act is duly recorded, processed, summarized and reported, within the time periods specified in rules and forms of the United States Securities and Exchange Commission (the “SEC”). Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed in the Company’s reports and filings is accumulated and communicated to management, including the Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”) as appropriate, to allow timely decisions regarding required disclosure.

The Company evaluated, with the participation of its CEO and CFO, the effectiveness of its disclosure controls and procedures as of December 31, 2024. Based on that evaluation, the CEO and the CFO have concluded that, as of the end of the period covered by this Annual Report on Form 40-F, the disclosure controls and procedures were effective to provide reasonable assurance that information required to be disclosed in the Company’s annual filings and interim filings and other reports filed or submitted under the Exchange Act, is recorded, processed, summarized and reported within time periods specified in SEC rules and forms and is accumulated and communicated to management, including the CEO and CFO, as appropriate to allow timely decisions regarding required disclosure.

Notwithstanding the foregoing, because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that the Company’s disclosure controls and procedures will detect or uncover every situation involving the failure of persons within the Company and its subsidiaries to disclose material information otherwise required to be set forth in the Company’s periodic reports. The Company’s disclosure controls and procedures are designed to provide reasonable assurance of achieving their objective of ensuring that information required to be disclosed in the reports that the Company files or submits under the Exchange Act is communicated to management to allow timely decisions regarding required disclosure.

Management’s Annual Report on Internal Control Over Financial Reporting.

Management is responsible for establishing and maintaining adequate internal control over financial reporting (as such term is defined in Rule 13a-15(f) and Rule 15d-15(f) under the Exchange Act) and has designed such internal controls over financial reporting to provide reasonable assurance regarding the reliability of financial reporting and preparation of financial statements for external purposes in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board.

In designing and evaluating the Company’s internal control over financial reporting, the Company’s management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives and management necessarily applies its reasonable judgment in evaluating the cost-benefit relationship of possible controls and procedures. Because of its inherent limitations, internal controls over financial reporting may not prevent or detect misstatements. Projections of any evaluation of effectiveness to future periods are subject to the risks that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies and procedures may deteriorate.

Management assessed the effectiveness of the Company’s internal control over financial reporting as of December 31, 2024. In making this assessment, management used the Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on this assessment, management concluded that the Company’s internal control over financial reporting was effective as of December 31, 2024.

See “Management’s Report on Internal Control Over Financial Reporting” in the Management’s Discussion and Analysis for the fiscal years ended December 31, 2024 and 2023, included as Exhibit 99.3 to this Annual Report on Form 40-F. The Company’s auditors have issued an attestation report on management’s assessment of the Company’s internal control over financial reporting. See “Attestation Report of the Registered Public Accounting Firm” below.

Attestation Report of the Independent Registered Public Accounting Firm. The Company’s internal control over financial reporting as of December 31, 2024 has been audited by KPMG LLP, Independent Registered Public Accounting Firm, Vancouver, BC, Canada, Audit Firm ID 85. The required report is included in the “Report of Independent Registered Public Accounting Firm,” that accompanies the Company’s audited consolidated financial statements as at and for the fiscal years ended December 31, 2024 and 2023, filed as part of this Annual Report on Form 40-F in Exhibit 99.2.

Changes in Internal Control Over Financial Reporting. During the fiscal year ended December 31, 2024, there were no changes in the Company’s internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

NOTICES PURSUANT TO REGULATION BTR

None.

IDENTIFICATION OF THE AUDIT COMMITTEE

The Company has a separately-designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Exchange Act. The members of the audit committee are Kylie Dickson, Alfredo Sillau and David Farrell. The board of directors has determined that each of Kylie Dickson, Alfredo Sillau and David Farrell is independent, as that term is defined in Rule 10A-3 under the Exchange Act and the Listed Company Manual of the New York Stock Exchange.

AUDIT COMMITTEE FINANCIAL EXPERT

The board of directors of the Company has determined that Kylie Dickson, a member of the Company’s audit committee, qualifies as an audit committee financial expert for purposes of paragraph (8) of General Instruction B to Form 40-F. The SEC has indicated that the designation of Kylie Dickson as an audit committee financial expert does not: (i) make her an “expert” for any purpose, (ii) impose any duties, obligations or liabilities on her that are greater than those imposed on members of the audit committee and the board of directors who do not carry this designation, and (iii) or affect the duties, obligations or liabilities of any other member of the audit committee or the board of directors.

CODE OF ETHICS

The Company has adopted a “code of ethics” (as that term is defined in Form 40-F), entitled the “Code of Business Conduct and Ethics and Whistle-Blower Policy”, that applies to all of its directors, officers, employees, and consultants including its principal executive officer, principal financial officer, principal accounting officer or controller, and persons performing similar functions.

The Code of Business Conduct and Ethics and Whistle-Blower Policy is available for viewing on the Company’s website at www.fortunamining.com under “Library - Policies”.

PRINCIPAL ACCOUNTANT FEES AND SERVICES

The required disclosure is included under the heading “Audit Committee” in the Company’s Annual Information Form for the fiscal year ended December 31, 2024, filed as part of this Annual Report on Form 40-F in Exhibit 99.1.

PRE-APPROVAL POLICIES AND PROCEDURES

The auditors of the Company obtain, as necessary, the pre-approval of the Audit Committee for any anticipated additional services required of the auditors for the coming fiscal year. If other service requirements arise during the year, the Audit Committee will pre-approve such services at that time, prior to the commencement of such services. During the fiscal year ended December 31, 2024, the Audit Committee did not approve any audit-related, tax or other services pursuant to paragraph (c) (7) (i) (C) of Rule 2-01 of Regulation S-X, with the exception of certain financial statement preparation services relating to the statutory audits of certain of the Company's subsidiaries, the fees for which represented less than 5% of total fees for the fiscal year ended December 31, 2024.

OFF-BALANCE SHEET ARRANGEMENTS

The Company does not have any off-balance sheet arrangements required to be disclosed in this Annual Report on Form 40-F.

MINE SAFETY DISCLOSURE

The Company is currently not required to disclose the information required by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

NEW YORK STOCK EXCHANGE CORPORATE GOVERNANCE

The Company is a “foreign private issuer” as defined in Rule 3b-4 under the Exchange Act and Rule 405 under the United States Securities Act of 1933, as amended, and the Company’s common shares are listed on the New York Stock Exchange (the “NYSE”). Sections 103.00, 303A.00 and 303A.11 of the NYSE Listed Company Manual permit foreign private issuers to follow home country practices in lieu of certain provisions of the NYSE Listed Company Manual. A foreign private issuer that follows home country practices in lieu of certain provisions of the NYSE Listed Company Manual must disclose any significant ways in which its corporate governance practices differ from those followed by domestic companies either on its website or in the annual report that it distributes to shareholders in the United States. A description of the significant ways in which the Company’s governance practices differ from those followed by domestic companies pursuant to NYSE standards is disclosed on the Company’s website at www.fortunamining.com under “Library – Stock Exchange Listings - New York Stock Exchange”.

The Company’s corporate governance practices, as described on its website, are consistent with the laws, customs and practices in Canada.

UNDERTAKING

The Company undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the SEC staff, and to furnish promptly, when requested to do so by the SEC staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

CONSENT TO SERVICE OF PROCESS

A Form F-X signed by the Company and its agent for service of process has been previously filed with the SEC together with the Company’s Registration Statement on Form 40-F (File No. 001-35297) in connection with its securities registered on such form.

Any changes to the name or address of the agent for service of process of the Company shall be communicated promptly to the SEC by an amendment to the Form F-X referencing the file number of the Company.

SIGNATURE

Pursuant to the requirements of the Exchange Act, the Company certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

|

|

|

|

|

Date: March 27, 2025 |

FORTUNA MINING CORP. |

|

||

|

By: |

“Jorge Ganoza Durant” |

|

|

|

|

Name: Jorge Ganoza Durant |

|

|

|

|

Title:President, Chief Executive Officer & Director |

||

| ||||

EXHIBIT INDEX

Exhibit |

|

Description |

|

|

|

97 |

|

|

|

|

|

|

Annual Information Form for the year ended December 31, 2024 |

|

|

|

|

99.2 |

|

|

|

|

|

99.3 |

|

Management’s Discussion and Analysis for the years ended December 31, 2024 and 2023 |

|

|

|

|

Consent of KPMG LLP (PCAOB ID 85) |

|

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

Certification of Chief Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

|

|

|

|

|

Certification of Chief Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

|

|

|

|

|

Certification of Chief Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

|

|

|

|

|

Certification of Chief Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

|

|

|

|

101.INS |

|

XBRL Instance |

|

|

|

101.SCH |

|

XBRL Taxonomy Extension Schema |

|

|

|

101.CAL |

|

XBRL Taxonomy Extension Calculation Linkbase |

|

|

|

101.DEF |

|

XBRL Taxonomy Extension Definition Linkbase |

|

|

|

101.LAB |

|

XBRL Taxonomy Extension Label Linkbase |

|

|

|

101.PRE |

|

XBRL Taxonomy Extension Presentation Linkbase |

|

|

|

104 |

|

Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101) |

ANNUAL INFORMATION FORM

For the Fiscal Year Ended December 31, 2024

DATED: March 20, 2025

CORPORATE OFFICE: |

MANAGEMENT HEAD OFFICE: |

|

|

1111 Melville Street, Suite 820 |

Piso 5, Av. Jorge Chávez #154 |

Vancouver, BC V6E 3V6, Canada |

Miraflores, Lima, Peru |

Tel: 604.484.4085 |

Tel: 511.616.6060, ext. 2 |

Fax: 604.484.4029 |

|

TABLE OF CONTENTS

PRELIMINARY NOTES |

1 |

Cautionary Statement – Forward Looking Statements |

1 |

Notice Regarding Non-IFRS Measures |

5 |

Cautionary Note to United States Investors Concerning Estimates of Reserves and Resources |

7 |

Documents Incorporated by Reference |

7 |

Scientific and Technical Information |

7 |

Currency |

7 |

|

|

CORPORATE STRUCTURE |

8 |

Name, Address and Incorporation |

8 |

Intercorporate Relationships |

8 |

|

|

GENERAL DEVELOPMENT OF THE BUSINESS |

9 |

Business of the Company |

9 |

Three-Year History and Recent Developments |

9 |

|

|

DESCRIPTION OF THE BUSINESS |

28 |

General |

28 |

Risk Factors |

32 |

Material Mineral Properties (see Schedules “A”, “B”, “C” and “D”) |

59 |

Non-Material Mineral Properties |

61 |

|

|

DIVIDENDS |

62 |

|

|

DESCRIPTION OF CAPITAL STRUCTURE |

62 |

Common Shares |

62 |

Notes |

63 |

Debentures |

63 |

|

|

MARKET FOR SECURITIES |

64 |

Trading Price and Volume |

64 |

Prior Sales |

64 |

|

|

DIRECTORS AND EXECUTIVE OFFICERS |

64 |

Name, Occupation and Shareholding |

64 |

Cease Trade Orders or Bankruptcies |

66 |

Penalties or Sanctions |

67 |

Conflicts of Interest |

67 |

|

|

AUDIT COMMITTEE |

68 |

|

|

LEGAL PROCEEDINGS |

69 |

|

|

TRANSFER AGENT AND REGISTRAR |

69 |

|

|

MATERIAL CONTRACTS |

70 |

|

|

INTERESTS OF EXPERTS |

70 |

|

|

ADDITIONAL INFORMATION |

71 |

|

|

Material Mineral Properties: |

|

Séguéla Mine, Côte d’Ivoire |

Schedule “A” |

Yaramoko Mine, Burkina Faso |

Schedule “B” |

Lindero Mine, Argentina |

Schedule “C” |

Caylloma Mine, Peru |

Schedule “D” |

Audit Committee Charter |

Schedule “E” |

FORTUNA MINING CORP.

PRELIMINARY NOTES

This Annual Information Form (“AIF”) is dated March 20, 2025 and presents information about Fortuna Mining Corp. (formerly called Fortuna Silver Mines Inc.) (referred to herein as the “Company” or “Fortuna”). Except as otherwise indicated, the information contained herein is presented as at December 31, 2024, being the date of the Company’s most recently completed financial year end.

Fortuna has a number of direct and indirect subsidiaries which own and operate assets and conduct activities in different jurisdictions. The terms "Fortuna" or the "Company" are use in this AIF for simplicity of the discussion provided herein and may include references to subsidiaries that have an affiliation with Fortuna, without necessarily identifying the specific nature of such affiliation.

Cautionary Statement – Forward-Looking Statements

Certain statements contained in this AIF and the documents incorporated by reference into this AIF constitute forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and Section 21E of the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”) and Section 27A of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and forward-looking information within the meaning of applicable Canadian securities legislation (collectively, “forward-looking statements”). All statements included herein, other than statements of historical fact, are forward-looking statements and are subject to a variety of known and unknown risks and uncertainties which could cause actual events or results to differ materially from those reflected in the forward-looking statements. The forward-looking statements in this AIF include, without limitation, statements relating to:

| ● | Mineral Reserves (as defined herein) and Mineral Resources (as defined herein) at the Caylloma, Lindero, Séguéla and Yaramoko Mines and at the Arizaro Project and the Diamba Sud gold project ("Diamba Sud Project"), as they involve implied assessment, based on estimates and assumptions that the Mineral Reserves and Mineral Resources described exist in the quantities predicted or estimated and can be profitably produced in the future; |

| ● | estimated rates of production for gold silver and the other metals that we produce, timing of production and the cash costs and all-in sustaining cash costs (“AISC”) estimates; |

| ● | expectations with respect to metal grade estimates and the impact of any variations relative to metal grades experienced; |

| ● | the Company's anticipated financial and operational performance in 2025 as well as anticipated financial and operational performance at the Séguéla Mine in 2026; estimated production forecasts for 2025 as well for 2026 at the Séguéla Mine; |

| ● | the Company's plans and expectations for its material properties and future Brownfields and Greenfields exploration, development and operating activities, including, without limitation, capital expenditures, exploration activities and budgets, forecasts and schedule estimates, as well as their impact on the results of operations or financial condition of the Company; |

| ● | life of mine estimates for the Caylloma, Lindero, Séguéla and Yaramoko Mines, including the expected timing of the closure of the Yaramoko Mine; |

| ● | timing for delivery of materials and equipment for the Company’s properties; |

| ● | the sufficiency of the Company’s cash on hand and available credit lines and estimated cash flows to fund planned capital and exploration programs at its properties; |

| ● | the Company’s financial performance being closely linked to the prices of silver and gold and other metals; |

| ● | rising costs caused by the effect of the Ukraine - Russian conflict and the Israel - Hamas war, causing increased rates of inflation and pressures on the global supply chain; |

| ● | the anticipated rates of returns from mining projects, as reflected in preliminary economic assessments, pre-feasibility and feasibility studies or other reports prepared in relation to development of projects; |

| ● | future sales of the metals and concentrates or other products that the Company produces, the availability and location of refineries and sales counterparts, and any plans and expectations with respect to hedging; |

ANNUAL INFORMATION FORM |

Page | 1 |

FORTUNA MINING CORP.

| ● | the Company’s plans and expectations in respect of the Diamba Sud Project regarding exploration activities to be undertaken and the preparation of a preliminary economic assessment in order to determine that the mineral resource is supportive of project development; |

| ● | the Company’s expectations relating to timing for applying for an exploitation permit at the Diamba Sud Project; |

| ● | statements that future mining at the Séguéla Mine may include underground mining as well as open pit mining; |

| ● | statements regarding the Company’s intention to sell the San Jose Mine; |

| ● | statements regarding the expected timing for the completion of the expansion of the leach pad at the Lindero Mine; |

| ● | the payments due under, and the maturity dates of the Company’s financial liabilities, lease obligations and other contractual commitments; |

| ● | compliance with environmental, health, safety and other regulations; |

| ● | the Company’s commitment to sustainable development, by conducting its operations in an environmentally and socially responsible manner, including complying with its Sustainability Framework, its environmental, social and governance (“ESG”) policies and targets and other operational and governance policies; |

| ● | the ability of the Company to reduce its greenhouse gas (“GHG”) emissions to contribute to a lower carbon economy and lessen the impact of its operations on climate change, through projects such as solar power plants at the Lindero and Séguéla Mines and the construction of a new cyclone plant at Caylloma; |

| ● | the Company’s commitment to mitigating the physical risks of climate change at its mine sites and to minimize its operational water consumption as well as to reduce its exposure to climate-related transition risks; |

| ● | complying with anti-corruption laws; |

| ● | litigation matters; |

| ● | estimated mine closure costs, including remediation and reclamation and timing thereof; and |

| ● | future income tax rate. |

Often, but not always, these forward-looking statements can be identified by the use of words such as “anticipates”, “believes”, “plans”, “estimates”, “expects”, “forecasts”, “scheduled”, “targets”, “possible”, “strategy”, “potential”, “intends”, “advance”, “goal”, “objective”, “projects”, “budget”, “calculates” or statements that events, “will”, “may”, “could” or “should” occur or be achieved and similar expressions, including negative variations.

The forward-looking statements in this AIF also include financial outlooks and other forward-looking metrics relating to Fortuna and its business, including references to financial and business prospects and future results of operations, including production, and cost guidance and anticipated future financial performance. Such information, which may be considered future oriented financial information or financial outlooks within the meaning of applicable Canadian securities legislation (collectively, “FOFI”), has been approved by management of the Company and is based on assumptions which management believes were reasonable on the date such FOFI was prepared, having regard to the industry, business, financial conditions, plans and prospects of Fortuna and its business and properties. These projections are provided to describe the prospective performance of the Company’s business. Nevertheless, readers are cautioned that such information is highly subjective and should not be relied on as necessarily indicative of future results and that actual results may differ significantly from such projections. FOFI constitutes forward-looking statements and is subject to the same assumptions, uncertainties, risk factors and qualifications as set forth below.

Material Risks and Assumptions

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual events, results, performance or achievements of the Company to be materially different from any events, results, performance or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and factors include, among others:

ANNUAL INFORMATION FORM |

Page | 2 |

FORTUNA MINING CORP.

| ● | operational risks associated with mining and mineral processing; |

| ● | uncertainty relating to Mineral Resource and Mineral Reserve estimates; |

| ● | uncertainty relating to capital and operating costs, production schedules and economic returns; |

| ● | uncertainty relating to the financing and timing of the Company’s sustaining capital projects at its mines due to the increased costs and rising rates of inflation; |

| ● | risks relating to the Company’s ability to replace its Mineral Reserves; |

| ● | risks associated with mineral exploration and project development; |

| ● | risk related to the exploration of projects such as the Diamba Sud Project, including whether mineral resources confirmed at the project will be in an amount satisfactory to the Company; |

| ● | risks associated with the ability of the Company to obtain an exploitation permit at the Diamba Sud Project; |

| ● | risks relating to delays in receiving VAT receivables; |

| ● | risks associated with political instability and changes to the regulations governing the Company’s business operations; |

| ● | uncertainty relating to the repatriation of funds as a result of currency controls; |

| ● | environmental matters including obtaining or renewing environmental permits and potential liability claims; |

| ● | uncertainties related to the potential disposition or closure of the San Jose Mine; |

| ● | changes in national and local government legislation, taxation, controls, regulations and political or economic developments in countries in which the Company does or may carry on business, including potential changes by the new Argentine Government to national macroeconomic policies, the taxation system and import and export duties; |

| ● | the potential impact of any tariffs, countervailing duties or other trade restrictions; |

| ● | risks associated with war, hostilities or other conflicts, such as the Ukrainian – Russian conflict and the Israel – Hamas war, and the possible impact of such conflicts on global economic activity; |

| ● | risks relating to the termination of the Company’s mining concessions in certain circumstances; |

| ● | risks related to International Labour Organization (“ILO”) Convention 169 compliance; |

| ● | developing and maintaining relationships with local communities and stakeholders; |

| ● | risks associated with losing control of public perception as a result of social media and other web-based applications; |

| ● | potential opposition to the Company’s exploration, development and operational activities; |

| ● | risks related to the Company’s ability to obtain adequate financing for planned exploration and development activities; |

| ● | substantial reliance on the Séguéla Mine, the Lindero Mine, the Yaramoko Mine and the Caylloma Mine for revenues; |

| ● | property title matters; |

| ● | risks relating to the integration of businesses and assets acquired by the Company; |

| ● | failure to meet covenants under the 2024 Credit Facility (as defined herein), or an event of default which may reduce the Company’s liquidity and adversely affect its business; |

| ● | impairments; |

| ● | reliance on key personnel; |

| ● | uncertainty relating to potential conflicts of interest involving the Company’s directors and officers; |

| ● | risks associated with the Company’s reliance on local counsel and advisors and its management and Board (as defined herein) in foreign jurisdictions; |

| ● | adequacy of insurance coverage; |

| ● | operational safety and security risks; |

| ● | risks related to the Company’s compliance with the Sarbanes-Oxley Act; |

| ● | risks related to the foreign corrupt practices regulations and anti-bribery laws; |

| ● | legal proceedings and potential legal proceedings; |

| ● | uncertainties relating to general economic conditions; |

| ● | competition; |

| ● | fluctuations in metal prices; |

| ● | risks associated with entering into commodity forward and option contracts for base metals production; |

ANNUAL INFORMATION FORM |

Page | 3 |

FORTUNA MINING CORP.

| ● | fluctuations in currency exchange rates; |

| ● | tax audits and reassessments; |

| ● | risks related to hedging; |

| ● | sufficiency of monies allotted by the Company for land reclamation and mine closure; |

| ● | risks associated with dependence upon information technology systems, which are subject to disruption, damage, failure and risks with implementation and integration; |

| ● | the possibility of an outbreak of a communicable disease, epidemic or pandemic in areas in which Fortuna operates, which could affect global economic growth and impact the Company’s business, operations, financial condition and share price; |

| ● | uncertainty relating to nature and climate conditions; |

| ● | risks associated with climate change legislation and uncertainty surrounding the interpretation of omnibus Bill C - 59 and the related amendments to the Competition Act (Canada); |

| ● | our ability to manage physical and transition risks related to climate change and successfully adapt our business strategy to a low carbon global economy; |

| ● | the anticipated nature and effect of climate related risks; |

| ● | risks related to the volatility of the trading price of the Company’s common shares (“Common Shares”); |

| ● | dilution from future equity or convertible debt financings; |

| ● | risks related to future insufficient liquidity resulting from a decline in the price of the Common Shares; |

| ● | uncertainty relating to the Company’s ability to pay dividends in the future; |

| ● | risks relating to the market for the Company’s securities; |

| ● | risks relating to the Notes (as defined herein) of the Company; |

| ● | uncertainty relating to the enforcement of U.S. judgments against the Company; and |

| ● | risk factors referred to in the “Risk Factors” section in this AIF, and the documents incorporated by reference herein (if any). |

Forward-looking statements contained in this AIF are based on the assumptions, beliefs, expectations and opinions of management, including but not limited to:

| ● | that all required third party contractual, regulatory and governmental approvals will be obtained and maintained for the exploration, development, construction and production of its properties; |

| ● | the accuracy of the Company's current Mineral Resource and Mineral Reserve estimates; |

| ● | there being no significant disruptions affecting operations, whether relating to labor, supply, power, damage to equipment or any other matter; |

| ● | there being no material and negative impact to the various contractors, suppliers and subcontractors at the Company’s mine sites as a result of the Ukrainian – Russian conflict and the Isarael – Hamas war or otherwise that would impair their ability to provide goods and services; |

| ● | permitting, construction, development and expansion proceeding on a basis consistent with the Company’s current expectations; |

| ● | expected trends and specific assumptions regarding metal prices and currency exchange rates; |

| ● | prices for and availability of fuel, electricity, parts and equipment and other key supplies remaining consistent with current levels; |

| ● | production forecasts meeting expectations; and |

| ● | any investigations, claims, and legal, labor and tax proceedings arising in the ordinary course of business will not have a material effect on the results of operations or financial condition of the Company. |

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. These forward-looking statements are made as of the date of this AIF. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers are cautioned not to place undue reliance on forward-looking statements. Except as required by law, the Company does not assume the obligation to revise or update these forward looking-statements after the date of this document or to revise them to reflect the occurrence of future unanticipated events.

ANNUAL INFORMATION FORM |

Page | 4 |

FORTUNA MINING CORP.

Notice Regarding Non-IFRS Measures

Fortuna’s audited consolidated financial statements for the years ended December 31, 2024 and 2023 (the “2024 Financial Statements”) which are referred to in this AIF have been prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board. However, this AIF includes certain financial measures and ratios that are not defined under IFRS and are not disclosed in the 2024 Financial Statements, including but not limited to: cash cost per ounce of gold sold; cash cost per ounce of silver equivalent; consolidated cash cost per ounce of gold equivalent; AISC per gold ounce sold; and AISC per silver equivalent ounce sold.

These non-IFRS financial measures and non-IFRS ratios are widely reported in the mining industry as benchmarks for performance and are used by management to monitor and evaluate the Company’s operating performance and ability to generate cash. The Company believes that, in addition to financial measures and ratios prepared in accordance with IFRS, certain investors use these non-IFRS financial measures and ratios to evaluate the Company’s performance. However, the measures do not have a standardized meaning under IFRS and may not be comparable to similar financial measures disclosed by other companies. Accordingly, non-IFRS financial measures and non-IFRS ratios should not be considered in isolation or as a substitute for measures and ratios of the Company's performance prepared in accordance with IFRS.

Except as otherwise described below, the Company has calculated these non-IFRS financial measures and non-IFRS ratios consistently for all periods presented.

In the fourth quarter (“Q4”) of 2024, Management elected to include the gain on blue chip swaps in Argentina in the calculation of all-in sustaining costs for both Lindero and the consolidated entity. Management reached this decision after evaluating the peso appreciation relative to the US dollar and the impact it has had on the cost structure of the Lindero Mine as a result of government macro-economic policy.

A blue chip swap is a mechanism provided by the Argentine government to exporters to provide relief to the impact of macro economic policy on their cost structure. These economic policies have resulted in two exchange rates in Argentina, the official exchange rate managed by the central bank and the unofficial ‘blue dollar’ rate received in the public market. Exporters are required to repatriate their US dollars at the official rate which provides fewer pesos for each dollar exchanged compared to the blue dollar rate. This effectively increases the operating costs of the Lindero Mine as fewer pesos are available to meet expenses denominated in local currency. A blue chip swap allows an exporter to use 20% of export proceeds to access the ‘blue dollar’ rate and partially offset this impact.

A blue chip swap is executed through the purchase of a US dollar denominated bond on an Argentine exchange and then immediately selling the peso denominated equivalent which provides a superior exchange rate to the official one. As a blue chip swap is executed through the acquisition and sale of bonds, IFRS requires that it be recognized as an investment gain in the income statement creating a mismatch between the impact to cost of sales from peso appreciation and the relief provided by the government. Management believes including the gains on blue chip swaps in the AISC calculation addresses this mismatch and provides better information to the end user of our financial statements and management’s discussion and analysis as it provides a more accurate view of the sustaining costs of producing an ounce of gold in Argentina.

The gain on blue chip swaps has been included in both the Q4 and full year 2024 AISC calculation for Lindero and on a consolidated basis, as well as all comparable periods as required under National Instrument 52-112 Non-IFRS and Other Financial Measures Disclosures.

To facilitate a better understanding of these measures and ratios as calculated by the Company, descriptions are provided below. In addition, see “Non-IFRS Financial Measures” in the Company’s management’s discussion and analysis for the fiscal year ended December 31, 2024 (“2024 MD&A”), which section on pages 28 to 31 of the 2024 MD&A is incorporated by reference in this AIF, for additional information regarding each non-IFRS financial measure and non-IFRS ratio disclosed in this AIF, including an explanation of their composition; an explanation of how such

ANNUAL INFORMATION FORM |

Page | 5 |

FORTUNA MINING CORP.

measures and ratios provide useful information to an investor and the additional purposes, if any, for which management of Fortuna uses such measures and ratios; and a qualitative reconciliation of each non-IFRS financial measure to the most directly comparable financial measure that is disclosed in the Company’s 2024 Financial Statements. The 2024 MD&A may be accessed on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov under the Company’s profile, Fortuna Mining Corp.

Equivalent Ounces

For the San Jose and Caylloma Mines, production and sales of other metals are treated as a silver equivalent in determining a combined precious metal production or sales unit, commonly referred to as silver equivalent ounces. Silver equivalent ounces are calculated by converting other metal production to its silver equivalent using relative metal/silver metal prices at realized prices and adding the converted metal production expressed in silver ounces to the ounces of silver production. The Lindero, Yaramoko and Séguéla Mines do not make use of an equivalent ounce measure as all material production is gold.

However, consolidated cash costs for production of all mines is provided on a gold equivalent basis. Gold equivalent ounces are calculated by converting other metal production to its gold equivalent using relative metal/gold metal prices at realized prices and adding the converted metal production expressed in gold ounces to the ounces of gold production.

Cash Cost and AISC

In this AIF, the Company has disclosed certain cash cost and AISC figures on a per unit basis, with each such per unit measure being a non-IFRS ratio.

Cash cost is a non-IFRS measure that is an industry-standard method of comparing certain costs on a per unit basis. Cash costs include all direct and indirect operating cash costs related directly to the physical activities of producing metals, including mining and processing costs, third-party refining and treatment charges, on-site general and administrative expenses, applicable production taxes and royalties which are not based on sales or taxable income calculations , net of by-product credits, but are exclusive of the impact of non-cash items that are included as part of the cost of sales that is calculated in the consolidated Income Statement including depreciation and depletion, reclamation, capital, development and exploration costs.

The most directly comparable financial measure to cash cost that is defined in IFRS and disclosed in the Company’s 2024 Financial Statements is cost of sales. Unit based cash cost ratios contained in this AIF include:

| ● | cash cost per ounce of gold sold; |

| ● | cash cost per ounce of payable silver equivalent sold; and |

| ● | consolidated cash cost per ounce of gold equivalent sold |

AISC: The Company, in conjunction with an initiative undertaken within the gold mining industry, has adopted AISC and all-in sustaining cost measures based on guidance published by World Gold Council. The Company conforms its AISC and all-in cash cost definitions to that set out in the guidance and the Company presents the cash cost figures on a sold ounce basis.

AISC is a non-IFRS measure which the Company defines as total production cash costs incurred at the applicable mining operation but excludes mining royalty recognized as income tax within the scope of IAS-12, as well as non-sustaining capital expenditures. Sustaining capital expenditures, corporate selling, general and administrative expenses, gains from blue - chip swaps and Brownfields exploration expenditures are added to the cash cost. AISC is estimated at realized metal prices.

The most directly comparable financial measure to AISC that is defined in IFRS and disclosed in the Company's 2024 Financial Statements is cost of sales. Unit based AISC ratios contained in this AIF include:

ANNUAL INFORMATION FORM |

Page | 6 |

FORTUNA MINING CORP.

| ● | all-in sustaining cash cost per gold ounce sold; |

| ● | all-in sustaining cash cost per ounce of silver equivalent sold; and |

| ● | consolidated all-in sustaining cash cost per ounce of gold equivalent sold |

Cautionary Note to United States Investors Concerning Estimates of Reserves and Resources

The Company is a Canadian “foreign private issuer” as defined in Rule 3b-4 under the Exchange Act and is permitted to prepare the technical information contained herein in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of the securities laws currently in effect in the United States.

Technical disclosure regarding our properties included herein and, in the documents, incorporated herein by reference, if applicable, was prepared in accordance with National Instrument 43-101 — Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. NI 43-101 differs significantly from the disclosure requirements of the Securities and Exchange Commission (the “SEC”) generally applicable to U.S. companies. Accordingly, information contained herein is not comparable to similar information made public by U.S. companies reporting pursuant to SEC disclosure requirements.

Documents Incorporated by Reference

The information provided in this AIF is supplemented by disclosure contained in the documents listed below which are incorporated by reference into this AIF. These documents must be read together with the AIF in order to provide full, true and plain disclosure of all material facts relating to Fortuna. The documents listed below are not contained within or attached to this document. The documents may be accessed on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov under the Company’s profile for Fortuna Mining Corp.

Document |

Effective Date |

Date Filed on |

Document |

Technical Report, Séguéla Gold Mine, Côte d’Ivoire |

December 31, 2023 |

February 16, 2024 |

Technical Report(s) |

Technical Report, Yaramoko Gold Mine, Burkina Faso |

December 31, 2022 |

March 24, 2023 |

Technical Report(s) |

Technical Report, Lindero Mine and Arizaro Project, Argentina |

December 31, 2022 |

March 28, 2023 |

Technical Report(s) |

Technical Report, Caylloma Mine, Peru |

December 31, 2023 |

February 16, 2024 |

Technical Report(s) |

Scientific and Technical Information

Eric Chapman, Senior Vice President of Technical Services of the Company, is a “Qualified Person” as defined by NI 43-101. Mr. Chapman is responsible for ensuring that the technical information contained in this AIF is an accurate summary of the original reports and data provided to or developed by the Company and he has reviewed and approved the scientific and technical information contained in this AIF.

Currency

Unless otherwise noted, all dollar amounts in this AIF are expressed in United States dollars. References to “$” or “US$” in this AIF are to United States dollars and references to CAD$ are to Canadian dollars.

ANNUAL INFORMATION FORM |

Page | 7 |

FORTUNA MINING CORP.

CORPORATE STRUCTURE

Name, Address and Incorporation

The Company was incorporated on September 4, 1990 pursuant to the Company Act (British Columbia) under the name Jopec Resources Ltd. and subsequently transitioned under the Business Corporations Act (British Columbia). The Company changed its name to Fortuna Ventures Inc. on February 3, 1999, on June 28, 2005 to Fortuna Silver Mines Inc., and on June 20, 2024 to Fortuna Mining Corp.

The management head office of the Company is located at Piso 5, Av. Jorge Chávez #154, Miraflores, Lima, Peru. The corporate head office of the Company is located at 1111 Melville Street, Suite 820, Vancouver, BC V6E 3V6. The registered office of the Company is located at 1133 Melville Street, Suite 3500, Vancouver, BC V6E 4E5.

Intercorporate Relationships

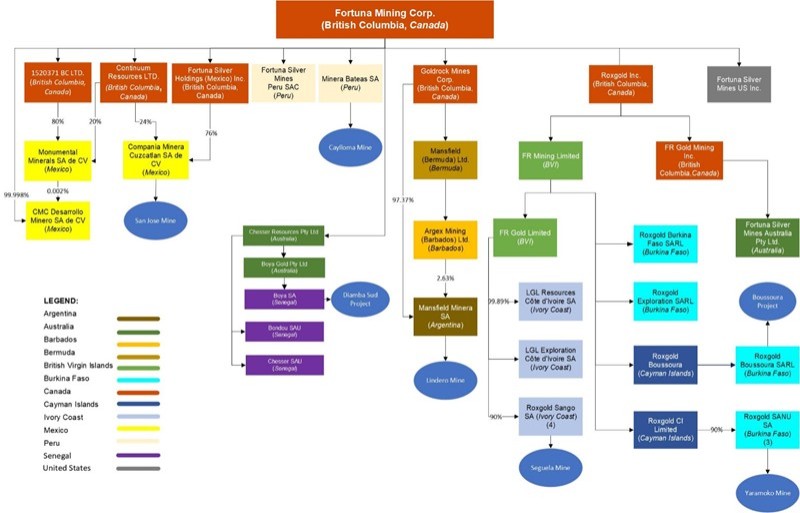

The chart below illustrates the Company’s intercorporate relationships with its subsidiaries as at the date of this AIF, including the name, jurisdiction of incorporation and the Company’s respective percentage ownership of each subsidiary:

Notes:

1. |

In some jurisdictions where the Company operates, laws require that a company operating mineral properties must have more than one shareholder. For those jurisdictions, a nominal interest may be held by an individual or other affiliated entity and this may not be represented on the above chart. |

2. |

All ownership of subsidiaries is 100% unless otherwise indicated. |

3. |

10% of the issued and outstanding shares of Roxgold Sanu S.A. are held by the State of Burkina Faso |

4. |

10% of the issued and outstanding shares of Roxgold Sango S.A. are held by the State of Côte d’Ivoire. |

ANNUAL INFORMATION FORM |

Page | 8 |

FORTUNA MINING CORP.

GENERAL DEVELOPMENT OF THE BUSINESS

Business of the Company

Fortuna is engaged in precious and base metals mining and related activities in Latin America and West Africa, including exploration, extraction, and processing. The Company’s principal products are gold and silver, although it also produces and sells lead and zinc.

As at December 31, 2024, Fortuna:

| ● | operates the Lindero open pit gold mine (the “Lindero Mine”) (100% ownership) in northern Argentina; |

| ● | operates the Yaramoko underground gold mine (the “Yaramoko Mine”) (90% ownership) in southwestern Burkina Faso; |

| ● | operates the underground Caylloma silver, lead and zinc mine (the “Caylloma Mine”) (100% ownership) in southern Peru, and |

| ● | operates the Séguéla open pit gold mine (the “Séguéla Mine”) (90% ownership) in northwestern Côte d’Ivoire. |

Also as at December 31, 2024, Fortuna operated the underground San Jose silver and gold mine (the "San Jose Mine") in southern Mexico. Due to the pending exhaustion of its Mineral Reserves, the San Jose Mine was placed on care and maintenance prior to the year end, as it was scheduled to commence a progressive closure process in early 2025. See "2025 Recent Developments" herein.

The Company also has various Greenfields exploration properties at different stages of development in Côte d’Ivoire, Mexico, and Senegal.

Three-Year History and Recent Developments

Over the three most recently completed financial years, the significant events described below contributed to the development of the Company’s business.

2022 Developments

One of the Company’s main focuses for 2022 was the construction of the mine at Séguéla. Construction at the Séguéla Project advanced during 2022 in accordance with the project timeline and budget, despite worldwide supply chain challenges. The Séguéla Project was 29% complete at the end of 2021 and by the end of January 2023 it was approximately 90% complete.

On March 15, 2022, the Company announced a maiden inferred mineral resource estimate for the Sunbird discovery located at the Séguéla Project. It was estimated that the Sunbird deposit contains an inferred mineral resource of 3.4 million tonnes at an average grade of 3.16 g/t gold containing 350,000 gold ounces. The inferred mineral resource does not materially change the existing mineral resource estimate at Séguéla.

In April 2022, the Company disclosed its commitments towards the reduction of GHG emissions and the transition to a lower carbon economy under a formal Climate Change Position Statement.

On May 2, 2022, the Company initiated a share repurchase program to purchase up to 5% of its issued and outstanding Common Shares, expiring on the earlier of May 1, 2023 and the date on which Fortuna has acquired the maximum number of Common Shares allowable under the Normal Course Issuer Bid (“NCIB”) or the date on which the Company otherwise decides not to make any further repurchases under the NCIB. From the commencement of the share repurchase program to December 31, 2022, in accordance with the Company’s NCIB, the Company re-purchased an aggregate of 2,201,404 Common Shares at a weighted average price of $2.69 per share via open market purchases through the facilities of the New York Stock Exchange (“NYSE”) for a total repurchase value of approximately $5.9 million, all of which shares were subsequently returned to treasury and cancelled. No share

ANNUAL INFORMATION FORM |

Page | 9 |

FORTUNA MINING CORP.

repurchases under the NCIB were made in 2023. See “2024 Developments” regarding share repurchases made in 2024 under the NCIB.

Effective June 27, 2022, the Board of Directors of the Company (the “Board”) approved the appointment of Ms. Salma Seetaroo as an additional director of the Company. Ms. Seetaroo brings her skills and experience in commodities, financing, investment banking, and project development in West Africa. She has spent the last 17 years working on debt, equity, and special situations investments in Africa as an investment banker.

On August 17, 2022, the Company announced the voluntary resignation of Paul Criddle from the position of Chief Operating Officer – West Africa effective September 30, 2022. David Whittle, formerly the Vice-President Operations – West Africa, assumed the role of Chief Operating Officer – West Africa effective October 1, 2022.

On December 5, 2022, the Company announced that additional exploration drilling at the Sunbird deposit has resulted in an upgraded mineral resource estimate, including a maiden indicated mineral resource of 3.2 million tonnes at an average grade of 2.66 g/t gold containing 279,000 ounces and an inferred mineral resource of 4.2 million tonnes at an average grade of 3.73 g/t gold containing 506,000 ounces.

On December 15, 2022, the Company announced that it had entered into an amendment to the fourth amended and restated credit agreement (the “2021 Credit Facility”) with a syndicate of banks led by BNP Paribas and including the Bank of Nova Scotia, Bank of Montreal and Societe Generale, which increased the maximum facility amount by US$50 million to US$250 million, but which would step down to US$175 million in November 2024. The facility had a US$50 million accordion option exercisable on or after June 1, 2023 and before October 2024 The maturity date of the 2021 Credit Facility remained unchanged and matures in November 2025. The 2021 Credit Facility was further amended in 2023. See “2023 Developments” below for further details.

2023 Developments

Construction of the Séguéla Mine was completed in mid-2023, on time and on budget, and its first gold pour took place on May 24, 2023, making it the Company’s fifth operating mine.

In August 2023, the Company published (refer to Fortuna news release dated August 8, 2023) an update on exploration activities at the Yaramoko Mine. The Company had completed a drilling program of 29 holes for a total of 7,011 meters, testing the strike and vertical extent of high grade extensions to the Zone 55 mineralization to the west, and limited strike extent testing to the lower east levels of the underground operation.

Zone 55 drilling highlights:

| ● | YRM-22-GCDD-184: 9.6 g/t Au over an estimated true width of 5.5 meters from 254.10 meters |

| ● | YRM-23-GCDD-203: 32.8 g/t Au over an estimated true width of 3.1 meters from 287.90 meters |

| ● | YRM-23-GCDD-205: 13.2 g/t Au over an estimated true width of 4.6 meters from 302.28 meters |

| ● | YRM-23-GCDD-224: 8.9 g/t Au over an estimated true width of 8.2 meters from 120.95 meters |

| ● | YRM-23-GCDD-227: 8.8 g/t Au over an estimated true width of 8.6 meters from 140.10 meters |

Drilling to the west intersected new high grade mineralization beyond the boundary of the 2022 Mineral Resource at Yaramoko, with recent mine development extending approximately 130 meters beyond the previous design. Drilling continued in the second half of 2023 to test the depth potential.

Step-out drilling to the east and at depth also continued to identify the Zone 55 mineralized structure beyond the limits of the 2022 Mineral Resource boundary, with results including drill hole GCDD-224 returning 8.9 g/t Au over a true width of 8.2 meters. Drilling continued in the second half of 2023.

In September 2023, the Company expanded its presence in West Africa with the acquisition (the “Chesser Acquisition”) of all of the issued and outstanding common shares (“Chesser Shares”) of Chesser Resources Limited (“Chesser”) by way of a court-approved scheme of arrangement pursuant to the Australian Corporations Act 2001. Under the terms of the Chesser Acquisition, holders of Chesser Shares received 0.0248 of a Fortuna Common Share

ANNUAL INFORMATION FORM |

Page | 10 |

FORTUNA MINING CORP.

for each Chesser Share held. Upon completion of the Chesser Acquisition, Fortuna issued an aggregate of 15,545,368 Fortuna Common Shares and Chesser became a wholly-owned subsidiary of Fortuna. As a result of the Chesser Acquisition, the Company acquired the Diamba Sud gold exploration project (“Diamba Sud Project”) in Senegal, one of the new and emerging gold discoveries in the region. See “Non-Material Mineral Properties” herein.

In December 2023, the 2021 Credit Facility was further amended to include additional security to the lenders in the form of guarantees and share pledges from the Company’s subsidiaries which indirectly own the Diamba Sud Project in Senegal, acquired pursuant to the Chesser Acquisition. These guarantees are in addition to the guarantees already provided by Fortuna’s operating subsidiaries in Burkina Faso, Côte d’Ivoire, Mexico and Peru.

2024 Developments

The expansion of the leach pad at the Lindero Mine which began in 2024 was the Company’s largest capital expenditure project during the year, with the Company investing $38.7 million in the project in 2024. The leach pad was designed for approximately 93 million tonnes of ore when considering an average bulk density of 1.60 t/m3, and will cover approximately 106 hectares of lined surface. The leach pad is being constructed over three phases. The first phase which covers approximately 49 hectares is complete. Construction on Phase 2 began in 2024 and will increase the total surface by approximately 45 hectares to approximately 94 hectares. The mine started placing the first lift of ore on the new leach pad expansion area in the second half of October 2024. As at December 31, 2024, Phase 2 of the leach pad expansion project was approximately 89% complete, and the project will complete during the first half of 2025. Detailed engineering for Phase 3 of the leach pad which will cover 12 hectares is expected to start in the next two to three years.

On February 8, 2024, the Company announced its target to reduce Scope 1 and Scope 2 GHG emissions by 15% in 2030 compared to “business as usual” forecast GHG emissions if no intervention measures were taken.

In alignment with the Company’s commitment to reduce GHG emissions, in 2024 the Company began the construction of three significant projects:

| ● | a solar plant at the Lindero Mine. The project is expected to result in the development of a Photovoltaic plant and a battery energy storage system, which will be incorporated into the existing diesel generation plant forming a hybrid electric power generation plant. The plant will prioritize the generation of renewable electric energy. As at December 31, 2024, the construction of the solar plant was 44 percent completed, and it is expected to start production in the second half of 2025. |

| ● | the construction of a 6 mega watt photovoltaic solar plant at the Séguéla Mine to provide power during daylight hours and reduce consumption from the grid. The plant is intended to produce up to 30 percent of the mine’s energy requirements. The plant is expected to provide operational cost savings and contribute to the reduction of GHG emissions for the mine. As at December 31, 2024, the project was in the engineering stage and was 25 percent completed. It is expected that the solar plant will be commissioned in the fourth quarter of 2025. |

| ● | the construction of a new cyclone plant at Caylloma. The purpose of the plant is to separate fine and coarse tailings. Coarse tailings will be pumped to the top of the mine area, which will then be used to backfill underground mine workings. Fine tailings will be sent to a tailings storage facility for storage. The cyclone plant will save operational costs, improve safety during operations and reduce GHG emissions by avoiding the use of trucks to haul coarse tailings. The construction of the plant is nearing completion, and is expected to begin operations in the second quarter of 2025. |

On April 1, 2024, the Company exercised its right to acquire one-half of the 1.2% net smelter return royalty at the Séguéla Mine for $10.0 million Australian Dollars pursuant to a royalty agreement with Franco Nevada Corporation dated March 30, 2021.

ANNUAL INFORMATION FORM |

Page | 11 |

FORTUNA MINING CORP.

The Company renewed its NCIB on May 2, 2024 for a further 12-month period. During 2024, the Company repurchased an aggregate of 7,433,015 Common Shares at a weighted average price of $4.59 per share via open market purchases through the facilities of the NYSE for a total repurchase value of approximately $34.1 million, all of which shares were returned to treasury and cancelled.

On June 10, 2024, the Company announced the completion of an offering of 3.75% convertible senior notes (the “Notes”) which raised gross proceeds of $172.5 million (the “Offering”). The initial conversion rate for the Notes is 151.7220 Common Shares per $1,000 principal amount of Notes, equivalent to an initial conversion price of approximately $6.59 per Common Share. Refer to “Description of Capital Structure – Notes” herein.

Immediately prior to the closing of the Offering, the Company issued a notice of redemption in respect of its existing debentures (“Debentures”). As a result, $35.9 million of principal amount of the Debentures were converted into a total of 7,184,000 Common Shares at a conversion rate of $5.00 per Common Share, and the balance of $9.8 million of outstanding principal amount of Debentures were redeemed in cash. An aggregate of $0.4 million was also paid to the Debenture holders for accrued interest.

During 2024, the Company conducted extensive drill programs at the Séguéla Mine property in Côte d’Ivoire (refer to Fortuna news releases dated March 11, June 20, September 10 and December 16, 2024). A total of 163 holes totalling 26,787 meters were drilled at the Kingfisher prospect which remains open for most of the drilled 2-kilometer strike, with the deepest drilling only testing to approximately 250 metres below surface. Mineralization at Kingfisher demonstrates a clear association with the strongly deformed contact zone between a series of felsic intrusives, quartz veining, and host basaltic units. The change in strike orientation along the structure from north-south to north-east coincides with the higher grade, broader mineralization intervals. Mineralization is characterized by silica-biotite-sericite-carbonate alteration and pyrite development within and adjacent to the quartz veining. Two drill rigs will continue working into the second quarter of 2025 to support resource infill drilling for resource conversion as well as drilling for depth and strike extensions. See “2025 Recent Developments” below.

A total of 41 holes totalling 17,909 meters were drilled at the Sunbird prospect at Séguéla. The drill program is designed to infill and extend the current mineralized footprint as part of a program to evaluate underground mining potential, with mineralization remaining open more than 600 meters below surface, or more than 800 meters down plunge from the margin of the planned open pit. The most recent drill hole which stepped out 150 meters to the south of the reported drilling and for which assays are pending, reported more than 15 points of visible gold (VG) associated with extensive alteration and quartz veining over an interval of 28 meters. Drilling will continue into the first half of 2025 to support an updated resource model and underground mining studies. See “2025 Recent Developments” below.

During 2024, the Company completed 363 holes totalling 47,595 meters of drilling at the Diamba Sud Project in Senegal (refer to Fortuna news releases dated March 11, June 25 and September 12, 2024). The current exploration focus is to test and expand some of the previously lightly drilled anomalies, with Western Splay rapidly emerging as the next potential prospect. Encouraging results such as 6.9 g/t Au over an estimated true width of 33.3 meters from 115.4 meters in drill hole DSDD293, and 8.9 g/t Au over an estimated true width of 27.7 meters from 104 meters in drill hole DSR680 highlight the potential.

The focus of the recent program has been to expand the extent of the Western Splay and Kassasoko prospects, as well as testing the margins of the Bougouda and Karakara prospects. Recent results from Western Splay have highlighted the potential for this prospect to continue to grow as the mineralization remains open along strike and at depth.

A detailed review of the overall geological model to further advance the understanding of the mineralization controls was completed in July, improving the understanding of the relationships and linkages between the different prospects, including the nearby Moungoundi and Kassasoko prospects. This revised geological model has identified several additional targets for testing across the property. Results from this program will be incorporated into the ongoing project development work, with the encouraging results from Western Splay and Kassasoko expected to

ANNUAL INFORMATION FORM |

Page | 12 |

FORTUNA MINING CORP.

contribute toward growing the project portfolio and resource base, while also improving confidence in the regional geological understanding.

Effective October 31, 2024, the Company entered into a fifth amended and restated credit agreement (the “2024 Credit Facility”) which reduced its secured revolving credit facility, with a syndicate of banks led by The Bank of Nova Scotia, and including Bank of Montreal, ING Capital LLC and National Bank of Canada. The amended and restated facility agreement reduced the amount of the facility to US$150.0 million from US$250.0 million (the facility would have stepped down to US$175.0 million in November 2024), and increased the uncommitted accordion option from US$50.0 million to US$75.0 million. The 2024 Credit Facility has a term of four years. Lower interest rates across certain levels of the margin grid and lower commitment fees were negotiated under the 2024 Credit Facility. Interest accrues on USBR Loans at the applicable US base rate plus an applicable margin of between 1.25% and 2.25% across all levels of the margin grid, and on Benchmark Loans at the adjusted term SOFR rate for the applicable term plus the applicable margin of between 2.25% and 3.25% across all levels of the margin grid. Commitment fees decreased approximately 0.6% to 0.9% across the margin grid.

The Company’s principal operating subsidiaries in Argentina, Burkina Faso, Côte d’Ivoire and Peru, and their respective direct and indirect holding companies, have guaranteed the obligations of the Company under the 2024 Credit Facility. The Company has pledged all of its assets to secure the payment of its obligations under the amended and restated credit facility, and the Company’s principal operating subsidiary in Peru has pledged all of its respective assets to secure its guarantees. All of the shares in the Company’s principal operating subsidiaries in Burkina Faso, Côte d’Ivoire, Peru and Senegal have also been pledged to secure the obligations owing under the 2024 Credit Facility and the loan documents entered into in connection therewith. In addition, the Company’s principal operating subsidiary in Burkina Faso has also pledged its bank accounts to secure the obligations under its guarantee. All security granted by the Company’s operating subsidiary in Mexico and indirect holding companies under the previous credit facility agreement has been released.

In December 2024, the Company announced (refer to Fortuna news release dated December 10, 2024) updated Mineral Reserves and Mineral Resources at its Séguéla Mine with the discovery of over 500,000 gold ounces of new Inferred Resources. See “Updated Mineral Reserve and Mineral Resource Estimates” herein.

2025 Recent Developments

The San Jose Mine was placed on care and maintenance on December 24, 2024, as the Company decided to enter into a strategic process to divest of this non-core asset. On January 15, 2025, the Company announced that it had entered into a binding agreement with Minas del Balsas S.A. de C.V. (“MdB”), a private Mexican company, for the sale of the San Jose Mine. On March 6, 2025, the Company terminated the sale agreement with MdB and is now continuing with the sale process to divest the asset.

In December 2021, Fortuna’s Mexican subsidiary, Companía Minera Cuzcatlan (“Minera Cuzcatlan”) received a 12-year extension to the term of the environmental impact authorization (“EIA”) for the San Jose Mine. Since that time, Minera Cuzcatlan has been involved in various legal proceedings brought by Secretaria de Medio Ambiente y Recursos Naturales (“SEMARNAT”) which have challenged the extension of the EIA. On February 21, 2025, the SEMARNAT appeals were dismissed by the Mexican Collegiate Court and the extension of the EIA has been confirmed.

In March 2025, the Company announced results of recent exploration drilling at the Séguéla Mine property in Côte d’Ivoire (refer to Fortuna news release dated March 13, 2025). At the Kingfisher deposit, drilling has moved to infilling and improving the resource confidence along the 1-kilometer strike length of the current resource pit, with several notable intersections including 7.2 g/t Au over an estimated true width of 31.5 meters in drill hole SGRC2278.

An additional 100 drill holes, totaling 10,978 meters of a planned 28,000-meter drilling program, have been completed at Kingfisher as part of the resource confidence infill program. Drilling remains ongoing across the current pit-constrained Inferred Resource and will also extend to test the immediate margins, both at depth and along strike, where late 2024 drilling identified several promising intervals intersected after the initial resource estimate was

ANNUAL INFORMATION FORM |

Page | 13 |

FORTUNA MINING CORP.

completed (refer to Fortuna’s news release dated December 16, 2024). The recent drilling at Kingfisher has continued to highlight the widths and grade tenor intersected in the first drilling phase, supporting and refining the geological interpretation. Kingfisher remains open at depth for most of the drilled 2-kilometer strike length, with the deepest drilling testing to only approximately 250 meters below surface.

At the Sunbird deposit, drilling has now extended mineralization approximately 700 meters to the south beyond the limit of the current underground Inferred Resource and some 600 meters below surface. Results from a further 10 holes, totaling 5,120 meters of a planned 12,000-meter drilling program have been received, including an interval of 4.3 g/t Au over a true width of 23.1 meters from 733 meters in drill hole SGRD2215, which is the deepest intersection drilled at Séguéla. The last phase of the current program is intended to step out above and below the current intersection to further refine the geometry and controls on the interpreted mineralized shoot during the second quarter of 2025.

On January 10, 2025, the Government of Côte d’Ivoire revised a portion of the Côte d’Ivoire Mining Code and increased the gold price sliding scale royalty payable to the State by two percent. The royalty now ranges from between 5 percent and 8 percent, depending on the price of gold, and is calculated on the gross revenue from gold produced after deduction of transportation and refining costs.

In July of 2024, the Government of Burkina Faso published a new mining code (the “2024 Burkina Faso Mining Code”) and related local content law in the Official Journal which, among other changes from the prior mining code, provides for an increased interest of the State in the share capital of mining companies from 10 percent to 15 percent and the opening up of mining companies’ share capital to local investors. However, the 2024 Burkina Faso Mining Code provides that existing mining permits and the associated mining conventions remain in force for their current term (not to exceed five years) and continue to be governed by the laws and regulations (including the then version of the mining code) which were in force at the time of their issuance or entry. Notwithstanding the foregoing, the Government has invited existing mining companies to implement the provisions of the 2024 Burkina Faso Mining Code related to the increase in the State’s free carried interest. The Company has agreed to an increase in the State's ownership interest in Roxgold Sanu from 10 percent to 15 percent which is to take effect in 2025. The timing for the implementation of the increase is to be determined.

Subsequent to December 31, 2024 and up to the date of this AIF, in accordance with the Company’s NCIB the Company repurchased an aggregate of 916,900 Common Shares at a weighted average price of $4.54 per share via open market purchases through the facilities of the NYSE for a total repurchase cost of approximately $4.16 million, all of which shares were returned to treasury and cancelled.

Production and Costs From 2022 to 2024

The following table discloses the production and costs of production at each of the Company’s operating mines for fiscal 2022 to 2024 and on a consolidated basis.

|

2024 |

2023 |

2022 |

Lindero, Argentina | |||

Ore placed on pad (t) |

6,367,505 |

6,005,049 |

5,498,064 |

Gold production (oz)1 |

97,287 |

101,238 |

118,418 |

Gold grade (g/t) |

0.62 |

0.64 |

0.81 |

Cash Cost ($/oz Au)5 |

1,051 |

920 |

739 |

AISC ($/oz Au) 5, 6 |

1,793 |

1,444 |

1,140 |

Yaramoko, Burkina Faso | |||

Tonnes milled |

454,969 |

531,578 |

546,651 |

Gold production (oz)2 |

116,206 |

117,711 |

106,108 |

Gold grade (g/t) |

8.21 |

6.81 |

6.37 |

Gold recovery (%) |

98.12 |

98.0 |

97.5 |

Cash Cost ($/oz Au) 5 |

860 |

809 |

840 |

AISC ($/oz Au) 5 |

1,359 |

1,499 |

1,529 |

ANNUAL INFORMATION FORM |

Page | 14 |

FORTUNA MINING CORP.

Séguéla, Côte d’Ivoire4 | |||

Tonnes milled |

1,561,800 |

807,617 |

- |

Gold production (oz)2 |

137,781 |

78,617 |

- |

Gold grade (g/t) |

2.95 |

3.42 |

- |

Gold recovery (%) |

93.0 |

93.9 |

- |

Cash Cost ($/oz Au) 5 |

584 |

357 |

- |

AISC ($/oz Au) 5 |

1,153 |

760 |

- |

San Jose, Mexico | |||

Tonnes milled |

735,591 |

930,200 |

1,029,590 |

Silver production (oz) |

2,548,402 |