UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of report (Date of earliest event reported): May 17, 2022

Oaktree Acquisition Corp. II

(Exact Name of Registrant as Specified in Charter)

| Cayman Islands | 001-39526 | 98-1551592 | ||

|

(State or Other Jurisdiction of Incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

333 South Grand Avenue

28th Floor

Los Angeles, CA 90071

(Address of Principal Executive Offices, and Zip Code)

(213) 830-6300

Registrant’s Telephone Number, Including Area Code

Not Applicable

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☒ | Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

||

| Units, each consisting of one Class A ordinary share, $0.0001 par value, and one-fourth of one redeemable warrant | OACB.U | New York Stock Exchange | ||

| Class A ordinary shares included as part of the units | OACB | New York Stock Exchange | ||

| Warrants included as part of the units, each whole warrant exercisable for one Class A ordinary share at an exercise price of $11.50 | OACB WS | New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2 of this chapter).

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 7.01. | Regulation FD Disclosure. |

Attached as Exhibit 99.1 to this Current Report on Form 8-K and incorporated into this Item 7.01 by reference is the investor presentation that OACB and Alvotech S.A. (each as defined below) has prepared for use in connection with its investor meetings, scheduled for May 18, 2022, related to the proposed business combination of OACB and Alvotech S.A.

The foregoing (including Exhibit 99.1) is being furnished pursuant to Item 7.01 and will not be deemed to be filed for purposes of Section 18 of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise be subject to the liabilities of that section, nor will it be deemed to be incorporated by reference in any filing under the Securities Act or the Exchange Act.

Additional Information

In connection with the proposed business combination (the “Business Combination”) between Oaktree Acquisition Corp. II (“OACB”) and Alvotech Holdings S.A. (“Alvotech S.A.”), OACB and Alvotech (“TopCo”) have filed with the U.S. Securities and Exchange Commission (the “SEC”) a Registration Statement on Form F-4 (the “Registration Statement”) containing a proxy statement of OACB and a preliminary prospectus of TopCo. The Registration Statement has been declared effective by the SEC and OACB is mailing a definitive proxy statement/prospectus related to the proposed Business Combination to its shareholders. This Current Report on Form 8-K does not contain all the information that should be considered concerning the proposed Business Combination and is not intended to form the basis of any investment decision or any other decision in respect of the proposed Business Combination. OACB’s shareholders and other interested persons are advised to read, when available, the preliminary proxy statement/prospectus and the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed Business Combination, as these materials will contain important information about Alvotech S.A., OACB and the proposed Business Combination. When available, the definitive proxy statement/prospectus and other relevant materials for the proposed Business Combination will be mailed to shareholders of OACB as of a record date to be established for voting on the proposed Business Combination. Shareholders of OACB will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a written request to: OACB, 333 South Grand Avenue, 28th Floor, Los Angeles, California 90071.

Participants in the Solicitation

OACB and Alvotech S.A. and their directors and executive officers may be deemed participants in the solicitation of proxies from OACB’s shareholders with respect to the Business Combination. A list of the names of those directors and executive officers and a description of their interests in OACB is contained in OACB’s annual report on Form 10-K for the fiscal year ended December 31, 2021, which was filed with the SEC and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a written request to OACB, 333 South Grand Avenue, 28th Floor, Los Angeles, California 90071. Additional information regarding the interests of such participants will be contained in the proxy statement/prospectus for the proposed Business Combination when available.

TopCo and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of OACB in connection with the proposed Business Combination. A list of the names of such directors and executive officers and information regarding their interests in the proposed Business Combination will be included in the proxy statement/prospectus for the proposed Business Combination when available.

Forward Looking Statements

Certain statements in this Current Report on Form 8-K may be considered “forward-looking statements.” Forward-looking statements generally relate to future events or the future financial operating performance of OACB or Alvotech S.A. For example, Alvotech S.A.’s expectations regarding future growth, results of operations, performance, future capital and other expenditures including the development of critical infrastructure for the global healthcare markets, competitive advantages, business prospects and opportunities including pipeline product development, future plans and intentions, results, level of activities, performance, goals or achievements or other future events; and the potential approval and commercial launch of AVT02. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expect”, “intend”, “will”, “estimate”, “anticipate”, “believe”, “predict”, “potential” or “continue”, or the negatives of these terms or variations of them or similar terminology. Such forward-looking statements are subject to risks, uncertainties, and other factors which could cause actual results to differ materially from those expressed or implied by such forward looking statements. These forward-looking statements are based upon estimates and assumptions that, while considered reasonable by OACB and its management, and Alvotech S.A. and its management, as the case may be, are inherently uncertain and are inherently subject to risks, variability and contingencies, many of which are beyond OACB’s and Alvotech S.A.’s control. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of negotiations and any subsequent definitive agreements with respect to the Business Combination; (2) the outcome of any legal proceedings that may be instituted against OACB, the combined company or others following this announcement of the Business Combination and any definitive agreements with respect thereto; (3) the inability to complete the Business Combination due to the failure to obtain approval of the shareholders of OACB, to obtain financing to complete the Business Combination or to satisfy other conditions to closing; (4) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the Business Combination; (5) the inability to execute final agreement with respect to the loan facility with Sculptor Capital Management on acceptable terms or at all; (6) the inability to consummate the transactions contemplated by the Standby Equity Purchase Agreement by and between TopCo and Yorkville; (7) the ability to meet stock exchange listing standards following the consummation of the Business Combination; (8) the risk that the Business Combination disrupts current plans and operations of Alvotech S.A. as a result of the announcement and consummation of the Business Combination; (9) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitably, maintain key relationships and retain its management and key employees; (10) costs related to the Business Combination; (11) changes in applicable laws or regulations; (12) the possibility that Alvotech S.A. or the combined company may be adversely affected by other economic, business, and/or competitive factors; (13) Alvotech S.A.’s estimates of expenses and profitability; (14) pending litigation related to AVT02; (15) the potential impact of the ongoing COVID-19 pandemic on the FDA’s review timelines, including its ability to complete timely inspection of manufacturing sites; (16) the commercial launch date of AVT02 in the United States or elsewhere, and (17) other risks and uncertainties set forth in the section entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” in OACB’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021 or in other documents filed by OACB with the SEC. There may be additional risks that neither OACB nor Alvotech S.A. presently know or that OACB and Alvotech S.A. currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Nothing in this Current Report on Form 8-K should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. Neither OACB nor Alvotech S.A. undertakes any duty to update these forward-looking statements or to inform the recipient of any matters of which any of them becomes aware of which may affect any matter referred to in this Current Report on Form 8-K. Alvotech S.A. and OACB disclaim any and all liability for any loss or damage (whether foreseeable or not) suffered or incurred by any person or entity as a result of anything contained or omitted from this Current Report on Form 8-K and such liability is expressly disclaimed. The recipient agrees that it shall not seek to sue or otherwise hold Alvotech S.A., OACB or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives liable in any respect for the provision of this Current Report on Form 8-K, the information contained in this Current Report on Form 8-K, or the omission of any information from this Current Report on Form 8-K.

No Offer

This communication is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities pursuant to the proposed transaction or otherwise, nor shall there be any sale of any such securities in any state or jurisdiction in which such offer, solicitation, or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933, as amended.

| Item 9.01. | Financial Statements and Exhibits. |

(d) Exhibits.

| Exhibit |

Description of Exhibit |

|

| 99.1 | Investor Day Presentation, dated May 17, 2022. | |

| 104 | Cover Page Interactive Data File (the cover page XBRL tags are embedded within the inline XBRL document) | |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| OAKTREE ACQUISITION CORP. II | ||||||

| Date: May 17, 2022 | By: | /s/ Zaid Pardesi |

||||

| Name: | Zaid Pardesi | |||||

| Title: | Chief Financial Officer and Head of M&A | |||||

Exhibit 99.1 INVESTOR PRESENTATION May 2022 This investor presentation (this “Presentation”) is for informational purposes only to assist interested parties in making their own evaluation with respect to the proposed business combination (the “Business Combination”) between Oaktree Acquisition Corp.

II (“SPAC”) and Alvotech Holdings S.A. (together with its subsidiaries, the “Company”). The information contained herein does not purport to be all-inclusive and none of SPAC, the Company or their respective affiliates makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained in this Presentation. Neither the Company nor SPAC has verified, or will verify, any part of this Presentation. The recipient should make its own independent investigations and analyses of the Company and its own assessment of all information and material provided, or made available, by the Company, SPAC or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives. This Presentation does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed Business Combination or (ii) an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any security of SPAC, the Company, or any of their respective affiliates. You should not construe the contents of this Presentation as legal, tax, accounting or investment advice or a recommendation. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the information contained herein to make any decision. The distribution of this Presentation may also be restricted by law and persons into whose possession this Presentation comes should inform themselves about and observe any such restrictions. The recipient acknowledges that it is (a) aware that the United States securities laws prohibit any person who has material, non-public information concerning a company from purchasing or selling securities of such company or from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities, and (b) familiar with the Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder (collectively, the Exchange Act ), and that the recipient will neither use, nor cause any third party to use, this Presentation or any information contained herein in contravention of the Exchange Act, including, without limitation, Rule 10b-5 thereunder. This Presentation and information contained herein constitutes confidential information and is provided to you on the condition that you agree that you will hold it in strict confidence and not reproduce, disclose, forward or distribute it in whole or in part without the prior written consent of SPAC and the Company and is intended for the recipient hereof only. This investor presentation supersedes all previous investor presentations delivered in connection with the Business Combination. You should only refer to the information in this version of the investor presentation. Forward-Looking Statements Disclaimer Certain statements in this Presentation may be considered forward-looking statements. Forward-looking statements generally relate to future events or SPAC’s or the Company’s future financial or operating performance. For example, projections of future Revenue and Adjusted EBITDA and other metrics are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expect”, “intend”, “will”, “estimate”, “anticipate”, “believe”, “predict”, “potential” or “continue”, or the negatives of these terms or variations of them or similar terminology. Such forward-looking statements are subject to risks, uncertainties, and other factors which could cause actual results to differ materially from those expressed or implied by such forward looking statements. These forward-looking statements are based upon estimates and assumptions that, while considered reasonable by SPAC and its management, and the Company and its management, as the case may be, are inherently uncertain and are inherently subject to risks, variability and contingencies, many of which are beyond the Company’s control. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of negotiations and any subsequent definitive agreements with respect to the Business Combination; (2) the outcome of any legal proceedings that may be instituted against SPAC, the combined company or others following the announcement of the Business Combination and any definitive agreements with respect thereto; (3) the inability to complete the Business Combination due to the failure to obtain approval of the shareholders of SPAC, to obtain financing to complete the Business Combination or to satisfy other conditions to closing; (4) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the Business Combination; (5) the ability to meet stock exchange listing standards following the consummation of the Business Combination; (6) the risk that the Business Combination disrupts current plans and operations of the Company as a result of the announcement and consummation of the Business Combination; (7) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitably, maintain key relationships and retain its management and key employees; (8) costs related to the Business Combination; (9) changes in applicable laws or regulations; (10) the possibility that the Company or the combined company may be adversely affected by other economic, business, and/or competitive factors; (11) the Company’s estimates of expenses and profitability; and (12) other risks and uncertainties set forth in the section entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” in SPAC’s final prospectus relating to its initial public offering dated September 16, 2020, in the registration statement on Form F-4, initially filed by the Company with the SEC on December 20, 2021 (as amended or supplemented through the date hereof, the Registration Statement ) or in other documents filed by SPAC or the Company with the SEC. There may be additional risks that neither SPAC nor the Company presently know or that SPAC and the Company currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Nothing in this Presentation should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. Neither SPAC nor the Company undertakes any duty to update these forward-looking statements or to inform the recipient of any matters of which any of them becomes aware of which may affect any matter referred to in this Presentation. The Company and SPAC disclaim any and all liability for any loss or damage (whether foreseeable or not) suffered or incurred by any person or entity as a result of anything contained or omitted from this Presentation and such liability is expressly disclaimed. The recipient agrees that it shall not seek to sue or otherwise hold the Company, SPAC or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives liable in any respect for the provision of this Presentation, the information contained in this Presentation, or the omission of any information from this Presentation. Only those particular representations and warranties of the Company or SPAC made in a definitive written agreement regarding the transaction (which will not contain any representation or warranty relating to this Presentation) when and if executed, and subject to such limitations and restrictions as specified therein, shall have any legal effect. Non-GAAP Financial Measures This Presentation includes projections of certain financial measures not presented in accordance with generally accepted accounting principles (“GAAP”) including, but not limited to, Adjusted EBITDA and certain ratios and other metrics derived therefrom. These non-GAAP financial measures are not measures of financial performance in accordance with GAAP and may exclude items that are significant in understanding and assessing the Company’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to net income, cash flows from operations or other measures of profitability, liquidity or performance under GAAP. You should be aware that the Company’s presentation of these measures may not be comparable to similarly-titled measures used by other companies. The Company believes these non-GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to the Company’s financial condition and results of operations. The Company believes that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends in and in comparing the Company’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. Due to the high variability and difficulty in making accurate forecasts and projections of some of the information excluded from these projected measures, together with some of the excluded information not being ascertainable or accessible, the Company is unable to quantify certain amounts that would be required to be included in the most directly comparable GAAP financial measures without unreasonable effort. Consequently, no disclosure of estimated comparable GAAP measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included. For the same reasons, the Company is unable to address the probable significance of the unavailable information, which could be material to future results.

Use of Projections This Presentation contains financial forecasts with respect to the Company’s projected financial results, including Revenue and Adjusted EBITDA, for the Company's fiscal years 2021, 2022, 2025 and from 2025-2030. The Company's independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this Presentation. These projections should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this Presentation should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved. Neither of the placement agents, in any capacity, has warranted or warrants the accuracy, reliability, appropriateness or completeness of the prospective financial information contained herein to anyone. Industry and Market Data This presentation also contains estimates and other statistical data made by independent parties and by the Company relating to market size and growth and other data about the Company’s industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions, and estimates of the future performance of the markets in which the Company operates are necessarily subject to a high degree of uncertainty and risk. This presentation concerns drugs that are in development and which have not yet been approved for marketing by the U.S. Food and Drug Administration (FDA). No representation is made as to the safety or effectiveness of any of the products in development, nor for any products which may have applications pending before the FDA. Any trademarks, servicemarks, trade names and copyrights of the Company and other companies contained in this Presentation are the property of their respective owners. Disclaimer Additional Information In connection with the proposed Business Combination, the parties have filed the Registration Statement with the SEC containing a preliminary proxy statement of SPAC and a preliminary prospectus of the combined company, and after the registration statement is declared effective, SPAC will mail a definitive proxy statement/prospectus relating to the proposed Business Combination to its shareholders. This Presentation does not contain all the information that should be considered concerning the proposed Business Combination and is not intended to form the basis of any investment decision or any other decision in respect of the Business (Cont’d) Combination. SPAC’s shareholders and other interested persons are advised to read the preliminary proxy statement/prospectus and the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed Business Combination, as these materials will contain important information about SPAC, the Company and the Business Combination. When available, the definitive proxy statement/prospectus and other relevant materials for the proposed Business Combination will be mailed to shareholders of SPAC as of a record date to be established for voting on the proposed Business Combination. Shareholders can obtain copies of the preliminary proxy statement/prospectus and will be able to obtain copies of the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to: Oaktree Acquisition Corp. II, 333 South Grand Avenue, 28th Floor, Los Angeles, CA 90071. Participants in the Solicitation SPAC and its directors and executive officers may be deemed participants in the solicitation of proxies from SPAC’s shareholders with respect to the proposed Business Combination. A list of the names of those directors and executive officers and a description of their interests in SPAC is contained in SPAC’s final prospectus related to its initial public offering dated September 16, 2020, which was filed with the SEC and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to Oaktree Acquisition Corp. II, 333 South Grand Avenue, 28th Floor, Los Angeles, CA 90071. Additional information regarding the interests of such participants is contained in the Registration Statement. The Company and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of SPAC in connection with the proposed Business Combination. A list of the names of such directors and executive officers and information regarding their interests in the proposed Business Combination is contained in the Registration Statement. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. The Company and SPAC reserve the right to negotiate with one or more parties and to enter into a definitive agreement relating to the transaction at any time and without prior notice to the recipient or any other person or entity. The Company and SPAC also reserve the right, at any time and without prior notice and without assigning any reason therefor, (i) to terminate the further participation by the recipient or any other person or entity in the consideration of, and proposed process relating to, the transaction, (ii) to modify any of the rules or procedures relating to such consideration and proposed process and (iii) to terminate entirely such consideration and proposed process. No representation or warranty (whether express or implied) has been made by the Company, the SPAC or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives with respect to the proposed process or the manner in which the proposed process is conducted, and the recipient disclaims any such representation or warranty. The recipient acknowledges that the Company, SPAC and their respective directors, officers, employees, affiliates, agents, advisors or representatives are under no obligation to accept any offer or proposal by any person or entity regarding the transaction. None of the Company, SPAC or any of their respective directors, officers, employees, affiliates, agents, advisors or representatives has any legal, fiduciary or other duty to any recipient with respect to the manner in which the proposed process is conducted.

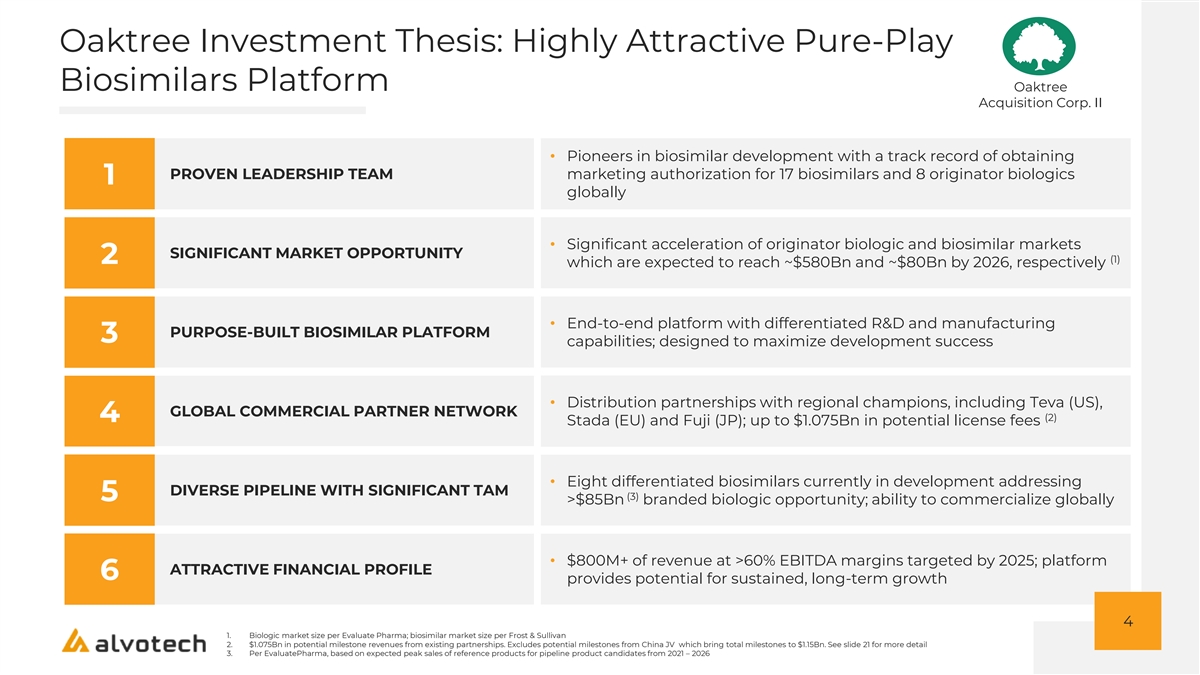

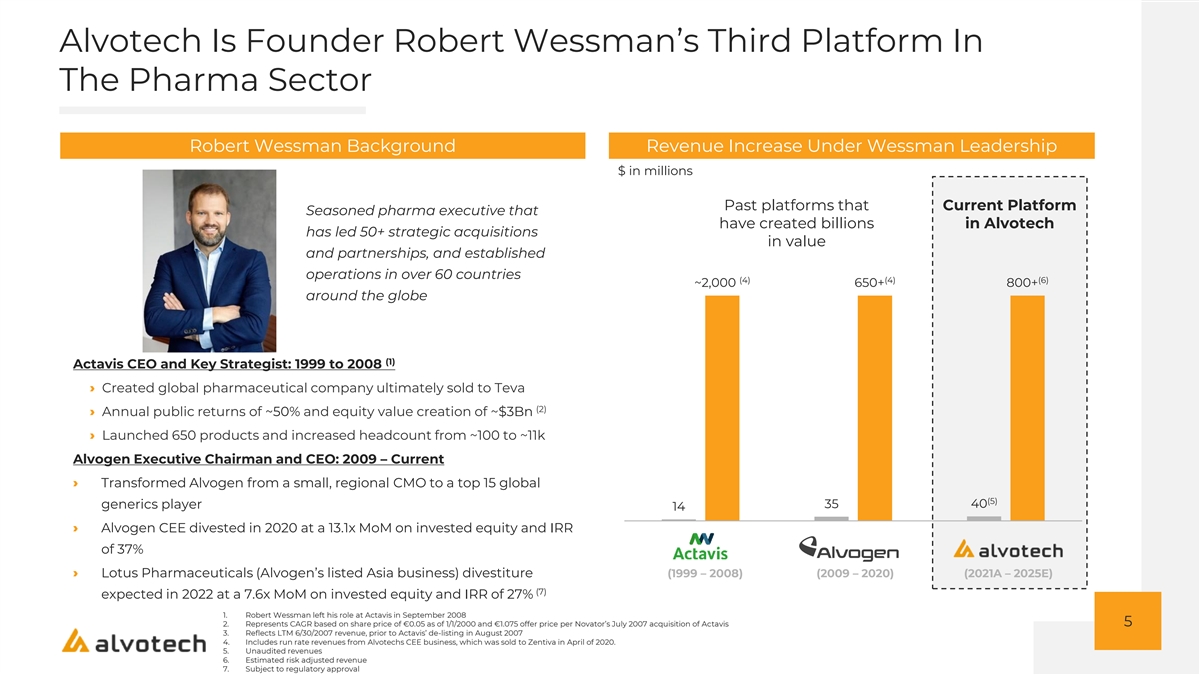

Oaktree Investment Thesis: Highly Attractive Pure-Play Biosimilars Platform Oaktree Acquisition Corp. II • Pioneers in biosimilar development with a track record of obtaining PROVEN LEADERSHIP TEAM marketing authorization for 17 biosimilars and 8 originator biologics 1 globally • Significant acceleration of originator biologic and biosimilar markets SIGNIFICANT MARKET OPPORTUNITY (1) 2 which are expected to reach ~$580Bn and ~$80Bn by 2026, respectively • End-to-end platform with differentiated R&D and manufacturing PURPOSE-BUILT BIOSIMILAR PLATFORM 3 capabilities; designed to maximize development success • Distribution partnerships with regional champions, including Teva (US), GLOBAL COMMERCIAL PARTNER NETWORK (2) 4 Stada (EU) and Fuji (JP); up to $1.075Bn in potential license fees • Eight differentiated biosimilars currently in development addressing DIVERSE PIPELINE WITH SIGNIFICANT TAM (3) 5 >$85Bn branded biologic opportunity; ability to commercialize globally • $800M+ of revenue at >60% EBITDA margins targeted by 2025; platform ATTRACTIVE FINANCIAL PROFILE 6 provides potential for sustained, long-term growth 4 1. Biologic market size per Evaluate Pharma; biosimilar market size per Frost & Sullivan 2. $1.075Bn in potential milestone revenues from existing partnerships. Excludes potential milestones from China JV which bring total milestones to $1.15Bn. See slide 21 for more detail 3. Per EvaluatePharma, based on expected peak sales of reference products for pipeline product candidates from 2021 – 2026 Alvotech Is Founder Robert Wessman’s Third Platform In The Pharma Sector Robert Wessman Background Revenue Increase Under Wessman Leadership $ in millions Past platforms that Current Platform Seasoned pharma executive that have created billions in Alvotech has led 50+ strategic acquisitions in value and partnerships, and established operations in over 60 countries (4) (4) (6) ~2,000 650+ 800+ around the globe (1) Actavis CEO and Key Strategist: 1999 to 2008 › Created global pharmaceutical company ultimately sold to Teva (2) › Annual public returns of ~50% and equity value creation of ~$3Bn › Launched 650 products and increased headcount from ~100 to ~11k Alvogen Executive Chairman and CEO: 2009 – Current › Transformed Alvogen from a small, regional CMO to a top 15 global (5) 40 generics player 35 14 › Alvogen CEE divested in 2020 at a 13.1x MoM on invested equity and IRR of 37% › Lotus Pharmaceuticals (Alvogen’s listed Asia business) divestiture (1999 – 2008) (2009 – 2020) (2021A – 2025E) (7) expected in 2022 at a 7.6x MoM on invested equity and IRR of 27% 1.

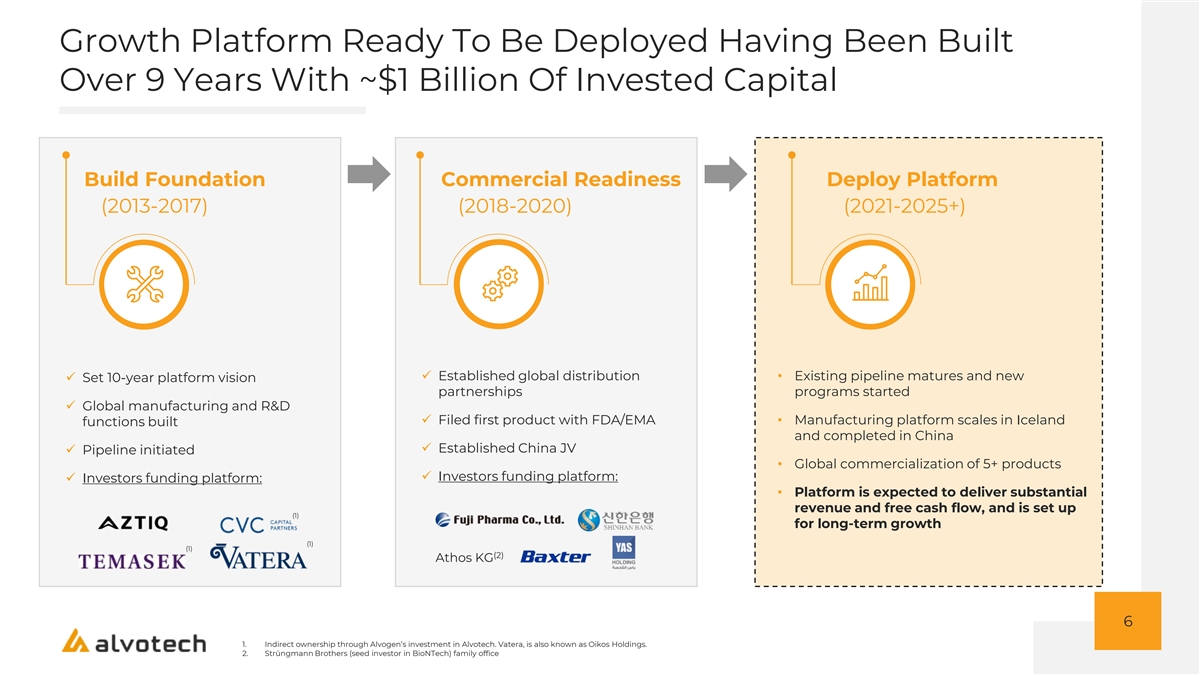

Robert Wessman left his role at Actavis in September 2008 5 2. Represents CAGR based on share price of €0.05 as of 1/1/2000 and €1.075 offer price per Novator’s July 2007 acquisition of Actavis 3. Reflects LTM 6/30/2007 revenue, prior to Actavis’ de-listing in August 2007 4. Includes run rate revenues from Alvotechs CEE business, which was sold to Zentiva in April of 2020. 5. Unaudited revenues 6. Estimated risk adjusted revenue 7. Subject to regulatory approval Growth Platform Ready To Be Deployed Having Been Built Over 9 Years With ~$1 Billion Of Invested Capital Build Foundation Commercial Readiness Deploy Platform (2013-2017) (2018-2020) (2021-2025+) ✓ Established global distribution • Existing pipeline matures and new ✓ Set 10-year platform vision partnerships programs started ✓ Global manufacturing and R&D ✓ Filed first product with FDA/EMA• Manufacturing platform scales in Iceland functions built and completed in China ✓ Established China JV ✓ Pipeline initiated • Global commercialization of 5+ products ✓ Investors funding platform: ✓ Investors funding platform: • Platform is expected to deliver substantial revenue and free cash flow, and is set up (1) for long-term growth (1) (1) (2) Athos KG 6 1.

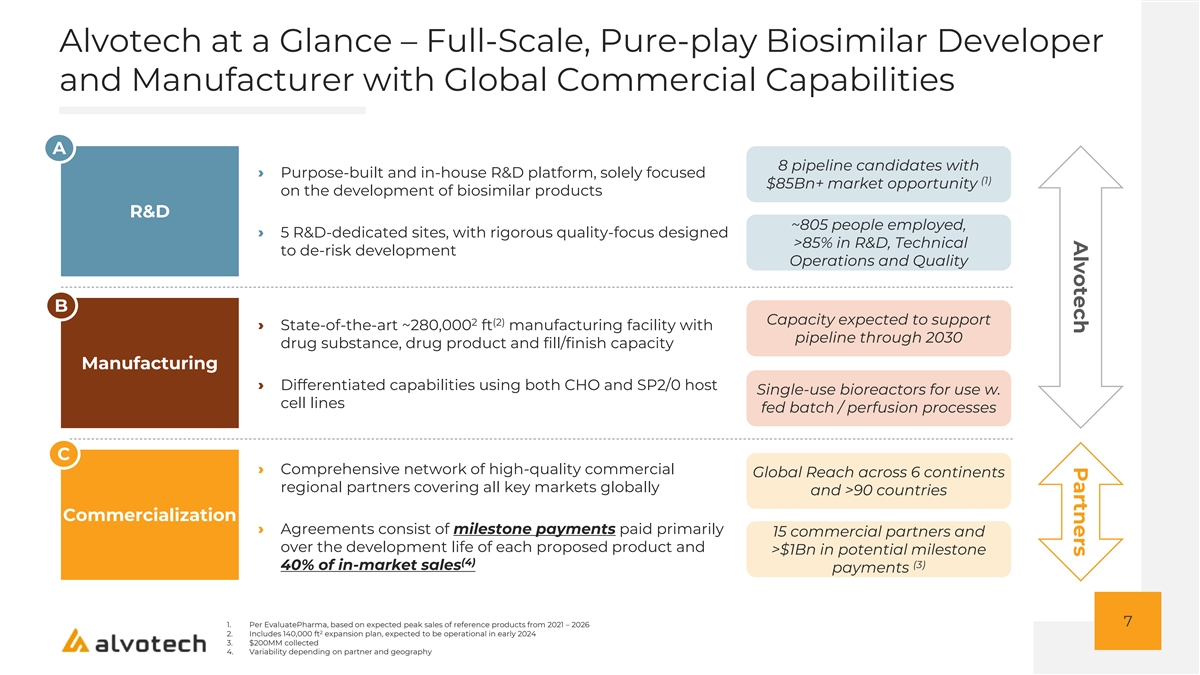

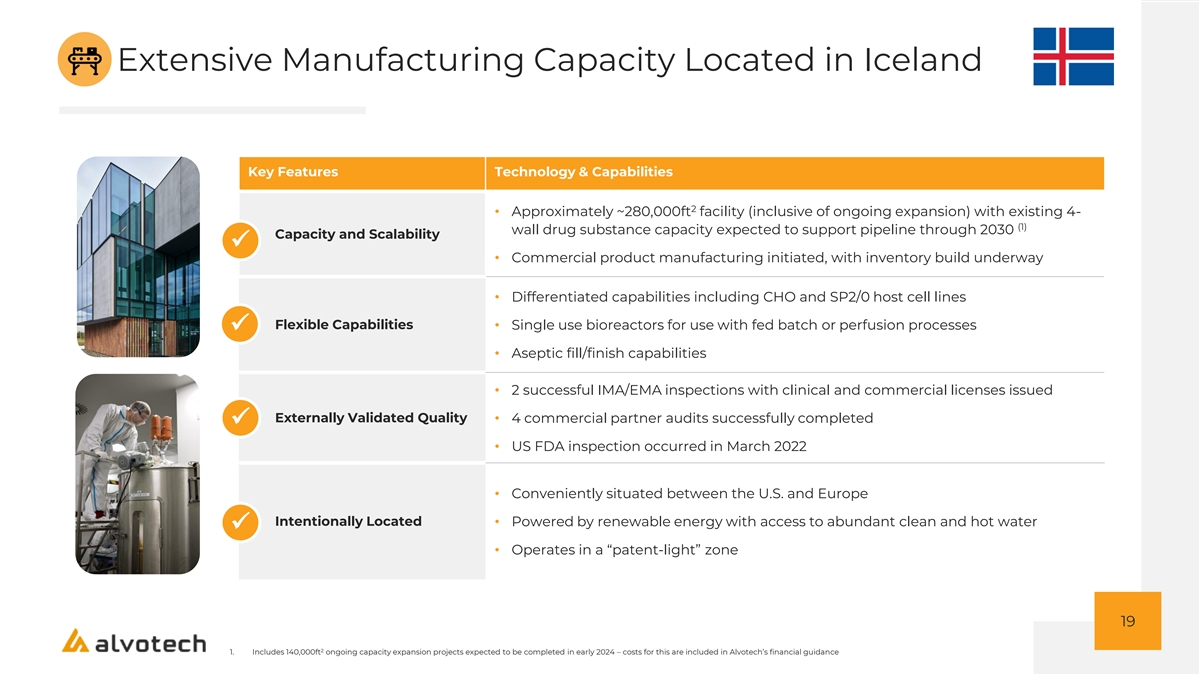

Indirect ownership through Alvogen’s investment in Alvotech. Vatera, is also known as Oikos Holdings. 2. Strüngmann Brothers (seed investor in BioNTech) family office Alvotech Partners Alvotech at a Glance – Full-Scale, Pure-play Biosimilar Developer and Manufacturer with Global Commercial Capabilities A 8 pipeline candidates with › Purpose-built and in-house R&D platform, solely focused (1) $85Bn+ market opportunity on the development of biosimilar products R&D ~805 people employed, › 5 R&D-dedicated sites, with rigorous quality-focus designed >85% in R&D, Technical to de-risk development Operations and Quality B Capacity expected to support 2 (2) › State-of-the-art ~280,000 ft manufacturing facility with pipeline through 2030 drug substance, drug product and fill/finish capacity Manufacturing › Differentiated capabilities using both CHO and SP2/0 host Single-use bioreactors for use w.

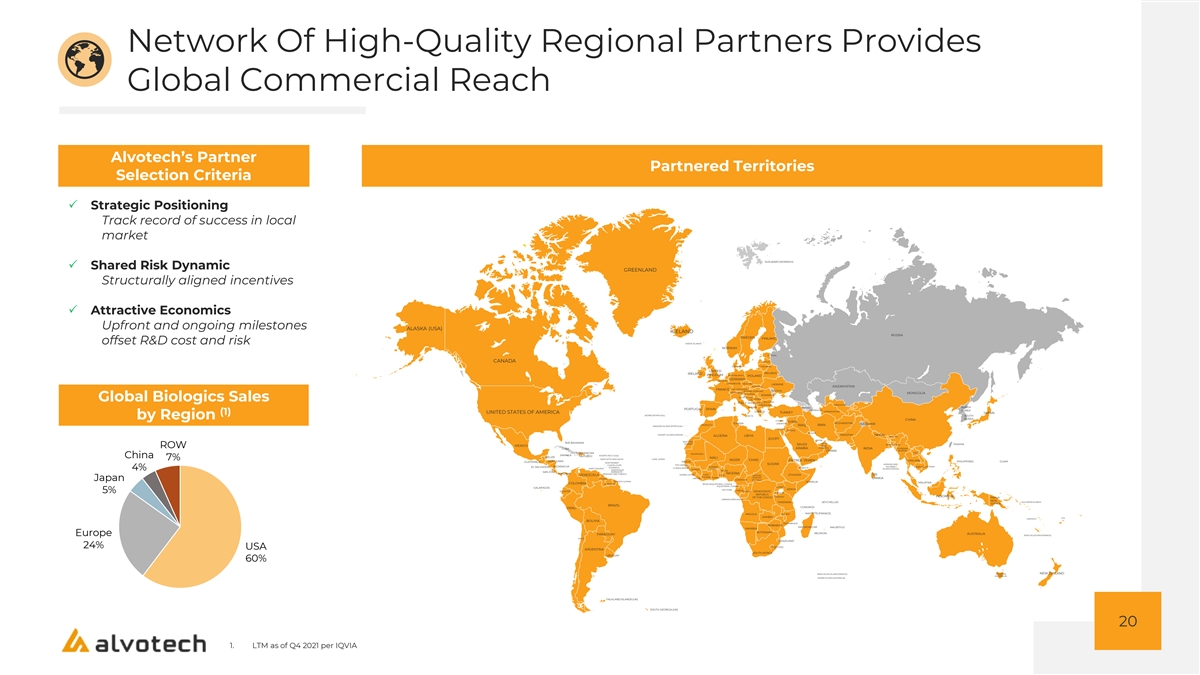

cell lines fed batch / perfusion processes C › Comprehensive network of high-quality commercial Global Reach across 6 continents regional partners covering all key markets globally and >90 countries Commercialization › Agreements consist of milestone payments paid primarily 15 commercial partners and over the development life of each proposed product and >$1Bn in potential milestone (4) (3) 40% of in-market sales payments 7 1. Per EvaluatePharma, based on expected peak sales of reference products from 2021 – 2026 2 2. Includes 140,000 ft expansion plan, expected to be operational in early 2024 3. $200MM collected 4. Variability depending on partner and geography Proven & Highly Experienced Management Team Having Successfully Developed 17 Biosimilars 30 20 20 15 20 MARK LEVICK, JOSEPH E. JOEL MORALES, ANIL OKAY, MING LI, MCCLELLAN, Chief Chief Executive Chief Financial Chief Strategy Commercial Officer Chief Scientific Officer Officer Officer Officer 20 15 29 20 15 TANYA ZHAROV, SEAN GASKELL, REEM MALKI, PHILIP ANDREW ROBERTS, Chief Technical CARAMANICA, Deputy CEO Chief Quality Officer Chief Portfolio Officer Officer Chief IP Counsel, Deputy General Counsel 9 Years of Experience Today’s Presenters

PROVEN LEADERSHIP TEAM

SIGNIFICANT MARKET OPPORTUNITY

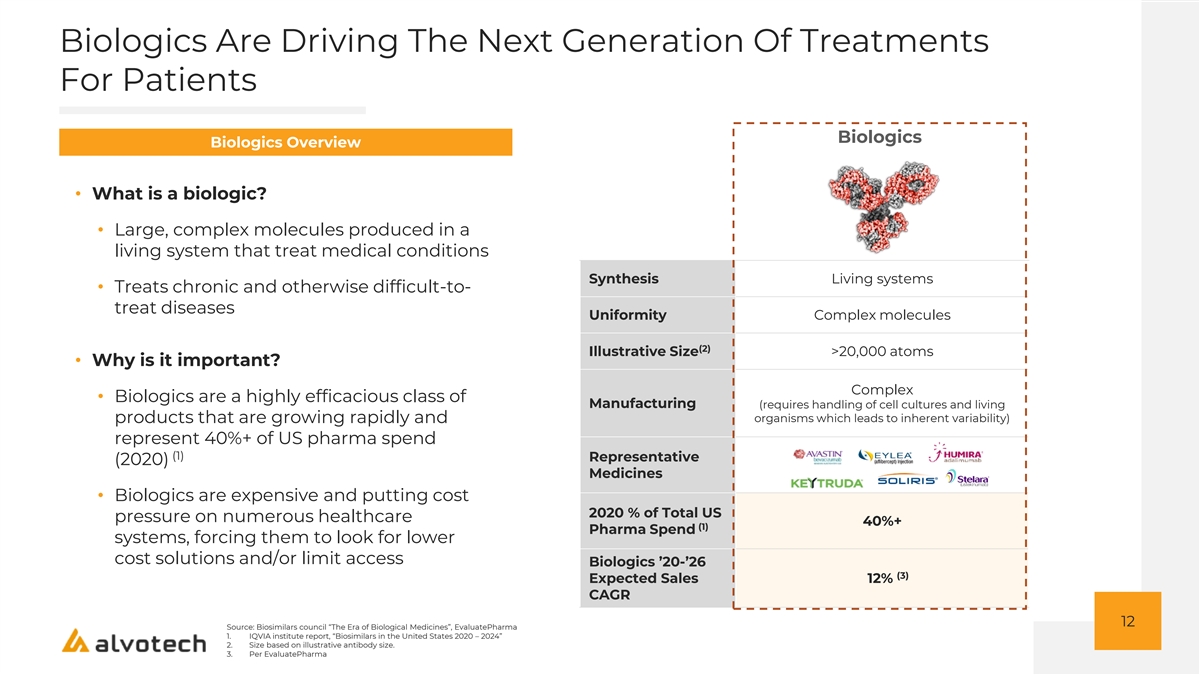

Highly Aligned Social And Corporate Purpose Corporate Purpose Social Purpose Alvotech is dedicated to Alvotech aims to be the making patients’ lives leading supplier of better by improving access biosimilars globally to affordable biosimilar medicines and the sustainability Our corporate purpose is aligned with our social of healthcare systems purpose 11 Biologics Are Driving The Next Generation Of Treatments For Patients Biologics Biologics Overview • What is a biologic? • Large, complex molecules produced in a living system that treat medical conditions Synthesis Living systems • Treats chronic and otherwise difficult-to- treat diseases Uniformity Complex molecules (2) Illustrative Size >20,000 atoms • Why is it important? Complex • Biologics are a highly efficacious class of Manufacturing (requires handling of cell cultures and living organisms which leads to inherent variability) products that are growing rapidly and represent 40%+ of US pharma spend (1) Representative (2020) Medicines • Biologics are expensive and putting cost 2020 % of Total US pressure on numerous healthcare 40%+ (1) Pharma Spend systems, forcing them to look for lower cost solutions and/or limit access Biologics ’20-’26 (3) Expected Sales 12% CAGR 12 Source: Biosimilars council “The Era of Biological Medicines”, EvaluatePharma 1.

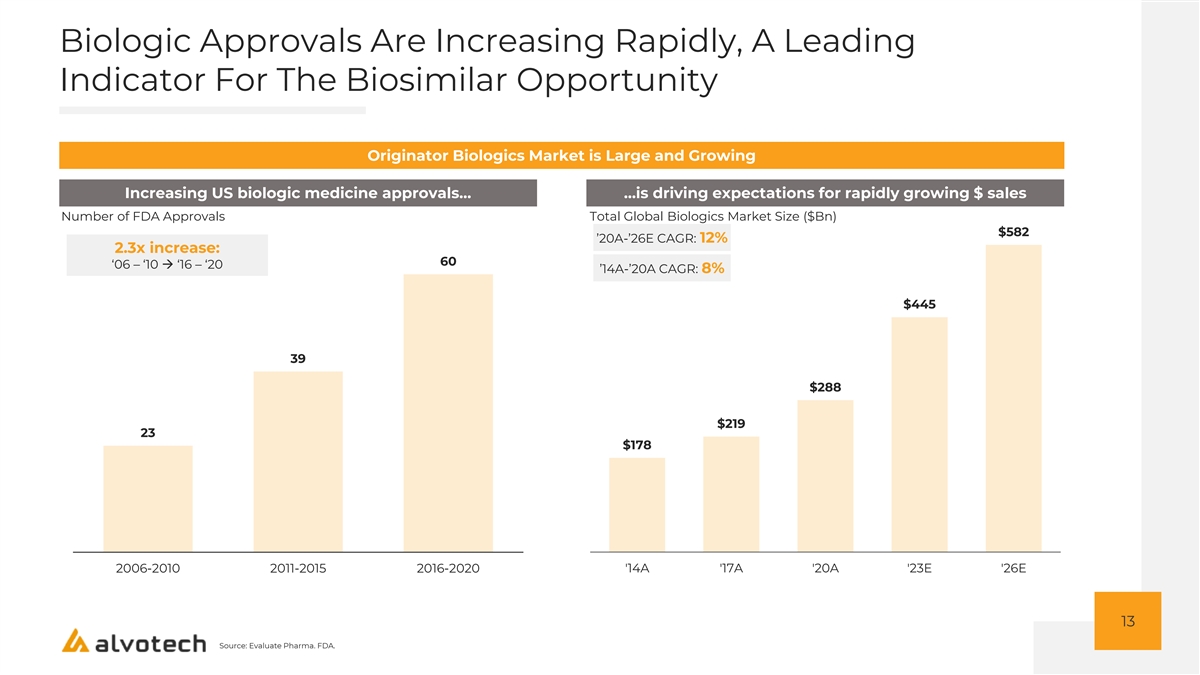

IQVIA institute report, “Biosimilars in the United States 2020 – 2024” 2. Size based on illustrative antibody size. 3. Per EvaluatePharma Biologic Approvals Are Increasing Rapidly, A Leading Indicator For The Biosimilar Opportunity Originator Biologics Market is Large and Growing Increasing US biologic medicine approvals… …is driving expectations for rapidly growing $ sales Number of FDA Approvals Total Global Biologics Market Size ($Bn) $582 ’20A-’26E CAGR: 12% 2.3x increase: 60 ‘06 – ‘10 → ‘16 – ‘20 ’14A-’20A CAGR: 8% $445 39 $288 $219 23 $178 2006-2010 2011-2015 2016-2020 '14A '17A '20A '23E '26E 13 Source: Evaluate Pharma.

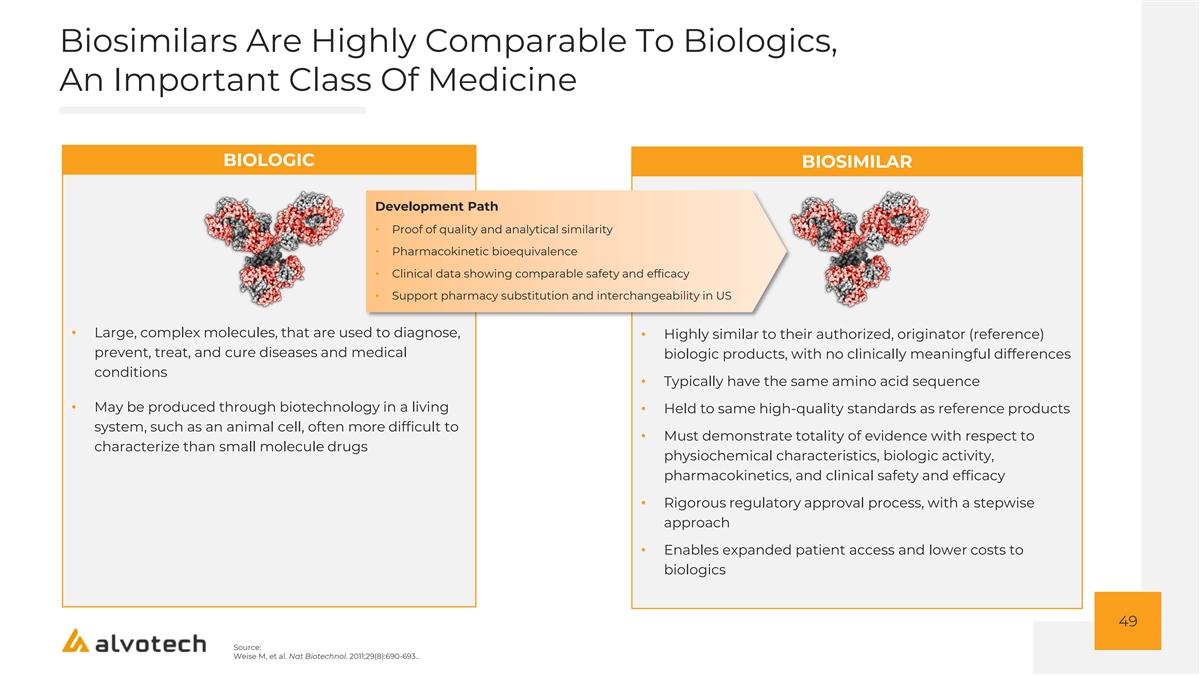

FDA.

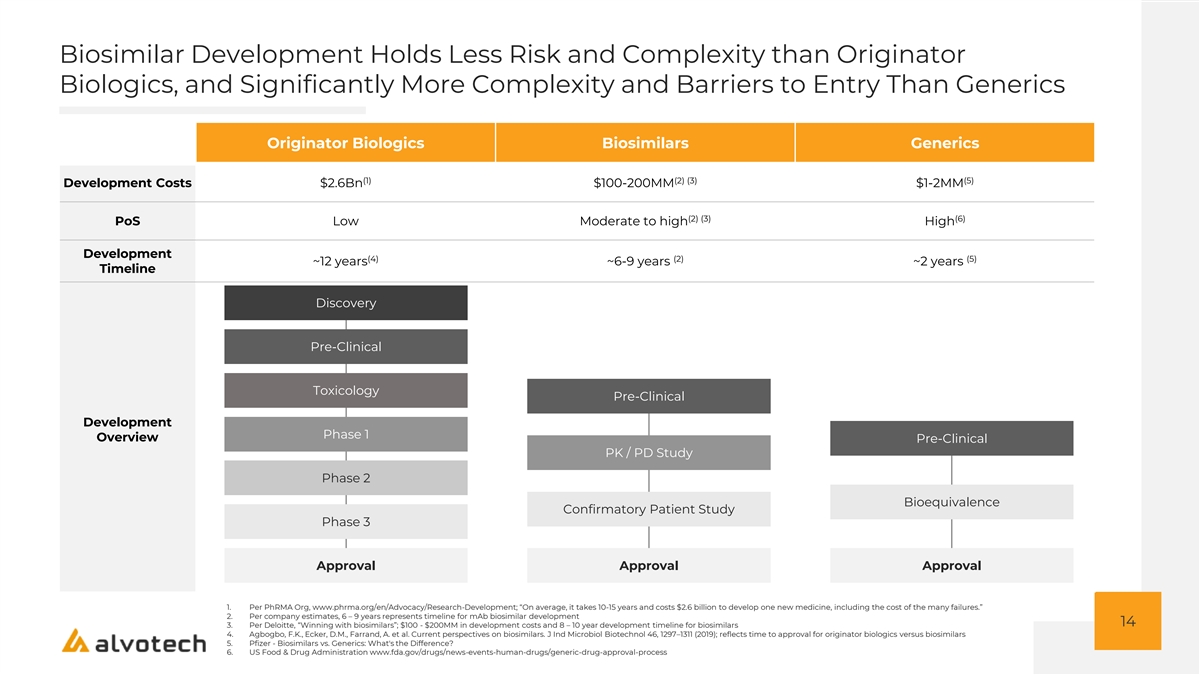

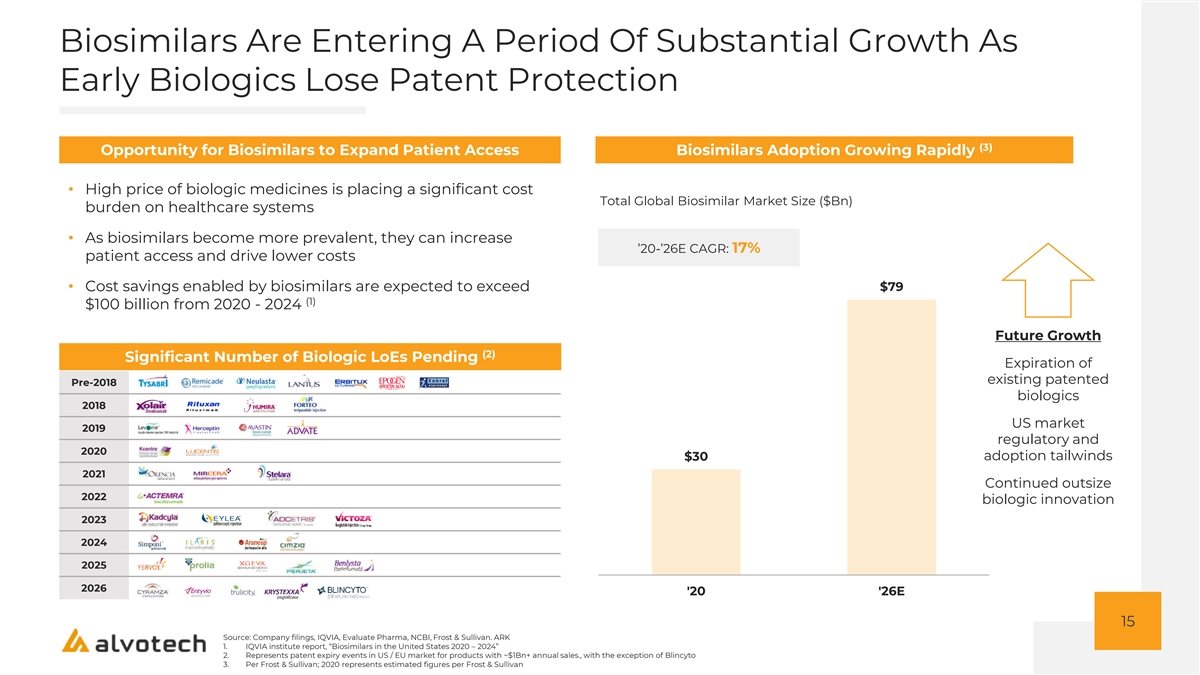

Biosimilar Development Holds Less Risk and Complexity than Originator Biologics, and Significantly More Complexity and Barriers to Entry Than Generics Originator Biologics Biosimilars Generics (1) (2) (3) (5) Development Costs $2.6Bn $100-200MM $1-2MM (2) (3) (6) PoS Low Moderate to high High Development (4) (2) (5) ~12 years ~6-9 years ~2 years Timeline Discovery Pre-Clinical Toxicology Pre-Clinical Development Phase 1 Overview Pre-Clinical PK / PD Study Phase 2 Bioequivalence Confirmatory Patient Study Phase 3 Approval Approval Approval 1. Per PhRMA Org, www.phrma.org/en/Advocacy/Research-Development; “On average, it takes 10-15 years and costs $2.6 billion to develop one new medicine, including the cost of the many failures.” 2. Per company estimates, 6 – 9 years represents timeline for mAb biosimilar development 14 3. Per Deloitte, “Winning with biosimilars”; $100 - $200MM in development costs and 8 – 10 year development timeline for biosimilars 4. Agbogbo, F.K., Ecker, D.M., Farrand, A. et al. Current perspectives on biosimilars. J Ind Microbiol Biotechnol 46, 1297–1311 (2019); reflects time to approval for originator biologics versus biosimilars 5. Pfizer - Biosimilars vs. Generics: What's the Difference? 6. US Food & Drug Administration www.fda.gov/drugs/news-events-human-drugs/generic-drug-approval-process Biosimilars Are Entering A Period Of Substantial Growth As Early Biologics Lose Patent Protection (3) Opportunity for Biosimilars to Expand Patient Access Biosimilars Adoption Growing Rapidly • High price of biologic medicines is placing a significant cost Total Global Biosimilar Market Size ($Bn) burden on healthcare systems • As biosimilars become more prevalent, they can increase ’20-’26E CAGR: 17% patient access and drive lower costs • Cost savings enabled by biosimilars are expected to exceed $79 (1) $100 billion from 2020 - 2024 Future Growth (2) Significant Number of Biologic LoEs Pending Expiration of existing patented Pre-2018 biologics 2018 US market 2019 regulatory and 2020 adoption tailwinds $30 2021 Continued outsize 2022 biologic innovation 2023 2024 2025 2026 '20 '26E 15 Source: Company filings, IQVIA, Evaluate Pharma, NCBI, Frost & Sullivan.

ARK 1. IQVIA institute report, “Biosimilars in the United States 2020 – 2024” 2. Represents patent expiry events in US / EU market for products with ~$1Bn+ annual sales., with the exception of Blincyto 3. Per Frost & Sullivan; 2020 represents estimated figures per Frost & Sullivan PURPOSE-BUILT BIOSIMILAR PLATFORM GLOBAL COMMERCIAL PARTNER NETWORK

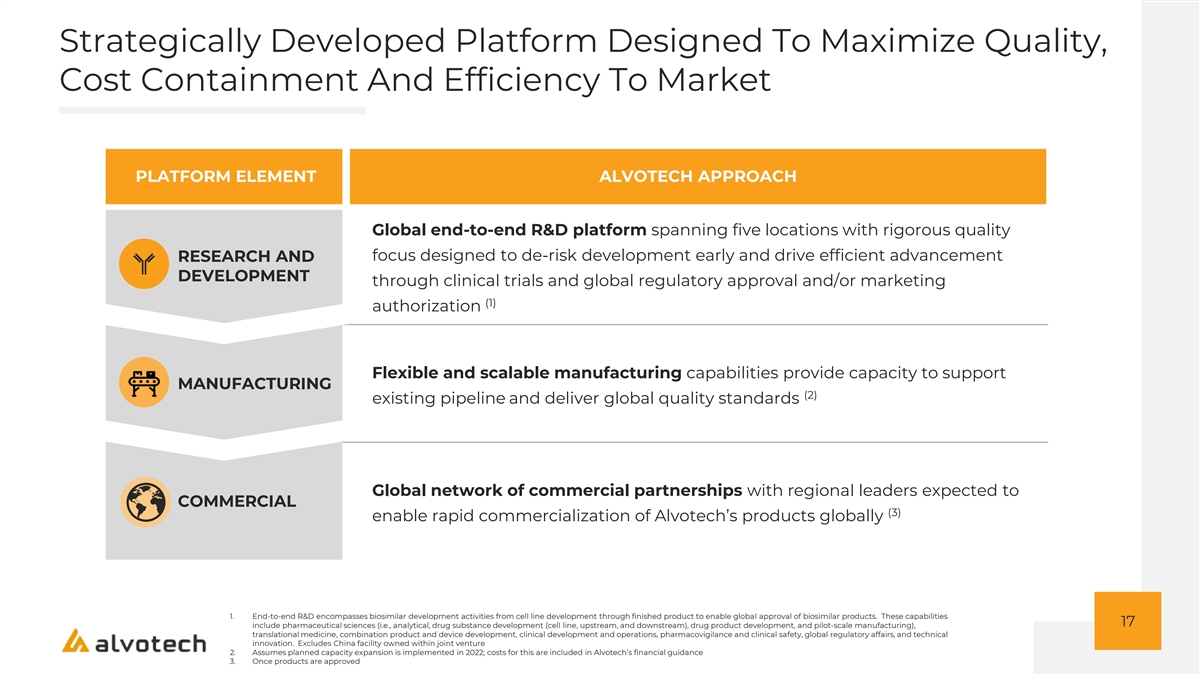

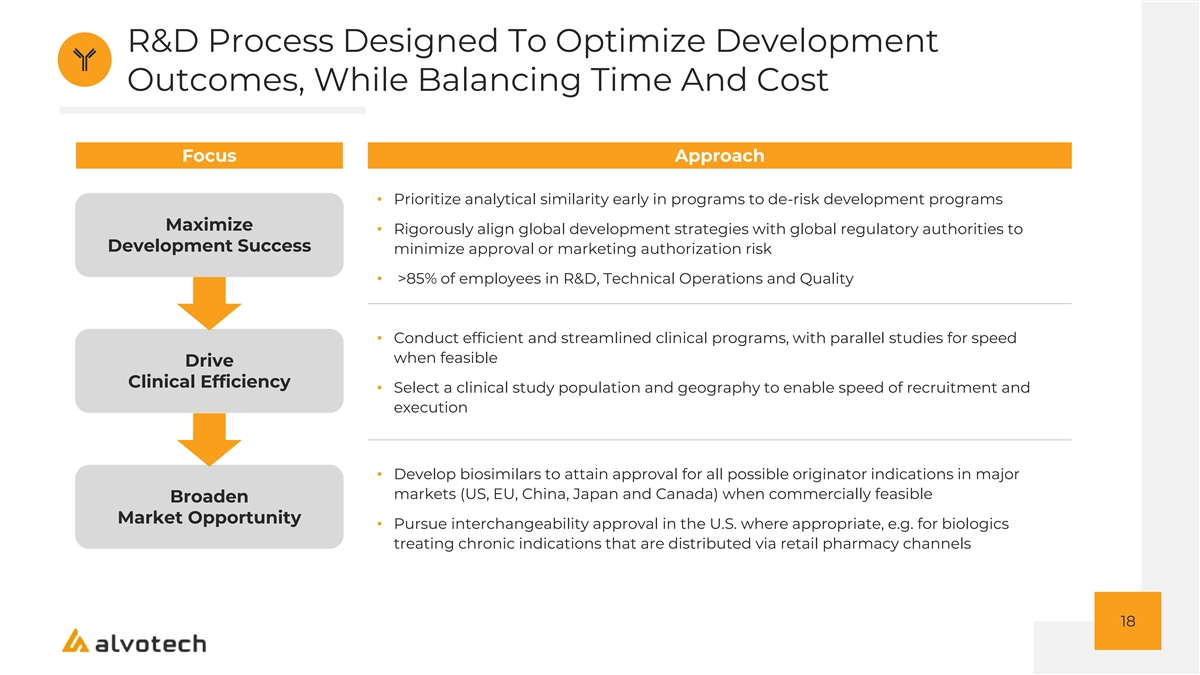

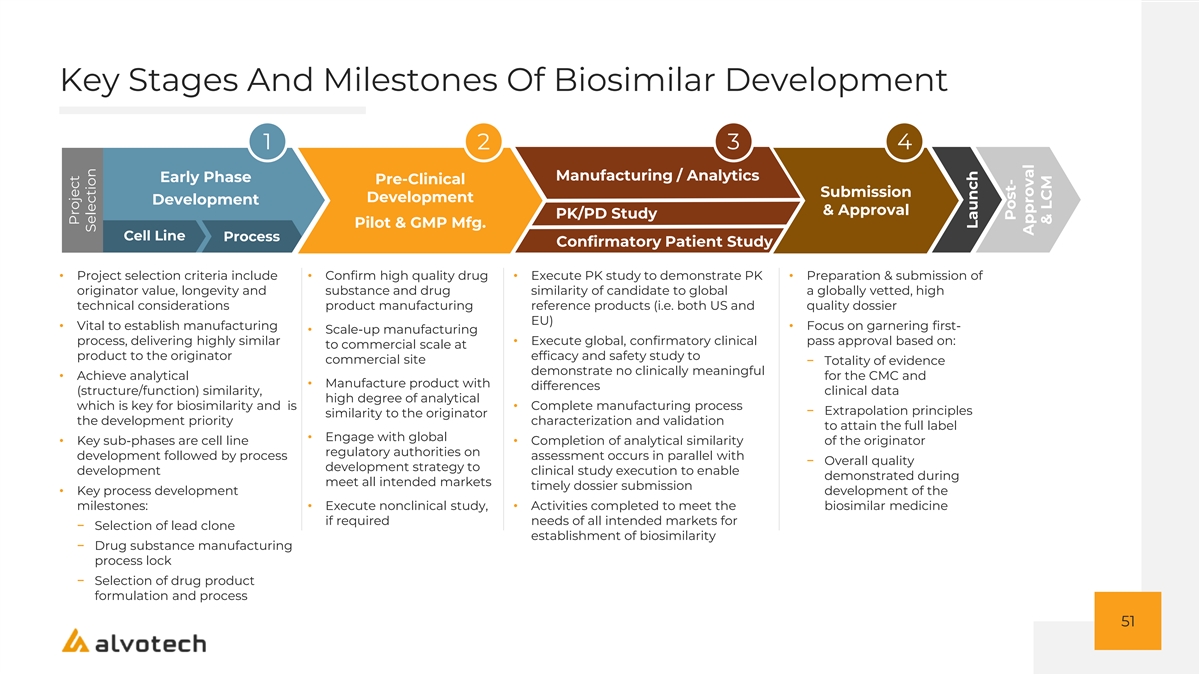

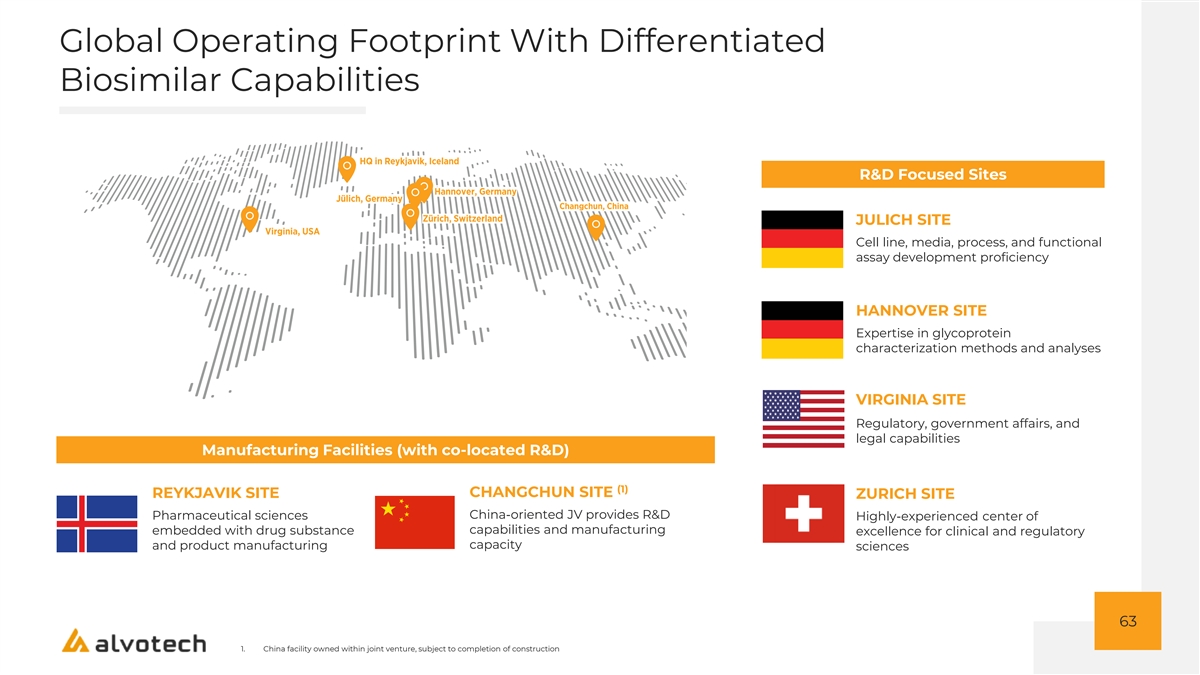

Strategically Developed Platform Designed To Maximize Quality, Cost Containment And Efficiency To Market PLATFORM ELEMENT ALVOTECH APPROACH Global end-to-end R&D platform spanning five locations with rigorous quality focus designed to de-risk development early and drive efficient advancement RESEARCH AND DEVELOPMENT through clinical trials and global regulatory approval and/or marketing (1) authorization Flexible and scalable manufacturing capabilities provide capacity to support MANUFACTURING (2) existing pipeline and deliver global quality standards Global network of commercial partnerships with regional leaders expected to COMMERCIAL (3) enable rapid commercialization of Alvotech’s products globally 1. End-to-end R&D encompasses biosimilar development activities from cell line development through finished product to enable global approval of biosimilar products. These capabilities 17 include pharmaceutical sciences (i.e., analytical, drug substance development (cell line, upstream, and downstream), drug product development, and pilot-scale manufacturing), translational medicine, combination product and device development, clinical development and operations, pharmacovigilance and clinical safety, global regulatory affairs, and technical innovation. Excludes China facility owned within joint venture 2. Assumes planned capacity expansion is implemented in 2022; costs for this are included in Alvotech’s financial guidance 3. Once products are approved R&D Process Designed To Optimize Development Outcomes, While Balancing Time And Cost Focus Approach • Prioritize analytical similarity early in programs to de-risk development programs Maximize • Rigorously align global development strategies with global regulatory authorities to Development Success minimize approval or marketing authorization risk • >85% of employees in R&D, Technical Operations and Quality • Conduct efficient and streamlined clinical programs, with parallel studies for speed when feasible Drive Clinical Efficiency • Select a clinical study population and geography to enable speed of recruitment and execution • Develop biosimilars to attain approval for all possible originator indications in major markets (US, EU, China, Japan and Canada) when commercially feasible Broaden Market Opportunity • Pursue interchangeability approval in the U.S. where appropriate, e.g. for biologics treating chronic indications that are distributed via retail pharmacy channels 18

Extensive Manufacturing Capacity Located in Iceland Key Features Technology & Capabilities 2 • Approximately ~280,000ft facility (inclusive of ongoing expansion) with existing 4- (1) wall drug substance capacity expected to support pipeline through 2030 Capacity and Scalability ✓ • Commercial product manufacturing initiated, with inventory build underway • Differentiated capabilities including CHO and SP2/0 host cell lines Flexible Capabilities • Single use bioreactors for use with fed batch or perfusion processes ✓ • Aseptic fill/finish capabilities • 2 successful IMA/EMA inspections with clinical and commercial licenses issued Externally Validated Quality• 4 commercial partner audits successfully completed ✓ • US FDA inspection occurred in March 2022 • Conveniently situated between the U.S. and Europe Intentionally Located• Powered by renewable energy with access to abundant clean and hot water ✓ • Operates in a “patent-light” zone 19 2 1. Includes 140,000ft ongoing capacity expansion projects expected to be completed in early 2024 – costs for this are included in Alvotech’s financial guidance Network Of High-Quality Regional Partners Provides Global Commercial Reach Alvotech’s Partner Partnered Territories Selection Criteria P Strategic Positioning Track record of success in local market SVALBARD (NORWAY) P Shared Risk Dynamic GREENLAND Structurally aligned incentives P Attractive Economics Upfront and ongoing milestones ALASKA (USA) ICELAND RUSSIA SWEDEN FINLAND offset R&D cost and risk FAROE ISLANDS NORWAY ESTONIA CANADA LATVIA DENMARK LITHUANIA UNITED BELARUS IRELAND KINGDOM NETHERLANDS POLAND GERMANY BELGIUM LUXEMBOURG CZECH REP UKRAINE SLOVAKIA KAZAKHSTAN LIECHTENSTEIN FRANCE MOLDOVA AUSTRIA HUNGARY SWITZERLAND SLOVENIA MONGOLIA ROMANIA BOSNIA CROATIA AND SERBIA Global Biologics Sales HERZ.

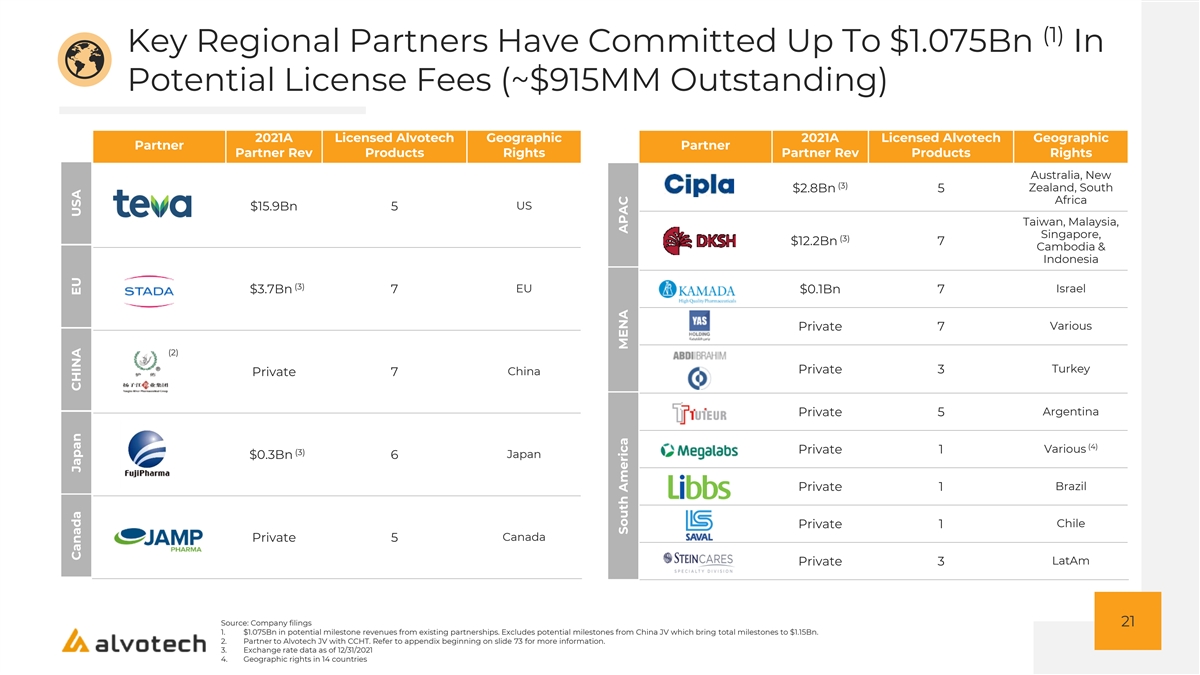

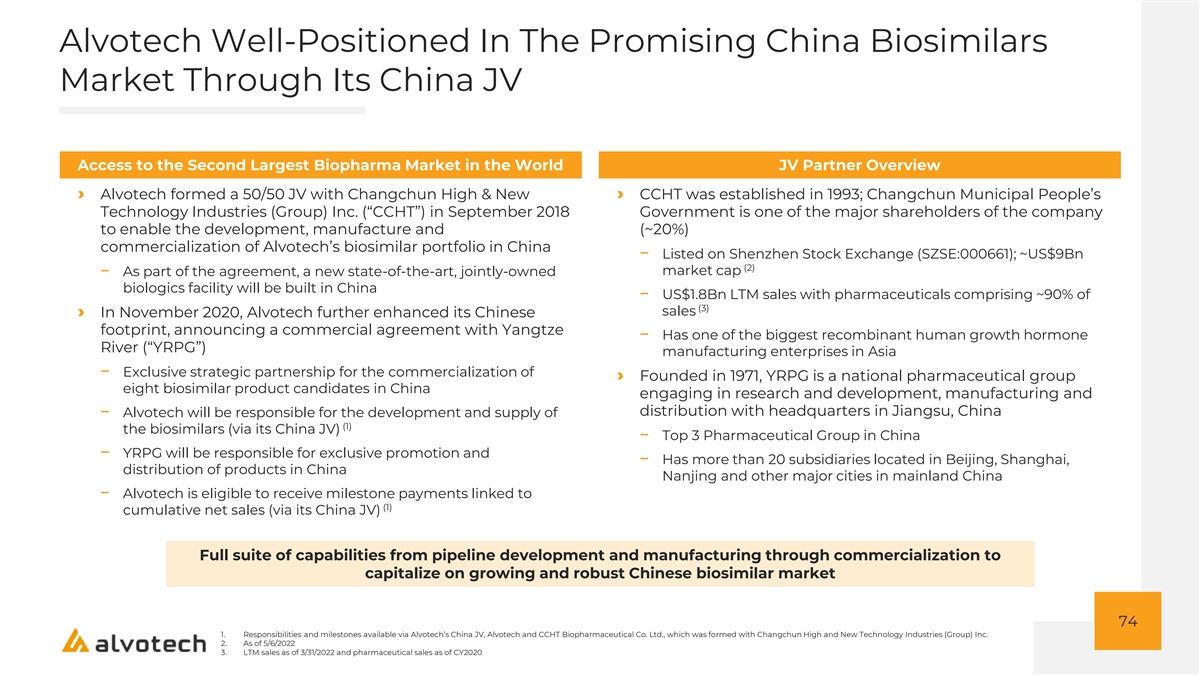

BULGARIA ITALY MONTENEGRO MACEDONIA UZBEKISTAN ALBANIA ARMENIA NORTH PORTUGAL SPAIN AZERBAIJAN KOREA GREECE TURKMENISTAN UNITED STATES OF AMERICA TURKEY JAPAN (1) AZORES (PORTUGAL) MALTA SOUTH by Region KOREA CHINA CYPRUS SYRIA AFGHANISTAN TUNISIA LEBANON KASHMIR MOROCCO IRAQ IRAN MADEIRA ISLAND (PORTUGAL) ISRAEL JORDAN KUWAIT CANARY ISLANDS (SPAIN) PAKISTAN NEPAL ALGERIA LIBYA BHUTAN EGYPT QATAR WESTERN THE BAHAMAS SHARAH UNITED TAIWAN SAUDI ARAB BANGLADESH MEXICO ROW EMIRATES CUBA ARABIA INDIA MYANMAR (BURMA) OMAN HAITI DOMINICAN LAOS MAURITANIA JAMAICA PUERTO RICO (USA) REPUBLIC China BELIZE MALI SAINT KITTS AND NEVIS CAPE VERDE 7% NIGER CHAD ERITREA YEMEN THAILAND GUATEMALA HONDURAS SENEGAL PHILIPPINES GUAM MONTSERRAT SUDAN ADAMAN AND GUADELOUPE THE GAMBIA EL SALVADOR NICARAGUA BURKINA NICOBAR CAMBODIA VIETNAM DOMINICA GUINEA-BISSAU DJIBOUTI SAINT VINCENT GUINEA FASO ISLANDS (INDIA) 4% MARTINIQUE BENIN SAN JOSE BARBADOS PANAMA TRINIDAD AND TOBAGO NIGERIA VENEZUELA SIERRA LEONE COTE TOGO CENTRAL ETHIOPIA SRI D’IVOIRE GHANA AFRICAN GUYANA LIBERIA LANKA Japan CAMEROON REPUBLIC FRENCH GUIANA SOMALIA MALAYSIA COLOMBIA SURINAME BIOKO (EQUATORIAL GUINEA) EQUATORIAL GUINEA UGANDA GALAPAGOS KENYA SAO TOME GABON ECUADOR CONGO DEMOCRATIC 5% RWANDA REPUBLIC BURUNDI INDONESIA OF THE CONGO PAPUA CABINDA (PROVINCE) NEW SOLOMON ISLANDS TANZANIA SEYCHELLES GUINEA BRAZIL COMOROS PERU ANGOLA MALAWI MAYOTTE (FRANCE) ZAMBIA FIJI VANUATU BOLIVIA MOZAMBIQUE ZIMBABWE MADAGASCAR MAURITIUS NAMIBIA BOTSWANA REUNION AUSTRALIA Europe PARAGUAY NEW CALEDONIA (FRANCE) CHILE SWAZILAND 24% LESOTHO USA ARGENTINA SOUTH AFRICA URUGUAY 60% KERGUELEN ISLAND (FRANCE) TASMANIA NEW ZEALAND (AUSTRALIA) HEARD ISLAND (AUSTRALIA) FALKLAND ISLANDS (UK) SOUTH GEORGIA (UK) 20 1. LTM as of Q4 2021 per IQVIA (1) Key Regional Partners Have Committed Up To $1.075Bn In Potential License Fees (~$915MM Outstanding) 2021A Licensed Alvotech Geographic 2021A Licensed Alvotech Geographic Partner Partner Partner Rev Products Rights Partner Rev Products Rights Australia, New (3) Zealand, South $2.8Bn 5 Africa US $15.9Bn 5 Taiwan, Malaysia, Singapore, (3) $12.2Bn 7 Cambodia & Indonesia (3) EU Israel $3.7Bn 7 $0.1Bn 7 Various Private 7 (2) Turkey Private 3 China Private 7 Argentina Private 5 (4) Various Private 1 (3) $0.3Bn 6 Japan Brazil Private 1 Chile Private 1 Canada Private 5 LatAm Private 3 Source: Company filings 21 1.

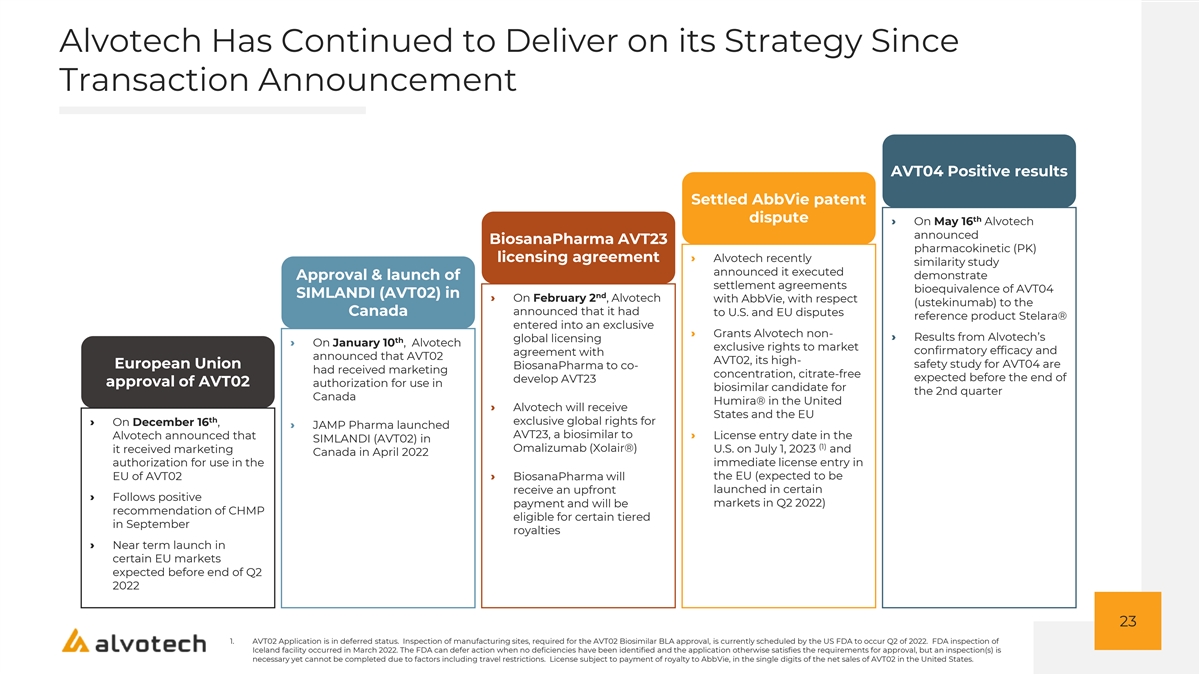

$1.075Bn in potential milestone revenues from existing partnerships. Excludes potential milestones from China JV which bring total milestones to $1.15Bn. 2. Partner to Alvotech JV with CCHT. Refer to appendix beginning on slide 73 for more information. 3. Exchange rate data as of 12/31/2021 4. Geographic rights in 14 countries Canada Japan CHINA EU USA South America MENA APAC Alvotech Has Continued to Deliver on its Strategy Since Transaction Announcement AVT04 Positive results Settled AbbVie patent dispute th › On May 16 Alvotech announced BiosanaPharma AVT23 pharmacokinetic (PK) licensing agreement› Alvotech recently similarity study announced it executed Approval & launch of demonstrate settlement agreements bioequivalence of AVT04 SIMLANDI (AVT02) in nd › On February 2 , Alvotech with AbbVie, with respect (ustekinumab) to the announced that it had Canada to U.S. and EU disputes reference product Stelara® entered into an exclusive › Grants Alvotech non- › Results from Alvotech’s global licensing th › On January 10 , Alvotech exclusive rights to market confirmatory efficacy and agreement with announced that AVT02 AVT02, its high- safety study for AVT04 are European Union BiosanaPharma to co- had received marketing concentration, citrate-free expected before the end of develop AVT23 approval of AVT02 authorization for use in biosimilar candidate for the 2nd quarter Canada Humira® in the United › Alvotech will receive States and the EU th exclusive global rights for › On December 16 , › JAMP Pharma launched AVT23, a biosimilar to › License entry date in the Alvotech announced that SIMLANDI (AVT02) in (1) Omalizumab (Xolair®) U.S. on July 1, 2023 and it received marketing Canada in April 2022 authorization for use in the immediate license entry in EU of AVT02› BiosanaPharma will the EU (expected to be receive an upfront launched in certain › Follows positive markets in Q2 2022) payment and will be recommendation of CHMP eligible for certain tiered in September royalties › Near term launch in certain EU markets expected before end of Q2 2022 23 1.

DIVERSE PIPELINE WITH SIGNIFICANT TAM

AVT02 Application is in deferred status. Inspection of manufacturing sites, required for the AVT02 Biosimilar BLA approval, is currently scheduled by the US FDA to occur Q2 of 2022. FDA inspection of Iceland facility occurred in March 2022. The FDA can defer action when no deficiencies have been identified and the application otherwise satisfies the requirements for approval, but an inspection(s) is necessary yet cannot be completed due to factors including travel restrictions. License subject to payment of royalty to AbbVie, in the single digits of the net sales of AVT02 in the United States.

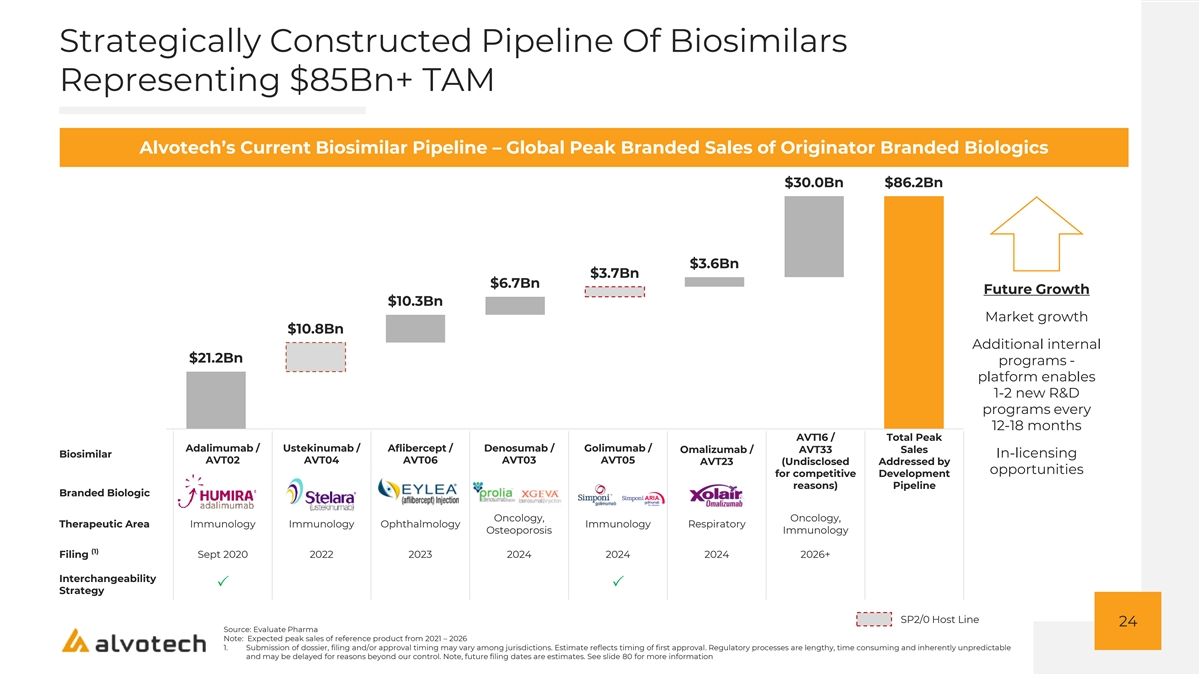

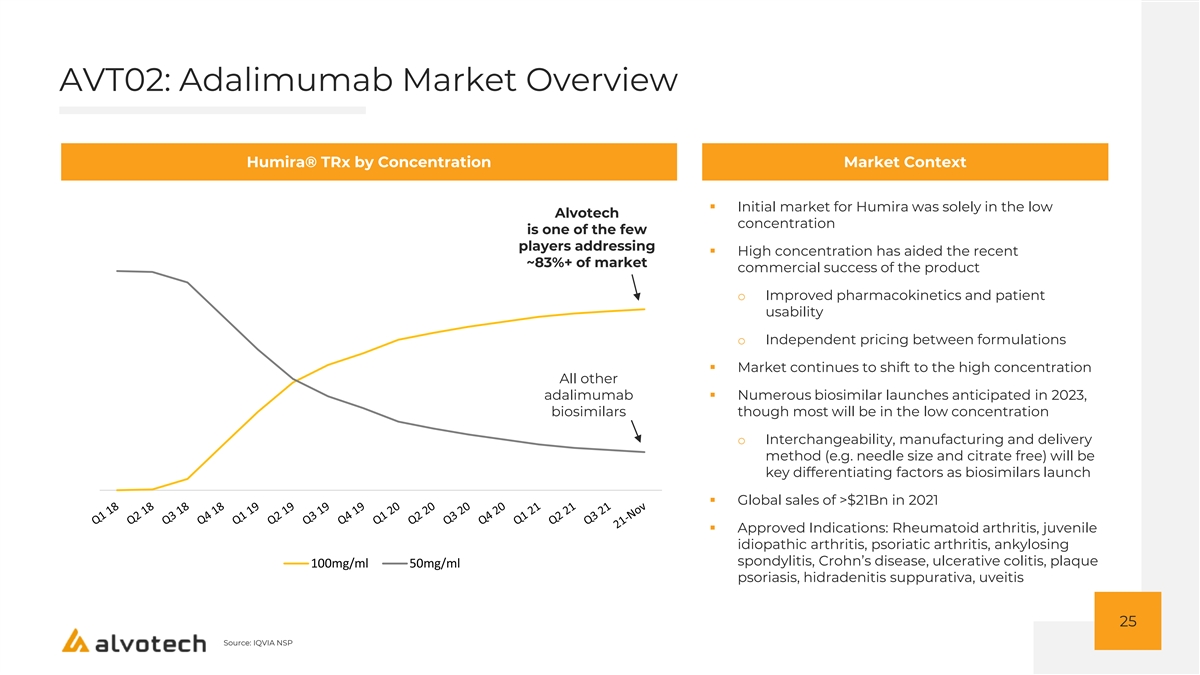

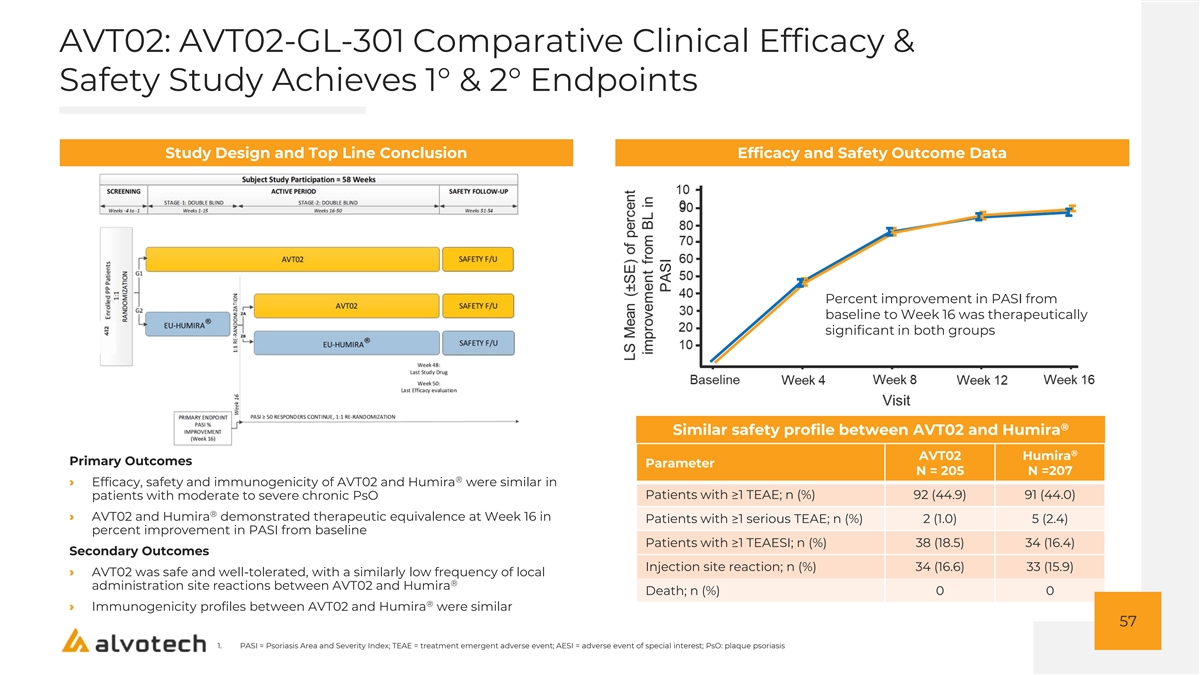

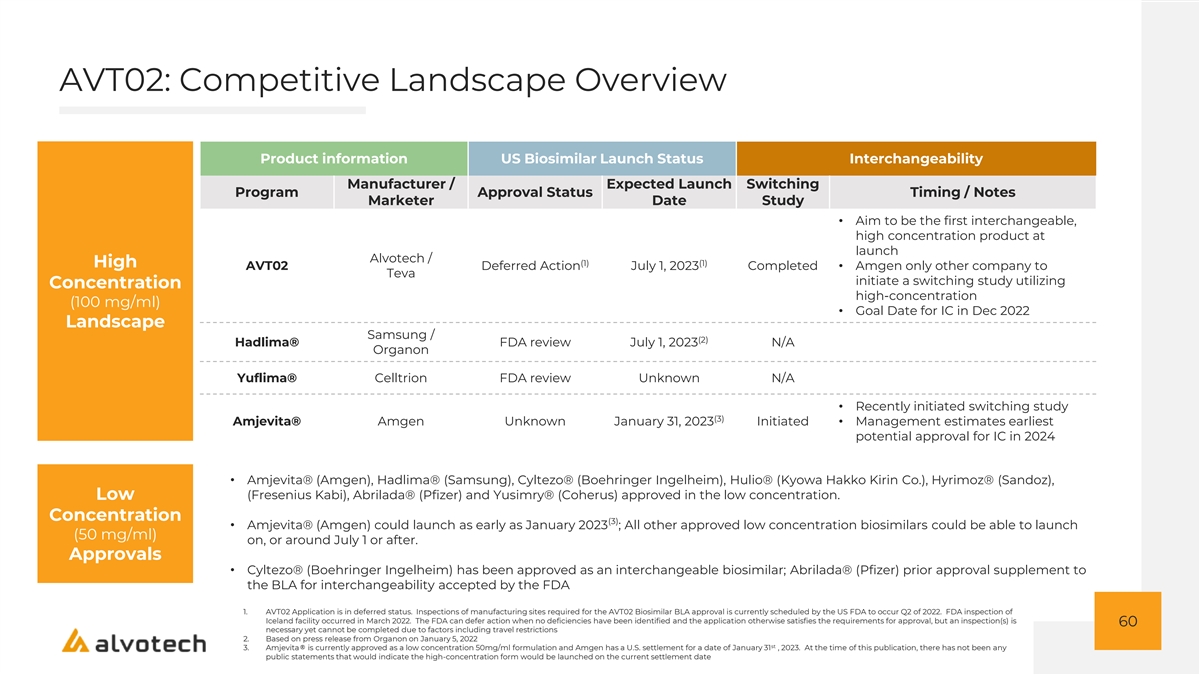

Strategically Constructed Pipeline Of Biosimilars Representing $85Bn+ TAM Alvotech’s Current Biosimilar Pipeline – Global Peak Branded Sales of Originator Branded Biologics $30.0Bn $86.2Bn $3.6Bn $3.7Bn $6.7Bn Future Growth $10.3Bn Market growth $10.8Bn Additional internal $21.2Bn programs - platform enables 1-2 new R&D programs every 12-18 months AVT16 / Total Peak Adalimumab / Ustekinumab / Aflibercept / Denosumab / Golimumab / Omalizumab / AVT33 Sales Biosimilar In-licensing AVT02 AVT04 AVT06 AVT03 AVT05 AVT23 (Undisclosed Addressed by opportunities for competitive Development reasons) Pipeline Branded Biologic Oncology, Oncology, Therapeutic Area Immunology Immunology Ophthalmology Immunology Respiratory Osteoporosis Immunology (1) Filing Sept 2020 2022 2023 2024 2024 2024 2026+ Interchangeability PP Strategy SP2/0 Host Line 24 Source: Evaluate Pharma Note: Expected peak sales of reference product from 2021 – 2026 1. Submission of dossier, filing and/or approval timing may vary among jurisdictions. Estimate reflects timing of first approval. Regulatory processes are lengthy, time consuming and inherently unpredictable and may be delayed for reasons beyond our control. Note, future filing dates are estimates. See slide 80 for more information AVT02: Adalimumab Market Overview Humira® TRx by Concentration Market Context ▪ Initial market for Humira was solely in the low Alvotech concentration is one of the few players addressing ▪ High concentration has aided the recent ~83%+ of market commercial success of the product o Improved pharmacokinetics and patient usability o Independent pricing between formulations ▪ Market continues to shift to the high concentration All other adalimumab ▪ Numerous biosimilar launches anticipated in 2023, biosimilars though most will be in the low concentration o Interchangeability, manufacturing and delivery method (e.g.

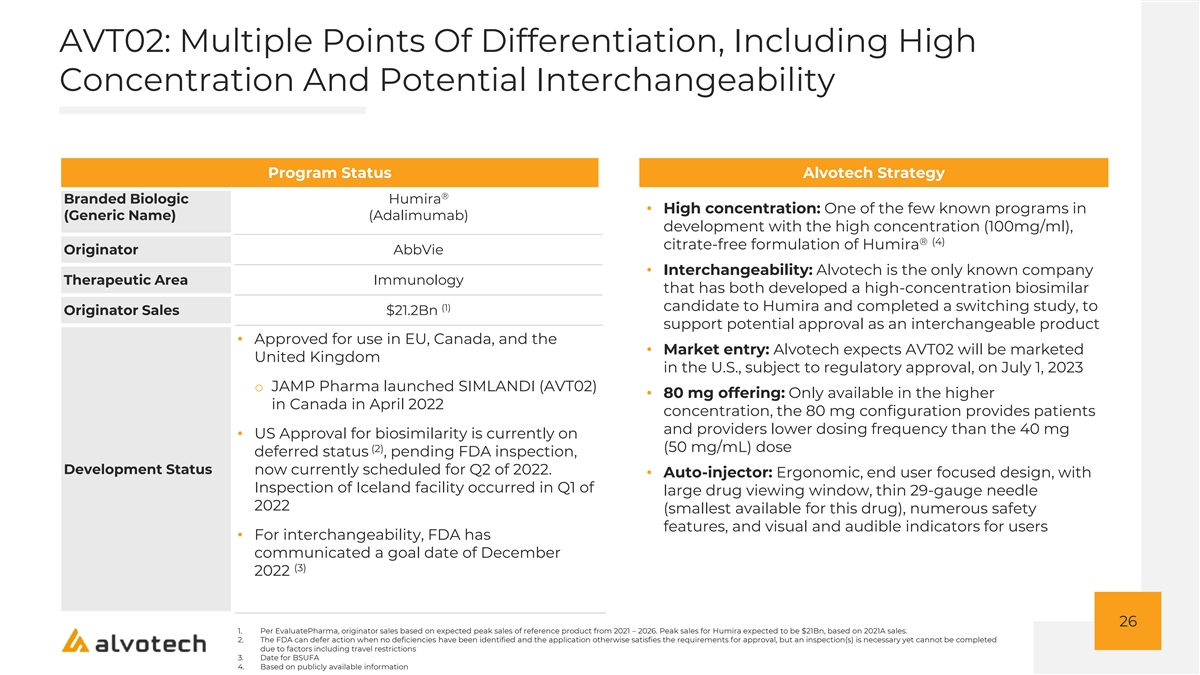

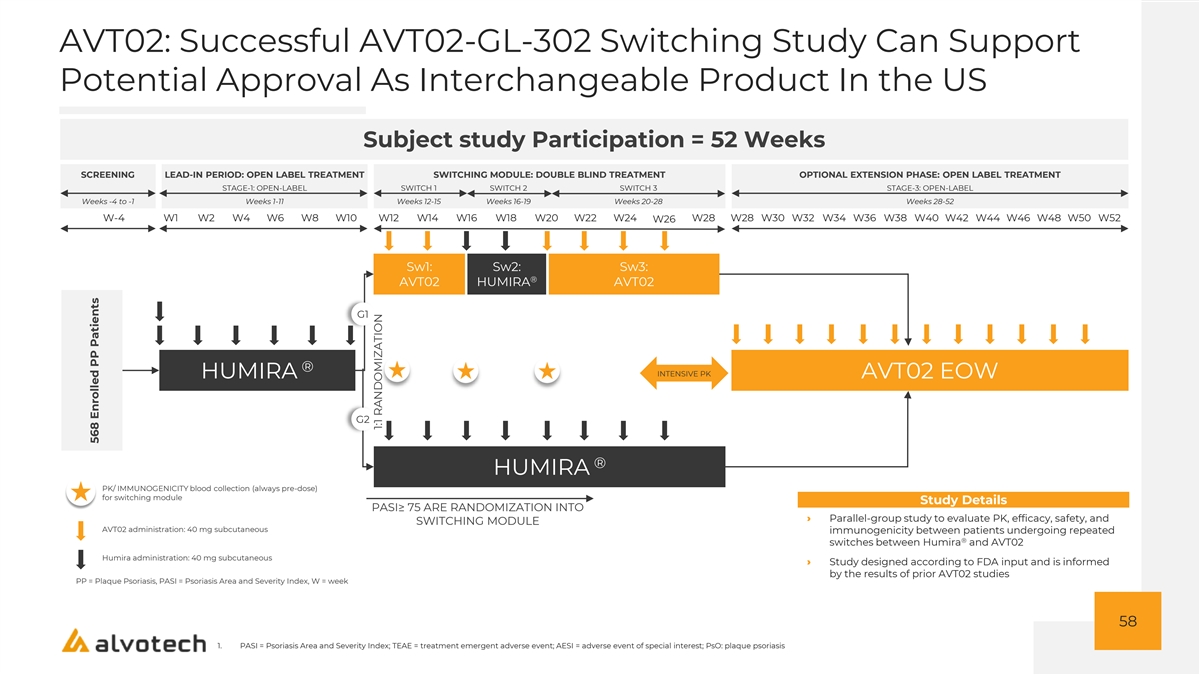

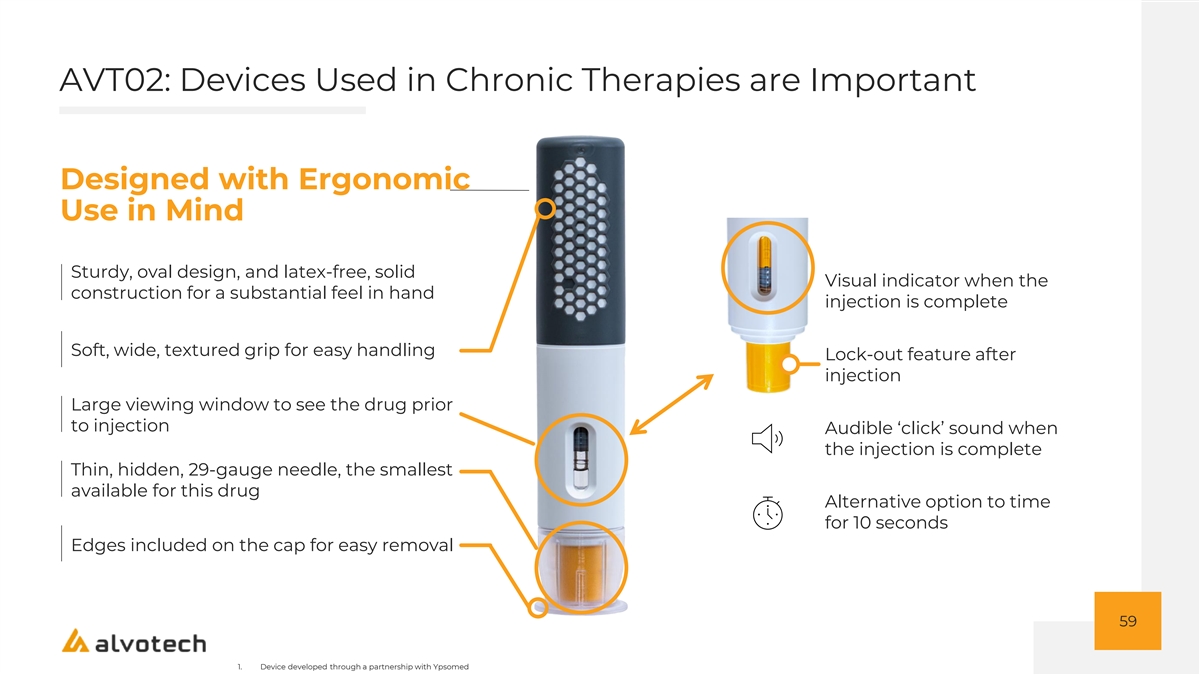

needle size and citrate free) will be key differentiating factors as biosimilars launch ▪ Global sales of >$21Bn in 2021 ▪ Approved Indications: Rheumatoid arthritis, juvenile idiopathic arthritis, psoriatic arthritis, ankylosing spondylitis, Crohn’s disease, ulcerative colitis, plaque 100mg/ml 50mg/ml psoriasis, hidradenitis suppurativa, uveitis 25 Source: IQVIA NSP AVT02: Multiple Points Of Differentiation, Including High Concentration And Potential Interchangeability Program Status Alvotech Strategy ® Branded Biologic Humira • High concentration: One of the few known programs in (Generic Name) (Adalimumab) development with the high concentration (100mg/ml), ® (4) citrate-free formulation of Humira Originator AbbVie • Interchangeability: Alvotech is the only known company Therapeutic Area Immunology that has both developed a high-concentration biosimilar (1) candidate to Humira and completed a switching study, to Originator Sales $21.2Bn support potential approval as an interchangeable product • Approved for use in EU, Canada, and the • Market entry: Alvotech expects AVT02 will be marketed United Kingdom in the U.S., subject to regulatory approval, on July 1, 2023 o JAMP Pharma launched SIMLANDI (AVT02) • 80 mg offering: Only available in the higher in Canada in April 2022 concentration, the 80 mg configuration provides patients and providers lower dosing frequency than the 40 mg • US Approval for biosimilarity is currently on (2) (50 mg/mL) dose deferred status , pending FDA inspection, Development Status now currently scheduled for Q2 of 2022.

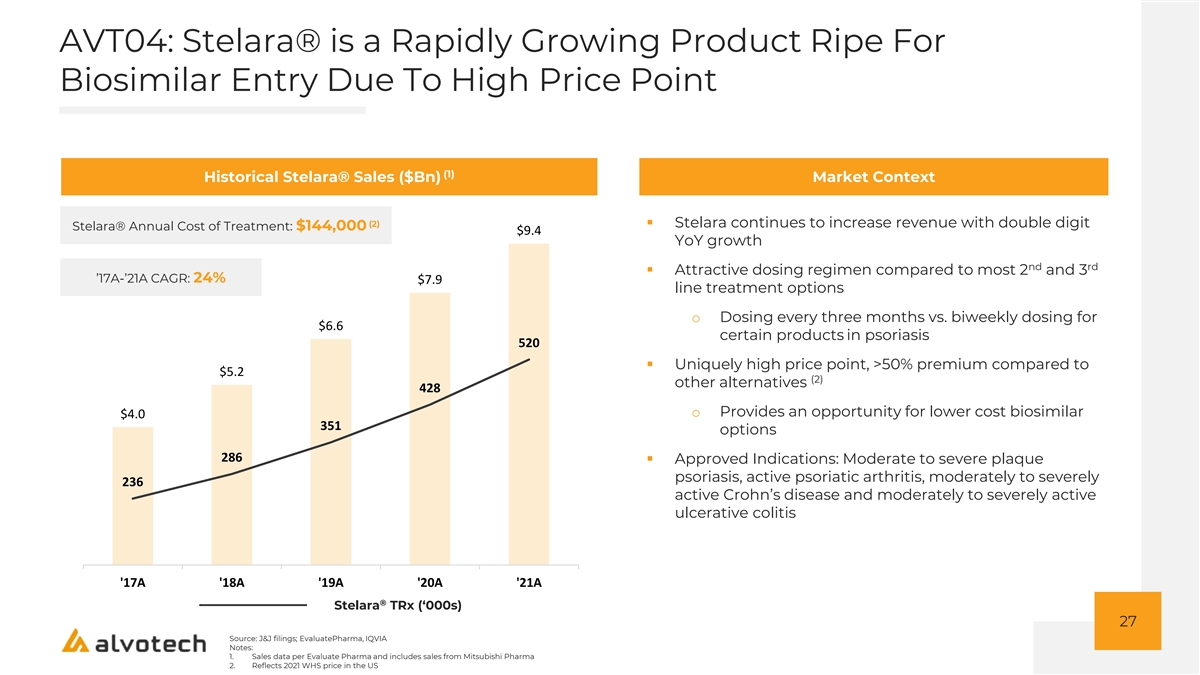

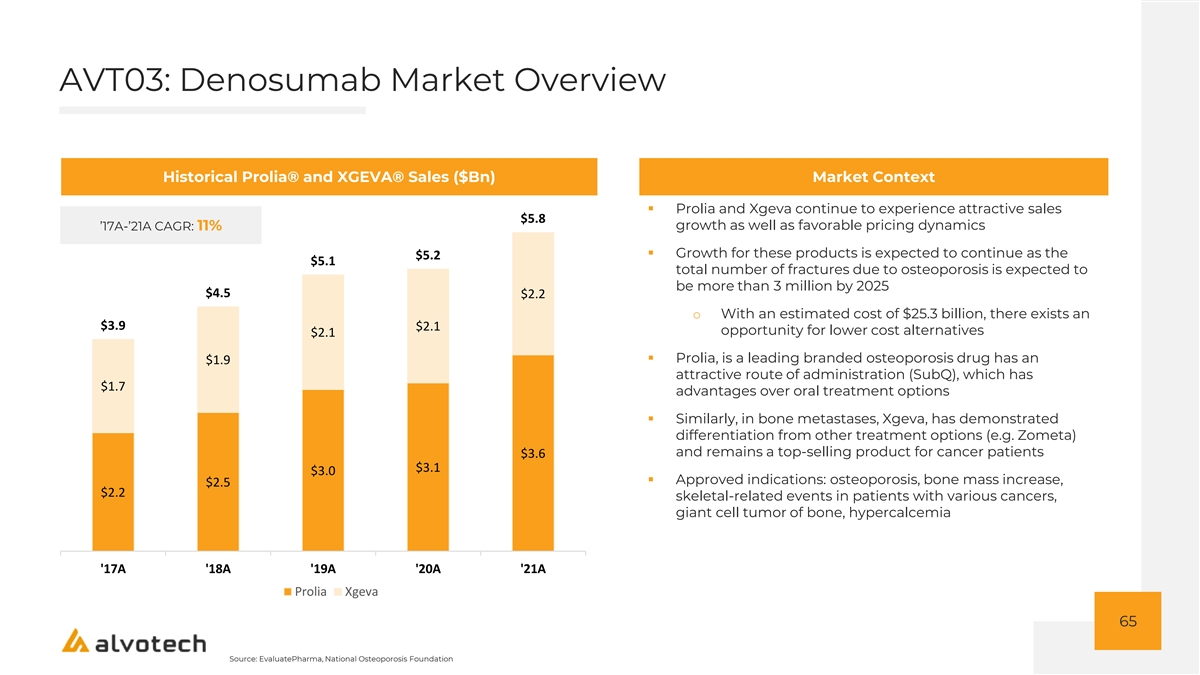

• Auto-injector: Ergonomic, end user focused design, with Inspection of Iceland facility occurred in Q1 of large drug viewing window, thin 29-gauge needle 2022 (smallest available for this drug), numerous safety features, and visual and audible indicators for users • For interchangeability, FDA has communicated a goal date of December (3) 2022 26 1. Per EvaluatePharma, originator sales based on expected peak sales of reference product from 2021 – 2026. Peak sales for Humira expected to be $21Bn, based on 2021A sales. 2. The FDA can defer action when no deficiencies have been identified and the application otherwise satisfies the requirements for approval, but an inspection(s) is necessary yet cannot be completed due to factors including travel restrictions 3. Date for BSUFA 4. Based on publicly available information AVT04: Stelara® is a Rapidly Growing Product Ripe For Biosimilar Entry Due To High Price Point (1) Historical Stelara® Sales ($Bn) Market Context 10.0 (2)▪ Stelara continues to increase revenue with double digit Stelara® Annual Cost of Treatment: $144,000 $9.4 YoY growth 9.0 nd rd ▪ Attractive dosing regimen compared to most 2 and 3 ’17A-’21A CAGR: 24% $7.9 line treatment options 8.0 o Dosing every three months vs. biweekly dosing for 7.0 $6.6 certain products in psoriasis 520 6.0 ▪ Uniquely high price point, >50% premium compared to $5.2 (2) other alternatives 428 5.0 o Provides an opportunity for lower cost biosimilar $4.0 351 4.0 options 286 ▪ Approved Indications: Moderate to severe plaque 3.0 psoriasis, active psoriatic arthritis, moderately to severely 236 2.0 active Crohn’s disease and moderately to severely active ulcerative colitis 1.0 0.0 '17A '18A '19A '20A '21A ® Stelara TRx (‘000s) 27 Source: J&J filings; EvaluatePharma, IQVIA Notes: 1.

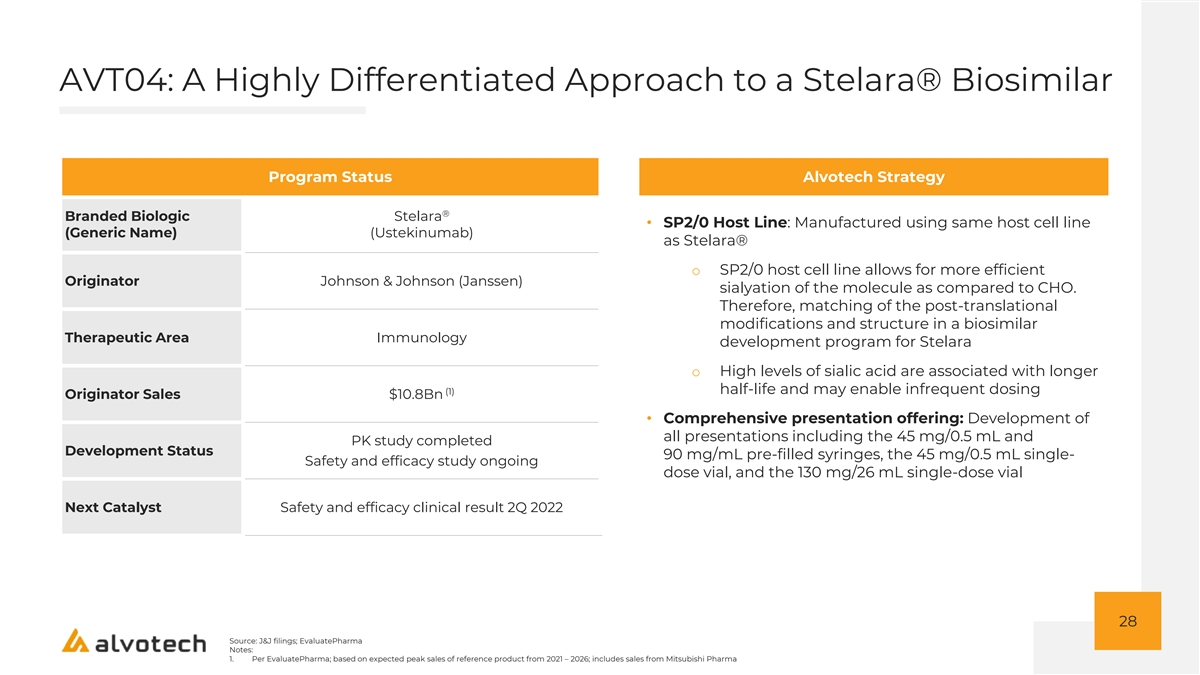

Sales data per Evaluate Pharma and includes sales from Mitsubishi Pharma 2. Reflects 2021 WHS price in the US AVT04: A Highly Differentiated Approach to a Stelara® Biosimilar Program Status Alvotech Strategy ® Branded Biologic Stelara • SP2/0 Host Line: Manufactured using same host cell line (Generic Name) (Ustekinumab) as Stelara® o SP2/0 host cell line allows for more efficient Originator Johnson & Johnson (Janssen) sialyation of the molecule as compared to CHO. Therefore, matching of the post-translational modifications and structure in a biosimilar Therapeutic Area Immunology development program for Stelara o High levels of sialic acid are associated with longer half-life and may enable infrequent dosing (1) Originator Sales $10.8Bn • Comprehensive presentation offering: Development of all presentations including the 45 mg/0.5 mL and PK study completed Development Status 90 mg/mL pre-filled syringes, the 45 mg/0.5 mL single- Safety and efficacy study ongoing dose vial, and the 130 mg/26 mL single-dose vial Next Catalyst Safety and efficacy clinical result 2Q 2022 28 Source: J&J filings; EvaluatePharma Notes: 1.

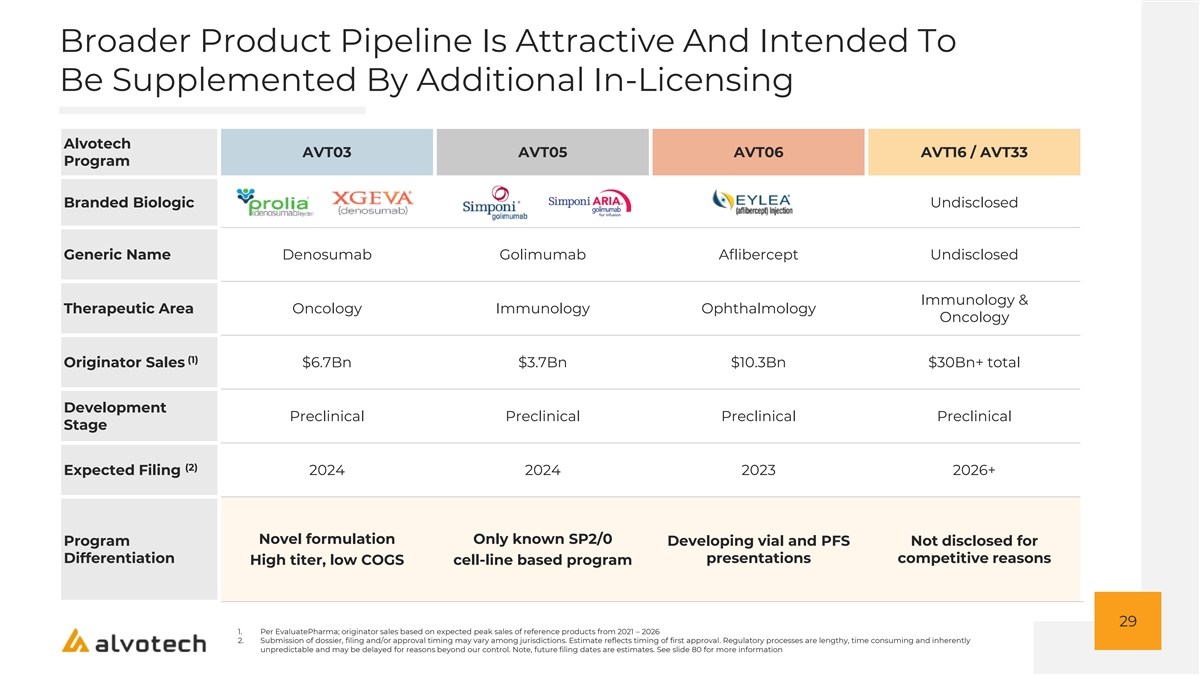

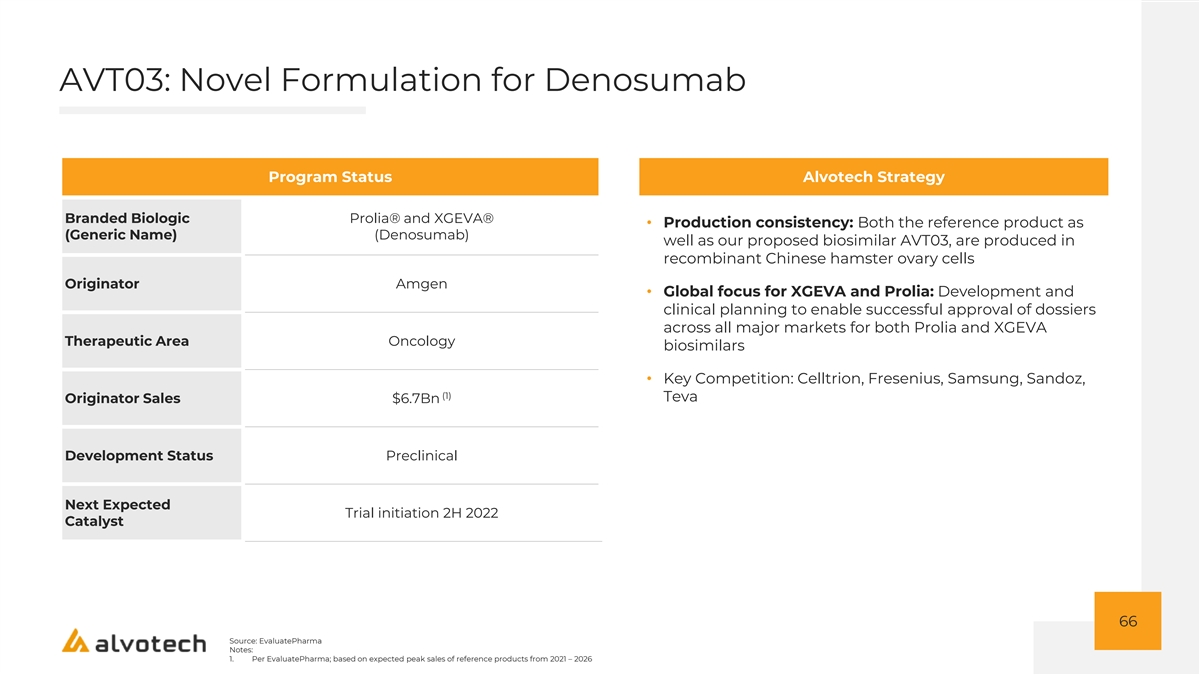

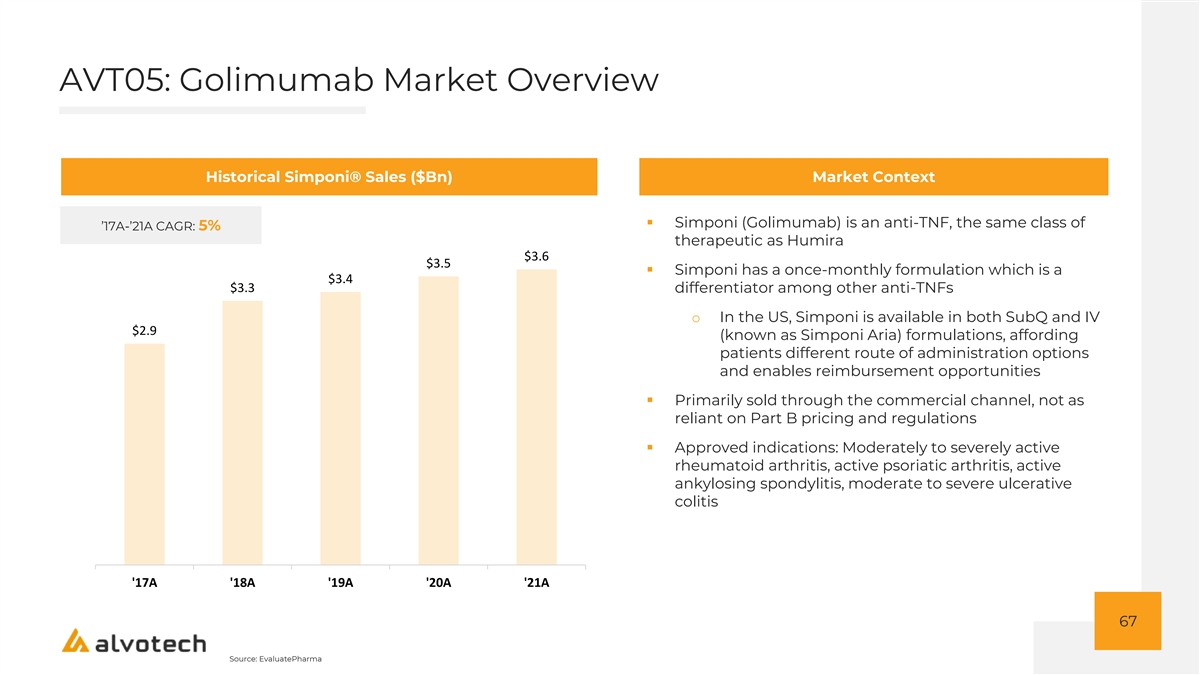

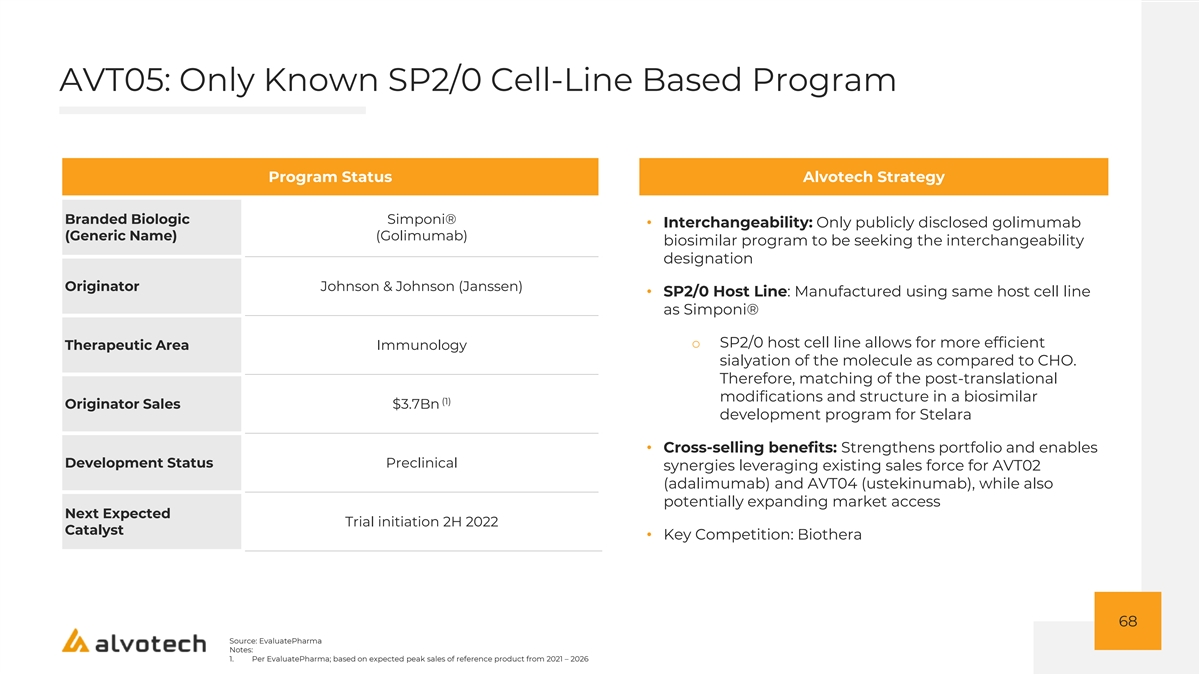

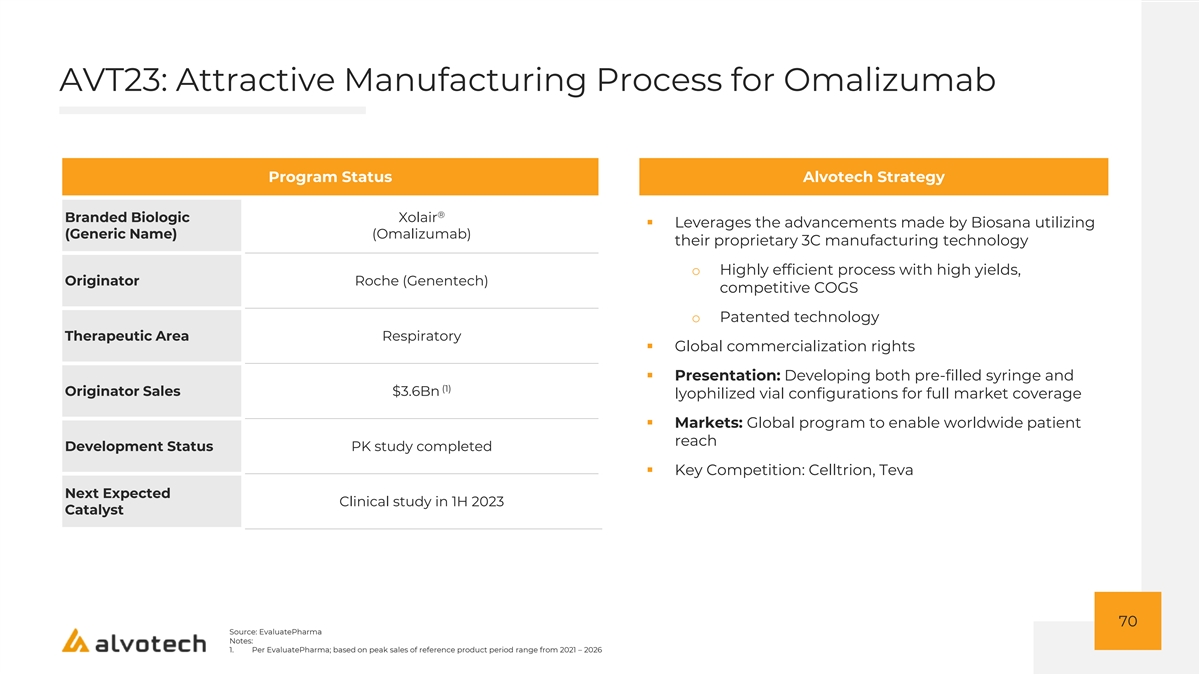

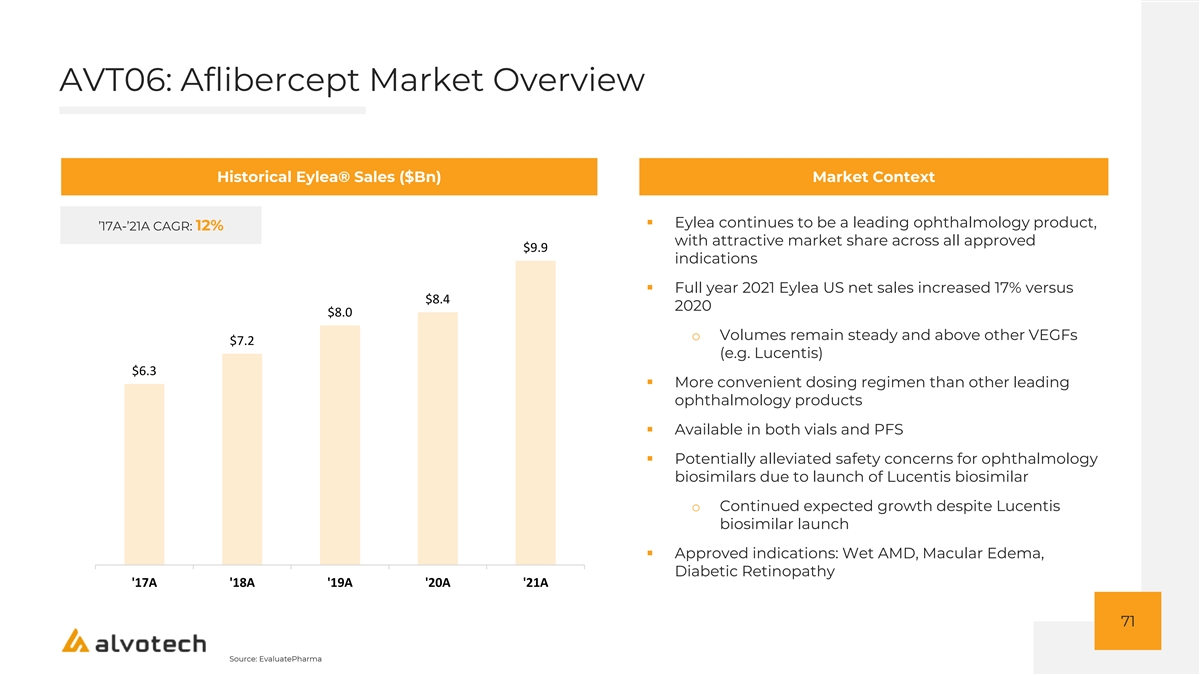

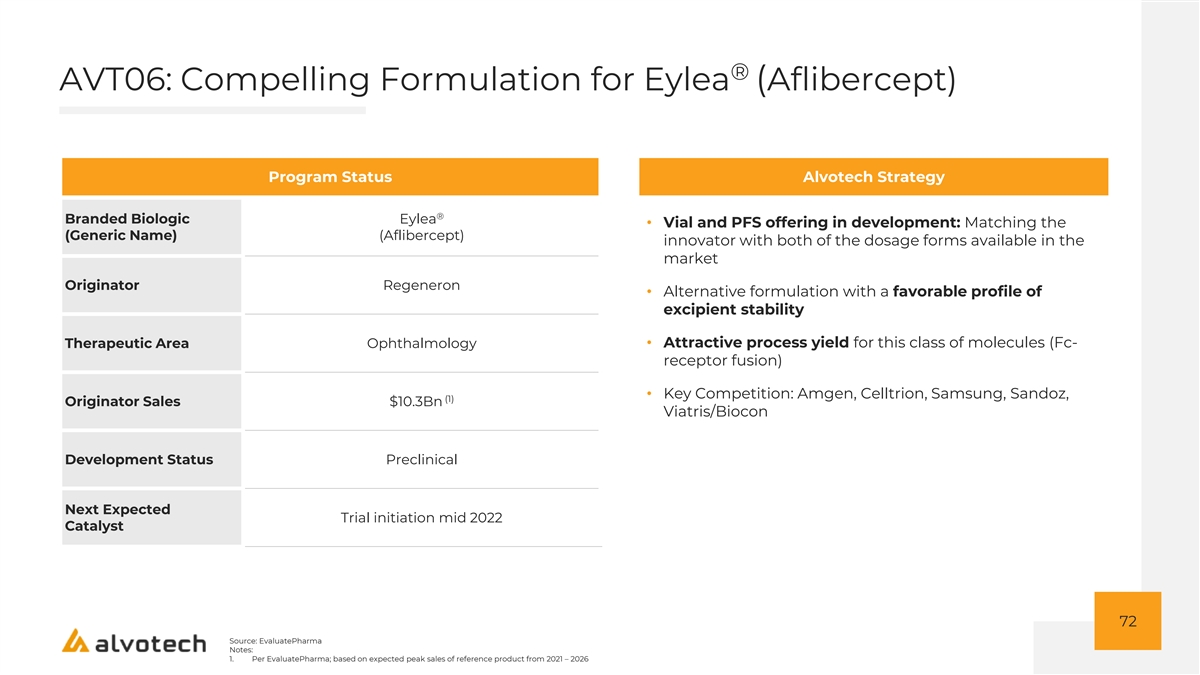

Per EvaluatePharma; based on expected peak sales of reference product from 2021 – 2026; includes sales from Mitsubishi Pharma Broader Product Pipeline Is Attractive And Intended To Be Supplemented By Additional In-Licensing Alvotech AVT03 AVT05 AVT06 AVT16 / AVT33 Program Branded Biologic Undisclosed Generic Name Denosumab Golimumab Aflibercept Undisclosed Immunology & Therapeutic Area Oncology Immunology Ophthalmology Oncology (1) Originator Sales $6.7Bn $3.7Bn $10.3Bn $30Bn+ total Development Preclinical Preclinical Preclinical Preclinical Stage (2) Expected Filing 2024 2024 2023 2026+ Novel formulation Only known SP2/0 Program Developing vial and PFS Not disclosed for Differentiation presentations competitive reasons High titer, low COGS cell-line based program 29 1.

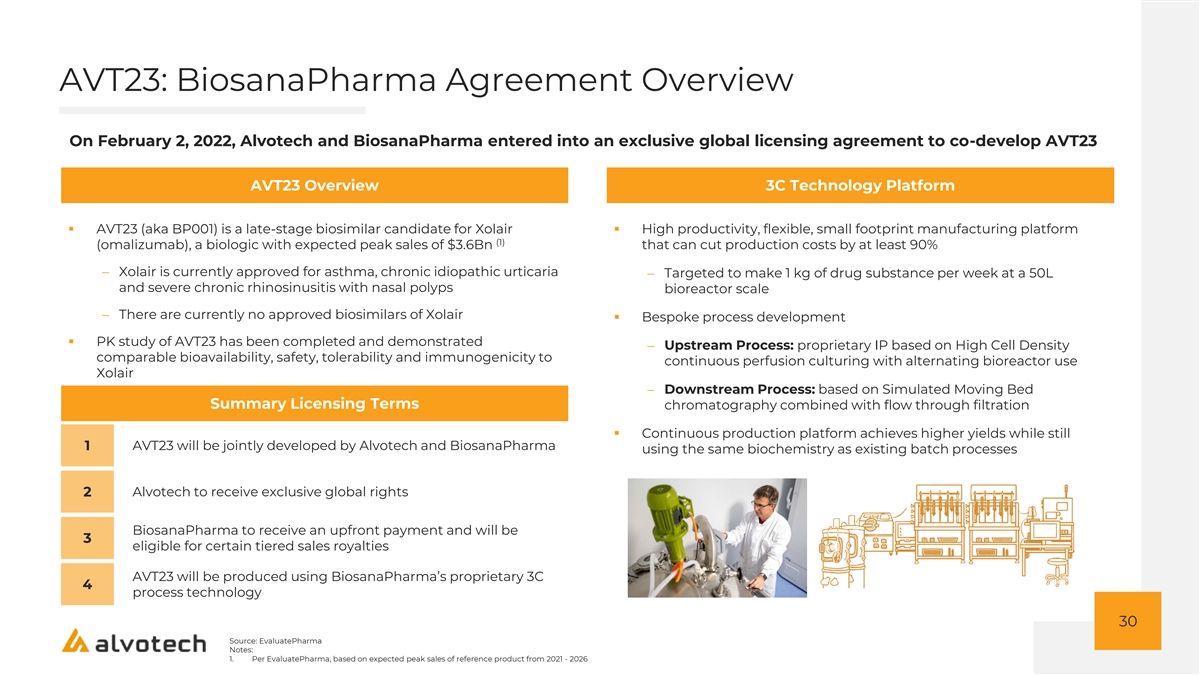

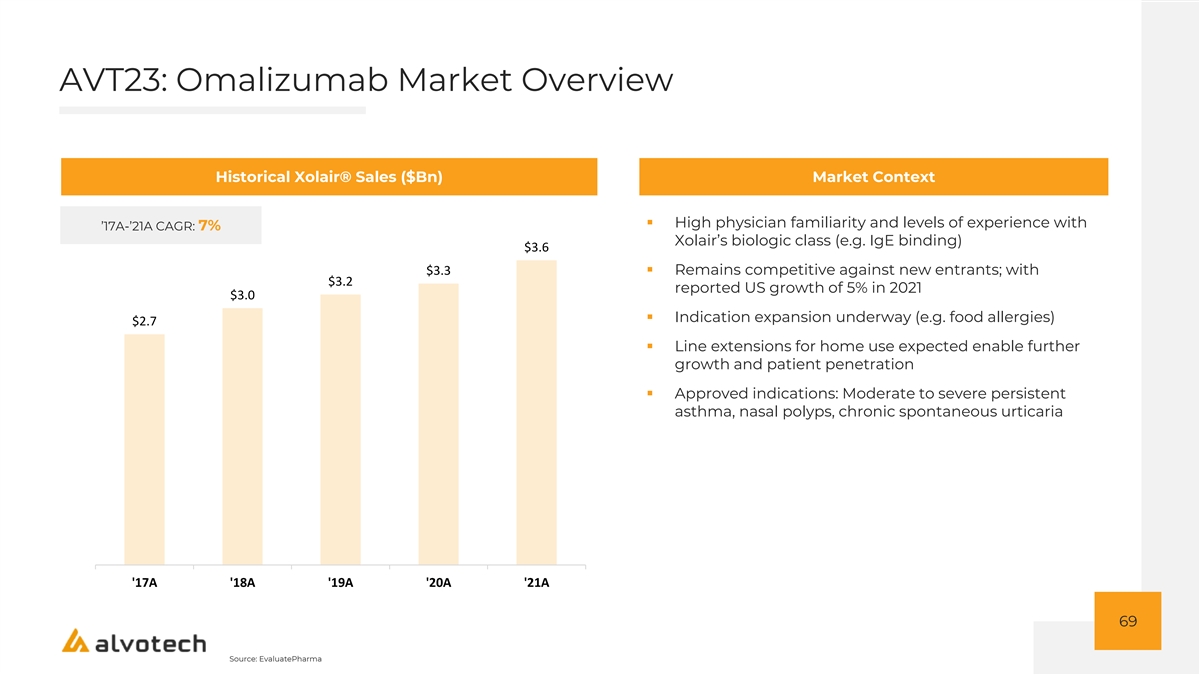

Per EvaluatePharma; originator sales based on expected peak sales of reference products from 2021 – 2026 2. Submission of dossier, filing and/or approval timing may vary among jurisdictions. Estimate reflects timing of first approval. Regulatory processes are lengthy, time consuming and inherently unpredictable and may be delayed for reasons beyond our control. Note, future filing dates are estimates. See slide 80 for more information AVT23: BiosanaPharma Agreement Overview On February 2, 2022, Alvotech and BiosanaPharma entered into an exclusive global licensing agreement to co-develop AVT23 AVT23 Overview 3C Technology Platform ▪ AVT23 (aka BP001) is a late-stage biosimilar candidate for Xolair ▪ High productivity, flexible, small footprint manufacturing platform (1) (omalizumab), a biologic with expected peak sales of $3.6Bn that can cut production costs by at least 90% − Xolair is currently approved for asthma, chronic idiopathic urticaria − Targeted to make 1 kg of drug substance per week at a 50L and severe chronic rhinosinusitis with nasal polyps bioreactor scale − There are currently no approved biosimilars of Xolair ▪ Bespoke process development ▪ PK study of AVT23 has been completed and demonstrated − Upstream Process: proprietary IP based on High Cell Density comparable bioavailability, safety, tolerability and immunogenicity to continuous perfusion culturing with alternating bioreactor use Xolair − Downstream Process: based on Simulated Moving Bed Summary Licensing Terms chromatography combined with flow through filtration ▪ Continuous production platform achieves higher yields while still 1 AVT23 will be jointly developed by Alvotech and BiosanaPharma using the same biochemistry as existing batch processes 2 Alvotech to receive exclusive global rights BiosanaPharma to receive an upfront payment and will be 3 eligible for certain tiered sales royalties AVT23 will be produced using BiosanaPharma’s proprietary 3C 4 process technology 30 Source: EvaluatePharma Notes: 1.

Per EvaluatePharma, based on expected peak sales of reference product from 2021 - 2026 Corporate Sustainability and ESG at Alvotech Strong Thematic Basis Strong Intrinsic Qualities Strong Commitment to ESG • Materiality assessment performed • Biosimilars promote the • Scope 1 and 2 carbon neutral sustainability of healthcare systems • Expect to publish up to 30 ESG o Manufacturing utilizes nearly by improving patient access: disclosures & indicators after close, 100% of electricity from providing lower cost alternatives to based on NASDAQ and/or GRI renewable energy sources higher priced biologics frameworks o Located in Iceland which is an • Key policies to be implemented in • Biologics are a growing class of isolated energy system based on connection with business combination medicines that in 2020 accounted hydro and geothermal resources for almost one third of the global o Governance, code of ethics, market for pharmaceuticals by • Limited water scarcity and wildfire risks whistleblower, anti-harassment, (1) value and data privacy protection • Biologics are biodegradable: limits • Limited public comps for global pure exposure to Pharmaceuticals in o Annual equal pay audits and play model provides investors Environment (PIE) issues employee engagement survey exposure to the social and economic • Long term commitment to investing benefits of biosimilars• R&D driven business model and advancing our ESG platform 31 1.

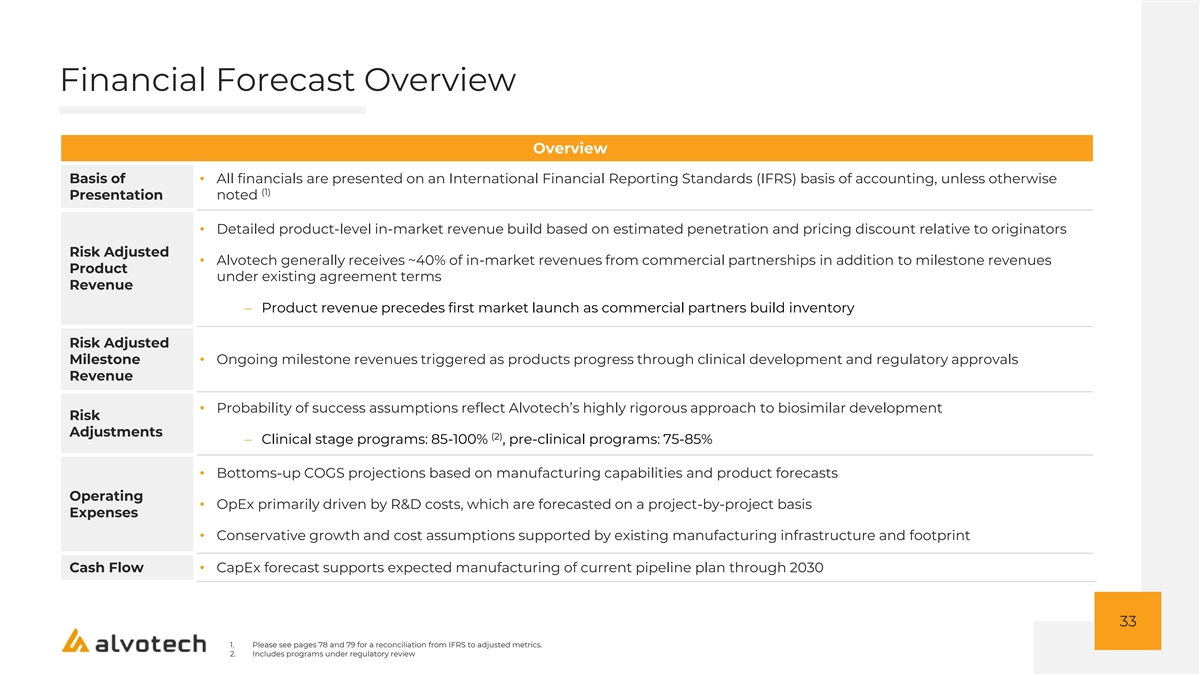

IQVIA INSTITUTE; Spotlight on Biosimilars, Optimizing The Sustainability of Healthcare Systems, June 2021 Financial Forecast Overview Overview Basis of • All financials are presented on an International Financial Reporting Standards (IFRS) basis of accounting, unless otherwise (1) Presentation noted • Detailed product-level in-market revenue build based on estimated penetration and pricing discount relative to originators Risk Adjusted • Alvotech generally receives ~40% of in-market revenues from commercial partnerships in addition to milestone revenues Product under existing agreement terms Revenue − Product revenue precedes first market launch as commercial partners build inventory Risk Adjusted Milestone • Ongoing milestone revenues triggered as products progress through clinical development and regulatory approvals Revenue • Probability of success assumptions reflect Alvotech’s highly rigorous approach to biosimilar development Risk Adjustments (2) − Clinical stage programs: 85-100% , pre-clinical programs: 75-85% • Bottoms-up COGS projections based on manufacturing capabilities and product forecasts Operating • OpEx primarily driven by R&D costs, which are forecasted on a project-by-project basis Expenses • Conservative growth and cost assumptions supported by existing manufacturing infrastructure and footprint Cash Flow• CapEx forecast supports expected manufacturing of current pipeline plan through 2030 33 1.

ATTRACTIVE FINANCIAL PROFILE

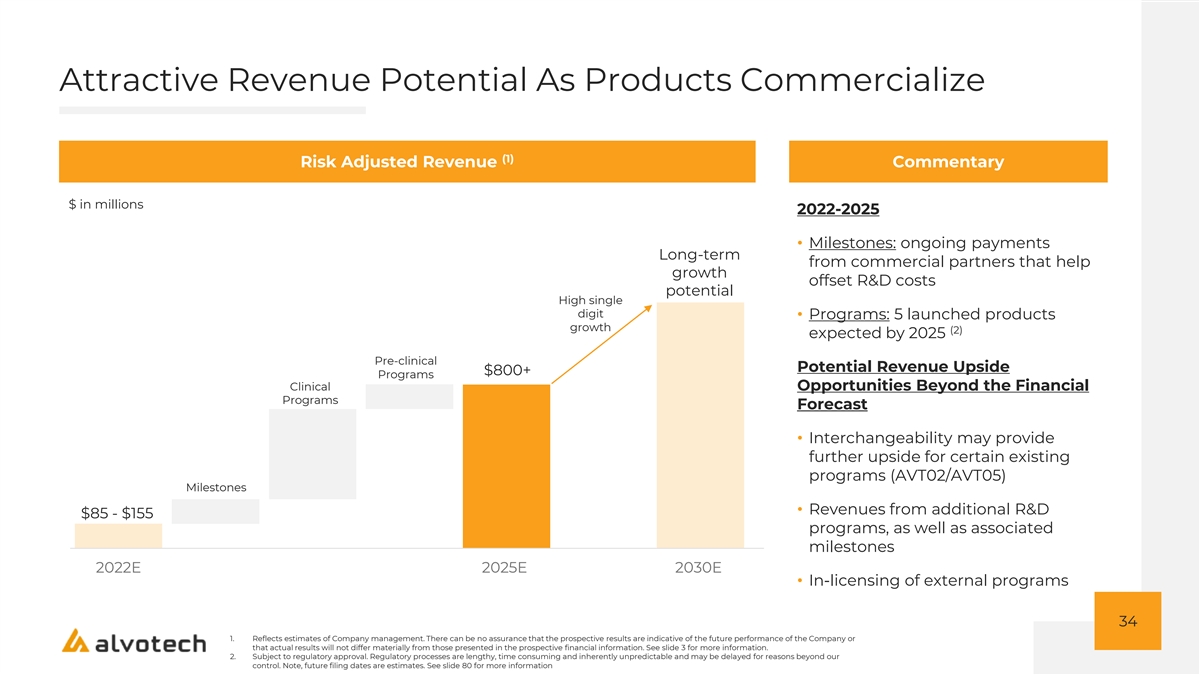

Please see pages 78 and 79 for a reconciliation from IFRS to adjusted metrics. 2. Includes programs under regulatory review Attractive Revenue Potential As Products Commercialize (1) Risk Adjusted Revenue Commentary $ in millions 2022-2025 • Milestones: ongoing payments Long-term from commercial partners that help growth offset R&D costs potential High single digit • Programs: 5 launched products growth (2) expected by 2025 Pre-clinical Potential Revenue Upside $800+ Programs Clinical Opportunities Beyond the Financial Programs Forecast • Interchangeability may provide further upside for certain existing programs (AVT02/AVT05) Milestones • Revenues from additional R&D $85 - $155 programs, as well as associated milestones 2022E 2025E 2030E • In-licensing of external programs 34 1.

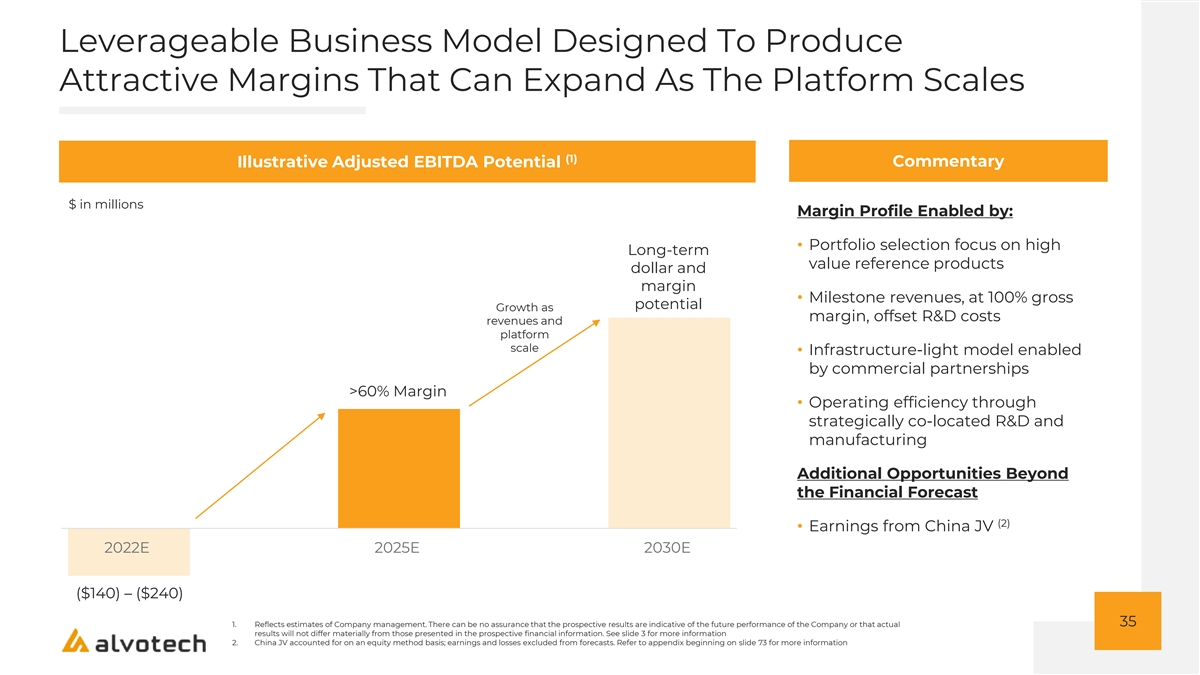

Reflects estimates of Company management. There can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. See slide 3 for more information. 2. Subject to regulatory approval. Regulatory processes are lengthy, time consuming and inherently unpredictable and may be delayed for reasons beyond our control. Note, future filing dates are estimates. See slide 80 for more information Leverageable Business Model Designed To Produce Attractive Margins That Can Expand As The Platform Scales (1) Illustrative Adjusted EBITDA Potential Commentary $ in millions Margin Profile Enabled by: • Portfolio selection focus on high Long-term value reference products dollar and margin • Milestone revenues, at 100% gross potential Growth as margin, offset R&D costs revenues and platform scale • Infrastructure-light model enabled by commercial partnerships >60% Margin • Operating efficiency through strategically co-located R&D and manufacturing Additional Opportunities Beyond the Financial Forecast (2) • Earnings from China JV 2022E 2025E 2030E ($140) – ($240) 35 1.

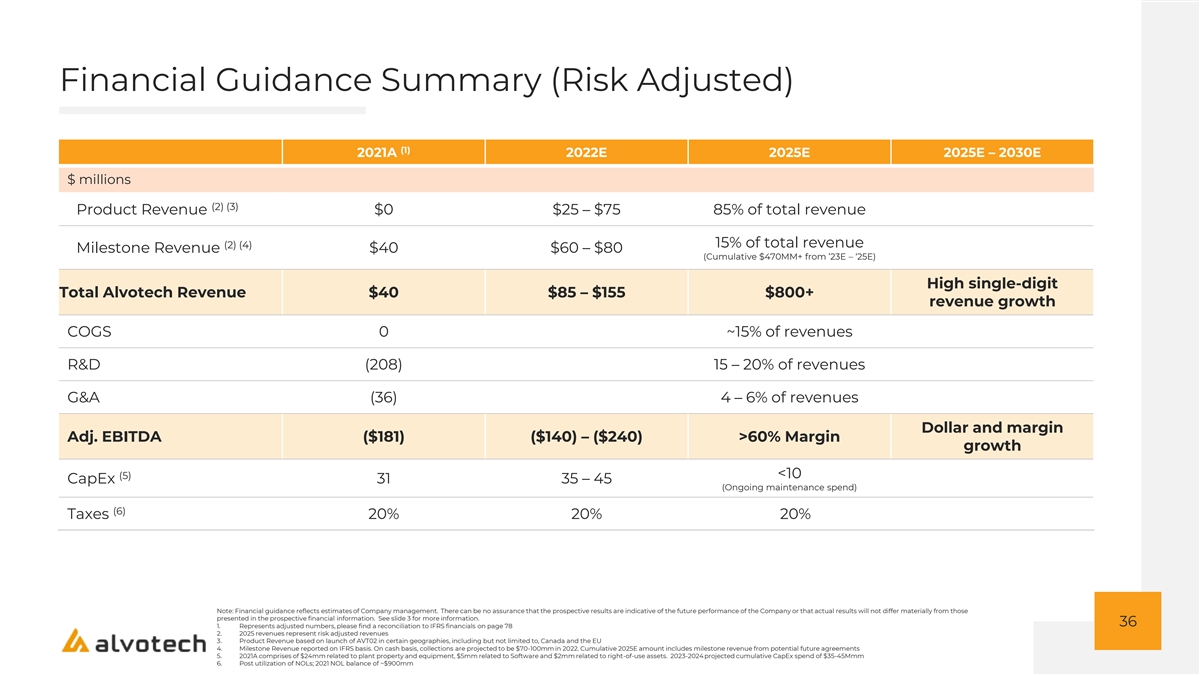

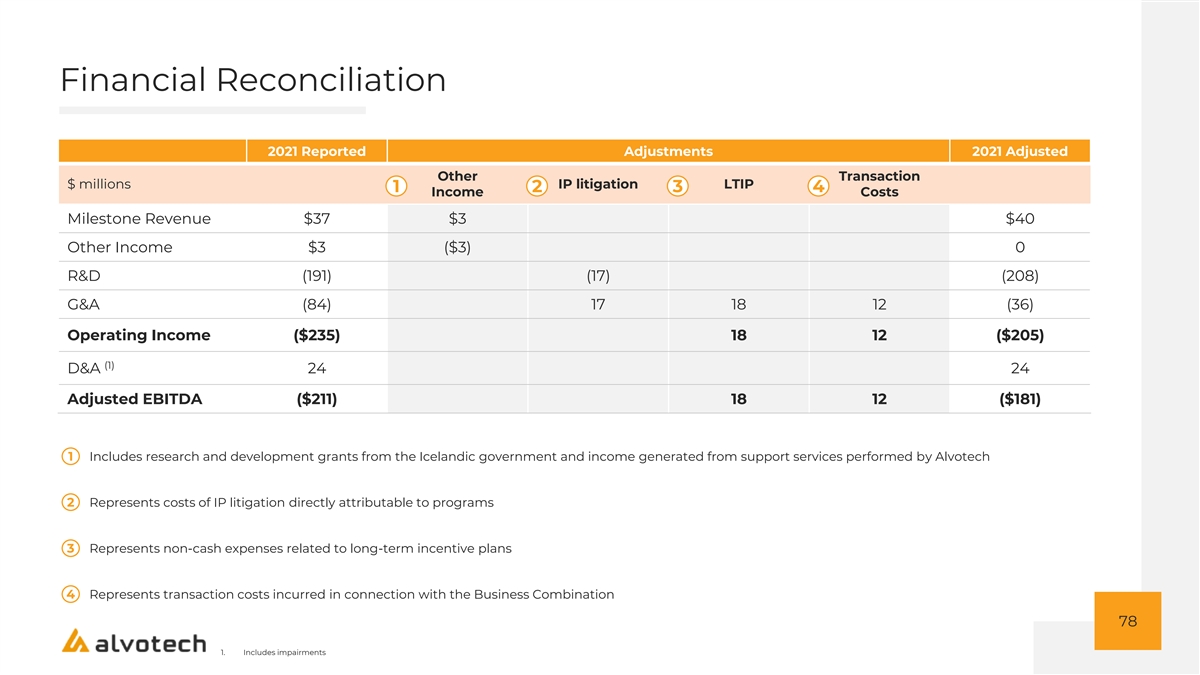

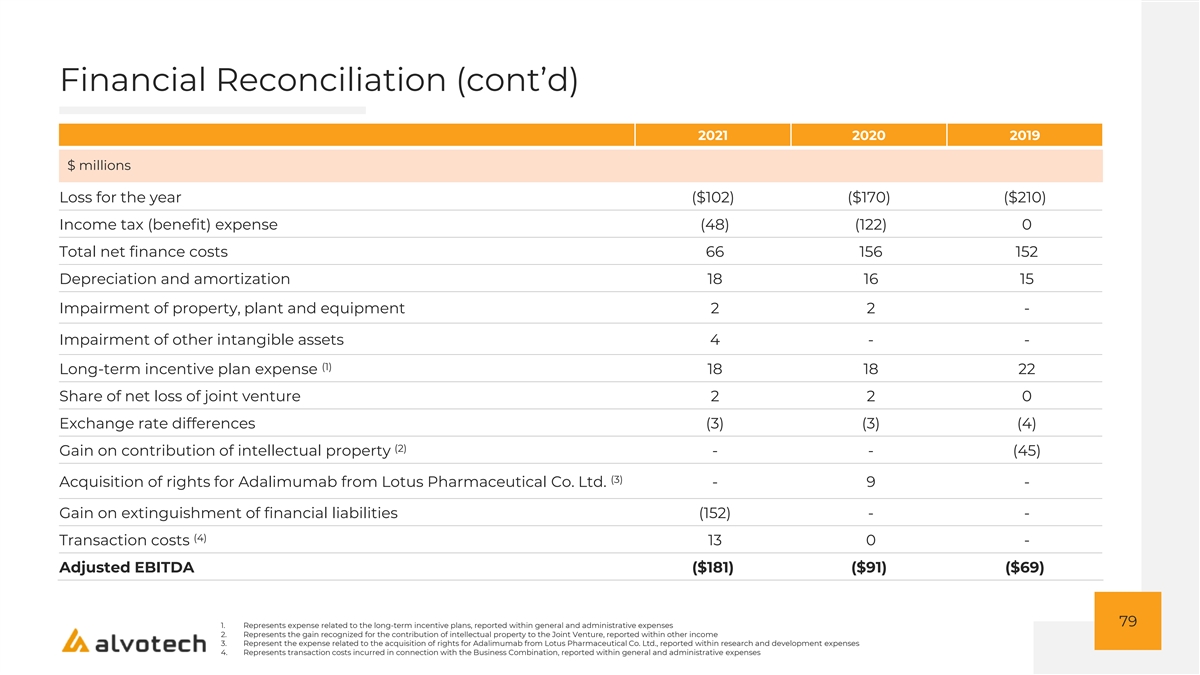

Reflects estimates of Company management. There can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. See slide 3 for more information 2. China JV accounted for on an equity method basis; earnings and losses excluded from forecasts. Refer to appendix beginning on slide 73 for more information Financial Guidance Summary (Risk Adjusted) (1) 2021A 2022E 2025E 2025E – 2030E $ millions (2) (3) Product Revenue $0 $25 – $75 85% of total revenue 15% of total revenue (2) (4) Milestone Revenue $40 $60 – $80 (Cumulative $470MM+ from ’23E – ‘25E) High single-digit Total Alvotech Revenue $40 $85 – $155 $800+ revenue growth COGS 0 ~15% of revenues R&D (208) 15 – 20% of revenues G&A (36) 4 – 6% of revenues Dollar and margin Adj.

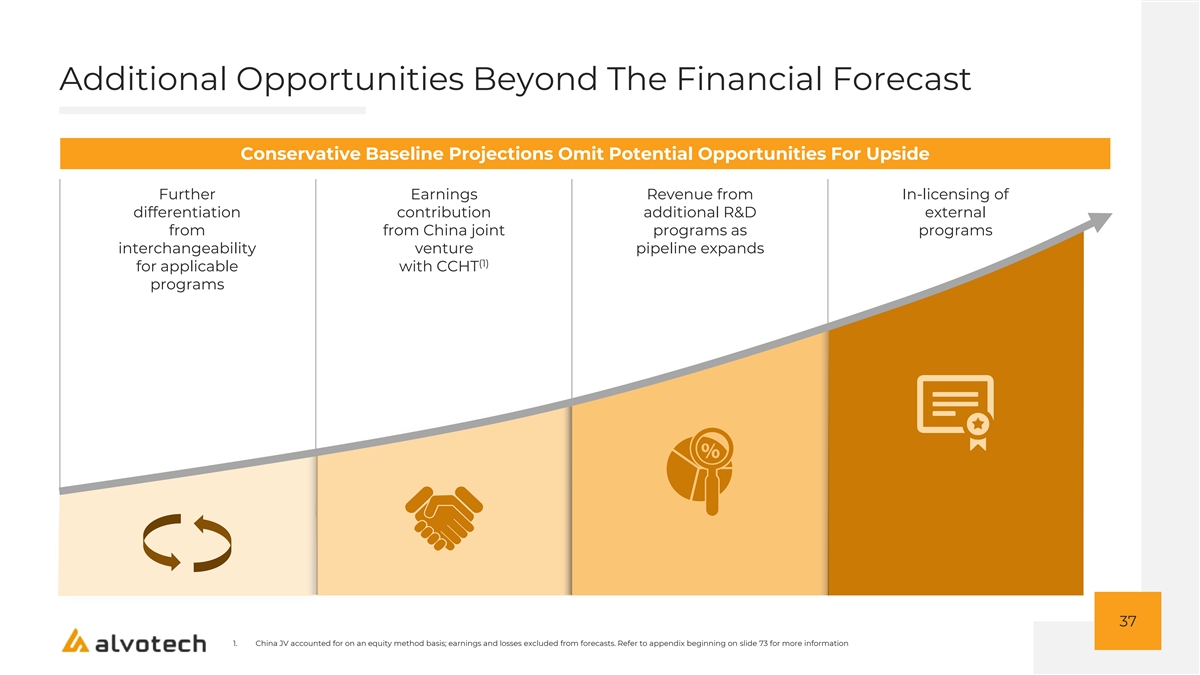

EBITDA ($181) ($140) – ($240) >60% Margin growth (5) <10 CapEx 31 35 – 45 (Ongoing maintenance spend) (6) Taxes 20% 20% 20% Note: Financial guidance reflects estimates of Company management. There can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. See slide 3 for more information. 36 1. Represents adjusted numbers, please find a reconciliation to IFRS financials on page 78 2. 2025 revenues represent risk adjusted revenues 3. Product Revenue based on launch of AVT02 in certain geographies, including but not limited to, Canada and the EU 4. Milestone Revenue reported on IFRS basis. On cash basis, collections are projected to be $70-100mm in 2022. Cumulative 2025E amount includes milestone revenue from potential future agreements 5. 2021A comprises of $24mm related to plant property and equipment, $5mm related to Software and $2mm related to right-of-use assets. 2023-2024 projected cumulative CapEx spend of $35-45Mmm 6. Post utilization of NOLs; 2021 NOL balance of ~$900mm Additional Opportunities Beyond The Financial Forecast Conservative Baseline Projections Omit Potential Opportunities For Upside Further Earnings Revenue from In-licensing of differentiation contribution additional R&D external from from China joint programs as programs interchangeability venture pipeline expands (1) for applicable with CCHT programs 37 1.

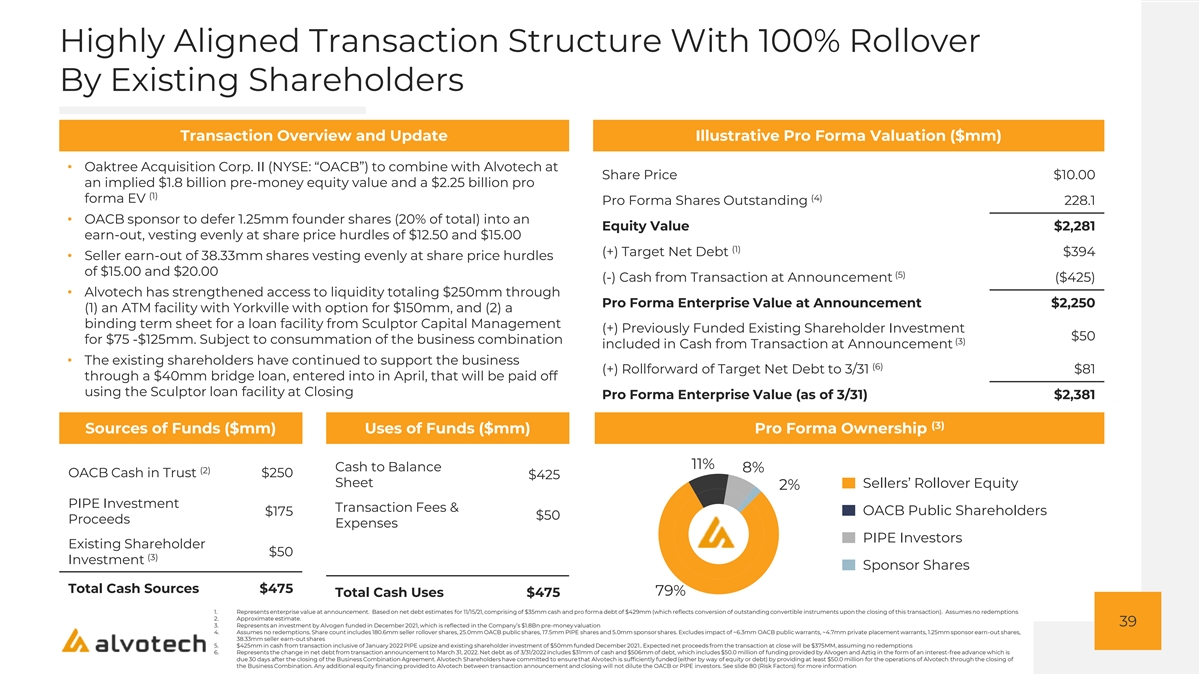

China JV accounted for on an equity method basis; earnings and losses excluded from forecasts. Refer to appendix beginning on slide 73 for more information Highly Aligned Transaction Structure With 100% Rollover By Existing Shareholders Transaction Overview and Update Illustrative Pro Forma Valuation ($mm) • Oaktree Acquisition Corp.

TRANSACTION SUMMARY

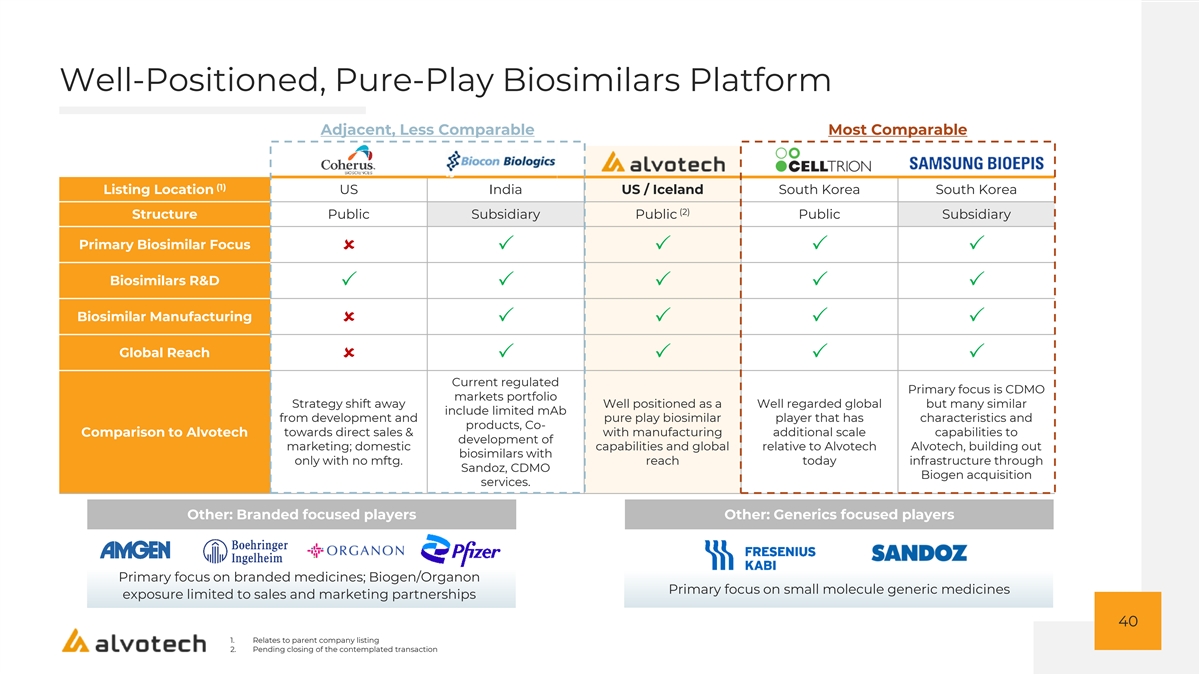

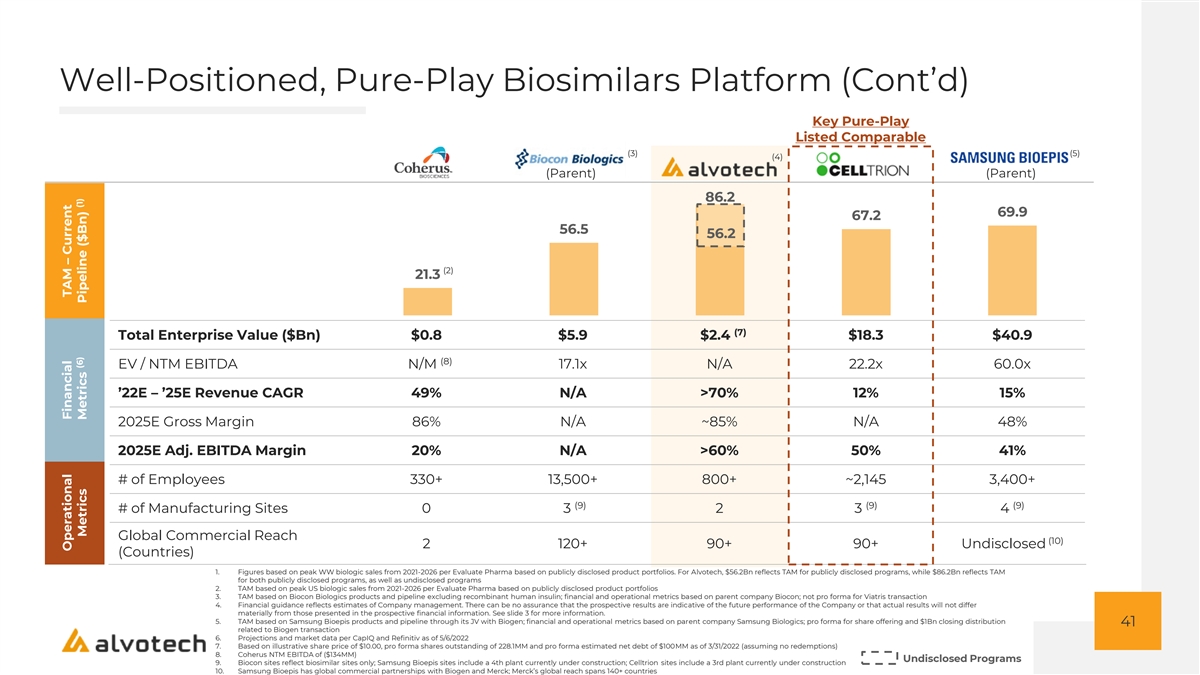

II (NYSE: “OACB”) to combine with Alvotech at Share Price $10.00 an implied $1.8 billion pre-money equity value and a $2.25 billion pro (1) (4) forma EV Pro Forma Shares Outstanding 228.1 • OACB sponsor to defer 1.25mm founder shares (20% of total) into an Equity Value $2,281 earn-out, vesting evenly at share price hurdles of $12.50 and $15.00 (1) (+) Target Net Debt $394 • Seller earn-out of 38.33mm shares vesting evenly at share price hurdles of $15.00 and $20.00 (5) (-) Cash from Transaction at Announcement ($425) • Alvotech has strengthened access to liquidity totaling $250mm through Pro Forma Enterprise Value at Announcement $2,250 (1) an ATM facility with Yorkville with option for $150mm, and (2) a binding term sheet for a loan facility from Sculptor Capital Management (+) Previously Funded Existing Shareholder Investment $50 for $75 -$125mm. Subject to consummation of the business combination (3) included in Cash from Transaction at Announcement • The existing shareholders have continued to support the business (6) (+) Rollforward of Target Net Debt to 3/31 $81 through a $40mm bridge loan, entered into in April, that will be paid off using the Sculptor loan facility at Closing Pro Forma Enterprise Value (as of 3/31) $2,381 (3) Sources of Funds ($mm) Uses of Funds ($mm) Pro Forma Ownership 11% Cash to Balance 8% (2) OACB Cash in Trust $250 $425 Sheet Sellers’ Rollover Equity 2% PIPE Investment Transaction Fees & OACB Public Shareholders $175 $50 Proceeds Expenses PIPE Investors Existing Shareholder $50 (3) Investment Sponsor Shares Total Cash Sources $475 79% Total Cash Uses $475 1. Represents enterprise value at announcement. Based on net debt estimates for 11/15/21, comprising of $35mm cash and pro forma debt of $429mm (which reflects conversion of outstanding convertible instruments upon the closing of this transaction). Assumes no redemptions 2. Approximate estimate. 39 3. Represents an investment by Alvogen funded in December 2021, which is reflected in the Company’s $1.8Bn pre-money valuation 4. Assumes no redemptions. Share count includes 180.6mm seller rollover shares, 25.0mm OACB public shares, 17.5mm PIPE shares and 5.0mm sponsor shares. Excludes impact of ~6.3mm OACB public warrants, ~4.7mm private placement warrants, 1.25mm sponsor earn-out shares, 38.33mm seller earn-out shares 5. $425mm in cash from transaction inclusive of January 2022 PIPE upsize and existing shareholder investment of $50mm funded December 2021.. Expected net proceeds from the transaction at close will be $375MM, assuming no redemptions 6. Represents the change in net debt from transaction announcement to March 31, 2022. Net debt as of 3/31/2022 includes $31mm of cash and $506mm of debt, which includes $50.0 million of funding provided by Alvogen and Aztiq in the form of an interest-free advance which is due 30 days after the closing of the Business Combination Agreement. Alvotech Shareholders have committed to ensure that Alvotech is sufficiently funded (either by way of equity or debt) by providing at least $50.0 million for the operations of Alvotech through the closing of the Business Combination. Any additional equity financing provided to Alvotech between transaction announcement and closing will not dilute the OACB or PIPE investors. See slide 80 (Risk Factors) for more information Well-Positioned, Pure-Play Biosimilars Platform Adjacent, Less Comparable Most Comparable (1) Listing Location US India US / Iceland South Korea South Korea (2) Structure Public Subsidiary Public Public Subsidiary Primary Biosimilar Focus ûPPPP Biosimilars R&D PPPPP Biosimilar Manufacturing ûPPPP Global Reach ûPPPP Current regulated Primary focus is CDMO markets portfolio Strategy shift away Well positioned as a Well regarded global but many similar include limited mAb from development and pure play biosimilar player that has characteristics and products, Co- towards direct sales & with manufacturing additional scale capabilities to Comparison to Alvotech development of marketing; domestic capabilities and global relative to Alvotech Alvotech, building out biosimilars with only with no mftg.

reach today infrastructure through Sandoz, CDMO Biogen acquisition services. Other: Branded focused players Other: Generics focused players Primary focus on branded medicines; Biogen/Organon Primary focus on small molecule generic medicines exposure limited to sales and marketing partnerships 40 1. Relates to parent company listing 2. Pending closing of the contemplated transaction Well-Positioned, Pure-Play Biosimilars Platform (Cont’d) Key Pure-Play Listed Comparable (3) (5) (4) (Parent) (Parent) 86.2 69.9 67.2 56.5 56.2 (2) 21.3 (7) Total Enterprise Value ($Bn) $0.8 $5.9 $2.4 $18.3 $40.9 (8) EV / NTM EBITDA N/M 17.1x N/A 22.2x 60.0x ’22E – ’25E Revenue CAGR 49% N/A >70% 12% 15% 2025E Gross Margin 86% N/A ~85% N/A 48% 2025E Adj.

EBITDA Margin 20% N/A >60% 50% 41% # of Employees 330+ 13,500+ 800+ ~2,145 3,400+ (9) (9) (9) # of Manufacturing Sites 0 3 2 3 4 Global Commercial Reach (10) 2 120+ 90+ 90+ Undisclosed (Countries) 1. Figures based on peak WW biologic sales from 2021-2026 per Evaluate Pharma based on publicly disclosed product portfolios. For Alvotech, $56.2Bn reflects TAM for publicly disclosed programs, while $86.2Bn reflects TAM for both publicly disclosed programs, as well as undisclosed programs 2. TAM based on peak US biologic sales from 2021-2026 per Evaluate Pharma based on publicly disclosed product portfolios 3. TAM based on Biocon Biologics products and pipeline excluding recombinant human insulin; financial and operational metrics based on parent company Biocon; not pro forma for Viatris transaction 4. Financial guidance reflects estimates of Company management. There can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. See slide 3 for more information. 5. TAM based on Samsung Bioepis products and pipeline through its JV with Biogen; financial and operational metrics based on parent company Samsung Biologics; pro forma for share offering and $1Bn closing distribution 41 related to Biogen transaction 6. Projections and market data per CapIQ and Refinitiv as of 5/6/2022 7. Based on illustrative share price of $10.00, pro forma shares outstanding of 228.1MM and pro forma estimated net debt of $100MM as of 3/31/2022 (assuming no redemptions) 8. Coherus NTM EBITDA of ($134MM) Undisclosed Programs 9. Biocon sites reflect biosimilar sites only; Samsung Bioepis sites include a 4th plant currently under construction; Celltrion sites include a 3rd plant currently under construction 10. Samsung Bioepis has global commercial partnerships with Biogen and Merck; Merck’s global reach spans 140+ countries Operational Financial TAM – Current (6) (1) Metrics Metrics Pipeline ($Bn)

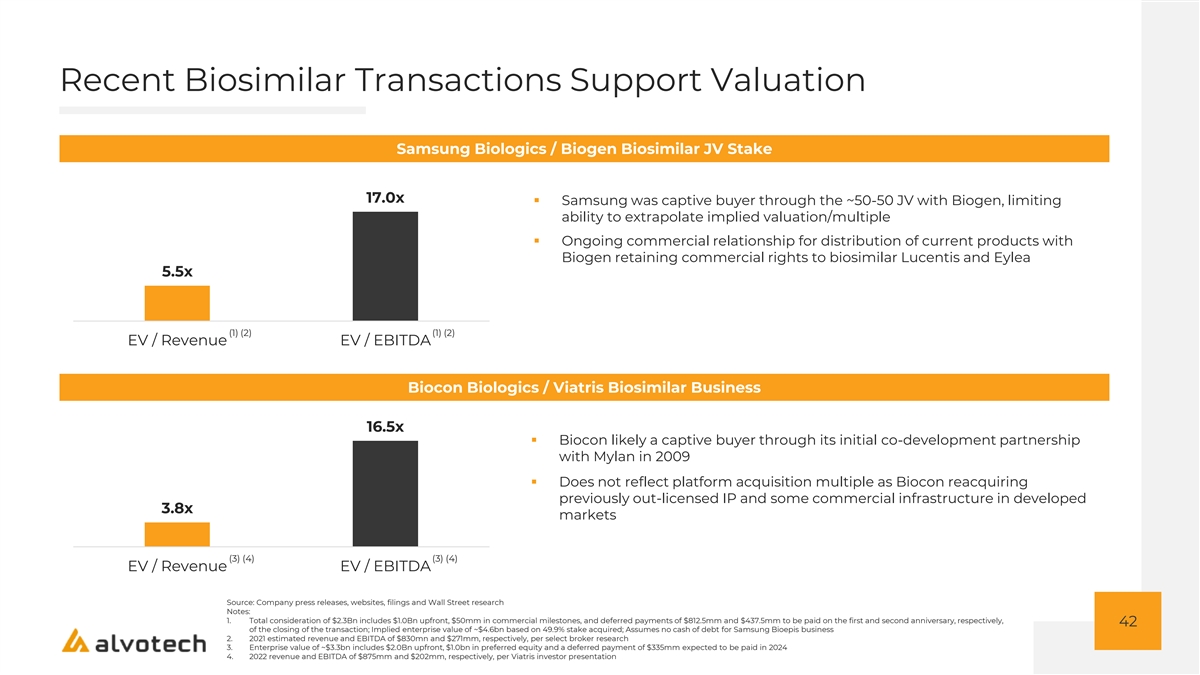

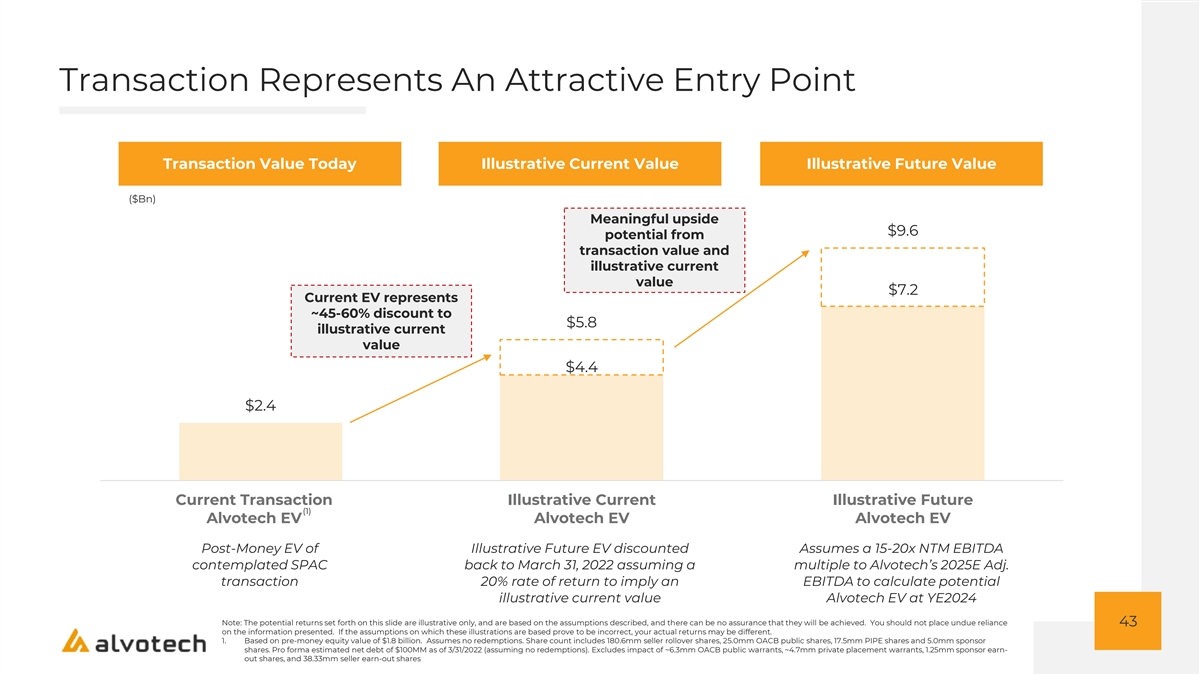

Recent Biosimilar Transactions Support Valuation Samsung Biologics / Biogen Biosimilar JV Stake 17.0x ▪ Samsung was captive buyer through the ~50-50 JV with Biogen, limiting ability to extrapolate implied valuation/multiple ▪ Ongoing commercial relationship for distribution of current products with Biogen retaining commercial rights to biosimilar Lucentis and Eylea 5.5x (1) (2) (1) (2) EV / Revenue EV / EBITDA Biocon Biologics / Viatris Biosimilar Business 16.5x ▪ Biocon likely a captive buyer through its initial co-development partnership with Mylan in 2009 ▪ Does not reflect platform acquisition multiple as Biocon reacquiring previously out-licensed IP and some commercial infrastructure in developed 3.8x markets (3) (4) (3) (4) EV / Revenue EV / EBITDA Source: Company press releases, websites, filings and Wall Street research Notes: 1. Total consideration of $2.3Bn includes $1.0Bn upfront, $50mm in commercial milestones, and deferred payments of $812.5mm and $437.5mm to be paid on the first and second anniversary, respectively, 42 of the closing of the transaction; Implied enterprise value of ~$4.6bn based on 49.9% stake acquired; Assumes no cash of debt for Samsung Bioepis business 2. 2021 estimated revenue and EBITDA of $830mn and $271mm, respectively, per select broker research 3. Enterprise value of ~$3.3bn includes $2.0Bn upfront, $1.0bn in preferred equity and a deferred payment of $335mm expected to be paid in 2024 4. 2022 revenue and EBITDA of $875mm and $202mm, respectively, per Viatris investor presentation Transaction Represents An Attractive Entry Point Transaction Value Today Illustrative Current Value Illustrative Future Value ($Bn) Meaningful upside $9.6 potential from transaction value and illustrative current value $7.2 Current EV represents ~45-60% discount to $5.8 illustrative current value $4.4 $2.4 Current Transaction Illustrative Current Illustrative Future (1) Alvotech EV Alvotech EV Alvotech EV Post-Money EV of Illustrative Future EV discounted Assumes a 15-20x NTM EBITDA contemplated SPAC back to March 31, 2022 assuming a multiple to Alvotech’s 2025E Adj.

transaction 20% rate of return to imply an EBITDA to calculate potential illustrative current value Alvotech EV at YE2024 Note: The potential returns set forth on this slide are illustrative only, and are based on the assumptions described, and there can be no assurance that they will be achieved. You should not place undue reliance 43 on the information presented. If the assumptions on which these illustrations are based prove to be incorrect, your actual returns may be different. 1. Based on pre-money equity value of $1.8 billion. Assumes no redemptions. Share count includes 180.6mm seller rollover shares, 25.0mm OACB public shares, 17.5mm PIPE shares and 5.0mm sponsor shares. Pro forma estimated net debt of $100MM as of 3/31/2022 (assuming no redemptions). Excludes impact of ~6.3mm OACB public warrants, ~4.7mm private placement warrants, 1.25mm sponsor earn- out shares, and 38.33mm seller earn-out shares Alvotech: A Differentiated Global Biosimilars Company PROVEN LEADERSHIP TEAM 1 SIGNIFICANT MARKET OPPORTUNITY 2 PURPOSE-BUILT BIOSIMILAR PLATFORM 3 GLOBAL COMMERCIAL PARTNER NETWORK 4 5 DIVERSE PIPELINE WITH SIGNIFICANT TAM ATTRACTIVE FINANCIAL PROFILE 6 44

APPENDIX SELECT MANAGEMENT TEAM BIOGRAPHIES