|

Oklahoma

|

001-38656

|

20-0763496

|

|

(State or other jurisdiction of incorporation)

|

(Commission File Number)

|

(IRS Employer Identification No.)

|

| ☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

|

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

|

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

|

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

|

|

Title of each class

|

Trading Symbol(s)

|

Name of each exchange on which registered

|

|

| Common Stock, $0.01 par value |

BSVN |

The NASDAQ Global Select Market

|

| Item 2.02. |

Results of Operations and Financial Condition

|

| Item 7.01 |

Regulation FD Disclosure

|

| Item 9.01 |

Financial Statements and Exhibits

|

|

(d)

|

Exhibits.

|

|

Item

|

Description

|

||

|

Press Release dated October 15, 2025

|

|||

|

Third Quarter 2025 Investor Presentation

|

|

BANK7 CORP.

|

||

|

Date: October 15, 2025

|

By:

|

/s/ Kelly J. Harris

|

|

Kelly J. Harris

|

||

|

Executive Vice President and Chief Financial Officer

|

||

|

-

|

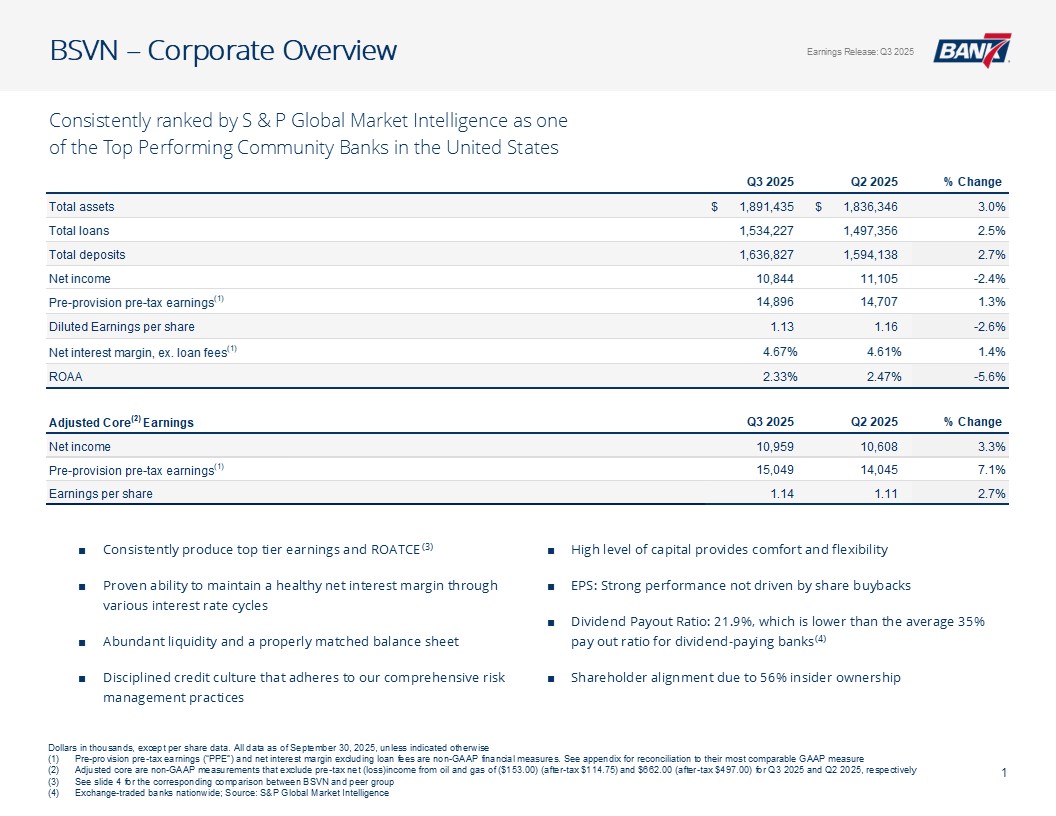

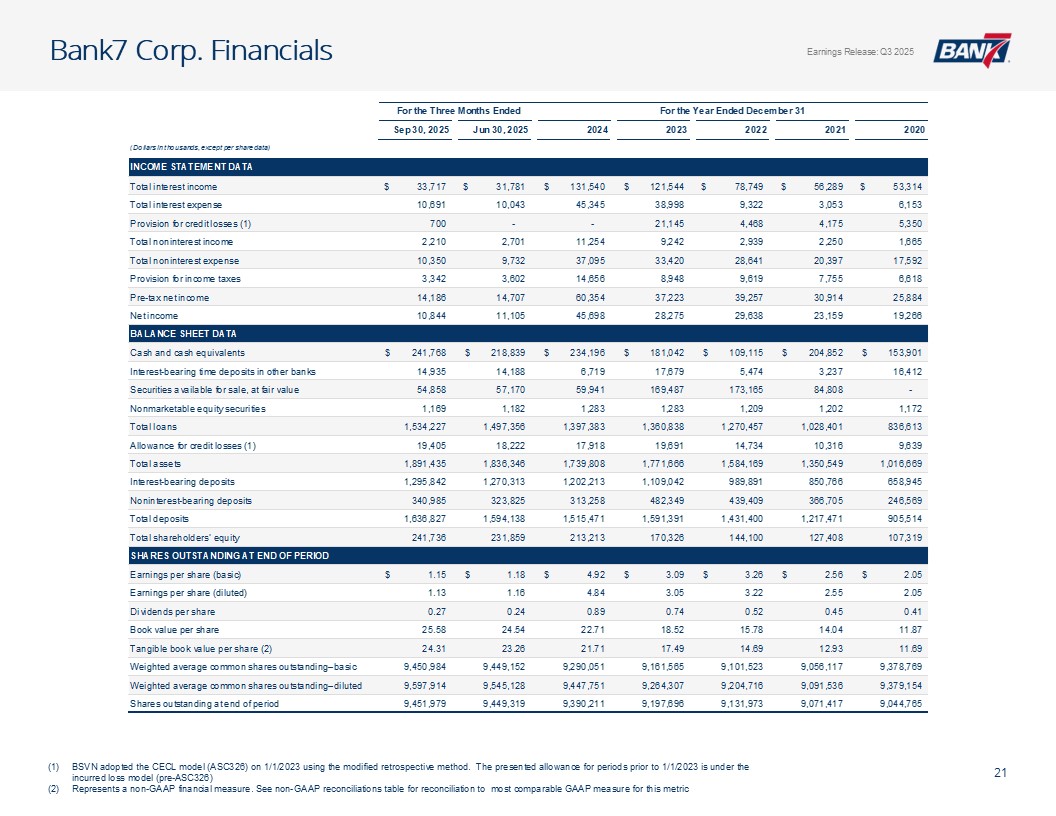

Net income of $10.8 million compared to $11.1 million, a decrease of 2.35%

|

|

-

|

Earnings per share of $1.13 compared to $1.16, a decrease of 2.59%

|

|

-

|

Total assets of $1.9 billion compared to $1.8 billion, an increase of 3.00%

|

|

-

|

Total loans of $1.5 billion compared to $1.5 billion, an increase of 2.46%

|

|

-

|

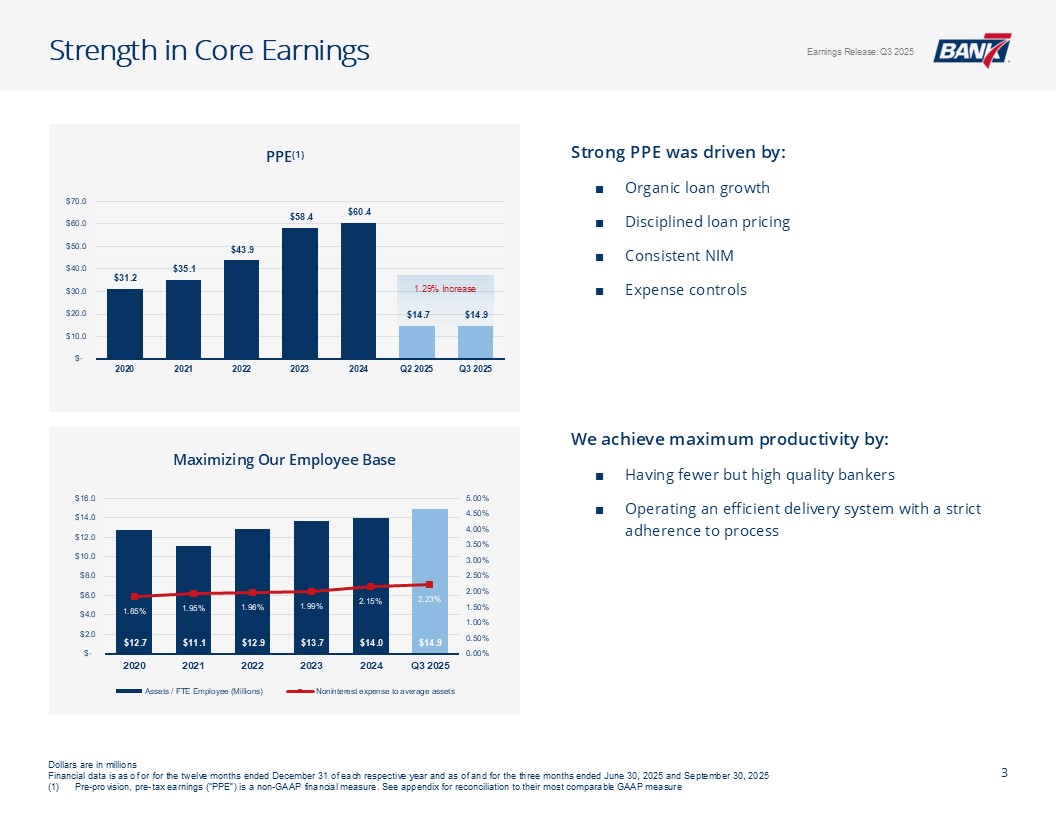

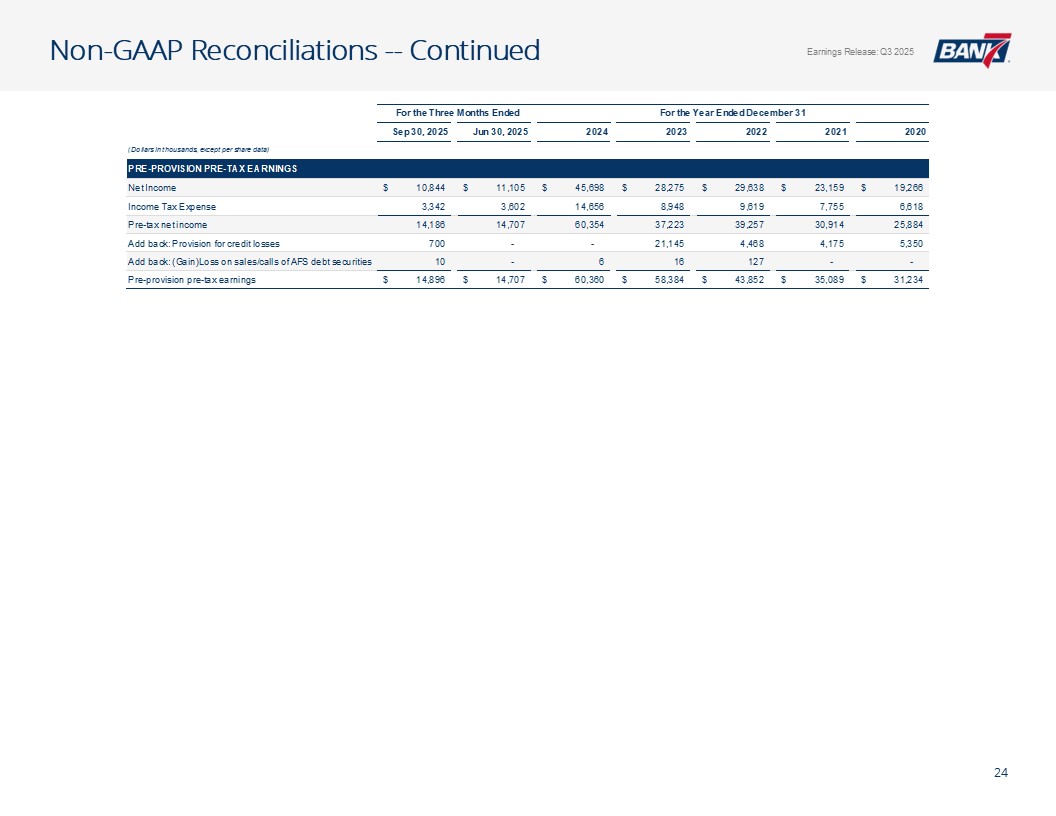

Pre-provision pre-tax earnings (“PPE”) of $14.9 million compared to $14.7 million, an increase of 1.29%

|

|

-

|

Total interest income of $33.7 million compared to $31.8 million, an increase of 6.09%

|

|

For the Three Months Ended

|

||||||||

|

September 30,

2025

|

June 30,

2025

|

|||||||

|

Calculation of Pre-Provision Pre-Tax Earnings (“PPE”)

|

(Dollars in thousands)

|

|||||||

|

Net Income

|

$

|

10,844

|

$

|

11,105

|

||||

|

Income Tax Expense

|

3,342

|

3,602

|

||||||

|

Pre-tax net income

|

14,186

|

14,707

|

||||||

|

Add back: Provision for credit losses

|

700

|

-

|

||||||

|

Add back: (Gain)Loss on sales/calls of AFS debt securities

|

10

|

-

|

||||||

|

Pre-provision pre-tax earnings

|

$

|

14,896

|

$

|

14,707

|

||||

|

Assets

|

September 30, 2025

(unaudited) |

December 31, 2024

|

||||||

|

|

(Dollars in thousands)

|

|||||||

|

Cash and due from banks

|

$

|

241,768

|

$

|

234,196

|

||||

|

Interest-bearing time deposits in other banks

|

14,935

|

6,719

|

||||||

|

Available-for-sale debt securities (amortized cost of $58,771 and

$66,445 at September 30, 2025 and December 31, 2024)

|

54,858

|

59,941

|

||||||

|

Loans, net of allowance for credit losses of $19,405 and $17,918 at September 30,

2025 and December 31, 2024, respectively

|

1,514,822

|

1,379,465

|

||||||

|

Loans held for sale

|

1,883

|

-

|

||||||

|

Premises and equipment, net

|

21,057

|

18,137

|

||||||

|

Nonmarketable equity securities

|

1,169

|

1,283

|

||||||

|

Core deposit intangibles

|

784

|

878

|

||||||

|

Goodwill

|

11,208

|

8,458

|

||||||

|

Interest receivable and other assets

|

28,951

|

30,731

|

||||||

|

|

||||||||

|

Total assets

|

$

|

1,891,435

|

$

|

1,739,808

|

||||

|

|

||||||||

|

Liabilities and Shareholders’ Equity

|

||||||||

|

|

||||||||

|

Deposits

|

||||||||

|

Noninterest-bearing

|

$

|

340,985

|

$

|

313,258

|

||||

|

Interest-bearing

|

1,295,842

|

1,202,213

|

||||||

|

|

||||||||

|

Total deposits

|

1,636,827

|

1,515,471

|

||||||

|

|

||||||||

|

Income taxes payable

|

146

|

77

|

||||||

|

Interest payable and other liabilities

|

12,726

|

11,047

|

||||||

|

|

||||||||

|

Total liabilities

|

1,649,699

|

1,526,595

|

||||||

|

|

||||||||

|

Shareholders’ equity

|

||||||||

|

Common stock, $0.01 par value; 50,000,000 shares authorized; shares issued and outstanding: 9,451,979 and

9,390,211 at September 30, 2025and December 31, 2024, respectively

|

95

|

94

|

||||||

|

Additional paid-in capital

|

103,184

|

101,809

|

||||||

|

Retained earnings

|

141,478

|

116,281

|

||||||

|

Accumulated other comprehensive loss

|

(3,021

|

)

|

(4,971

|

)

|

||||

|

|

||||||||

|

Total shareholders’ equity

|

241,736

|

213,213

|

||||||

|

|

||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,891,435

|

$

|

1,739,808

|

||||

|

|

Three Months Ended

|

Nine Months Ended

|

||||||||||||||

|

|

September 30,

|

September 30,

|

||||||||||||||

|

|

2025

(unaudited) |

2024

(unaudited) |

2025

(unaudited) |

2024

(unaudited) |

||||||||||||

|

Interest Income

|

(Dollars in thousands)

|

|||||||||||||||

|

Loans, including fees

|

$

|

30,914

|

$

|

30,791

|

$

|

87,207

|

$

|

89,834

|

||||||||

|

Interest-bearing time deposits in other banks

|

160

|

177

|

406

|

675

|

||||||||||||

|

Debt securities, taxable

|

266

|

303

|

827

|

2,266

|

||||||||||||

|

Debt securities, tax-exempt

|

60

|

69

|

187

|

214

|

||||||||||||

|

Other interest and dividend income

|

2,317

|

2,148

|

7,315

|

6,221

|

||||||||||||

|

|

||||||||||||||||

|

Total interest income

|

33,717

|

33,488

|

95,942

|

99,210

|

||||||||||||

|

|

||||||||||||||||

|

Interest Expense

|

||||||||||||||||

|

Deposits

|

10,691

|

12,271

|

30,334

|

34,752

|

||||||||||||

|

|

||||||||||||||||

|

Total interest expense

|

10,691

|

12,271

|

30,334

|

34,752

|

||||||||||||

|

|

||||||||||||||||

|

Net Interest Income

|

23,026

|

21,217

|

65,608

|

64,458

|

||||||||||||

|

|

||||||||||||||||

|

Provision for Credit Losses

|

700

|

-

|

700

|

-

|

||||||||||||

|

|

||||||||||||||||

|

Net Interest Income After Provision for Credit Losses

|

22,326

|

21,217

|

64,908

|

64,458

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest Income

|

||||||||||||||||

|

Mortgage lending income

|

391

|

103

|

1,000

|

233

|

||||||||||||

|

Loss on sales, prepayments, and calls of available-for-sale debt securities

|

(10

|

)

|

(4

|

)

|

(10

|

)

|

(4

|

)

|

||||||||

|

Service charges on deposit accounts

|

248

|

233

|

697

|

742

|

||||||||||||

|

Other

|

1,581

|

3,345

|

4,976

|

7,881

|

||||||||||||

|

|

||||||||||||||||

|

Total noninterest income

|

2,210

|

3,677

|

6,663

|

8,852

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest Expense

|

||||||||||||||||

|

Salaries and employee benefits

|

5,829

|

5,333

|

16,829

|

15,740

|

||||||||||||

|

Furniture and equipment

|

342

|

258

|

954

|

813

|

||||||||||||

|

Occupancy

|

668

|

711

|

1,890

|

1,985

|

||||||||||||

|

Data and item processing

|

515

|

498

|

1,615

|

1,437

|

||||||||||||

|

Accounting, marketing and legal fees

|

221

|

218

|

484

|

582

|

||||||||||||

|

Regulatory assessments

|

248

|

261

|

545

|

984

|

||||||||||||

|

Advertsing and public relations

|

212

|

129

|

629

|

358

|

||||||||||||

|

Travel, lodging and entertainment

|

112

|

87

|

289

|

270

|

||||||||||||

|

Other

|

2,203

|

1,903

|

5,729

|

5,507

|

||||||||||||

|

|

||||||||||||||||

|

Total noninterest expense

|

10,350

|

9,398

|

28,964

|

27,676

|

||||||||||||

|

|

||||||||||||||||

|

Income Before Taxes

|

14,186

|

15,496

|

42,607

|

45,634

|

||||||||||||

|

Income tax expense

|

3,342

|

3,719

|

10,322

|

11,045

|

||||||||||||

|

Net Income

|

$

|

10,844

|

$

|

11,777

|

$

|

32,285

|

$

|

34,589

|

||||||||

|

|

||||||||||||||||

|

Earnings per common share - basic

|

$

|

1.15

|

$

|

1.26

|

$

|

3.42

|

$

|

3.73

|

||||||||

|

Earnings per common share - diluted

|

1.13

|

1.24

|

3.38

|

3.68

|

||||||||||||

|

Weighted average common shares outstanding - basic

|

9,450,984

|

9,323,622

|

9,440,655

|

9,264,616

|

||||||||||||

|

Weighted average common shares outstanding - diluted

|

9,597,914

|

9,498,318

|

9,565,726

|

9,402,214

|

||||||||||||

|

|

||||||||||||||||

|

Other Comprehensive Income

|

||||||||||||||||

|

Unrealized gains on securities, net of tax expense of $223 and $515 for the three months ended September 30, 2025 and 2024,

respectively; net of tax expense of $406 and $638 for the nine months ended September 30, 2025 and 2024, respectively

|

$

|

713

|

$

|

1,628

|

$

|

1,942

|

$

|

2,025

|

||||||||

|

Reclassification adjustment for realized losses included in net income net of tax of $2 and $1 for the three months ended September 30, 2025, and 2024, respectively; $2 and $1 for the nine

months ended September 30, 2025 and 2024, respectively

|

8

|

3

|

8

|

3

|

||||||||||||

|

Other comprehensive income

|

$

|

721

|

$

|

1,631

|

$

|

1,950

|

$

|

2,028

|

||||||||

|

Comprehensive Income

|

$

|

11,565

|

$

|

13,408

|

$

|

34,235

|

$

|

36,617

|

||||||||

|

|

Net Interest Margin

|

|||||||||||||||||||||||

|

|

For the Three Months Ended September 30,

|

|||||||||||||||||||||||

|

|

2025

(unaudited) |

2024

(unaudited) |

||||||||||||||||||||||

|

|

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

||||||||||||||||||

|

|

(Dollars in thousands)

|

|||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

228,755

|

$

|

2,477

|

4.30

|

%

|

$

|

191,583

|

$

|

2,325

|

4.81

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

45,853

|

266

|

2.30

|

51,172

|

303

|

2.35

|

||||||||||||||||||

|

Debt securities, tax exempt

|

11,972

|

60

|

1.99

|

16,889

|

69

|

1.62

|

||||||||||||||||||

|

Loans held for sale

|

1,780

|

-

|

-

|

250

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,512,147

|

30,914

|

8.11

|

1,418,512

|

30,791

|

8.61

|

||||||||||||||||||

|

Total interest-earning assets

|

1,800,507

|

33,717

|

7.43

|

1,678,406

|

33,488

|

7.92

|

||||||||||||||||||

|

Noninterest-earning assets

|

42,578

|

40,002

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,843,085

|

$

|

1,718,408

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

1,040,322

|

$

|

8,388

|

3.20

|

%

|

$

|

922,117

|

$

|

9,237

|

3.97

|

%

|

||||||||||||

|

Time deposits

|

233,433

|

2,303

|

3.91

|

253,640

|

3,034

|

4.75

|

||||||||||||||||||

|

Total interest-bearing deposits

|

1,273,755

|

10,691

|

3.33

|

1,175,757

|

12,271

|

4.14

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

$

|

1,273,755

|

10,691

|

3.33

|

$

|

1,175,757

|

12,271

|

4.14

|

||||||||||||||||

|

|

||||||||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

$

|

320,238

|

$

|

332,487

|

||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

11,501

|

12,221

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

331,739

|

344,708

|

||||||||||||||||||||||

|

Shareholders’ equity

|

237,591

|

197,943

|

||||||||||||||||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,843,085

|

$

|

1,718,408

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Net interest income

|

$

|

23,026

|

$

|

21,217

|

||||||||||||||||||||

|

Net interest spread

|

4.10

|

%

|

3.78

|

%

|

||||||||||||||||||||

|

Net interest margin

|

5.07

|

%

|

5.02

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|

|

|

Net Interest Margin

|

|||||||||||||||||||||||

|

|

For the Nine Months Ended September 30,

|

|||||||||||||||||||||||

|

|

2025

(unaudited) |

2024

(unaudited) |

||||||||||||||||||||||

|

|

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

||||||||||||||||||

|

|

(Dollars in thousands)

|

|||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

238,118

|

$

|

7,721

|

4.34

|

%

|

$

|

180,426

|

$

|

6,896

|

5.09

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

47,248

|

827

|

2.34

|

103,507

|

2,266

|

2.92

|

||||||||||||||||||

|

Debt securities, tax exempt

|

12,327

|

187

|

2.03

|

17,468

|

214

|

1.63

|

||||||||||||||||||

|

Loans held for sale

|

1,453

|

-

|

-

|

281

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,453,557

|

87,207

|

8.02

|

1,381,200

|

89,834

|

8.66

|

||||||||||||||||||

|

Total interest-earning assets

|

1,752,703

|

95,942

|

7.32

|

1,682,882

|

99,210

|

7.85

|

||||||||||||||||||

|

Noninterest-earning assets

|

41,871

|

39,499

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,794,574

|

$

|

1,722,381

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

1,001,583

|

$

|

23,182

|

3.09

|

%

|

$

|

872,635

|

$

|

25,726

|

3.93

|

%

|

||||||||||||

|

Time deposits

|

235,278

|

7,152

|

4.06

|

255,348

|

9,026

|

4.71

|

||||||||||||||||||

|

Total interest-bearing deposits

|

1,236,861

|

30,334

|

3.28

|

1,127,983

|

34,752

|

4.10

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

$

|

1,236,861

|

$

|

30,334

|

3.28

|

$

|

1,127,983

|

$

|

34,752

|

4.10

|

||||||||||||||

|

|

||||||||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

$

|

319,346

|

$

|

395,822

|

||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

10,657

|

12,219

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

330,003

|

408,041

|

||||||||||||||||||||||

|

Shareholders’ equity

|

227,710

|

186,357

|

||||||||||||||||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,794,574

|

$

|

1,722,381

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Net interest income

|

$

|

65,608

|

$

|

64,458

|

||||||||||||||||||||

|

Net interest spread

|

4.04

|

%

|

3.75

|

%

|

||||||||||||||||||||

|

Net interest margin

|

5.00

|

%

|

5.10

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|