|

Oklahoma

|

001-38656

|

20-0764349

|

|

(State or other jurisdiction of incorporation)

|

(Commission File Number)

|

(IRS Employer Identification No.)

|

| ☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

|

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

|

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

|

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

|

|

Title of each class

|

Trading

Symbol(s)

|

Name of each exchange on which

registered

|

| Common Stock, $0.01 par value |

BSVN

|

The NASDAQ Global Select Market

|

|

|

Emerging growth company ☐ |

| Item 2.02. |

Results of Operations and Financial Condition

|

| Item 7.01 |

Regulation FD Disclosure

|

| Item 9.01 |

Financial Statements and Exhibits

|

|

(d)

|

Exhibits.

|

|

|

Item

|

|

Description

|

|

|

|

|

|

|

|

|

Press Release dated July 17, 2025

|

|

|

|

|

Second Quarter 2025 Investor Presentation

|

|

|

BANK7 CORP.

|

|

|

|

|

|

|

Date: July 17, 2025

|

By:

|

/s/ Kelly J. Harris

|

|

|

|

Kelly J. Harris

|

|

|

Executive Vice President and Chief Financial Officer

|

|

|

|

- |

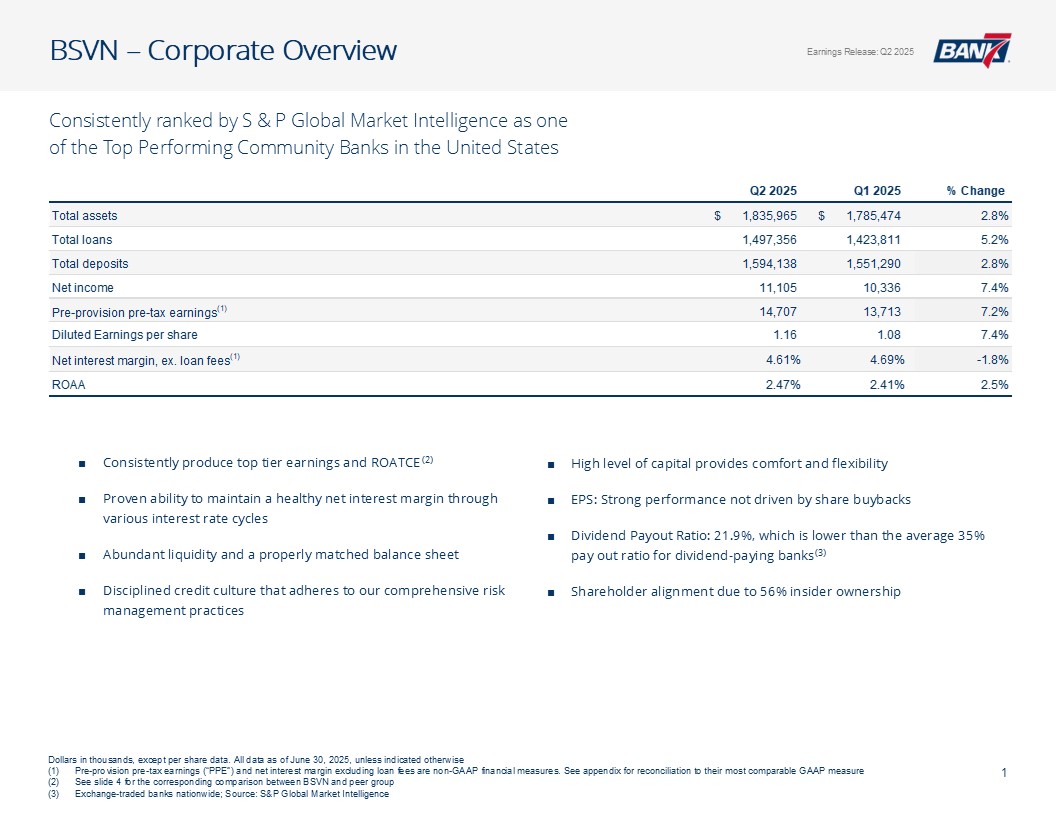

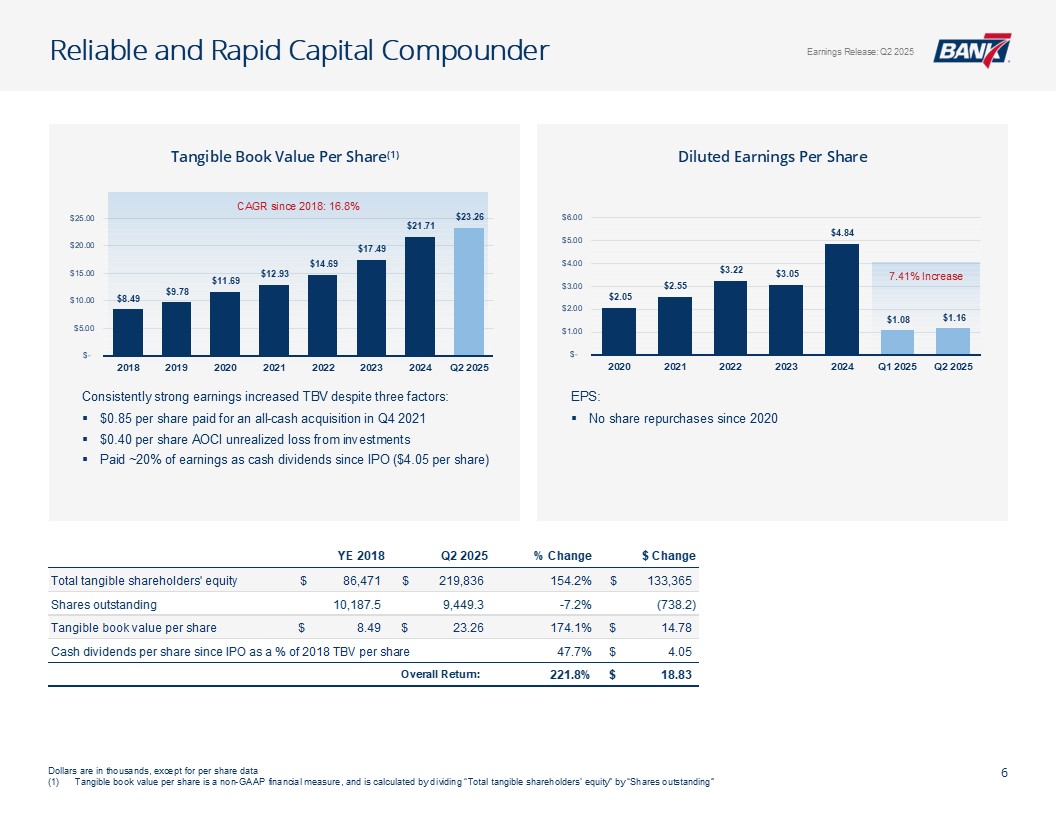

Net income of $11.1 million compared to $10.3 million, an increase of 7.44%

|

|

|

- |

Earnings per share of $1.16 compared to $1.08, an increase of 7.41%

|

|

|

- |

Total assets of $1.8 billion compared to $1.8 billion, an increase of 2.83%

|

|

|

- |

Total loans of $1.5 billion compared to $1.4 billion, an increase of 5.17%

|

|

|

- |

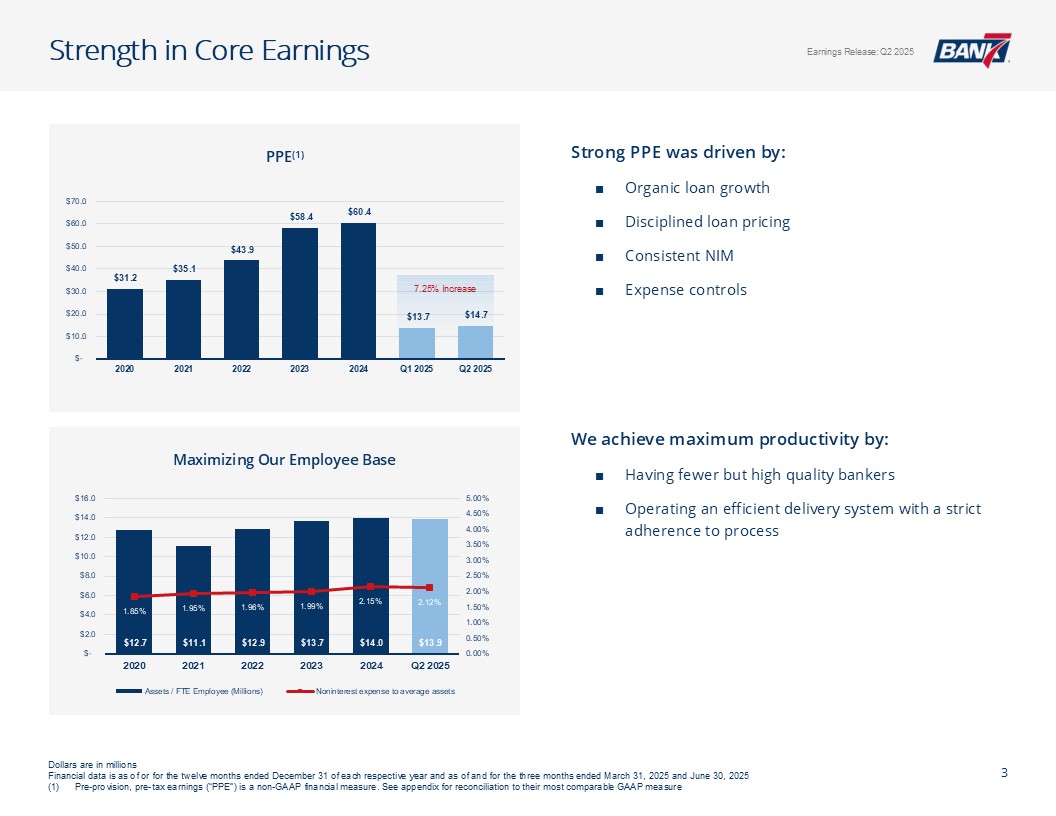

PPE of $14.7 million compared to $13.7 million, an increase of 7.25%

|

|

|

- |

Total interest income of $31.8 million compared to $30.4 million, an increase of 4.41%

|

|

|

For the Three Months Ended

|

|||||||

|

|

June 30,

2025 |

March 31,

2025 |

||||||

|

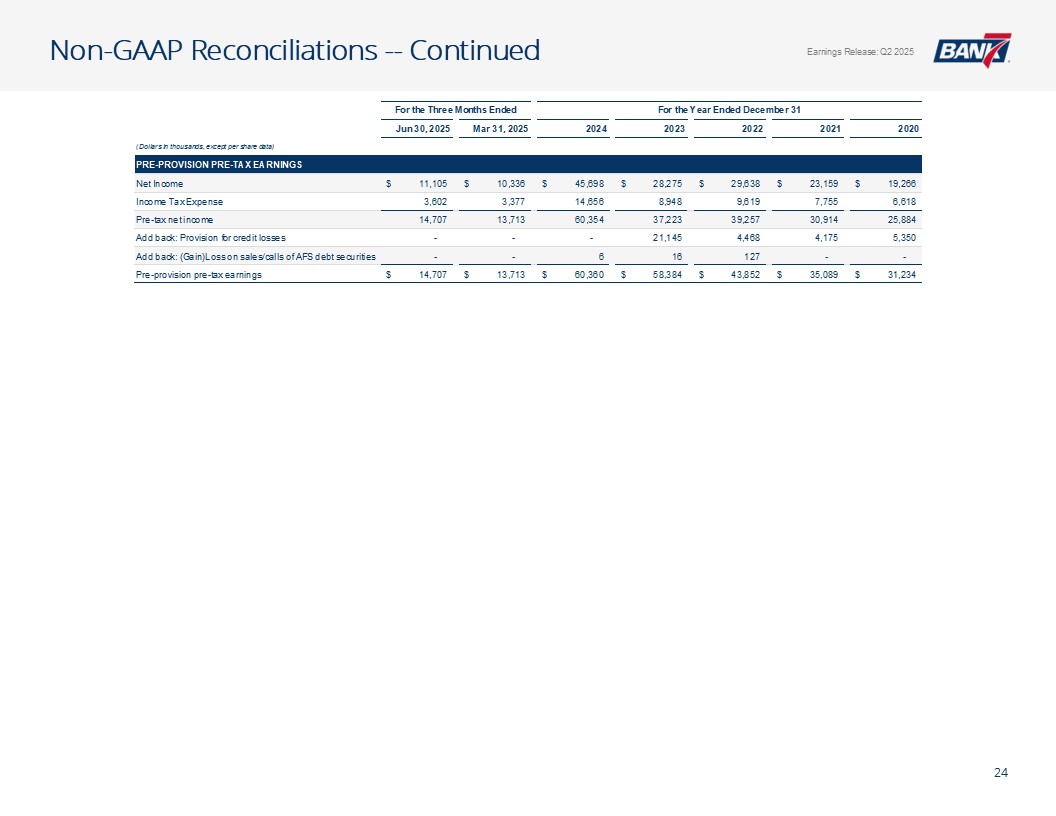

Calculation of Pre-Provision Pre-Tax Earnings ("PPE")

|

(Dollars in thousands)

|

|||||||

|

Net Income

|

$

|

11,105

|

$

|

10,336

|

||||

|

Income Tax Expense

|

3,602

|

3,377

|

||||||

|

Pre-tax net income

|

14,707

|

13,713

|

||||||

|

Add back: Provision for credit losses

|

-

|

-

|

||||||

|

Add back: (Gain)Loss on sales/calls of AFS debt securities

|

-

|

-

|

||||||

|

Pre-provision pre-tax earnings

|

14,707

|

13,713

|

||||||

|

Assets

|

June 30, 2025

(unaudited) |

December 31, 2024

|

||||||

|

|

||||||||

|

Cash and due from banks

|

$

|

218,839

|

$

|

234,196

|

||||

|

Interest-bearing time deposits in other banks

|

14,188

|

6,719

|

||||||

|

Available-for-sale debt securities

|

57,170

|

59,941

|

||||||

|

Loans, net of allowance for credit losses of $18,222 and

$17,918 at June 30, 2025 and December 31, 2024, respectively

|

1,479,134

|

1,379,465

|

||||||

|

Loans held for sale, at fair value

|

2,541

|

-

|

||||||

|

Premises and equipment, net

|

21,102

|

18,137

|

||||||

|

Nonmarketable equity securities

|

1,182

|

1,283

|

||||||

|

Core deposit intangibles

|

815

|

878

|

||||||

|

Goodwill

|

11,208

|

8,458

|

||||||

|

Income taxes receivable

|

381

|

-

|

||||||

|

Interest receivable and other assets

|

29,786

|

30,731

|

||||||

|

|

||||||||

|

Total assets

|

$

|

1,836,346

|

$

|

1,739,808

|

||||

|

|

||||||||

|

Liabilities and Shareholders’ Equity

|

||||||||

|

|

||||||||

|

Deposits

|

||||||||

|

Noninterest-bearing

|

$

|

323,825

|

$

|

313,258

|

||||

|

Interest-bearing

|

1,270,313

|

1,202,213

|

||||||

|

|

||||||||

|

Total deposits

|

1,594,138

|

1,515,471

|

||||||

|

|

||||||||

|

Income taxes payable

|

-

|

77

|

||||||

|

Interest payable and other liabilities

|

10,349

|

11,047

|

||||||

|

|

||||||||

|

Total liabilities

|

1,604,487

|

1,526,595

|

||||||

|

|

||||||||

|

Shareholders’ equity

|

||||||||

|

Common stock, $0.01 par value; 50,000,000 shares authorized; shares issued and outstanding: 9,449,319 and 9,390,211 at June 30, 2025 and

December 31, 2024, respectively

|

94

|

94

|

||||||

|

Additional paid-in capital

|

102,321

|

101,809

|

||||||

|

Retained earnings

|

133,186

|

116,281

|

||||||

|

Accumulated other comprehensive loss

|

(3,742

|

)

|

(4,971

|

)

|

||||

|

|

||||||||

|

Total shareholders’ equity

|

231,859

|

213,213

|

||||||

|

|

||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,836,346

|

$

|

1,739,808

|

||||

|

|

Three Months Ended

|

Six Months Ended

|

||||||||||||||

|

|

June 30,

|

June 30,

|

||||||||||||||

|

|

2025

(unaudited) |

2024

(unaudited) |

2025

(unaudited) |

2024

(unaudited) |

||||||||||||

|

Interest Income

|

|

|

|

|

||||||||||||

|

Loans, including fees

|

$

|

28,965

|

$

|

28,926

|

$

|

56,293

|

$

|

59,043

|

||||||||

|

Interest-bearing time deposits in other banks

|

145

|

246

|

246

|

499

|

||||||||||||

|

Debt securities, taxable

|

278

|

951

|

561

|

1,963

|

||||||||||||

|

Debt securities, tax-exempt

|

63

|

71

|

126

|

144

|

||||||||||||

|

Other interest and dividend income

|

2,330

|

2,242

|

4,997

|

4,074

|

||||||||||||

|

|

||||||||||||||||

|

Total interest income

|

31,781

|

32,436

|

62,223

|

65,723

|

||||||||||||

|

|

||||||||||||||||

|

Interest Expense

|

||||||||||||||||

|

Deposits

|

10,043

|

11,204

|

19,643

|

22,481

|

||||||||||||

|

|

||||||||||||||||

|

Total interest expense

|

10,043

|

11,204

|

19,643

|

22,481

|

||||||||||||

|

|

||||||||||||||||

|

Net Interest Income

|

21,738

|

21,232

|

42,580

|

43,242

|

||||||||||||

|

|

||||||||||||||||

|

Provision for Credit Losses

|

-

|

-

|

-

|

-

|

||||||||||||

|

|

||||||||||||||||

|

Net Interest Income After Provision for Credit Losses

|

21,738

|

21,232

|

42,580

|

43,242

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest Income

|

||||||||||||||||

|

Mortgage lending income

|

520

|

78

|

610

|

129

|

||||||||||||

|

Service charges on deposit accounts

|

232

|

260

|

450

|

509

|

||||||||||||

|

Other

|

1,949

|

2,827

|

3,396

|

4,536

|

||||||||||||

|

|

||||||||||||||||

|

Total noninterest income

|

2,701

|

3,165

|

4,456

|

5,174

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest Expense

|

||||||||||||||||

|

Salaries and employee benefits

|

5,721

|

5,118

|

11,000

|

10,407

|

||||||||||||

|

Furniture and equipment

|

361

|

324

|

612

|

554

|

||||||||||||

|

Occupancy

|

630

|

613

|

1,222

|

1,273

|

||||||||||||

|

Data and item processing

|

590

|

481

|

1,100

|

939

|

||||||||||||

|

Accounting, marketing and legal fees

|

158

|

264

|

263

|

364

|

||||||||||||

|

Regulatory assessments

|

213

|

336

|

297

|

723

|

||||||||||||

|

Advertsing and public relations

|

223

|

83

|

417

|

229

|

||||||||||||

|

Travel, lodging and entertainment

|

121

|

131

|

177

|

183

|

||||||||||||

|

Other

|

1,715

|

1,792

|

3,528

|

3,606

|

||||||||||||

|

|

||||||||||||||||

|

Total noninterest expense

|

9,732

|

9,142

|

18,616

|

18,278

|

||||||||||||

|

|

||||||||||||||||

|

Income Before Taxes

|

14,707

|

15,255

|

28,420

|

30,138

|

||||||||||||

|

Income tax expense

|

3,602

|

3,731

|

6,979

|

7,326

|

||||||||||||

|

Net Income

|

$

|

11,105

|

$

|

11,524

|

$

|

21,441

|

$

|

22,812

|

||||||||

|

|

||||||||||||||||

|

Earnings per common share - basic

|

$

|

1.18

|

$

|

1.25

|

$

|

2.27

|

$

|

2.47

|

||||||||

|

Earnings per common share - diluted

|

1.16

|

1.23

|

2.25

|

2.44

|

||||||||||||

|

Weighted average common shares outstanding - basic

|

9,449,152

|

9,250,332

|

9,435,414

|

9,235,176

|

||||||||||||

|

Weighted average common shares outstanding - diluted

|

9,545,128

|

9,367,247

|

9,548,583

|

9,343,047

|

||||||||||||

|

|

||||||||||||||||

|

Other Comprehensive Income (Loss)

|

||||||||||||||||

|

Unrealized gains (losses) on securities, net of tax expense of $189 and $123 for the three months ended June 30, 2025 and 2024, respectively; net of tax expense of $425 and $123 for the six

months ended June 30, 2025 and 2024, respectively

|

$

|

587

|

$

|

(59

|

)

|

$

|

1,229

|

$

|

397

|

|||||||

|

Other comprehensive income (loss)

|

$

|

587

|

$

|

(59

|

)

|

$

|

1,229

|

$

|

397

|

|||||||

|

Comprehensive Income

|

$

|

11,692

|

$

|

11,465

|

$

|

22,670

|

$

|

23,209

|

||||||||

|

|

Net Interest Margin

|

|||||||||||||||||||||||

|

|

For the Three Months Ended June 30,

|

|||||||||||||||||||||||

|

|

2025

(unaudited) |

2024

(unaudited) |

||||||||||||||||||||||

|

|

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

||||||||||||||||||

|

|

(Dollars in thousands)

|

|||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

247,652

|

$

|

2,475

|

4.01

|

%

|

$

|

173,502

|

$

|

2,488

|

5.75

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

47,285

|

278

|

2.36

|

106,457

|

951

|

3.58

|

||||||||||||||||||

|

Debt securities, tax exempt

|

12,502

|

63

|

2.02

|

17,252

|

71

|

1.65

|

||||||||||||||||||

|

Loans held for sale

|

1,987

|

-

|

-

|

355

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,448,924

|

28,965

|

8.02

|

1,354,985

|

28,926

|

8.56

|

||||||||||||||||||

|

Total interest-earning assets

|

1,758,350

|

31,781

|

7.25

|

1,652,551

|

32,436

|

7.87

|

||||||||||||||||||

|

Noninterest-earning assets

|

43,048

|

38,722

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,801,398

|

$

|

1,691,273

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

1,006,484

|

$

|

7,676

|

3.06

|

%

|

$

|

851,751

|

$

|

8,293

|

3.91

|

%

|

||||||||||||

|

Time deposits

|

236,108

|

2,367

|

4.02

|

247,452

|

2,911

|

4.72

|

||||||||||||||||||

|

Total interest-bearing deposits

|

1,242,592

|

10,043

|

3.24

|

1,099,203

|

11,204

|

4.09

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

$

|

1,242,592

|

10,043

|

3.24

|

$

|

1,099,203

|

11,204

|

4.09

|

||||||||||||||||

|

|

||||||||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

$

|

321,351

|

$

|

394,010

|

||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

10,471

|

12,778

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

331,822

|

406,788

|

||||||||||||||||||||||

|

Shareholders' equity

|

226,984

|

185,282

|

||||||||||||||||||||||

|

Total liabilities and shareholders' equity

|

$

|

1,801,398

|

$

|

1,691,273

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Net interest income

|

$

|

21,738

|

$

|

21,232

|

||||||||||||||||||||

|

Net interest spread

|

4.01

|

%

|

3.78

|

%

|

||||||||||||||||||||

|

Net interest margin

|

4.96

|

%

|

5.15

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|

|

|

Net Interest Margin

|

|||||||||||||||||||||||

|

|

For the Six Months Ended June, 30

|

|||||||||||||||||||||||

|

|

2025

(unaudited) |

2024

(unaudited) |

||||||||||||||||||||||

|

|

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

||||||||||||||||||

|

|

(Dollars in thousands)

|

|||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

242,876

|

$

|

5,243

|

4.35

|

%

|

$

|

174,787

|

$

|

4,573

|

5.25

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

47,957

|

561

|

2.36

|

129,963

|

1,963

|

3.03

|

||||||||||||||||||

|

Debt securities, tax exempt

|

12,508

|

126

|

2.03

|

17,761

|

144

|

1.63

|

||||||||||||||||||

|

Loans held for sale

|

1,287

|

-

|

-

|

297

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,423,776

|

56,293

|

7.97

|

1,362,339

|

59,043

|

8.69

|

||||||||||||||||||

|

Total interest-earning assets

|

1,728,404

|

62,223

|

7.26

|

1,685,147

|

65,723

|

7.82

|

||||||||||||||||||

|

Noninterest-earning assets

|

41,511

|

39,246

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,769,915

|

$

|

1,724,393

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

981,833

|

$

|

14,794

|

3.04

|

%

|

$

|

848,764

|

$

|

16,489

|

3.90

|

%

|

||||||||||||

|

Time deposits

|

236,216

|

4,849

|

4.14

|

256,212

|

5,992

|

4.69

|

||||||||||||||||||

|

Total interest-bearing deposits

|

1,218,049

|

19,643

|

3.25

|

1,104,976

|

22,481

|

4.08

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

1,218,049

|

19,643

|

3.25

|

1,104,976

|

22,481

|

4.08

|

||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

318,952

|

426,696

|

||||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

10,228

|

12,218

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

329,180

|

438,914

|

||||||||||||||||||||||

|

Shareholders' equity

|

222,686

|

180,503

|

||||||||||||||||||||||

|

Total liabilities and shareholders' equity

|

$

|

1,769,915

|

$

|

1,724,393

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Net interest income

|

$

|

42,580

|

$

|

43,242

|

||||||||||||||||||||

|

Net interest spread

|

4.01

|

%

|

3.74

|

%

|

||||||||||||||||||||

|

Net interest margin

|

4.97

|

%

|

5.15

|

%

|

||||||||||||||||||||