|

CREDICORP LTD.

(Registrant)

|

|||

|

By:

|

/s/ Milagros Cigüeñas

|

||

|

Milagros Cigüeñas

|

|||

|

Authorized Representative

|

|||

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Operating and Financial Highlights | 03 |

|

|

||

|

Senior Management Quotes

|

04 |

|

|

||

|

First Quarter 2025 Earnings Conference Call

|

05 |

|

|

||

|

Summary of Financial Performance and Outlook

|

06 |

|

|

Financial Overview | 12 |

|

|

Credicorp’s Strategy Update | 13 |

|

|

Analysis of 1Q25 Consolidated Results |

|

01

|

Loan Portfolio

|

17

|

|

|

02

|

Deposits

|

20

|

|

|

03

|

Interest Earning Assets and Funding

|

23

|

|

|

04

|

Net Interest Income (NII)

|

25

|

|

|

05

|

Portfolio Quality and Provisions

|

28

|

|

|

06

|

Other Income

|

32

|

|

|

07

|

Insurance Underwriting Results and the Medical Services

|

36

|

|

|

08

|

Operating Expenses

|

39

|

|

|

09

|

Operating Efficiency

|

41

|

|

|

10

|

Regulatory Capital

|

42

|

|

|

11

|

Economic Outlook

|

44

|

|

|

12

|

Appendix

|

49

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

| • |

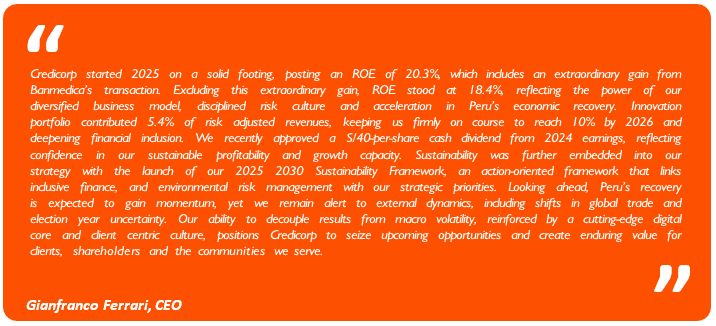

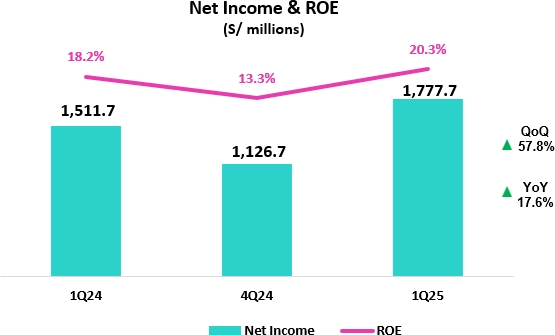

Net Income attributed to Credicorp increased 57.8% QoQ and 17.6% YoY to S/1,777.7 million, delivering an ROE of 20.3%. Excluding the extraordinary gain related to the

previously disclosed acquisition of the remaining 50% stake in the JV with Empresas Banmedica, Net Income attributed to Credicorp increases 43.0% QoQ and 6.6% YoY, with an ROE at 18.4%.

|

| • |

In March 2025, Credicorp revalued Bolivia´s balance sheet using a market-reflective FX rate, resulting in an accounting contraction of 2.0% in Credicorp Total Assets. The loan and deposit figures cited below

exclude this adjustment.

|

| • |

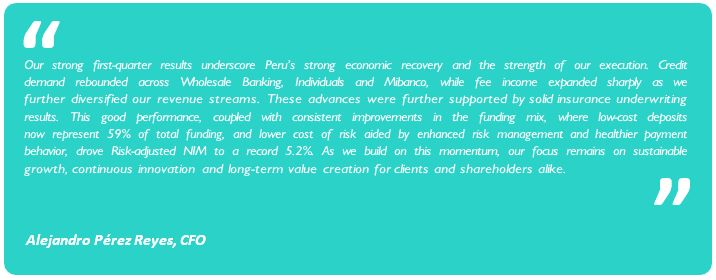

Total Loans measured in average daily balances (ADB) expanded by 1.5% YoY, mainly driven by short-term loans in Wholesale Banking and Mortgages. QoQ, Total Loans rose 0.8%

led by growth in Wholesale Banking, Consumer (supported by Yape and BCP Stand-alone), and Mortgages.

|

| • |

Total Deposits increased by 9.7% YoY fueled by Low-cost deposits, amid higher system liquidity, and 0.3% QoQ. Low-cost deposits accounted for 71.8% of total deposits and

represent 59.0% of the total funding base.

|

| • |

Portfolio quality indicators and the Cost of Risk have improved notably as a result of the cumulative impact of a more dynamic

portfolio management, enhancements in underwriting and risk management and a more favorable macroeconomic environment.

|

| • |

NPL Ratio improved 16 bps QoQ to stand at 5.1%, driven by debt repayments at BCP Stand-alone and by a drop in internal overdue loans at both BCP Stand-alone and Mibanco.

YoY, the NPL Ratio improved 112 bps.

|

| • |

Provisions, excluding provision reversals in 1Q24, declined 45.5% YoY, while CoR stood at 1.6%, reflecting an improvement in payment performance and in the economic

backdrop; successful risk management measures at both BCP and Mibanco; and some one-time events outlined in the Portfolio Quality chapter. QoQ, provisions declined 21.7%.

|

| • |

Core Income increased 7.0% YoY, underpinned by diversified revenue streams, which drove a 15.1% YoY increase in other core income. Achieved record-high Risk-Adjusted NIM of 5.24%.

|

| • |

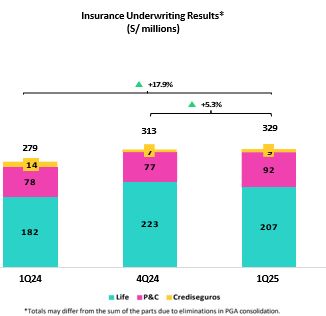

Insurance Underwriting Results rose 17.9% YoY, largely due to stronger reinsurance results in the P&C business, and was up 5.3% QoQ.

|

| • |

Yape reached 14.3 million Monthly Active Users (MAU), with average monthly transactions per user rising to 52. The platform sustained its growth trajectory and captured

4.8% of Credicorp’s total risk-adjusted revenue share.

|

| • |

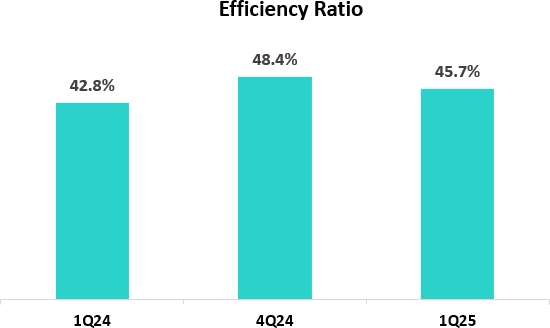

Efficiency Ratio reached 45.7%, aligned with our full-year guidance. Operating expenses increased 15.6% YoY, mainly due to the core business at BCP Stand-alone and

investments in disruptive initiatives.

|

| • |

Capital base moving closer to target, with the IFRS CET 1 Ratio falling 24 bps YoY at BCP Stand-alone and 18 bps YoY at Mibanco, standing at 11.6% and 15.9%, respectively.

|

| • |

After quarter-end, on April 14, 2025, Credicorp declared an ordinary cash dividend of S/40 per share based on 2024 results, to be paid out in June 13, 2025, as capital

levels advance closer to target across subsidiaries.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

First Quarter 2025 Earnings Conference Call

|

|||

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

|

|

|

1

|

Beginning in 1Q25, reclassifications have been incorporated, affecting the presentation of Fee Income, Net Gain on Foreign Exchange Transactions, and Net Gain on Derivatives Held for

Trading. Figures for prior periods have been restated to ensure comparability and may differ from those previously reported.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

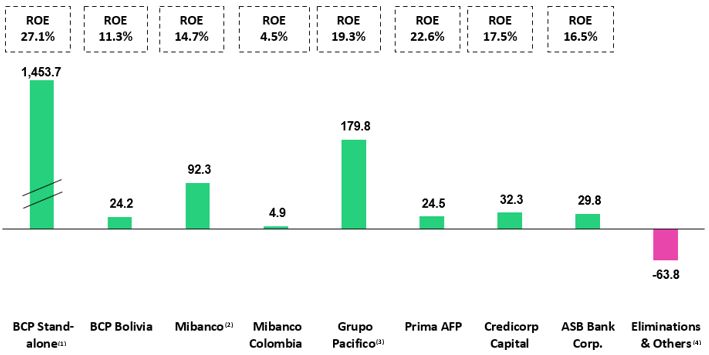

| (1) |

In BCP Stand-alone, the figure is lower than the net profit since the contribution eliminates investment gains in other subsidiaries of Credicorp (Mibanco)

|

| (2) |

In Mibanco, the figure is less than the net profit because Credicorp owns (directly and indirectly) 99.921% of Mibanco.

|

| (3) |

The contribution for Grupo Pacifico presented here is greater than the profit of Pacifico Seguros since 100% of Crediseguros is being included (including 48% under Grupo Crédito).

|

| (4) |

Includes the extraordinary gain of approximately S/ 166 million (net of taxes) related to the acquisition of Empresas Banmedica.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

Universal Banking

|

|

|

|

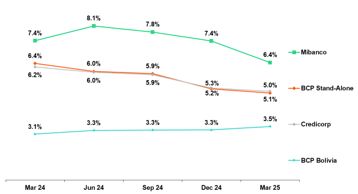

BCP Stand-alone reported good results, which were driven mainly by an improvement in risk management indicators and diversified sources of income, which continued to represent a core

strength. NIM stood at 5.8%, supported in large part by an improvement in the cost of funding. YoY, other core income rose 15.1% on the back of Yape’s consolidation as a key source of income and alongside a strong transactions level.

These dynamics were partially offset by growth in operating expenses.

|

|

|

|

Insurance and Pensions1

|

|

Profitability at Grupo Pacífico dropped AaA due to a reduction in the Net gain on Securities, on the back of deterioration in the investment portfolio. This dynamic was partially offset

by an uptick in the Insurance Underwriting Result via Life and P & C and supported by solid commercial dynamics in both businesses.

|

|

Microfinance

|

|

Mibanco’s profitability rose YoY, fueled mainly by a resilient NIM and fortified risk management. NIM stood at 13.9%, driven by active price management and a decrease in the funding

cost.

Mibanco Colombia’s profitability improved thanks to its focus on efficiency; improvements in processes and controls; and disciplined risk management, which helped

attenuate the impact of a challenging business environment.

|

|

|

|

Investment Management and Advisory

|

|

Operating dynamics for Investment Banking and Advisory were solid in 1Q25, which reaffirms that our strategic focus is on-target and puts us in good stead for 2025. Net earnings rose

10% YoY, driven primarily by a reduction in operating expenses. Our Asset Management and Capital Markets businesses also contributed to results through an uptick in AUMs and growth in transactions, respectively.

|

|

|

|

Outlook

|

|

Although ROE in 1Q25 situates us in an advantageous position going forward, uncertainty at the global level has led us to maintain our guidance for ROE for the year 2025 at

around 17.5%. These results will be supported by: (i) acceleration in the pace of growth of our loan portfolio, in the retail segment in particular, (ii) the resilience of our NIM, and (iii) a controlled cost of risk.

|

|

1

|

In March 2025. Credicorp concluded the acquisition of the remaining 50% of the stake Empresas Banmedica under the joint venture with Pacifico Seguros. This consolidation did not materially

impact Grupo Pacifico’s results in 1Q25.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

Financial Overview

|

|

Credicorp Ltd.

|

|

Quarter |

% change

|

||

|

S/000

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

Net interest, similar income and expenses

|

3,426,123

|

3,629,794

|

3,572,012

|

-1.6%

|

4.3%

|

|

Provision for credit losses on loan portfolio, net of recoveries

|

(814,699)

|

(743,296)

|

(581,893)

|

-21.7%

|

-28.6%

|

|

Net interest, similar income and expenses, after provision for credit losses on loan portfolio

|

2,611,424

|

2,886,498

|

2,990,119

|

3.6%

|

14.5%

|

|

Other income

|

1,392,559

|

1,582,732

|

1,690,216

|

6.8%

|

21.4%

|

|

Insurance underwriting result

|

279,062

|

312,683

|

329,134

|

5.3%

|

17.9%

|

|

Medical services result

|

-

|

-

|

42,689

|

n.a.

|

n.a.

|

|

Total expenses

|

(2,212,482)

|

(3,026,227)

|

(2,532,874)

|

-16.3%

|

14.5%

|

|

Profit before income tax

|

2,070,563

|

1,755,686

|

2,519,284

|

43.5%

|

21.7%

|

|

Income tax

|

(528,466)

|

(598,348)

|

(704,469)

|

17.7%

|

33.3%

|

|

Net profit

|

1,542,097

|

1,157,338

|

1,814,815

|

56.8%

|

17.7%

|

|

Non-controlling interest

|

30,440

|

30,625

|

37,118

|

21.2%

|

21.9%

|

|

Net profit attributable to Credicorp

|

1,511,657

|

1,126,713

|

1,777,697

|

57.8%

|

17.6%

|

|

Dividends paid to third parties

|

-

|

-

|

-

|

n.a.

|

n.a.

|

|

Net income / share (S/)

|

19.0

|

14.1

|

22.3

|

57.8%

|

17.6%

|

|

Dividends per Share (S/)

|

-

|

-

|

-

|

n.a.

|

n.a.

|

|

Loans

|

140,798,083

|

145,732,273

|

141,196,646

|

-3.1%

|

0.3%

|

|

Deposits and obligations

|

147,857,127

|

161,842,066

|

157,619,082

|

-2.6%

|

6.6%

|

|

Net equity

|

33,853,460

|

34,346,451

|

35,843,202

|

4.4%

|

5.9%

|

|

Profitability

|

|||||

|

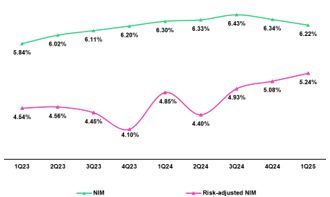

Net interest margin(1)

|

6.30%

|

6.34%

|

6.22%

|

-12 bps

|

-8 bps

|

|

Risk-adjusted Net interest margin

|

4.85%

|

5.08%

|

5.24%

|

16 bps

|

39 bps

|

|

Funding cost(2)

|

2.98%

|

2.56%

|

2.42%

|

-14 bps

|

-56 bps

|

|

ROAE

|

18.2%

|

13.3%

|

20.3%

|

697 bps

|

203 bps

|

|

ROAA

|

2.5%

|

1.8%

|

2.8%

|

100 bps

|

30 bps

|

|

Loan portfolio quality

|

|||||

|

Internal overdue ratio(3)

|

4.4%

|

3.7%

|

3.7%

|

-3 bps

|

-72 bps

|

|

Internal overdue ratio over 90 days

|

3.3%

|

3.0%

|

3.0%

|

-1 bps

|

-34 bps

|

|

NPL ratio(4)

|

6.2%

|

5.3%

|

5.1%

|

-16 bps

|

-112 bps

|

|

Cost of risk(5)

|

2.3%

|

2.1%

|

1.6%

|

-44 bps

|

-66 bps

|

|

Coverage ratio of IOLs

|

132.0%

|

147.4%

|

148.7%

|

130 bps

|

1672 bps

|

|

Coverage ratio of NPLs

|

93.5%

|

104.3%

|

107.4%

|

308 bps

|

1395 bps

|

|

Operating efficiency

|

|||||

|

Operating income(6)

|

4,933,778

|

5,396,202

|

5,340,199

|

-1.0%

|

8.2%

|

|

Operating expenses(7)

|

2,112,810

|

2,612,878

|

2,442,089

|

-6.5%

|

15.6%

|

|

Efficiency ratio(8)

|

42.8%

|

48.4%

|

45.7%

|

-270 bps

|

291 bps

|

|

Operating expenses / Total average assets

|

3.5%

|

4.1%

|

3.8%

|

-30 bps

|

31 bps

|

|

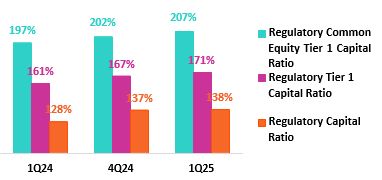

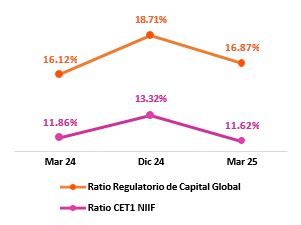

Capital adequacy - BCP Stand-alone

|

|||||

|

Global Capital Ratio(9)

|

16.12%

|

18.71%

|

16.87%

|

-184 bps

|

75 bps

|

|

Ratio Tier 1(10)

|

11.72%

|

13.08%

|

11.34%

|

-174 bps

|

-38 bps

|

|

Ratio common equity tier 1(11) (13)

|

11.86%

|

13.32%

|

11.62%

|

-170 bps

|

-24 bps

|

|

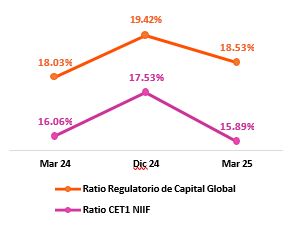

Capital adequacy - Mibanco

|

|||||

|

Global Capital Ratio(9)

|

18.03%

|

19.42%

|

18.53%

|

-89 bps

|

50 bps

|

|

Ratio Tier 1(10)

|

15.69%

|

17.07%

|

15.48%

|

-159 bps

|

-21 bps

|

|

Ratio common equity tier 1(11) (13)

|

16.06%

|

17.53%

|

15.89%

|

-164 bps

|

-17 bps

|

|

Employees(14)

|

36,912

|

38,695

|

46,621

|

20.5%

|

26.3%

|

|

Share Information

|

|||||

|

Issued Shares

|

94,382

|

94,382

|

94,382

|

0.0%

|

0.0%

|

|

Treasury Shares(12)

|

14,908

|

14,948

|

15,016

|

0.5%

|

0.7%

|

|

Outstanding Shares

|

79,474

|

79,434

|

79,366

|

-0.1%

|

-0.1%

|

| (1) |

Net Interest Margin = Net Interest Income (Excluding Net Insurance Financial Expenses)/ Average Interest Earning Assets

|

| (2) |

Funding Cost = Interest Expense (Does not include Net Insurance Financial Expenses) / Average Funding

|

| (3) |

Internal Overdue Loans: include overdue loans and loans under legal collection, according to our internal policy for overdue loans. Internal Overdue Ratio: Internal overdue loans/ Total loans

|

| (4) |

Non-performing loans (NPL): Internal overdue loans + Refinanced loans. NPL ratio: NPL / Total loans.

|

| (5) |

Cost of risk = Annualized provision for loan losses, net of recoveries/ Total loans.

|

|

(6)

|

Operating Income = Net interest, similar income and expenses + Fee Income+ Net gain on foreign exchange transactions + Net Gain From associates + Net gain on derivatives held for

trading + Result on exchange differences + Insurance Underwriting Result + Results for Medical Services

|

| (7) |

Operating Expenses = Salaries and employee benefits + Administrative expenses + Depreciation and amortization + Association in participation + Acquisition cost.

|

|

(8)

|

Efficiency Ratio = (Salaries and employee benefits + Administrative expenses + Depreciation and amortization + Association in participation) / (Net

interest, similar income and expenses + Fee Income+ Net gain on foreign exchange transactions + Net Gain From associates + Net gain on derivatives held for trading + Result on exchange differences + Insurance Underwriting Result)

|

| (9) |

Regulatory Capital/ Risk-weighted assets (legal minimum = 10% since July 2011).

|

|

(10)

|

Tier 1 = Capital + Legal and other capital reserves + Accumulated earnings with capitalization agreement + (0.5 x Unrealized profit and net income in

subsidiaries) - Goodwill - (0.5 x Investment in subsidiaries) + Perpetual subordinated debt (the maximum amount that can be included is 17.65% of Capital + Reserves + Accumulated earnings with capitalization agreement + Unrealized

profit and net income in subsidiaries - Goodwill).

|

| (11) |

Common Equity TierI = Capital + Reserves – 100% of applicable deductions (investment in subsidiaries, goodwill, intangibles, and net deferred taxes that rely on future profitability) +

retained earnings + unrealized gains.

|

| (12) |

Consider shares held by Atlantic Security Holding Corporation (ASHC) and stock awards.

|

| (13) |

Common Equity Tier I calculated based on IFRS Accounting

|

| (14) |

Internal management figures. Since 1Q25, includes corporate health and medical services employees.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|||

|

Core Businesses Transformation (1)

|

1Q24

|

4Q24

|

1Q25

|

|

Credicorp

|

|||

|

Innovation Portfolio Risk-Adjusted Revenue Share (2)

|

3.1%

|

5.6%

|

5.4%

|

|

BCP

Stand-alone

|

|||

|

Digital clients (3)

|

70%

|

76%

|

78%

|

|

Digital monetary transactions (4)

|

83%

|

88%

|

89%

|

|

Cashless transactions (5)

|

62%

|

69%

|

69%

|

|

Mibanco

|

|||

|

Disbursements through leads (6)

|

69%

|

65%

|

70%

|

|

Disbursements through alternative channels (7)

|

22%

|

24%

|

26%

|

|

Relationship managers productivity (8)

|

25.0

|

24.5

|

28.2

|

| (1) |

Management figures. Figures for March 2024, December 2024, and March 2025.

|

| (2) |

As a percentage of Credicorpʼs total Risk-Adjusted Revenue.

|

| (3) |

Retail clients that made 70%, or more, of their transactions through digital channels in the last 6 months (including Yape).

|

| (4) |

Monetary Transactions conducted through Mobile Banking, Internet Banking, Yape and Telecredito/Total Monetary Transactions in Retail Banking.

|

| (5) |

Amount transacted through Mobile Banking, Internet Banking, Yape y POS/Total amount transacted through Retail Banking.

|

| (6) |

Disbursements generated through leads/Total disbursements.

|

| (7) |

Disbursements conducted through alternative channels/Total disbursements. Figures differ from previously reported due to a methodological change.

|

| (8) |

Number of loans disbursed/Total relationship managers.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|||

|

Management KPI’s (1)

|

Quarter

|

Change %

|

|||

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

|

Users

|

|||||

|

Users (millions)

|

15.1

|

17.3

|

18.0

|

3.9%

|

18.9%

|

|

Monthly Active Users (MAU) (millions) (2)

|

11.5

|

13.7

|

14.3

|

4.4%

|

24.3%

|

|

Fee Income Generating MAU (millions)

|

8.6

|

11.4

|

12.0

|

5.2%

|

38.7%

|

|

Engagement

|

|||||

|

# Transactions (millions)

|

1,127.7

|

1,953.1

|

2,025.4

|

3.7%

|

79.6%

|

|

# Transactions / MAU

|

36.0

|

51.0

|

52.1

|

2.1%

|

44.5%

|

|

# Average Functionalities / MAU

|

2.2

|

2.6

|

2.6

|

2.7%

|

18.0%

|

|

Experience

|

|||||

|

NPS (3)

|

78

|

79

|

77

|

-200.0%

|

-140.0%

|

|

Unit Economics

|

|||||

|

Monthly Indicators (4)

|

|||||

|

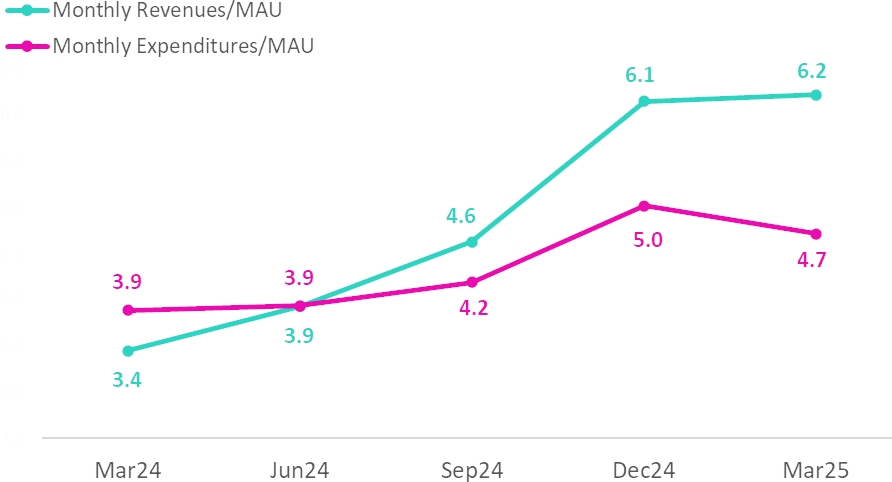

Revenues / MAU (S/) (5)

|

3.4

|

6.1

|

6.2

|

1.1%

|

80.4%

|

|

Expenses / MAU (S/) (5)

|

-3.9

|

-5.0

|

-4.7

|

-6.1%

|

21.2%

|

|

Quarterly Indicators (6)

|

|||||

|

Revenues / MAU (S/)

|

9.8

|

16.0

|

16.6

|

4.0%

|

69.0%

|

|

Expenses / MAU (S/)

|

-11.5

|

-13.4

|

-12.7

|

-5.4%

|

10.5%

|

|

Drivers Monetization

|

|||||

|

Total TPV (S/, billions) (7)

|

50.5

|

90.3

|

91.6

|

1.4%

|

81.4%

|

|

Payments

|

|||||

|

# Bill Payments transactions (millions)

|

23.4

|

40.5

|

45.0

|

11.3%

|

92.0%

|

|

Financials

|

|||||

|

# Loans Disbursements (thousands)

|

472.4

|

2,143.1

|

3,097.1

|

44.5%

|

555.7%

|

|

E-Commerce

|

|||||

|

GMV (S/, millions) (8)

|

59.1

|

120.4

|

119.2

|

-1.0%

|

101.7%

|

| (1) |

Management Figures.

|

| (2) |

Yape users that have made at least one outgoing transaction in the measurement month.

|

| (3) |

Net Promoter Score.

|

| (4) |

Monthly indicators consider the results of the last month of the quarter for the numerator and denominator.

|

|

(5)

|

Beginning in 1Q25, Credicorp incorporated reclassifications between Operating Expenses and Fee Income, along with new accounting allocations—primarily

related to interest expenses associated with the Deposit Insurance Fund. Figures for prior periods have been restated for comparability and may differ from those previously reported.

|

| (6) |

Quarterly indicators are calculated using the sum of the three months in the period for numerator accounts, and the average of the denominator—based on the last month’s data from both the

current and previous quarters.

|

| (7) |

Total Payment Volume.

|

| (8) |

Gross Merchant Volume, includes the following functionalities: Yape Promos, Yape Store, Ticketing, Gaming, Delivery, Buses, Insurance, Gas, Brand Solutions and

Insurance.

|

|

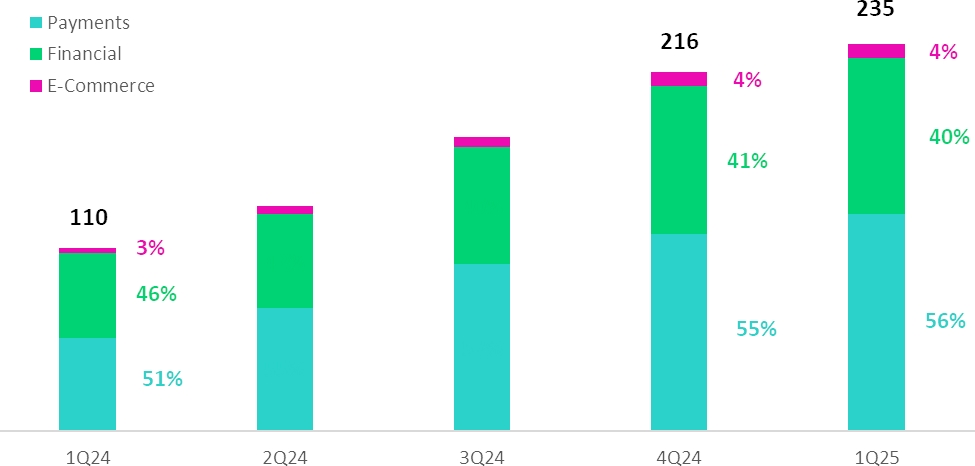

Financial results (1)

S/ millions

|

Quarter

|

Change %

|

|||

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

|

Net Interest Income after Provisions (2)

|

50.7

|

88.3

|

93.0

|

5.3%

|

83.6%

|

|

Other Income (3)

|

59.7

|

127.7

|

141.6

|

10.9%

|

137.1%

|

|

Total Income

|

110.4

|

216.0

|

234.6

|

8.6%

|

112.5%

|

|

Total Operating Expenses

|

-128.8

|

-181.3

|

-179.1

|

-1.2%

|

39.1%

|

|

(1)

|

Management figures. Beginning in 1Q25, reclassifications between Operating Expenses and Fee Income have been incorporated, along with new accounting

allocations — primarily related to interest expenses associated with the Deposit Insurance Fund. Figures for prior periods have been restated for comparability and may differ from those previously reported.

|

| (2) |

Includes interest income, interest expense and net provisions.

|

| (3) |

Includes Other Income recorded in BCP and in Yape Market.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|||

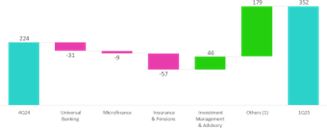

|

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|||

| o |

Inclusion: Includes the financial inclusion and financial education fronts, as well as access to quality healthcare.

|

| o |

Finance for the Future: involves the fronts of support to micro, small and medium enterprises (MSMEs), resilience of businesses and people, and sustainable financing and

investments.

|

| o |

Trust: Encompasses promoting trust in Credicorp and its subsidiaries, as well as in the private sector in general.

|

| o |

Country Vision: Seeks to promote development in the countries in which we operate by leveraging the three pillars mentioned above.

|

| o |

BCP and Yape financially included 200 thousand people this quarter, accumulating a total of 6.0 million since 2020. More than 1.6 million clients received loan disbursements through Yape in the first quarter.

|

| o |

BCP reached 81 thousand clients in 1Q25 through financial education initiatives that focus on promoting changes in behavior to safeguard and improve their financial health (avoid over-indebtedness, late payments,

overdraws on credit cards, among others).

|

| o |

Pacifico closed the 1Q25 with +2.7 million clients included through inclusive insurance products1 placed through the BCP, Mibanco and Yape channels.

|

| o |

Mibanco reported a YTD increase of 16 thousand SME clients in its loan portfolio. Additionally, the bank reached more than 108 thousand clients through its financial education programs.

|

| o |

Mibanco disbursed 231 million soles in the 1Q25 through its Crediagua product, which equips households with drinking water and sewage connections.

|

| o |

BCP, in the framework of the program “Contigo Emprendedor,” rolled out the program “Despegue Empresarial,” which benefitted more than 70 thousand clients by helping them improve their credit score.

|

| o |

BCP disbursed more than US$ 430 million in sustainable financing in the 1Q25, led by loans for working capital for sustainable fishing and agriculture.

|

| o |

Pacifico certified more than 11 thousand people (including clients, non-clients and businesses’ employees) in risk prevention through its “ABC de Pacifico”, “Comunidad Segura” and “Protege365” programs, which

bolster resilience.

|

|

Indicator

|

Company

|

Unit

|

2024

|

1Q24

|

1Q25

|

|

Inclusion

|

|||||

|

People included financially through BCP and Yape – cumulative since 20202

|

BCP Peru and Yape

|

Million

|

5.7

|

4.2

|

6.0

|

|

Clients included in inclusive insurance services

|

Pacifico

|

Million

|

2.67

|

N.D.

|

2.77

|

|

Finance for the Future

|

|||||

|

Total loan balance for micro and small businesses

|

Mibanco Peru

|

S/ Million

|

11,356

|

11,618

|

11,629

|

|

Disbursements of sustainable financings

|

BCP Peru

|

$ Million

|

1,600

|

147

|

430

|

| 1 |

Simple and affordable optional insurance products with single or monthly payments of S/40 or less.

|

|

2

|

Stock of financially included clients through BCP since 2020: (i) New clients with savings accounts or affiliated to Yape. (ii) New clients without debt in the financial system

or BCP products in the last twelve months. (iii) Clients with 3 monthly average transactions in the last three months.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

| 01 |

Loan Portfolio

|

|

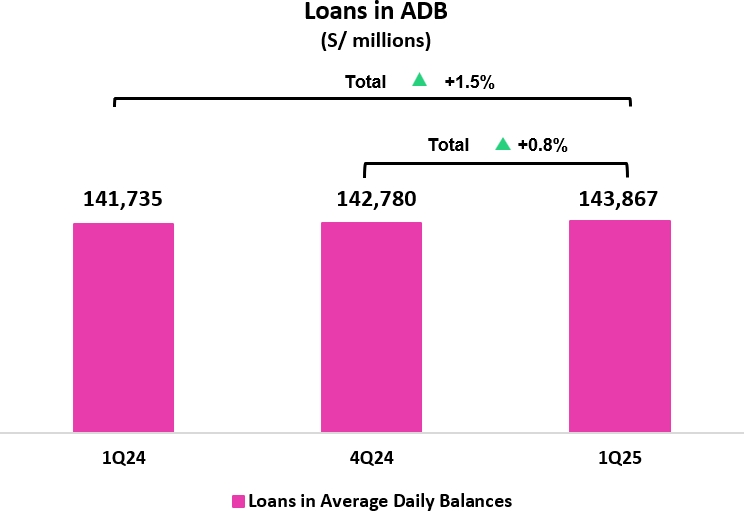

After reaching a turning point last quarter, total loans in average daily balances (ADB) rose 0.8% (+1.4% FX Neutral). QoQ, this

evolution was primarily driven by i) an increase in disbursements of short-term loans in Wholesale Banking, and ii) growth in loan disbursements through Yape and BCP in Consumer, and iii) an upturn in disbursements at Mibanco. This growth

was partially offset by a drop in loans in Small Businesses.

YoY, total loans in average daily balances rose 1.5% (+2.3% FX Neutral). This evolution was mainly driven by i) an uptick in

disbursements of short-term loans in Corporate Banking, ii) an upturn in disbursements in Mortgage and by iii) growth in disbursements in SME-Business. YoY growth was partially attenuated by the application of stricter loan guidelines at

Mibanco and by a drop in disbursements for long-term loans in SME-Pyme.

|

||||

| 1.1. |

Loans

|

|

Total Loans (1) (2) (3)

|

|

As of

|

Volume change

|

% change

|

% Part. In total

|

loans | ||||

|

(S/ millions)

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

QoQ

|

YoY

|

Mar 24

|

Dec 24

|

Mar 25

|

|

BCP Stand-alone

|

115,412

|

117,601

|

118,771

|

1,169

|

3,359

|

1.0%

|

2.9%

|

81.4%

|

82.4%

|

82.6%

|

|

Wholesale Banking

|

51,835

|

53,068

|

54,548

|

1,480

|

2,713

|

2.8%

|

5.2%

|

36.6%

|

37.2%

|

37.9%

|

|

Corporate

|

30,063

|

32,318

|

32,977

|

659

|

2,914

|

2.0%

|

9.7%

|

21.2%

|

22.6%

|

22.9%

|

|

Middle - Market

|

21,772

|

20,750

|

21,571

|

821

|

-201

|

4.0%

|

-0.9%

|

15.4%

|

14.5%

|

15.0%

|

|

Retail Banking

|

63,577

|

64,533

|

64,223

|

-311

|

646

|

-0.5%

|

1.0%

|

44.9%

|

45.2%

|

44.6%

|

|

SME - Business

|

7,294

|

7,956

|

7,590

|

-367

|

295

|

-4.6%

|

4.0%

|

5.1%

|

5.6%

|

5.3%

|

|

SME - Pyme

|

16,499

|

16,251

|

15,940

|

-311

|

-559

|

-1.9%

|

-3.4%

|

11.6%

|

11.4%

|

11.1%

|

|

Mortgage

|

21,050

|

21,709

|

21,870

|

161

|

821

|

0.7%

|

3.9%

|

14.9%

|

15.2%

|

15.2%

|

|

Consumer

|

12,723

|

12,755

|

12,961

|

206

|

237

|

1.6%

|

1.9%

|

9.0%

|

8.9%

|

9.0%

|

|

Credit Card

|

6,010

|

5,862

|

5,862

|

1

|

-148

|

0.0%

|

-2.5%

|

4.2%

|

4.1%

|

4.1%

|

|

Mibanco

|

13,244

|

12,057

|

12,147

|

90

|

-1,097

|

0.7%

|

-8.3%

|

9.3%

|

8.4%

|

8.4%

|

|

Mibanco Colombia

|

1,730

|

1,715

|

1,832

|

118

|

103

|

6.9%

|

5.9%

|

1.2%

|

1.2%

|

1.3%

|

|

Bolivia

|

9,362

|

9,628

|

9,469

|

-159

|

107

|

-1.7%

|

1.1%

|

6.6%

|

6.7%

|

6.6%

|

|

ASB

|

1,989

|

1,779

|

1,648

|

-131

|

-340

|

-7.4%

|

-17.1%

|

1.4%

|

1.2%

|

1.1%

|

|

BAP’s total loans

|

141,735

|

142,780

|

143,867

|

1,087

|

2,132

|

0.8%

|

1.5%

|

100.0%

|

100.0%

|

100.0%

|

|

For consolidation purposes. Loans generated in Foreign Currency (FC) are converted into Local Currency (LC).

|

|

| (1) |

Includes Special Accounts and other banking. For Quarter-end balance figures, please refer to “12. Annexes – 12.3 Loan Portfolio Quality”.

|

|

(2)

|

Internal Management Figures, non-audited.

|

| (3) |

Segmentation criteria have been updated and historical information restated to ensure comparability and better alignment with managerial reporting standards.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

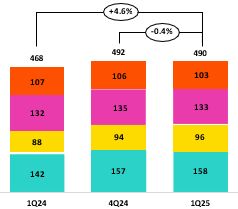

|

01. Loan Portfolio

|

|

|

• |

Wholesale Banking, due to an uptick in financing for working capital. In Middle Market Banking, growth was concentrated mainly

in the fishing sector, spurred by the fishing campaign that began at the end of 2024. In Corporate Banking, expansion was driven primarily by the construction and mining sectors.

|

|

|

• |

Consumer, mainly through an uptick in disbursements through Yape and BCP.

|

|

|

• |

Mibanco, due to an upturn in disbursements, particularly in the month of March, which reflects the improvements incorporated in our models to better assess risk

profiles and subsequently expand loan offerings.

|

|

|

• |

SME-Business, due to a seasonal effect given that clients that took on debt for working capital in 4Q24 amortized loans in 1Q25.

|

| • |

SME-Pyme, attributable to a drop in disbursements for long-term loans.

|

|

|

• |

Corporate Banking, due to the same dynamics seen QoQ.

|

|

|

• |

Mortgage, attributable to an uptick in the demand for loans due to favorable interest rates and economic reactivation.

|

|

|

• |

SME-Business, due to growth in loan disbursements through Government Programs (Impulso MyPerú), which were rolled out in 2Q24, and to an increase in

disbursements of negotiable invoices.

|

|

|

• |

Mibanco, after stricter lending guidelines were into effect at the end of 2Q24.

|

|

|

• |

Pyme, due to the same drivers in play QoQ.

|

|

|

|

Total Loans

|

Local Currency (LC) - S/ millions

|

% change

|

Foreign Currency (FC) - US$ millions

|

% change

|

% part. by currency

|

|||||||

|

Total

|

Total

|

Mar 25

|

||||||||||

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

LC

|

FC

|

|

|

BCP Stand-alone

|

78,329

|

79,978

|

79,947

|

0.0%

|

2.1%

|

9,842

|

10,011

|

10,526

|

5.1%

|

6.9%

|

67.3%

|

32.7%

|

|

Wholesale Banking

|

22,594

|

23,501

|

23,512

|

0.0%

|

4.1%

|

7,760

|

7,868

|

8,415

|

7.0%

|

8.4%

|

43.1%

|

56.9%

|

|

Corporate

|

13,126

|

14,540

|

14,110

|

-3.0%

|

7.5%

|

4,495

|

4,731

|

5,116

|

8.1%

|

13.8%

|

42.8%

|

57.2%

|

|

Middle-Market

|

9,468

|

8,961

|

9,401

|

4.9%

|

-0.7%

|

3,265

|

3,137

|

3,299

|

5.2%

|

1.0%

|

43.6%

|

56.4%

|

|

Retail Banking

|

55,735

|

56,478

|

56,436

|

-0.1%

|

1.3%

|

2,082

|

2,144

|

2,111

|

-1.5%

|

1.4%

|

87.9%

|

12.1%

|

|

SME - Business

|

4,141

|

4,738

|

4,529

|

-4.4%

|

9.4%

|

837

|

856

|

830

|

-3.1%

|

-0.9%

|

59.7%

|

40.3%

|

|

SME - Pyme

|

16,349

|

16,121

|

15,808

|

-1.9%

|

-3.3%

|

40

|

35

|

36

|

3.2%

|

-10.1%

|

99.2%

|

0.8%

|

|

Mortgage

|

19,100

|

19,794

|

20,049

|

1.3%

|

5.0%

|

518

|

510

|

494

|

-3.1%

|

-4.6%

|

91.7%

|

8.3%

|

|

Consumer

|

11,108

|

11,030

|

11,199

|

1.5%

|

0.8%

|

429

|

459

|

478

|

4.1%

|

11.4%

|

86.4%

|

13.6%

|

|

Credit Card

|

5,036

|

4,794

|

4,850

|

1.2%

|

-3.7%

|

259

|

284

|

274

|

-3.4%

|

6.1%

|

82.7%

|

17.3%

|

|

Mibanco

|

12,922

|

12,045

|

12,136

|

0.8%

|

-6.1%

|

85

|

3

|

3

|

-8.2%

|

-96.5%

|

99.9%

|

0.1%

|

|

Mibanco Colombia

|

-

|

-

|

-

|

-

|

-

|

459

|

456

|

497

|

8.9%

|

8.2%

|

-

|

100.0%

|

|

Bolivia

|

-

|

-

|

-

|

-

|

-

|

2,485

|

2,562

|

2,567

|

0.2%

|

3.3%

|

-

|

100.0%

|

|

ASB Bank Corp.

|

-

|

-

|

-

|

-

|

-

|

528

|

473

|

447

|

-5.6%

|

-15.3%

|

-

|

100.0%

|

|

Total loans

|

91,251

|

92,023

|

92,083

|

0.1%

|

0.9%

|

13,399

|

13,506

|

14,039

|

3.9%

|

4.8%

|

64.0%

|

36.0%

|

|

For consolidation purposes. Loans generated in Foreign Currency (FC) are converted into Local Currency (LC).

|

|

| (1) |

Includes Workout unit and other banking. For Quarter-end balance figures, please refer to “12. Annexes – 12.3 Loan Portfolio Quality”.

|

|

(2)

|

Internal Management Figures, non-audited.

|

| (3) |

Segmentation criteria have been updated and historical information restated to ensure comparability and better alignment with managerial reporting standards.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

01. Loan Portfolio

|

| (1) |

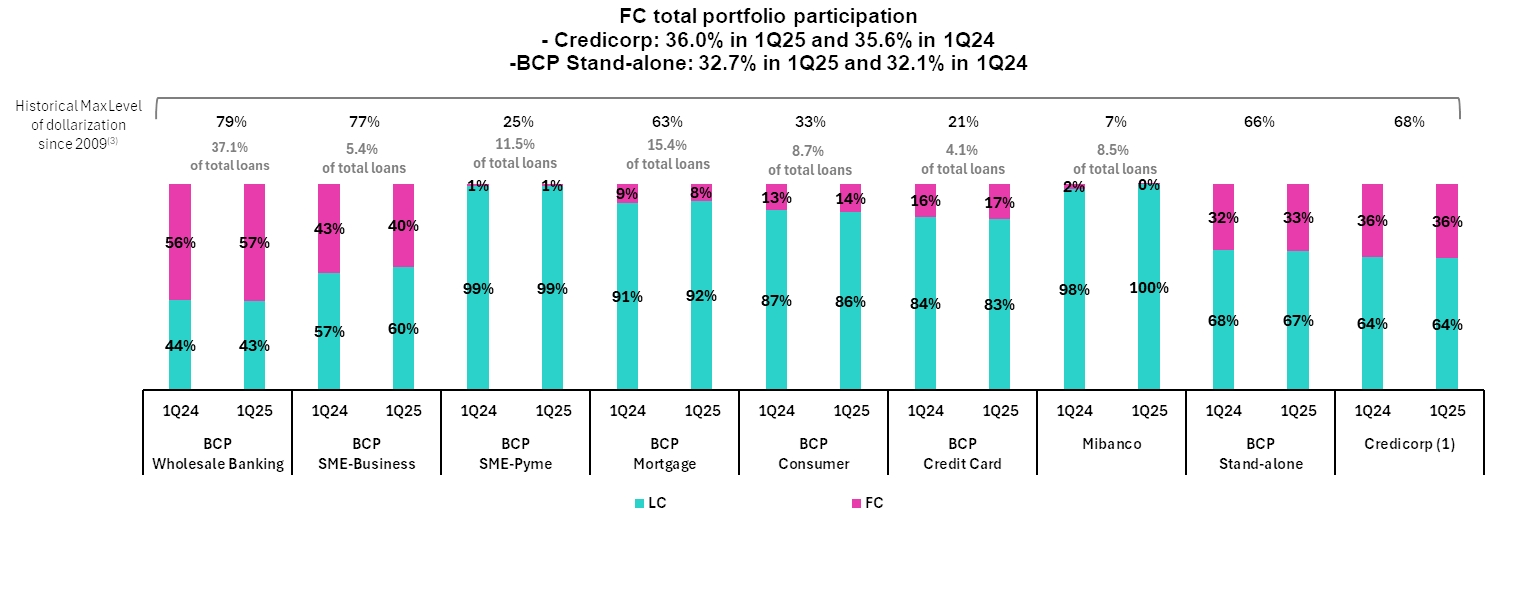

The FC share of Credicorp’s loan portfolio is calculated including BCP Bolivia and ASB Bank Corp., however the chart shows only the loan books of BCP Stand-alone and Mibanco.

|

| (2) |

The year with the historical maximum level of dollarization for Wholesale Banking was 2012, for Mibanco was 2016, for Credit Card was in 2021 and for the rest of segments was 2009.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

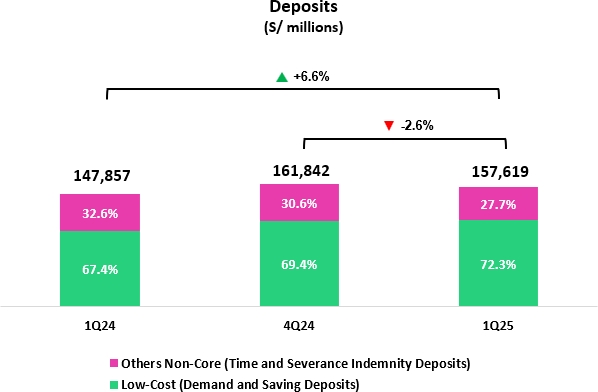

| 02 |

Deposits

|

|

Excluding the effect of the accounting adjustment related to the balance sheet of BCP Bolivia, the evolution of Deposists presented the

following dynamics.

Total Deposits rose slightly QoQ, driven primarily by a 5.2% increase in Demand Deposits, which was fueled by mainly by

growth in institutional activity and, to a lesser extent, by a 1.9% increase in Savings Deposits, which rose due to an uptick in Individuals through fund inflows from payments of employee profit sharing. YoY, the balance of deposits grew

due to a rise the low-cost deposit balance (+16.9%), where Savings Deposits rose 16.6% due to our ability to continue capturing funds and Demand Deposits were up 17.1%, driven by the same dynamics as those seen QoQ.

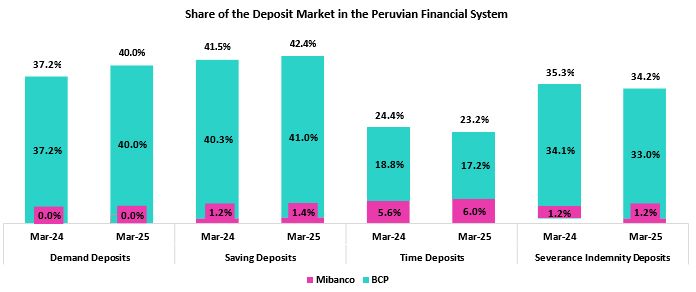

At the end of 1Q25, 71.8% of total deposits were low-cost deposits (Demand + Savings). Credicorp continues to lead the market for

low-cost deposits with a market share of 41.3% at the end of March.

|

|

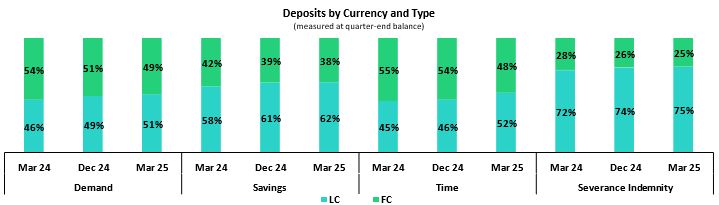

Deposits

|

|

As of

|

|

Change %

|

Currency

|

||

|

S/ 000

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

LC

|

FC

|

|

Demand deposits

|

47,384,819

|

52,590,952

|

53,992,480

|

2.7%

|

13.9%

|

50.9%

|

49.1%

|

|

Saving deposits

|

52,238,357

|

59,757,825

|

59,969,559

|

0.4%

|

14.8%

|

61.6%

|

38.4%

|

|

Time deposits

|

43,775,526

|

45,217,785

|

39,779,546

|

-12.0%

|

-9.1%

|

52.4%

|

47.6%

|

|

Severance indemnity deposits

|

3,086,767

|

2,996,020

|

2,921,196

|

-2.5%

|

-5.4%

|

75.1%

|

24.9%

|

|

Interest payable

|

1,371,658

|

1,279,484

|

956,301

|

-25.3%

|

-30.3%

|

29.4%

|

70.6%

|

|

Low-cost deposits (1)

|

99,623,176

|

112,348,777

|

113,962,039

|

1.4%

|

14.4%

|

56.5%

|

43.5%

|

|

Total Deposits

|

147,857,127

|

161,842,066

|

157,619,082

|

-2.6%

|

6.6%

|

55.6%

|

44.4%

|

|

(1)

|

Includes Demand Deposits and Saving Deposits

|

|

|

• |

5.2% growth in the balance of Demand Deposits, which was fueled primarily by an uptick in LC volumes at BCP Stand-alone. This expansion was driven mainly by Middle Market

Banking, principally via an increase in institutional activity and to a lesser degree through fund migration to Time Deposits following maturity.

|

|

|

• |

1.9% growth in Savings Deposits, which was driven mainly by an increase in LC volumes at BCP Stand-alone via clients in Individuals in the private sector, who received

profit-sharing payments in March.

|

|

|

• |

An 8.6% reduction in the Time Deposit balance. This decline was fueled by a drop in FC deposits at BCP Stand-alone after some wholesale deposits reached maturity and were

not renewed, in line with strategic decisions to optimize our funding structure.

|

|

|

• |

A 16.6% increase in the Savings Deposit balance, which was driven by growth in LC deposits at BCP Stand-alone. The primary driver of the uptick was our on-going efforts

to capture funds in a high-liquidity context; growth was also driven, albeit to a lesser extent, by the dynamics in play QoQ.

|

|

|

• |

17.1% growth in the balance of Demand Deposits, which was fueled by growth in the LC balance at BCP Stand-alone. The increase in LC was mainly attributable to the

evolution of the balance for Wholesale Banking, which rose due same dynamics seen QoQ, and secondarily to SMEs, where the balance increased through fund inflows from government loan disbursements.

|

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

02. Deposits

|

|

•

|

A 4.9% contraction in the Time Deposit balance, which was mainly fueled by a drop in the FC balance at BCP Stand-alone. This decrease was

due to the same dynamics seen QoQ, but was partially offset by growth in the LC balance in Individuals, which rose on the back of fund inflows from profit-sharing payments.

|

|

|

|

|

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

02. Deposits

|

|

|

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

| 03 |

Interest-Earning Assets (IEA) and Funding |

|

Excluding the effect of the accounting adjustment associated with the balance sheet of BCP Bolivia, the evolution of

the IEA and funding presented the following dynamics:

QoQ, IEA dropped 0.1% primarily due to a contraction in Cash and due from banks and secondarily to a decrease in the

Loan balance. These dynamics were partially offset by an increase in the investment balance in a context of a gradual acceleration in loan growth. Funding dropped 0.5%, mainly on the back of a bond maturity at BCP.

YoY, IEA rose 6.4% due to growth in Cash and due from banks, which reflects a high-liquidity environment.

Balances for Loans and Total Investments also contributed to growth in IEA, albeit to a lesser extent. Funding rose 6.7% due to expansion in deposits, which was concentrated in low-cost deposits, reflecting BCP’s solid

transactional offering.

|

||||

|

3.1.

|

IEA

|

|

Interest earning assets

|

As of

|

% change

|

|||

|

S/000

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

|

Cash and due from banks

|

31,134,572

|

40,119,937

|

37,521,839

|

-6.5%

|

20.5%

|

|

Total investments

|

52,555,386

|

53,825,858

|

55,604,610

|

3.3%

|

5.8%

|

|

Cash collateral, reverse repurchase agreements and securities borrowing

|

1,526,232

|

1,033,177

|

1,835,893

|

77.7%

|

20.3%

|

|

Loans

|

140,798,083

|

145,732,273

|

141,196,646

|

-3.1%

|

0.3%

|

|

Total interest earning assets

|

226,014,273

|

240,711,245

|

236,158,988

|

-1.9%

|

4.5%

|

| 3.2. |

Funding

|

|

Funding

|

As of

|

% change

|

|||

|

S/000

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

|

Deposits and obligations

|

147,857,127

|

161,842,066

|

157,619,082

|

-2.6%

|

6.6%

|

|

Due to banks and correspondents

|

10,684,673

|

10,754,385

|

10,899,579

|

1.4%

|

2.0%

|

|

BCRP instruments

|

6,854,368

|

6,646,830

|

7,064,476

|

6.3%

|

3.1%

|

|

Repurchase agreements with clients and third parties

|

2,636,908

|

2,413,880

|

3,094,138

|

28.2%

|

17.3%

|

|

Bonds and notes issued

|

17,541,121

|

17,268,443

|

14,391,733

|

-16.7%

|

-18.0%

|

|

Total Funding

|

185,574,197

|

198,925,604

|

193,069,008

|

-2.9%

|

4.0%

|

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

03. Interest-earning Assets (IEA) and Funding

|

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

|

04

|

Net Interest Income (NII)

|

|

|

In 1Q25, Net Interest Income (NII) fell 1.6% QoQ due to a drop in Interest and similar income, which registered a reduction in income on loans due to lower interest rates and an

uptick in Wholesale Loans’ share of total loans. Interest and similar expenses partially offset the reduction in income, given lower interest rates and a reduction in the funding volume.

YoY, NII rose 4.3%, driven by a reduction in Interest and similar expenses. This decline was attributable to a drop in interest on deposits, which reflected lower interest rates,

and an uptick in low-cost deposits’ share of the funding structure. Interest and similar income had a negative impact on NII, due primarily to a drop in interest on investments in a context of lower rates and

secondarily to a decline in interest on loans, given the same factors mentioned in the QoQ analysis.

NIM fell 12 bps QoQ to stand at 6.22%, spurred by a drop the yield on IEAs, which was partially offset by a reduction in the cost of funding. It is important to

note that Risk-adjusted NIM continued to trend upward and stood at a record high1 of 5.24%.

|

|

Net interest income

|

Quarter

|

% change

|

|||

|

S/000

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

Interest and Similar Income

|

4,925,926

|

5,012,121

|

4,894,790

|

-2.3%

|

-0.6%

|

|

Interest and Similar Expenses

|

(1,499,803)

|

(1,382,327)

|

(1,322,778)

|

-4.3%

|

-11.8%

|

|

Interest Expense (excluding Net Insurance Financial Expenses)

|

(1,377,799)

|

(1,250,239)

|

(1,187,156)

|

-5.0%

|

-13.8%

|

|

Net Insurance Financial Expenses

|

(122,004)

|

(132,088)

|

(135,622)

|

2.7%

|

11.2%

|

|

Net Interest, similar income and expenses

|

3,426,123

|

3,629,794

|

3,572,012

|

-1.6%

|

4.3%

|

|

|

|

|

|

|

|

|

Balances

|

|

|

|

||

|

Average Interest Earning Assets (IEA)

|

225,297,538

|

237,518,087

|

238,435,117

|

0.4%

|

5.8%

|

|

Average Funding

|

185,160,542

|

195,200,202

|

195,997,306

|

0.4%

|

5.9%

|

|

|

|

|

|||

|

Yields

|

|

|

|

||

|

Yield on IEAs

|

8.75%

|

8.44%

|

8.21%

|

-23 bps

|

-54 bps

|

|

Cost of Funds(1)

|

2.98%

|

2.56%

|

2.42%

|

-14 bps

|

-56 bps

|

|

Net Interest Margin (NIM)(1)

|

6.30%

|

6.34%

|

6.22%

|

-12 bps

|

-8 bps

|

|

Risk-Adjusted Net Interest Margin(1)

|

4.85%

|

5.08%

|

5.24%

|

16 bps

|

39 bps

|

|

Peru’s Reference Rate

|

6.25%

|

5.00%

|

4.75%

|

-25 bps

|

-150 bps

|

|

FED funds rate

|

5.50%

|

4.50%

|

4.50%

|

0 bps

|

-100 bps

|

|

(1)

|

For further details on the NIM and Cost of Funds calculation, please refer to Annex 12.7.

|

|

1

|

Since the implementation of IFRS 9 in 2018.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

04. Net Interest Income (NII)

|

|

|

|

Interest Income / IEA

|

|

1Q24 |

|

4Q24

|

|

1Q25 | |||

|

S/ millions

|

Average

|

|

Average

|

Average

|

|||||

|

|

Balance

|

Income

|

Yields

|

Balance

|

Income

|

Yields

|

Balance

|

Income

|

Yields

|

|

Cash and equivalents

|

28,556

|

334

|

4.7%

|

38,564

|

386

|

4.0%

|

38,821

|

345

|

3.6%

|

|

Other IEA

|

1,469

|

28

|

7.6%

|

1,227

|

18

|

5.9%

|

1,434

|

19

|

5.3%

|

|

Investments

|

52,385

|

694

|

5.3%

|

53,578

|

667

|

5.0%

|

54,715

|

683

|

5.0%

|

|

Loans

|

142,887

|

3,869

|

10.8%

|

144,150

|

3,940

|

10.9%

|

143,464

|

3,848

|

10.7%

|

|

Total IEA

|

225,297

|

4,925

|

8.7%

|

237,519

|

5,011

|

8.4%

|

238,434

|

4,895

|

8.2%

|

|

IEA (LC)

|

58.0%

|

69.9%

|

10.5%

|

54.7%

|

68.8%

|

10.6%

|

55.6%

|

70.5%

|

10.4%

|

|

IEA (FC)

|

42.0%

|

30.1%

|

6.3%

|

45.3%

|

31.2%

|

5.8%

|

44.4%

|

29.5%

|

5.5%

|

|

Interest Expense / Funding

|

|

1Q24 |

|

4Q24 |

|

1Q25

|

|||

|

S/ millions

|

Average

|

Average

|

Average

|

||||||

|

|

Balance

|

Expense

|

Yields

|

Balance

|

Expense

|

Yields

|

Balance

|

Expense

|

Yields

|

|

Deposits

|

147,782

|

780

|

2.1%

|

158,139

|

655

|

1.7%

|

159,731

|

620

|

1.6%

|

|

BCRP + Due to Banks

|

18,640

|

265

|

5.7%

|

17,447

|

287

|

6.6%

|

17,683

|

266

|

6.0%

|

|

Bonds and Notes

|

16,068

|

197

|

4.9%

|

17,110

|

201

|

4.7%

|

15,830

|

168

|

4.2%

|

|

Others

|

2,672

|

259

|

38.8%

|

2,504

|

239

|

38.2%

|

2,754

|

269

|

39.1%

|

|

Total Funding

|

185,162

|

1,501

|

3.2%

|

195,200

|

1,382

|

2.8%

|

195,998

|

1,323

|

2.7%

|

|

Funding (LC)

|

49.5%

|

51.9%

|

3.4%

|

49.6%

|

49.8%

|

2.8%

|

51.7%

|

53.4%

|

2.8%

|

|

Funding (FC)

|

50.5%

|

48.1%

|

3.1%

|

50.4%

|

50.2%

|

2.8%

|

48.3%

|

46.6%

|

2.6%

|

|

NIM(1)

|

225,297

|

3,424

|

6.1%

|

237,519

|

3,629

|

6.1%

|

238,434

|

3,572

|

6.0%

|

|

NIM (LC)

|

58.0%

|

77.8%

|

8.2%

|

54.7%

|

76.1%

|

8.5%

|

55.6%

|

76.8%

|

8.3%

|

|

NIM (FC)

|

42.0%

|

22.2%

|

3.2%

|

45.3%

|

23.9%

|

3.2%

|

44.4%

|

23.2%

|

3.1%

|

|

(1)

|

Unlike the NIM figure calculated according to the formula in Appendix 12.7, the NIM presented in this table includes “Financial Expense associated

with the insurance and reinsurance activity, net”.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

04. Net Interest Income (NII)

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

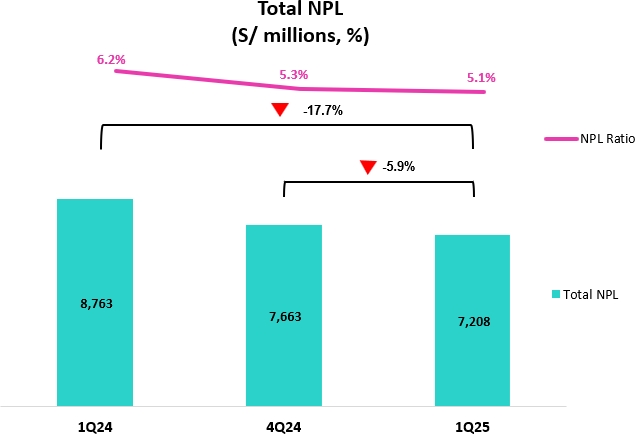

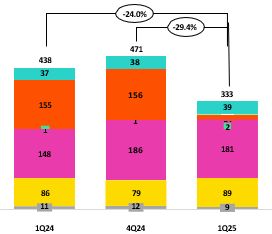

| 05 |

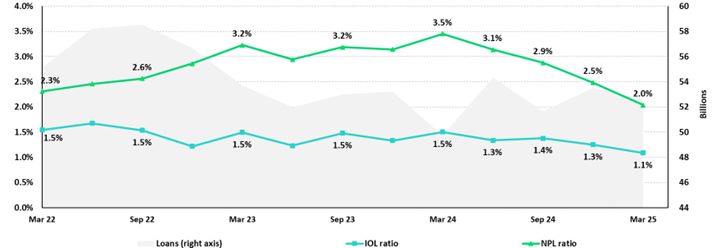

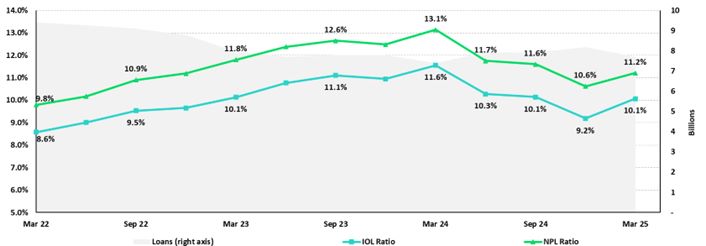

Portfolio Quality and Provisions

|

|

|

This quarter, the NPL ratio and Cost of Risk clearly reflect a noteworthy improvement and

continue to contract across segments, as a result of the cumulative impact of fortified underwriting and risk management, a relatively strong Peru economy, and some one-time events.

QoQ, the decline in NPLs at BCP Stand-alone was driven mainly by debt repayments in Wholesale and to a lesser extent,

by a drop in internal overdue loans in SME-Pyme. At Mibanco, the decrease in NPL volumes was fueled mainly by a reduction in internal overdue loans. In this context, the NPL ratio fell 16 bps and 112 bps QoQ and

YoY to stand at 5.1% at quarter-end.

QoQ, the decline in provisions was mainly attributable to BCP Stand-alone, where provisions

dropped primarily due to (i) a base effect base via calibrations in our risk models and an improvement in payment performance in Credit Cards and Consumer, and (ii) due to an uptick in reversals in Wholesale

Banking. This evolution was partially offset by an increase in provisions at Mibanco, due to a base effect given that write-offs were low last quarter. In this context, the cost of risk fell 44 bps and 66 bps QoQ

and YoY respectively to stand at 1.6% at quarter-end.

|

|

5.1

|

Portfolio Quality

|

|

Loan Portfolio quality and Delinquency ratios

|

|

As of

|

% change

|

||

|

S/000

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

|

Total loans (Quarter-end balance)

|

140,798,083

|

145,732,273

|

141,196,646

|

-3.1%

|

0.3%

|

|

Write-offs

|

950,433

|

896,714

|

716,585

|

-20.1%

|

-24.6%

|

|

Internal overdue loans (IOLs)

|

6,205,024

|

5,423,212

|

5,206,395

|

-4.0%

|

-16.1%

|

|

Internal overdue loans over 90-days

|

4,702,733

|

4,383,795

|

4,232,843

|

-3.4%

|

-10.0%

|

|

Refinanced loans

|

2,557,749

|

2,239,445

|

2,001,282

|

-10.6%

|

-21.8%

|

|

Non-performing loans (NPLs)

|

8,762,773

|

7,662,657

|

7,207,677

|

-5.9%

|

-17.7%

|

|

IOL ratio

|

4.4%

|

3.7%

|

3.7%

|

-3 bps

|

-72 bps

|

|

IOL over 90-days ratio

|

3.3%

|

3.0%

|

3.0%

|

-1 bps

|

-34 bps

|

|

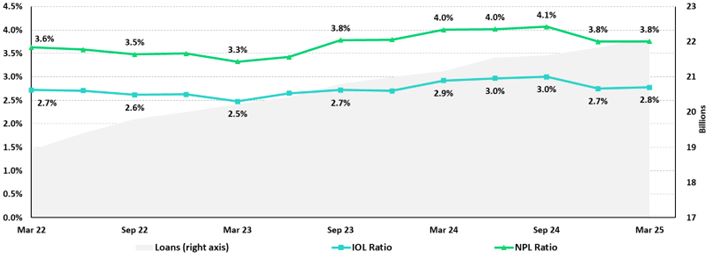

NPL ratio

|

6.2%

|

5.3%

|

5.1%

|

-16 bps

|

-112 bps

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

05. Portfolio Quality and Provisions

|

|

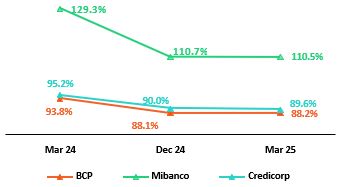

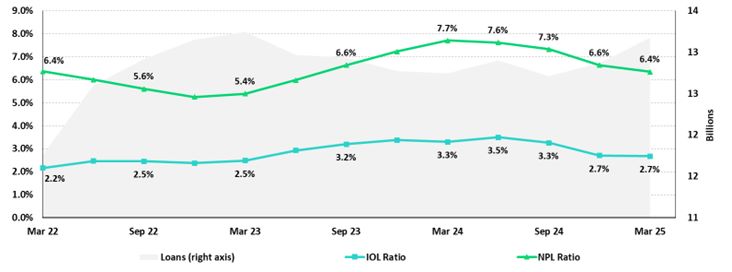

NPL Ratio for Total Loans

|

|

|

|

|

•

|

Mibanco, where the NPL Ratio dropped 99 bps, driven mainly by a decrease in NPL volumes and secondarily by slight growth in total loans.

|

|

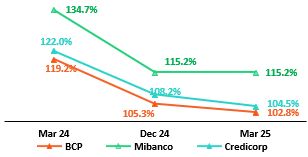

NPL Ratio for Total Loans at BCP (1)(2)

|

|

|

|

|

|

•

|

Mibanco, where the NPL Ratio fell 101 bps, due to a decrease in NPL Volumes, which was partially offset by a contraction in total loans.

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

05. Portfolio Quality and Provisions

|

|

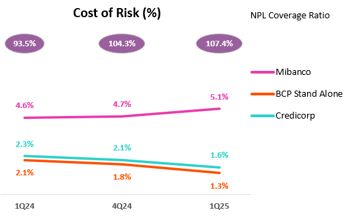

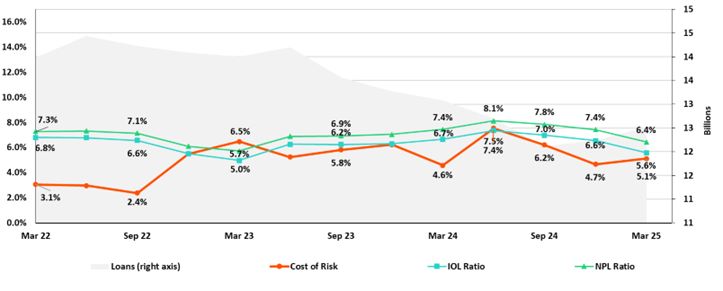

5.2

|

Provisions and Cost of Risk of the Total Portfolio

|

|

Loan Portfolio Provisions

|

|

Quarter |

% change

|

||

|

S/000

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

Gross provision for credit losses on loan portfolio

|

(910,189)

|

(857,694)

|

(695,733)

|

-18.9%

|

-23.6%

|

|

Recoveries of written-off loans

|

95,490

|

114,398

|

113,840

|

-0.5%

|

19.2%

|

|

Provision for credit losses on loan portfolio, net of recoveries

|

(814,699)

|

(743,296)

|

(581,893)

|

-21.7%

|

-28.6%

|

|

Cost of risk (1)

|

2.3%

|

2.1%

|

1.6%

|

-44 bps

|

-66 bps

|

|

|

|

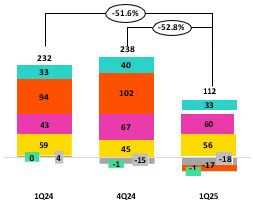

Cost of Risk by Subsidiary (1)

|

|

|

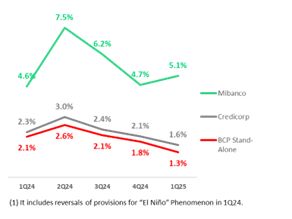

YoY, provisions fell 45.5%, driven by BCP Stand-alone

and Mibanco, which reported an improvement in payment performance in a context of economic recovery. At BCP Stand-alone, the drop in

provisions was primarily attributable to i) Consumer and Credit Cards, due to the same dynamics seen QoQ; and ii) SME-Pyme, due primarily to growth in the share of lower- risk vintages in the loan mix. This evolution was partially offset by an uptick in

provisions in Wholesale, which was associated with a base effect given that reversals were higher in 1Q24. At Mibanco, the drop was spurred by an improvement in underlying

risk as lower-risk vintages gained traction in the portfolio mix. In this context, the Cost of Risk at Credicorp fell 137 bps YoY to

stand at 1.6%.

|

|

|

|

|

QoQ Cost of Risk Evolution

|

|

YoY Underlying Cost of Risk Evolution*

|

|

(1) Others include BCP Bolivia, Mibanco Colombia, ASB and eliminations.

|

|

(*) It excludes reversals of provisions for “El Niño” Phenomenon in 1Q24.

(1) Others include BCP Bolivia, Mibanco Colombia, ASB and eliminations.

|

|

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

|

05. Portfolio Quality and Provisions

|

|

Loan Portfolio Quality and Delinquency Ratios

|

|

As of

|

% change

|

||

|

S/000

|

Mar 24

|

Dec 24

|

Mar 25

|

QoQ

|

YoY

|

|

Total loans (Quarter-end balance)

|

140,798,083

|

145,732,273

|

141,196,646

|

-3.1%

|

0.3%

|

|

Allowance for loan losses

|

8,190,343

|

7,994,977

|

7,742,792

|

-3.2%

|

-5.5%

|

|

Non-performing loans (NPLs)

|

8,762,773

|

7,662,657

|

7,207,677

|

-5.9%

|

-17.7%

|

|

Allowance for loan losses over Total loans

|

5.8%

|

5.5%

|

5.5%

|

-1 bps

|

-34 bps

|

|

Coverage ratio of NPLs

|

93.5%

|

104.3%

|

107.4%

|

308 bps

|

1395 bps

|

|

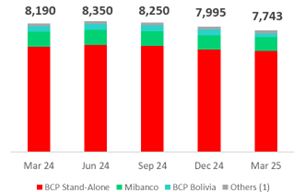

Allowance for loan losses

(in S/ millions)

|

|

|

|

|

|

QoQ, Allowances for Loan Losses fell 3.2%, driven primarily by BCP Bolivia and Mibanco.

YoY, Allowances for Loan Losses dropped 5.5%, driven primarily by Small Businesses and

Consumer at BCP Individual and secondarily by BCP Bolivia.

|

|

|

|

|

|

|

|

(1) Others include Mibanco Colombia, ASB and eliminations.

|

|

|

|

|

|

|

|

|

|

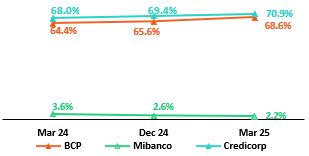

NPL Coverage Ratio

|

|

|

|

|

|

The NPL Coverage Ratio at Credicorp stood at 107.4% at the end of 1Q25. If we exclude NPL volumes from Government Loans (PG),

the ratio stands at 110.6%.

QoQ

the NPL Coverage Ratio at Credicorp rose 308 bps, driven by the evolution at BCP Stand-alone and Mibanco. Next, our analysis of this evolution will isolate the effect of NPL volumes of Government loans, which have broad guarantees and

are being honored satisfactorily.

QoQ, the NPL Coverage Ratio at BCP

Stand-alone, excluding Government Loans (GP), increased 431 bps to stand at 111.3%. This evolution was primarily driven by a decrease in NPL loans in Wholesale Banking and

Consumer. The NPL Coverage Ratio at Mibanco, excluding Government Loans (GP), rose 562 bps to stand at 108.5%, fueled by a

drop in NPLs, which was originated by the same factors seen QoQ.

|

|

|

|

|||

|

|

|||

|

| |

Earnings Release 1Q / 2025

|

Analysis of 1Q25 Consolidated Results

|

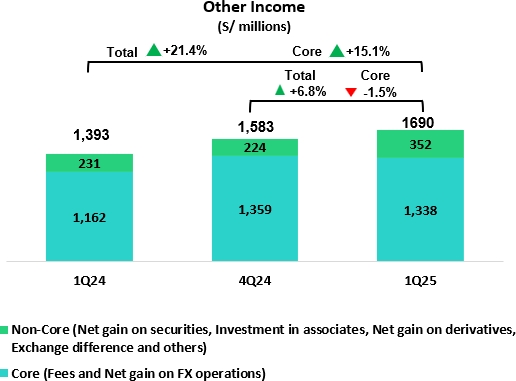

| 06 |

Other Income

|

|

|

This quarter, Other Income grew by 6.8% QoQ and 21.4% YoY. This evolution includes an

extraordinary gain of approximately S/236 million, resulting from the acquisition of the remaining 50% of Empresas Banmedica in the joint venture with Pacifico Seguros. Excluding this extraordinary gain, Other

Income showed the following dynamics:

QoQ, Other Income decreased by 8.1%. Other Core Income dropped 1.5% due to a decrease in Net Gain

on FX Transactions. Although Fee Income grew by 2.1%, reflecting solid recurring transactional dynamics, this evolution was offset by lower FX results, due to a loss in the USD position at BCP Bolivia. Other

Non-Core Income decreased by 47.9%, due to a base effect from the sale of real estate in BCP Stand-alone, as well as lower derivative income in ASB.

YoY, Other Income increased by 4.5%. Other Core Income rose 15.1%, driven by BCP

Stand-alone, which registered an uptick in fee income from Yape and gains on a rise in the volume of FX transactions by Retail clients.

|

|

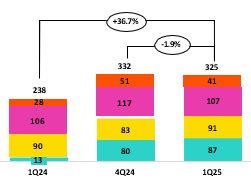

6.

|

Other Income

|

|

Other Income (1)

|

|

Quarter

|

% Change

|

||

|

(S/ 000)

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

Other Core Income

|

1,161,935

|

1,358,568

|

1,337,838

|

-1.5%

|

15.1%

|

|

Other Non-Core Income

|

230,624

|

224,164

|

352,378

|

57.2%

|

52.8%

|

|

Total Other Income

|

1,392,559

|

1,582,732

|

1,690,216

|

6.8%

|

21.4%

|

|

(1)

|

Beginning in 1Q25, accounting reclassifications have been incorporated affecting Fee Income, Net Gain on Foreign Exchange

Transactions, and Net Gain on Derivatives Held for Trading. Prior periods have been restated for comparability and may differ from previously reported figures.

|

|

6.1.

|

Other Core Income

|

|

Other Core Income (1)

|

|

Quarter |

% Change

|

||

|

(S/ 000)

|

1Q24

|

4Q24

|

1Q25

|

QoQ

|

YoY

|

|

Fee Income

|

856,565

|

973,338

|

994,024

|

2.1%

|

16.0%

|

|

Net Gain on Foreign Exchange Transactions

|

305,370

|

385,230

|

343,814

|

-10.8%

|

12.6%

|

|

Total Other Core Income

|

1,161,935

|

1,358,568

|

1,337,838

|

-1.5%

|

15.1%

|

|

•

|

QoQ, Other Core Income recorded solid results, maintaining levels above S/1.3 billion for the third consecutive quarter. The recurring