UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT PURSUANT

TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported): September 15, 2025

AMERICAN AXLE & MANUFACTURING HOLDINGS, INC.

(Exact Name of Registrant as Specified in Its Charter)

Delaware

(State or Other Jurisdiction of Incorporation)

| 1-14303 | 38-3161171 | |

| (Commission File Number) | (IRS Employer Identification No.) | |

| One Dauch Drive, Detroit, Michigan | 48211-1198 | |

| (Address of Principal Executive Offices) | (Zip Code) |

| (313) 758-2000 |

| (Registrant's Telephone Number, Including Area Code) |

| (Former Name or Former Address, if Changed Since Last Report) |

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

¨ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

¨ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

¨ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

¨ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock, par value $0.01 per share | AXL | The New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 7.01. | Regulation FD Disclosure |

In connection with the proposed senior notes offering described in Item 8.01 below, American Axle & Manufacturing Holdings, Inc. (“AAM”) is providing potential investors with a preliminary offering memorandum, dated September 15, 2025 (the “Preliminary Offering Memorandum”). The Preliminary Offering Memorandum contains (i) certain information not previously disclosed by AAM; (ii) unaudited pro forma condensed combined financial information giving effect to AAM’s pending combination (the “Combination”) with Dowlais Group plc (“Dowlais”) as of and for the six months ended June 30, 2025 and for the year ended December 31, 2024 and the related notes thereto; (iii) the audited financial statements of Dowlais as of December 31, 2024 and 2023 and for the years then ended and the related notes thereto and (iv) the unaudited financial statements of Dowlais as of June 30, 2025 and for the six-month periods ended June 30, 2025 and 2024 and the related notes thereto. This information is included in Exhibits 99.1, 99.2, 99.3 and 99.4 attached to this Current Report on Form 8-K (the “Form 8-K”), respectively, and incorporated herein by reference.

The information in this Item 7.01 and the exhibits attached to this Form 8-K as Exhibits 99.1, 99.2, 99.3 and 99.4 are being furnished pursuant to Item 7.01 of Form 8-K and shall not be deemed “filed” for purposes of Section 18 of the Securities Act of 1934, as amended, or otherwise subject to the liabilities of that Section nor shall they be deemed incorporated by reference into any filing under the Securities Act of 1933, as amended (the “Securities Act”), or the Securities Exchange Act of 1934, as amended, except as shall be expressly stated by specific reference in such filing.

| Item 8.01. | Other Events |

On September 15, 2025, AAM announced that its wholly-owned subsidiary, American Axle & Manufacturing, Inc. (the “Issuer”), intends to offer, subject to market and other conditions, $843 million of senior secured notes due 2032 (the “Secured Notes”) and $600 million of senior unsecured notes due 2033 (the “Unsecured Notes,” and together with the Secured Notes, the “Notes”) in an offering that is exempt from the registration requirements of the Securities Act.

The Secured Notes will be secured by a first priority security interest in substantially all of the assets of the Issuer, AAM and AAM’s subsidiaries (other than the Issuer) that guarantee its existing credit agreement, subject to certain thresholds, exceptions and permitted liens. Such assets will also continue to secure borrowings under the Issuer’s existing credit agreement on a pari passu basis. The Secured Notes will be unconditionally guaranteed on a senior secured basis and the Unsecured Notes will be unconditionally guaranteed on a senior unsecured basis by AAM and its subsidiaries (other than the Issuer) that guarantee its existing credit agreement.

The Issuer intends to use the net proceeds from this offering, together with borrowings under its existing credit agreement and cash on hand, (i) to pay the cash consideration payable in connection with the Combination with Dowlais and related fees and expenses, (ii) to repay in full all outstanding borrowings under the existing credit facilities of Dowlais and to pay related fees, expenses and premiums, after which the existing credit facilities of Dowlais will be terminated, (iii) to fund a change of control offer for certain outstanding notes of Dowlais and (iv) the remainder, if any, for general corporate purposes, which may include, among other things, repayment of debt.

Unless the Combination is consummated concurrently with the closing of the offering of the Notes, the Issuer will deposit into segregated escrow accounts for each of the Secured Notes and the Unsecured Notes an amount of cash equal to (i) in the case of the escrow account for the Secured Notes, the gross proceeds from the sale of such series of Secured Notes, together with additional amounts on the issue date and from time to time to prefund interest on the Secured Notes and (ii) in the case of the escrow account for the Unsecured Notes, the gross proceeds from $600 million aggregate principal amount of Unsecured Notes, together with additional amounts on the issue date and from time to time to prefund interest on $600 million aggregate principal amount of Unsecured Notes, in each case, until the date that certain escrow release conditions, including the consummation of the Combination, have been satisfied or a special mandatory redemption has occurred. The Notes of each series will be secured by a first priority security interest in its respective escrow account and all funds deposited therein. The consummation of the Combination is subject to the satisfaction of customary closing conditions.

The Issuer may elect to increase the amount of the Unsecured Notes in order to fund the redemption or other repayment in full of its outstanding unsecured 6.50% Senior Notes due 2027 and related fees and expenses, in which case the Issuer would expect to increase the offering size of the Unsecured Notes by approximately $500 million to $1.1 billion. If more than $600 million aggregate principal amount of Unsecured Notes is issued in this offering, the escrow and special mandatory redemption provisions described above will only apply to $600 million aggregate principal amount of Unsecured Notes. This 8-K does not constitute a notice of redemption with respect to the Issuer’s outstanding unsecured 6.50% Senior Notes due 2027.

A copy of the press release of AAM is filed as Exhibit 99.5 hereto. The press release is incorporated herein by reference in its entirety.

This Form 8-K, including the exhibits attached hereto, does not constitute an offer to sell, or a solicitation of an offer to buy, any security. No offer, solicitation, or sale will be made in any jurisdiction in which such an offer, solicitation, or sale would be unlawful. The Notes will not be registered under the Securities Act or the securities laws of any state or other jurisdiction, and, unless so registered, may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements.

Forward-Looking Statements

This report may contain statements concerning our expectations, beliefs, plans, objectives, goals, strategies, and future events or performance, including, but not limited to, the statements about the proposed offering of the Notes, our intention to issue the Notes, the expected use of proceeds and the Combination. Such statements are “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995 and relate to trends and events that may affect our future financial position and operating results. The terms such as “will,” “may,” “could,” “would,” “plan,” “believe,” “expect,” “anticipate,” “intend,” “project,” “target,” and similar words or expressions, as well as statements in future tense, are intended to identify forward-looking statements. Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time those statements are made and/or management’s good faith belief as of that time with respect to future events and are subject to risks and may differ materially from those expressed in or suggested by the forward-looking statements. These risks and uncertainties related to AAM include factors detailed in the reports AAM files with the Securities and Exchange Commission, including those described under “Risk Factors” in its most recent Annual Report on Form 10-K and its Quarterly Reports on Form 10-Q. It is not possible to foresee or identify all such factors and we make no commitment to update any forward-looking statement or to disclose any facts, events or circumstances after the date hereof that may affect the accuracy of any forward-looking statement.

| Item 9.01. | Financial Statements and Exhibits |

(d) Exhibits

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned, hereunto duly authorized.

| AMERICAN AXLE & MANUFACTURING HOLDINGS, INC. | |||

| Date: | September 15, 2025 | By: | /s/ Matthew K. Paroly |

| Matthew K. Paroly | |||

| Vice President, General Counsel & Secretary | |||

Exhibit 99.1

Basis of presentation

AAM Holdings’ historical financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). AAM Holdings publishes its financial statements in U.S. Dollars. Dowlais’ historical financial statements included in this offering memorandum have been prepared in accordance with IFRS® Accounting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). Dowlais publishes its financial statements in Pound Sterling. Certain financial information of Dowlais in this offering memorandum has been translated into U.S. Dollars for comparability and convenience purposes only. Unless otherwise indicated or the context otherwise requires, the rate used to translate Pound Sterling amounts to U.S. Dollars was 1.3574, which is the exchange rate reported by Bloomberg on September 11, 2025.

Prospective investors should consult their professional advisors for an understanding of: (i) any differences between GAAP, IFRS as issued by the IASB and other systems of generally accepted accounting principles and how these differences might affect the financial information included in this offering memorandum, and (ii) the impact that future additions to, or amendments of any such accounting principles may have on the results of operations and/or financial condition of AAM or Dowlais, as well as on the comparability of the prior periods.

This offering memorandum also includes certain financial and operating metrics for AAM Holdings and Dowlais combined as one company. These “combined” metrics are provided for illustrative purposes, are derived by combining the relevant historical financial or operating information of AAM Holdings and Dowlais and do not reflect pro forma adjustments and are not prepared in compliance with the requirements of Article 11 of Regulation S-X, as would be required if this offering of notes were registered with the SEC. These figures do not reflect what the Combined Group’s financial condition or results of operations would have been had the Transactions (as defined herein) occurred on or prior to the dates indicated. The Combined Group’s actual financial position and results of operations may differ significantly from the amounts reflected herein due to a variety of factors. See “Risk Factors—Risks Related to the Pending Combination with Dowlais.”

The statements and information included or incorporated by reference in this offering memorandum regarding synergies, cost savings and similar information were prepared by AAM Holdings and relate to the synergies and cost savings being targeted by AAM Holdings following the consummation of the Combination only, and are conditional upon the consummation of the Combination. Such statements and information are forward-looking statements subject to risks, and actual results may vary materially from such statements and information.

Unless otherwise stated herein, pro forma financial information gives effect to the Combination, anticipated incurrence of new indebtedness pursuant to the Second Amendment (as defined herein) and the Bridge Credit Agreements (as defined herein) and the use of proceeds therefrom (collectively, the “Transactions”), as described under “Unaudited Pro Forma Condensed Combined Financial Information.” References to financial or other data presented as “pro forma” or “on a pro forma basis” refer to a presentation that applies adjustments to give pro forma effect to the Transactions. The unaudited pro forma condensed combined financial information contained in this offering memorandum was calculated on the basis of assumptions made by the respective management of AAM Holdings and Dowlais at the time such information was prepared. For example, such unaudited pro forma condensed combined financial information reflects assumptions regarding the terms on which the Transactions will be completed and the terms of the indebtedness of the Combined Group that will be outstanding following completion of the Transactions. In particular, the unaudited pro forma condensed combined financial information contained in this offering memorandum does not give effect to any amendments to the Credit Agreement or the Co-operation Agreement or other modifications to the terms of the Transactions that may be agreed by the parties thereto and assumes the indebtedness incurred to fund the cash consideration payable in connection with the Combination and related fees and expenses and to repay certain existing indebtedness of Dowlais will be pursuant to the Second Amendment and the Bridge Credit Agreements rather than giving effect to this offering or to actual terms of the notes issued in this offering. See “Risk Factors—Risks Related to the Pending Combination with Dowlais—The unaudited pro forma financial information included in this offering memorandum may not be an indication of the Combined Group’s financial condition or results of operations following the Combination.”

The information included in this offering memorandum is not intended to, and does not, comply with all of the disclosure requirements of the SEC that would apply if this offering were being made pursuant to a registration statement filed with the SEC. Compliance with such requirements could require the modification or exclusion of certain financial measures and/or other information included in this offering memorandum and the inclusion of certain information not included in this offering memorandum. For example, the twelve months ended June 30, 2025 is not a fiscal period for us or Dowlais under GAAP or IFRS and, accordingly, the unaudited pro forma condensed combined financial information for the twelve months ended June 30, 2025 has not been prepared in compliance with the requirements of Article 11 of Regulation S-X, as would be required if this offering of notes were registered with the SEC. Similarly, certain “combined” metrics are derived by combining the relevant historical financial or operating information of AAM Holdings and Dowlais and do not reflect pro forma adjustments and are not prepared in compliance with the requirements of Article 11 of Regulation S-X, as would be required if this offering of notes were registered with the SEC.

Numerical figures included in this offering memorandum have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

In this offering memorandum, unless otherwise specified or the context otherwise requires:

| · | “Pound Sterling,” “Pounds,” “£,” “Pence” or “p” each refer to the lawful currency of the United Kingdom; and |

| · | “U.S. Dollars,” “Dollars,” “$” or “U.S.$” each refer to the lawful currency of the United States. |

Non-GAAP and non-IFRS financial measures

In addition to results reported in accordance with GAAP and IFRS as issued by the IASB in this offering memorandum, we have provided certain non-GAAP and non-IFRS financial measures such as EBITDA, Adjusted EBITDA, Segment Adjusted EBITDA, Adjusted Revenue, Free Cash Flow, Adjusted Free Cash Flow and Adjusted Operating Profit. Such information is reconciled to its closest GAAP or IFRS measure, as applicable, in accordance with SEC rules under “Summary—AAM Holdings Summary Consolidated Financial Data” and “Summary—Dowlais Summary Consolidated Financial Data.”

AAM Holdings defines EBITDA to be earnings before interest expense, income taxes, depreciation and amortization. AAM Holdings defines Adjusted EBITDA as EBITDA excluding the impact of restructuring and acquisition-related costs, debt refinancing and redemption costs, gains or losses on the derivative associated with the Combination, gains or losses on equity securities, pension curtailment and settlement charges, impairment charges and non-recurring items. AAM Holdings defines Segment Adjusted EBITDA as EBITDA for its reportable segments excluding the impact of restructuring and acquisition-related costs, debt refinancing and redemption costs, gains or losses on the derivative associated with the Combination, gains or losses on equity securities, pension curtailment and settlement charges, impairment charges and non-recurring items. AAM Holdings defines Free Cash Flow to be net cash provided by operating activities less capital expenditures net of proceeds from the sale of property, plant and equipment and from government grants. AAM Holdings defines Adjusted Free Cash Flow as Free Cash Flow excluding the impact of cash payments for restructuring and acquisition-related costs and cash payments related to the Malvern fire, including payments for capital expenditures, net of recoveries.

Dowlais defines Adjusted Revenue as external revenue including Dowlais’ share of revenue of equity accounted investments. Dowlais defines Adjusted Operating Profit as operating profit excluding items which are significant in size or volatility or by nature are non-trading or non-recurring and including the adjusted operating profit of equity accounted investments. Dowlais defines Adjusted EBITDA as Adjusted Operating Profit after adding back depreciation and impairment of property, plant and equipment and amortization of computer software and development costs, including that of equity accounted investments. Dowlais defines Free Cash Flow as cash generated after accounting for all trading costs, restructuring, pension contributions, and tax payments, but before any cash flows associated with financing activities (i.e. net cash from operating and investing activities). Dowlais defines Adjusted Free Cash Flow as Free Cash Flow adjusted for cash flows related to its demerger from Melrose Industries PLC, cash spend on AAM combination and net cash on business disposals.

We believe that EBITDA, Adjusted EBITDA, Segment Adjusted EBITDA, Adjusted Revenue, Free Cash Flow, Adjusted Free Cash Flow and Adjusted Operating Profit are meaningful measures of performance as they are commonly utilized by management and investors to analyze operating performance and entity valuation. Our management, the investment community and the banking institutions routinely use EBITDA and Adjusted EBITDA, together with other measures, to measure our operating performance relative to other Tier 1 automotive suppliers. We also use Segment Adjusted EBITDA as the measure of earnings to assess the performance of each segment and determine the resources to be allocated to the segments. We also believe Free Cash Flow and Adjusted Free Cash Flow are meaningful measures as they are commonly utilized by management and investors to assess our ability to generate cash flow from business operations to repay debt and return capital to our stockholders. EBITDA, Adjusted EBITDA, Free Cash Flow and Adjusted Free Cash Flow are also key metrics used in our calculation of incentive compensation. These non- GAAP and non-IFRS financial measures are not and should not be considered a substitute for any GAAP or IFRS measure. Additionally, non-GAAP and non-IFRS financial measures as presented may not be comparable to similarly titled measures reported by other companies.

Summary

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements (including the notes thereto) appearing elsewhere or incorporated by reference in this offering memorandum. Because this is a summary it may not contain all the information that may be important to you. You should read the entire offering memorandum, including the information incorporated by reference herein, before making an investment decision. Some of the statements in this “Summary” are forward-looking statements. Please see “Forward-Looking Statements” for more information regarding these statements.

Our company

AAM is a leading global tier 1 automotive and mobility supplier that designs, engineers and manufactures driveline and metal forming technologies to support electric, hybrid and internal combustion vehicles. AAM has its principal executive office in Detroit Michigan and operates over 75 facilities in 15 countries across North America, Europe, Asia, and South America. AAM has approximately 19,000 associates globally.

AAM has established a broad product portfolio that is designed to improve axle efficiency and fuel economy through innovative product design technologies. Its portfolio includes highly engineered axles, aluminum axles and all-wheel-drive applications. AAM’s metal forming segment represents the largest automotive forging operation in the world, and provides engine, transmission, driveline and safety-critical components for light, commercial and industrial vehicles.

We have aligned our business strategy to build value for our key stakeholders. We accomplish our strategic objectives by capitalizing on our competitive strengths and continuing to diversify our customer, product and geographic sales mix, while providing exceptional value to our customers. We are focused on securing and enhancing our core business of manufacturing products that support internal combustion engine (ICE) vehicle programs by delivering operational excellence and quality products to our customers, while growing our hybrid and electric vehicle business, as end-user acceptance of these vehicle types is expected to grow in the future. We have delivered on our objective, securing substantially all of our core platforms lasting beyond 2030. We believe we are favorably positioned in North America.

For the year ended December 31, 2024, we generated total revenues of $6,125 million and net income and adjusted EBITDA of $35 million and $749 million, respectively. For the six months ended June 30, 2025, we generated total revenues of $2,948 million and net income and adjusted EBITDA of $46 million and $380 million, respectively. Adjusted EBITDA is a non-GAAP financial measure. See “—AAM Holdings Summary Historical and Pro Forma Consolidated Financial Data” for a discussion of our use of our non-GAAP financial measures in this offering memorandum, including the reasons that we believe this information is useful to management and to investors, and a reconciliation of these non-GAAP financial measures to the most directly comparable financial measure calculated in accordance with GAAP.

Dowlais

Dowlais is a specialist engineering group focused on the automotive sector. Dowlais develops and delivers precisely engineered solutions for the automotive industry through its two high- technology engineering businesses: GKN Automotive and GKN Powder Metallurgy. Dowlais is headquartered in the United Kingdom, and operates in 22 countries and in 100 locations across the Americas, Europe and Asia, with over 70 manufacturing facilities and seven global innovation centers. Dowlais employes over 29,000 employees globally, including as part of its joint ventures. Dowlais has relationships with over ninety percent of global original equipment manufacturers, which are typically light vehicle original equipment manufacturers, and its components are present in approximately 45% of light vehicles in use globally.

GKN Automotive is a global leader in the development and production of side-shafts, propshafts, AWD systems and advanced differentials and a trusted partner to automotive OEMs globally. Its products drive the wheels of light vehicles around the world, and it has been a pioneer in the development of eDrive systems, remaining at the forefront of electric vehicle powertrain technology.

GKN Powder Metallurgy is a global leader in the production of sintered metal products for the automotive and industrial sectors and a leading manufacturer of atomized metal powders. Its world-class engineering expertise and sustainable technology enables the design and production of parts with complex geometries, higher densities and improved physical properties. It serves more than 2,000 customers globally and produces approximately ten million components daily.

Dowlais has a robust powertrain-agnostic product portfolio. 80.1% of its adjusted revenue is derived from the GKN Automotive segment, where 49% of its adjusted revenue is attributed to its market-leading side-shaft products, where it is approximately twice as large as the next-largest global competitor. The side-shaft product also benefits from the global mix shift towards more electrified vehicles, with approximately 14% more side shafts in a battery electric vehicle on average as compared to a vehicle powered by an internal combustion engine. 20% of Dowlais revenue is generated from its GKN Powder Metallurgy segment across three production flows: sinter metals, powder and additive manufacturing. GKN Powder Metallurgy serves both the automotive and industrial end markets.

Transaction overview

On January 29, 2025, we announced the terms of an offer (the “Offer”) by AAM Holdings to acquire the entire issued and to be issued share capital of Dowlais. Under the terms of the Offer, shareholders of Dowlais will be entitled to receive, for each ordinary share of Dowlais (each, a “Dowlais Share” and, collectively, the “Dowlais Shares”), 43 pence per share in cash and 0.0881 new shares of common stock of AAM Holdings, par value $0.01 per share (each share, an “AAM Share” and, collectively, the “AAM Shares”). In addition to the consideration payable in connection with the Combination, shareholders of Dowlais also received the payment of a final cash dividend by Dowlais of 2.8 pence for each Dowlais Share paid on May 29, 2025 (the “FY24 Final Dividend”).

The Combination has been unanimously approved by the Boards of Directors of AAM Holdings and Dowlais and by both companies’ shareholders. Following the close of the transaction, the combined company will be headquartered in Detroit, Michigan and will be led by AAM’s Chairman and CEO. The transaction is expected to close by the end of 2025, subject to the receipt of regulatory approvals and satisfaction of customary closing conditions.

We intend to use the net proceeds from this offering, together with borrowings under the Credit Agreement and cash on hand, (i) to pay the cash consideration payable in connection with the Combination and related fees and expenses, (ii) to repay in full all outstanding borrowings under the Dowlais Credit Facilities and to pay related fees, expenses and premiums, after which Dowlais Credit Facilities will be terminated, (iii) to fund the Dowlais Notes Change of Control Offer and (iv) the remainder, if any, for general corporate purposes, which may include, among other things, repayment of debt. See “Use of Proceeds.”

Strategic rationale

AAM and Dowlais are leading global tier-one automotive suppliers specializing in driveline and metal forming technologies for internal combustion, electric and hybrid vehicles. The combination of AAM and Dowlais will create a leading global manufacturer with the scale, product portfolio, technology and global diversification required to lead and innovate in a transitioning business environment. The Combined Group is expected to have 48,000 associates and operate in 25 countries over 170 locations.

We believe that the Combined Group will benefit from a more diversified business model across both customers and geographies as well as the synergies expected to arise from the combination of AAM and Dowlais. This business will feature a robust cash-generative financial profile, a strong balance sheet, and a more competitive and margin enhancing position than the standalone businesses, enabling continued innovation, growth, and long-term value creation for shareholders as the industry transitions to alternate propulsion technologies.

The Combination will bring together two companies with highly complementary customer bases, geographic footprints, powertrain-agnostic product portfolios and manufacturing operations. It will benefit from an experienced management team and the significant leadership depth present in both organizations.

Leading global driveline and metal-forming supplier with significant size and scale: The Combined Group benefits from greater scale and diversification, leading to enhanced financial and operational resilience. We believe this greater scale enables the business to better adapt to demand fluctuations and macroeconomic events; strengthens relationships with customers and other industry stakeholders; provides a competitive cost base driven by economies of scale; greater sharing of resources for research, development and investment, including electric vehicle transition and new technologies; and increased agility and flexibility in a dynamic, fast-moving industry.

Comprehensive powertrain-agnostic product portfolio with leading technology: The Combination creates an industry-leading portfolio of products across a broad range of automotive segments supporting internal combustion engine, hybrid and electric powertrains. Our leading position in beam axles is complemented by Dowlais’ strong position in side-shafts, and the two together position us to better compete for business with our existing and new customers. The metal forming and powder metallurgy product groups provide vertical integration capabilities as well as enhanced diversification with attractive and growing non-automotive industrial end markets. The Combined Group also benefits from enhanced scale to fund investments in future innovation across its powertrain-agnostic product portfolio.

Diversified customer base with expanded and balanced geographic presence: The Combined Group is positioned to take advantage of global markets by serving a wide range of vehicles with a well-diversified and complementary customer base. As adjusted for the Combination, the top three customers of the Group would account for only 48% of revenue with General Motors, Stellantis and Ford each representing 27%, 11% and 10%, respectively, as compared to approximately 68% of revenue for AAM standalone in the year ended December 31, 2024. Toyota, Volkswagen and Renault-Nissan will be the fourth, fifth and sixth largest customers, each representing 5%, 4% and 3% of sales, respectively. Additionally, the Combined Group is expected to benefit from a more balanced regional presence. AAM’s position in pickup trucks and SUVs and Dowlais’ position across multiple other vehicle segments globally would create an attractive business portfolio. The combined business will also have a strong foundation to serve the large and growing Chinese vehicle market, in particular with emerging domestic Chinese OEMs that are positioned for global growth, while also remaining favorably exposed to the profitable North American automotive market. As adjusted for the Combination, North America is expected to account for 57% of revenue, while Europe will account for 23%, the Asia-Pacific region will account for 18% and South America will account for the remaining 1% each for the year ended December 31, 2024, including Dowlais’ joint venture operations Compelling industrial logic with approximately $300 million of expected synergies: The complementary nature of AAM’s and Dowlais’ businesses is expected to enable the creation of annual run rate cost synergies of approximately $300 million, expected to be substantially achieved by the end of the third year after consummation of the Combination.

We estimate the costs required to achieve our synergy plan are approximately equal to one year of savings. The AAM management team has a proven acquisition track record, having successfully integrated and delivered cost synergy value through the acquisitions of MPG and Tekfor Group. Additionally, the Dowlais management team has demonstrated a proven track record of restructuring resulting in operational improvements.

High margins, with strong earnings accretion, cash flow and balance sheet: The Combined Group’s enhanced customer, geographic, and product diversification supports a best-in-class financial profile and greater free cash flow generation relative to our standalone business, with combined revenue of approximately $12 billion (calculated based on the unaudited pro forma financial information for the year ended December 31, 2024 included in the section of this offering memorandum entitled “Unaudited Pro Forma Condensed Combined Financial Information”) and combined Adjusted EBITDA margin of approximately 14% (calculated based on AAM’s definition of Adjusted EBITDA, the unaudited pro forma financial information for the year ended December 31, 2024 included in the section of this offering memorandum entitled “Unaudited Pro Forma Condensed Combined Financial Information” and certain other financial information of both AAM and Dowlais and assuming the full $300 million of estimated run rate synergies were achieved at the beginning of the period). See Basis of Presentation” regarding “combined” metrics, “Forward-Looking Statements” regarding synergies and “—AAM Holdings Summary Historical and Pro Forma Consolidated Financial Data” for a reconciliation of Adjusted EBITDA and Adjusted EBITDA margins to the most directly comparable GAAP metrics. The Combination could illustratively generate approximately $575 million of annual Adjusted Free Cash Flow when combining AAM historical annual average 2023 and 2024 Adjusted Free Cash Flow of approximately $225 million, Dowlais historical annual average 2023 and 2024 Adjusted Free Cash Flow of approximately $175 million excluding restructuring payments, synergy implementation costs and other items as per AAM’s definition of Adjusted Free Cash Flow, and assuming full realization of annual run rate synergy potential of $300 million, and after giving effect to illustrative incremental interest expense and taxes of approximately $125 million. This illustrative free cash flow generation would represent approximately 5% of combined sales. In addition, we took a prudent approach to funding this acquisition through a combination of both cash and shares.

AAM’s capital allocation policy will prioritize debt repayment while supporting organic growth until our net leverage ratio (defined as net debt (defined as total debt, less cash and cash equivalents) divided by the trailing 12 months of Adjusted EBITDA) is below 2.5 times, at which point AAM would be open to a more balanced capital allocation strategy, while continuing to target further net leverage reductions.

Competitive strengths

Sustained operational excellence and focus on cost management

We deliver operational excellence by leveraging our global standards, policies and best practices across all disciplines through the use of the AAM Operating System, which includes, among other elements, our S4 (S-to-the-fourth) safety system, Q4 (Q-to-the-fourth) quality system and E4 (E-to-the-fourth) energy and environmental sustainability system. We use this system to focus on customer satisfaction, lean production and efficient cost management, which allows us to improve quality, eliminate waste, and reduce lead time and total costs globally.

We maintain a cost competitive, operationally flexible global manufacturing, engineering and sourcing footprint to compete in global growth markets, support global product development initiatives and maintain regional cost competitiveness and generally produce products in-region for- region to better serve our global OEM customers.

Our business is vertically integrated to reduce cost and mitigate risk. Our Metal Forming segment, in addition to supplying component parts to many external customers, is a key supplier to our Driveline segment, helping to ensure continuity of supply and high level of quality for parts to our largest manufacturing facilities.

During 2024, we launched 11 programs across our business units for our customers including GM, Stellantis, Mercedes-AMG and Audi. In the first half of 2025, we also announced a significant new business win with Volkswagen’s Scout brand for their electrified Traveler SUV and Terra pickup truck.

Delivering exceptional quality, which is the foundation of our products’ durability and reliability

AAM’s Q4 internal quality assurance system drives continuous improvement to meet and exceed the growing expectations of our OEM customers.

In 2024, five of our global facilities received the GM Supplier Quality Excellence Award for outstanding quality performance during the 2023 performance year.

AAM was also recognized in 2024 for quality by several other customers including the Paccar 10 PPM Quality Award at our Hausach, Germany facility, the Ashok Leyland Certificate of Appreciation for Consistent Quality Performance at our Chennai, India facility and Pune, India facility, the Chery Excellent Supplier Award at our Changshu, China facility and the Jaguar Land Rover Quality Award at our Eisenach, Germany facility.

For the 2024 performance year, AAM was recognized by Ford with the Q1 Quality Award at our Bluffton, Indiana facility and our Pyeongtaek, South Korea facility.

Achieving technology leadership by delivering innovative products that enhance our product portfolio while increasing our total global served market

We are focused on securing and enhancing our core business, as the cash flows generated from our existing programs and products contribute to our research and development (“R&D”) investments that are expected to bring the future of the automotive industry faster. We leverage the extensive capabilities of our Driveline and Metal Forming business units to serve the future platforms of our global OEM customers. Our e-beam axle design is well-positioned to compete in the electrified powertrains of the future, exemplified by the recent announcement of the Scout Terra and Scout Traveler programs, and showcase the innovative product design approach our customers rely upon. In addition, we are the named supplier for the Scout brand’s front electric drive unit, showcasing our ability to bring our diverse product offerings together to support global OEMs and provide an integrated solution for their propulsion needs at a compelling value.

Our strategy

Securing and enhancing our core business

AAM has established a high-efficiency product portfolio that is designed to improve axle efficiency and fuel economy through innovative product design technologies. As our customers focus on reducing weight through the use of aluminum and other lightweighting alternatives, AAM is well positioned to offer innovative, industry leading solutions. Our portfolio includes high-efficiency axles, aluminum axles and AWD applications. AAM’s lightweight axle technology features an innovative design, which offers significant mass reduction and increased fuel economy and efficiency that is scalable across multiple applications without the loss of performance or power.

We have secured our core business as we have been awarded multiple next-generation full-size pickup truck front and rear axle programs, sport utility vehicle programs and crossover vehicle programs with OEM customers, and by also being named as the axle supplier for GM’s Chevrolet Colorado and GMC Canyon mid-size pickup trucks. Collectively, these awards secure a large portion of our revenues through 2030 and beyond. In addition, we believe we are favorably positioned for resurging quoting activity for ICE and hybrid powertrain programs as a result of slowing electric vehicle penetration in North America.

Our Metal Forming segment represents the largest automotive forging operation in the world, and provides engine, transmission, driveline and safety-critical components for light, commercial and industrial vehicles. We have developed advanced forging and machining process technologies to manufacture lightweight, highly precise and power-dense products. During 2024, our Metal Forming segment was awarded multiple internal combustion engine vehicle component programs by global OEMs.

We continue to evaluate our existing product portfolio for areas that are not core to our business in order to enhance AAM’s ability to compete globally while remaining cost competitive. During 2024, we entered into a definitive agreement to sell our commercial vehicle axle business and related assets in India (AAM India Manufacturing Corporation Pvt., Ltd.) for a sales price of $65 million, subject to certain customary adjustments at closing. The sale closed on July 1, 2025. In addition, during the first quarter of 2025 we exited our 50% ownership of Hefei AAM and Liuzhou AAM in China and collected $30 million in proceeds as a result.

Bringing the future faster

AAM’s Advanced Technology Development Center (ATDC) at our Detroit campus, allows us to accelerate technological advancements. This state-of-the-art facility is our center for technology benchmarking, prototype development, advanced technology development, supplier collaboration, customer showcasing and associate training on our future products, processes, and systems. Our Rochester Hills Technical Center (RHTC) in Michigan works closely with the ATDC to test and validate new and advanced technologies focused on lightweighting, efficiency and vehicle performance using enhanced diagnostic and hardware assessment capabilities. Our European Headquarters and Engineering Center (EHEC) in Langen, Germany, serves as our center of excellence for research and development, product testing and prototype development in Europe, and our Innovation Center at the Richard E. Dauch Institute in Mexico is focused on identifying ways to improve productivity while implementing manufacturing solutions, as well as educating our associates on process optimization and technology advances.

AAM’s investment in R&D has resulted in the development of advanced technology products designed to assist our customers in meeting the market demands for vehicle electrification; advanced and sophisticated electronic controls; lower emissions; enhanced power density; improved ride and handling performance; and enhanced reliability and durability.

AAM’s electric drive technology is designed, engineered and manufactured to provide a diverse and scalable product portfolio of hybrid and electric driveline systems to our customers that range from low-cost value-oriented offerings to high-performance solutions. This includes our e-Beam axles which incorporate high-reduction gearboxes and highly-integrated inverters. These hybrid and electric driveline systems leverage AAM’s experience in power density, torque transfer, noise- vibration-harshness reduction, heat management and systems integration, and are designed to improve fuel efficiency, reduce CO2 emissions and provide AWD capability. Our e-drive technology is designed to be segment agnostic, enabling our products to support a variety of markets and vehicle types.

During 2024, AAM announced new business awards in the Chinese market to supply Xpeng with 3-in-1 electric drive units, and to supply e-Beam axles to Skywell which is expected to launch in 2025.

Also during 2024, AAM announced a new business award to supply components to a global OEM for its new modular platform that will support multiple propulsion systems, as well as new business awards to supply various electric vehicle components for multiple OEM customers, including electric drive gears for a European OEM.

We are focused on increasing our presence in global markets to support our customers’ platforms

As our customers design their products for global markets, they will continue to require global support from their suppliers. For this reason, it is critical that we maintain a global presence in these markets in order to remain competitive for new contracts. To expand our global capabilities, we have established business offices and engineering centers of excellence in research and development, product testing and prototype development in North America, Europe and Asia.

We continue to evaluate and consider strategic opportunities that will complement our core strengths, supplement our diversification strategies and increase our presence in global markets, while providing future, profitable growth prospects. On January 29, 2025, we announced that we had reached an agreement with the Board of Directors of Dowlais Group plc (Dowlais) on the terms of a recommended cash and share offer to be made by AAM to acquire the entire issued and to be issued ordinary share capital of Dowlais for approximately $1.44 billion in cash and AAM shares. Our pending combination with Dowlais is a key step in achieving our goals of customer, product and geographic diversification.

The transactions

The combination

On January 29, 2025, we announced the Offer by AAM Holdings to acquire the entire issued and to be issued share capital of Dowlais. Under the terms of the Offer, shareholders of Dowlais will be entitled to receive, for each Dowlais Share, 43 pence per share in cash and 0.0881 new AAM Shares. In addition to the consideration payable in connection with the Combination, shareholders of Dowlais also received the FY24 Final Dividend.

As of September 11, 2025, the terms of the Combination (including the FY24 Final Dividend) represent a total implied value of 85.1 pence per Dowlais Share, based on the closing share price of $6.05 for each AAM Share and the Pound Sterling to U.S. Dollars exchange rate included in this offering memorandum. See “Basis of Presentation”. Upon the closing of the Combination, stockholders of AAM Holdings and shareholders of Dowlais would be expected to own approximately 51% and 49%, respectively, of AAM Holdings.

Following the closing of the Combination, AAM Holdings will continue to be the ultimate parent of its subsidiaries and will become the direct parent of Dowlais and the ultimate parent of Dowlais’ subsidiaries. The Combined Group will be headquartered in Detroit, Michigan and will be led by AAM Holdings’ Chairman and CEO. Two directors of Dowlais are expected to join AAM Holdings’ board of directors and certain senior Dowlais executives will be invited to join the senior executive management team of the Combined Group, in roles to be confirmed. The transaction is expected to close by the end of 2025, subject to receipt of regulatory approvals and satisfaction of customary closing conditions.

On July 15, 2025, AAM Holdings’ stockholders approved all proposals relating to the Combination, including a charter amendment to increase the number of authorized AAM Shares and the issuance of additional AAM Shares to shareholders of Dowlais. On July 22, 2025, the requisite majority of scheme shareholders voted to approve the Scheme at the court meeting held by Dowlais and the requisite majority of Dowlais shareholders voted to approve the special resolution put forth at the general meeting held by Dowlais, each of which meetings was held in connection with the Combination. Following these approvals, the remaining conditions to closing of the Combination are:

| · | the sanction (which is incapable of being waived by either AAM or Dowlais) of the Scheme by the High Court of Justice in England and Wales (the “Court”) (without modification or with modification on terms agreed by AAM and Dowlais) and delivery of a copy of the Court Order sanctioning the Scheme to the Registrar of Companies in England and Wales; |

| · | the hearing of the Court at which Dowlais will seek an order sanctioning the Scheme (the “Sanction Hearing”) being held on or before the 22nd day after the expected date of the Sanction Hearing to be set out in due course in the scheme document sent to Dowlais shareholders describing the terms and conditions of the Scheme and notices of Dowlais meetings and the forms of proxy applicable to Dowlais (or such later date (a) as AAM and Dowlais may agree or (b) (in a competitive situation) as may be specified by AAM with the consent of the UK Panel on Takeovers and Mergers (the “Panel”), and in each case that, if so required, the Court may allow); |

| · | the Scheme becoming effective by June 29, 2026 (or such later date (if any) as AAM and Dowlais may agree, with the consent of the Panel and the Court may allow), which is incapable of being waived by either AAM or Dowlais; |

| · | confirmation having been received by AAM (which is incapable of being waived by either AAM or Dowlais) that the new shares of AAM issued pursuant to the Offer have been approved for listing, subject to official notice of issuance, on the NYSE; and |

| · | the receipt of certain required antitrust approvals as well as regulatory, foreign direct investment and other approvals, certain of which may be capable of being waived by AAM. |

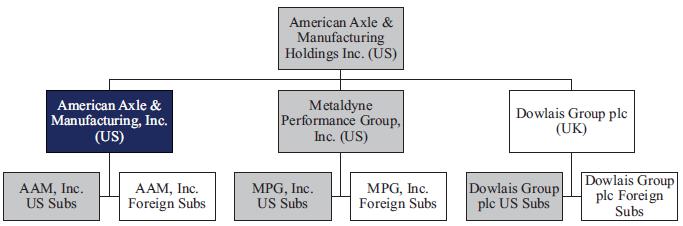

Pro forma organizational chart

The following chart provides a summary of our simplified corporate structure, as of June 30, 2025 on a pro forma as adjusted basis to give effect to the Transactions. This chart is provided for illustrative purposes only, and does not represent all legal entities affiliated with, or all obligations of, the Combined Group and does not distinguish between direct and indirect ownership. For example, not all subsidiaries of the Combined Group are depicted and not all depicted subsidiaries are wholly-owned subsidiaries.

The following chart should be read in conjunction with the other more detailed information appearing elsewhere or incorporated by reference into this offering memorandum.

|

Issuer of the existing notes and the notes offered hereby and borrower under the Credit Agreement |

|

Guarantors of the existing notes and the notes offered hereby and the Credit Agreement (including subsidiaries of Dowlais that will become guarantors of the existing notes and the notes offered hereby and the Credit Agreement, and, in each case, subject to certain exceptions) |

Financing related to the combination

AAM Holdings expects to fund the cash portion of the consideration in connection with the Combination and related transactions costs using $843.0 million principal amount of borrowings under an incremental Tranche C Term Facility (as defined herein) under the Credit Agreement, the proceeds from this issuance of notes and cash on hand. See “Use of Proceeds.”

This offering of notes is not contingent upon the completion of the Combination. As a result, we cannot assure you that the Combination will be consummated or, if consummated, that it will be consummated for the price, within the timeframe or on the terms and with the anticipated benefits we currently expect. However, in the event the Combination is not completed, the entire principal amount of secured notes and $600 million aggregate principal amount of unsecured notes, will be subject to a special mandatory redemption. See “Description of Secured Notes—Escrow of proceeds; Special Mandatory Redemption” and “Description of Unsecured Notes—Escrow of proceeds; Special Mandatory Redemption.”

Credit agreement amendment

AAM Holdings and AAM Inc. are parties to an amended and restated credit agreement that was entered into on March 11, 2022 and has been subsequently amended by the Second Amendment, as defined below (as may be amended from time to time, the “Credit Agreement”) which provides for a term loan A facility (the “Term Loan A Facility”), term loan B facility (the “Term Loan B Facility”), the incremental tranche C term facility (the “Tranche C Term Facility”) and a multi-currency revolving credit facility (the “Revolving Credit Facility”).

On February 24, 2025, AAM Holdings and AAM Inc. entered into the Second Amendment to the Amended and Restated Credit Facility and the Incremental Facility Agreement (the “Second Amendment”). The Second Amendment, among other things, (i) increased the maximum under the Revolving Credit Facility from $925.0 million to $1,495.0 million, effective upon closing of the Combination, (ii) provided for an $843.0 million incremental Tranche C Term Facility in connection with the Combination and (iii) extended the maturity of the Revolving Credit Facility and Term Loan A Facility for five years from the date of the Second Amendment, resetting for another five years upon the closing of the Combination.

Bridge facilities

On January 29, 2025, in connection with the announcement of the Combination, AAM Holdings and AAM Inc. entered into a First Lien Bridge Credit Agreement (the “First Lien Bridge Facility”), and a Second Lien Bridge Credit Agreement (the “Second Lien Bridge Facility” and together with the First Lien Bridge Facility, the “Bridge Facilities”).

Additionally, in connection with entry into the Second Amendment, on February 24, 2025, AAM Holdings and AAM Inc. entered into (i) an Amended and Restated First Lien Bridge Credit Agreement which will provide us with a $843.0 million interim loan facility in connection with the Combination (the “Amended and Restated First Lien Bridge Credit Agreement”) and (ii) an Amended and Restated Second Lien Bridge Credit Agreement which will provide us with a $500.0 million interim loan facility in connection with the Combination (the “Amended and Restated Second Lien Bridge Credit Agreement”, and together with the Amended and Restated First Lien Bridge Credit Agreement, the “Bridge Credit Agreements”).

The amounts available under the Bridge Credit Agreements will be reduced by, among other things, the net proceeds we receive from this offering. We currently expect that the net proceeds of this offering, along with borrowings under our Credit Agreement and cash on hand, will be sufficient to fund the cash consideration of the Combination. While not anticipated, if and to the extent we do not receive sufficient net proceeds in this offering, we may be required to borrow additional amounts under our Credit Agreement or under the Bridge Credit Agreements in order to finance the Combination. The funding of the Bridge Credit Agreements is contingent upon the satisfaction of customary conditions the consummation of the Combination.

Certain of the initial purchasers are lenders under our Credit Agreement. In addition, certain of the initial purchasers and/or their affiliates provided the committed financing under the Bridge Credit Agreements. See “Plan of Distribution.”

Transactions related to the outstanding debt of Dowlais

Repayment of the Dowlais Credit Facilities

In connection with the closing of the Combination, we intend to repay in full all outstanding borrowings of Dowlais under its £100 million and €100 million term loans as well as its £350 million, $660 million and €450 million revolving credit facilities (collectively, the “Dowlais Credit Facilities”) and to pay related fees, expenses and premiums. Following such repayment, the Dowlais Credit Facilities will be terminated. As of June 30, 2025, the aggregate principal amount outstanding under the Dowlais Credit Facilities was $1.29 billion (based on the exchange rate included in this offering memorandum. See “Basis of Presentation”).

Change of control offer for the Dowlais Notes

Following the closing of the Combination, AAM will be required to make a change of control offer for the outstanding Dowlais Notes (the “Dowlais Notes Change of Control Offer”). Pursuant to the terms of the note purchase agreement governing the Dowlais Notes (the “Note Purchase Agreement”), the consummation of the Combination will constitute a “Change of Control.” Under the terms of the Note Purchase Agreement, the holders of the Dowlais Notes will have the right to require Dowlais to repurchase all of the holders’ Dowlais Notes at a purchase price equal to 100% of the principal amount of the applicable Dowlais Notes, plus accrued and unpaid interest thereon to the repurchase date. Pursuant to the terms of the Note Purchase Agreement, the Dowlais Notes Change of Control Offer will be made within 15 business days after the closing of the Combination and the repurchase date will be not less than 30 days and not more than 60 days after the date on which we make the Dowlais Notes Change of Control Offer to the holders of the Dowlais Notes.

As of June 30, 2025, Dowlais had the following outstanding notes: (i) 5.77%. Series A Senior Notes due 2029, having the aggregate outstanding principal amount of $145,000,000, (ii) 5.97% Series B Senior Notes due 2031, having the aggregate outstanding principal amount of $48,000,000, (iii) 6.07% Series C Senior Notes due 2032, having the aggregate outstanding principal amount of $100,000,000, (iv) 6.26% Series D Senior Notes due 2034, having the aggregate outstanding principal amount of $102,000,000 and (v) 6.36% Series E Senior Notes due 2036, having the aggregate outstanding principal amount of $105,000,000, in each case, issued by GKN Industries Limited, a subsidiary of Dowlais, and guaranteed by Dowlais and certain of its subsidiaries (collectively, the “Dowlais Notes”). As of June 30, 2025, Dowlais had $500 million of Dowlais Notes outstanding.

The decision as to whether to tender the Dowlais Notes in the Dowlais Notes Change of Control Offer will be made by each holder of Dowlais Notes at their discretion and for this reason, we cannot accurately predict the outcome of the Dowlais Notes Change of Control Offer. Any remaining proceeds not used to fund the Dowlais Notes Change of Control Offer will be used for general corporate purposes, which may include, among other things, repayment of debt.

Transfer of U.S. subsidiaries of Dowlais to AAM and the related disposal offer

Following the closing of the Combination, Dowlais will consider selling to AAM all U.S. subsidiaries of Dowlais at fair value of the subsidiaries (the “Disposal”). AAM expects to fund the Disposal with cash on hand and, if needed, borrowings under the Revolving Credit Facility.

In accordance with the terms of the Notes Purchase Agreement, if this transaction occurs, Dowlais will be required to make a disposal offer (the “Disposal Offer”) to the holders of the Dowlais Notes to repurchase the Dowlais Notes with the net proceeds (defined as cash consideration for the Disposal less payments of certain expenses, taxes and pension contributions) from the Disposal, at a purchase price equal to 100% of the principal amount of the applicable Dowlais Notes, plus accrued and unpaid interest thereon to the repurchase date. The Disposal Offer would be made concurrently with the Dowlais Notes Change of Control Offer and Dowlais would repurchase any Dowlais Notes tendered pursuant to the Disposal Offer concurrently with the Dowlais Notes tendered for repurchase in connection with the Dowlais Notes Change of Control Offer.

The decision as to whether to tender the Dowlais Notes in the Disposal Offer will be made by each holder of Dowlais Notes at their discretion and for this reason, we cannot accurately predict the outcome of the Disposal Offer.

The completion of the Dowlais Notes Change of Control Offer or the Disposal Offer will not be a condition to closing of the Combination.

The notes will be structurally subordinated to any Dowlais Notes that remain outstanding following completion of the Dowlais Notes Change of Control Offer and the Disposal Offer. See “Risk Factors—If the Dowlais Notes Change of Control Offer and the Disposal Offer are not fully accepted, the notes will be structurally subordinated to the Dowlais Notes.”

Certain of the initial purchasers or their affiliates may be lenders under the Dowlais Credit Facilities or owners of the Dowlais Notes, in which case such initial purchasers or their affiliates may receive a portion of the net proceeds of this offering in connection with the repayment in full or in part of amounts outstanding under the Dowlais Credit Facilities or the Dowlais Notes following the Dowlais Notes Change of Control Offer (to the extent any such notes are tendered in the Dowlais Notes Change of Control Offer). See “Plan of Distribution.”

Escrow arrangements

The issuance of the notes may occur prior to the date on which a copy of the Court Order sanctioning the Scheme is duly filed on behalf of Dowlais with the Registrar of Companies in England and Wales and the Scheme becomes effective in accordance with section 899 of the Companies Act 2006 (the “Scheme Effective Date”). If so, on the issue date, pending the occurrence of the Scheme Effective Date, AAM Inc. will deposit into segregated escrow accounts for each of the secured notes and the unsecured notes (i) an amount of cash equal to (1) in the case of the escrow account for the secured notes, the gross proceeds from the sale of such series of secured notes in this offering and (2) in the case of the escrow account for the unsecured notes, the gross proceeds from $600 million aggregate principal amount of unsecured notes and (ii) an amount of cash equal to (1) in the case of the escrow account for the secured notes, the amount of interest that would accrue on the secured notes from and including the issue date to, but excluding October 31, 2025 and (2) in the case of the escrow account for the unsecured notes, the amount of interest that would accrue on $600 million aggregate principal amount of unsecured from and including the issue date to, but excluding October 31, 2025. Prior to the release of the proceeds from escrow, the respective escrow accounts and the funds therein will be pledged on a first- priority basis as collateral for the benefit of holders of the applicable series of notes. If neither the Escrow Release Date nor a special mandatory redemption has previously occurred, no later than three business days prior to the end of each month (commencing October 31, 2025) and ending with the Escrow Outside Date (as defined herein), AAM Inc. will deposit (or cause to be deposited) in each escrow account an amount of additional cash equal to the interest that would accrue on the applicable series of notes from and including the last day of the then-current month to, but excluding, the last day of the next succeeding month.

Upon delivery to the escrow agent, the Secured Notes Trustee (as defined herein) and the Unsecured Notes Trustee (as defined herein) of an officer’s certificate instructing the escrow agent to release the escrowed funds and certifying that (1) all conditions precedent to the Combination have been satisfied or waived in accordance with the terms of the Scheme documents as in effect on the date of this offering memorandum, without amendment or waiver in a manner that would be materially adverse to the holders of the secured notes, other than (A) the payment of the consideration to be paid for the Combination for which the escrowed funds are required (but subject to the payment of such consideration using the escrowed funds), and (B) such other conditions precedent that by their nature are to be satisfied at the time of completion of the Combination (but subject to the satisfaction or waiver of such conditions); (2) the Scheme Effective Date has occurred or substantially concurrently with the release of the escrowed funds will occur and (3) no Default or Event of Default has occurred and is continuing at the time of, or immediately after giving effect to, the Combination (clauses (1), (2) and (3), collectively, the “Escrow Conditions”), the escrowed funds will be released to AAM Inc. See “Description of Secured Notes—Escrow of proceeds; Special Mandatory Redemption” and “Description of Unsecured Notes—Escrow of proceeds; Special Mandatory Redemption.” In addition, if the Escrow Conditions are satisfied, a deferred discount will be paid to the initial purchasers in connection with this offering.

If the Escrow Conditions are not satisfied on or prior to the later of (i) June 29, 2026 and (ii) such later date (if any) as AAM Holdings and Dowlais may agree to extend the “Long Stop Date” (as defined in the Co-operation Agreement in accordance with the Co-operation Agreement) (such later date, the “Escrow Outside Date”), or such earlier date if AAM Inc. determines in its sole discretion that the Escrow Conditions cannot be satisfied or AAM Inc. notifies the escrow agent, the Secured Notes Trustee and the Unsecured Notes Trustee in writing that AAM Inc. will not pursue the consummation of the Combination and/or the Scheme lapses or is terminated (such earliest date, the “Special Termination Date”), AAM Inc. will be required to redeem all of the outstanding secured notes and $600 million aggregate principal amount of the unsecured notes on the third business day thereafter at a price equal to 100% of the initial issue price of such notes, together with accrued and unpaid interest on such notes, if any, to, but excluding, the date of such special mandatory redemption. Escrowed funds would be released and applied to pay for any such redemption. See “Description of Secured Notes—Escrow of proceeds; Special Mandatory Redemption” and “Description of Unsecured Notes—Escrow of proceeds; Special Mandatory Redemption.”

If the issuance of the notes occurs on or after the Scheme Effective Date, none of the escrow provisions described in this offering memorandum will be applicable, no proceeds of this offering will be deposited into the escrow accounts and all such proceeds will be provided to AAM Inc. on the issue date for use as described under “Use of Proceeds.” We may elect to increase the amount of unsecured notes being offered hereby in order to fund the redemption or other repayment in full of our outstanding unsecured 6.50% Senior Notes due 2027 and related fees and expenses, in which case we would expect to increase the offering size of the unsecured notes by approximately $500 million to $1.1 billion. Even if more than $600 million aggregate principal amount of unsecured notes is issued in this offering, the special mandatory redemption provisions described herein will only apply to $600 million aggregate principal amount of unsecured notes and the amount of proceeds from the unsecured notes that is deposited into escrow upon issuance will remain equal to the gross proceeds of $600 million aggregate principal amount of unsecured notes. See “Risk Factors—Risks Related to the Unsecured Notes—If we issue more than $600 million aggregate principal amount of unsecured notes in this offering, the special mandatory redemption provisions will only apply to $600 million aggregate principal amount of unsecured notes and will not apply to the entire aggregate principal amount of the unsecured notes.” and “Description of Notes—Escrow of Proceeds; Special Mandatory Redemption.”

References in this offering memorandum to the “Escrow Release Date” refer to (i) the issue date, if this offering closes on or after the Scheme Effective Date and (ii) otherwise, the date of release of the escrowed notes proceeds from escrow.

Sources and uses of funds

The following table sets forth the estimated sources and uses of funds in connection with the Transactions. The actual sources and uses of funds may vary from the estimated sources and uses of funds set forth below. The estimated sources and uses of funds presented below should be read in conjunction with the other information included or incorporated by reference herein, including “—The Transactions,” “Use of Proceeds,” “Capitalization” and “Unaudited Pro Forma Condensed Combined Financial Statements.”

| Sources of funds | Amount | |||

| (millions) | ||||

| Secured notes offered hereby(1) | $ | 843 | ||

| Unsecured notes offered hereby(2) | 600 | |||

| Incremental Tranche C Term Facility(3) | 843 | |||

| Total Sources | $ | 2,286 | ||

| Use of funds | Amount | |||

| (millions) | ||||

| Cash consideration for Combination(4) | $ | 717 | ||

| Refinancing of Dowlais Credit Facilities(5) | 920 | |||

| Estimated fees and expenses(6) | 340 | |||

| Cash to balance sheet | 309 | |||

| Total Uses(7) | $ | 2,286 | ||

(1) Represents the aggregate principal amount of secured notes offered hereby. Assumes the secured notes are issued at par.

(2) Represents the aggregate principal amount of unsecured notes offered hereby. Assumes the unsecured notes are issued at par.

(3) On February 24, 2025, AAM Holdings and AAM Inc. entered into the Second Amendment to the Amended and Restated Credit Facility and the Incremental Facility Agreement which, among other things, provided for an $843.0 million incremental Tranche C Term Facility in connection with the Combination.

(4) Reflects our estimate of the total cash consideration to be paid to holders of all issued and outstanding ordinary shares of Dowlais pursuant to the Offer.

(5) Reflects our estimate of amounts necessary to repay in full all outstanding borrowings under the Dowlais Credit Facilities and to pay related fees, expenses and premiums. Reflects the net debt of Dowlais as of June 30, 2025 (calculated as $1.29 billion outstanding under the Dowlais Credit Facilities less cash and cash equivalents of Dowlais).

(6) Represents our estimate of fees and expenses associated with the Transactions, including financing fees, original issue discounts, initial purchaser discounts, legal, advisory and professional fees and other transaction costs, such as printing and rating agency fees. To the extent any refinancing fees, original issue discounts and other fees and expenses exceed the estimated amounts, we expect to fund such amounts with cash on our balance sheet at the closing of the Transactions.

(7) We intend to use the net proceeds from this offering, together with cash on hand, to fund the Dowlais Notes Change of Control Offer for outstanding Dowlais Notes. However, the decision as to whether to tender the Dowlais Notes in the Dowlais Notes Change of Control Offer will be made by each holder of Dowlais Notes at their discretion and for this reason, we cannot accurately predict the outcome of the Dowlais Notes Change of Control Offer. For purposes of the table above, we have assumed that none of the Dowlais Notes will be tendered in the Dowlais Notes Change of Control Offer, and that none of the sources of funds will be used to fund the Dowlais Notes Change of Control Offer. To the extent any Dowlais Notes are tendered in the Dowlais Notes Change of Control Offer, we intend to use the amount shown above as “Cash to balance sheet” and, if needed, cash on hand to fund the Dowlais Notes Change of Control Offer. See “Use of Proceeds.”

On an actual basis and without giving effect to any of the Transactions (and, for the avoidance of doubt, excluding Dowlais and its subsidiaries), the non-guarantor Subsidiaries:

| · | as of June 30, 2025, had approximately $23.8 million of outstanding indebtedness and approximately $862.5 million of other liabilities (including trade payables); |

| · | for the six-months ended June 30, 2025, accounted for approximately $854.1 million, or 29%, of AAM Holdings’ consolidated total revenue, and approximately $77.2 million, or 79%, of AAM Holdings’ consolidated operating income; |

| · | for the year ended December 31, 2024, accounted for approximately $1.8 billion, or 30%, of AAM Holdings’ consolidated total revenue, and approximately $167.5 million, or 69%, of AAM Holdings’ consolidated operating income; and |

| · | as of June 30, 2025, had approximately $1.6 billion, or 30%, of AAM Holdings’ consolidated total assets, and $886.3 million, or 19%, of AAM Holdings’ consolidated total liabilities. |

On a pro forma as adjusted basis to give effect to the Transactions on the assumptions described in “Capitalization,” the non-guarantor Subsidiaries (including Dowlais and the subsidiaries of Dowlais that will not become Subsidiary Guarantors after the Scheme Effective Date):

| · | as of June 30, 2025, would have had approximately $524 million of outstanding indebtedness (including the Dowlais Notes) and approximately $2.7 billion of other liabilities (including trade payables); |

| · | for the six-months ended June 30, 2025, would have accounted for approximately $2.6 billion, or 45%, of AAM Holdings’ consolidated total revenue, and approximately $69 million, or 56%, of AAM Holdings’ consolidated operating income; |

| · | for the year ended December 31, 2024, would have accounted for approximately $5.2 billion, or 45%, of AAM Holdings’ consolidated total revenue, and approximately $30 million, or 31%, of AAM Holdings’ consolidated operating income; and |

| · | as of June 30, 2025, would have had approximately $6 billion, or 53%, of AAM Holdings’ consolidated total assets, and $3.3 billion, or 33%, of AAM Holdings’ consolidated total liabilities. |

AAM Holdings summary historical and pro forma consolidated financial data

The summary consolidated financial data of AAM Holdings for each of the years ended December 31, 2024, 2023 and 2022 and as of December 31, 2024 and 2023 have been derived from our audited consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2024, which is incorporated by reference herein. The balance sheet data of AAM Holdings presented as of December 31, 2022 has been derived from AAM Holdings’ audited consolidated financial statements not incorporated by reference herein.

The summary consolidated financial data for AAM Holdings for the six months ended June 30, 2025 and 2024 have been derived from our unaudited consolidated financial statements incorporated by reference in this offering memorandum. The balance sheet data of AAM Holdings presented as of June 30, 2024 has been derived from AAM Holdings’ unaudited consolidated financial statements not incorporated by reference herein. The unaudited consolidated financial statements have been prepared on the same basis as the audited consolidated financial statements and, in the opinion of management, include all adjustments, consisting of normal recurring adjustments, necessary for a fair statement of the results for those periods.